Over-the-Counter Derivatives Regulation - Marie Curie Initial

55

Over-the-Counter Derivatives Regulation: The US Law and its Implementation Marti G. Subrahmanyam (based on the chapter with Viral Acharya and Or Shachar from the NYU-Stern book “Regulating Wall Street”) For presentation at Marie Curie Initial Training Network on Risk Management and Risk Reporting Deutsche Bundesbank Conference Berlin, May 5-6, 2011

Transcript of Over-the-Counter Derivatives Regulation - Marie Curie Initial

Over-the-Counter Derivatives Regulation:The US Law and its Implementation

Marti G. Subrahmanyam(based on the chapter with Viral Acharya and Or Shachar

from the NYU-Stern book “Regulating Wall Street”)

For presentation at Marie Curie Initial Training Network on Risk Management and Risk Reporting

Deutsche Bundesbank Conference Berlin, May 5-6, 2011

Vorführender

Präsentationsnotizen

I thank the organizers for inviting me to this conference. I will provide an overview of the Dodd Frank bill, insofar as it refers to OTC derivatives. These sections of the bill account for about a third of the document, but are likely to be among the most challenging in terms of implementation, due to the need for extensive rule making and implementation.

2

Restoring Financial Stability:How to Repair a Failed System

November 2009

Vorführender

Präsentationsnotizen

When the Lehman bankruptcy was announced on September 15, 2008, it was a watershed event in financial markets, but it also raised the consciousness of academic financial economists. It forced them to rethink their theories and also to comment about the aftermath of this event and how the financial system should be repaired. At my own school, NYU Stern, several of my colleagues came together to publish a book containing several chapters written by 30+ colleagues on various aspects of the crisis and how to ensure that it did not happen again.

3

Regulating Wall Street:

The Dodd-Frank Act and the New Architecture of

Global Finance

November 2010

Vorführender

Präsentationsnotizen

Meanwhile, Congress in the US and equivalent legislative bodies in Europe and many other parts of the world, was extremely concerned about this. There were pulls and pushes in different directions, but ultimately the Dodd-Frank Act become law in July 2010. My colleagues, again took a look at different parts of the bill and dissected it to come to grips with this complex piece of legislation, which ran to 2319 pages in its final version.

Outline• The Financial Crisis and the OTC derivatives market

• The Dodd-Frank bill and OTC derivatives

• Evaluation of the main proposals

• Overview of the OTC derivatives market

• Margin requirements vs. transparency

• How derivatives dealers will be affected

• How end-users will be affected

• Disclosure practices and how they will change

• Clearinghouses and systemic risk

• Implementation of the Dodd-Frank bill: Further work

• Implementation of the Dodd-Frank bill: Recent developments

• Prospects for the future4

Vorführender

Präsentationsnotizen

Let me review the outline of my presentation. I will focus on the bill and its key features. I will also discuss the challenges in the implementation in the past few months, since the passage of the bill. I will end with my personal forecasts for how this bill affect global financial markets and institutions.

The Financial Crisis and the OTC Derivatives Market

The financial crisis of 2007-2009 has highlighted two aspects of the OTC derivatives market that deserve attention and potential reform:

1. Leverage

• Thus far, regulatory capital requirements have not been suitably adjusted to reflect all aspects of OTC derivatives exposures, such as their illiquidity and their counterparty and systemic risks

2. The opacity of exposures in OTC derivatives

• The risk monitoring function in OTC derivatives markets is left to the individual counter-parties

• A counterparty risk externality

• Primary concerns surrounding the failures or near-failures of Bear Stearns, Lehman Brothers and AIG all had to do with uncertainty about how counterparty risks would spread through the web of OTC connections

5

Vorführender

Präsentationsnotizen

Two aspects of OTC derivatives came into focus in the discussion of what went wrong with the financial system that led to the crisis: Various regulatory rules that affected institutions and markets did not accurately reflect OTC derivaitives exposures, particularly counterparty and systemic risks. The opacity of derivatives exposures. The risk of counterparty exposure had an externality that affected the whole system, due to the interconnectedness of the OTC network.

Timeline of the Proposed Bills• December 11, 2009: “The Wall Street Reform and Consumer

Protection Act of 2009” approved by the U.S. House ofRepresentatives Financial Services Committee chaired byCongressman Barney Frank

• March 15, 2010: “The Restoring American Financial Stability Act”was proposed by the U.S. Senate Banking Committee under SenatorChristopher Dodd

• April 21, 2010: The Senate Committee on Agriculture, Nutrition andForestry approved the “Wall Street Transparency and AccountabilityAct of 2010”

• July 15, 2010: The Senate passed the Dodd-Frank Wall StreetReform and Consumer Protection Act by a vote of 60 to 39 (TheHouse of Representatives approved the Act on June 30 by a vote of237 to 192). It was signed by President Obama on June 20.

6

Vorführender

Präsentationsnotizen

Here is the timeline of the key events that led to the legislation. As I mentioned, there were various twists and turns, but the final bill was passed on July 15, 2010.

“Wall Street Transparency and Accountability” Part of the Dodd-Frank Act of 2010

• Which derivatives will be affected?– Essentially, all derivatives, with a few exceptions

– FX derivatives (forwards and swaps, among others) could be excluded, based on a later decision of the Treasury Secretary

• Clearing– The default treatment of derivatives will be that they remain

uncleared

– Exemption process is laid out

– Clearinghouse management

– Uncleared swaps to maintain mandated margin/collateral

• Transparency & Reporting Requirements– Position limits, position accountability and large trade reporting

7

Vorführender

Präsentationsnotizen

Key aspects of the bill…..

“Wall Street Transparency and Accountability” Part of the Dodd-Frank Act of 2010

• Bankruptcy related issues– Bankruptcy exemption

– Collateral segregation

• Trading and risk mitigation– Systemically important institutions in derivatives markets

– Exemptions for banks for balance sheet hedging and end-user exemption for entities with hedges in other business positions

– De Minimis investment requirement

– Leverage limitation requirement

– The Lincoln Amendment (Section 716)

– Prohibition on lender-of-last-resort support for derivatives dealers8

Vorführender

Präsentationsnotizen

Key aspects of the bill (contd.)…..

“Wall Street Transparency and Accountability” Part of the Dodd-Frank Act of 2010

• Enforcement authority with SEC and CFTC– Details left for rule making

– Coordination and conflict resolution across regulators

• Extraterritorial enforcement and international cooperation– Foreign platforms (boards of trade)

– International harmonization

9

Vorführender

Präsentationsnotizen

Key aspects of the bill (contd.)…..

