Outbound Investments by Cyril Shroff Managing Partner Amarchand & Mangaldas & Suresh A. Shroff & Co....

36

Outbound Investments by Cyril Shroff Managing Partner Amarchand & Mangaldas & Suresh A. Shroff & Co. Peninsula Chambers, Peninsula Corporate Park, Ganpatrao Kadam Marg, Lower Parel, Mumbai - 400 013 Tel: (91-22) 2496-4455 Fax:(91-22) 2496-3666 Email: [email protected] February 21, 2015 12.15 p.m. to 1.30 p.m. Privileged & Confidential

-

Upload

bryce-skinner -

Category

Documents

-

view

228 -

download

1

Transcript of Outbound Investments by Cyril Shroff Managing Partner Amarchand & Mangaldas & Suresh A. Shroff & Co....

Privileged & Confidential

Outbound Investments

by

Cyril ShroffManaging Partner

Amarchand & Mangaldas & Suresh A. Shroff & Co. Peninsula Chambers, Peninsula Corporate Park,

Ganpatrao Kadam Marg, Lower Parel, Mumbai - 400 013Tel: (91-22) 2496-4455 Fax:(91-22) 2496-3666

Email: [email protected]

February 21, 2015

12.15 p.m. to 1.30 p.m.

2

About Amarchand Mangaldas

Privileged & Confidential

India’s Leading and Largest Law Firm

• Over 650 lawyers including 82 partners

• Presence in 8 major cities in India - new office in Gurgaon

• Over 95 years of experience

• Full service offering

Consistently Voted as One of the Top Law Firms in Asia Pacific

• IFLR Asia Awards - National Law Firm of the Year (India) for 2014, 2013 & 2012

• ALB SE Asia Law Awards - India Deal Firm of the Year for 2014, 2013, 2012 & 2011

• Acritas’ Elite Law Firm Brand Index – 4th in Asia Pacific & 20th Globally for 2014

• Asian Legal Business – 10th Largest Firm in Asia 2014

• The Lawyer Asia Pacific - Ranked 13th in Asia Pacific Top 100 Independent Law Firms for 2014

• Asian Legal Business Employer of Choice for 2014 & 2013

• IBLJ Indian Law Firm Awards – Law Firm of the Year & Best Overall Law Firm for 2013, 2012 & 2011

• RSG India - Ranked 1 amongst India’s Top 40 Law Firms for 2013, 2012 & 2011

Leading clients include domestic and foreign commercial enterprises, financial institutions, leading private equity funds and venture capital funds as well as state and regulatory bodies

Mumbai

A

A

New Delhi

Hyderabad

Chennai

Bangalore

Kolkata

A

A

Ahmedabad

A

Consistently been rated as top ranked law firm in India by various professional organizations

