OWNERSHIP STRUCTURE AND FIRM …erg/research/japan411f.pdf566 Academy of Management Journal June...

12

® Academy of Management Journal 2002. Vol. 45, No. 2. 565-575. OWNERSHIP STRUCTURE AND FIRM PROFITABILITY IN JAPAN ERIC GEDAJLOVIC Erasmus University DANIEL M. SHAPIRO Simon Fraser University We examined the relationship hetween the ownership structure and financial perfor- mance of 334 Japanese corporations for the 1986-91 period. The positive relationship we found between ownership concentration and financial performance is consistent with agency theory predictions. In addition, we observed a more pronounced profit redistribution effect characterized hy the transferring of financial resources from more to less profitable firms. These findings indicate the need to account for both economic incentives and social context in corporate governance research. In the economics, finance, and strategic manage- ment literatures, agency theory represents a domi- nant theoretical frame of reference for the study of the relationship between ownership and perfor- mance (Shleifer & Vishny, 1997). Agency theory highlights the idea that principals and agents often have divergent goals and divergent capacities to influence corporate behavior and outcomes (Mil- grom & Roberts, 1992). An important contribution of agency theory is that it facilitates a structured approach to the analysis of economic motivations and the incentives of managers and shareholders (Eisenhardt, 1989). Agency theory has been criti- cized in the sociology literature, however, for its proponents' failure to pay sufficient attention to the contexts in which exchange and principal-agent relations are embedded (Hamilton & Biggart, 1988). Ownership concentration is a variable of interest to scholars in a number of disciplines, and its in- fluence on strategic behavior and corporate perfor- mance has been, studied in a wide variety of na- tional contexts (Gedajlovic & Shapiro, 1998) and from differing theoretical perspectives. In research emphasizing the influence of economic incentives on top executives and investors, ownership con- centration has been used primarily as a barometer of agency costs (Shleifer & Vishny, 1997). In studies We would like to thank three anonymous reviewers and two editors for their helpful comments and sugges- tions; Phil Bobko, Erwin van Gulik, Pursey Heugens, Peter Kennedy, Masao Nakamura, and Aidan Vining for comments and discussion; and Bogdan Baduru for pro- gramming assistance. The usual disclaimer applies; any errors that may remain are the sole responsibility of the authors. emphasizing social context, ownership concentra- tion has been used as an indicator of the strength of the ties a firm has to its investors (Gerlach, 1992; Lincoln, Gerlach, & Ahmadjian, 1996). Previous empirical studies examining the ownership-perfor- mance link have had frames of reference restricted to one or the other of these perspectives. In this study, we bridge this divide by combining insights from both streams of research to analyze the impact of ownership concentration on firm performance in Japan. We first used standard agency theory logic to develop the hypothesis that ownership concentra- tion and firm performance are directly and posi- tively related in Japan. Subsequently, we devel- oped hypotheses that account for a unique feature of Japan's institutional context. Specifically, we evaluated the possibility that an important effect of ownership concentration in Japanese firms is to promote intercorporate goals of risk reduction and mutual assistance (Aoki, 1988; Dore, 1983; Naka- tani, 1984). We built upon the work of Lincoln and colleagues (1996), who found that the performance of firms with close ties to one of the "Big Six"^ Japanese keiretsus is conditioned by past perfor- mance in a manner that benefits weaker performers at the expense of stronger companies. Our context- specific hypotheses address the likelihood that a similar pattern of structured interaction extends to a much broader set of Japanese firms through own- ership ties. Although the theoretical underpinnings of agency and redistribution effects emanate from different lit- ^ The "Big Six" keiretsus are Mitsubishi, Mitsui, Sumi- tomo, Fuji, Sanwa, and Dai-Ichi Kangyo. 565

Transcript of OWNERSHIP STRUCTURE AND FIRM …erg/research/japan411f.pdf566 Academy of Management Journal June...

® Academy of Management Journal2002. Vol. 45, No. 2. 565-575.

OWNERSHIP STRUCTURE AND FIRM PROFITABILITYIN JAPAN

ERIC GEDAJLOVICErasmus University

DANIEL M. SHAPIROSimon Fraser University

We examined the relationship hetween the ownership structure and financial perfor-mance of 334 Japanese corporations for the 1986-91 period. The positive relationshipwe found between ownership concentration and financial performance is consistentwith agency theory predictions. In addition, we observed a more pronounced profitredistribution effect characterized hy the transferring of financial resources from moreto less profitable firms. These findings indicate the need to account for both economicincentives and social context in corporate governance research.

In the economics, finance, and strategic manage-ment literatures, agency theory represents a domi-nant theoretical frame of reference for the study ofthe relationship between ownership and perfor-mance (Shleifer & Vishny, 1997). Agency theoryhighlights the idea that principals and agents oftenhave divergent goals and divergent capacities toinfluence corporate behavior and outcomes (Mil-grom & Roberts, 1992). An important contributionof agency theory is that it facilitates a structuredapproach to the analysis of economic motivationsand the incentives of managers and shareholders(Eisenhardt, 1989). Agency theory has been criti-cized in the sociology literature, however, for itsproponents' failure to pay sufficient attention to thecontexts in which exchange and principal-agentrelations are embedded (Hamilton & Biggart, 1988).

Ownership concentration is a variable of interestto scholars in a number of disciplines, and its in-fluence on strategic behavior and corporate perfor-mance has been, studied in a wide variety of na-tional contexts (Gedajlovic & Shapiro, 1998) andfrom differing theoretical perspectives. In researchemphasizing the influence of economic incentiveson top executives and investors, ownership con-centration has been used primarily as a barometerof agency costs (Shleifer & Vishny, 1997). In studies

We would like to thank three anonymous reviewersand two editors for their helpful comments and sugges-tions; Phil Bobko, Erwin van Gulik, Pursey Heugens,Peter Kennedy, Masao Nakamura, and Aidan Vining forcomments and discussion; and Bogdan Baduru for pro-gramming assistance. The usual disclaimer applies; anyerrors that may remain are the sole responsibility of theauthors.

emphasizing social context, ownership concentra-tion has been used as an indicator of the strength ofthe ties a firm has to its investors (Gerlach, 1992;Lincoln, Gerlach, & Ahmadjian, 1996). Previousempirical studies examining the ownership-perfor-mance link have had frames of reference restrictedto one or the other of these perspectives. In thisstudy, we bridge this divide by combining insightsfrom both streams of research to analyze the impactof ownership concentration on firm performance inJapan.

