PALFINGER BilPK 2012 d eng RS

38

PALFINGER AG Record year with exceptional increase in earnings Presentation on the 2011 financial year February 2012

Transcript of PALFINGER BilPK 2012 d eng RS

PALFINGER AGRecord year with exceptional increase in earnings

Presentation on the 2011 financial yearFebruary 2012

Market volatility

2

Importance of flexibility and internationality is increasing

-50

50100150200250300350400450500

2005 2006 2007 2008 2009 2010 2011

Revenue (half year)AREA UNITSEUROPEAN UNITS

0

Acc. to IFRS in EUR million.

Highlights 2011 (1)

• Further increase in revenue of 30% – historic record• Exceptionally strong increase in earnings: EBIT + 83%• Internationalization and flexibility support sustainable growth

High growth rates outside Europe (Brazil, North America, Asia)CIS becomes important market for PALFINGER following acquisition of INMANMajority takeover of Palfinger Crane Rus (Area Management CIS)Share buyback and authorized capital create flexibility in financing growth measures

3

Highlights 2011 (2)

• PALFINGER once again outperformer in its industry • Growth achieved in nearly all product areas and regions

Great success in the field of offshore wind energy

• Basis created for maintaining the high level in the years to come• Proposed dividend: EUR 0.38 per share

4

Strategy

PALFINGER at a glance

• Leading international manufacturer of innovative lifting, loading and handling systems

Number one in knuckle boom cranes, timber and recycling cranesand hookloadersNumber two in tail lifts and transportable forkliftsLeading specialist in high-tech railway system solutions

• Global distribution and service network(more than 200 general importers/dealers and 4,500 sales and service centres worldwide)

• Global procurement, production and assembly (28 manufacturing and assembly locations)

• Strategic pillars: Innovation – internationalization – flexibility

6

Maintaining and expanding the Group’s competitive advantage

Strategic objectives 2015

• Diversification will be limited to the core competences • Further increase in flexibility is a priority (strategic pillar)• Internationalization directed towards future markets (Russia, Asia)• Innovation as basis for enhancement of products and services

Catering to regional requirements

• Profitability of all business units – targeted packages of measures

7

Continuation of sustainably profitable growth

Strategic highlights 2011

• Innovation: Research and development a priorityDevelopment of a new crane series Product adjustments to meet specific regional requirements Further development in the field of electronics and mechatronics

• Internationalization: Focus on future marketsAssembly activities started in India Continuous consolidation of market presence in Russia – INMAN acquisitionMarket positioning strategy for China

• Flexibility: 3rd pillar of the Group’s strategyIncrease in flexibility at all value-creation levels Continuation of structural and cost-related programmes

