OSBIE AUDIT COMMITTEE MEETING AGENDA Thursday February …

168

OSBIE AUDIT COMMITTEE MEETING AGENDA Thursday February 11, 2021 9:00am Virtual ITEM LEADER 1. Welcome & Attendance a) Confirmation of Agenda b) Declaration of Pecuniary Interest MOTION: To confirm the agenda Chair 2. Approval of previous meeting minutes MOTION: To approve the minutes of the December 11, 2020 Audit Committee meeting Chair 3. Report from the Appointed Actuary Report of the Appointed Actuary MOTION: To recommend to the Board to receive the Appointed Actuary’s report for year end 2020. Raul Martin, JSCP 4. Report of the Auditor Audited Financial Statements MOTION: To recommend to the Board to receive the Audit Findings report from KPMG for the audit of 2020 OSBIE financial statements. MOTION: To recommend to the Board the approval of the audited financial statements for the Ontario School Boards’ Insurance Exchange, for the year ended December 31, 2020. Kim Haley, KPMG 5. P&C-1 MOTION: To recommend approval of the 2020 annual P&C-1 form as presented. CFO 6. Audit Services Contract Discussion Contract renewal date July 01, 2021 Chair 7. In Camera Session The Audit Committee will meet with KPMG and JSCP. Chair 8. Future Meeting Dates • June 25, 2021 • Dec 10, 2021 9. Adjournment MOTION: To adjourn the Audit Committee meeting Chair

Transcript of OSBIE AUDIT COMMITTEE MEETING AGENDA Thursday February …

OSBIE AUDIT COMMITTEE MEETING AGENDA Thursday February 11, 2021 9:00am

Virtual

ITEM LEADER

1. Welcome & Attendance a) Confirmation of Agenda

b) Declaration of Pecuniary Interest

MOTION: To confirm the agenda

Chair

2. Approval of previous meeting minutes

MOTION: To approve the minutes of the December 11, 2020 Audit Committee meeting

Chair

3. Report from the Appointed Actuary

Report of the Appointed Actuary

MOTION: To recommend to the Board to receive the Appointed Actuary’s report for year end 2020.

Raul Martin, JSCP

4. Report of the Auditor

Audited Financial Statements

MOTION: To recommend to the Board to receive the Audit Findings report from KPMG for the audit of 2020 OSBIE financial statements.

MOTION: To recommend to the Board the approval of the audited financial statements for the Ontario School Boards’ Insurance Exchange, for the year ended December 31, 2020.

Kim Haley, KPMG

5. P&C-1

MOTION: To recommend approval of the 2020 annual P&C-1 form as presented.

CFO

6. Audit Services Contract Discussion

Contract renewal date July 01, 2021

Chair

7. In Camera Session

The Audit Committee will meet with KPMG and JSCP.

Chair

8. Future Meeting Dates

• June 25, 2021

• Dec 10, 2021

9. Adjournment

MOTION: To adjourn the Audit Committee meeting

Chair

Agenda 2

MOTION

TO: Audit Committee

FROM: CEO

RE: Previous Meeting Minutes

MOVED: SECONDED:

BE IT RESOLVED,

MOTION: To approve the minutes of the December 11, 2020 Audit Committee meeting.

OSBIE Audit Committee Meeting Minutes Virtual Meeting

Friday December 11, 2020

Present: Jeff Pratt Marc Cantin Isabel Grace Chris Arnew Amy Janssens Pearl Fong-West Craig Young Kirsti Alaksa Brian Coburn Cathy Modesto Chris Spina Peter Marshall Jaspal Gill

Regrets: Lynn Schaule

Resources: Jim Sami, CEO Sandra Taylor, CFO, Mark Anderson, Director of Claims Tammy Hicks, Director of Risk Management and Member Services Traci Decaro, Claims Manager Harjit Douglas, Recording Secretary

1. Call to Order

The Chair called the meeting to order at 9:02am. He called for any Declarations of PecuniaryInterest. There were none declared. He asked for a motion to confirm the agenda.

Motion: Moved by Marc Cantin, seconded by Peter Marshall to confirm the agenda. Carried.

2. Approval of previous meeting minutes

The Chair asked for a motion to approve the Audit Committee’s minutes of the June 26, 2020meeting.

Motion: Moved by Brian Coburn, seconded by Craig Young to approve the minutes of the June 26, 2020 Audit Committee meeting. Carried.

3. Electronic Business Between Meetings

Motion: Moved by Brian Coburn, seconded by Pearl Fong-West to confirm the motion torecommend the approval of the September 30, 2020 P&C1. Carried.

4. Report of the Auditor

The Chair invited Kim Haley and Dale Percival of KPMG to make their presentation.

MOTION: Moved by Brian Coburn, seconded by Isabel Grace to recommend the approval of the

audit plan for OSBIE’s 2020-year end as presented by KPMG. Carried.

5. In camera session

It was agreed amongst the directors that an In Camera session was not required for this meeting.

6. Future Meeting Dates

The Board Chair asked that the February 12,2021 date be amended as that date is tied to theFamily Day long weekend and some directors may want to use the February 12th date to extend the weekend. A suggestion was made to alter the date to Thursday February 11,2021 which was acceptable to the directors.

• February 11, 2021

• June 25, 2021

• December 10, 2021

MOTION: Moved by Brian Coburn, seconded by Pearl Fong-West to recommend the approval of the proposed meeting dates for 2021. Carried.

7. Adjournment

Motion: Moved by Brian Coburn, seconded by Jeff Pratt to adjourn the Audit Committeemeeting at 9:37am. Carried

Chair ____________________________________________________________

Secretary _________________________________________________________

MOTION: To approve the minutes of the December 11, 2020 Audit Committee meeting.

Agenda 3

MOTION

TO: Audit Committee

FROM: CEO

RE: Year end Report from the Appointed Actuary

MOVED: SECONDED:

BE IT RESOLVED,

MOTION: To recommend to the Board to receive the Appointed Actuary’s report for year end 2020.

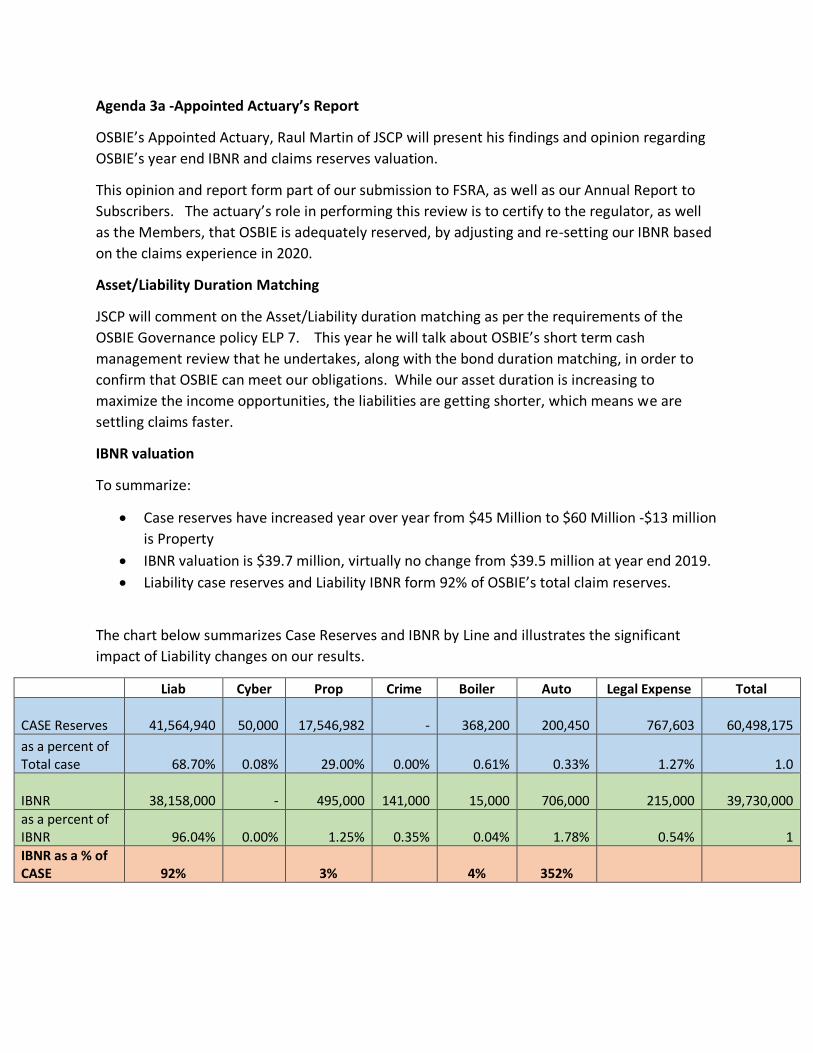

Agenda 3a -Appointed Actuary’s Report

OSBIE’s Appointed Actuary, Raul Martin of JSCP will present his findings and opinion regarding

OSBIE’s year end IBNR and claims reserves valuation.

This opinion and report form part of our submission to FSRA, as well as our Annual Report to

Subscribers. The actuary’s role in performing this review is to certify to the regulator, as well

as the Members, that OSBIE is adequately reserved, by adjusting and re-setting our IBNR based

on the claims experience in 2020.

