Organization of Aab Petroleum Exporting Countries (OAPEC)s3.amazonaws.com/zanran_storage/ ·...

267

Transcript of Organization of Aab Petroleum Exporting Countries (OAPEC)s3.amazonaws.com/zanran_storage/ ·...

Organization of Aab Petroleum Exporting Countries (OAPEC)

The Secretary General’s 35th Annual Report

A.H. 1428-1429 / A.D. 2008

All rights reserved. The Organization of Arab Petroleum Exporting Countries (OAPEC), 2008

OAPEC

P.O.Box 20501 SAFAT, 13066 Kuwait

State of Kuwait,

Tel: (00965) 495000 Fax: (00965) 4959755

Email: [email protected] & [email protected]

Website: http://www.oapecorg.oro

______________________________________________________________________________

THE MINISTERIAL COUNCIL

H.E. Dr. Chakib Khelil People’s Democratic Republic of Algeria

H.E. Abdul Hussein bin Ali Mirza Kingdom of Bahrain

H.E. Eng. Samih Samir Fahmy Arab Republic of Egypt

H.E. Dr.Hussein Al-Shahrastani Republic of Iraq

H.E. Eng. Mohammad Abdullah Al-Ulaim State of Kuwait

H.E. Dr. Shokri Mohammad Ghanim Great Socialist People’s

Libyan Arab Jamahiriyah H.E. Abdullah bin Hamad Al-Attiyah State of Qatar

H.E. Eng. Ali bin Ibrahim Al-Naimi Kingdom of Saudi Arabia

H.E. Eng. Sufian Al-Alaw Syrian Arab Republic H.E. Mohammad Bin Zaen Al-Hamly United Arab Emirates

______________________________________________________________________________

THE EXECUTIVE BUREAU

Mr. Mohamed Ras Al Kaf People’s Democratic Republic of Algeria

Mr. Ali Abdul Jabar Al-Sawad Kingdom of Bahrain

Mr. Ahmad Saeed Al Ashmawi Arab Republic of Egypt

Mr. Abdul Sahib Salman Qutob Republic of Iraq

Eng. Adel Abdul Aziz Al-Jasim State of Kuwait Mr. Fathi Mohammed El-Abbar Great Socialist People’s

Libyan Arab Jamahiriyah Mr. Salem Buti Al-Naimi State of Qatar

Mr. Nasser Bin Ibrahim Al-Fouzan(1) Kingdom of Saudi Arabia Dr. Hassan Zainub Syrian Arab Republic

Mr. Nasser Mohammed Al-Sharhan United Arab Emirates

_____________________________________________________

______________________________________________________________________________

THE JUDICIAL TRIBUNAL

Dr. Moustafa Abdul Hayy Al-Sayed President

Shaikh Abdul Rahman bin Jaber Al Khalifa

Vice-President

Mr. Jawad Omar Al-Sakka Member

Dr. Nabil Abdullah El-Araby Member

Mr. Khalifa Daalouj Al-Kobaissi Member

______________________________________________________________________________

THE GENERAL SECRETARIAT

Mr. Abdul Aziz A. Al-Turki(1) Secretary General

The Arab Center for Energy Studies

Dr. Mohammed Mukhtar Al-Lababidi Director of the Technical Affairs Department

Dr. Jamil Mohammed Tahir Director of the Economics Department

Mr. Aissa Siouda Acting Supervisor of the Information and Library Department

_____________________________

Director of the Finance and Administrative Affairs Department*

* The Finance and Administrative Affairs

Department is currently under the supervision of the Secretary General

____________________________________________________

Contents

CONTENTS PREFACE ................................................................................................................ 1

PART ONE

INTERNATIONAL DEVELOPMENTS IN OIL AND ENERGY

CHAPTER ONE: DEVELOPMENTS IN GLOBAL MARKETS AND THEIR IMPACT ON OAPEC MEMBER COUNTRIES

Foreword…… ….… .. …………………….…...……………………………………… 3 I. Major Developments in the World Oil Market in 2008And Related

Factors …………………………………………………………………….……4

1. Supplies………………..…………………….……………..……………….. 4 1-1 OPEC Supplies………….…………………………………………. 5 1-2 Non-OPEC Supplies……………..………………………………….. 7 2. World Oil Demand…………………..………………………...………….. 7 2-1 OECD Countries…………………….…………………………..…… .…. 11 2-2 Developing Countries…………………..…..…..………………….….... 12 2-3 Countries in Transition……………………...……………………… 12 3. Price Trends …... ….… …..……... …..… .. .…………….…..….………… 13 3-1 Crude Oil Prices…………………………………………………… 13

3-2 Spot Prices for Oil Products………………………………...……… 14 3-2-1 Premium Gasoline Prices …………………………………………. 15 3-2-2 Gasoil /Diesel Prices……………………...…………………… 16 3-2-3 Fuel Oil Prices……………………………………………………… 16 3-3 Oil Freight Prices………………………..……………...……… 16 4. World Oil Inventories…………………………………………… 17 4.1 World Commercial Stocks……………………………………...…… 18 4.2 US Strategic Petroleum Reserve………………...…………...… 18

II. Value of OAPEC Member Countries Petroleum Exports……………. 19 III. Developments in Oil and Energy Consumption in the Arab Countries…...

20 1. Arab Countries……..………………….. ………..….….………………… 20

1-1 Total and Per Capita Energy Consumption……..……...............… 21

Contents

1-2 Energy Consumption by Source…….……............…. …….…….……. 23

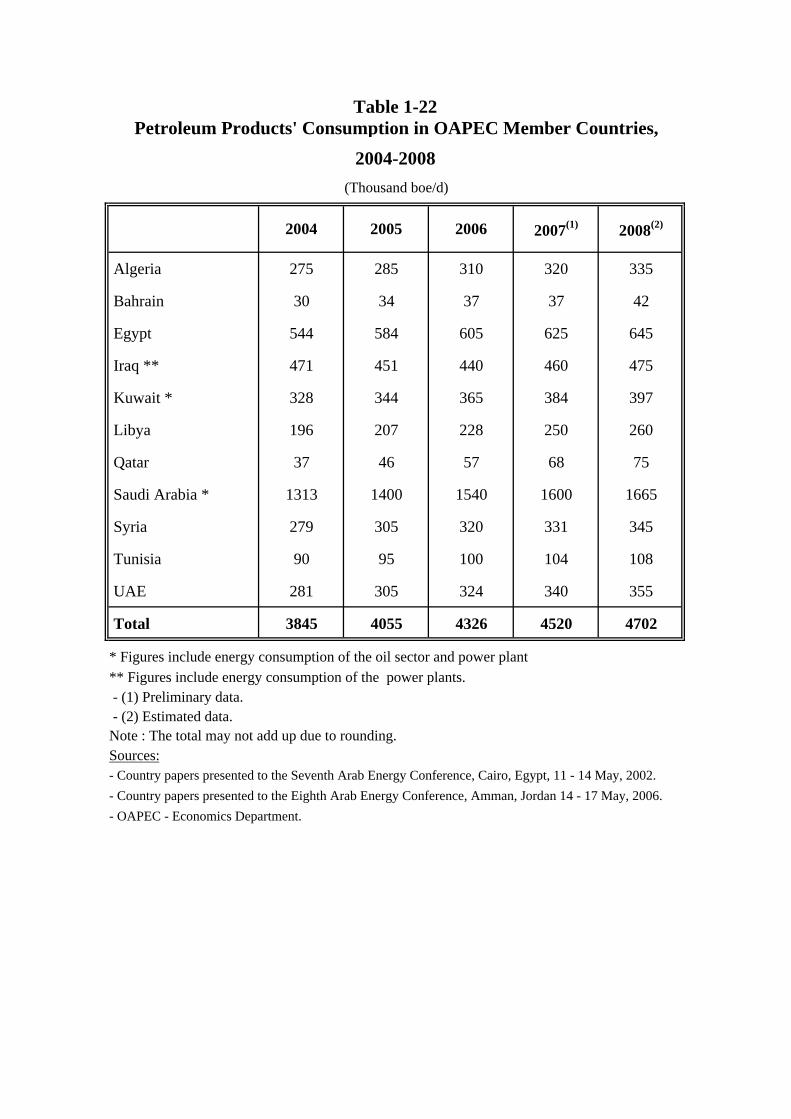

1-2-1 Petroleum Products…………………………………………………….. 26

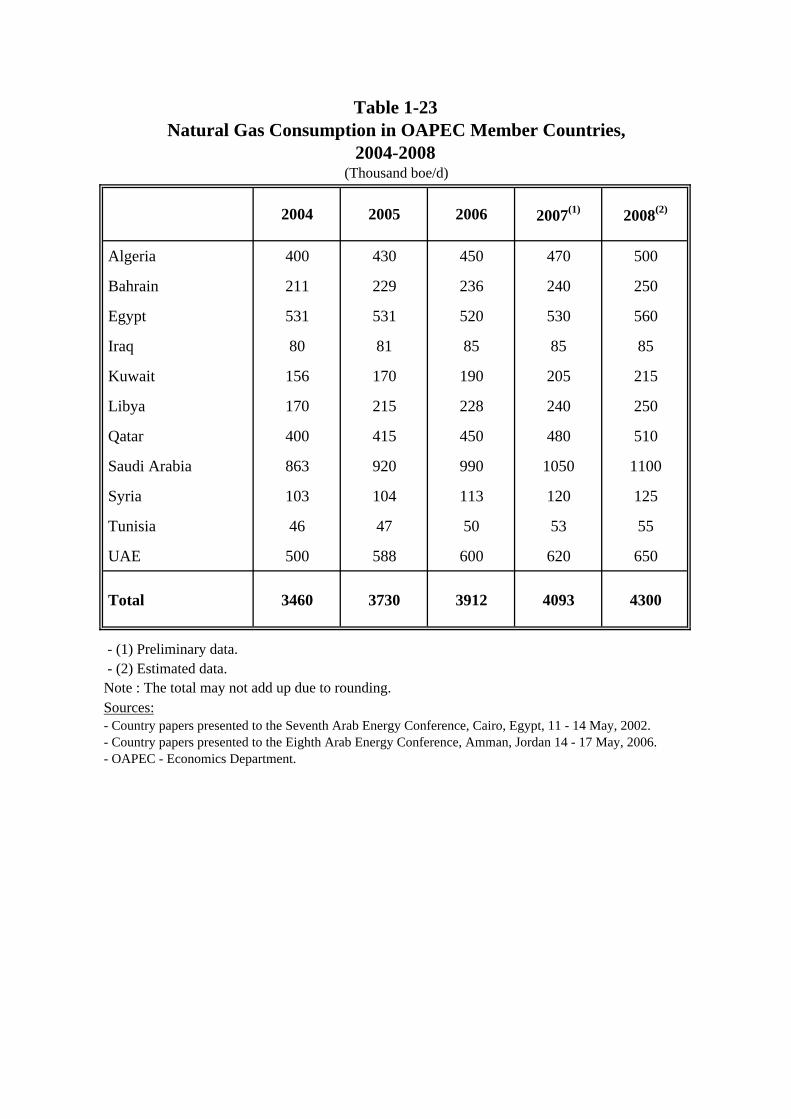

1-2-2 Natural Gas………... ………………..… ………..………………………. 27

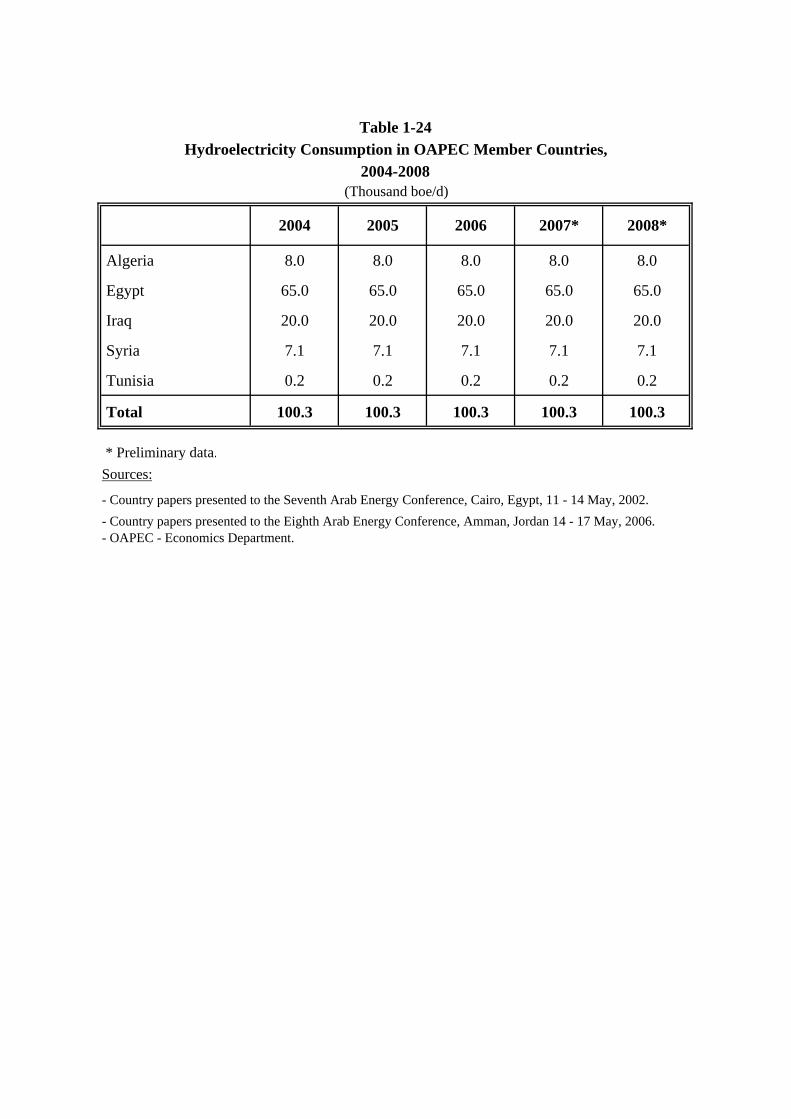

1-2-3 Hydroelectricity…………………..…………………… …..….………… 28

1-2-4 Coal……... ……………….…………………… ……… …..….………… .. 28

2. Total Energy Consumption in OAPEC Member Countries.. ………. 29

2-1 Total and Per Capita Energy Consumption………………….. 29

2-2 Energy Consumption by Source…………………….…………… 30

2-2-1 Petroleum Products. ……….……… . ………………..… ………. .……… 31

2-2-2 Natural Gas ……………..… . ……….……… ………. ………………..…. 32

2-2-3 Hydroelectricity and Coal………… ……... .. .……………………….. 33 3. Final Energy Consumption in Arab Countries……...………………… 34

3-1 Final Energy Consumption by Source...…………………….……… 34

3-1-1 Final Consumption of Petroleum Products….………………………... 34

3-1-2 Final Consumption of Natural Gas………….…………….………… 35

3-1-3 Final Consumption of Electricity………..…………………….…….. 35

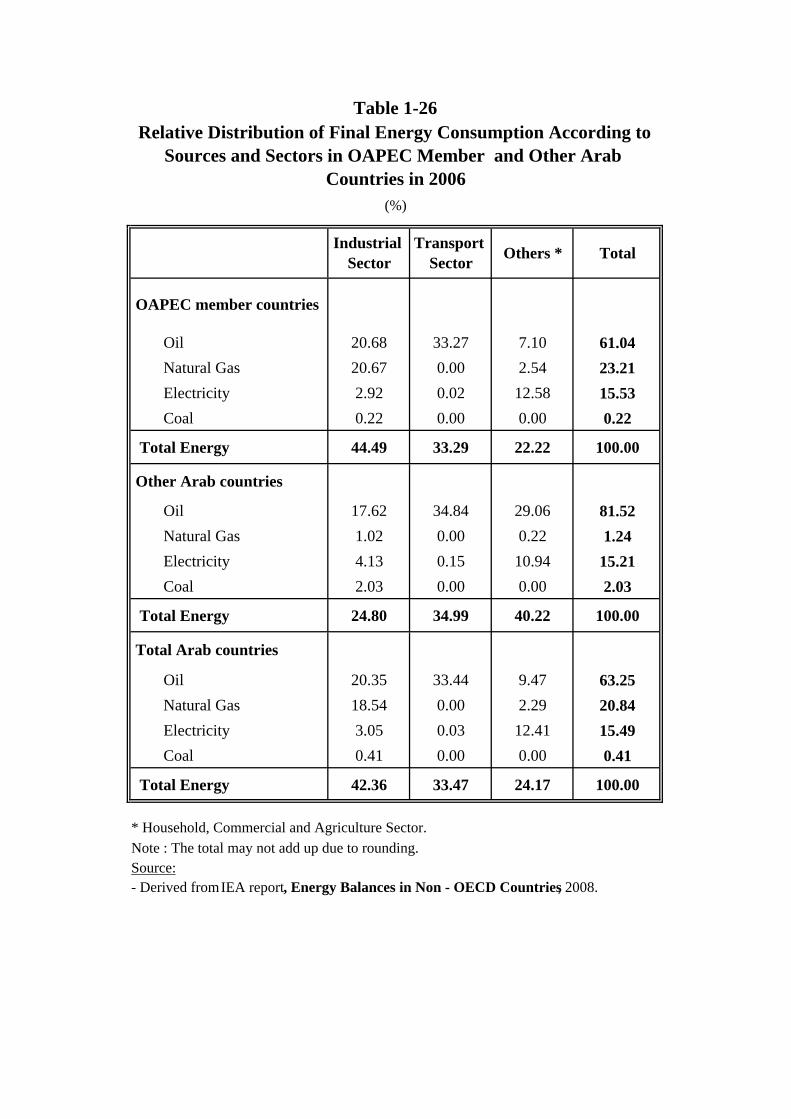

3-2 Final Energy Consumption by Sector ..........… ..……………………. 35

3-2-1 Energy Consumption in the Industrial Sector……………….…..……. 36

3-2-2 Energy Consumption in the Transport Sector……………………… 36

3-2-3 Energy Consumption in Other Sectors of the Economy………….….. 36

4. Local Prices………………………………………………….……………... 37

CHAPTER TWO: ARAB AND WORLD DEVELOPMENTS IN

THE EXPLORATION, RESERVES AND PRODUCTION OF ENERGY RESOURCES

I. Oil and Gas……. .……… .………… …………………….…………….……… 69

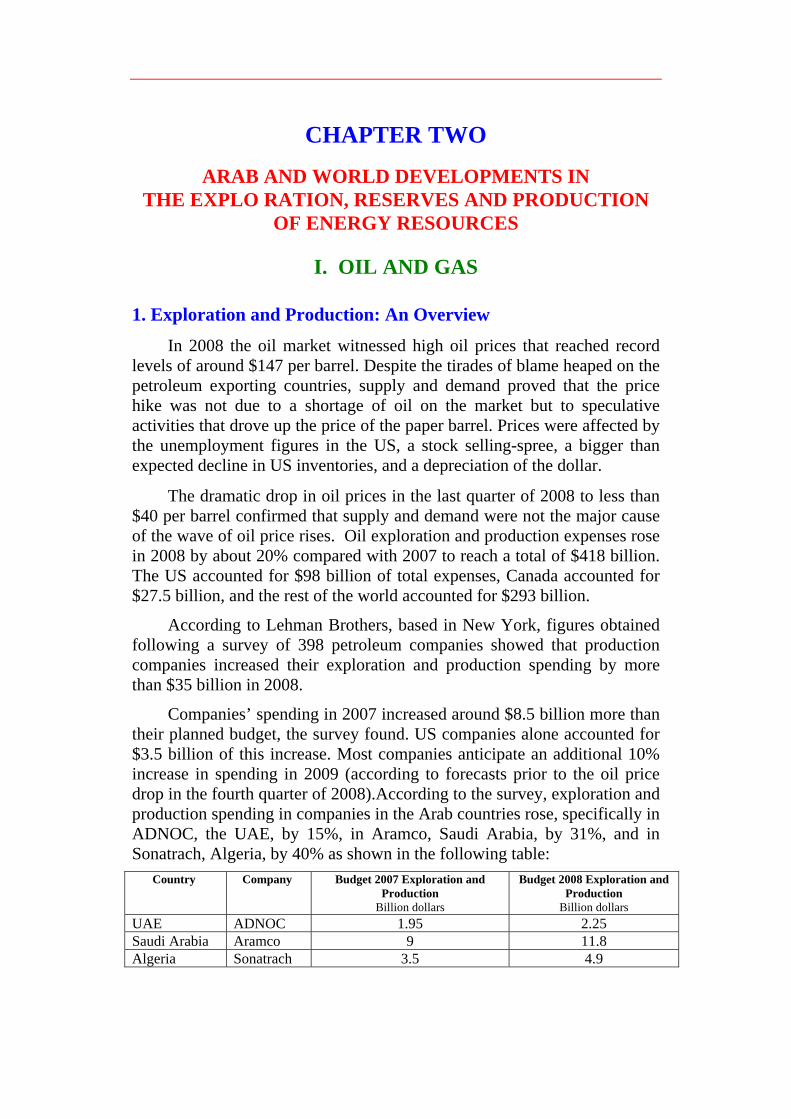

1. Exploration and Production: An Overview…….. .……… … ….……… 69

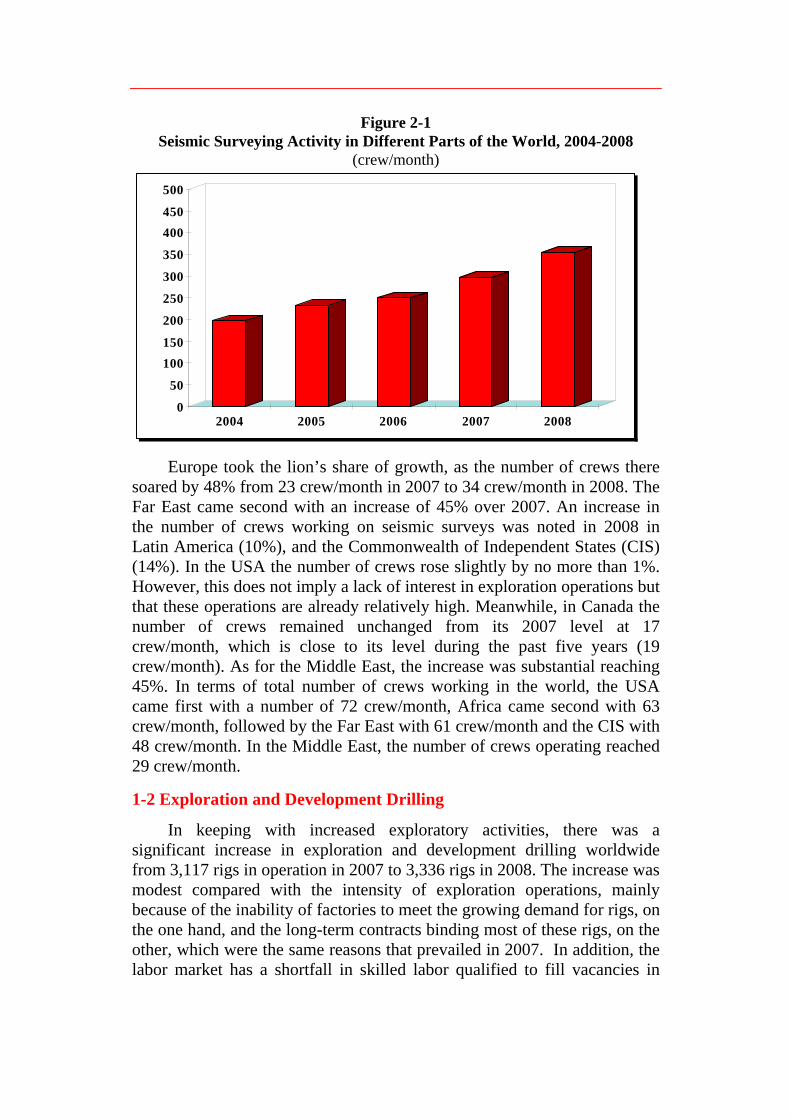

1-1 Seismic Surveys……..... ……….………….……………………… …….... 74

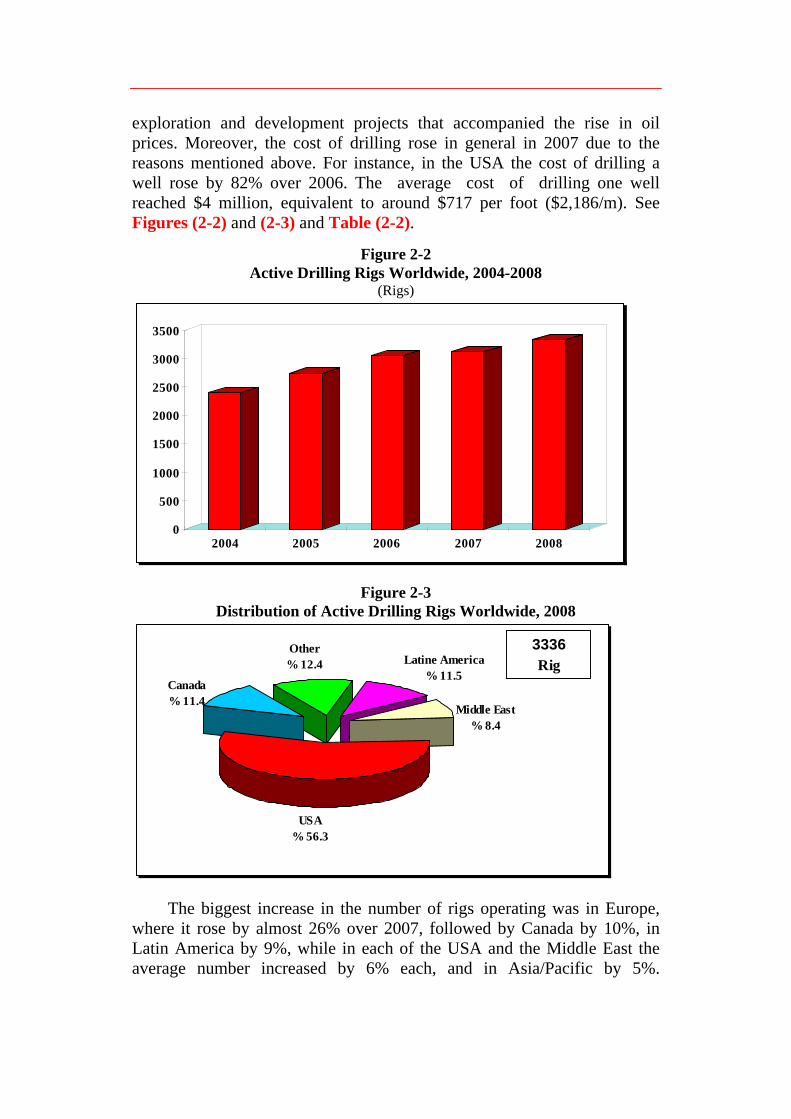

1-2 Exploratory and Developmental Drilling………….............................. 75

2. Oil and Natural Gas Reserves………..... ……………….………. .……… 78

2-1 Oil Reserves………..…………….. ……….……………… ………………. 78

Contents

2-1-1 OAPEC Members and Other Arab Countries............................................. 78

