Outlook for Renewable Energy Marketeneken.ieej.or.jp/data/6927.pdf-term Outlook:Germany Renewable...

20

IEEJ:September 2016 © IEEJ2016 Outlook for Renewable Energy Market The Institute of Energy Economics, Japan Yoshiaki Shibata Senior Economist, Manager, New and Renewable Energy Group, New and Renewable Energy & International Cooperation Unit 423 rd Forum on Research Works on July 26, 2016

Transcript of Outlook for Renewable Energy Marketeneken.ieej.or.jp/data/6927.pdf-term Outlook:Germany Renewable...

IEEJ:September 2016 © IEEJ2016

Outlook for Renewable Energy Market

The Institute of Energy Economics, Japan

Yoshiaki Shibata

Senior Economist, Manager, New and Renewable Energy Group, New and Renewable Energy & International Cooperation Unit

423rd Forum on Research Works on July 26, 2016

IEE

J ©

201

6

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

200

5

200

6

200

7

200

8

200

9

201

0

201

1

201

2

201

3

201

4

201

5

GW

Marine

Solar

Wind

Geothermal

Biomass

Hydro

0%

5%

10%

15%

20%

25%

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

200

5

200

6

200

7

200

8

200

9

201

0

201

1

201

2

201

3

201

4

201

5

TWh

World Renewable Energy Expansion

Renewable energy power generation capacity exceeded 1,800 GW in 2015. Renewable

power generation accounted for 24% of total power generation (the share includes 17

percentage points for hydro, 4 points for wind and 1 point for solar energy).

1 Source: Estimated from IEA, IRENA, REN21

Note: Including large-scale hydro power generation, excluding pumped-storage power generation

Accumulated capacity

Share of total power

generation (right scale)

Power generation

IEEJ:September 2016 © IEEJ2016

IEE

J ©

201

6

0

20

40

60

80

100

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

GW/year

Others

Africa

Middle East

Oceania

Asia

Non-OECD Europe

OECD Europe

Latin America

North America

0

10

20

30

40

50

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

GW/year

Others

Africa

Middle East

Oceania

Asia

Non-OECD Europe

OECD Europe

Latin America

North America

31

8

6

3 01

0

20

40

60

80

100

120

140

160

180

GW

Δ2015

Δ2014

2013

151

10

7

0

4

0

10

20

30

40

50

60

GW

Δ2015

Δ2014

2013

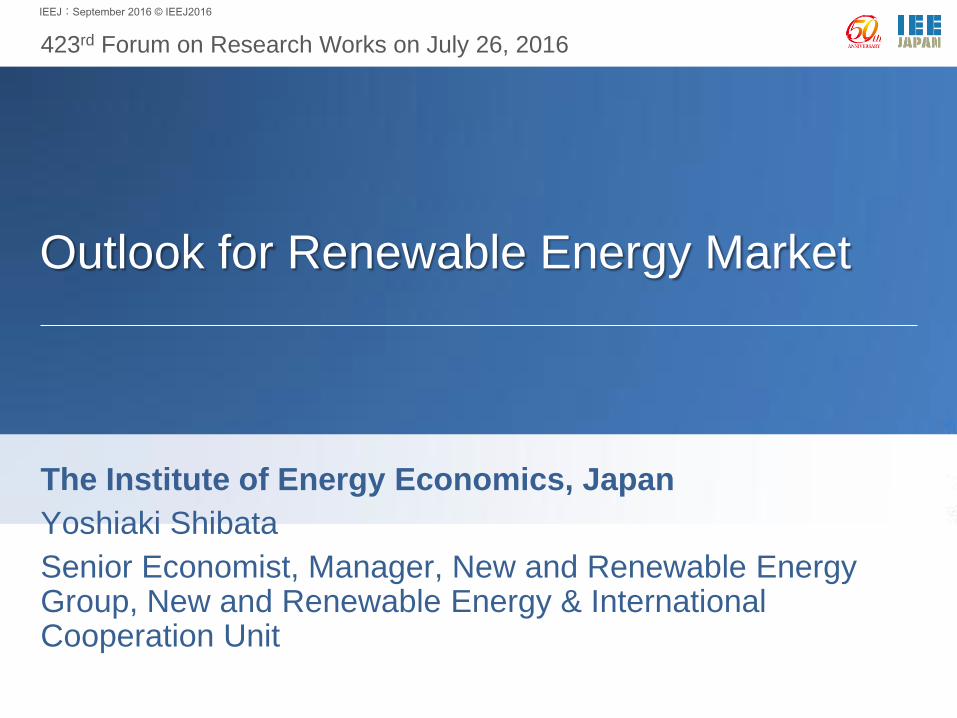

Wind and Solar PV Expansion by Region

The market is shifting from Europe to Asia and North America. China is

accelerating wind and solar PV expansion, being followed by the United States.

The expansion is decelerating in Europe going ahead with institutional reform.

2 Source: Estimated from IRENA, REN21

Capacity expansion by region Accumulated capacity in major countries

Global total growth:

63GW

Wind

Solar PV

Wind Solar PV Global total growth:

