Overview & Outlook for the P/C Insurance Industry: Behind the Numbers Alabama I-Day Tuscaloosa, AL...

51

Overview & Outlook for the P/C Insurance Industry: Behind the Numbers Alabama I-Day Tuscaloosa, AL October 8, 2014 Steven N. Weisbart, Ph.D., CLU, Senior Vice President & Chief Economist Insurance Information Institute 110 William Street New York, NY 10038

-

Upload

phyllis-horn -

Category

Documents

-

view

216 -

download

1

Transcript of Overview & Outlook for the P/C Insurance Industry: Behind the Numbers Alabama I-Day Tuscaloosa, AL...

Overview & Outlookfor the P/C Insurance Industry:

Behind the Numbers

Alabama I-DayTuscaloosa, ALOctober 8, 2014

Steven N. Weisbart, Ph.D., CLU, Senior Vice President & Chief EconomistInsurance Information Institute 110 William Street New York, NY 10038

Tel: 212.346.5540 Cell: 917.494.5945 [email protected] www.iii.org

2

2013: Best Year (So Far)in the Post-Crisis Era

Performance Improved with Lower CATs, Firming Markets

2

3

P/C Net Premiums Written: % Change, Quarter vs. Year-Prior Quarter

Sources: ISO, Insurance Information Institute.

Sustained growth in written premiums(vs. the same quarter, prior year) should continue through 2014.

10.2

%15

.1%

16.8

%16

.7%

12.5

%10

.1%

9.7%

7.8%

7.2%

5.6%

2.9%

5.5%

-4.6

%-4

.1%

-5.8

%-1

.6%

10.3

%10

.2% 13

.4%

6.6%

-1.6

%2.

1%0.

0%-1

.9%

0.5%

-1.8

%-0

.7%

-4.4

%-3

.7%

-5.3

%-5

.2%

-1.4

%-1

.3%

1.3% 2.

3%1.

7% 3.5%

1.6%

4.1%

3.8%

3.0% 4.

2% 5.1%

4.8%

4.1% 4.7%

4.2% 4.7%

3.6% 4.2%

-10%

-5%

0%

5%

10%

15%

20%20

02:Q

120

02:Q

220

02:Q

320

02:Q

420

03:Q

120

03:Q

220

03:Q

320

03:Q

420

04:Q

120

04:Q

220

04:Q

320

04:Q

420

05:Q

120

05:Q

220

05:Q

320

05:Q

420

06:Q

120

06:Q

220

06:Q

320

06:Q

420

07:Q

120

07:Q

220

07:Q

320

07:Q

420

08:Q

120

08:Q

220

08:Q

320

08:Q

420

09:Q

120

09:Q

220

09:Q

320

09:Q

420

10:Q

120

10:Q

220

10:Q

320

10:Q

420

11:Q

120

11:Q

220

11:Q

320

11:Q

420

12:Q

120

12:Q

220

12:Q

320

12:Q

420

13:Q

120

13:Q

120

13:Q

320

13:Q

420

14:Q

120

14:Q

2

2014:Q1 marked the 16th consecutive quarter of y-o-y

growth

Underwriting Gain (Loss)All Lines Combined, 1975–2014*

* Includes mortgage and financial guaranty insurers in all years. 2014:1H is estimated.Sources: A.M. Best, ISO, Insurance Information Institute.

High CAT losses in 2011 led to the highest underwriting loss since 2001. Lower CAT losses in 2013

led to the highest underwriting profit since 2007.

-$60

-$50

-$40

-$30

-$20

-$10

$0

$10

$20

$30

75 76 77 78 79 80 81 82 83 84 85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13

14:1

H

($ Billions)Underwriting profit in 2013 was $15.5B

$1.22B 2014:1H profit

5

P/C Insurance Industry Combined Ratio, 2001–2014:1H

* Excludes Mortgage & Financial Guaranty insurers 2008--2012. Including M&FG, 2008=105.1, 2009=100.7, 2010=102.4, 2011=108.1; 2012:=103.2; 2013: = 96.1; 2014.1H: 98.9 Sources: A.M. Best, ISO.

95.7

99.3100.8

106.3

102.4

96.799.0

101.0

92.6

100.898.4

100.1

107.5

115.8

90

100

110

120

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

:1H

Best Combined

Ratio Since 1949

(87.6)

As Recently as 2001, Insurers

Paid Out Nearly $1.16 for Every

$1 in Earned Premiums

Relatively Low CAT Losses, Reserve Releases

Heavy Use of Reinsurance Lowered Net

Losses

Relatively Low CAT Losses, Reserve Releases

Avg. CAT Losses,

More Reserve Releases

Higher CAT

Losses, Shrinking Reserve

Releases, Toll of Soft

Market

Cyclical Deterioration

Sandy Impacts

Lower CAT

Losses

P/C Industry Net Income After Taxes1991–2014:1H

2005 ROE*= 9.6% 2006 ROE = 12.7% 2007 ROE = 10.9% 2008 ROE = 0.1% 2009 ROE = 5.0% 2010 ROE = 6.6% 2011 ROAS1 = 3.5% 2012 ROAS1 = 5.9% 2013 ROAS1 = 10.3%

• ROE figures are GAAP; 1Return on avg. surplus. Excluding Mortgage & Financial Guaranty insurers yields a 8.9% ROAS through 2013:Q3, 6.2% ROAS in 2012, 4.7% ROAS for 2011, 7.6% for 2010 and 7.4% for 2009.

Sources: A.M. Best, ISO; Insurance Information Institute

$1

4,1

78

$5

,84

0

$1

9,3

16

$1

0,8

70

$2

0,5

98

$2

4,4

04 $3

6,8

19

$3

0,7

73

$2

1,8

65

$3

,04

6

$3

0,0

29

$6

2,4

96

$3

,04

3

$3

5,2

04

$1

9,4

56 $

33

,52

2

$6

3,7

84

$2

5,9

80

$2

8,6

72

-$6,970

$6

5,7

77

$4

4,1

55

$2

0,5

59

$3

8,5

01

-$10,000

$0

$10,000

$20,000

$30,000

$40,000

$50,000

$60,000

$70,000

$80,000

91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13

14:1

H

Net income rose strongly (+81.9%)

vs. 2012$ Millions

-5%

0%

5%

10%

15%

20%

25%

75

76

77

78

79

80

81

82

83

84

85

86

87

88

89

90

91

92

93

94

95

96

97

98

99

00

01

02

03

04

05

06

07

08

09

10

11

12

13

14

Profitability Peaks & Troughs in the P/C Insurance Industry, 1975 – 2014:1H*

*Profitability = P/C insurer ROEs. 2011-13 figures are estimates based on ROAS data. Note: Data for 2008-2013 exclude mortgage and financial guaranty insurers.Source: Insurance Information Institute; NAIC, ISO, A.M. Best.

1977:19.0%1987:17.3%

1997:11.6% 2006:12.7%

1984: 1.8%1992: 4.5% 2001: -1.2%

10 Years

10 Years9 Years

History suggests next ROE peak will be in 2016-2017

ROE

1975: 2.4%

2013 10.4%

8

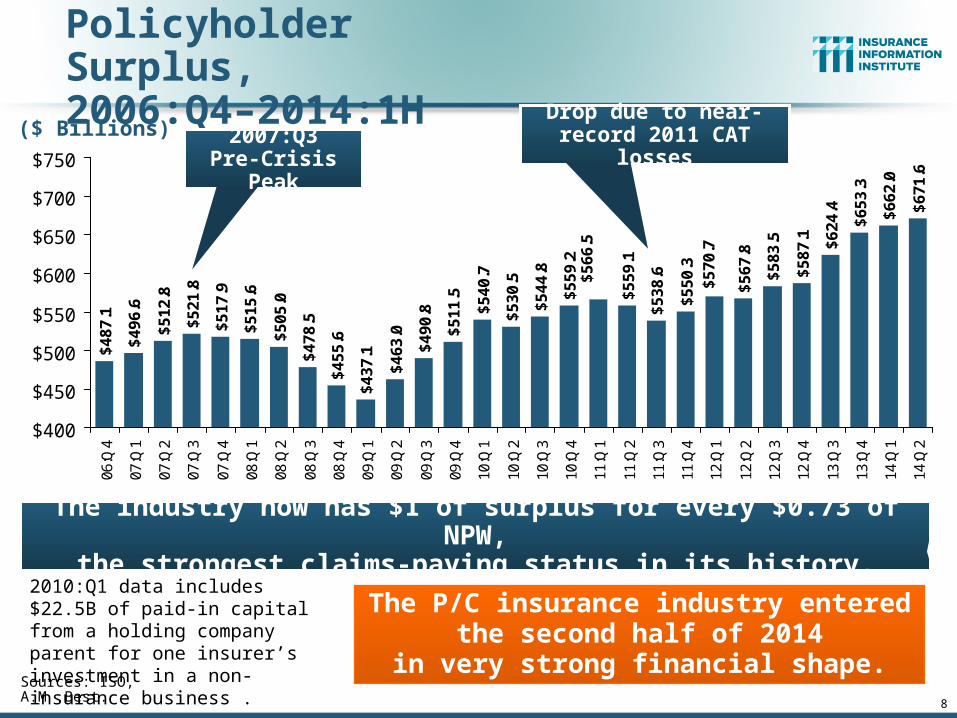

Policyholder Surplus, 2006:Q4–2014:1H

Sources: ISO, A.M .Best.

