OOG Restructuring · operate the PLSV Polar Onyx with Ceona 2015 - today OOG is provisionally...

65

OOG Restructuring May 2017 CONFIDENTIAL SETTLEMENT COMMUNICATION SUBJECT TO FRE 408

Transcript of OOG Restructuring · operate the PLSV Polar Onyx with Ceona 2015 - today OOG is provisionally...

OOG Restructuring

May 2017

CONFIDENTIAL SETTLEMENT COMMUNICATION SUBJECT TO FRE 408

The material that follows is a confidential presentation of general background information about Odebrecht Óleo e Gás S.A. and

certain of its subsidiaries and joint venture projects (together, the “Company”) as of the date of this material. This material has

been prepared solely for informational purposes. This presentation is not an offer with respect to any securities or a solicitation of

votes to accept a plan of reorganization within the meaning of the U.S. Bankruptcy Code. Any such offer or solicitation will comply

with all applicable securities laws and/or provisions of the U.S. Bankruptcy Code.

No representation or warranty, express or implied, is made by the Company or any of its affiliates or representatives concerning,

and no reliance should be placed on, the accuracy, fairness, or completeness of this information. This material may contain

certain “forward-looking statements” and information relating to the Company that reflects the current views and/or expectations

of the Company and its management with respect to performance, business and future events. Such statements are subject to a

number of risks, uncertainties and assumptions. Such statements are only predictions and are not guarantees of future

performance. A number of important factors could cause actual results to differ materially from the plans, objectives,

expectations, estimates and intentions expressed in these materials. All forward-looking statements in this presentation are based

on information and data available as of the date they were made, and the Company makes no undertaking to update them in

light of new information or future developments.

This presentation and its contents are proprietary information and may not be reproduced or otherwise disseminated in whole or

in part without the Company’s prior written consent.

Confirmation of your Representation: In order to be eligible to view these materials, the recipient must be either (1) a

Qualified Institutional Buyer (a “QIB”) (within the meaning of Rule 144A under the U.S. Securities Act of 1933, as amended (the

“Securities Act ”) or (2) a non-U.S. person (within the meaning of Regulation S under the Securities Act) outside the U.S. These

materials are being delivered to you at your request and by accepting and accessing these materials, you shall be deemed to

have represented to us that you and any customers you represent are either (a) QIBs or (b) non-U.S. persons (within the

meaning of Regulation S under the Securities Act).

Disclaimer

Agenda

1. Company Overview

2. Why Restructuring

3. Summary of Restructuring

4. Restructuring Implementation Proceeding

5. Appendix

a) OOG Corporate Structure

b) Quarterly Budget

c) Overview of Contract Rates

d) Opex Detailing

CONFIDENTIAL SETTLEMENT COMMUNICATION SUBJECT TO FRE 408

4

Odebrecht Presence in the Oil & Gas Sector($ in millions)

Company Overview

Odebrecht Oil & Gas (“OOG”) is a leading Brazilian oilfield services

company and is the oilfield services arm of Odebrecht Group, one of the

largest business conglomerates in Latin America

Created in 2006 to concentrate the Group’s oil & gas investments in a

new company

OOG provides integrated, customized solutions for the upstream oil

industry in Brazil and around the world. It can serve its customers

throughout their business cycle from design engineering, project

management, and integrated service delivery to offshore drilling rigs and

production platforms

Backlog Breakdown

(1) Excludes Sete Brasil contracts.(2) Does not consolidate Cidade de Itajaí, Pioneiro de Libra and PLSVs Assets. (3) No audited financial statements have been issued since December 31, 2015. 1H16 are unaudited figures.(4) Annualized Net Debt EBITDA.

Business Segments

US$ MM 2012 2013 2014 2015 1H15 1H16(3)

Income Statement

Net Revenue 691 988 1,187 1,101 582 478

Growth (%) 86.5% 42.9% 20.1% (7.3%) n/a (17.9%)

EBITDA 273 475 505 556 307 275

EBITDA Margin (%) 39.5% 48.1% 42.5% 50.5% 53% 58%

Net Income (22) (34) (75) (218) 53 (57)

Net Margin (%) (3.2%) (3.4%) (6.3%) (20%) 9.1% (12%)

Balance Sheet

Total Assets 6,160 6,044 6,205 5,707 6,141 5,578

Total Fixed Assets 5,193 5,153 5,041 4,698 5,011 4,638

Cash 431 298 445 244 364 152

Cash and Equivalents 390 212 331 69 148 66

Short-Term Investments

41 86 114 175 216 86

Total Debt 4,683 4,564 4,809 4,539 4,674 4,476

Shareholders' Equity 1,269 1,211 1,121 859 1,169 783

Consolidated Net Debt/ EBITDA

15.6x 9.0x 8.6x 7.7x 7.0x(4) 7.9x(4)

Consolidated Financial Highlights(2)

CONFIDENTIAL SETTLEMENT COMMUNICATION SUBJECT TO FRE 408

Total Backlog: US$ 4.8bn (as of December 31, 2016)(1)

Drilling (excl. Sete Br), 68%

Production, 24%

Subsea, 5% Maintenance, 4%

5

OOG ParentCo

PLSVs(Coral do Atlântico and Estrela do Mar)

Maintenance and Offshore Services

(MSO)

2022 Structure (ODN I & II, Tay IV,

Norbe VI)ODN Delba III

FPSOs CDI and Libra

100% 100% 100% 100%50%

2021 Structure (Norbe VIII & IX)

50%

OOG Current Simplified Corporate Structure

Economicinterest:

100%

ODN I & II: 60%Norbe VI: 100%Tay IV: 100% 48% 100%50% 50%Ownership

6

Odebrecht Oil & Gas History

Growth opportunities Incorporation of Odebrecht Oil & Gas

Consolidation of the offshore oilfield services capabilities

Increased exposure to oil and gas sector

Divestment of all shallow and mid water assets by the end of the decade

Joint venture with Maersk to operate an FPSO in the North Sea

1990’s1970’s to 1980’s 2000’s 2011 - 2014

Starts

operating in

the offshore

drilling

industry

Operations in the

offshore segment

First Brazilian

company to provide

offshore drilling

services to Petrobras

Largest privately

owned offshore

drilling and

exploration fleet

8 platforms in Brazil

by the end of the

1980's

Contract for Norbe VI

Contracts for Norbe VIII and Norbe IX

2010

Increasing drilling portfolio

Contracts for ODN I and ODN II

Norbe VIII / IX Project Bond

Partnership with Temasek (1st round of private placement)

Contracts for ODN Delba III and ODN TAY IV

Strengthening

position in

Production and

Subsea with

Cidade de

Itajaí and 2

PLSVs with

Technip

Partnership

with Gávea

Investimentos

(2nd round of

private

placement)

Partnership

with Sete

Brasil –

Contract to

operate 5 rigs

to be built in

Brazil

Operations of

3 third-party

deepwater

rigs

ODN Tay IV

Project Bond

retap and

Perpetual

Bond Issuance

Libra FPSO

contract

(OOG-TK)

Start of drop

in oil prices

Start of

“Carwash”

investigations

ODN I & II and

Norbe VI Project

Bond and

contract to

operate the PLSV

Polar Onyx with

Ceona

2015 - today

OOG is

provisionally

blocked by

Petrobras from

submitting

new proposals

ODN TAY IV

contract

termination

OOG write off

in Sete Brasil

investment

OOG ParentCo

loses

Investment

Grade Rating

Project Bonds

2021 and 2022

lose

Investment

Grade Rating

Gávea

Investimentos sells

equity interest to

ODB for nominal

value

Temasek sells

equity interest to

ODB for nominal

value

Perpetual Bond

coupon payment

default

OOG Debt

Restructuring

Libra FPSO

start of

Operations

Oil & gas down cycle

To occur

CONFIDENTIAL SETTLEMENT COMMUNICATION SUBJECT TO FRE 408

7

OOG Management – Key Executives

Board of Directors(1) – 8 members (1 Independent)

OOG ParentCo corporate governance includes a board of directors and 3 supporting committees

Name Function

Roberto Lopes Pontes Simões CEO

Herculano de Almeida Barbosa Engineering & Technology

Rogerio Luis Murat Ibrahim CFO

Heitor Gioppo Drilling

Jorge Luis Uchoa MitidieriSubsea, Production and

Maintenance

Guilherme Pacheco de Britto Legal

Marco Aurélio Fonseca Sustainability

José Cláudio Breviglieri Grossi Human Resources

Nir Lander Head of Compliance

Helena Ramos Head of Corporate Finance

Name Function Representative of

Luciano Guidolin Chairman Odebrecht S.A.

André Amaro Director Odebrecht S.A.

Daniel Villar Director Odebrecht S.A.

Marcela Drehmer Director Odebrecht S.A.

Ticiana Marianetti Director Odebrecht S.A.

Monica Bahia Director Odebrecht S.A.

Mauro Motta Director Odebrecht S.A.

José Coutinho Director Independent

OOG Key Executives

Note: As of Jan/31/2017(1) At OOG Par level. Refer to appendix for complete OOG corporate structure.

CONFIDENTIAL SETTLEMENT COMMUNICATION SUBJECT TO FRE 408

8

OOG Supporting Committees

Name Committee Role

Marcela Drehmer Coordinator

Mauro Figueiredo Motta Member

Ticiana Marianetti Member

Rogerio Ibrahim Guest

Guilherme Britto Guest

Danielli Santiago Pugliese Secretary

Name Committee Role

Daniel Villar Coordinator

Marco Aurelio Fonseca Guest

José Cláudio Grossi Guest

Danielli Santiago Pugliese Secretary

Pre-approval of financial statements (before board)

Evaluation and pre-approval (before board) of new projects

Monitoring of ongoing projects (before operations)

Pre-approval of financial transactions (before board)

Monitor key personnel performance

Establishment of human resources policy

Replacement and promotion plans for top and middle management

CPO (People & Organization Committee)

CFI (Financial Investment Committee)

Name Committee Role

Andre Amaro Coordinator

Ticiana Marianetti Member

Nir Lander Guest

Alexandre Cezimbra Secretary

Monitoring the internal compliance control systems and compliance with laws, standards, and regulations

Conducting and/or authorizing investigations into matters within its scope

Proposing periodic updates to the OOG Policy on Compliance and Proposing supplemental guidelines needed for the activity

Promoting interaction with national and international entities, oriented toward best practices in Compliance

