OTT VIDEO POTENTIAL IN MENA: THREATS AND ... #AMTMT OTT VIDEO POTENTIAL IN MENA: THREATS AND...

19

Saudi Arabia Telecoms Summit 2016: Building blocks for successful operator strategies © Analysys Mason Limited 2016 SAUDI ARABIA TELECOMS SUMMIT 2016 BUILDING BLOCKS FOR SUCCESSFUL OPERATOR STRATEGIES #AMTMT OTT VIDEO POTENTIAL IN MENA: THREATS AND OPPORTUNITIES FOR TELECOMS OPERATORS KARIM YAICI NOVEMBER 2016 EVENT SPONSOR

-

Upload

truongxuyen -

Category

Documents

-

view

223 -

download

5

Transcript of OTT VIDEO POTENTIAL IN MENA: THREATS AND ... #AMTMT OTT VIDEO POTENTIAL IN MENA: THREATS AND...

Saudi Arabia Telecoms Summit 2016: Building blocks for successful operator strategies

© Analysys Mason Limited 2016

SAUDI ARABIA TELECOMS SUMMIT 2016

BUILDING BLOCKS FOR SUCCESSFUL OPERATOR

STRATEGIES

#AMTMT

OTT VIDEO POTENTIAL IN MENA:

THREATS AND OPPORTUNITIES FOR

TELECOMS OPERATORS

KARIM YAICI

NOVEMBER 2016

EVENT SPONSOR

Saudi Arabia Telecoms Summit 2016: Building blocks for successful operator strategies

© Analysys Mason Limited 2016

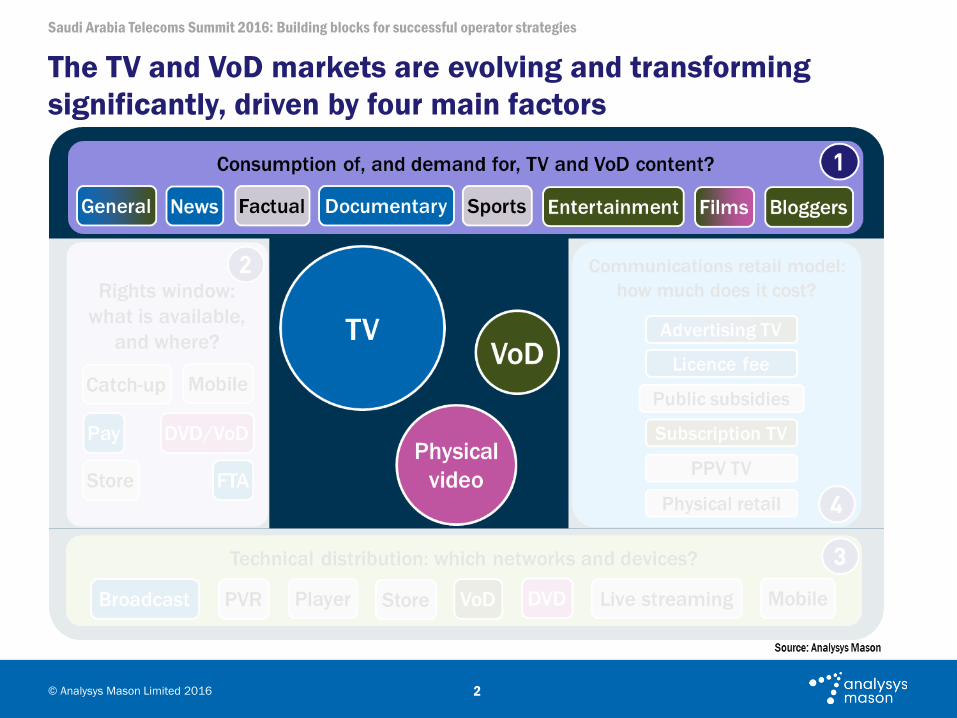

The TV and VoD markets are evolving and transforming

significantly, driven by four main factors

2

Saudi Arabia Telecoms Summit 2016: Building blocks for successful operator strategies