($ Billions)$4

87.1

$496

.6

$512

.8

$521

.8

$478

.5

$455

.6

$437

.1

$463

.0

$490

.8

$511

.5

$540

.7

$530

.5

$544

.8

$559

.2

$559

.1

$538

.6

$550

.3

$567

.8

$583

.5

$587

.1 $624

.4

$653

.3

$662

.0

$671

.6

$570

.7

$566

.5

$505

.0

$515

.6

$517

.9

$400

$450

$500

$550

$600

$650

$700

$750

06:Q

4

07:Q

1

07:Q

2

07:Q

3

07:Q

4

08:Q

1

08:Q

2

08:Q

3

08:Q

4

09:Q

1

09:Q

2

09:Q

3

09:Q

4

10:Q

1

10:Q

2

10:Q

3

10:Q

4

11:Q

1

11:Q

2

11:Q

3

11:Q

4

12:Q

1

12:Q

2

12:Q

3

12:Q

4

13:Q

3

13:Q

4

14:Q

1

14:Q

2

2007:Q3Pre-Crisis Peak

2010:Q1 data includes $22.5B of paid-in capital from a holding company parent for one insurer’s investment in a non-insurance business .

The industry now has $1 of surplus for every $0.73 of NPW,the strongest claims-paying status in its history.

Drop due to near-record 2011 CAT losses

The P/C insurance industry enteredthe second half of 2014

in very strong financial shape.

9

Profitability in P/C Marketsin Alabama

and Neighboring States

Analysis by Line and State

10

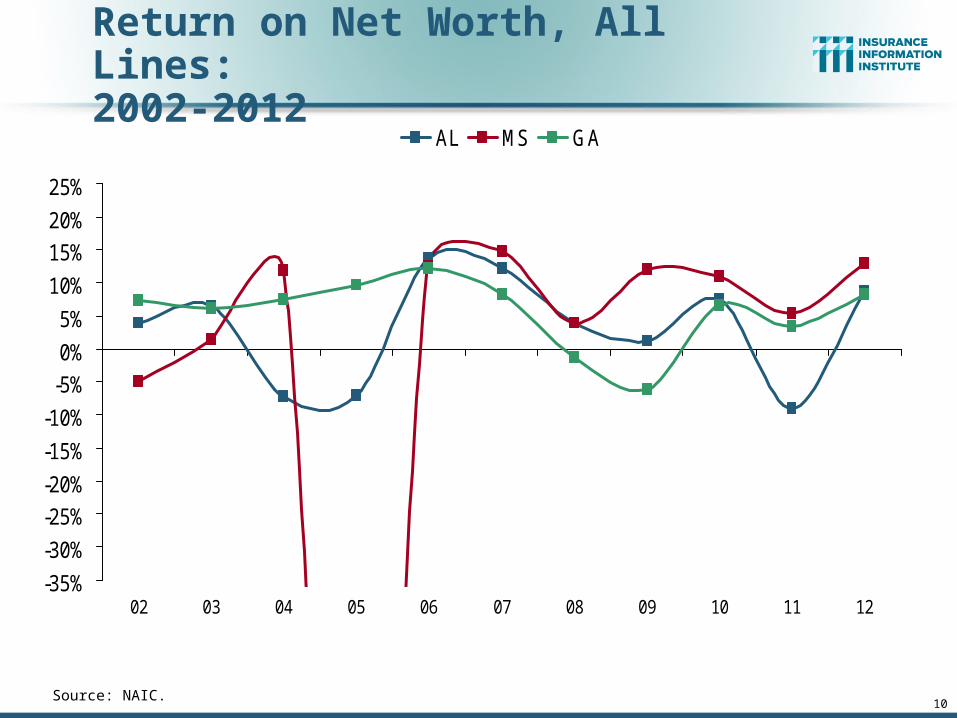

Return on Net Worth, All Lines:2002-2012

Source: NAIC.

-35%

-30%

-25%

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

02 03 04 05 06 07 08 09 10 11 12

AL MS GA

11

Return on Net Worth, All Lines:2002-2012

Sources: NAIC.

-35%

-30%

-25%

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

02 03 04 05 06 07 08 09 10 11 12

AL FL TN

12

Return on Net Worth, All Lines:2003-2012 Average, by State

Sources: NAIC.

8.6%7.9%

5.5%4.9%

2.0%

-6.5%-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

FL US GA TN AL MS

13

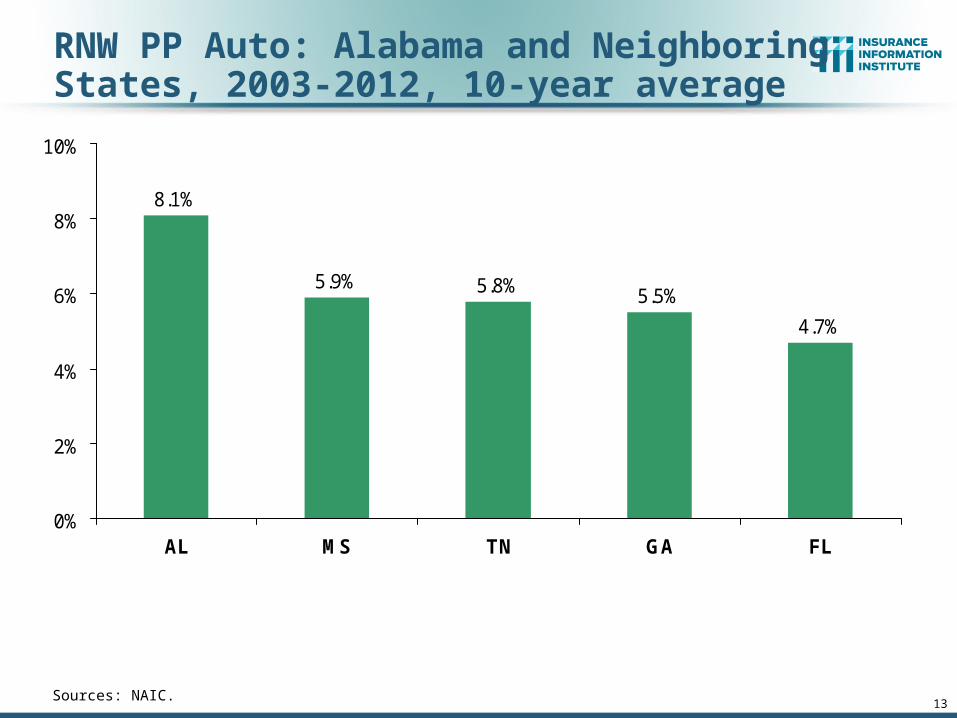

RNW PP Auto: Alabama and Neighboring States, 2003-2012, 10-year average

Sources: NAIC.

8.1%

5.9% 5.8% 5.5%

4.7%

0%

2%

4%

6%

8%

10%

AL MS TN GA FL

14

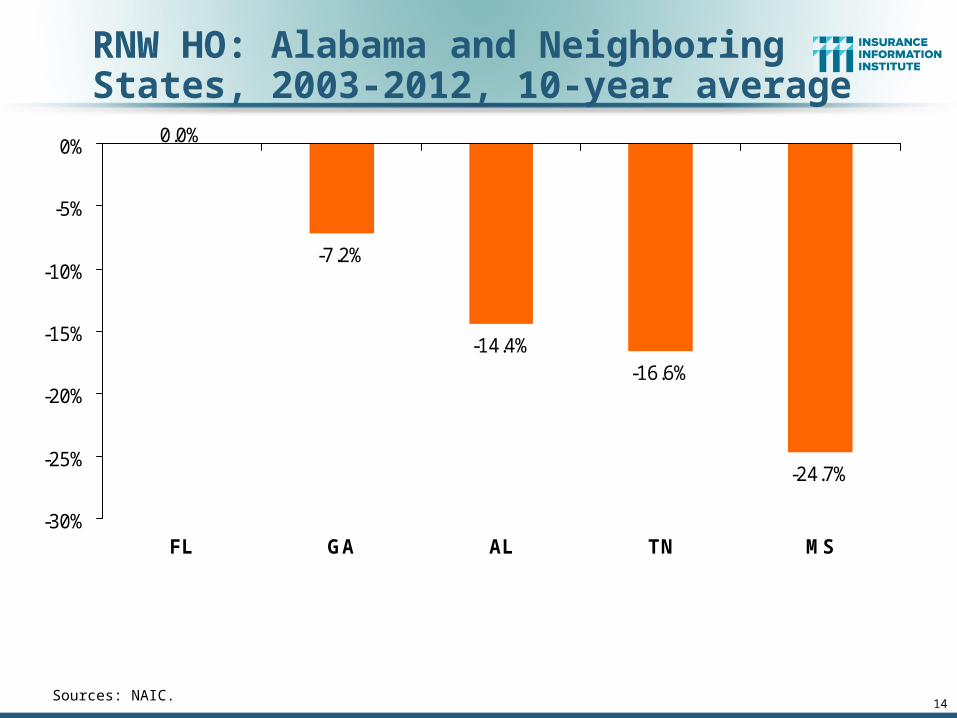

RNW HO: Alabama and NeighboringStates, 2003-2012, 10-year average

Sources: NAIC.