2-1-2 OPEC Countries………………………………………...………………… 79

2-1-3 North Sea………………………………………………………………….. 80

2-1-4 North America……………...……………………………………………... 80

2-1-5 CIS and China…………………...………………………………………... 80

2-1-6 Brazil………………...………………………….………………………... 80

2-1-7 Rest of the World…………………………………………………...……… 80

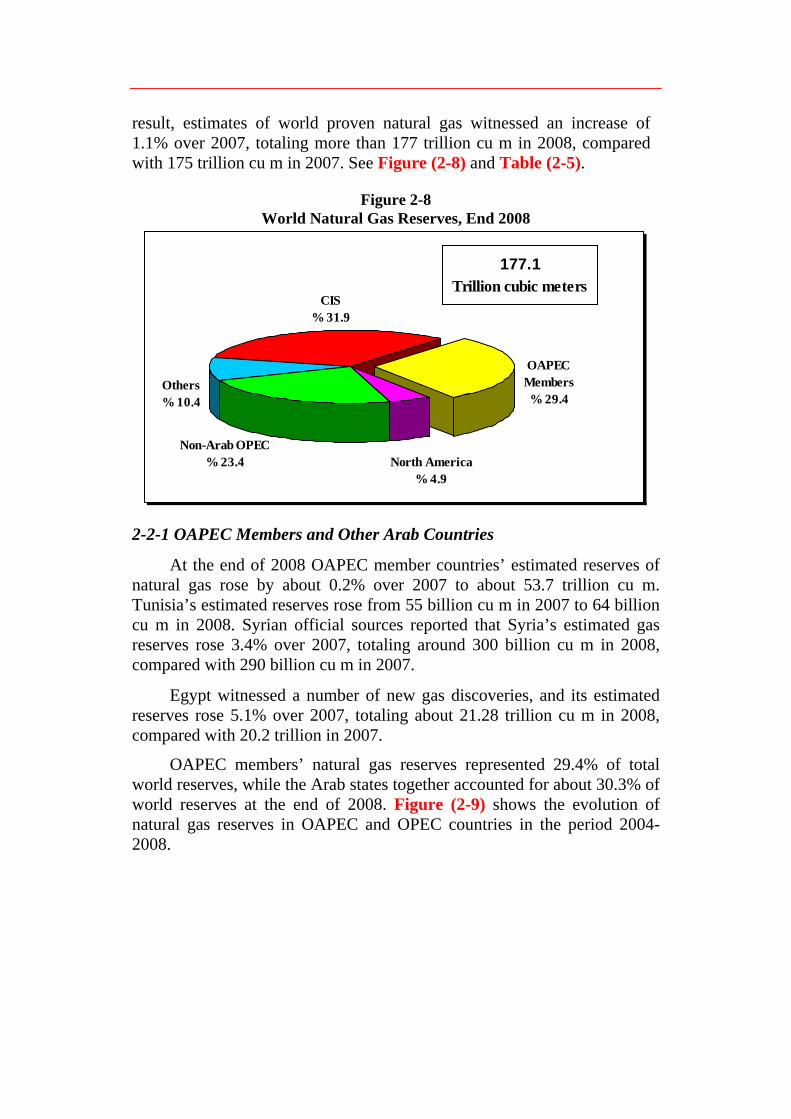

2-2 Natural Gas Reserves……………………………..………………...…. 81

2-2-1 OAPEC Members and Other Arab Countries……………..…………….. 81

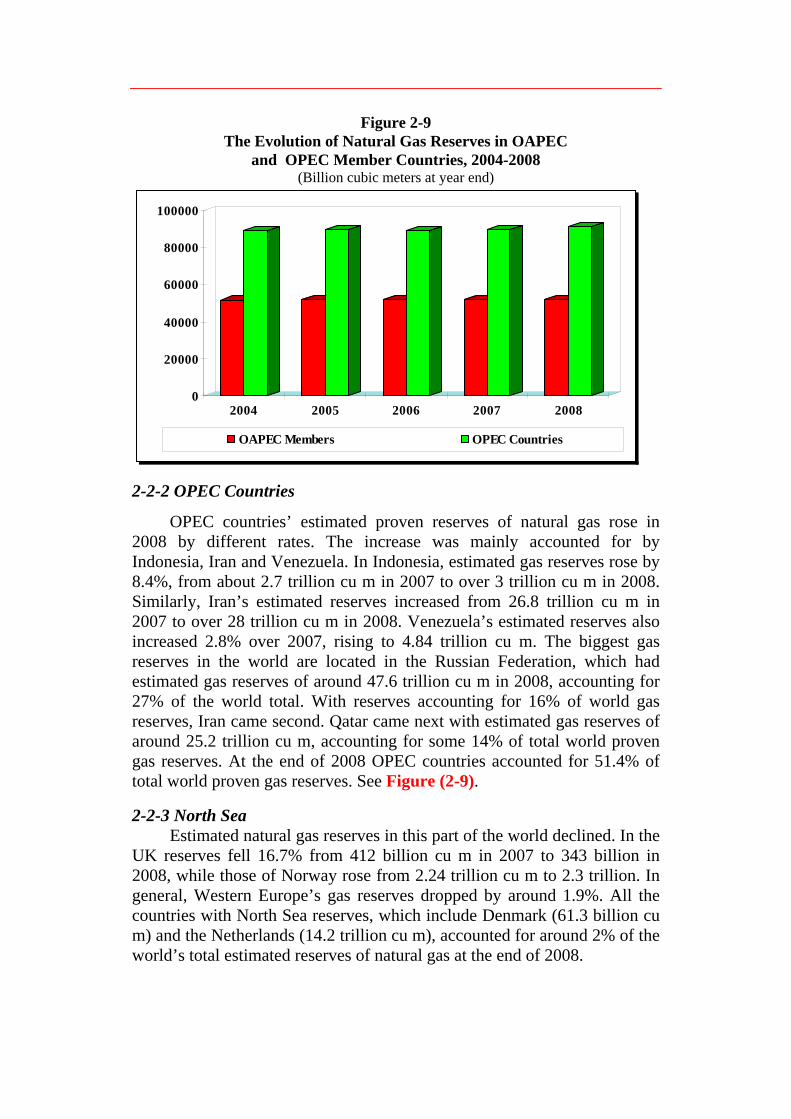

2-2-2 OPEC Countries…………………………………………..……………... 82

2-2-3 North Sea…………………………………….…………………………... 82

2-2-4 North America………….……………………………………………… 83

2-2-5 CIS and China............................................................................................ 83

2-2-6 Brazil......................................................................................................... 83

2-2-7 Rest of the World....................................................................................... 83

3. Hydrocarbon Liquids and Natural Gas Production…...……. …… ….. 83

3-1 Hydrocarbon Liquids Production…… .…… …...…………... …….……… 83

3-1-1 Oil Production…………..………………………………..……………….. 83

3-1-1-1 OAPEC Members and Other Arab Countries ………………………….. 84

3-1-1-2 OPEC Countries………………………………………………………… 86

3-1-1-3 North Sea………………………………………………………………... 86

3-1-1-4 North America………………………………...………………………… 86

3-1-1-5 CIS and China………………………………...………………………… 86

3-1-1-6 Brazil……………………………………………………………………. 87

3-1-1-7 Rest of the World ………………………………………….……………. 87

3-1-2 NGL Production in OAPEC Members and the World……………..… 87

3-2 Marketed Natural Gas ………………………………………….…………. 87 3-2-1 OAPEC Members and Other Arab Countries…………………………….. 87 3-2-2 OPEC Countries………………………………………...………………… 88 3-2-3 North Sea…………………………………………………...……………... 89 3-2-4 North America………………………………………………...…………... 89 3-2-5 CIS and China………………………………………….………...……….. 89

Contents

3-2-6 Rest of the World…………………………………………………...……... 90

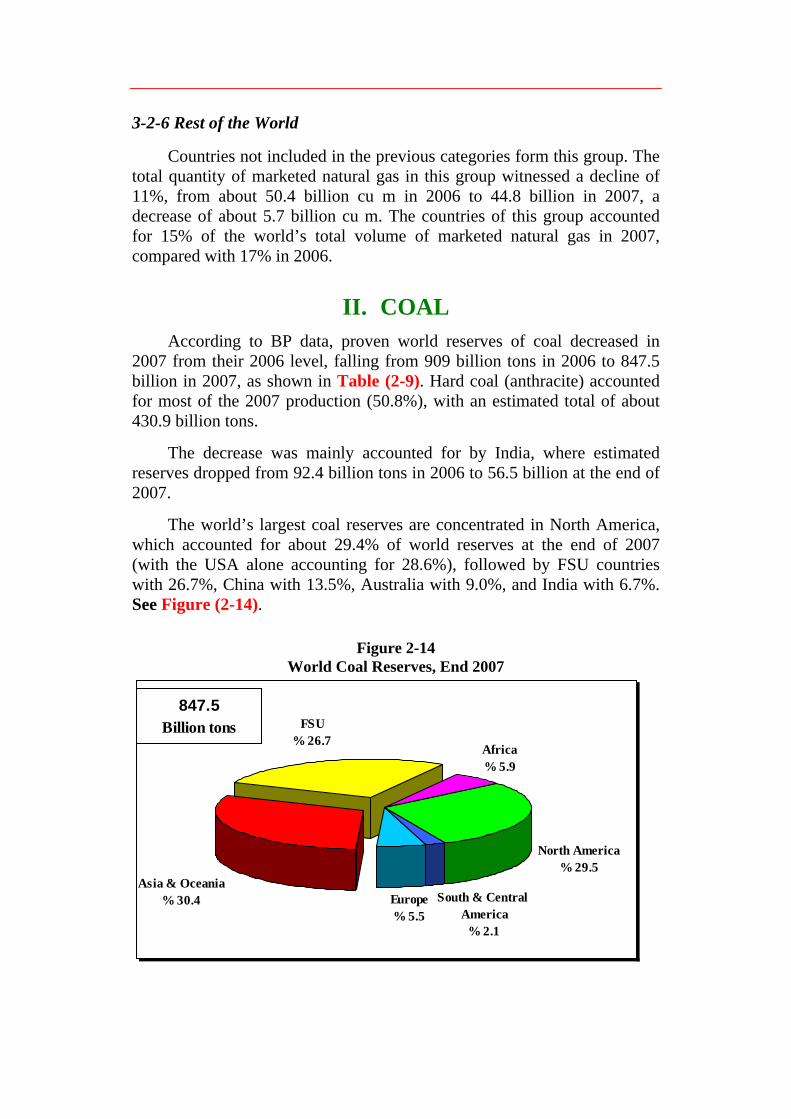

II. Coal ………..……… …….. ……………………………….…………….……… 90

III. Nuclear Energy………………………..…….. ………….….………….……… 92

IV. Renewable Energy Sources .........… . …..… ……….. ……….… .. …….……… 93

1. Hydropower... ….…..… ……...……. ……….……………… …. ………….. 95

1-1 Hydropower in the World……………….………………………………… 95

1-2 Hydropower in the Arab Countries……...…………………………..…… 96

2. Wind Power ..……... .……………………....…..................….…………… 96 2-1 Wind Power in the World………………..………………………………… 96 2-2 Wind Power in the Arab Countries……..…………...…………………. 97 3. Solar Power ..................................................... …….…………………..…. 99

3-1 Solar Power in the World………………………..……….……………... 99

3-2 Solar Power in the Arab Countries……………………..………………… 99

4. Geothermal Power.…………. ………….… .. ………….………… …..… 100

4-1 Geothermal Power in the World……………..……………………...…….. 100

4-2 Geothermal Power in the Arab Countries ……………………..……..…. 101

5. Solid Biomass Energy………………………………………………… 101

5.1 Solid Biomass Energy in the World …………………...……… 101

5.2 Solid Biomass Energy in the Arab Countries …………………….. 102

6. Ocean and Tidal Power………………………………………………. 102

CHAPTER THREE: ARAB AND WORLD DEVELOPMENTS IN PETROLEUM DOWNSTREAM INDUSTRIES

I. Refining Industry………………………………….. .….…………….……… .. 127

1. World Developments .………………… ……..………….. ……….……… .. 127 2. Developments in Arab Countries………… ……..……..………….……. 133

II. Petrochemical Industries ……..………… ……... ….… . …………….……… .. 138

1. World Developments .……… ...………….. ……………………….…… ..… 138

Contents

2. Arab Developments………….….……………………………….. .……… . 141 2-1 Egypt………………….………………..……………………………… 141 2-2 Kuwait……………………………………………………………….. 141 2-3 Qatar………...……………………………………………………… 142 2-4 Saudi Arabia………………………………………………………... 142 2-5 UAE…………………………………………………………………... 144 III. Natural Gas Consumption, Trade and Processing………….. …. .………. 145

1. World Developments .… ……..…….. …………………………….……… .. 145 1-1 Natural Gas Consumption……………..………….. …… ...……….……. 145

1-2 Natural Gas Trade………….………………………………….……..……. 147 2. Arab Developments…………………..…………... ……………….……… . 150 2-1 Algeria………………………………………………………………… 150 2-2 Bahrain……………………………………………………………… 151 2-3 Egypt……………………….……………………………………….. 151 2-4 Iraq………………………………………………………………….. 152 2-5 Kuwait……………………………………………...………………… 153 2-6 Libya……………………...……..………………………………….. 153 2-7 Oman………………..………………………………………………... 153 2-8 Qatar………………………………………...…………………...….. 154 2-9 Saudi Arabia……………………………………………….………... 155 2-10 Syria…………………………………………..…………………………… 155 2-11 Tunisia…………….…….………………..……………………………… 156 2-12 UAE…………………...….………………..……………………………… 156 2-13 Yemen…………...….……………………………………….………..…… 156 3. World’s Most Important Gas Activities………….………….………… 156

PART TWO OAPEC ACTIVITIES IN 2008

CHAPTER ONE: THE MINISTERIAL COUNCIL AND THE EXECUTIVE BUREAU

I. The Ministerial Council….. ….……………….………… ……... …….……… 181 II. The Executive Bureau ……...……………….……….…… ……..... ….……… 181

CHAPTER TWO: THE GENERAL SECRETARIAT I. The Data Bank and Related Activities ……. . ……...…… ……… …….…… 182

Contents

1. Data Bank …….…… ……………………… …..…… .. ..………….…… .… 182 1-1 Monitoring Development of the Data Bank………………………… 182

1-2 Reports and Papers……………………………...………………….. 182 1-3 Other Activities…………………………………………………... 183

2. Information and Library Services …….………… ……...…………….. 183

2-1 Bibliographical Services……………………………………………. 183

2-2 Indexing and Classification………………………………………… 184

2-3Acquisition…………………………...…………………………. 184

2-4 Current Awareness and Lending……………………………………….. 184 3. Studies, Papers, and Reports …….…………… …….... …….…… .…

3-1 Study on the “Features of Some Developments in the Ptroleum-Drilling Domain …………………………………………………

185

3-2 Study on “Options for Refining to Refine HeavyCrudes”…………..…………………………………………………

185

3-3 Paper Entitled “Natural Gas Supply and Demand Outlook to2017”……………….…………………………………………………

186

3-4 Paper Entitled “The Current and Future Role of Improved Productionof Petroleum in the Arab Countries…………………………...….…

186

3-5 Paper Entitled “Investments in OAPEC Member Countries RefiningIndustry” ……….……..…………………………………………..

187

3-6 Paper Entitled “ The Petrochemical Industry and its Status in the ArabCountries”………..………………………..……………………..

187

3-7 Paper Entitled “Transportation of Natural Gas and its Uses in theArab Countries…………………………………………..………….

188

3-8 Paper Entitled ‘Reducing the Environmental Impacts of Oil and GasExploration and Production Activities”…...…………………………….

188

3-9 Paper Entitled: The Petroleum Industry in Reducing ClimateChange………………………………………………………………..…….

189

3-10 Study Entitled “Fluctuations in Exchange Rates of US DollarAgainst Other Major Currencies and Their Imapct in MemberCountries’ Oil Revenues”…………………………………...…………...

190 3-11 Study Entitled ‘Development of Renewable Energy and their

Implications in World Oil Markets and member Countries………….

191 3-12 Study Entitled ‘Development of Oil and Gas Production in Sub-

Sahara” …………………………..………………...………………………

192

Contents

3-13 Study Entitled “Fluctuations in Oil Prices: Factors and Implicationson Member Countries’ Oil Revenues” ………………………………...

193

3-14 Study Entitled “Sources of Energy in the Global Energy Balance:Current Situation and Future Prospects” ………………………………..

194

3-15 Study Entitled “The Global Financial Crisis and its Initial PotentialImpact on the Petroleum Industry in the Arab Counties”……………

195

II. Arab and International Cooperation…………………………………….

1. Seminars and Meetings Organized by General Secretariat……….…. 196 1-1 Seminar on “Natural Gas Industry: Present and Future” ……………….. 196 1-2 15th Coordination Meeting of Environment Experts in OAPEC

Countries ……………………………….……….………………...………

197 1-3 8th Meeting of Working Group on Prospects for Cooperation in

Natural Gas Investment in OAPEC Member Countries ……………

198 1-4 Conference on “Developments in Techniques of Exploration and

Production”……………..……………………………………………

199 2. Conferences, Seminars and Meetings Attended by the General

Secretariat …….… ………………… …..……… ………. …….… . .…………

2-1 Joint Kuwaiti-Japanese Symposium on Fuel Cells Under the Rubric of “Research and Development and Applications of Fuel Cells and Hydrogen Production Technology……………………………….…

200 2-2 14th International Annual Fertilizer Forum and Exhibition…......…..… 201 2-3 10th Mediterranean Petroleum Conference and Exhibition

International Energy Foundation …………………...………….…..

202 2-4 GCC Policy Development Meeting on Clean Fuels and Vehicles…… 202 2-5 Fourth Coordination Meeting of Oil Training Institute Officials in

OAPEC Member Countries………….………………...……..…….

203 2-6 Syrian International Oil and Gas Exhibition SYROIL 2008 ……… 204 2-7 Middle East Gasoline and Diesel Conference 2008………………….. 205 2-8 First Arab Chemical and Petrochemical Industries Forum………… 205 2-9 13th Meeting of the Climate Change Subcommittee……………….. 206 2-10 Extraordinary Session of the Council of Arab Ministers

Responsible for Environment Affairs (CAMRE)…………………...

207 2-11 30th Oxford Seminar………………………...………………….…… 207 2-12 14th Meeting of the Climate Change Subcommittee…….……….… 208 2-13 OPEC’s Coordination Meeting in Preparation for “Cop-14, and

CMP-4” Meetings …………...…………………………….…..…

209 2-14 Forty Meeting of the Executive Office of the Council of Arab

Ministers Responsible for the Environment………………………

210

Contents

2-15 Meeting of the Conference of the Parties (COP-14) and theConference of the Parties Serving as the Meeting of the Parties tothe Kyoto Protocol (CMP-4)………………………………....……

210 2-16 1st Conference on Arab-Sino Cooperation in Energy………..……. 212 2-17 Meeting of WEC Cleaner Fossil Fuels Systems Committee………… 212 2-18 Meeting of 81st Session of Arab Economic and Social Council…… 213 2-19 Experts Meeting and Meeting of Executive Bureau of Council of

Arab Ministers Responsible for Electricity…………..….………….

214 2-20 International Energy Forum Meeting Atheist …………..………….. 214 2-21 orkshop on Energy Poverty in Africa…………..………………… 215 2-22 Meeting of Institutions Participating in the Joint Arab Economic

Report,2008…………………..…………………..…………………

216 2-23 39th Meeting if the Higher Coordination Committee on Joint Arab

Action…………..……………………………………………………

216 2-24 Meeting of Economic and Social Council …………..………….… 217 2-25 Experts Meeting and Meeting of Executive Bureau of Council of

Arab Ministers Responsible for Electricity…………..……………..

217 2-26 2nd IEA Meeting on International Energy Statistics……......……..… 218 2-27 Preliminary Meeting for Preparing the Joint Arab Economic Report,

2009……………………………………….....……………………

219

III. Energy Resources Monitor-Arab and International……………..…… 219

IV. The Promotion of Scientific Research ….…..…………..…… …….....…… 219

VI. Supporting Activities………………………………………………………..... 221

1. Media Activities .…….……… …….…. ……….……………….………… 221

1-1 Editing, Printing, Publishing, and Distribution .…..… ….....….……

1-2 Press and Media…………………. .…… ….. …….……………………

1-3 33rd Arab Book Fair……………….. ….………… ….…..… ..………

221

221

221

2. Administrative and Financial Activities………………... ..…..……… 222 2-1 Evolution of the Administrative Structure…………….…….. ….…

2-2 Evolution of Actual Expenditure …..….…… ……….. …….…….…

222

222

CHAPTER THREE: OAPEC-SPONSORED VENTURES I. The Arab Maritime Petroleum Transport Company (AMPTC)

230

II. The Arab Shipbuilding and Repair Yard Company (ASRY)…............. 232

Contents

III. The Arab Petroleum Investments Corporation (APICORP) .............…. 235

IV. The Arab Petroleum Services Company (APSCO) ...…......... ………… 240

1. Arab Drilling and Workover Company (ADWOC) …........... . …..… 242

2. Arab Well Logging Company (AWLCO)…………………………. 243

3. Arab Geophysical Exploration Services Company (AGESCO) … 245

4. Arab Company for Detergent Chemicals (ARADAT) ………… 246

APPENDICES

I. Press Releases of OAPEC Ministerial Council Meetings in 2008……. 248

1- The 80th Meeting of OAPEC’s Council of Ministers………………... 248

2- The Eighty-First Meeting of OAPEC’s Council of Ministers…… 248

II. Meetings and Seminars Sponsored or Attended by the GeneralSecretariat,2008…………………………………………………………..

250

Contents

TABLES

PART ONE

CHAPTER ONE

1-1 Total & Annual changes in World Oil and NGLs Supply,2004 - 2008............................................................................................... 41

1-2 Growth in the World Economy and Oil Demand by Region, 2004-2008...................................................................................................

