Pannonia Ethanol - Innovation Day 2015 Market Outlook & the Hungarian Paradigm

20

Jaime Nolan Miralles Senior Commodity Risk Manager INTLFCStone Ltd. PANNONI A ETHANOL – I NNOVATI ON DAY 2015 MARKET OUTLOOK & THE HUNGARIAN International Assets Holding Corporation | www.intlassets.com

-

Upload

agroinformcom -

Category

Business

-

view

837 -

download

0

Transcript of Pannonia Ethanol - Innovation Day 2015 Market Outlook & the Hungarian Paradigm

Jaime Nolan Miralles Senior Commodity Risk Manager

INTLFCStone Ltd.

PANNONIA ETHANOL – INNOVATION DAY 2015

MARKET OUTLOOK & THE HUNGARIAN PARADIGM

International Assets Holding Corporation | www.intlassets.com

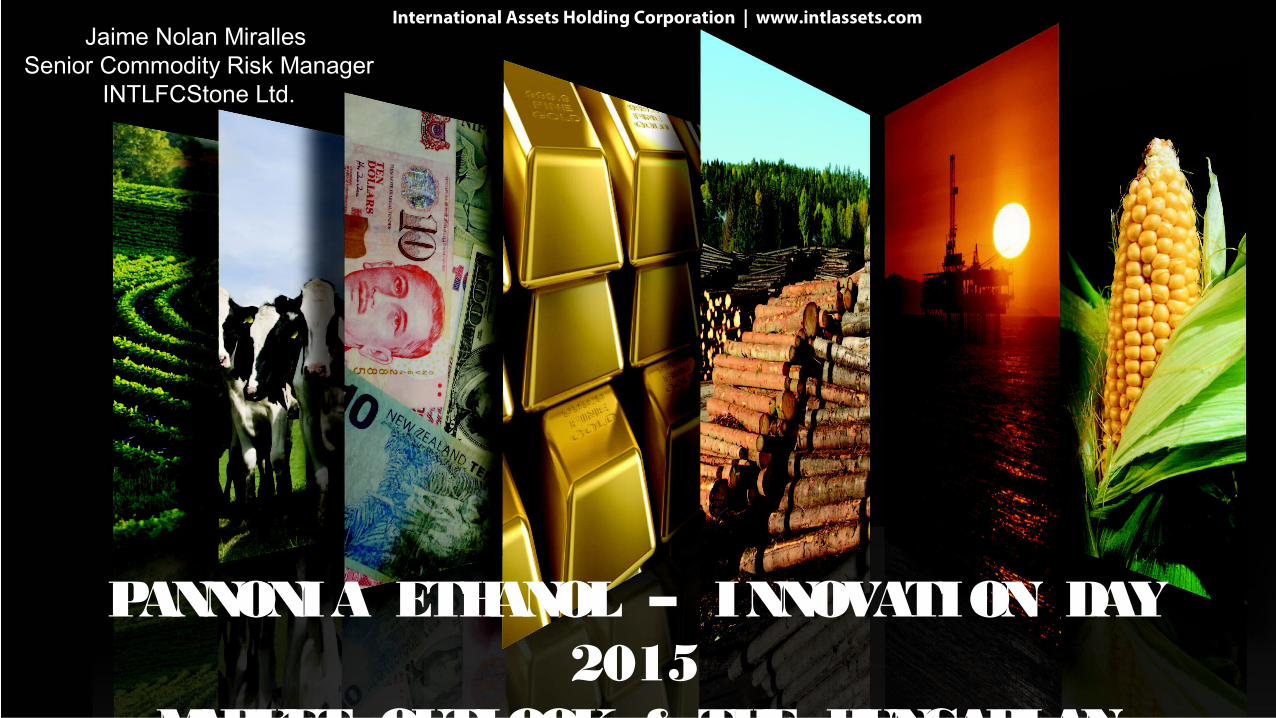

Hungarian Corn

Corn yield and output has been hurt by dryness and heat stress.Output at am estimated 6.5Mmt falls below the ten year average of 7.2Mmt and sharply lower than last years record 9.3Mmt output

4.5mmt 10 year average output

7.2mmt 10 year average output

Hungarian Wheat

Hungarian wheat output of 5.2mmt is on a par with last years output and is the third largest output the last ten years. 700kt over the 10 year average.

What do we store and what do we sell?

HUNGARIAN WHEAT & MAIZE SUPPLY

Ethanol Sector providing leading role to Hungarian producer

Ethanol sector provides demand engine in domestic Hungarian maize market

Tighter maize S&D Shifts feed demand to Wheat

Creating sustainable demand in Hungary over the next ten yearsCreating strong & reliable counterpartiesKey partners in your success