0.0%

-7.2%

-14.4%-16.6%

-24.7%

-30%

-25%

-20%

-15%

-10%

-5%

0%

FL GA AL TN MS

15

RNW CMP: Alabama and NeighboringStates, 2003-2012, 10-year average

Sources: NAIC.

7.3%

5.7%

1.8%

-2.2%

-3.7%

-6%

-4%

-2%

0%

2%

4%

6%

8%

FL GA TN AL MS

16

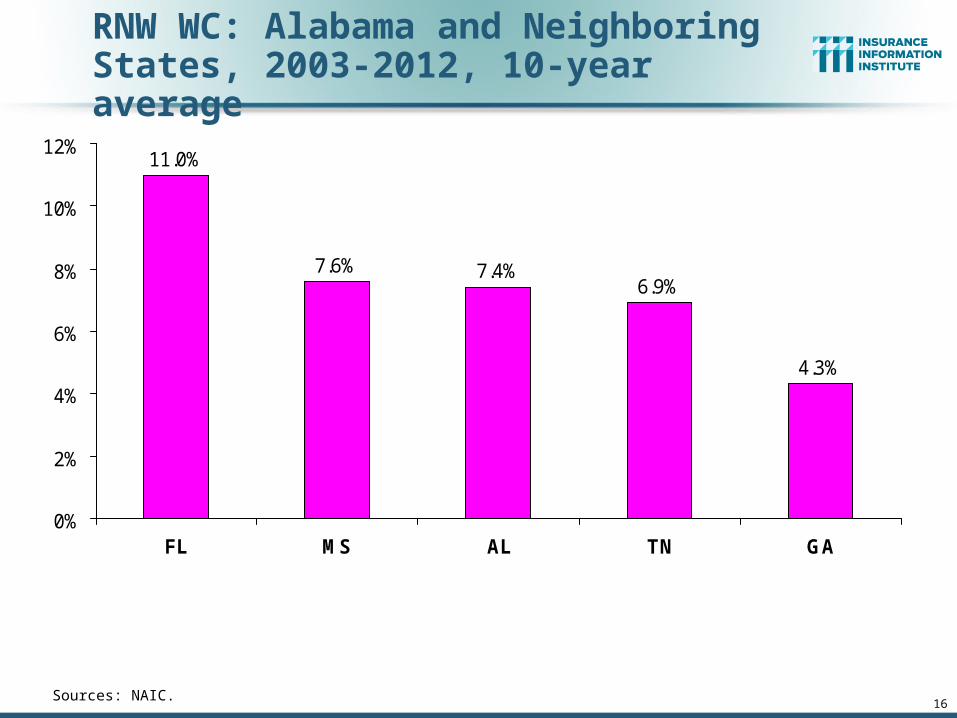

RNW WC: Alabama and NeighboringStates, 2003-2012, 10-year average

Sources: NAIC.

11.0%

7.6% 7.4%6.9%

4.3%

0%

2%

4%

6%

8%

10%

12%

FL MS AL TN GA

The Strength of the Economy Will Influence P/C Insurer

Growth Opportunities

17

Growth Will Expand Insurer Exposure Base Across Most Lines

17

18

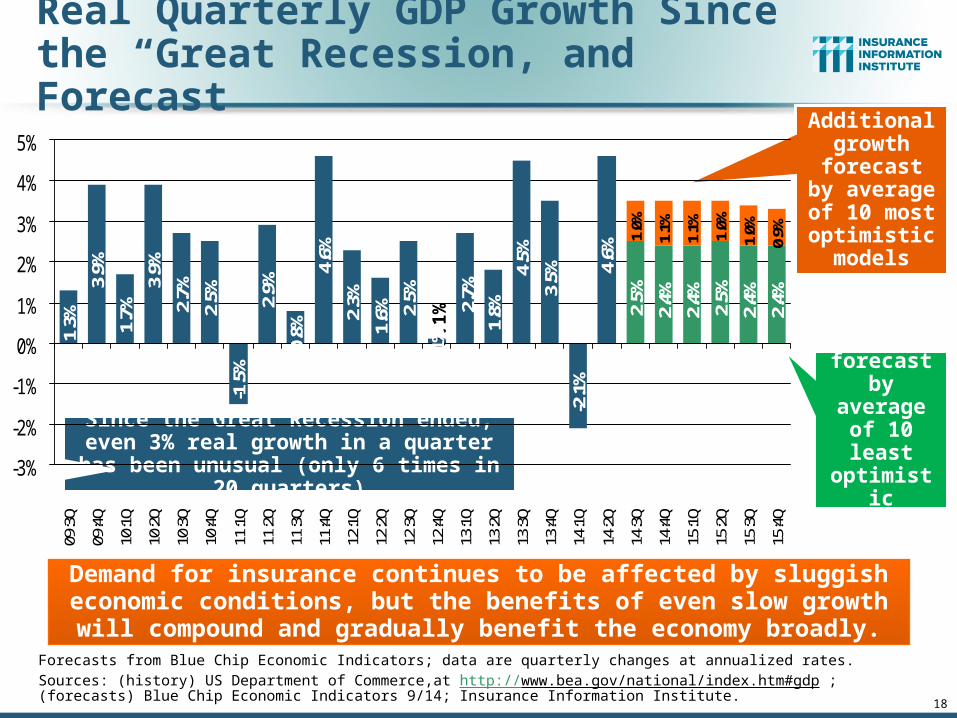

Real Quarterly GDP Growth Sincethe “Great Recession, and Forecast

Forecasts from Blue Chip Economic Indicators; data are quarterly changes at annualized rates.Sources: (history) US Department of Commerce,at http://www.bea.gov/national/index.htm#gdp ; (forecasts) Blue Chip Economic Indicators 9/14; Insurance Information Institute.

-1.5

%2.

9%0.

8%4.

6%2.

3%1.

6% 2.5%

0.1%

1.8%

4.5%

3.5%

-2.1

%4.

6%2.

5%2.

4%2.

4% 2.5%

2.4%

2.4%

1.0%

1.1%

1.1% 1.0%

1.0%

0.9%

2.7%

1.3%

3.9%

1.7%

3.9%

2.7%

2.5%

-3%

-2%

-1%

0%

1%

2%

3%

4%

5%

09:3

Q

09:4

Q

10:1

Q

10:2

Q

10:3

Q

10:4

Q

11:1

Q

11:2

Q

11:3

Q

11:4

Q

12:1

Q

12:2

Q

12:3

Q

12:4

Q

13:1

Q

13:2

Q

13:3

Q

13:4

Q

14:1

Q

14:2

Q

14:3

Q

14:4

Q

15:1

Q

15:2

Q

15:3

Q

15:4

Q

Demand for insurance continues to be affected by sluggish economic conditions, but the benefits of even slow growth will compound and

gradually benefit the economy broadly.

Additional growth

forecast by average of

10 most optimistic

models

Growth forecast by average of

10 least optimistic

models

Since the Great Recession ended, even 3% real growth in a quarter has been unusual

(only 6 times in 20 quarters)

0.1%

19

Real Quarterly GDP Growth by State, 2013

Data are seasonally-adjusted quarterly changes at annualized ratesSource: US Department of Commerce,at http://www.bea.gov/newsreleases/regional/gdp_state/2014/pdf/qgsp0814.pdf

5.7%

1.9%2.3%

0.1% 0.

8%

0.9%

3.3%

10.3

%

4.4%

2.0%

4.0%

0.7%

-3.0

%

3.7% 3.9%

2.3%

-0.4

%

4.2%

3.2%

-3%

0%

3%

6%

9%

12%

AL MS FL GA TN

Q1 Q2 Q3 Q4

Economic growth varied widely among Alabama and its neighbors in 2013. Not only were the rates of growth different from state to state,

but even the direction of growth differed.