Compliance Committee

Note: As of Jan/31/2017

CONFIDENTIAL SETTLEMENT COMMUNICATION SUBJECT TO FRE 408

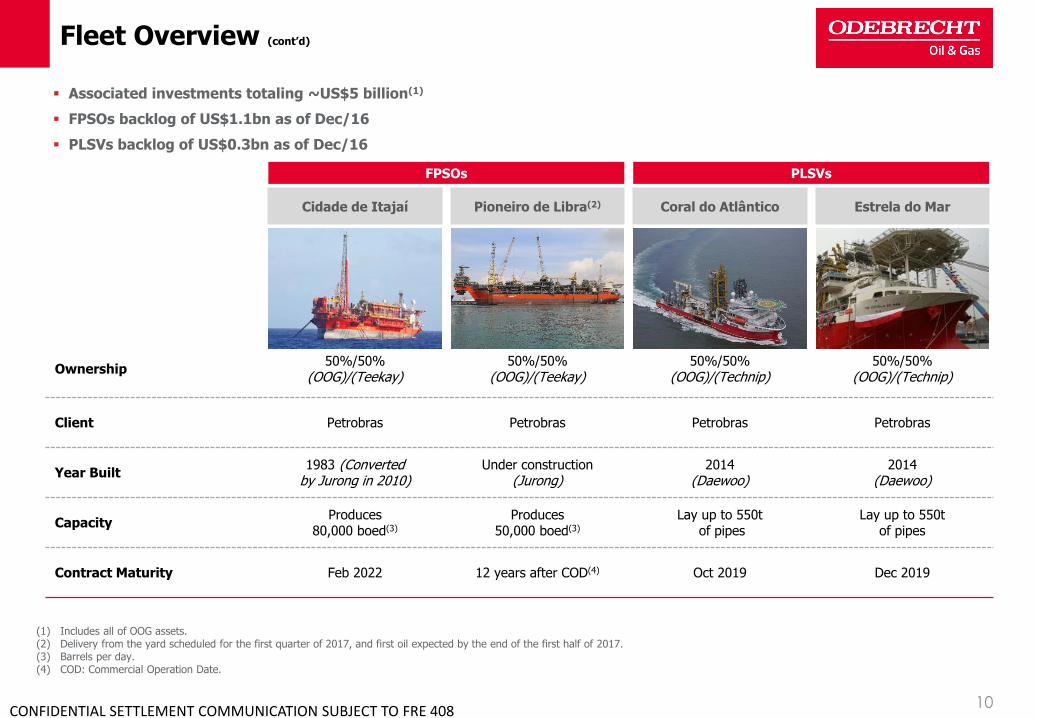

Associated investments totaling ~US$5 billion(1)

Drilling Unit backlog of US$3.3bn as of Dec/16(2)

9

Fleet Overview

Norbe VIII Norbe IX Norbe VI ODN I ODN II ODN Tay IV ODN Delba III

[PIC] [PIC] [PIC] [PIC] [PIC] [PIC] [PIC]

Ownership 100% 100% 100% 60%(5) 60%(5) 100% 48%(5)

Client Petrobras Petrobras Petrobras Petrobras Petrobras Not Chartered Petrobras

Charter daily rate (3) US$381 US$358 US$210 US$335 US$335 n.m. US$223

Services daily rate (3) R$123 R$116 R$450 R$109 R$109 n.m. R$477

Contract Maturity

Jul 2021 Oct 2021 Jul 2018(4) Sep 2022 Aug 2022 n.m. Aug 2019

Year Built2011

(DSME)2011

(DSME)2010 (SBM)

2011 (DSME)

2011(DSME)

1981/ converted to drilling rig in 1999 / refurbished in 2011

2011 (SBM)

DrillingCapacitywater depth

3,000m 3,000m 2,400m 3,000m 3,000m 2,400m 2,400m

DesignDSME 10,000

DSME 10,000

TDS-2000 Plus

DSME 10,000

DSME 10,000

Friede & Goldman L-767C

TDS-2500

2021 BOND STRUCTURE 2022 BOND STRUCTURE DELBA III

(1) Includes all of OOG assets.(2) Excludes Sete Brasil contracts.(3) As of March/2017. Charter daily rates in $ 000’. Service daily rates in R$ 000’. (4) Norbe VI contract was originally scheduled to expire on July 11, 2018 and was extended for an additional 258 days as a result of an unilateral extension right exercised by Petrobras in 2013.

Afterwards (in 2016), Petrobras decided to revoke its decision and the original expiration date was restated.

(5) Economic interest of 100%.

Currently idle in Tenerife and will

likely be scrapped in 2H2017

CONFIDENTIAL SETTLEMENT COMMUNICATION SUBJECT TO FRE 408

10

Fleet Overview (cont’d)

Cidade de Itajaí Pioneiro de Libra(2) Coral do Atlântico Estrela do Mar

[PIC] [PIC] [PIC] [PIC]

Ownership50%/50%

(OOG)/(Teekay)50%/50%

(OOG)/(Teekay)50%/50%

(OOG)/(Technip)50%/50%

(OOG)/(Technip)

Client Petrobras Petrobras Petrobras Petrobras

Year Built1983 (Converted

by Jurong in 2010)Under construction

(Jurong)2014

(Daewoo)2014

(Daewoo)

CapacityProduces

80,000 boed(3)

Produces 50,000 boed(3)

Lay up to 550tof pipes

Lay up to 550t of pipes

Contract Maturity Feb 2022 12 years after COD(4) Oct 2019 Dec 2019

PLSVsFPSOs

Associated investments totaling ~US$5 billion(1)

FPSOs backlog of US$1.1bn as of Dec/16

PLSVs backlog of US$0.3bn as of Dec/16

(1) Includes all of OOG assets.(2) Delivery from the yard scheduled for the first quarter of 2017, and first oil expected by the end of the first half of 2017.(3) Barrels per day.(4) COD: Commercial Operation Date.

CONFIDENTIAL SETTLEMENT COMMUNICATION SUBJECT TO FRE 408

11

Operational Track Record

CONFIDENTIAL SETTLEMENT COMMUNICATION SUBJECT TO FRE 408

OOG’s Drilling Fleet historical performance (yearly)

(1) Excludes ODN Tay IV.

(1) (1)

12

Operational Track Record (cont’d)

CONFIDENTIAL SETTLEMENT COMMUNICATION SUBJECT TO FRE 408

96%

70%

80%

99%

90% 92%97% 97%

89%94%

84%

100%

90%86%

97%

70%

81%

108%

93%98%

101% 103%

91%94% 94%

100%

88% 88%

3Q13 4Q13 1Q14 2Q14 3Q14 4Q14 1Q15 2Q15 3Q15 4Q15 1Q16 2Q16 3Q16 4Q16

ODEBRE 21'

Operational Uptimes Economic Uptimes

88%83%

96%

80%

72%

94%90% 88%

96%

76%

97% 98%92%

85%

93%88%

102%

83%76%

97%93% 93%

104%

77%

104%101% 98%

86%

3Q13 4Q13 1Q14 2Q14 3Q14 4Q14 1Q15 2Q15 3Q15 4Q15 1Q16 2Q16 3Q16 4Q16

ODEBRE 22'

Operational Uptimes Economic Uptimes

(1)

Original Series

Issuance

New Series

Issuance

(1) (1) (1) (1) (1)

(1) Excludes ODN Tay IV.

13

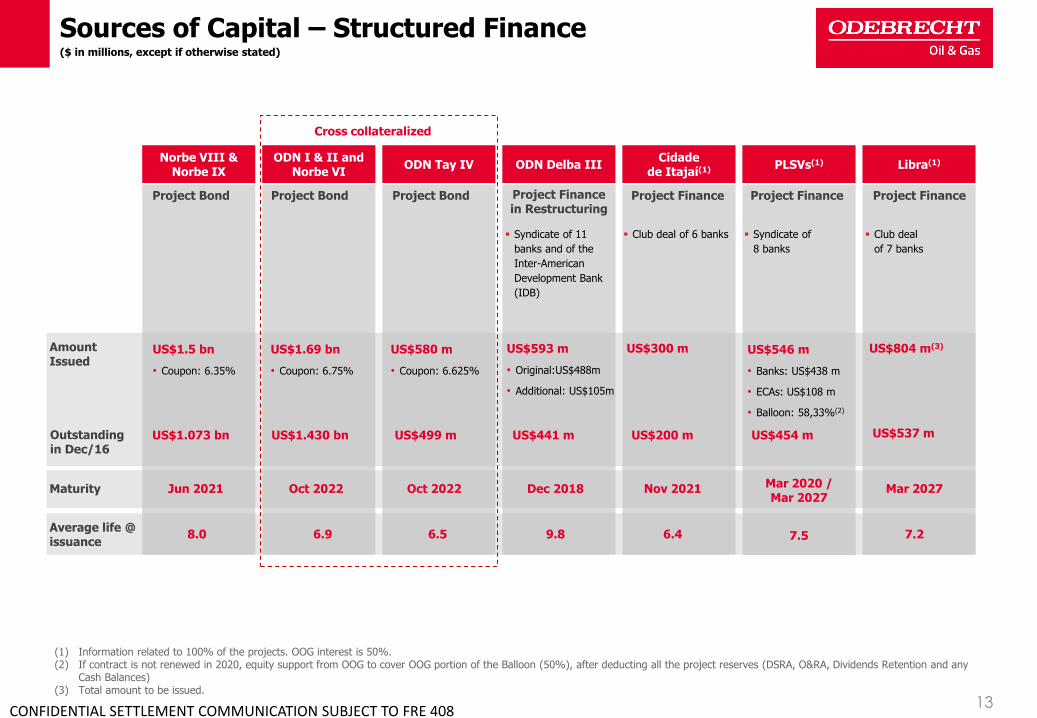

Sources of Capital – Structured Finance($ in millions, except if otherwise stated)

Project FinanceProject Bond Project Finance in Restructuring

Project Bond

Amount Issued

Average life @ issuance

Cidade de Itajaí(1)

ODN I & II and Norbe VI

ODN Tay IV ODN Delba III

US$1.69 bn

• Coupon: 6.75%

6.9

US$593 m

• Original:US$488m

• Additional: US$105m

9.8

Syndicate of 11

banks and of the

Inter-American

Development Bank

(IDB)

6.5

US$300 m

6.4

Club deal of 6 banks

Maturity Oct 2022 Dec 2018Oct 2022 Nov 2021

Project Finance

PLSVs(1)

7.5

Mar 2020 /Mar 2027

Syndicate of

8 banks

US$546 m

• Banks: US$438 m

• ECAs: US$108 m

• Balloon: 58,33%(2)

US$580 m

• Coupon: 6.625%

Cross collateralized

Outstandingin Dec/16

Project Bond

Norbe VIII &Norbe IX

US$1.5 bn

• Coupon: 6.35%

8.0

Jun 2021

US$1.073 bn US$1.430 bn US$499 m US$441 m US$200 m US$454 m

Project Finance

Libra(1)

Club deal

of 7 banks

US$804 m(3)

Mar 2027

7.2

US$537 m

(1) Information related to 100% of the projects. OOG interest is 50%.(2) If contract is not renewed in 2020, equity support from OOG to cover OOG portion of the Balloon (50%), after deducting all the project reserves (DSRA, O&RA, Dividends Retention and any

Cash Balances) (3) Total amount to be issued.

