Overview Strategic Cost and Financial Management.

18

Overview Strategic Cost and Financial Management

-

Upload

brooke-alexander -

Category

Documents

-

view

213 -

download

0

Transcript of Overview Strategic Cost and Financial Management.

Overview

Strategic Cost and Financial

Management

Session Objectives

• Recognize how to control fixed and variable costs

• Understand the importance of financial statements

• Be familiar with financial ratios and what they mean

• Insert a polling question:

• Do you track fixed costs?

• Do you track variable costs?

Four Steps to Cutting Cost

1). Know your fixed and variable costs

2). Identify benchmarks

3). Get buy-in from staff

4). Determine when to take action

Concepts

• Numbers Don’t Lie!!!

• Benchmarking

• Report Preparation– Frequency of report preparation– Review of practice management and

financials should be the first agenda item in management meetings

Development of the Financial Reporting System

Step 3: Tailor / customizethe system to

meet your needs.

Step 2: Develop reports to meet the needs

of the various users.

Step 1: Identify the needs of the users of the information.

Step 5: Continually re-evaluate systemneeds vs. output.

Step 4: Develop standard processing list of reports,

timing and distribution.

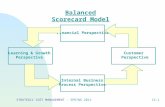

Financial Statement Interpretation

• Balance Sheet– Snapshot of the health center’s finances taken

at a single point in time

– Also known as a statement of financial position

• Income Statement– Measure of a health center’s financial

performance over a specific accounting period

– Also known as the statement of revenue and expenses

Tips on Analyzing the Balance Sheet

• Current Ratio

• Days in Accounts Receivable

• Days in Accounts Payable

• Days in working Capital

Tips on Analyzing the Balance Sheet

• Current Ratio = current assets divided by current liabilities.

Want this ratio to be at least 1:1 and do not want to decrease over time.

–$528,000/$600,500 = 0.88

Tips on Analyzing the Balance Sheet

• Days in Accounts Receivable = net patient accounts receivable, divided by average daily patient revenue

([Patient revenue, net of adjustments and bad debt, excluding managed care capitation] divided by # of days in period)

Increase in ratio indicates potential billing problem and could hurt cash flow.

($272,000/(($900,000-$230,370)/365) = 148 days

Tips on Analyzing the Balance Sheet (cont.)

• Days in Accounts Payable = Trade accounts payable and accrued expenses divided by average daily trade expenses

([Total expenses less salaries and wages, donated services, bad debt and depreciation] divided by # of days in period)

An increase indicates that the health center is paying vendors more slowly, indicating a cash flow problem.

$225,500/(($2,004,500 - $1,216,475 - $47,500)/365) = 111 days

Tips on Analyzing the Balance Sheet (cont.)

• Days in Working Capital = Working capital (current assets minus current liabilities) divided by average daily operating expenses (Total expenses divided by # of days in period)

This is a reserve ratio indicating the financial condition of the health center; goal is to be greater than 30 days.

($528,000-$600,500)/(($2,004,500 + $25,000)/365) = (13) days

Income Statement Analysis

• Trend and Relationships– Cost per encounter– Net revenue per encounter– Shift in payor mix– Change in reimbursement rates

Tips on Analyzing the Statement of Operations

Trends and Relationships:

• Analyze changes in patient revenue as compared to changes in patient volume (i.e., visits), prior year vs. current year and current year vs. budget.

• Any unusual trends should be researched:

Change in reimbursement rates

Shifts in payor mix

What to Look for …

• Balance Sheet– Accounts payable– Excessive debt

• Income Statement– Proper presentation– Comparing revenue to payment posting– How to analyze overhead

What to Look for … (cont.)

• Sudden change in A/R tendencies

• Failing to reach benchmarks

• Sudden changes in production by Clinician( or other staff)

• Escalating overhead costs

• Inability to pay vendors in timely fashion

• Borrowing money

Things to Consider

• Flex- Time

• Volunteers/Interns

• New Revenue Streams

• Low Cost Incentives for Productivity

Questions?

Gervean Williams

Director of Finance and Operations

NACHCNational Association Community Health Care Centers