70

16

8 21

23

22

10

22

17

10

61

22

22

11

83

16

4 19

63

60

22

62

43

96 11

08

81

60

15

01

61

22

52

03

21

41

97

28

01

41

20

31

99

20

11

492

02

16

42

37 2

74

84

14

42

22

20

33

04

22

9 26

72

43

18

02

48

0

50

100

150

200

250

300

350

400

Jan-1

1F

eb

-11

Mar-

11

Apr-

11

May-1

1Jun-1

1Jul-1

1A

ug

-11

Sep

-11

Oct-

11

Nov-1

1D

ec-1

1Jan-1

2F

eb

-12

Mar-

12

Apr-

12

May-1

2Jun-1

2Jul-1

2A

ug

-12

Sep

-12

Oct-

12

Nov-1

2D

ec-1

2Jan-1

3F

eb

-13

Mar-

13

Apr-

13

May 1

3Jun-1

3Jul-1

3A

ug

-13

Sep

-13

Oct-

13

Nov-1

3D

ec 1

3Jan-1

4F

eb

-14

Mar-

14

Apr-

14

May 1

4Jun-1

4Jul-1

4A

ug

-14

Sep

-14

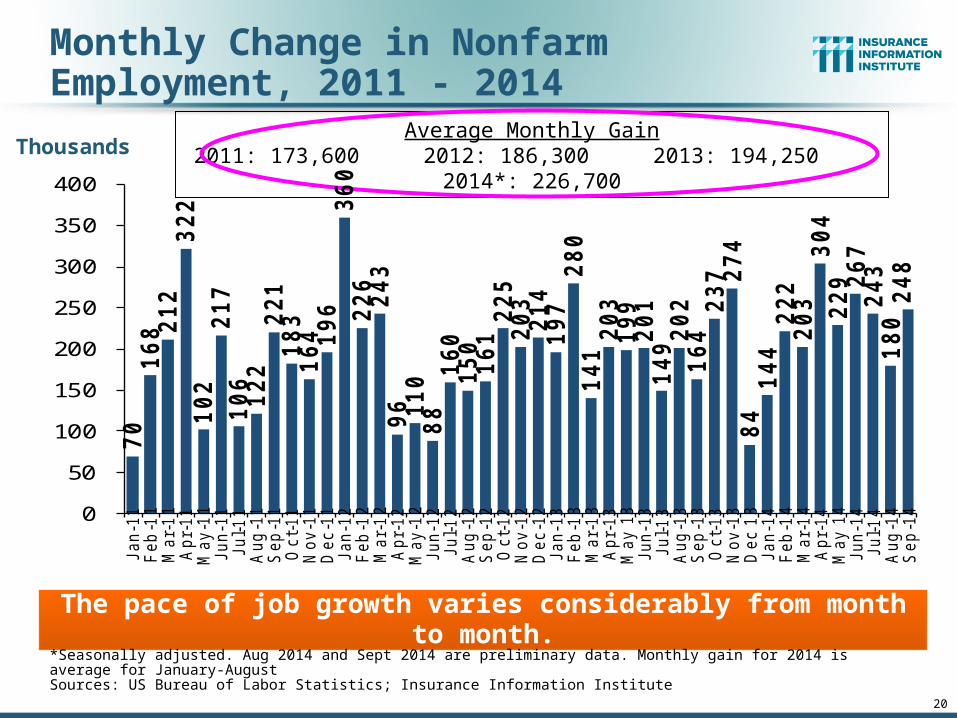

Monthly Change in Nonfarm Employment, 2011 - 2014

Thousands

The pace of job growth varies considerably from month to month.

*Seasonally adjusted. Aug 2014 and Sept 2014 are preliminary data. Monthly gain for 2014 is average for January-AugustSources: US Bureau of Labor Statistics; Insurance Information Institute

20

Average Monthly Gain2011: 173,600 2012: 186,300 2013: 194,250 2014*: 226,700

21

AL Change in Nonfarm Employment: Quarterly, 2009:Q3—2014:Q3*

-16.2

-3.4

0.2

13.2

-8.6

4.4

-4.6-2.9

10.78.4

2.1

6.5 5.3 5.2 5.2

-1.2

14.2

-4.4

0.71.6

-20

-15

-10

-5

0

5

10

15

20

09

:Q3

20

09

:Q4

20

10

:Q1

20

10

:Q2

20

10

:Q3

20

10

:Q4

20

11

:Q1

20

11

:Q2

20

11

:Q3

20

11

:Q4

20

12

:Q1

20

12

:Q2

20

12

:Q3

20

12

:Q4

20

13

:Q1

20

13

:Q2

20

13

:Q3

20

13

:Q4

20

14

:Q1

20

14

:Q2

(Thousands)

*seasonally-adjustedSource: US Bureau of Labor Statistics http://www.bls.gov/data/#employment; Insurance Information Institute

Nonfarm employment growth in Alabama since the end of the “Great Recession” is still very variable, quarter to quarter; still, there are now 36,000 more people working in Alabama than in June 2009.

Nonfarm Employment, Birmingham vs. Montgomery, Mobile, & Tuscaloosa: Quarterly, 2008:Q1—2014:Q2*

92

93

94

95

96

97

98

99

100

101

102

103

20

08

.1

20

08

.3

20

09

.1

20

09

.3

20

10

.1

20

10

.3

20

11

.1

20

11

.3

20

12

.1

20

12

.3

20

13

.1

20

13

.3

20

14

.1

Mobile Birmingham Montgomery Tuscaloosa

*seasonally adjusted. Sources: US Bureau of Labor Statistics, US Department of Labor; Insurance Information Institute.

Index 2008:Q1=100

Employment in Alabama’s major urban areas slumped sharply in the “Great Recession,” and all but Tuscaloosa are still down vs. 2008:Q1

Full-time vs. Part-time Employment,Quarterly, 2003-2014: WC Implications

110

113

116

119

122

2003

.120

03.2

2003

.320

03.4

2004

.120

04.2

2004

.320

04.4

2005

.120

05.2

2005

.320

05.4

2006

.120

06.2

2006

.320

06.4

2007

.120

07.2

2007

.320

07.4

2008

.120

08.2

2008

.320

08.4

2009

.120

09.2

2009

.320

09.4

2010

.120

10.2

2010

.320

10.4

2011

.120

11.2

2011

.320

11.4

2012

.120

12.2

2012

.320

12.4

2013

.120

13.2

2013

.320

13.4

2014

.120

14.2

Jul-1

4

24.0

24.5

25.0

25.5

26.0

26.5

27.0

27.5

28.0

28.5

Full-time Part-time

Data are seasonally-adjusted. Sources: US Bureau of Labor Statistics, US Department of Labor; Insurance Information Institute.

The Great Recession shifted employment from full-time to part-time, and the recovery to date hasn’t changed that. Full-time employment is still 3.2 million

below its pre-recession peak, but part-time recently reached a new peak.

Millions Millions

Recession

Recession shifted employment growth from

full-time to part-time

Pre-recession, most new jobs were full-time

24

Forces Affecting Personal Lines

25

Millions of Units

Private Housing Unit Starts, 1990-2015F

1.4

8

1.4

7 1.6

2

1.6

4

1.5

7

1.6

0 1.7

1 1.8

5 1.9

6 2.0

7

1.8

0

1.3

6

0.9

1

0.5

5

0.5

9

0.6

1 0.7

8 0.9

3

1.0

1 1.2

01.3

51.4

6

1.2

9

1.2

0

1.0

11.1

9

0.3

0.5

0.7

0.9

1.1

1.3

1.5

1.7

1.9

2.1

90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14F 15F

Sources: U.S. Department of Commerce; Blue Chip Economic Indicators (8/14); Insurance Information Institute.

Housing starts are rising, but this could be retarded by rising mortgage interest rates. Recently, the fastest growth is in multi-unit residences.

Personal lines exposure will grow, and commercial insurers with Workers Comp, Construction risk exposure, and Surety also benefit.

Housing unit starts plunged 72% from 2005-

2009, down 1.5 million, to lowest level since records

began in 1959

Still well below the levels reached in 1998-2002, before the bubble began

26

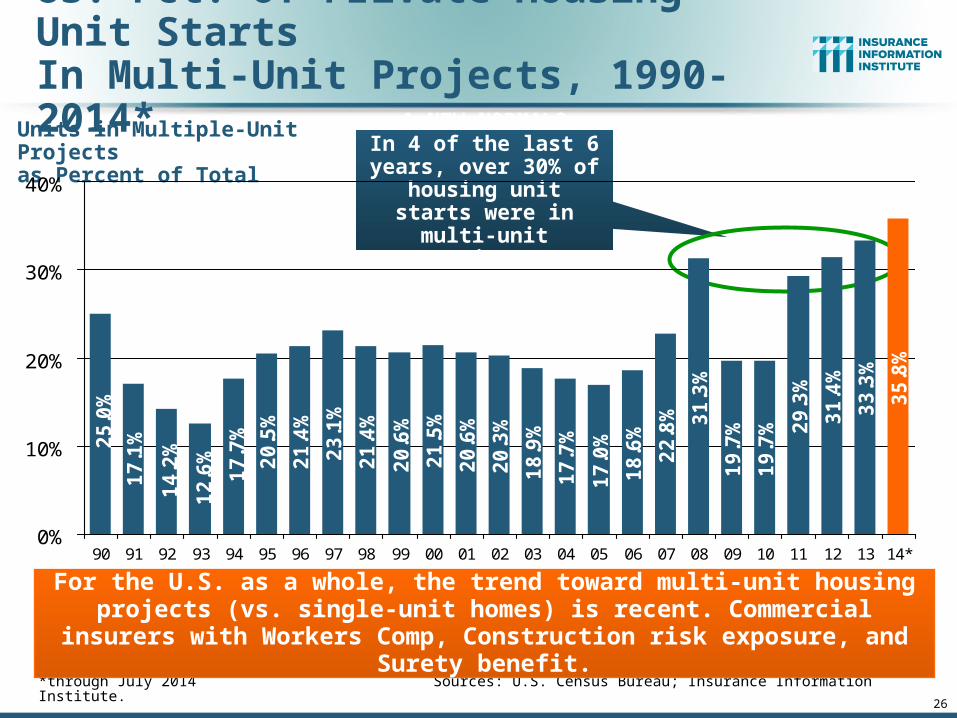

Units in Multiple-Unit Projectsas Percent of Total

US: Pct. Of Private Housing Unit StartsIn Multi-Unit Projects, 1990-2014*

21

.4%

23

.1%

21

.4%

20

.6%

21

.5%

20

.6%

20

.3%

18

.9%

17

.7%

17

.0%

18

.6%

22

.8% 31

.3%

19

.7%

19

.7% 2

9.3

%

31

.4%

33

.3%

35

.8%

20

.5%

17

.7%

12

.6%

14

.2%

17

.1%25

.0%

0%

10%

20%

30%

40%

90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14*

*through July 2014 Sources: U.S. Census Bureau; Insurance Information Institute.