Evaluation of Current Proposals• Overall impact

– Have the potential to stabilize the markets and mitigatesystemic risk

• Clearing– Many important details remain unspecified and subject to

further examination by various regulators, including the SEC,CFTC and the Secretary of the Treasury

– Exact implementation of clearing provisions should contain themoral hazard of clearinghouses given their systemic importance

– Systemic risk in OTC derivatives lies with dealers and not withend-users. The exemption for hedging transactions makes sense

– Clearinghouses to require members to fully collateralize theirlargest exposures, in each class reducing systemic risk

10

Vorführender

Präsentationsnotizen

Overall assessment…

Evaluation of Current Proposals• Transparency & Reporting Requirements

– The Act’s biggest strength lies in legislating counterparty-leveltransparency for the regulators, price-volume level transparencyfor all market participants, and aggregated transparency ofpositions and players in different derivatives markets (twice ayear)

• The modified Lincoln amendment– Not requiring – or even recommending – “audit-and-punish”

treatment of exemptions that are based on hedging motives isan important weakness of the Act

11

Vorführender

Präsentationsnotizen

Overall assessment (contd.)…

Evaluation of Current Proposals• Bankruptcy resolution relating to derivatives entities

– The restriction on Federal assistance to swap entities includingclearinghouses seems to rule out an important mechanism todeal ex-post with systemic risk

– In the event that a clearinghouse gets to the point of insolvency,the Act explicitly prohibits its positions from being transferred toanother clearinghouse. The Act seems to overly restrict ex-postresolution options for stress scenario at a clearinghouse

– In the case of sale and repurchase agreements (“repo markets”),there is a case for softening the bankruptcy exemption forderivative transactions in scenarios where there is a systemicallyimportant counterparty that is going bankrupt

12

Vorführender

Präsentationsnotizen

Overall assessment (contd.)…

• Other issues– Does not recognize the difference between credit derivatives

and other derivatives. A gradual implementation from the mostproblematic to the least would have been better.

– Many issues relegated to regulators for rule making e.g.separation of normal banking from derivatives transactions willrequire a lot of regulatory intervention

Evaluation of Current Proposals

13

Vorführender

Präsentationsnotizen

Overall assessment (contd.)…

The Growth in the OTC Derivatives Market

Vorführender

Präsentationsnotizen

Brief overview of the market size and structure….

• OTC derivatives are a significant proportion of activities of global banks

• Used for both hedging and speculation

• Customized vs. standardized derivatives products

• Systemic risk of OTC derivatives demonstrated in the financial crisis of 2007-2009

• Opacity of exposures to OTC derivatives

• Cost of bailouts borne by taxpayers, while benefits of speculation go to bank employees/shareholders

Overview of the OTC Derivatives Business

15

Vorführender

Präsentationsnotizen

Overview…

Why Credit Derivatives are Different

• “Jump to default” risk

• Difficulty in setting margin

• Risk to clearing house

• Rule of 100% of loss given default of largest position

• No obvious sellers of credit derivatives

• Pro-cyclical risks of credit derivatives

• Legitimate use of sovereign CDS – to hedge sovereign risk in sovereign bonds as well as bonds of corporate headquartered in a country

• Banning/restricting sovereign reduces CDS market liquidity in the underlying bond market, without any benefits

• Better to insist on greater transparency from participants

16

Vorführender

Präsentationsnotizen

The importance of credit derivatives, which were the main problem…

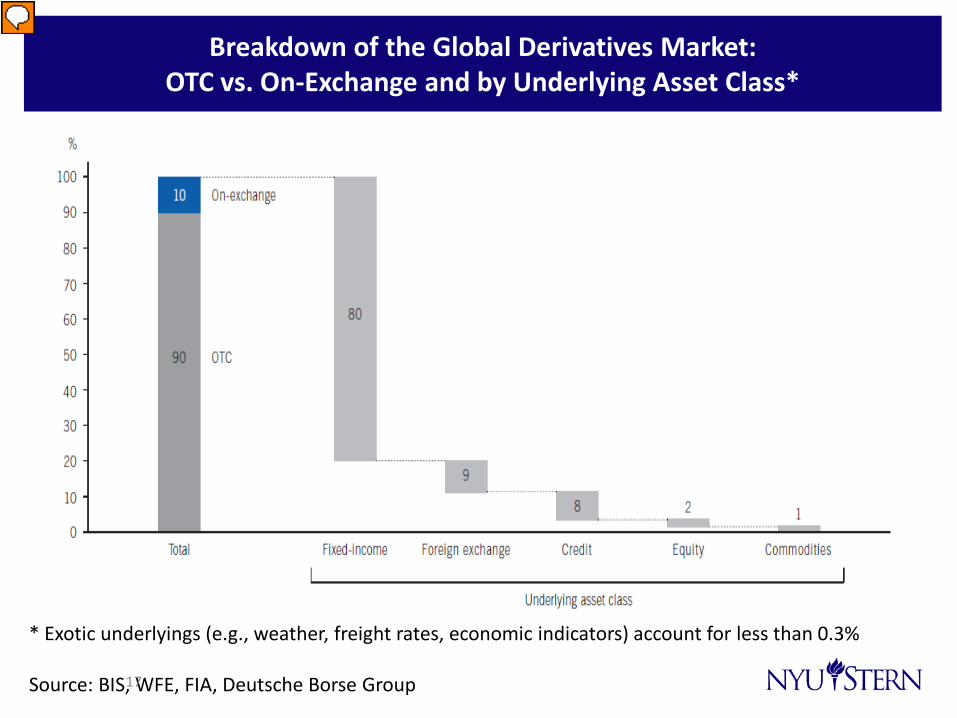

Breakdown of the Global Derivatives Market:OTC vs. On-Exchange and by Underlying Asset Class*

* Exotic underlyings (e.g., weather, freight rates, economic indicators) account for less than 0.3%

Source: BIS, WFE, FIA, Deutsche Borse Group17

Vorführender

Präsentationsnotizen

The relative size of different segments. Note that fixed income is 80%, with FX being 9%. Credit is the next most important one at 8%, while equity and commodities are relatively small.

The Size of the OTC Derivatives Market

Notional amounts outstanding (in trillions of US dollars)

Gross market values and gross credit exposure (in trillions of US dollars)

Source: BIS

18

Vorführender

Präsentationsnotizen

600 trillion dollar market, with about 30 trillion in terms of value of exposure at the peak.