© Analysys Mason Limited 2016

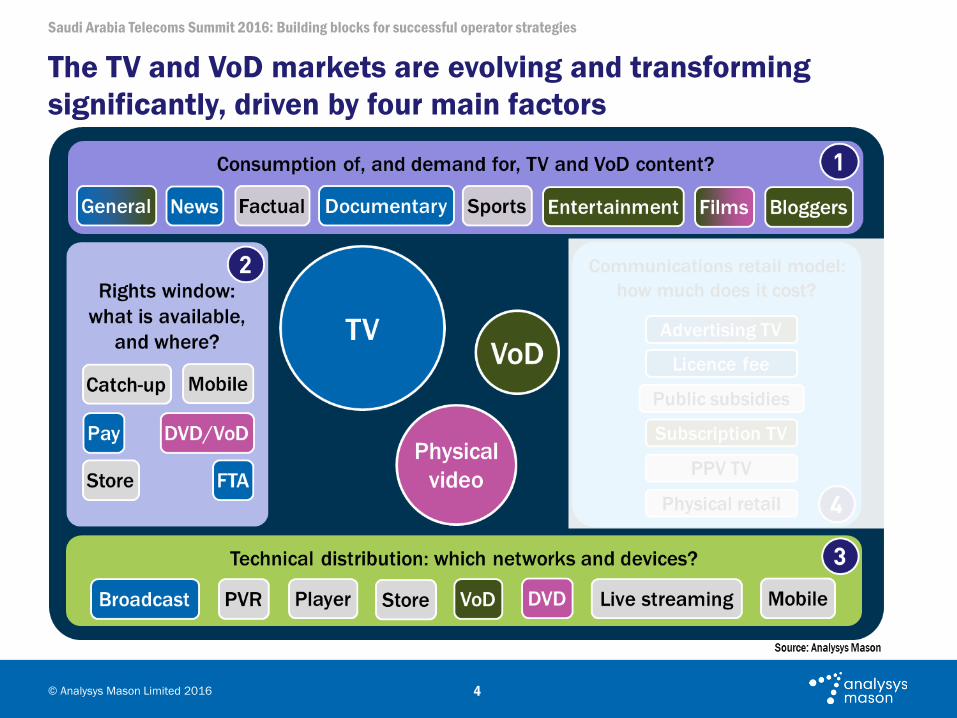

The TV and VoD markets are evolving and transforming

significantly, driven by four main factors

3

Saudi Arabia Telecoms Summit 2016: Building blocks for successful operator strategies

© Analysys Mason Limited 2016

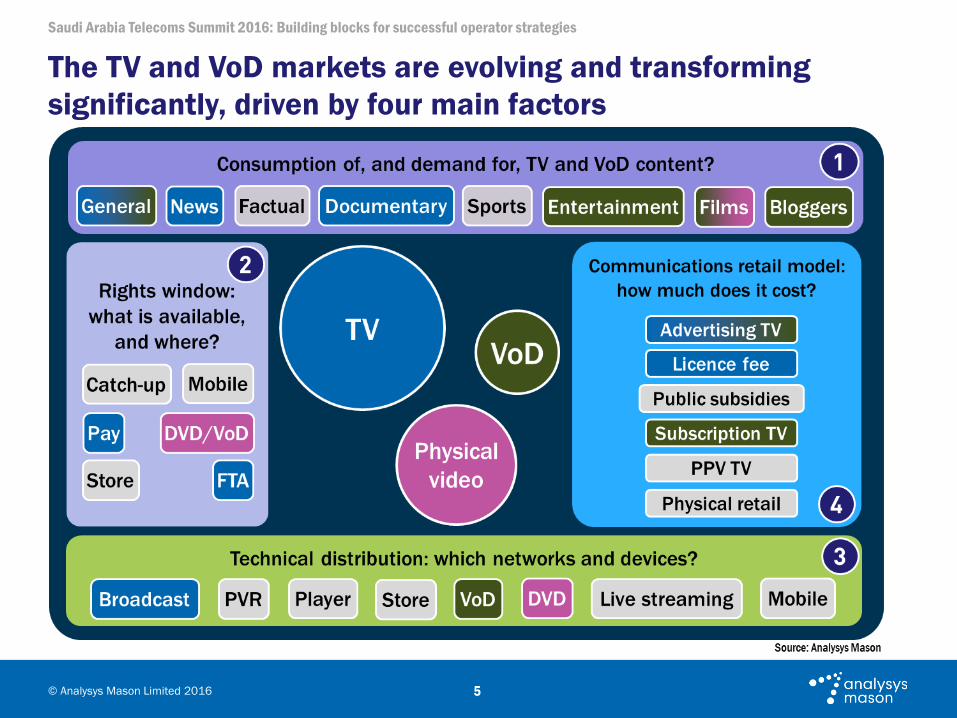

The TV and VoD markets are evolving and transforming

significantly, driven by four main factors

4

Saudi Arabia Telecoms Summit 2016: Building blocks for successful operator strategies