CONFIDENTIAL SETTLEMENT COMMUNICATION SUBJECT TO FRE 408

14

Sources of Capital – Corporate Debt Profile($ in millions, as of 12/31/2016)

550

41

550

42

197 198

31 27 27 27

59 43

-

100

200

300

400

500

600

Accrued Interest12/31/2016

2017 2018 2019 2020 2021 2022 >2023

Perpetual Bond Other Corporate Debt Project Bonds Promissory Notes(1)

(1) Perpetual Bond is redeemable in 2024 at OOG’s discretion. Information as of December 31, 2016. Debt is at OOG level, does not include project level debt.(2) Includes Banco do Brasil, HSBC, Bradesco, BNDES, FINEP, SwissRe and ING.

CONFIDENTIAL SETTLEMENT COMMUNICATION SUBJECT TO FRE 408

(2)

Amortization Profile

Agenda

CONFIDENTIAL SETTLEMENT COMMUNICATION SUBJECT TO FRE 408

1. Company Overview

2. Why Restructuring

3. Summary of Restructuring

4. Restructuring Implementation Proceeding

5. Appendix

a) OOG Corporate Structure

b) Quarterly Budget

c) Overview of Contract Rates

d) Opex Detailing

16

Changes in Market Environment

Contract Termination

ODN Tay IV charter and services contract terminated by Petrobras

Termination was unexpected by OOG

No market to recontract or sell ODN Tay IV

Odebrecht SA and Petrobras involvement in Carwash investigations

Brazilian oil & gas sector is not able to attract new investors

OOG has no access to lines of credit

OOG has no ability to renew and issue letters of credit associated to its projects

Operational uptimes have been lower than originally forecasted

OpEx and CapEx higher than originally forecasted due to high demand for offshore drilling between 2011-mid 2015:

Labor costs increased above inflation

Equipment suppliers consistently increased costs

Macondo accident has raised industry safety standards and consequently, maintenance costs

Changes in REPETRO rules increased importation costs

Increase in ANP inspections due to recent accidents in the industry

Change in taxation on income tax (IRRF) not entirely absorbed by Petrobras until now

BRL / USD exchange rate variation from approximately 2:1 to 4:1 significantly increased equity support necessity from OOG ParentCo

Pursuant to bonds indentures, OOG ParentCo (“Operator”) would be reimbursed by project bond structuresregarding opex, limited to a defined cap

Such reimbursement would be reduced by the amount received by the Operator in BRL. Such amount would be converted to USD based on a fixed 2:1 exchange rate (cap fx)

Credit Liquidity Operational Metrics Foreign Exchange

Since their issuance, operating environment for assets securing Bonds 2021 and 2022 has changed. Additionally, certain targeted operating metrics have not been achieved

CONFIDENTIAL SETTLEMENT COMMUNICATION SUBJECT TO FRE 408

17

Existing Structural Issues

Higher opex and capex than originally forecasted, exceeding caps, and therefore generating funding requirements by ParentCo

Existing cap OpEx and restriction to pay CapEx

One less asset

Petrobras terminated ODN Tay IV contract, which no longer generates cash flow for the 2022 structure

Re-chartering of Norbe VI at an acceptable rate may be difficult

Norbe VI renewal

Currency movements have significantly impacted OOG’s funding requirements

Existing exchange rate cap

Between 2010 and 2015, OOG supported the drilling assets with US$705m (net of dividends received) through CapEx/OpEx overage andinterest on corporate debt issued at OOG ParentCo level(1)

Starting in 2016, 2021/2022 bondholders agreed to waive OOG ParentCo CapEx/OpEx cap obligation in exchange for promissory notes at OOGParentCo, resulting in the issuance of $142.1m in promissory notes until April-2017

Based on current estimates, OOG would have to support the drilling assets with an additional US$1.0bn to US$1.1bn to keep the rigs inoperation throughout project bonds maturity (starting on May-2017)

From US$399 to US$505m in OpEx/CapEx above the existing caps as set forth under the project bonds indentures (notwithstanding thisamount could be substantially higher depending on operational and market conditions)

US$568m to support debt service obligations

At issuance, structures were intended to receive little, if any, support from ParentCo

Since their issuance, operating environment for assets securing Bonds 2021 and 2022 has changed. Additionally, certain targeted operating metrics have not been achieved

(1) For further details refer to page 18.

CONFIDENTIAL SETTLEMENT COMMUNICATION SUBJECT TO FRE 408

18

OOG Historical Support($ in millions)

Since the beginning of 2021 and 2022 assets operations, OOG has made significant funding contributions to support:

OpEx requirements above the opex cap (as set in the indentures)

Capital expenditures

Equity injections to fund the ramp up of the rigs

Shortfalls to cover debt service

From Project Bonds issuance to December 2015, OOG supported the structures with $705 million

In 2016, 2021/2022 bondholders agreed to waive OOG ParentCo capex/opex cap obligation in exchange for promissory

notes at OOG ParentCo

Promissory notes were issued for project bonds 2021/2022. As of 04/30/2017, total amount outstanding was $142.1m(1) ($87.5m for

2021 and $54.6m for 2022)

In addition, a total of $23.2m ($22.1m for 2022 and $1.2m for 2021) of letters of credits guaranteeing debt service payments were

withdrawn

CONFIDENTIAL SETTLEMENT COMMUNICATION SUBJECT TO FRE 408

(1) As of 12/31/2016, total amount outstanding was $102m ($59m for 2021 and $43m for 2022)(2) Calculated as the average interest on OOG ParentCo debt multiplied by Cumulative Total Equity Investment

OOG Funding to Date 2010 2011 2012 2013 2014 2015

2021 Structure

Dividends - 64 32 21 32 21

Equity Injections - (285) (40) (47) (76) (59)

Net Equity Investment (a) - (220) (8) (26) (44) (38)

2022 Structure

Dividends - - 20 320 179 73

Equity Injections (41) (105) (198) (245) (132) (129)

Net Equity Investment (b) (41) (105) (177) 74 48 (56)

Total

Net Equity Investment (a) + (b) (41) (325) (186) 48 4 (94)

Allocated Interest Costs(2) - (4) (12) (27) (31) (36)

Total Equity Investment (41) (330) (198) 21 (27) (131)

Cumulative Total Equity Investment (41) (371) (568) (547) (574) (705)

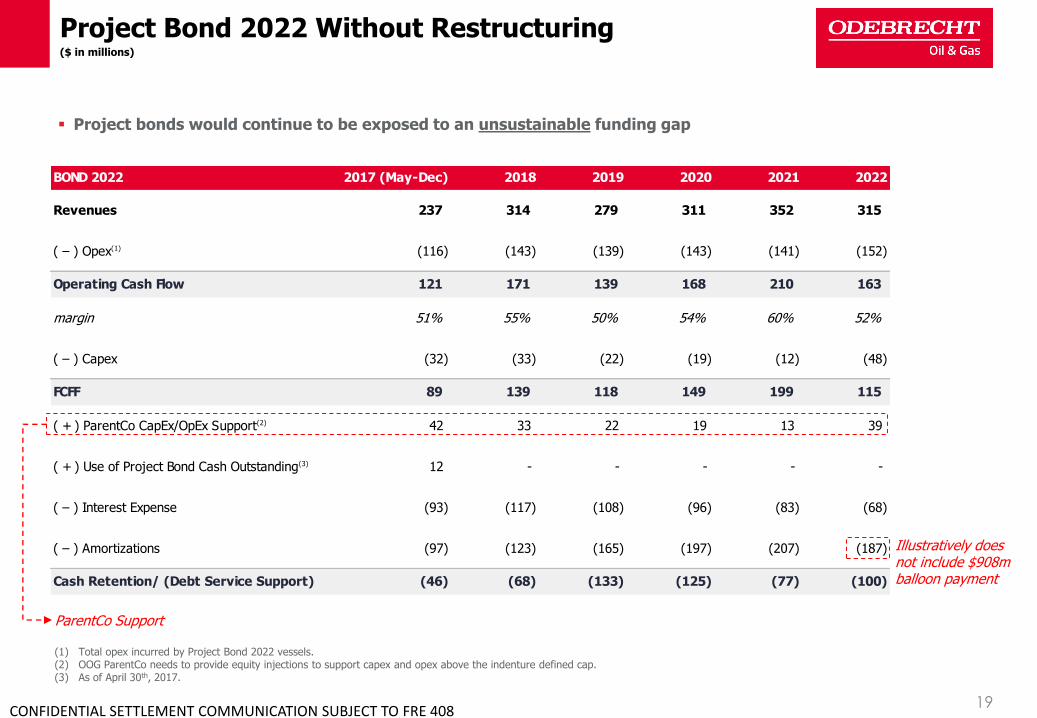

BOND 2022 2017 (May-Dec) 2018 2019 2020 2021 2022

Revenues 237 314 279 311 352 315

( – ) Opex(1) (116) (143) (139) (143) (141) (152)

Operating Cash Flow 121 171 139 168 210 163

margin 51% 55% 50% 54% 60% 52%

( – ) Capex (32) (33) (22) (19) (12) (48)

FCFF 89 139 118 149 199 115

( + ) ParentCo CapEx/OpEx Support(2) 42 33 22 19 13 39

( + ) Use of Project Bond Cash Outstanding(3) 12 - - - - -

( – ) Interest Expense (93) (117) (108) (96) (83) (68)

( – ) Amortizations (97) (123) (165) (197) (207) (187)

Cash Retention/ (Debt Service Support) (46) (68) (133) (125) (77) (100)

19

Project Bond 2022 Without Restructuring($ in millions)

Project bonds would continue to be exposed to an unsustainable funding gap

Illustratively does not include $908m balloon payment

CONFIDENTIAL SETTLEMENT COMMUNICATION SUBJECT TO FRE 408

(1) Total opex incurred by Project Bond 2022 vessels.(2) OOG ParentCo needs to provide equity injections to support capex and opex above the indenture defined cap.(3) As of April 30th, 2017.

ParentCo Support

BOND 2021 2017 (May-Dec) 2018 2019 2020 2021

Revenues 175 278 277 279 227

( – ) Opex(1) (68) (94) (93) (100) (104)

Operating Cash Flow 107 184 185 179 123

margin 61% 66% 67% 64% 54%

( – ) Capex (17) (16) (8) (16) (39)

FCFF 90 168 176 163 84

( + ) ParentCo CapEx/OpEx Support(2) 41 45 38 56 49

( + ) Use of Project Bond Cash Outstanding(3) 37 - - - -

( – ) Interest Expense (66) (59) (50) (41) (31)

( – ) Amortizations (120) (128) (143) (150) (83)

Cash Retention(4)/ (Debt Service Support) (19) 27 22 28 20

20

Project Bond 2021 Without Restructuring($ in millions)

Project bonds would continue to be exposed to an unsustainable funding gap

Illustratively does not include $450m balloon payment

CONFIDENTIAL SETTLEMENT COMMUNICATION SUBJECT TO FRE 408

(1) Total opex incurred by Project Bond 2021 vessels.(2) OOG ParentCo needs to provide equity injections to support capex and opex above the indenture defined cap. (3) As of April 30th, 2017. (4) Cash required to be retained in Project Bond structure in order to support $450m balloon payment in 2021.