We first used standard agency theory logic todevelop the hypothesis that ownership concentra-tion and firm performance are directly and posi-tively related in Japan. Subsequently, we devel-oped hypotheses that account for a unique featureof Japan's institutional context. Specifically, weevaluated the possibility that an important effect ofownership concentration in Japanese firms is topromote intercorporate goals of risk reduction andmutual assistance (Aoki, 1988; Dore, 1983; Naka-tani, 1984). We built upon the work of Lincoln andcolleagues (1996), who found that the performanceof firms with close ties to one of the "Big Six"^Japanese keiretsus is conditioned by past perfor-mance in a manner that benefits weaker performersat the expense of stronger companies. Our context-specific hypotheses address the likelihood that asimilar pattern of structured interaction extends toa much broader set of Japanese firms through own-ership ties.

Although the theoretical underpinnings of agencyand redistribution effects emanate from different lit-

^ The "Big Six" keiretsus are Mitsubishi, Mitsui, Sumi-tomo, Fuji, Sanwa, and Dai-Ichi Kangyo.

565

566 Academy of Management Journal June

eratures and suggest different associations betweenownership concentration and financial performance,there is no a priori reason why both effects cannotoccur contemporaneously. On the contrary, since Ja-pan's unique form of industrial organization is char-acterized by both a pronounced separation of owner-ship and control (Glaessens, Djankov, & Lang, 2000)and a complex network of intercorporate relation-ships (Gerlach, 1992), there is reason to expect thatboth agency and redistribution effects will be appar-ent. Accordingly, we derived and specified a modelthat accounts for the possible existence of both typesof effects. We evaluated this model on a pooled cross-sectional sample of 334 publicly listed Japanese firmsspanning their 1986-91 fiscal years.

BACKGROUND

National systems of corporate governance evolvein order to exploit the advantages of the corporateform of organization while mitigating concomitantagency costs in a manner consistent with a coun-try's history and legal, political, and social tradi-tions. In this regard, nations differ significantly interms of the variety and the effectiveness of theconstraints placed upon their top executives (Gedaj-lovic & Shapiro, 1998). Japan's system of gover-nance represents an interesting case insofar asfirms characterized by a clear separation of owner-ship and control are embedded in dense intercor-porate networks. In contrast to the norm in otherEast Asian economies, decision control over Ja-pan's largest corporations is vested with profes-sional managers rather than entrepreneurs andtheir extended families (Hamilton & Biggart, 1988).Historically, the shareholdings of Japanese profes-sional managers have been negligible (Charkham,1994). At the same time, Japan's system of corpo-rate governance is intimately tied to the variety ofintercorporate groupings and alliances that domi-nate its enterprise system. Joint and reciprocalmonitoring among business partners engaged in amultiplexity of business relations is a distinctivefeature of Japan's system of corporate governance(Roe, 1994). Gerlach (1992) described how theseintercorporate networks transcend formal group-ings and pervade much of the Japanese economy.Although the most formal of these groupings areoff en referred to as keiretsus, Gerlach suggestedthat the term be used as "a metaphor for generalpatterns of inter-firm organization in Japan—as anideal type" (1992; 5-6).

In terms of corporate governance, two varieties ofthese networks are particularly relevant; industrial,or vertical keiretsus, and financial, or horizontalkeiretsus. Industrial keiretsus link vertically re-

lated firms along an industry value chain throughthe cross-ownership of equity (Dyer, 1996). Thus,the members are typically a large manufacturer andits major suppliers. An exchange of employees anddirectors offen accompanies the cross-ownership ofshares. Financial keiretsus link companies (usuallyin different industries) through a common mainbank, which typically has an ownership stake in anetwork's firms and provides loans and commer-cial services to them (Hoshi, Kashyap, & Scharf-stein, 1990).

There exists a large body of research on the ef-fects of network, or keiretsu, ties (e.g., Gerlach,1992) and the role of main banks (e.g., Aoki,Patrick, & Sheard, 1994), but empirical evidenceconcerning the relationship between ownershipand firm performance in that country is quitesparse and equivocal. Cable and Yasuki (1985)found that ownership concentration outside keiret-sus was positively related to firm performance butthat shareholdings within these groups were unre-lated to performance. Prowse (1992) found no sig-nificant relationship between ownership concen-tration and financial performance among eitherkeiretsu or nonkeiretsu firms. In the same year,Gerlach (1992) reported a positive relationship be-tween ownership concentration and firm perfor-mance in a regression model that controlled forboth keiretsu membership and debt ties to a mainbank.

THEORY AND HYPOTHESES

Agency theory suggests that the corporate form oforganization characterized by a professional man-agement with little ownership operating a businesson behalf of a large number of widely dispersedshareholders represents an archetypal principal-agent problem (Eisenhardt, 1989). This agencyproblem stems from the fact that managers offenhave both the discretion and incentive to pursuestrategies and practices that benefit themselves atthe expense of shareholders (Jensen & Meckling,1976). The exercise of managerial discretion can beharmful to shareholders in two broad ways. Man-agers may engage in short-run cost augmenting ac-tivities to enhance their nonsalary income and/orthey may indulge their need for power, prestige,and status by attempting to maximize corporatesize and growth rather than corporate profits (Gedaj-lovic & Shapiro, 1998).