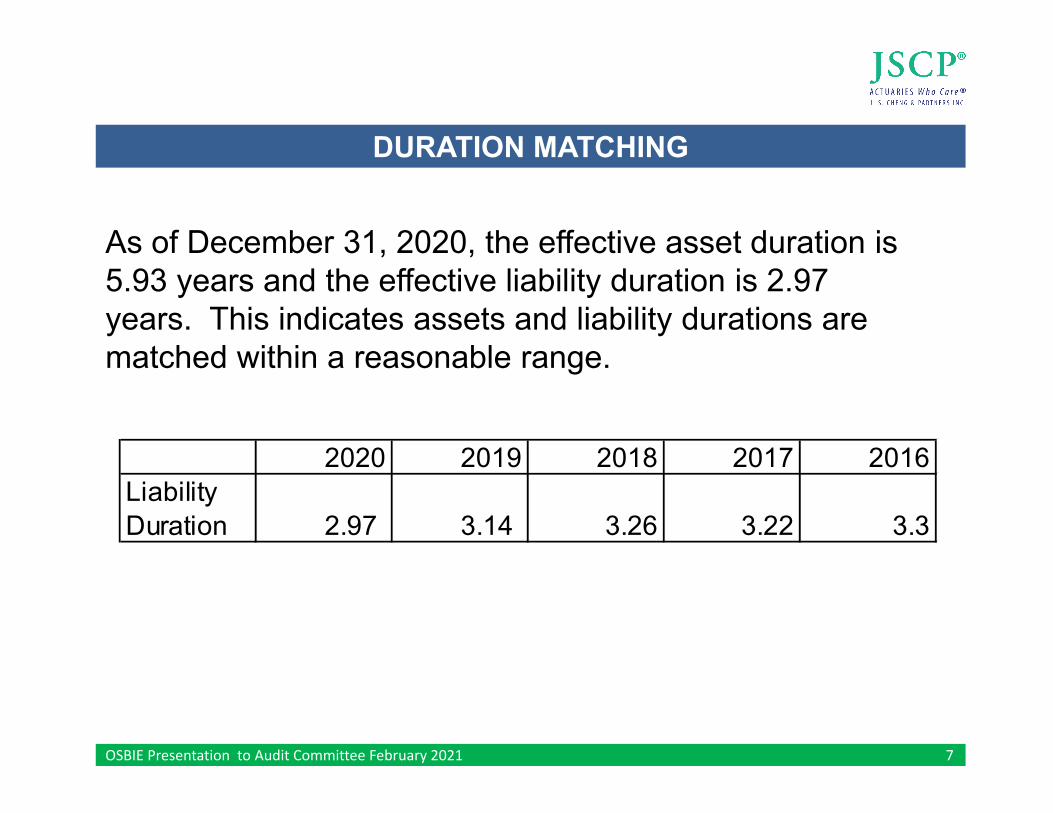

Asset/Liability Duration Matching

JSCP will comment on the Asset/Liability duration matching as per the requirements of the

OSBIE Governance policy ELP 7. This year he will talk about OSBIE’s short term cash

management review that he undertakes, along with the bond duration matching, in order to

confirm that OSBIE can meet our obligations. While our asset duration is increasing to

maximize the income opportunities, the liabilities are getting shorter, which means we are

settling claims faster.

IBNR valuation

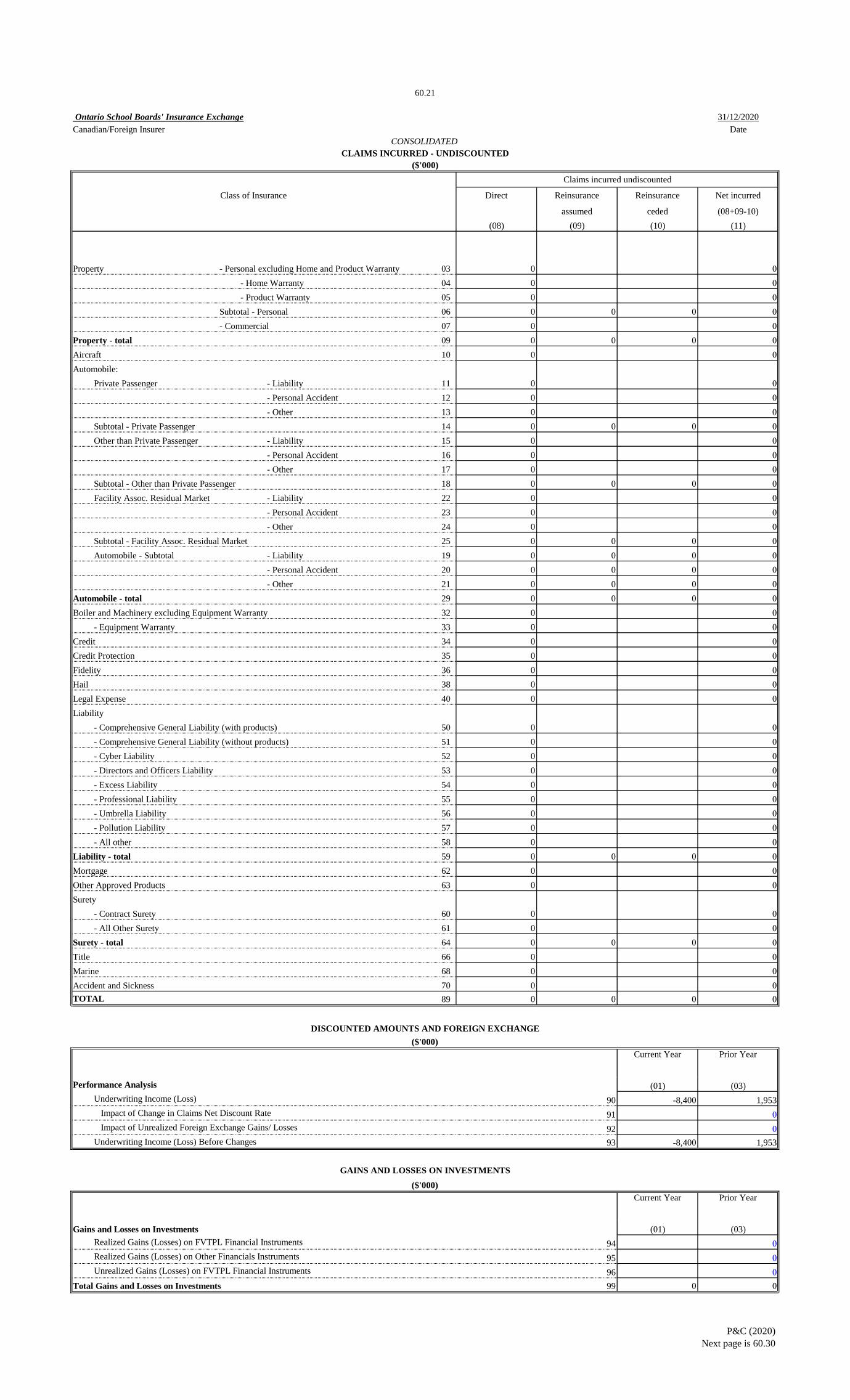

To summarize:

• Case reserves have increased year over year from $45 Million to $60 Million -$13 million

is Property

• IBNR valuation is $39.7 million, virtually no change from $39.5 million at year end 2019.

• Liability case reserves and Liability IBNR form 92% of OSBIE’s total claim reserves.

The chart below summarizes Case Reserves and IBNR by Line and illustrates the significant

impact of Liability changes on our results.

Liab Cyber Prop Crime Boiler Auto Legal Expense Total

CASE Reserves

41,564,940

50,000

17,546,982 -

368,200

200,450

767,603

60,498,175

as a percent of Total case 68.70% 0.08% 29.00% 0.00% 0.61% 0.33% 1.27%

1.0

IBNR

38,158,000 -

495,000

141,000

15,000

706,000

215,000

39,730,000

as a percent of IBNR 96.04% 0.00% 1.25% 0.35% 0.04% 1.78% 0.54%

1

IBNR as a % of CASE 92% 3% 4% 352%

Large Loss Fund

JSCP will also speak to the treatment of the large loss fund for 2021 and beyond. Until we

experience a large loss, there are no offsetting claims liabilities, so the fund will continue to

build as a part of our surplus. The fund closed 2020 with a balance of $8,091,000.

Presentation slides from JSCP follow this summary.

MOTION: To recommend to the Board to receive the Appointed Actuary’s report for year end 2020.

To the Audit Committee of

Ontario School Boards’ Insurance Exchangeon

11 February 2021

PRESENTATION OF APPOINTED ACTUARY’S REPORT

1. Expression of Opinion2. Comparison of 2019 and 2020 Actuarial Present Value

(APV) Net Claims Liabilities3. List of important changes in 20204. Effect of Actuarial Present Value (APV) Calculation5. Duration Matching6. Loss Ratio by Segment7. Loss Ratio by Year 8. Claims Run-off by Segment9. Reinsurance/Retention

TABLE OF CONTENTS

OSBIE Presentation to Audit Committee February 2021 2

I have valued the policy liabilities and reinsurance recoverables of Ontario School Boards’Insurance Exchange for its statement of financial position at December 31, 2020 and their changesin the statement of income for the year then ended in accordance with the accepted actuarialpractice in Canada including selection of appropriate assumptions and methods.

In my opinion, the amount of policy liabilities net of reinsurance recoverables makes appropriateprovision for all policy obligations and the financial statements fairly present the results of thevaluation.

The results of my valuation together with the amounts carried in the Annual Return are thefollowing:

EXPRESSION OF OPINION

OSBIE Presentation to Audit Committee February 2021 3

AppointedCarried in Actuary's

Annual Return Estimate($'000) ($'000)

(1) Direct unpaid claims and adjustment expenses: 108,857 108,857

(2) Assumed unpaid claims and adjustment expenses: 0 0

(3) Gross unpaid claims and adjustment expenses: 108,857 108,857

(4) Ceded unpaid claims and adjustment expenses: 2,943 2,943

(5) Other amounts to recover: 5,863 5,863

(6) Other net liabilities: 0 0

(7) Net unpaid claims and adjustment expenses(3)-(4)-(5)+(6): 100,051 100,051

Claim Liabilities

EXPRESSION OF OPINION (Cont’d)

OSBIE Presentation to Audit Committee February 2021 4

AppointedPremium Liabilities Carried in Actuary's

Annual Return Estimate($'000) ($'000)(Col.1) (Col.2)

(1) Gross policy liabilities in connection with unearned premiums: 0 (2) Net policy liabilities in connection with unearned premiums: 0 (3) Gross unearned premiums: 0 (4) Net unearned premiums: 0 (5) Premium deficiency: 0 0 (6) Other net liabilities: 0 0 (7) Deferred policy acquisition expenses: 0 (8) Maximum policy acquisition expenses deferrable: [(4)+(5)+(9)]Col.1 - (2) Col.2

(9) Unearned Commissions + Ceded Deferred Premium Taxes + Ceded Deferred Insurance Operations Expenses:

0

0

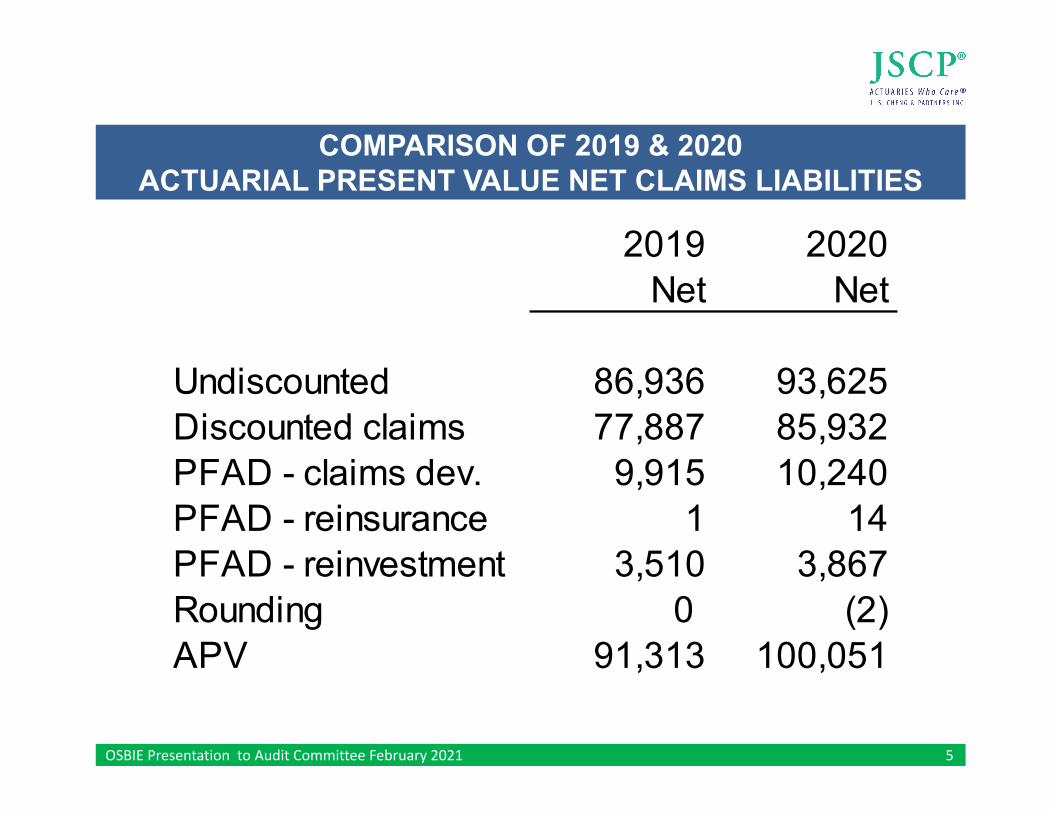

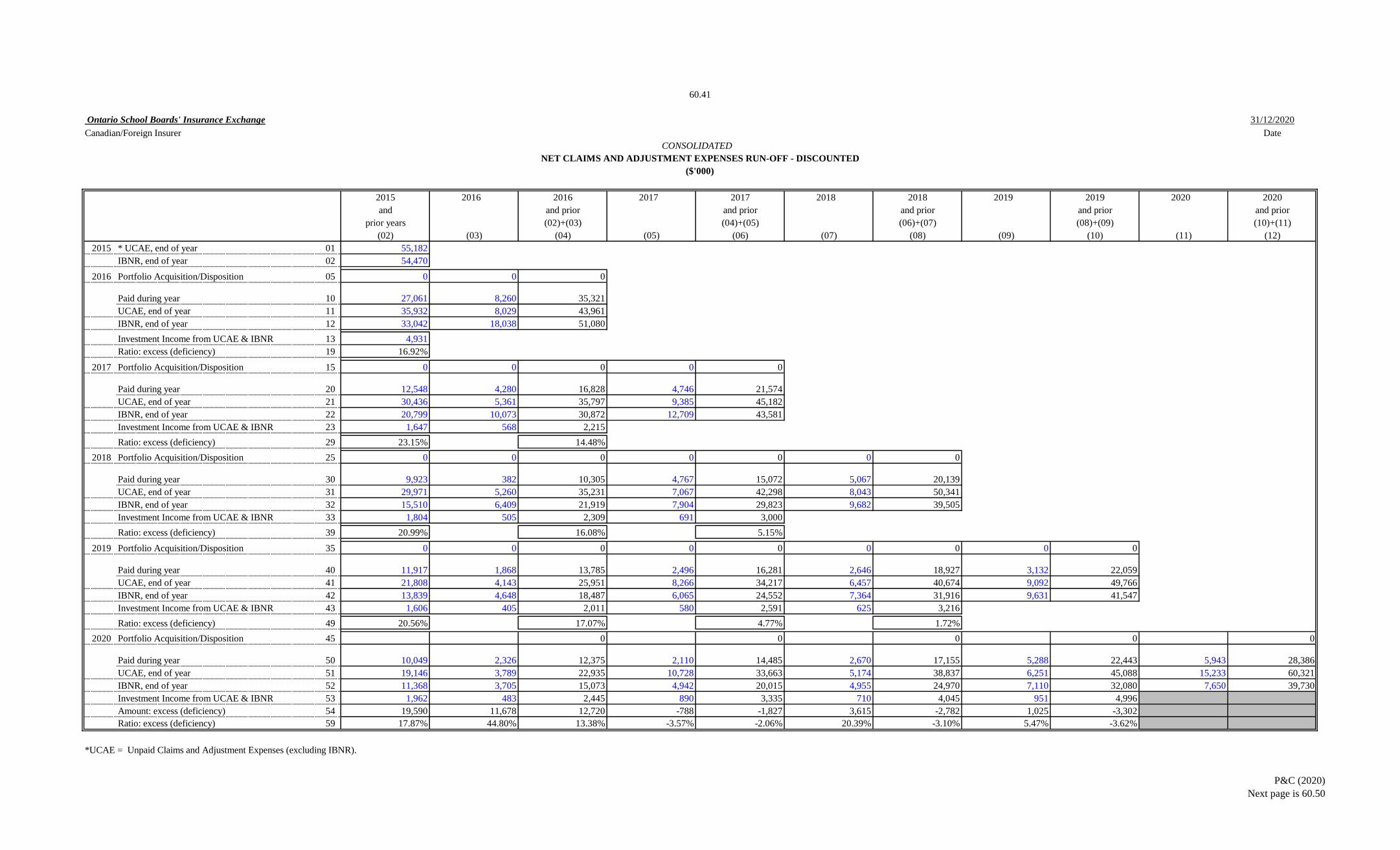

COMPARISON OF 2019 & 2020 ACTUARIAL PRESENT VALUE NET CLAIMS LIABILITIES

OSBIE Presentation to Audit Committee February 2021 5

2019 2020Net Net

Undiscounted 86,936 93,625Discounted claims 77,887 85,932PFAD - claims dev. 9,915 10,240PFAD - reinsurance 1 14PFAD - reinvestment 3,510 3,867Rounding 0 (2)APV 91,313 100,051

LIST OF IMPORTANT CHANGES IN 2020

OSBIE Presentation to Audit Committee February 2021 5

1. Impact of COVID-19 on Liability losses

2. Impact of COVID-19 on the discount rate

3. Large Property Loss

EFFECT OF APV CALCULATION

OSBIE Presentation to Audit Committee February 2021 6

Impact($000)

Net discount rate before MFAD 3.48% 2.93%Net discount rate after MFAD 2.03% 1.38%

MFAD for discount rate 1.45% 1.55%

Margin for claims development- SA/Environmental Liability 15.00% 15.00%

- Other Liability 12.50% 12.50%- Property, B&M, Crime 2.50% 2.50%- Automobile 10.00% 10.00%- Legal Expense 5.00% 5.00%- ILAE 15.00% 15.00%

2019 2020

(1,829)

0

DURATION MATCHING

OSBIE Presentation to Audit Committee February 2021 7

As of December 31, 2020, the effective asset duration is 5.93 years and the effective liability duration is 2.97 years. This indicates assets and liability durations are matched within a reasonable range.

2020 2019 2018 2017 2016Liability Duration 2.97 3.14 3.26 3.22 3.3

CURRENT POLICY YEAR UNDISCOUNTED LOSS RATIO

OSBIE Presentation to Audit Committee February 2021 8

(Before ILAE)

Gross Gross Gross GrossEarned Loss Earned Loss

Segment Premium Ratio Premium Ratio($000's) ($000's)

Liability 17,853 80.42% 19,732 54.18%Property 10,360 32.99% 10,914 164.35%Boiler & Machinery 354 97.74% 794 55.16%Crime 881 77.07% 905 15.47%Automobile 1,100 50.00% 1,040 49.90%Legal Expense 531 88.51% 1,013 67.62%

OSBIE Total 31,079 63.78% 34,398 88.41%

2019 Appointed Actuary Report

2020 Appointed Actuary Report

GROSS UNDISCOUNTED LOSS RATIO BY YEAR(Excluding ILAE)

OSBIE Presentation to Audit Committee February 2021 9

0%

20%

40%

60%

80%

100%

120%

140%

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

Gross Loss Ratio: Policy Year 2000-2020

2019

2020

ONE-YEAR CLAIMS RUN-OFF BY SEGMENT(Undiscounted Basis Excluding ILAE)

OSBIE Presentation to Audit Committee February 2021 10

Gross Basis Redundancy (Deficiency)($000's)

Liability (6,906)

Property 490

Boiler & Machinery (46)

Crime (347)

Automobile 330

Total OSBIE (6,528)

* Net Runoff (6,457)

Reinsurance Coverage

2019 2020

Liability $22M xs $5M No Reinsurance

Property $5M xs Board deductible

$5M xs Board deductible

Crime No Reinsurance No ReinsuranceBoiler & Machinery 50% co-insured No Reinsurance

Automobile $17M xs $3M No ReinsuranceLegalExpense No Reinsurance No Reinsurance

REINSURANCE / RETENTION

OSBIE Presentation to Audit Committee February 2021 12

Agenda 4a

MOTION

TO: Audit Committee FROM: CEO RE: KPMG year end reports: Audit Findings Report

Presentation of Audited Financial Statements

MOVED: SECONDED:

BE IT RESOLVED, MOTION: To recommend to the Board to receive the Audit Findings report from KPMG for the audit of 2020 OSBIE financial statements. MOTION: To recommend to the Board the approval of the audited financial statements for the Ontario School Boards’ Insurance Exchange for the year ended December 31, 2020.

