Otis Gold Corp. · $400/ounce. With the technical ... Otis Gold Corp. Jeff Wu, ... EBM, which...

20

Equity Research Please see end of this report for important disclosures December 13, 2010 Rating: BUY Otis Gold Corp. Target Price: C$2.00 (OOO-TSXV) All figures in C$, unless otherwise noted Kilgore: US Gold Is Shining An Excellent Opportunity To Gain Exposure On Low-Cost Gold In The U.S.: Otis Gold’s Kilgore property provides investors with the opportunity to gain exposure to a potential new gold mine in the U.S., which was economic in 1996 when the price of gold was below $400/ounce. With the technical heritage from Echo Bay Mines, Otis Gold has the perfect management team to develop the Kilgore gold deposit. Potential Multi-Million-Ounce Gold Resource At Kilgore Property: With an updated NI 43-101 report expected in 2011, Otis Gold is expected to increase its existing gold resource at Kilgore’s Mine Ridge deposit in size and possibly grade. New drilling results from the adjacent Dog Bone Ridge target area could generate positive surprises for Otis’ shareholders. It is highly possible that the Kilgore property could become a million-ounce low-cost open-pit gold mine in the near future. Nearly 200% Upside Potential Toward Its Intrinsic Value: Based on our financial model, Otis Gold’s stock price is trading at 0.34x NAV, a significant discount to other junior gold mining companies. We initiate coverage on Otis Gold with a BUY recommendation and a $2.00 price target based on a 1x NAV multiple. Source: www.bigcharts.com Recent Price: $0.64 52 Week Range $0.37–$0.76 Shares O/S basic (MM): 33.3 f.d. (MM): 45.6 Market Cap (MM): $21.3 Net Cash (Estimated) (MM): $3.2 Enterprise Value (MM) $18.1 Fiscal Year End: Jun. 30 Financials 2011E 2012E Production (oz 000s) 0 0 Revenue (US$M) $0 $0 Cash Flow/Share ($0.04) ($0.06) Price/Cash Flow N/A N/A Commodities 2011E 2012E Gold (avg. in US$/oz) $1,325 $1,225 Company Description: Otis Gold Corp. engages in the acquisition and development of gold and precious metal properties primarily in the United States. On July 15, 2008, the company acquired an option to acquire a 75% interest in the Kilgore Gold Project, located in Clark County, Idaho and the Hai and Gold Bug properties, located in Lemhi County, Idaho. Additionally, they signed an agreement to acquire a 100% interest in the Blue Hill Creek Project located in Cassia County, Idaho. On November 30, 2010, the company announced an agreement to increase its interest in the Kilgore Gold, Hai and Gold Bug projects to 100%. Its current projects include the: Kilgore Gold Project, Oakley Gold Project, Buckhorn Silver Project, Hai Gold Project and the Gold Bug Project. Jeff Wu, CFA Mining Analyst 604-697-2455 [email protected]

Transcript of Otis Gold Corp. · $400/ounce. With the technical ... Otis Gold Corp. Jeff Wu, ... EBM, which...

Equity Research

Please see end of this report for important disclosures

December 13, 2010

Rating: BUY Otis Gold Corp. Target Price: C$2.00 (OOO-TSXV)

All figures in C$, unless otherwise noted Kilgore: US Gold Is Shining

An Excellent Opportunity To Gain Exposure On Low-Cost Gold In The U.S.: Otis Gold’s Kilgore property provides investors with the opportunity to gain exposure to a potential new gold mine in the U.S., which was economic in 1996 when the price of gold was below $400/ounce. With the technical heritage from Echo Bay Mines, Otis Gold has the perfect management team to develop the Kilgore gold deposit.

Potential Multi-Million-Ounce Gold Resource At Kilgore Property: With an updated NI 43-101 report expected in 2011, Otis Gold is expected to increase its existing gold resource at Kilgore’s Mine Ridge deposit in size and possibly grade. New drilling results from the adjacent Dog Bone Ridge target area could generate positive surprises for Otis’ shareholders. It is highly possible that the Kilgore property could become a million-ounce low-cost open-pit gold mine in the near future.

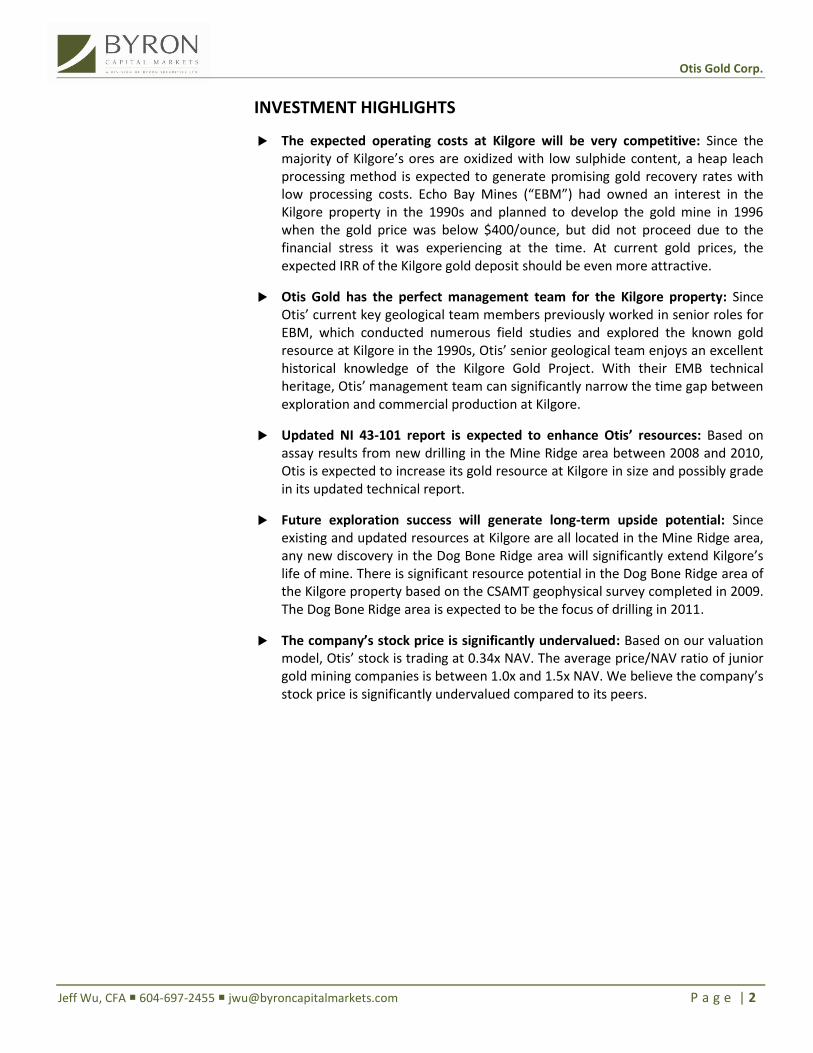

Nearly 200% Upside Potential Toward Its Intrinsic Value: Based on our financial model, Otis Gold’s stock price is trading at 0.34x NAV, a significant discount to other junior gold mining companies. We initiate coverage on Otis Gold with a BUY recommendation and a $2.00 price target based on a 1x NAV multiple.

Source: www.bigcharts.com

Recent Price: $0.64 52 Week Range $0.37–$0.76 Shares O/S basic (MM): 33.3 f.d. (MM): 45.6 Market Cap (MM): $21.3 Net Cash (Estimated) (MM): $3.2 Enterprise Value (MM) $18.1 Fiscal Year End: Jun. 30

Financials 2011E 2012E Production (oz 000s) 0 0 Revenue (US$M) $0 $0 Cash Flow/Share ($0.04) ($0.06) Price/Cash Flow N/A N/A

Commodities 2011E 2012E Gold (avg. in US$/oz) $1,325 $1,225

Company Description: Otis Gold Corp. engages in the acquisition and development of gold and precious metal properties primarily in the United States. On July 15, 2008, the company acquired an option to acquire a 75% interest in the Kilgore Gold Project, located in Clark County, Idaho and the Hai and Gold Bug properties, located in Lemhi County, Idaho. Additionally, they signed an agreement to acquire a 100% interest in the Blue Hill Creek Project located in Cassia County, Idaho. On November 30, 2010, the company announced an agreement to increase its interest in the Kilgore Gold, Hai and Gold Bug projects to 100%. Its current projects include the: Kilgore Gold Project, Oakley Gold Project, Buckhorn Silver Project, Hai Gold Project and the Gold Bug Project.