ParentCo Support

OOG ParentCo May-17 Jun-17 Jul-17 Aug-17 Sep-17 Oct-17 Nov-17

Sources

Cash Flow from Project Bond 2022 (4) (1) (3) (5) (6) (6) (6)

Cash Flow from Project Bond 2021 (8) (4) (4) (4) (4) (4) (4)

Cash Flow from Other Projects (0) 1 (1) (0) (0) 2 (0)

Total Sources (a) (12) (4) (8) (10) (10) (7) (10)

Uses

Expenses at OOG ParentCo (1) (1) (3) (1) (1) (2) (0)

Total Uses (b) (1) (1) (3) (1) (1) (2) (0)

Change in Cash (a)+(b) (13) (5) (11) (11) (10) (10) (10)

Beginning Cash Balance 54 41 36 25 14 3 (6)

Ending Cash Balance 41 36 25 14 3 (6) (16)

21

OOG ParentCo Without Restructuring($ in millions)

Equity injections on project bonds would generate a cash insufficiency at OOG ParentCo

Cash flow forecast does not include corporate debt service payments (US$111m of accrued interest as of Apr/17 and

US$136m of principal due in the 1H17)

OOG monthly working capital requirement is US$30m

CONFIDENTIAL SETTLEMENT COMMUNICATION SUBJECT TO FRE 408

Agenda

CONFIDENTIAL SETTLEMENT COMMUNICATION SUBJECT TO FRE 408

1. Company Overview

2. Why Restructuring

3. Summary of Restructuring

4. Restructuring Implementation Proceeding

5. Appendix

a) OOG Corporate Structure

b) Quarterly Budget

c) Overview of Contract Rates

d) Opex Detailing

23

Proposal Development

Amending Project Bonds 2021 and 2022 existing securitization structures will significantly improve their long-term viability

Amending the current financing structure would allow all disbursement requirements, including capex and opex above the current cap, to be borne by Drilling Assets cash flows

Viability of the operator is crucial to both the 2021 and 2022 Notes and for preserving agreements with Petrobras

OOG and its advisors developed a proposal to address the Drilling Assets liquidity and capital structure

The proposal developed by OOG and its advisors seeks:

A sustainable debt structure for the Drilling Assets

Deleveraging OOG ParentCo, which is the operator of the rigs

Limitation on incurring debt at ParentCo

Preserving services agreement and charter agreements with Petrobras (not only Project Bonds 2021 and 2022 vessels, but also FPSOs, PLSVs and MSO)

Mitigating risk of acceleration of the 2022 Notes as a result of the termination of Tay IV and potential adverse impact on other agreements with Petrobras

Value to Noteholders in the form of both interest and amortization

Keeps LC support in place

Flexibility to deal with uncertainty in re-chartering Norbe VI in 2018

A viable operating company

In addition to its debt restructuring, the company has been involved in contract renegotiations with Petrobras. The negotiation is currently on hold at Petrobras’s request while it completes its investment plan process

Nonetheless, the operating scenarios herein illustrate potential outcomes OOG management worked with prior to the negotiation being put on hold

CONFIDENTIAL SETTLEMENT COMMUNICATION SUBJECT TO FRE 408

24CONFIDENTIAL SETTLEMENT COMMUNICATION SUBJECT TO FRE 408

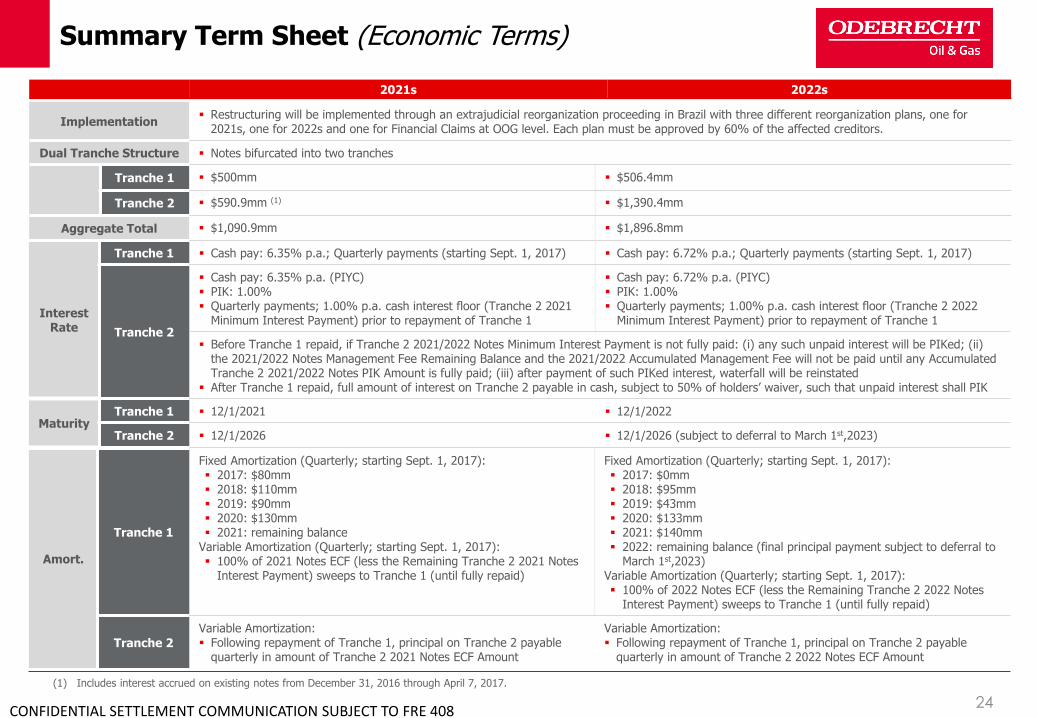

Summary Term Sheet (Economic Terms)

2021s 2022s

Implementation Restructuring will be implemented through an extrajudicial reorganization proceeding in Brazil with three different reorganization plans, one for

2021s, one for 2022s and one for Financial Claims at OOG level. Each plan must be approved by 60% of the affected creditors.

Dual Tranche Structure Notes bifurcated into two tranches

Tranche 1 $500mm $506.4mm

Tranche 2 $590.9mm (1) $1,390.4mm

Aggregate Total $1,090.9mm $1,896.8mm

Interest Rate

Tranche 1 Cash pay: 6.35% p.a.; Quarterly payments (starting Sept. 1, 2017) Cash pay: 6.72% p.a.; Quarterly payments (starting Sept. 1, 2017)

Tranche 2

Cash pay: 6.35% p.a. (PIYC) PIK: 1.00% Quarterly payments; 1.00% p.a. cash interest floor (Tranche 2 2021

Minimum Interest Payment) prior to repayment of Tranche 1

Cash pay: 6.72% p.a. (PIYC) PIK: 1.00% Quarterly payments; 1.00% p.a. cash interest floor (Tranche 2 2022

Minimum Interest Payment) prior to repayment of Tranche 1

Before Tranche 1 repaid, if Tranche 2 2021/2022 Notes Minimum Interest Payment is not fully paid: (i) any such unpaid interest will be PIKed; (ii) the 2021/2022 Notes Management Fee Remaining Balance and the 2021/2022 Accumulated Management Fee will not be paid until any Accumulated Tranche 2 2021/2022 Notes PIK Amount is fully paid; (iii) after payment of such PIKed interest, waterfall will be reinstated

After Tranche 1 repaid, full amount of interest on Tranche 2 payable in cash, subject to 50% of holders’ waiver, such that unpaid interest shall PIK

MaturityTranche 1 12/1/2021 12/1/2022

Tranche 2 12/1/2026 12/1/2026 (subject to deferral to March 1st,2023)

Amort.

Tranche 1

Fixed Amortization (Quarterly; starting Sept. 1, 2017): 2017: $80mm 2018: $110mm 2019: $90mm 2020: $130mm 2021: remaining balance

Variable Amortization (Quarterly; starting Sept. 1, 2017): 100% of 2021 Notes ECF (less the Remaining Tranche 2 2021 Notes

Interest Payment) sweeps to Tranche 1 (until fully repaid)

Fixed Amortization (Quarterly; starting Sept. 1, 2017): 2017: $0mm 2018: $95mm 2019: $43mm 2020: $133mm 2021: $140mm 2022: remaining balance (final principal payment subject to deferral to

March 1st,2023)Variable Amortization (Quarterly; starting Sept. 1, 2017): 100% of 2022 Notes ECF (less the Remaining Tranche 2 2022 Notes

Interest Payment) sweeps to Tranche 1 (until fully repaid)

Tranche 2

Variable Amortization: Following repayment of Tranche 1, principal on Tranche 2 payable

quarterly in amount of Tranche 2 2021 Notes ECF Amount

Variable Amortization: Following repayment of Tranche 1, principal on Tranche 2 payable

quarterly in amount of Tranche 2 2022 Notes ECF Amount

(1) Includes interest accrued on existing notes from December 31, 2016 through April 7, 2017.

25CONFIDENTIAL SETTLEMENT COMMUNICATION SUBJECT TO FRE 408

Summary Term Sheet (Economic Terms) (cont’d)

2021s 2022s

Amort. (cont.)

Waterfall (1)

Prior to the Tranche 1 2021/2022 Notes Maturity Date, the waterfall occurs as follows (on a quarterly basis, except for (v)):

Mandatory Obligations:

(i) 2021/2022 Notes OPEX/CAPEX Monthly Expense

(ii) 2021/2022 Notes Offshore Minimum Cash Reserve Account Required Balance

(iii) cash interest on Tranche 1

(iv) fixed amortization on Tranche 1(2)

(v) 2021/2022 Notes Management Incentive Payment (annually, beginning in March 2018) (after withdrawing all amounts from 2021/2022

Notes MIP Quarterly Accrual)

(vi) 35% of 2021/2022 Notes Management Fee

(vii) Minimum Tranche 2 2021/2022 Notes Interest Payment

(viii) 2021/2022 Notes Management Fee Remaining Balance(3) and 2021/2022 Notes Accumulated Management Fee, after satisfying any

Accumulated Tranche 2 2021/2022 Notes PIK Amount(4)

(ix) 2021/2022 Notes MIP Quarterly Accrual

Excess Funds Sweep:

(i) Remaining Tranche 2 2021/2022 Notes Interest Payment (PIYC, no reserve account),

(ii) 100% of remaining 2021/2022 Notes ECF to pay principal before all Drilling Units are recontracted,

(iii) 90% of remaining 2021/2022 Notes ECF to pay principal / 10% to Operator after all Drilling Units are recontracted

After the Tranche 1 2021/2022 Notes Maturity Date, the waterfall occurs as follows:

Mandatory Obligations:

(i) 2021/2022 Notes OPEX/CAPEX Monthly Expense

(ii) 2021/2022 Notes Offshore Minimum Cash Reserve Account Required Balance

(iii) 35% of 2021/2022 Notes Management Fee

(iv) full cash interest on Tranche 2 and any Accumulated Tranche 2 2021/2022 Notes PIK Amount (failure to pay constitutes an event of default,

subject to 50% holders’ waiver, in which case unpaid interest to PIK)

(v) 2021/2022 Notes Management Fee Remaining Balance and 2021/2022 Notes Accumulated Management Fee

Excess Funds Sweep:

(i) Tranche 2 2021/2022 Notes ECF Amount sweep to repay principal (equal to 90% of remaining 2021/2022 Notes ECF if all Drilling Units under

Charter Agreement Recontracting Period, otherwise equal to 100% of remaining 2021/2022 Notes ECF)

(ii) 2021/2022 Notes Operator ECF Sweep Amount (equal to 10% of remaining 2021/2022 Notes ECF, only if all Drilling Units under Charter

Agreement Recontracting Period)

(1) Proceeds from asset sales will be used to pay down Tranche 1 first then Tranche 2.(2) Amortization payment for 2022 Notes due on December 1st, 2022 moved to seventh priority in the waterfall and will not be an event of default if not paid in full in December 1st, 2022. Any amount not paid

deferred to March 1st, 2023 and due in full at that date.(3) 2021/2022 Notes Management Fee Remaining Balance means 65% of the 2021/2022 Notes Management Fee minus amount of CAPEX/OPEX spent in excess of certain ranges set forth in the annual budget

for such quarter and minus an amount equivalent to revenues lost for operating at downtime in excess of 15% (such amount not to exceed 65% of the Management Fee applicable to such vessel).(4) In case of insufficiency to make full payment of 2021/2022 Note Management Fee Remaining Balance, amounts to accrue and be payable on following payment date.