Ontario School Boards Insurance Exchange (OSBIE)

Audit Findings Report for the year ended December 31, 2020

Licensed Public Accountants

Prepared as of February 2, 2021 for

the Audi t Commit tee meet ing on

February 11, 2021

kpmg.ca/audi t

Table of contents Changes from the audit plan 1

What’s new in 2020 2

Audit risks and results 5

Significant accounting policies and practices 11

Financial statement presentation and disclosure 12

Uncorrected differences and corrected adjustments 13

Appendices 14

Appendix 1: Other Required Communications 15

Appendix 2: Management Representation Letter 16

Appendix 3: Independence Letter 23

Appendix 4: Draft Auditors’ Report 25

Appendix 5: KPMG’s System of Quality Control 30

Appendix 6: Technology in the audit 31

Appendix 7: Audit and Assurance Insights 32

Audit Findings Report P a g e | 1

Executive summary Purpose of this report1

The purpose of this Audit Findings Report is to assist you, as a member of the Audit Committee, in your review of the results of our audit of the financial

statements as at and for the period ended December 31, 2020. This Audit Findings Report builds on the Audit Plan we presented to the Audit Committee.

What’s new in 2020

There have been significant changes in 2020 which impacted financial reporting,

the Entity’s internal control over financial reporting and our audit:

• COVID-19 pandemic – See pages 2 - 3

• New CAS auditing standards – See page 4

Changes from the audit plan

There have been no significant changes regarding our audit from the Audit

Planning Report previously presented to you.

Independence

We have included a copy of our annual independence letter dated as of the date of

this report, which notes that we are independent of the Entity in accordance with

the ethical requirements that are relevant to our audit of the financial statements in

Canada.

Uncorrected differences

We did not identify differences that remain uncorrected.

1 This Audit Findings Report is intended solely for the information and use of Management, the Audit Committee, and the Board of Directors and should not be used for any other purpose or any other

party. KPMG shall have no responsibility or liability for loss or damages or claims, if any, to or by any third party as this Audit Findings Report has not been prepared for, and is not intended for, and

should not be used by, any third party or for any other purpose.

Finalizing the audit

As of February 4, 2021, we have completed the audit of the financial statements,

with the exception of certain remaining procedures, which include amongst others:

– Receipt of the legal letter

– Completing our final tie in of the financial statement and note disclosures

– Review of the French translation and Annual Reports

– Obtaining the signed management representation letter

– Completing our discussions with the Audit Committee

– Obtaining evidence of the Board’s approval of the financial statements

We will update the Audit Committee, and not solely the Chair, on significant

matters, if any, arising from the completion of the audit, including the completion of

the above procedures.

Our auditors’ report, a draft of which is provided in Appendix 4, will be dated upon

the completion of any remaining procedures.

Control deficiencies

We did not identify any control deficiencies that we determined to be significant

deficiencies in internal control over financial reporting.

Audit Findings Report P a g e | 2

What’s new in 2020 COVID-19 pandemic

On December 11, 2020, our audit plan highlighted potential impacts of the COVID-19 pandemic. We adapted our audit to respond to the continued changes

in your business, including the impacts on financial reporting and internal control over financial reporting.

Area of Impact Key Observations

Company’s financial reporting impacts

- We considered impacts to financial reporting due to COVID-19 pandemic and the increased disclosures needed in the financial statements

as a result of the significant judgements.

- In areas of the financial statements where estimates involved significant judgements, we evaluated whether the method, assumptions and

data used by management to derive the accounting estimates, and their related financial statement disclosures were still appropriate per the

relevant financial reporting framework given the changed economic conditions and increased estimation uncertainty

- The areas of the financial statements most affected included:

o Disclosures – See Note 16 to the financial statements

Company’s internal control over financial reporting

- As part of our risk assessment we examined the financial reporting risks, including fraud risks, given possible new pressures on

management or new opportunities to commit fraud given changes in the Entity’s internal controls over financial reporting.

- As a result of the Entity’s remote working environment, it was necessary to assess the impact to the Entity’s internal controls.

o In areas of the audit where we are evaluating controls, we obtained an understanding of any changes to processes and controls during

the year to assess if there was a need to change the extent of testing. No changes were noted that had a significant impact on the

scope of audit work.

Materiality

- We considered impacts to financial reporting on both the determination and the re-assessment of materiality for the audit of the financial

statements.

- No adjustment to materiality was considered necessary.

Risk Assessment

- We performed a more thorough risk assessment specifically targeted at the impacts of the COVID-19 pandemic, including an assessment of

fraud risk factors (i.e., conditions or events that may be indicative of an incentive/pressure to commit fraud, opportunities to commit fraud,

rationalizations of committing fraud).

Audit Findings Report P a g e | 3

COVID-19 pandemic (continued)

Area of Impact Key Observations

Working remotely

- We used virtual work rooms, video conferencing, and internally shared team sites to collaborate in real-time, both amongst the audit team

as well as with management.

- We increased our professional skepticism when evaluating electronic evidence received and performed additional procedures to validate the

authenticity and reliability of electronic information used as audit evidence.

Direction and Supervision of the audit

- The manager and partner were actively involved in determining the impact that the COVID-19 pandemic had on the audit (as discussed

above), including the impact on the Entity’s financial reporting and changes in the Entity’s internal control over financial reporting.

- Managers and partners implemented new supervision processes to deal with working in a remote environment, and our audit approach

allowed us to manage the audit using meaningful milestones and frequent touch points.

Substantive Testing - Response

- Our evaluation of management’s assessment of going concern was enhanced to respond to the uncertainties relating to prospective

financial information and judgements about appropriate financial statement disclosures in the rapidly changing environment.

Audit Findings Report P a g e | 4

New auditing standards

The following new auditing standards that are effective for the current year had an impact on our audit.

Standard Key observations

CAS 540, Auditing

Accounting Estimates

and Related Disclosures

— The new standard was applied on all estimates within the financial statements that had a risk of material misstatement due to estimation

uncertainty and not just “key estimates”, “critical accounting estimates”, or “estimates with significant risk”.

— The granularity and complexity of the new standard along with our interpretation of the application of that standard necessitated more

planning and discussion and increased involvement of more senior members of the engagement team.

— We performed more granular risk assessments based on the elements making up each accounting estimate such as the method, the

assumptions used, the data used and the application of the method.

— We considered the potential for management bias.

— We assessed the degree of uncertainty, complexity, and subjectivity involved in making each accounting estimate to determine the level of

audit response; the higher the level of response, the more persuasive the audit evidence was needed.

— We involved professionals with appropriate skills and knowledge to assist us in auditing certain estimates as appropriate.

— See pages 5 and 7 under Audit Risk and Results for estimates that related to significant risk or other areas of focus, which are a subset of

all the estimates subject to the new standard.

Audit Findings Report P a g e | 5

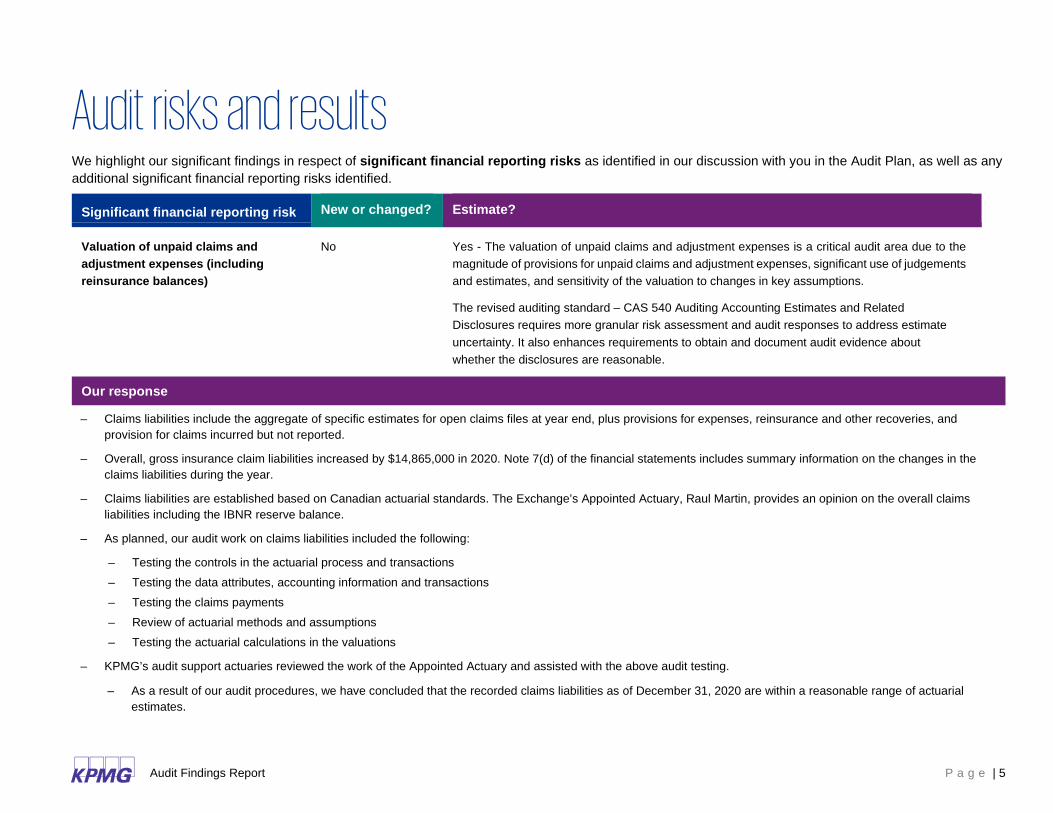

Audit risks and results We highlight our significant findings in respect of significant financial reporting risks as identified in our discussion with you in the Audit Plan, as well as any

additional significant financial reporting risks identified.

