Overview on the EU Common Agricultural Policy - Page 1May 2008 Seminar „Marketing of Fresh Fruits...

18

May 2008 Overview on the EU Common Agricultural Policy - Page 1 Seminar „Marketing of Fresh Fruits and Vegetables“ SS 2008 Overview on the EU Common Agricultural Policy Presented by Milana Ruffin

-

date post

20-Dec-2015 -

Category

Documents

-

view

213 -

download

0

Transcript of Overview on the EU Common Agricultural Policy - Page 1May 2008 Seminar „Marketing of Fresh Fruits...

May 2008Overview on the EU Common Agricultural Policy - Page 1

Seminar „Marketing of Fresh Fruits and Vegetables“ SS 2008

Overview on the EU Common Agricultural Policy

Presented by

Milana Ruffin

May 2008Overview on the EU Common Agricultural Policy - Page 2

1. Introduction

2. The 2003 CAP Reform:Mechanisms in the grand cultures and FFV sector

3. Comparing sectoral market distortions

4. Conclusion

CONTENTS

May 2008Overview on the EU Common Agricultural Policy - Page 3

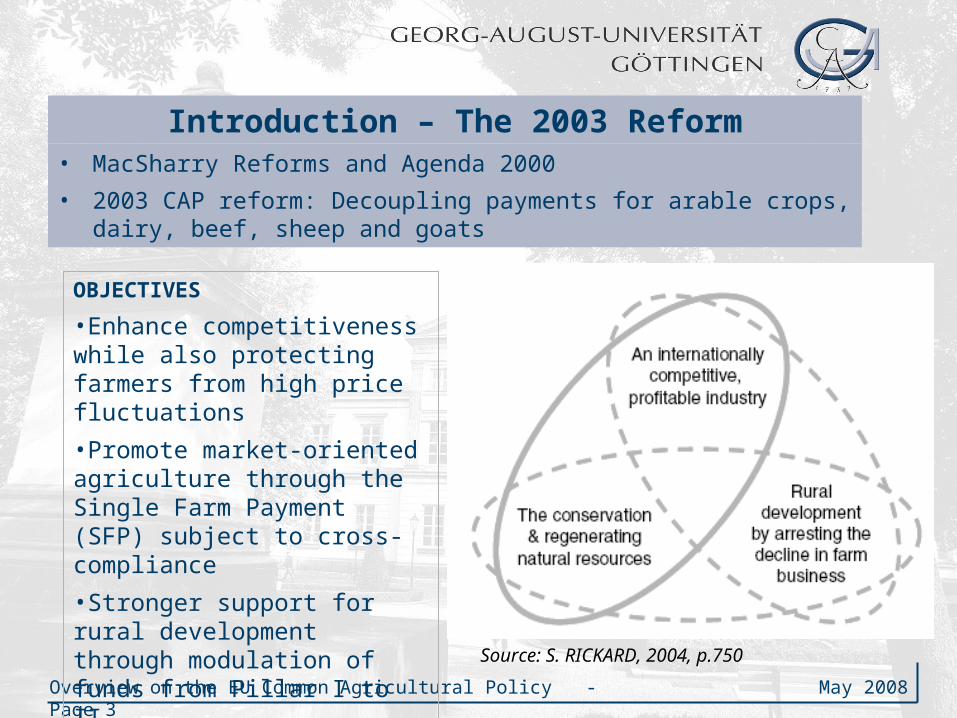

Introduction – The 2003 Reform• MacSharry Reforms and Agenda 2000

• 2003 CAP reform: Decoupling payments for arable crops, dairy, beef, sheep and goats

Source: S. RICKARD, 2004, p.750

OBJECTIVES

•Enhance competitiveness while also protecting farmers from high price fluctuations

•Promote market-oriented agriculture through the Single Farm Payment (SFP) subject to cross-compliance

•Stronger support for rural development through modulation of funds from Pillar I to II

An irreconcilable trinity?

