Opportunity Day Q2/2021 Operating Results

40

World’s Greenergy Icon Evolving the world through the greener ways 1 Opportunity Day Q2/2021 Operating Results 27 August 2021 Ticker: BCPG (SET)

Transcript of Opportunity Day Q2/2021 Operating Results

World’s Greenergy IconEvolving the world through the greener ways 11

Opportunity DayQ2/2021 Operating Results27 August 2021Ticker: BCPG (SET)

2Q21 Highlights

The project had already become the first renewable energy project in Thailand to deploy an energy storage system (ESS) as the solution to the intermittency of wind power and was selected as an ERC Sandbox Project.

Lom Ligor Wind Farm won “Battery Storage Deal of The Year” at the Triple A Infrastructure Asset Awards 2021

Impressive recurring earnings growth from Hydropower projects

33.6%

Strong revenue contribution from Hydropower project in Lao PDR named “Nam San 3A” and “Nam San 3B” owing to higher rainfall.

Assigned credit rating of A- by TRIS Rating with a stable outlook and issue rating of A-

Credit rating “A-” with Stable Outlook”

Issue rating of “A-” in senior unsecured debentures

Entering high season

High season

Efficiency improvement scheme to solar projects in Thailand

Improved efficiency to 3 solar projects in Thailand to enhance revenue contribution and projects return.

Efficiency improvement by installed tracking system and change PV module.

2

Forecast capacity factor of Nam san 3A and Nam

San 3B

…. And new investments followed by

3

Monsoon Wind power projectInstalled capacity: 600MWEquity capacity: 270MWHolding (%): 45%COD: 2025

VRB® Energy is a global leader in vanadium redox battery- Utility scale- Long life cycle- Scalability / Flexibility- Depth of discharge- Safety- Recyclable

✓ ✓

New Investments in pipeline

Monsoon Signed PPA with EVN Investment in VRB Energy

4

Key developments

Performance & Guidelines

Agenda

Portfolio & Pipelines

5

Key developments

Performance & Guidelines

Agenda

Portfolio & Pipelines

6

860.0 MWppa

165.8 MW 10.0 MW

THAILAND

Operating Developing

157.5 MW 24.0 MW

INDONESIA

Operating Developing

14.4 MW 5.6 MW

THE PHILIPPINES

Operating Developing

14.7 MW 75.0 MW

JAPAN

Operating Developing

114.0 MW

LAOS TO VIETNAM

Unit: Contracted capacity or equity MWppa

9.0 MW

475.4 384.6

Operating Developing

270.0 MWDevelopingOperating

Business footprints in 5 countries in Asia

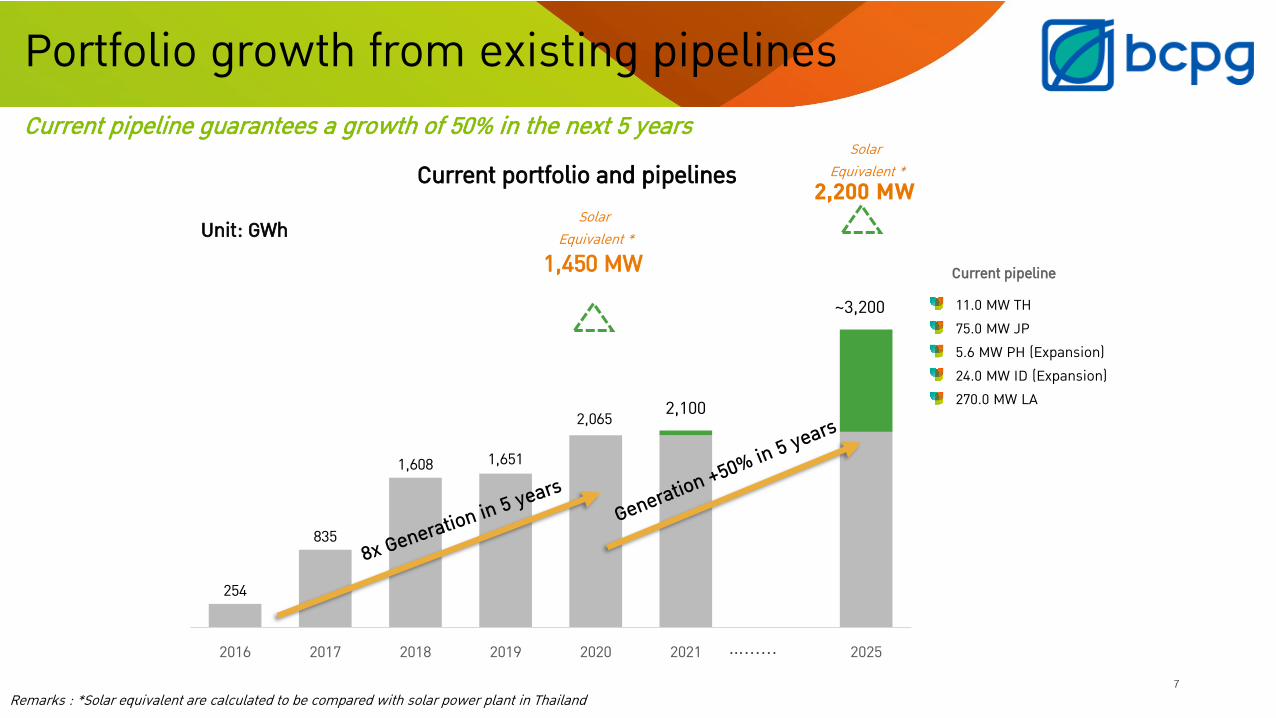

254

835

1,608 1,651

2,065

2016 2017 2018 2019 2020 2021 20257

…......

