Partnership Tax returns Form 1065 - PwC€¦ · Partnerships Form 1065 - Who must file? Domestic...

29

Partnership Tax returns – Form 1065 January 10, 2017

Transcript of Partnership Tax returns Form 1065 - PwC€¦ · Partnerships Form 1065 - Who must file? Domestic...

•

Partnership

Tax returns – Form 1065

January 10, 2017

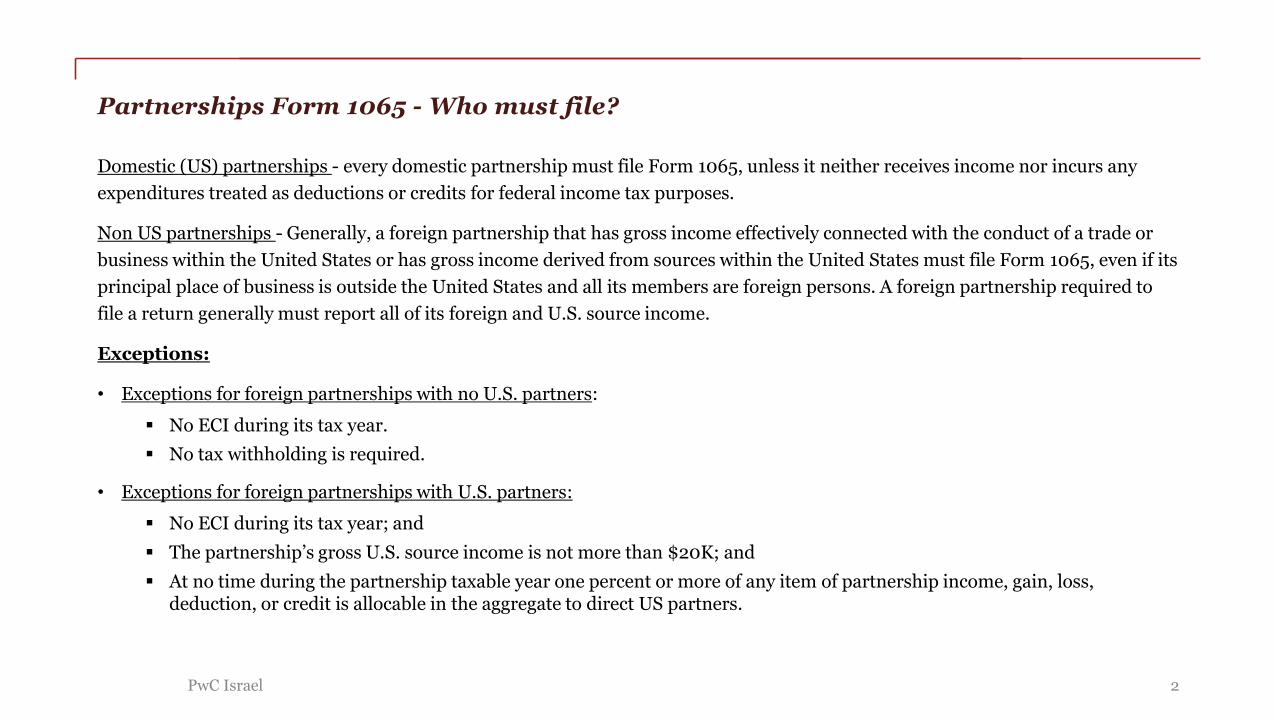

Partnerships Form 1065 - Who must file?

Domestic (US) partnerships - every domestic partnership must file Form 1065, unless it neither receives income nor incurs any

expenditures treated as deductions or credits for federal income tax purposes.

Non US partnerships - Generally, a foreign partnership that has gross income effectively connected with the conduct of a trade or

business within the United States or has gross income derived from sources within the United States must file Form 1065, even if its

principal place of business is outside the United States and all its members are foreign persons. A foreign partnership required to

file a return generally must report all of its foreign and U.S. source income.

Exceptions:

• Exceptions for foreign partnerships with no U.S. partners:

No ECI during its tax year.

No tax withholding is required.

• Exceptions for foreign partnerships with U.S. partners:

No ECI during its tax year; and

The partnership’s gross U.S. source income is not more than $20K; and

At no time during the partnership taxable year one percent or more of any item of partnership income, gain, loss, deduction, or credit is allocable in the aggregate to direct US partners.

2PwC Israel

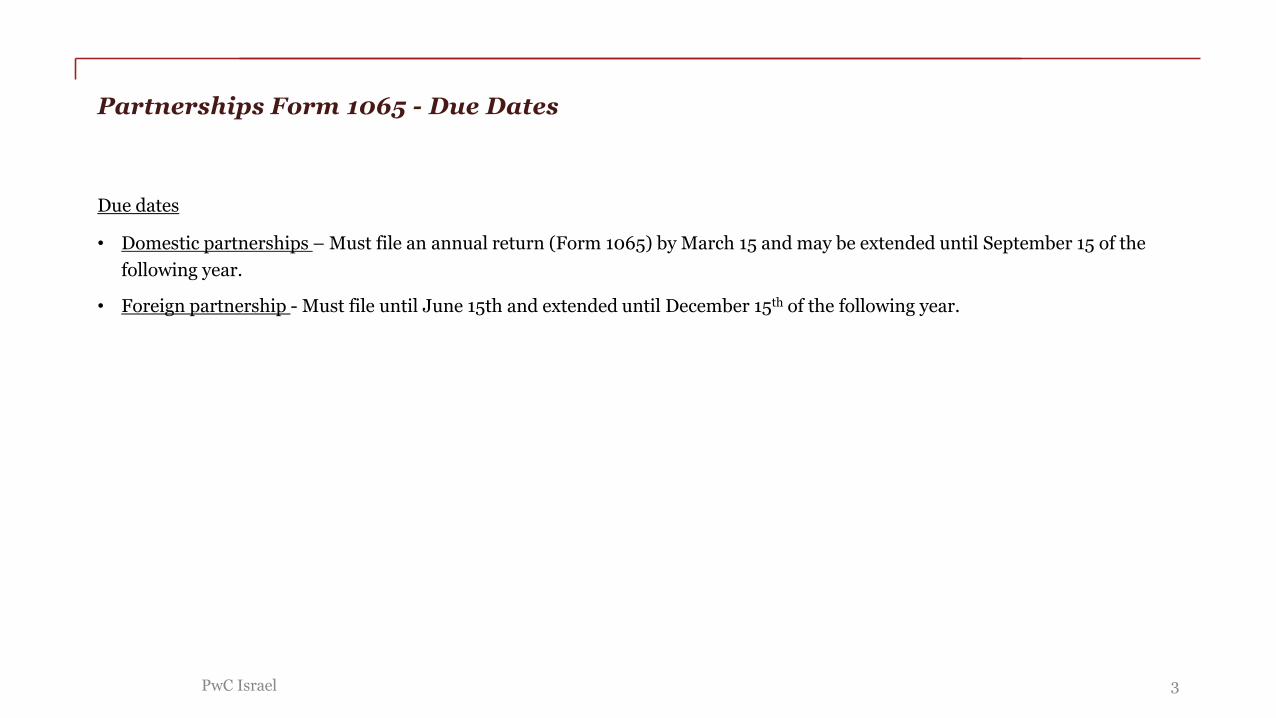

Partnerships Form 1065 - Due Dates

Due dates

• Domestic partnerships – Must file an annual return (Form 1065) by March 15 and may be extended until September 15 of the

following year.

• Foreign partnership - Must file until June 15th and extended until December 15th of the following year.

3PwC Israel

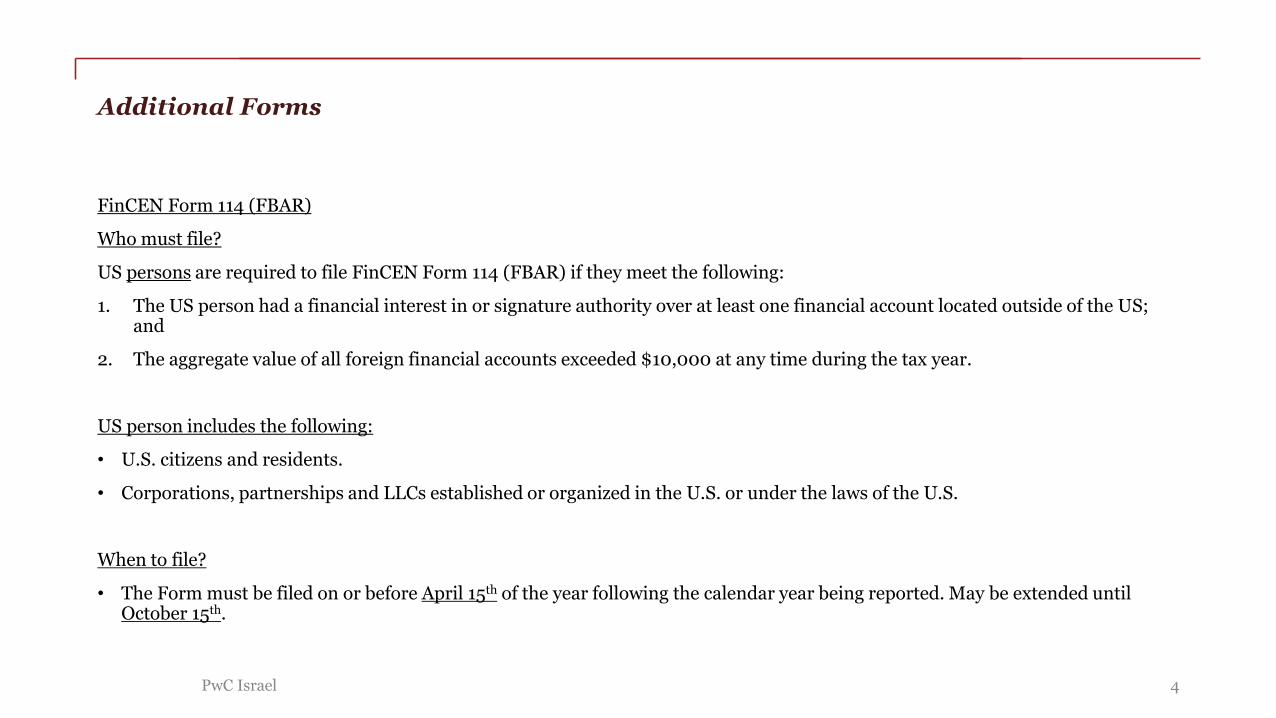

Additional Forms

FinCEN Form 114 (FBAR)

Who must file?