26CONFIDENTIAL SETTLEMENT COMMUNICATION SUBJECT TO FRE 408

Summary Term Sheet (Economic Terms) (cont’d)

2021s 2022s

Payments to OOG

Management Fee: $3,250,000 per Drilling Unit per year; if any Drilling Unit is Stacked, the 2021/2022 Notes Management Fee applicable to such Drilling Unit

is reduced to $2,437,500; payable quarterly and in accordance with waterfall

After the Tranche 1 2021/2022 Notes Maturity Date, Operator to receive 10% of any remaining 2021/2022 Notes ECF, subject to all 2021/2022 Drilling Units

being under Charter Agreement Recontracting Period.

Management Incentive Program:

25% of aggregate operational cost-savings achieved vs. Annual Budget to be distributed to relevant operator

Tested and distributed annually

2021/2022 Notes Management Incentive Payment to cease upon Tranche 1 2021/2022 Notes Maturity Date

No fee payable to OOG if Payment Default is ongoing, and no fee payable with respect to a Drilling Unit if related charter or services agreements terminated

due to OOG breach

Annual Budget

Annual Budget for 2017, 2018 and 2019 to be approved by holders as part of restructuring

Annual Budget for 2020 and 2021 subject to approval by Creditor Representative

Extraordinary Increases in Annual Budget for 2017, 2018 and 2019 to be approved by the Creditor Representative and notified to trustee and holders; if

holders representing 50% of aggregate principal amount of Tranche 1 do not object in writing within 30 days from date of notice, changes are deemed

approved

Project-Level Governance

Creditor Representative: individual jointly appointed by holders of New 2021 and 2022 Notes; will remain engaged so long as any New 2021 or 2022 Notes

are outstanding; selected consensually for first mandate as part of restructuring

Affirmative consent of Creditor Representative required for approval of Annual Budget for each Drilling Unit and certain related party transactions

Creditor Representative entitled to observe any meetings of OOG Par board of directors and OOG board of executive officers in which the New Notes,

Drilling Units, Collateral and Annual budget are discussed, and to have access to documents and information necessary to perform its duties

Creditor Representative may be replaced at any time by holders of 50% of either Tranche 1 2021 Notes or Tranche 1 2022 Notes. Procedures for selection

of replacement upon resignation or removal of Creditor Representative detailed in legal term sheet

Step-in Rights: Majority holders of 2021/2022 Notes can instruct collateral agent to replace relevant operator upon 2021/2022 Notes Material Performance

Event or an event of default under related indenture (any obligations of OOG as operator to cease upon replacement)

Collective Action: until repayment of Tranche 1, only Tranche 1 to vote on certain matters including acceleration, waiver of defaults, collateral enforcement,

approval of Annual Budget and Petrobras negotiations, among others

Other governance practices, including engagement of Independent Consultant, detailed in legal term sheet

ODN Tay IV

To be scrapped by later of 120 days from ER Filing Date and 45 days from the ER Approval Date (subject to extension); no costs associated with Tay IV to be

payable from waterfall structure from earlier of (A) completion of ODN Tay IV Disposition or (B) the later of 120 days from ER Filing Date and 45 days from

the ER Approval Date.

27CONFIDENTIAL SETTLEMENT COMMUNICATION SUBJECT TO FRE 408

Summary Term Sheet (Economic Terms) (cont’d)

2021s 2022s

Minimum Cash Balance/ Reserve

$25mm cash reserve established, to be funded by waterfall (2021 Notes

Offshore Minimum Cash Reserve Account Required Balance)

$40mm cash reserve established, to be funded by waterfall (2022 Notes

Offshore Minimum Cash Reserve Account Required Balance)

Collateral Structure

All existing collateral remains in place. First priority lien on substantially all of the assets of the respective project entities enforceable in Brazil and offshore,

including but not limited to the drilling rigs, cash collateral, interests in the charter and services agreements and accounts receivable, and lien on equity in

structures. Implementation of measures to enhance collateral package and protect the security interests on the collateral, as described in legal term sheet

LCs

All new LCs will cover Debt Service (i.e. no more O&M LCs)

Existing LCs issued by LC Creditors that do not adhere to restructuring plan will be drawn in full and shall receive Participating Titles to extent necessary to

restructure their LC Reimbursement Claims

LC Creditors that adhere to restructuring plan to issue new LCs as provided below and their existing undrawn LCs will be released

Tranche 1: New LCs to be issued to cover Tranche 1 in amount equal to 1/4 of the then outstanding undrawn amounts of the LCs and not to exceed such

undrawn amounts. Will be released at maturity unless a shortfall exists; OOG guarantee

LC providers may seek reimbursement against OOG only in amounts up to 35% of the Management Fee paid to OOG with respect to any draws on

Tranche 1 LCs while Tranche 1 debt is outstanding

Tranche 2: New LCs to be issued to cover Tranche 2 in amount equal to 3/4 of the then outstanding undrawn amounts of the LCs and not to exceed such

undrawn amounts. Will be released at maturity unless a shortfall exists; Participating Titles to be issued to LC Creditors as OOG guarantee

Termination of

ESA /

Undertaking

Agreement

Pursuant to ESA / Undertaking Agreement, OOG is currently required to pay for CAPEX and OPEX in excess of caps provided for under the 2021 / 2022

Agreements

ESA and Undertaking Agreement will be terminated in connection with the Restructuring and each structure will support its own CAPEX/OPEX needs

2021/2022 holders will receive a claim against OOG for future OPEX/CAPEX claims. These Financial Claims will be restructured as part of OOG restructuring

Financial Claims

of 2021/2022

holders at OOG

level

OOG has issued promissory notes in connection with past cap relief

In exchange for their Financial Claims against OOG, holders to receive OOG ParentCo Participating Titles

As per current forecasts, issued promissory notes and claims resulting from termination of ESA and Undertaking Agreement, would entitle Project Bonds

holders to an economic interest of ~10% of OOG ParentCo via Participating Titles (~6% to 2021 holders and ~4% to 2022 holders)

Amendments to

Charter/Services

Agreements

The company has been engaged in contract renegotiations of its existing charter and services agreements.

The company is permitted to enter into amendments of existing charter and services agreements to the extent that these amendments result in cash flows

that are substantially consistent with the cash flows set forth in the annual budget (refer to appendix).

28CONFIDENTIAL SETTLEMENT COMMUNICATION SUBJECT TO FRE 408

Summary Term Sheet (Economic Terms) (cont’d)

Financial Claims at OOG Level

Restructuring of

Financial Claims

at OOG Level

Financial Claims to be restructured at OOG level are comprised of (a) the Banks Claim; (b) the LC Reimbursement Claims; (c) the Perpetual Notes Claim; (d)

the NPs; (e) the ESA Termination Claim; and (f) the Undertaking Termination Claim.

All holders of Financial Claims will have equal treatment and are to receive Participating Titles in exchange for their Financial Claims

Participating

Titles

Participating Titles to be issued as perpetual securities paying interest calculated as a variable percentage of any OOG Shareholder Distributions

Redemption/Repurchase: Participating Titles can be redeemed or repurchased by the issuer or guarantor at their option. Participating Titles also to be

repurchased at option of holder in the event of a merger or change of control or IPO of OOG; in such cases, repurchase price for Participating Titles will

reflect consideration received in exchange for any OOG capital stock transferred pursuant to such transaction

Anti-dilution: Upon any issuance of OOG equity, subject to certain exceptions, holders can subscribe such additional Participating Titles to maintain their share

of Participating Titles Distributions

Conversion: Participating Titles are convertible into OOG preferred shares in case of an Event of Default (nonpayment of Participating Titles Distributions or

non-payment of redemption price or repurchase price, nonperformance of covenants and certain events of bankruptcy or insolvency of OOG)

BRLPayments under

Services Agreements

29CONFIDENTIAL SETTLEMENT COMMUNICATION SUBJECT TO FRE 408

New Cash Waterfall – 2021 and 2022 Notes: Tranche 1

$25 million cash reserve for 2021s

$40 million cash reserve for 2022s

1st

2nd

3rd

4th

USDPayments under

Charter Agreements

5th

Pledged

Not Pledged

Guarantor service account (All O&M / CAPEX needs after Onshore Proceeds Account)

Minimum Cash Reserve Account

Debt service account (Tranche 1 Cash Interest)

Guarantor service account (Management Incentive Program) (annually)

Debt service account (Tranche 1 Fixed Amortization)

Guarantor service account (35% Management Fee)

Debt service account (Tranche 2 Minimum Cash Interest)

Project OPEX/CAPEX

Guarantor service account (Management Fee Remaining Balance)

Management Incentive Program Accrual

Excess Cash Flow Pay-if-you-can interest on Tranche 2

ECF sweep to Tranche 1

6th

7th

8th

Reserve to pay incentive fee if company has

accumulated savings

65% minus OPEX/CAPEX paid in excess of budgeted ranges minus an amount

equivalent to revenues lost for operating at downtime in excess of 15%, limited to

the remaining balance of the Management Fee of the rig that suffered downtime

9th

10th

Onshore Proceeds Account

Failure to pay is event of default

Failure to pay is not event of default; company may PIK (but then cannot pay

Management Fee Remaining Balance until all PIKed interest is repaid)

Offshore Proceeds Account

Failure to pay is event of default

Pledged (in Management Incentive Program Accrual

Account) until released annually

10% ECF Sweep to ParentCo (after rigs re-contracted)

30CONFIDENTIAL SETTLEMENT COMMUNICATION SUBJECT TO FRE 408

New Cash Waterfall – 2021 and 2022 Notes: Tranche 2 (after repayment of Tranche 1)

1st

2nd

3rd

4th

5th

Pledged

Not Pledged

Guarantor service account (All O&M / CAPEX needs after Onshore Proceeds Account)

Minimum Cash Reserve Account

Guarantor Service Account(35% Management Fee)

Guarantor service account (Management Fee Remaining Balance)

Debt service account (Tranche 2 Cash Interest)

Project OPEX/CAPEX

Excess Cash Flow 100% ECF sweep to Tranche 2 (before rigs re-contracted) 90% ECF sweep to Tranche 2 (after rigs re-contracted)

6th

Onshore Proceeds Account

Failure to pay constitutes event of default, subject to waiver by 50% of holders

Offshore Proceeds Account

BRLPayments under

Services Agreements

USDPayments under

Charter Agreements

65% minus OPEX/CAPEX paid in excess of budgeted ranges minus an amount

equivalent to revenues lost for operating at downtime in excess of 15%, limited to

the remaining balance of the Management Fee of the rig that suffered downtime

31

Bond 2021 Post Restructuring Cash Flow - Case A($ in millions)

No changes to PBR current contracts

CONFIDENTIAL SETTLEMENT COMMUNICATION SUBJECT TO FRE 408

Note 1: This cash flow statement is for illustrative purposes and represents estimates subject to significant change depending on variations on assumptions used, future measures taken by Petrobras and changes in

macroeconomic factors.