42

1-3 World Economic Growth, 2004-2008…………………………………... 43 1-4

Total & Annual Change in World Oil Demand, 2004-2008…....... 44

1-5 World Oil Demand by Region, 2004-2008…………………….. 45 1-6 Total & Annual Change in Oil Demand in OECD Countries,

2004-2008………..……………………………………..……………

46 1-7 Total & Annual Change in Oil Demand in Developing

Countries, 2004-2008……………………………………………..

47 1-8 Total & Annual Change in Oil Demand in Oil Demand in

Countries in Transition, 2004-2008………...…………………….

48 1-9 Spot Price of OPEC Basket of Crudes, 2004-2008………..….…… 49 1-10 Average Spot Prices of the OPEC Basket and Selected Arab

Crudes, 2004-2008…………………………………………………

50 1-11 Nominal and Real Prices of Crude Oil, 1995-2008…………… 51 1-12 Average Monthly Market Spot Prices of Petroleum Products,

2007-2008…………………………………………………………..

52 1-13 Share of Tax in Gasoline Prices in some Industrial

Countries,2007- 2008…………………………………………....

53 1-14 Spot Tanker Freight Rates, 2007-2008…………………………... 54 1-15 OECD Oil Inventories at Quarter End, 2007 & 2008.................... 55 1-16 Value of Oil Exports in OAPEC Member Countries, 2004-2008.. 56 1-17 Value of OAPEC Oil Exports in Current and Real Prices, 1995-

2008………………………………………………..…...…

57 1-18 Energy Consumption in the Arab Countries, 2004-2008………. 58 1-19 Per Capita Energy Consumption in the Arab Countries, 2004 and

2008…………………………………………………….

59

1-21 Energy Consumption in OAPEC Member Countries, 2004-2008. 60 1-22 Energy Consumption in OAPEC Member Countries by Source,

Contents

2004-2008……………………………...………………………… 61 1-22 Petroleum Products' Consumption in OAPEC Member

Countries, 2004-2008 ……………………………………….. 62 1-23 Natural Gas Consumption in OAPEC Member Countries, 2004-

2008…………………………………………………………. 63 1-24 Hydroelectricity Consumption in OAPEC Member Countries,

2004-2008……………………………………………………... 64 1-25 Coal Consumption in OAPEC Member Countries, 2004-2008….. 65 1-26 Relative Distribution of Final Energy Consumption According to

Sources and Sectors in OAPEC Member and Other Arab Countries in 2006…………………………………………… 66

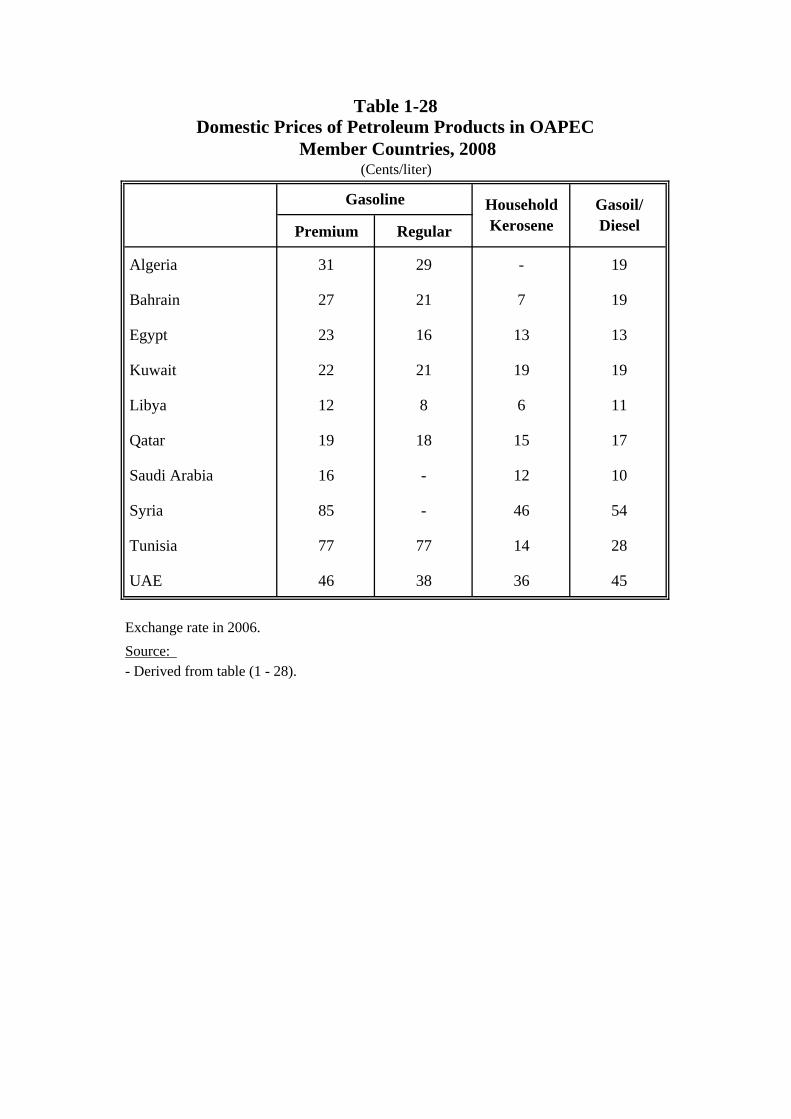

1-27 Domestic Prices of Petroleum Products in OAPEC Member Countries, 2008………………………………………...……… 67

1-28 Domestic Prices of Petroleum Products in OAPEC Member Countries, 2008………………………………………………... 68

CHAPTER TWO

2-1 Seismic Surveys Worldwide, 2004-2008........................................... 105

2-2 Average Number of Active Rigs Worldwide, 2004-2008…………. 106

2-3 Petroleum Discoveries in OAPEC Members and Other Arab Countries, 2004- 2008....................................................................

107

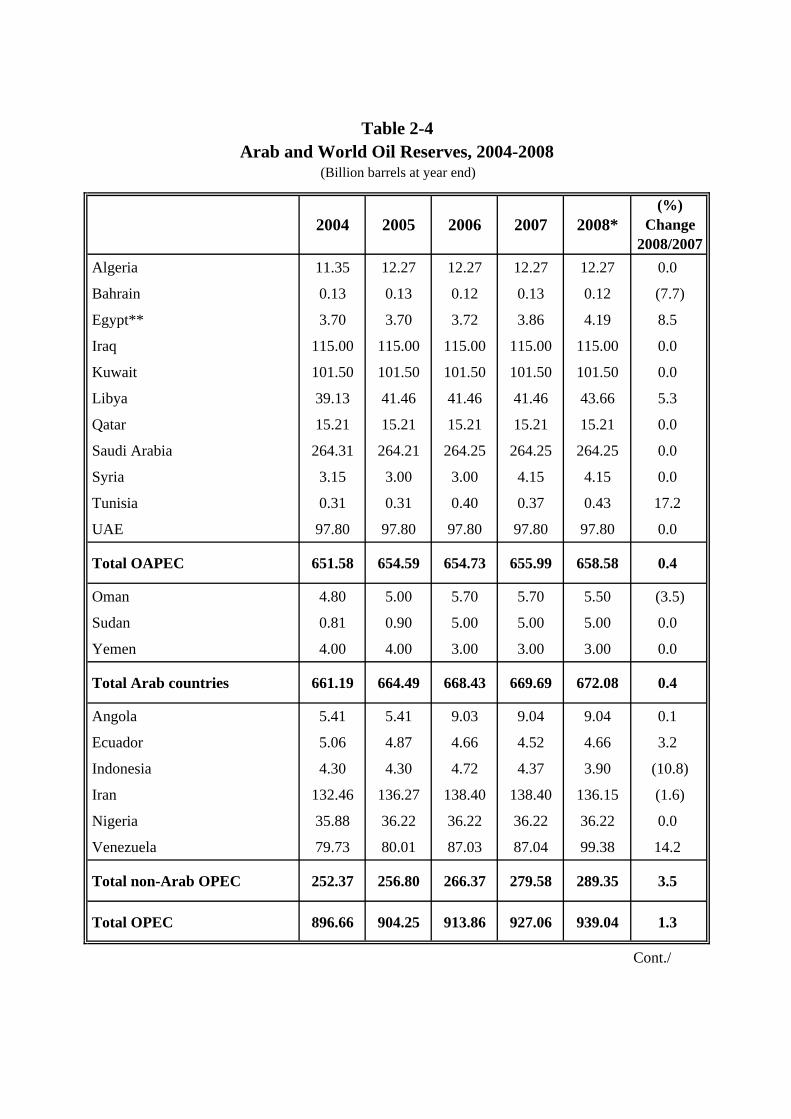

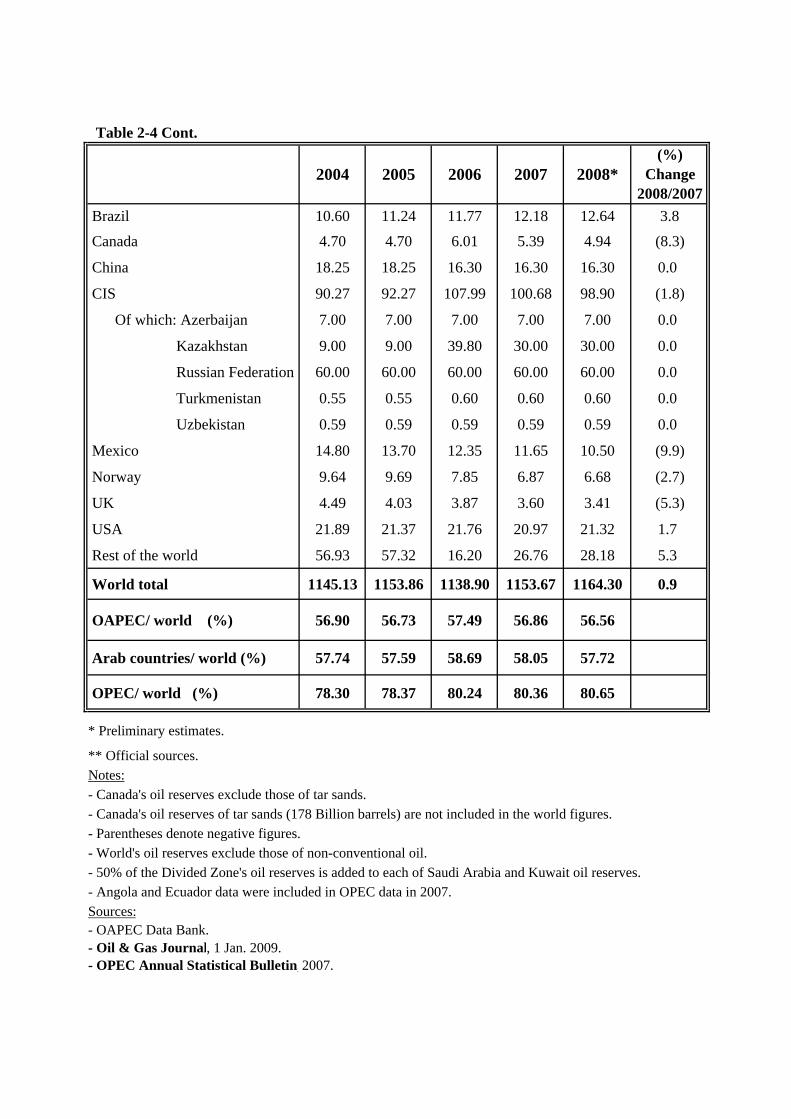

2-4 Arab and World Oil Reserves, 2004-2008………………….…….. 108

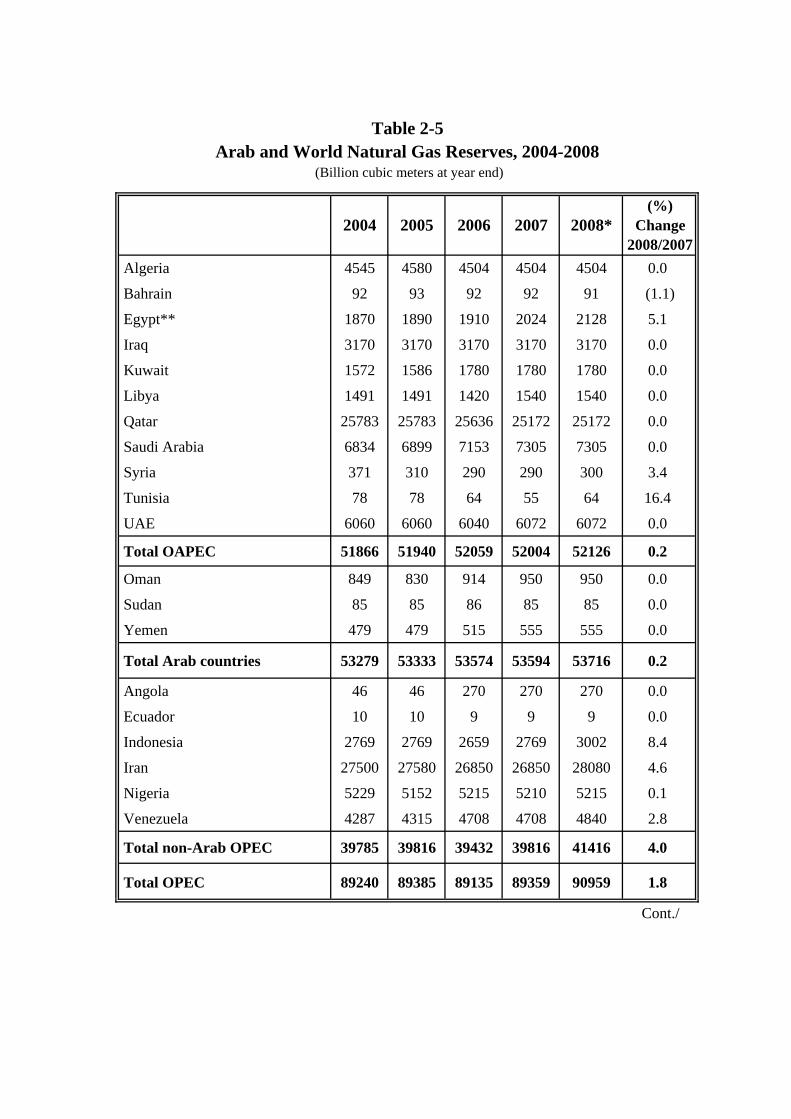

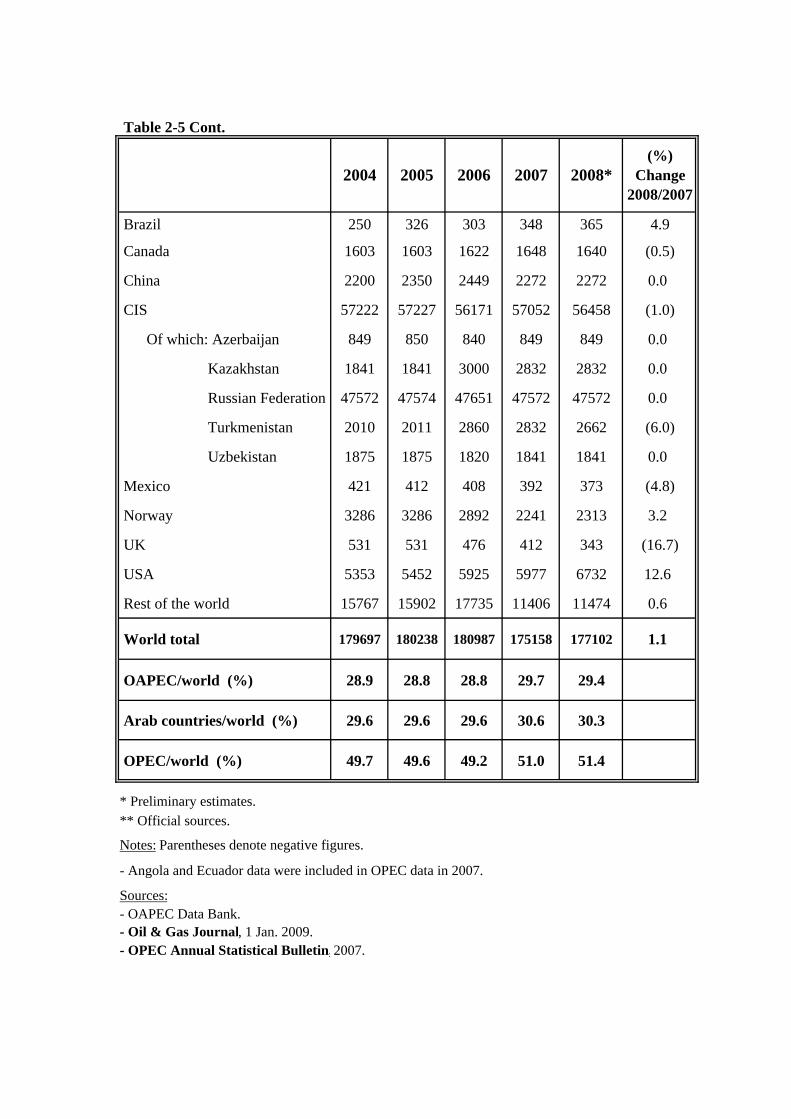

2-5 Arab and World Natural Gas Reserves, 2004-2008………………. 110

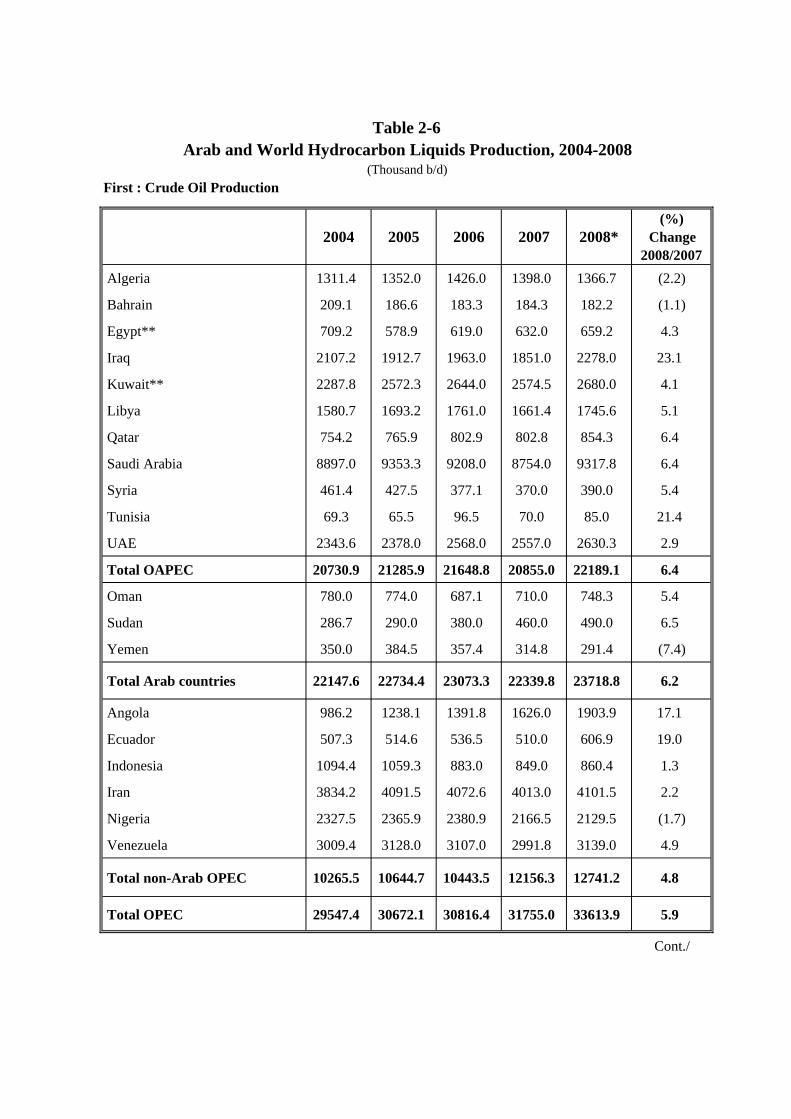

2-6 Arab and World Hydrocarbon Liquids Production, 2004-2008… 112 2-7 NGL Production in OAPEC Members and Other Arab Countries,

2004-2007…………………………………………………. 114 2-8 Arab and World Marketed Natural Gas, 2004-2007…………. 115 2-9 World Coal Reserves, 2004-2007…………………………. 1172-10 World Coal Production, 2004-2007………………….………. 1182-11 Nuclear Power Reactors in Operation and Under Construction

Worldwide ………………………………………………………... 1192-12 Installed Hydro Power Capacities in Some Countries, 2005 and

2006…………………………………………………………………. 1212-13 Installed Wind Power Capacities in Some Countries 2006,2007…. 1222-14 Cumulative Installed Photovoltaic Power Capacities in Some

Countries, 2006 and 2007………………………………………….

1232-15 Installed Geothermal Capacities in Some Countries, 2006 and

Contents

2007…………………………………………………………………….. 1242-16 Solid Biomass Installed Capacities in Some Countries, 2005 and

2006…………………………………………………………………….