47GW

IEEJ:September 2016 © IEEJ2016

IEE

J ©

201

6

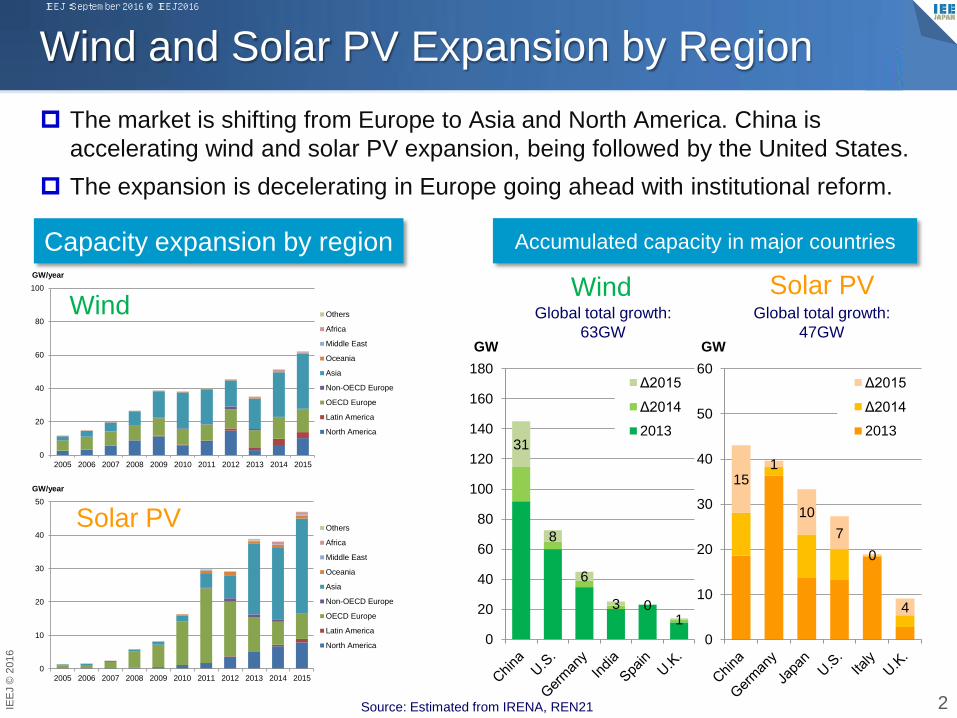

Solar PV Price Fall and Intensifying Competition

Solar PV prices have fallen rapidly in the past five years.

In recent years, bid prices slipped below US10¢/kWh for many deals.

Solar PV expansion is intensifying in developing countries.

3

Source: IRENA

PV module cost trend Recent bid prices for solar PV

Source: Prepared from media reports

Note: Megasolar projects. Attention must be paid to U.S.

projects that may include auxiliary facilities.

Country/region Month Bid price

(US¢/kWh)

Dubai January 2015 5.84

India July 2015 7.95

India July 2015 8.27

Nevada July 2015 3.87

Texas August 2015 4.00

India November 2015 7.29

Mexico March 2016 3.60

Dubai May 2016 2.99

IEEJ:September 2016 © IEEJ2016

IEE

J ©

201

6

0

100

200

300

400

500

600

700

800

900

1000

2010 2011 2012 2013 2014 2015

TWh PV Germany

Italy

Spain

France

U.K.

Others

Wind Germany

Italy

Spain

Sweden

France

Others

0

100

200

300

400

500

600

700

800

900

1000

2010 2011 2012 2013 2014 2015

TWh

Steam coal Germany

U.K.

Poland

Spain

Italy

Others

Brown coal Germany

Poland

Czech Republic

Greece

Bulgaria Others0

100

200

300

400

500

600

700

800

900

1000

2010 2011 2012 2013 2014 2015

TWh

Italy

Others

Spain

U.K.

Germany

Netherlands

768 485

679923

0

500

1000

1500

2000

2500

3000

3500

4000

2010 2011 2012 2013 2014 2015

TWh

Nuclear

Coal

Natural gas

Renewables

3,2043,337

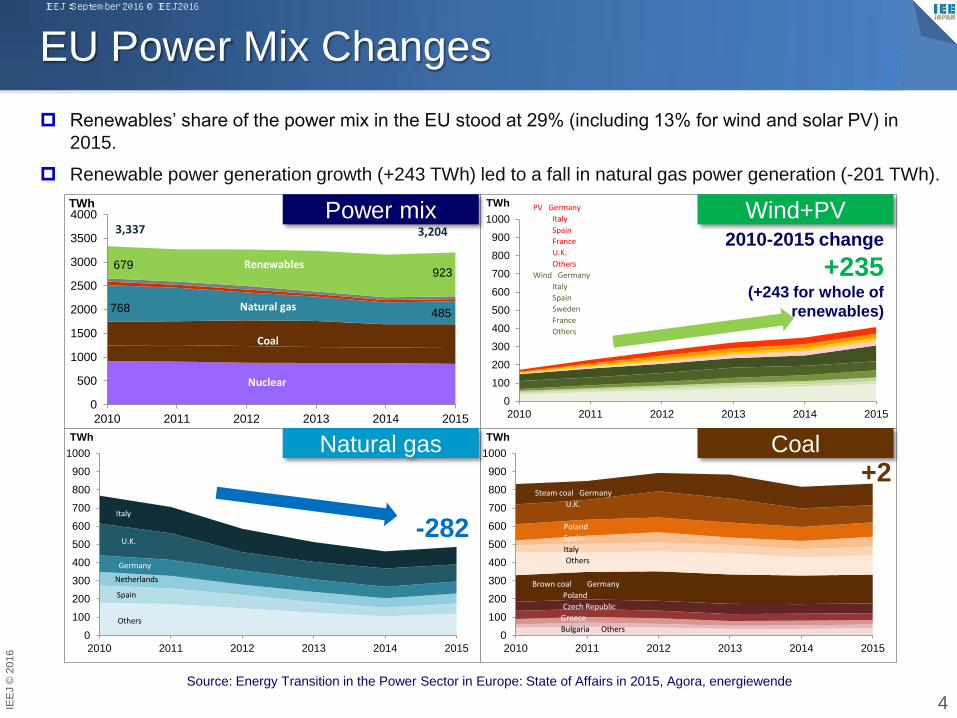

EU Power Mix Changes

Renewables’ share of the power mix in the EU stood at 29% (including 13% for wind and solar PV) in

2015.

Renewable power generation growth (+243 TWh) led to a fall in natural gas power generation (-201 TWh).

4

Wind+PV

Coal Natural gas

Source: Energy Transition in the Power Sector in Europe: State of Affairs in 2015, Agora, energiewende

2010-2015 change

+235 (+243 for whole of

renewables)

-282

+2

Power mix

IEEJ:September 2016 © IEEJ2016

IEE

J ©

201

6

8

-32

-76

-3

30

3

17

8 2

-100

-80

-60

-40

-20

0

20

40

TWh

-49

10

-30

-3

50

-2

15

27

1

-60

-40

-20

0

20

40

60

TWh

Electricity source shift: Germany, U.K.

Germany Renewables’ share of the power mix stood at 30.1% (19%

for wind and solar PV) in 2015 (their share of total power

consumption stood at 32.6%).

In the past five years, wind and solar PV power generation

expanded substantially, with natural gas power generation

falling substantially.

5

U.K. Renewables’ share of the power mix stood at 25.7% (14%

for wind and solar PV) in 2015.

