Pace Oil and Gas Investor Presentation

28

An Intermediate-Sized Real Growth Company Oil Growth Drives Cash Flow Investor Update | 2011 Year End | March 2012 “BUILDING A TOP TIER ENERGY COMPANY, BUILDING IN GROWTH, BUILDING UP VALUE.”

-

Upload

company-spotlight -

Category

Investor Relations

-

view

897 -

download

1

description

Transcript of Pace Oil and Gas Investor Presentation

An Intermediate-Sized

Real Growth Company Oil Growth Drives Cash Flow

Inv

esto

r U

pd

ate

| 2

011 Y

ear

En

d

| M

arc

h 2

012

“BUILDING A TOP TIER ENERGY COMPANY,

BUILDING IN GROWTH, BUILDING UP VALUE.”

2 PACE OIL & GAS | Q4 & YE UPDATE | MARCH 2012

Forward Looking Statements

Forward-Looking Statements: This presentation contains certain forward-looking statements and forward-looking

information (collectively referred to herein as "forward-looking statements") within the meaning of applicable Canadian

securities laws. All statements other than statements of present or historical fact are forward-looking statements. In some

cases, forward-looking statements can be identified by terminology such as "may", "will", "should", "believes", "expects",

"intends", "projects", "plans", "anticipates", “positions”, “potential”, “objective”, “continuous”, “ongoing”, "estimates" or

"contains" or similar words or the negative thereof. In particular, this presentation contains forward-looking statements

relating to: the estimated production of Pace Oil & Gas Ltd. (“Pace”), the estimated reserves of Pace Oil & Gas Ltd., the

estimated pro-forma funds from operation of Pace Oil & Gas Ltd., the expected credit facility available to Pace Oil & Gas

Ltd., the anticipated number of wells and completions to be carried out, the anticipated replacement production from our

new completions, the expected reserve additions, future plans and expenditures of Pace Oil & Gas Ltd., the forecasted

commodity prices.

These statements represent management's expectations or beliefs concerning, among other things, future capital

expenditures and future operating results and various components thereof or the economic performance of Pace and

include, without limitation, statements with respect to the future financial position, business strategy, budgets, projected

costs and plans, objectives of or involving Pace or any of its respective affiliates; access to credit facilities; capital taxes;

income taxes; commodity prices; administration costs; commodity price risk management activities; expectation of future

production rates and components of cash flow and earnings. Actual events or results may differ materially. The

projections, estimates and beliefs contained in such forward-looking statements are based on management's estimates,

opinions and assumptions at the time the statements were made including assumptions relating to the production

performance of Pace’s oil and gas assets, the cost and competition for services throughout the oil and gas industry in

2012 and beyond and the continuation of the current regulatory and tax regime in Canada, and necessarily involve known

and unknown risks and uncertainties which may cause actual performance and financial results in future periods to differ

materially from any projections of future performance or results expressed or implied by such forward-looking statements.

Accordingly, readers are cautioned that events or circumstances could cause results to differ materially from those

predicted. Pace does not undertake to update any forward-looking information contained in this presentation whether as

to new information, future events or otherwise except as required by securities rules and regulations. Barrels of Oil

Equivalency: Barrels of oil equivalent (BOE's) may be misleading, particularly if used in isolation. In accordance with NI

51-101, a BOE conversion ratio for natural gas of 6 Mcf:1 bbl has been used, which is based on an energy equivalency

conversion method primarily applicable at the burner tip and does not represent a value equivalency at the wellhead.

PACE OIL & GAS | Q4 & YE UPDATE | MARCH 2012 3

Corporate Overview Strong Real Growth

Top tier growth - oil weighted & cash flow per share

Strong Performance Metrics

High quality, long life, oil weighted assets

Significant Upside

Portfolio of top tier resource plays

Multiple valued-added visible growth opportunities

Significant upside potential/large scale catalysts

Continued Strong (Real) Growth –

Oil Weighted and Cash Flow per share

will deliver multiple expansion

PACE OIL & GAS | Q4 & YE UPDATE | MARCH 2012 4

Corporate Highlights

Current – December 31, 2011

Basic Shares Outstanding (mm) 47.2

FD Shares Outstanding (mm) 51.0

Bank Debt (mm) $151

Net Debt (mm) $186

Credit Facility (mm) (1) $275

Proved Reserves (mmboe) (2) 44.5

2P Reserves (mmboe) (2) ~50% Oil 69.6

2012 Outlook (3)

Est. Production (boe/d) 14,500 - 15,250

Oil & NGLs (bbls/d) 7,200 - 7,500

CapEx 2012 (mm) $90 - 100

Production Mix 50% - 52% Oil 1. Banking syndicate - CIBC, NBF, BMO, BNS, HSBC, ATB – renewed December 2011

2. Reserves December 31, 2011 evaluated by McDaniels & Associates Consultants Ltd.

3. $95/bbl WTI, $3.00/mcf AECO

PACE OIL & GAS | Q4 & YE UPDATE | MARCH 2012 5

3,531 3,542 4,668

5,391 5,868 6,077 6,061

6,965

8,000

9,808 10,271

12,403

13,089

14,141 14,262

13,558

14,205

15,000

-

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000Gas (boe/d)

Oil+NGL (bbls/d)