US persons are required to file FinCEN Form 114 (FBAR) if they meet the following:

1. The US person had a financial interest in or signature authority over at least one financial account located outside of the US; and

2. The aggregate value of all foreign financial accounts exceeded $10,000 at any time during the tax year.

US person includes the following:

• U.S. citizens and residents.

• Corporations, partnerships and LLCs established or organized in the U.S. or under the laws of the U.S.

When to file?

• The Form must be filed on or before April 15th of the year following the calendar year being reported. May be extended until October 15th.

4PwC Israel

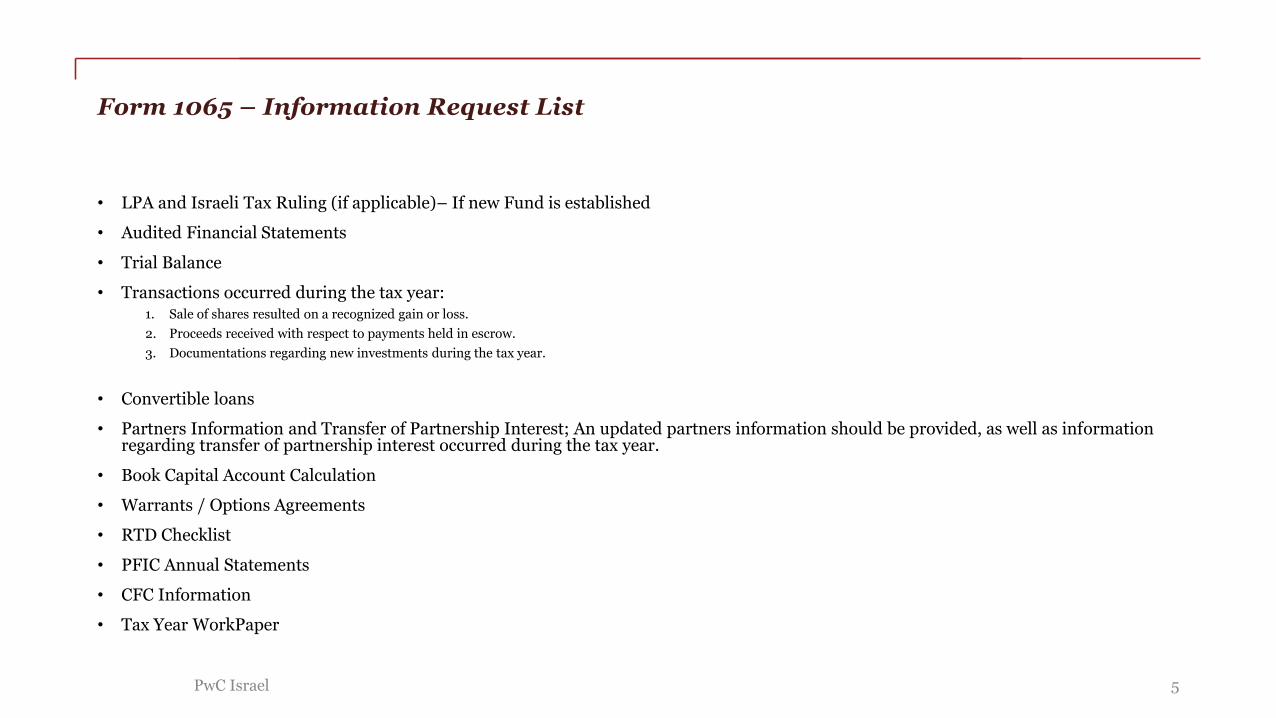

Form 1065 – Information Request List

• LPA and Israeli Tax Ruling (if applicable)– If new Fund is established

• Audited Financial Statements

• Trial Balance

• Transactions occurred during the tax year: 1. Sale of shares resulted on a recognized gain or loss.

2. Proceeds received with respect to payments held in escrow.

3. Documentations regarding new investments during the tax year.

• Convertible loans

• Partners Information and Transfer of Partnership Interest; An updated partners information should be provided, as well as information regarding transfer of partnership interest occurred during the tax year.

• Book Capital Account Calculation

• Warrants / Options Agreements

• RTD Checklist

• PFIC Annual Statements

• CFC Information

• Tax Year WorkPaper

5PwC Israel

Form 1065 – Sch K-1 & Work Papers

6PwC Israel

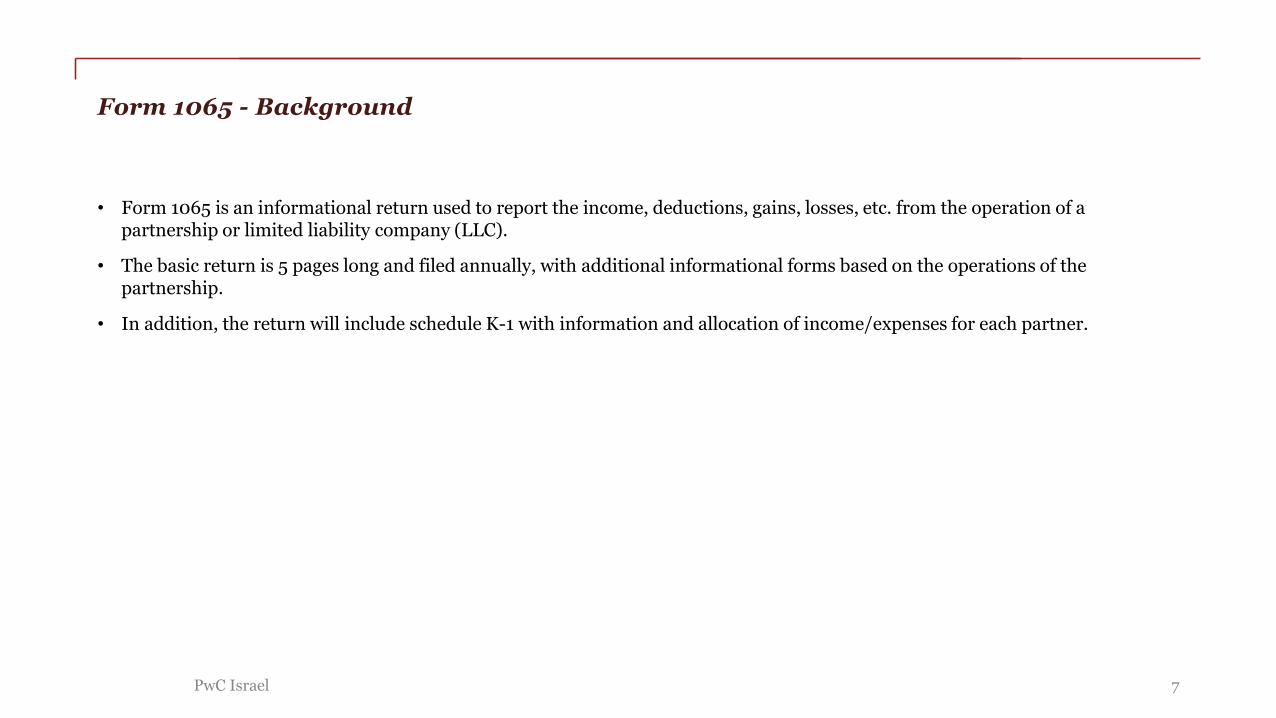

Form 1065 - Background

• Form 1065 is an informational return used to report the income, deductions, gains, losses, etc. from the operation of a partnership or limited liability company (LLC).

• The basic return is 5 pages long and filed annually, with additional informational forms based on the operations of the partnership.

• In addition, the return will include schedule K-1 with information and allocation of income/expenses for each partner.