8

Internationalization

9

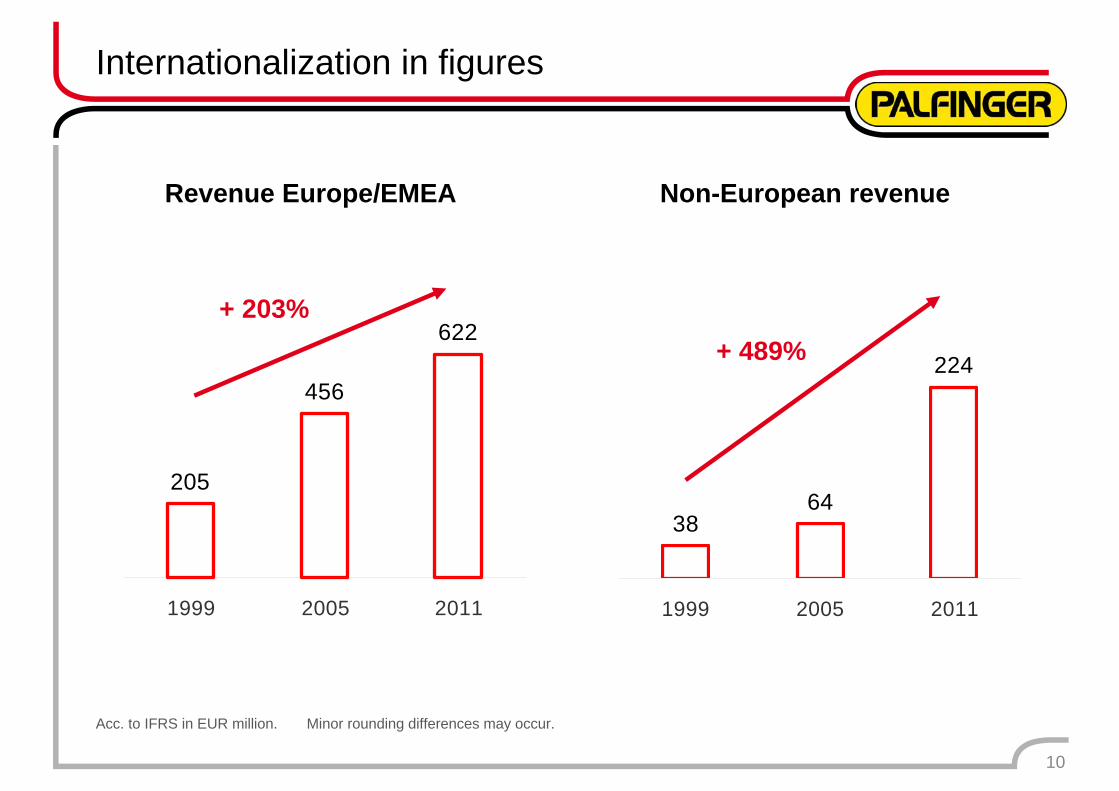

Revenue 2006

87.5% EUROPEAN UNITS

12.5% AREA UNITS

73.5% EUROPEAN UNITS

Revenue 2011

26.5% AREA UNITS

3864

224

1999 2005 2011

205

456

622

1999 2005 2011

Internationalization in figures

Acc. to IFRS in EUR million. Minor rounding differences may occur.

Revenue Europe/EMEA Non-European revenue

+ 489%+ 203%

10

INMAN acquisition

• Leading Russian crane manufacturer (Republic of Bashkortosan)Approx. 400 employeesRevenue 2011: EUR 20.5 million

• Local value creation and recognized product• Expansion of sales and service network

In particular in the Ural region

• Initial consolidation with effect from 26 August 2011

11

28 production sites

12

Lengau/AUT Köstendorf/AUT Elsbethen/AUT Löbau/GER Krefeld/GER

Seifhennersdorf/GER

Ganderkesee/GER

Welwyn Garden City/GBR Cadelbosco/ITA Caussade/FRA

Delnice/CRO

Barneveld/NED Maribor/SLO

Tenevo/BUL Cherven Brjag/BUL

Tiffin/USA Oklahoma City/USANiagara Falls/CAN Trenton/USA

Caxias do Sul/BRA

Cerritos/USACouncil Bluffs/USA

Shenzhen/CHN Hanoi/VIE Chennai/IND

Lazuri/ROUSkrljevo/CRO Ishimbay/RUS

Product portfolio

13

• Truck-mounted knuckle boom cranes• MADAL telescopic cranes• EPSILON timber and recycling cranes• OMAHA STANDARD truck bodies• Marine cranes (incl. davits)• Cranes for offshore wind energy plants• PALIFT/OMAHA STANDARD

hookloaders• RAILWAY rail transport system

solutions• CRAYLER transportable forklifts• RATCLIFF/MBB tail lifts and passenger