While power demand declined, wind and biomass power

generation increased substantially in the past five years,

with natural gas and coal power generation decreasing

substantially.

Sources: Energy Trends, DECC, etc. Sources: AGEB, etc.

Changes by electricity source

(2010⇒2015)

Changes by electricity source

(2010⇒2015)

IEEJ:September 2016 © IEEJ2016

IEE

J ©

201

6

0

1,000

2,000

3,000

4,000

5,000

2013 2014 2015 2016 2017

MWOnshore wind power generation

5000

1,000

2,000

3,000

4,000

2013 2014 2015 2016 2017

MWSolar PV

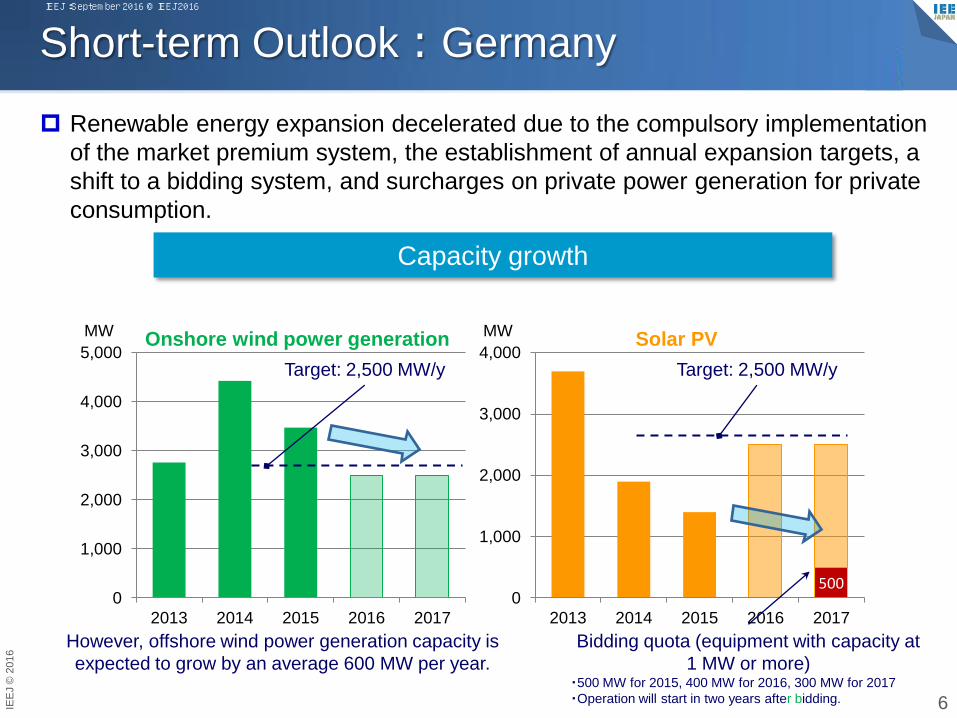

Short-term Outlook:Germany

Renewable energy expansion decelerated due to the compulsory implementation

of the market premium system, the establishment of annual expansion targets, a

shift to a bidding system, and surcharges on private power generation for private

consumption.

6

Capacity growth

Target: 2,500 MW/y Target: 2,500 MW/y

Bidding quota (equipment with capacity at

1 MW or more) ・500 MW for 2015, 400 MW for 2016, 300 MW for 2017

・Operation will start in two years after bidding.

However, offshore wind power generation capacity is

expected to grow by an average 600 MW per year.

IEEJ:September 2016 © IEEJ2016

IEE

J ©

201

6

0

500

1,000

1,500

2,000

2013 2014 2015 2016 2017

MW Onshore wind power generation

0

1,000

2,000

3,000

4,000

2013 2014 2015 2016 2017

MW Solar PV

0

500

1,000

1,500

2,000

2013 2014 2015 2016 2017

MW Offshore wind power generation

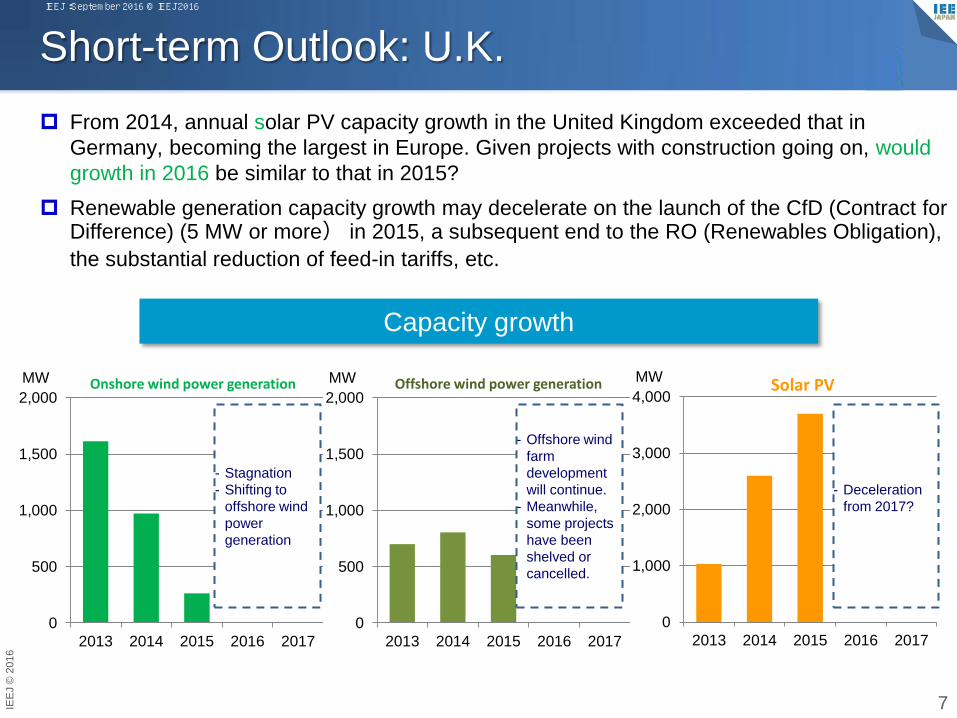

Short-term Outlook: U.K.

From 2014, annual solar PV capacity growth in the United Kingdom exceeded that in

Germany, becoming the largest in Europe. Given projects with construction going on, would

growth in 2016 be similar to that in 2015?

