Overview of Finance and Budgeting February 9, 2006.

43

Overview of Finance and Budgeting February 9, 2006

-

Upload

sidney-critchlow -

Category

Documents

-

view

221 -

download

0

Transcript of Overview of Finance and Budgeting February 9, 2006.

Overview of Finance

and Budgeting

February 9, 2006

Community Charter – Financial Officer Responsibilities

(SS149):

• Receive all monies paid

• Keeping of all funds and securities

• Investing municipal funds

• Expending funds authorized by council

• Records retention

• Exercise control and supervision

Financial ModelTaxes

DCC & DevelopmentContributions

Other sources of revenue

Operating Costs

Total Income

Reserves

Capital Program

Utilities

The Fraser Institute's Canadian Tax Simulator 2003

0

5

10

15

20

25

30

35

40

1981 1984 1987 1990 1993 1996 1999 2002

Total taxes

Federal taxes

Municipal taxes

Provincial taxes

VendorVendor

Income / ProfitIncome / Profit SalariesSalaries SuppliersSuppliers

Federal / ProvincialGovernment

Federal / ProvincialGovernment

PSTPST

GSTGST

PSTPST

GST GST

Business /Business /Income TaxIncome Tax

Business /Business /Income TaxIncome Tax

IncomeIncomeTaxTax

$1.00$1.00

Taxation Assessment Classes

1. Residential

2. Utilities

4. Major Industry

5. Light Industry

6. Business and Other

7. Managed Forest Land

8. Recreational property / Non-profit organization

9. Farm

‘Constant’ ‘Constant’‘Variable’

A x B = CA x B = C

Assessment Value/ 1000

Assessment Value/ 1000

Tax Revenue

Tax Revenue

Tax‘Mill Rate’

Tax‘Mill Rate’

X =

Calculation Of Property Tax Rates

Calculation Of Property Tax Rates

‘Unknown’ ‘Known’‘Known’

B = C / AB = C / A

Assessment Value/ 1000

Assessment Value/ 1000

Tax Revenue

Tax Revenue

Tax‘Mill Rate’

Tax‘Mill Rate’ = /

Calculation Of Property Tax Rates (Cont.)

Calculation Of Property Tax Rates (Cont.)

Example

2004:

(293,000 / 1000) x 3.4653= $1,015

2005 (at 2004 Mill Rates):

(338,000 / 1000) x 3.4653= $1,171

2005 (new Mill Rate,Tax Revenue required):

(338,000 / 1000) x 3.0625 = $1,035

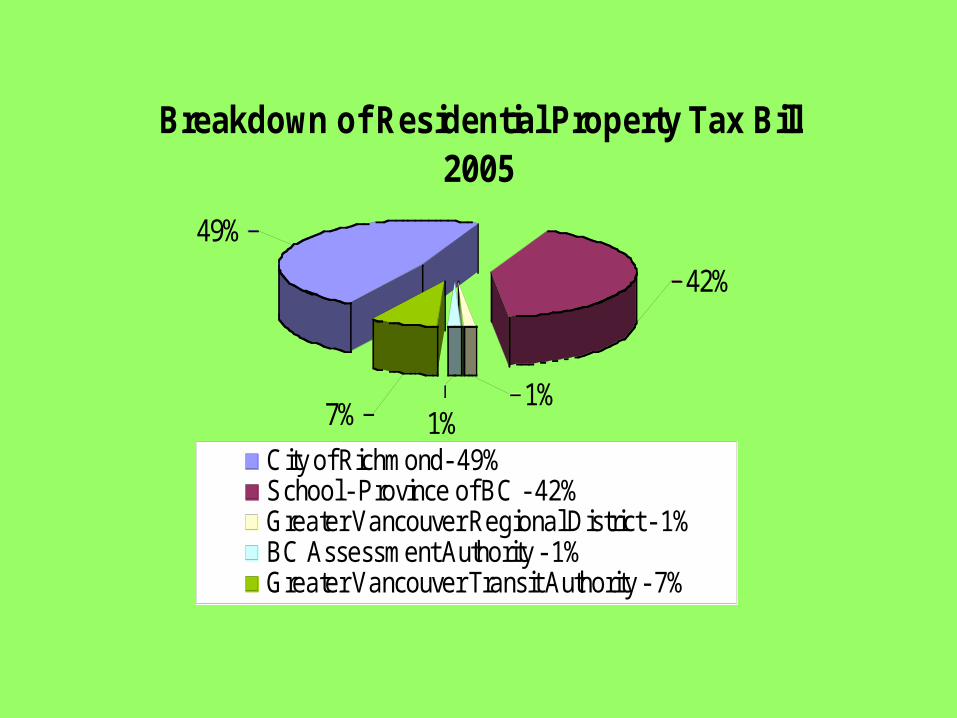

Breakdown of Residential Property Tax Bill 2005

49%

7%

42%

1%1%

City of Richmond- 49%School - Province of BC - 42%Greater Vancouver Regional District - 1%BC Assessment Authority - 1%Greater Vancouver Transit Authority - 7%