lifts• BISON/WUMAG ELEVANT/ETI access

platforms

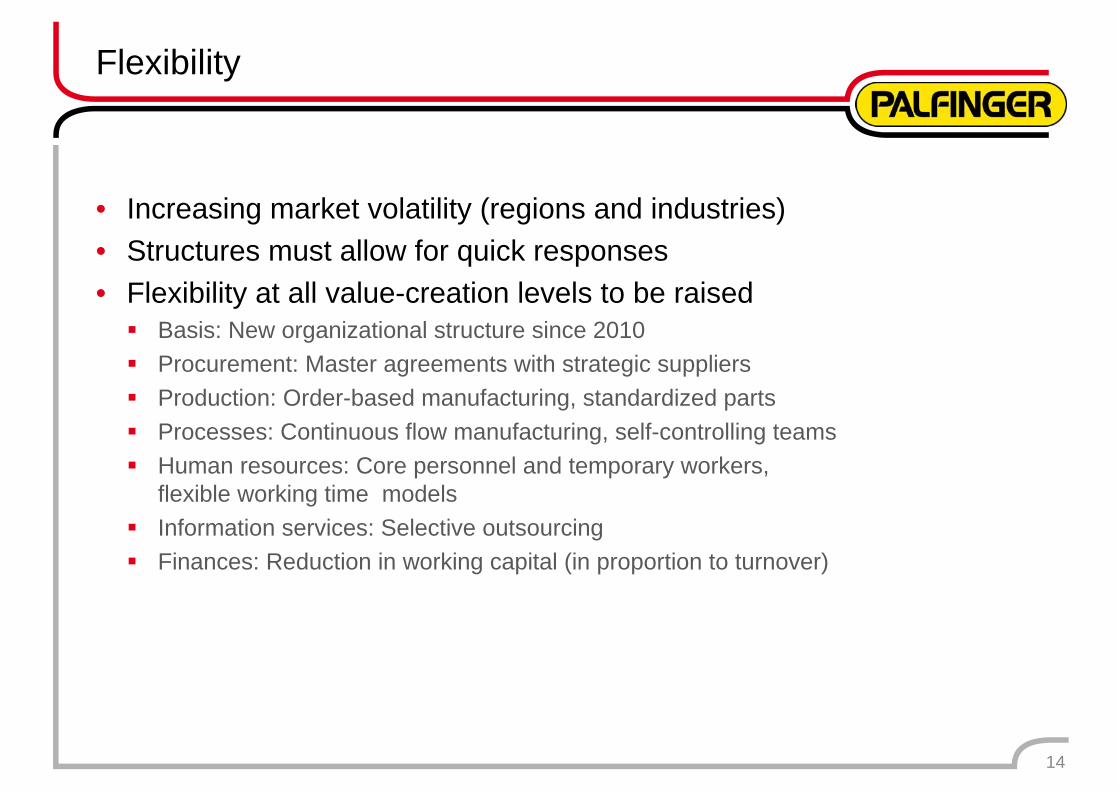

Flexibility

• Increasing market volatility (regions and industries)• Structures must allow for quick responses• Flexibility at all value-creation levels to be raised

Basis: New organizational structure since 2010Procurement: Master agreements with strategic suppliersProduction: Order-based manufacturing, standardized partsProcesses: Continuous flow manufacturing, self-controlling teamsHuman resources: Core personnel and temporary workers, flexible working time modelsInformation services: Selective outsourcingFinances: Reduction in working capital (in proportion to turnover)

14

Segments

Segment financials

16

Acc. to IFRS in EUR million. Minor rounding differences may occur.

Segment revenue

2010 2011 %

EUROPEAN UNITS 479.2 621.8 + 29.8%AREA UNITS 172.6 223.9 + 29.7%

VENTURES – – –

Segment EBIT

2010 2011 %

EUROPEAN UNITS 52.7 80.1 + 51.9%AREA UNITS (7.6) (1.1) + 85.5%

VENTURES (7.7) (10.3) (33.0%)

EUROPEAN UNITS segment

• Revenue increased by 30%Increases in nearly all product areas, particulary in cranesBusiness unit Marine Systems contributed approx. 1/3 to this increaseStagnation in railway systems