7PwC Israel

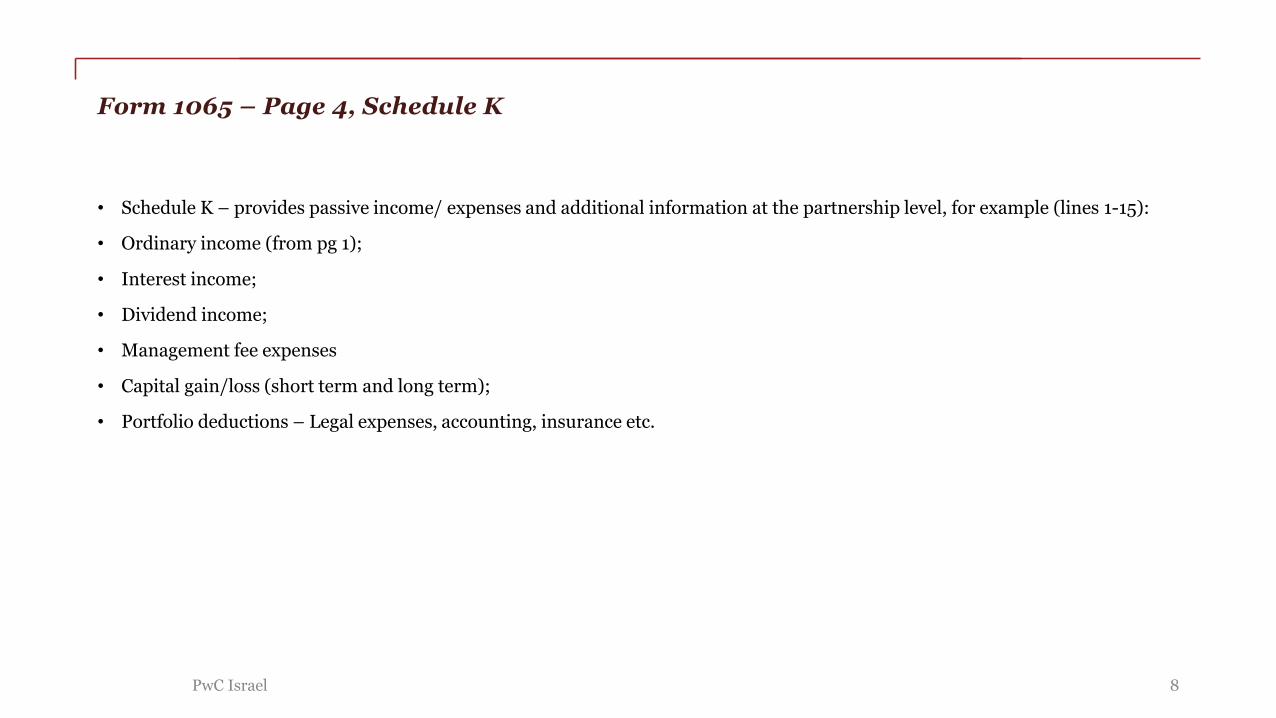

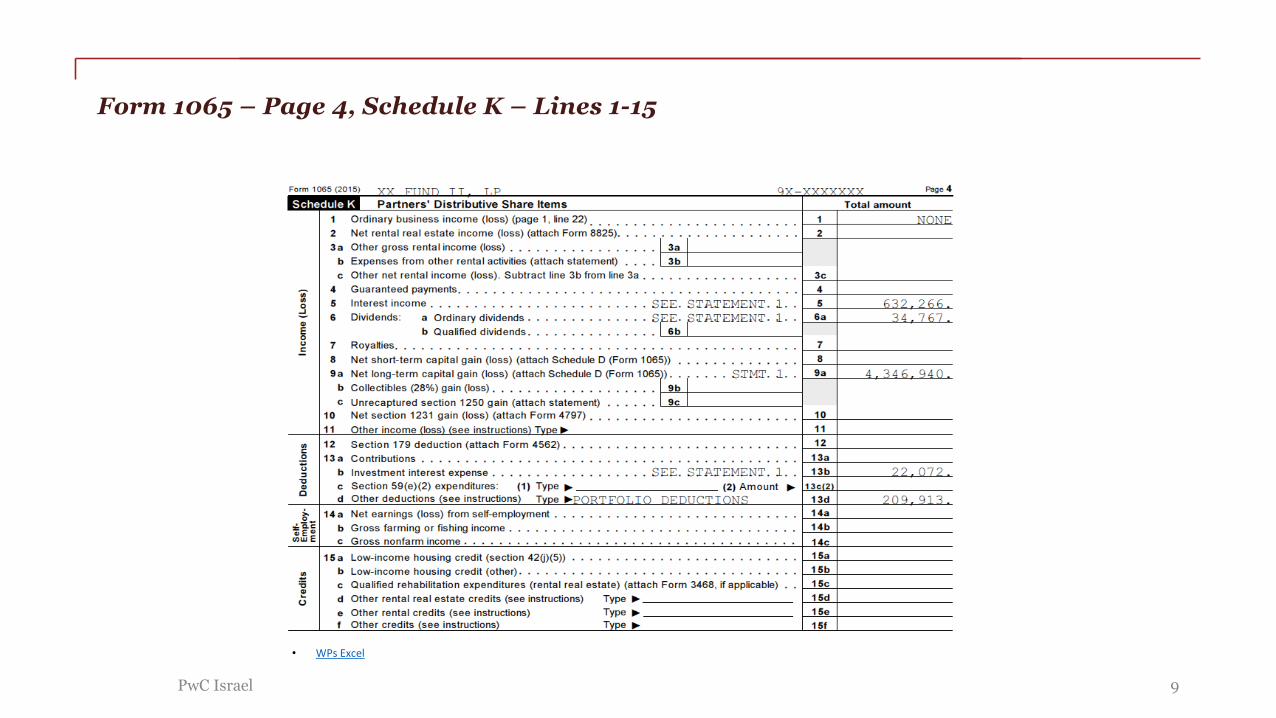

Form 1065 – Page 4, Schedule K

• Schedule K – provides passive income/ expenses and additional information at the partnership level, for example (lines 1-15):

• Ordinary income (from pg 1);

• Interest income;

• Dividend income;

• Management fee expenses

• Capital gain/loss (short term and long term);

• Portfolio deductions – Legal expenses, accounting, insurance etc.

8PwC Israel

Form 1065 – Page 4, Schedule K – Lines 1-15

PwC Israel 9

• WPs Excel

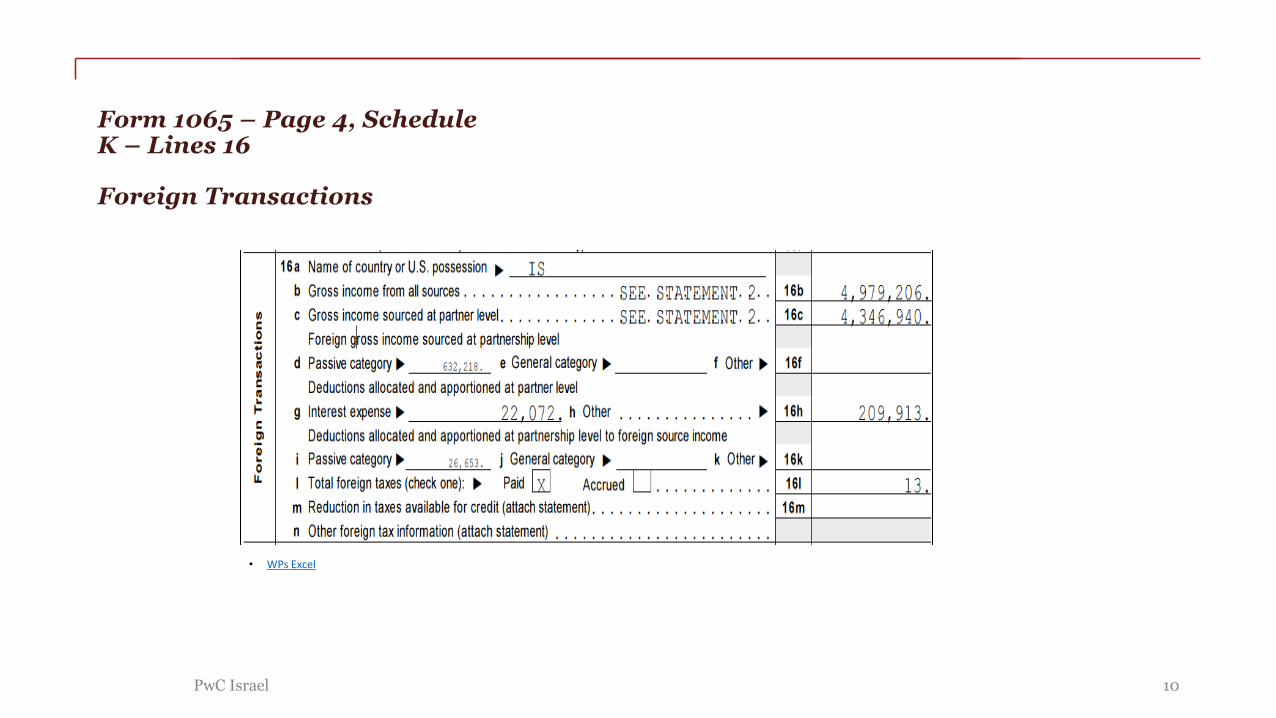

Form 1065 – Page 4, Schedule K – Lines 16

Foreign Transactions

• WPs Excel

PwC Israel 10

Form 1065 – Schedule D & Form 8949

• Schedule D

Reports capital gains and losses – short and long term.

• Form 8949

Reports a detailed schedule of sales and exchanges of capital assets and reconciles amounts that were reported on Form

1099 (if applicable).