Note 2: Norbe VIII Operational Assumptions (averages between 2017 and 2021): Opex: USD 144 k/day, Capex: USD 27 k/day and Economic Uptime: 95%; Starting on 3Q2021, projections based on new contracts and OOG’s

future recontracting assumptions. Operational Assumptions (averages between 2017 and 2026): Opex: USD 150 k/day, Capex: USD 25 k/day and Economic Uptime: 96%

Note 3: Norbe IX Operational Assumptions (averages between 2017 and 2021): Opex: USD 145 k/day, Capex: USD 30 k/day and Economic Uptime: 97%; Starting on 3Q2021, projections based on new contracts and OOG’s

future recontracting assumptions. Operational Assumptions (averages between 2017 and 2026): Opex: USD 151 k/day, Capex: USD 25 k/day and Economic Uptime: 97%

BOND 2021 2018 2019 2020 2021 2022 2023 2024 2025 2026

Revenues 175 278 277 279 227 240 251 252 252 243

( – ) Opex (72) (94) (93) (100) (104) (101) (106) (111) (116) (121)

Operating Cash Flow 103 184 185 179 123 139 145 141 136 122

( – ) Capex (17) (16) (8) (16) (39) (10) (10) (10) (10) (35)

Cash Flow From Assets 86 168 176 163 84 130 136 131 127 87

( +/– ) Minimum Cash Reserve ($25m) 9 (9) - - - - - - - -

( – ) Tranche 1 Cash Interest (20) (24) (17) (10) (2) - - - - -

( – ) Tranche 1 Fixed Amortization (80) (110) (90) (130) (71) - - - - -

( – ) Mandatory Cash Interest on Tranche 2 (4) (6) (7) (7) (7) (46) (41) (36) (32) (27)

( – ) Management Fees to ParentCo (3) (6) (6) (6) (6) (6) (6) (6) (6) (6)

Cash Flow After Mandatory Payments (12) 13 57 10 (2) 78 89 89 89 53

( – ) Additional Cash interest on Tranche 2 - - (35) (15) - - - - - -

( – ) ECF Sweep to Tranche 1 - - (19) - - - - - - -

Cash Flow Before Tranche 2 Amortizations (12) 13 3 (5) (2) 78 89 89 89 53

( – ) ECF Sweep to Tranche 2 (90% ) - - - - - (66) (80) (80) (80) (48)

( – ) ECF Sweep to ParentCo (10% ) - - - - - (7) (9) (9) (9) (5)

Change in Excess Cash (12) 13 3 (5) (2) 4 (0) (0) (0) (0)

Memo: Minimum Cash Account Balance 16 25 25 25 25 25 25 25 25 25

Memo: Excess Cash Account Balance - 13 16 11 8 13 12 12 12 11

Debt Balance 2017 2018 2019 2020 2021 2022 2023 2024 2025 2026

( + ) Tranche 1 EoP 500 420 310 201 71 - - - - - -

( + ) Tranche 2 EoP 591 615 655 662 690 734 675 602 527 452 408

Total Debt 1,091 1,035 965 864 761 734 675 602 527 452 408

2017 (May- Dec)

April 7, 2017

32

Bond 2022 Post Restructuring Cash Flow - Case A($ in millions)

CONFIDENTIAL SETTLEMENT COMMUNICATION SUBJECT TO FRE 408

Note 1: This cash flow statement is for illustrative purposes and represents estimates subject to significant change depending on variations on assumptions used, future measures taken by Petrobras and changes in macroeconomic factors. Note 2: ODN I Operational Assumptions (averages between 2017 and 2022): Opex: USD 140 k/day, Capex: USD 32 k/day and Economic Uptime: 97%; Starting on 3Q2022, projections based on new contracts and OOG’s future

recontracting assumptions. Operational Assumptions (averages between 2017 and 2026): Opex: USD 148 k/day, Capex: USD 24 k/day and Economic Uptime: 97%Note 3: ODN II Operational Assumptions (averages between 2017 and 2022): Opex: USD 148 k/day, Capex: USD 34 k/day and Economic Uptime: 97%; Starting on 3Q2022, projections based on new contracts and OOG’s future

recontracting assumptions. Operational Assumptions (averages between 2017 and 2026): Opex: USD 152 k/day, Capex: USD 25 k/day and Economic Uptime: 97%Note 4: Norbe VI Operational Assumptions (averages between 2017 and 2022): Opex: USD 132 k/day, Capex: USD 16 k/day and Economic Uptime: 83%; Starting on 3Q2018, projections based on new contracts and OOG’s future

recontracting assumptions. Operational Assumptions (averages between 2017 and 2026): Opex: USD 142 k/day, Capex: USD 20 k/day and Economic Uptime: 90%Note 5: Tay IV: Scrapped in 2017 with associated costs of $17m (net of scrapping proceeds).

No changes to PBR current contracts

BOND 2022 2018 2019 2020 2021 2022 2023 2024 2025 2026

Revenues 237 314 279 311 352 315 352 364 369 371

( – ) Opex (123) (143) (139) (143) (141) (152) (158) (166) (173) (181)

Operating Cash Flow 114 171 139 168 210 163 194 198 196 190

( – ) Capex (32) (33) (22) (19) (12) (48) (15) (28) (15) (15)

Cash Flow From Assets 82 139 118 149 199 115 179 171 181 175

( – ) March LC Withdrawal Reimbursement (10) - - - - - - - - -

( +/– ) Minimum Cash Reserve ($40m) (28) 9 (9) 19 (19) 12 (12) - - -

( – ) Tranche 1 Cash Interest (22) (32) (26) (22) (12) (4) - - - -

( – ) Tranche 1 Fixed Amortization - (95) (43) (133) (140) (95) - - - -

( – ) Mandatory Cash Interest on Tranche 2 (9) (15) (16) (17) (18) (19) (108) (136) (136) (136)

( – ) Management Fees to ParentCo (6) (9) (8) (10) (9) (9) (9) (10) (9) (10)

Cash Flow After Mandatory Payments 8 (4) 16 (14) 1 (1) 50 24 36 29

( – ) Additional Cash interest on Tranche 2 (2) (2) (2) - - - (3) - - -

( – ) ECF Sweep to Tranche 1 - - - - - - - - - -

Cash Flow Before Tranche 2 Amortizations 6 (6) 14 (14) 1 (1) 46 24 36 29

( – ) ECF Sweep to Tranche 2 (90% ) - - - - - - (27) (29) (26) (34)

( – ) ECF Sweep to ParentCo (10% ) - - - - - - (3) (3) (3) (4)

Change in Excess Cash 6 (6) 14 (14) 1 (1) 17 (8) 7 (8)

Memo: Minimum Cash Account Balance 40 31 40 21 40 28 40 40 40 40

Memo: Excess Cash Account Balance 6 - 14 - 1 - 17 9 16 8

Debt Balance 2017 2018 2019 2020 2021 2022 2023 2024 2025 2026

( + ) Tranche 1 EoP 506 506 411 368 235 95 - - - - -

( + ) Tranche 2 EoP 1,390 1,450 1,547 1,652 1,765 1,887 2,017 2,036 2,028 2,022 2,008

Total Debt 1,897 1,956 1,959 2,020 2,001 1,982 2,017 2,036 2,028 2,022 2,008

2017 (May- Dec)

April 7, 2017

33

OOG ParentCo Post Restructuring Cash Flow - Case A($ in millions)

No changes to PBR current contracts

CONFIDENTIAL SETTLEMENT COMMUNICATION SUBJECT TO FRE 408

Note 1: This cash flow statement is for illustrative purposes and represents estimates subject to significant change depending on variations on assumptions used, future measures taken by Petrobras and changes in macroeconomic factors.

(1) Net of LC Issuers reimbursements relative to pre-restructuring withdrawals.

OOG ParentCo 2017 (May-Dec) 2018 2019 2020 2021 2022 2023 2024 2025 2026

Sources

Cash Flow 2022 Structure (1) 4 7 5 7 6 7 12 13 12 14

Cash Flow 2021 Structure (1) 3 6 6 6 6 13 15 15 15 11

Project A - - - - - - - - - -

Project B (2) 32 28 25 33 38 42 45 58 60

Project C 2 8 12 12 13 13 14 14 14 15

Project D - - - - - - - - - -

ODB Capital Increase 30 - - - - - - - - -

Total Sources (a) 37 53 51 51 59 71 83 87 99 99

Uses

Unallocated G&A (13) (12) (14) (14) (14) (14) (14) (14) (14) (14)

Restructuring Costs (3) - - - - - - - - -

LC Costs (Other Projects) (2) (3) (3) (3) (3) (3) (3) (3) (2) (2)

LC Costs (Project Bonds) (1) (2) (2) (2) (2) (2) (2) (2) (2) (2)

FINEP & BNDES Debt Service (1) (1) (1) (1) (0) (0) - - - -

Total Uses (b) (20) (18) (20) (19) (19) (19) (19) (19) (18) (18)

OOG ParentCo Cash Flow (a)+(b) 17 35 31 31 40 53 64 68 80 81

34

Assumes stacking of one rig for the maximum considered period of time, with revenue reduction in exchange of optional maximum backlog extension

Bond 2021 Post Restructuring Cash Flow - Case B($ in millions)

CONFIDENTIAL SETTLEMENT COMMUNICATION SUBJECT TO FRE 408

Note 1: This cash flow statement is for illustrative purposes and represents estimates subject to significant change depending on variations on assumptions used, future measures taken by Petrobras and changes in

macroeconomic factors.

