Analysis of Customer’s Decision to Choose Sharia Banking ...

1

INDONESIA’S ISLAMIC BANKING & FINANCE

DEVELOPMENT AND ROLE OF SOVEREIGN

SUKUK

Edy Setiadi Executive Director, Islamic Banking Department, Bank Indonesia

IIFM Industry Seminar on Islamic Capital and Money Market

Bahrain, December 3th 2013

OUTLINE

• Indonesia’s Economic and Financial

Profile

• Indonesia Islamic Banking Policy and

Direction

• Indonesia’s Sovereign Sukuk

• Indonesian Islamic Finance : Expecting

for the future

2

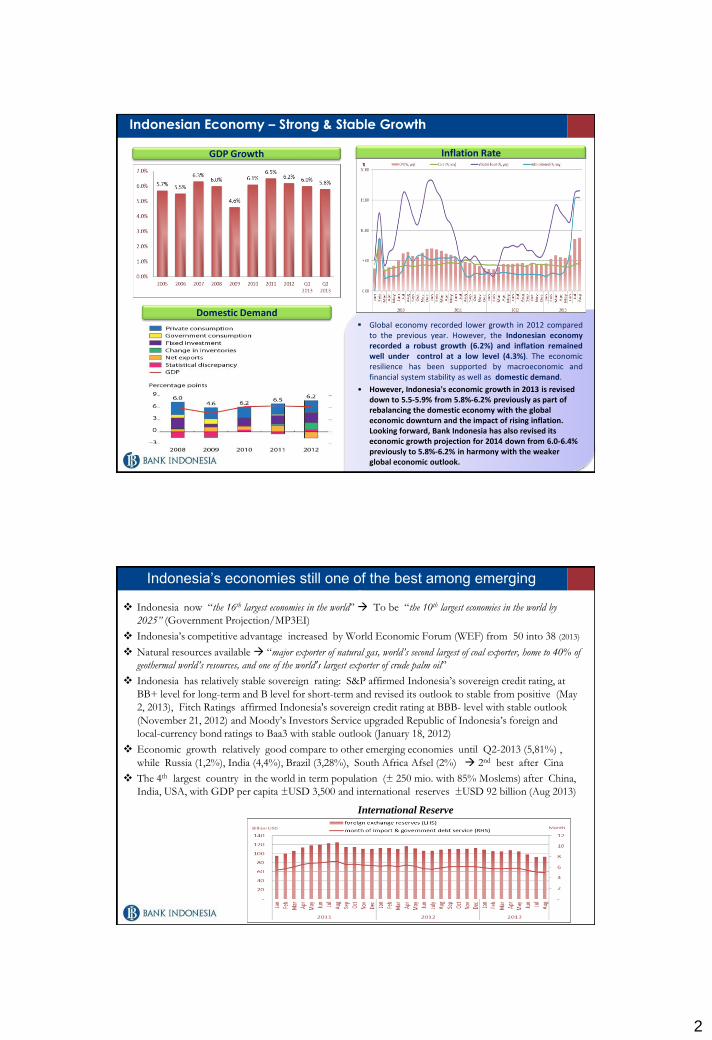

Indonesian Economy – Strong & Stable Growth

Global economy recorded lower growth in 2012 compared to the previous year. However, the Indonesian economy recorded a robust growth (6.2%) and inflation remained well under control at a low level (4.3%). The economic resilience has been supported by macroeconomic and financial system stability as well as domestic demand.

• However, Indonesia's economic growth in 2013 is revised down to 5.5-5.9% from 5.8%-6.2% previously as part of rebalancing the domestic economy with the global economic downturn and the impact of rising inflation. Looking forward, Bank Indonesia has also revised its economic growth projection for 2014 down from 6.0-6.4% previously to 5.8%-6.2% in harmony with the weaker global economic outlook.

GDP Growth Inflation Rate

Domestic Demand

Indonesia now “the 16th largest economies in the world” To be “the 10th largest economies in the world by

2025” (Government Projection/MP3EI)

Indonesia’s competitive advantage increased by World Economic Forum (WEF) from 50 into 38 (2013)

Natural resources available “major exporter of natural gas, world’s second largest of coal exporter, home to 40% of

geothermal world’s resources, and one of the world's largest exporter of crude palm oil”

Indonesia has relatively stable sovereign rating: S&P affirmed Indonesia’s sovereign credit rating, at

BB+ level for long-term and B level for short-term and revised its outlook to stable from positive (May