Jeff Wu, CFA Mining Analyst 604-697-2455 [email protected]

Otis Gold Corp.

Jeff Wu, CFA 604-697-2455 [email protected] P a g e | 2

INVESTMENT HIGHLIGHTS

The expected operating costs at Kilgore will be very competitive: Since the majority of Kilgore’s ores are oxidized with low sulphide content, a heap leach processing method is expected to generate promising gold recovery rates with low processing costs. Echo Bay Mines (“EBM”) had owned an interest in the Kilgore property in the 1990s and planned to develop the gold mine in 1996 when the gold price was below $400/ounce, but did not proceed due to the financial stress it was experiencing at the time. At current gold prices, the expected IRR of the Kilgore gold deposit should be even more attractive.

Otis Gold has the perfect management team for the Kilgore property: Since Otis’ current key geological team members previously worked in senior roles for EBM, which conducted numerous field studies and explored the known gold resource at Kilgore in the 1990s, Otis’ senior geological team enjoys an excellent historical knowledge of the Kilgore Gold Project. With their EMB technical heritage, Otis’ management team can significantly narrow the time gap between exploration and commercial production at Kilgore.

Updated NI 43-101 report is expected to enhance Otis’ resources: Based on assay results from new drilling in the Mine Ridge area between 2008 and 2010, Otis is expected to increase its gold resource at Kilgore in size and possibly grade in its updated technical report.

Future exploration success will generate long-term upside potential: Since existing and updated resources at Kilgore are all located in the Mine Ridge area, any new discovery in the Dog Bone Ridge area will significantly extend Kilgore’s life of mine. There is significant resource potential in the Dog Bone Ridge area of the Kilgore property based on the CSAMT geophysical survey completed in 2009. The Dog Bone Ridge area is expected to be the focus of drilling in 2011.

The company’s stock price is significantly undervalued: Based on our valuation model, Otis’ stock is trading at 0.34x NAV. The average price/NAV ratio of junior gold mining companies is between 1.0x and 1.5x NAV. We believe the company’s stock price is significantly undervalued compared to its peers.

Otis Gold Corp.

Jeff Wu, CFA 604-697-2455 [email protected] P a g e | 3

INTRODUCTION

Overview

Otis Gold Corp. engages in the acquisition and development of gold and precious metal properties, primarily in the United States. On July 15, 2008, the company acquired an option to acquire a 75% interest in the Kilgore Gold Project, located in Clark County, Idaho and the Hai and Gold Bug properties, located in Lemhi County, Idaho. Additionally, they signed an agreement to acquire a 100% interest in the Blue Hill Creek Project located in Cassia County, Idaho. On November 30, 2010, the company announced an agreement to increase its interest in the Kilgore Gold, Hai and Gold Bug projects to 100% interest. Its current projects include the: Kilgore Gold Project, Oakley Gold Project, Buckhorn Silver Project, Hai Gold Project and the Gold Bug Project.

Otis’ current flagship asset is the Kilgore Gold Project, a potential open-pit gold mine with low operating costs. Otis recently entered a purchase agreement to acquire a 100% interest in the Kilgore property at a relatively low cost. With an environmental scoping study to be completed in December 2010, and 3-D modelling and an updated NI 43-101 compliant resource report expected in 2011, Otis will be ready to move Kilgore toward a feasibility study and ultimately become a low-cost gold producer.

Based in Vancouver, B.C., Otis’ management team is led by President Craig Lindsay, a financial and industry expert. Mr. Lindsay has assembled an excellent management team with strong track records in the industry.

MANAGEMENT AND DIRECTORS (Full bios can be found in Appendix I) Craig Lindsay President Mitch Bernardi Chief Geologist John Carden Consulting Geologist Donald E. Ranta Director Charles W. (“Bill”) Reed Director Norm Eyolfson Director Sean Mitchell Director

KILGORE GOLD PROJECT

History

Although early gold exploration at the prospect started in the 1930s, major exploration activities at Kilgore were completed in the 1990s, especially by EBM.

Otis Gold Corp.

Jeff Wu, CFA 604-697-2455 [email protected] P a g e | 4

EBM acquired an interest in the Kilgore property through a joint venture with Placer Dome on June 30, 1994. Work performed by EBM was focused at the Mine Ridge deposit and included: 82,987 feet of drilling in 122 holes; re-logging of all previous drill holes; bottle roll and column leach metallurgical studies; airborne HEM surveying; regional geologic mapping; soil sampling of the back-side sinter target; collection of baseline environmental data; manual cross-sectional resource estimates; and 3D geologic modeling. EBM optioned the property to Latitude Minerals Corporation in early 1998 due to its own financial stress.

In 2002, Kilgore Minerals acquired a 100% interest in the Kilgore property and in the fall of 2003, carried out a program of geologic mapping, surface sampling and structural interpretation at the Dog Bone Ridge target area. In 2004, Kilgore Minerals carried out a diamond drill program at Dog Bone Ridge, which entailed drilling six holes for a total of 5,319 feet. The drill program discovered high-grade gold mineralization within a wide zone of bulk tonnage gold mineralization. Subsequently, Kilgore Minerals (which also controlled a range of uranium assets in the USA) was acquired by Bayswater.

On November 30, 2010, Otis announced that it entered an agreement to purchase a 100% interest in the Kilgore Gold Project and related assets from Bayswater for staged payments of $1.75 million and 2 million shares. The deal also eliminated the existing 2% NSR. The purchase agreement replaced the previous agreement signed in 2008, in which Otis was required to issue an additional 2.2 million shares and complete a pre-feasibility study to acquire a 75% interest in the Kilgore Gold Project and related assets.

Property Description

The property is located in southeastern Idaho within Clark County, 72 miles north of Idaho Falls. The Kilgore property is covered by 162 federal lode mining claims totalling 3,240 acres. The highest elevation on the property is 8,362 feet and the area receives a significant amount of snowfall in the winter. Experienced mining labour for the project’s development can be easily found from northern Idaho and Nevada.

Since the drainage system at Kilgore is internal with no salmon or other spawning issues, and the property is located outside of Yellowstone “viewshed”, the Kilgore property’s environmental risks are limited.

The Kilgore deposit is a volcanic-hosted epithermal gold deposit. The deposit type is common in the western United States with notable examples like Round Mountain in Nevada and McDonald Meadows in Montana. Controls on gold mineralization are typically a combination of host-rock permeability and structure.

The recent acquisition

of a 100% interest in

the Kilgore Gold Project

significantly enhanced

shareholders’ value.

Otis Gold Corp.

Jeff Wu, CFA 604-697-2455 [email protected] P a g e | 5

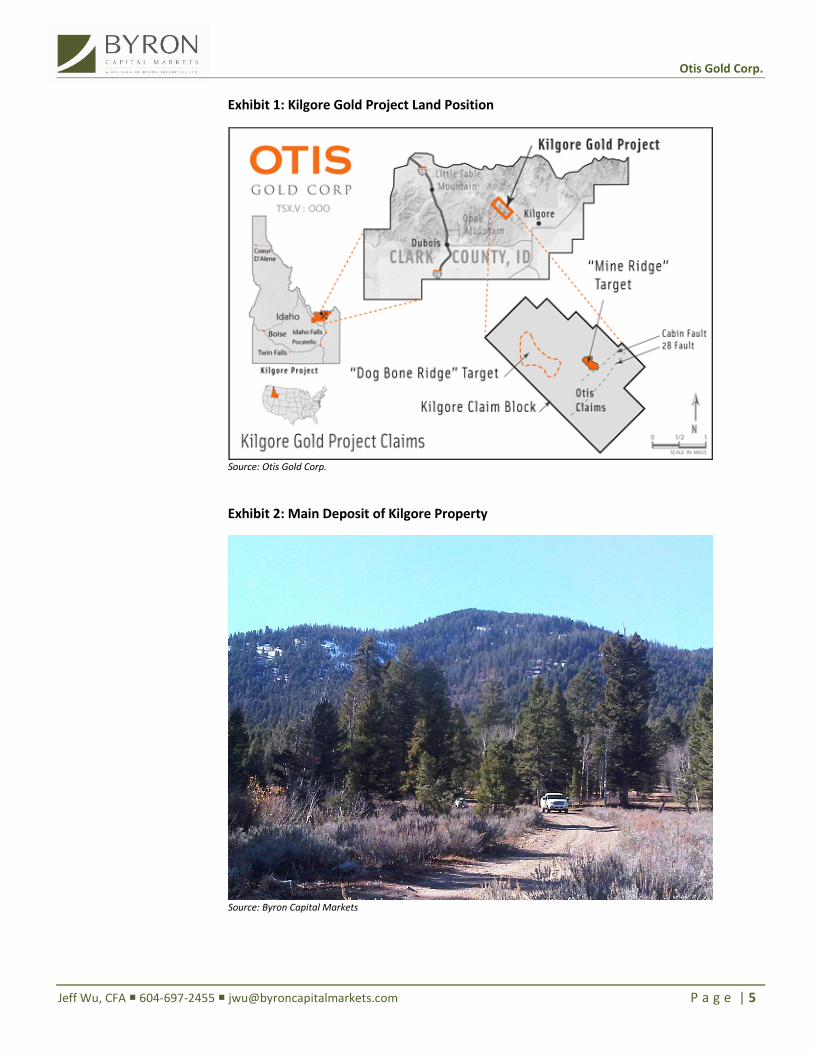

Exhibit 1: Kilgore Gold Project Land Position

Source: Otis Gold Corp.