From an agency perspective, many Japanesemanagers may have both the incentive and the dis-cretion necessary to pursue their own interests atthe expense of shareholders. Top executives typi-cally lack ownership incentives insofar as their

2002 Gedajlovic and Shapiro 567

shareholdings are negligible and because the use ofstock-based and other performance-based incen-tives has been very uncommon (Fukao, 1999). Un-der such conditions, agency theory suggests, man-agers lack the incentive to maintain tight costcontrol (Alchian & Demsetz, 1972) and will tend toadopt strategies and practices that benefit them-selves at the expense of shareholders. At the sametime, the absence of an active market for corporatecontrol in Japan (Walsh & Seward, 1990) and thetendency for Japanese corporations to have insider-dominated boards (Charkham, 1994) create condi-tions that afford managers a broad scope of exercis-able discretion. In the absence of either capitalmarket constraints or vigilant outside directors, themonitoring of managers by shareholders who holdlarge blocks of shares (blockholders) takes onheightened significance (Shleifer & Vishny, 1997).As a consequence, we expected to find a posi-tive relationship between the ownership concen-tration and financial performance of Japanesecorporations.

Hypothesis la. There is a positive relationshipbetween the sizes of the ownership stakes ofshareholders and profitability among Japanesefirms.

Hypothesis la does not distinguish among vari-ous types of blockholders. Recent theory and evi-dence suggest that shareholder identity may matterbecause shareholders can have heterogeneous in-centives and capacities to monitor managers (Gedaj-lovic, 1993; Thomsen & Pederson, 2000). In thisregard, shareholdings by Japanese financial institu-tions and nonfinancial corporations may imposeimportant limits on managerial discretion. Sincethese firms are commonly not only a corporation'sshareholders, but are also its creditors, buyers, sup-pliers, and business partners, they are exception-ally well positioned to monitor the managers offirms within their network (Berglof & Perotti, 1994).In such an information-rich context, managers areless likely to have the discretion necessary to pur-sue their own interests at the expense of theirshareholders or stakeholders. Further, any such be-havior is likely to be detected early because of thedense web of equity, debt, and commercial ties thatcharacterize such relations.

Hypothesis lb. There is a positive relationshipbetween the sizes of the shareholdings of finan-cial institutions and nonfinancial corporationsand profitability among Japanese firms.

Hypotheses la and lb are derived from an agencyperspective that suggests that ownership concen-tration promotes the pursuit of profit maximiza-

tion. However, it is offen argued that the multipleequity, debt, and commercial ties characterizingthe Japanese economy are linked to intercorporategoals of risk reduction and mutual assistance (Dore,1983; Gerlach, 1992) that result in systematic pat-terns of profit redistribution among Japanese firms(Lincoln et al., 1996). In this respect, there is someevidence that firms pay "insurance premiums" totheir main banks against the possibility of futurefinancial distress in the form of overborrowing(Aoki, 1988) at high rates of interest (Weinstein &Yafeh, 1994).

Hoshi and colleagues (1990) and Morck and Na-kamura (1999) have offered evidence supportingthis view insofar as they have observed that Japa-nese banks treated firms with which they had closeties and those with which they did not have closeties differently during times of financial distress.Morck and Nakamura (1999) noted that banks act toprop up weak firms with which they have closeties. Lincoln and colleagues (1996) extended theinsurance metaphor beyond the banking sector andsuggested that by "taxing" prosperous members toensure the survival and speed the recovery of trou-bled affiliates, keiretsu networks distribute benefitsand burdens in a discriminating way. The processof redistribution is facilitated by the multiplicity ofdirect and indirect debt, equity, and commercialties that characterize intercorporate relations in Ja-pan. In such a context, banks can extend benefits toaffiliated firms by increasing their shareholdings orby providing loans or professional services on fa-vorable terms (Morck & Nakamura, 1999). Simi-larly, industrial firms can purchase or supply prod-ucts and/or services on favorable terms in order toassist a troubled business partner (Lincoln et al.,1996).

The norm of redistribution may be widespread.In describing the pervasiveness of formal and in-formal links throughout Japanese industrial organi-zation, Gerlach noted that intercorporate relation-ships within keiretsus have much in common withthose found in ostensibly more independent firms(1992; 6). This assessment receives support inHoshi, Kashyap, and Scharfstein's (1991) findingthat the benefits of bank-led bailouts extended tononkeiretsu firms that nevertheless had strong tiesto a bank. Thus, there is some evidence that theredistribution patterns observed by Lincoln et al.(1996) are a discernible characteristic of Japan'sbroader business system rather than a keiretsu-onlyphenomena. In this regard, Clark's widely citedcomment that in Japan "shareholding is the mereexpression of their relationship, not the relation-ship itself" (1979; 86) suggests that equity ties aresymbolic indicators of more profound relational

568 Academy of Management Journal June

ties that extend beyond the shareholder-firm rela-tions observed in arm's-length governance systems.

In this study, we considered the effects of own-ership structure on intercorporate profit redistribu-tion. Specifically, we evaluated whether ownershipties in particular, the ties between Japanese finan-cial institutions and nonfinancial corporations andthe firms in which they hold shares—result in thesame pattern of profit redistribution observed byLincoln et al. (1996) with respect to keiretsu ties.Accordingly, we propose;

Hypothesis 2a. The relationship between thesize of the ownership stake of corporate block-holders and firm profitability is conditioned byprior profitability. Firms with low prior profitsbenefit from high levels of ownership in thehands of blockholders, but firms with highprior profits have their profitability reduced.

Hypothesis 2b. The relationship between thesize of the shareholdings of Japanese financialinstitutions and Japanese nonfinancial corpo-rations and firm profitability is conditioned byprior profitability. Firms with low prior profitsbenefit from these equity ties, but firms with highprior profits have their profitability reduced.

METHODS

Specification

Agency theory suggests that the empirical rela-tionship between ownership concentration andperformance can be estimated by an equation in theform

77,, = a + filownership concentration^

(1)

Equation 1 estimates the direct impact of owner-ship concentration on firm profitability (TT), hold-ing constant a vector of control variables (X).Agency theory suggests that the equation's beta co-efficient is greater than zero (j31 > 0). Our use ofpanel data is indicated by the subscripts, with idenoting a cross-sectional observation (a firm) andt denoting time. Our hypotheses are framed interms of three measures of ownership structure de-scribed below; ownership concentration amongblockholders without regard to identity, the totalownership shares of Japanese financial institutions,and the ownership shares of Japanese nonfinancialcorporations. Accordingly, we estimated Equation1 three times. Estimates indicating a beta greaterthan zero for each measure of ownership concen-tration would support Hypotheses la and lb.

which claim that there is a positive, direct relation-ship between ownership structure and firm perfor-mance in Japan.