Remarks : *Solar equivalent are calculated to be compared with solar power plant in Thailand

Unit: GWh

Current portfolio and pipelines

Current pipeline guarantees a growth of 50% in the next 5 years

Solar Equivalent *

11.0 MW TH75.0 MW JP 5.6 MW PH (Expansion)24.0 MW ID (Expansion)270.0 MW LA

Current pipeline1,450 MW

2,200 MWSolar

Equivalent *

Portfolio growth from existing pipelines

2,100

~3,200

50%

25%

25%

DevelopingMature

Frontier

158

114

249

300

Target PortfolioMix

Future Project

Target PortfolioMix

2025F

Balancing our portfolio risk appetite

Technology mix can be flexible given dynamic environment and availability of potential projects

Portfolio mix design based on risk appetite and mitigation capability

Concentrate in matured and developing countries to balance our portfolio risk appetite

Operating – Quick win to generate immediate contributionGreenfield – Assurance to medium and long term growth

Geog

raph

ies

Maintain focus on clean energy, with endeavor in advanced technologies like ESS & Digital Energy

Tech

nolo

gies

Inve

stm

ent S

tage

9

Expanding through organic and inorganic growthto sustain growth after end of government subsidization

Remark:Matured Countries : Fitch’s Rating “A” and aboveDeveloping Countries : Fitch’s Rating Between “B” and “BBB+”

“Accelerating growth by focusing on large scale projects”

1010

VRB® Energy is a global leader in vanadium redox battery

MW & GW-class are available

VRB Energy: Footprint to ESS business

11

Key developments

Performance & Guidelines

Agenda

Portfolio & Pipelines

12

Lao: Hydropower PlantNam San 3A & 3B Hydro Power Plants (Run-of-the-river)

Projects: Nam San 3A Nam Sam 3B Total

Installed MW 69 MW 45 MW 114 MW

Holding (%): 100%

COD: 29 Jan 2016 25 Sep 2015

Acquisition Date: 20 Sep 2019 26 Feb 2020

Investment: USD 173.2 mn(THB 5,326 mn)

USD113.2 mn(THB 3,581 mn)

USD 286.4 mn(THB 8,907 mn)

PPA: Laos Terms: 27 years from COD (2015 – 2042)Tariff: 6.72 Uscent/kWh (2020)Take-or-pay: 95%Currency: 90% USD/10% KIP

PPA: Vietnam Terms: 25 years from COD ([2022] – 2047)Tariff: 6.95 Uscent/kWhTake-or-pay: 90%Currency: 100% USD

Location: Xiengkhouang, Laos PRD

Capacity Factor: 44% - 47% (Q3 66% - 75%)Range capacity factor after acquisition since Sep 2019

Nam San 3A 69 MWOperating

Nam San 3B 45 MWOperating

Transmission LineDeveloping

Thailand

Cambodia

Vietnam

32 1

Laos

220kV Transmission line>500 MW capacity

1

2

3

Northern Region

Developing: 0.0 MWOperating: 114.0 MW

Hold: 100.0%

Subsidiaries

13

220 kV transmission line

Transmission line 3A & 3B: LA-VNMilestones tracking to be COD within 2022

1

Substation construction2

Switching station at border3

79 km Transmission Line

BorderNam San 3A

Nam San 3B

1

2 3

Foundation excavation

Steel binding Framework installationConcrete pouring Foundation

Land preparation & substation foundation work

Overall construction progress as plan at 44% completed.

Tower

Nam San 3A & 3B HPP milestones

Prime Minister’s Approval

PPA signed with EVN

- Acceptance of Grid Study- Tariff Negotiation Range- Project Timeline

- Inclusion of Energy Import into VN’s PDP - Construction of transmission line in VN- COD by 2022- Tariff Ceiling Price

- Signing of Definitive PPA and other ancillary agreements

3 steps of PPA issuance process completed, transmission line is well under wayCross-border PPA milestones: Hydropower

23

Jan-20

14

Tariff MOU: Hydropower✓

✓

✓

1

Switc

h of

f-tak

er to

EV

N wi

thin

2022

Transmission line construction

15

Laos: Wind Power Plant

Monsoon Wind Power Plant Installed MW 600 MW

Equity MW 270 MW

Holding (%): 45%

Area Exploration area of over 425,000 rais

Status Advanced DevelopmentMet mast installed >3 yearsPPA signed in July 2021

COD: 2025

Location: Attopu, Lao PRD

Capacity Factor: Est. 33%

Leverage (D:E) [70:30]

Thailand

Cambodia

Vietnam

Project Area

Laos

Large scale development, with cross-border PPA

16

Lao-VN 600MW Wind Farm milestones

Cross-border milestones: Wind farm

Project and transmission line construction

16

Financial close

- Financing in place

To b

e CO

D wi

thin

2025

Prime Minister’s Approval

- Acceptance of Grid Study- Tariff Negotiation Range- Project Timeline

- Inclusion of Energy Import into VN’s PDP - Construction of transmission line in VN- COD by 2023- Tariff Ceiling Price