A

A

Gurgaon

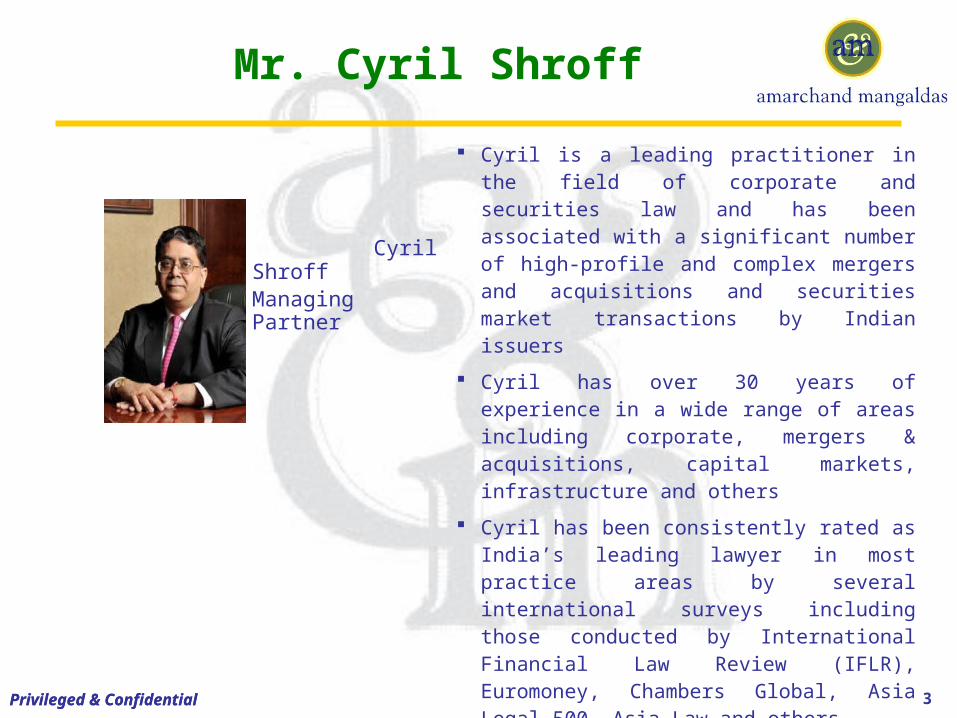

Mr. Cyril Shroff

Cyril Shroff Managing Partner

Cyril is a leading practitioner in the field of corporate and securities law and has been associated with a significant number of high-profile and complex mergers and acquisitions and securities market transactions by Indian issuers

Cyril has over 30 years of experience in a wide range of areas including corporate, mergers & acquisitions, capital markets, infrastructure and others

Cyril has been consistently rated as India’s leading lawyer in most practice areas by several international surveys including those conducted by International Financial Law Review (IFLR), Euromoney, Chambers Global, Asia Legal 500, Asia Law and others

Cyril has authored several publications on legal topics and has written many articles. He is a member of the Centre for Study of the Legal Profession established by the Harvard Law School (HLS)

Cyril is a full member of the Society of Trust Estate Practitioners. He is also the only member from India in the International Academy of Estate and Trust Law.

Privileged & ConfidentialPrivileged & Confidential 3

Overview

Introduction

Investing in Companies Overseas – What are the laws?

Establishing Overseas Branch Office

Liberalized Remittance Scheme (LRS)

Recent Developments and Issues

Privileged & Confidential 4

Introduction

Privileged & Confidential

Introduction

Liberalization• Phase I – 1992 to 1995

− ‘Automatic route’ for overseas investments introduced − Cash remittances permitted for the first time− Value restricted to US$ 2 million, with cash component not exceeding US$ 0.5

million, in a block of 3 years

• Phase II – 1995 to 2000− Policy framework laid down – Creation of Fast Track Route− Limits raised to US$ 4 million and linked to average export earnings of the

preceding 3 years − Cash remittances continued to be restricted to US$ 0.5 million− Beyond US$ 4 million – Approval of committee consisting of members from

RBI, MoF, MoEA and MoC− Beyond US$ 15 million – Considered by MoF + Special Committee− Indian promoters allowed to set up 2nd and subsequent generation companies,

provided first generation company set up under Fast Track Route − Neutrality condition done away with in 1999

Privileged & Confidential 6

Introduction

• Phase III – 2000 till date− Scope of outward investments increased considerably pursuant to FEMA − In 2002, per annum upper limit for automatic approval raised to US$100 million − In 2003, investment limit was 100% of net worth , and gradually increased to

400% of net worth − ECB policy modified and funding of JV/ WOS abroad included as permissible

end-use− Capital control measures introduced in 2013, but reversed in 2014

Trend Analysis – 2000 till date• Level of ODI has increased manifold since 1999 – 2000

− Sharp uptrend at US$ 74.3 billion recorded during 2nd half of 2000s, compared to US$ 8.2 billion in the 1st half of 2000s