Exhibit 2: Main Deposit of Kilgore Property

Source: Byron Capital Markets

Otis Gold Corp.

Jeff Wu, CFA 604-697-2455 [email protected] P a g e | 6

Exhibit 3: NI 43-101 Compliant Resources for Kilgore Gold Deposit (2002)

* Based on the NI 43-101 report for Kilgore Minerals Ltd. (2002) Source: Otis Gold Corp.

Mineralization

The Kilgore deposit is related to a zoned epithermal hot-spring system in volcanic rocks of Miocene age. The age of the property’s mineralization is around 5.3 million years. The main Kilgore resource is located along a major northwest trending fault zone. Higher gold values are typically associated with pyrite enrichment.

Exhibit 4: Generalized Geologic Cross Section of Kilgore Gold Property

Source: Otis Gold Corp.

Kilgore’s geologic model is low-sulphide, associated with quartz-adularia-carbonate-sericite alteration. In general, volcanic-hosted precious metal deposits have the potential to be high-tonnage and low-grade overall. For example, the Round Mountain deposit is mined with an average grade of about 0.02 ounces per tonne (“opt”) of ore and will produce more than 200 million tons of ore over the mine’s life. Locally, the deposit may have high-grade zones, typically within discrete structures.

Category Cut-Off Grade Tonnes Au Grade Au Ounces

Indicated Resources 0.01 oz/t 7.043 million 0.031 oz/t 218,000

Inferred Resources 0.01 oz/t 9.661 million 0.028 oz/t 269,000

Total 0.01 oz/t 16.704 million 0.029 oz/t 487,000

An historic non-NI

43-101 compliant

resource of 706,000

ounces with an

average grade of 1.1

grams/tonne was

calculated by EBM

Otis Gold Corp.

Jeff Wu, CFA 604-697-2455 [email protected] P a g e | 7

Exhibit 5: Drilling Samples from Mine Ridge Area of Kilgore Property

Hole 10 OKC-228 (assays pending) Source: Byron Capital Markets

Metallurgical Testing

The Kilgore Gold Project has three distinct ore types identified as oxide, non-oxide and mixed (partially oxidized). In 1995, the first metallurgical study was performed using both RC cuttings and core composites. Gold extractability results are very encouraging (see Exhibit 6).

Exhibit 6: Metallurgical Test Results

Source: Otis Gold Corp.

In 1996, column leach tests were performed on a coarser crush size, in which low-grade (0.023 opt Au) mixed oxide-sulfide ore was crushed to minus 1 inch. The extraction of 86.9% Au after 75 days of leach time is excellent.

Based on the promising metallurgical recovery rates, a heap leaching operation method could be used in future gold production.

Otis Gold Corp.

Jeff Wu, CFA 604-697-2455 [email protected] P a g e | 8

Exploration

The Kilgore gold deposit has received a considerable amount of exploration attention beginning in the 1990s. The most active period was from 1994 to 1997, when EBM conducted numerous field studies and drilled out the known gold resource. From 1994 to 1996, EBM drilled 55 RC holes and 67 diamond holes at Kilgore for a total of 82,897 feet.

Since Otis’ key geological team members previously worked for EBM, Otis’ senior geological team enjoys an excellent historical knowledge of the Kilgore Gold Project. For example, Mr. Mitch Bernadi, Otis’s Chief Geologist, was a senior geologist responsible for a 3.5-year EBM drill program at Kilgore. Dr. John Carden, Otis’ Consulting Geologist, was EBM’s Director of U.S. Exploration.

In 2008, Otis submitted a “20 site” Plan of Operation that was accepted by the Caribou-Targhee National Forest. Otis completed four core drilling holes with 700 metres in 2008. The assay results of those four core holes confirm the presence of high-grade gold values from potentially mineable thicknesses and intervals within a higher-grade core zone in the Kilgore Mine Ridge area. The results also confirm the presence of quartz stockwork vein-type gold mineralization.

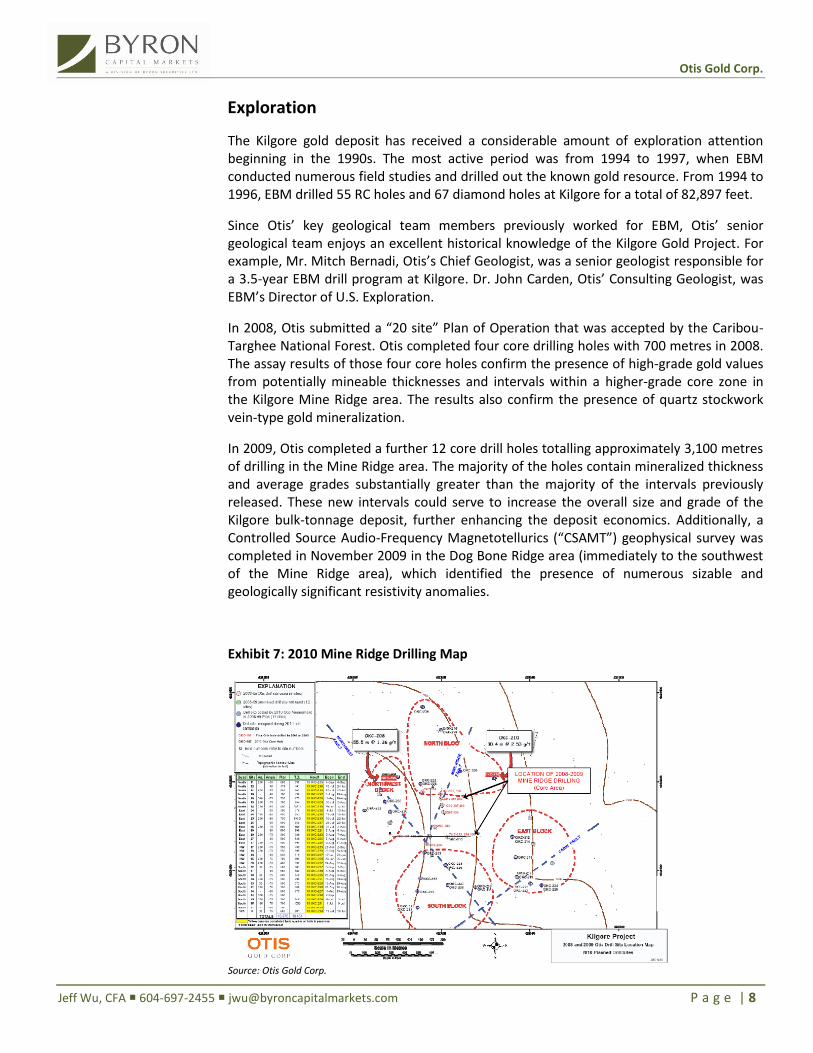

In 2009, Otis completed a further 12 core drill holes totalling approximately 3,100 metres of drilling in the Mine Ridge area. The majority of the holes contain mineralized thickness and average grades substantially greater than the majority of the intervals previously released. These new intervals could serve to increase the overall size and grade of the Kilgore bulk-tonnage deposit, further enhancing the deposit economics. Additionally, a Controlled Source Audio-Frequency Magnetotellurics (“CSAMT”) geophysical survey was completed in November 2009 in the Dog Bone Ridge area (immediately to the southwest of the Mine Ridge area), which identified the presence of numerous sizable and geologically significant resistivity anomalies.

Exhibit 7: 2010 Mine Ridge Drilling Map

Source: Otis Gold Corp.

Otis Gold Corp.