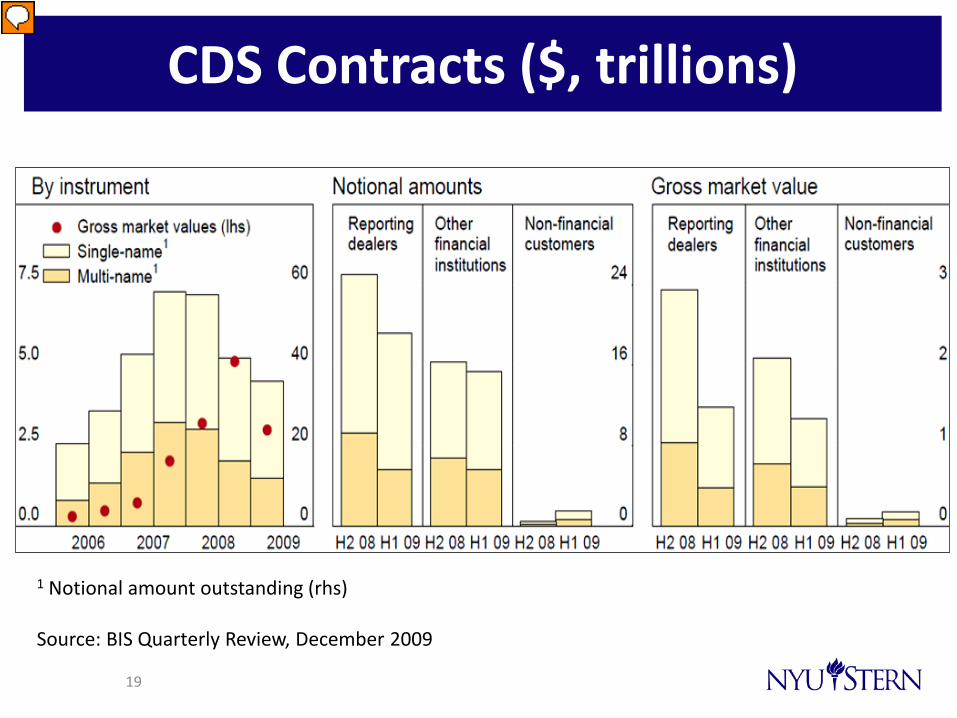

CDS Contracts ($, trillions)

1 Notional amount outstanding (rhs)

Source: BIS Quarterly Review, December 2009

19

Vorführender

Präsentationsnotizen

Most of the credit derivatives are single-name across different slices of the market. Bets/Hedges on a single risk.

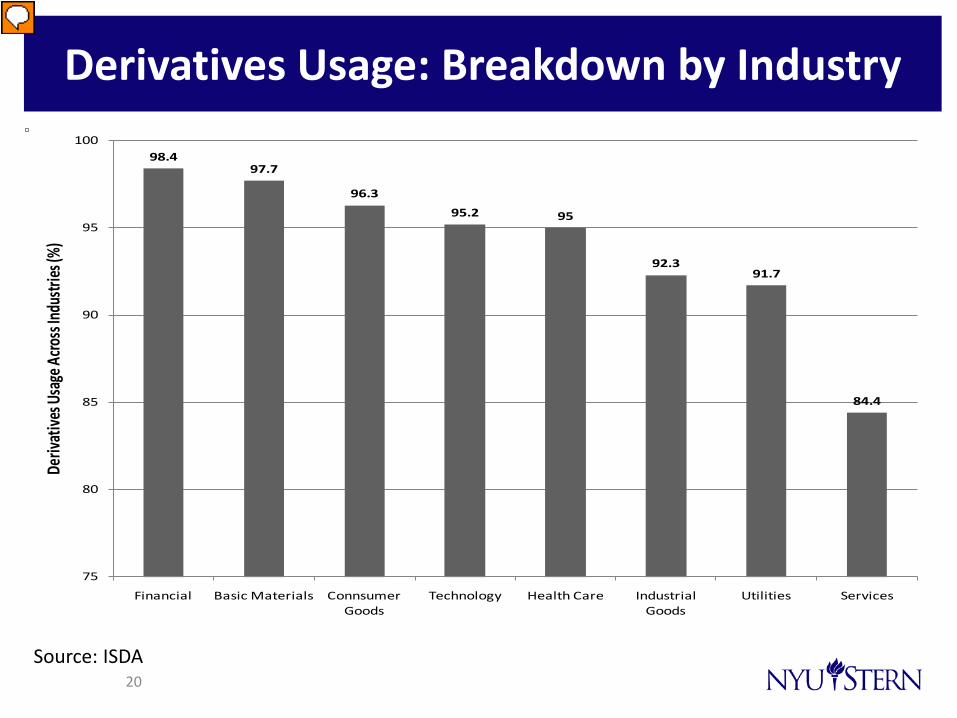

Derivatives Usage: Breakdown by Industry

98.497.7

96.3

95.2 95

92.391.7

84.4

75

80

85

90

95

100

Financial Basic Materials Connsumer Goods

Technology Health Care Industrial Goods

Utilities Services

Deriv

ative

s Usa

ge A

cross

Indu

stries

(%)

Source: ISDA20

Vorführender

Präsentationsnotizen

Who uses derivatives? Most industries, although financials and commodities are the biggest users.

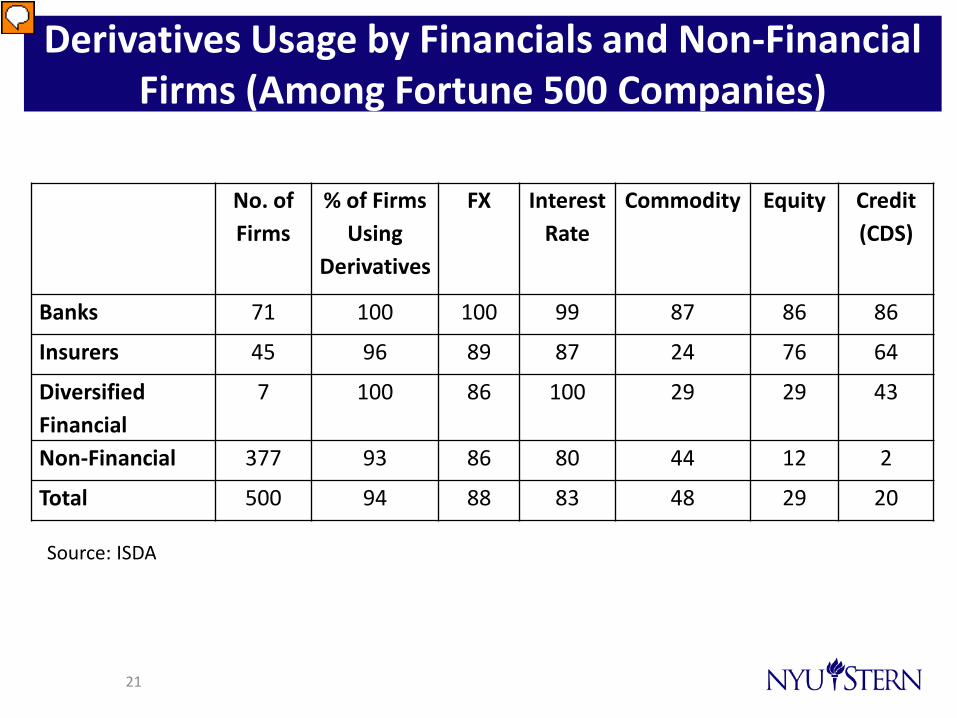

Derivatives Usage by Financials and Non-Financial Firms (Among Fortune 500 Companies)

No. of Firms

% of Firms Using

Derivatives

FX Interest Rate

Commodity Equity Credit (CDS)

Banks 71 100 100 99 87 86 86

Insurers 45 96 89 87 24 76 64

Diversified Financial

7 100 86 100 29 29 43

Non-Financial 377 93 86 80 44 12 2

Total 500 94 88 83 48 29 20

Source: ISDA

21

Vorführender

Präsentationsnotizen

Most popular derives are FX and interest rates, with heavy usage by banks, insurance and financial companies.