Significant financial reporting risk New or changed? Estimate?

Valuation of unpaid claims and

adjustment expenses (including

reinsurance balances)

No Yes - The valuation of unpaid claims and adjustment expenses is a critical audit area due to the

magnitude of provisions for unpaid claims and adjustment expenses, significant use of judgements

and estimates, and sensitivity of the valuation to changes in key assumptions.

The revised auditing standard – CAS 540 Auditing Accounting Estimates and Related

Disclosures requires more granular risk assessment and audit responses to address estimate

uncertainty. It also enhances requirements to obtain and document audit evidence about

whether the disclosures are reasonable.

Our response

– Claims liabilities include the aggregate of specific estimates for open claims files at year end, plus provisions for expenses, reinsurance and other recoveries, and

provision for claims incurred but not reported.

– Overall, gross insurance claim liabilities increased by $14,865,000 in 2020. Note 7(d) of the financial statements includes summary information on the changes in the

claims liabilities during the year.

– Claims liabilities are established based on Canadian actuarial standards. The Exchange’s Appointed Actuary, Raul Martin, provides an opinion on the overall claims

liabilities including the IBNR reserve balance.

– As planned, our audit work on claims liabilities included the following:

– Testing the controls in the actuarial process and transactions

– Testing the data attributes, accounting information and transactions

– Testing the claims payments

– Review of actuarial methods and assumptions

– Testing the actuarial calculations in the valuations

– KPMG’s audit support actuaries reviewed the work of the Appointed Actuary and assisted with the above audit testing.

– As a result of our audit procedures, we have concluded that the recorded claims liabilities as of December 31, 2020 are within a reasonable range of actuarial

estimates.

Audit Findings Report P a g e | 6

Audit risks and results We highlight our significant findings in respect of areas of focus as identified in our discussion with you in the Audit Plan, as well as any additional areas of

focus identified.

Area of focus Why is it significant?

Fraud risk from management override of controls This is a presumed fraud risk under Canadian auditing standards.

We have not identified any specific additional risks of management override relating to this audit.

Our response and Significant findings

– Our procedures included:

- We tested the design and implementation of controls surrounding the recording of journal entries, and the business rationale for significant entries.

- We tested the process for critical accounting estimates, including performing a retrospective review of prior period estimates.

– No issues were noted in the performance of the above procedures.

Audit Findings Report P a g e | 7

Audit risks and results Area of focus Why are we focusing here?

Valuation of investments All of OSBIE’s invested assets continue to be carried on the statement of financial position at fair value

determined from publicly available sources of market data.

Available-for-sale (AFS) assets are carried at market value; unrealized gains and losses on AFS assets are

held in accumulated other comprehensive income until realized through sale or through recognition of

impairment losses. For these assets it is necessary to consider whether an impairment in value has occurred.

Our response and Significant findings

− Management has established valuation procedures for the majority of the portfolio based on the use of a third party pricing source. Fair values are categorized and

disclosed as Levels 1, 2 and 3, with Level 1 and Level 2 being based on market quotes and market-observable inputs, respectively, and Level 3 being based on other

valuation and appraisal techniques.

− As disclosed in note 4(c) of the financial statements, at December 31, 2020, management has categorized assets as $55.4 million in Level 1, $157.6 million in Level 2,

and $nil in Level 3. KPMG tested the allocation of investments between categories of the fair value hierarchy.

− Management has a process to review the valuation of investments and evaluates investment impairment on a regular basis. Management’s assessment as at

December 31, 2020 was that no provision was required for any impairment in value of AFS securities, which consist of $157.6 million of bonds and debentures and

$55.4 million of equities.

− KPMG tested management’s valuation of investments and performed an assessment of possible impairments in AFS securities. We identified an equity position in

Bank of Nova Scotia that has had a market value below book value for a prolonged period and proposed an adjustment to record an impairment write-down of

$287,000. Management has recorded this adjustment in the financial statements.

− In completing our review of service organization auditor’s reports over controls at investment custodians, we noted that there are no reports available for TD Direct

Investing or National Bank. We performed alternative procedures to gain comfort over the custodians.

− We performed Data & Analytics procedures on investments using KPMG proprietary software, iRADAR. We performed independent price testing of management’s

pricing for bonds and debentures, and equities:

− Bonds with a market value of $127.8 million, and equities with a market value of $51.3 million were tested by iRADAR.

− For bonds and debentures, KPMG’s iRADAR team analyzes the security’s market to determine whether there is an active market for the security.

− We independently priced the market value of the remaining bonds and equities excluded from iRADAR testing.

− Based on our testing, the aggregate difference where market values were out of the range amounted to $59,000.

− As a result of our audit procedures, no other issues were identified.

Audit Findings Report P a g e | 8

Data & Analytics: valuation of investments

The market value of all bonds and pooled funds tested amounts to $179.1 million. For bonds and debentures, KPMG’s iRADAR team analyses the security’s market to determine whether there is an active market for the security. For those investments that are determined to not have an active market, further pricing analysis is done to develop an internal valuation of the security to better reflect a true fair value as at December 31, 2020. After applying investment specific ranges of acceptable prices, the netted deviation out of range of acceptable prices for equites is $nil, and for bonds is $59,000, which is less than our audit misstatement posting threshold of $210,000. From this graph, one can observe that the higher pricing deviations have small monetary impact and that the positions with high notional value have deviations close to zero.

-400

-300

-200

-100

0

100

200

300

400

500

0 1 2 3 4 5 6 7

Price D

iffe

rence (

bps)

Notional (CAD) in millions

Price Dispersion

Corp

Govt / Municipals

Preferreds / Perpetuals

Structured Notes

Audit Findings Report P a g e | 9

Data & Analytics: benchmarking prices – fixed income securities For the fixed income securities held by OSBIE, we have summarized our findings to compare the Exchange’s portfolio to other KPMG client portfolios where there are prices

from at least two clients other than OSBIE. The average standard deviation per security measured for the various price contributions is also presented below.

Overall, the difference between OSBIE’s average price of 104.60 and the average price of its industry group of 104.58 falls within one standard deviation and is well within the

range we would find acceptable for any variations noted in the pricing of your portfolio

0

20

40

60

80

100

120

140

160

0 20 40 60 80 100 120 140 160

Clie

nt

Price

Industry Average Price

Industry Average Price vs. Client Price

Corp

Govt / Municipals

Client's AverageIndustry's Average

Industry +/-1 Standard Deviation

104.3 104.35 104.4 104.45 104.5 104.55 104.6 104.65 104.7 104.75 104.8 104.85

Industry Benchmarking Results

Audit Findings Report P a g e | 10

Audit risks and results Area of focus Why are we focusing here?

Claims expense (including related reinsurance) Claims payments require a degree of judgment in ascertaining whether coverage is adequate and the

payment is within authorized limits.

Our response and Significant findings

– We tested the controls over the approval of claim payments and the review of claims files by the claims manager. No control deficiencies were noted.

– We tested a sample of claim payments, tracing the pay out to the supporting source documentation.

– As a result of our audit procedures, no issues or audit misstatements were identified.

Area of focus Why are we focusing here?

Written premiums and premiums paid in advance

(including related reinsurance balances)

Written premiums represent the largest balance on the statement of comprehensive income.

Our response and Significant findings

– We substantively tested gross written premiums and premiums received in advance by agreeing a sample of premium amounts through to the general ledger and

receipt of payment.

– We tested the accuracy of the reinsurance ceded balance.

– As a result of our audit procedures, no issues or audit misstatements were identified.

Audit Findings Report P a g e | 11

Significant accounting policies and practices

Changes

There have been no changes to significant accounting policies and practices during the year.

Future Implementation

Accounting pronouncements issued but not yet effective are disclosed in Note 2(l) to the financial statements.

IFRS 17, Insurance Contracts

- On May 18, 2017 the IASB issued IFRS 17 Insurance Contracts. On June 25, 2020, the IASB issued amendments to IFRS 17 aimed at helping companies implement the Standard and to defer the effective date. The new standard is effective for annual periods beginning on or after January 1, 2023. IFRS 17 will replace IFRS 4 Insurance Contracts.

- The IASB has deferred the effective date of IFRS 17 to January 1, 2023. The fixed expiry date for the optional temporary exemption from applying IFRS 9 Financial Instruments, granted to insurers meeting certain criteria, would also be deferred to 2023. This means that all companies preparing financial statements under IFRS would be required to apply both IFRS 9 and IFRS 17 for annual periods beginning on or after January 1, 2023.

IFRS 9, Financial Instruments

- On July 24, 2014 the IASB issued the complete amended IFRS 9. The mandatory effective date of IFRS 9 is for annual periods beginning on or after January 1, 2018.

- As at January 1, 2018, the Entity has elected to apply the optional transitional relief under IFRS 4 that permits the deferral of the adoption of IFRS 9 for eligible insurers. The Entity will continue to apply IAS 39 until January 1, 2023.

Audit Findings Report P a g e | 12

Financial statement presentation and disclosure Misstatements, including omissions, if any, related to financial statement presentation and disclosure items are in the management representation letter.

We also highlight the following:

Form, arrangement, and

content of the financial

statements

Adequate

Significant accounting policies or practices are disclosed in note 2 to the financial statements. There are no changes in accounting policies

during the current year.

Significant qualitative

aspects of financial

statement presentation

and disclosure

COVID-19 pandemic disclosures

The COVID-19 pandemic has resulted in significant financial, market and societal impacts in Canada and around the world. Management has

added Note 16 to the financial statements to highlight this impact.

Audit Findings Report P a g e | 13

Uncorrected differences and corrected adjustments Differences and adjustments include disclosure and presentation differences and adjustments.

Professional standards require that we request of management and the Audit Committee that all identified differences be corrected. We have already made

this request of management.

Uncorrected differences

We did not identify differences that remain uncorrected.