2, 2013), Fitch Ratings affirmed Indonesia's sovereign credit rating at BBB- level with stable outlook

(November 21, 2012) and Moody’s Investors Service upgraded Republic of Indonesia’s foreign and

local-currency bond ratings to Baa3 with stable outlook (January 18, 2012)

Economic growth relatively good compare to other emerging economies until Q2-2013 (5,81%) ,

while Russia (1,2%), India (4,4%), Brazil (3,28%), South Africa Afsel (2%) 2nd best after Cina

The 4th largest country in the world in term population (± 250 mio. with 85% Moslems) after China,

India, USA, with GDP per capita ±USD 3,500 and international reserves ±USD 92 billion (Aug 2013)

Indonesia’s economies still one of the best among emerging

economies

International Reserve

3

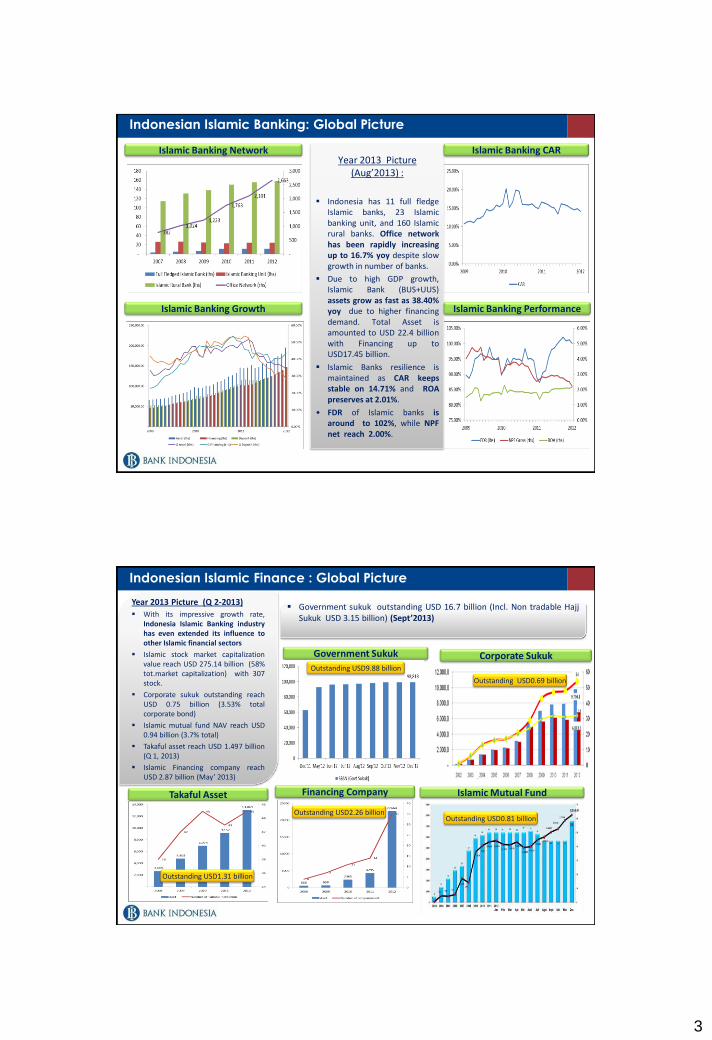

Indonesian Islamic Banking: Global Picture

Year 2013 Picture (Aug’2013) :

Indonesia has 11 full fledge

Islamic banks, 23 Islamic banking unit, and 160 Islamic rural banks. Office network has been rapidly increasing up to 16.7% yoy despite slow growth in number of banks.

Due to high GDP growth, Islamic Bank (BUS+UUS) assets grow as fast as 38.40% yoy due to higher financing demand. Total Asset is amounted to USD 22.4 billion with Financing up to USD17.45 billion.

Islamic Banks resilience is maintained as CAR keeps stable on 14.71% and ROA preserves at 2.01%.

• FDR of Islamic banks is around to 102%, while NPF net reach 2.00%.

Islamic Banking Network

Islamic Banking Growth

Islamic Banking CAR

Islamic Banking Performance

Indonesian Islamic Finance : Global Picture

Corporate Sukuk

Outstanding USD0.81 billion

Government Sukuk

Outstanding USD9.88 billion

Takaful Asset

Outstanding USD0.69 billion

Islamic Mutual Fund

Outstanding USD1.31 billion

Financing Company

Outstanding USD2.26 billion

Government sukuk outstanding USD 16.7 billion (Incl. Non tradable Hajj Sukuk USD 3.15 billion) (Sept’2013)

Year 2013 Picture (Q 2-2013)

With its impressive growth rate, Indonesia Islamic Banking industry has even extended its influence to other Islamic financial sectors

Islamic stock market capitalization value reach USD 275.14 billion (58% tot.market capitalization) with 307 stock.