Credit Derivatives Composition by Product Type as of 4Q09

Credit Default Swaps98.10%

Total Return Swaps0.68%

Credit Options0.26% Other Credit

Derivatives0.96%

Credit Default Swaps

Total Return Swaps

Credit Options

Other Credit Derivatives

Source: OCC, 4Q09 Report22

Vorführender

Präsentationsnotizen

Most of the credit derivatives are CDS.

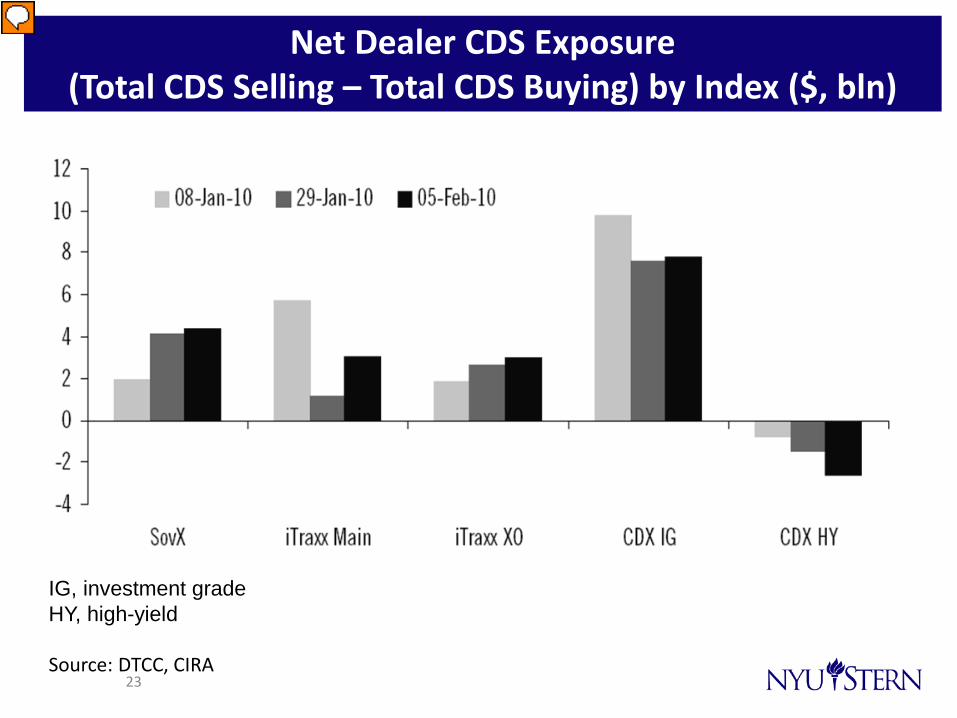

Net Dealer CDS Exposure (Total CDS Selling – Total CDS Buying) by Index ($, bln)

IG, investment gradeHY, high-yield

Source: DTCC, CIRA23

Vorführender

Präsentationsnotizen

The biggest index products are the CDS IG and the main iTraxx indices, with SovX being a close second.

Margin Requirements vs

Transparency

Vorführender

Präsentationsnotizen

We now look at the parts of the bill dealing with margins, a big piece of the bill.

The Size of the OTC Derivatives Market• Regulations are easy to implement for standardized products

• Non-standardized products: collateral?

• Risks mainly in these products with the major dealers (global banks) who do not post enough margin

• What about others such as large insurers and corporates?

• Tradeoff between excessive collateral requirements and systemic risk created by OTC derivatives

• Require disclosure of trades and positions in an aggregated manner, including collateral posted

• Rely more on transparency rather than regulatory rules, which could become rigid

Margin Requirements vs. Transparency

25

Vorführender

Präsentationsnotizen

Challenge of margins for non-standard products.

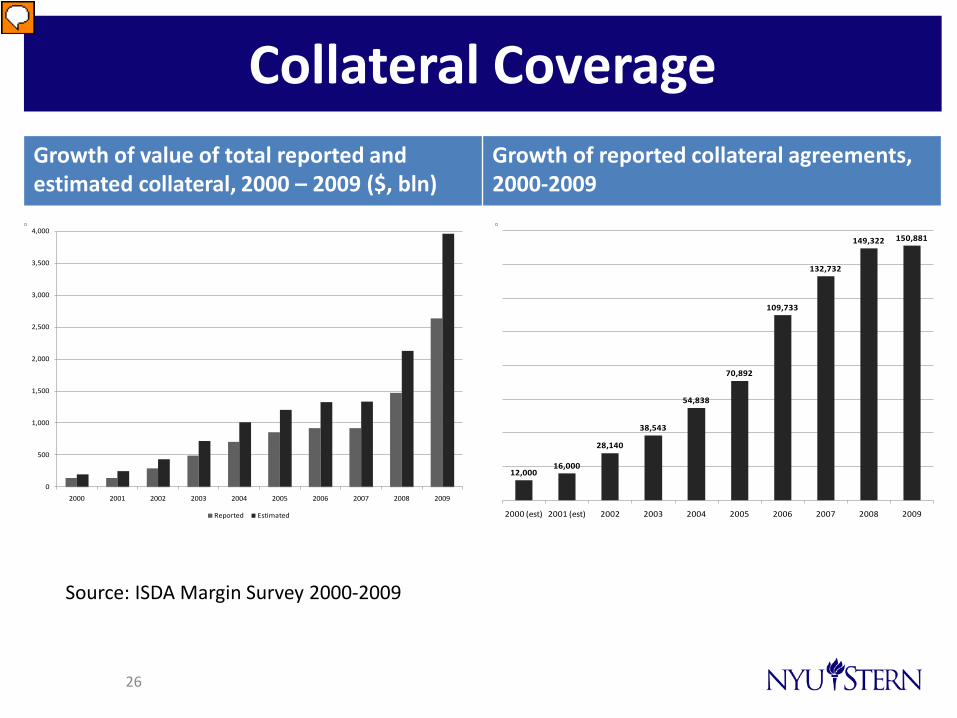

Collateral CoverageGrowth of value of total reported and estimated collateral, 2000 – 2009 ($, bln)

Growth of reported collateral agreements, 2000-2009

12,00016,000

28,140

38,543

54,838

70,892

109,733

132,732

149,322 150,881

2000 (est) 2001 (est) 2002 2003 2004 2005 2006 2007 2008 2009

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

Reported Estimated

Source: ISDA Margin Survey 2000-2009

26

Vorführender

Präsentationsnotizen

Collateral value and numbers of agreements have been growing…

Counterparties of Collateralized Transactions

Source: ISDA Margin Survey 2009

• A total of 67 ISDA member firms responded to the 2009 Margin Survey..

• Based on the number of collateral agreements executed, the Survey classifies respondents into: – A “large” program: at least 1,000 agreements (under this criterion, 20 firms are classified as “large”).