For the U.S. as a whole, the trend toward multi-unit housing projects (vs. single-unit homes) is recent. Commercial insurers with Workers Comp,

Construction risk exposure, and Surety benefit.

A NEW NORMAL?In 4 of the last 6 years, over 30% of housing

unit starts were in multi-unit projects

27

Rental Vacancy Rates, Quarterly, 1990-2014

6.5

7.0

7.5

8.0

8.5

9.0

9.5

10.0

10.5

11.0

11.59

0:Q

1

91

:Q1

92

:Q1

93

:Q1

94

:Q1

95

:Q1

96

:Q1

97

:Q1

98

:Q1

99

:Q1

00

:Q1

01

:Q1

02

:Q1

03

:Q1

04

:Q1

05

:Q1

06

:Q1

07

:Q1

08

:Q1

09

:Q1

10

:Q1

11

:Q1

12

:Q1

13

:Q1

14

:Q1

Sources: US Census Bureau, Residential Vacancies & Home Ownership in the Second Quarter of 2014 (released July 29, 2014) and earlier issues; Insurance Information Institute. Next Census Bureau report to be released on October 28, 2014.

Peak vacancy rate 11.1% in

2009:Q3

Before the 2001 recession, rental vacancy rates were 8% or less.We’re close to those levels again. => More multi-unit construction?

27

Percent vacant

Latest vacancy rate was 7.5%

in 2014:Q2

Vacancy rate 10.4% in 2004:Q1

28

16.9

16.5

16.1

13.2

10.4

11.6

12.7

14.4

15.5 16

.3 16.7

16.9

16.617

.117.5

17.8

17.4

9

10

11

12

13

14

15

16

17

18

19

99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14F 15F

(Millions of Units)

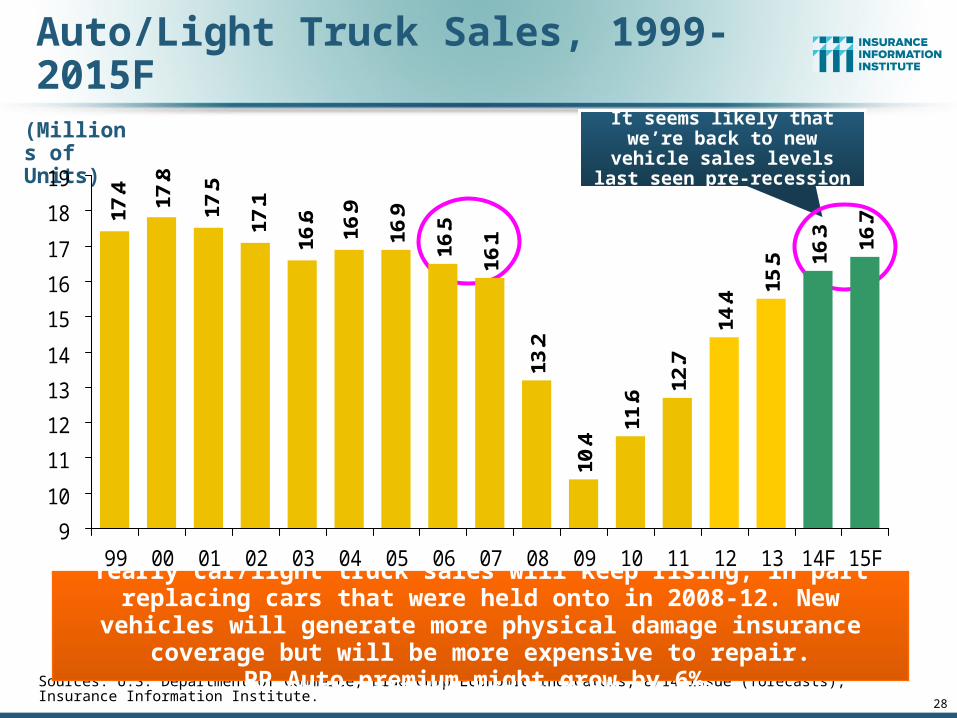

Auto/Light Truck Sales, 1999-2015F

Sources: U.S. Department of Commerce; Blue Chip Economic Indicators, 8/14 issue (forecasts); Insurance Information Institute.

Yearly car/light truck sales will keep rising, in part replacing cars that were held onto in 2008-12. New vehicles will generate more physical

damage insurance coverage but will be more expensive to repair.PP Auto premium might grow by 6%.

It seems likely that we’re back to new vehicle sales

levels last seen pre-recession

29

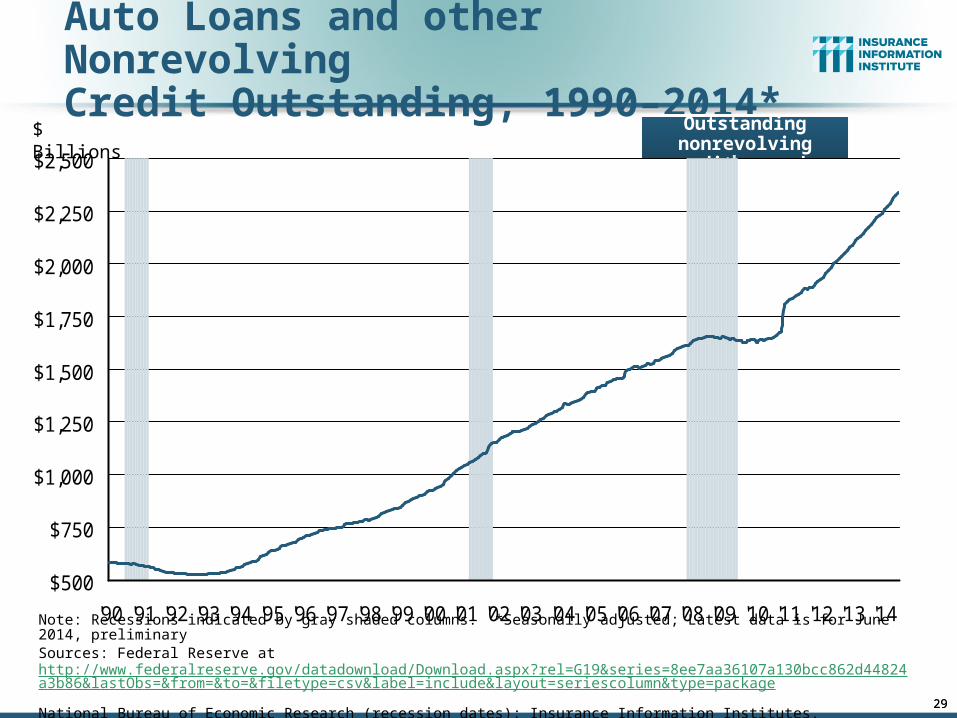

Auto Loans and other NonrevolvingCredit Outstanding, 1990–2014*

Note: Recessions indicated by gray shaded columns. *Seasonally adjusted; Latest data is for June 2014, preliminarySources: Federal Reserve at http://www.federalreserve.gov/datadownload/Download.aspx?rel=G19&series=8ee7aa36107a130bcc862d44824a3b86&lastObs=&from=&to=&filetype=csv&label=include&layout=seriescolumn&type=package National Bureau of Economic Research (recession dates); Insurance Information Institutes.