May 2008Overview on the EU Common Agricultural Policy - Page 4

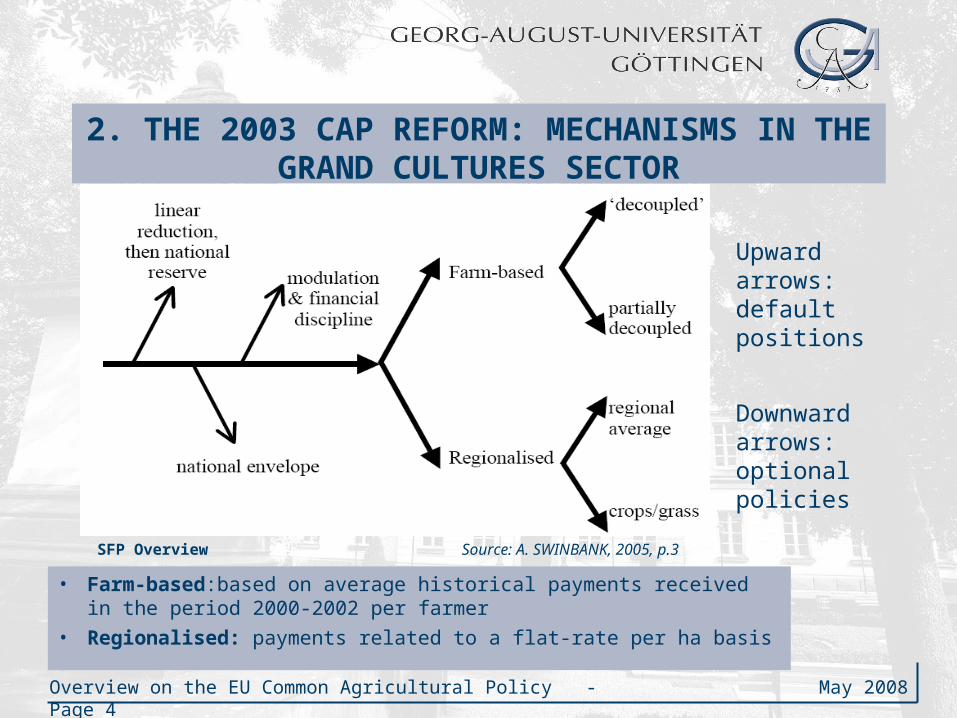

2. THE 2003 CAP REFORM: MECHANISMS IN THE GRAND CULTURES SECTOR

• Farm-based:based on average historical payments received in the period 2000-2002 per farmer

• Regionalised: payments related to a flat-rate per ha basis

SFP Overview Source: A. SWINBANK, 2005, p.3

Upward arrows: default positions

Downward arrows: optional policies

May 2008Overview on the EU Common Agricultural Policy - Page 5

Mechanisms in the grand cultures sector

• National Reserve: obligatory fund through a linear percentage reduction (up to 3%)

• Modulation: obligatory 5% since 2007; with a franchise of 5,000 Euro

• National Envelope: optional path refers to redirecting 10% of direct payments for environmental projects or for improving the quality and marketing of agricultural products

• New member countries: apply for the Single Area Payment System based on a national flat rate

May 2008Overview on the EU Common Agricultural Policy - Page 6

Support product Max. rate of coupled

support (%)

Cereals and oilseeds 25

Durum wheat 40

Rice 42

Specific Commodity Support:

• Cereals: Unchanged intervention prices at 101.31 Euro p.t., monthly increments payments for storage halved from 1 to 0.5 Euro p.t. Exception is rye: intervention abolished

Mechanisms in the grand cultures sector

Maximum rates of coupled support, selected products, Source: GAIN report E34044, 2004, p.8

May 2008Overview on the EU Common Agricultural Policy - Page 7

Mechanisms in the FFV sector

Producer Organisations (POs):

• EU subsidies paid not to individual farmers but to the POs

• Financed by an operational fund paid for by the EU, limited to 50% of PO expenditures or 4,1% of the value of marketed production

• Degree to which individual member states are organised varies greatly, between 5% to 70%

• The Fischler Reform did not reform the FFV sector

• FFV productions not eligible to claim SFPs in the historical model, unlike in regional model

May 2008Overview on the EU Common Agricultural Policy - Page 8

Mechanisms in the FFV sector

Operational Funds:• Operational funds used for operational programmes approved by EU

member states

• Typical operational programs: packing equipment purchases, irrigation and greenhouse facilities investments, subsidies to growers for replanting fruit trees