Tariff MOU: Wind Farm

PPA signed with EVN EPC Selection

- Final negotiation with EPC bidders

✓

Jul-2021

1

2

34

✓

✓Aug-2020

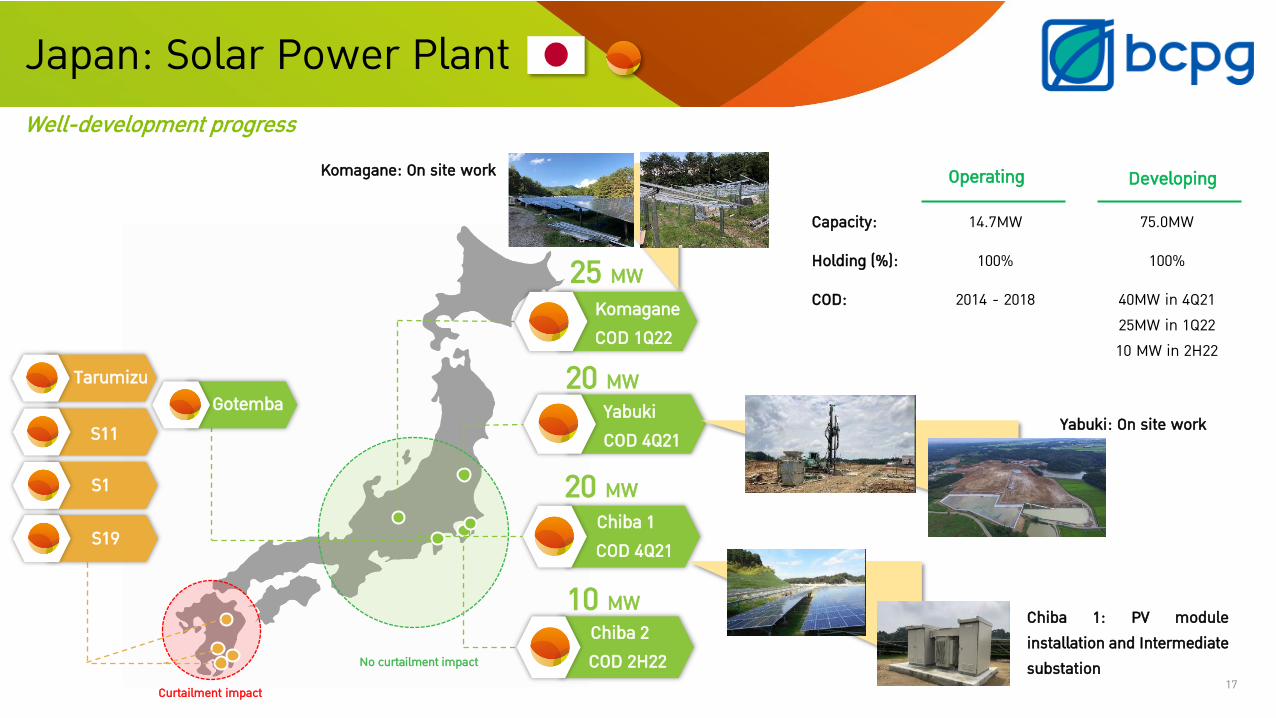

Japan: Solar Power Plant

Operating

Capacity: 14.7MW 75.0MW

Holding (%): 100% 100%

COD: 2014 - 2018 40MW in 4Q2125MW in 1Q22 10 MW in 2H22

Developing

25 MW

20 MWYabukiCOD 4Q21

Chiba 1COD 4Q21

Chiba 2COD 2H22

20 MW

10 MW

S1

S19

S11

TarumizuGotemba

KomaganeCOD 1Q22

Curtailment impact

No curtailment impact

Well-development progress

Chiba 1: PV module installation and Intermediate substation

Yabuki: On site work

17

Komagane: On site work

18

Efficiency Improvement of 15 MW of Solar THOpportunity to enhance efficiency of 15MW solar TH

No. Projects LocationTariff Power

StructureContracted

Capacity (MW)COD

1 RPV Energy KanchanaburiAdder THB

8/kWh

5.015/10/12

2 JKR Energy Kanchanaburi 5.0

3 Lopburi Solar Lopburi 5.0 4/2/14

4 Prachinburi Solar Prachinburi FiT: THB 5.66/kWh 5.0 30/12/16

1-23

4

Efficiency improvement by installed tracking system and change PV

module for “Better operating performance”

Lopburi SolarEfficiency improvement COD: 18 May 2021

RPV & JKREfficiency improvement COD: 3 June 2021

19

Key developments

Performance & Guidelines

Agenda

Portfolio & Pipelines

20

2Q21 QoQ YoY 1H21 YoY 2Q21 YoY

EBITDA 992.1 +4.7% +15.4% 1,940 15.2% MW 475.4 +5.1%

Core profit 503.9 +3.1% +33.6% 992.8 27.1% D/E 1.1 -0.4

Unit: THB mn

YoY

(+) Full quarter contribution from 4 new solar power projects in Thailand (20MW) and higher revenue contribution from hydropower projects, owing to higher rainfall. (+) Higher share of profit from both geothermal power plants in Indonesia and wind power plant in Philippine.

Key Takeaway

Financial highlights for 2Q21Core profit grew YoY and QoQ

QoQ

(+) Higher revenue contribution from hydropower projects (entering high season) and solar projects in Japan (better irradiation).(+) Higher share of profit from geothermal power plants in Indonesia thanks to lower shutdown days.

YoY

(+) Full 6-month of revenue contribution from new projects including hydropower project, “Nam San 3B” and the 4 new solar power projects in Thailand (20MW). (+) Higher revenue contribution from hydropower project in Lao PDR, owing to higher rainfall. (+) Higher share of profit from both geothermal power plants in Indonesia and wind power plant in Philippines.

Developing: 0.0 MWOperating: 9.0 MW

Hold: 100.0%

Subsidiaries

Developing: 11.0 MWOperating: 164.2 MW

Hold: 100.0%

Subsidiaries

TH performanceTH revenue growth YoY was backed by better performance of solar and wind projects.

21

Unit: GWh Unit: GWh

Power generation & Capacity factor (%)

In 2Q21, solar revenue increased YoY from the full quarter contribution of the 4 new solar power plants (20MW) but decreased QoQ following the drop in capacity factor. For 1H21, solar revenue increased YoY from the contribution of the 4 new solar power plants (20MW).

Revenue (TH) Unit: THB million

TH revenue grew YoY, driven by the increase in solar and wind revenue but dropped QoQdue to the decrease in solar and wind revenue.

In 2Q21, wind revenue rose YoY from higher wind speed at the project. However, wind revenue declined QoQ due to entering low season.For 1H21, wind revenue rose YoY from higher wind speed at the project.

Solar Wind

LA Performance

22

LA revenue grew YoY from higher rainfall and QoQ from entering high season.

Unit: GWh

2Q21 electricity generation grew YoY. “Nam San 3A” and “Nam San 3B” capacity factor was 41% thanks to higher rainfall.Also, 2Q21 electricity generation rose QoQ owing to seasonal factor of hydro power plants.For 1H21, electricity generation enhanced YoY from the full 6-month recognition of “Nam San 3B” and higher capacity factor from higher rainfall.

Unit: THB millionRevenue (LA) Power generation & Capacity factor (%)

Developing: 0.0 MWOperating: 114.0 MW

Hold: 100.0%

Subsidiaries

LA (Hydro)

Developing: 75.0 MWOperating: 14.7 MW

Hold: 100.0%

Subsidiaries

JP performance

23

JP revenue rose QoQ from favorable weather condition but dropped YoY due to lower irradiation.