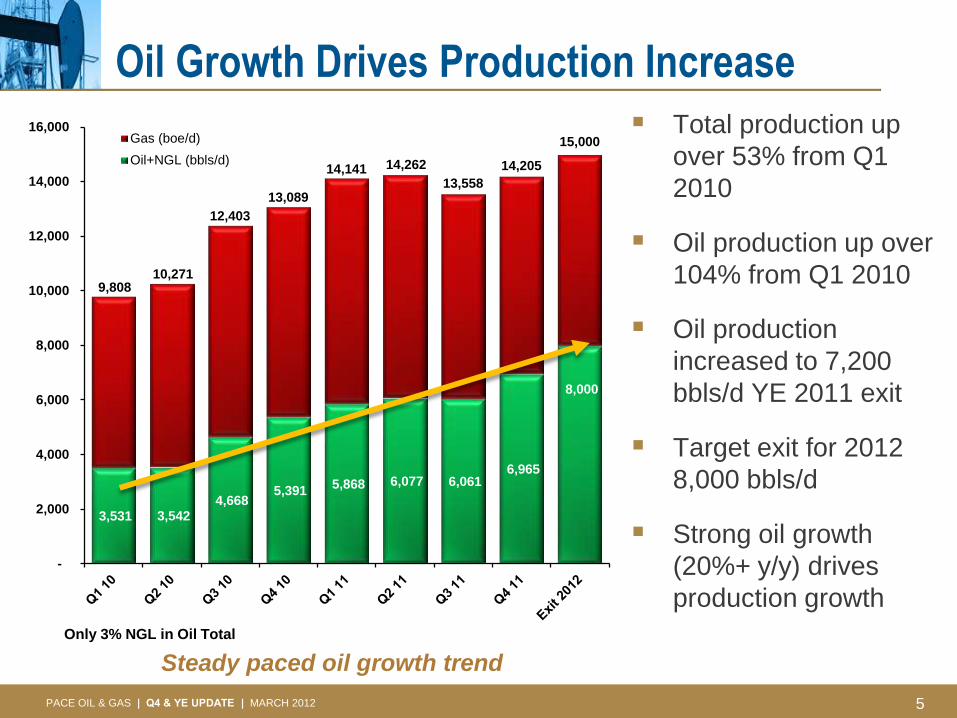

Oil Growth Drives Production Increase

Total production up

over 53% from Q1

2010

Oil production up over

104% from Q1 2010

Oil production

increased to 7,200

bbls/d YE 2011 exit

Target exit for 2012

8,000 bbls/d

Strong oil growth

(20%+ y/y) drives

production growth

Only 3% NGL in Oil Total

Steady paced oil growth trend

PACE OIL & GAS | Q4 & YE UPDATE | MARCH 2012 6

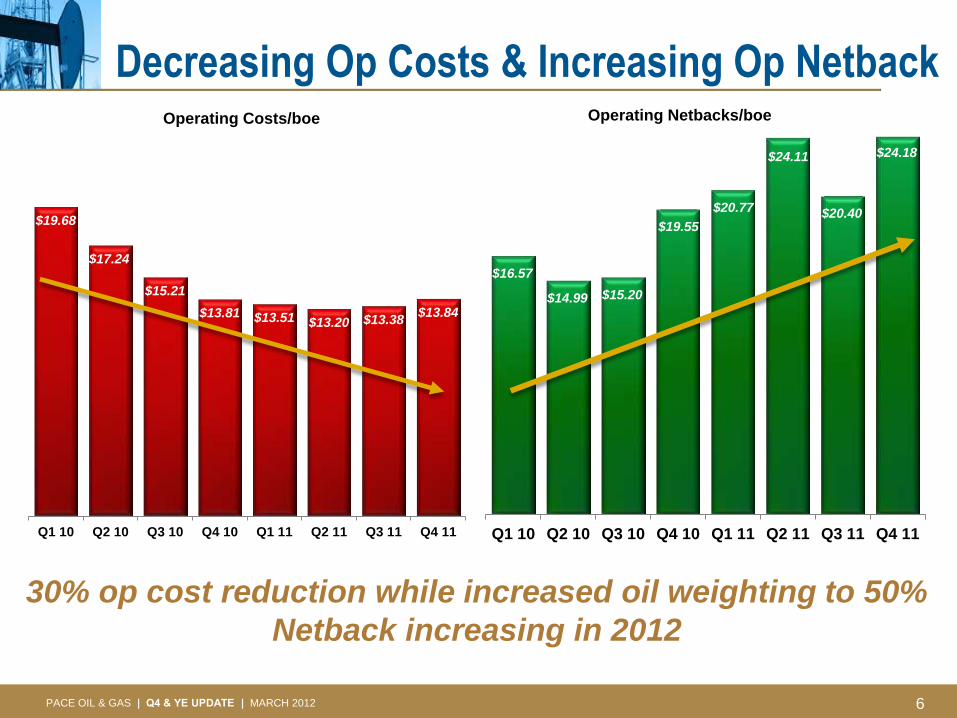

Decreasing Op Costs & Increasing Op Netback

30% op cost reduction while increased oil weighting to 50%

Netback increasing in 2012

$19.68

$17.24

$15.21

$13.81 $13.51 $13.20 $13.38 $13.84

Q1 10 Q2 10 Q3 10 Q4 10 Q1 11 Q2 11 Q3 11 Q4 11

Operating Costs/boe

$16.57

$14.99 $15.20

$19.55

$20.77

$24.11

$20.40

$24.18

Q1 10 Q2 10 Q3 10 Q4 10 Q1 11 Q2 11 Q3 11 Q4 11

Operating Netbacks/boe

PACE OIL & GAS | Q4 & YE UPDATE | MARCH 2012 7

Pace Delivered Top Finding Costs

2011 2010

$/boe Proved Proved Plus

Probable Proved

Proved Plus

Probable

E&D Capital $ 16.19 $ 15.81 $ 13.10 $ 12.91

Change in future capital (0.02) 1.23 (1.10) 4.29

F&D Costs $ 16.17 $ 17.04 $ 12.00 $ 17.20

A&D Capital $ 23.26 $ 7.36 $ 15.25 $ 10.05

A&D FDCs - - 4.79 4.87

A&D Costs $ 23.26 $ 7.36 $ 20.03 $ 14.93

Total Capital $ 16.11 $ 16.09 $ 14.65 $ 10.63

Change in future capital (0.02) 1.27 3.16 4.75

FD&A Costs $ 16.09 $ 17.36 $ 17.81 $ 15.39

% Reserve Adds by Product

Oil 75% 53% 62% 52%

NGLs 4% 7% 1% 1%

Natural Gas 21% 40% 37% 47%

100% 100% 100% 100%

Pace replaced 268% of oil & NGLs proven production – Over 2.1x recycle