HUNGARIAN –DOMESTIC DEMAND

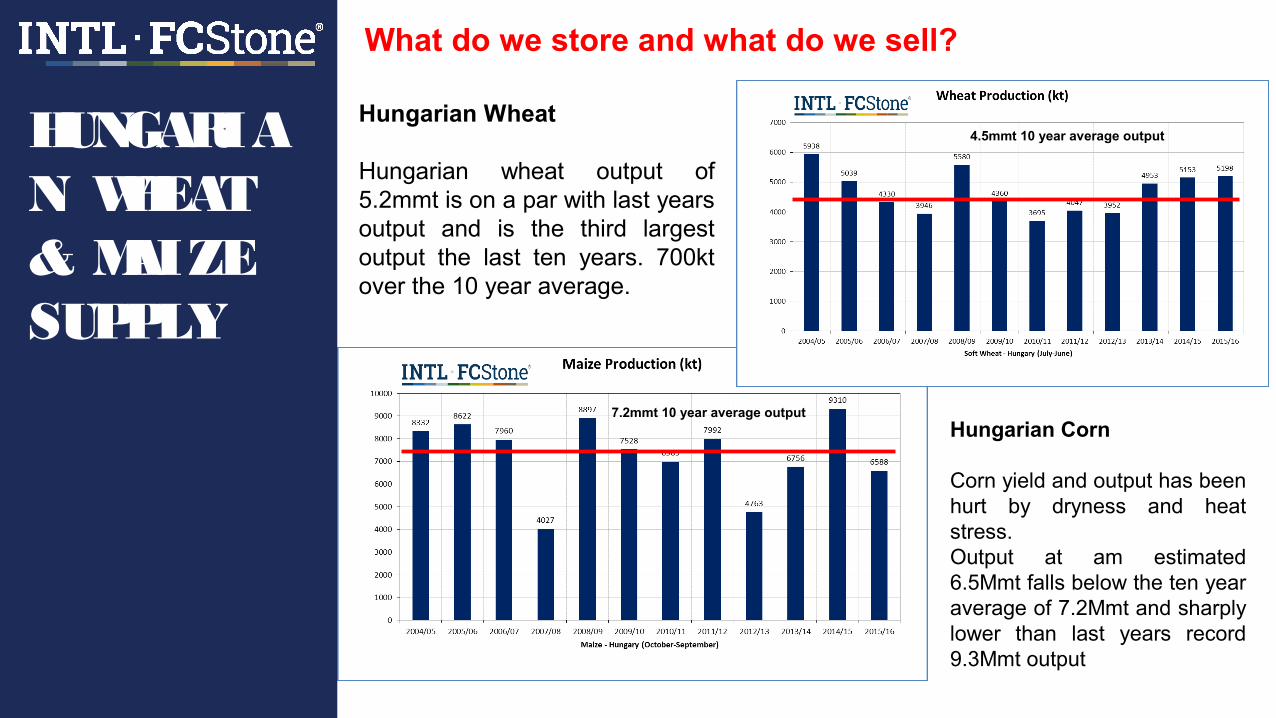

Just under 50% of output moves to export market

54% of output moves to export market

EXPORT MARKET – KEY PRICE DRIVER

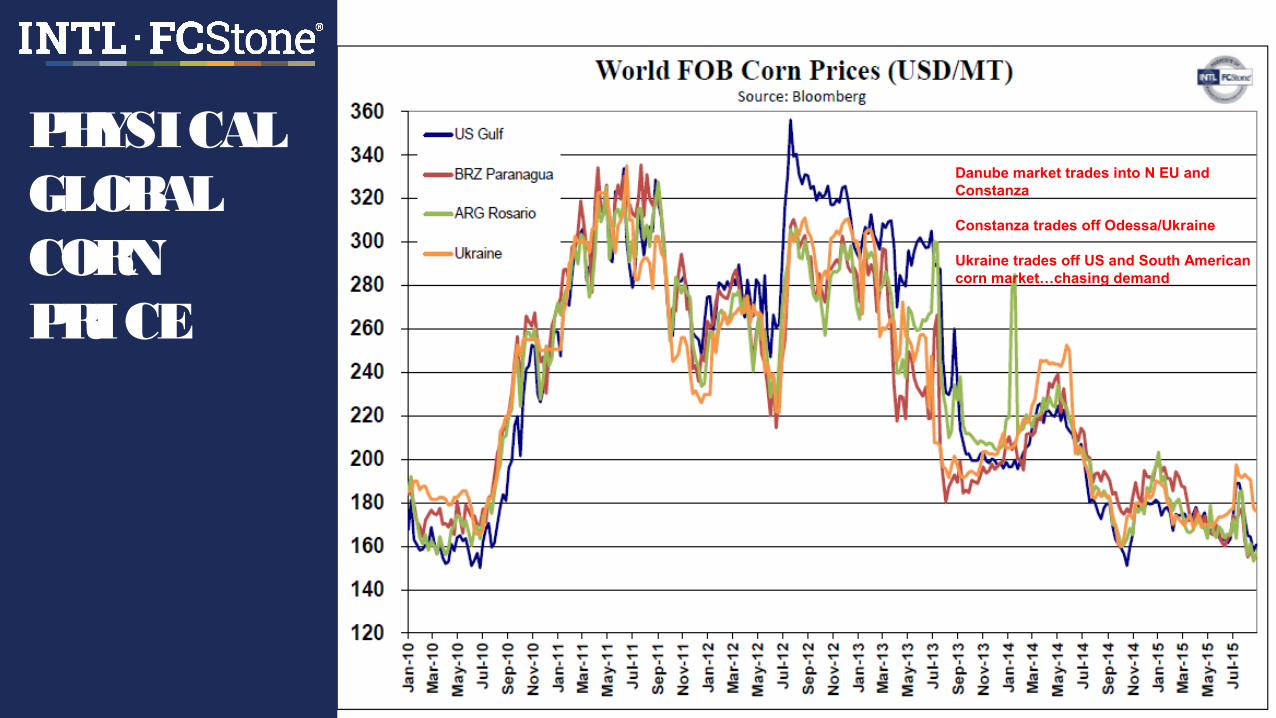

Danube market trades into N EU and Constanza

Constanza trades off Odessa/Ukraine

Ukraine trades off US and South American corn market…chasing demand

PHYSICAL GLOBAL CORN PRICE

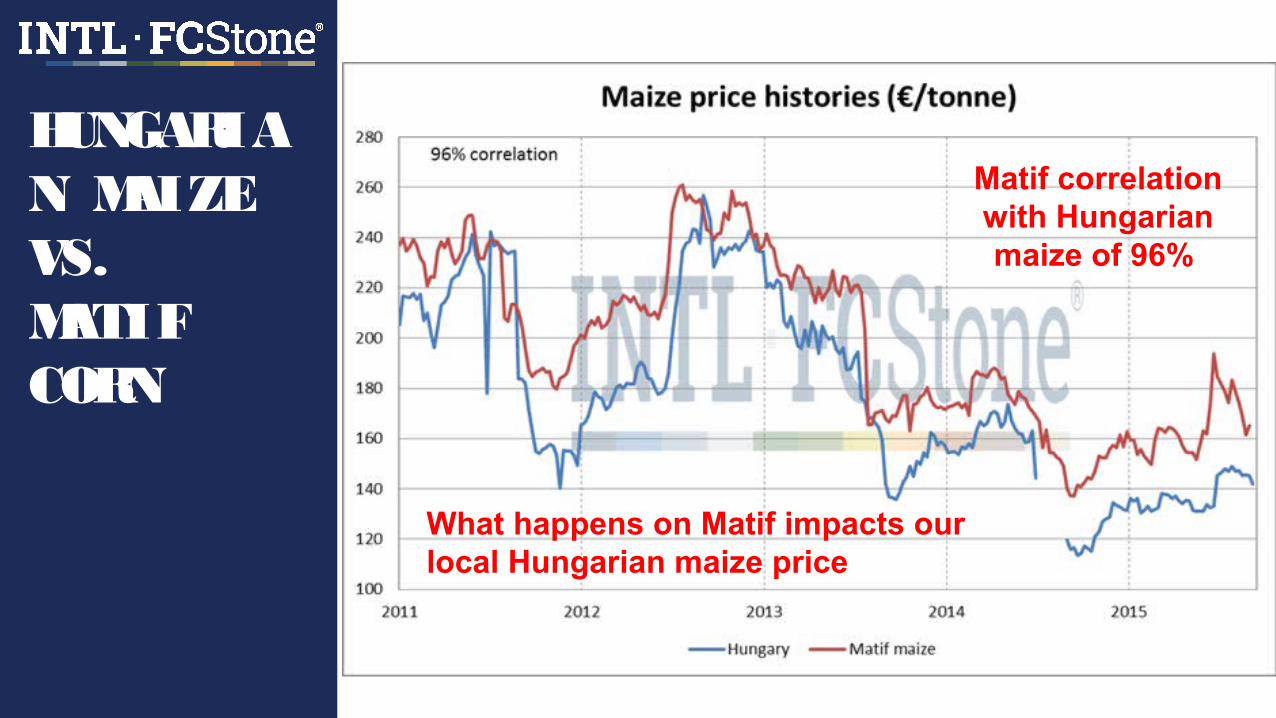

Matif correlation with Hungarian maize of 96%