Unit: THB million

2Q21 electricity generation dropped YoY due to lower irradiation.However, 2Q21 electricity generation increased QoQ from higher irradiation from favorable weather condition compared to winter season in Q1/2021 (low season). For 1H21, electricity generation rose YoY from better irradiation.

Unit: GWh

Subsidiaries

Power generation & Capacity factor (%) Revenue (JP)

Developing: 24.0 MWOperating: 157.5 MW

Hold: 33.3%

Associates

ID PerformanceGeothermal power plants in Indonesia

24Remark: *Generation based on holding percentage

Share of profit improved both YoY and QoQ.

Unit: GWh

Power generation & Capacity factor (%)

Unit: THB million

In 2Q21, the improvement YoY came from higher tariff, increase in electricity generation and lower finance cost. Meanwhile, the increase QoQ resulted from lower shutdown days. For 1H21, the increase YoY came from higher tariff rate and lower finance cost.

Amortization (96.5) (90.8) (95.1) (190.9) (185.9)

One-time items* - - - (66.7)* -

Net share of profit 117.6 121.5 152.6 251.5 274.0*Including Tax provision THB 23.9 mn and Allowance for account receivable THB 42.8 mn in 1Q20.

Share of profit

Developing: 5.6 MWOperating: 14.4 MW

Hold: 40.0%

Associates

PH PerformanceWind power plant in the Philippines

25

Growth YoY was supported by higher wind speed and tariff escalation.

Remark: *Generation based on holding percentage

Unit: GWh

Amortization (8.2) (7.7) (8.1) (16.3) (15.8)

One-time items - - - - -

Net share of profit (15.1) 19.0 4.5 9.1 23.5

2Q21 Electricity generation rose YoY from higher wind speed. Also, tariff escalation for Jan – May 2021 has been recently approved. However, 2Q21 Electricity generation dropped QoQ due to entering low season.For 1H21, electricity generation increased YoY from higher wind speed and approved tariff escalation for Jan – May 2021.

Unit: THB million

Power generation & Capacity factor (%) Share of profit

Remark: EBITDA from operation including share of profit from associates (after amortization and before one-time items)

Revenue and EBITDA grew YoY and QoQ.

26

EBITDA (Incl. shares of profit)

EBTIDA growth YoY and QoQ followed the increase of operating revenue and share of profit. For 1H21, EBITDA increased YoY in line with revenue growth and share of profit growth.

Financial Performance: Revenue & EBITDA

2Q21 revenue grew YoY from the increase in TH and LA revenue. Meanwhile, 2Q21 revenue increased QoQ from the increase in JP and LA revenue. For 1H21, revenue rose YoY thanks to the increase in TH, JP and LA revenue.

Unit: THB millionUnit: THB millionRevenue

27

Unit: THB million

IBD breakdown by maturity IBD breakdown by currency IBD breakdown by Fixed-Floating rate

Cost of debt (Kd) was lower YoY thanks to declining of market interest rate resulted in floating rate loan (majority portion) had lower finance cost and partial loan repayment.

Finance cost and Kd (%)

Remark: The average finance costs calculated by a simple average method.

Kd reduction YoY from benefit of floating portion after market rate decline

Finance cost

28

2Q21 core profit grew YoY and QoQCore profit & Core profit margin (%)

Remark: Core profit equals to net profit minus FX gain/loss and one-time items

Unit: THB million

Net profit & Net profit margin (%)

Core profit & Net profit

Unit: THB million

2Q21 core profit growth YoY and QoQ was mainly driven by revenue growth and share of profit growth. For 1H21, core profit improved from the recognition of 6-month contribution from the new projects, better contribution from existing power plants and receiving tariff escalation.

2Q21 net profit increased YoY and QoQ, mainly came the improvement of core profit as mentioned. Also, there was FX gain of THB 80.3 million in 2Q21, compared to FX loss of THB 98.4 million in 2Q20 and FX gain of THB 22.7 million in 1Q21. For 1H21, FX gain was THB 103.0 million compared to FX gain of THB 226.8 million in1H20. As a result, net profit growth was slightly lower than core profit growth.

29

Total assets

D/E ratio below covenant level

Financial position

Remark: Dividend policy = not less than 40% of the Company’s net profit based on separated yearly Financial Statement

Covenant = 3.0x

2021 Dividend Payment

D/E Ratio Credit Rating

Period Per share (THB) Amount (THB mn)

1H21 0.16 434

Payout Ratio 40.0%

Credit rating “A-” with Stable Outlook”

