Overview of Successful Mobile Banking Initiatives from Around the

20

Overview of Successful Mobile Banking Initiatives from Around the World Amarante Consulting Aiaze MITHA March 2013

Transcript of Overview of Successful Mobile Banking Initiatives from Around the

Overview of Successful Mobile Banking

Initiatives from Around the World

Amarante Consulting

Aiaze MITHA

March 2013

Page 2

Content

Overview of Successful Mobile Banking Initiatives

1. What is m-banking?

2. Some inspiring m-banking initiatives

3. So, what’s in it for Banks?

Page 3

Access to Finance Remains a Global Challenge

Close to 50% of adults in Central and Eastern Europe do not have access to formal financial services

Page 4

Mobile Channel Helps Broaden the Reach to the Large Unbanked

Masses who Own a Mobile Phone

World Economic Pyramid

Source: World Resources Institute (*Individual Annual Income: 2005 USD Purchasing Power Parity)

500 Mill *>$20k/yr

2 Billion *$3260 to $20k/yr

4 Billion *<$3260/yr or <$9/day

Reach of

MNOs

Opportunity: 1.7 Billion

people

Source: CGAP

Reach of

Banks

Page 5

What is M-Banking?

Branchless

Banking

Delivery of financial services outside conventional bank branches using information and communications technologies and nonbank retail agents.

Source: CGAP

Page 6

This is What M-Banking Looks Like B

ank

or

MN

O

or

PSP

Age

nt

Clie

nt

Page 7

Content

Overview of Successful Mobile Banking Initiatives

1. What is m-banking?

2. Some inspiring m-banking initiatives

3. So, what’s in it for banks?

Page 8

160 Mobile Banking Deployments and 110 Planned Deployments

LEGEND Mobile Commerce projects

1 live mobile banking project

3 or more live mobile banking projects

2 live mobile banking projects

LAC

18 live projects

Africa 89 live projects

APAC

44 live projects

Source : GSMA MMU, Amarante Consulting, February 2013

EE

2 live projects

Middle East

7 live projects

Page 9

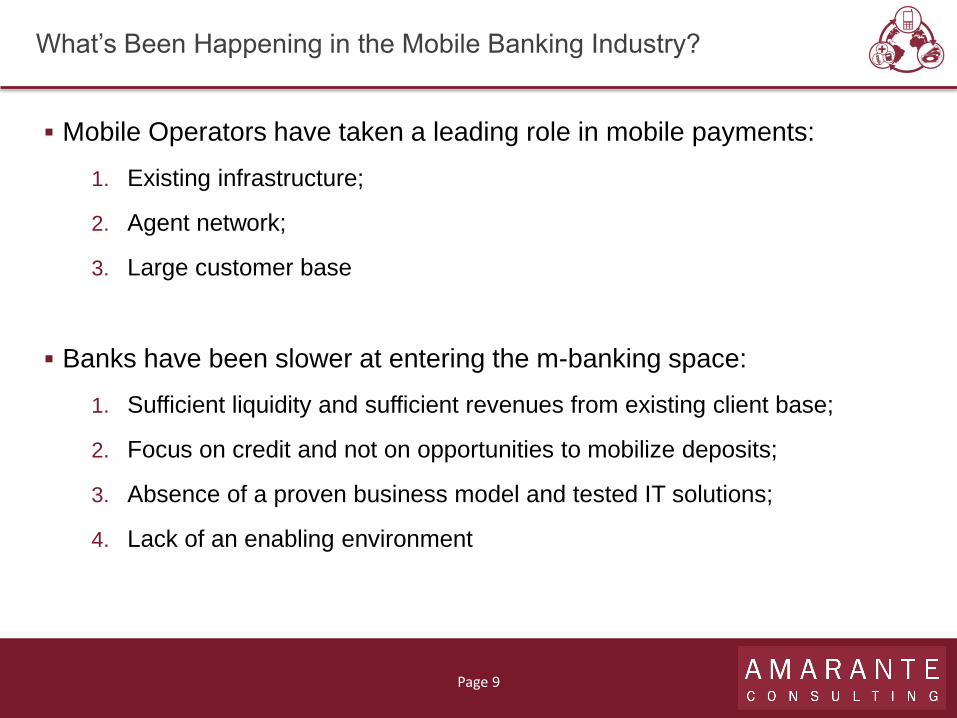

What’s Been Happening in the Mobile Banking Industry?