ratio on weighted average netback by product

PACE OIL & GAS | Q4 & YE UPDATE | MARCH 2012 8

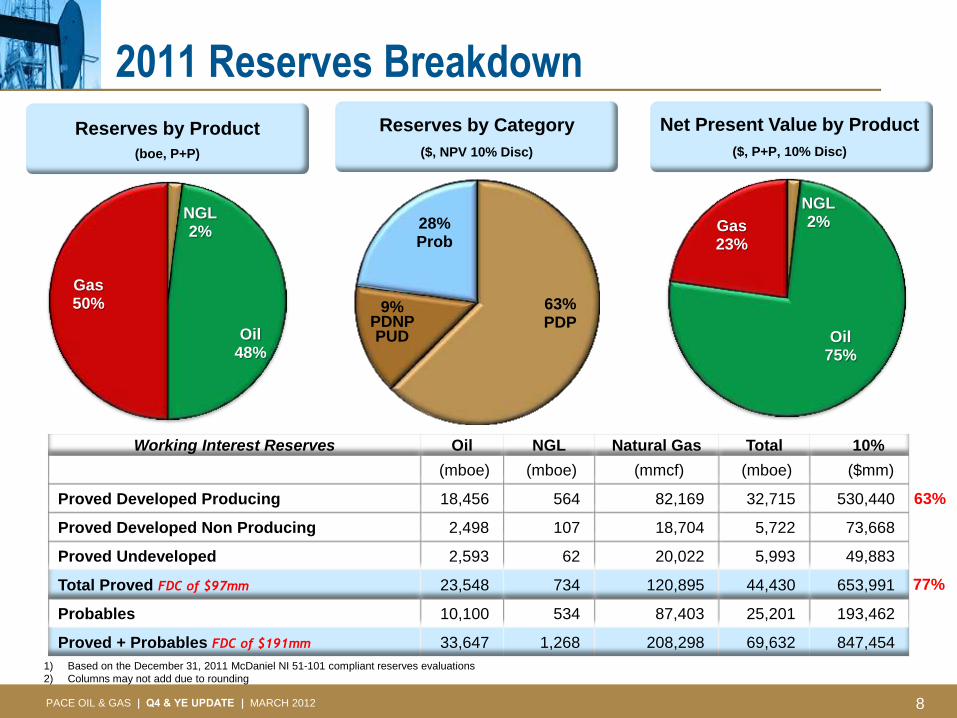

2011 Reserves Breakdown

Reserves by Product

(boe, P+P)

Reserves by Category

($, NPV 10% Disc)

Net Present Value by Product

($, P+P, 10% Disc)

NGL 2%

Oil 48%

Gas 50%

NGL 2%

Oil 75%

Gas 23%

63% PDP

9% PDNP PUD

28% Prob

Working Interest Reserves Oil NGL Natural Gas Total 10%

(mboe) (mboe) (mmcf) (mboe) ($mm)

Proved Developed Producing 18,456 564 82,169 32,715 530,440

Proved Developed Non Producing 2,498 107 18,704 5,722 73,668

Proved Undeveloped 2,593 62 20,022 5,993 49,883

Total Proved FDC of $97mm 23,548 734 120,895 44,430 653,991

Probables 10,100 534 87,403 25,201 193,462

Proved + Probables FDC of $191mm 33,647 1,268 208,298 69,632 847,454

63%

77%

1) Based on the December 31, 2011 McDaniel NI 51-101 compliant reserves evaluations

2) Columns may not add due to rounding

PACE OIL & GAS | Q4 & YE UPDATE | MARCH 2012 9

Proved PV10 $13.85 / share

Probable PV10 4.10 / share

2P PV10 $17.95 / share

Pace Underlying Value

Each common share owns

1.48 boe of reserves

(0.71 bbl of oil)

2011 Net Asset Value - ($mm) PDP Total P

Oil P+P

BT 10% reserve value (1) 530 534 $ 847

Less: net debt (186.1) (186.1) (186.1)

Add: undeveloped land value (354,000 acres @ $250/acre) (2) 88.5 88.5 88.5

Add: seismic and other assets 2.9 2.9 2.9

Net asset value $ 752.7

Shares outstanding (mm basic) 47.2 47.2 47.2

10 NAV/Share $9.22 $9.30 $ 15.95

(1) McDaniels & Associates Forecast Price & Costs (12/31/2011)