Corrected adjustments

The management representation letter includes all adjustments identified as a result of the audit, communicated to management and subsequently corrected in the financial

statements.

As at and year ended December 31, 2020 Income effect Financial position

Description of differences greater than $210,000 individually

(Decrease) Increase Assets

(Decrease) Increase Liabilities

(Decrease) Increase Equity

(Decrease) Increase

To record the investment impairment provision on the Bank of

Nova Scotia equity holdings with prolonged decline in value.

Investment Income

Other comprehensive income

($286,574)

$286,574

– –

($286,574)

$286,574

Total differences – – – –

Appendices Content

Appendix 1: Other Required communications

Appendix 2: Management Representation Letter

Appendix 3: Independence Letter

Appendix 4: Draft Auditors’ Report

Appendix 5: KPMG’s System of Quality Control

Appendix 6: Technology in the Audit

Appendix 7: Audit and Assurance Insights

Audit Findings Report P a g e | 15

Appendix 1: Other Required Communications Report Engagement terms

The conclusion of our audit is set out in our draft auditors’ reports as included in

Appendix 4.

Unless you inform us otherwise, we understand that you acknowledge and agree to the

terms of the engagement set out in the engagement letter and any subsequent

amendments as provided by management.

Reports to the Audit Committee Representations of management

At the completion of the audit, we will provide our findings report to the Audit

Committee.

A copy of the management representation letter is attached. See Appendix 2.

Audit Quality in Canada Matters pertaining to independence

The reports available through the following links were published by the Canadian

Public Accountability Board to inform Audit Committees and other stakeholders

about the results of quality inspections conducted over the past year:

• CPAB Audit Quality Insights Report: 2020 Interim Inspection Results

• CPAB Audit Quality Insights Report: 2019 Annual Inspections Results

Visit our Audit Quality Resources page for more information including access to our Transparency report

We have attached our annual independence letter dated as of the date of this report in

Appendix 3.

Audit Findings Report P a g e | 16

Appendix 2: Management Representation Letter KPMG LLP Chartered Professional Accountants 115 King Street South 2nd Floor Waterloo, ON N2J 5A3

February 11, 2021

Ladies and Gentlemen:

We are writing at your request to confirm our understanding that your audit was for the purpose of expressing an opinion on the financial statements (hereinafter referred to as “financial statements”) of Ontario School Boards’ Insurance Exchange (“the Entity”) as at and for the period ended December 31, 2020.

General:

We confirm that the representations we make in this letter are in accordance with the definitions as set out in Attachment I to this letter.

We also confirm that, to the best of our knowledge and belief, having made such inquiries as we considered necessary for the purpose of appropriately informing ourselves:

Responsibilities:

1) We have fulfilled our responsibilities, as set out in the terms of the engagement letter dated December 11, 2020, including for:

a) the preparation and fair presentation of the financial statements and believe that these financial statements have been prepared and present fairly in accordance with the relevant financial reporting framework.

b) providing you with all information of which we are aware that is relevant to the preparation of the financial statements (“relevant information”), such as financial records, documentation and other matters, including:

— the names of all related parties and information regarding all relationships and transactions with related parties;

— the complete minutes of meetings, or summaries of actions of recent meetings for which minutes have not yet been prepared, of shareholders, board of directors and committees of the board of directors that may affect the financial statements. All significant actions are included in such summaries.

c) providing you with unrestricted access to such relevant information.

d) providing you with complete responses to all enquiries made by you during the engagement.

e) providing you with additional information that you may request from us for the purpose of the engagement.

Audit Findings Report P a g e | 17

f) providing you with unrestricted access to persons within the Entity from whom you determined it necessary to obtain audit evidence.

g) such internal control as we determined is necessary to enable the preparation of financial statements that are free from material misstatement, whether due to fraud or error. We also acknowledge and understand that we are responsible for the design, implementation and maintenance of internal control to prevent and detect fraud.

h) ensuring that all transactions have been recorded in the accounting records and are reflected in the financial statements.

i) ensuring that internal auditors providing direct assistance to you, if any, were instructed to follow your instructions and that we, and others within the entity, did not intervene in the work the internal auditors performed for you.

Internal control over financial reporting:

2) We have communicated to you all deficiencies in the design and implementation or maintenance of internal control over financial reporting of which we are aware.

Fraud & non-compliance with laws and regulations:

3) We have disclosed to you:

a) the results of our assessment of the risk that the financial statements may be materially misstated as a result of fraud.

b) all information in relation to fraud or suspected fraud that we are aware of that involves:

— management;

— employees who have significant roles in internal control over financial reporting; or

— others

where such fraud or suspected fraud could have a material effect on the financial statements.

c) all information in relation to allegations of fraud, or suspected fraud, affecting the financial statements, communicated by employees, former employees, analysts, regulators, or others.

d) all known instances of non-compliance or suspected non-compliance with laws and regulations, including all aspects of contractual agreements, whose effects should be considered when preparing financial statements.

e) all known actual or possible litigation and claims whose effects should be considered when preparing the financial statements.

Subsequent events:

4) All events subsequent to the date of the financial statements and for which the relevant financial reporting framework requires adjustment or disclosure in the financial statements have been adjusted or disclosed.

Related parties:

5) We have disclosed to you the identity of the Entity’s related parties.

6) We have disclosed to you all the related party relationships and transactions/balances of which we are aware.

Audit Findings Report P a g e | 18

7) All related party relationships and transactions/balances have been appropriately accounted for and disclosed in accordance with the relevant financial reporting framework.

Estimates:

8) The methods, the data and the significant assumptions used in making accounting estimates, and their related disclosures are appropriate to achieve recognition, measurement or disclosure that is reasonable in the context of the applicable financial reporting framework

Going concern:

9) We have provided you with all information relevant to the use of the going concern assumption in the financial statements.

10) We confirm that we are not aware of material uncertainties related to events or conditions that may cast significant doubt upon the Entity’s ability to continue as a going concern.

Misstatements:

11) We approve the corrected misstatements identified by you during the audit described in Attachment II.

Other information:

12) We confirm that the final version of Annual Report and French Annual Report will be provided to you when available, and prior to issuance by the Entity, to enable you to complete your audit procedures in accordance with professional standards.

Non-SEC registrants or non-reporting issuers:

13) We confirm that the Entity is not a Canadian reporting issuer (as defined under any applicable Canadian securities act) and is not a United States Securities and Exchange Commission (“SEC”) Issuer (as defined by the Sarbanes-Oxley Act of 2002).

14) We also confirm that the financial statements of the Entity will not be included in the group financial statements of a Canadian reporting issuer audited by KPMG or an SEC Issuer audited by any member of the KPMG organization.

Accounting Policies:

15) There have been no changes in, or newly adopted, accounting policies that have not been disclosed to you and appropriately reflected in the financial statements.

Assets & Liabilities – General:

16) There are no formal or informal compensating balance arrangements with any of our cash accounts.

17) The Entity has satisfactory title to all assets.

18) We have no knowledge of arrangements with financial institutions involving restrictions on cash balances and lines of credit or similar arrangements and not disclosed to you.

19) We confirm that during the period we complied with the externally imposed capital requirements.

Comparative Figures/Financial Statements:

20) We have no knowledge of any significant matters that may have arisen that would require a restatement of the comparative financial statements.

Audit Findings Report P a g e | 19

Representations Regarding Management Intent and Plans, and Other Information that is Known Only to Management:

21) We confirm that we have disclosed to you all information in relation to the following matters:

onerous contracts, i.e. those contracts under which the unavoidable costs of meeting the obligation exceed the economic benefits to be received under it, including losses arising from sale and purchase commitments that are onerous contracts under IAS 37 Provisions, Contingent Liabilities and Contingent Assets;

losses from transactions not recognised in the statement of financial position;

assets pledged as collateral;

arrangements with financial institutions involving restrictions on cash balances and lines of credit or similar arrangements;

22) The Entity has complied with all aspects of contractual agreements that could have a material effect on the financial statements in the event of non-compliance, for example debt covenants.

23) We have no plans or intentions that may affect the carrying amount or classification of assets and liabilities.

Representations Regarding Title to Assets, Classification and Carrying Amount of Assets, and Impairment of Assets:

24) The Entity has satisfactory title to all assets.

Financial Assets:

25) We have assessed all financial assets, except those measured at fair value through profit or loss, to determine whether there is any objective evidence of impairment as a result of one or more loss events that occurred subsequent to their initial recognition, and any impairments identified have been recognised in the financial statements, as appropriate. In respect of investments in equity instruments, we have recognised an impairment loss when there has been a significant or prolonged decline in the fair value of the instrument below cost, or other objective evidence of impairment. We have determined whether a decline in fair value below cost is ‘significant’ or ‘prolonged’ in accordance with criteria as represented to you.

Representations regarding the Entity’s appointed actuary:

26) We agree with the findings of the Appointed Actuary as the Entity’s specialist in evaluating the policy liabilities. In connection with the specialist’s valuation, we provided the specialist with all significant and relevant information of which we are aware. We did not give or cause any instructions to be given to the specialist with respect to the values or amounts derived in an attempt to bias their work, and we are not otherwise aware of any matters that have had an impact on the independence or objectivity of the specialists.

Representation Regarding Compliance with Externally Imposed Capital Requirements:

27) The Entity has complied with all externally imposed capital requirements.

Representations Regarding Exposures to Risks Arising from Financial Instruments:

28) We confirm that we have disclosed information relating to the Entity’s exposures to risks arising from financial instruments that is adequate to enable users to evaluate the nature and extent of those risks to which the Entity is exposed at the end of the reporting period, in accordance with IFRS 7, including the exposures to risks and how they arise, our objectives, policies and procedures for managing the risks, the methods used to measure risks, and a summary of quantitative data about our exposure to risks.

Audit Findings Report P a g e | 20

Representations Regarding Fair Values of Financial Assets and Financial Liabilities:

29) We believe the assumptions and techniques used by us are appropriate and that all fair value measurements are determined in accordance with IFRS 13.

30) We have appropriately disclosed fair values of financial assets and financial liabilities in the financial statements in accordance with IFRS 13. We believe the disclosures appropriately categorise those fair value measurements in the fair value hierarchy.