Renewable generation capacity growth may decelerate on the launch of the CfD (Contract for Difference) (5 MW or more) in 2015, a subsequent end to the RO (Renewables Obligation),

the substantial reduction of feed-in tariffs, etc.

7

Capacity growth

- Deceleration

from 2017?

- Offshore wind

farm

development

will continue.

- Meanwhile,

some projects

have been

shelved or

cancelled.

- Stagnation

- Shifting to

offshore wind

power

generation

IEEJ:September 2016 © IEEJ2016

IEE

J ©

201

6

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

2001 2004 2007 2010 2013

MWOnshore power generation

-10

-491

349

-9

96

-9

8 25 1 2

-600

-500

-400

-300

-200

-100

0

100

200

300

400

TWh

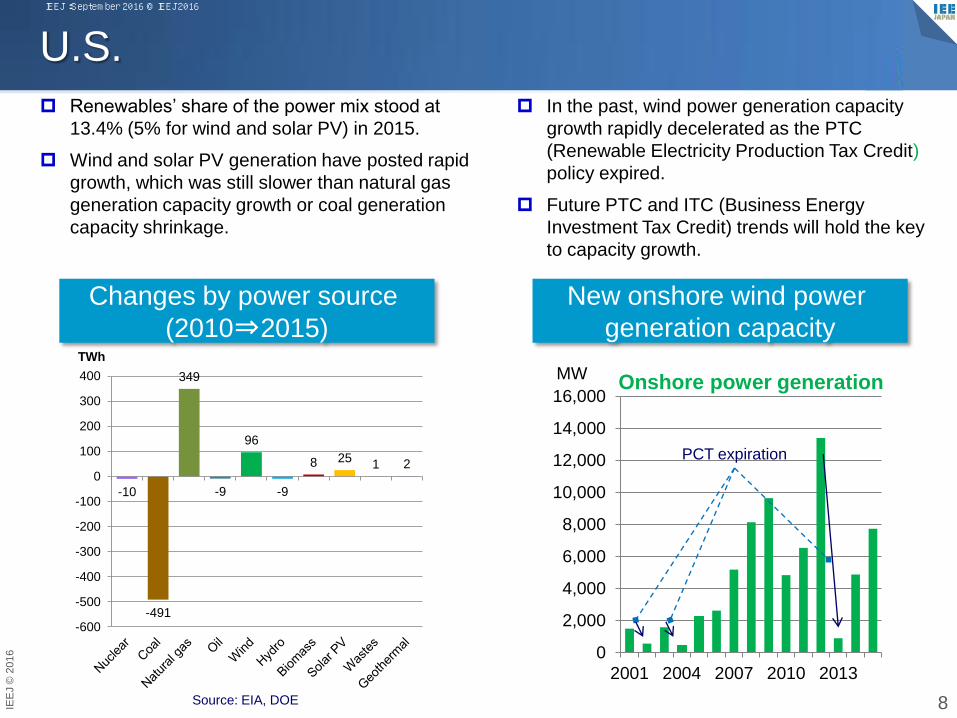

U.S.

Renewables’ share of the power mix stood at

13.4% (5% for wind and solar PV) in 2015.

Wind and solar PV generation have posted rapid

growth, which was still slower than natural gas

generation capacity growth or coal generation

capacity shrinkage.

8 Source: EIA, DOE

In the past, wind power generation capacity

growth rapidly decelerated as the PTC

(Renewable Electricity Production Tax Credit)

policy expired.

Future PTC and ITC (Business Energy

Investment Tax Credit) trends will hold the key

to capacity growth.

Changes by power source

(2010⇒2015)

New onshore wind power

generation capacity

PCT expiration

IEEJ:September 2016 © IEEJ2016

IEE

J ©

201

6

Summary of World Trends

Developed countries After driving renewable energy expansion, major European countries,

though expected to expand renewable energy further over a long term,

are exploring how best to reduce the burden on consumers and

integrate renewable energy into the electricity market to break away

from the FIT system.

Amid the institutional reform, renewable energy expansion will

decelerate over a short term.

Developing countries

Solar PV is expanding in developing countries as well thanks to cost

cuts and competitive bidding. The elimination of subsidies for

traditional energy sources also supports renewable energy expansion.

However, developing countries are required to address a great

number of challenges including grid stabilization, the rising burden on

consumers under the FIT system and an industrial shakeout under

excessive competition. 9

IEEJ:September 2016 © IEEJ2016

IEE

J ©

201

6

0

10

20

30

40

50

60

70

80

90

100

7 10 1 4 7 10 1 4 7 10 1 4 7 10 1

2012 2013 2014 2015 2016

GW Small/medium-scale hydro

Geothermal

Biomass

Wind

Non-residential solar PV

Residential solar PV

0

5

10

15

20

25

30

7 10 1 4 7 10 1 4 7 10 1 4 7 10 1

2012 2013 2014 2015 2016

GW Small/medium-scale hydro

Geothermal

Biomass

Wind

Non-residential solar PV

Residential solar PV

0

10

20

30

40

50

Solar PV(non-residential)

Wind Solar PV(residential)