(2) Internal value estimate

NGL 2%

Oil 75%

Gas 23%

PACE OIL & GAS | Q4 & YE UPDATE | MARCH 2012 10

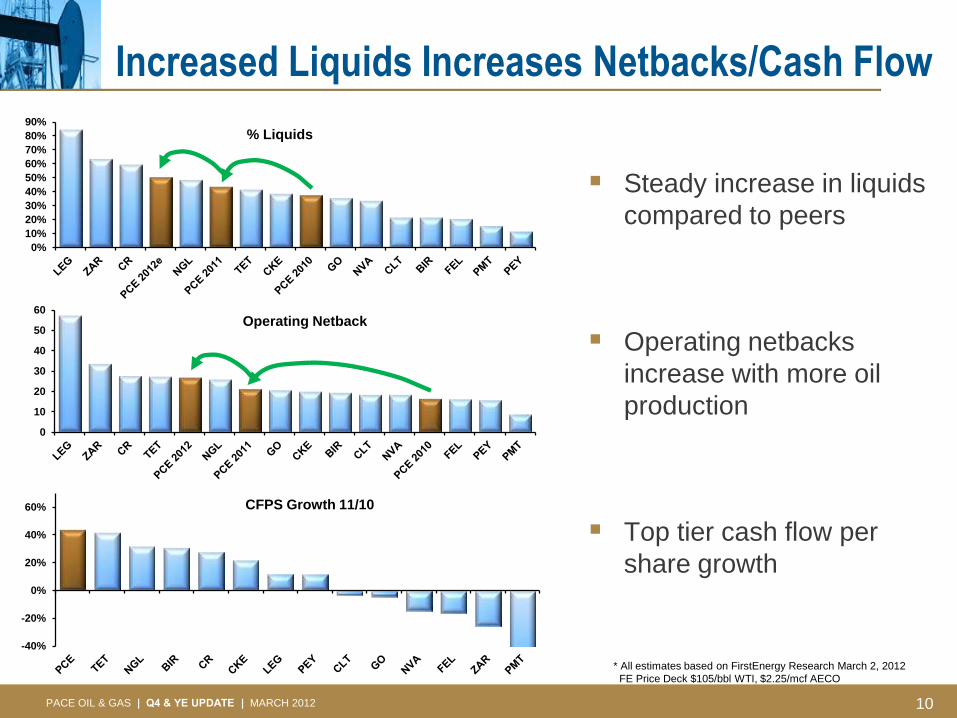

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

% Liquids

0

10

20

30

40

50

60Operating Netback

Increased Liquids Increases Netbacks/Cash Flow

Steady increase in liquids

compared to peers

Operating netbacks

increase with more oil

production

Top tier cash flow per

share growth

* All estimates based on FirstEnergy Research March 2, 2012

FE Price Deck $105/bbl WTI, $2.25/mcf AECO

-40%

-20%

0%

20%

40%

60% CFPS Growth 11/10

PACE OIL & GAS | Q4 & YE UPDATE | MARCH 2012 11

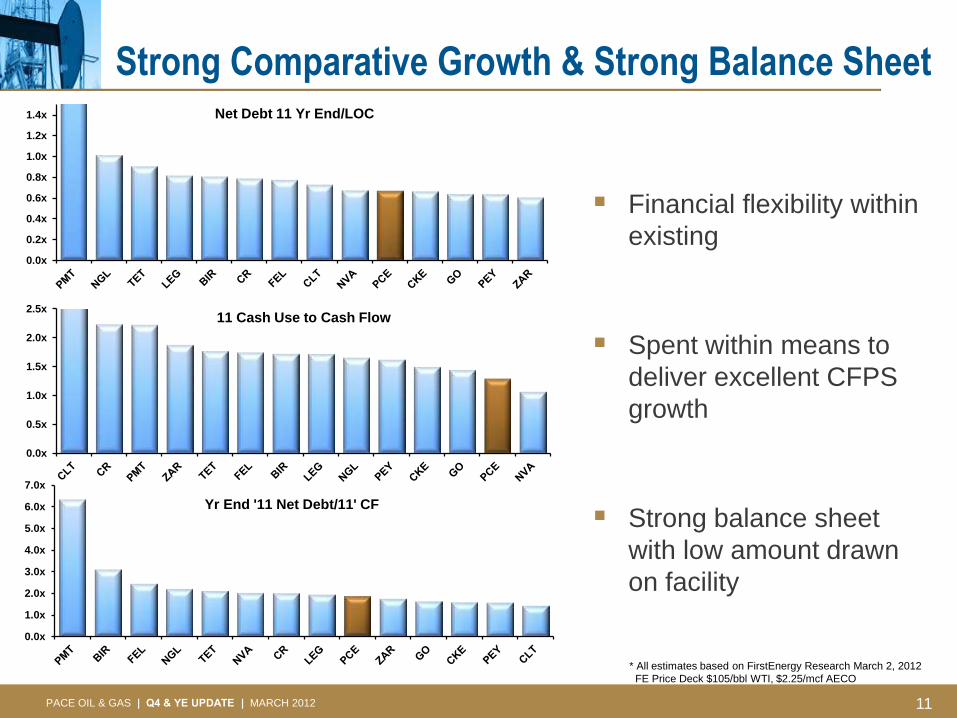

Strong Comparative Growth & Strong Balance Sheet

Financial flexibility within

existing

Spent within means to

deliver excellent CFPS

growth

Strong balance sheet

with low amount drawn

on facility

* All estimates based on FirstEnergy Research March 2, 2012

FE Price Deck $105/bbl WTI, $2.25/mcf AECO

0.0x

0.5x

1.0x

1.5x

2.0x

2.5x11 Cash Use to Cash Flow

0.0x

0.2x

0.4x

0.6x

0.8x

1.0x

1.2x

1.4x Net Debt 11 Yr End/LOC

0.0x

1.0x

2.0x

3.0x

4.0x

5.0x

6.0x

7.0x

Yr End '11 Net Debt/11' CF

PACE OIL & GAS | Q4 & YE UPDATE | MARCH 2012 12

Strong Results & Exceptional Value

Pace trades at low

multiple compared to

peer group

At peer group average,

Pace shares equate to

$12 – $15

Solid oil (real) growth will

drive multiple expansion

* All estimates based on FirstEnergy Research March 2, 2012

Pace closing price on March 2, 2012 - $5.67

-

20,000

40,000

60,000

80,000

100,000

120,000

140,000EV/2012 boe/d

0.0x

2.0x

4.0x

6.0x

8.0x

10.0x

12.0x

14.0xEV/2012 DACF

0.0x

2.0x

4.0x

6.0x

8.0x

10.0x

12.0x

14.0xPrice/2012 CF

PACE OIL & GAS | Q4 & YE UPDATE | MARCH 2012 13

Significant Upside & Visible Long Term Growth Areas

Key Attributes

Play Type Project

Capital

MM$

Gross

Operated

Wells

Net Wells

Southern

Alberta

Glauconite

Lithic

Pekisko

Waterflood

$35 – 40 24 18

Dixonville Montney C

Waterflood

$15 – 20 3 3

Red Earth Slave Point $15 – 20 2 2

Northwest

Alberta

Pekisko $10 4 4

Total Oil $75 - 90 33 27

Deep Basin $5 - -

Land,