Jeff Wu, CFA 604-697-2455 [email protected] P a g e | 9

In 2010, Otis completed 35 core drill holes totalling approximately 6,300 metres of drilling in the Mine Ridge area and five core drill holes totalling approximately 1,100 metres of drilling in the Dog Bone Ridge area. The focus of the drilling was on resource delineation at Mine Ridge and the testing of geophysical targets at Dog Bone Ridge. Assay results of the initial 13 holes at Mine Ridge were released recently and generated promising results. All holes except 10 OKC-216, which was drilled along the northern periphery of the deposit, encountered mineralization. Hole 10 OKC-208 and Hole 10 OKC-210 intersected 1.36 gram per tonne (“gpt”) Au and 2.53 gpt Au over true widths of 55.5 metres and 30.4 metres, respectively. Hole 10 OKC-215 and Hole 10 OKC-222 intersected 1.3 gpt Au and 1.32 gpt Au over true widths of 41.1 metres and 45.7 metres, respectively.

All existing drilling data supports a high degree of confidence concerning the continuity of mineralization throughout the deposit. Based on new drilling results, Otis is expected to increase the overall size (and possibly grade) and enhance the economic viability of the Kilgore deposit. An updated NI 43-101 report is expected to be released in 2011. The company is also working on a plan to outline a sizeable bulk mineable deposit area that can be mined by open-pit methods. An environmental scoping study report is expected to be completed by the end of this year.

Valuation

We use a NAV methodology to value the Kilgore project, similar to other companies in our universe. We have employed an 8% discount rate in our valuation.

Our assumptions of life of mine (“LOM”), mining and processing methods are based on EBM’s Initial Engineering Assessment1. EBM had planned to develop the Kilgore gold mine 14 years ago, but failed to proceed due to EBM’s subsequent financial stress. We assume the LOM at Kilgore is seven years, beginning in July 2013 (fiscal 2014), with annual production of approximately 60,000 ounces of gold. We expect the company to adopt an open-pit mining and heap leaching operation with processing capacity of 5,000 tonnes per day. In our model, we include only the published NI 43-101 compliant resources and assume the average gold recovery rate is 86%.

Exhibit 8: Key Parameters Comparison between Kilgore and La India

* Byron Capital Markets estimates Source: Grayd Resource, Echo Bay Mines, Byron Capital Markets

1 Echo Bay Mines: Memorandum, Kilgore, Idaho Project – Initial Engineering Assessment (August 27, 1996)

Company Project Life of

Mine

(Years)

Initial

Capex

($million)

Sustaining

Capex

($million)

Open-pit

Capacity

(tpd)

Au Grade

(g/t)

Recovery

Rate

Annual

Production

(ounce Au)

Strip

Ratio

Total

Operating

Cost ($/t ore)

Cash Cost Per

Ounce Au ($)

Grayd Resource La India 11 90 23 16,000 0.63 84% 93,900 0.69 8.45 496

Otis Gold Kilgore* 7 30 18 5,000 1.2 86% 60,000 2.7 19.1 576

Based on released

assay results from

new drilling holes,

updated gold

resource at Kilgore

could reach nearly 1

million ounces in the

near future

EBM had planned to

develop the Kilgore

mine when the gold

price was below

$400/ounce; Kilgore’s

projected operating

cost will be very

competitive at current

gold prices

Otis Gold Corp.

Jeff Wu, CFA 604-697-2455 [email protected] P a g e | 10

Since Otis’ Kilgore project and Grayd Resource’s (GYD-TSXV, Buy, Target $2.60) La India Gold Project share many similarities, key parameters of those two projects’ capex are comparable for their future development (Exhibit 8). Based on our analyst’s research report on Grayd Resource, the initial capex on La India is about $90 million for processing capacity of 16,000 tpd or $5,625 per tpd. Our initial capex assumption for Kilgore is around $6,000 per tpd or $30 million for processing capacity of 5,000 tpd, with overall sustaining capex of $18 million during the production period.

Since Otis currently has no financing plan, we have not included any financing activity in our model. According to our NPV model, the Kilgore property is valued at $74 million or $1.60/share based on the company’s expected fully diluted capital structure.

Exhibit 9: NPV Model — Kilgore Gold Project

Source: Otis Gold, Echo Bay Mine, Byron Capital Markets

Outlook

With an environmental scoping study, 3-D modelling, an updated NI 43-101 report and a last round of infill drilling at Mine Ridge slated for 2011, Otis will be ready to move toward a feasibility study and ultimately transform itself into a low-cost production company. With the technical heritage from EBM, Otis’ management team can significantly narrow the time gap between exploration and commercial production at Kilgore.

Since existing and updated resources at Kilgore are all located in the Mine Ridge area, any new discovery in the Dog Bone Ridge area will significantly extend Kilgore’s LOM. There is significant potential for additional discoveries in the Dog Bone Ridge area based on the CSAMT geophysical survey completed in 2009 and historic drilling conducted in the area.

2011E 2012E 2013E 2014E 2015E 2016E 2017E 2018E 2019E 2020E Total

Au Price ($/oz) 1,325 1,225 1,125 1,050 1,000 1,000 1,000 1,000 1,000 1,000

C$ / US$ 1.02 1.08 1.10 1.04 1.11 1.11 1.11 1.11 1.11 1.11

Au Production(Koz) 60 60 60 60 60 60 60 418

Revenue(million $) 63 60 60 60 60 60 60 421

Ore mined (million tons) 1.8 1.8 1.8 1.8 1.8 1.8 1.8 12.6

Mining cost (million $) 20.0 20.0 20.0 20.0 20.0 20.0 20.0 139.9

Processing cost (million $) 14.4 14.4 14.4 14.4 14.4 14.4 14.4 100.8

Cash cost ($/oz) 576 576 576 576 576 576 576 576

Operating cash cost (million $) (34) (34) (34) (34) (34) (34) (34) (241)

Capex (million $) (15) (15) (2) (2) (2) (2) (2) (2) (6) (48)

Other expense (million $) (4.00) (1.25)

Operating cash flow (million C$) (4) (17) (16) 27 26 26 26 26 26 21 141

Discount rate 8%

NPV (million C$) 74

1.2

2.70

Processing capacity (tpd) 5,000

86%

3.00

Processing cost and G&A($/t) 8.00

Strip ratio

Mining cost ($/t)

Recovery rate

Ore grade (g/t)

With incremental

resources from an

updated NI 43-101

report expected in

2011, Kilgore’s NPV

could increase

significantly

Otis Gold Corp.

Jeff Wu, CFA 604-697-2455 [email protected] P a g e | 11

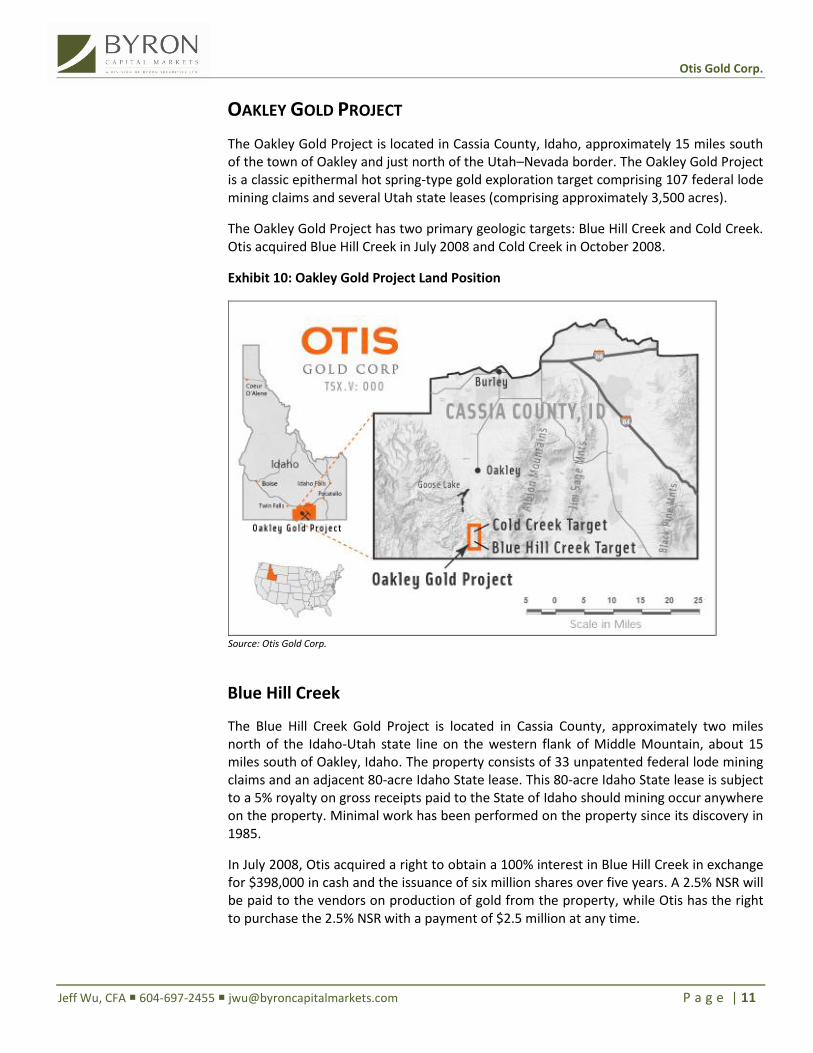

OAKLEY GOLD PROJECT

The Oakley Gold Project is located in Cassia County, Idaho, approximately 15 miles south of the town of Oakley and just north of the Utah–Nevada border. The Oakley Gold Project is a classic epithermal hot spring-type gold exploration target comprising 107 federal lode mining claims and several Utah state leases (comprising approximately 3,500 acres).