What happens on Matif impacts our local Hungarian maize price

HUNGARIAN MAIZE VS. MATIF CORN

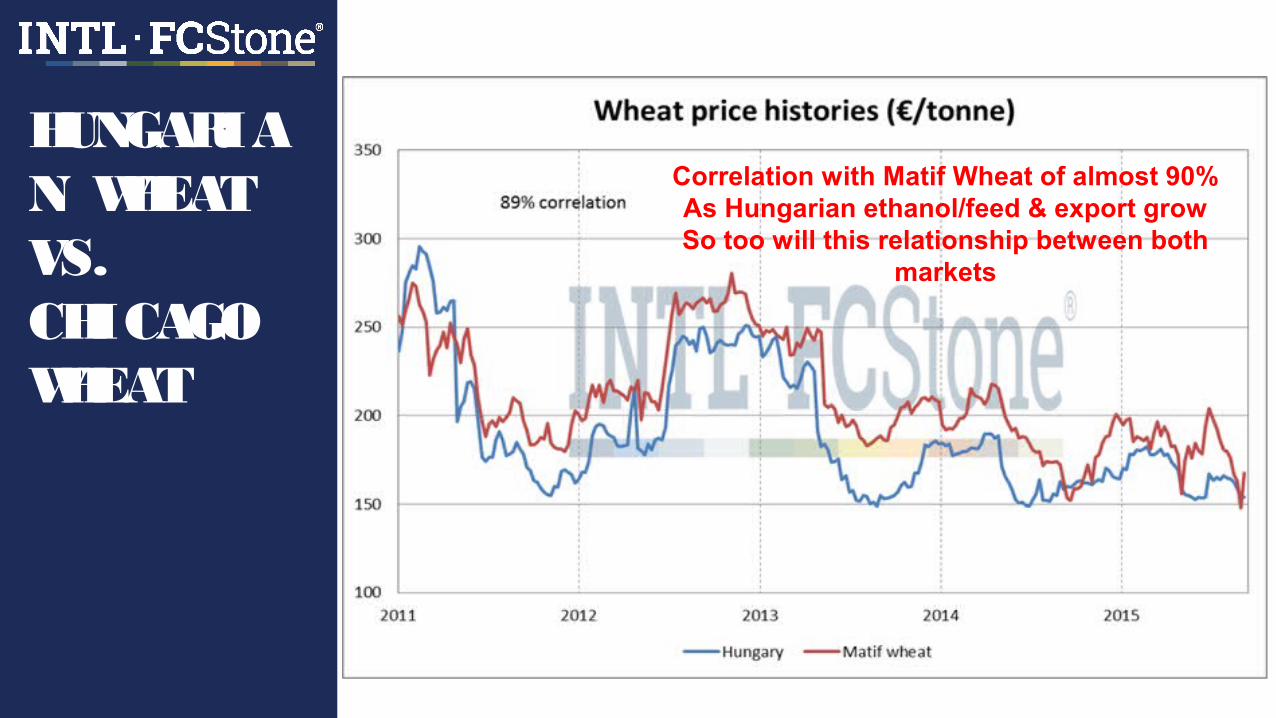

Correlation with Matif Wheat of almost 90%As Hungarian ethanol/feed & export growSo too will this relationship between both

markets

HUNGARIAN WHEAT VS. CHICAGO WHEAT

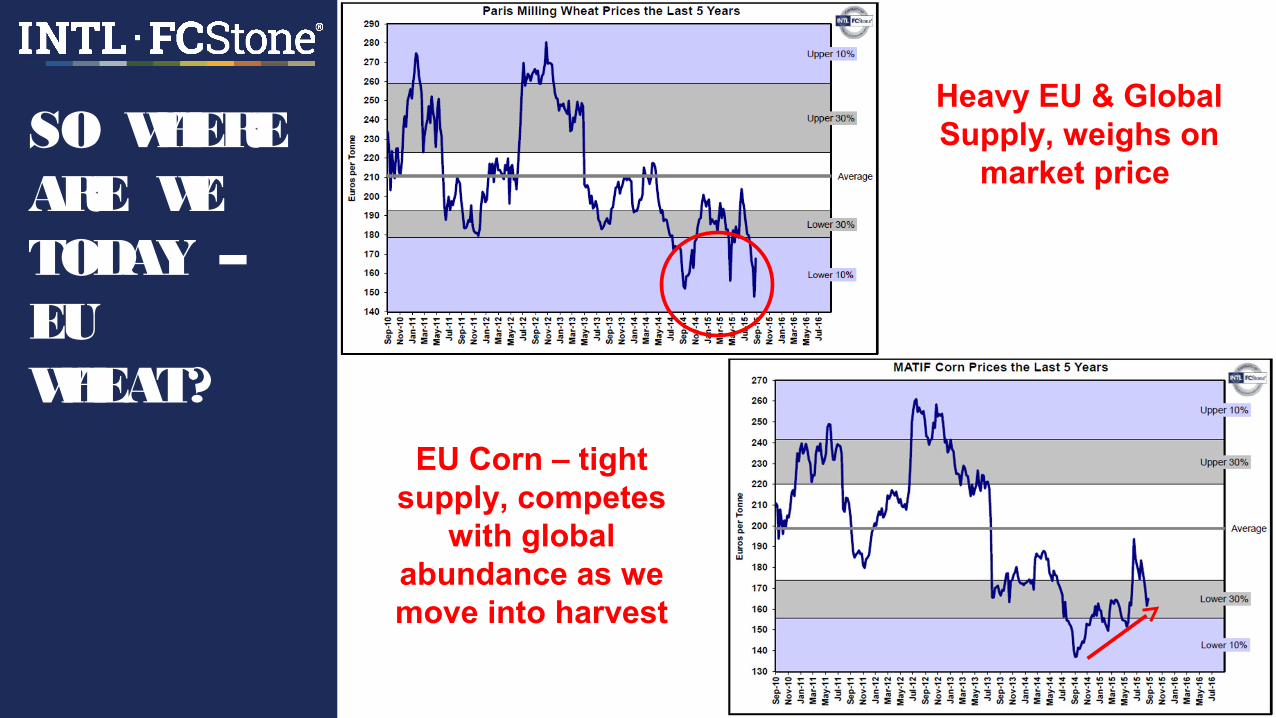

Heavy EU & Global Supply, weighs on

market price

EU Corn – tight supply, competes

with global abundance as we move into harvest

SO WHERE ARE WE TODAY – EU WHEAT?