Issue rating of “A-” in senior unsecured debentures

30

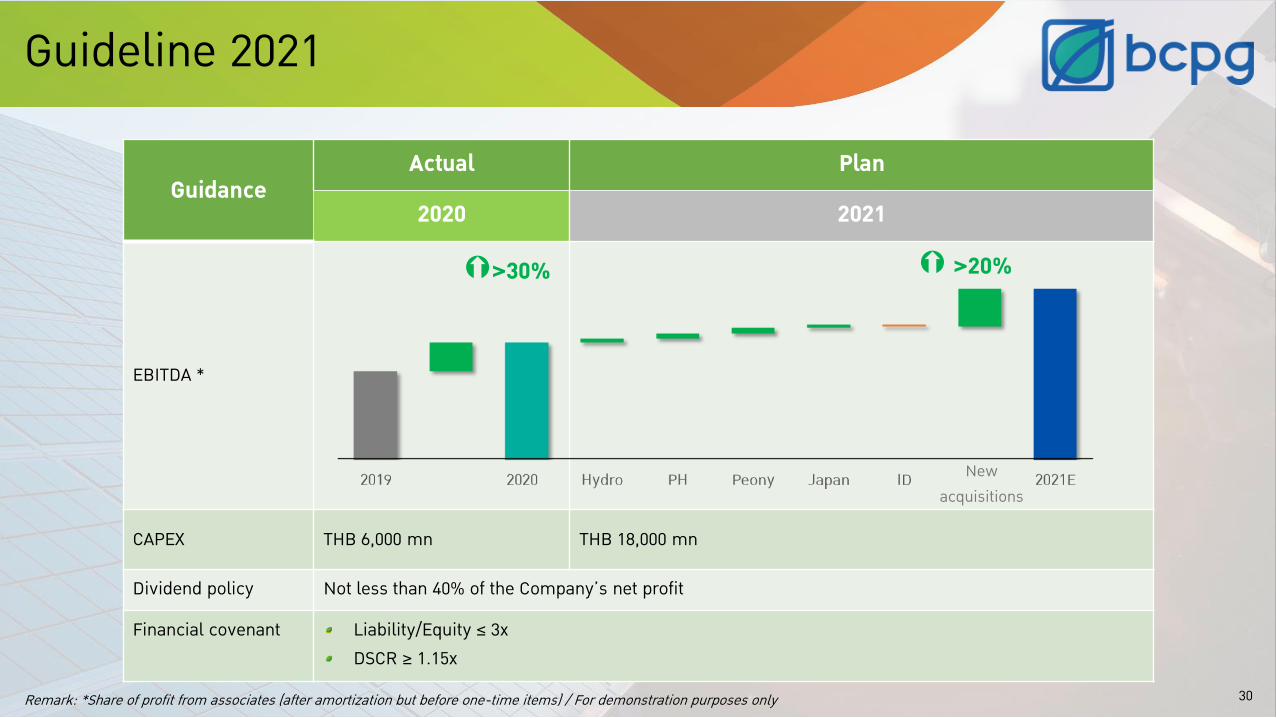

GuidanceActual Plan

2020 2021

EBITDA *

CAPEX THB 6,000 mn THB 18,000 mn

Dividend policy Not less than 40% of the Company’s net profit

Financial covenant Liability/Equity ≤ 3xDSCR ≥ 1.15x

Remark: *Share of profit from associates (after amortization but before one-time items) / For demonstration purposes only

Guideline 2021

>20%

New acquisitions

>30% >20%

31

Q&A

32

Financial Statement

Unit: THB million 2Q20 2Q21 ∆ (%) 1Q21 ∆ (%) 1H20 1H21 ∆ (%)

Revenue from sale and redering of service 969.6 1,088.2 12.2% 1,046.6 4.0% 1,856.0 2,134.9 15.0%Cost of sale and rendering of services (358.1) (396.1) 10.6% (393.7) 0.6% (667.0) (789.7) 18.4%Administrative expenses (114.2) (148.9) 30.3% (137.5) 8.3% (261.7) (286.3) 9.4%Operating profit 497.3 543.3 9.2% 515.5 5.4% 927.3 1,058.8 14.2%Share of profit of investment in associates (exlcuding one-time item) 102.4 157.0 53.3% 140.5 11.8% 260.6 297.5 14.2%

EBITDA 860.0 992.1 15.4% 947.9 4.7% 1,684.4 1,939.9 15.2%Other income/(expense) 4.4 15.3 244.0% 24.8 (38.6%) 14.4 40.1 178.1%FX gain/(loss) (98.4) 80.3 NA 22.7 NA 226.8 103.0 NAOther one-time item (1.1) (14.4) 1192.8% 6.9 (309.5%) (70.1) (7.5) (89.3%)EBIT 504.7 781.5 54.8% 710.3 10.0% 1,359.0 1,491.8 9.8%Finance costs (220.3) (192.8) (12.5%) (185.5) 3.9% (407.9) (378.3) (7.3%)EBT 284.4 588.8 107.0% 524.8 12.2% 951.1 1,113.6 17.1%Income tax (expense) benefit 70.4 (23.9) NA (1.6) NA (22.7) (25.5) NAMinority interest 0.0 0.2 NA 0.2 NA (0.0) 0.3 NANet profit 354.8 565.1 59.3% 523.4 8.0% 928.5 1,088.4 17.2%Recurring profit * 377.1 503.9 33.6% 488.8 3.1% 780.8 992.8 27.1%Basic Earnings per Share (THB) 0.18 0.21 16.7% 0.20 5.0% 0.46 0.41 (10.9%)Remark:*Excluding gain/(loss) on FX and one-time items

33

Financial StatementUnit: THB million 2020

% of total assets

2Q21 % of total

assets ∆ (%)

Cash and cash equivalents 11,138.3 21.7% 6,297.6 12.2% (43.5%)Current investments 4.6 0.0% 3,000.0 5.8% 65164.2%Trade accounts receivables 1,219.2 2.4% 1,544.9 3.0% 26.7%Other current assets 130.9 0.3% 246.7 0.5% 88.5%Total current assets 12,492.9 24.4% 11,089.3 21.4% (11.2%)Investments in associate & subsidiaries 11,722.8 22.9% 12,719.8 24.6% 8.5%Property, plant and equipment 14,667.8 28.6% 15,141.1 29.3% 3.2%Goodwill and Intangible assets 11,313.7 22.1% 11,661.6 22.5% 3.1%Other non-current assets 1,022.4 2.0% 1,151.5 2.2% 12.6%Total non-current assets 38,726.6 75.6% 40,674.0 78.6% 5.0%Total Assets 51,219.6 100.0% 51,763.3 100.0% 1.1%Short-term borrowings from financial institutions 1,770.6 3.5% 0.0 0.0% (100.0%)Current portions of long-term borrowings 1,701.0 3.3% 2,568.7 5.0% 51.0%Long-term borrowings 23,589.7 46.1% 23,593.4 45.6% 0.0%Other liabilities 1,609.3 3.1% 1,477.5 2.9% (8.2%)Total liabilities 28,670.6 56.0% 27,639.6 53.4% (3.6%)Equity attributable to owners of the Company 22,480.1 43.9% 24,055.2 46.5% 7.0%Non-controlling interests 68.8 0.1% 68.5 0.1% (0.5%)Total liabilities and Equity 51,219.6 100.0% 51,763.3 100.0% 1.1%

34

Financial Statement

Unit: THB million 1H20 1H21 ∆ YoYNet cash from (used in) operating activities 1,599.5 1,451.1 (148.4)