• Operational funds as crisis management mechanism for product withdrawals

• 16 produces are eligible for Community Withdrawal Compensation (CWC)

• Since 2002, the EU pays the POs a CWC compensation p.t. of product withdrawn within the ceilings of 5% for citrus, 8,5% for apples and pears, or 10% for other products of the marketed quantity

May 2008Overview on the EU Common Agricultural Policy - Page 9

3. Sectoral market distortions – domestic support

Grand Cultures Sector

• Measurement: OECD’s Producer Support Estimate

A) Support to farmers by maintaining domestic prices for farm goods at levels higher than border prices (market price support)

B) Providing payments to farmers (budgetary payments)

Market price support responsible for the largest share of the EU‘s Aggregated Measure of Support (AMS)

May 2008Overview on the EU Common Agricultural Policy - Page 10

Sectoral market distortions – domestic support

LEVEL

% CHANGE

2002 base year

Max. decoupling

Euro m

Min. decoupling

Euro m

Max. decoupling

Min. decoupling

Wheat 199 153 155 -24 -22

Coarse grains

290 295 297 2 2

Beef 12665 13116 12778 4 1

Changes in market price support by commodity 2002-08

Source: OECD secretariat calculations, OECD PSE database, 2004

May 2008Overview on the EU Common Agricultural Policy - Page 11

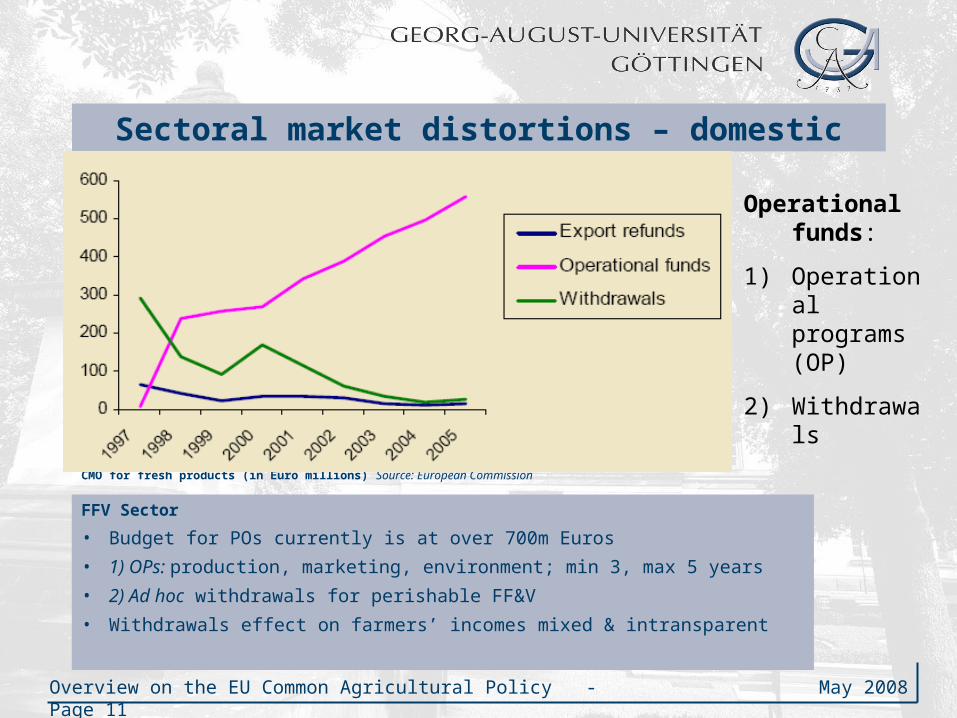

Sectoral market distortions – domestic support

CMO for fresh products (in Euro millions) Source: European Commission

FFV Sector

• Budget for POs currently is at over 700m Euros

• 1) OPs: production, marketing, environment; min 3, max 5 years

• 2) Ad hoc withdrawals for perishable FF&V

• Withdrawals effect on farmers’ incomes mixed & intransparent

Operational funds:

1) Operational programs (OP)