Seismic, G&A

other

$15 – 25

Grand Total $90 - 100 33 27

High Working Interest

Operational Control

CapEx to match Cash Flow

2012 CapEx directed towards oil program

PACE OIL & GAS | Q4 & YE UPDATE | MARCH 2012 14

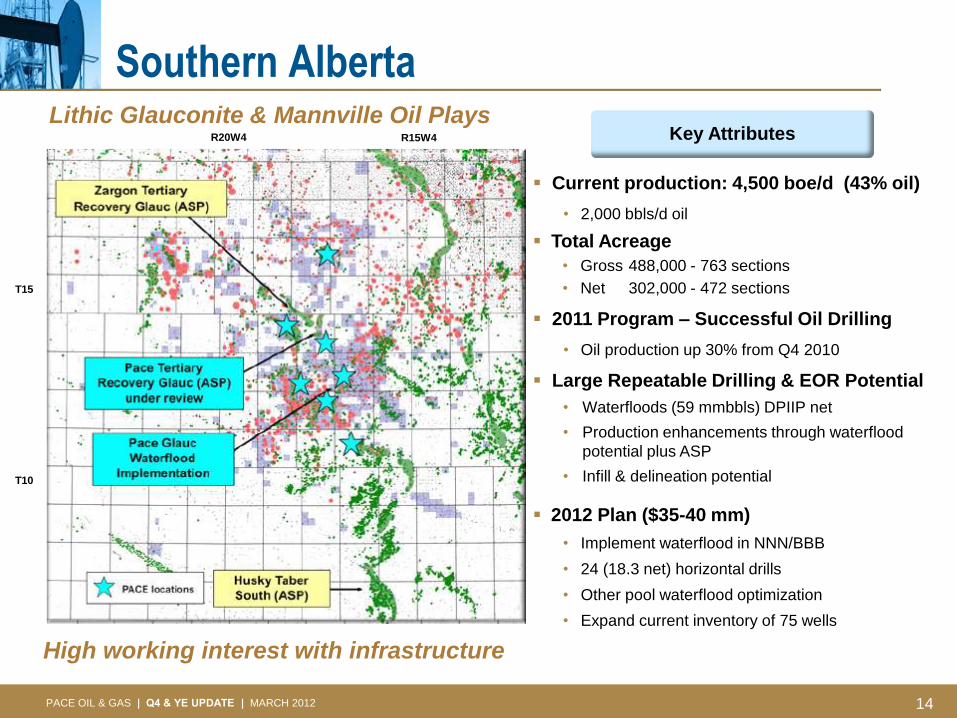

Southern Alberta

Current production: 4,500 boe/d (43% oil)

• 2,000 bbls/d oil

Total Acreage

• Gross 488,000 - 763 sections

• Net 302,000 - 472 sections

2011 Program – Successful Oil Drilling

• Oil production up 30% from Q4 2010

Large Repeatable Drilling & EOR Potential

• Waterfloods (59 mmbbls) DPIIP net

• Production enhancements through waterflood

potential plus ASP

• Infill & delineation potential

2012 Plan ($35-40 mm)

• Implement waterflood in NNN/BBB

• 24 (18.3 net) horizontal drills

• Other pool waterflood optimization

• Expand current inventory of 75 wells

Key Attributes Lithic Glauconite & Mannville Oil Plays

High working interest with infrastructure

T10

T15

R20W4 R15W4

PACE OIL & GAS | Q4 & YE UPDATE | MARCH 2012 15

Southern Alberta - Economics

Play Type Curve

D,C, Equip $1.9 mm

Production, boe/d (IP 30 day) 130

Reserves (mboe) 125

NPV 10%($mm/well) $2.0

Profit to Investment 1.05

Rate of Return 56%

Reserve Cost ($/boe) $15.25

Netback (1st year) ($/boe) $54.40

$97/bbl WTI, $3.50/mcf AECO

0

100

200

300

400

500

0 12 24

BO

E/D

Months

Type Curve

R19W4 R17W4

T14

T12

Successful 2011 drilling program drives oil growth

2012 Plan ($30 mm+/-)

• 24 (18.3 net) horizontal drills

• Expand current inventory of 75 wells

PACE OIL & GAS | Q4 & YE UPDATE | MARCH 2012 16

NNN & BBB Production Forecast

Implement waterflood in NNN/BBB

• 400 bbl/d production adds forecasted

• 52% IRR, 1.5 mmbbls PDP additions

Infill horizontals possible once pressures

restored

Other pool waterflood optimization

Additional ASP potential

-1000

0

1000

2000

3000

4000

5000

0

200

400

600

800

1000Retlaw Unit WF Forecast

Cal Day Oil

Water Inj, bwpd

R17W4 R18W4

T13

T12

2012 Plan ($5 mm net capital)

PACE OIL & GAS | Q4 & YE UPDATE | MARCH 2012 17

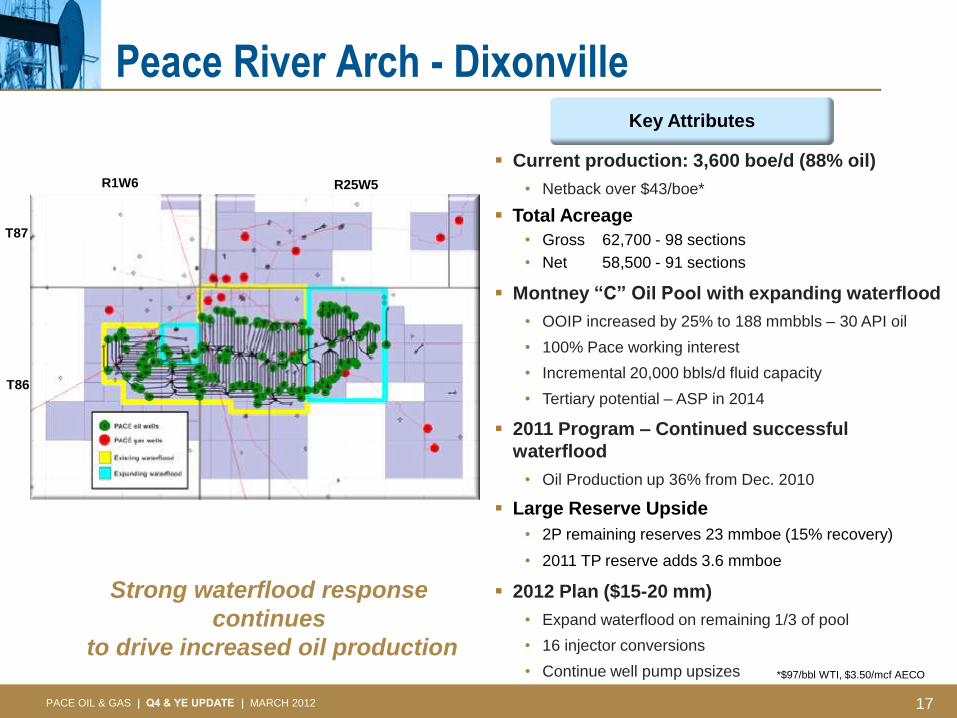

Peace River Arch - Dixonville Key Attributes

Current production: 3,600 boe/d (88% oil)