Mobile Operators have taken a leading role in mobile payments:

1. Existing infrastructure;

2. Agent network;

3. Large customer base

Banks have been slower at entering the m-banking space:

1. Sufficient liquidity and sufficient revenues from existing client base;

2. Focus on credit and not on opportunities to mobilize deposits;

3. Absence of a proven business model and tested IT solutions;

4. Lack of an enabling environment

Page 10

What’s Been Happening in the Mobile Banking Industry?

But there are more and more examples of Bank-Led Models:

Equity Bank: after launching M-Kesho in partnership with Safaricom’s M-Pesa; Eazzy24/7 as

Equity Bank’s own mobile banking channel that the Bank’s customers can access through all

mobile phone operators; and a mobile application that Orange mobile phone customers use

to access their Equity Bank account, Equity decided to build its own agent network.

Tameer – EasyPaisa: is a joint initiative by Telenor Pakistan and Tameer Microfinance Bank

to provide branchless banking in Pakistan. Easypaisa is available to all walk in customers and

Telenor subscribers in Pakistan. With Easypaisa, customers can pay bills, send/receive

money within Pakistan and from abroad, purchase airtime for their mobile phones, make

donations etc.

Transfer: is a joint initiative by Banco AV Villas and COMCEL in Colombia. It is a

transactional account operated via mobile phones that enables clients to make and receive

payments. It will be further complemented by a savings, credit and insurance offering

targeting the unbanked, all operated via mobile and agent channels.

Until recently, we mostly heard about Telco-led models: Safaricom Mis Safaricom’s successful mobile payment product, with over 18 million

customers served through 60,000 agents distributed across Kenya and over $1 billion worth

of transactions processed every month through the systemPesa:.

Page 11

Africa: M-Pesa Has Progressively Introduced a Complete Set of Mobile

Banking Products

M-Pesa

to Bank

M-Pesa

Na Bonga

M-Pesa

Transactional

Services

M-Pesa

P2P

Payments

M-Shwari

Savings

& Credit

M-Kesho

Savings

Account

2007: launch of M-Pesa by

Safaricom that quickly becomes a

leading service for cash transfers

Starting 2007: introduction of

additional payment services available

to M-Pesa customers (airtime,

merchant payment, bill payment…)

2009: M-Kesho is one of the first

product created to offer micro finance

products over the mobile channel

2012: within 3 months, M-Shwari,

that provides access to savings and

credit for M-Pesa Customers, has

captured a significant part of M-Pesa

customers

Starting 2009: Kenyan

banks started integrating

their banking infrastructure

with M-Pesa allowing

transfers between M-Pesa

and any bank accounts

2009: loyalty program that

allows M-Pesa customers

to earn Bonga Points on

chargeable transaction

M-Pesa: 18 million customers Over 60,000 agents

M-Kesho: 0.5 million customers after 6months launch

M-Shwari: 70,000 accounts opened the first day

Page 12

National remittance is the main product offering of M-PESA.

Safaricom positioned the product as a fast, safe and easy way to ‘send money home’. The service also enables airtime purchase,

bill payment, ATM withdrawal and purchase of goods and

services

Customers that have registered for M-PESA can send money to

non-registered mobile phone users on any network. This capability spurred initial subscriber growth since it enabled early

registrants to use the system even when there were few other

customers registered.

Large BTL and ATL educational camapign Safaricom invested a

large amount in marketing and customer education The product is aggressively advertised through. The initial TV and radio

advertisements of the product played on the emotional aspects

of national money transfer (“send money home”) and used the local culture to explain the benefits of the product.