– A “medium” program: 51-1,000 agreements (25 firms)

– A “small” program: less than 50 agreements (22 firms)

27

Vorführender

Präsentationsnotizen

Who are the counterparties? Banks, Hedgefunds and Others (mainly insurance cos.)

Trade volume and exposure collateralized:2003-2009 Survey (%)

Percent of Trade Volume requiring Collateral Percent of Exposure Collateralized

2009 2008 2007 2006 2005 2004 2003 2009 2008 2007 2006 2005 2004 2003

OTC Derivatives

65 63 59 59 56 51 30 66 65 59 63 55 52 29

Fixed Income

63 68 62 57 58 58 53 71 66 65 57 58 55 48

FX 36 44 36 37 32 24 21 48 55 44 44 43 37 28

Equity 52 52 51 46 51 45 27 52 56 56 56 61 52 24

Metals 39 38 37 37 31 24 18 47 41 34 34 44 40 18

Energy 39 40 42 48 36 26 16 47 39 41 44 37 30 15

Credit 71 74 66 70 59 45 30 66 66 66 62 58 39 25

Source: ISDA Margin Survey 2009 and earlier years28

Vorführender

Präsentationsnotizen

Skip

Deal with the Dealers First

Vorführender

Präsentationsnotizen

The bill focuses on swap dealers.

• A few large dealers account for a significant portion of outstanding amounts and volume

• Significant systemic risk resides here

• Need to separate hedging from pure speculation through “prop trading” – Volcker rule

• Not necessary to hive off trading/asset management, but simply require higher capital/collateral

• Strictly monitor hedge exemptions and impose penalties if there are violations

How Dealers will be Regulated

30

Vorführender

Präsentationsnotizen

This focus on a few large dealers is justified because they dominate the industry. Other issues…

Concentration of Derivative Contracts:All Commercial Banks, 1Q09 ($, Trillions)

Source: Call Reports, OCC 4Q0931

Vorführender

Präsentationsnotizen

Among banks, top 5 banks in the US account for most of the market in all key products….

Notional value of derivatives contracts outstanding held by US Banks as of 1Q09 ($, Trillions)

81.1

77.9

47.8

39.1

31.7

0 10 20 30 40 50 60 70 80 90 100

JP Morgan Chase

Bank of America

Goldman Sachs

Morgan Stanley

Citigroup

Source: Deutsche Bank, WSJ, OCC32

Vorführender

Präsentationsnotizen

Size data….

The Proposed Reforms will Help the End-Users

Vorführender

Präsentationsnotizen

What about end-users, who use derivatives to hedge the risks in their business? Should they be treated differently?

How End-users will be affected

• Corporations use derivatives to hedge business risks• Use is mostly concentrated in small percentage of firms• Cost of customized derivatives may go up• Standardized products create basis risk• Dealer counter-party risk will go down due to clearing

and greater transparency• End-users will get special exemption, but subject to

monitoring with penalties for violation of hedging norms

34

Vorführender

Präsentationsnotizen

Arguments for why end-users should be treated differently…

Company Total Assets Total Derivative Assetsa

Total DerivativeLiabilitiesa

Selected Insurance Companies

American International Group 819,758 10,192 5,197 MetLife, Inc. 491,408 9,351 4,009Prudential Financial 427,529 7,430b 4,621b

MBIA, Inc. 27,907 1,126 5,332Selected Utilities and Power Companies

Duke Energy Corporation 53,584 491 649Southern Company 49,557 20 461Exelon Corporation 48,863 1,437 506American Electric Power 45,865 710 353FPL Group, Inc. 45,304 1,016 1,762Edison Intl 44,429 950 948Dominion Resources, Inc. 41,687 2,219 2,219PG&E Corporation 41,335 298 542Entergy Corporation 36,613 351 91AES Corporation 34,838 202 467Consolidated Edison, Inc. 34,224 279 464FirstEnergy Corporation 33,557 383 869Progress Energy, Inc. 30,903 5 935Centerpoint Energy, Inc. 19,676 142 221

Selected Energy and Oil Companies

Exxon Mobil Corporation 222,491 N/A N/AConocoPhillips 143,251 7,442 7,211Anadarko Petroleum Corporation 48,154 533 84XTO Energy, Inc. 37,056 2,397 66Chesapeake Energy Corporation 29,661 1,978 635El Paso Corporation 22,424 873 896Spectra Energy Corporation 21,417 26 22

Derivative Assets and Liabilitiesas of June 6, 2009 ($, mln)

a Includes the impact of netting adjustments.b Presented gross without netting benefits.

Source: Fitch, quarterly filings.

35

Vorführender

Präsentationsnotizen

Skip…

Current OTC Disclosure Provided by Dealer Banks

Vorführender

Präsentationsnotizen

OTC derivatives by banks not sufficiently detailed….

Goldman Sachs’ accounting disclosures of credit default swap exposures: Sep 2009

37

Vorführender

Präsentationsnotizen

Very high level…Hard to interpret.

Goldman Sachs’ accounting disclosures of credit default swap exposures: June 2009

38

Vorführender

Präsentationsnotizen

Similar….

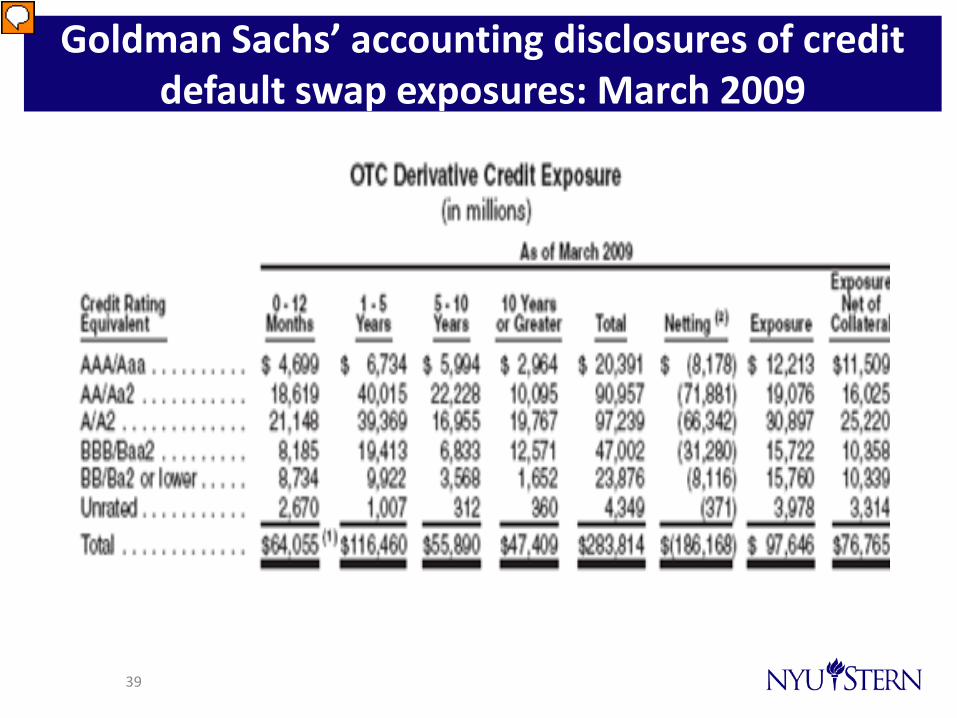

Goldman Sachs’ accounting disclosures of credit default swap exposures: March 2009

39

Vorführender

Präsentationsnotizen

Similar….