The Oakley Gold Project has two primary geologic targets: Blue Hill Creek and Cold Creek. Otis acquired Blue Hill Creek in July 2008 and Cold Creek in October 2008.

Exhibit 10: Oakley Gold Project Land Position

Source: Otis Gold Corp.

Blue Hill Creek

The Blue Hill Creek Gold Project is located in Cassia County, approximately two miles north of the Idaho-Utah state line on the western flank of Middle Mountain, about 15 miles south of Oakley, Idaho. The property consists of 33 unpatented federal lode mining claims and an adjacent 80-acre Idaho State lease. This 80-acre Idaho State lease is subject to a 5% royalty on gross receipts paid to the State of Idaho should mining occur anywhere on the property. Minimal work has been performed on the property since its discovery in 1985.

In July 2008, Otis acquired a right to obtain a 100% interest in Blue Hill Creek in exchange for $398,000 in cash and the issuance of six million shares over five years. A 2.5% NSR will be paid to the vendors on production of gold from the property, while Otis has the right to purchase the 2.5% NSR with a payment of $2.5 million at any time.

Otis Gold Corp.

Jeff Wu, CFA 604-697-2455 [email protected] P a g e | 12

Cold Creek

The Cold Creek Gold Project, located in Cassia County, Idaho, comprises 53 unpatented federal lode mining claims located approximately five miles north of the company’s Blue Hill Creek Gold Project.

Gold mineralization at Cold Creek was originally discovered by Meridian Minerals in the summer of 1985. In October 2008, Otis acquired those 53 claims in exchange for payment of the costs associated with staking the property.

Property Description

The Blue Hill Creek gold property is located in southern Cassia County, Idaho. The Cold Creek gold property lies approximately 13 miles south of Oakley, Idaho.

Exhibit 11: Landscape of Oakley Property

Source: Otis Gold Corp.

The topography of Cassia County is primarily high mountain desert with elevations ranging from 4,100 feet to 8,000 feet. The Blue Hill Creek precious metal system is part of a larger, north-trending, 5-mile- by 1-mile-wide belt of scattered precious metal anomalies along the west flank of Middle Mountain, which serves as the westernmost extension of the Albion Range metamorphic core complex.

Exhibit 12: Resources of Oakley Gold Project

Source: Otis Gold Corp.

Area Category Tonnes Au Grade Au Ounces Status

Blue Hill Creek Inferred Resources 14.439 million 0.0163 oz/t 235,200 NI 43-101

Cold Creek Inferred Resources 3.4 million 0.025 oz/t 85,000 Historic

Otis Gold Corp.

Jeff Wu, CFA 604-697-2455 [email protected] P a g e | 13

Mineralization

Mineralization at Blue Hill Creek is an epithermal precious metals deposit type, classically characterized by its bulk-tonnage, low-grade, open-pittable nature and commonly found in the Basin and Range geologic province of the western United States.

Gold mineralization and alteration are present within two distinct environments in the Blue Hill Creek area. Of the two environments, the altered Tertiary section and underlying Paleozoics contain the best potential for the discovery of a bulk-tonnage epithermal gold deposit. Prior drilling results showed that oxidation extends throughout the entire length of most holes and into the carbonate basement, suggesting potential for good deposit metallurgy.

Similar to Blue Hill Creek, disseminated, bulk-tonnage, epithermal hot spring-type gold mineralization was discovered at Cold Creek in 1985, where alteration and gold mineralization are hosted by Tertiary Salt Lake Formation epiclastic sedimentary and tuffaceous volcanic rocks.

Exploration

A total of 7,717 feet in 21 RC holes was drilled by Meridian Minerals at Blue Hill Creek and surrounding targets during 1986 and 1987. These drill results confirmed the presence of substantial thicknesses of gold mineralization in the known resource area, as well as the potential for additional mineralization along the open-ended, lateral and at depth extensions of the deposit.

In July 1998, Latitude Minerals Corp. conducted a 4,528-foot drilling program spread among nine RC holes. Overall, the results confirmed the mineralization indicated by Meridian Mineral’s drilling programs and increased the known extent of the mineralization, which remains open in all directions laterally and at depth. Results of Latitude’s drilling increased the dimensions of the main target area to 3,350-feet long by 1,000-feet wide by an average of 250-feet thick, all of which remains open-ended.

Gold mineralization at Cold Creek was originally discovered by Meridian Minerals in the summer of 1985. A total of 9,205 feet in 38 RC holes was drilled by Meridian in 1986 and 1987 and by WestGold in 1988 to partially test the Tertiary-hosted target. These results confirmed the presence of significant thicknesses of mineralization in the known resource area, as well as the potential for additional mineralization along the open-ended, lateral extensions of the deposit.

In January 2009, Otis announced the results of a CSAMT geophysical survey that indicated the presence of a sizeable and geologically significant, 1.5-kilometre low-resistivity anomaly underlying and extending downdip from Blue Hill Creek and the precious metals target area. Smaller, but geologically significant, CSAMT anomalies were also identified underlying and extending beyond Otis’ Cold Creek gold deposit and target area. Otis has permitted a drill program at Blue Hill Creek, and is seeking a joint-venture partner for drilling operations.

There is a high-

growth potential

for Oakley’s long-

term resources

Otis Gold Corp.

Jeff Wu, CFA 604-697-2455 [email protected] P a g e | 14

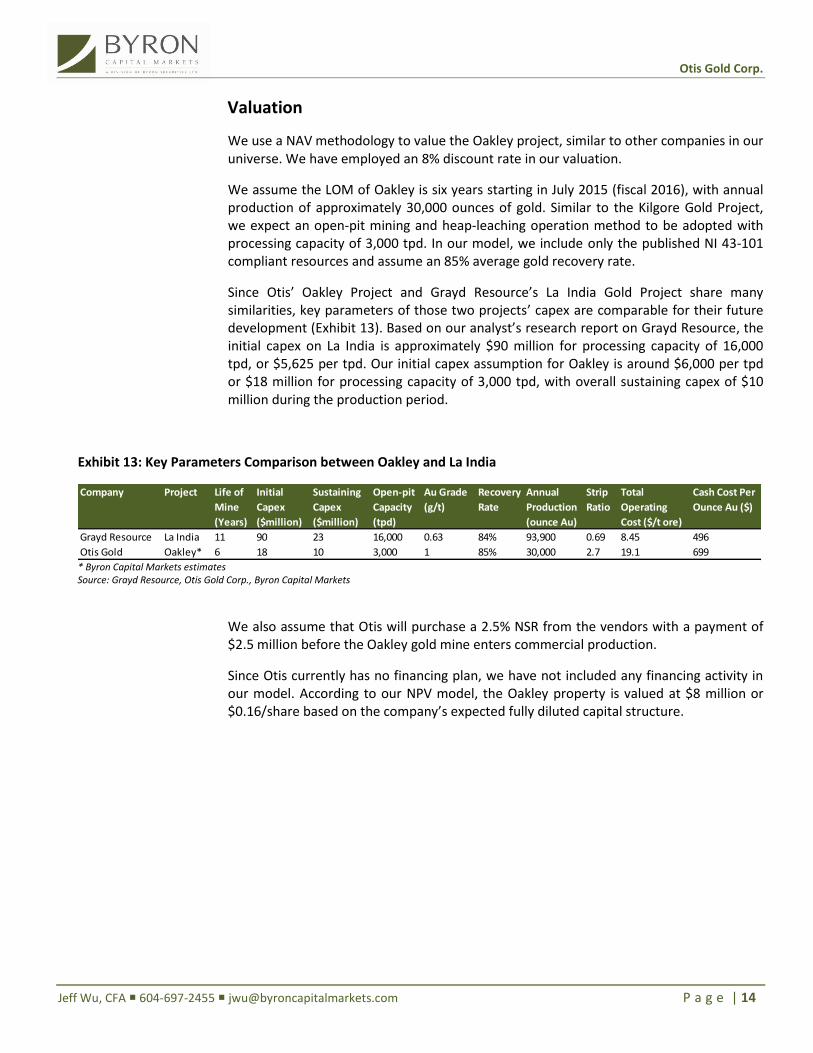

Valuation

We use a NAV methodology to value the Oakley project, similar to other companies in our universe. We have employed an 8% discount rate in our valuation.