11PwC Israel

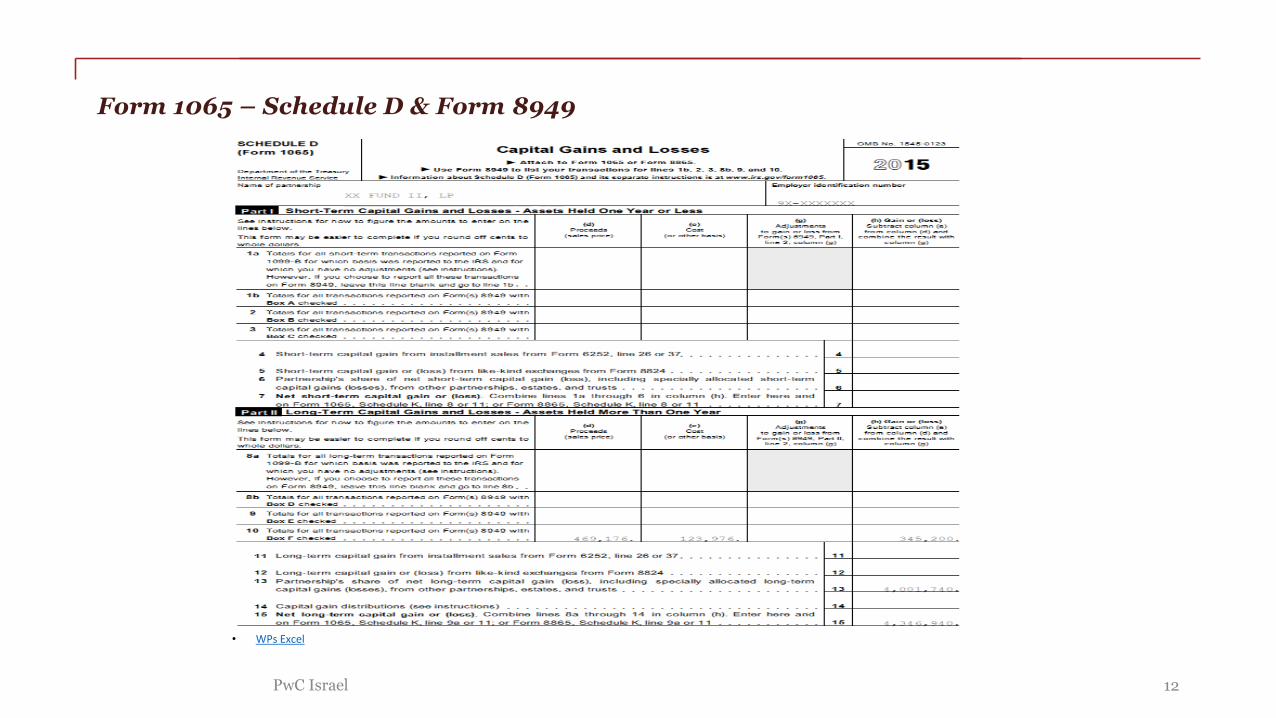

Form 1065 – Schedule D & Form 8949

• WPs Excel

PwC Israel 12

Form 1065 – Schedule D & Form 8949 (Cont.)

Installment Sale

• Reporting

• An installment sale is the disposition of property resulting in a gain, and is reported in installment payments (cash and escrow/milestone).

• Treatment

• Applies only to transactions where an overall GAIN is realized

• Gain is recognized ratably as total payments are received.

• Taxpayer can elect out of installment sale treatment and recognize all gain in year of sale.

13PwC Israel

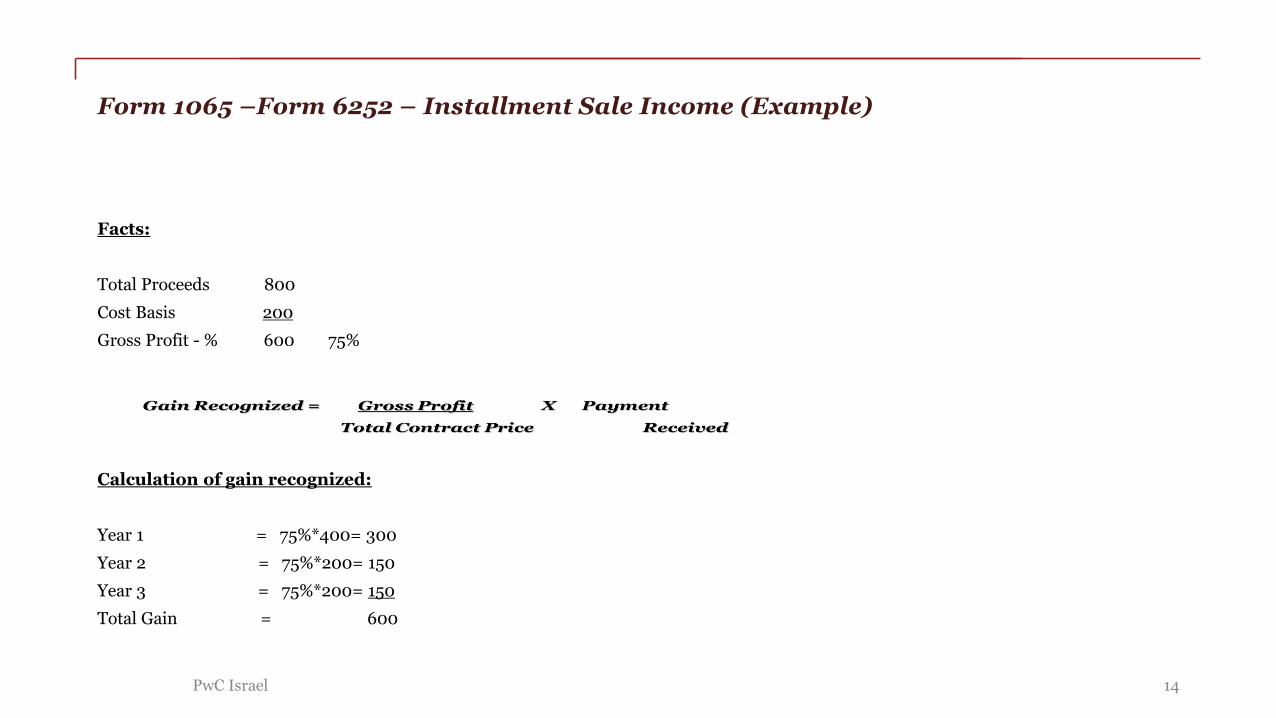

Form 1065 –Form 6252 – Installment Sale Income (Example)

Facts:

Total Proceeds 800

Cost Basis 200

Gross Profit - % 600 75%

Calculation of gain recognized:

Year 1 = 75%*400= 300

Year 2 = 75%*200= 150

Year 3 = 75%*200= 150

Total Gain = 600

PwC Israel 14

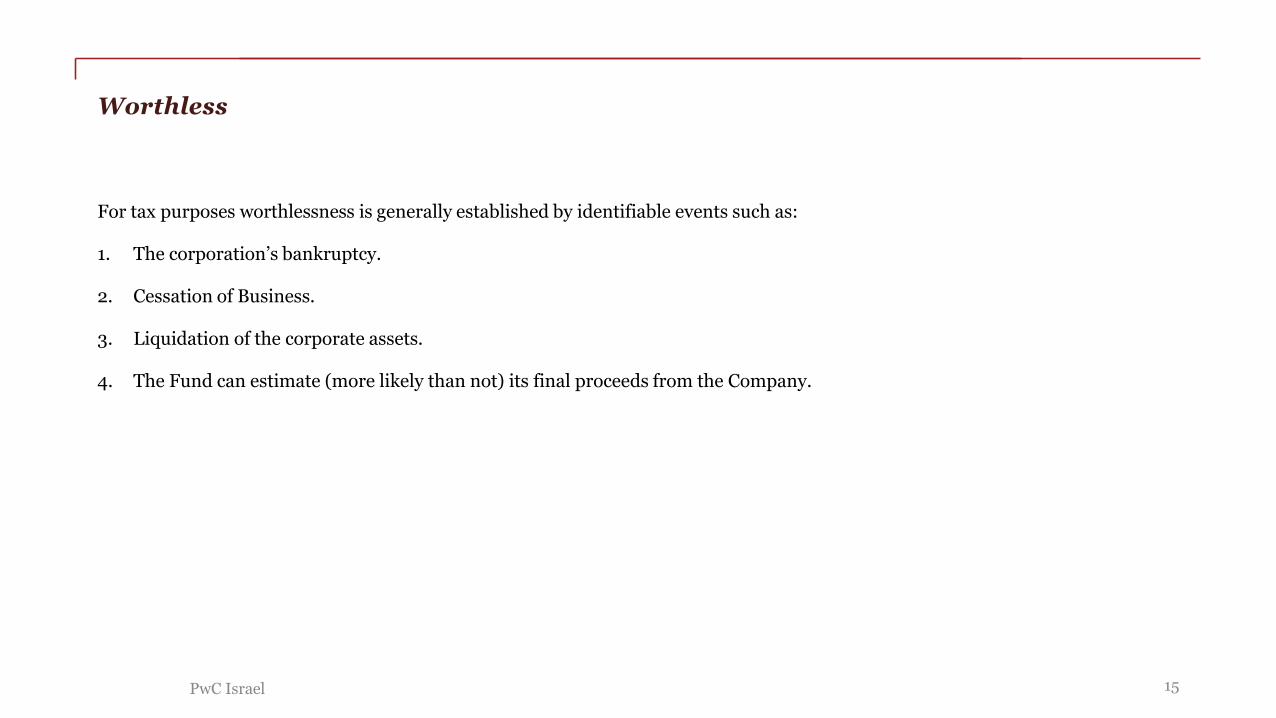

Worthless

For tax purposes worthlessness is generally established by identifiable events such as:

