ORSERO GROUP Management · PDF fileORSERO GROUP Management Presentation Four Seasons Hotel,...

42

November 15, 2016 ORSERO GROUP Management Presentation Four Seasons Hotel, Milan

Transcript of ORSERO GROUP Management · PDF fileORSERO GROUP Management Presentation Four Seasons Hotel,...

November 15, 2016

ORSERO GROUP Management Presentation Four Seasons Hotel, Milan

2

Disclaimer

This document (the Document) was prepared by Glenalta Food S.p.A. (Company) and GF Group S.p.A. only for the purposes of presenting the business combination proposal between the Company and the GF Group S.p.A. target company (the Transaction). The information contained herein may not be complete and exhaustive and no guarantee can be given as to its accuracy. This Document was drafted on the basis of data and information of the Company and/or GF Group and/or in the public domain, and on parameters and assumptions determined in good faith by the Company. However, these parameters and assumptions are not the only ones that could have been selected for the purpose of preparing this document, therefore the application of additional parameters and assumptions, or the existence of different market conditions, could lead, in good faith, to analyses and assessments that may differ, in whole or in part, from those contained herein. The information and/or the assessments contained herein have not been subjected to verification by independent experts, and are subject to changes and/or updates. The Company and GF Group S.p.A. undertake no duty to give prior or subsequent communication in the event that any such changes and additions may become necessary or appropriate. No information contained in this Document can or shall be considered a guarantee or an indication of future operating, financial and equity results of the Company, of GF Group S.p.A. and/or of the company resulting from the Transaction. Within the law, the Company, GF Group S.p.A. and their corporate officers, managers, employees, and consultants do not make any declaration or guarantee and do not take any obligation, either express or implied, or responsibility as to the accuracy, sufficiency, completeness and update of any information contained in the Document nor in respect of any errors, omissions, inaccuracies or negligence herein. This Document is provided merely for information and indicative purposes and does not constitute in any way a proposal to enter into any contract nor a public offering of financial products, nor advice or a recommendation to buy or sell any financial products. You are the exclusive addressee of this Document which as such cannot be delivered nor disclosed to any third parties nor reproduced, in whole or in part, without the prior authorization of the Company.

3

Agenda

• Why Orsero?

• Presentation of the Orsero Group

• Key success factors

• Key Financials

Transaction structure and timetable

View of the European market

4

Why Orsero?

• FOOD segment has seen steady growth

• Strong competitive advantage

• Significant consolidated position in 5 Mediterranean countries/second largest group in the AIM

• New, enthusiastic, competent and motivated management team

• Solid cash flow, no CAPEX, no technological innovation

• The Group has shown its strength and ability in getting out of a challenging situation

• Group’s attractive entry price

• Glenalta Food’s significant contribution of new capital, specific expertise in the food and financial fields combined with listing on the stock exchange make up the necessary ingredients to start on an already well-defined growth path

5

• Why Orsero?

• Presentation of the Orsero Group

• Key Strengths

• Key Financials

Transaction structure and timetable

View of the European Market

Agenda

6

SHORT OVERVIEW OF THE ORSERO GROUP

Overview of the Orsero Group – Who We Are

• Mediterranean Europe leader in the import and distribution of fruit and vegetables

• Great attention to product quality: in 2012 the brand F.lli Orsero® for bananas and pineapples was launched, it is synonymous with tradition and passion for high-end products

• Over half a million tons of fruit and vegetable product distributed, with a pro forma consolidated sales* of approximately € 617 million (total turnover of about 850 M€**) in 2015

• International presence, mainly in Italy, France, Spain, Portugal, Greece, Costa Rica, Colombia and Mexico

• More than 2,000 employees worldwide (including more than 1,000 people in Europe)

GROUP STRUCTURE, ACTIVITIES AND SEGMENTS IN WHICH THE GROUP OPERATES

• 3 integrated business divisions coordinated by the Holding parent company, 10 main società subsidiaries and 6 relevant 50%-owned Joint Ventures

Group Structure

Main activities

Clients and segments

• Fruit and Vegetable Products distributed to large-scale retail chains and traditional wholesalers

• Shipping services for third parties (other product importers and distributors) and forwarding agent

• Import and Distribution of fruit and vegetables

• Bananas and Pineapples Tropical division and own ships for transport

• Tropical Fruit Production (bananas and avocados)

* Pro forma financials include the effects of transactions preliminary to the Business Combination ** Proportionally consolidated revenues of the Group amounted to approx. €730 million, including the JVs portion attributable to the GF Group.

