Ort, Datum Autor Tax Relief for energy-intensive business in the framework of the ecological tax...

18

Ort, Datum Autor Tax Relief for energy- intensive business in the framework of the ecological tax reform and the climate change levy Michael Kohlhaas Presented at ECOTAXES IN GERMANY AND THE UNITED KINGDOM - A BUSINESS VIEW Berlin, 25 June 2004

-

date post

19-Dec-2015 -

Category

Documents

-

view

215 -

download

2

Transcript of Ort, Datum Autor Tax Relief for energy-intensive business in the framework of the ecological tax...

Ort, DatumAutor

Tax Relief for energy-intensive business in the framework of the

ecological tax reform and the climate change levy

Michael Kohlhaas

Presented at

ECOTAXES IN GERMANY AND THE UNITED KINGDOM - A BUSINESS VIEW

Berlin, 25 June 2004

M. Kohlhaas18.04.23

Outline

• Ecological Tax Reform in Germany• What are special provisions / tax concessions?• Motives for tax concessions• Criteria and constraints for special provisions• Design of special provisions• Tax concessions in Germany and the UK • Perspectives for Germany

M. Kohlhaas18.04.23

Ecological tax reform in Germany– Revenue-neutral tax reform – 5 steps between 1999 and 2003– Energy taxation

• Increase of taxes on petroleum products

• New tax on electricity

• Special provisions for energy-intensive production

• Additional revenue about € 18.6 milliard (billion)

– Revenue recycling• Reduction of social security contributions

M. Kohlhaas18.04.23

What are special provisions?

– Economic theory: uniform taxes induce efficient reduction of energy use or emissions

– Special provisions: deviations from a uniform taxation

– Tax differentiation between • energy carriers• users and • usage

M. Kohlhaas18.04.23

Motives for special provisions

Fear of adverse effects of taxes

– Economic Effects• International competitiveness • Premature retirement of capital (physical, human)• Distributive effects• Principle of “protection of confidence”

– Environmental Effects• Carbon leakage: reduction of emissions in one country may be (partially or

(over-)compensated by increase of emissions in other countries

Political acceptance

M. Kohlhaas18.04.23

Criteria and constraints for special provisions

– Avoid negative economic effects– Avoid carbon leakage– Preserve incentive effect of eco-tax– Legal constraints (national, European, international)– Administrative constraints– Market-based instrument, not discretionary– Conflicting objectives: weighting necessary

M. Kohlhaas18.04.23

Demarcation of beneficiaries

– The more precise the demarcation of the beneficiaries, the smaller will be the loss of incentive to reduce emissions and the loss of tax revenue.

– However, the necessary administrative procedures would be very complicated, be subject to substantial uncertainties and require ample scope of discretion.

Discretionary special provisions should be kept to a minimum if the idea of environmental taxes as a market-oriented instrument is taken seriously.

M. Kohlhaas18.04.23

Special provisions in Germany

– Do not apply to road fuels

– Broad and rules-based system:• Tax rates differentiated by energy carriers

• Reduced rates for broad-based categories

• Firm-specific tax rebates

M. Kohlhaas18.04.23

Tax rates (Euro per ton CO2)

0 50 100 150 200 250 300

Gasoline, unleaded

Diesel fuel

Electricity 1)

Natural gas

Heating oil

Heavy fuel oil

Coal

Euro per ton CO2

tax rate before April '99

Tax increase 1999 to 2003

1) Average CO2 emissions (0.56 kg per kWh)

M. Kohlhaas18.04.23

Germany 1 (draft law - not implemented)

– Reduced tax rates of 25% for all producers of the goods and materials sectors

– Tax exemption for producers which belong to an “energy-intensive” sector (energy-intensity > 2%

– Criticism:• energy intensity inappropriate indicator• statistical categories imply unequal treatment• reduction of net tax burden for energy-intensive activities

(perverse incentive effect)

M. Kohlhaas18.04.23

Germany 2 (1999 - 2002)

– Reduced tax rates of 20% (of the regular rates) for all producers of the goods and materials sectors

– Individual compensation for all tax payments exceeding reduction of pension contributions by more than 20% (tax cap)