© Analysys Mason Limited 2016

The TV and VoD markets are evolving and transforming

significantly, driven by four main factors

5

Saudi Arabia Telecoms Summit 2016: Building blocks for successful operator strategies

© Analysys Mason Limited 2016

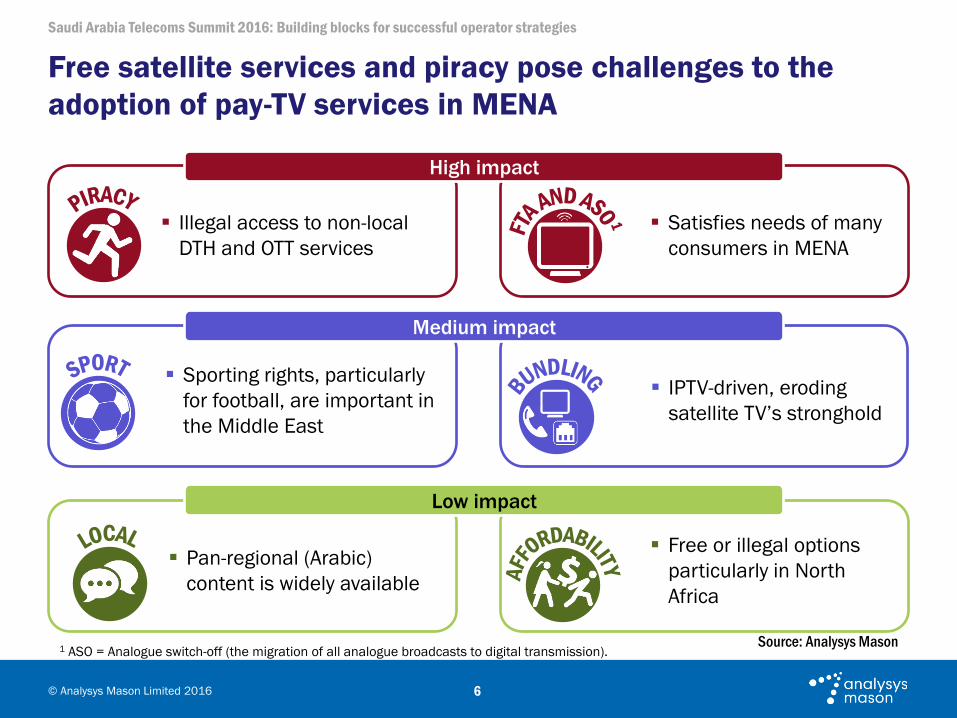

Free or illegal options

particularly in North

Africa

IPTV-driven, eroding

satellite TV’s stronghold

Satisfies needs of many

consumers in MENA

Free satellite services and piracy pose challenges to the

adoption of pay-TV services in MENA

6

Illegal access to non-local

DTH and OTT services

High impact

Sporting rights, particularly

for football, are important in

the Middle East

Medium impact

Pan-regional (Arabic)

content is widely available

Low impact

1 ASO = Analogue switch-off (the migration of all analogue broadcasts to digital transmission).Source: Analysys Mason

Saudi Arabia Telecoms Summit 2016: Building blocks for successful operator strategies