Corporate sukuk outstanding reach USD 0.75 billion (3.53% total corporate bond)

Islamic mutual fund NAV reach USD 0.94 billion (3.7% total)

Takaful asset reach USD 1.497 billion (Q 1, 2013)

Islamic Financing company reach USD 2.87 billion (May’ 2013)

4

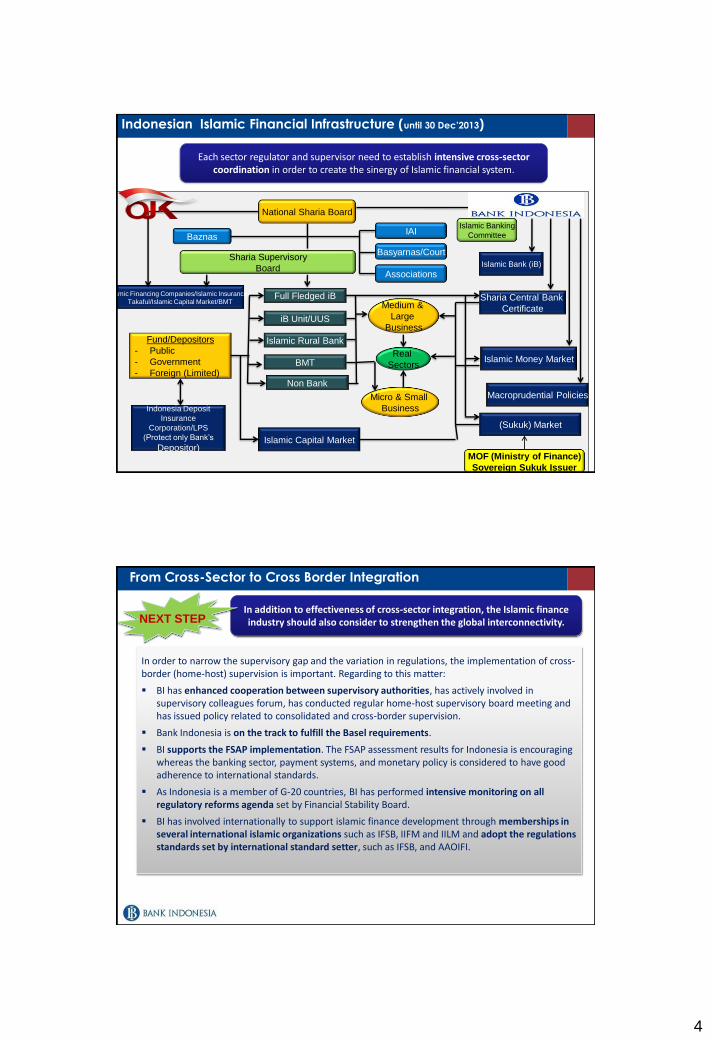

Indonesian Islamic Financial Infrastructure (until 30 Dec’2013)

National Sharia Board

IAI

Associations

Basyarnas/Court

Islamic Banking

Committee

Sharia Central Bank

Certificate

Islamic Money Market

(Sukuk) Market

Sharia Supervisory

Board

Baznas

Islamic Financing Companies/Islamic Insurance /

Takaful/Islamic Capital Market/BMT

Indonesia Deposit

Insurance

Corporation/LPS

(Protect only Bank’s

Depositor) Islamic Capital Market

Fund/Depositors

- Public

- Government

- Foreign (Limited)

Full Fledged iB

iB Unit/UUS

Islamic Rural Bank

BMT Real

Sectors

Medium &

Large

Business

Micro & Small

Business

Each sector regulator and supervisor need to establish intensive cross-sector coordination in order to create the sinergy of Islamic financial system.

Islamic Bank (iB)

Non Bank

Macroprudential Policies

MOF (Ministry of Finance)

Sovereign Sukuk Issuer

In order to narrow the supervisory gap and the variation in regulations, the implementation of cross-border (home-host) supervision is important. Regarding to this matter:

BI has enhanced cooperation between supervisory authorities, has actively involved in supervisory colleagues forum, has conducted regular home-host supervisory board meeting and has issued policy related to consolidated and cross-border supervision.

Bank Indonesia is on the track to fulfill the Basel requirements.