31) We have disclosed the methods and assumptions applied in determining the fair values of each class of financial instrument.

Other:

32) All reinsurance transactions entered into by the Entity are final and there are no side agreements with re-insurers, or other terms in effect, which allow for the modification of terms under existing reinsurance arrangements. Furthermore, the Entity’s reinsurance arrangements meet the risk transfer provisions under IFRS or are accounted for as deposits.

33) We have complied with OSFI guidelines in preparing the P&C Annual Return, specifically those financial statements contained on pages 20.010 to 20.060 of the P&C Annual Return.

34) We have complied with the provisions of the Insurance Companies Act, Canada.

Communications between actuaries involved in the preparation of financial statements and auditors:

35) We acknowledge that, in addition to your report on the financial statements of the Entity, you will also communicate on procedures and findings on data used in making accounting estimates relating to the valuation of actuarial liabilities as a result of the Joint Policy Statement Concerning Communications between Actuaries Involved in the Preparation of Financial Statements and Auditors (the “Joint Policy Statement”), at the request of the Appointed Actuary.

36) We consent to you providing the information resulting from your work as required by the Joint Policy Statement to the Chief Financial Officer and the Appointed Actuary.

37) We confirm that, to the best of our knowledge and belief, having made such inquiries as we considered necessary for the purposes of appropriately informing ourselves and understand that we are responsible for, and have fulfilled such responsibilities that the data used in making accounting estimates relating to the valuation of actuarial liabilities, and their related disclosures is complete and accurate to achieve recognition, measurement or disclosure that is reasonable in the context of the applicable financial reporting framework.

38) We acknowledge that the communication does not constitute an audit or review of data used in making accounting estimates relating to the valuation of actuarial liabilities and their related disclosures and therefore, you are not expressing an opinion on the completeness or accuracy of the data. Rather, the matters addressed in the communication with the Appointed Actuary are a by-product of your audit process in respect of the Entity’s financial statements.

39) We acknowledge that the communication is intended solely for the Chief Financial Officer and the Appointed Actuary and should not be used by, or distributed to, other parties.

Audit Findings Report P a g e | 21

Yours very truly,

______________________________________ Jim Sami, Chief Executive Officer and Attorney in Fact

_______________________________________ Sandra Taylor, Chief Financial Officer I have the recognized authority to take, and assert that I have taken, responsibility for the financial statements

cc: Audit Committee

Audit Findings Report P a g e | 22

Attachment I – Definitions

Materiality

Certain representations in this letter are described as being limited to matters that are material. Misstatements, including omissions, are considered to be material if they, individually or in the aggregate, could reasonably be expected to influence the economic decisions of users taken on the basis of the financial statements. Judgments about materiality are made in light of surrounding circumstances, and are affected by the size or nature of a misstatement, or a combination of both.

Fraud & error

Fraudulent financial reporting involves intentional misstatements including omissions of amounts or disclosures in financial statements to deceive financial statement users.

Misappropriation of assets involves the theft of an entity’s assets. It is often accompanied by false or misleading records or documents in order to conceal the fact that the assets are missing or have been pledged without proper authorization.

An error is an unintentional misstatement in financial statements, including the omission of an amount or a disclosure.

Attachment II – Summary of Audit Misstatements Schedule

Corrected Audit Misstatements

Income effect Financial position

Description F/J/P (Decrease) Increase

Assets (Decrease) Increase

Liabilities (Decrease) Increase

Equity (Decrease) Increase

To record the investment impairment provision on the Bank of Nova Scotia equity holdings with prolonged decline in value.

F ($286,574)

$286,574 $ - $ -

($286,574)

$286,574

Total misstatements $ - $ - $ - $ -

Audit Findings Report P a g e | 23

Appendix 3: Independence Letter

KPMG LLP 115 King Street South 2nd Floor Waterloo ON N2J 5A3 Tel 519-747-8800 Fax 519-747-8830 The Audit Committee of the Board of Directors Ontario School Boards’ Insurance Exchange 91 Westmount Road Guelph, ON N1H 5J2

February 2, 2020

Ladies and Gentlemen:

We have been engaged to express an opinion on the financial statements of Ontario School Boards’ Insurance Exchange (“the Exchange”) as at and for the year ended December 31, 2020.

In determining which relationships to report, we consider relevant rules and related interpretations prescribed by the relevant professional bodies and any applicable legislation or regulation, covering such matters as:

a) provision of services in addition to the audit engagement

b) other relationships such as:

- holding a financial interest, either directly or indirectly, in a client

- holding a position, either directly or indirectly, that gives the right or responsibility to exert significant influence over the financial or accounting policies

of a client

- personal or business relationships of immediate family, close relatives, partners or retired partners, either directly or indirectly, with a client

- economic dependence on a client

Audit Findings Report P a g e | 24

Provision of services

Except for pre-approved audit services, there are no other professional services rendered by us to the Companies from January 1, 2020, up to the date of this letter.

Professional standards require that we communicate the related safeguards that have been applied to eliminate identified threats to independence or to reduce them to an acceptable level. We have not provided any prohibited services. We have applied the following safeguards regarding threats to independence created by the services listed above:

- We instituted policies and procedures to prohibit us from making management decisions or assuming responsibility for such decisions.

- We obtained pre-approval of non-audit services and during this pre-approval process we discussed the nature of the engagement and other

independence issues related to the services.

- We obtained management’s acknowledgement of responsibility for the results of the work performed by us regarding non-audit services and we have

not made any management decisions or assumed responsibility for such decisions.

Other relationships

We are not aware of any other relationships between our firm and the Exchange that, in our professional judgement, may reasonably be thought to bear on our independence.

Confirmation of independence

We confirm that, as of the date of this letter, we are independent of the Exchange in accordance with the ethical requirements that are relevant to our audit of the financial statements in Canada.

Other matters

This letter is confidential and intended solely for use by those charged with governance in carrying out and discharging their responsibilities and should not be used for any other purposes.

KPMG shall have no responsibility for loss or damages or claims, if any, to or by any third party as this letter has not been prepared for, and is not intended for, and should not be used by, any third party or for any other purpose.

Yours very truly,

Licensed Public Accountants

Audit Findings Report P a g e | 25

Appendix 4: Draft Auditors’ Report INDEPENDENT AUDITORS’ REPORT (financial statements)

To the Subscribers of Ontario School Boards’ Insurance Exchange

Opinion

We have audited the financial statements of Ontario School Boards’ Insurance Exchange (the "Entity"), which comprise:

• the statement of financial position as at December 31, 2020

• the statement of income and comprehensive income for the year then ended

• the statement of changes in guarantee fund for the year then ended

• the statement of cash flows for the year then ended

• and notes to the financial statements, including a summary of significant accounting policies

(Hereinafter referred to as the "financial statements").

In our opinion, the accompanying financial statements present fairly, in all material respects, the financial position of the Entity as at December 31, 2020, and

its financial performance and its cash flows for the year then ended in accordance with International Financial Reporting Standards (IFRS).

Basis for Opinion

We conducted our audit in accordance with Canadian generally accepted auditing standards. Our responsibilities under those standards are further described

in the "Auditors' Responsibilities for the Audit of the Financial Statements" section of our auditors' report.

We are independent of the Entity in accordance with the ethical requirements that are relevant to our audit of the financial statements in Canada and we have

fulfilled our other ethical responsibilities in accordance with these requirements.

We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our opinion.

Other Information

Management is responsible for the other information. Other information comprises information, other than the financial statements and the auditors’ report

thereon, included in the Annual Report.

Our opinion on the financial statements does not cover the other information and we do not and will not express any form of assurance conclusion thereon.

In connection with our audit of the financial statements, our responsibility is to read the other information identified above and, in doing so, consider whether

the other information is materially inconsistent with the financial statements or our knowledge obtained in the audit, or otherwise appears to be materially

misstated.

Audit Findings Report P a g e | 26

We obtained the Information, other than the financial statements and the auditors’ report thereon, included in Annual Report at the date of this auditors’ report.

If, based on the work we have performed on this other information, we conclude that there is a material misstatement of this other information, we are required

to report that fact in the auditors’ report. We have nothing to report in this regard.

Responsibilities of Management and Those Charged with Governance for the Financial Statements

Management is responsible for the preparation and fair presentation of the financial statements in accordance with IFRS, and for such internal control as

management determines is necessary to enable the preparation of financial statements that are free from material misstatement, whether due to fraud or error.

In preparing the financial statements, management is responsible for assessing the Entity's ability to continue as a going concern, disclosing as applicable,

matters related to going concern and using the going concern basis of accounting unless management either intends to liquidate the Entity or to cease

operations, or has no realistic alternative but to do so.

Those charged with governance are responsible for overseeing the Entity's financial reporting process.

Auditors' Responsibilities for the Audit of the Financial Statements

Our objectives are to obtain reasonable assurance about whether the financial statements as a whole are free from material misstatement, whether due to

fraud or error, and to issue an auditors' report that includes our opinion.

Reasonable assurance is a high level of assurance, but is not a guarantee that an audit conducted in accordance with Canadian generally accepted auditing

standards will always detect a material misstatement when it exists.

Misstatements can arise from fraud or error and are considered material if, individually or in the aggregate, they could reasonably be expected to influence the

economic decisions of users taken on the basis of the financial statements.

As part of an audit in accordance with Canadian generally accepted auditing standards, we exercise professional judgment and maintain professional

skepticism throughout the audit.

We also:

• Identify and assess the risks of material misstatement of the financial statements, whether due to fraud or error, design and perform audit procedures

responsive to those risks, and obtain audit evidence that is sufficient and appropriate to provide a basis for our opinion.

The risk of not detecting a material misstatement resulting from fraud is higher than for one resulting from error, as fraud may involve collusion, forgery,

intentional omissions, misrepresentations, or the override of internal control.

• Obtain an understanding of internal control relevant to the audit in order to design audit procedures that are appropriate in the circumstances, but not for the

purpose of expressing an opinion on the effectiveness of the Entity's internal control.

• Evaluate the appropriateness of accounting policies used and the reasonableness of accounting estimates and related disclosures made by management.