M. Kohlhaas18.04.23

Germany 2: Criticism

– No perverse incentive effect – Individual firm data and not statistical

categories important for tax rebates– Restriction to goods and materials sectors

may imply unequal treatment – No incentive to improve energy efficiency

for energy-intensive enterprises

M. Kohlhaas18.04.23

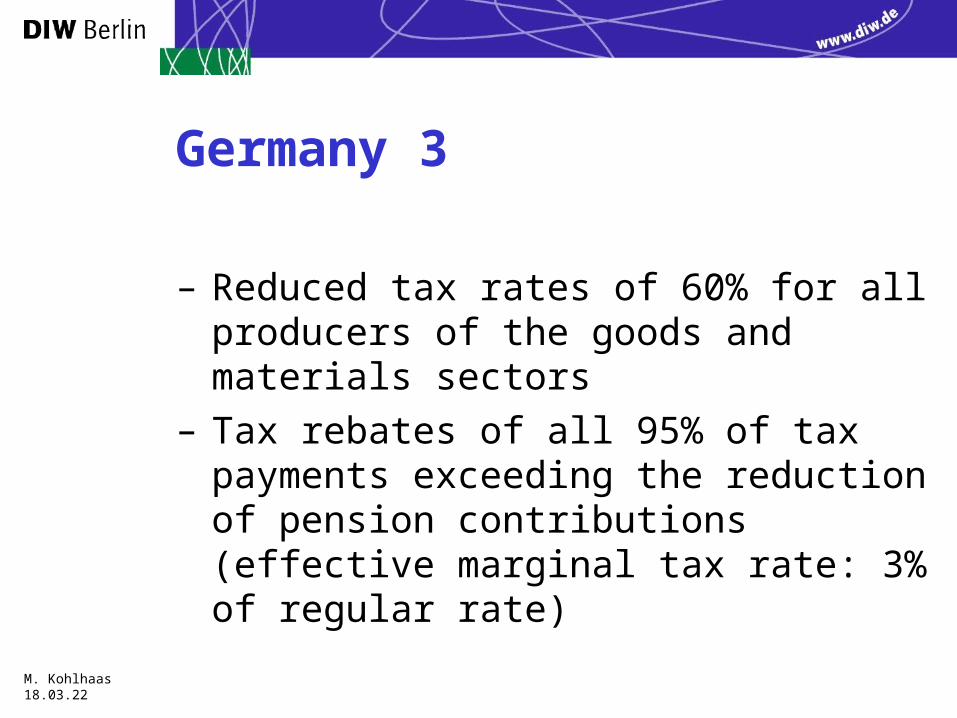

Germany 3

– Reduced tax rates of 60% for all producers of the goods and materials sectors

– Tax rebates of all 95% of tax payments exceeding the reduction of pension contributions (effective marginal tax rate: 3% of regular rate)

M. Kohlhaas18.04.23

Germany 2 and 3: Comparison

– Incentive effect is higher for some enterprises, but lower for others: net effect ambiguous

– Average tax burden is higher for most enterprises: positive revenue effect

– Danger: revenue raising may dominate environmental objectives

M. Kohlhaas18.04.23

Climate Change Levy

– Non-domestic users only– Taxable commodities

• Electricity• Natural gas• Coal and lignite• Coke, semi-coke and petroleum coke• LPG

– Not taxable commodities• Oil, gas oil, kerosene (subject to excise duties) • Road fuel gas (subject to fuel price escalator)• Heat• Steam

M. Kohlhaas18.04.23

Special provisions in UK

– Tax exemptions• Energy supplied in small quantities• Electricity used in electrolysis processes

- primary aluminum smelting- chlor-alkali processes

• Others:- Electricity from “new” renewables - good quality CHP

– Tax reductions: -80%• Energy-intensive sectors (as defined in PPC Regulations)• that are covered by Climate Change Agreements

M. Kohlhaas18.04.23

Some stylised differences

Germany– Broad rules-based system with little scope

and need for discretionary decisions– Weak incentive effect in industry

UK– CCL integrated with CCA and ET from the

beginning

M. Kohlhaas18.04.23

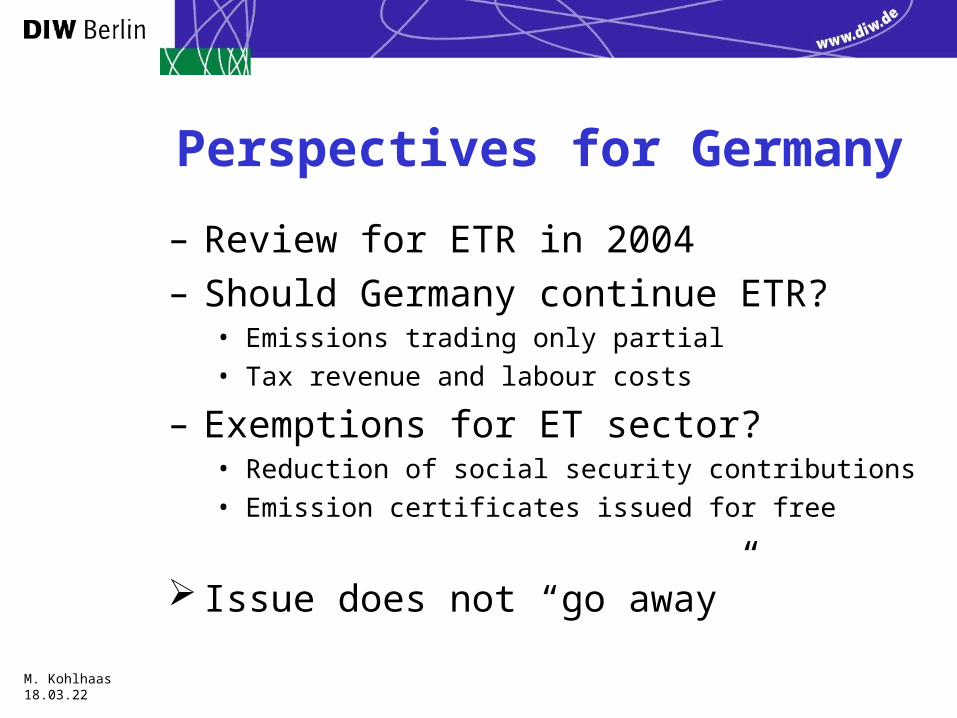

Perspectives for Germany

– Review for ETR in 2004– Should Germany continue ETR?

• Emissions trading only partial• Tax revenue and labour costs

– Exemptions for ET sector?• Reduction of social security contributions• Emission certificates issued for free

Issue does not “go away”