BI supports the FSAP implementation. The FSAP assessment results for Indonesia is encouraging whereas the banking sector, payment systems, and monetary policy is considered to have good adherence to international standards.

As Indonesia is a member of G-20 countries, BI has performed intensive monitoring on all regulatory reforms agenda set by Financial Stability Board.

BI has involved internationally to support islamic finance development through memberships in several international islamic organizations such as IFSB, IIFM and IILM and adopt the regulations standards set by international standard setter, such as IFSB, and AAOIFI.

From Cross-Sector to Cross Border Integration

In addition to effectiveness of cross-sector integration, the Islamic finance industry should also consider to strengthen the global interconnectivity. NEXT STEP

5

Indonesian Islamic Banks – Policy Direction and Prospect

Maintaining Strong Growth

• Innovation of genuine sharia Products and services : support the people need ,more broaden customer base and more productive activities

• Strategic alliance and strong infrastructure support : i.e. Government support, Optimization synergy with iB’s holding/Grup companies.

• More professionals & qualified HRD

• Intensified Education and Promotion

This strategy will attract more broaden

customers to use services from islamic

banks, and in the end this will have an

impact to strong growth

With Rp.228,8 trilion of iB (BUS+UUS+BPRS) asset in Aug’13 (eq US$ 23 billion) we only account for 4.9% of Indonesian banking industry, but annual growth in last 5 yrs ± 40% which double from global Islamic finance growth

6

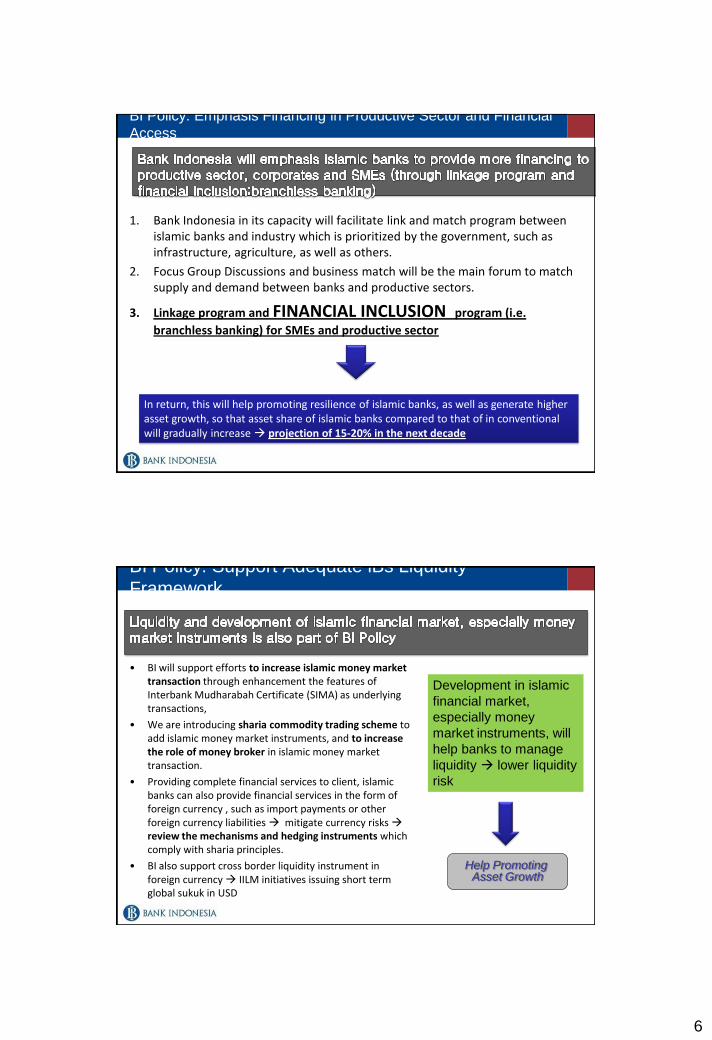

BI Policy: Emphasis Financing in Productive Sector and Financial

Access

1. Bank Indonesia in its capacity will facilitate link and match program between islamic banks and industry which is prioritized by the government, such as infrastructure, agriculture, as well as others.

2. Focus Group Discussions and business match will be the main forum to match supply and demand between banks and productive sectors.