125

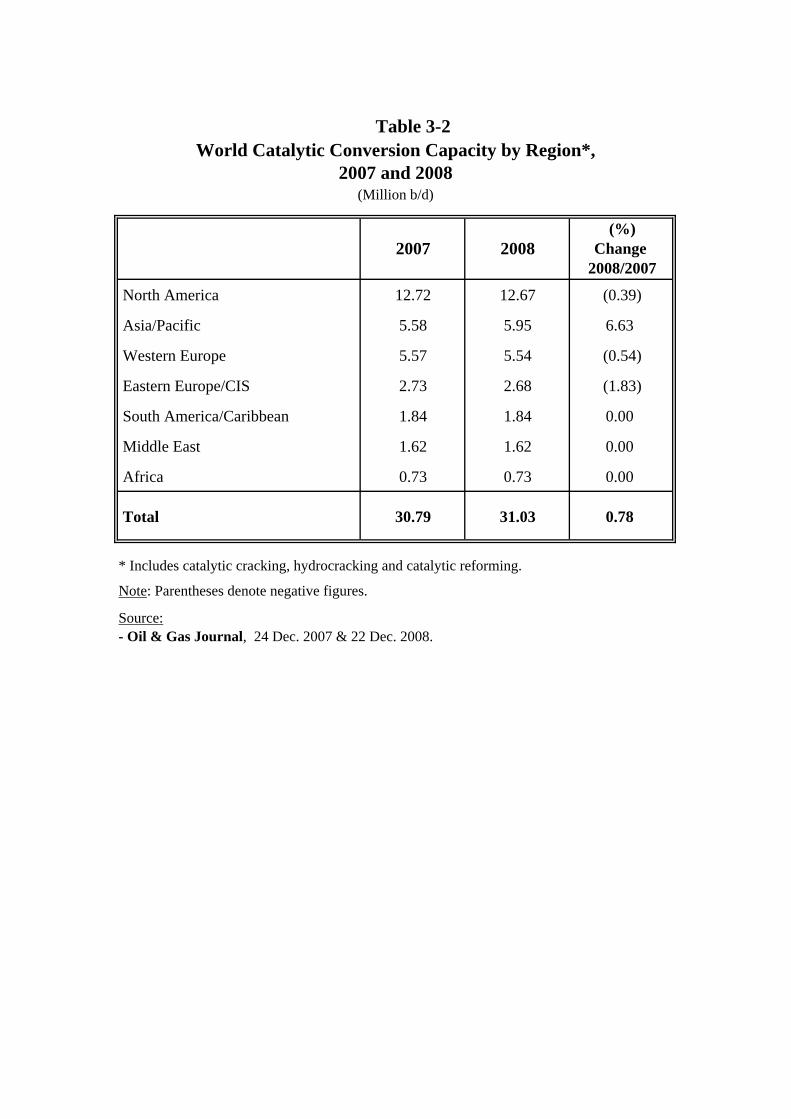

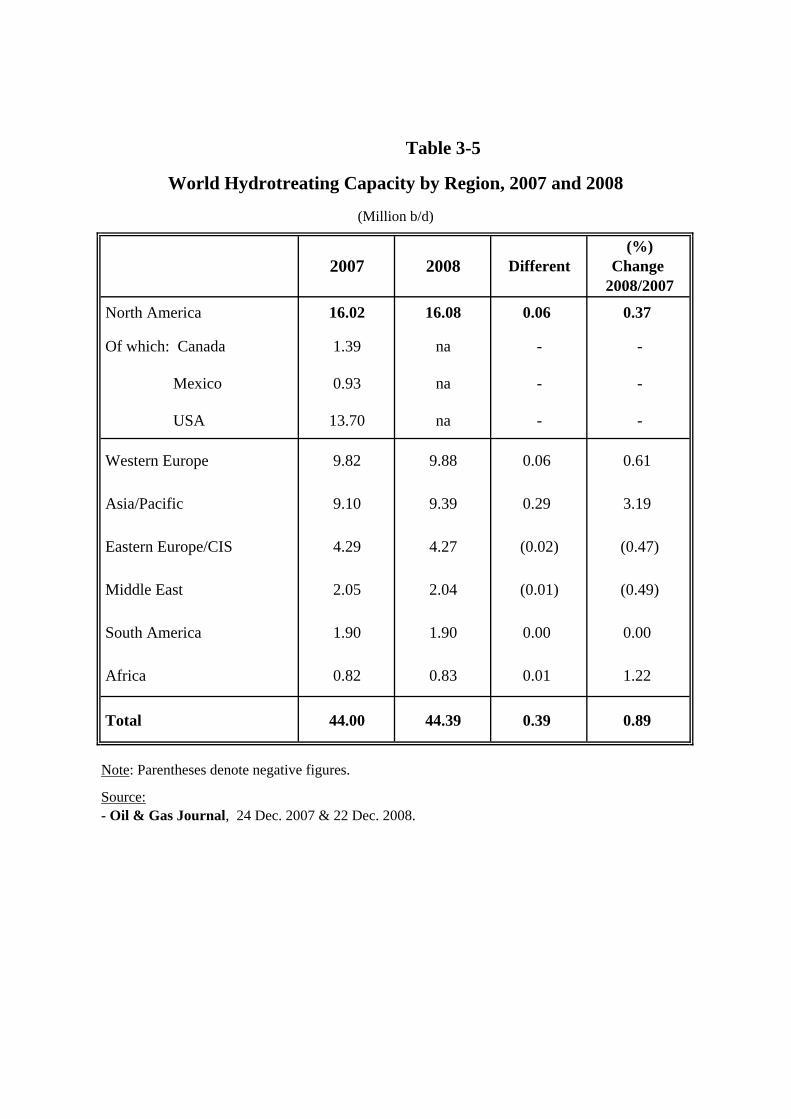

CHAPTER THREE 3-1 World Existing Topping Distillation Capacity by Region, 2007-

2008 ………………………………………………………………….....

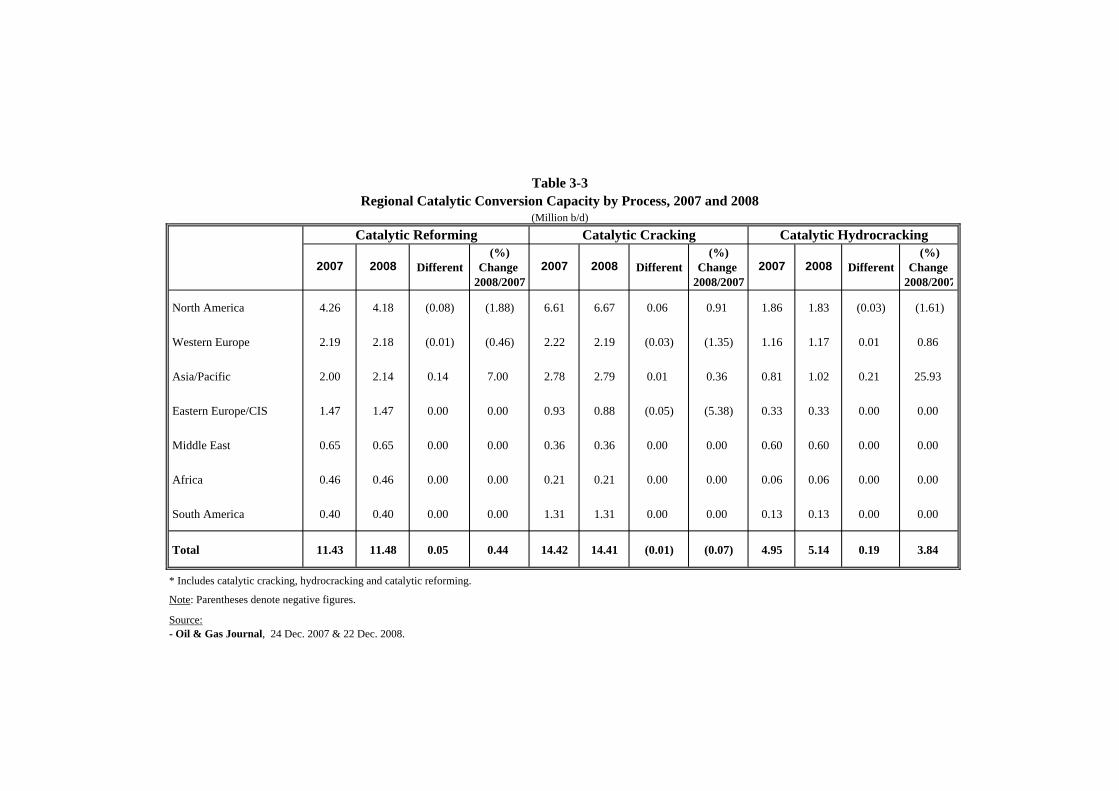

163 3-2 World Catalytic Conversion Capacity by Region, 2007-2008…… 164 3-3 Regional Catalytic Conversion Capacity by Process, 2007-2008.... 165 3-4 World Coke Production Capacity from Thermal Conversion

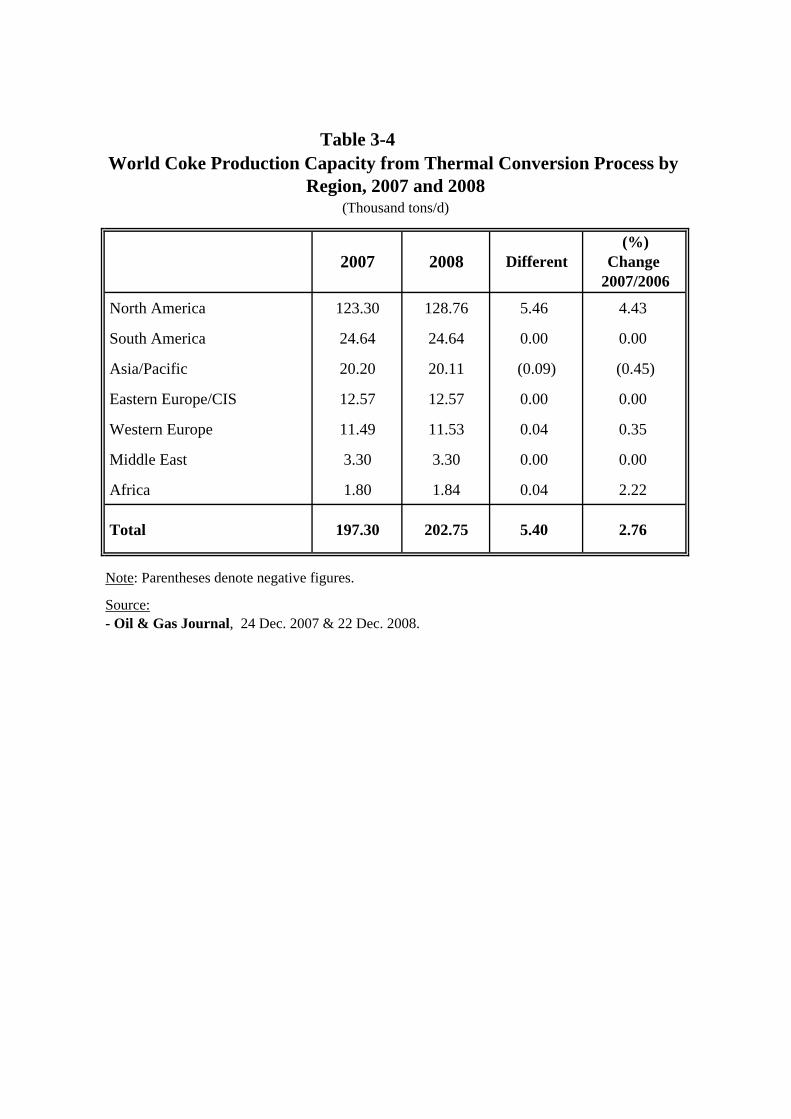

Process by Region, 2007-2008……………………………..….......

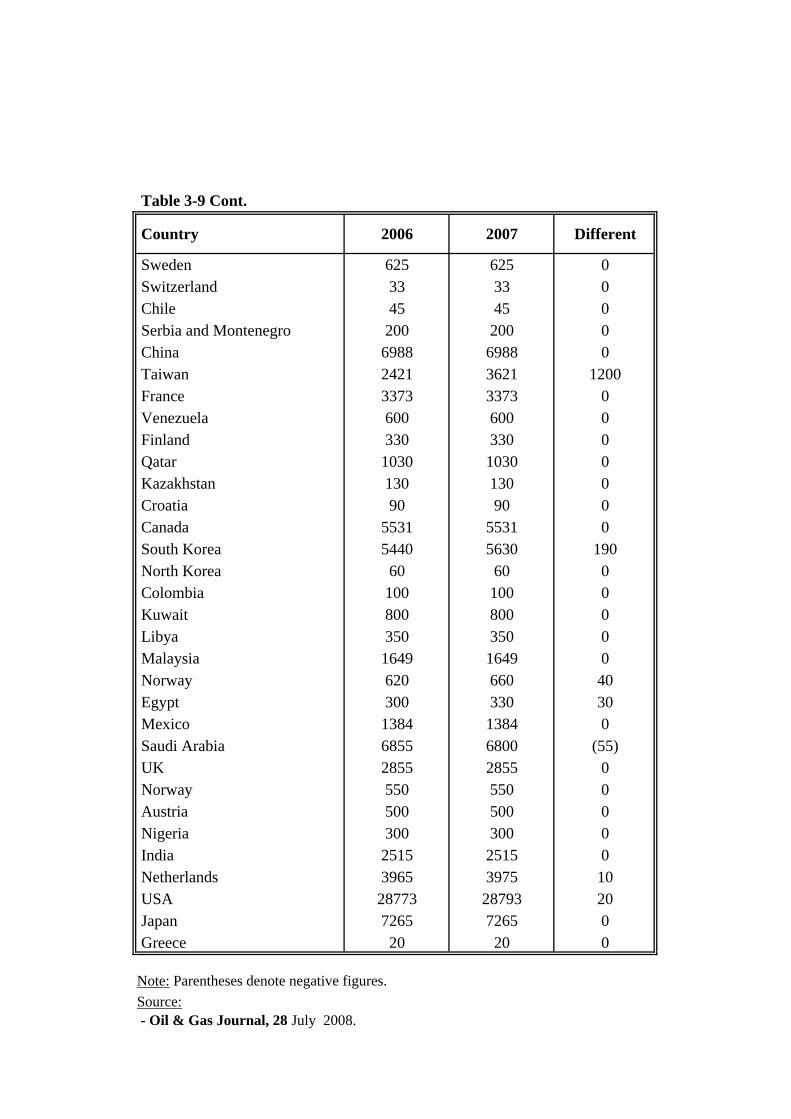

1663-5 World Hydrotreating Capacity by Region, 2007 and 2008…….…. 1673-6 Installed Refining Capacity in the Arab Countries, 2004-2008…... 1683-7 Top 10 Ethylene Complex ……….............................................……... 1693-8 World Ethylene Capacity by Region, 2006 and 2007….....……….. 1703-9 World Ethylene Production Capacity by Country,…………….. 1713-10 Top 10 Ethylene Producers……...................................……….… 1733-11 Consumption of Natural Gas by Region, 2006 and 2007 ……...… 1743-12 Share of Natural Gas in the Total Consumption of Commercial

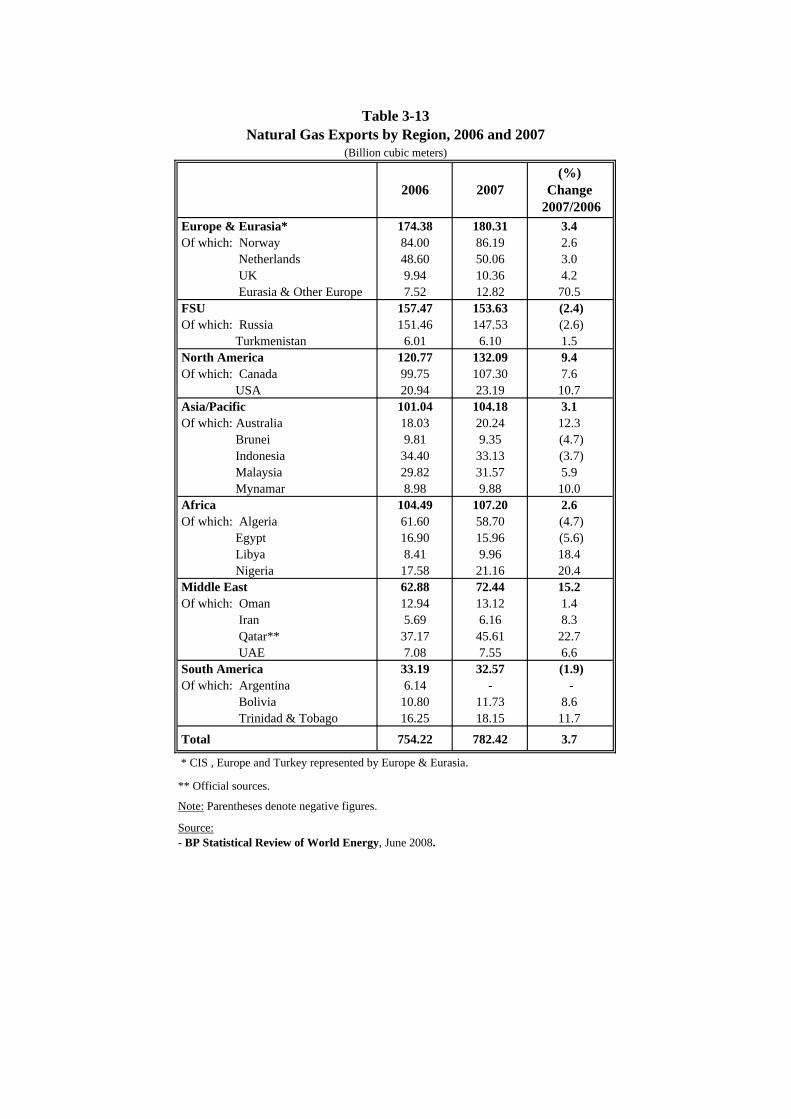

Energy by Region, 2004-2007………..............................………..

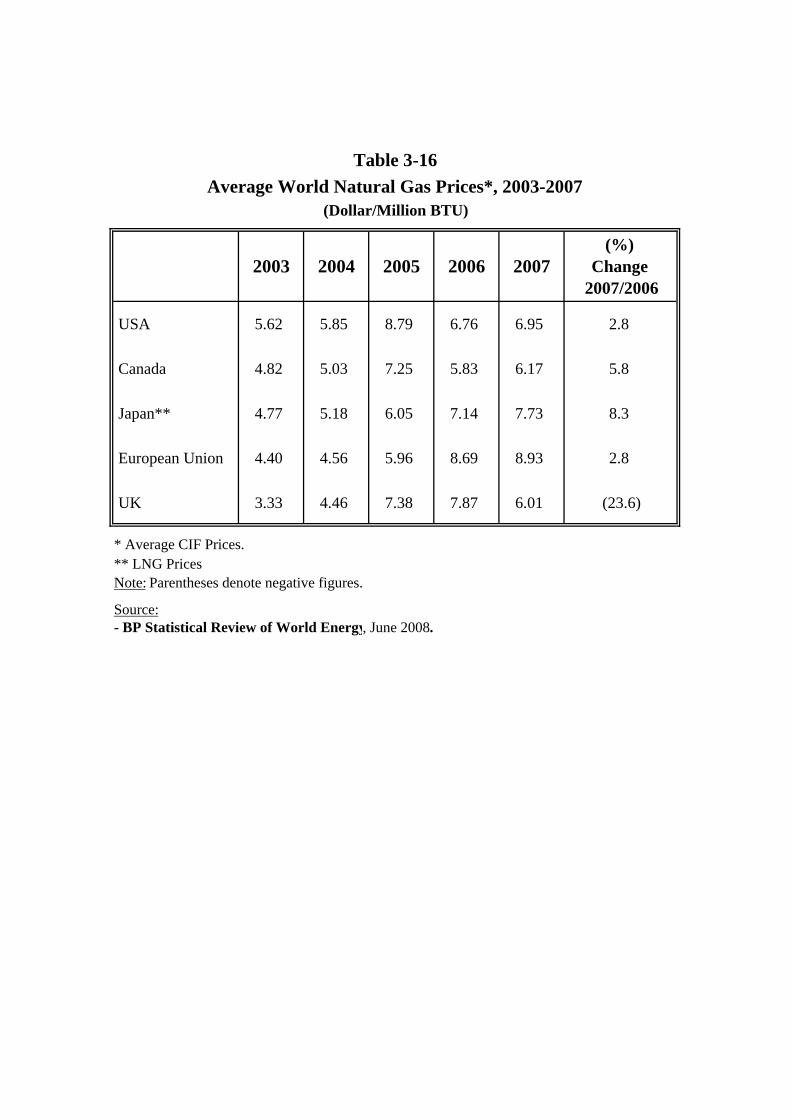

1753-13 Natural Gas Exports by Region ,2006 and 2007…………......…… 1763-14 World Natural Gas Exports by Region, 2006 and 2007....….......… 1773-15 Arab Natural Gas Exports, 2003 and 2007.......................................... 1783-16 Average World Natural Gas Prices 2003-2007.................................. 179

PART TWO CHAPTER ONE

5-1 Publications Issued and Distributed by the General Secretariat in2008..................................................................................

225

5-2 General Secretariat Employees, 1968-2008............................... 2265-3 General Secretariat Actual Expenditure by Budget Category,

1968-2008..........................................................................

227

FIGURES PART ONE

CHAPTER ONE 1-1 World Supplies of Oil and NGLs, 2004-2008…………...….. 5

Contents

1-2 OPEC Memebers’ Production Quotas Cut Decisions to Avoid Future Price Slide During 2008……………………………………..

6

1-3 Annual Change in World Supplies of Crude Oil and NGL’s,2004-2008……………………………………………………...

7

1-4 World Economic Growth and Demand Growth 2004-2008…….. 8

1-5 World Economic Growth 2007-2008…………………………………. 9

1-6 World Oil Demand, 2004-2008………………………………………. 10 1-7 Distribution of World Oil Demand by Region, 2004-2008……… 10 1-8 OECD Demand for Oil by Region, 2004-2008……………. 11

1-9 Weekly Movement of OPEC Basket of Crudes, 2008………….. 14

1-10 Premium Gasoline Prices, 2007-2008………………………... 15

1-11 Gasoline Prices in some OECD Countries, November 2008………… 16

1-12 US SPR at Quarter End, 2007-2008………………………….. 19 1-13 Monthly Oil Prices and Value of OAPEC Oil Exports January-

December, 2008……………………………………………….

20 1-14 Arab Countries GDP in Current Prices 2003-2007……………………. 21 1-15 Per Capita GDP of Arab Countries in Current Prices, 2003-2007 22 1-16 Energy Consumption in the Arab Countries by Source, 2008………… 24

1-17 Per Capita Energy Consumption in the Arab Countries, 2008….. 25 1-18 Energy Consumption in Arab Countries and the World, 2007… 25 1-19 Breakdown of Petroleum Product Consumption in the Arab

Countries, 2008…………………………………….…………….

26 1-20 Oil Consumption in the Arab Countries and the World, 2007………… 27

1-21 Natural Gas Consumption in the Arab Countries and theWorld,2007…………………………………………………….

28

1-22 Energy Consumption in OAPEC Member Countries, 2004-2008…... 29 1-23 Per Capita Energy Consumption in OAPEC Member

Countries,2008…………………………………………………..

30 1-24 Energy Consumption in OAPEC Member Countries by Source,

2008…………………………………………………………….

31 1-25 Natural Gas Consumption in OAPEC Member Countries and the

World, 2004-2008………………………………………………..

32 1-26 Natural Gas Consumption as a percentage of Total Energy

Consumption in OAPEC Member Countries,2008………………

33 1-27 Relative Distribution of Final Energy Consumption by Source

and Sector in the Arab Countries,2006……………………...

35

Contents

1-28 Relative Distribution of Final Energy Consumption by Sectorand Source in the Arab Countries,2006……………………….

36

CHAPTER TWO

2-1 Seismic Surveying Activity in Different Parts of the World, in 2004-2008…………………………………………………..…………

75

2-2 Active Drilling Rigs Worldwide,2004-2008……….………..…… 76 2-3 Distribution of Active Drilling Rigs Worldwide, 2008………..… 76 2-4 Oil Discoveries in OAPEC Member Countries and Other Arab

Countries, 2004-2008………………………………………..…….…

77 2-5 Gas Discoveries in OAPEC Member Countries and Other Arab

Countries, 2004-2008…………………………………………..…….

77 2-6 World Oil Reserves by International Grouping, End 2008…….… 78 2-7 The Evolution of Oil Reserves in OAPEC and OPEC Member

Countries, 2004-2008…………………………………..…………….

79 2-8 World Natural Gas Reserves, End 2008 ………………………..…. 81 2-9 The Evolution of Natural Gas Reserves in OAPEC and OPEC

Member Countries, 2004-2008……………………………..…….

82 2-10 World Oil Production by International Grouping, 2008............... 84 2-11 Oil Production Rates in OAPEC and OPEC Member Countries,

2004-2008……………………………………………..……….

85 2-12 Marketed Natural Gas by International Grouping, 2007…....…... 88 2-13 Marketed Natural Gas in OAPEC and OPEC Member Countries,

2004-2007..............................................................................................

88 2-14 World Coal Reserves, End 2007………………………...….…. 90 2-15 World Production of Hard Coal, 2007……………...………. 91

CHAPTER THREE

3-1 World Primary Distillation Capacity by Region, End 2008……….. 128

3-2 World Catalytic Conversion Capacity by Region, End 2007.. 128

3-3 World Catalytic Reforming Capacity by Region, End 2007-2008.. 129

3-4 World Catalytic Cracking Capacity by Region, End 2007-2008…. 130

3-5 World Hydrocracking Capacity by Region, End 2007-2008……. 1313-6 World Capacity for producing Coke from Thermal Conversion

Processes by Region, End 2008………………………………....

1323-7 Distribution of Hydrotreating capacity by Region, End 2008…..… 133

Contents

3-8 Evolution of Primary Distillation Capacity in the Arab Countries,2004-2008………...…………………………………………….…....