• Hoodloaders sustainably profitable • Segment EBIT increased from EUR 53 million to EUR 80 million• Market shares gained in timber and recycling cranes and access

platforms• Success achieved in the field of offshore wind energy

17

AREA UNITS segment

• Revenue increased by 30%, success achieved reflected in earningsAdditional one-time effect from acquisitions

• Strong upward trend, particularly in North America• Establishment of new products in South America • Strong growth in Asia, still at a low level • Distribution continues to be successful in India• CIS becomes important market for PALFINGER following acquisition

of INMAN

18

VENTURES unit

• Continuation of cost-related and structural programmes • Acquisition of INMAN completed• Intensive development of strategic options for China

19

Key financial figures

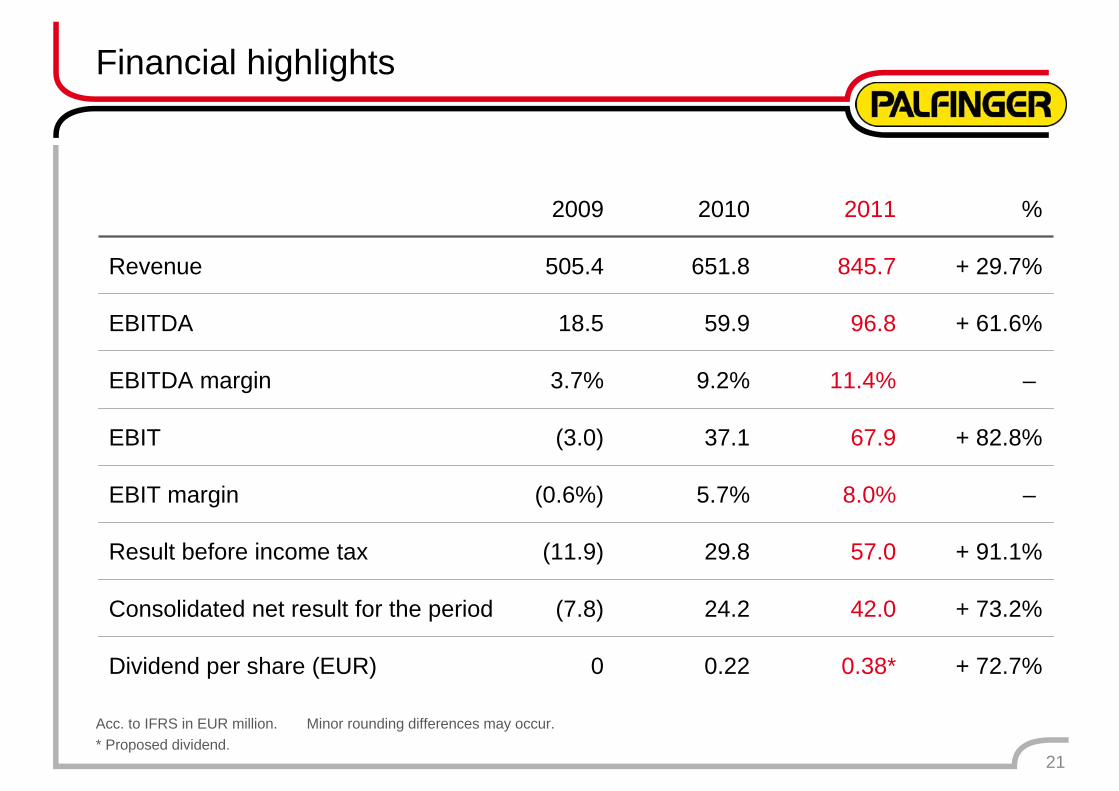

Financial highlights

2009 2010 2011 %

Revenue 505.4 651.8 845.7 + 29.7%

EBITDA 18.5 59.9 96.8 + 61.6%

EBITDA margin 3.7% 9.2% 11.4% –

EBIT (3.0) 37.1 67.9 + 82.8%

EBIT margin (0.6%) 5.7% 8.0% –

Result before income tax (11.9) 29.8 57.0 + 91.1%

Consolidated net result for the period (7.8) 24.2 42.0 + 73.2%

Dividend per share (EUR) 0 0.22 0.38* + 72.7%

21

Acc. to IFRS in EUR million. Minor rounding differences may occur. * Proposed dividend.