Development Cost Charges(DCC)

• Parks Acquisition & Parks Development

• Roads

• Sanitary Sewer• Storm Sewer• Water

DCCs are fees from new development to help pay for cost of infrastructure services needed to accommodate growth, specifically for:

Community Charter – Reserves Funds

(SS188)

• Council may, by bylaw, establish a reserve fund for a specified purpose

• Money and interest must be used only for the purpose of which the funds was established

• Examples: Affordable Housing Capital Building &

Infrastructure Child Care Development Drainage Improvement

Leisure Facilities Local Improvements Neighbourhood Improvement Sanitary Sewer

Watermain Replacement

ALLOCATION OF COST BY DEPT. – 2005ALLOCATION OF COST BY DEPT. – 2005

Police 21%

Fire Rescue17%

Recreation 8% Parks Maintenance

6%

Facilities Management 2%

Urban Development 3%

Finance & Corp Services 3%

Engineering 4%

Storm Drainage 2%Corporate Admin 2%

Community Centres 4%

Library Services 5%

Information Technology5%

Roads 5%

Transfer to Reserves5%

Fiscal Expenditures incl. Debt

6%

Human Resources 2%

Long Term Financial Management Strategy

• Tax Revenue• Gaming Revenue• Alternative Revenues

& Economic Development

• Changes to Senior Government Service Delivery

• Capital Plan• Cost Containment• Efficiencies & Service

Level Reductions• Land Management• Administrative• Debt Management

10 Principals are:

BUDGETING

Budget Process

Community Charter

PublicFeedback

Prior Year’s Base Budget

City Council Direction

Actual Trend Analysis

City Corporate Plan (LTFMS)

External & Internal Factors

Establish ServiceLevels / Budget

Guidelines

Business Planning &Systems Set Up

Prepare & ReviewAnnual Budget

Prepare & Review5 YFP

Public Consultation

Annual Budget

Document

5YFPDocument

Utility Rates& PropertyTax Rates

City CouncilReview &Approves

PROCESSOUTPUTINPUT

Budget Cycle

Apr*Set Tax Rates

Feb – Mar*Finalize 5YFP

Aug – SepPrepare BudgetsBy Organization(Business Unit)

Jun – JulBusiness Planning &

System Set-Up

Oct – Nov*Budget

Presentation

Jan – Feb*5YFP Presentation &Public Consultation

Dec –JanPrepare & Review

5YFP Nov – Dec*Finalize Annual

Budget & Set UtilityRates

May*Establish Service

Levels

YEAR – ROUND

Control & Monitor Budgets

Feb – AprYear End

Financials & Audit

Council Involvement

Sep - OctReview Budgets(Incl. Additional

Levels)

