Oregon's Timber History

14

Historical Look at Oregon’s Wood Products Industry September 2017 Oregon Office of Economic Analysis

-

Upload

oregon-office-of-economic-analysis -

Category

Economy & Finance

-

view

4.156 -

download

0

Transcript of Oregon's Timber History

Historical Look at Oregon’s Wood Products Industry

September 2017

Oregon Office of Economic Analysis

Oregon Office of

Economic Analysis2

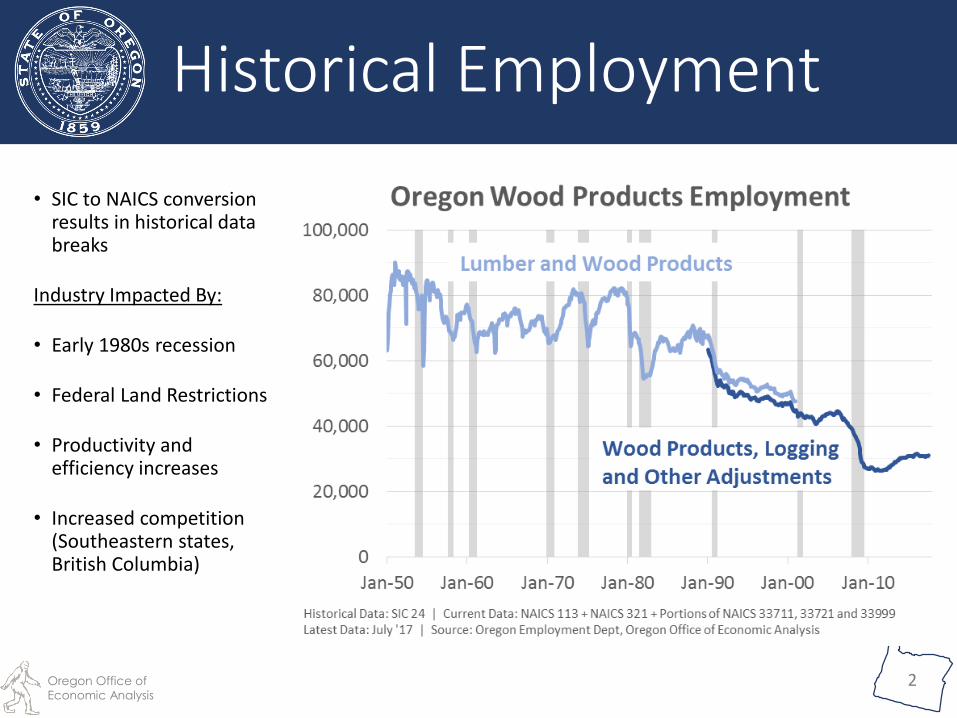

Historical Employment

• SIC to NAICS conversion results in historical data breaks

Industry Impacted By:

• Early 1980s recession

• Federal Land Restrictions

• Productivity and efficiency increases

• Increased competition (Southeastern states, British Columbia)

Oregon Office of

Economic Analysis3

Oregon Wood Products Employment

Data Not Perfectly Compatible: 1978 Lumber and Wood Products (SIC 24), 2015 Wood Products + Logging (NAICS 321, 113)Source: Oregon Employment Department, Oregon Office of Economic Analysis

1978: 81,400

500 - 1,000

> 5,000

3 – 5,000

1 - 3,000

200 - 500

< 200

No Data

2016: 29,000

Number of Jobs

County Employment

Oregon Office of

Economic Analysis4

Oregon Wood Products EmploymentShare of All Private Sector Jobs

Data Not Perfectly Compatible: 1978 Lumber and Wood Products (SIC 24), 2015 Wood Products + Logging (NAICS 321, 113)Source: Oregon Employment Department, Oregon Office of Economic Analysis

1978: 10.2%

> 33%

20 – 33%

10 – 20%

2 – 10%

< 2%

No Data

2016: 1.9%

Share of County Employment

Oregon Office of

Economic Analysis5

Share of State GDP

• Industry output has actually held steady since mid-1970s

• However, other Oregon industries(especially high tech) have grown substantially

• Thus, Wood Products’ share of state GDP continues to decline

Oregon Office of

Economic Analysis6

Harvest: Back to the Future

• Timber harvest increasedsubstantially beginning during the Great Depression

• Harvest levels held steady through the mid-70s

• Following federal restrictions, harvest declined dramatically in the 1990s

Oregon Office of

Economic Analysis7

Changes in Harvest

• Biggest change in Oregon’s timber harvest has been the decreased logging on federal lands, particularly since the late 1980s

• Private land harvests have fallen some over time

• Harvests on state and local lands has increased in recent decades, but remain a small portion of the market

8

Federal Payments to Counties Decline

• Since 1908

counties

received 25% of

sales

• Secure Rural

Schools and

Community Self-

Determination

Act of 2000

• Continued for 4

years at

declining levels,

included in

ARRA

Oregon Office of Economic Analysis

$0

$100

$200

$300

$400

$500

1986 1990 1994 1998 2002 2006 2010

Mill

ions

Fiscal Year

Timber Payments

OWL

25% Fund (FS)

Secure Rural Schools

Mineral

BLM

PILT

Chart not updated

Oregon Office of

Economic Analysis9

Flat Wages, Falling Premium

• Timber-related jobs used to be great,paying a 30%+ premium compared to the average industry

• Total industry wages accounted for 13% of statewide wages, approx. the same as High-Tech today

• Automation and industry decline led to stagnant wages

• Industry jobs today are middle-wage, not low-wage, but no wage premium remains relative to statewide average

Oregon Office of

Economic Analysis10

Increased Competition for Scarce Supply of Logs

• Chinese demand for NW logs didn’t really used to exist

• Following recession and Russian tariffs, Chinese sought out other log sources

• Impact raises log prices (good for landowners, bad for mills facing weak domestic housing demand for finished goods)

• Chinese demand has ebbed some, but remains

• Of course, would love to export finished lumber, not raw logs

Oregon Office of

Economic Analysis11

• In recent years, Pacific Northwest mill margins under pressure from both sides. High log prices due to low harvest levels and increased competition from China for raw logs. Weak domestic demand and increased Canadian exports hold down final prices.

• Under either a tariff or another softwood lumber agreement, it should help Pacific Northwest mills with pricing power• Better margins for mills, supporting their operation, but also higher

consumer prices

• Some of this pricing power will flow to land owners. At higher lumber prices, mills can afford to pay more for logs, thus raising or at least supporting log prices too.

• Higher log prices should result in higher private land harvest levels. Unclear how much. Economic impact likely smallish.

• The tariff (if it sticks) or a SLA may help Northwest mills some, but it cannot solve their biggest obstacle: raw logs

Canadian Tariff

Oregon Office of

Economic Analysis12

•During the 1940s-1970s the industry employed 70,000+ workers and paid 30% above the state average

•Events with significant impact:•Early 1980s recession, industry restructuring,

Federal Land restrictions, increased competition from Southeastern U.S. and British Columbia, increased productivity and mechanization

•Today there are about 30,000 jobs that pay the state average

Conclusion

Oregon Office of

Economic Analysis13

Finally, Quality of Life vs Economic Performance

• The Timber Belt suffered economic shock as bad as the Rust Belt, the Corn Belt or old textile mills across the South

• As jobs disappeared, people moved away from those other locations

• In the Timber Belt, people kept moving in

For more: https://oregoneconomicanalysis.com/2015/04/28/the-timber-belt/

Oregon Office of

Economic Analysis14

(503) 378-4052

www.OregonEconomicAnalysis.com

@OR_EconAnalysis

Questions and Contact