7

Main Areas of Activity

Production

The Group is active in three macro-areas

3 Import and Distribution

Bananas and Pineapples

Tropical division

2

5 countries

2 different SKUs

5 countries

~ 300 different SKUs

~ 500,000 tons Distributed every year

1

2 countries

2 different SKUs

~ 14 million boxes imported every year

~ 4,500 hectares of land of which 2,500 hectares currently in production

GR

IT FR PL ES

CR

PA

CO EC

DOM

MEX

CR

8

• Careful checks on product quality throughout the supply chain

Our Business

Sourcing

Import

Quality Control

Storage Ripening

Distribution

• 25 warehouses throughout Southern Europe for storage and control of fresh produce

5

20 centres across Southern Europe dedicated to the ripening of bananas

4

Personal long-term relationships and partnership with industry-

leading suppliers

Sales

6 3

2 7

1

Selection of the world’s best production areas to offer the best

produce

Wide spread daily distribution and

bespoke solutions for customers

Logistics efficiency also thanks to the our owned "Cala Rosse"

reefer fleet

Daily sales through distribution to large-scale

retail chains and traditional channels in different key

markets

Import and

distribution of perishable

fresh produce

9

Main Milestones from 1940 to Date

1940s

1970s

1990s

Beginning of our fruit distribution business in

Italy

Development of distribution and import of exotic fruits and counter season fruits

thanks to the launch of a new commercial partnership with

Del Monte

1980s

Beginning of our investment in banana production through the purchase of plantations in

Costa Rica and in the banana ripening and

distribution business in France

2000

2006

Investments in the distribution sector in Italy, Portugal and Greece and beginning of the shipping

business with the construction of the first "Cala Bianche" reefer

fleet

Expansion in Spain and Italy through the acquisition of stakes in

certain retail sector businesses.

2007

2013

2014

2015

Diversification into adjacent/third

businesses

Interruption of business relationship with Del Monte and launch of the “fratelli

Orsero” brand

The crisis

Refocusing on the Group’s core business and beginning of the

disinvestment policy.

In 2015, organisational review and management

reinforcement.

10

• Why Orsero?

• Presentation of the Orsero Group

• Key success factors

• Key Financials

Transaction structure and timetable

View of the European Market

Agenda

11

Factors behind our Success

LEADERSHIP POSITION FOR OVER 50 YEARS

• in the import and distribution of fruit and vegetables in Mediterranean Europe

WIDESPREAD PRESENCE IN THE INTERNATIONAL ARENA

LOGISTICS AND DISTRIBUTION EFFICIENCY BRAND REPUTATION

STRATEGIC VISION

• Global product sourcing

• Extensive domestic presence

• since 2012 the brand «Fratelli Orsero" has been synonymous with market excellence

• direct control over daily/weekly transportation of main products

• Wide product range and bespoke distribution capabilities

• traceability along the entire chain

FRESH PRODUCE KNOW HOW

• both commercially and organisationally

12

Turnover and Product Mix – Distribution BU

2015 TURNOVER

In 2015, the Group reported a total turnover of some €850 million, of which some €720 million from its distribution

core business in Southern Europe*

DISTRIBUTED PRODUCT FAMILIES

# 1

Each year, the Group markets 50 million product boxes containing over 300

different SKUs

Data in %

# 3 # 2 # 1

Bananas

Pineapples

Citrus fruits

Pears & Apples

Kiwis

Exotic fruits

Melons

Grapes

Vegetables

Other

* Total turnover, including 100% of the Orsero Group’s JVs, and excluding the companies belonging to the BU Production (Acapulco), BU Tropical division (Cosiarma, Simba) and BU other activities (Fresh produce, holding and subholding) Source: Orsero financial statements, management

Dati in M€ 720 337

148170

3520

Spain France Italy Total Greece Portugal

35

85 120

Share owned by the Orsero Group

312

85

600

347

13

Main Customers and Distributed Brands

BRANDS AND PRIVATE LABELS MAIN CUSTOMERS

The Group supplies all leading large-scale retail chains in Southern Europe

and is present in the main fruit and vegetable market stands of major

international players

In addition to its own brands, the Group is a leading distributor of main fruit and vegetable brands (and private labels)

in Europe

Distributed brands

14

Industrial Footprint and Distribution Channels

EUROPEAN DISTRIBUTION MAP MAIN PRODUCT ORIGINS

27 Fruit and vegetable market stands

35,000 Capacity of fruit and banana storage (pallets)

160,000 sqm of total working area

EUROPEAN DISTRIBUTION MIX

Data in %

49%

20%

55%39% 46%

51%

80%

45%61% 54%

Spain

100%

France

100%

Greece Italy

100% 100%

Portugal

100%

Supermarkets Wholesalers Data in %

25 Warehouses for product handling

20 Ripening centres in Europe

500,000+ Tons of products distributed each year

Overseas products

14%

Bananas and Pineapples

49%

Total

100%

25%

EU products

12%

Domestic products

15

Global Logistics Management

01

02

03

04

05

06

Distribution efficiency guaranteed by an extensive

network of Group subsidiaries and affiliates in Europe

Efficiency of distribution by sea guaranteed by 4 owned reefer

vessels engaged in weekly transportation services

Top-notch product quality guaranteed by ability to control

product temperature at all times including during shipment (by sea or

by land)

High quality and reliability of distribution to wholesalers and

large-scale retail chains guaranteed by widespread domestic presence, with

platforms specialized in fresh produce storage and handling

Bespoke customer service guaranteed by 360° product handling capabilities (i.e.

picking)

Strong orientation towards ever greater efficiency and

optimization of logistics/distribution

performance

16

"Cala Rossa" Service for the Import of Bananas and Pineapples

THE "CALA ROSSA" ROUTE

"CALA ROSSA" MAIN FEATURES

Rio Haina

Moin

Turbo

Central America

Europe

Tarragona

Vado Ligure

Lisbon

4 owned reefer vessels carrying produce of the Orsero Group (40-50% of the total) and of major international importers (50-60% of the total)

Storage (50% in the hold and 50% in reefer containers)

10,500 pallets

Average cruise speed of each cargo ship

22 knots

Total round trip (1 week ahead of the competition)

28 days Average time of unloading

(50% less than competitors)

<18 hours

17

Quality Control throughout the Supply Chain

SUPPLY CHAIN OF OVERSEAS PRODUCE

PLANTATION PORT OF

SHIPMENT REEFER CARGO

SHIP

PORT OF DISCHARGE

WAREHOUSE / MARKET

CUSTOMER

• Quality control in the boarding phase carried out by the owner as per the importer's details.