• Conclude on the appropriateness of management's use of the going concern basis of accounting and, based on the audit evidence obtained, whether a

material uncertainty exists related to events or conditions that may cast significant doubt on the Entity's ability to continue as a going concern. If we conclude

that a material uncertainty exists, we are required to draw attention in our auditors' report to the related disclosures in the financial statements or, if such

disclosures are inadequate, to modify our opinion. Our conclusions are based on the audit evidence obtained up to the date of our auditors' report. However,

future events or conditions may cause the Entity to cease to continue as a going concern.

Audit Findings Report P a g e | 27

• Evaluate the overall presentation, structure and content of the financial statements, including the disclosures, and whether the financial statements represent

the underlying transactions and events in a manner that achieves fair presentation.

• Communicate with those charged with governance regarding, among other matters, the planned scope and timing of the audit and significant audit findings,

including any significant deficiencies in internal control that we identify during our audit.

Audit Findings Report P a g e | 28

INDEPENDENT AUDITORS’ REPORT (OSFI regulatory format financial statements)

To the Provincial Superintendents of Financial Institutions/Insurance

Opinion

We have audited the financial statements of Ontario School Boards’ Insurance Exchange (the "Entity"), which comprise:

• the statement of assets as at December 31, 2020

• the statement of liabilities, equity, head office account, reserves and AOCI as at December 31, 2020

• the statement of income for the year then ended

• the statement of comprehensive income (loss) and accumulated other comprehensive income (loss) for the year then ended

• the statement of reserves for the year then ended

• the statement of cash flows for the year then ended

• the statement of changes in equity for the year then ended

on pages 20.10 through 20.54 of the Entity’s P&C Quarterly Return and pages 20.52 and 20.60 of the Entity’s P&C Annual Supplement which includes the notes

to the financial statements, including a summary of significant accounting policies (collectively referred to as the "financial statements").

In our opinion, the accompanying financial statements present fairly, in all material respects, the financial position of the Entity as at December 31, 2020, and

its financial performance and its cash flows for the year then ended in accordance with International Financial Reporting Standards (IFRS).

Basis for Opinion

We conducted our audit in accordance with Canadian generally accepted auditing standards. Our responsibilities under those standards are further described

in the "Auditors' Responsibilities for the Audit of the Financial Statements" section of our auditors' report.

We are independent of the Entity in accordance with the ethical requirements that are relevant to our audit of the financial statements in Canada and we have

fulfilled our other ethical responsibilities in accordance with these requirements.

We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our opinion.

Other Matter – Unaudited Information

We have not audited or reviewed the schedules and exhibits except for those on pages 20.10 through 20.54 of the Entity’s P&C Quarterly Return and those on

pages 20.52 and 20.60 of the Entity’s P&C Annual Supplement. Accordingly, this auditors’ report and our opinion do not cover the schedules and exhibits on

other pages of the Entity’s P&C Quarterly Return and P&C Annual Supplement.

Audit Findings Report P a g e | 29

Responsibilities of Management and Those Charged with Governance for the Financial Statements

Management is responsible for the preparation and fair presentation of the financial statements in accordance with IFRS, and for such internal control as

management determines is necessary to enable the preparation of financial statements that are free from material misstatement, whether due to fraud or error.

In preparing the financial statements, management is responsible for assessing the Entity's ability to continue as a going concern, disclosing as applicable,

matters related to going concern and using the going concern basis of accounting unless management either intends to liquidate the Entity or to cease

operations, or has no realistic alternative but to do so.

Those charged with governance are responsible for overseeing the Entity's financial reporting process.

Auditors' Responsibilities for the Audit of the Financial Statements

Our objectives are to obtain reasonable assurance about whether the financial statements as a whole are free from material misstatement, whether due to

fraud or error, and to issue an auditors' report that includes our opinion.

Reasonable assurance is a high level of assurance, but is not a guarantee that an audit conducted in accordance with Canadian generally accepted auditing

standards will always detect a material misstatement when it exists.

Misstatements can arise from fraud or error and are considered material if, individually or in the aggregate, they could reasonably be expected to influence the

economic decisions of users taken on the basis of the financial statements.

As part of an audit in accordance with Canadian generally accepted auditing standards, we exercise professional judgment and maintain professional

skepticism throughout the audit.

We also:

• Identify and assess the risks of material misstatement of the financial statements, whether due to fraud or error, design and perform audit procedures

responsive to those risks, and obtain audit evidence that is sufficient and appropriate to provide a basis for our opinion.

The risk of not detecting a material misstatement resulting from fraud is higher than for one resulting from error, as fraud may involve collusion, forgery,

intentional omissions, misrepresentations, or the override of internal control.

• Obtain an understanding of internal control relevant to the audit in order to design audit procedures that are appropriate in the circumstances, but not for the

purpose of expressing an opinion on the effectiveness of the Entity's internal control.

• Evaluate the appropriateness of accounting policies used and the reasonableness of accounting estimates and related disclosures made by management.

• Conclude on the appropriateness of management's use of the going concern basis of accounting and, based on the audit evidence obtained, whether a

material uncertainty exists related to events or conditions that may cast significant doubt on the Entity's ability to continue as a going concern. If we conclude

that a material uncertainty exists, we are required to draw attention in our auditors' report to the related disclosures in the financial statements or, if such

disclosures are inadequate, to modify our opinion. Our conclusions are based on the audit evidence obtained up to the date of our auditors' report. However,

future events or conditions may cause the Entity to cease to continue as a going concern.

• Evaluate the overall presentation, structure and content of the financial statements, including the disclosures, and whether the financial statements represent

the underlying transactions and events in a manner that achieves fair presentation.

Communicate with those charged with governance regarding, among other matters, the planned scope and timing of the audit and significant audit findings,

including any significant deficiencies in internal control that we identify during our audit.

Audit Findings Report P a g e | 30

Appendix 5: KPMG’s System of Quality Control Quality control is fundamental to our business and is the responsibility of every partner and employee. To help all audit professionals concentrate on the

fundamental skills and behaviors required to deliver a quality audit, KPMG has developed the Audit Quality Framework shown below. These are the

cornerstones of how we execute our responsibilities

What do we mean by audit quality?

Audit Quality (AQ) is at the core of everything we do at KPMG.

We believe that it is not just about reaching the right opinion,

but how we reach that opinion.

We define ‘audit quality’ as being the outcome when audits are

executed consistently, in line with the requirements and intent

of applicable professional standards within a strong system of

quality controls.

All of our related activities are undertaken in an environment of

the utmost level of objectivity, independence, ethics, and

integrity.

Visit our Audit Quality Resources page for more information

including access to our Transparency report.

Audit Findings Report P a g e | 31

Appendix 6: Technology in the audit As previously communicated in our Audit Planning Report, we have utilized technology to enhance the quality and effectiveness of the audit.

Technology Our results and insights

KPMG iRADAR Our derivatives and securities valuation tool brings advanced valuation capability to independently re-price 100% of

your level 1, 2 investment securities and derivative instruments. Our detailed reporting provides you greater insight,

revealing instances where your pricing vendors may value sub-asset classes more conservatively or aggressively

than others.

Journal Entry Analysis Our journal entry tool assists in the performance of detailed journal entry testing based on engagement-specific risk

identification and circumstances. Our tool provides auto-generated journal entry population statistics and focusses

our audit effort on journal entries that are riskier in nature.

We use KPMG’s application software (IDEA) to evaluate the completeness of the journal entry population through a

roll-forward of all accounts.

We use computer-assisted audit techniques (CAATs) to assess journal entries and apply certain criteria to identify

potential high-risk journal entries for further testing.

Audit Findings Report P a g e | 32

Appendix 7: Audit and Assurance Insights Our latest thinking on the issues that matter most to audit committees, Boards and Management.

Featured insight Summary Reference

Audit & Assurance Insights Curated thought leadership, research and insights from subject matter experts across KPMG in Canada Learn more

The business implications of

coronavirus (COVID 19)

Resources to help you understand your exposure to COVID-19, and more importantly, position your

business to be resilient in the face of this and the next global threat. Learn more

Financial reporting and audit considerations: The impact of COVID-19 on financial reporting and audit

processes. Learn more

KPMG Global IFRS Institute - COVID-19 financial reporting resource center Learn more

Accelerate 2020 Perspective on the key issues driving the audit committee agenda Learn more

IFRS Breaking News A monthly Canadian newsletter that provides the latest insights on international financial reporting standards and IASB activities.

Learn more

Momentum

A quarterly Canadian newsletter which provides a snapshot of KPMG's latest thought leadership, audit

and assurance insights and information on upcoming and past audit events – keeping management and

board members abreast on current issues and emerging challenges within audit. Sign-up now

Current Developments Series of quarterly publications for Canadian businesses including Spotlight on IFRS, Canadian

Securities & Auditing Matters and US Learn more

Board Leadership Centre Leading insights to help board members maximize boardroom opportunities. Learn more

kpmg.ca/audit

© 2021 KPMG LLP, an Ontario limited liability partnership and a member firm of the KPMG global organization of independent member firms affiliated with KPMG International Limited, a private English company limited by guarantee. All rights reserved. The KPMG name and logo are trademarks used under license by the independent member firms of the KPMG global organization.

KPMG member firms around the world have 227,000 professionals, in 146 countries.

Financial Statements of

ONTARIO SCHOOL BOARDS' INSURANCE EXCHANGE

And Independent Auditors’ Report thereon

Year ended December 31, 2020

INDEPENDENT AUDITORS' REPORT

To the Subscribers of Ontario School Boards' Insurance Exchange

Opinion

We have audited the financial statements of Ontario School Boards’ Insurance

Exchange (the “Entity”), which comprise:

• the statement of financial position as at December 31, 2020

• the statement of comprehensive income for the year then ended

• the statement of changes in guarantee fund for the year then ended

• the statement of cash flows for the year then ended

• and notes to the financial statements, including a summary of significant

accounting policies

(Hereinafter referred to as the “financial statements”).

In our opinion, the accompanying financial statements present fairly, in all material

respects, the financial position of Ontario School Boards’ Insurance Exchange as at