• Netback over $43/boe*

Total Acreage

• Gross 62,700 - 98 sections

• Net 58,500 - 91 sections

Montney “C” Oil Pool with expanding waterflood

• OOIP increased by 25% to 188 mmbbls – 30 API oil

• 100% Pace working interest

• Incremental 20,000 bbls/d fluid capacity

• Tertiary potential – ASP in 2014

2011 Program – Continued successful

waterflood

• Oil Production up 36% from Dec. 2010

Large Reserve Upside

• 2P remaining reserves 23 mmboe (15% recovery)

• 2011 TP reserve adds 3.6 mmboe

2012 Plan ($15-20 mm)

• Expand waterflood on remaining 1/3 of pool

• 16 injector conversions

• Continue well pump upsizes

Strong waterflood response

continues

to drive increased oil production *$97/bbl WTI, $3.50/mcf AECO

R1W6 R25W5

T87

T86

PACE OIL & GAS | Q4 & YE UPDATE | MARCH 2012 18

Dixonville: Montney C Reservoir Simulation

Waterflood response exceeds base case (booked reserves) and current model

3,200 bbls/d

Prod, 5.7 Prod, 5.7 Prod, 5.7

1P, 16.2 1P, 16.2 1P, 16.2

2P, 7.0 2P, 7.0 2P, 7.0

Upside, 9.4 Upside, 9.4

Tertiary, 28.2

15%

20%

35%

-

0.05

0.10

0.15

0.20

0.25

0.30

0.35

0.40

0

10

20

30

40

50

60

70

Base Case WaterfloodOptimization

EUR (SP)

ULT

IMA

TE R

ECO

VER

Y O

F O

OIP

(%

)

REM

AIN

ING

REC

OV

ERA

BLE

OIL

(M

MB

BL)

DIXONVILLE: MONTNEY C

Prod 1P 2P Upside Total OOIP Rec.

PACE OIL & GAS | Q4 & YE UPDATE | MARCH 2012 19

Peace River Arch - Red Earth Area

Southern Alberta

Current Production: 590 bbls/d (oil)

Total Acreage

• Gross 72,800 - 114 sections

• Net 51,800 – 81 sections

Top Quality light oil property

• Netback > $60/boe*

Slave Point Resource Play

• High industry activity

• Gross 42,800 (32,200 net) acres

2012 Plan ($15-20 mm)

• Drill 2 Hz wells & test 4 wells

• Create Slave Point program for Q4 2012

• Current inventory of 50 wells & growing

Key Attributes

*$97/bbl WTI, $3.50/mcf AECO

T88

R7W5

T86

R9W5

PACE OIL & GAS | Q4 & YE UPDATE | MARCH 2012 20

Peace River Arch - Red Earth Area - Economics

0 1 2 3

Oil

Ra

te (

bb

l/d

)

Years

100/1-9-88-8W5/0

100/8-1-88-12W5/0

Southern Alberta

Play Type Curve

D,C, Equip $3.0 mm

Production, boe/d (IP 30 day) 125 - 150

Reserves (mboe) 150

NPV 10%($mm/well) $2.1

Profit to Investment 0.7

Rate of Return 50%

Reserve Cost ($/boe) $20.00

Netback (1st year) ($/boe) $73.00

$97/bbl WTI, $3.50/mcf AECO

Type Curve

1st Generation Wells

2011 Wells

R10W5 R6W5

T85

T87

T89

PACE OIL & GAS | Q4 & YE UPDATE | MARCH 2012 21

Northern Alberta: Rainbow/Haro – Resource play

Key Attributes

Current production: 3,800 boe/d (27% oil)

Total Acreage • Gross 376,000 - 587 sections

• Net 328,000 - 513 sections

Stable, long term production

• Large low decline (5-7%/yr) Bluesky gas

• 925 bbl/d Muskeg & Keg River sweet crude

Haro – early stage oil resource play

• 1.16 B bbls DPIIP, Net 71,000 acres – 111 sections

• 22º API with cold production

• Potential 4-8 wells per section

• 500 m depth – low capital cost per well

2012 Plan ($10 mm)

• 4 Pekisko oil horizontals with smaller fracs

• Establish non-stimulation base line

• Hold land 5 years

• ARC has licensed 4 Pekisko wells to be drilled this winter

(1) Discovered petroleum initially-in-place

R10W6 R6W6 R2W6

T110

T105

T100

PACE OIL & GAS | Q4 & YE UPDATE | MARCH 2012 22

Haro Pekisko Encouragement

Unrisked 300 to 600 locations

0

25

50

75

100

125

150

175

200

0 12 24 36

Oil R

ate

(b

bl/d

)

Months

Type Curve 00/02-36

D,C, Equip $2.1 – 2.5 mm

Production, boe/d (IP 30 day) 100 - 125

Reserves (mboe) 100 - 150

NPV 10%($mm/well) $2.0 – 2.4

Profit to Investment 0.8 – 1.1

Rate of Return 35 - 75%

Reserve Cost ($/boe) $14 - 25

Netback (1st year) ($/boe) $55 - 60

2-36-101-5W6

$97/bbl WTI, $3.50/mcf AECO

R3W6 R6W6

T100

T98

T102

PACE OIL & GAS | Q4 & YE UPDATE | MARCH 2012 23

Large Repeatable Gas

Current Production: ~ 7.6 mmcf/d

16,300 Chinook Ridge

Deep Basin Land

Elmworth 3,500

Red Rock 19,000

Bilbo 6,600

5,800

27,000

20,100

19,200

Gross Acres Net Acres Area

Total 72,100 45,400

Working interest: 75%-100%

(operated)