$500

$750

$1,000

$1,250

$1,500

$1,750

$2,000

$2,250

$2,500

'90 '91 '92 '93 '94 '95 '96 '97 '98 '99 '00 '01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11 '12 '13 '14

No growth in outstanding nonrevolving credit for

three years

29

$ Billions

Spurt began in Dec. 2010

Outstanding nonrevolving credit

grew by 7.8% in 2013

30

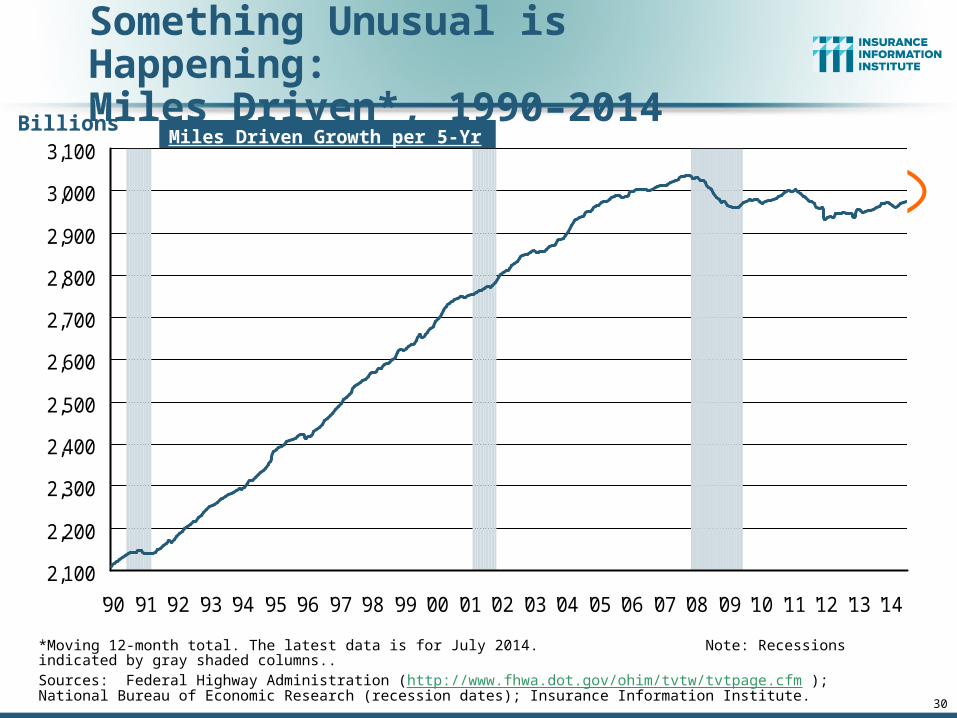

Something Unusual is Happening:Miles Driven*, 1990–2014

*Moving 12-month total. The latest data is for July 2014. Note: Recessions indicated by gray shaded columns..Sources: Federal Highway Administration (http://www.fhwa.dot.gov/ohim/tvtw/tvtpage.cfm ); National Bureau of Economic Research (recession dates); Insurance Information Institute.

Billions

2,100

2,200

2,300

2,400

2,500

2,600

2,700

2,800

2,900

3,000

3,100

'90 '91 '92 '93 '94 '95 '96 '97 '98 '99 '00 '01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11 '12 '13 '14

A record: miles driven has been below the prior peak for 80

straight months (through June 2014). Previous record was in the early 1980s (39 months)

Miles Driven Growth per 5-Yr Span1997 vs. 1992: 13.9%2002 vs. 1997: 11.5%2007 vs. 2002: 6.1%2012 vs. 2007: -3.0%

Some of the growth in miles driven is due to population growth: 1997 vs. 1992: +5.1%2002 vs. 1997: +7.4%2007 vs. 2002: +4.7%2012 vs. 2007: +3.4%

31

Forces Affecting Commercial Lines

32

Index of Total Industrial Production:*A New Peak in July 2014

*Monthly, seasonally adjusted, through July 2014 (which is preliminary). Index based on year 2007 = 100Sources: Federal Reserve Board at http://www.federalreserve.gov/releases/g17/ipdisk/ip_sa.txt . National Bureau of Economic Research (recession dates); Insurance Information Institute.

55

65

75

85

95

105

1/31

/19

90

1/31

/19

91

1/31

/19

92

1/31

/19

93

1/31

/19

94

1/31

/19

95

1/31

/19

96

1/31

/19

97

1/31

/19

98

1/31

/19

99

1/31

/20

00

1/31

/20

01

1/31

/20

02

1/31

/20

03

1/31

/20

04

1/31

/20

05

1/31

/20

06

1/31

/20

07

1/31

/20

08

1/31

/20

09

1/31

/20

10

1/31

/20

11

1/30

/20

12

1/31

/20

13

1/31

/20

14

Recession

Peak at 100.82 in December 2007 (officially the 1st

month of the Great Recession)

Insurance exposures for industrial production will continue growing in 2014, and commercial insurance premium volume with them.

32

July 2014 Index at 103.9,

a new peak

Many economists expect business

investment to rise in 2014, 2015,

and 2016

33

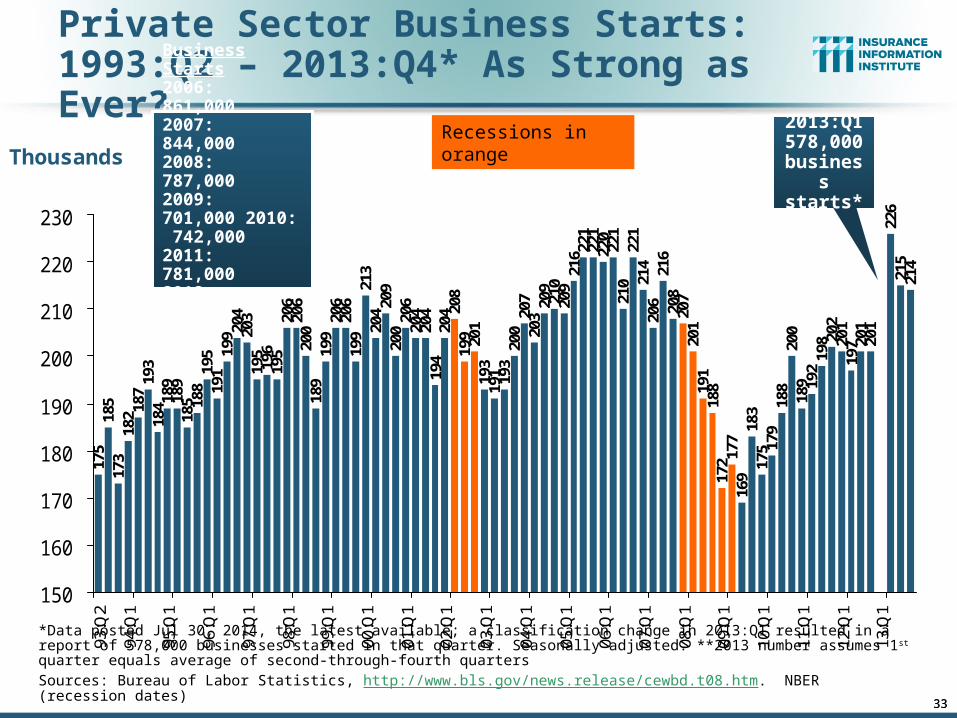

Private Sector Business Starts:1993:Q2 – 2013:Q4* As Strong as Ever?

175

185

173

182 18

719

318

4 189

189

185 18

819

519

119

9 204

203

195

196

195

206

206

200

189

199

206

206

199

213

204 20

920

020

620

420

419

420

4 208

199

193

191 19

320

020

720

320

921

020

921

6 221

221

220

221

210

221

214

206

216

208

207

201

191

188

172 17

716

918

317

5 179

188

200

189 19

219

8 202

201

197 20

120

122

621

521

4

201

150

160

170

180

190

200

210

220

230

93:Q

2

94:Q

1

95:Q

1

96:Q

1

97:Q

1

98:Q

1

99:Q

1

00:Q

1

01:Q

1

02:Q

1

03:Q

1

04:Q

1

05:Q

1

06:Q

1

07:Q

1

08:Q

1

09:Q

1

10:Q

1

11:Q

1

12:Q

1

13:Q

1

*Data posted Jul 30, 2014, the latest available; a classification change in 2013:Q1 resulted in a report of 578,000 businesses started in that quarter. Seasonally adjusted. **2013 number assumes 1st quarter equals average of second-through-fourth quartersSources: Bureau of Labor Statistics, http://www.bls.gov/news.release/cewbd.t08.htm. NBER (recession dates)

Thousands

Business Starts2006: 861,0002007: 844,0002008: 787,0002009: 701,000 2010: 742,000 2011: 781,0002012: 800,0002013: 870,000**

33

Recessions in orange 2013:Q1 578,000

business starts*

34

$200,000

$300,000

$400,000

$500,000

Dollar Value* of Manufacturers’ Shipments Monthly, January 1992—June 2014

*seasonally adjusted; June 2014 is preliminary; data published July 25, 2014.Source: U.S. Census Bureau, Full Report on Manufacturers’ Shipments, Inventories, and Orders, http://www.census.gov/manufacturing/m3/

Monthly shipments in November 2013 exceeded the pre-crisis (July 2008) peak; December 2013, January 2014, and February 2014 slipped a bit.

March 2014, then April, then May, then June 2014 (prelim.) set new record highs.

$ Millions

34

The value of Manufacturing Shipments in June 2014 was $499.8B—a new record high.

35

Nonfarm Payroll (Wages and Salaries):Quarterly, 2005–2014:Q2

Note: Recession indicated by gray shaded column. Data are seasonally adjusted annual rates.Sources: http://research.stlouisfed.org/fred2/series/WASCUR; National Bureau of Economic Research (recession dates); Insurance Information Institute.