1. The corporation’s bankruptcy.

2. Cessation of Business.

3. Liquidation of the corporate assets.

4. The Fund can estimate (more likely than not) its final proceeds from the Company.

PwC Israel 15

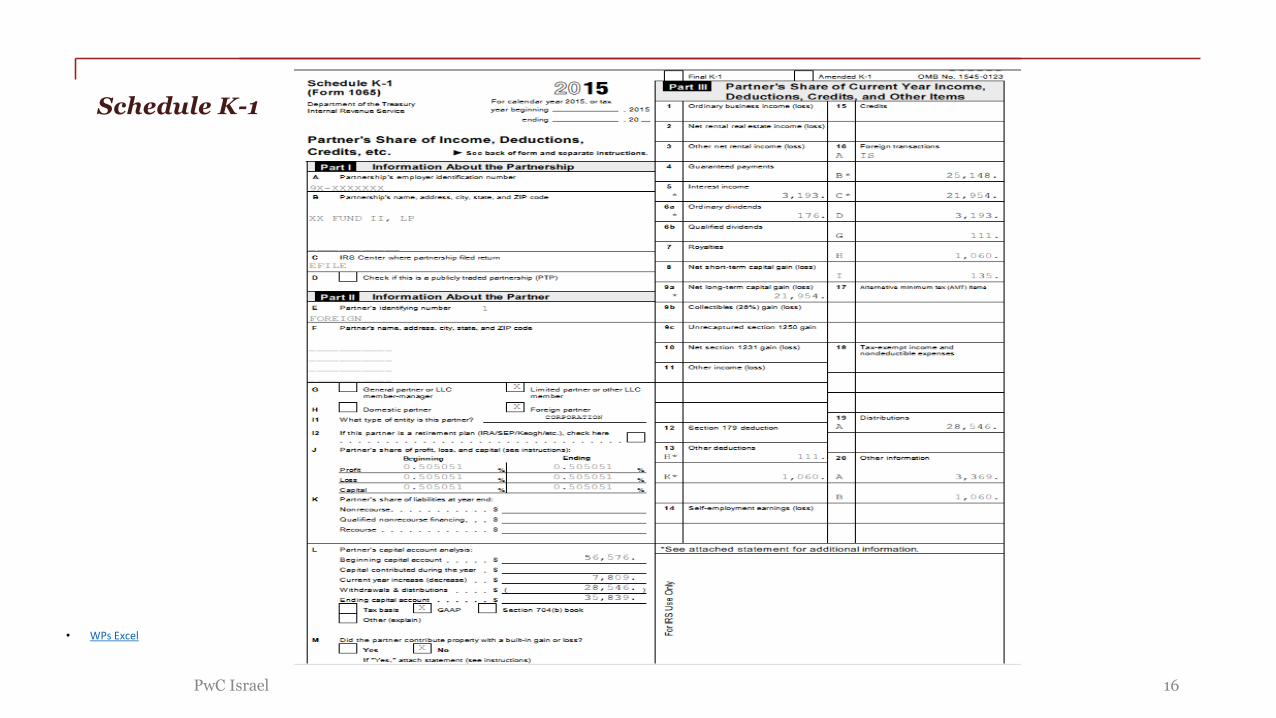

Schedule K-1

• WPs Excel

PwC Israel 16

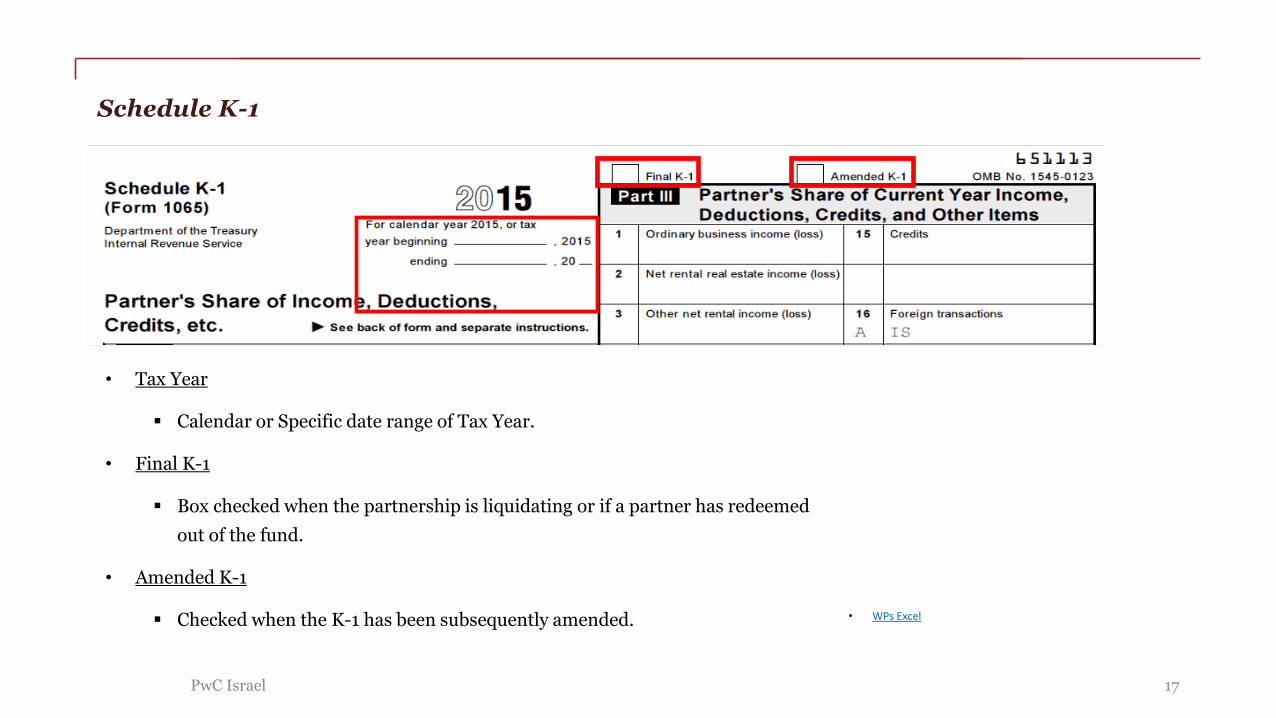

Schedule K-1

• Tax Year

Calendar or Specific date range of Tax Year.

• Final K-1

Box checked when the partnership is liquidating or if a partner has redeemed

out of the fund.

• Amended K-1

Checked when the K-1 has been subsequently amended.

17PwC Israel

• WPs Excel

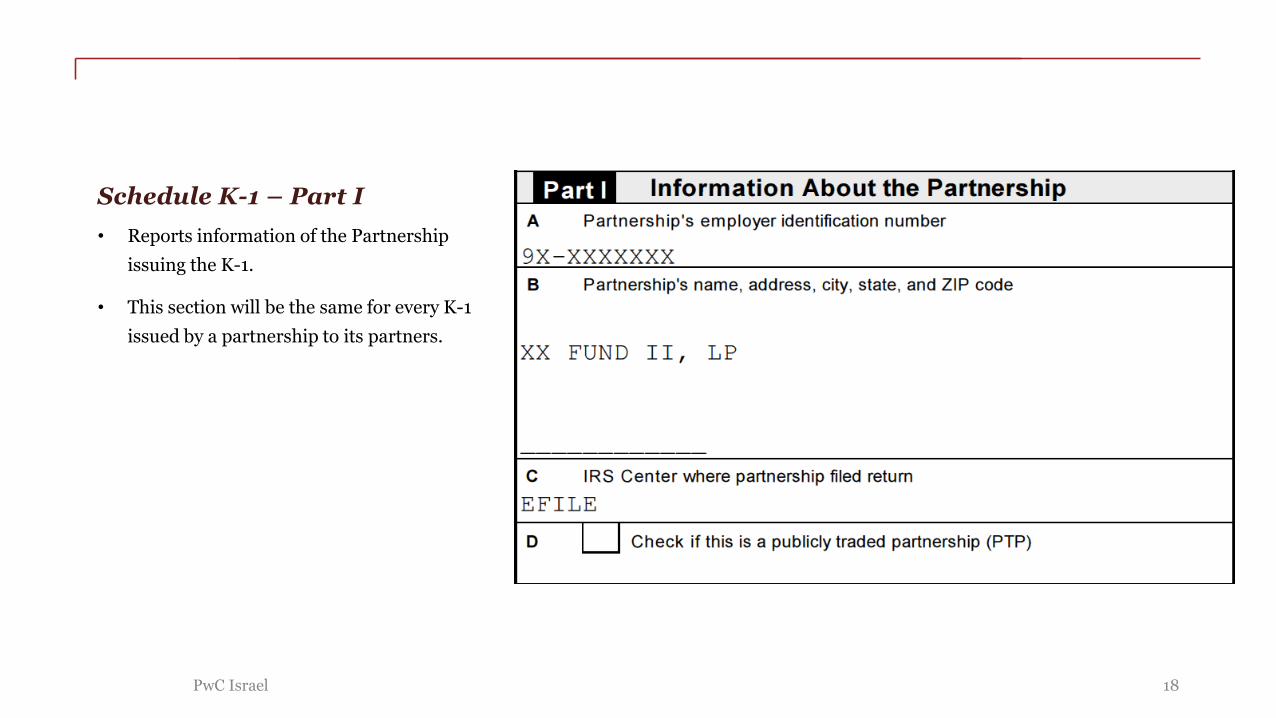

Schedule K-1 – Part I

• Reports information of the Partnership

issuing the K-1.

• This section will be the same for every K-1

issued by a partnership to its partners.