© Analysys Mason Limited 2016

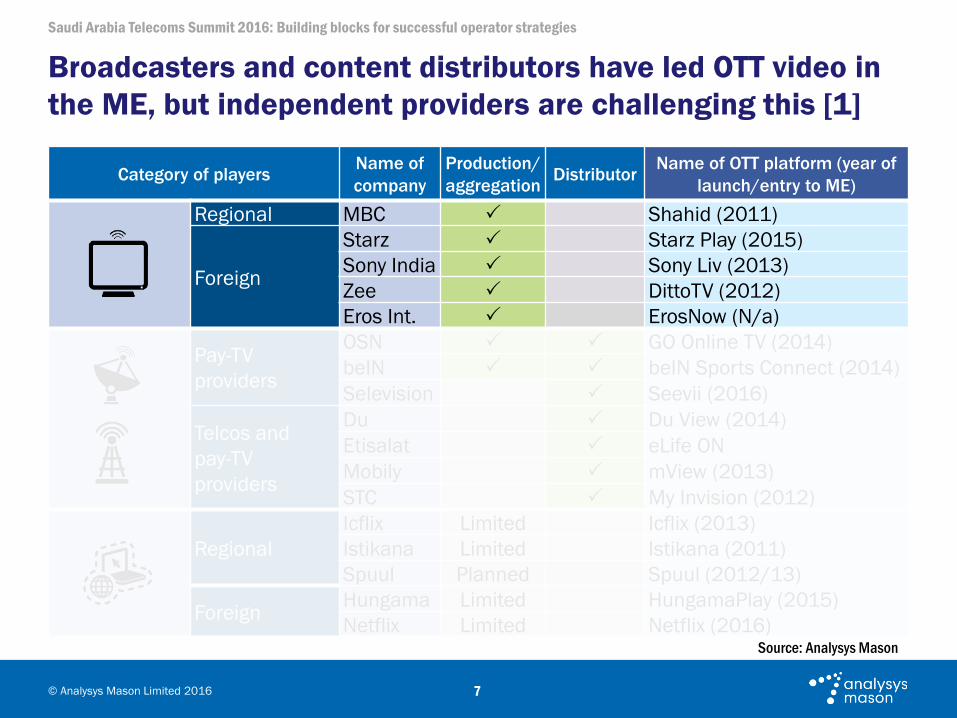

Broadcasters and content distributors have led OTT video in

the ME, but independent providers are challenging this [1]

7

Category of playersName of

company

Production/

aggregationDistributor

Name of OTT platform (year of

launch/entry to ME)

Regional MBC Shahid (2011)

Foreign

Starz Starz Play (2015)

Sony India Sony Liv (2013)

Zee DittoTV (2012)

Eros Int. ErosNow (N/a)

Pay-TV

providers

OSN GO Online TV (2014)

beIN beIN Sports Connect (2014)

Selevision Seevii (2016)

Telcos and

pay-TV

providers

Du Du View (2014)

Etisalat eLife ON

Mobily mView (2013)

STC My Invision (2012)

Regional

Icflix Limited Icflix (2013)

Istikana Limited Istikana (2011)

Spuul Planned Spuul (2012/13)

ForeignHungama Limited HungamaPlay (2015)

Netflix Limited Netflix (2016)Source: Analysys Mason

Saudi Arabia Telecoms Summit 2016: Building blocks for successful operator strategies

© Analysys Mason Limited 2016

Source: Analysys Mason

Broadcasters and content distributors have led OTT video in

the ME, but independent providers are challenging this [2]

8

Category of playersName of

company

Production/

aggregationDistributor

Name of OTT platform (year of

launch/entry to ME)

Regional MBC Shahid (2011)

Foreign

Starz Starz Play (2015)

Sony India Sony Liv (2013)

Zee DittoTV (2012)

Eros Int. ErosNow (N/a)

Pay-TV

providers

OSN GO Online TV (2014)

beIN beIN Sports Connect (2014)

Selevision Seevii (2016)

Telcos and

pay-TV

providers

Du Du View (2014)

Etisalat eLife ON

Mobily mView (2013)

STC My Invision (2012)

Regional

Icflix Limited Icflix (2013)

Istikana Limited Istikana (2011)

Spuul Planned Spuul (2012/13)

ForeignHungama Limited HungamaPlay (2015)

Netflix Limited Netflix (2016)

Saudi Arabia Telecoms Summit 2016: Building blocks for successful operator strategies