Note 2: Norbe VIII Operational Assumptions (averages between 2017 and 2021): Opex: USD 124 k/day, Capex: USD 15 k/day and Economic Uptime: 95%; Starting on 3Q2022, projections based on new contracts and OOG’s

future recontracting assumptions. Operational Assumptions (averages between 2017 and 2026):, Opex: USD 138 k/day, Capex: USD 18 k/day and Economic Uptime: 96%;

Note 3: Norbe IX Operational Assumptions (averages between 2017 and 2021): Opex: USD 145 k/day, Capex: USD 26 k/day and Economic Uptime: 97%; Starting on 3Q2021, projections based on new contracts and OOG’s

future recontracting assumptions. Operational Assumptions (averages between 2017 and 2026): Opex: USD 151 k/day, Capex: USD 24 k/day and Economic Uptime: 97%

BOND 2021 2018 2019 2020 2021 2022 2023 2024 2025 2026

Revenues 173 232 236 274 254 222 258 247 259 255

( – ) Opex (70) (75) (83) (100) (104) (101) (106) (111) (116) (121)

Operating Cash Flow 103 157 153 174 150 121 153 137 143 134

( – ) Capex (9) (8) (15) (12) (27) (10) (10) (22) (10) (22)

Cash Flow From Assets 94 149 138 162 123 112 143 114 134 112

( +/– ) Minimum Cash Reserve ($25m) 0 (0) - - - - - 0 - -

( – ) Tranche 1 Cash Interest (20) (24) (18) (11) (4) - - - - -

( – ) Tranche 1 Fixed Amortization (80) (110) (90) (130) (89) - - - - -

( – ) Mandatory Cash Interest on Tranche 2 (4) (6) (7) (7) (7) (47) (43) (38) (35) (30)

( – ) Management Fees to ParentCo (3) (6) (5) (6) (6) (6) (6) (6) (6) (6)

Cash Flow After Mandatory Payments (12) 3 19 8 18 59 94 70 93 76

( – ) Additional Cash interest on Tranche 2 - - (7) (7) (21) - - - - -

( – ) ECF Sweep to Tranche 1 - - - - (1) - - - - -

Cash Flow Before Tranche 2 Amortizations (12) 3 12 0 (5) 59 94 70 93 76

( – ) ECF Sweep to Tranche 2 (90% ) - - - - - (50) (85) (66) (81) (69)

( – ) ECF Sweep to ParentCo (10% ) - - - - - (6) (9) (7) (9) (8)

Change in Excess Cash (12) 3 12 0 (5) 3 (0) (3) 3 (0)

Memo: Minimum Cash Account Balance 25 25 25 25 25 25 25 25 25 25

Memo: Excess Cash Account Balance - 3 15 15 10 13 13 10 12 12

Debt Balance 2017 2018 2019 2020 2021 2022 2023 2024 2025 2026

( + ) Tranche 1 EoP 500 420 310 220 90 - - - - - -

( + ) Tranche 2 EoP 591 615 655 691 729 754 711 633 573 497 433

Total Debt 1,091 1,035 965 911 819 754 711 633 573 497 433

2017 (May- Dec)

April 7, 2017

35

Bond 2022 Post Restructuring Cash Flow - Case B ($ in millions)

CONFIDENTIAL SETTLEMENT COMMUNICATION SUBJECT TO FRE 408

(1)

Note 1: This cash flow statement is for illustrative purposes and represents estimates subject to significant change depending on variations on assumptions used, future measures taken by Petrobras and changes in macroeconomic factors. Note 2: ODN I Operational Assumptions (averages between 2017 and 2022): Opex: USD 140 k/day, Capex: USD 31 k/day and Economic Uptime: 97%; Starting on 3Q2022, projections based on new contracts and OOG’s future

recontracting assumptions. Operational Assumptions (averages between 2017 and 2026): Opex: USD 148 k/day, Capex: USD 23 k/day and Economic Uptime: 97%Note 3: ODN II Operational Assumptions (averages between 2017 and 2022): Opex: USD 148 k/day, Capex: USD 32 k/day and Economic Uptime: 97%; Starting on 3Q2022, projections based on new contracts and OOG’s future

recontracting assumptions. Operational Assumptions (averages between 2017 and 2026): Opex: USD 152 k/day, Capex: USD 24 k/day and Economic Uptime: 97%Note 4: Norbe VI Operational Assumptions (averages between 2017 and 2022): Opex: USD 121 k/day, Capex: USD 14 k/day and Economic Uptime: 82%; Starting on 4Q2020, projections based on new contracts and OOG’s future

recontracting assumptions. Operational Assumptions (averages between 2017 and 2026): Opex: USD 136 k/day, Capex: USD 18 k/day and Economic Uptime: 89%Note 5: Tay IV: Scrapped in 2017 with associated costs of $17m (net of scrapping proceeds).

Assumes stacking of one rig for the maximum considered period of time, with revenue reduction in exchange of optional maximum backlog extension

BOND 2022 2018 2019 2020 2021 2022 2023 2024 2025 2026

Revenues 230 282 290 331 331 294 330 343 346 348

( – ) Opex (120) (125) (138) (143) (141) (152) (158) (166) (173) (181)

Operating Cash Flow 111 157 151 187 189 142 172 177 173 167

( – ) Capex (22) (29) (24) (19) (12) (48) (15) (28) (15) (15)

Cash Flow From Assets 89 128 127 168 177 94 157 149 158 152

( – ) March LC Withdrawal Reimbursement (10) - - - - - - - - -

( +/– ) Minimum Cash Reserve ($40m) (28) 13 (13) 2 2 34 (38) - - -

( – ) Tranche 1 Cash Interest (22) (32) (26) (22) (12) (4) - - - -

( – ) Tranche 1 Fixed Amortization - (95) (43) (133) (140) (95) - - - -

( – ) Mandatory Cash Interest on Tranche 2 (9) (15) (16) (17) (18) (19) (108) (139) (140) (141)

( – ) Management Fees to ParentCo (6) (9) (8) (10) (9) (9) (9) (10) (9) (10)

Cash Flow After Mandatory Payments 15 (9) 22 (11) - - 2 1 9 1

( – ) Additional Cash interest on Tranche 2 (5) - (6) (5) - - - - - -

( – ) ECF Sweep to Tranche 1 - - - - - - - - - -

Cash Flow Before Tranche 2 Amortizations 9 (9) 16 (16) - - 2 1 9 1

( – ) ECF Sweep to Tranche 2 (90% ) - - - - - - - - (0) (5)

( – ) ECF Sweep to ParentCo (10% ) - - - - - - - - (0) (1)

Change in Excess Cash 9 (9) 16 (16) - - 2 1 9 (5)

Memo: Minimum Cash Account Balance 40 27 40 38 36 2 40 40 40 40

Memo: Excess Cash Account Balance 9 - 16 - - - 2 3 11 6

Debt Balance 2017 2018 2019 2020 2021 2022 2023 2024 2025 2026

( + ) Tranche 1 EoP 506 506 411 368 235 95 - - - - -

( + ) Tranche 2 EoP 1,390 1,446 1,546 1,647 1,755 1,876 2,005 2,054 2,075 2,095 2,111

Total Debt 1,897 1,953 1,957 2,015 1,990 1,971 2,005 2,054 2,075 2,095 2,111

2017 (May- Dec)

April 7, 2017

36

OOG ParentCo Post Restructuring Cash Flow - Case B ($ in millions)

CONFIDENTIAL SETTLEMENT COMMUNICATION SUBJECT TO FRE 408

Note 1: This cash flow statement is for illustrative purposes and represents estimates subject to significant change depending on variations on assumptions used, future measures taken by Petrobras and changes in macroeconomic factors.

(1) Net of LC Issuers reimbursements relative to pre-restructuring withdrawals.

Assumes stacking of two rigs for the maximum considered period of time, with revenue reduction in exchange of optional maximum backlog extension

OOG ParentCo 2017 (May-Dec) 2018 2019 2020 2021 2022 2023 2024 2025 2026

Sources

Cash Flow 2022 Structure (1) 4 7 5 7 6 7 9 10 9 10

Cash Flow 2021 Structure (1) 2 5 5 6 6 12 15 13 15 14

Project A - - - - - - - - - -

Project B (2) 32 28 25 33 38 42 45 58 60

Project C 2 8 12 12 13 13 14 14 14 15

Project D - - - - - - - - - -

ODB Capital Increase 30 - - - - - - - - -

Total Sources (a) 36 52 50 51 59 70 80 82 96 98

Uses

Unallocated G&A (13) (12) (14) (14) (14) (14) (14) (14) (14) (14)

Restructuring Costs (3) - - - - - - - - -

LC Costs (Other Projects) (2) (3) (3) (3) (3) (3) (3) (3) (2) (2)

LC Costs (Project Bonds) (1) (2) (2) (2) (2) (2) (2) (2) (2) (2)

FINEP & BNDES Debt Service (1) (1) (1) (1) (0) (0) - - - -

Total Uses (b) (20) (18) (20) (19) (19) (19) (19) (19) (18) (18)

OOG ParentCo Cash Flow (a)+(b) 16 34 31 31 40 51 62 64 77 80

Agenda

CONFIDENTIAL SETTLEMENT COMMUNICATION SUBJECT TO FRE 408

1. Company Overview

2. Why Restructuring

3. Summary of Restructuring

4. Restructuring Implementation Proceeding

5. Appendix

a) OOG Corporate Structure

b) Quarterly Budget

c) Overview of Contract Rates

d) Opex Detailing

38

Restructuring Implementation Proceeding

Implementation through an extrajudicial restructuring proceeding in Brazil

Extrajudicial restructuring (”ER”) is a proceeding under Brazilian Bankruptcy Law through which a debtor(or a group of debtors) can implement a restructuring agreement entered into with creditors comprisingat least 60% of the total amount of restructured debt (the ”ER Plan”) that binds all creditors subject tothe Restructuring upon judicial confirmation of the ER Plan. The judicial confirmation binds non-signatorycreditors, including opposing creditors, if applicable.

Overview of the proceeding:

The ER is filed before the Rio de Janeiro Commercial Courts (”ER Court”). The ER Court approves therequest for ER and requires that all creditors subject to the restructuring are notified about theproceeding, granting a 30-day term for challengers or requests for adhesion, as and if applicable. The ERCourt may also approve, upon request, a stay period, which prevents any enforcement proceedingagainst the Company, with respect to all claims subject to the restructuring.

After the opposition period, the ER Court grants the Company a 5-day period to submit its response. Theduration of the discussions related to opposition from creditors depends on the number and materiality ofoppositions filed.

After the discussion period, the ER Court assesses the challenges and the content of the ER Plan, andmay confirm the ER Plan (”ER Confirmation”). Upon confirmation, all terms and conditions of the ER Planbecome binding upon all creditors subject to the restructuring.

CONFIDENTIAL SETTLEMENT COMMUNICATION SUBJECT TO FRE 408

39

Restructuring Implementation Proceeding (Cont’d.)