Billions

$5,500

$5,750

$6,000

$6,250

$6,500

$6,750

$7,000

$7,250

$7,500

$7,75005

:Q1

05:Q

205

:Q3

05:Q

406

:Q1

06:Q

206

:Q3

06:Q

407

:Q1

07:Q

207

:Q3

07:Q

408

:Q1

08:Q

208

:Q3

08:Q

409

:Q1

09:Q

209

:Q3

09:Q

410

:Q1

10:Q

210

:Q3

10:Q

411

:Q1

11:Q

211

:Q3

11:Q

412

:Q1

12:Q

212

:Q3

12:Q

413

:Q1

13:Q

213

:Q3

13:Q

414

:Q1

14:Q

2

Prior Peak was 2008:Q3 at $6.54 trillion

Latest (2014:Q2) was $7.46 trillion, a

new peak--$1T above 2009 trough

Recent trough (2009:Q1) was $6.23 trillion, down

5.3% from prior peak

35

36

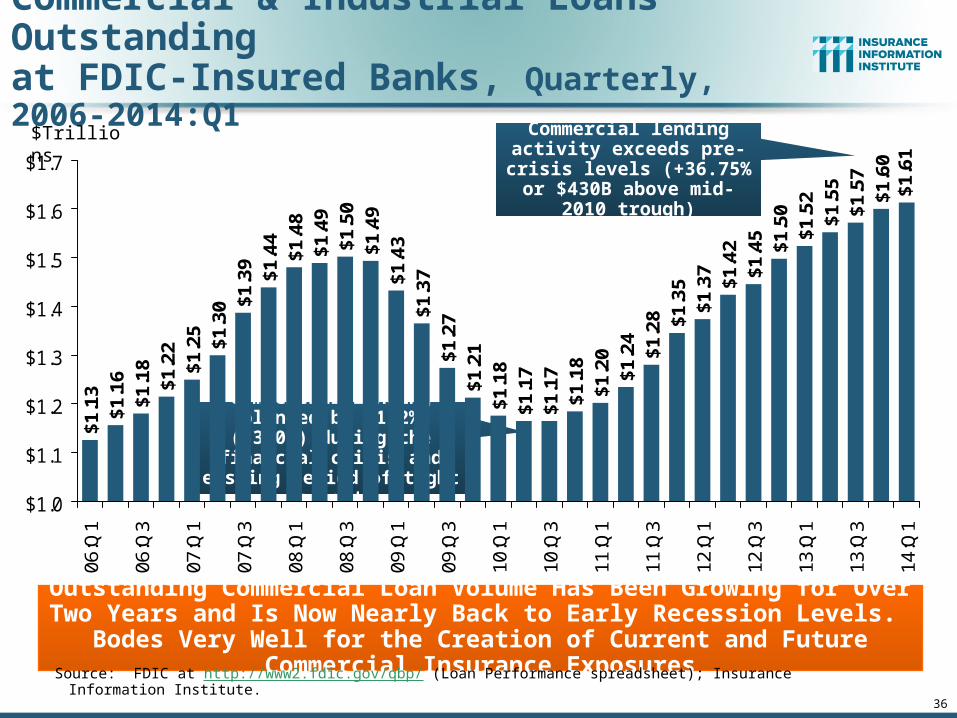

Commercial & Industrial Loans Outstandingat FDIC-Insured Banks, Quarterly, 2006-2014:Q1

$1.1

6$1

.18

$1.2

2

$1.4

4$1

.48

$1.4

9$1

.50

$1.4

9$1

.43

$1.3

7$1

.27

$1.2

1$1

.18

$1.1

7$1

.17

$1.1

8$1

.20

$1.2

4$1

.28 $1

.35

$1.3

7$1

.42

$1.4

5$1

.50

$1.5

2$1

.55

$1.5

7$1

.60

$1.6

1

$1.1

3

$1.2

5$1

.30 $1

.39

$1.0

$1.1

$1.2

$1.3

$1.4

$1.5

$1.6

$1.7

06:Q

1

06:Q

3

07:Q

1

07:Q

3

08:Q

1

08:Q

3

09:Q

1

09:Q

3

10:Q

1

10:Q

3

11:Q

1

11:Q

3

12:Q

1

12:Q

3

13:Q

1

13:Q

3

14:Q

1

Outstanding Commercial Loan Volume Has Been Growing for Over Two Years and Is Now Nearly Back to Early Recession Levels. Bodes Very Well for the Creation of Current and Future Commercial Insurance Exposures

Source: FDIC at http://www2.fdic.gov/qbp/ (Loan Performance spreadsheet); Insurance Information Institute.

$Trillions

Commercial lending plunged by 21.2% ($330B) during the financial crisis and ensuing

period of tight credit

Commercial lending activity exceeds pre-crisis levels (+36.75% or $430B above

mid-2010 trough)

37

Percent of Non-current Commercial & Industrial Loans Outstanding at FDIC-Insured Banks,Quarterly, 2006-2014:Q1

0.70

%0.

74%

0.64

%

0.67

%0.

81%

1.07

%1.

18% 1.

69% 2.

25% 2.

80%

3.57

%3.

43%

3.05

%2.

83%

2.73

%2.

44%

1.89

%1.

65%

1.49

%1.

29%

1.17

%1.

09%

0.98

%0.

88%

0.80

%0.

74%

0.72

%0.

62%

0.60

%

0.71

%

0.63

%0.

62%

0.63

%

0%

1%

2%

3%

4%

06:Q

106

:Q2

06:Q

306

:Q4

07:Q

107

:Q2

07:Q

307

:Q4

08:Q

108

;Q2

08:Q

308

:Q4

09:Q

109

:Q2

09:Q

309

:Q4

10:Q

110

:Q2

10:Q

310

:Q4

11:Q

111

:Q2

11:Q

311

:Q4

12:Q

112

:Q2

12:Q

312

:Q4

13:Q

113

:Q2

13:Q

313

:Q4

14:Q

1

Non-current loans (those past due 90 days or more or in nonaccrual status) are below even pre-recession levels, fueling bank willingness to lend.

Source: FDIC at http://www2.fdic.gov/qbp/ (Loan Performance spreadsheet); Insurance Information Institute.

Back to “normal” levels of noncurrent industrial

& commercial loans

Recession

Tornados andOther Natural Catastrophes

38

2013 Was a Welcome Respite from the High Catastrophe Losses in Recent Years

2014 Winter Storm Losses Manageable

38

Nu

mb

er

Geophysical (earthquake, tsunami, volcanic activity)

Climatological (temperature extremes, drought, wildfire)

Meteorological (storm)

Hydrological (flood, mass movement)

Natural Disasters in the United States Number of Events (Annual Totals 1980 – 2013)

Source: MR NatCatSERVICE 39

22

19

81

6

50

100

150

200

250

1980 1982 1984 1986 1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012

2013 was the first year since 2005 with fewer

than 150 natural disaster events (it had 128)

40

$1

2.8

$1

1.1

$3

.8

$1

4.5

$1

1.7

$6

.2

$3

5.2

$7

.7 $1

6.5

$3

4.2

$7

4.5

$1

0.7

$7

.6

$2

9.6

$1

1.6

$1

4.6

$3

4.1

$3

5.5

$1

2.9

$9

.1$1

4.2

$4

.9

$8

.1

$3

8.3

$8

.9

$2

6.8

$0

$10

$20

$30

$40

$50

$60

$70

$80

$90

89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14*

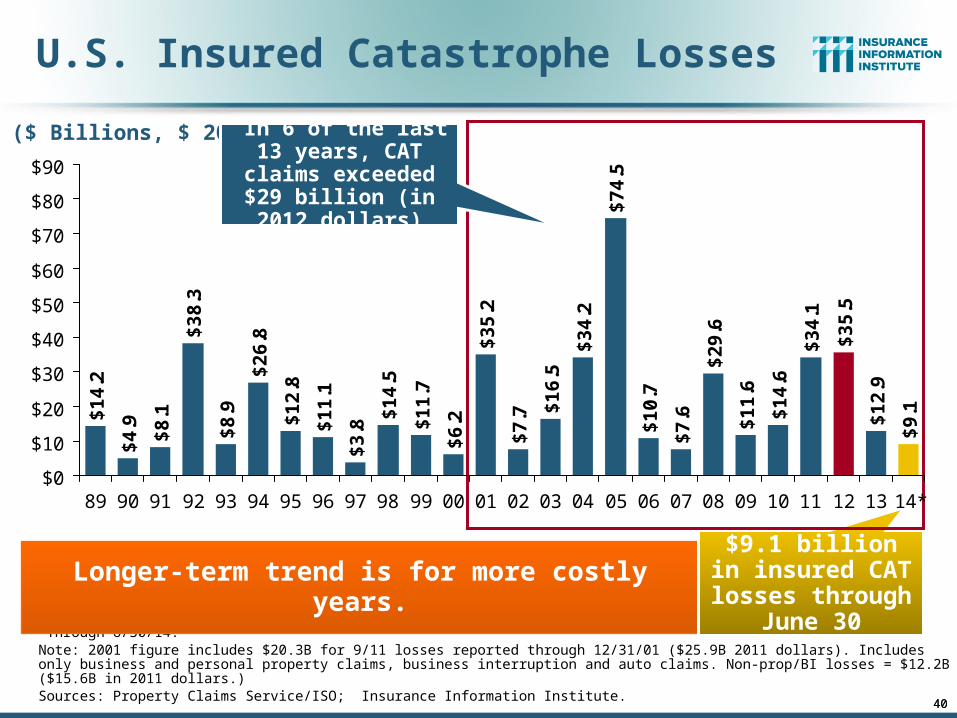

U.S. Insured Catastrophe Losses

*Through 6/30/14.Note: 2001 figure includes $20.3B for 9/11 losses reported through 12/31/01 ($25.9B 2011 dollars). Includes only business and personal property claims, business interruption and auto claims. Non-prop/BI losses = $12.2B ($15.6B in 2011 dollars.) Sources: Property Claims Service/ISO; Insurance Information Institute.