*

Planning

ApprovalPreparation

Review &

Presentation

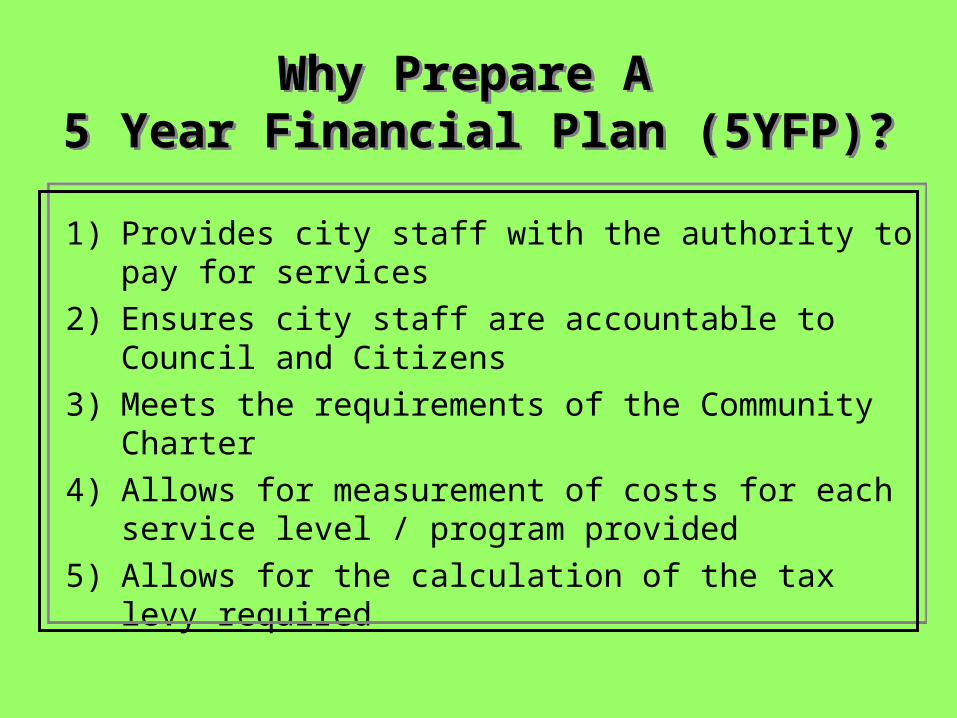

Why Prepare A 5 Year Financial Plan (5YFP)?

Why Prepare A 5 Year Financial Plan (5YFP)?

1) Provides city staff with the authority to pay for services

2) Ensures city staff are accountable to Council and Citizens

3) Meets the requirements of the Community Charter

4) Allows for measurement of costs for each service level / program provided

5) Allows for the calculation of the tax levy required

Community Charter

• SS 165(1)-adoption of financial plan by bylaw before property tax bylaw is adopted

• SS 165(3)-fin. plan is for a period of 5 years

• SS 165(4)-fin. plan must set out proposed expenditures transfers and funding sources

• SS 165(5)-fin. plan must be balanced

Community Charter

• SS 166-public consultation required before fin. plan adopted

• Div 3, SS 197(1)-ppty tax bylaw before May 15.

Budgets

• Led by Council

• About delivering services

• Ensuring accountability

Budgets

• The budget, is a projection of future revenues and expenditures

• The budget should also be used as a management and planning tool to guide the operations of the municipality

• The budget provides an opportunity to review the appropriateness of local tax policies in the context of the capacity of the local assessment base.

Uses of the Budget

Council

• Monitor and control departments/programs

• Establishing priorities for present and future work plans

• Communicating plans to constituents

• Resolve conflict (allocate scarce resources)

Uses of the Budget

Management Team

• Control expenditures

• Incentive performance planning of departments and personnel

• Planning for goal setting

• Communicating needs for additional resources

Uses of the Budget

Public

• Source of data for analysis and debate

• Scorecard

• Information of Council’s goals and priorities

Other Financial Controls

• Purchasing-spending limits

• Trend analysis/history

• HR-Personnel limits and pay scale

• PSAB-Public Sector Accounting Board-rules of accounting

Steps in the Budget Process

Finance Role

• Involve all departments

• Provide economic data & assumptions

• Review, analyze and provide feedback

• Review and approval from Mgmt & Committee

• Approval from Council (base for 5 YFP)

Steps in the Budget Process

• Additional Level Requests-represents new items such as new programs or program enhancements from the previous year’s budget

• Eg. Staffing, new programs• Review and approval from Mgmt &

Committee• Approval from Council (base for 5 YFP)

Issues and Conflict

• Finance role of guardian vs employee

• Special needs vs communal needs

• Present vs Future

• Financial vs Social

Popular Budgeting Methods

• Zero Base Budgeting

• Incremental Budgeting

Zero Based

• Zero-based budgeting (1977 President Jimmy Carter) federal budget

• each programme is examined in order to justify its existence, and is compared to alternative programmes.

• Priorities are established and each cost centre is challenged to prove its necessity

• Drawbacks-time and costs, effect on behavior and morale

Incremental

• The organisation's historical costs are the base from which budget planning starts. The focus of the budgeting process is on the changes anticipated in last year's figures.

• In comparison, there are dangers in using last year's figures as in incremental budgeting. There is a risk of 'creeping' costs year on year.

• Less time consuming and threatening to employees

Operating & Capital

• Operating expenditures (e.g., salary or power charges) are incurred to maintain and help the capital expenditure (e.g., building or machine) earn revenue (income).

Operating vs Capital

• Operating- funding is usually primarily by tax revenues, fees, grants.

• Expenditures are primarily period expenditures

• Operating impact from capital

• Capital-funding is usually primarily by reserves, surplus, DCC’s, grants or donations.