18PwC Israel

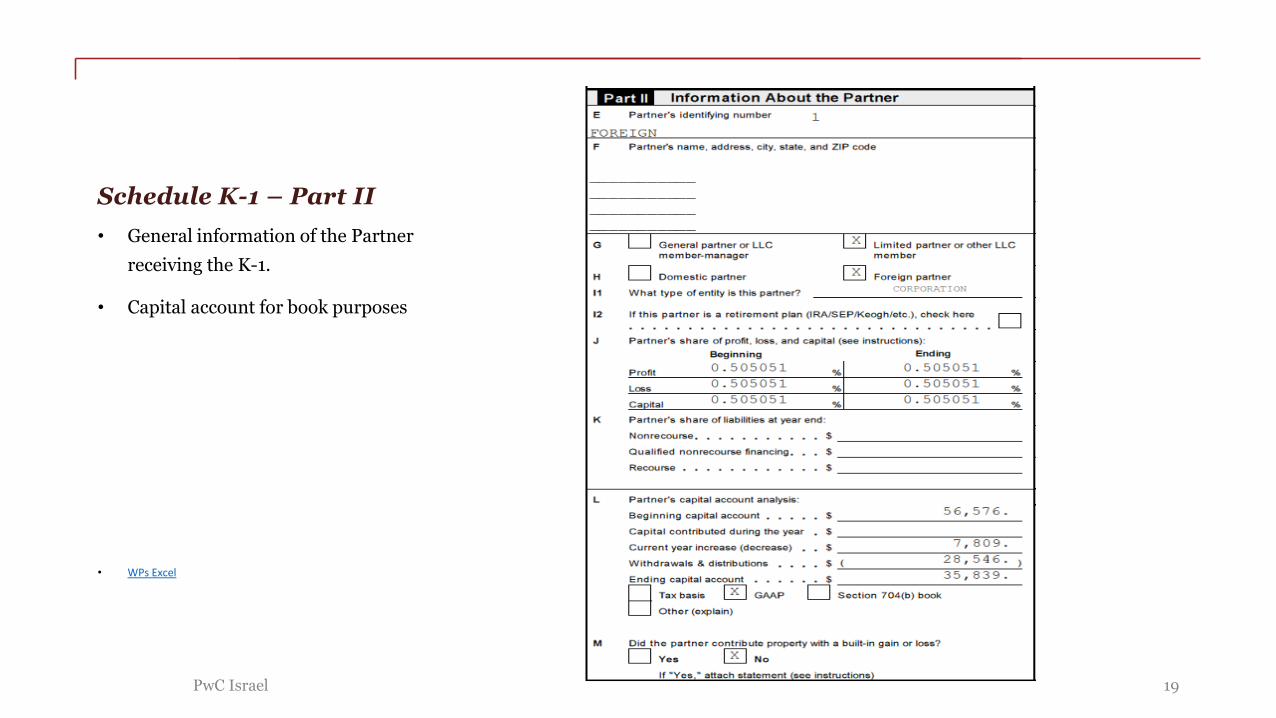

Schedule K-1 – Part II

• General information of the Partner

receiving the K-1.

• Capital account for book purposes

• WPs Excel

19PwC Israel

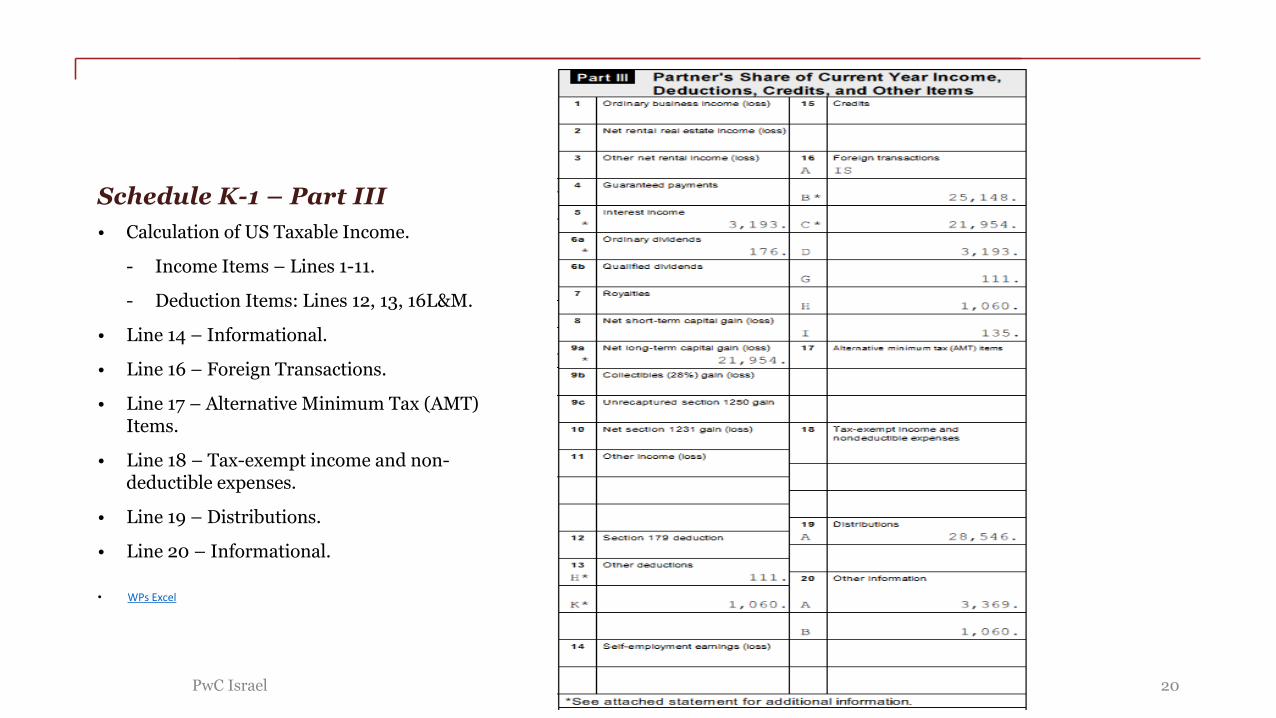

Schedule K-1 – Part III

• Calculation of US Taxable Income.

- Income Items – Lines 1-11.

- Deduction Items: Lines 12, 13, 16L&M.

• Line 14 – Informational.

• Line 16 – Foreign Transactions.

• Line 17 – Alternative Minimum Tax (AMT) Items.

• Line 18 – Tax-exempt income and non-deductible expenses.

• Line 19 – Distributions.

• Line 20 – Informational.

• WPs Excel

20PwC Israel

Schedule K-1 – Statement 1

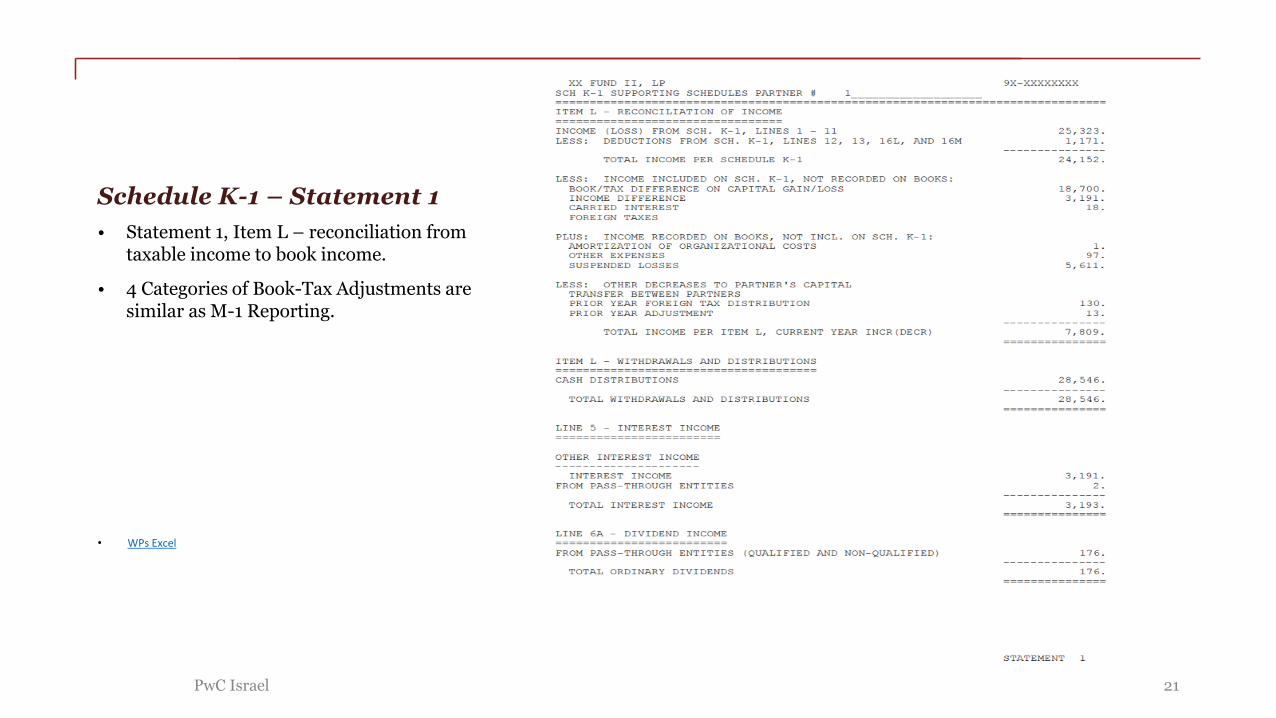

• Statement 1, Item L – reconciliation from taxable income to book income.