We assume the LOM of Oakley is six years starting in July 2015 (fiscal 2016), with annual production of approximately 30,000 ounces of gold. Similar to the Kilgore Gold Project, we expect an open-pit mining and heap-leaching operation method to be adopted with processing capacity of 3,000 tpd. In our model, we include only the published NI 43-101 compliant resources and assume an 85% average gold recovery rate.

Since Otis’ Oakley Project and Grayd Resource’s La India Gold Project share many similarities, key parameters of those two projects’ capex are comparable for their future development (Exhibit 13). Based on our analyst’s research report on Grayd Resource, the initial capex on La India is approximately $90 million for processing capacity of 16,000 tpd, or $5,625 per tpd. Our initial capex assumption for Oakley is around $6,000 per tpd or $18 million for processing capacity of 3,000 tpd, with overall sustaining capex of $10 million during the production period.

Exhibit 13: Key Parameters Comparison between Oakley and La India

* Byron Capital Markets estimates Source: Grayd Resource, Otis Gold Corp., Byron Capital Markets

We also assume that Otis will purchase a 2.5% NSR from the vendors with a payment of $2.5 million before the Oakley gold mine enters commercial production.

Since Otis currently has no financing plan, we have not included any financing activity in our model. According to our NPV model, the Oakley property is valued at $8 million or $0.16/share based on the company’s expected fully diluted capital structure.

Company Project Life of

Mine

(Years)

Initial

Capex

($million)

Sustaining

Capex

($million)

Open-pit

Capacity

(tpd)

Au Grade

(g/t)

Recovery

Rate

Annual

Production

(ounce Au)

Strip

Ratio

Total

Operating

Cost ($/t ore)

Cash Cost Per

Ounce Au ($)

Grayd Resource La India 11 90 23 16,000 0.63 84% 93,900 0.69 8.45 496

Otis Gold Oakley* 6 18 10 3,000 1 85% 30,000 2.7 19.1 699

Otis Gold Corp.

Jeff Wu, CFA 604-697-2455 [email protected] P a g e | 15

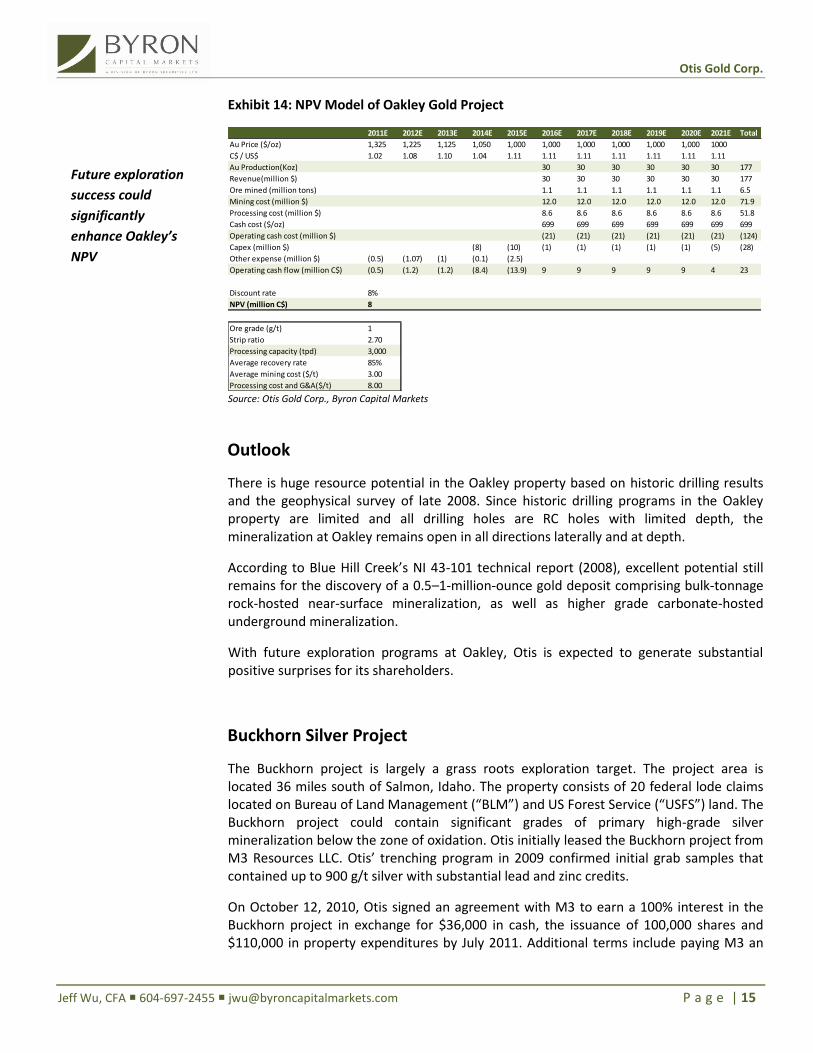

Exhibit 14: NPV Model of Oakley Gold Project

Source: Otis Gold Corp., Byron Capital Markets

Outlook

There is huge resource potential in the Oakley property based on historic drilling results and the geophysical survey of late 2008. Since historic drilling programs in the Oakley property are limited and all drilling holes are RC holes with limited depth, the mineralization at Oakley remains open in all directions laterally and at depth.

According to Blue Hill Creek’s NI 43-101 technical report (2008), excellent potential still remains for the discovery of a 0.5–1-million-ounce gold deposit comprising bulk-tonnage rock-hosted near-surface mineralization, as well as higher grade carbonate-hosted underground mineralization.

With future exploration programs at Oakley, Otis is expected to generate substantial positive surprises for its shareholders.

Buckhorn Silver Project

The Buckhorn project is largely a grass roots exploration target. The project area is located 36 miles south of Salmon, Idaho. The property consists of 20 federal lode claims located on Bureau of Land Management (“BLM”) and US Forest Service (“USFS”) land. The Buckhorn project could contain significant grades of primary high-grade silver mineralization below the zone of oxidation. Otis initially leased the Buckhorn project from M3 Resources LLC. Otis’ trenching program in 2009 confirmed initial grab samples that contained up to 900 g/t silver with substantial lead and zinc credits.

On October 12, 2010, Otis signed an agreement with M3 to earn a 100% interest in the Buckhorn project in exchange for $36,000 in cash, the issuance of 100,000 shares and $110,000 in property expenditures by July 2011. Additional terms include paying M3 an

2011E 2012E 2013E 2014E 2015E 2016E 2017E 2018E 2019E 2020E 2021E Total

Au Price ($/oz) 1,325 1,225 1,125 1,050 1,000 1,000 1,000 1,000 1,000 1,000 1000

C$ / US$ 1.02 1.08 1.10 1.04 1.11 1.11 1.11 1.11 1.11 1.11 1.11

Au Production(Koz) 30 30 30 30 30 30 177

Revenue(million $) 30 30 30 30 30 30 177

Ore mined (million tons) 1.1 1.1 1.1 1.1 1.1 1.1 6.5

Mining cost (million $) 12.0 12.0 12.0 12.0 12.0 12.0 71.9

Processing cost (million $) 8.6 8.6 8.6 8.6 8.6 8.6 51.8

Cash cost ($/oz) 699 699 699 699 699 699 699

Operating cash cost (million $) (21) (21) (21) (21) (21) (21) (124)

Capex (million $) (8) (10) (1) (1) (1) (1) (1) (5) (28)

Other expense (million $) (0.5) (1.07) (1) (0.1) (2.5)

Operating cash flow (million C$) (0.5) (1.2) (1.2) (8.4) (13.9) 9 9 9 9 9 4 23

Discount rate 8%

NPV (million C$) 8

Ore grade (g/t) 1

Strip ratio 2.70

Processing capacity (tpd) 3,000

Average recovery rate 85%

Average mining cost ($/t) 3.00

Processing cost and G&A($/t) 8.00

Future exploration

success could

significantly

enhance Oakley’s

NPV

Otis Gold Corp.