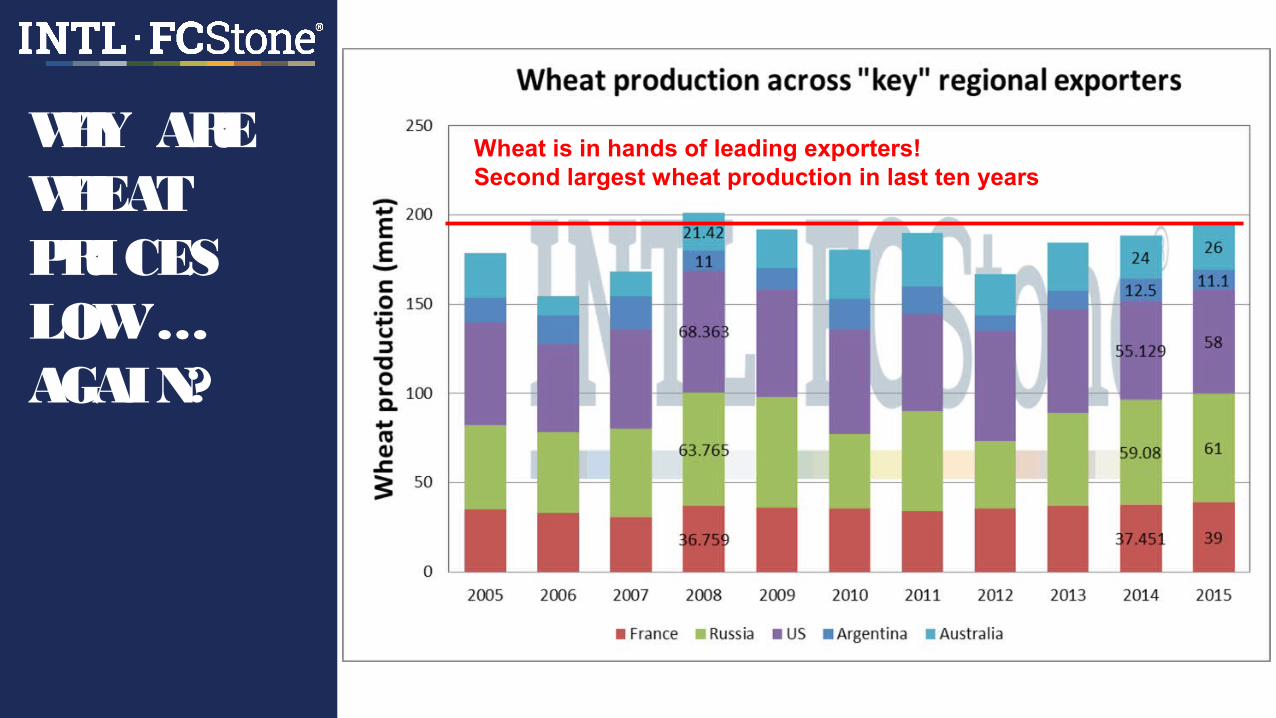

Wheat is in hands of leading exporters!Second largest wheat production in last ten years

WHY ARE WHEAT PRICES LOW … AGAIN?

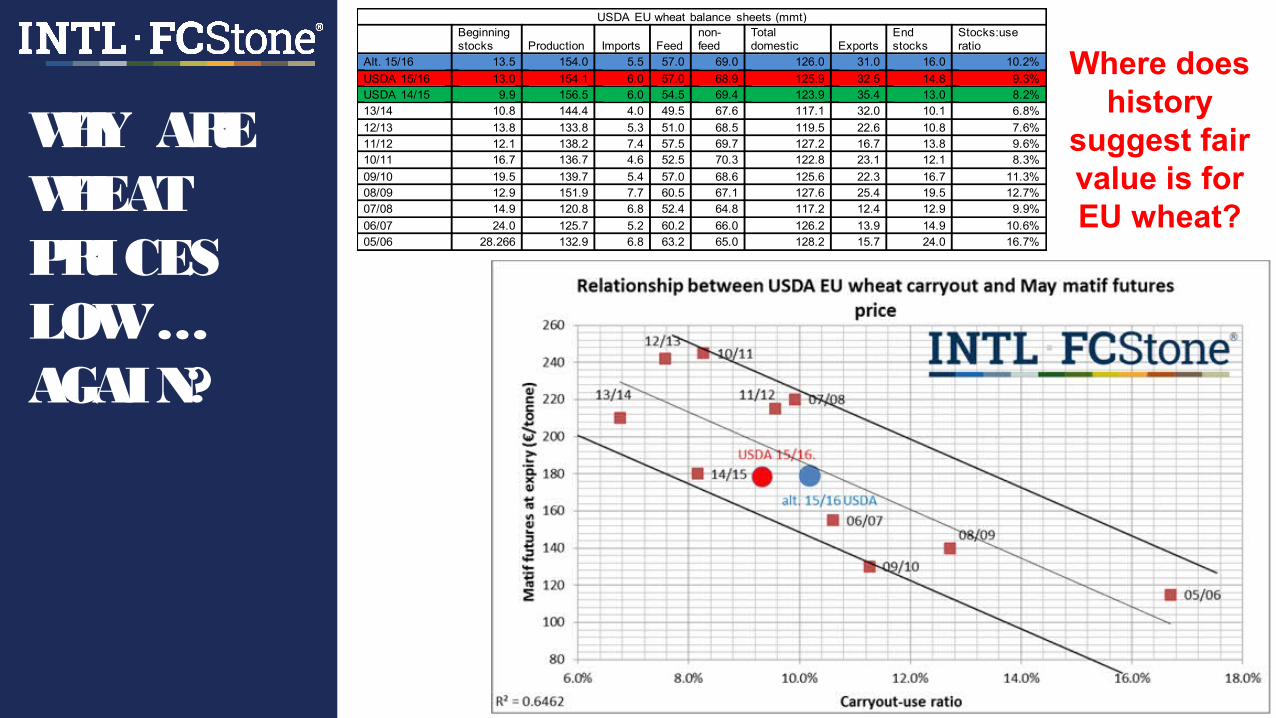

USDA EU wheat balance sheets (mmt)