Equation 1 does not account for redistributioneffects. Following Lincoln and colleagues (1996),we adopted a dynamic extension of the model thatallowed us to test both the agency and redistribu-tion hypotheses.

TT,, = a + ^2ownership share^ + 8X,, + A7r,,_i

+ ^ownership s/iare,, X TTH-I + e,-, (2)

Equation 2 suggests that firm performance dependsnot only on ownership, but also on past profitabil-ity. Lincoln et al. suggested that the coefficient onthe lagged profitability term would reflect the abil-ity of Japanese firms to redistribute profits. Thelower the coefficient, the greater is the redistribu-tion effect.^ In such a specification, a possibleagency effect is still captured by the direct effect ofownership on profitability, and Hypotheses la andlb would be supported by a finding that /32 isgreater than zero for each ownership measure. AsLincoln and coauthors suggested (1996; 73-74), thedegree to which ownership structures influence theextent of redistribution can be estimated by phi (4>),the coefficient on the interactive term betweenownership concentration and past profitability. Inour case, the hypotheses that redistribution is facil-itated by ownership concentrated in the hands ofblockholders (2a) or, more specifically, in thehands of either Japanese financial or nonfinancialcorporations (2b) will receive support if phi is lessthan zero for each ownership measure. That is, anegative phi coefficient would imply that an own-ership variable is associated with the redistributionof profits ffom more to less profitable firms.

Sample and Variables

The data consist of pooled time series and cross-sectional observations of 334 listed Japanese firmsspanning 1986-91 (fiscal years). Firms included inthe sample represent a broad cross-section of me-

^ This may be seen by considering the partial deriva-tive of current profitability with respect to past profit-ability in Equation 2. The higher the value, the morelikely it is that high (or low) profits persist. Redistribu-tion from high-profitability firms to low-profitabilityfirms smoothes out performance over time and lowersthe estimated coefficient on the lagged term. As indicatedin Equation 2, we have assumed a one-period lag. Thischoice is consistent with the literature on the persistenceof profitability [Mueller, 1990), though Lincoln et al.(1996) averaged the one- and two-year lagged profits.

2002 Gedajlovic and Shapiro 569

dium and large (minimum US $50 million), pub-licly traded, private sector Japanese firms drawnfrom eight industrial sectors (automobiles andparts, food and beverages, electronics, transporta-tion, retailing, oil and gas, pulp and paper, andindustrial machinery). The data source for the fi-nancial variables was Worldscope Disclosure, andtbis database established the maximum number ofobservations and the basic sample. WorldscopeDisclosure does not supply detailed ownership andbanking data on Japanese firms; these data werecollected from the Japan Company Handbook.

The dependent variable in all equations is firmprofitability. We measured profitability using re-turn on assets (ROA), the ratio of net income to totalassets. ROA is a commonly used measure of prof-itability and has been used by others in the Japa-nese context (e.g., Prowse, 1992; Lincoln et al.,1996). Prowse (1992) noted that since stock marketreturns are expected to adjust for any divergencesbetween shareholders and managers, accounting-based measures such as ROA are preferable in stud-ies relating ownersbip structure to financial perfor-mance.

Tbe most important independent variables interms of our bypotheses are three measures of own-ership structure. The first measure, ownership byfive largest blockholders, is a measure of ownershipconcentration that does not distinguish sharehold-ers' identities. This measure is identical to the pri-mary one used by Prowse (1992). Tbis variable wasused to evaluate Hypotheses la and 2a. As de-scribed above, a distinguishing feature of corporateownership in Japan is the fact that other Japanesefirms hold significant proportions of firms' out-standing shares. Consequently, we consider twoadditional ownership variables; ownership by fi-nancial institutions and ownership by nonfinancialcompanies. Each measure is equal to the percent-age of a company's outstanding shares held by Jap-anese financial and nonfinancial companies, re-spectively. These variables were used to evaluateHypotheses lb and 2b.

The following variables constituted control (ex-ogenous) variables, previously subsumed under thevector X in Equations 1 and 2. We chose thesevariables to control for factors other than owner-ship structure that have been sbown to affect prof-itability. Firm size, measured as the log of totalassets, was included to account for the potentialeconomies of scale and scope accruing to largefirms. If present, these would produce a positiverelationship between firm size and profitability.Firm growth, measured as year-over-year salesgrowth, was used as a control for demand condi-tions and product-cycle effects. Financial leverage.

measured as the ratio of debt to capital employed,was included because a firm's capital structure mayinfluence its investment decisions and the discre-tion afforded its managers (Harris & Raviv, 1991). Aseries of indicator variables was also included in allmodels, as controls for industry affiliation.

The focus of this study was on the effects ofownership structure rather than main bank^ or ke-reitsu ties. We controlled for main bank effectsthrough the use of an indicator variable represent-ing whether a firm's main bank was one of Japan'sBig Six banks (Sumitomo, Mitsui Taiyo Kobe, Dai-Ichi Kangyo, Fuji, Sanwa, or Mitsubishi). Approx-imately 70 percent (234) of the firms included inour sample had a Big Six main bank. To control forkereitsu ties, we followed Lincoln et al. (1996) andused an indicator variable measuring whether afirm was a member of the shacho-kai (Presidents'Club) of a Big Six keiretsu. Tbe sample contains 51firms with shacho-kai membership (15 percent ofthe sample).

ESTIMATION AND RESULTS

Equation 1 can be estimated by conventionalpanel data metbods (fixed- and random-effects).We first estimated the model using ordinary leastsquares (OLS). We then estimated the same modelusing a fixed-effects model and used a Lagrangemultiplier test (Greene, 1993; 476) to choose be-tween it and OLS. The fixed-effects model waspreferred in all cases. The model was then esti-mated with a generalized least squares (GLS) ran-dom-effects model. We compared this to the fixed-effects model using the Hausman test (Baltagi,1995; 68) and in all cases chose the random-effectsmodel. As a consequence, we report the random-effects results in Table 2 below.'*

Dynamic panel data models such as the one re-quired to test Hypotheses 2a and 2b, represented byEquation 2, can pose serious estimation cballengessince the lagged dependent variable will be corre-lated with the cross-sectional component of theerror term (Baltagi, 1995; 125-126). Standard paneldata techniques can produce parameter estimates

^ As noted, a typical Japanese corporation has a mainbank that extends it credit, owns its shares, providesprofessional services, and generally advances its busi-ness interests (Gerlach, 1992).