3. Linkage program and FINANCIAL INCLUSION program (i.e.

branchless banking) for SMEs and productive sector

In return, this will help promoting resilience of islamic banks, as well as generate higher asset growth, so that asset share of islamic banks compared to that of in conventional will gradually increase projection of 15-20% in the next decade

BI Policy: Support Adequate iBs Liquidity

Framework

• BI will support efforts to increase islamic money market transaction through enhancement the features of Interbank Mudharabah Certificate (SIMA) as underlying transactions,

• We are introducing sharia commodity trading scheme to add islamic money market instruments, and to increase the role of money broker in islamic money market transaction.

• Providing complete financial services to client, islamic banks can also provide financial services in the form of foreign currency , such as import payments or other foreign currency liabilities mitigate currency risks review the mechanisms and hedging instruments which comply with sharia principles.

• BI also support cross border liquidity instrument in foreign currency IILM initiatives issuing short term global sukuk in USD

Development in islamic

financial market,

especially money

market instruments, will

help banks to manage

liquidity lower liquidity

risk

Help Promoting Asset Growth

7

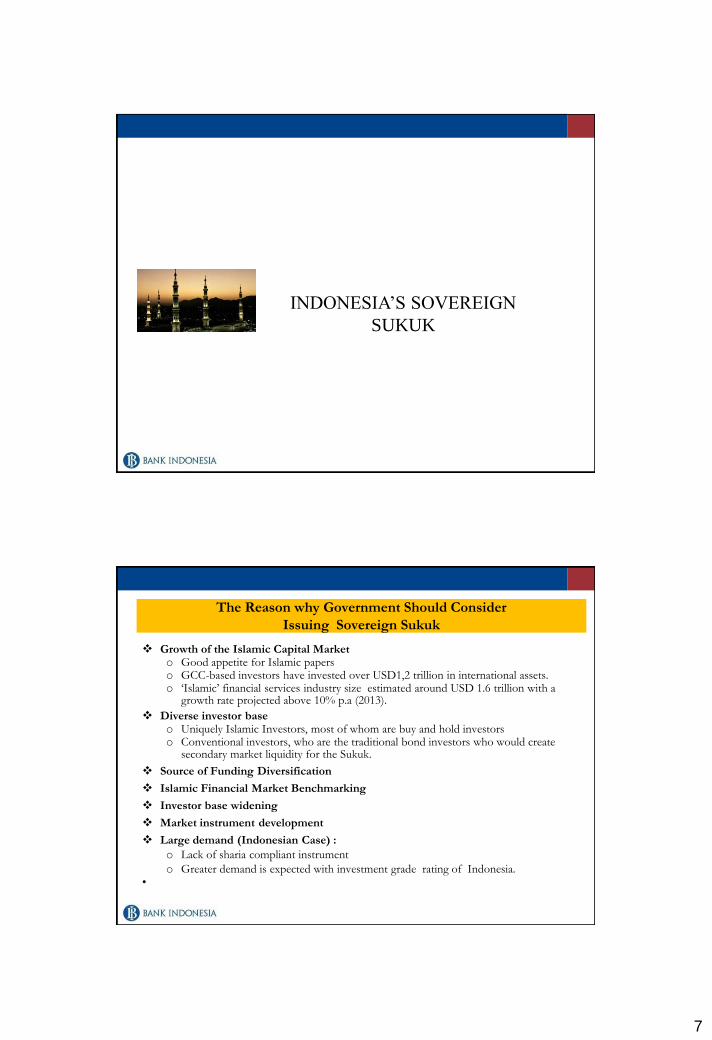

INDONESIA’S SOVEREIGN

SUKUK

Growth of the Islamic Capital Market o Good appetite for Islamic papers o GCC-based investors have invested over USD1,2 trillion in international assets. o ‘Islamic’ financial services industry size estimated around USD 1.6 trillion with a

growth rate projected above 10% p.a (2013).

Diverse investor base o Uniquely Islamic Investors, most of whom are buy and hold investors o Conventional investors, who are the traditional bond investors who would create

secondary market liquidity for the Sukuk.