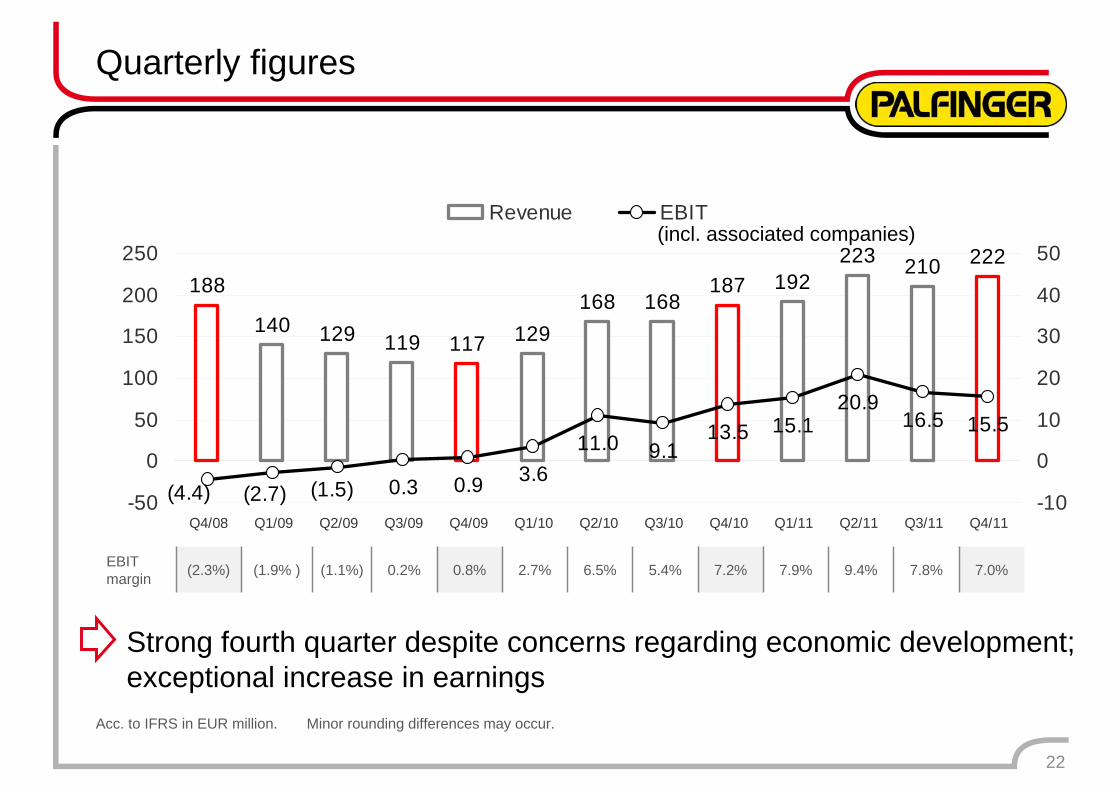

Quarterly figures

22

EBITmargin (2.3%) (1.9% ) (1.1%) 0.2% 0.8% 2.7% 6.5% 5.4% 7.2% 7.9% 9.4% 7.8% 7.0%

Strong fourth quarter despite concerns regarding economic development;exceptional increase in earnings

(incl. associated companies)

Acc. to IFRS in EUR million. Minor rounding differences may occur.