Net cash from (used in) investing activities (4,718.2) (4,026.0) 692.2

Net cash from (repay to) financing activities 5,624.5 (2,439.6) (8,064.1)

Net increase in cash and cash equivalents 2,505.8 (5,014.4) (7,520.3)

Cash and cash equivalents at 1 January 1,445.2 11,138.3 9,693.1

Effect of exchange rate changes on balances held in foreign currencies (195.6) 173.8 369.4

Cash and cash equivalents at end period 3,755.5 6,297.6 2,542.2

CAPEX (4,716.6) (966.1) 3,750.5

35

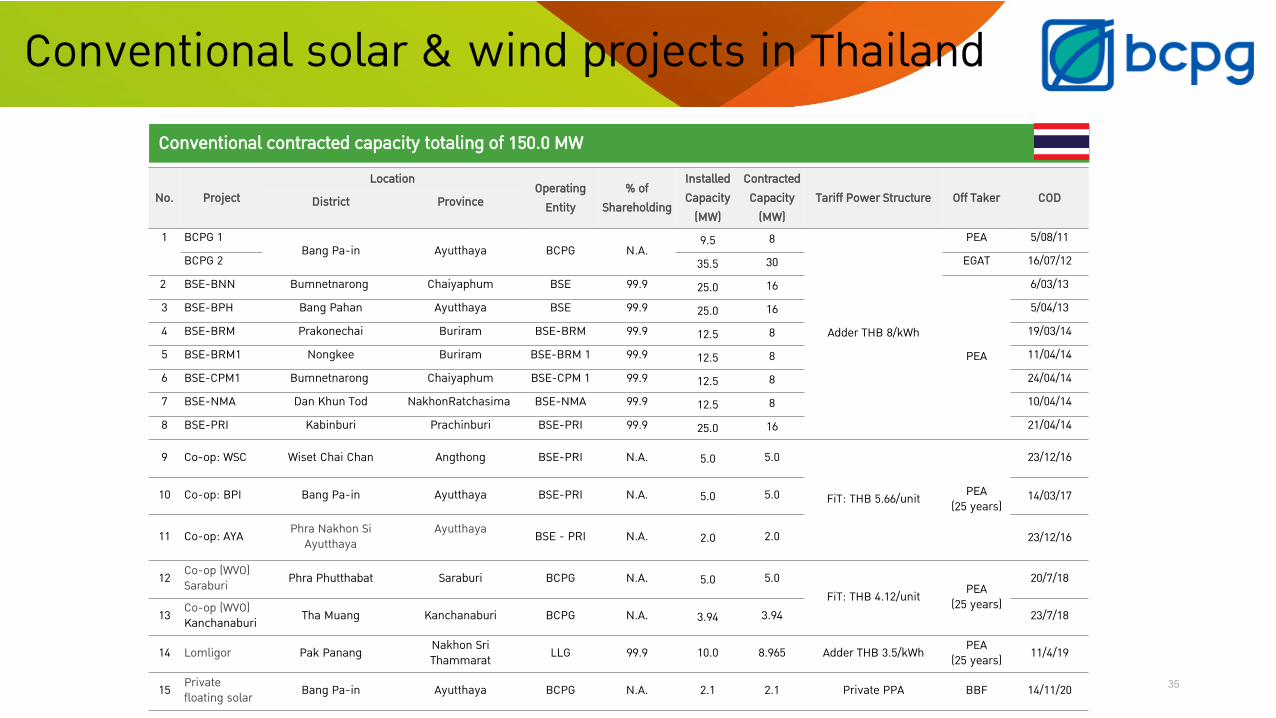

No. ProjectLocation

Operating Entity

% of Shareholding

Installed Capacity

(MW)

Contracted Capacity

(MW)Tariff Power Structure Off Taker CODDistrict Province

1 BCPG 1Bang Pa-in Ayutthaya BCPG N.A.

9.5 8

Adder THB 8/kWh

PEA 5/08/11BCPG 2 35.5 30 EGAT 16/07/12

2 BSE-BNN Bumnetnarong Chaiyaphum BSE 99.9 25.0 16

PEA

6/03/133 BSE-BPH Bang Pahan Ayutthaya BSE 99.9 25.0 16 5/04/134 BSE-BRM Prakonechai Buriram BSE-BRM 99.9 12.5 8 19/03/145 BSE-BRM1 Nongkee Buriram BSE-BRM 1 99.9 12.5 8 11/04/146 BSE-CPM1 Bumnetnarong Chaiyaphum BSE-CPM 1 99.9 12.5 8 24/04/147 BSE-NMA Dan Khun Tod NakhonRatchasima BSE-NMA 99.9 12.5 8 10/04/148 BSE-PRI Kabinburi Prachinburi BSE-PRI 99.9 25.0 16 21/04/14

9 Co-op: WSC Wiset Chai Chan Angthong BSE-PRI N.A. 5.0 5.0

FiT: THB 5.66/unit PEA(25 years)

23/12/16

10 Co-op: BPI Bang Pa-in Ayutthaya BSE-PRI N.A. 5.0 5.0 14/03/17

11 Co-op: AYA Phra Nakhon Si Ayutthaya

Ayutthaya BSE - PRI N.A. 2.0 2.0 23/12/16

12 Co-op (WVO)Saraburi Phra Phutthabat Saraburi BCPG N.A. 5.0 5.0

FiT: THB 4.12/unit PEA(25 years)