© Analysys Mason Limited 2016

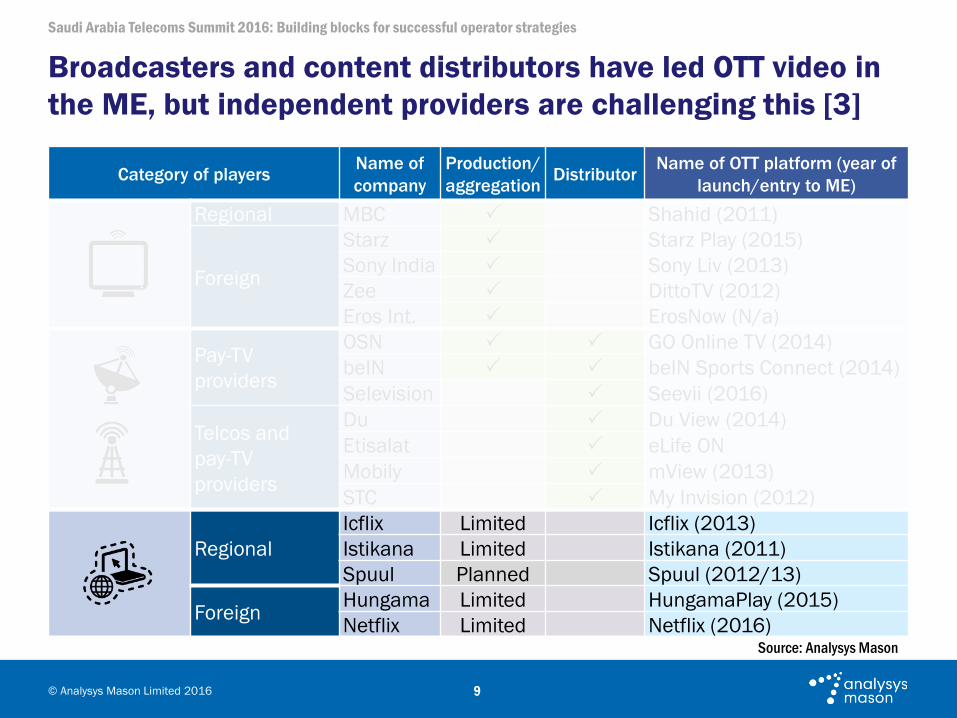

Broadcasters and content distributors have led OTT video in

the ME, but independent providers are challenging this [3]

9

Category of playersName of

company

Production/

aggregationDistributor

Name of OTT platform (year of

launch/entry to ME)

Regional MBC Shahid (2011)

Foreign

Starz Starz Play (2015)

Sony India Sony Liv (2013)

Zee DittoTV (2012)

Eros Int. ErosNow (N/a)

Pay-TV

providers

OSN GO Online TV (2014)

beIN beIN Sports Connect (2014)

Selevision Seevii (2016)

Telcos and

pay-TV

providers

Du Du View (2014)

Etisalat eLife ON

Mobily mView (2013)

STC My Invision (2012)

Regional

Icflix Limited Icflix (2013)

Istikana Limited Istikana (2011)

Spuul Planned Spuul (2012/13)

ForeignHungama Limited HungamaPlay (2015)

Netflix Limited Netflix (2016)Source: Analysys Mason

Saudi Arabia Telecoms Summit 2016: Building blocks for successful operator strategies

© Analysys Mason Limited 2016

OTT players have formed partnerships with operators and

vendors to increase their reach and facilitate payment

10

OTT value chain in the Middle East

Broadcasters and

movie producers

Access provider or

distributor

Device

manufacturers

Device

manufacturers

Distribution

partnership

Content partnership

OTT platform (local and foreign content

OTT platform (local and foreign content)

OTT platform (Western or niche content)

OTT platform (Arabic and local content)

Pay-TV operators

Telcos/IPTV operators

Local or regional

Foreign

Indian OTT players

Local and other foreign

players

OTT providers

Device partnership

Billing and discoverability partnership

No direct OTT

presence

Source: Analysys Mason

Saudi Arabia Telecoms Summit 2016: Building blocks for successful operator strategies

© Analysys Mason Limited 2016

Saudi Arabia: Rapid growth in the number of fibre

households will boost IPTV while OTT will be limited

11

PER MONTH

$

33.219%

PAY-TV MARKET KPIs 2021

11%

IPTV

DTH

OTT

Source: Analysys Mason

12%

67%

21%

IPTV DTH

OTT

33%

29%

22%

12%4%

beIN OSN

ART STC

PAY-TV MARKET LEADERS, 2015

Saudi Arabia Telecoms Summit 2016: Building blocks for successful operator strategies