188

140 129 119 117 129168 168

187 192223 210 222

0.3 0.9 3.611.0 9.1

13.5 15.120.9

16.5 15.5

(1.5)(2.7)(4.4)-50

0

50

100

150

200

250

Q4/08 Q1/09 Q2/09 Q3/09 Q4/09 Q1/10 Q2/10 Q3/10 Q4/10 Q1/11 Q2/11 Q3/11 Q4/11-10

0

10

20

30

40

50

Revenue EBIT

242 306 311 378 386

131170 133

103 134

0

100

200

300

400

500

600

2007 2008 2009 2010 2011

Net working capital (in relation to revenue)

Non-current operating assets

Capital employed*

* As at the reporting date.Acc. to IFRS in EUR million. Minor rounding differences may occur.

23

(19%)(21%) (26%)

(16%) (16%)373

477 444520

Increase due to business expansion, relation to revenue constant

481

Return on capital employed

Acc. to IFRS in EUR million. Minor rounding differences may occur.

24

80.3 55.6

443.8480.7

519.6

55.5

32.7(0.1)

476.7

373.1

11.1%7.1%0.0%

13.1%25.7%

-100

0

100

200

300

400

500

600

2007 2008 2009 2010 2011-10%

0%

10%

20%

30%

40%

50%

NOPLAT Capital employed Return on capital employed %

Investment

25

61.4

46.5

8.014.6 18.615.6

28.721.5 22.7

28.8

0102030

40506070

2007 2008 2009 2010 2011

Investment in property, plant, and equipment

Depreciation, amortization, and impairment

Acc. to IFRS in EUR million. Minor rounding differences may occur.