* We performed estimation using the panel procedurein LIMDEP 7.0, which allows computation of robust stan-dard errors. Output includes the degree of autocorrela-tion of the error terms, and these provided no indicationthat autocorrelation was present.

570 Academy of Management Journal June

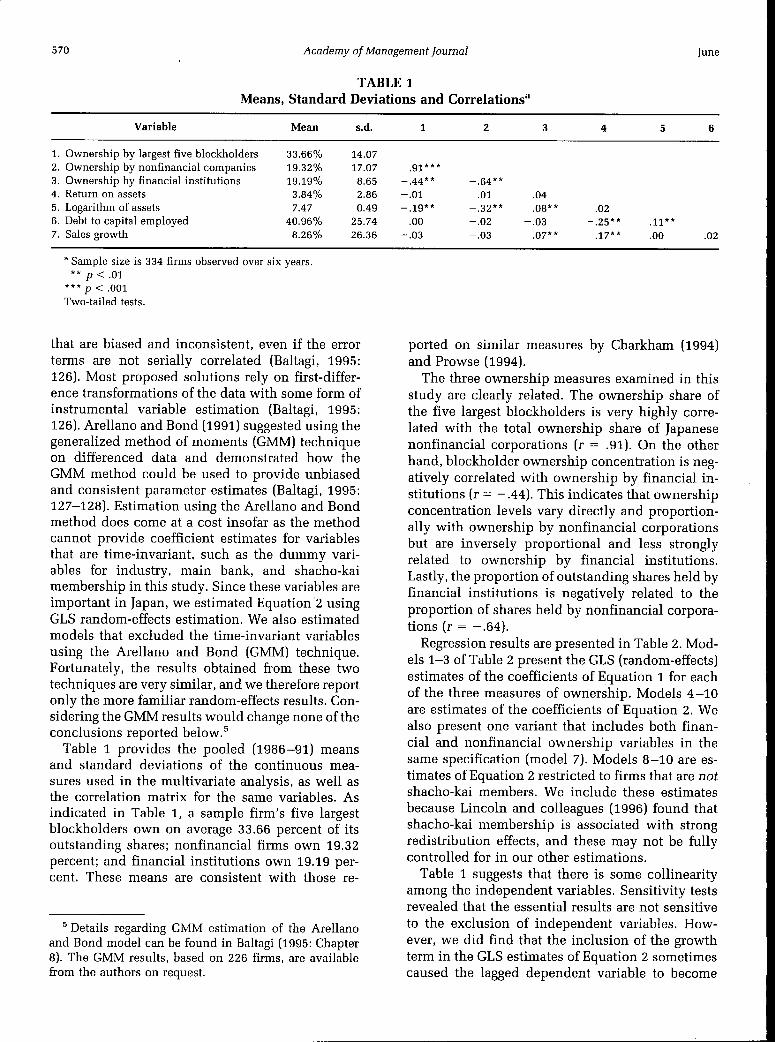

TABLE 1Means, Standard Deviations and Correlations"

Variable

1. Ownership by largest five blockholders2. Ownership by nonfinancial companies3. Ownership by financial institutions4. Return on assets5. Logarithm of assets6. Debt to capital employed7. Sales growth

Mean

33.66%19.32%19.19%3.84%7.47

40.96%8.26%

S.d.

14.0717.078.652.860.49

25.7426.36

1

.91***-.44**-.01-.19**

.00-.03

2

-.64**.01

-.32**-.02-.03

3

.04

.08**-.03

.07**

4

.02-.25**

.17**

5

.11**

.00

6

.02

" Sample size is 334 firms observed over six years.** p < .01

*** p < .001Two-tailed tests.

that are biased and inconsistent, even if the errorterms are not serially correlated (Baltagi, 1995:126). Most proposed solutions rely on first-differ-ence transformations of the data with some form ofinstrumental variable estimation (Baltagi, 1995:126). Arellano and Bond (1991) suggested using thegeneralized method of moments (GMM) techniqueon differenced data and demonstrated how theGMM method could be used to provide unbiasedand consistent parameter estimates (Baltagi, 1995:127-128). Estimation using the Arellano and Bondmethod does come at a cost insofar as the methodcannot provide coefficient estimates for variablesthat are time-invariant, such as the dummy vari-ables for industry, main bank, and shacho-kaimembership in this study. Since these variables areimportant in Japan, we estimated Equation 2 usingGLS random-effects estimation. We also estimatedmodels that excluded the time-invariant variablesusing the Arellano and Bond (GMM) technique.Fortunately, the results obtained from these twotechniques are very similar, and we therefore reportonly the more familiar random-effects results. Con-sidering the GMM results would change none of theconclusions reported below.^

Table 1 provides the pooled (1986-91) meansand standard deviations of the continuous mea-sures used in the multivariate analysis, as well asthe correlation matrix for the same variables. Asindicated in Table 1, a sample firm's five largestblockholders own on average 33.66 percent of itsoutstanding shares; nonfinancial firms own 19.32percent; and financial institutions own 19.19 per-cent. These means are consistent with those re-

^ Details regarding GMM estimation of the Arellanoand Bond model can be found in Baltagi (1995: Chapter8). The GMM results, based on 226 firms, are availablefrom the authors on request.

ported on similar measures by Gharkham (1994)and Prowse (1994).

The three ownership measures examined in thisstudy are clearly related. The ownership share ofthe five largest blockholders is very highly corre-lated with the total ownership share of Japanesenonfinancial corporations (r = .91). On the otherhand, blockholder ownership concentration is neg-atively correlated with ownership by financial in-stitutions (r = -.44). This indicates that ownershipconcentration levels vary directly and proportion-ally with ownership by nonfinancial corporationsbut are inversely proportional and less stronglyrelated to ownership by financial institutions.Lastly, the proportion of outstanding shares held byfinancial institutions is negatively related to theproportion of shares held by nonfinancial corpora-tions (r = -.64).