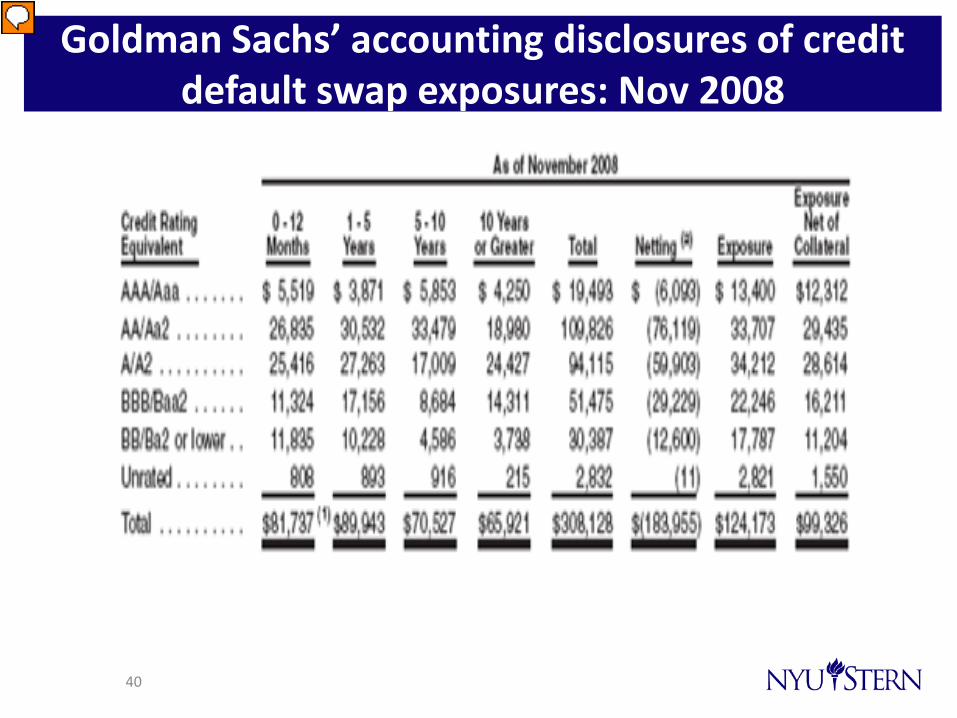

Goldman Sachs’ accounting disclosures of credit default swap exposures: Nov 2008

40

Vorführender

Präsentationsnotizen

Somewhat better…

Citigroup’s accounting disclosures ofcredit default swap exposures (Sep 2009)

41

Vorführender

Präsentationsnotizen

Accounting disclosures very sketchy…

Citigroup’s accounting disclosures ofcredit default swap exposures (June 2009)

42

Vorführender

Präsentationsnotizen

Ditto..

Citigroup’s accounting disclosures ofcredit default swap exposures (March 2009)

43

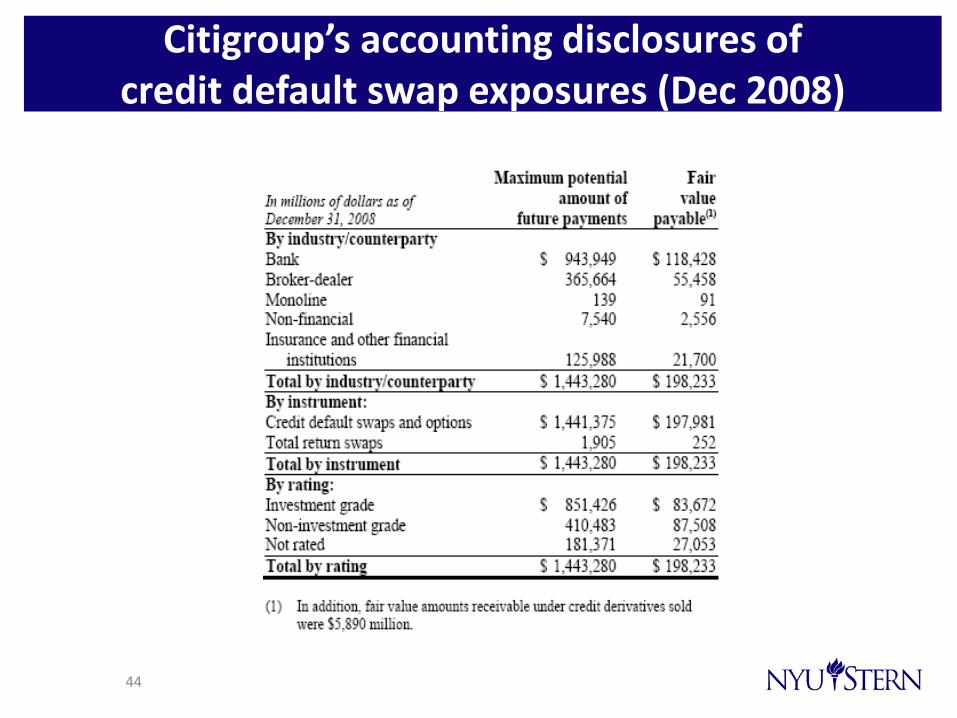

Citigroup’s accounting disclosures ofcredit default swap exposures (Dec 2008)

44

• Key aspect of the reforms

• Increases transparency and reduces risk due to more stringent collateral requirements

• Risk of fragmentation due to multiple CCPs vs. economies of scale and scope of a single CCP

• Risk of failure of the clearinghouse itself – historical precedent

• Need for Fed support through “lender of last resort” access, despite moral hazard

• Better to focus on one central place for fragility rather than multiple fragmented places as happened in 2008

Clearinghouses (CCPs) and Systemic Risk

45

Vorführender

Präsentationsnotizen

This is an important aspect of the new legislation….forcing more transactions to clearing houses. (CCPs)…

• SEC and CFTC jointly charged with rule-making

• CFTC has 30 rule making areas, each with its own committee

• Ranging from “Definition of Swap Contracts” to “Capital and Margin for Non-banks” to “Position Limits”