• 4 Categories of Book-Tax Adjustments are similar as M-1 Reporting.

• WPs Excel

21PwC Israel

Other Statements

22PwC Israel

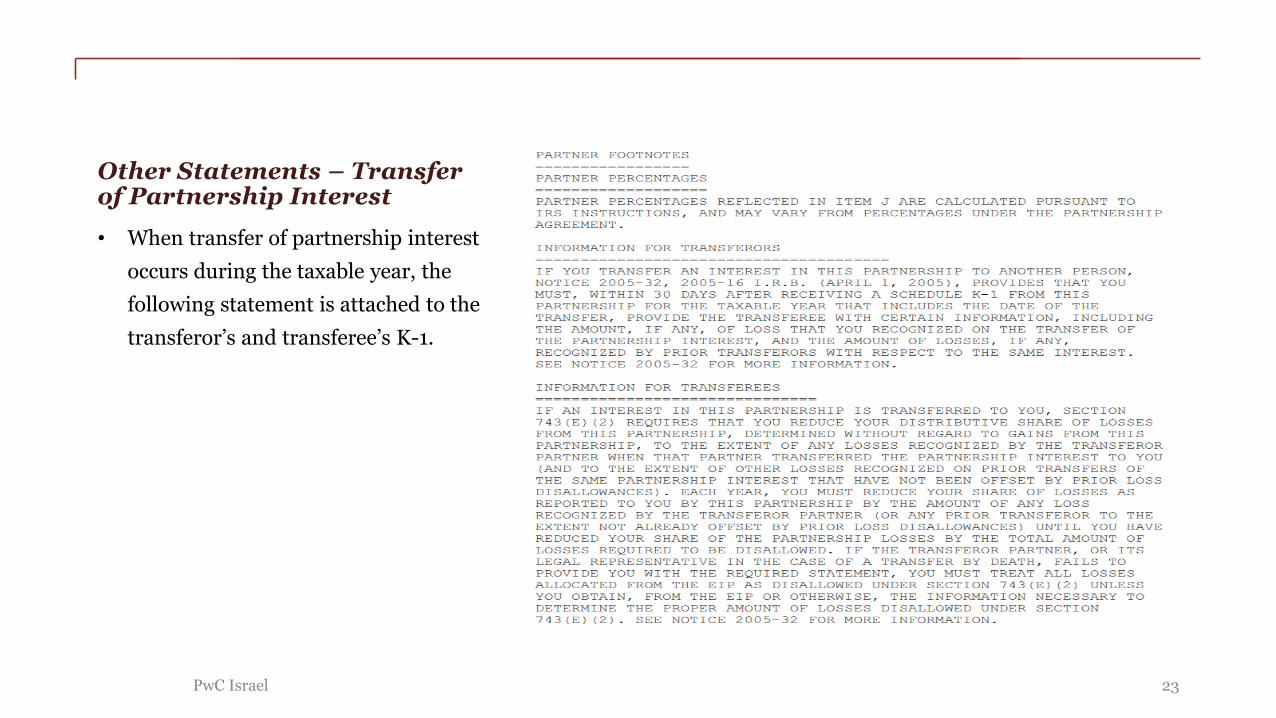

Other Statements – Transfer of Partnership Interest

• When transfer of partnership interest

occurs during the taxable year, the

following statement is attached to the

transferor’s and transferee’s K-1.

23PwC Israel

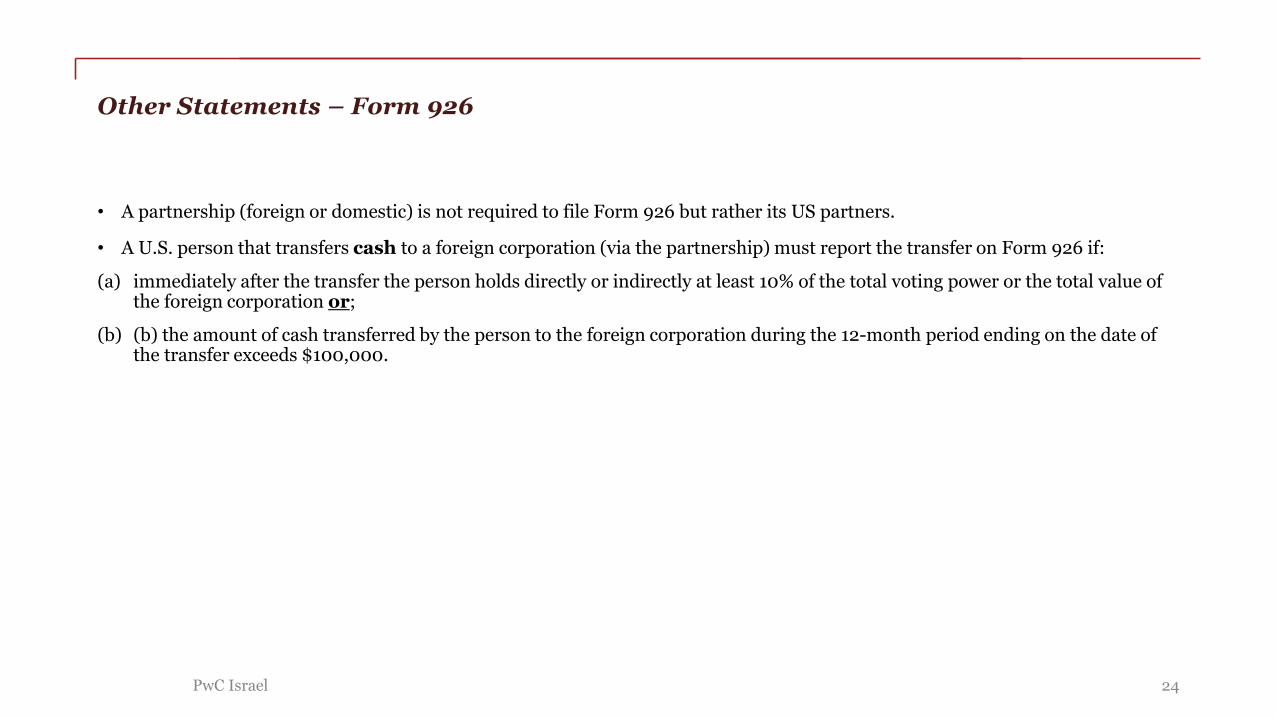

Other Statements – Form 926

• A partnership (foreign or domestic) is not required to file Form 926 but rather its US partners.

• A U.S. person that transfers cash to a foreign corporation (via the partnership) must report the transfer on Form 926 if:

(a) immediately after the transfer the person holds directly or indirectly at least 10% of the total voting power or the total value of the foreign corporation or;

(b) (b) the amount of cash transferred by the person to the foreign corporation during the 12-month period ending on the date of the transfer exceeds $100,000.

PwC Israel 24

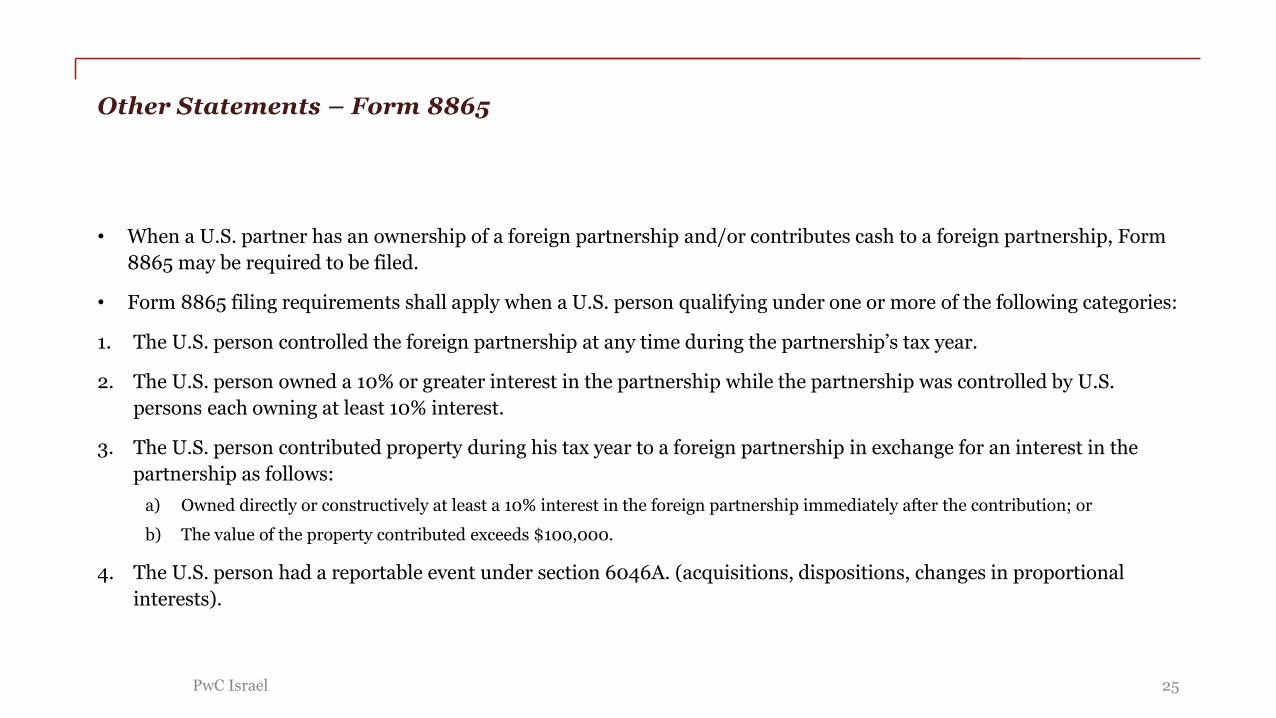

Other Statements – Form 8865

• When a U.S. partner has an ownership of a foreign partnership and/or contributes cash to a foreign partnership, Form

8865 may be required to be filed.