Beginning stocks Production Imports Feed

non-feed

Total domestic Exports

End stocks

Stocks:use ratio

Alt. 15/16 13.5 154.0 5.5 57.0 69.0 126.0 31.0 16.0 10.2%

USDA 15/16 13.0 154.1 6.0 57.0 68.9 125.9 32.5 14.8 9.3% USDA 14/15 9.9 156.5 6.0 54.5 69.4 123.9 35.4 13.0 8.2% 13/14 10.8 144.4 4.0 49.5 67.6 117.1 32.0 10.1 6.8%

12/13 13.8 133.8 5.3 51.0 68.5 119.5 22.6 10.8 7.6% 11/12 12.1 138.2 7.4 57.5 69.7 127.2 16.7 13.8 9.6% 10/11 16.7 136.7 4.6 52.5 70.3 122.8 23.1 12.1 8.3%

09/10 19.5 139.7 5.4 57.0 68.6 125.6 22.3 16.7 11.3% 08/09 12.9 151.9 7.7 60.5 67.1 127.6 25.4 19.5 12.7% 07/08 14.9 120.8 6.8 52.4 64.8 117.2 12.4 12.9 9.9%

06/07 24.0 125.7 5.2 60.2 66.0 126.2 13.9 14.9 10.6% 05/06 28.266 132.9 6.8 63.2 65.0 128.2 15.7 24.0 16.7%

Where does history

suggest fair value is for EU wheat?

WHY ARE WHEAT PRICES LOW … AGAIN?

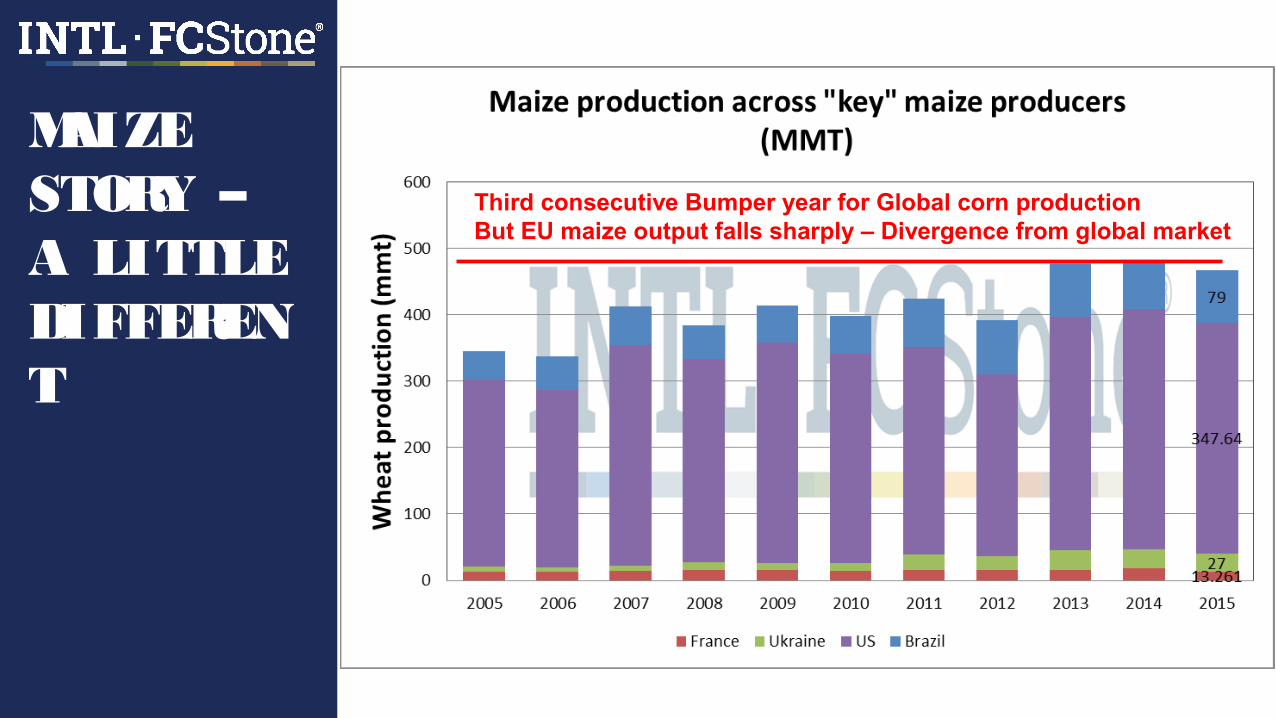

Third consecutive Bumper year for Global corn productionBut EU maize output falls sharply – Divergence from global market

MAIZE STORY – A LITTLE DIFFERENT

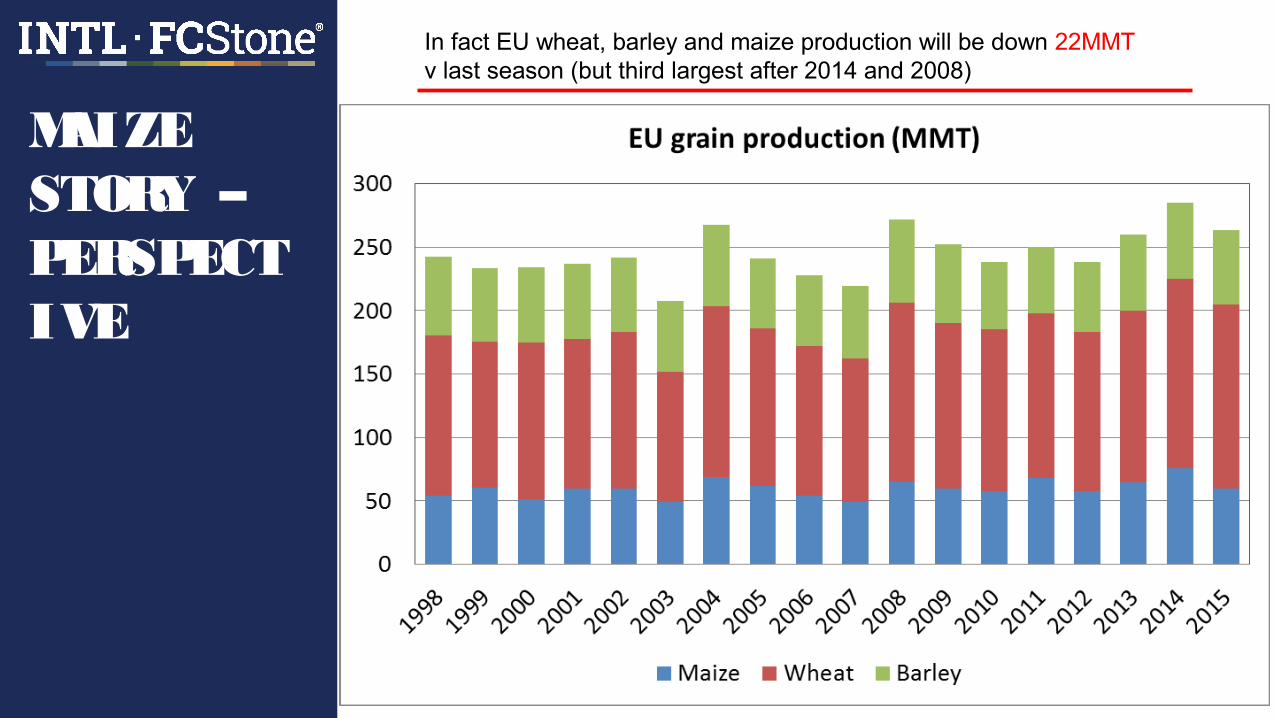

In fact EU wheat, barley and maize production will be down 22MMT v last season (but third largest after 2014 and 2008)