© Analysys Mason Limited 2016

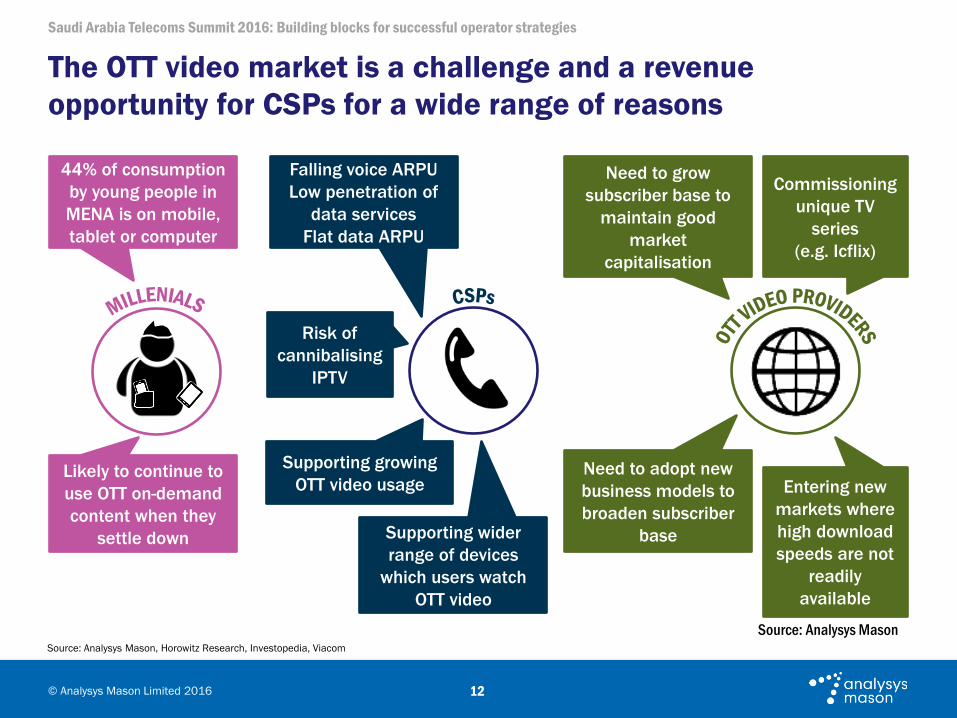

The OTT video market is a challenge and a revenue

opportunity for CSPs for a wide range of reasons

12

Likely to continue to

use OTT on-demand

content when they

settle down

44% of consumption

by young people in

MENA is on mobile,

tablet or computer

Supporting growing

OTT video usage

Supporting wider

range of devices

which users watch

OTT video

Falling voice ARPU

Low penetration of

data services

Flat data ARPU

Commissioning

unique TV

series

(e.g. Icflix)

Need to grow

subscriber base to

maintain good

market

capitalisation

Entering new

markets where

high download

speeds are not

readily

available

Need to adopt new

business models to

broaden subscriber

base

Source: Analysys Mason, Horowitz Research, Investopedia, Viacom

Risk of

cannibalising

IPTV

Source: Analysys Mason

Saudi Arabia Telecoms Summit 2016: Building blocks for successful operator strategies

© Analysys Mason Limited 2016

CSPs have several options for turning the growth of OTT video

consumption to their advantage

13

Partnerships

with OTT video

providers

Offering solutions

to providers of

OTT video

services

Launching OTT

video services to

extend reach and

revenue

Competition Co-operation

Co

st

co

ntr

ol

Re

ven

ue

ge

ne

rati

on 3 2

1

Source: Analysys Mason

Saudi Arabia Telecoms Summit 2016: Building blocks for successful operator strategies