Others

Trilli

on y

en Approved

capacity

Approvedcapacity inoperation

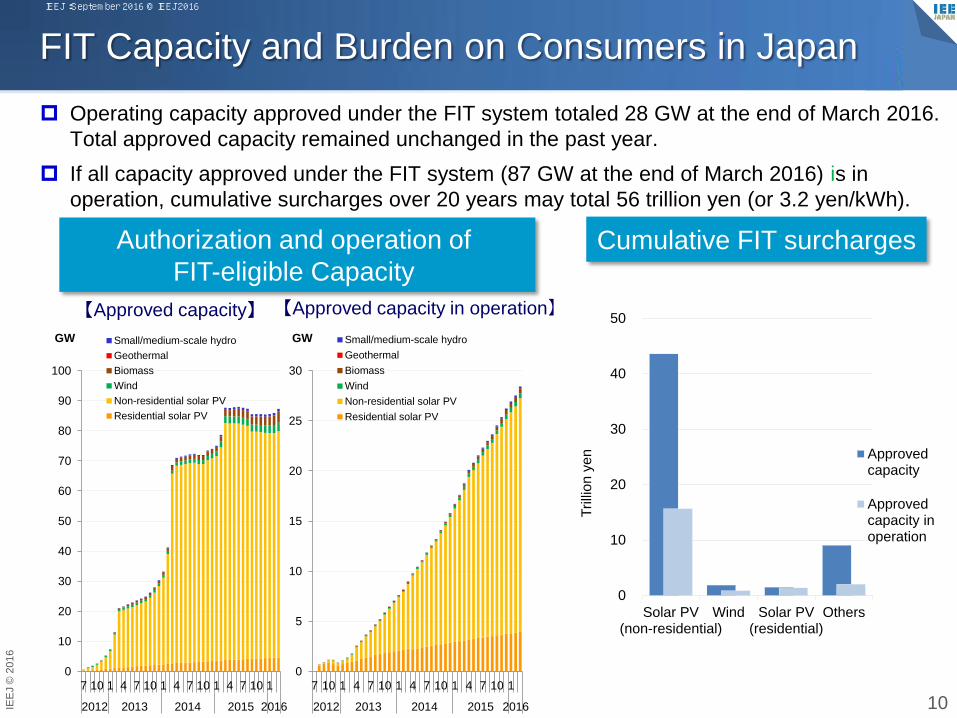

FIT Capacity and Burden on Consumers in Japan

Operating capacity approved under the FIT system totaled 28 GW at the end of March 2016.

Total approved capacity remained unchanged in the past year.

If all capacity approved under the FIT system (87 GW at the end of March 2016) is in

operation, cumulative surcharges over 20 years may total 56 trillion yen (or 3.2 yen/kWh).

10

Cumulative FIT surcharges Authorization and operation of

FIT-eligible Capacity

【Approved capacity】 【Approved capacity in operation】

IEEJ:September 2016 © IEEJ2016

IEE

J ©

201

6

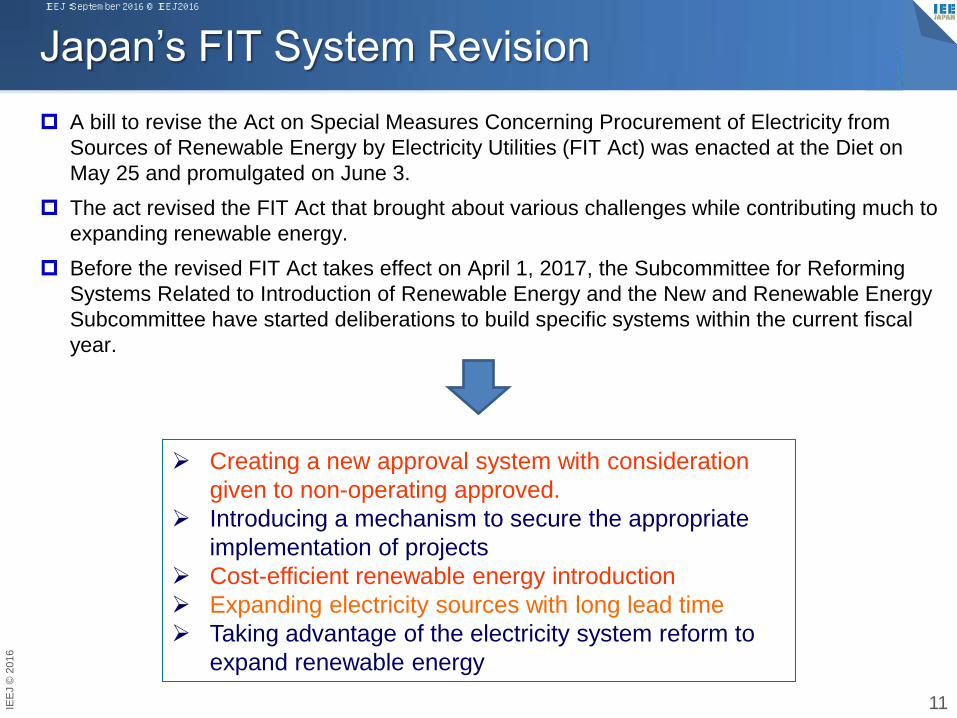

Japan’s FIT System Revision

A bill to revise the Act on Special Measures Concerning Procurement of Electricity from

Sources of Renewable Energy by Electricity Utilities (FIT Act) was enacted at the Diet on

May 25 and promulgated on June 3.

The act revised the FIT Act that brought about various challenges while contributing much to

expanding renewable energy.

Before the revised FIT Act takes effect on April 1, 2017, the Subcommittee for Reforming

Systems Related to Introduction of Renewable Energy and the New and Renewable Energy

Subcommittee have started deliberations to build specific systems within the current fiscal

year.

11

Creating a new approval system with consideration

given to non-operating approved.