Source of Funding Diversification

Islamic Financial Market Benchmarking

Investor base widening

Market instrument development

Large demand (Indonesian Case) :

o Lack of sharia compliant instrument

o Greater demand is expected with investment grade rating of Indonesia. •

The Reason why Government Should Consider

Issuing Sovereign Sukuk

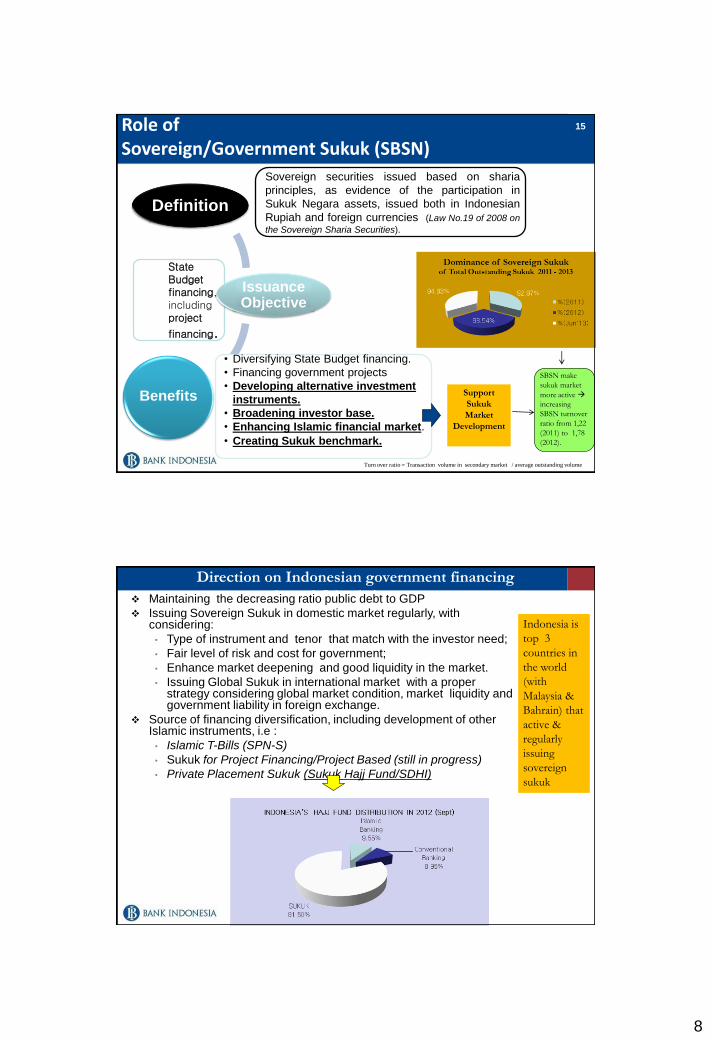

8

State Budget financing, including project

financing.

Role of Sovereign/Government Sukuk (SBSN)

Sovereign securities issued based on sharia

principles, as evidence of the participation in

Sukuk Negara assets, issued both in Indonesian

Rupiah and foreign currencies (Law No.19 of 2008 on

the Sovereign Sharia Securities).

Definition

Issuance Objective

Benefits

• Diversifying State Budget financing.

• Financing government projects

• Developing alternative investment

instruments.

• Broadening investor base.

• Enhancing Islamic financial market.

• Creating Sukuk benchmark.

15

Support

Sukuk

Market

Development

SBSN make

sukuk market

more active

increasing

SBSN turnover

ratio from 1,22

(2011) to 1,78

(2012).

Turn over ratio = Transaction volume in secondary market / average outstanding volume

Direction on Indonesian government financing through Islamic instrument

16

Maintaining the decreasing ratio public debt to GDP

Issuing Sovereign Sukuk in domestic market regularly, with considering:

• Type of instrument and tenor that match with the investor need;

• Fair level of risk and cost for government;

• Enhance market deepening and good liquidity in the market.

• Issuing Global Sukuk in international market with a proper strategy considering global market condition, market liquidity and government liability in foreign exchange.

Source of financing diversification, including development of other Islamic instruments, i.e :

• Islamic T-Bills (SPN-S)

• Sukuk for Project Financing/Project Based (still in progress)

• Private Placement Sukuk (Sukuk Hajj Fund/SDHI)