20/7/18

13 Co-op (WVO)Kanchanaburi Tha Muang Kanchanaburi BCPG N.A. 3.94 3.94 23/7/18

14 Lomligor Pak Panang Nakhon Sri Thammarat LLG 99.9 10.0 8.965 Adder THB 3.5/kWh PEA

(25 years) 11/4/19

15 Private floating solar Bang Pa-in Ayutthaya BCPG N.A. 2.1 2.1 Private PPA BBF 14/11/20

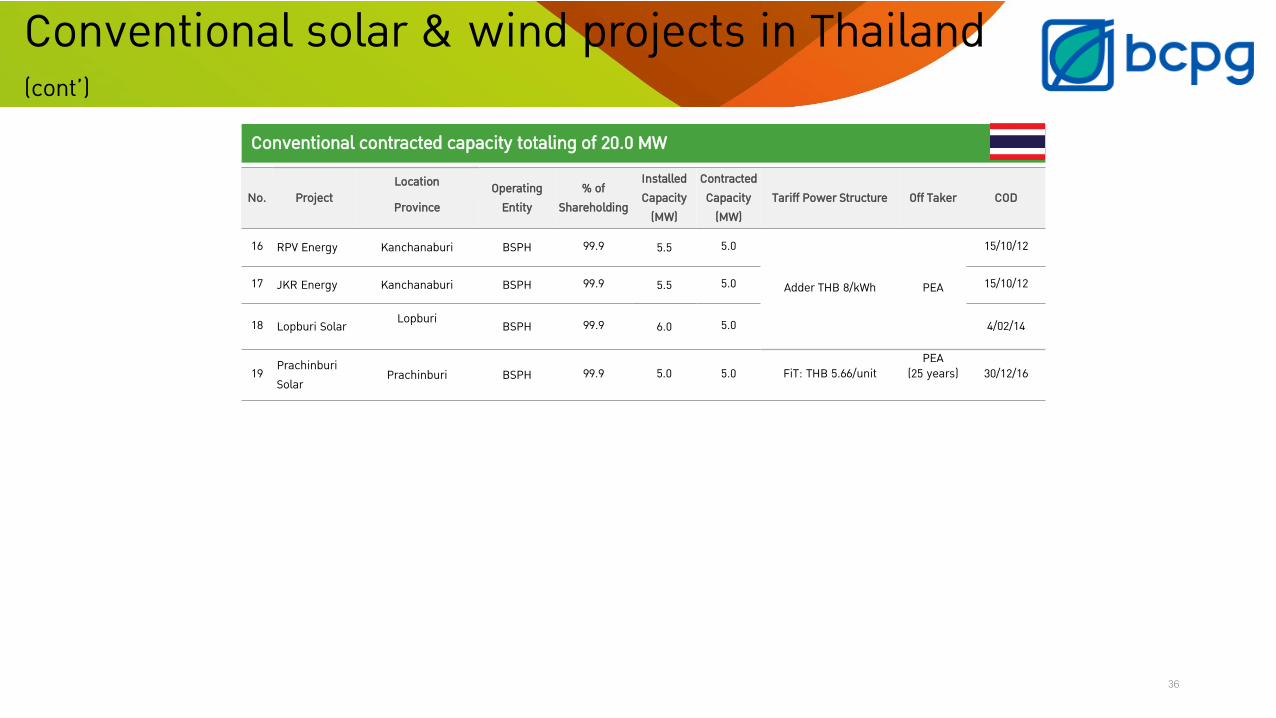

Conventional contracted capacity totaling of 150.0 MW

Conventional solar & wind projects in Thailand

36

No. ProjectLocation Operating

Entity% of

Shareholding

Installed Capacity

(MW)

Contracted Capacity

(MW)Tariff Power Structure Off Taker COD

Province

16 RPV Energy Kanchanaburi BSPH 99.9 5.5 5.0

Adder THB 8/kWh PEA

15/10/12

17 JKR Energy Kanchanaburi BSPH 99.9 5.5 5.0 15/10/12

18 Lopburi Solar Lopburi BSPH 99.9 6.0 5.0 4/02/14

19 Prachinburi Solar

Prachinburi BSPH 99.9 5.0 5.0 FiT: THB 5.66/unitPEA

(25 years) 30/12/16

Conventional contracted capacity totaling of 20.0 MW

Conventional solar & wind projects in Thailand(cont’)

37

Contracted operating capacity of 4.6 MW

# Type Segment Relation-ship

Project Location Contracted Capacity

Terms (year)