Introducing a mechanism to secure the appropriate

implementation of projects

Cost-efficient renewable energy introduction

Expanding electricity sources with long lead time

Taking advantage of the electricity system reform to

expand renewable energy

IEEJ:September 2016 © IEEJ2016

IEE

J ©

201

6

35

14

2629

0

5

10

15

20

25

30

35

40

Approved Operating

GW

40

9

1416

0

5

10

15

20

25

30

35

40

45

Approved Operating

GW

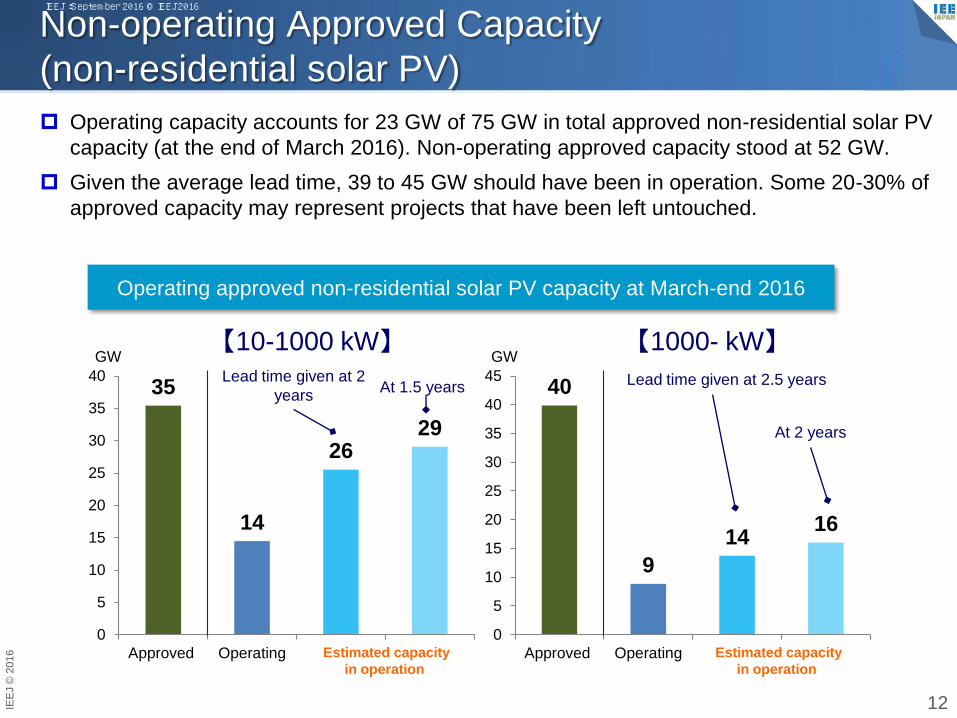

Non-operating Approved Capacity

(non-residential solar PV)

Operating capacity accounts for 23 GW of 75 GW in total approved non-residential solar PV

capacity (at the end of March 2016). Non-operating approved capacity stood at 52 GW.

Given the average lead time, 39 to 45 GW should have been in operation. Some 20-30% of

approved capacity may represent projects that have been left untouched.

12

Operating approved non-residential solar PV capacity at March-end 2016

【10-1000 kW】 【1000- kW】 Lead time given at 2

years Lead time given at 2.5 years

Estimated capacity

in operation

Estimated capacity

in operation

At 1.5 years

At 2 years

IEEJ:September 2016 © IEEJ2016

IEE

J ©

201

6

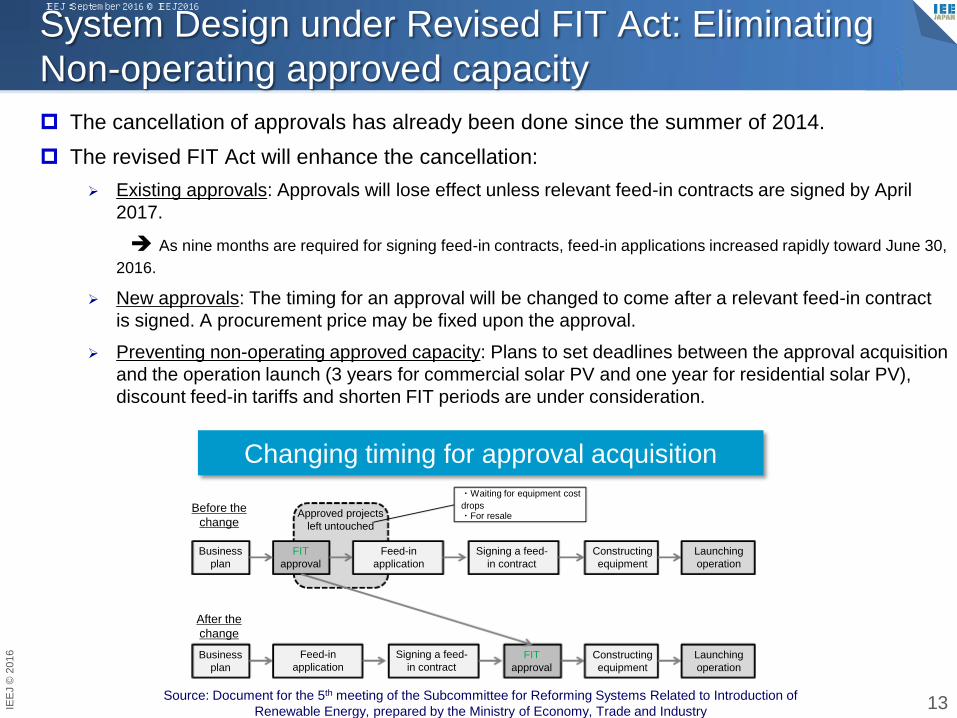

System Design under Revised FIT Act: Eliminating

Non-operating approved capacity

The cancellation of approvals has already been done since the summer of 2014.

The revised FIT Act will enhance the cancellation:

Existing approvals: Approvals will lose effect unless relevant feed-in contracts are signed by April

2017.

As nine months are required for signing feed-in contracts, feed-in applications increased rapidly toward June 30,

2016.

New approvals: The timing for an approval will be changed to come after a relevant feed-in contract

is signed. A procurement price may be fixed upon the approval.

Preventing non-operating approved capacity: Plans to set deadlines between the approval acquisition

and the operation launch (3 years for commercial solar PV and one year for residential solar PV),

discount feed-in tariffs and shorten FIT periods are under consideration.