− Trend moderately affected during 2009 – 2010 crises; however, rebound seen in 2010 – 2011; may have been affected again in 2013 – 2014

− January, 2015 – US$ 2.05 billion; down from US$ 7.3 billion invested in January, 2014

− June to December, 2014 – US$ 11.8 billion − India’s share in total developing economy ODI increasing continuously since

2005Privileged & Confidential 7

Introduction

India Inc looking abroad• Overseas assets – source of raw materials, research and technology

(primarily IP), base for untapped developing markets and diversification of revenue streams

• Acquisition not restricted to developing markets – includes developed markets as well

• Desire to compete globally • Increased foreign currency revenues• Easy accessibility to finance and low cost of debt capital – global

economic downturn / increased appetite of Western countries for M&A• Mid level firms also seeking to acquire assets abroad

Privileged & Confidential 8

Investing in Companies Overseas

Privileged & Confidential

Investing in Companies Overseas – What are the Laws?

Foreign Exchange Management Act, 1999

Foreign Exchange Management (Transfer or Issue of any Foreign Security) Regulations, 2004 (FEMA 120)

Master Circular on Direct Investments by Residents in Joint Venture (JV) / Wholly Owned Subsidiary (WOS) abroad, dated July 1, 2014

RBI Master Circular on Guarantees and Co-Acceptances, dated July 1, 2014

NBFC (Opening of Branch, Subsidiary, JV, Representative Office or Undertaking Investments Abroad by NBFCs) Directions, 2011

Privileged & Confidential 10

Investing in Companies Overseas

Automatic route v. Approval route Who can invest?• Until recently only companies and registered partnerships could invest• LLPs now included in ‘Indian Party’ definition• Resident individuals permitted to invest in JV/ WOS overseas – interplay with

LRS• Unregistered partnerships and proprietorships permitted under Approval Route• Registered societies and trusts engaged in manufacturing/ educational/ hospital

sector may invest in same sector, under Approval Route Conditions for equity investment• Total financial commitment of Indian company – limit reinstated to 400% from

100% in July, 2014− Financial commitment not to exceed US$ 1 billion under automatic route

• JV/WOS to be engaged in bona fide business activity• Indian party not to be on RBI’s exporters caution list or defaulters list or under

investigation by any investigation/ enforcement agency or regulator• Annual performance report filed• Transactions relating to the investment to be done through one branch of an ADPrivileged & Confidential 11

Investing in Companies Overseas

Overall Acquisition Ceiling = 4 X Net Worth – total financial commitment already incurred, subject to cap of US$ 1 billion

Calculating total financial commitment• 400% of the amount of equity shares; preference shares; loans; guarantees

(including 3rd party bank guarantees, but excluding performance guarantees (50% ))

Investments through SPVs – Permitted (Impact of S. 186 of the Companies Act, 2013)

Post investment• JV/ WOS permitted to diversify its activities/ set up step down subsidiaries/

alter its shareholding pattern• Further acquisitions by JV/ WOS can be funded from accruals offshore

Portfolio investments by listed Indian companies • Listed Indian companies permitted to invest up to 50% of net worth in

shares and bonds / fixed income securities, issued by listed overseas companiesPrivileged & Confidential 12

Investing in Companies Overseas

Valuation • Category I Merchant Banker registered with SEBI or an Investment

Banker/ Merchant Banker registered with appropriate regulatory authority in the host country for investment, when:− Higher than US$ 5 million

− By swap of shares (with prior FIPB approval)

• In all other cases, valuation to be done by Chartered Accountant or Certified Public Accountant

ODI by NBFCs• RBI approval required for overseas JV/ WOS/ representative office/

other investments

• Additional conditions

• Multi layered, cross jurisdictional structures – specifically prohibited

Privileged & Confidential 13

Investing in Companies Overseas

Sensitive Sectors• ODI in real estate business (buying and selling of real estate or trading

in TDRs) and banking business prohibited

• Additional compliances – investment in financial services sector− Conditions

» Register with the regulatory authority in India for financial sector activities