• Check of temperature adequacy during the boarding phase

• Daily quality controls of produce temperature, inside the hold or inside the containers

• Management of different temperatures according to:

- Organoleptic characteristics of produce (i.e. Banana 13.3° - 14.5°, pineapple 7/8°)

- "Behaviour" of produce during shipment

• Quality control during the unloading phase, carried out directly by the importer

• Measurement of:

- Temperature

- Pressure (which determines the product preservation)

- Brix (sugar content)

• Incoming Quality Control (temperature/pressure) to optimise produce rotation

• Outgoing Quality Control (compliance with customers’ requirements)

Quality control throughout the supply chain, utmost control of the cold chain and guaranteed traceability of the products for end customers

18

Reputation through Distribution of "Fratelli Orsero"-branded Products

“FRATELLI ORSERO” BRAND POTENTIAL AND DEVELOPMENT

• In 2012, after the termination of the business relationship with Del Monte (that had been in place since the early 1970s), the Group launched its own “Fratelli Orsero” brand

• The brand awareness has grown rapidly, from 27% in 2012 to 61% in 2014

• The brand has become an established name and showed excellent growth:

‣ in Europe, Orsero branded pineapples and bananas recorded average annual growth rates of over 20-25% between 2012 and 2015

• These results are even more evident at the Italian distribution level, including other categories of fruit (exotic, citrus fruits, etc.)

‣ The average annual growth rate between 2012 and 2015 of Orsero branded products has been 40% (~ 20% of total products sold - 45,000 tons)

• The excellent trend is being confirmed in 2016, in spite of the product availability issues at the product origin experienced in 2015

19

Strategic Vision

Internal Growth Operational efficiency Growth through acquisitions

• Consolidating Group's positioning in key markets

• Leveraging market leadership position in Italy

• Developing partnerships with local producers (at EU level)

• Assessing investment opportunities in other markets/ products

• Evolution of the logistics approach at European level

• Re-definition of business processes/procedures for harmonisation across the Group

• Targeted monitoring of performance of the distribution platforms

• Implementing a new integrated ERP system across the Group

• Market shares recovery

• Expansion in geographical areas throughout the country

• Further growth of the F.lli Orsero brand (fresh cut, exotic fruits, berries)

• Development of new business lines ('fresh cut' fruits, dried fruits)

• Identification and development of new sales channels (vending machines for Bananas, HORECA sector, etc.)

ACTION PLAN BASED ON CORE BUSINESS TO ACHIEVE

20

• Why Orsero?

• Presentation of the Orsero Group

• Key success factors

• Key Financials

• Transaction structure and timetable

• View of the European Market

Agenda

21

Key Financials – Evolution of Economic Indicators

Turnover

adjusted-EBITDA*

• Data shown in the charts are based on the Orsero Group’s pro forma consolidated financial statements reflecting the listing perimeter that reflect the effects of the transactions preliminary to the Business Combination

• The Orsero Group is recording significant growth of turnover and profitability (EBITDA and EBIT) at consolidated level

• The final pro forma data at June 30, 2016 consistently confirm this trend

Adjusted-EBIT*

* Note: adjusted-EBITDA and EBIT not include extraordinary items (i.e. extraordinary charges and income)

22

FY H1

P&L (M€) 2015 2016

Total sales 617,2 337,6

Other revenues 10,6 4,0

TOTAL REVENUES 627,8 341,6

Raw materials (428,2) (228,3)

Services (111,1) (58,8)

Use of thir party assets (14,9) (7,1)

Personnel (43,9) (22,4)

Change in raw materials 1,6 3,4

Other costs (3,8) (2,1)

Costs of goods sold (600) (315)

EBITDA adjusted 27,5 26,2

EBITDA % 4,4% 7,7%

Amortizations (17,6) (8,9)

Depreciations (3,4) (1,5)

EBIT adjusted 6,5 15,8

Financial items (4,8) (1,1)

Adjustments to financial operations 0,9 1,8

Extraordinary items 6,3 (3,0)

Net profit before tax 8,9 13,5

Taxes 7,1 (2,1)

Net profit 16,0 11,4

Key Financials – Pro forma Consolidated P&L

• Consolidated revenues for H1 2016 confirm the growth trend. These revenues do not include the portion of revenues relating to the 50% Italy-Spain JVs that are accounted by using the equity method

• Adjusted EBITDA does not include extraordinary items; in 2015 EBITDA was already aligned with industry 'best in class' globally. H1 2016 EBITDA is particularly positive due to the excellent performance of the 'Bananas and Pineapple Tropical Division BU’ and constant growth of the ‘Distribution BU’ in Italy, France and Portugal