Longer-term trend is for more costly years.

$9.1 billion in insured CAT

losses through June 30

($ Billions, $ 2013)

40

In 6 of the last 13 years, CAT claims

exceeded $29 billion (in 2012 dollars)

41

Combined Ratio Points Associated with Catastrophe Losses: 1960 – 2013*

*2010s represent 2010-2013.Notes: Private carrier losses only. Excludes loss adjustment expenses and reinsurance reinstatement premiums. Figures are adjusted for losses ultimately paid by foreign insurers and reinsurers.Source: ISO (1960-2011); A.M. Best (2012E) Insurance Information Institute.

0.4

1.2

0.4 0.

8 1.3

0.3

0.4 0.

71.

51.

00.

40.

4 0.7

1.8

1.1

0.6

1.4 2.

01.

3 2.0

0.5

0.5 0.7

3.0

1.2

2.1

8.8

2.3

5.9

3.3

2.8

1.0

3.6

2.9

1.6

5.4

1.6

3.3

3.3

8.1

2.7

1.6

5.0

2.6

3.4

8.7 8.9

3.43.6

0.9

0.1

1.1

1.1

0.8

0

1

2

3

4

5

6

7

8

9

10

1960

1962

1964

1966

1968

1970

1972

1974

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

The catastrophe loss component of private insurer losseshas increased sharply in the last 20 years.

Avg. CAT Loss Component of the Combined Ratio

by Decade

1960s: 1.04 1970s: 0.85 1980s: 1.31 1990s: 3.39 2000s: 3.52 2010s: 6.1E*

Combined Ratio Points

Catastrophe losses as a share of all losses reached

a record high in 2012

44

12 States with Most Growth in Total Value of Insured Coastal Exposure, 2012 vs. 2007$ Billions

Source: AIR Worldwide; I.I.I.

$76.8$78.4$87.9

$280.2

$403.7

$544.4

$69.1$47.7 $35.7 $30.7 $23.5 $21.3

$0

$100

$200

$300

$400

$500

$600

Delawar

e

Virgini

a

North

Caroli

na

Alaba

ma

South

Car

olina

Louis

iana

Mas

sach

uset

ts

New J

erse

y

Conne

cticu

t

Texas

Florid

a

New Y

ork

The insured value of all coastal property was $10.6 trillion in 2012,up 20% from $8.9 trillion in 2007, and up 48% from $7.2 trillion in 2004

Texas added $280 billion after

Hurricanes Gustav and Ike in 2008 Alabama added

$36 billion in insured value after Hurricanes Katrina

and Rita

U.S. Tornado Count, EF-1 and Stronger,(through May each year), 1953-2014

45Source: http://www.spc.noaa.gov/wcm/

2014 count was 152, lowest since 2005

Tornado occurrence is very variable

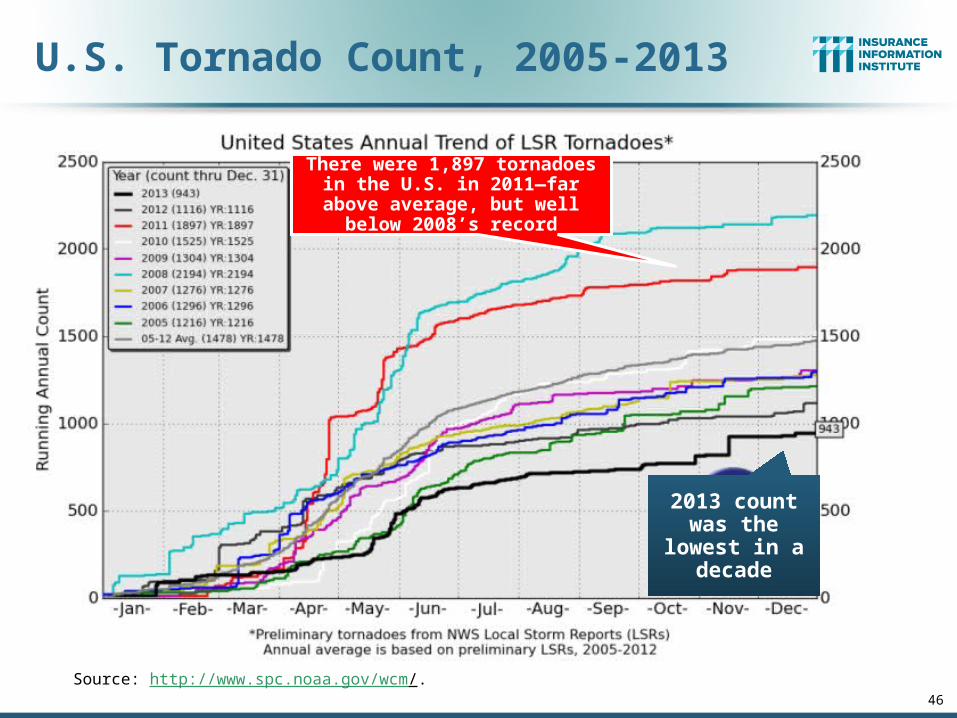

U.S. Tornado Count, 2005-2013

46

Source: http://www.spc.noaa.gov/wcm/.

There were 1,897 tornadoes in the U.S. in 2011—far above average,

but well below 2008’s record

2013 count was the lowest

in a decade

Reports of Severe Weather* in ALthrough Sept 2, 2014

47

*excluding floods, wildfires, droughtsSource: NOAA Storm Prediction Center; http://www.spc.noaa.gov/climo/online/monthly/2014_annual_summary.html#

Almost all of the tornados

are in the northern half of the state

Investment Performance: a Key Driver of Profitability

48

Depressed Yields Influence Underwriting & Pricing

48

49

Net Yield on Insurer Invested Assets, 2007-2014:1H

Sources: NAIC, via SNL Financial; I.I.I.

2007 2008 2009 2010 2011 2012 20130.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0% 5.75%5.41%

5.14% 5.24% 5.10% 4.93% 4.87%4.49%

4.20%3.93%

3.73% 3.83% 3.68%3.43%

P/C Insurer net yields to date dropped by 106 basis pointssince year-end 2007.

50

U.S. Treasury 2- and 10-Year Note Yields*: 1990–2014

*Monthly, constant maturity, nominal rates, through August 2014.Sources: Federal Reserve Bank at http://www.federalreserve.gov/releases/h15/data.htm. National Bureau of Economic Research (recession dates); Insurance Information Institutes.

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

1/31

/19

90

1/31

/19

91

1/31

/19

92

1/31

/19

93

1/31

/19

94

1/31

/19

95

1/31

/19

96

1/31

/19

97

1/31

/19

98

1/31

/19

99

1/31

/20

00

1/31

/20

01

1/31

/20

02

1/31

/20

03

1/31

/20

04

1/31

/20

05

1/31

/20

06

1/31

/20

07

1/31

/20

08

1/31

/20

09

1/31

/20

10

1/31

/20

11

1/30

/20

12

1/31

/20

13

1/31

/20

14

Recession2-Yr Yield10-Yr Yield

Yields on 10-Year U.S. Treasury Notes have been essentially below 5% for a full decade.

Since roughly 80% of P/C bond/cash investments are in 10-year or shorter durations, most P/C insurer portfolios will have low-yielding bonds for years to come.

U.S. Treasury 10-year note

yields recently “spiked” up

50

Bonds Rated NAIC Quality Category 3-6 as a Percent of Total Bonds, 2003–2013

2.69%

2.10% 2.17%1.98%

3.07% 3.10%

4.07% 3.99%

2.04%2.27%

2.58%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

There are many ways to capture higher yields on bond portfolios.One is to accept greater risk, as measured by NAIC bond ratings.

The ratings range from 1 to 6, with the highest quality rated 1.Even in 2012-13, over 95% of the industry’s bonds were rated 1 or 2.

Sources: SNL Financial; Insurance Information Institute.

From 2006-07 to year-end 2012, the percentage of lower-quality bonds in P/C industry portfolios doubled

Property/Casualty Insurance Industry Investment Gain: 1994–2014:Q11

$35.4

$42.8$47.2

$52.3

$44.4

$36.0

$45.3$48.9

$59.4$55.7

$64.0

$31.7

$39.2

$53.4$56.2$54.2

$58.8

$14.1

$58.0

$51.9$56.9

$0

$10

$20

$30

$40

$50

$60

$70

94 95 96 97 98 99 00 01 02 03 04 05* 06 07 08 09 10 11 12 1314:Q1

Low interest rates in 2013 caused investment income to keep fallingbut realized investment gains were up sharply.

The financial crisis caused investment gains to fall by 50% in 2008.1 Investment gains consist primarily of interest, stock dividends and realized capital gains and losses.* 2005 figure includes special one-time dividend of $3.2B; Sources: ISO; Insurance Information Institute.

$ Billions

Investment gains in 2013 were the highest in the post-crisis era

www.iii.org

Thank you for your timeand your attention!

Insurance Information Institute Online:

53