133

3-9 World Existing Ethylene Production Capacity by Region, End 2007…………….………………………………………………………

138

3-10 Ethylene Operating Rate Worldwide………………………….……… 139 3-11 Distribution of Total Existing Ethylene Capacities, end of 2007… 140 3-12 Natural Gas Exports Worldwide,2007……………………….. 1463-13 Share of Natural Gas in the Total Consumption of Commercial

Energy, 2004-2007……………………………………………

1473-14 Natural Gas Export Worldwide,2007…………………………….. 148 3-15 Natural Gas Export Worldwide, 2006-2007……………………. 149 3-16 Arab Natural Gas Export, 2007…………………………………… 149 3-17 World Prices of Natural Gas, 2003-2007…………………………. 150

PREFACE

This Report is being published at a time when the world is passing through a severe economic crisis that has resulted in a deep recession not witnessed since 1929 and 1933. The repercussions of the financial crisis first took the US financial and banking system by storm at the end of the summer, 2008. Then it moved on to attack other countries, upsetting sectors and industries of the global economy without exception. World petroleum markets (oil and natural gas) were some of the sectors worst affected by the crisis, which shook the world economy to its roots. A sharp drop in oil prices affected the socioeconomic situation in the Arab world, where petroleum constitutes the main source of wealth and the cornerstone of several Arab economies.

World oil prices were severely hit by the global economic crisis, especially in the fourth quarter of 2008. In the second and third quarters they had hit record levels of $147 per barrels (for the West Texas benchmark crude) and over $130/b for the OPEC basket (July 2008), giving an annual average price of $94.1/b, which was the highest annual average since the basket was introduced in 1987. The financial crisis brought these prices crashing down to $38/b in December 2008. World oil supplies, on the other hand, reached an annual average of 86 million b/d, which was unprecedented.

The 35th Secretary General’s Annual Report highlights the efforts of OPEC and OAPEC member countries to mitigate the impact of price fluctuations and restore balance to the petroleum market. They include efforts to activate dialogue and consultation between OPEC and various bodies and organizations representing oil importing countries for the mutual benefit of the two sides. The efforts culminated in the Jeddah Energy Meeting between producers and consumers on 22 June 2008.

On the other hand, the Report reviews the efforts exerted by OAPEC member countries to develop all phases of their oil industries and to implement many projects aimed at promoting sustainable socioeconomic development and using their petroleum export revenues to upgrade their infrastructure and enhance their health and education provision.

The Report provides a detailed analysis of data and statistics about various aspects of the oil and energy industry. Part One reviews international developments in oil and energy, including the fluctuations on global markets and their impact on OAPEC member countries. It also examines the factors affecting the market, whether they be the market

forces of supply, demand, and oil stocks, or those affecting market trends, such as geopolitical issues and energy policies adopted by various political and economic blocs. Moreover, it considers factors with an indirect impact on petroleum, such as the trend adopted by investment and hedge funds of looking for ‘new investment receptacles,’ which boosted activity on futures’ markets and resulted in paper barrels far exceeding actual demand for oil. In the same vein, the Report discusses price trends in 2008 and their impact on OAPEC members’ oil revenues, which fuel their socioeconomic development. It provides an initial indication of the evolution of oil and energy consumption in Arab countries in general, and OAPEC member countries in particular, according to the basic energy sources available (oil, natural gas, coal, and hydroelectricity). Furthermore, it highlights the final consumption of energy by economic sector and summarizes the latest oil price developments in Arab countries.

Part One also considers Arab and international developments in the energy sector, starting with the exploration and production of various energy sources, with a particular focus on oil and gas, and moving on to Arab and international developments in the downstream oil industry (refining and petrochemicals) and the natural gas industry.

Part Two of the Report relates to OAPEC's activities in 2008, ranging from the meetings of the Ministerial Council and Executive Bureau to the studies and reports compiled by the General Secretariat and the seminars and meetings convened by it. As usual, it contains a special section on the achievements of OAPEC-sponsored ventures in the past year, as they sought to benefit from the encouraging climate of high oil and gas prices in the first months of the year and the concomitant rise in demand for petroleum support services. The relative abundance of liquidity helped them to boost their capability and efficiency in their various fields of activity. It also reviews the measures they have taken to deal with the impact of the global financial crisis on their activities.

In conclusion, we hope that this Report illustrates clearly the features, activities and goals of the Organization of Arab Petroleum Exporting Countries and that the reader will find the information he or she seeks.

Secretary General Abbas Ali Naqi

3

PART ONE

INTERNATIONAL DEVELOPMENTS IN OIL AND ENERGY

CHAPTER ONE

DEVELOPMENTS IN GLOBAL MARKETS AND

THEIR IMPACT ON OAPEC MEMBER COUNTRIES

FOREWORD

The year 2008 witnessed the worst financial crisis the world had seen since the 1930s. The crisis, which had begun in August 2007 when the high-risk subPrime mortgage market collapsed in the US, escalated the following year, as the situation in global financial markets had a negative impact on the real economy. Many economies experienced a decline in growth rates in 2008, following several years of strong growth. Many advanced economies even went into or on the brink of recession.

US and European monetary authorities sought to take emergency measures to restore market stability, including the injection of vast amounts of liquidity, swift intervention to save vulnerable financial institutions, providing guarantees for deposits, and enacting legislation in the US for the use of public funds to buy bad debts from the banks. Nevertheless, the measures continue to be surrounded by considerable uncertainty and have not yet proved successful.

The oil market was not immune from developments in the global economy. They had a clear impact on world demand for oil, which began to drop, and on oil prices, which took an unprecedented downward turn.

OPEC countries resorted to new measures they had never used before. On three separate occasions they cut production quotas, the first being in September and the last being in December, making a total cut of 4.2 million b/d in output in 2008, which was the largest cut ever. These measures were taken as part of urgent efforts to stabilize the oil market and stem the slide in crude oil prices, restoring them to levels acceptable to all parties.

Although OPEC countries closely monitored events in the oil market throughout the year, oil prices continued to fluctuate and fell to their lowest level of less than $40 per barrel in December. The slide was reflected in the oil inventory levels of industrial countries, which jumped to their highest level in five years. Moreover, it affected the value of OAPEC members’ oil exports, which are closely linked to price movements and are the mainstay of socioeconomic development.

Chapter One of the Report examines major developments in the oil market, the factors behind them, and their impact on the value of oil exports. It also reviews oil and energy consumption developments in the Arab countries, and OAPEC members in particular.

I. MAJOR DEVELOPMENTS IN THE WORLD OIL MARKET IN 2008 AND RELATED FACTORS

In order to examine the key developments in the oil market in 2008, the following section reviews various aspects of the market, in particular, world oil supplies, world oil demand, price trends for crude oil and major oil products, crude oil freight rates, and changes in international oil inventories, and impact on OAPEC members revenue from oil exports.

1. Supplies

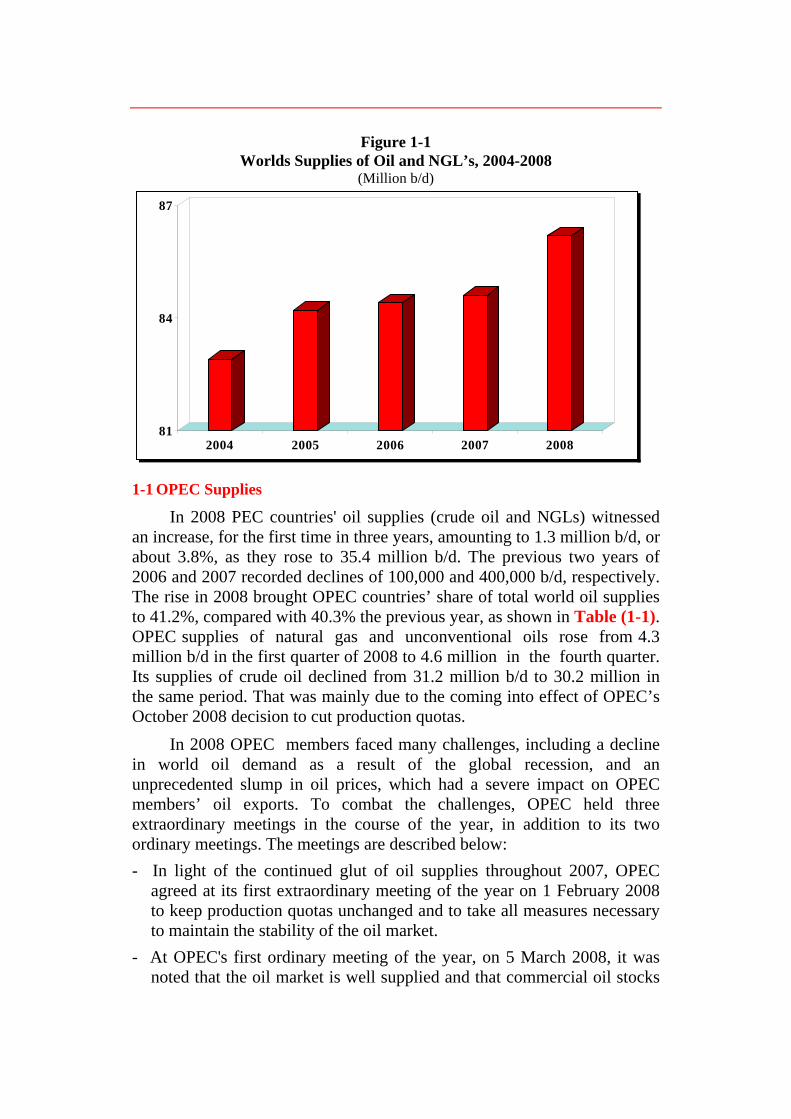

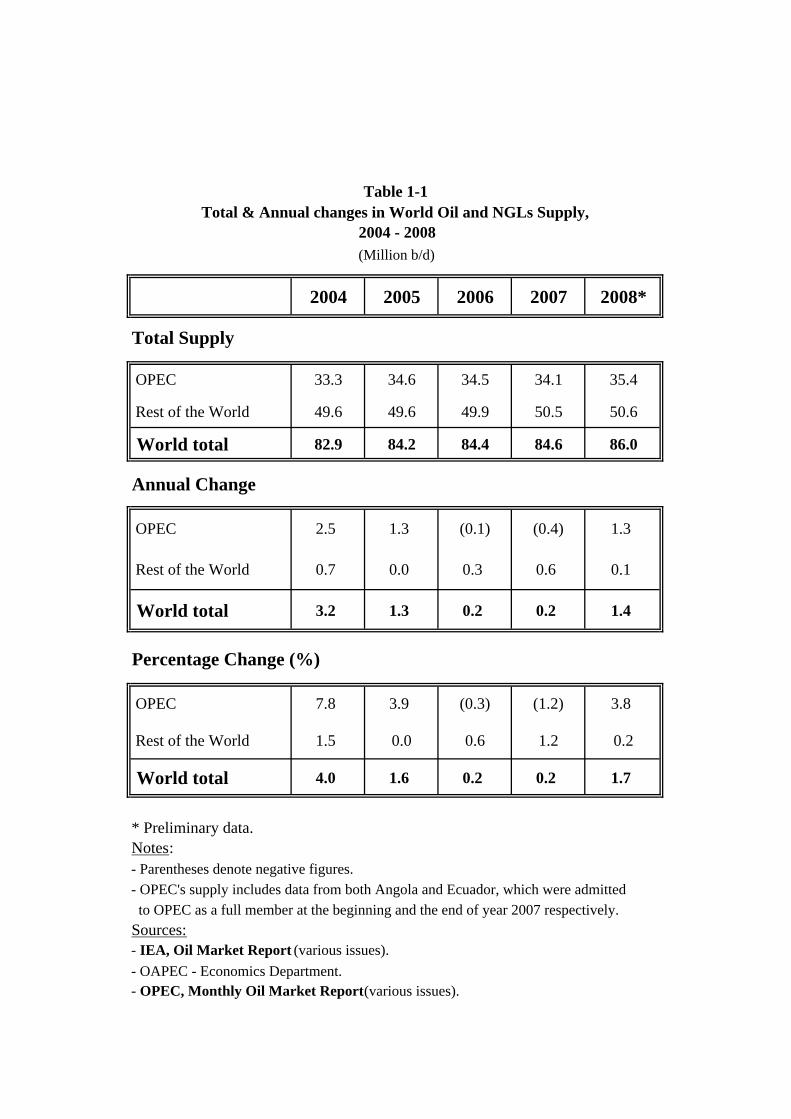

Average oil supplies (crude oil and natural gas liquids) in 2008 rose by 1.4 million b/d, or 1.7%, compared with 2007, rising to 86.0 million b/d, which was the highest annual rate of oil production ever recorded, as shown in Table (1-1) and Figure (1-1).

At the beginning of the first quarter of 2008 world supplies rose about 700,000 b/d above the last quarter of 2007, rising to 86.3 million b/d. Then they rose again in the second quarter by 300,000 b/d to 86.6 million b/d, but in the third and fourth quarters they changed course, falling by about 800,000 b/d and 300,000 b/d, respectively, to 85.5 million b/d at the end of the year.

The global financial crisis clearly affected the oil market, since the increase in world oil supplies witnessed in the first half of 2008, amounting to 1 million b/d more than the last quarter of 2007, was wiped out in the second half of the year, when supplies dropped by 1.1 million b/d from their first half level.

Figure 1-1

Worlds Supplies of Oil and NGL’s, 2004-2008 (Million b/d)

81

84

87

2004 2005 2006 2007 2008

1-1 OPEC Supplies

In 2008 PEC countries' oil supplies (crude oil and NGLs) witnessed an increase, for the first time in three years, amounting to 1.3 million b/d, or about 3.8%, as they rose to 35.4 million b/d. The previous two years of 2006 and 2007 recorded declines of 100,000 and 400,000 b/d, respectively. The rise in 2008 brought OPEC countries’ share of total world oil supplies to 41.2%, compared with 40.3% the previous year, as shown in Table (1-1). OPEC supplies of natural gas and unconventional oils rose from 4.3 million b/d in the first quarter of 2008 to 4.6 million in the fourth quarter. Its supplies of crude oil declined from 31.2 million b/d to 30.2 million in the same period. That was mainly due to the coming into effect of OPEC’s October 2008 decision to cut production quotas.

In 2008 OPEC members faced many challenges, including a decline in world oil demand as a result of the global recession, and an unprecedented slump in oil prices, which had a severe impact on OPEC members’ oil exports. To combat the challenges, OPEC held three extraordinary meetings in the course of the year, in addition to its two ordinary meetings. The meetings are described below: - In light of the continued glut of oil supplies throughout 2007, OPEC

agreed at its first extraordinary meeting of the year on 1 February 2008 to keep production quotas unchanged and to take all measures necessary to maintain the stability of the oil market.

- At OPEC's first ordinary meeting of the year, on 5 March 2008, it was noted that the oil market is well supplied and that commercial oil stocks

were at good levels, higher than average of the last five years. The OPEC Conference therefore decided once again to keep production quotas unchanged and reiterated member countries commitment to market stability and ensuring sufficient supplies.

- OPEC’s second ordinary meeting on 9-10 September 2008 noted that the output measures adopted by OPEC countries had ensured that oil market is well supplied. The conference therefore agreed to keep to the production quotas set in September 2007 (28.8 million b/d) after adjusting them to include new members (Angola and Ecuador) and exclude Indonesia and Iraq, which reduced the total quotas by 500,000 b/d.

- At its second extraordinary meeting on 24 October 2008, OPEC discussed the global financial crisis and economic situation and their impact on the oil market. In view of demand decline for energy in general, and oil in particular, and a collapse of oil prices, OPEC decided to cut the production quotas of its 11 members by 1.5 million b/d effective from 1 November 2008.

- At its third extraordinary meeting on 17 December 2008, OPEC agreed once again to cut 2.2 million b/d from the actual production of its 11 members in September, which totaled 29.045 million b/d. This brought the total quota cuts in 2008 effective from 1 January 2009 to 4.2 million b/d, which was the biggest quota cut in a single year since production quotas were introduced in 1982, as shown in Figure (1-2).

Figure 1-2 OPEC Members’ Production Quotas Cut Decisions to Avoid Further Price

Slide During 2008 (Thousand b/d)

0

1000

2000

3000

4000

5000

Septemer 2008 Oct-08 Dec-08 Total cuts in 2008

1-2 Non-OPEC Supplies

Total non-OPEC oil supplies rose to about 50.6 million b/d in 2008, which was on average 100,000 b/d more than in 2007, as shown in Table (1-1).

Among this group, China’s production rose by 100,000 b/d to 3.9 million b/d and that of developing countries rose by 300,000 b/d. In contrast OECD oil supplies declined by about 300,000 b/d to 19.8 b/d in 2008, while Former Soviet Union supplies remained unchanged from their 2007 level of 12.5 million b/d.

Figure (1-3) shows the annual change in oil supplies from OPEC and non-OPEC producers in 2004-2008.

Figure 1-3 Annual Change in World Supplies of Crude Oil and NGL’s, 2004-2008

(million b/d)

-1

-0.5

0

0.5

1

1.5

2

2.5

3

2004 2005 2006 2007 2008

OPEC Rest of the World

2. World Oil Demand

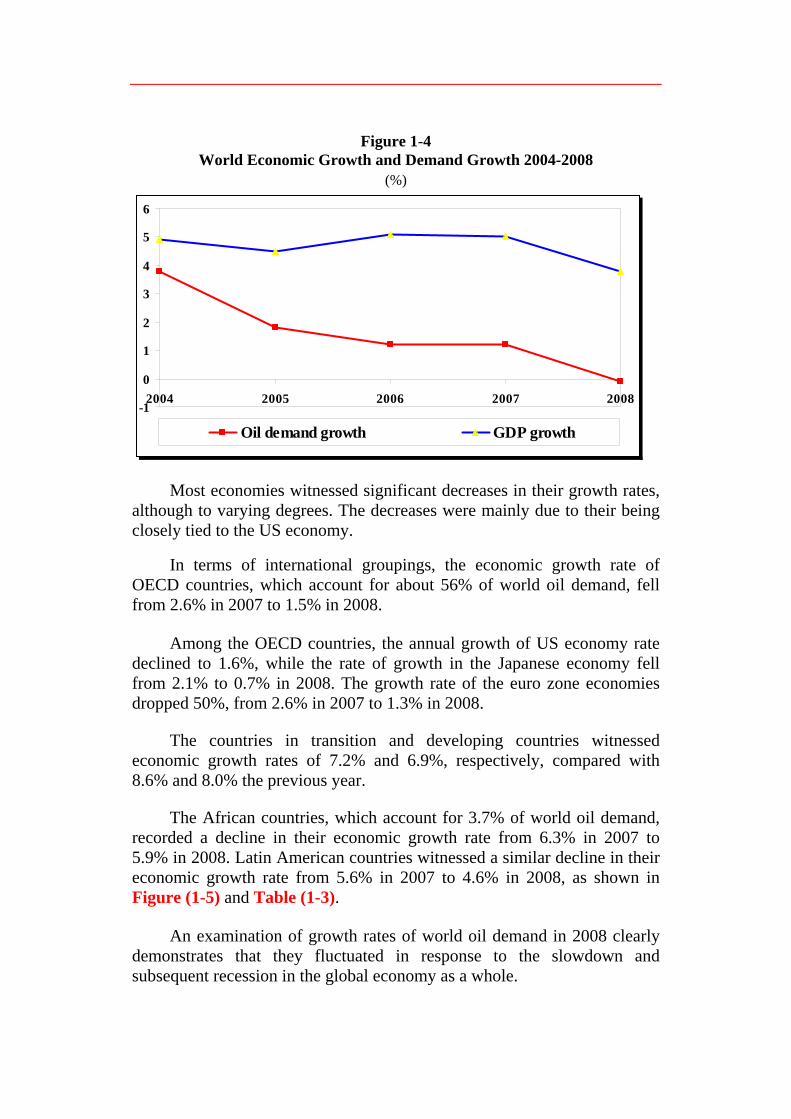

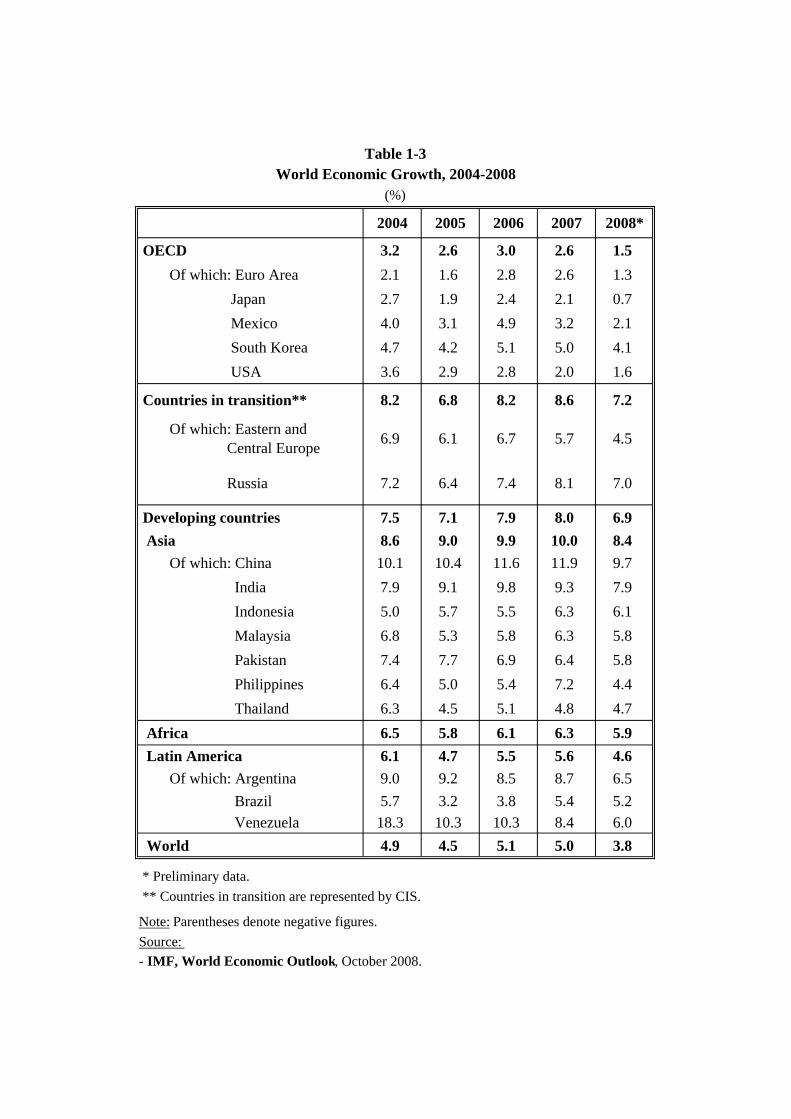

The events of 2008 highlighted the close link between world economic growth rates and world oil demand growth rates. The sharp drop in world economic growth rates from 5.0% in 2007 to 3.8% in 2008 was accompanied by a decline in world oil demand growth from 1.2% in 2007 to -0.1% in 2008. Figure (1-4) and Table (1-2) show the annual rates of growth in world oil demand compared with world economic growth rates.

Figure 1-4 World Economic Growth and Demand Growth 2004-2008

(%)

-1

0

1

2

3

4

5

6

2004 2005 2006 2007 2008

Oil demand growth GDP growth

Most economies witnessed significant decreases in their growth rates, although to varying degrees. The decreases were mainly due to their being closely tied to the US economy.

In terms of international groupings, the economic growth rate of OECD countries, which account for about 56% of world oil demand, fell from 2.6% in 2007 to 1.5% in 2008.

Among the OECD countries, the annual growth of US economy rate declined to 1.6%, while the rate of growth in the Japanese economy fell from 2.1% to 0.7% in 2008. The growth rate of the euro zone economies dropped 50%, from 2.6% in 2007 to 1.3% in 2008.

The countries in transition and developing countries witnessed economic growth rates of 7.2% and 6.9%, respectively, compared with 8.6% and 8.0% the previous year.

The African countries, which account for 3.7% of world oil demand, recorded a decline in their economic growth rate from 6.3% in 2007 to 5.9% in 2008. Latin American countries witnessed a similar decline in their economic growth rate from 5.6% in 2007 to 4.6% in 2008, as shown in Figure (1-5) and Table (1-3).