Net acreage: 19,300 acres (30.2

sections)

Farrell Creek, BC

PACE OIL & GAS | Q4 & YE UPDATE | MARCH 2012 24

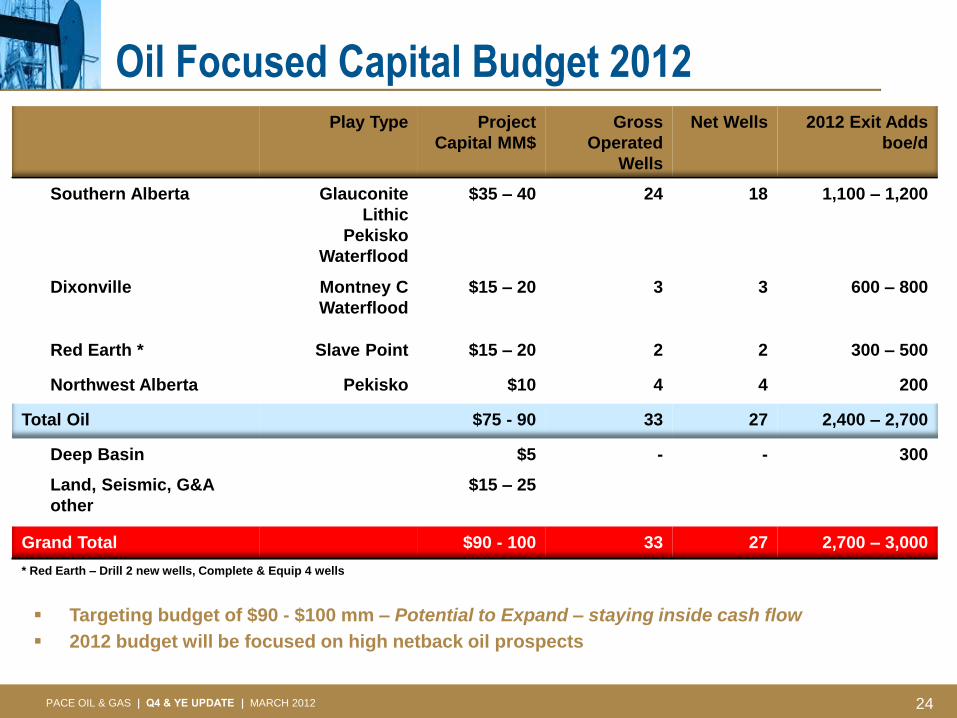

Oil Focused Capital Budget 2012 Play Type Project

Capital MM$

Gross

Operated

Wells

Net Wells 2012 Exit Adds

boe/d

Southern Alberta Glauconite

Lithic

Pekisko

Waterflood

$35 – 40 24 18 1,100 – 1,200

Dixonville Montney C

Waterflood

$15 – 20 3 3 600 – 800

Red Earth * Slave Point $15 – 20 2 2 300 – 500

Northwest Alberta Pekisko $10 4 4 200

Total Oil $75 - 90 33 27 2,400 – 2,700

Deep Basin $5 - - 300

Land, Seismic, G&A

other

$15 – 25

Grand Total $90 - 100 33 27 2,700 – 3,000

* Red Earth – Drill 2 new wells, Complete & Equip 4 wells

Targeting budget of $90 - $100 mm – Potential to Expand – staying inside cash flow

2012 budget will be focused on high netback oil prospects

PACE OIL & GAS | Q4 & YE UPDATE | MARCH 2012 25

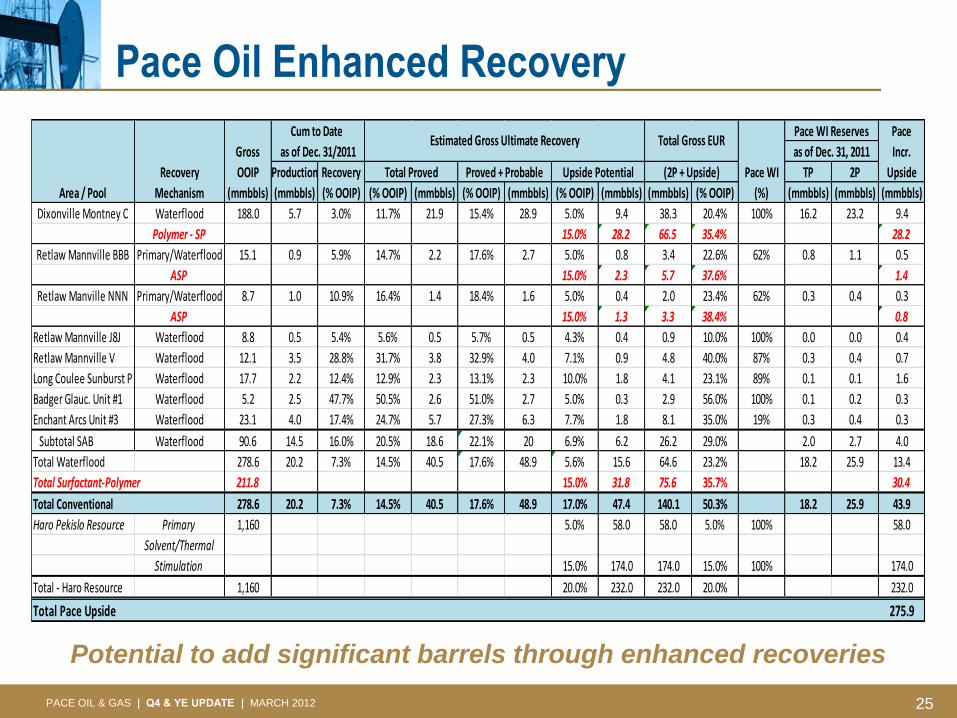

Pace Oil Enhanced Recovery

Potential to add significant barrels through enhanced recoveries

Pace

Gross Incr.