13 Source: Document for the 5th meeting of the Subcommittee for Reforming Systems Related to Introduction of

Renewable Energy, prepared by the Ministry of Economy, Trade and Industry

Changing timing for approval acquisition

Business

plan

FIT

approval

Feed-in

application

Signing a feed-

in contract

Constructing

equipment

Launching

operation

Launching

operation

FIT

approval

Approved projects

left untouched

・Waiting for equipment cost

drops ・For resale

Before the

change

After the

change

Business

plan

Feed-in

application

Signing a feed-

in contract Constructing

equipment

IEEJ:September 2016 © IEEJ2016

IEE

J ©

201

6

0

5

10

15

20

25

30

35

40

45

2012 2013 2014 2015 2016

Yen/kWh

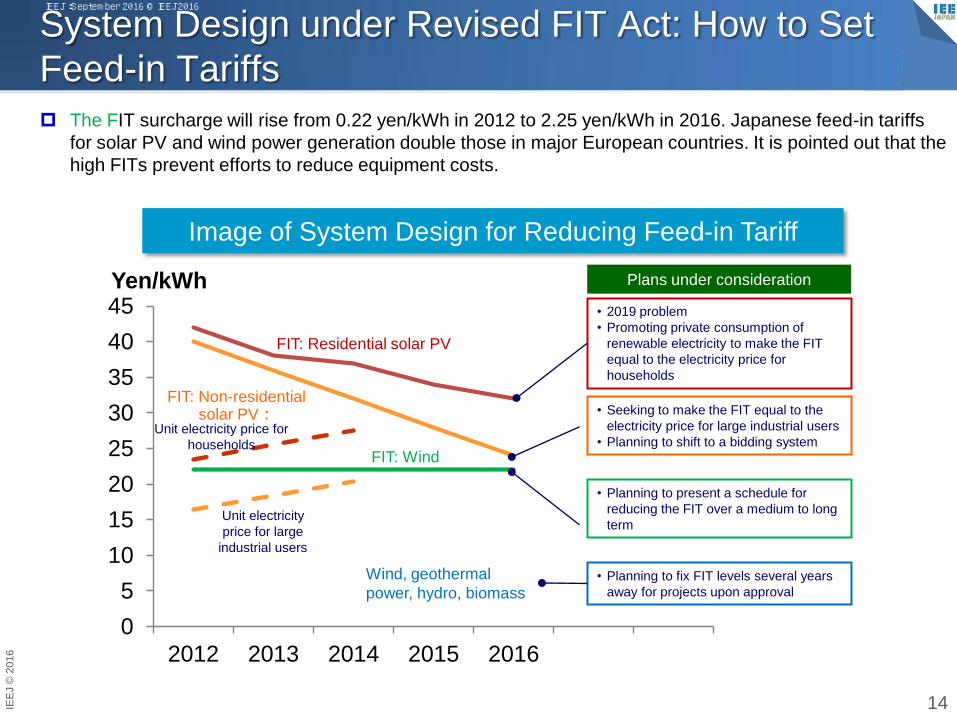

System Design under Revised FIT Act: How to Set

Feed-in Tariffs

The FIT surcharge will rise from 0.22 yen/kWh in 2012 to 2.25 yen/kWh in 2016. Japanese feed-in tariffs

for solar PV and wind power generation double those in major European countries. It is pointed out that the

high FITs prevent efforts to reduce equipment costs.

14

Image of System Design for Reducing Feed-in Tariff

FIT: Wind

FIT: Residential solar PV

FIT: Non-residential solar PV:

Unit electricity

price for large

industrial users

Unit electricity price for

households

• 2019 problem

• Promoting private consumption of

renewable electricity to make the FIT

equal to the electricity price for

households

• Seeking to make the FIT equal to the

electricity price for large industrial users

• Planning to shift to a bidding system

• Planning to present a schedule for

reducing the FIT over a medium to long

term

• Planning to fix FIT levels several years

away for projects upon approval

Wind, geothermal

power, hydro, biomass

Plans under consideration

IEEJ:September 2016 © IEEJ2016

IEE

J ©

201

6

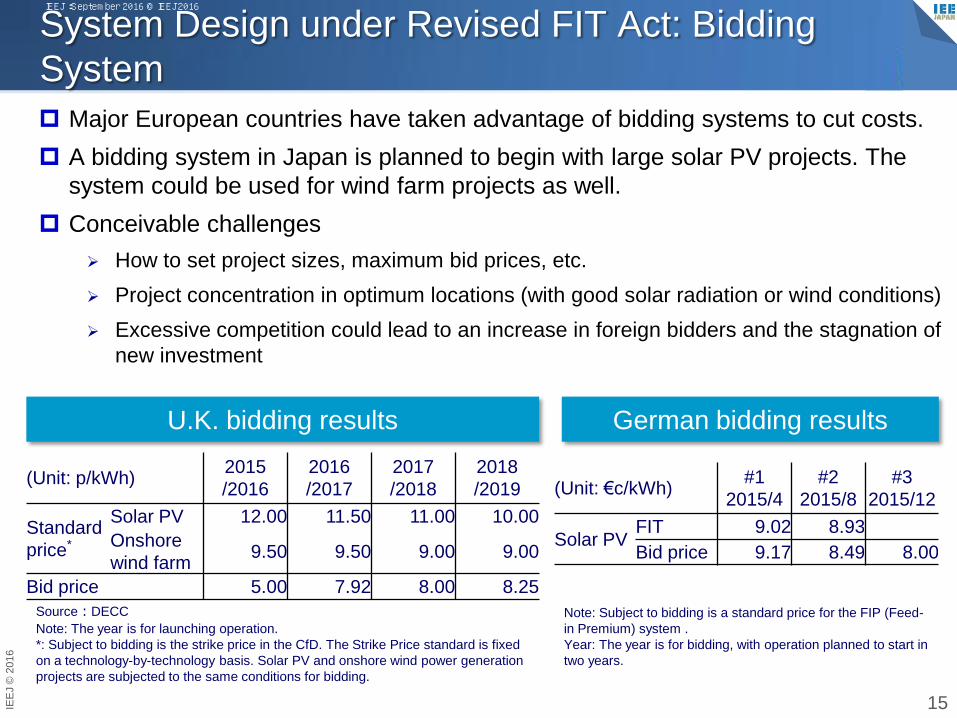

System Design under Revised FIT Act: Bidding

System

Major European countries have taken advantage of bidding systems to cut costs.

A bidding system in Japan is planned to begin with large solar PV projects. The

system could be used for wind farm projects as well.

Conceivable challenges

How to set project sizes, maximum bid prices, etc.

Project concentration in optimum locations (with good solar radiation or wind conditions)

Excessive competition could lead to an increase in foreign bidders and the stagnation of

new investment

15

U.K. bidding results

(Unit: p/kWh) 2015

/2016

2016

/2017

2017

/2018

2018

/2019

Standard

price*

Solar PV 12.00 11.50 11.00 10.00

Onshore

wind farm 9.50 9.50 9.00 9.00

Bid price 5.00 7.92 8.00 8.25

(Unit: €c/kWh) #1

2015/4

#2

2015/8

#3

2015/12

Solar PV FIT 9.02 8.93

Bid price 9.17 8.49 8.00

Source:DECC

Note: The year is for launching operation.

*: Subject to bidding is the strike price in the CfD. The Strike Price standard is fixed

on a technology-by-technology basis. Solar PV and onshore wind power generation

projects are subjected to the same conditions for bidding.

German bidding results

Note: Subject to bidding is a standard price for the FIP (Feed-

in Premium) system .

Year: The year is for bidding, with operation planned to start in

two years.