© Analysys Mason Limited 2016

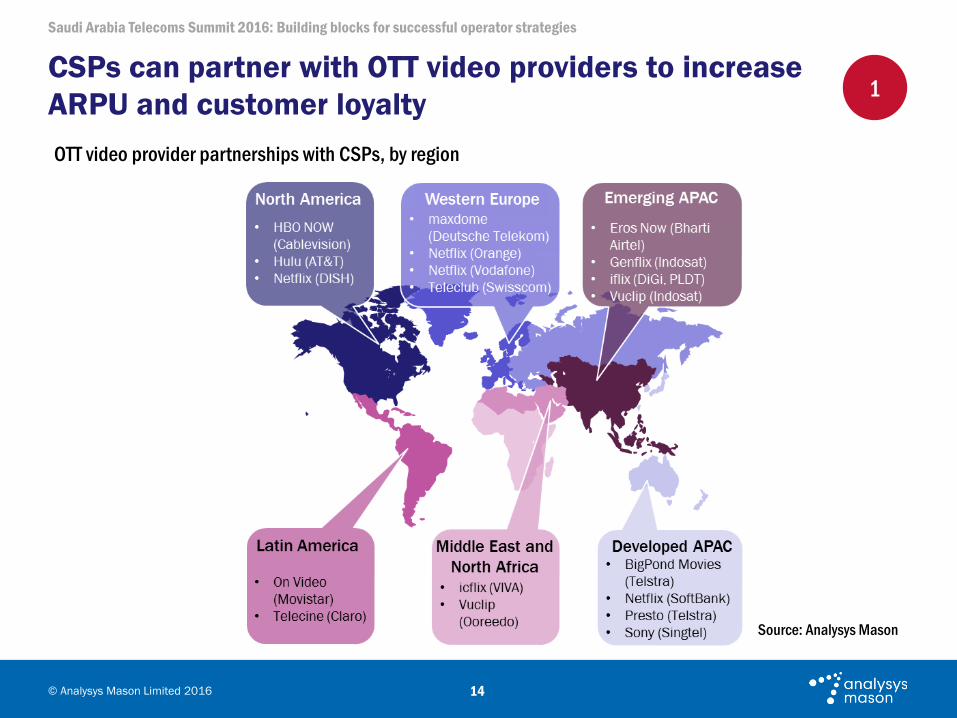

CSPs can partner with OTT video providers to increase

ARPU and customer loyalty

14

OTT video provider partnerships with CSPs, by region

1

Source: Analysys Mason

Saudi Arabia Telecoms Summit 2016: Building blocks for successful operator strategies

© Analysys Mason Limited 2016

OTT video providers can use CSPs to make content more

discoverable, but CSPs need to extend their capabilities

15

2

CSPs’ features and capabilities and their influence on the OTT video value chain

Subscriber

base

Basic

service

support

Enhanced

user

QoE

Enhanced

revenue

Increasing opportunity for CSPs and

appeal of CSPs to OTT video providers

Source: Analysys Mason

Saudi Arabia Telecoms Summit 2016: Building blocks for successful operator strategies

© Analysys Mason Limited 2016

CSPs can provide CDN services or partner with CDN

providers to support OTT video providers

16

Simple CDN and CSP network delivering OTT video

CSP CDN

Mobile

ISP (CSP)

Fixed ISP

(CSP)

Fixed broadband

access network

OTT video provider

Mobile broadband

access network

Users

Specialist CDN provider

2

Source: Analysys Mason

Saudi Arabia Telecoms Summit 2016: Building blocks for successful operator strategies

© Analysys Mason Limited 2016

CSPs may use OTT video to enhance an IPTV or pay-TV

service, or may offer OTT video as a standalone service

17

OTT video options to enable CSPs to extend reach and generate new revenue streams

Extend TV service

(TV everywhere)

1

Core CSP service1

(same country)

CSPThird party

OTT video options for CSP

Core CSP service

(different country)

Core CSP service

(same country)

Core CSP service

(fixed and mobile broadband) IPTV and

pay TV

Additional OTT video

2

Standalone OTT video

(foreign markets)

Standalone OTT video

and pay-TV lite

3

3

4

Source: Analysys Mason

Saudi Arabia Telecoms Summit 2016: Building blocks for successful operator strategies

© Analysys Mason Limited 2016

Key takeaways

18

1 The pay-TV subscription market in MENA will grow significantly

2 OTT video will have a mixed impact in the region

3 The growth of OTT video services provides CSPs with an opportunity

to support consumption and develop new revenue streams

Saudi Arabia Telecoms Summit 2016: Building blocks for successful operator strategies

© Analysys Mason Limited 2016

Contact details

19

Cambridge

Tel: +44 (0)1223 460600

Milan

Tel: +39 02 76 31 88 34

Dubai

Tel: +971 (0)4 446 7473

New Delhi

Tel: +91 124 4501860

Dublin

Tel: +353 (0)1 602 4755

Paris

Tel: +33 (0)1 72 71 96 96

London

Tel: +44 (0)20 7395 9000

Singapore

Tel: +65 6493 6038

Madrid

Tel: +34 91 399 5016

Manchester

Tel: +44 (0)161 877 7808

@AnalysysMason linkedin.com/company/analysys-mason youtube.com/AnalysysMason analysysmason.com/RSS

Karim Yaici

Senior Analyst

Boston

Tel: +1 202 331 3080

Hong Kong

Tel: +852 3669 7090

![[PreMoney MENA 2015] ArabNet >> Omar Christidis, "THE GLOBAL VC: MENA"](https://static.fdocuments.us/doc/165x107/58d198b51a28ab6f6b8b4a09/premoney-mena-2015-arabnet-omar-christidis-the-global-vc-mena.jpg)