• At adjusted-EBIT level, depreciation (mainly related to owned Ships, warehouse equipment and F.lli Orsero brand) shows consistency in H2 vs. H1, with the good performance of EBITDA in H1 (physiologically higher than in H2) creating an extremely positive effect on adjusted EBIT for the first six months of the year

• Net income had an excellent performance reflecting inter alia:

- reduced financial expenses in 2016 compared to 2015

- positive 2015 taxes due to the recognition of a “one-off tax assets/deferred tax assets”

Note: adjusted EBITDA and EBIT do not include extraordinary items (extraordinary charges and income) Note 2: Data shown in the table refer to the Group’s pro forma consolidated financial statements illustrative of the listing perimeter

23

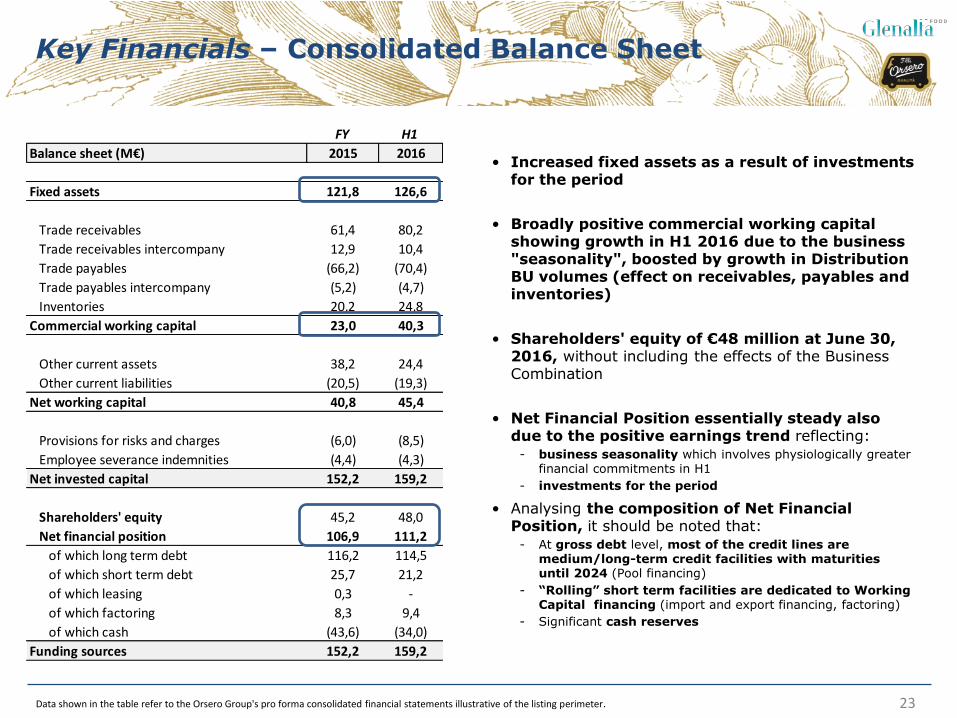

FY H1

Balance sheet (M€) 2015 2016

Fixed assets 121,8 126,6

Trade receivables 61,4 80,2

Trade receivables intercompany 12,9 10,4

Trade payables (66,2) (70,4)

Trade payables intercompany (5,2) (4,7)

Inventories 20,2 24,8

Commercial working capital 23,0 40,3

Other current assets 38,2 24,4

Other current liabilities (20,5) (19,3)

Net working capital 40,8 45,4

Provisions for risks and charges (6,0) (8,5)

Employee severance indemnities (4,4) (4,3)

Net invested capital 152,2 159,2

Shareholders' equity 45,2 48,0

Net financial position 106,9 111,2

of which long term debt 116,2 114,5

of which short term debt 25,7 21,2

of which leasing 0,3 -

of which factoring 8,3 9,4

of which cash (43,6) (34,0)

Funding sources 152,2 159,2

Key Financials – Consolidated Balance Sheet

• Increased fixed assets as a result of investments for the period

• Broadly positive commercial working capital showing growth in H1 2016 due to the business "seasonality", boosted by growth in Distribution BU volumes (effect on receivables, payables and inventories)

• Shareholders' equity of €48 million at June 30, 2016, without including the effects of the Business Combination

• Net Financial Position essentially steady also due to the positive earnings trend reflecting:

- business seasonality which involves physiologically greater financial commitments in H1

- investments for the period

• Analysing the composition of Net Financial Position, it should be noted that:

- At gross debt level, most of the credit lines are medium/long-term credit facilities with maturities until 2024 (Pool financing)

- “Rolling” short term facilities are dedicated to Working Capital financing (import and export financing, factoring)

- Significant cash reserves

Data shown in the table refer to the Orsero Group's pro forma consolidated financial statements illustrative of the listing perimeter.

24

• Why Orsero?

• Presentation of the Orsero Group

• Key success factors

• Key Financials

Transaction structure and timetable

View of the European Market

Agenda

25

Valuation at a glance

Valuation method:

Market multiples

EBITDA margin linear regression as "sanity check"

Equity Value: €80 m

Valuation method:

Net Asset Value

NAV of Glenalta(1): €80 m

(1) Assuming minimum withdrawal of shareholders

26

Benchmark with Market Peers

Source: Capital IQ – S&P, data updated at November 10, 2016

The table above shows a selected sample of listed companies operating in the same sector as the Target Company.