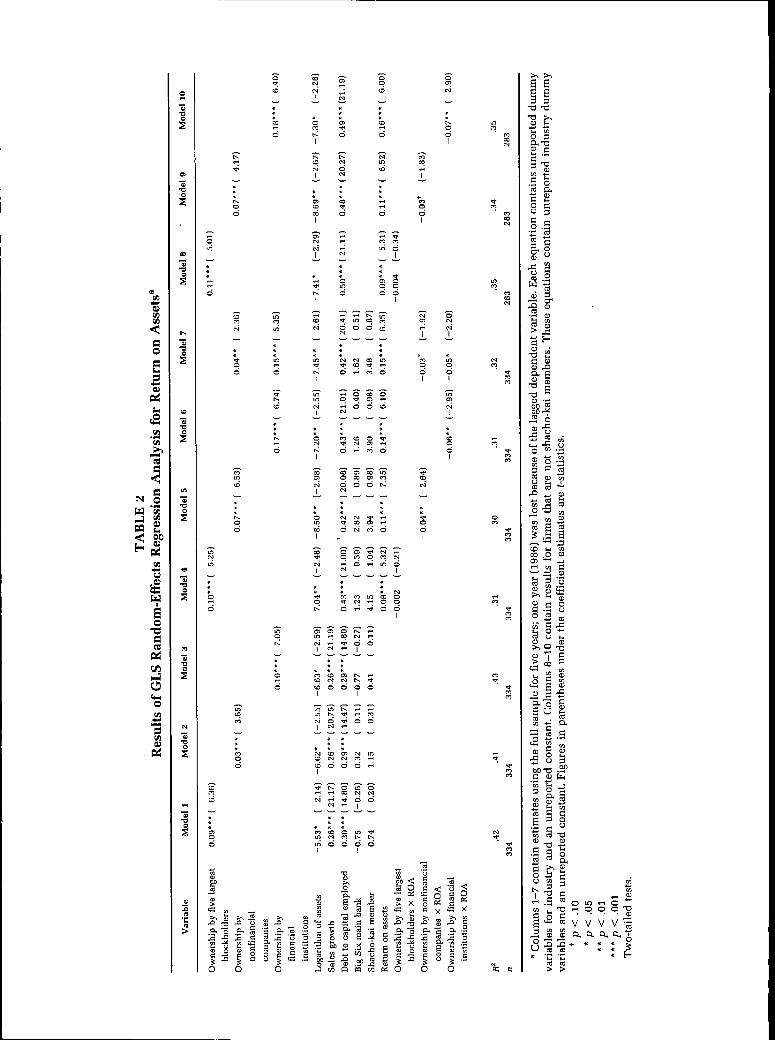

Regression results are presented in Table 2. Mod-els 1-3 of Table 2 present the GLS (random-effects)estimates of the coefficients of Equation 1 for eachof the three measures of ownership. Models 4-10are estimates of the coefficients of Equation 2. Wealso present one variant that includes both finan-cial and nonfinancial ownership variables in thesame specification (model 7). Models 8-10 are es-timates of Equation 2 restricted to firms that are notshacho-kai members. We include these estimatesbecause Lincoln and colleagues (1996) found thatshacho-kai membership is associated with strongredistribution effects, and these may not be fullycontrolled for in our other estimations.

Table 1 suggests that there is some collinearityamong the independent variables. Sensitivity testsrevealed that the essential results are not sensitiveto the exclusion of independent variables. How-ever, we did find that the inclusion of the growthterm in the GLS estimates of Equation 2 sometimescaused the lagged dependent variable to become

BQ

o•a

in CO m0 0(0

CM CMTP ID

d i-i

S 5rH d

O CM CO O

00)

39)

o

04;

32

)

in

21

)

o1

CD O O O O

CO O O O

CM

rr,in

rH

COCM

OCO

...0

cn

CM

1

in

oegn

in o o o o

--H "^

n.aa.a

572 Academy of Management Journal June

statistically insignificant. Since this result is notconsistent with our other estimates, nor with theresults of other studies (e.g., Lincoln et al., 1996),and since it could imply that the effects of laggedprofitability are negative (when the interactionterm is negative), we omitted the sales growth con-trol variable from models 4-10 of Table 2.

The results can be summarized quite concisely.Regardless of sample size or specification, there isstrong evidence that the direct effect of ownershipconcentration on firm profitability in Japan is pos-itive and statistically significant, for all three mea-sures of ownership structure considered here.Thus, we find evidence in support of Hypothesesla and lb and in support of the view that standardagency theory is relevant in Japan. At the sametime, regardless of sample size or specification, thesign of the interaction between lagged profitabilityand the shares of both financial and nonfinancialfirms is negative and statistically significant. Thatis, there is strong evidence that large ownershipstakes held by financial and/or nonfinancial firmsfacilitate redistribution and therefore raise (lower)profitability for the least (most) profitable firms.Thus, we find strong evidence in support of Hy-pothesis 2b. On the other hand, when ownershipstructure is evaluated simply in terms of concen-tration levels that do not account for the identity ofowners (the shares of the largest blockholders), theinteraction term is not statistically significant inany specification or sample. Thus, Hypothesis 2a isrejected. Insofar as redistribution effects are foundto be associated with ownership by strategic inves-tors (financial institutions and nonfinancial com-panies), but not with an undifferentiated measureof ownership concentration, these findings indicatethat shareholder identity matters.