Branding M-PESA has benefited directly from closely associating the product brand to Safaricom’s which is associated

with people’s idea of a modern Kenya and plays on nationalistic

sentiments. A distinct M-PESA sign is distributed to each retail shop and retail agents

Safaricom has developed an extensive agent network

nationwide. Currently, there are more than 22,000 by the end of 2010. Several large institutions such as Kenya Power and Light

Commission (KPLC), Kenya Airways, and Nakumatt

supermarkets also support MPSA

Agent Training and management is one of the key

achievements. Safaricom uses an external agency management firm (Top Image) with over 50 staff supporting the product to

train and manage M-PESA agents

Distribution & Ecosystem Marketing Campaign

Customer value proposition

Sources: CGAP, GSMA, IOM World, Various Web Publications

Africa: A Number of Factors Played a Key Role in the Success of

M-Pesa

Page 13

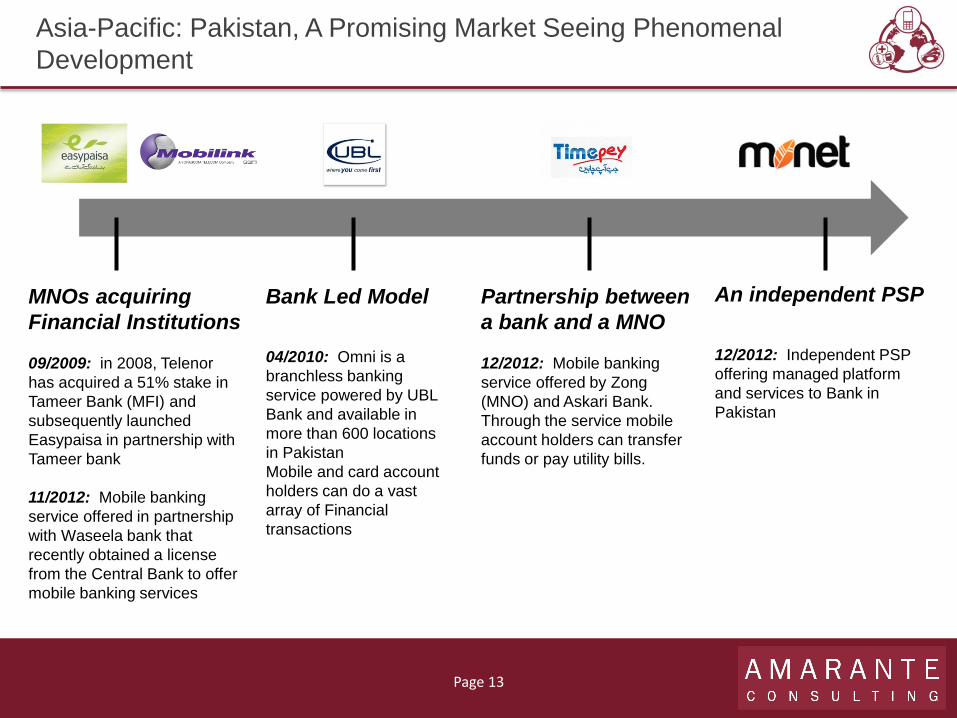

Asia-Pacific: Pakistan, A Promising Market Seeing Phenomenal

Development

MNOs acquiring

Financial Institutions

09/2009: in 2008, Telenor

has acquired a 51% stake in

Tameer Bank (MFI) and

subsequently launched

Easypaisa in partnership with

Tameer bank

11/2012: Mobile banking

service offered in partnership

with Waseela bank that

recently obtained a license

from the Central Bank to offer

mobile banking services

Bank Led Model

04/2010: Omni is a

branchless banking

service powered by UBL

Bank and available in

more than 600 locations

in Pakistan

Mobile and card account

holders can do a vast

array of Financial

transactions

An independent PSP

12/2012: Independent PSP

offering managed platform

and services to Bank in

Pakistan

Partnership between

a bank and a MNO

12/2012: Mobile banking

service offered by Zong

(MNO) and Askari Bank.

Through the service mobile

account holders can transfer

funds or pay utility bills.