The average reported in the table shows an EV/EBITDA multiple equal to 10.32x for LTM data.

Fruits - Public Comps Set - Sorted by Market Cap

EUR millions except per share data, as of

November 10, 2016 Current % of 52 P/E EV/FCF

Company Price Week High Equity Enterprise LTM 2016E LTM 2016E LTM 2016E LTM 2016E LTM LTM

Fresh Del Monte Produce Inc. - NYSE € 56,33 92% € 2.918 € 3.047 € 3.590 € 3.691 € 299 € 321 0,85x 0,83x 10,21x 9,50x 22,77x 22,43x

Total Produce plc - ISE 1,69 94% 541 € 712 3.033 3.141 69 73 0,23x 0,23x 10,33x 9,73x 18,74x 14,25x

Fyffes plc - ISE 1,43 86% 469 € 569 1.075 1.176 55 64 0,53x 0,48x 10,42x 8,89x 14,10x 18,34x

MAX 0,85x 0,83x 10,42x 9,73x 22,77x 22,43x

AVERAGE 0,54x 0,51x 10,32x 9,37x 18,54x 18,34x

MEDIAN 0,53x 0,48x 10,33x 9,50x 18,74x 18,34x

MIN 0,23x 0,23x 10,21x 8,89x 14,10x 14,25x

EV/EBITDA

Valuation MultiplesStock Performance

Market Value Revenues EBITDA EV/REV

27

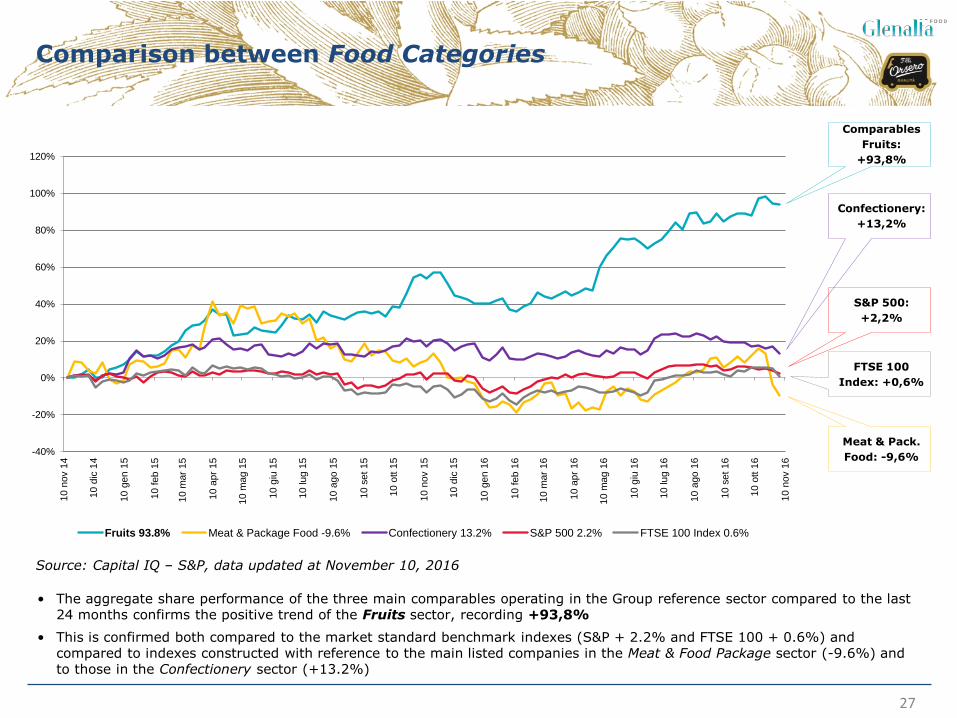

Comparison between Food Categories

Source: Capital IQ – S&P, data updated at November 10, 2016

• The aggregate share performance of the three main comparables operating in the Group reference sector compared to the last 24 months confirms the positive trend of the Fruits sector, recording +93,8%

• This is confirmed both compared to the market standard benchmark indexes (S&P + 2.2% and FTSE 100 + 0.6%) and compared to indexes constructed with reference to the main listed companies in the Meat & Food Package sector (-9.6%) and to those in the Confectionery sector (+13.2%)

Comparables

Fruits:

+93,8%

FTSE 100

Index: +0,6%

Confectionery:

+13,2%

S&P 500:

+2,2%

Meat & Pack.