» Earned profit in preceding 3 financial years from financial services activities

» Obtained approval from relevant Indian and overseas regulator

» Capital adequacy requirement complied with

− Conditions to be complied with for each step-down subsidiary

− Conditions also applicable to regulated entities in financial services sector in India investing in any sector overseas

Privileged & Confidential 14

Guarantees and Access to Debt Capital Overseas

Guarantees by Indian parties (subject to net worth limit)• JV/ WOS – guarantees permitted• First level operating step down – irrespective of whether direct JV/ WOS is

established as SPV or operating company, guarantee permitted • Second level/ subsequent level step down operating subsidiaries –

guarantee permitted if:− prior approval of RBI procured− Indian party holds at least 51% in the subsidiary indirectly

Financing investments – 3rd party credit enhancement• Guarantees/ LOC/ SBLC issued by Indian banks for overseas investments• LOC/ SBLC issued by AD on behalf of the Indian borrower with respect to

its JV/ WOS/ first level step down permitted (subject to net worth limit)• Faster and cheaper access to finance – leveraging Indian balance sheets for

financing abroad• Credit enhanced – offshore financing transactions now becoming a reality

Privileged & Confidential 15

Guarantees and Access to Debt Capital Overseas

Pledge of shares• Indian party can pledge shares of JV/ WOS/ step-down subsidiary overseas to

domestic or overseas lender for availing credit facility (funded and non-funded)

for itself or group companies or for JV/ WOS/ step-down subsidiary overseas − Liberalized in December, 2014 – includes pledge of shares of step-down subsidiaries− Value of facility included in financial commitment of Indian party

Creation of charge on assets• Approval route until December, 2014• Indian party can now create a charge under automatic route on its assets in

favour of an overseas lender for availing credit facility (funded and non-

funded) for its JV/ WOS/ step-down subsidiary overseas• Indian party can now create a charge under automatic route on the assets of its

overseas JV/ WOS/ step-down subsidiary in favour of an AD bank in India as

security for availing of facilities for itself or its JV/ WOS/ step-down outside

India− Value of facility included in financial commitment of Indian partyPrivileged & Confidential 16

Structuring Options:Investor Profile

Case Study Profile• The Patels are an Indian family – comprising of Father, Mother and 2

sons – Son 1 and Son 2. Patels are promoters of a conglomerate that is primary based in India, with interests in the manufacturing, steel, energy sectors

• Son 1 is engaged in the business. Son 2 is currently a UK resident

• The flagship company of the Patel Group is contemplating acquisition of a mid-sized steel processing business in the UK

• The family members are contemplating acquisition of a BPO company in the UK, as an investment by the family

17Privileged & Confidential

Structuring Options: Acquisition of Steel Co

Acquisition of shares of offshore target company to be in accordance with FEMA 120

Investment can be up to 400% of the ‘net worth’ of the Indian entity – subject to cap of US$ 1 billion

Valuation Report – Chartered Accountant or Category I Merchant Banker (depending on value)

Remittance through an Authorized Dealer

18Privileged & Confidential

Structuring Options: Acquisition of Steel Co

19Privileged & Confidential

Structuring • Direct investment unfavourable

• May be routed through an overseas SPV− Tax Benefits (accumulation

overseas)

− Leveraging on group strength to raise finance

− Borrowing of funds at the SPV level

− Foreign exchange fluctuation risk mitigated

• However, CFC implications under proposed Direct Taxes Code will require consideration

UK Target Company

Indian Party

Equity and Preference

Structuring Options: Acquisition of Steel Co

Factors to consider when choosing location for SPV• Low/ nil withholding tax on dividend and

interest• Low/ nil income tax and capital gains tax

on exit• Favourable tax treaty with Target and

Indian Party• Capitalization norms• Favorable Jurisdictions – Singapore,

Mauritius, the Netherlands, etc Use of SPVs for investment in the UK • Indian Tax Laws