2) Withdrawals

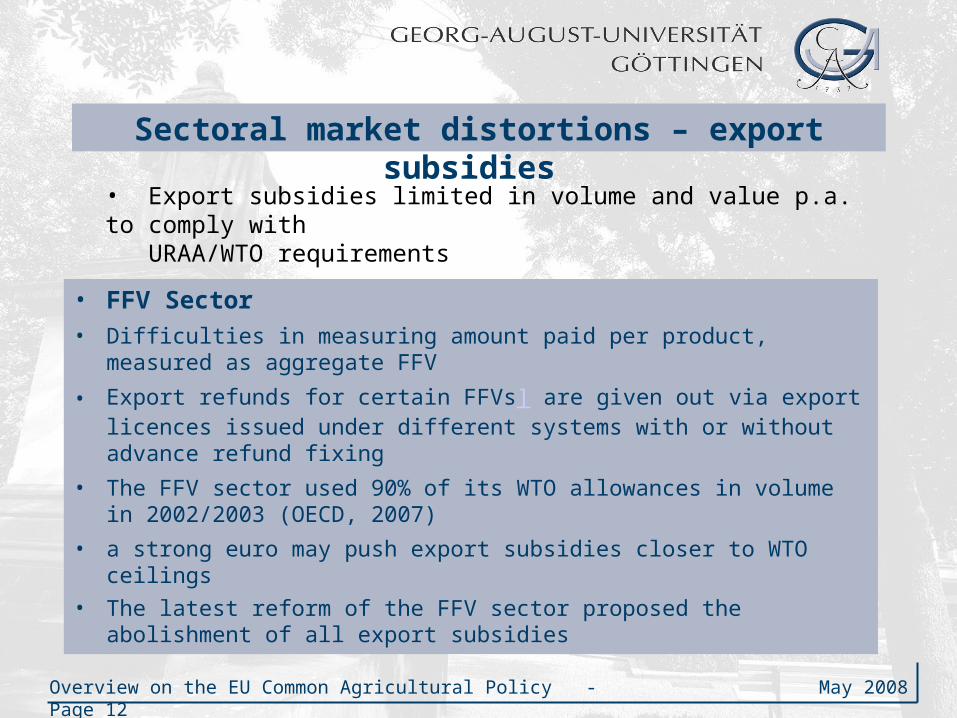

May 2008Overview on the EU Common Agricultural Policy - Page 12

• FFV Sector• Difficulties in measuring amount paid per product, measured as

aggregate FFV

• Export refunds for certain FFVs] are given out via export licences issued under different systems with or without advance refund fixing

• The FFV sector used 90% of its WTO allowances in volume in 2002/2003 (OECD, 2007)

• a strong euro may push export subsidies closer to WTO ceilings

• The latest reform of the FFV sector proposed the abolishment of all export subsidies

Sectoral market distortions – export subsidies

• Export subsidies limited in volume and value p.a. to comply with URAA/WTO requirements

May 2008Overview on the EU Common Agricultural Policy - Page 13

Sectoral market distortions – export subsidies

• Grand Cultures Sector

• in the marketing year 2002/2003, the EU remained well below the WTO ceiling for grand cultures

• Decoupling effects? Subsidies are likely to decrease only slightly

• In 2002 the EU paid 112.8 m Euro to export 3.9 m tons of coarse grains alone (GAINS REPORT, 2003)

• Export subsidies played a lesser role in recent years given the tendency of EU grand cultures prices convergence with world prices