Recovery OOIP Production Recovery Pace WI TP 2P Upside

Area / Pool Mechanism (mmbbls) (mmbbls) (% OOIP) (% OOIP) (mmbbls) (% OOIP) (mmbbls) (% OOIP) (mmbbls) (mmbbls) (% OOIP) (%) (mmbbls) (mmbbls) (mmbbls)

Dixonville Montney C Waterflood 188.0 5.7 3.0% 11.7% 21.9 15.4% 28.9 5.0% 9.4 38.3 20.4% 100% 16.2 23.2 9.4

Polymer - SP 15.0% 28.2 66.5 35.4% 28.2

Retlaw Mannville BBB Primary/Waterflood 15.1 0.9 5.9% 14.7% 2.2 17.6% 2.7 5.0% 0.8 3.4 22.6% 62% 0.8 1.1 0.5

ASP 15.0% 2.3 5.7 37.6% 1.4

Retlaw Manville NNN Primary/Waterflood 8.7 1.0 10.9% 16.4% 1.4 18.4% 1.6 5.0% 0.4 2.0 23.4% 62% 0.3 0.4 0.3

ASP 15.0% 1.3 3.3 38.4% 0.8

Retlaw Mannville J8J Waterflood 8.8 0.5 5.4% 5.6% 0.5 5.7% 0.5 4.3% 0.4 0.9 10.0% 100% 0.0 0.0 0.4

Retlaw Mannville V Waterflood 12.1 3.5 28.8% 31.7% 3.8 32.9% 4.0 7.1% 0.9 4.8 40.0% 87% 0.3 0.4 0.7

Long Coulee Sunburst P Waterflood 17.7 2.2 12.4% 12.9% 2.3 13.1% 2.3 10.0% 1.8 4.1 23.1% 89% 0.1 0.1 1.6

Badger Glauc. Unit #1 Waterflood 5.2 2.5 47.7% 50.5% 2.6 51.0% 2.7 5.0% 0.3 2.9 56.0% 100% 0.1 0.2 0.3

Enchant Arcs Unit #3 Waterflood 23.1 4.0 17.4% 24.7% 5.7 27.3% 6.3 7.7% 1.8 8.1 35.0% 19% 0.3 0.4 0.3

Subtotal SAB Waterflood 90.6 14.5 16.0% 20.5% 18.6 22.1% 20 6.9% 6.2 26.2 29.0% 2.0 2.7 4.0

Total Waterflood 278.6 20.2 7.3% 14.5% 40.5 17.6% 48.9 5.6% 15.6 64.6 23.2% 18.2 25.9 13.4

Total Surfactant-Polymer 211.8 15.0% 31.8 75.6 35.7% 30.4

Total Conventional 278.6 20.2 7.3% 14.5% 40.5 17.6% 48.9 17.0% 47.4 140.1 50.3% 18.2 25.9 43.9

Haro Pekislo Resource Primary 1,160 5.0% 58.0 58.0 5.0% 100% 58.0

Solvent/Thermal

Stimulation 15.0% 174.0 174.0 15.0% 100% 174.0

Total - Haro Resource 1,160 20.0% 232.0 232.0 20.0% 232.0

Total Pace Upside 275.9

Pace WI Reserves

as of Dec. 31, 2011

Cum to Date

as of Dec. 31/2011

Upside PotentialTotal Proved (2P + Upside)

Estimated Gross Ultimate Recovery Total Gross EUR

Proved + Probable

PACE OIL & GAS | Q4 & YE UPDATE | MARCH 2012 26

Key Investment Highlights

Strong Real Growth

• Production up, oil weighting up and growing

• Cash flow up and top tier per share growth Excellent results and continued oil focused growth

Solid Value

• Solid reserves, low decline, low risk Low cost reserves and very attractive trading multiple

Significant Upside

• Identified portfolio of visible long term, low risk,

oil growth opportunities

Oil weighted upside with large scale gas resource optionality

Oil Weighted Growth, Excellent Value,

Proven Team, Proven Results

27 PACE OIL & GAS | Q4 & YE UPDATE | MARCH 2012

Pace Corporate Information Management

Fred Woods President & CEO

Judy Stripling Executive Vice President & CFO

Todd Brown Vice President & COO

Volker Braun Vice President, Exploration

Chad Kalmakoff Vice President, Finance

Colin Merrick Vice President, HR, IR & Administration

Darrell Osinchuk Vice President, Exploitation

Martin Saizew Vice President, Engineering

George Swerdan Vice President, Production & Operations

Andrew Weldon Vice President, Business Development

Directors

Fred Woods Tom Simons

Tom Buchanan Jeff Smith

Peter Harrison Jay Squiers

Mike Shaikh David Tuer

Banking Syndicate

CIBC

National Bank

Bank of Montreal

Bank of Nova Scotia

Alberta Treasury Branches

HSBC Bank of Canada

Auditors

PriceWaterhouse Coopers LLP

Legal Counsel

Heenan Blaikie LLP

Evaluation Engineers

McDaniels & Associates Consultants Ltd.

Registrar & Transfer Agent

Computershare Trust Company of Canada

TSX Listing Symbol OTC Pinks Symbol

PCE PACEF

Address

Livingston Place, West Tower

Suite 1700, 250 – 2nd Avenue SW

Calgary, Alberta, Canada T2P 0C1

Ph: 403-303-8500

Investor Relations Email: [email protected]

Website: www.paceoil.ca

For Information Contact

Fred Woods President & CEO

Judy Stripling Executive VP & CFO

Chad Kalmakoff VP, Finance

Main: 403-303-8500

Investor Relations Email: [email protected]

Website: www.paceoil.ca

TSX: PCE OTC: PACEF