When we account for the identity of owners byusing the ownership shares of financial and nonfi-nancial companies, the results suggest that bothagency and redistributive effects are operative inJapan. However, they are not of equal strength. Anevaluation of the relevant equations (models 5, 6, 7,9, 10) indicates that, with other factors held con-stant, the combined effect of ownership by finan-cial and nonfinancial companies is negative whenprofitability is evaluated at the mean value oflagged ROA (3.6). That is, the net effect of theselarge ownership stakes is positive only for the leastprofitable Japanese firms. In these cases, the agencyeffect and the redistribution effect combine to ben-efit poorly performing firms. The estimates in Table2 indicate that firms with ROA levels below 2-2.5percent benefit from redistribution. However, for

firms with higher profit rates, the net effects ofthese large shareholdings are negative.^

The results are also clear as to whether financialor nonfinancial companies create stronger redistri-bution effects. Whether each term enters the equa-tion separately or jointly, and regardless of sample,GLS estimates suggest that financial firms providestronger redistribution effects. This is seen from themagnitude of the relevant coefficients on the inter-active ownership-lagged profitability terms. Thecoefficient for the ownership share of financial in-stitutions (-0.06 [-0.063]) is roughly twice that fornonfinancial firms (-0.04 [-0.035]) for the fullsample (models 5-6) and even greater when thesample is restricted to companies that are not sha-cho-kai members (-0.07 versus -0.03, in models9-10).

In concluding this section, we note that thecoefficients of the reported control variables arereasonably stable across specifications. Firmgrowth is positively related to profitability, andthe relationship with firm size is always negative.Both of these results are consistent with thoseobtained by Lincoln, Gerlach, and Ahmadjian(1996). The estimates also suggest that firms withhigher levels of debt are more profitable, reflect-ing perhaps the risk associated with debt. Fi-nally, we find no evidence that having a Big Sixmain bank or shacho-kai membership is directlyrelated to profitability. These results are not al-tered when one or the other of these two variablesis excluded from the equation.

® Statements in this paragraph are based on calcula-tions found by taking the partial derivative of profitabil-ity (the dependent variable) with respect to ownershipconcentration. Consider models 5 and 6. The effect of a 1percent change in the ownership share of nonfinancialcorporations is given by 0.07 — 0.04 x lagged ROA (mod-el 5) and .17 - 0.06 X lagged ROA (model 6). Thus, thereis a positive direct (agency) effect of 0.07 (.17), but anegative indirect (redistribution) effect, the magnitude ofwhich depends on past profitability. With evaluation atthe mean for lagged ROA (3.6), it is readily seen that thenet effect is negative. The point at which net negativeeffects set in is found by solving for the level of pastprofitability that sets .07 - 0.04 X lagged ROA equal tozero for model 5 and 0.17 -0.06 X lagged ROA equal tozero for model 6. This occurs where lagged ROA = 2.11(model 5) and 2.54 (model 6). Firms with lagged profitsbelow these amounts will experience a positive owner-ship effect. Calculations for other models produce simi-lar results.

2002 Gedajlovic and Shapiro 573

DISCUSSION AND CONCLUSIONS

In positing a positive relationship between own-ership concentration and firm performance, agencytheorists focus on the economic incentives associ-ated with separated ownership and control, with-out regard to social context. On the other hand,sociological treatments of Japanese industrial or-ganization highlight the distinctive character oftraditional Japanese business relationships distin-guished by intercorporate goals of risk reductionand mutual assistance (Dore, 1983; Gerlach, 1992).Insofar as clear agency and redistribution effectswere observed, our results indicate that the rela-tionship between ownership concentration andfirm performance in Japan reflects both economicincentives and social context.

Since the redistribution effects are stronger thanthe agency effects, the net impact of ownershipconcentration is negative for most Japanese firms.Although firms with relatively high profits sufferimpaired profitability, firms with low and, partic-ularly, those with negative profits appear to benefitfrom concentrated ownership in two ways. Ourfinding of a positive direct relationship betweenownership concentration and performance suggeststhat large Japanese investors can operate as effec-tive monitors of top executives in other firms. Atthe same time, our finding of significant redistribu-tion effects indicates that poorly performing firmswith concentrated ownership structures also bene-fit from the transfer of financial resources frommore profitable firms. Insofar as an investor's incli-nation to redistribute profits to a weaker firm islikely to be positively related to its ability to mon-itor how those proceeds are utilized, agency andredistribution effects may act in tandem and rein-force each other.

Our results clearly indicate that shareholderidentity matters. When we measured ownershipconcentration without reference to the identity ofthe investor, we found agency effects but not redis-tribution effects. Redistribution effects were foundonly when we examined the ownership shares offinancial and nonfinancial firms. Such a result isconsistent with the notion that distinct classes ofshareholders differ in their investment objectivesand capacities to influence corporate behavior(Thomsen & Pedersen, 2000). Research that exam-ines whether similar redistribution effects are ap-parent in other networked and/or relational gover-nance systems would constitute a logical follow-upto this research.

The findings reported here support and extendprevious research showing that Japanese financialinstitutions organize bailouts for troubled indus-

trial firms with whom they have close keiretsu ordebt ties (Morck & Nakamura, 1999; Hoshi et al.,1990). The result that similar (though weaker) re-distribution effects are associated with the share-holdings of nonfinancial corporations provides ev-idence that industrial firms also assist firms withwhich they have equity ties. Further, our resultsindicating that firms with ROA levels as high as2-2.5 percent benefit from profit redistribution sug-gests that redistribution is ongoing and is not re-stricted to situations of severe financial distress. Insummary, the study offers strong evidence that cor-porate ownership concentration is associated withthe same type of profit redistribution observed byLincoln and colleagues (1996) among firms sharingkeiretsu ties. As such, our study indicates that tra-ditional norms of mutual assistance (Dore, 1983)and risk reduction (Nakatani, 1984) extend beyondformal networks to Japan's broader enterprisesystem.

Since the results reported here pertain to a period(1986-91) that predates significant structural re-form to Japan's financial system as well as its bank-ing crisis, care must be taken in generalizing ourfindings to the current situation. On the one hand,it is widely believed that Japan's enterprise andgovernance systems have become much less rela-tional and that traditional business practices haveeroded significantly in recent years (Fukao, 1999).On the other hand, traditional Japanese businesspractices have proven remarkably resilient in thepast (Dore, 1983; Gerlach, 1992). Further, the redis-tribution effects observed here relate to a timewhen Japanese businesses were already under se-vere pressure from the endaka (high yen) shock aswell as the bubble economy of 1987-90 and itssubsequent collapse. Ultimately, the question ofwhether such traditional business practices havepersisted through Japan's recent economic travailsremains an open empirical question for subsequentresearch. In this regard, the findings reported heremay constitute a useful benchmark for future re-search aimed at gauging the scope and degree ofchange in Japanese traditional business practices asthat country continues to reform its financial andenterprise systems.