An examination of growth rates of world oil demand in 2008 clearly demonstrates that they fluctuated in response to the slowdown and subsequent recession in the global economy as a whole.

Figure 1-5

World Economic Growth 2007-2008 (%)

5.0

3.8

0123456789

O ECDCountries

Countries inTransition

DevelopingCountries

Africa Latin America World

2007 2008

At the beginning of the first quarter of 2008 it was forecast that world oil demand would grow by 1.2 million b/d, but before long, at the end of the second quarter, the forecast had been revised to 1.1 million b/d. By the end of third quarter it had fallen to 0.9 million b/d, and at the beginning of the fourth quarter the forecast was revised downwards to 0.6 million b/d. At the end of the year it dropped by another 100,000 b/d.

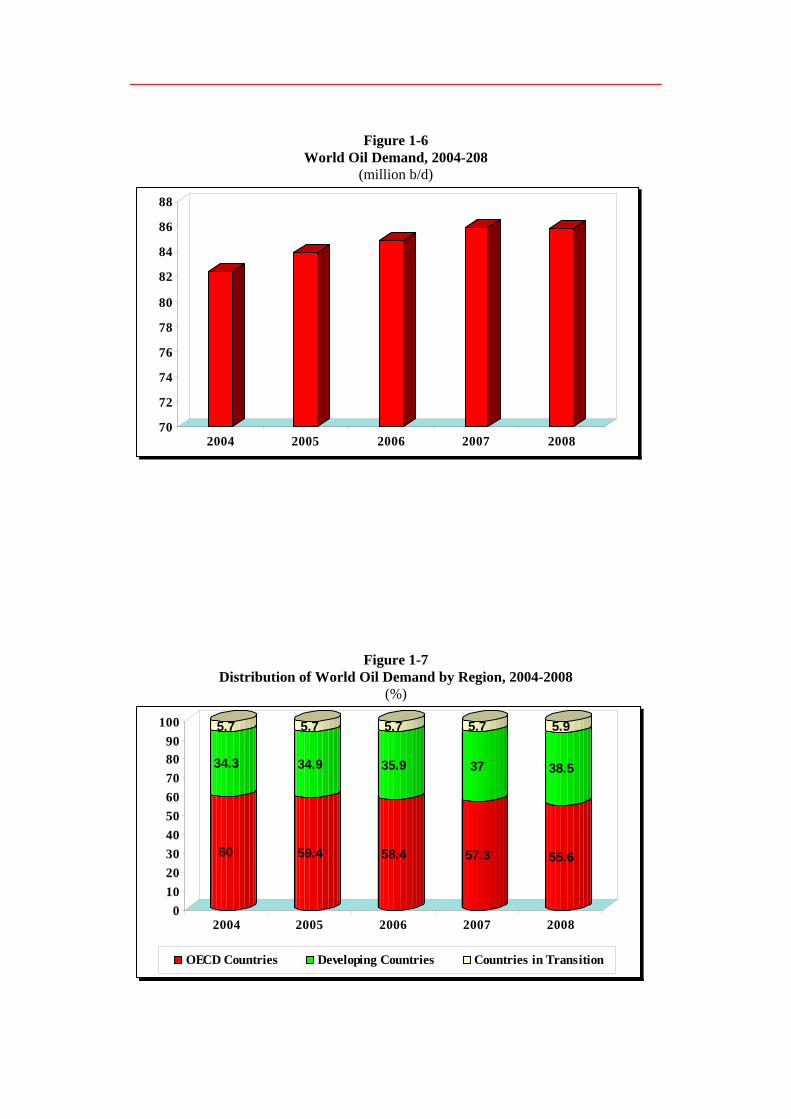

Low economic growth rates had a negative impact on world oil demand growth, which dropped by 100,000 b/d, or 0.1%, below its 2007 level. This was the lowest growth rate for the last ten years. World demand for oil in 2008 totaled 85.8 million b/d, as shown in Figure (1-6) and Table (1-4).

The level of oil demand varied from one international grouping to another. Whilst it dropped sharply in the OECD countries in 2008 by 1.5 million b/d from 2007 to 47.7 million b/d, it rose in the developing countries by about 1.2 million b/d and in the countries in transition by 200,000 b/d.

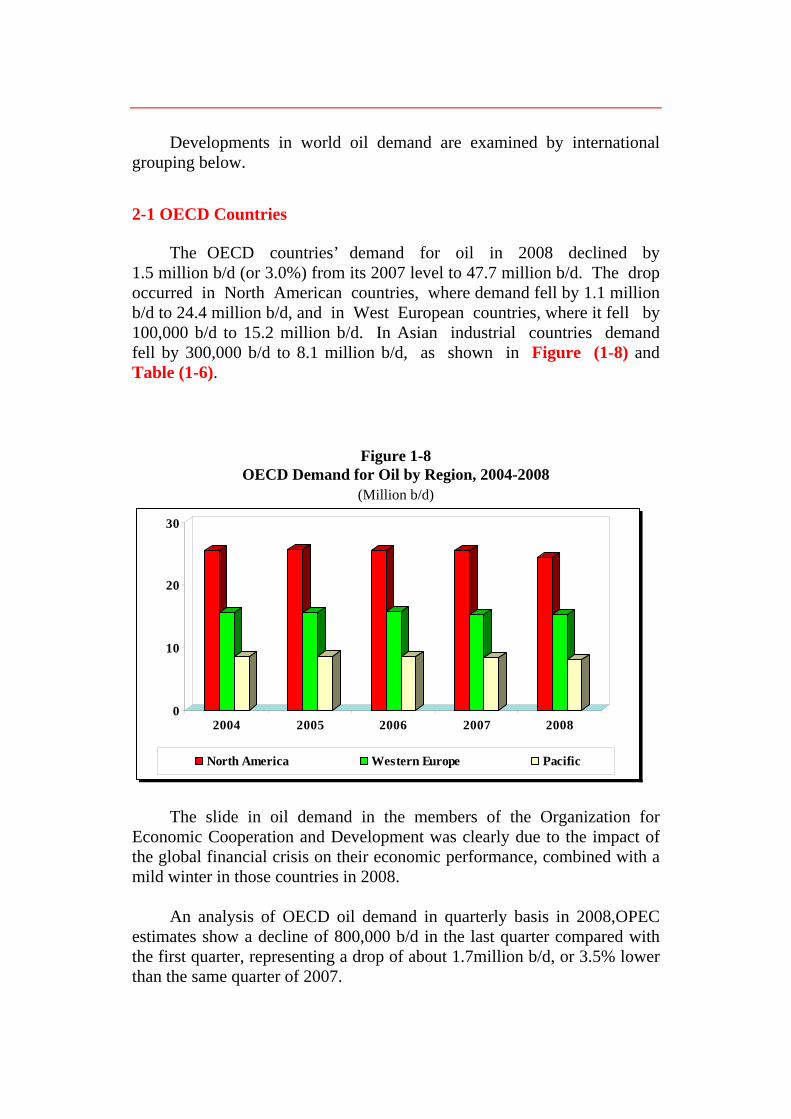

The change in demand levels of each grouping altered their shares in total world demand in 2008. The share of the OECD countries declined from 57.3% in its 2007 level to 55.6%, while that of the developing countries rose from 37% to 38.5%, and similarly countries in transition rose from 5.7% to 5.9%, as shown in Figure (1-7) and Table (1-5).

Figure 1-6 World Oil Demand, 2004-208

(million b/d)

70

72

74

76

78

80

82

84

86

88

2004 2005 2006 2007 2008

Figure 1-7 Distribution of World Oil Demand by Region, 2004-2008

(%)

60

34.3

5.7

59.4

34.9

5.7

58.4

35.9

5.7

57.3

37

5.7

55.6

38.5

5.9

0102030405060708090

100

2004 2005 2006 2007 2008

OECD Countries Developing Countries Countries in Transition

Developments in world oil demand are examined by international

grouping below.

2-1 OECD Countries

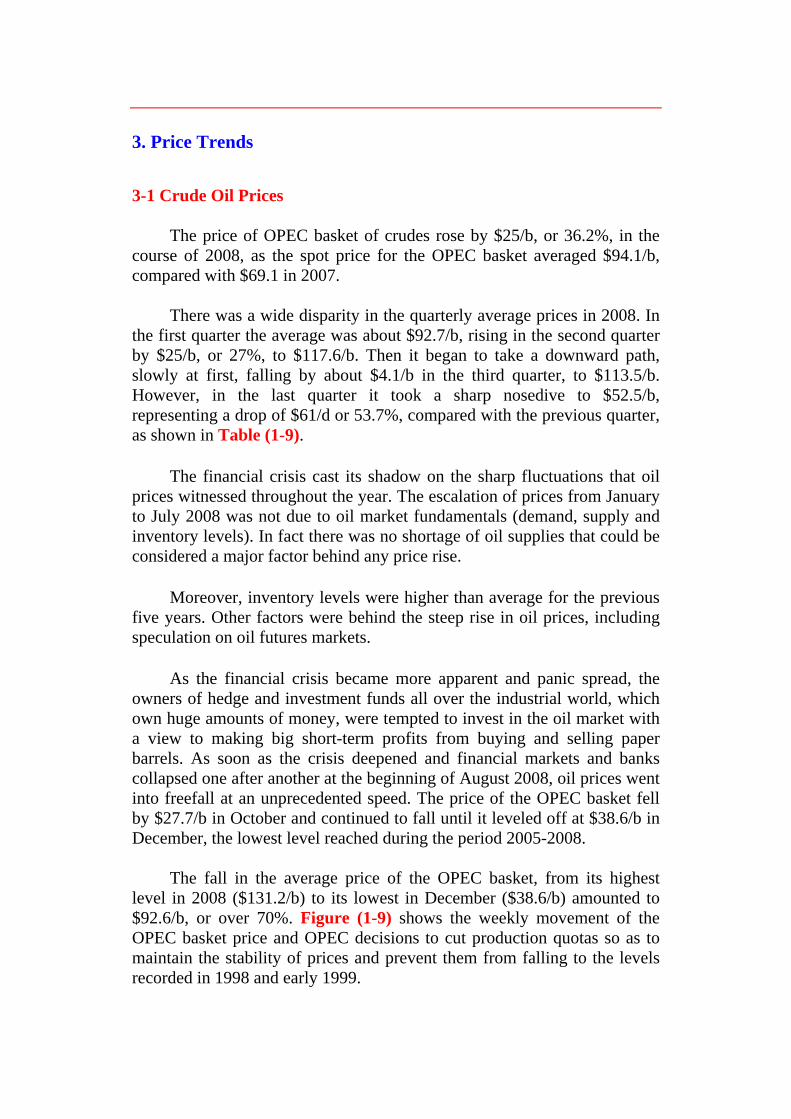

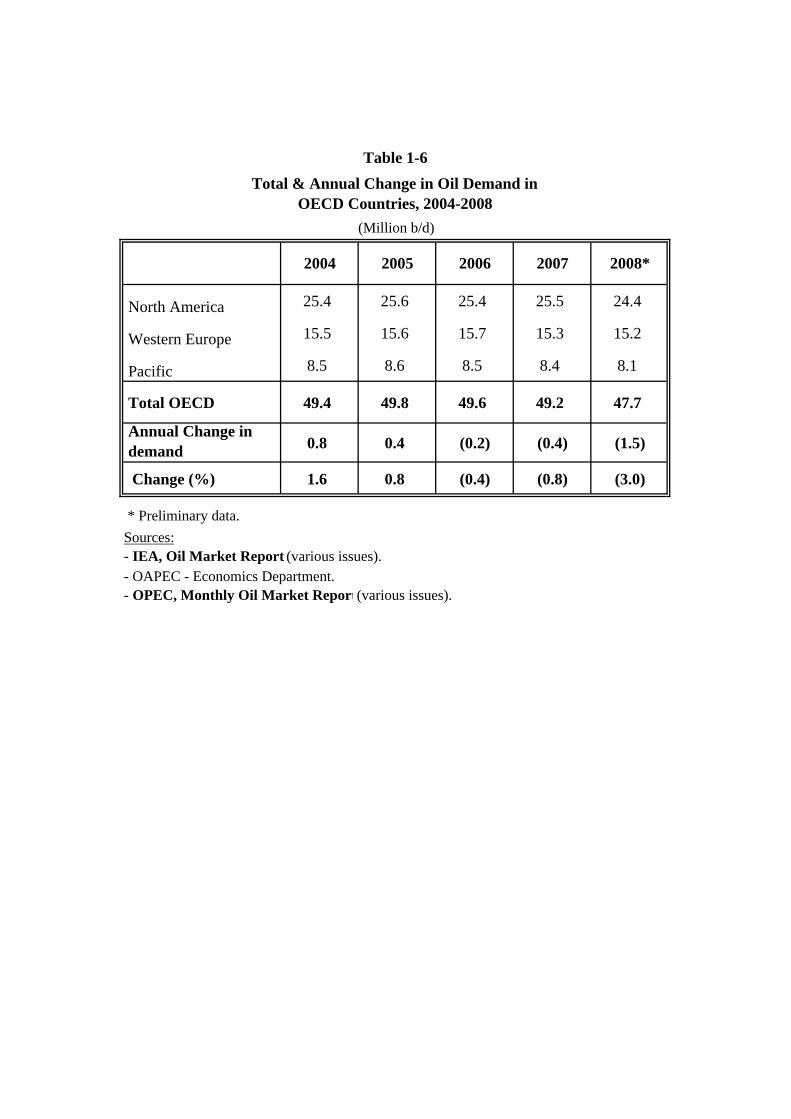

The OECD countries’ demand for oil in 2008 declined by 1.5 million b/d (or 3.0%) from its 2007 level to 47.7 million b/d. The drop occurred in North American countries, where demand fell by 1.1 million b/d to 24.4 million b/d, and in West European countries, where it fell by 100,000 b/d to 15.2 million b/d. In Asian industrial countries demand fell by 300,000 b/d to 8.1 million b/d, as shown in Figure (1-8) and Table (1-6).

Figure 1-8 OECD Demand for Oil by Region, 2004-2008

(Million b/d)

0

10

20

30

2004 2005 2006 2007 2008

North America Western Europe Pacific

The slide in oil demand in the members of the Organization for Economic Cooperation and Development was clearly due to the impact of the global financial crisis on their economic performance, combined with a mild winter in those countries in 2008.

An analysis of OECD oil demand in quarterly basis in 2008,OPEC estimates show a decline of 800,000 b/d in the last quarter compared with the first quarter, representing a drop of about 1.7million b/d, or 3.5% lower than the same quarter of 2007.

The major contribution made by OECD countries to world oil demand meant that world demand in the fourth quarter of 2008 decreased by about 400,000 b/d from the first quarter and by about 700,000 b/d compared with the same quarter of 2007.

2-2 Developing Countries

Although demand for oil in the developing countries in 2008 rose by 1.2 million b/d above its 2007 level to a record 33 million b/d, the annual rate of growth declined from 4.3% in 2007 to 3.7% in 2008.

Demand in the developing countries is the main driver of world oil demand, as it rose by 4.7 million b/d between 2004 and 2008.

Among this grouping, demand in the Middle East and Africa rose by 400,000 b/d to 10 million b/d, of which the Arab countries accounted for 5.4 million b/d, or 54% of the region’s demand and about 16.3% of total demand in the developing countries. The increase was largely due to high economic growth rates in most countries of the region, in contrast to other countries of the world.

Most of the increase in the Arab countries demand occurred in OAPEC member countries, where it rose 4.4% from 4.5 million b/d in 2007 to 4.7 million b/d in 2008.

Demand in the Asian developing countries rose by 600,000 b/d to 17.3 million b/d in 2008. China, which accounted for 46% of total demand in the Asian developing countries, accounted for 67% of the increase in demand of the Asian developing countries and for a third of the increase among all developing countries. Its demand rose by 400,000 b/d to 8 million b/d in 2008. Indian demand increased by about 200,000 b/d, bringing its demand to 3.1 million b/d in 2008, while demand in the Latin American countries rose by about 200,000 b/d to 5.7 million b/d, as shown in Table (1-7).

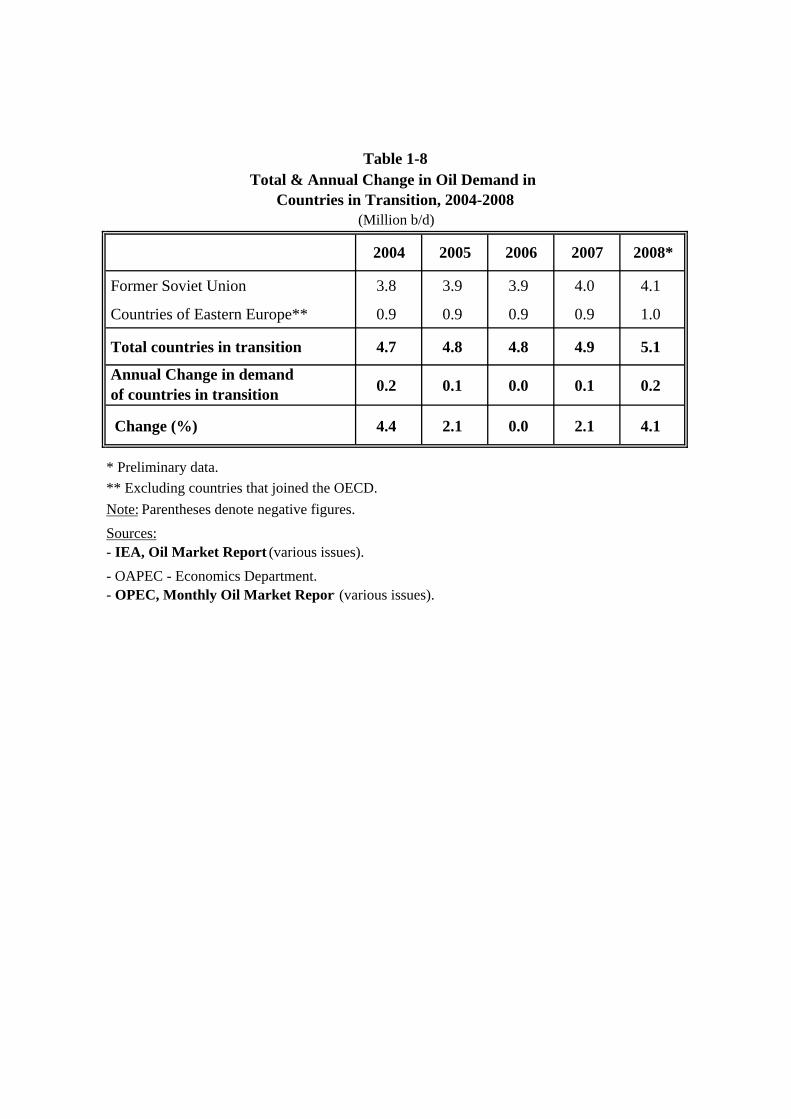

2-3 Countries in Transition

Oil demand in the countries in transition totaled 5.1 million b/d in 2008, which was 200,000 b/d, or 4.1%, higher than the previous year. Demand in the FSU rose by 100,000 b/d, which was the same rise recorded in 2007. Demand in the countries of Eastern Europe also rose by the same amount of 100,000 b/d, bringing their total to 1 million b/d in 2008, as shown in Table (1-8).

3. Price Trends

3-1 Crude Oil Prices

The price of OPEC basket of crudes rose by $25/b, or 36.2%, in the course of 2008, as the spot price for the OPEC basket averaged $94.1/b, compared with $69.1 in 2007.

There was a wide disparity in the quarterly average prices in 2008. In the first quarter the average was about $92.7/b, rising in the second quarter by $25/b, or 27%, to $117.6/b. Then it began to take a downward path, slowly at first, falling by about $4.1/b in the third quarter, to $113.5/b. However, in the last quarter it took a sharp nosedive to $52.5/b, representing a drop of $61/d or 53.7%, compared with the previous quarter, as shown in Table (1-9).

The financial crisis cast its shadow on the sharp fluctuations that oil prices witnessed throughout the year. The escalation of prices from January to July 2008 was not due to oil market fundamentals (demand, supply and inventory levels). In fact there was no shortage of oil supplies that could be considered a major factor behind any price rise.

Moreover, inventory levels were higher than average for the previous five years. Other factors were behind the steep rise in oil prices, including speculation on oil futures markets.

As the financial crisis became more apparent and panic spread, the owners of hedge and investment funds all over the industrial world, which own huge amounts of money, were tempted to invest in the oil market with a view to making big short-term profits from buying and selling paper barrels. As soon as the crisis deepened and financial markets and banks collapsed one after another at the beginning of August 2008, oil prices went into freefall at an unprecedented speed. The price of the OPEC basket fell by $27.7/b in October and continued to fall until it leveled off at $38.6/b in December, the lowest level reached during the period 2005-2008.

The fall in the average price of the OPEC basket, from its highest level in 2008 ($131.2/b) to its lowest in December ($38.6/b) amounted to $92.6/b, or over 70%. Figure (1-9) shows the weekly movement of the OPEC basket price and OPEC decisions to cut production quotas so as to maintain the stability of prices and prevent them from falling to the levels recorded in 1998 and early 1999.

Figure 1-9 Weekly Movement of OPEC Basket of Crudes, 2008

($/b)

18

38

58

78

98

118

138

158Ja

nuar

y

Febr

uary

Mar

ch

Apr

il

May

June

July

Aug

ust

Sept

embe

r

Oct

ober

Nov

embe

r

Dec

embe

r

First cut :500 tb/d

Second cut :1.5 mb/d

Third cut :2.2 mb/d

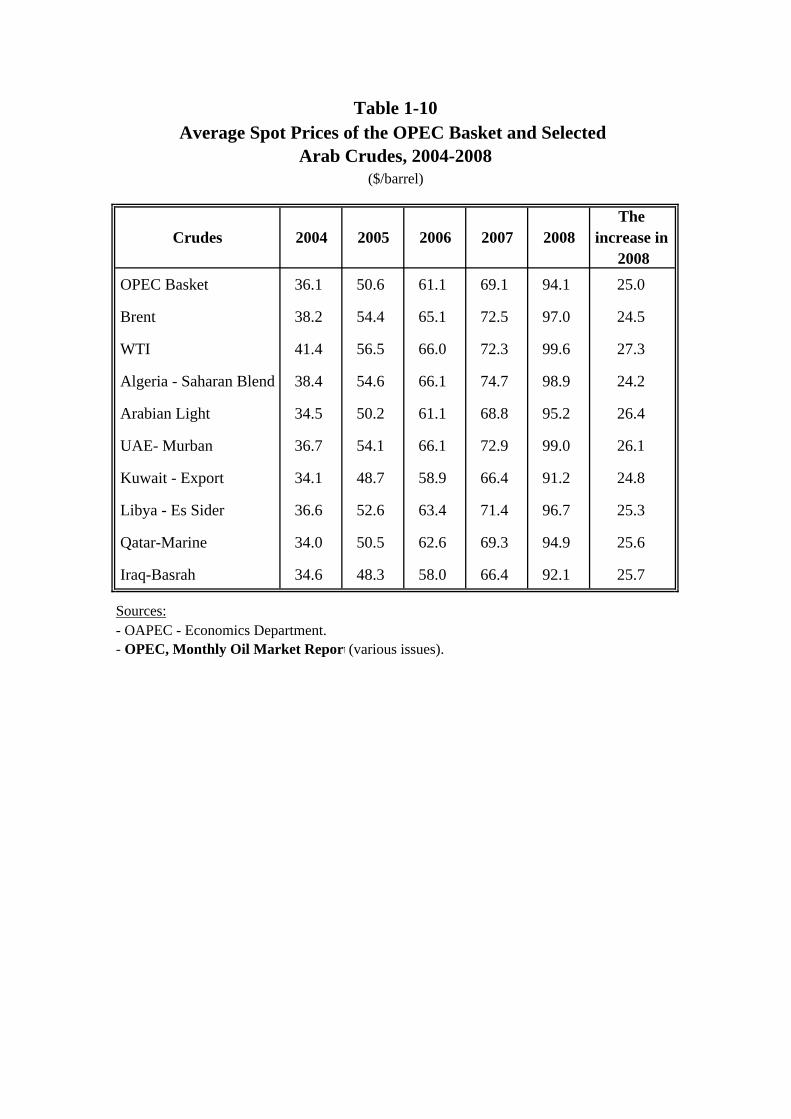

Spot prices for various Arab crudes followed the same general trend. They rose in the first half of 2008 and fell in the second half. However, the average price of these crudes was significantly higher than in 2007. The increases ranged from $24.2/b to $26.4/b, or between 32.4% and 38.4%. Algerian crude rose by 32.4% to $98.9/b, while Saudi Arabian Light rose by 38.4% to $95.2/b.