Food: -9,6% -40%

-20%

0%

20%

40%

60%

80%

100%

120%

10 n

ov 1

4

10 d

ic 1

4

10 g

en 1

5

10 feb 1

5

10 m

ar

15

10 a

pr

15

10 m

ag 1

5

10 g

iu 1

5

10 lug 1

5

10 a

go 1

5

10 s

et 15

10 o

tt 1

5

10 n

ov 1

5

10 d

ic 1

5

10 g

en 1

6

10 feb 1

6

10 m

ar

16

10 a

pr

16

10 m

ag 1

6

10 g

iu 1

6

10 lug 1

6

10 a

go 1

6

10 s

et 16

10 o

tt 1

6

10 n

ov 1

6

Fruits 93.8% Meat & Package Food -9.6% Confectionery 13.2% S&P 500 2.2% FTSE 100 Index 0.6%

28

Structure of the Transaction

Transaction structure

• The share exchange ratio was set at 43 newly issued ordinary shares of Glenalta for each 50 ordinary shares held by GF Group

• The Transaction will be implemented through the merger of GF Group into Glenalta

Equity Value of the GF Group: €80 million

Use of Glenalta resources

Lock-up Agreement

• The shareholders of GF Group will commit to locking up ordinary shares held by them for 36 months from the effective date of the Merger

• The Glenalta Promoters have committed to locking up ordinary shares for 18 months from the effective date of the Merger

Governance

• Up to €80.0 million which will be used as follows:

- €25 million for purchases of equity linked instruments

- up to €55 million cash contribution resulting from the merger for acquisitions and investments

• The Board of Directors of the Combined Entity will be composed by 7 members, of which: - 5 members appointed by the GF Group shareholders, of wich 2 independent

members

- 2 members, namely Mr Luca Giacometti and Mr Gino Lugli, appointed by Glenalta

29

Shareholdings upon the Business Combination M

inim

um

wit

hd

raw

als

%

% of the voting rights (1)

Max w

ith

draw

als

%

(1) The given percentages (i) take into account of the conversion of the first tranche of Glenalta special shares (equal to 50,000 special shares) into ordinary shares (equal to 300,000 ordinary shares) that in accordance with the Articles of Association of Glenalta will take place on the seventh trading day following the effective date of the Transaction and (ii) exclude the possible dilution resulting from the exercise of outstanding Glenalta warrants. (2) Figures were calculated using the same assumptions under (i), (ii) referred to in footnote (1), also assuming a first market price of the Combined Entity shares of €10.00 per share.

Market Cap(2): € 138,5 m Market Cap(2): € 114,5 m

FIF Holding

40,4%

Mercato

57,4%

Spac Promoters

2,2%

FIF Holding

48,7%

Mercato

48,7%

Spac Promoters

2,6%

Market

Market

30

• Why Orsero?

• Presentation of the Orsero Group

• Key success factors

• Key Financials

Transaction structure and timetable

View of the European Market

Agenda

31

In Europe, in the Coming Years

PEOPLE WILL CONSUME LESS

PEOPLE WILL CONSUME DIFFERENTLY

32

Five Interconnected Macro Social Phenomena

• IMPOVERISHMENT (consuming less and more selectively)

• AGEING (increase in average life expectancy)

• ATTENTION TO HEALTH (shift from the cure of diseases to health and wellbeing)

• ENVIRONMENTAL AWARENESS (perception of a world collapsing)

• TIMES AND WAYS OF EATING (eating at different times and in different ways)

33

Fruit: from occasionally eaten at the end of a meal to a daily food basis

• INCREASE IN CONSUMPTION FREQUENCY (fruit is healthy)

• INCREASE IN CONSUMPTION TIMES (breakfast, between meals)

• INCREASE IN CONSUMPTION OCCASIONS (snacks, ready meals)

• INCREASE IN CONSUMPTION PLACES (out of home, appetizers)

34

Who will take advantage of this great opportunity?

• BUSINESS SIZE AND GLOBAL MARKET COVERAGE

• EXPERTISE IN FRESH PRODUCE, WITH SHORT SHELF LIFE

• CONSOLIDATED INTERNATIONAL RELATIONSHIP NETWORK

• SUPPLIER CONFIDENCE

• CUSTOMER CONFIDENCE

• ABILITY TO EXPRESS LEADERSHIP THROUGH A GLOBAL BRAND

• CONSUMER CONFIDENCE IN THE BRAND

35

Special thanks

• Banca Aletti - NOMAD (Francesco Pili, Gianlorenzo Gatti, Matteo Sacco)

• Business Support (Andrea Silvello, Roberto Di Lauro, Mattia Vene, Andrea Stretti)

• AON (Massimo Germani, Emma Zolezi)

• CFO SIM (Filippo Maria Palmarini, Luca Di Liddo)

• CloseToMedia (Elisabetta Neuhoff, Luca Manzato)

• Deloitte (Santo Rizzo, Giovanna Rebolino, Angela Canepa)

• Kaleidos Finance (Lorenzo Bachschmid, Dario Di Iorio)

• KPMG (Paola Maiorana, Massimiliano Battaglia, Luca De Caprio)

• Long Term Partners (Marco Costaguta, Vincenzo Santelia, Lorenzo Colombo)

• PriceWaterHouse Coopers (Elena Cogliati, Fabrizio Cigliese, Giovanni Poggio, Aida Di Spiezio, Gabriele Ravanelli)

• Studio BonelliErede (Vittorio Lupoli, Fabio Macri)

• Studio Gatti Pavesi Bianchi (Stefano Valerio, Franco Barucci, Vanessa Sobrero, Jacopo Zingoni, Dario

Prestamburgo)

• Studio STS Deloitte (Fabrizio Cavalli, Roberto Famà)

• Studio Giliberti Triscornia (Federico Fisher)

• Studio Lombardi Molinari Segni (Federico Vermicelli, Alberto Recchia)