MAIZE STORY – PERSPECTIVE

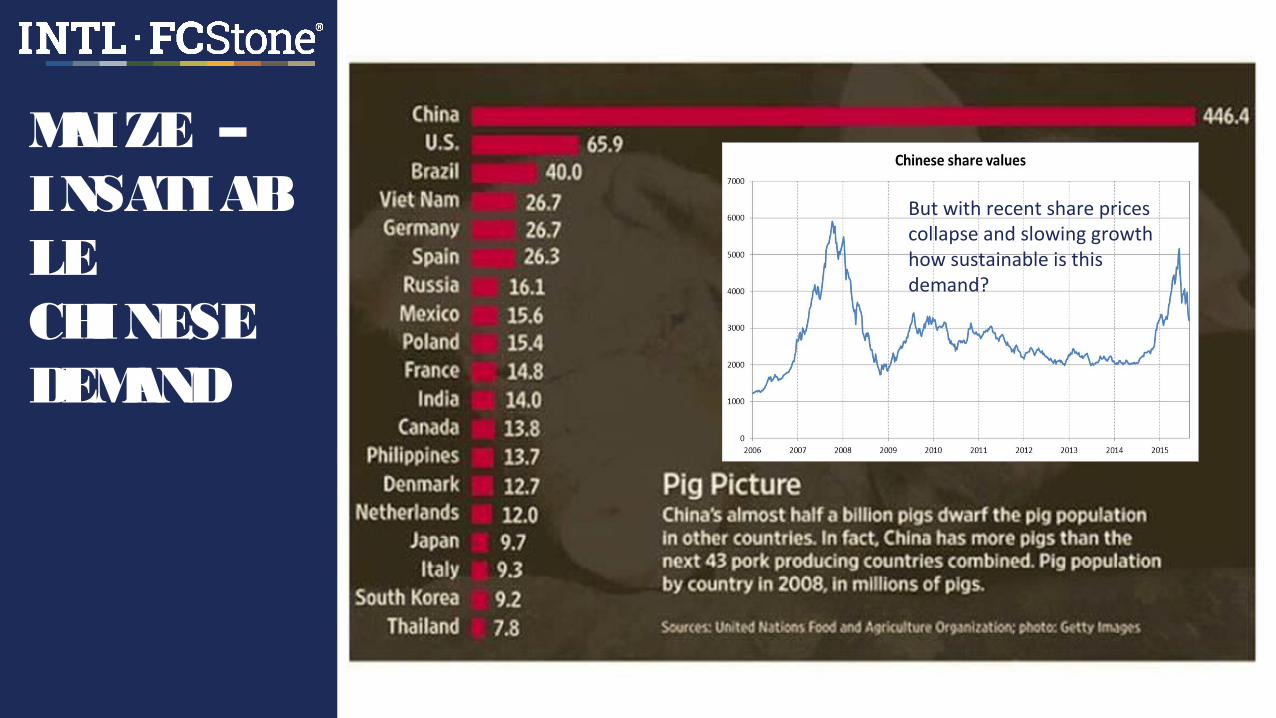

But with recent share prices collapse and slowing growth how sustainable is this demand?