The UAE’s Murban crude rose by 35.8% to $99/b, while Kuwaiti crude and Libyan Sidra rose by 37.3% and 35.3%, respectively. Qatar Marine crude and Iraqi Basra rose by 36.9% and 38.7%, respectively, as shown in Table (1-10).

The nominal value of the rise in crude oil prices of $25/b during 2008 was only slightly different from its real record value measured in 1995 prices, after adjustment according to the index, which represents the value of a unit of OECD exports. The real price increase amounted to $18.8/b, or 33.3%, to reach and average of $75.3/b during 2008, as shown in Table (1-11).

3-2 Spot Prices for Oil Products

There was a huge rise in the annual average prices of various oil products on all major markets in the world in 2008, although the amounts varied according to the product and the market.

3-2-1 Premium Gasoline Prices

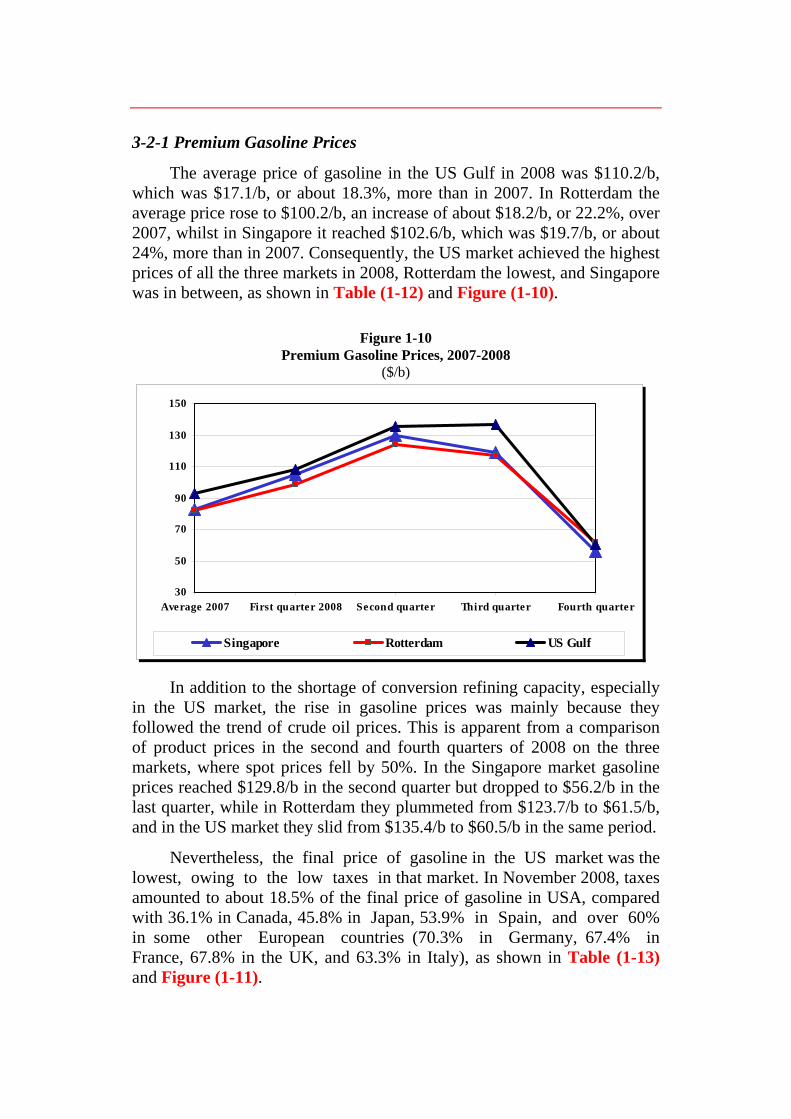

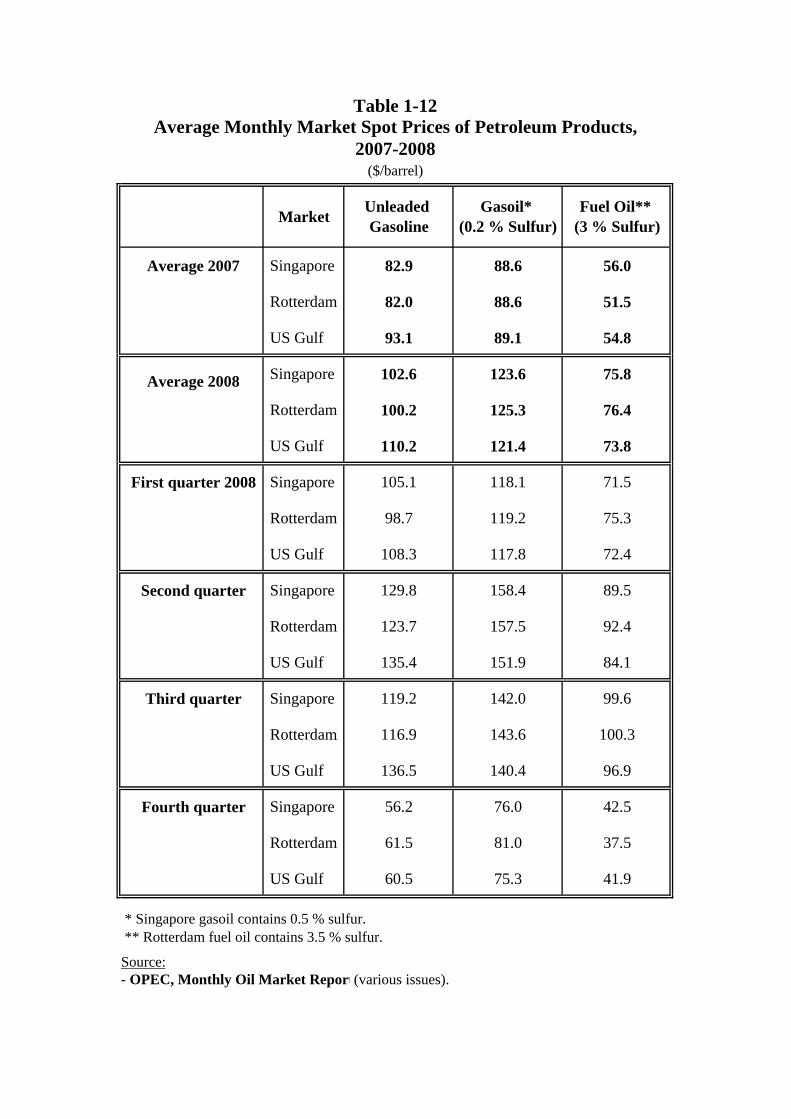

The average price of gasoline in the US Gulf in 2008 was $110.2/b, which was $17.1/b, or about 18.3%, more than in 2007. In Rotterdam the average price rose to $100.2/b, an increase of about $18.2/b, or 22.2%, over 2007, whilst in Singapore it reached $102.6/b, which was $19.7/b, or about 24%, more than in 2007. Consequently, the US market achieved the highest prices of all the three markets in 2008, Rotterdam the lowest, and Singapore was in between, as shown in Table (1-12) and Figure (1-10).

Figure 1-10 Premium Gasoline Prices, 2007-2008

($/b)

30

50

70

90

110

130

150

Average 2007 First quarter 2008 Second quarter Third quarter Fourth quarter

Singapore Rotterdam US Gulf

In addition to the shortage of conversion refining capacity, especially in the US market, the rise in gasoline prices was mainly because they followed the trend of crude oil prices. This is apparent from a comparison of product prices in the second and fourth quarters of 2008 on the three markets, where spot prices fell by 50%. In the Singapore market gasoline prices reached $129.8/b in the second quarter but dropped to $56.2/b in the last quarter, while in Rotterdam they plummeted from $123.7/b to $61.5/b, and in the US market they slid from $135.4/b to $60.5/b in the same period.

Nevertheless, the final price of gasoline in the US market was the lowest, owing to the low taxes in that market. In November 2008, taxes amounted to about 18.5% of the final price of gasoline in USA, compared with 36.1% in Canada, 45.8% in Japan, 53.9% in Spain, and over 60% in some other European countries (70.3% in Germany, 67.4% in France, 67.8% in the UK, and 63.3% in Italy), as shown in Table (1-13) and Figure (1-11).

Figure 1-11 Gasoline Prices in some OECD Countries, November 2008

($/litre)

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

1.8U

SA

Can

ada

Spai

n

Japa

n

Uni

ted

Kin

gdom

Fran

ce

Ital

y

Ger

man

y

Price without Tax Tax

3-2-2 Gasoil/Diesel Prices

Gasoil prices in 2008 were relatively high in most markets compared with gasoline and fuel oil, because gasoil is in demand throughout the year, especially in the transport, heating and cooling sectors. The highest increase occurred in Rotterdam, where gasoil prices were 41.5% higher than in 2007, as the average annual price rose to $125.3/b. The Singapore market came next with a 39.5% increase, bringing the average price to $123.6/b, while on the US market gasoil prices rose by 36.2%, giving an average price of $121.4/b.

3-2-3 Fuel Oil Prices

Fuel oil prices rose in 2008 on all markets. On the Rotterdam market the average price of fuel oil rose 48.3% above 2007 to $76.4/b, on the Singapore market it rose by about 35.3% to $75.8/b, while on the US market the average price rose by 34.7% to $73.8/b.

3-3 Oil Freight Prices

Crude oil freight prices on all routes rose by over 40% in 2008 compared with their 2007 levels for several reasons, but mainly because of the oil market was in contango, which prompted some participants to store crude oil at sea. Reports indicate that over 40 very large crude carriers (VLCCs), or over 8% of the global fleet, were used for storage in the

Middle East, the Gulf of Mexico, Asia, and the North Sea. The freight price rise may also be attributed to the poor weather conditions that closed some ports and made crossing some Turkish straits difficult. Moreover, the strike at the Fos-Lavera port in France caused more bottlenecks and affected the available tonnage.

The average price for oil shipments from Arabian Gulf ports to the East on VLCCs (230,000-280,000 DWT) was 136 points on the World Scale (WS)1. This was 45 points, or 49.7%, higher than in 2007.

Freight prices for shipments from Arabian Gulf ports to the West, on crude carriers with a capacity of 270,000-285,000 DWT, averaged 99 points on the WS, which was 32 points, or about 47.6%, higher than in 2007, as shown in Table (1-14).

In the Mediterranean region there was a similar rise in freight prices for small and medium-sized tankers (80,000-85,000 dwt). The average freight price in 2008 was 205 WS points, which was 60 points, or about 41.4%, higher than in 2007.

In July 2008 crude oil freight prices on all routes registered the highest level. Average freight prices on the Arabian Gulf-East route reached 235 WS points and on the Arabian Gulf-West route they topped 144 WS points, while cross the Mediterranean route they peaked at 278 WS points. Then in November 2008 they fell, to 70, 61, and 120 WS points, respectively.

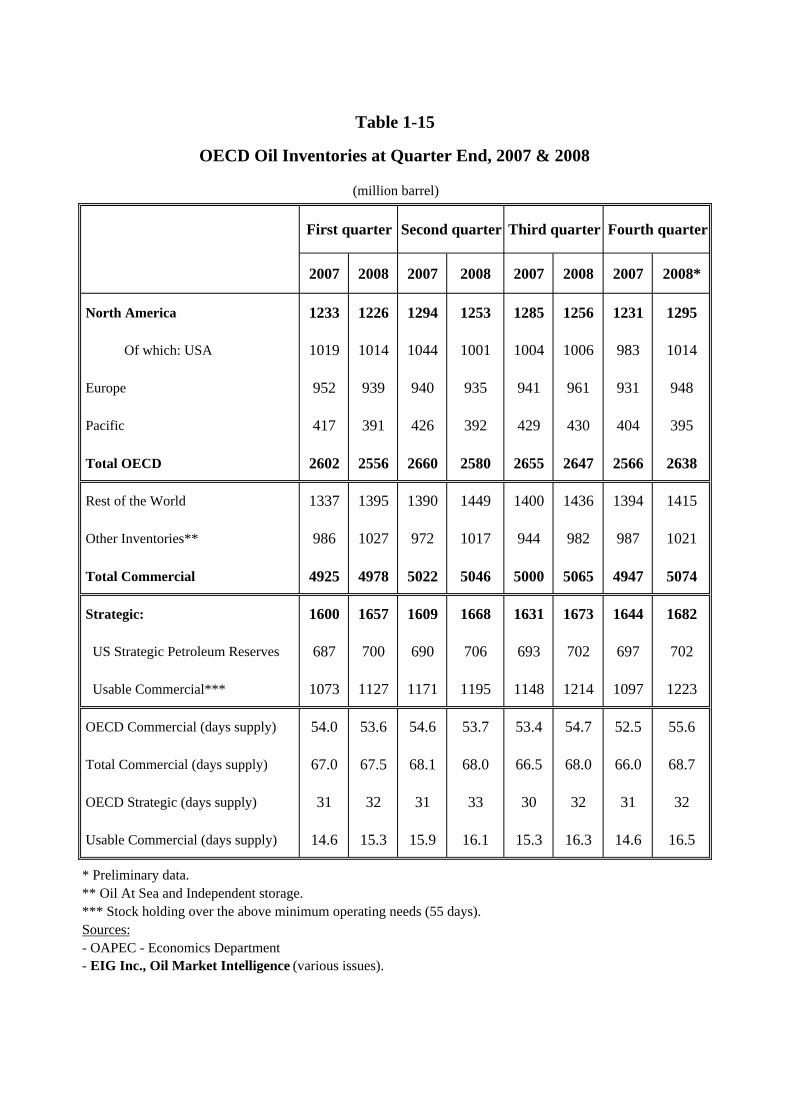

4. World Oil Inventories

The year 2008 witnessed a significant rise in total world oil stocks (commercial and strategic) as they rose by about 165 million barrels, or 2.5%, to 6756 million barrels at the end of December 2008. Crude oil stocks at sea account for about 80% of the tanker business worldwide. Independent stocks near consumption centers such as in Caribbean ports and the ports of Rotterdam and Singapore exceeded 1000 million barrels at the end of 2008, totaling 1021 million barrels.

The significant rises in the commercial stocks of OECD countries, and the US in particular, placed a downward pressure on prices. The lack of cooperation on the part of non-OPEC producers jeopardized the stability of

the world oil market. There is a real need for effective cooperation between OPEC and non-OPEC producers to maintain oil market stability. 4-1 OECD Commercial Stocks

The rise in supply levels before OPEC’s decisions to cut production quotas helped build up the levels of commercial stocks in OECD countries in 2008. Total stocks rose by 24 million barrels in the second quarter of the year above their level in the first quarter, or by 3.3%, to 2580 million barrels. In the third quarter they rose once again by 67 million barrels above second quarter levels. In the last quarter of the year there was a significant increase of about 72 million barrels compared with the end of 2007, bringing them to 2638 million barrels at year end.

All commercial stocks in the OECD countries amounted to 56 days of forward consumption, which is four days higher than the usual average of 52 days. This level is three times the annual production of Kuwait, four times that of Libya, and five times that of Algeria. Saudi Arabia’s declaration in June 2008 that it would raise its production by 500,000 b/d in an attempt to curb rising oil prices added another 45 million barrels to the stocks at that time.

4-2 US Strategic Petroleum Reserve

The US Strategic Petroleum Reserve (SPR) passed the 700 million barrel level for the first time in 2008, as it totaled 702 million barrels at year end, 5 million barrels higher than at the end of 2007.

What is more, the SPR did not fall below the 700 million barrel mark throughout the year. After reaching 700 million barrels in the first quarter of 2008, the SPR rose by 6 million barrels to 706 million barrels at the end of the second quarter, then dropped slightly to 702 million barrels in the third quarter, and remained at the 702 million barrel level in the fourth quarter.

Since 2004, the US Administration has adopted a more flexible attitude toward releasing quantities of the SPR to compensate for any shortage of supply. This gives more importance to the commercial aspect of the SPR than the previous policy, which regarded the SPR as a last line of defense to be used only at times of major crisis. See Figure (1-12) and Table (1-15).

Usable commercial stocks are the stocks kept by oil companies as a hedging measure to counter any sudden interruption of supplies or for

speculation purposes when prices rise. The level of these stocks rose sharply by about 126 million barrels, or 11.5%, at the end of 2008 to 1223 million barrels.

Figure 1-12 US SPR at Quarter End, 2007-2008

(Million barrels)

675

680

685

690

695

700

705

710

First quarter Second quarter Third quarter Fourth quarter

2008 2007

II. VALUE OF OAPEC MEMBERS’ COUNTRIES PETROLEUM EXPORTS

The oil price fluctuations of 2008, which saw prices fall by $92.6/b, or 70%, from their peak of $131.2/b in July to their lowest level of $38.6/b in December, had a detrimental effect on the value oil exports. Oil exports are the main engine of socioeconomic development in the oil producing Arab Countries, the mainstay of their central bank reserves of foreign exchange, and the main source of their budget surpluses.

On examining the impact of recent developments in oil prices on the value of OAPEC members’ oil exports, the initial estimates show, they totaled $145.7 billion in the first quarter of 2008, when prices were about $92.7/b. Then in the second and third quarter they rose to $188.7 billion and $191.2 billion, respectively, as oil prices rose to $117.6/b and $113.5/b respectively in those periods. After oil prices began to fall below the $100/b threshold from September to the end of 2008, the value of oil exports suffered a similar sharp drop, reaching $83.3 billion in the last quarter, which was 56% less than the previous quarter and 43% less than the first quarter of the year.

A comparison of the estimated value of oil revenues for each quarter of 2008 with the previous quarter shows a sharp decline of $107.9 billion in the last quarter from the third quarter. This is mainly attributable to the drop

in oil prices resulting from the repercussions of the global financial crisis. Monthly data on the movement of oil prices and the estimated monthly value of OAPEC members’ oil exports may give a clearer picture of the damage done by the drop in prices from August 2008 until the end of the year, owing to the fallout from the global financial crisis, as shown in Figure (1-13).

Figure 1-13 Monthly Oil Prices and Value of OAPEC Oil Exports, January-December

2008 ($/b)

0

10

20

30

40

50

60

70

80

90

Jan. Feb. Mar. Apr. May June July Aug. Sept. Oct. Nov. Dec.

$Bill

ion

0

20

40

60

80

100

120

140

$/b

Value of OAPEC Oil Exports OPEC Basket Price

A year-on-year comparison shows that the value of members’ oil exports rose by 45.6%, from $425 billion in 2007 to $618 billion in 2008, or by $193 billion. An analysis of individual countries shows that the rise varied from one country to another. It ranged in Iraq, Libya, Qatar, Saudi Arabia, Syria, and the UAE, for example, from 40%-65%, while in Algeria it was 38.9%, in Kuwait 20.7%, and in Egypt 19.8%, as shown in Table (1-16). The value of OAPEC members’ oil exports in real 1995 prices, after adjustment for GDP in the OECD countries, rose from $347.2 billion in 2007 to $494.6 billion in 2008, or by 42.5%, as shown in Table (1-17).

III. DEVELOPMENTS IN OIL AND ENERGY CONSUMPTION IN THE ARAB COUNTRIES

1. Arab Countries

This section provides a rough picture of total energy consumption in

the Arab countries in general, and OAPEC member countries in particular, according to energy sources. It also attempts to shed light on final primary energy consumption by major economic sectors.

1-1 Total and Per Capita Energy Consumption

Energy consumption growth in the Arab countries, like all countries in the world, is affected by three key variables: GDP, population, and prevailing energy prices on local markets. The following paragraphs provide an overview of these variables.

1- GDP: Data published in the Joint Arab Economic Report in September 2008 indicate that GDP growth rate followed a downward trend in constant prices in the Arab countries. It peaked at 7.4% in 2003 but in 2004 it declined to 7.1%, in 2005 to 6.7%, in 2006 to 6.4%, and to 5.6% in 2007, when it amounted to $1472 billion, as shown in Figure (1-14). The overall average energy intensity in the Arab countries was about 6.5 kg of oil equivalent per $1000 of GDP in 2007. The Arab countries may be divided into three groups on the basis of GDP in 2007 constant prices, as follows:

Figure 1-14 Arab Countries’ GPD in Current Prices 2003-2007

($billion)

0

200

400

600

800

1000

1200

1400

1600

2003 2004 2005 2006 2007

a) Countries with a growth rate of less than 5.0%: The seven countries in this group are Mauritania (0.9%), Morocco (2.2%), Yemen (3.1%), Saudi Arabia (3.5%), Lebanon (4%), and Algeria and Kuwait (4.6%).

b) Countries with a growth rate of 5%-10%: The 11 countries in this group are Djibouti (5.2%), Jordan and Iraq (5.9%), Tunisia (6.3%), Bahrain (6.6%), Syria and Oman (6.7%), Libya (6.8%), Egypt (7.1%), the UAE (7.4%), and Sudan (9.7%).

c) Countries with a growth of over 10%: The only country in this group is the Qatar (14.2%).

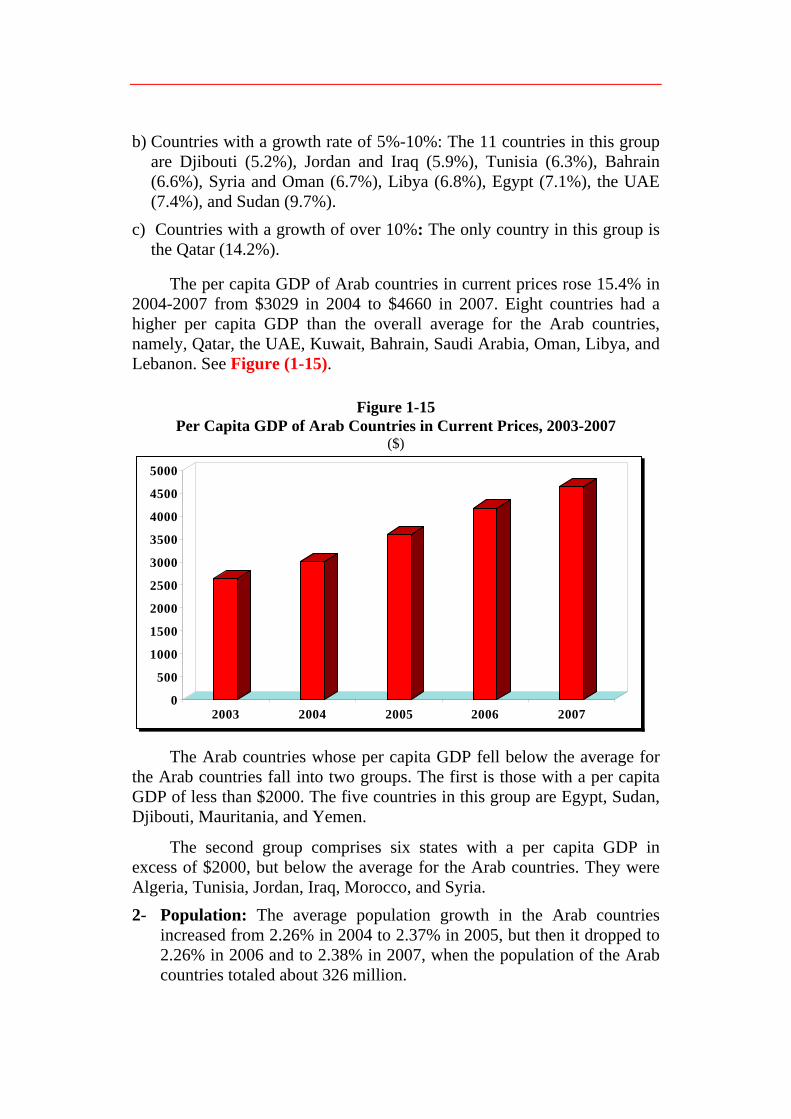

The per capita GDP of Arab countries in current prices rose 15.4% in 2004-2007 from $3029 in 2004 to $4660 in 2007. Eight countries had a higher per capita GDP than the overall average for the Arab countries, namely, Qatar, the UAE, Kuwait, Bahrain, Saudi Arabia, Oman, Libya, and Lebanon. See Figure (1-15).