Jeff Wu, CFA 604-697-2455 [email protected] P a g e | 16

Advanced Minimum Royalty (“AMR”) of $25,000 in 2011, $30,000 per year thereafter, and a 3.5% NSR should the property go to production.

On November 9, 2010, Otis announced that it received permits from the USFS and the BLM to drill its Buckhorn High-Grade Silver Project. The planned drilling comprises a 1,000-metre, seven-hole program designed to test multi-ounce silver chip-channel intervals obtained from shallow trenches in the fall of 2009.

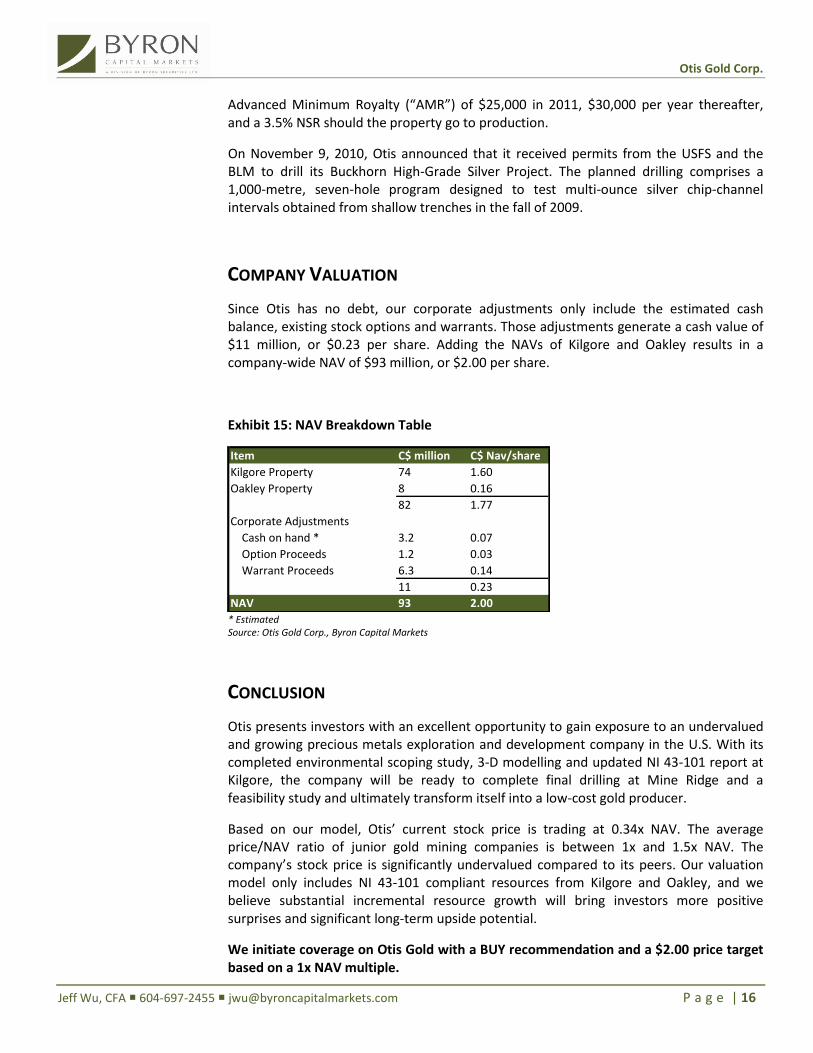

COMPANY VALUATION

Since Otis has no debt, our corporate adjustments only include the estimated cash balance, existing stock options and warrants. Those adjustments generate a cash value of $11 million, or $0.23 per share. Adding the NAVs of Kilgore and Oakley results in a company-wide NAV of $93 million, or $2.00 per share.

Exhibit 15: NAV Breakdown Table

* Estimated Source: Otis Gold Corp., Byron Capital Markets

CONCLUSION

Otis presents investors with an excellent opportunity to gain exposure to an undervalued and growing precious metals exploration and development company in the U.S. With its completed environmental scoping study, 3-D modelling and updated NI 43-101 report at Kilgore, the company will be ready to complete final drilling at Mine Ridge and a feasibility study and ultimately transform itself into a low-cost gold producer.

Based on our model, Otis’ current stock price is trading at 0.34x NAV. The average price/NAV ratio of junior gold mining companies is between 1x and 1.5x NAV. The company’s stock price is significantly undervalued compared to its peers. Our valuation model only includes NI 43-101 compliant resources from Kilgore and Oakley, and we believe substantial incremental resource growth will bring investors more positive surprises and significant long-term upside potential.

We initiate coverage on Otis Gold with a BUY recommendation and a $2.00 price target based on a 1x NAV multiple.

Item C$ million C$ Nav/share

Kilgore Property 74 1.60

Oakley Property 8 0.16

82 1.77

Corporate Adjustments

Cash on hand * 3.2 0.07

Option Proceeds 1.2 0.03

Warrant Proceeds 6.3 0.14

11 0.23

NAV 93 2.00

Otis Gold Corp.

Jeff Wu, CFA 604-697-2455 [email protected] P a g e | 17

APPENDIX I: MANAGEMENT AND DIRECTORS

(From company website)

Craig Lindsay, MBA, CFA – President: Mr. Lindsay has in excess of 20 years’ experience in corporate finance, investment banking and business development in both North America and Asia. He is currently Managing Director of Arbutus Grove Capital Corp., a private company offering corporate finance and merchant banking services. Mr. Lindsay was a Founder and President of Magnum Uranium Corp. until its merger with Energy Fuels Inc. (TSX: EFR in June 2009). As well, Mr. Lindsay was a Vice President in the Corporate Finance and Investment Banking Group at PricewaterhouseCoopers LLP. Mr. Lindsay was Founder of Malaspina Capital Ltd., a junior capital pool company, and was responsible for identifying its merger with Miranda Mining Corp (a Mexican-based gold producer that was subsequently acquired by Wheaton River Minerals). Mr. Lindsay has a Bachelor of Commerce from UBC (1989), a Masters of Business Administration from Dalhousie University (1993) and is a Chartered Financial Analyst. He is the President of the Hong Kong Canada Business Association — Vancouver Section, and the immediate past Chairman of the Family Services of Greater Vancouver.

John Carden, Ph.D., Lic. Geo. — Consulting Geologist: Dr. Carden has more than 30 years’ experience in exploration management, teaching and research. He has broad experience in managing large exploration programs including tracking costs, managing personnel, negotiating leases and contracts, writing technical reports, delivering verbal presentations, writing permitting and compliance documents for state and federal agencies, and managing remote drilling programs involving camp logistics. He has a proven track record for discovery of ore deposits in the western United States, with a gross metal value of more than $765 million. From 1986 through 1998, Dr. Carden was with Echo Bay Mines. From 1992 to 1998, he was Echo Bay’s Director of U.S. Exploration, where he directed the work of two district geologists, eight senior geologists and a GIS specialist. This group was successful in generating 35 funded projects over a five-year period. While at Echo Bay, he discovered the 600,000-ounce Lamefoot gold deposit, Echo Bay’s highest grade and lowest cost producer, and the Easy Junior gold deposit, a 250,000-ounce sediment-hosted gold deposit located in White Pine County, Nevada. Most recently, Dr. Carden has consulted on gold projects in Mexico for Minefinders in Chihuahua and Sonora states, in Zacatecas for Corex Gold Corp. and in the U.S. for Magnum Uranium Corp. Dr. Carden has a Ph.D. in Geology from the Geophysical Institute, University of Alaska, and a M.Sc. degree in Geology from Kent State University. He is a Licensed Geologist in the State of Washington and a member of the American Institute of Professional Geologists and a Fellow of the Society of Economic Geologists. Dr. Carden is currently a Director of Paramount Gold and Silver Corp.

Mitch Bernardi, M.Sc. Geology – Chief Geologist: Mr. Bernardi has over 30 years of experience in the mining industry and a proven exploration track record in mineral resources and discoveries in gold, zinc, copper, yttrium, rare earths and uranium. The bulk of Mr. Bernardi’s experience, some 20 years, has been in precious metals property generation, exploration and development, having worked on numerous deposit types while employed by Latitude Minerals, Echo Bay Mines, Cyprus Metals Exploration, Meridian Minerals, Unocal – Molycorp, Inc., Amoco Minerals and Magnum Uranium Corp. Discoveries directly associated with Mr. Bernardi as project leader or as co-discoverer of include the Kilgore gold deposit, Idaho (706,000 ounces Au), Coulterville gold project,

Otis Gold Corp.