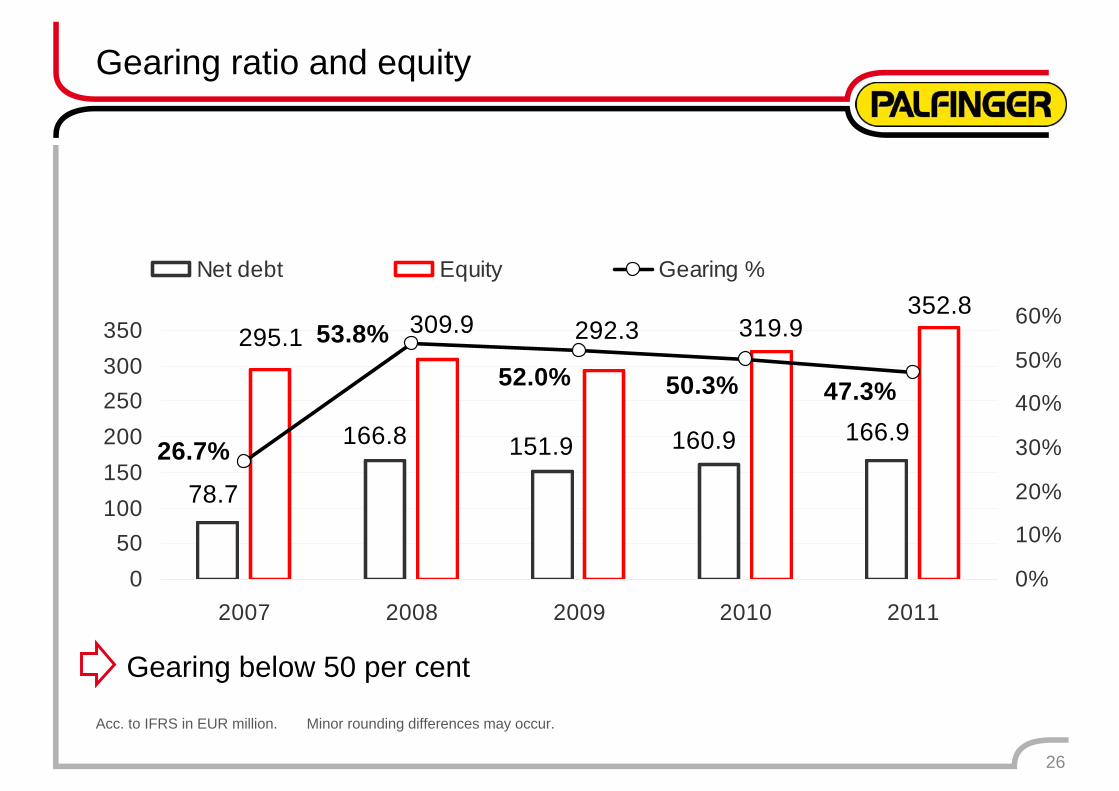

Gearing ratio and equity

26

Gearing below 50 per cent

319.9

78.7

166.8 166.9151.9 160.9

292.3309.9352.8

295.1

26.7%

52.0%53.8%

50.3% 47.3%

050

100150200250300350

2007 2008 2009 2010 20110%

10%

20%

30%

40%

50%

60%

Net debt Equity Gearing %

Acc. to IFRS in EUR million. Minor rounding differences may occur.

320 353

195 161

162 226

0

200

400

600

800

2010 2011

Current liabilitiesNon-current liabilitiesEquity

381 392

296 348

0

200

400

600

800

2010 2011

Current assetsNon-current assets

Balance sheet structure

Acc. to IFRS in EUR million. Minor rounding differences may occur.

27

Long-term financial structure; promissory note loan due in 2012

677 740

Assets Liabilities

677 740

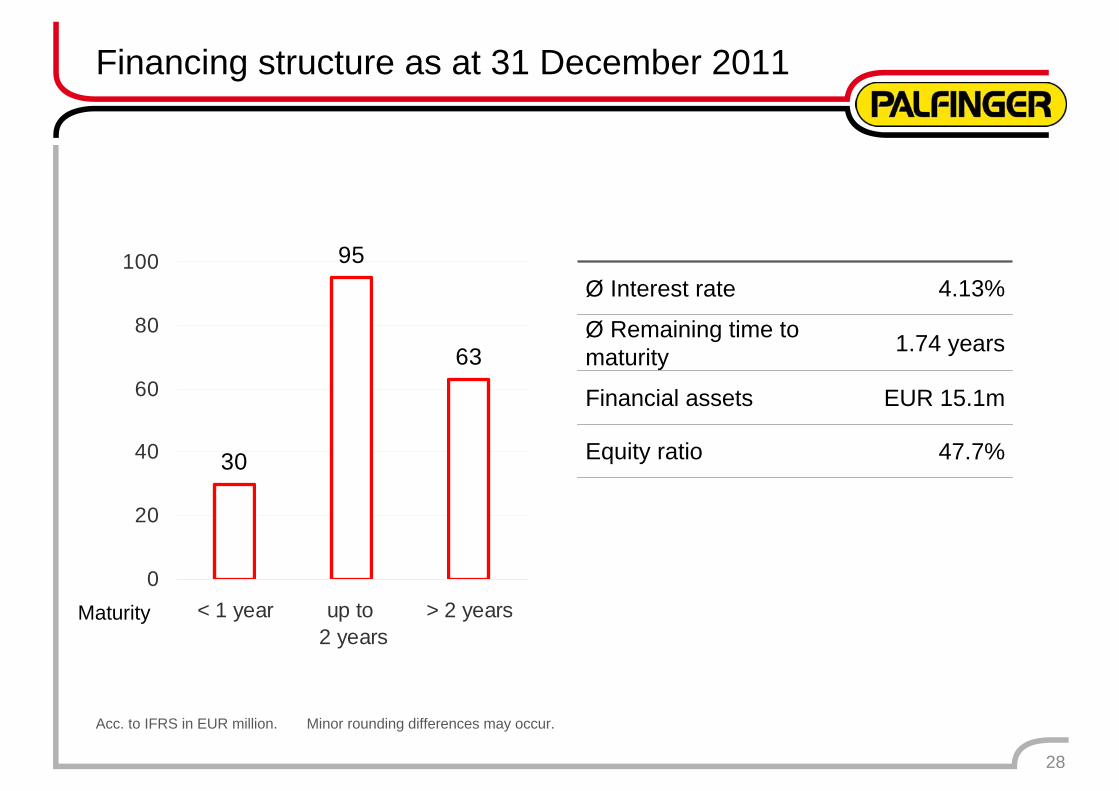

Financing structure as at 31 December 2011

Acc. to IFRS in EUR million. Minor rounding differences may occur.