Figure 1-15 Per Capita GDP of Arab Countries in Current Prices, 2003-2007

($)

0

500

1000

1500

2000

2500

3000

3500

4000

4500

5000

2003 2004 2005 2006 2007

The Arab countries whose per capita GDP fell below the average for the Arab countries fall into two groups. The first is those with a per capita GDP of less than $2000. The five countries in this group are Egypt, Sudan, Djibouti, Mauritania, and Yemen.

The second group comprises six states with a per capita GDP in excess of $2000, but below the average for the Arab countries. They were Algeria, Tunisia, Jordan, Iraq, Morocco, and Syria. 2- Population: The average population growth in the Arab countries

increased from 2.26% in 2004 to 2.37% in 2005, but then it dropped to 2.26% in 2006 and to 2.38% in 2007, when the population of the Arab countries totaled about 326 million.

3- Prices: Several Arab countries in the recent years have resorted to

raising the prices of oil products, especially gasoline. In 20006 ten Arab countries raised gasoline prices on the local market, namely, Egypt, Iraq, Jordan, Lebanon, Morocco, Sudan, Syria, Tunisia, Yemen and the UAE. Moreover, Morocco raised the prices of some oil products on local markets. The data available for 20007 indicate that one country, Syria, raised gasoline prices on the local market. Among OAPEC member countries in 2008, Syria raised the prices of oil products in March, while Jordan cut oil product prices six times starting on 10 July 2008 in response to the fall in crude oil prices on world markets.

1-2 Energy Consumption by Source

Initial estimates show that energy consumption growth in the Arab countries between 2004 and 2008 was stable at about 4.3% in 2007-2008, after registering increases of 7.9% in 2004, 6.3% in 2005, and 5.5% in 2006. Total energy consumption in the Arab countries exceeded the 10 million barrels of oil equivalent per day (boe/d) threshold in 2008.

Energy consumption in the Arab countries is increasingly dependent on petroleum (oil and natural gas), owing to the declining share of other sources, such as hydroelectricity and coal.

The biggest increase in consumption occurred in natural gas consumption, which rose by 5.7% a year between 2004 and 2008, while oil consumption grew by 4.9% in the same period.

There was no significant increase in the consumption of hydroelectricity and coal. Oil continues to be the main source of energy consumption in the Arab countries, despite the increasing use of natural gas. Oil meets over half the Arab countries energy requirements, accounting for 53.9% in 2008, compared with 44.5% for natural gas, 1.4% for hydroelectricity, and 0.2% for coal.

Among non-OAPEC Arab countries oil plays a bigger role in the energy mix, accounting for over three quarters (77.5%) of their energy needs, compared with 51.6% in OAPEC member countries. On the other hand, natural gas plays a bigger role in OAPEC member countries, accounting for 47.2% of their total energy consumption, compared with 17.2% in other Arab countries, as shown in Figure (1-16) and Table (1-18). The disparity in energy consumption may be attributed to the differing availability of hydrocarbon resources in the Arab countries.

Energy consumption in the Arab countries grew at different rates in the period 2004-2008, averaging per annum 5.3% for OAPEC member countries and 3.7% for other Arab countries. OAPEC members accounted for 91% of total energy consumption in the Arab countries in 2008 and other Arab countries for 9%.

This disparity in energy consumption mainly reflects the disparity in the size of their national economies, the size and exploitation of their hydrocarbon resources, and their populations.

• Size of national economy: The GDP of OAPEC member countries accounted for about 83.9% of the Arab countries GDP in 2007.

• Energy resources: OAPEC member countries possessed 98% of the Arab countries crude oil reserves at the end of 2008 and 97.4% of their natural gas reserves.

• Population: OAPEC member countries accounted for about 63.3% of the total population of the Arab countries in 2008.

Figure 1-16 Energy Consumption in the Arab Countries by Source, 2008

(%)

0

10

20

30

40

50

60

Petroleumproducts

Natural Gas Hydroelectricity Coal

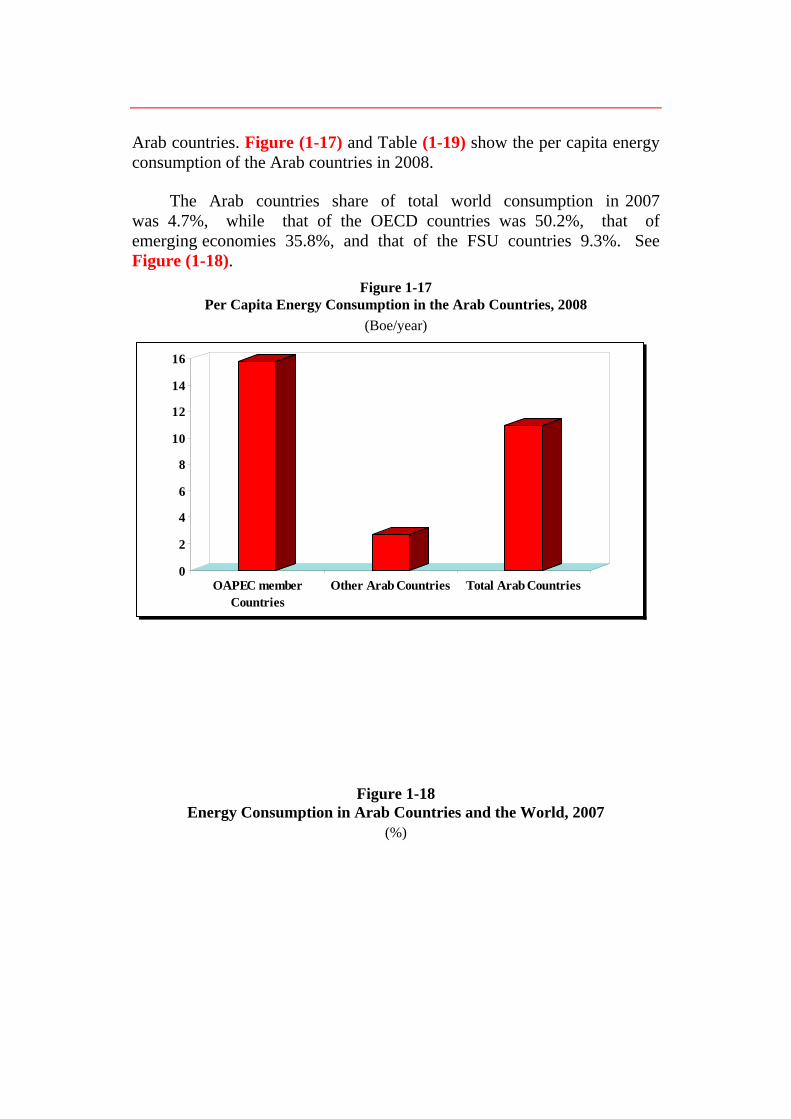

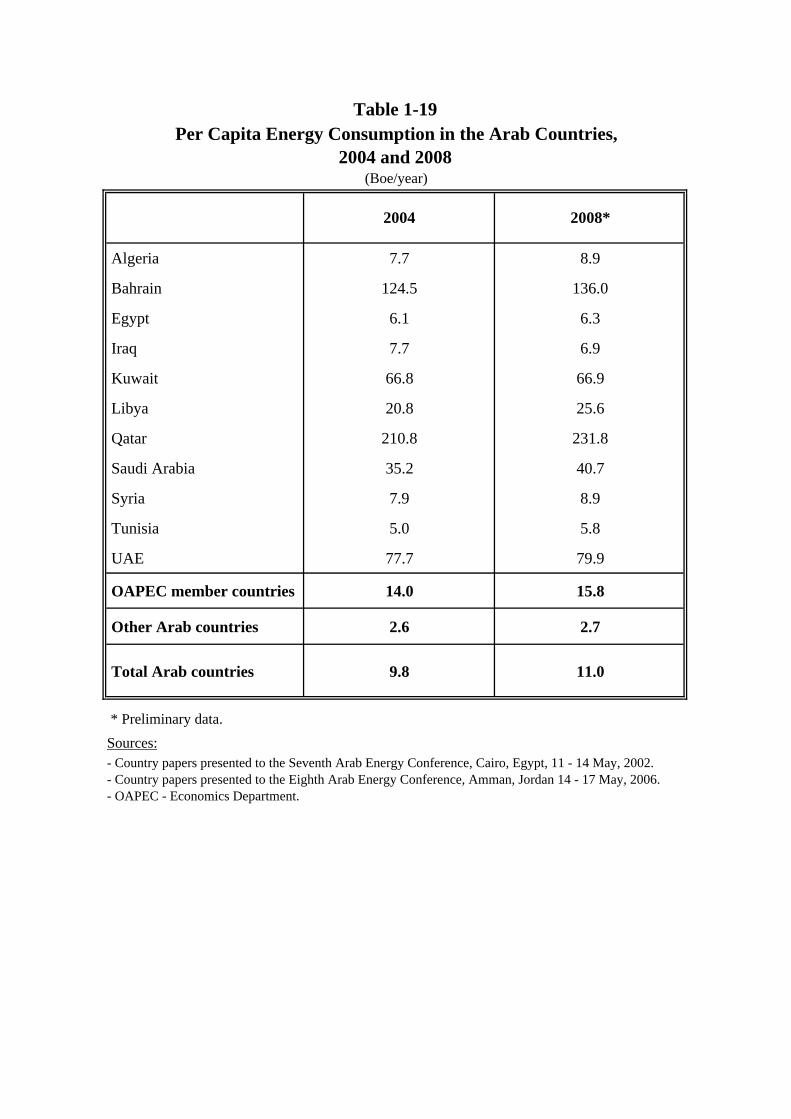

The disparity in energy consumption is particularly stark when one examines per capita energy consumption, which amounted to 15.8 boe in OAPEC member countries in 2008, compared with 2.7 boe among other

Arab countries. Figure (1-17) and Table (1-19) show the per capita energy consumption of the Arab countries in 2008.

The Arab countries share of total world consumption in 2007 was 4.7%, while that of the OECD countries was 50.2%, that of emerging economies 35.8%, and that of the FSU countries 9.3%. See Figure (1-18).

Figure 1-17 Per Capita Energy Consumption in the Arab Countries, 2008

(Boe/year)

0

2

4

6

8

10

12

14

16

OAPEC memberCountries

Other Arab Countries Total Arab Countries

Figure 1-18 Energy Consumption in Arab Countries and the World, 2007

(%)

0

10

20

30

40

50

60

Arab Countries

OECD Countries

EmergingEconomies

FSU

1-2-1 Petroleum Products

There was a slowdown in the growth rate of petroleum products’ consumption in the Arab countries in 2008, when it fell to 3.9%, compared with 6.1% in 2006 and 4.2%in 2007. The actual consumption of petroleum products in these countries in 2008 amounted to 5.4 million boe/d, compared with 4.5 million boe/d in 2004. Moreover, the share of petroleum products in total energy consumption in the Arab countries in the period 2004-2008 declined from 54.4% in 2004 to 53.9% in 2008.

The OAPEC members’ share of total petroleum products’ consumption in the Arab countries in 2008 was 87.1%, while that of other Arab countries was 12.9%.

The relative breakdown of petroleum product consumption in the Arab countries in 2007 puts gasoil/diesel in first place with 32.8%, followed by gasoline with 20.3%, and fuel oil in third place with 20.1%. LPG came next with 8.1% of the total, followed by jet fuel with 4.6%, and lastly kerosene with 1.8%.

Crude oil is still used directly as a fuel in power plants and refineries in several Arab countires, accounting for 9.1% of total petroleum products' consumption. Figure (1-19) shows the breakdown of petroleum product consumption in the Arab countries.

Figure 1-19 Breakdown of Petroleum Product Consumption in the Arab Countries, 2008

(%)

Fuel Oil% 20.1

Others% 3.2

Crude Oil% 9.1

Gas Oil/Diesel% 32.8

Jet Fuel% 4.6

Gasoline% 20.3

LPG% 8.1

Kerosene% 1.8

The Arab countries accounted for 6.9% of world oil consumption in 2007, while the OECD countries took a 56.9% share, emerging economies 31.5%, and FSU countries 4.7%. See Figure (1-20).

Figure 1-20 Oil Consumption in the Arab Countries and the World, 2007

(%)

0

10

20

30

40

50

60

Arab Countries

OECD Countries

EmergingEconomies

FSU

1-2-2 Natural Gas

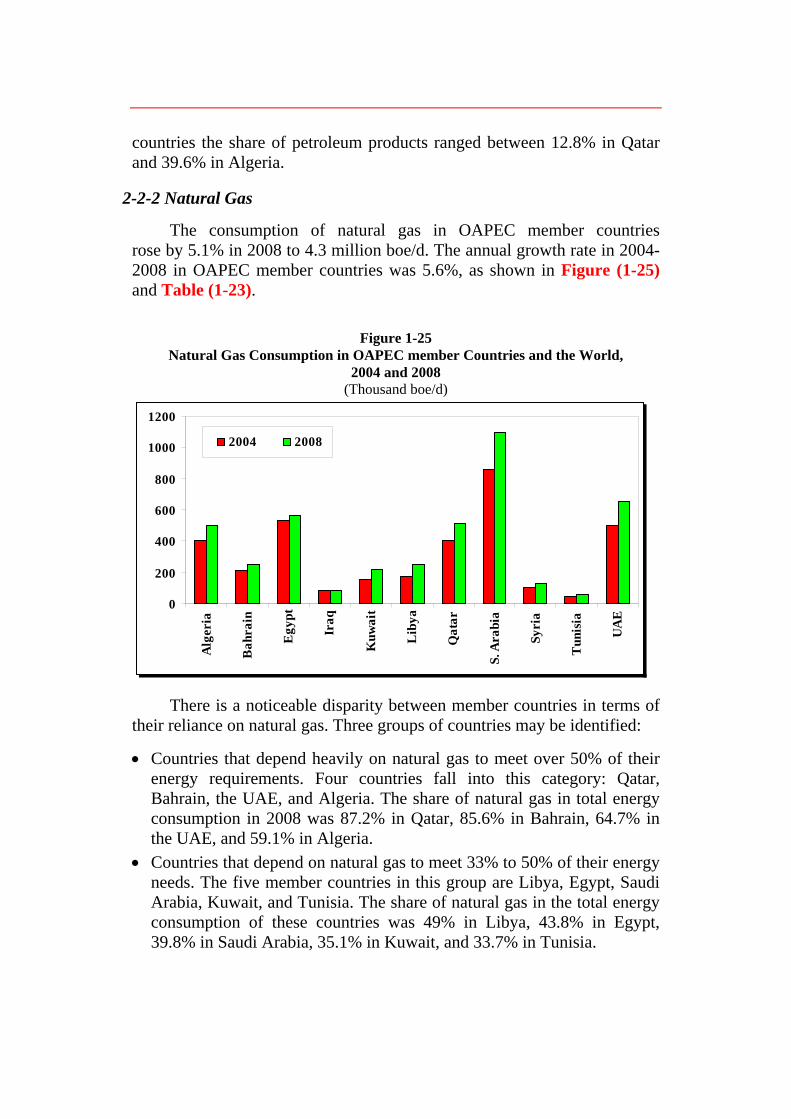

Natural gas is the second biggest source in the energy balances of Arab countries. Owing to the huge efforts they have exerted to expand their

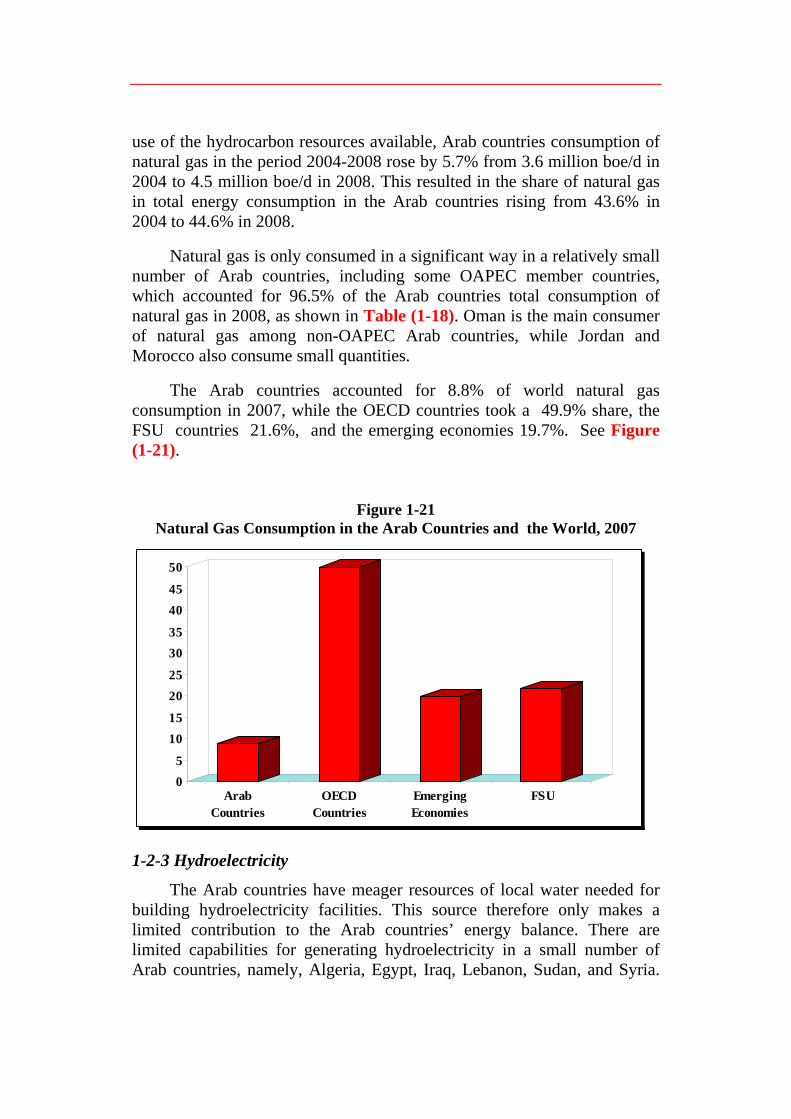

use of the hydrocarbon resources available, Arab countries consumption of natural gas in the period 2004-2008 rose by 5.7% from 3.6 million boe/d in 2004 to 4.5 million boe/d in 2008. This resulted in the share of natural gas in total energy consumption in the Arab countries rising from 43.6% in 2004 to 44.6% in 2008.

Natural gas is only consumed in a significant way in a relatively small number of Arab countries, including some OAPEC member countries, which accounted for 96.5% of the Arab countries total consumption of natural gas in 2008, as shown in Table (1-18). Oman is the main consumer of natural gas among non-OAPEC Arab countries, while Jordan and Morocco also consume small quantities.

The Arab countries accounted for 8.8% of world natural gas consumption in 2007, while the OECD countries took a 49.9% share, the FSU countries 21.6%, and the emerging economies 19.7%. See Figure (1-21).

Figure 1-21 Natural Gas Consumption in the Arab Countries and the World, 2007

05

1015

2025

3035

4045

50

Arab Countries

OECD Countries

EmergingEconomies

FSU

1-2-3 Hydroelectricity

The Arab countries have meager resources of local water needed for building hydroelectricity facilities. This source therefore only makes a limited contribution to the Arab countries’ energy balance. There are limited capabilities for generating hydroelectricity in a small number of Arab countries, namely, Algeria, Egypt, Iraq, Lebanon, Sudan, and Syria.

Initial estimates show that the hydroelectricity production and consumption in these countries were stable in the period 2004-2008 at about 136,000 boe/d. The share of hydroelectricity in total Arab energy consumption declined from 1.65% in 2004 to 1.35% in 2008.

The Arab countries accounted for 0.8% of total world hydroelectricity consumption in 2006, while the emerging economies accounted for 49.5%, the OECD countries for 41.7%, and the FSU countries for 8%.

1-2-4 Coal

Coal resources are only found in a small number of Arab countries, namely, Algeria and Egypt, which are OAPEC members, and Lebanon and Morocco, which are not. Even in these four countries, coal makes a limited contribution to the energy balance, with an estimated total consumption of about 24,700 boe/d in 2008, compared with 23,100 boe/d in 2004. Its share of total energy consumption in the Arab countries declined from 0.29% in 2004 to 0.25% in 2008. The Arab countries accounted for 0.1% of world coal consumption in 2007, while the emerging economies accounted for 57.4%, the OECD countries for 37.3%, and the FSU countries for 5.2%. 2. Total Energy Consumption in OAPEC Member Countries

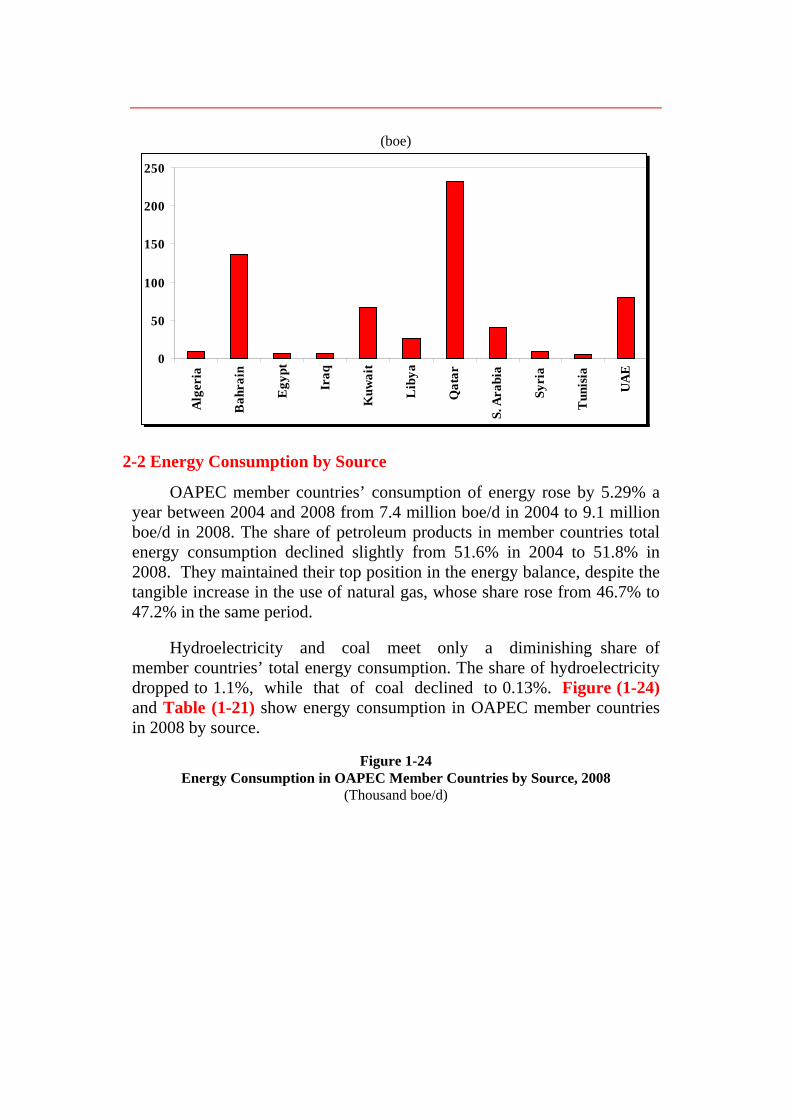

2-1 Total and Per Capita Energy Consumption

Initial estimates indicate that energy consumption in OAPEC member countries in 2008 rose by 4.5% to about 9.1 million boe/d, although the annual rate of growth in 2004-2008 was 5.3%.

There was a marked difference between OAPEC member countries in terms of energy consumption. Three groups may be identified: 1. Five members with a growth rate of over 6%, namely, Libya (8.7%),