• Expenditures have an enduring benefit

• Fruit vs Tree

Operating Budget

Property Tax 70$ Grants 7 Community Revenue 3 Permits 3 Other 17

100$

Salaries 55$ Policing 18 Reserves 10 Materials supplies 3 Utilities 1 Other 13

100$

Balance SheetReservesOpening 50$ Cont'n 10 Exp 8 )( Ending 52$

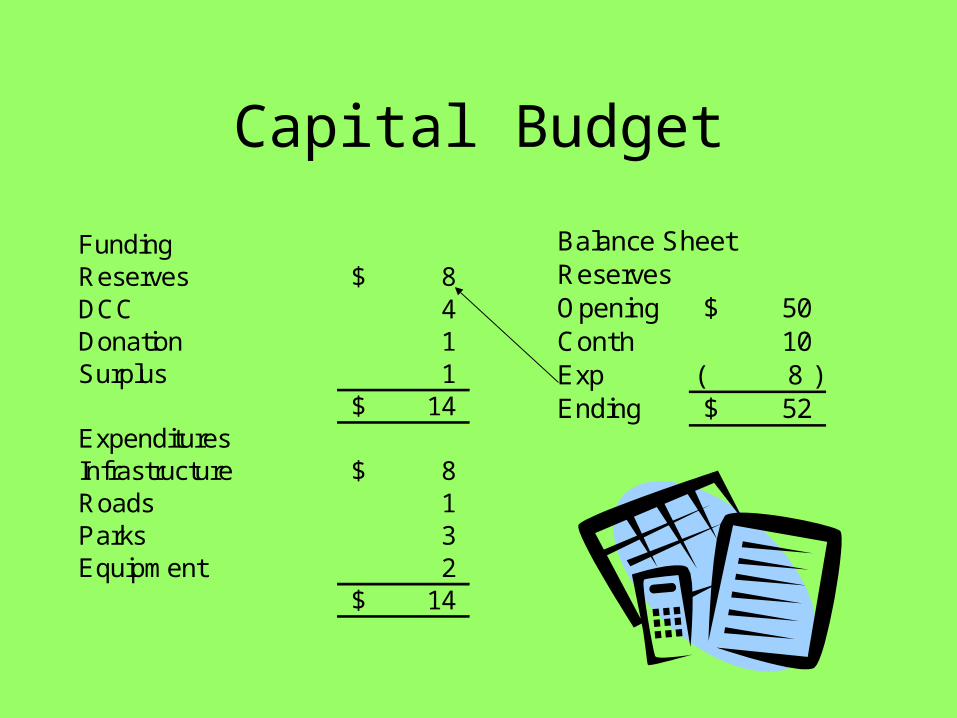

Capital Budget

FundingReserves 8$ DCC 4 Donation 1 Surplus 1

14$ ExpendituresInfrastructure 8$ Roads 1 Parks 3 Equipment 2

14$

Balance SheetReservesOpening 50$ Cont'n 10 Exp 8 )( Ending 52$

Operating Budgets

• Attention should be focused on policy issues such as tax policy, funding priorities and macro issues instead of detailed reviews

• Monitor the budget to avoid surprises at year end

• Maintain adequate fund balances in the event of contingencies

• Look at long term goals and plans

Capital Planning

• Plan should involve conducting analysis of infrastructure needs

• Transparent process for selecting projects• An effective process for monitoring design

and construction• An effective process to maintain

infrastructure in accordance to generally recognized engineering practices - Lifecycle

Capital

Criteria• Level of demand-(essential, established, potential) • Consistent with Council’s strategic plans• Technically feasible• Financial cost-benefit and risk• Societal/Environmental cost-benefit and risk• Funding availability and source

Capital funding

• Pay as you go (reserves, grants, partnering, special levies)

• Debt (LT debt, capital lease)

• Inter-government funding

• Restricted and private donations

Tax Rates

• Measurement • CPI basket relevant to Municipalities?

(food, shelter, clothing, footwear, alcoholic beverages and tobacco products)

• Municipalities - compensation for a unionized workforce, non-finished goods such as asphalt, salt, steel, diesel fuel and electricity.

Tax Rates2005 Increase 2006

Taxes 73.0 4.00% 75.9 Facility Rev & Permits 6.0 2.00% 6.1 Investment income 6.0 2.00% 6.1 Other 15.0 0.00% 15.0

100.0 103.2

Salaries 47.0 3.50% 48.6 RCMP 12.0 5.00% 12.6 Reserves 10.0 0.00% 10.0 Materials supplies 3.0 10.00% 3.3 Utilities 1.0 7.00% 1.1 Other contracts 27.0 2.00% 27.5

100.0 103.2

Questions?