• Studio Ludovici (Paolo Ludovici, Michele Aprile)

• Studio Munari Giudici Maniglio (Francesco Munari, Paolo Giudici, Paolo Terrile, Matteo Bet)

37

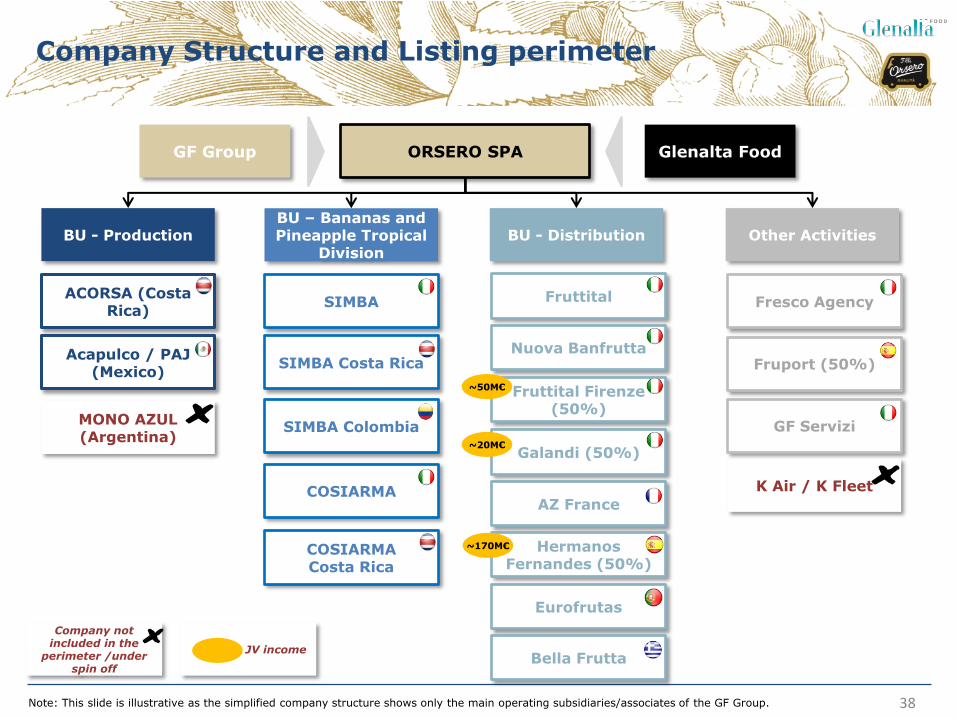

Annexes

• Company Structure and Scope of Transaction

• Management Team

38

JV income

Company Structure and Listing perimeter

ORSERO SPA

BU - Production BU - Distribution BU – Bananas and Pineapple Tropical

Division

GF Group Glenalta Food

Other Activities

COSIARMA

Fruttital

AZ France

SIMBA

SIMBA Costa Rica

SIMBA Colombia

COSIARMA Costa Rica

ACORSA (Costa Rica)

Acapulco / PAJ (Mexico)

MONO AZUL (Argentina)

Eurofrutas

Nuova Banfrutta

Bella Frutta

Hermanos Fernandes (50%)

Fruttital Firenze (50%)

Fresco Agency

Fruport (50%)

GF Servizi

K Air / K Fleet

Galandi (50%)

Company not included in the

perimeter /under spin off

Note: This slide is illustrative as the simplified company structure shows only the main operating subsidiaries/associates of the GF Group.

~50M€

~20M€

~170M€

39

Management Team - GF Group

Manager Function/ Company

Professional Background

Raffaella Orsero

Paolo Prudenziati

Matteo Colombini

Tommaso Cotto

Daniele Gazzano

President of GF Group Spa since 2013. Born in Savona (Italy) on 1966, after graduating in law, in 1993 she began her career in Simba SpA, a GF Group subsidiary and appointed CEO thereof in 2002. From 2003 to 2007 she also served as CEO of Reefer Terminal S.p.A. In September 2013 she was appointed Group CEO, a position she held until July 2015.

Born in Milan (Italy) on 1956. After graduating in Agricultural Sciences, in 1981 he began his career at Cargill. In 1989, he joined Chiquita Brands International with various management responsibilities at international level, to then become Senior Vice President Trading and Emerging Markets and CEO of Chiquita Italia. He joined the Group in 2016 and was appointed CEO.

Born in Bologna (Italy) on 1983. After graduating in Law and Business Administration and obtaining a Master’s Degree in General Management from Milan Bocconi University, he started out his career at Bank of Ireland, then in 2008 he joined Bain & Company Italy Inc. where he remained until 2015 when he joined GF Group SpA as Group Chief Financial Officer.

Born in Biella (Italy) in 1986. He holds a degree in Industrial Engineering from Italy’s Turin Polytechnic and a degree in Business Administration from ESCP-Europe. He began his career at Bain & Company Italy Inc. in 2010 as a consultant. He joined GF Group Spa in November 2015 as Chief Operating Officer.

Born in Alassio (SV, Italy) on 1958. He holds a degree in Economics, is a chartered accountant and is registered with the Register of Auditors. Mr Gazzano began his professional career in 1984 at the company Olivetti. He joined GF Group in 1991 as Managing Director of Fruttital Srl and in 1998 he was appointed Managing Director of the parent company. He sits on several Boards of Directors of subsidiaries of the Group.