Tariff power structure

Status/ COD

1 Rooftop Industrial Subsidiary Kingboard Uthai, Ayutthaya 0.752 MW 20 Private PPA COD 1/12/2018

2Rooftop Commercial Partner

Habito, T77, Sansiri

Wattana, Bangkok 0.053 MW 25 Private PPA COD 12/1/2019

3Rooftop

Commercial/Residential

Partner T77, Sansiri Wattana, Bangkok 0.376 MW 25 Private PPA COD 1/5/2019

4 Rooftop Commercial/Residential

Partner Escape, Sansiri

Lam Luk Ka, Phathum Thani

0.277 MW25 Private PPA COD 1/2/2020

5 Rooftop Industrial Partner PCF, Sansiri Pak Chong, Nakhon Ratchasima

0.063 MW25 Private PPA COD 1/2/2020

6 Rooftop Mix Others Lots Several cities 2.131 MW 15 – 20 Private PPA 4Q20-2Q21

7 Rooftop Commercial Partner (75%)

CMU Mueang, Chiangmai 0.9 MW 20 Private PPA COD 1/7/2020

8 Rooftop Commercial Partner (75%)

CMU Mueang, Chiangmai 8.1 MW 20 Private PPA Under construction

9 Rooftop Mix Others Lots Several cities 2.8 MW 15 – 20 Private PPA Under construction

Other solar rooftop projects in Thailand

38

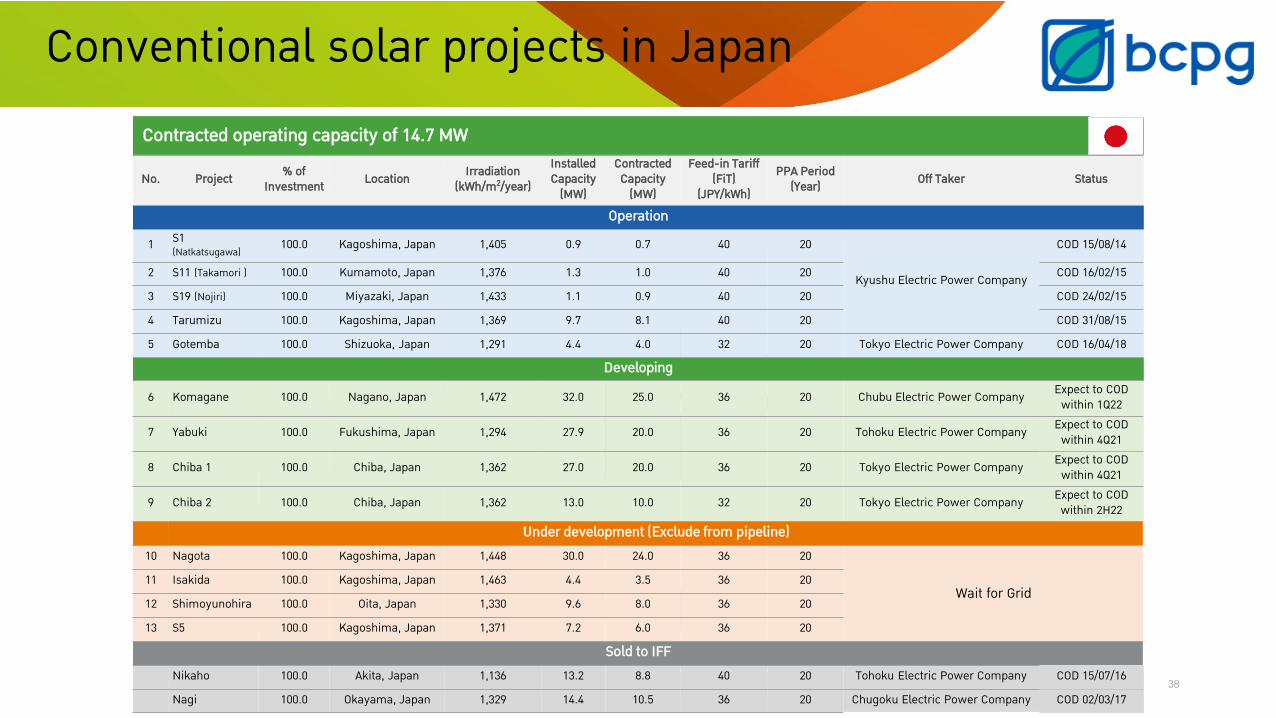

Contracted operating capacity of 14.7 MW

38

No. Project % ofInvestment Location Irradiation

(kWh/m2/year)Installed Capacity

(MW)

Contracted Capacity

(MW)

Feed-in Tariff (FiT)

(JPY/kWh)PPA Period

(Year) Off Taker Status

Operation1 S1

(Natkatsugawa) 100.0 Kagoshima, Japan 1,405 0.9 0.7 40 20

Kyushu Electric Power Company

COD 15/08/14

2 S11 (Takamori ) 100.0 Kumamoto, Japan 1,376 1.3 1.0 40 20 COD 16/02/15

3 S19 (Nojiri) 100.0 Miyazaki, Japan 1,433 1.1 0.9 40 20 COD 24/02/15

4 Tarumizu 100.0 Kagoshima, Japan 1,369 9.7 8.1 40 20 COD 31/08/15

5 Gotemba 100.0 Shizuoka, Japan 1,291 4.4 4.0 32 20 Tokyo Electric Power Company COD 16/04/18

Developing

6 Komagane 100.0 Nagano, Japan 1,472 32.0 25.0 36 20 Chubu Electric Power Company Expect to COD within 1Q22

7 Yabuki 100.0 Fukushima, Japan 1,294 27.9 20.0 36 20 Tohoku Electric Power Company Expect to COD within 4Q21

8 Chiba 1 100.0 Chiba, Japan 1,362 27.0 20.0 36 20 Tokyo Electric Power Company Expect to COD within 4Q21

9 Chiba 2 100.0 Chiba, Japan 1,362 13.0 10.0 32 20 Tokyo Electric Power Company Expect to COD within 2H22

Under development (Exclude from pipeline)10 Nagota 100.0 Kagoshima, Japan 1,448 30.0 24.0 36 20

Wait for Grid11 Isakida 100.0 Kagoshima, Japan 1,463 4.4 3.5 36 20

12 Shimoyunohira 100.0 Oita, Japan 1,330 9.6 8.0 36 20

13 S5 100.0 Kagoshima, Japan 1,371 7.2 6.0 36 20

Sold to IFFNikaho 100.0 Akita, Japan 1,136 13.2 8.8 40 20 Tohoku Electric Power Company COD 15/07/16

Nagi 100.0 Okayama, Japan 1,329 14.4 10.5 36 20 Chugoku Electric Power Company COD 02/03/17

Conventional solar projects in Japan

39

Public

BSE BSE-BRM BSE-BRM1 BSE-CPM1 BSE-NMA BSE-PRI LLG TDED

Thailand

Singapore

99.9% 99.9% 99.9% 99.9% 99.9% 99.9% 99.9% 75.0%

BSEH

100.0%

BCPGI SEGHPL

GreenergyHoldings

GreenergyPower BCPG Wind

100.0% 100.0% 100.0%The Netherlands

JapanPetrowind

Energy

The Philippines 40.0%HMJ BCPGJ

EPC(1) AM(2) Investment(3) Project Under Development

Operating Projects

Operating Projects

Operating Projects

100.0% 100.0%

100.0% 51.0% 100.0% 100.0% 100.0% 100.0%

100.0%

(1) EPC = Groups of companies doing such business as (1) a turnkey EPC contractor and (2) an operation and maintenance contractor for solar power plants in Japan(2) AM = an Asset Management company rendering operation and maintenance service for the Tiramizu project and its remaining shares of 49.0% are held by a juristic person (3) Investment = companies investing in solar farms in Japan as TK investor

Laos

BCPGIndochina

99.9%

Nam San 3A

100.0%

IDO(New SG)

100.0% 33.33%

Nam San 3B

100.0%

Monsoon100.0%

Group’s Business Structure

RPV

99.9%

JKRAQU

LS PS

99.9%99.9%

99.9% 99.9%

BSPH

99.9%

CDC

60.0%

Hong Kong 45.0%

IEAD

100.0%

40Survey link