• Form 8865 filing requirements shall apply when a U.S. person qualifying under one or more of the following categories:

1. The U.S. person controlled the foreign partnership at any time during the partnership’s tax year.

2. The U.S. person owned a 10% or greater interest in the partnership while the partnership was controlled by U.S.

persons each owning at least 10% interest.

3. The U.S. person contributed property during his tax year to a foreign partnership in exchange for an interest in the

partnership as follows:

a) Owned directly or constructively at least a 10% interest in the foreign partnership immediately after the contribution; or

b) The value of the property contributed exceeds $100,000.

4. The U.S. person had a reportable event under section 6046A. (acquisitions, dispositions, changes in proportional

interests).

PwC Israel 25

Other Statements – Form 8858

• U.S. Person that is a tax owner of Foreign Disregarded Entity (FDE) at any time during the U.S. person’s taxable year or

annual accounting period, has to file Form 8858.

• U.S. Person definition includes a domestic Partnership.

• U.S. person filing Form 8858 is any U.S. person that:

1. Is the tax owner of an FDE

2. Owns a specified interest in an FDE indirectly or constructively through a CFC or CFP.

PwC Israel 26

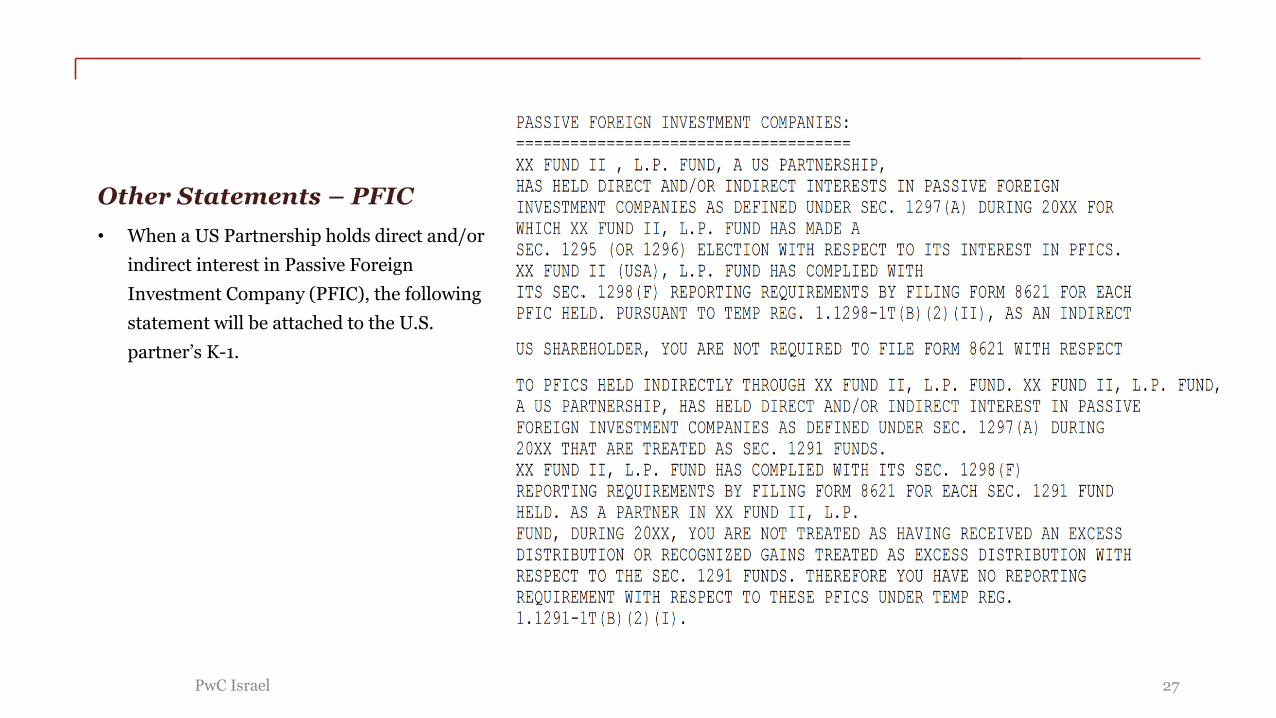

Other Statements – PFIC

• When a US Partnership holds direct and/or

indirect interest in Passive Foreign

Investment Company (PFIC), the following

statement will be attached to the U.S.

partner’s K-1.

27PwC Israel

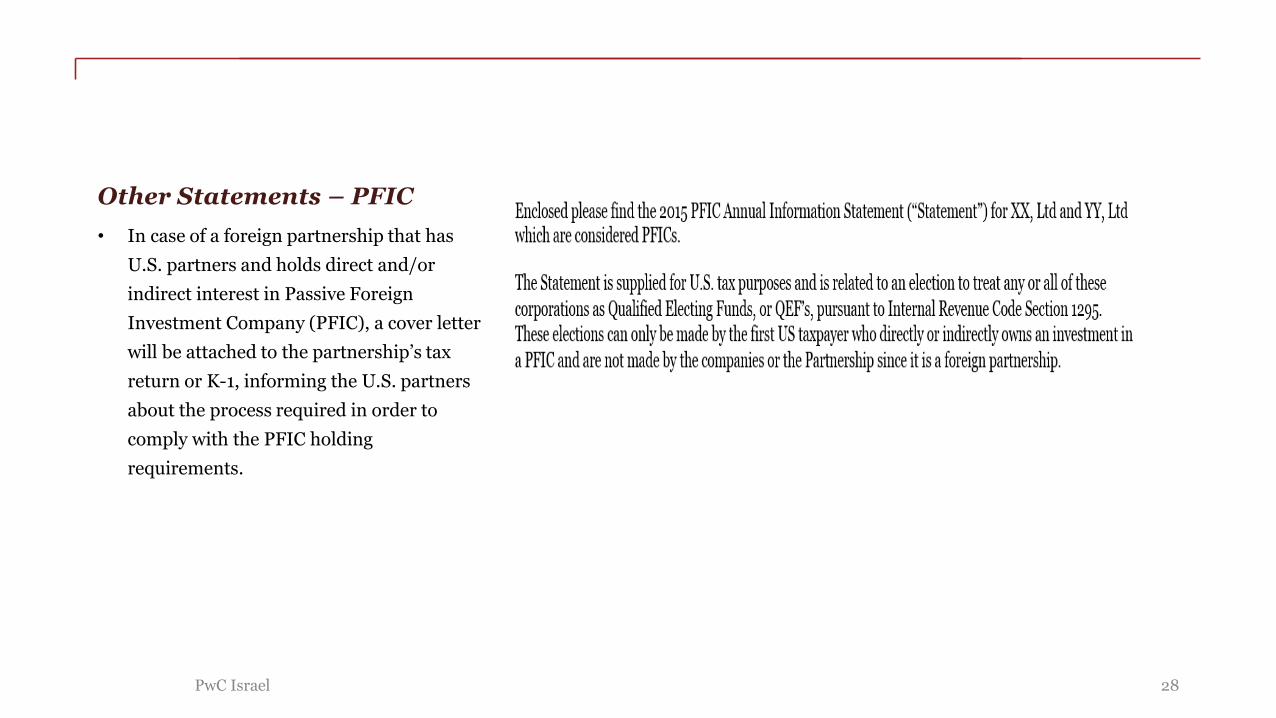

Other Statements – PFIC

• In case of a foreign partnership that has

U.S. partners and holds direct and/or

indirect interest in Passive Foreign

Investment Company (PFIC), a cover letter

will be attached to the partnership’s tax

return or K-1, informing the U.S. partners

about the process required in order to

comply with the PFIC holding

requirements.

28PwC Israel

©2016 Kesselman & Kesselman. All rights reserved. In this document, “PwC Israel” refers to Kesselman & Kesselman, which is a member firm of PricewaterhouseCoopers International Limited, each member firm of which is a separate legal entity. Please see www.pwc.com/structure for further details.

PwC Israel helps organisationsand individuals create the value they’re looking for. We’re a member of the PwC network of firms with 223,000 people in more than 158 countries. We’re committed to delivering quality in assurance, tax and advisory services. Tell us what matters to you and find out more by visiting us at www.pwc.com/il

This publication has been prepared for general guidance on matters of interest only, and does not constitute professional advice. It does not take into account any objectives, financial situation or needs of any recipient. Any recipient should not act upon the information contained in this publication without obtaining specific professional advice. No representation or warranty (express or implied) is given as to the accuracy or completeness of the information contained in this publication, and, to the extent permitted by law, Kesselman & Kesselman, and any other member firm of PwC, its members, employees and agents do not accept or assume any liability, responsibility or duty of care for any consequences of you or anyone else acting, or refraining to act, in reliance on the information contained in this publication or for any decision based on it, or for any direct and/or indirect and/or other damage caused as a result of using the publication and/or the information contained in it.

Thank you!

Karen Efrati, U.S. Tax Compliance Senior Manager, PwC Israel

972-3-7954821

Yonatan Kaplan, U.S. Tax Compliance Manager, PwC Israel

972 -3-7955033

29