Alessandro Piccardo

Born in Albenga (SV, Italy) on 1964. He holds a degree in History, and joined GF Group Spa in 1998 as assistant to the Sales Director of the Reefer Terminal Spa. From 2007 to 2015 he served as Chairman and CEO. He sits on the Boards of Directors of several companies of GF Group, and since 2014 he has been Group HR & External Relations Manager.

Vice president, MD

and CEO

President, MD and

CCO

MD and CFO

COO

General Counsel

HR and external

relationships

40

The Management Team – Main subsidiaries

Manager Function/ Company

Professional Background

Philippe Pons

João Mendes

AZ France

Eurofrutas

Chairman of AZ France SA, born in Algiers (Algeria) on 1958, he holds a degree in Agricultural Sciences. Mr Pons began his career in 1983 in Pomona SA, a company that is the market leader in France in fruit and vegetable trade. He joined the AZ Group in 1989, in 1997 he became sales director and in 2000 he was appointed General Manager.

Born in Setubal (Portugal) on 1961. Bachelor of Administration at the Stonehill College, Massachusetts, in 1984. After several experiences in some companies of the sector, in 2006 became MD of Chiquita Portugal, in 2012 was appointed Deputy Managing Director of Bargosa Fruit Company. In 2015 joined the Group as CEO of the company Eurofrutas Lda.

Manlio Ginocchio

Luca Tarabella

Cosiarma

Bella Frutta

Born in Camogli (GE, Italy) on 1967. After finishing high-school (Scientific Lycee), at a young age he started his career in the Reefer Container Maintenance & Repair sector. He joined the Group in 1997 as Container Division Manager at Costa Container Lines SpA. In 2014 he was appointed CEO of Cosiarma Spa.

Born in Mesagne (BR, Italy) on 1971. He holds a degree in Economics. After various experiences as Export Sales Manager in food companies, he joined the Group as sales director of Bella Frutta SA and appointed CEO thereof in 2012.

Calogero Canalella

Fruttital/ Simba

Born in Alassio (SV, Italy) on 1971. Soon after graduating in Economics, he joined the Group in the administration and finance department of the company Simba S.p.A., then he moved to the sales department where he held positions of increasing responsibility up to becoming CEO in 2012. Since 2013 he has also been a member of the Board of Directors of the company Fruttital Srl where he serves as sales director.

41

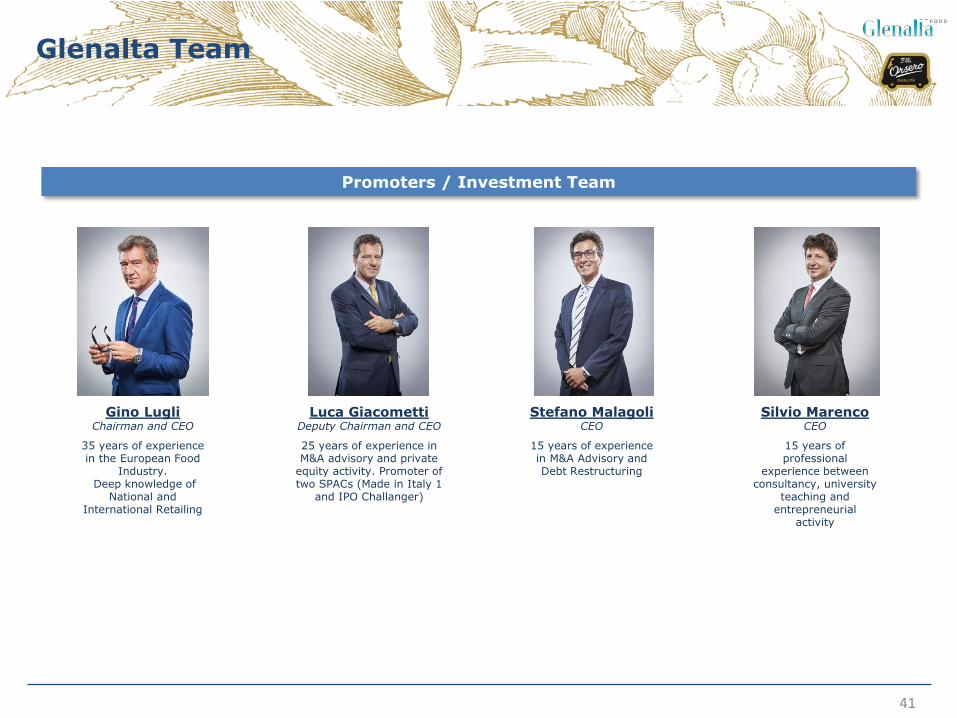

Glenalta Team

Gino Lugli Chairman and CEO

35 years of experience in the European Food

Industry. Deep knowledge of

National and International Retailing

Promoters / Investment Team

Luca Giacometti Deputy Chairman and CEO

25 years of experience in M&A advisory and private

equity activity. Promoter of two SPACs (Made in Italy 1

and IPO Challanger)

Stefano Malagoli CEO

15 years of experience in M&A Advisory and Debt Restructuring

Silvio Marenco CEO

15 years of professional

experience between consultancy, university

teaching and entrepreneurial

activity