Indonesia is

top 3

countries in

the world

(with

Malaysia &

Bahrain) that

active &

regularly

issuing

sovereign

sukuk

9

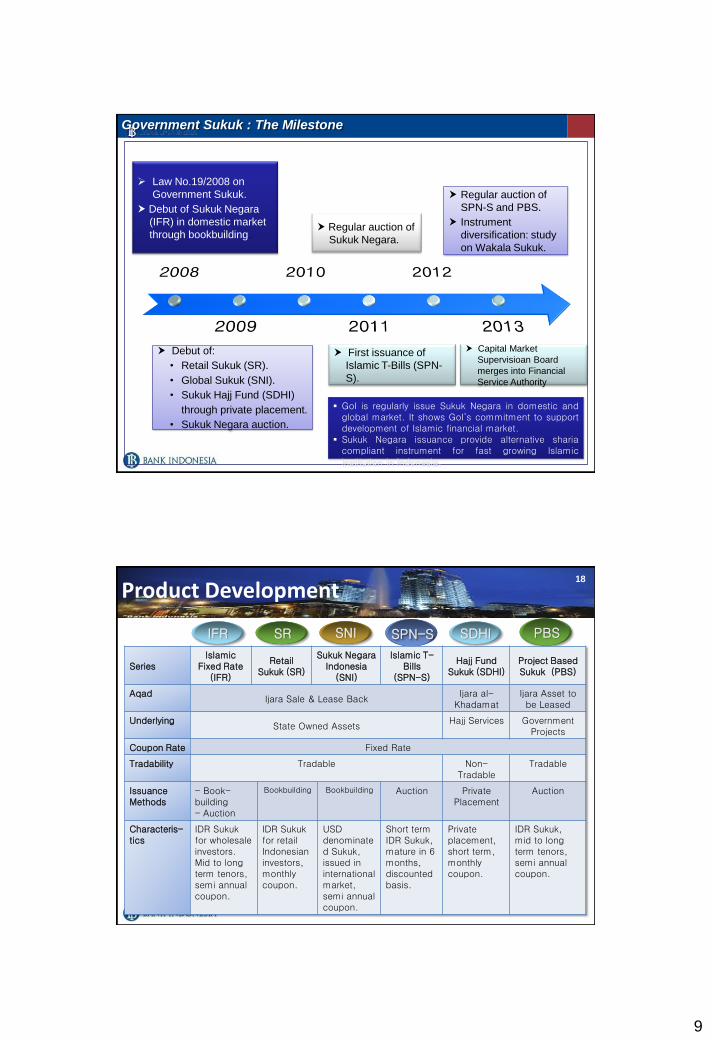

17

Debut of:

• Retail Sukuk (SR).

• Global Sukuk (SNI).

• Sukuk Hajj Fund (SDHI)

through private placement.

• Sukuk Negara auction.

Regular auction of

Sukuk Negara.

First issuance of

Islamic T-Bills (SPN-

S).

Regular auction of

SPN-S and PBS.

Instrument

diversification: study

on Wakala Sukuk.

GoI is regularly issue Sukuk Negara in domestic and global market. It shows GoI’s commitment to support development of Islamic financial market.

Sukuk Negara issuance provide alternative sharia compliant instrument for fast growing Islamic institution in Indonesia.

Law No.19/2008 on

Government Sukuk.

Debut of Sukuk Negara

(IFR) in domestic market

through bookbuilding.

Government Sukuk : The Milestone

Capital Market

Supervisioan Board

merges into Financial

Service Authority

Product Development

IFR SR SNI SDHI PBS

Series Islamic

Fixed Rate (IFR)

Retail Sukuk (SR)

Sukuk Negara Indonesia

(SNI)

Islamic T-Bills

(SPN-S)

Hajj Fund Sukuk (SDHI)

Project Based Sukuk (PBS)

Aqad Ijara Sale & Lease Back

Ijara al-Khadamat

Ijara Asset to be Leased

Underlying State Owned Assets

Hajj Services Government Projects

Coupon Rate Fixed Rate

Tradability Tradable Non-Tradable

Tradable

Issuance Methods

- Book-building - Auction

Bookbuilding Bookbuilding Auction Private Placement

Auction

Characteris-tics

IDR Sukuk for wholesale investors. Mid to long term tenors, semi annual coupon.

IDR Sukuk for retail Indonesian investors, monthly coupon.

USD denominated Sukuk, issued in international market, semi annual coupon.

Short term IDR Sukuk, mature in 6 months, discounted basis.

Private placement, short term, monthly coupon.

IDR Sukuk, mid to long term tenors, semi annual coupon.