− Dividend received from Singapore SPV taxable in India @ 15%

− Redemption of preference shares at par not subject to tax in India

20Privileged & Confidential

Indian Party

Singapore SPV

UK Target Company

Counter Guarantee by Indian Parent

Equity and Preference

Equity

(Operating / SPV)

(Operating / can not be

holding company)

Borrowings

Structuring Options: Acquisition of BPO Co

Possible to now acquire 100% of shares of the BPO company under LRS

• Father, Mother and Son 1 can combine remittances under LRS

− Total remittance – US$ 375,000

− Son 2 cannot remit under LRS, as non-resident

• Mandatory to invest directly into the BPO Co – no SPVs permitted

• No step-down subsidiaries allowed under LRS

21Privileged & Confidential

Key Tax Considerations

Privileged & Confidential

Key Tax Considerations

Profit repatriation#• Reduced rate of taxation @15% for dividends from overseas subsidiary

(shareholding of 26% or more) Transfer pricing issues • Indian holding companies required to charge guarantee fees at arms

length (Indian corporate tax rate – 30%)• The remittance to overseas subsidiary is loan, not equity – thus, interest

earnings on deemed loans to be taxed in India Benefits / advantages for overseas hold co/ regional hold co• Income from target company – taxed in India only when remitted to

India – income accumulation in overseas hold co pre-Indian tax permitted

• Minimum tax leakage – consider tax benefits for dividend, interest and capital gain between hold co jurisdiction and target company jurisdiction, including the beneficial provisions contained in the relevant tax treaties

# Surcharge and education cess additionalPrivileged & Confidential 23

Key Tax Considerations

Going Forward• Controlled Foreign Company Rules under the proposed Direct Tax Code

− Passive income earned by an overseas subsidiary, controlled directly or indirectly, by Indian resident shall be charged to tax, even if such income is not distributed to shareholders in India

• Place of Effective Management under the proposed Direct Tax Code− Foreign company regarded as resident in India if at anytime in the year its

POEM is in India (based on where BoD/ executive directors make commercial and strategic decisions)

• General Anti-Avoidance Rules – Expected to be postponed

Privileged & Confidential 24

No clarity on the fate of DTCCan mitigate risk through appropriate structuring, strong

commercial rationales and substance

Establishing Overseas Branch Offices

Privileged & Confidential

Establishing Overseas Branch Offices

Under FERA: Regulated by Chapter 9 of Exchange Control Manual issued by RBI

No specific regulations or guidelines under FEMA Regime Section 1(3) of FEMA – Provisions apply to all branches, offices and

agencies outside India owned or controlled by a person resident in India Section 2(iv) of FEMA - a ‘Person Resident in India’ includes “any

office, branch or agency outside India owned or controlled by a person resident in India”

For setting up and operations of overseas branch offices, companies need to open bank account in such jurisdiction • Regulation 7(4A) of FEM (Foreign Currency Accounts by a Person Resident in

India) Regulations, 2000 read with Master Circular on Export of Goods and Services, July 1, 2014 – Permits opening of a foreign currency account with a bank outside India by an Indian entity, its overseas branch or representative posted outside India

Privileged & Confidential 26

Establishing Overseas Branch Offices

• Conditions include: − Branch is set up for normal business operations

− Remittances (for initial expenses and recurring expenses) made to all such accounts in an accounting year to be within specified ceilings, unless remittance out of EEFC Account or if overseas branch is set up by 100% EOU, or a unit in export processing zone, hardware/ software technology park (within 2 years of establishment)

− Such branch should not enter into contract or agreement in contravention of FEMA

− Branch should not create any financial liabilities, contingent or otherwise, for the head office in India

− Branch should not invest surplus funds abroad without prior approval of RBI

− Details of bank accounts opened overseas to be promptly reported to the AD Bank