Jeff Wu, CFA 604-697-2455 [email protected] P a g e | 18

California (70,000 ounces Au), Crypto zinc deposit, Utah (6.01MM Tons @ 8.68% sulfide zinc), Pan gold deposit, Nevada (400,000 ounces Au), Santiam copper breccia pipe, Oregon and the Blue Hill Creek gold/silver deposit, Idaho (230,000 ounces Au).

Donald E. Ranta, Ph.D., P.Geo. – Director: Dr. Ranta is an exploration and development mining executive experienced in planning, implementing and directing successful exploration and acquisitions throughout North and South America and internationally. He is a former president and board member of the Society for Mining, Metallurgy, and Exploration (SME) and former Vice President, Finance and board member of the American Institute of Mining, Metallurgical, and Petroleum Engineers (AIME). He has successfully directed and led innovative exploration efforts resulting in the discovery, evaluation and/or acquisition of several major deposits, including Montana’s McDonald and Mexico’s Santa Gertrudis gold ore bodies. He has also participated in the acquisition or discovery of Baja California’s Paradones Amarillos, Idaho’s Kilgore, Montana’s Seven-Up Pete, Mexico’s Dolores gold-silver, Burkina Faso’s Youga gold and Russia’s Kuranakh gold deposits. In addition, has been a Vice President of Exploration for Echo Bay Mines and Manager/Vice President for North American Exploration at Phelps Dodge Mining Company. Dr. Ranta is currently President, CEO and Director of Rare Element Resources and a Director of Animas Resources Ltd.

Charles W. (“Bill”) Reed, Lic. Geo. — Director: Mr. Reed is currently Vice President of Exploration for Paramount Gold and Silver Corp. (AMEX and TSX: PZG). He has significant mining experience in both Mexico and North America. From 1998 to 2004, he held the position of Chief Geologist – Mexico for Minera Hecla S.A. de C.V., a subsidiary of Hecla Mining (NYSE: HL). From 1993 to 1998, he was Regional Geologist in Mexico and Central America for Echo Bay Exploration. While at Hecla, Mr. Reed supervised detailed exploration at the Noche Buena project, Sonora, and the San Sebastian silver and gold mine, Durango. He also discovered and drilled the Don Sergio vein that was later put into production. While at Echo Bay, Mr. Reed identified the potential of the Dolores mining district in Chihuahua, Mexico and recommended acquisitions that resulted in the discovery of more than 44 million ounces of silver and 2.5 million ounces of gold. Mr. Reed holds a Bachelor of Science Degree in Mineralogy from the University of Utah and is a Registered Professional Geologist in the State of Utah. He also completed an Intensive Spanish Program at Institute De Lengua Espanola, San Jose, Costa Rica (1969).

Norm Eyolfson — Director: Mr. Eyolfson is President of Outlier Capital, a firm specializing in Research, Investments and Technical Analysis. Since 1998, Mr. Eyolfson has been actively involved in the junior capital markets in various capacities, ranging from Investor Relations to Corporate Development.

Sean Mitchell — Director: Mr. Mitchell has 16 years’ experience in business, with a specific focus on corporate financing and investment banking activities.

Otis Gold Corp.

Jeff Wu, CFA 604-697-2455 [email protected] P a g e | 19

IMPORTANT DISCLOSURES

Analyst's Certification All of the views expressed in this report accurately reflect the personal views of the responsible analyst(s) about any and all of the subject securities or issuers. No part of the compensation of the responsible analyst(s) named herein is, or will be, directly or indirectly, related to the specific recommendations or views expressed by the responsible analyst(s) in this report. The particulars contained herein were obtained from sources which we believe to be reliable but are not guaranteed by us and may be incomplete. Byron Capital Markets (“BCM”) is a division of Byron Securities Limited which is a Member of IIROC and CIPF. BCM compensates its research analysts from a variety of sources. The research department is a cost centre and is funded by the business activities of BCM including institutional equity sales and trading, retail sales and corporate and investment banking. Since the revenues from these businesses vary the funds for research compensation vary. No one business line has greater influence than any other for research analyst compensation. Dissemination of Research BCM endeavours to make all reasonable efforts to provide research simultaneously to all eligible clients. BCM equity research is distributed electronically via email and is posted on our proprietary websites to ensure eligible clients receive coverage initiations and ratings changes, targets and opinions in a timely manner. Additional distribution may be done by the sales personnel via email, fax or regular mail. Clients may also receive our research via a third party. Company Specific Disclosures: 1. The research analyst(s) and/or associate(s) who prepared this research report have viewed the material operations of Otis Gold Corp.

2. BCM has been paid or reimbursed by the issuer for the analyst(s) travel expenses to view the material operations of Otis Gold Corp.

3. BCM has received compensation for investment banking and advisory services from Otis Gold Corp. during the preceding 12 months.

Investment Rating Criteria STRONG BUY BUY

The security represents extremely compelling value and is expected to appreciate significantly from the current price over the next 12-18 month time horizon. The security represents attractive value and is expected to appreciate significantly from the current price over the next 12-18 month time horizon.

SPECULATIVE BUY The security is considered a BUY but in the analyst’s opinion possesses certain operational and/or

financial risks that may be higher than average. HOLD The security represents fair value and no material appreciation is expected over the next 12-18 month

time horizon. SELL The security represents poor value and is expected to depreciate over the next 12-18 month time

horizon.

Other Disclosures

This report has been approved by BCM, which takes responsibility for this report and its dissemination in Canada. This report is for the sole use of BCM’s Canadian clients. Canadian clients wishing to effect transactions in any security discussed should do so through a qualified salesperson of BCM. Informational Reports From time to time BCM will issue reports that are for information purposes only and will not include investment ratings. These reports will be clearly labelled accordingly.

Otis Gold Corp.

Jeff Wu, CFA 604-697-2455 [email protected] P a g e | 20

Company Directory Executive

Campbell Becher, President 647-426-1657 [email protected]

Investment Banking

Cliff Rich, CFA, Managing Director – Vancouver 604-616-1211 [email protected]

Robert Orviss, CFA, Managing Director – Toronto 647-426-1668 [email protected]

John Rak, VP- Investment Banking 647-426-1663 [email protected]

Alex Watson, Associate 604-616-0190 [email protected]

Russell Mills, Associate 647-426-0290 [email protected]

Elisa Chio, Analyst 647-426-0288 [email protected]

Mary Stuart, Analyst 604-616-5311 [email protected]

Research

Guy Gordon, CFA, Head of Research – Oil & Gas Analyst 647-426-1672 [email protected]

Al P. Nagaraj, Special Situations Analyst 647-426-0291 [email protected]

Drew Clark, Mining Analyst 647-426-1673 [email protected]

Jeff Wu, CFA, Mining Analyst 604-697-2455 [email protected]

Jon Hykawy, PhD, Clean Technologies & Materials Analyst 647-426-1656 [email protected]

Gabriela Casasnovas, Associate 647-426-0287 [email protected]

Jonathan Lee, Associate 647-426-1674 [email protected]

Sales & Trading

Main Trading Line 647-426-1670 Cyrus Osena, Head of Institutional Sales 647-426-1675 [email protected]

David Kemp, Head of Institutional Trading 647-426-1666 [email protected]

Byron Berry, Desk Analyst 416-867-1623 [email protected]

Graham Farrell, Institutional Sales & Trading 647-426-1667 [email protected]

Jonathan Samahin, CFA, Institutional Sales & Trading 647-426-1670 [email protected]

Kariv Oretsky, Institutional Sales 647-426-1658 [email protected]

Nick Perkell, Institutional Trading 647-426-1671 [email protected]

Nick Stajduhar, Institutional Sales 647-426-1664 [email protected]

Tom Chudnovsky, Institutional Sales 647-426-1665 [email protected]

Sandy Lam, Associate 416-867-2375 [email protected]

Operations

Derrick Chiu, Head of Syndication 647-426-1662 [email protected]

Dale Sampson, Chief Compliance Officer 416-867-1569 [email protected]

Marco Beretta, Associate 647-426-0289 [email protected]

Elisabeth Wightwick, Executive Assistant 416-867-8881 [email protected]

Robyn Lyle 647-426-1660 [email protected]

Sandra Day– Vancouver 604-697-2540 [email protected]