REFERENCES

Alchian, A. A., & Demsetz, H. 1972. Production, infor-mation costs and economic organization. AmericanEconomic Review, 62: 777-795.

Aoki, M. 1988. Information, incentives and bargainingin the Japanese economy. Cambridge, England:Cambridge University Press.

574 Academy of Management Journal June

Aoki, M., Patrick, H., & Sheard, P. 1994. Monitoringcharacteristics of the main bank system: An analyti-cal and historical view. In M. Aoki & H. Patrick(Eds.), The Japanese main bank system: Its rele-vancy for developing and transforming economies:1-50. Oxford, England: Oxford University Press.

Arellano, M., & Bond, E. 1991. Some tests of specificationfor panel data. Review of Economic Studies, 58:277-297.

Baltagi, B. 1995. Econometric analysis of panel data.New York: Wiley.

Berglof, E., & Perotti, E. 1994. The governance structureof the Japanese financial keiretsu. Journal of Finan-cial Economics, 36: 259-284.

Cable, ]., & Yasuki, H. 1985. Internal organization, busi-ness groups and corporate performance: An empiri-cal test of the multi-divisional hypothesis in Japan.International Journal of Industrial Organization,3: 401-420.

Charkham, J. P. 1994. Keeping good company: A studyof corporate governance in five countries. NewYork: Oxford University Press.

Claessens, S., Djankov, S., & Lang, L. 2000. The separa-tion of ownership and control in East Asian corpo-rations. Journal of Financial Economics, 58: 81-112.

Clark, R. 1979. The Japanese company. New Haven, CT:Yale University Press.

Dore, R. 1983. Goodwill and the spirit of market capital-ism. Rritish Journal of Sociology, 34: 459-482.

Dyer, J. H. 1996. Does governance matter? Keiretsu alli-ances and asset specificity as sources of Japanesecompetitive advantage. Organization Science, 7:649-667.

Eisenhardt, K. 1989. Agency theory: An assessmentand review. Academy of Management Review, 14:57-74.

Fukao, M. 1999. Japanese financial instability andweakness in the corporate governance structure.Paris: OECD.

Gedajlovic, E. R. 1993. Ownership, strategy and perfor-mance: Is the dichotomy sufficient? OrganizationStudies, 14: 731-752.

Gedajlovic, E. R., & Shapiro, D. M. 1998. Managementand ownership effects: Evidence from five countries.Strategic Management Journal, 19: 533-553.

Cerlach, M. L. 1992. Alliance capitalism: The socialorganization of Japanese business. Berkeley: Uni-versity of California Press.

Greene, W. 1993. Econometric analysis. New York:Macmillan.

Hamilton, G. G., & Biggart, N. W. 1988. Market, cultureand autbority: A comparative analysis of manage-ment and organization in the far east. AmericanJournal of Sociology, 94: S52-S94.

Harris, M., & Raviv, A. 1991. The theory of capital struc-ture. Journal of Finance, 46: 297-355.

Hoshi, T., Kashyap, A., & Scharfstein, D. 1990. The roleof banks in the costs of financial distress in Japan.Journal of Financial Economics, 27: 67-88.

Hoshi, T., Kashyap, A., & Scharfstein, D. 1991. Corporatestructure liquidity and investment: Evidence fromJapanese industrial groups. Quarterly Journal ofEconomics, 106: 33-60.

Jensen, M. C, & Meckling, W. H. 1976. Theory of thefirm: Managerial behavior, agency costs and owner-ship structure. Journal of Financial Economics, 3:305-360.

Lincoln, J. R., Gerlach, M. L., & Ahmadjian, C. L. 1996.Keiretsu networks and corporate performance in Ja-pan. American Sociological Review, 61: 67-88.

Milgrom, P., & Roberts, J. 1992. Economics, organiza-tion, and management. Englewood Cliffs, NJ: Pren-tice-Hall.

Morck, R., & Nakamura, M. 1999. Banks and corporatecontrol in Japan. Journal of Finance, 54: 319-341.

Mueller, D. C. 1990. The dynamics of company profits:An international comparison. Cambridge, England:Cambridge University Press.

Nakatani, I. 1984. The economic role of the financialcorporate grouping. In M. Aoki (Ed.), The economicanalysis of the Japanese firm: 227-259. Amster-dam: North-Holleind.

Prowse, S. 1992. The structure of corporate ownersbip inJapan. Journal of Finance, 47: 1121-1140.

Prowse, S. 1994. Corporate governance in an interna-tional perspective. Basel: Bank for International Set-tlements.

Roe, M. f. 1994. Strong managers, weak owners. Prince-ton, NJ: Princeton University Press.

Shleifer, A., & Vishny, R. W. 1997. A survey of corporategovernance. Journal of Finance, 52: 737-783.

Thomsen, S., & Pedersen, T. 2000. Ownership structureand economic performance in the largest Europeancompanies. Strategic Management Journal, 21:689-705.

Walsh, J. P., & Seward, J. K. 1990. On the efficiency ofinternal and external corporate control mechanisms.Academy of Management Review, 15: 421-458.

Weinstein, D., & Yafeh, Y. 1995. Japan's corporategroups: Collusive or competitive. Journal of Indus-trial Economics, 43: 359-377.

2002 Gedajlovic and Shapiro 575

Eric Gedajlovic ([email protected] is an associateprofessor of international business in the Strategy andBusiness Environment Department at tbe RotterdamSchool of Management. He received his Ph.D. from Con-cordia University. Much of his research focuses on thecomparative analysis of business, financial, and gover-nance systems and their impacts upon the developmentof firm capabilities, strategic assets, and national compet-itiveness.

Daniel Shapiro is a professor of business and economicpolicy in tbe Faculty of Business Administration, SimonFraser University. He received his Ph.D. from CornellUniversity. His recent research focuses on national sys-tems of corporate governance and tbeir impact on firmperformance and tbe role of governance infrastructure asa determinant of foreign direct investment flows.