IEEJ:September 2016 © IEEJ2016

IEE

J ©

201

6

0

20

40

60

80

100

120

140

160

180

200

China U.S. Germany Japan India Italy Spain

GW

Solar

Wind

Geothermal

Biomass

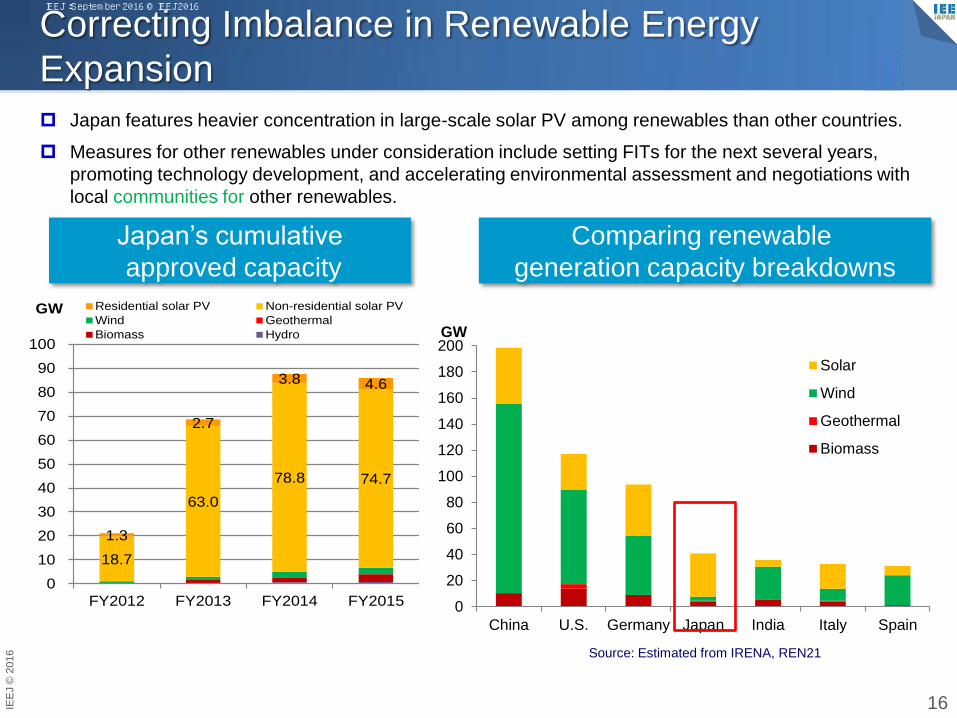

18.7

63.0

78.8 74.7

1.3

2.7

3.8 4.6

0

10

20

30

40

50

60

70

80

90

100

FY2012 FY2013 FY2014 FY2015

GW Residential solar PV Non-residential solar PV

Wind Geothermal

Biomass Hydro

Correcting Imbalance in Renewable Energy

Expansion

Japan features heavier concentration in large-scale solar PV among renewables than other countries.

Measures for other renewables under consideration include setting FITs for the next several years,

promoting technology development, and accelerating environmental assessment and negotiations with

local communities for other renewables.

16

Comparing renewable

generation capacity breakdowns

Source: Estimated from IRENA, REN21

Japan’s cumulative

approved capacity

IEEJ:September 2016 © IEEJ2016

IEE

J ©

201

6

0

20

40

60

80

100

120

140

0

50

100

150

200

250

300

Jan-1

2

Apr-

12

Jul-1

2

Oct-

12

Jan-1

3

Apr-

13

Jul-1

3

Oct-

13

Jan-1

4

Apr-

14

Jul-1

4

Oct-

14

Jan-1

5

Apr-

15

Jul-1

5

Oct-

15

Jan-1

6

Million units

Yen/Ah

Topic: Storage Battery Trends

In March 2016, one of the world’s largest NaS sodium-sulfur batteries (with

capacity at 300 MWh) started operation (on the grid side) in Buzen, Kyushu.

Prices of lithium-ion batteries for electric vehicles have declined rapidly. Storage

batteries on the demand side are expected to help stabilize the grid.

17

Source: Björn Nykvist and Måns Nilsson, ”Rapidly falling costs of battery packs for electric vehicles,” 2015 Source: Estimated from machinery production

statistics

World Japan

Unit price: Down 60% in

past 4 years

Sales

volume

Unit price

Lithium-ion battery (for vehicles) price trends

IEEJ:September 2016 © IEEJ2016

IEE

J ©

201

6

7.3

15.9

24.2

30.8

37.7

6.6

7.48.3

9.09.7

3.0 3.8 3.8

2.93.6

3.80

10

20

30

40

2011 2012 2013 2014 2015 2016 2017

GW

Fiscal year end

Solar PV(Non-residential)

Solar PV(rediential)

Wind

Biomass

Renewable Power Generation Capacity Outlook

Renewable power generation capacity at the end of FY2017 is projected at 65 GW (including 38GW for

non-residential solar PV), accounting for more than 10% of total power generation.

Additional capacity approvals for renewables other than solar PV will be required to meet the best energy

mix for 2030.

18

Renewable power generation capacity

8.5GW/年

7.0GW/year (GW) Additional capacity

required to be in

operation by 2030

Non-operating

approved capacity

(at March-end 2016)

Solar PV 31.5 52.7

Wind 7.0 2.4

Biomass 3.1~4.4 3.2

Geothermal 0.8~0.9 0.1

Small/mediu

m-scale

hydro

1.2~1.9 0.6

Capacity required to meet

the best energy mix for 2030

IEEJ:September 2016 © IEEJ2016

IEE

J ©

201

6

Summary of Renewable Energy Trends in Japan

and Challenges

Short-term outlook

Approved capacity is expected to decline under traditional measures and the enhancement of measures against non-operating approved capacity under the revised FIT Act.

In line with the decline, Japan’s renewable energy expansion will decelerate over a short term.

Challenges

How to design a bidding system and a schedule for reducing FITs holds the key to maintaining an appropriate pace for renewable energy expansion.

Japan features a greater imbalance among renewables than other countries and is required to enhance wind and geothermal power generation.

19

IEEJ:September 2016 © IEEJ2016

Contact :[email protected]

![Resources [renewable and non renewable]](https://static.fdocuments.us/doc/165x107/55643cd7d8b42ad3308b522b/resources-renewable-and-non-renewable.jpg)