Page 14

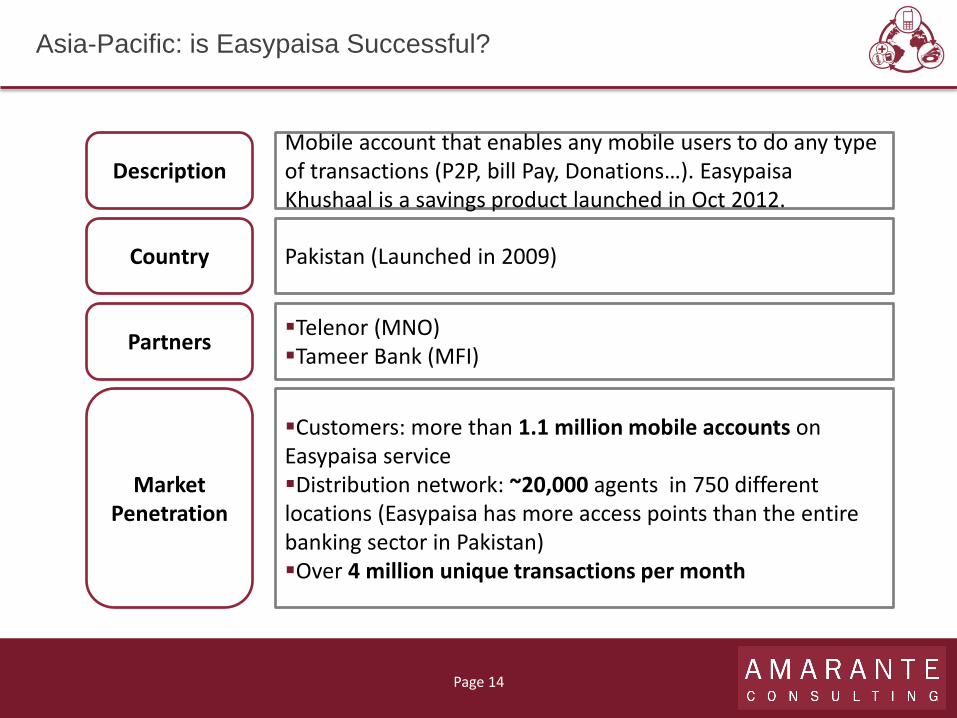

Asia-Pacific: is Easypaisa Successful?

Description Mobile account that enables any mobile users to do any type of transactions (P2P, bill Pay, Donations…). Easypaisa Khushaal is a savings product launched in Oct 2012.

Country Pakistan (Launched in 2009)

Partners Telenor (MNO) Tameer Bank (MFI)

Market Penetration

Customers: more than 1.1 million mobile accounts on Easypaisa service Distribution network: ~20,000 agents in 750 different locations (Easypaisa has more access points than the entire banking sector in Pakistan) Over 4 million unique transactions per month

Page 15

30 millon

subscribers

MOBILE BANKING

ALLIANCE WITH

CLARO AGENT NETWORK

~10,000 agents

~4,000 agents

TECHNOLOGY

BEING USED

2,700 ATMs

Latin America: Banco AV Villas, A Bank That Has a Mass Retail Vision

Page 16

Latin America: Banco AV Villas Will Gradually Introduce Financial

Products Targeting Low Income Segments

Transactional Account

Loan Products

Savings product

INSURANCE

PRODUCT

INSURANCE

PRODUCT

UNBANKED BANKED

Holistic approach to solving the challenges of the unbanked Strategic considerations around the partnership with a MNO Clear financial rationale

Enable

customers

to make

payments

Page 17

Content

Overview of Successful Mobile Banking Initiatives

1. What is m-banking?

2. Some inspiring m-banking initiatives

3. So, what’s in it for Banks?

Page 18

Bank Expand bank outreach at

low cost

Portfolio growth

Deposit mobilization

Selling other financial products

MNO Customer retention

Increase in ARPU

Generating new revenue stream

Customer acquisition (individual/corporate)

Perspectives for Banks and MNOs are Different

Page 19

A business case based on transaction revenues only is likely to be unsustainable

Significant CAPEX (e.g. mobile banking platform) and OPEX investments are only going to be offset by offering core financial products to a large customer base

The impact on the Bank’s P&L should be built around:

Revenue growth from float intermediation margin

Reduction in costs of funds

Improved operating cost ratio

Client growth (expand in

areas that cannot be

served by a Branch)

Deposit mobilization

Portfolio growth

Expected Returns for Financial Institutions