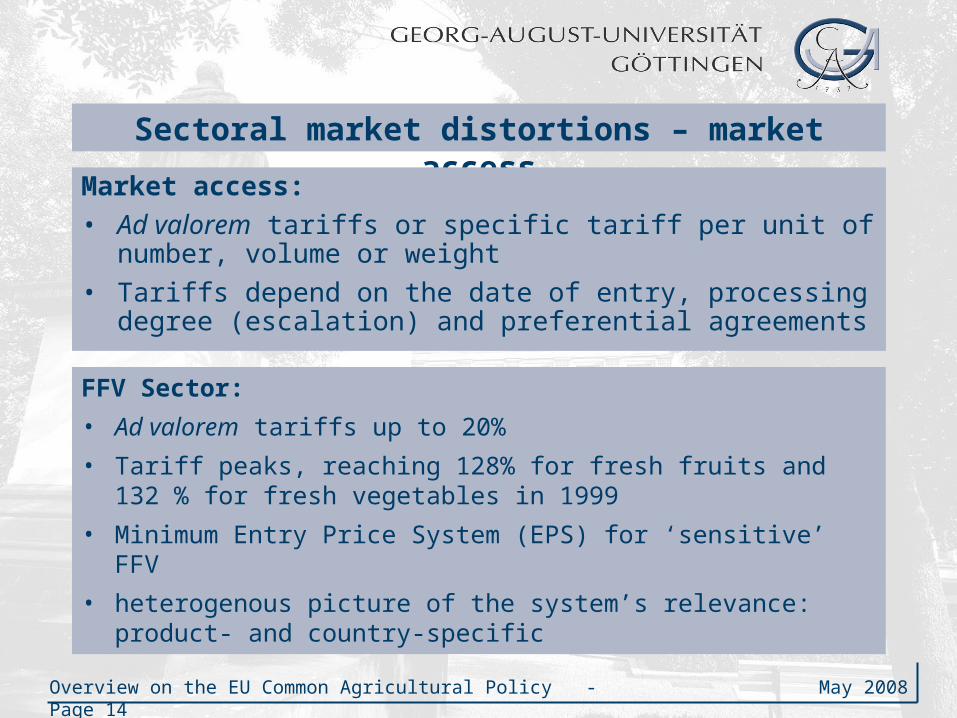

May 2008Overview on the EU Common Agricultural Policy - Page 14

Sectoral market distortions – market access

FFV Sector:

• Ad valorem tariffs up to 20%

• Tariff peaks, reaching 128% for fresh fruits and 132 % for fresh vegetables in 1999

• Minimum Entry Price System (EPS) for ‘sensitive’ FFV

• heterogenous picture of the system’s relevance: product- and country-specific

Market access:

• Ad valorem tariffs or specific tariff per unit of number, volume or weight

• Tariffs depend on the date of entry, processing degree (escalation) and preferential agreements

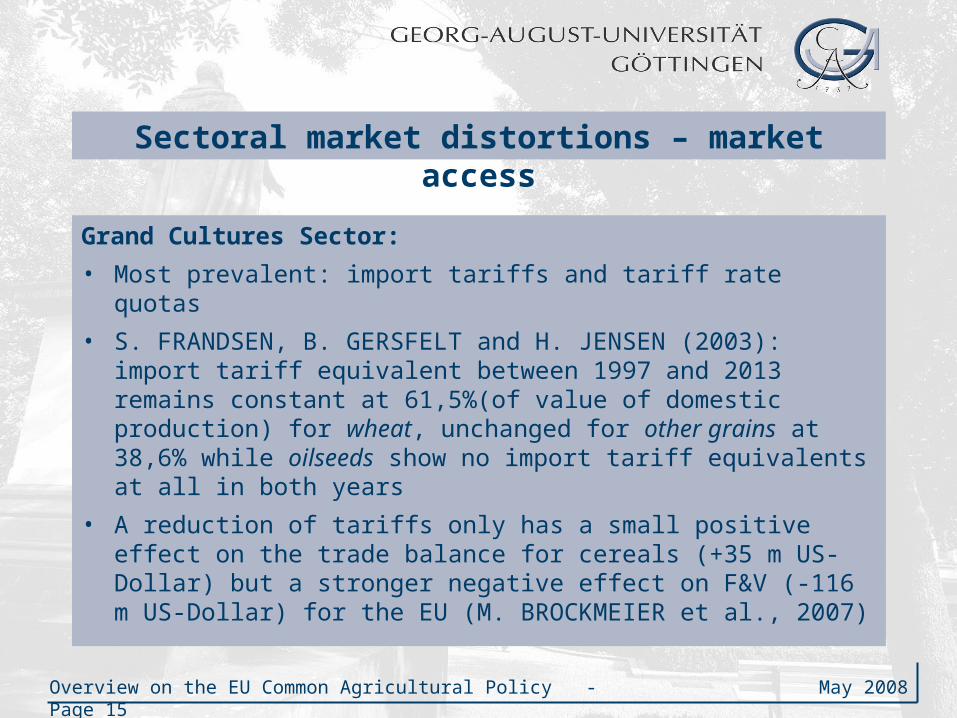

May 2008Overview on the EU Common Agricultural Policy - Page 15

Sectoral market distortions – market access

Grand Cultures Sector:

• Most prevalent: import tariffs and tariff rate quotas

• S. FRANDSEN, B. GERSFELT and H. JENSEN (2003): import tariff equivalent between 1997 and 2013 remains constant at 61,5%(of value of domestic production) for wheat, unchanged for other grains at 38,6% while oilseeds show no import tariff equivalents at all in both years

• A reduction of tariffs only has a small positive effect on the trade balance for cereals (+35 m US-Dollar) but a stronger negative effect on F&V (-116 m US-Dollar) for the EU (M. BROCKMEIER et al., 2007)

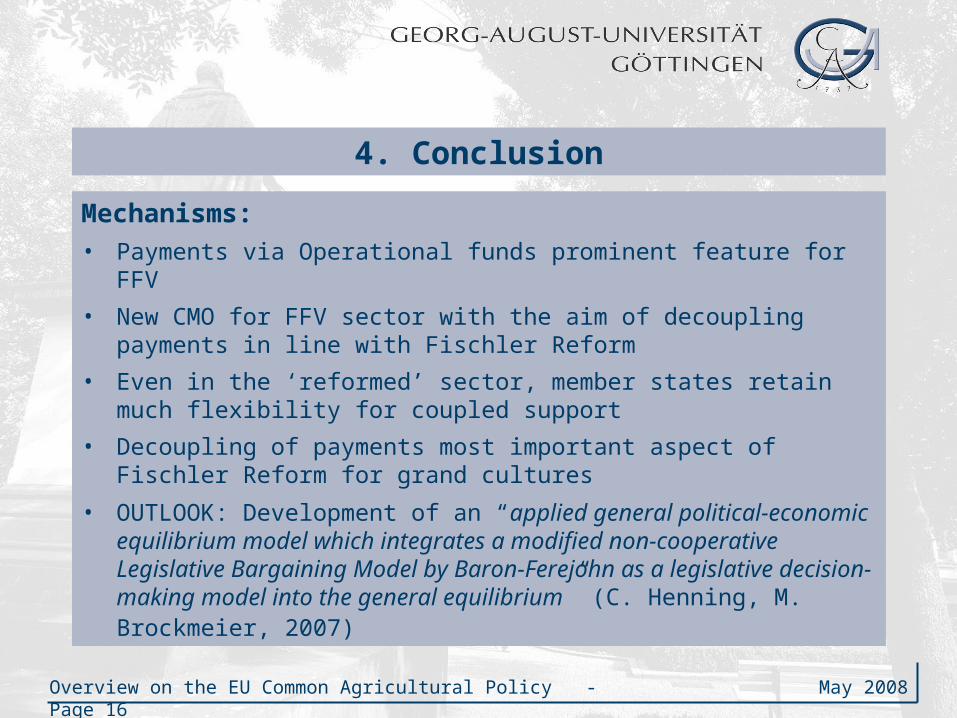

May 2008Overview on the EU Common Agricultural Policy - Page 16

4. Conclusion

Mechanisms:• Payments via Operational funds prominent feature for FFV

• New CMO for FFV sector with the aim of decoupling payments in line with Fischler Reform

• Even in the ‘reformed’ sector, member states retain much flexibility for coupled support

• Decoupling of payments most important aspect of Fischler Reform for grand cultures

• OUTLOOK: Development of an “applied general political-economic equilibrium model which integrates a modified non-cooperative Legislative Bargaining Model by Baron-Ferejohn as a legislative decision-making model into the general equilibrium” (C. Henning, M. Brockmeier, 2007)

May 2008Overview on the EU Common Agricultural Policy - Page 17

4. Conclusion

Market distortions:

• In both sectors there are significant market access and export competition distortions belonging to the WTO’s ‘amber box’

• Principal change was in domestic support pillar for the grand cultures sector, having witnessed the decoupling or likely ‘green-boxing’ of payments

• In the FFV sector, withdrawals and other payments via operational programs, if taken together, remained largely unchanged sources of domestic support.

Overview on the EU Common Agricultural Policy - Page 18

Thank you for your attention!