• Comments from concerned parties received

• Several groups have published comments and interim rules

• Final rules supposed to be published soon: 360 days after the bill –July 2011

46

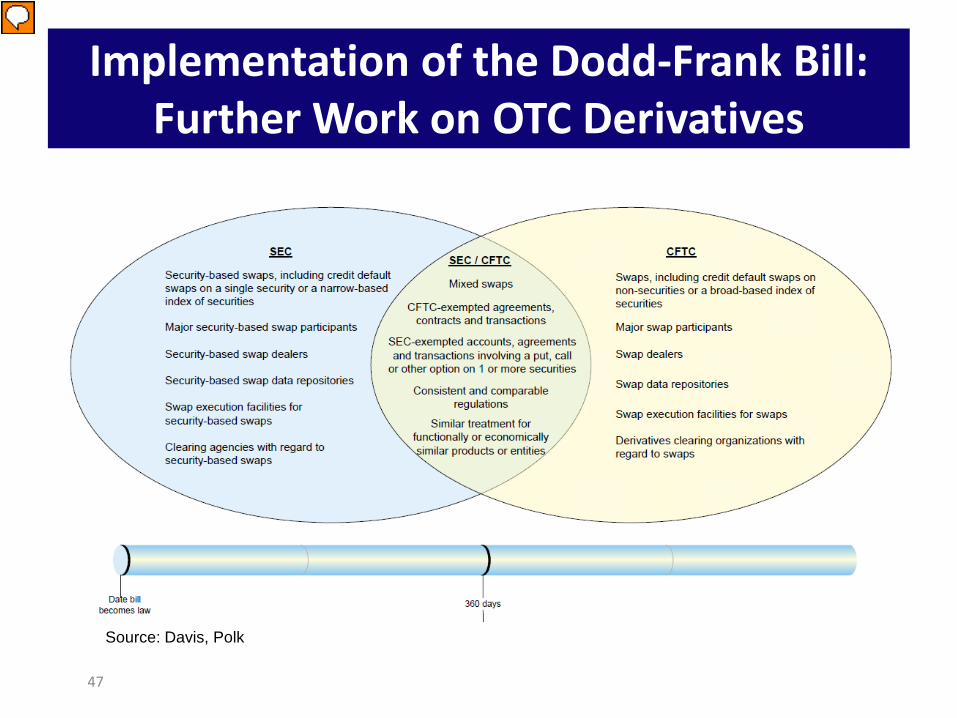

Implementation of the Dodd-Frank Bill: Further Work on OTC Derivatives

Vorführender

Präsentationsnotizen

I now turn to what has happened since the bill was passed. Much of the implementation in the area of OTC derivatives has been delegated to the SEC and CFTC for detailed rule making. A lot of work has been done,but much remains.

47

Implementation of the Dodd-Frank Bill: Further Work on OTC Derivatives

Source: Davis, Polk

Vorführender

Präsentationsnotizen

The joint responsibility of the SEC and CFTC is somewhat strange. The bulk of the work seems to come under the purview of the CFTC, which has grabbed the spotlight, given that the SEC has many more responsibilties, except in the case of securities-based swaps. Since the challenges are more in non-standardized strucutres including credit, the bulk of the oversight would fall under the CFTC. Time line indicates that the rule making should be completed in 360 days, but this is unlikely at this point.

• Example of rule making: Definitions of new swap entities

- Swap dealer

- Major swap participant

- Swap Execution Facility

- Other entitles eg. Futures and commodities brokers, pools etc.

- Swap data repository

48

Implementation of the Dodd-Frank Bill: Further Work on OTC Derivatives

Vorführender

Präsentationsnotizen

Just to give you a flavor of the details of rule making, let me take one example of “Defintions of new swap entities.”

Work on OTC DerivativesurtherWorkon OTC

Derivatives

49

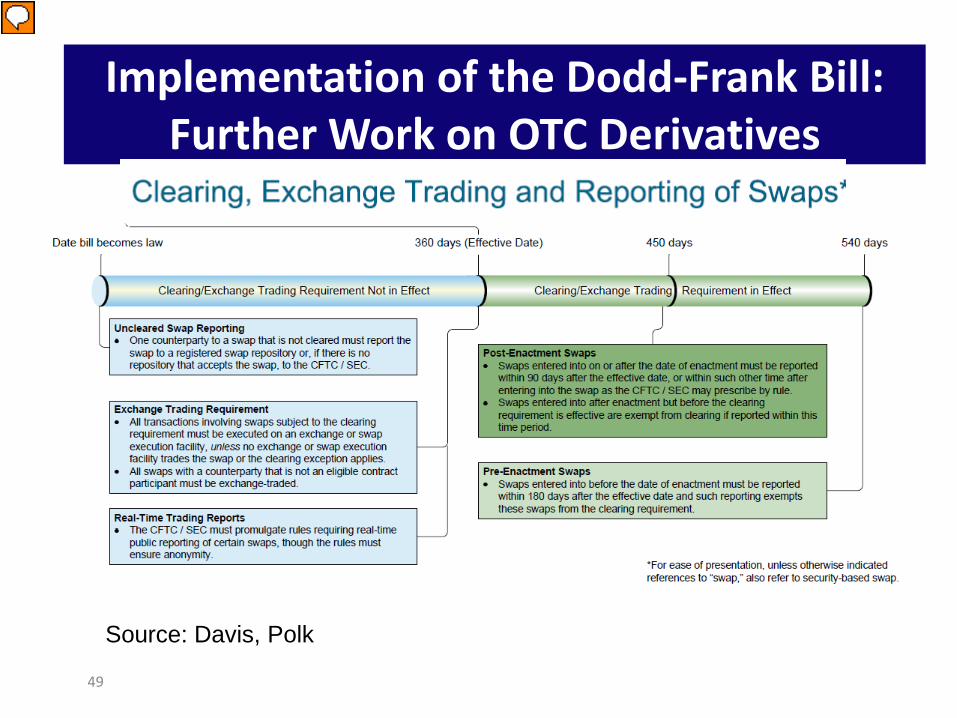

Implementation of the Dodd-Frank Bill: Further Work on OTC Derivatives

Source: Davis, Polk

Vorführender

Präsentationsnotizen

This is the time line for reporting structures. Accordingly tot the bill, the reporting would take effect in 450 days, meaning mid-October 2011. Again, unlikely to happen.

• Draft rules for about half of the 30 areas published

• Deadlines will slip: “What difference does it make if it‘s a month later or six weeks later?,“ - Rep. Barney Frank (D. – Mass.), former Chairman House

• Do the SEC/CFTC have the resources to frame/implement rules?

• Political battle: “…lack of due diligence in the implementation of Dodd-Frank will result in unduly burdensome regulations that will undermine the competitiveness of our domestic financial industry.” – Sen. Orrin Hatch (R. – Utah) , Ranking Member, Senate Finance Committee

• Need for International coordination: “Assurances from partners.”

• The Treasury Department plans to exclude foreign-exchange swaps from key portions of Dodd-Frank, because not doing so could expose the market to greater risk and instability.

Implementation OTC Implementation of the Dodd-Frank Bill: Recent developments

Vorführender

Präsentationsnotizen

What has actually been done so far? Meanwhile, the whole bill has got caught in the political battles of Washington. Discuss.