28

Ø Interest rate 4.13%

Ø Remaining time to maturity 1.74 years

Financial assets EUR 15.1m

Equity ratio 47.7%

Maturity

30

95

63

0

20

40

60

80

100

< 1 year up to 2 years

> 2 years

Free cash flows

Acc. to IFRS in EUR million. Minor rounding differences may occur.

29

(17.2)

(17.0)

42.0

7.8

34.2

(15.9)50.0(2.1)41.51.09.6

2009 2010 2011EBTDA 52.6 85.6+/– Cash flows from companies at equity 1.5 (7.9)+/– Cash flows from working capital (1.2) (28.7)+/– Cash flows from tax payments (3.8) (11.3)Cash flows from operating activities 49.1 37.7+/– Cash flows from investing activities (54.1) (34.6)Cash flows after changes in working capital & investments (5.0) 3.1

+/– Cash flows from interest on borrowingsadjusted by tax expense 9.1 8.6

Free cash flows 4.2 11.7

Cash flows from equity/investor capital (1.1) (12.1)

Cash flows from net debt 6.1 9.0

PALFINGER share

30

ISIN AT0000758305

Number of sharesthereof own shares

35,730,000368,840

Share price as at end of period EUR 12.33

Market capitalization EUR 440.6m

65%Palfinger family

Shareholder structure Shareholder informationas at 30 December 2011

29%free float

1% PALFINGER AG

5% Delta Lloyd

Outlook

Outlook and objectives – internally

32

• Internationalization strategy to be continuedFocus on Asia, particularly China, and RussiaExpansion of product portfolio in the areas

• Further increase in flexibility throughout all units • Complexity management is a priority• Research, development and innovation

Regional product adjustmentsGradual introduction of a new crane series

• Further strengthening of weaker units and areas

Outlook and objectives – externally

• High level of uncertainty in the financial markets impacts real economy

• Situation for PALFINGER clearly better than in 2008/09• Strong fourth quarter signals continued good order situation• Market growth in non-European regions expected

33

PALFINGER strives to increase revenue slightly in 2012 as well

Research reports

Berenberg Bank Hauck & AufhäuserCheuvreux HSBCDeutsche Bank RCBErste Group UBSGoldman Sachs

34

Earnings estimates – consensus (in EUR million) 2012e 2013e

Revenue 806.5 865.3EBIT 62.0 78.8

Earnings per share (EUR) 1.03 1.43

Financial calendar 2012

35

3 February 2012 Balance sheet press conference

16 February 2012 Publication of Annual Report 2011

8 March 2012 Annual General Meeting

12 March 2012 Ex-dividend day

14 March 2012 Dividend payment day

10 May 2012 Publication of resultsfor the first quarter of 2012

9 August 2012 Publication of resultsfor the first half of 2012

9 November 2012 Publication of resultsfor the first three quarters of 2012

Investor relations

36

Herbert Ortner, CEOPhone: +43 662 46 84-2222

Hannes Roither, Company SpokespersonPhone: +43 662 46 84-2260

PALFINGER AGFranz-Wolfram-Scherer-Strasse 24

5020 Salzburg Fax: +43 662 46 84-2280

This presentation contains forward-looking statements made on the basis of all information available at the time of preparation of this presentation. Actual outcomes and results may be substantially different from those predicted.

Backup

60

80

100

120

140

160

180

200

Performance of the PALFINGER share since 2010

38

4 Jan 2010 3 Jan 2011 30 Dec 2011

PALFINGER AGEUR 12.33

ATX

DAX