MAIZE – INSATIABLE CHINESE DEMAND

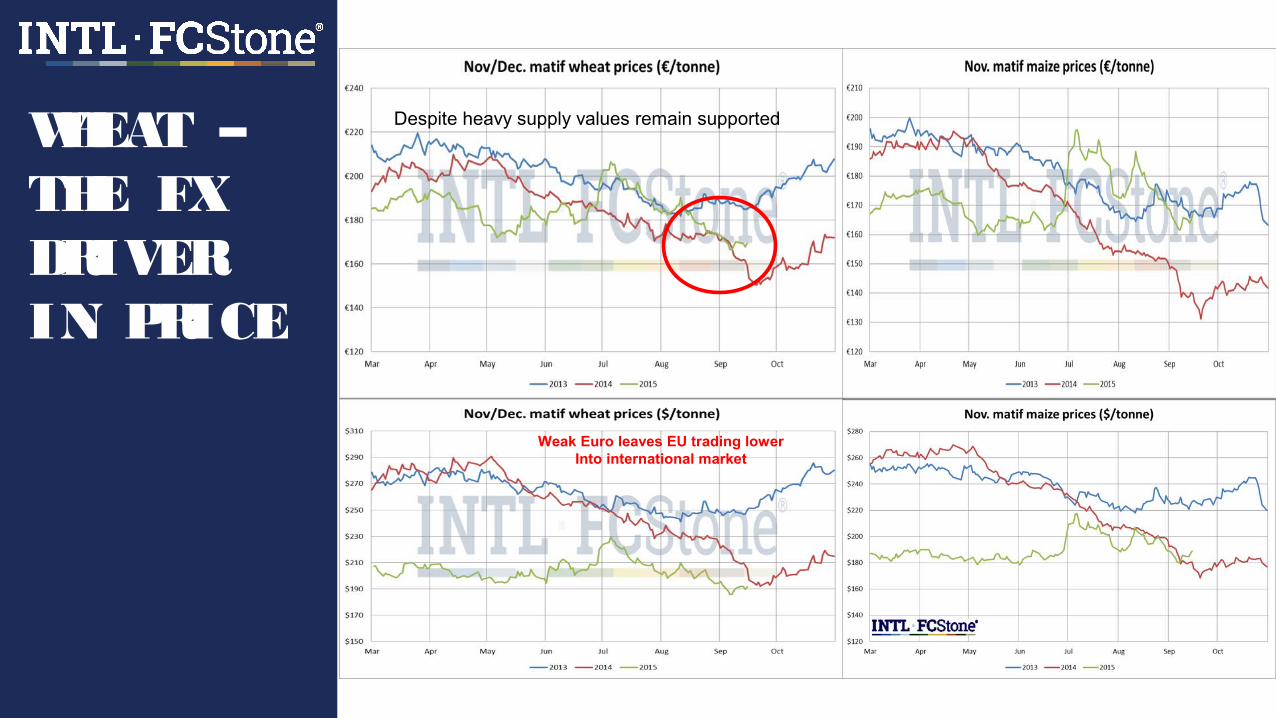

Despite heavy supply values remain supported

Weak Euro leaves EU trading lowerInto international market

WHEAT – THE FX DRIVER IN PRICE

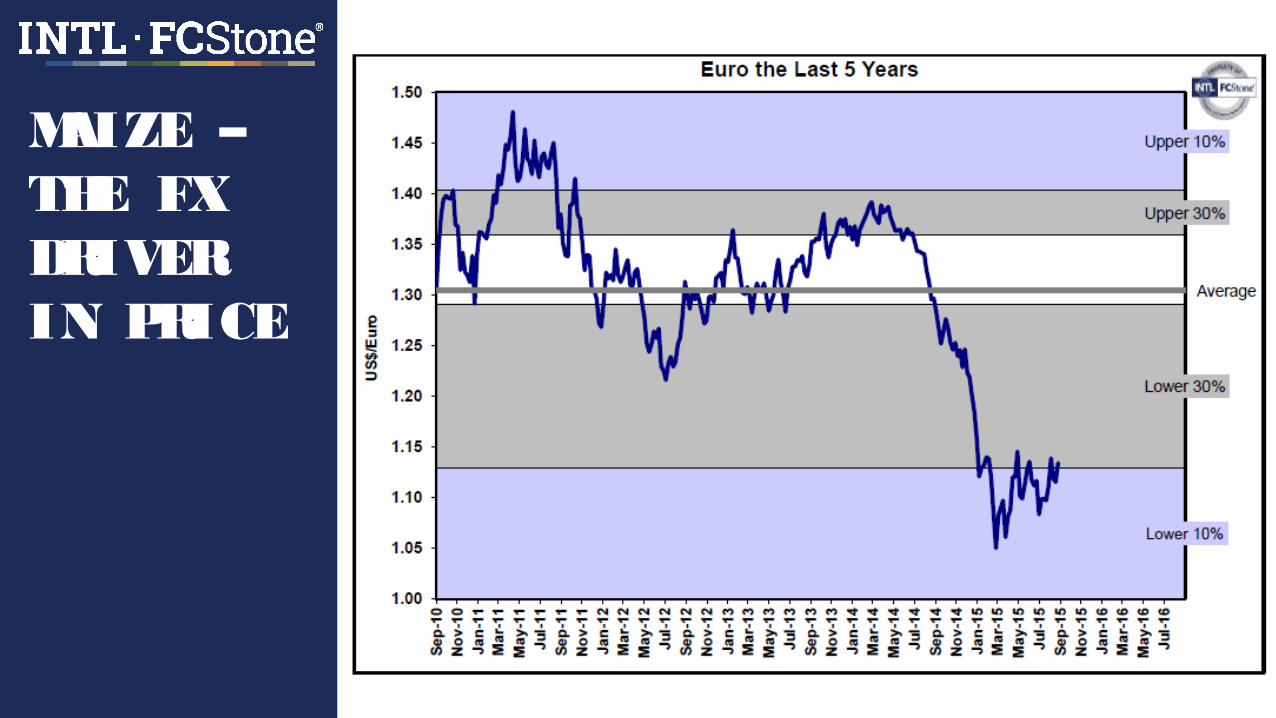

MAIZE – THE FX DRIVER IN PRICE

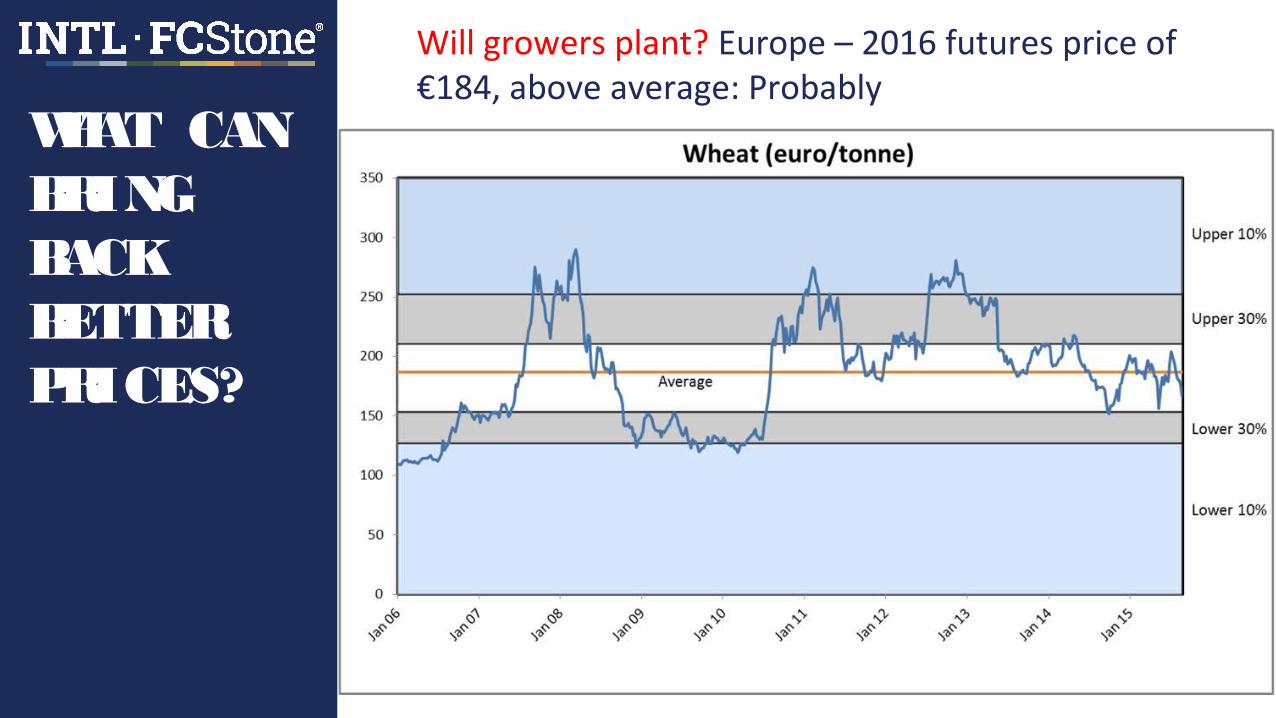

Will growers plant? Europe – 2016 futures price of €184, above average: Probably

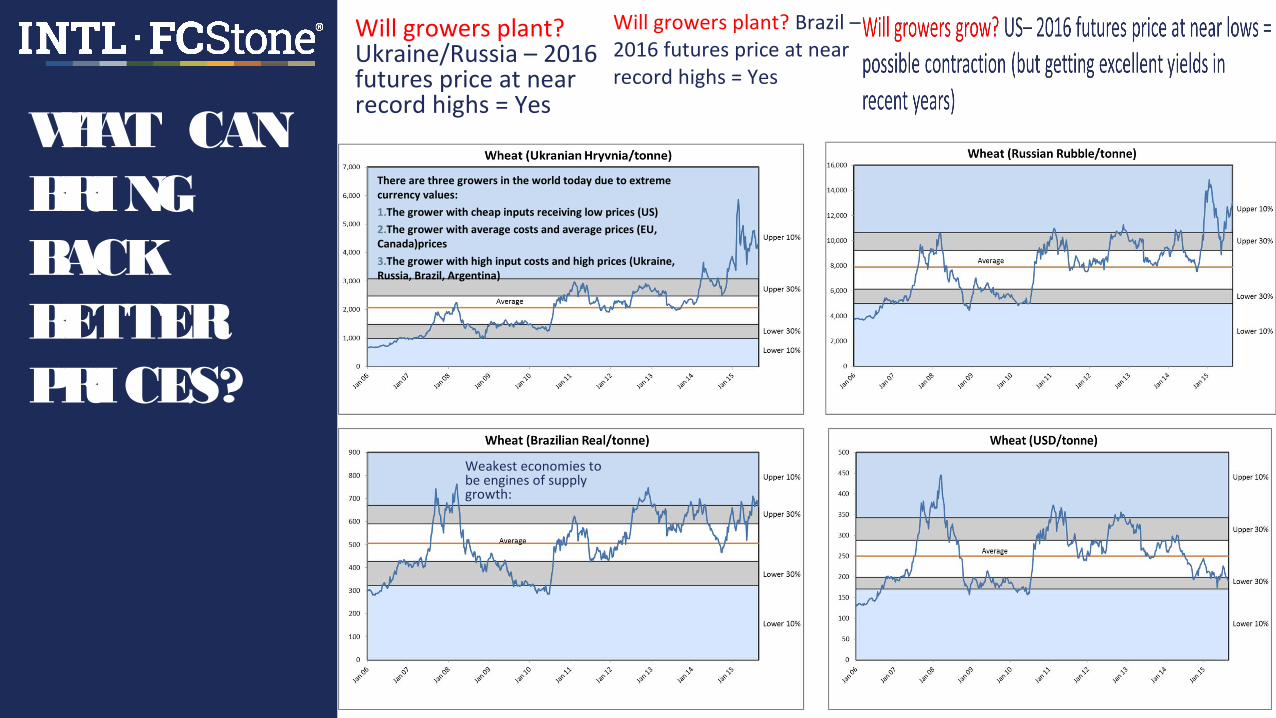

WHAT CAN BRING BACK BETTER PRICES?

Will growers plant? Ukraine/Russia – 2016 futures price at near record highs = Yes

Will growers plant? Brazil – 2016 futures price at near record highs = Yes

Weakest economies to be engines of supply growth:

There are three growers in the world today due to extreme currency values:

1.The grower with cheap inputs receiving low prices (US)

2.The grower with average costs and average prices (EU, Canada)prices

3.The grower with high input costs and high prices (Ukraine, Russia, Brazil, Argentina)

WHAT CAN BRING BACK BETTER PRICES?

When prices are low

When prices are high

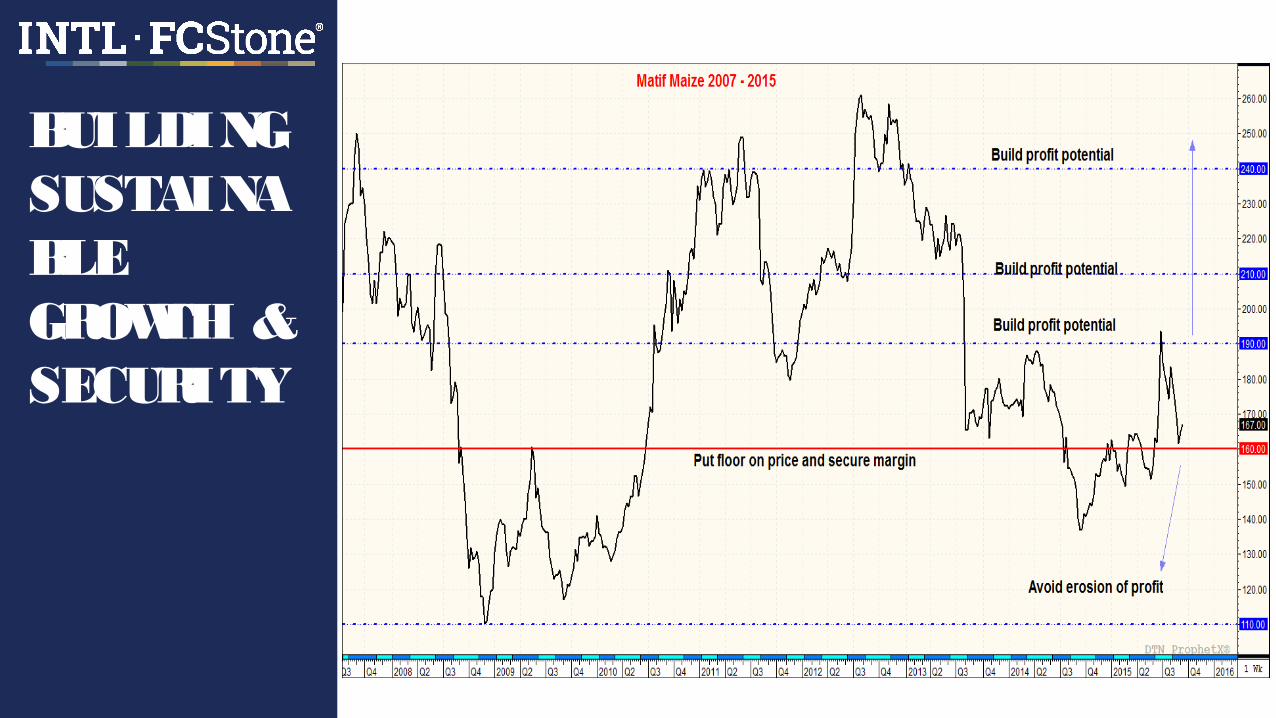

SO WHAT TO DO? WHERE TO FROM HERE?

Work with your partners to create certainty and profitability

Remove price volatility & secure margins

Forward contract and reduce downside price risk

Continue to Innovate and pioneer in grain production

Set the benchmark for international market

Create quality, quantity, reliability and sustainability

Development and investment – key to success

HOW DO WE SECURE MARGINS/INCREASE PROFIT?

BUILDING SUSTAINABLE GROWTH & SECURITY