(CCPs) and Systemic Risk Risklearinghouses (CCPs) and SystemicProspects for the Future

• Consolidation across the world of clearinghouses and exchanges, and potentially also large dealer banks

• Emergence of global transparency platforms and services related to processing of new data on derivatives transactions and positions

• Transition of (some) end-user hedging demand to centralized platforms and exchanges

• Separation of market-making and proprietary trading/asset management positions in large financial institutions

51

Vorführender

Präsentationsnotizen

What is likely to emerge internationally….

Appendices

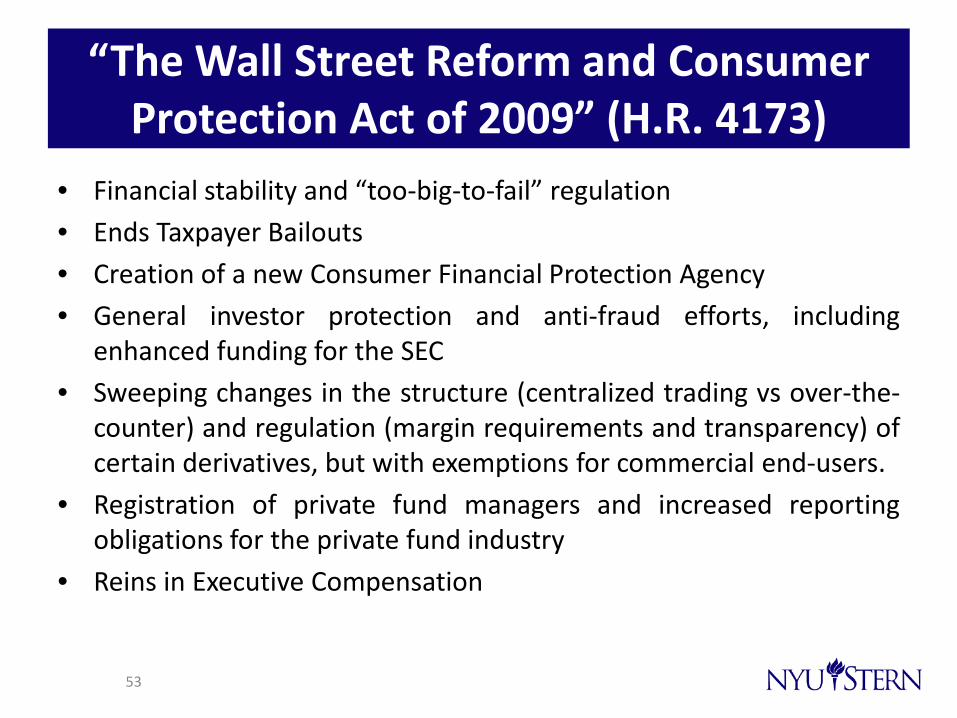

“The Wall Street Reform and Consumer Protection Act of 2009” (H.R. 4173)

• Financial stability and “too-big-to-fail” regulation• Ends Taxpayer Bailouts• Creation of a new Consumer Financial Protection Agency• General investor protection and anti-fraud efforts, including

enhanced funding for the SEC• Sweeping changes in the structure (centralized trading vs over-the-

counter) and regulation (margin requirements and transparency) ofcertain derivatives, but with exemptions for commercial end-users.

• Registration of private fund managers and increased reportingobligations for the private fund industry

• Reins in Executive Compensation

53

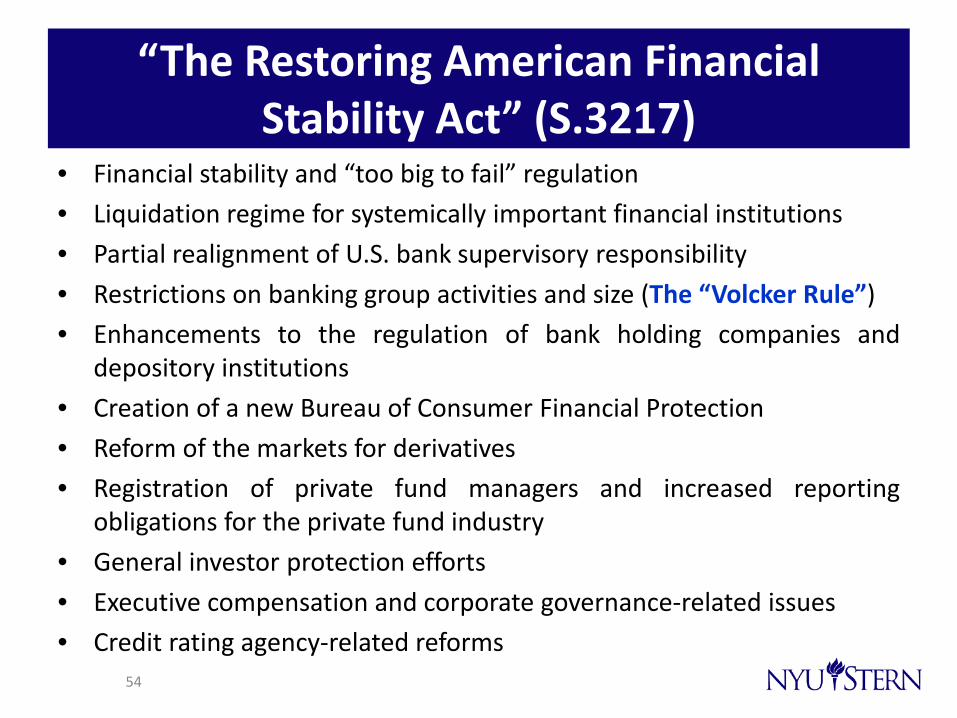

“The Restoring American Financial Stability Act” (S.3217)

• Financial stability and “too big to fail” regulation

• Liquidation regime for systemically important financial institutions

• Partial realignment of U.S. bank supervisory responsibility

• Restrictions on banking group activities and size (The “Volcker Rule”)

• Enhancements to the regulation of bank holding companies anddepository institutions

• Creation of a new Bureau of Consumer Financial Protection

• Reform of the markets for derivatives

• Registration of private fund managers and increased reportingobligations for the private fund industry

• General investor protection efforts

• Executive compensation and corporate governance-related issues

• Credit rating agency-related reforms54

“Wall Street Transparency and Accountability Act of 2010” (“Lincoln Bill”)

• Mandatory clearing and exchange trading for certain transactions

• Registration and regulatory requirements for derivatives dealers and major market participants

• capital and margin requirements for cleared and uncleared transactions

• Segregation requirements for collateral

• Position limits

• Split regulatory responsibility between the CFTC and SEC

• Goes beyond the House and Dodd bills: – Prohibits U.S. federal assistance (including Federal Reserve advances and access to the

discount window as well as emergency liquidity or debt guarantee program assistance) to any dealer, major market participant, exchange or clearing organization in connection with derivatives activities or other activities.

– Broad new enforcement authorities that could apply to a range of derivatives market activities.

– Unlike the House bill, the bill would also cover foreign exchange forward and swap transactions absent a specific exemption.55