SPN-S

18

10

19

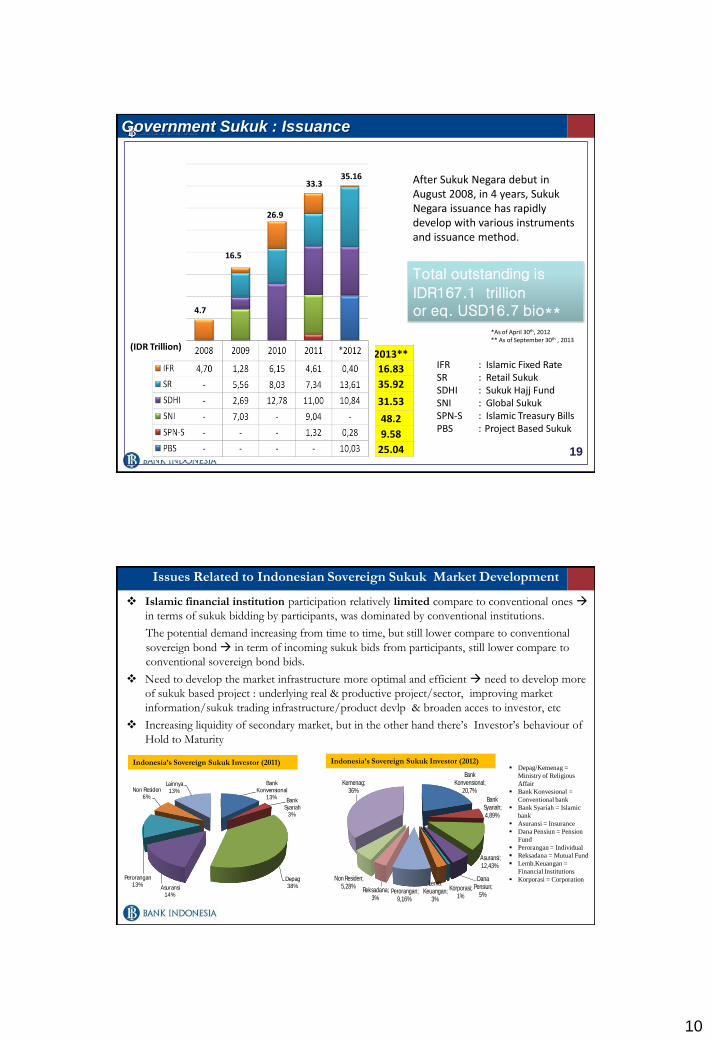

Government Sukuk : Issuance

After Sukuk Negara debut in August 2008, in 4 years, Sukuk Negara issuance has rapidly develop with various instruments and issuance method.

Total outstanding is

IDR167.1 trillion or eq. USD16.7 bio**

IFR : Islamic Fixed Rate SR : Retail Sukuk SDHI : Sukuk Hajj Fund SNI : Global Sukuk SPN-S : Islamic Treasury Bills PBS : Project Based Sukuk

*As of April 30th, 2012 ** As of September 30th , 2013

2013**

16.83

35.92

31.53

48.2

9.58

25.04

(IDR Trillion)

4.7

16.5

26.9

33.3 35.16

Issues Related to Indonesian Sovereign Sukuk Market Development

Islamic financial institution participation relatively limited compare to conventional ones

in terms of sukuk bidding by participants, was dominated by conventional institutions.

The potential demand increasing from time to time, but still lower compare to conventional

sovereign bond in term of incoming sukuk bids from participants, still lower compare to

conventional sovereign bond bids.

Need to develop the market infrastructure more optimal and efficient need to develop more

of sukuk based project : underlying real & productive project/sector, improving market

information/sukuk trading infrastructure/product devlp & broaden acces to investor, etc

Increasing liquidity of secondary market, but in the other hand there’s Investor’s behaviour of

Hold to Maturity

Bank Konvensional

13%Bank

Syariah3%

Depag38%Asuransi

14%

Perorangan13%

Non Residen6%

Lainnya13%

Indonesia’s Sovereign Sukuk Investor (2011)

Bank Konvensional;

20,7%

Bank Syariah; 4,89%

Asuransi; 12,43%

Dana Pensiun;

5%Korporasi;

1%

Lemb. Keuangan;

3%Perorangan;

9,16%

Reksadana; 3%

Non Residen; 5,28%

Kemenag; 36%

Indonesia’s Sovereign Sukuk Investor (2012) Depag/Kemenag =

Ministry of Religious

Affair

Bank Konvesional =

Conventional bank

Bank Syariah = Islamic

bank

Asuransi = Insurance

Dana Pensiun = Pension

Fund

Perorangan = Individual

Reksadana = Mutual Fund

Lemb.Keuangan =

Financial Institutions

Korporasi = Corporation

11

Indonesian Islamic Finance : Expectation for the

future

• Actively and contribute more to the development of Islamic Financial Services Industry in the world (i.e involvement in various international organization:IDB, IFSB, IILM, IIFM)

• Maintaining the uniqueness of Indonesian Islamic Finance characteristic (i.e. Islamic microfinance, prudential & sharia fullfilment and real sector/productive financing framework) reference for Islamic banking/finance development in the world