Some AD Banks continue to require submission of Form OBR (issued under the erstwhile FERA regime) at the time of remittance for opening an overseas branch

Privileged & Confidential 27

Liberalized Remittance Scheme

Privileged & Confidential

Liberalized Remittance Scheme

Introduced in 2004 Available only to resident individuals Limit reduced from US$ 200,000 to US$ 75,000 in 2013 – Increased to US$

125,000 per financial year in 2014• RBI Sixth Bi-Monthly Monetary Policy (released in February, 2015) – proposed increase of

limit to US$ 250,000

Scheme available for minors Consolidation of LRS remittances of family members permitted Residents can open, maintain and hold foreign currency accounts with a bank

outside India Permitted to retain, reinvest the income earned on the investments overseas Jurisdictional restrictions – Facility not available for direct or indirect

remittances to:• Bhutan, Nepal, Mauritius and Pakistan• Countries identified by Financial Action Task Force as non-co-operative countries and

territoriesPrivileged & Confidential 29

Liberalized Remittance Scheme

End-use• Permitted current and/ or capital account transactions• Acquisition of shares, debt instruments, units of mutual funds, venture capital

funds, unrated debt securities, promissory notes, acquisition of ESOPs• Rupee gift/ loan to a NRI /PIO, who is a close relative • Acquisition of immovable property

− Prohibited in 2013 – Permitted again in 2014• Acquisition of JV/WOS overseas

− Lack of clarity until August, 2013» Permission available under LRS, but not under FEMA 120» Numerous instances of compounding

− W.e.f. August 1, 2013 individuals permitted to set up JV/WOS abroad− Linked to FEMA 120

» Permission only to set up operating companies» No step-down subsidiaries permitted» Sectoral restrictions same as that on Indian companies, and includes financial services

− Welcome move, but pragmatic?

Privileged & Confidential 30

Recent Developments and Issues

Privileged & Confidential

Recent Developments and Issues

RBI’s capital control measures – 2013 • INR v. USD – Rupee’s free fall• August, 2013

− Total financial commitment of Indian party for JV/ WOS reduced from 400% to 100% of total net worth» Exceptions - Financial commitments made on or before August 14, 2013

− LRS limits reduced to US$ 75,000 per financial year

Reversal of capital control measures – 2014• ODI – 400% limit reinstated, albeit with condition• LRS limit – Increased to US$ 125,000

− Recent proposal for increase to US$ 250,000 per financial year

Individuals permitted to set up JV/ WOS overseas Creation of charges on shares of JV/ WOS/ Step down

subsidiaries, domestic assets in favour of overseas lenders, overseas assets in favour of domestic lenders – liberalized in 2014Privileged & Confidential 32

Recent Developments and Issues

Emerging issues in ODI• Use/ abuse of multilayered structures

− Two levels SPVs or structures involving Hold Co-Op Co-Hold Co structure permitted?

− “Matter under consideration” per RBI circular of December 29, 2014

− NBFC exception – specific prohibition on multi-layered structures (June, 2011)

− Section 186(1) of Companies Act, 2013

• RBI’s round tripping concerns

• Investments in financial services− Requirement to procure approval of overseas regulator for each investment

• Stock swap deals not easy – FIPB approval mandatory − Impact on timelines

• Increased disclosure requirements under Clause 36 of Listing Agreement – applicable only to listed companies

Privileged & Confidential 33

Recent Developments and Issues

Cross border mergers – Companies Act, 2013• Indian companies now permitted to merge into foreign companies, with

resulting company being a foreign company

• Prior RBI approval required

• Concept of notified territories made applicable to inbound and outbound mergers

• Provision not yet notified by MCA –1956 Act stands as of today

Privileged & Confidential 34

Privileged & Confidential

Questions?

Privileged & Confidential

Thank You© Amarchand & Mangaldas & Suresh A. Shroff & Co.

Mumbai, February 2015