This restructuring will be implemented through a single ER procedure comprised of 3 differentER Plans signed by creditors representing at least 60% of the total amount of claims for eachrelevant ER Plan, as follows:

• An ER Plan involving the Company entities and creditors related to the 2021 Notes, which sets forthall terms and conditions for the restructuring of claims in connection with the 2021 Notes;

• An ER Plan involving the Company entities and creditors related to the 2022 Notes, which sets forthall terms and conditions for the restructuring of claims in connection with the 2022 Notes;

• An ER Plan involving the Company and other holding entities and related financial creditors, whichsets forth all terms and conditions for the restructuring of financial claims in connection withfinancial creditors;

Holders adhesion to the ER Plans

In order to sign each of the ER Plans, holders must duly submit to the ER Court proof of their claims in the form of an ownership statement indicating the ownership and the amount of claims they hold under the 2021 or 2022 Notes, as well as other documents verifying signing entities powers, such as a certificate of incumbency, in a process known as “Individualization”. Holders must complete the Individualization procedure before the filing of the ER Plans.

Upon the signature of each ER Plan, holders will be restricted and prevented from trading their 2021 or 2022 Notes until the filing of the ER before the ER Courts. After the filing, the titles are freely transferable, provided that any transferee is fully bound to all terms and conditions of the ER Plan.

CONFIDENTIAL SETTLEMENT COMMUNICATION SUBJECT TO FRE 408

40

Restructuring Implementation Proceeding (Cont’d.)

Chapter 15 Proceeding

After the ER Confirmation, the Company will enter into an ancillary Chapter 15 Proceeding (”Chapter 15 Proceeding”) in the United States pursuant to the U.S. Bankruptcy Code, to the extent necessary for recognition of the effects of the Brazilian ER in the United States. Upon approval of the ancillary Chapter 15 Proceeding, the U.S. Bankruptcy Court will issue a court order determining the due recognition and confirmation of all effects of the ER Plans in the United States.

Mandatory Exchange before DTC.

After the issuance of the U.S. Bankruptcy Court recognition court order, the Company will conduct a mandatory exchange through DTC through which all former 2021 and 2022 notes will be substituted by New 2021 and 2022 notes subject to all terms and conditions agreed in the ER Plan.

Financial creditors will also receive new notes issued as an effect of the mandatory exchange. The procedure will be conducted through an agent via DTC, in accordance with DTC’s internal procedures.

CONFIDENTIAL SETTLEMENT COMMUNICATION SUBJECT TO FRE 408

41

Restructuring Timeline(1)

Restructuring implementation expected timeline

CONFIDENTIAL SETTLEMENT COMMUNICATION SUBJECT TO FRE 408

Deadline for submission of

creditors’ adhesions and

challenges

ER Confirmation

in Brazil

Decision granting the

ER Proceeding

• all creditors are notified about the ER Proceeding and are able to file adhesions or challenges, as applicable

• granting of stay period binds all creditors subject to the restructuring

ER Filing

10 days

(1) Estimates based in recent ER Proceedings and Chapter 15 recognitions. All estimates consider the absence of challenges or oppositions. The timing related to the Brazilian ER might be

considered in business days in accordance with recent developments under the new Brazilian civil procedure code.

(2) The filing for the Chapter 15 Proceeding might occur simultaneously with the ER Filing in Brazil, if necessary.

60 days

30 days

Chapter 15

Filing(2)

Exchange of Notes

Completed

Chapter 15 Recognition

45 days

Request for mandatory

exchange before DTC

15 days

Almost Simultaneous

Almost Simultaneous

Agenda

CONFIDENTIAL SETTLEMENT COMMUNICATION SUBJECT TO FRE 408

1. Company Overview

2. Why Restructuring

3. Summary of Restructuring

4. Restructuring Implementation Proceeding

5. Appendix

a) OOG Corporate Structure

b) Quarterly Budget

c) Overview of Contract Rates

d) Opex Detailing

43

OOG Current Complete Corporate Structure

Apicatus HoldingGmbH

ODN I Perfurações

Ltda

Cayman

UK

60%

50%

49%

ODN IODN II

NSP

OOSL

ODN Tay IV Holding

GmbH

ODN Tay IV

OOGServiços em Óleo e Gás

Ltda

Ownerships of 100%, except if otherwise noted

ODN Tay IV GmbH

NSPC

89,75%

Uruguay

Netherlands

Delba Drilling International

Coöperatie

ODN Drilling Services B.V.

ODN Delba III

53%

OOG Subsea GmbH

OOG Pipe Laying

B.V.

TechnipOdebrechtPLSV C.V.

Delba Perfuradora Internacional S.A.

49%

49,95%0,10%

50%

Neptune Drilling

Coöperatief

15%

TechnipOdebrechtPLSV B.V.

Cayman

USA

Brazil

Austria

Netherlands

UruguayUK

OOG-TKP Oil Services Ltd

50%

Norbe IX

Norbe VIII

Norbe VI

ODN VIII/IX Ltd

50% 50%

ODN Six GmbH

ODN Nine GmbH

ODN Eight GmbH

USA

OOG FPSO GmbH

50%

OOG-TKP FPSO

GmbH & Co KG

Brazil

OOG-TKP Produção de

Petróleo Ltda

OOG-TKP Operator

Holdings Ltd

Cayman

OOG-TKP FPSO GmbH

Pituba Drilling

B.V.

Boipeba Drilling

B.V.

Botinas Drilling

B.V.

Interlagos Drilling

B.V.

15% 15% 15% 15%

Odebrecht Offshore Drilling Finance Limited

50,18%

Odebrecht Drilling

Services LLC

1 quota

24,27%25,55%

Odebrecht Oil & Gas Finance Limited

OOG Offshore

Services Ltd

50%

OOGTK LIBRA

GmbH & Co KG

OOGTK LIBRA GmbH

50% 50%

OOGTK Libra Produção de

Petróleo Ltda

Ondina Drilling

B.V.

1 quota

ODN IGmbH

ODN Holding GmbH

OOG GmbH

OOG Participações

S.A.

OOG S.A.

11% 51% 51% 49%

AIAS Holding GmbH

OOG Holding S.A.

OOGTK Libra

Operator Holdings

Ltd.

Agenda

CONFIDENTIAL SETTLEMENT COMMUNICATION SUBJECT TO FRE 408

1. Company Overview

2. Why Restructuring

3. Summary of Restructuring

4. Restructuring Implementation Proceeding

5. Appendix

a) OOG Corporate Structure

b) Quarterly Budget

c) Overview of Contract Rates

d) Opex Detailing

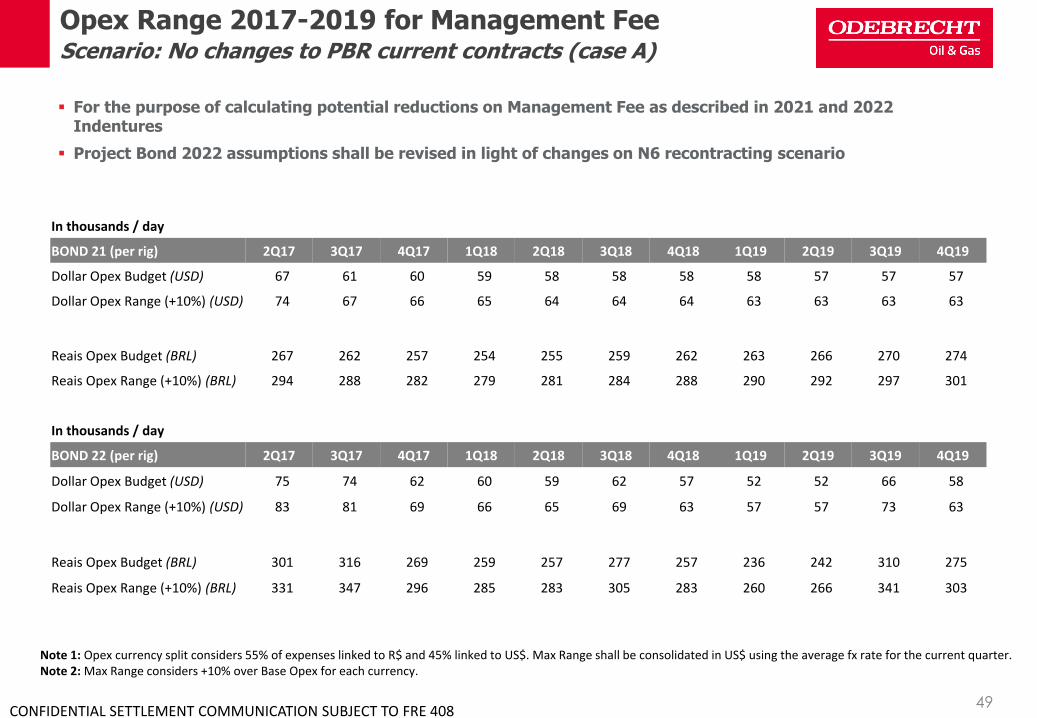

45

Bond 21 & Bond 22 Cash Flows Forecasts for MIP CalculationScenario: No changes to PBR current contracts (case A)

CONFIDENTIAL SETTLEMENT COMMUNICATION SUBJECT TO FRE 408

Note: Since MIP accruals are calculated as of March 1st, June 1st, Sep 1st and Dec 1st, abovementioned quarters include the three preceding months prior to each accrual date (i.e., 1Q = Dec/Jan/Feb; 2Q = Mar/Apr/May; 3Q = Jun/Jul/Aug; 4Q = Sep/Oct/Nov).(1) Management Incentive Plan as described in Bonds 2021 and 2022 Indentures.(2) Assumes conclusion of transaction in August with payment of advisor’s success fee on the same month.

US$ mm

BOND 21 2Q17 3Q17 4Q17 1Q18 2Q18 3Q18 4Q18 1Q19 2Q19 3Q19 4Q19

Gross Revenue 61.5 60.4 76.1 72.7 64.3 72.8 75.0 73.0 71.8 64.7 73.4

(-) WH Taxes (1.8) (1.7) (2.0) (2.0) (1.7) (1.7) (1.6) (1.4) (1.4) (1.3) (1.4)

(=) Net Revenue 59.7 58.7 74.1 70.7 62.6 71.1 73.4 71.6 70.4 63.4 72.0

(-) Opex (27.4) (25.1) (24.1) (23.5) (23.8) (23.8) (23.5) (23.0) (23.4) (23.4) (23.2)

(-) Capex (7.0) (3.0) (3.0) (8.6) (2.5) (5.4) (5.4) (2.2) (2.1) (2.1) (2.1)

(-) Restructuring Costs (2) (2.0) (4.8) - - - - - - - - -

(=) Unleveraged Free Cash Flow 23.3 25.8 47.0 38.6 36.3 41.8 44.4 46.4 44.9 37.9 46.8

US$ mm

BOND 22 2Q17 3Q17 4Q17 1Q18 2Q18 3Q18 4Q18 1Q19 2Q19 3Q19 4Q19

Gross Revenue 104.6 95.5 89.1 96.9 89.7 88.0 67.4 59.7 65.9 71.9 75.7

(-) WH Taxes (4.9) (4.5) (4.4) (4.5) (4.1) (3.2) (1.3) (1.2) (1.3) (1.8) (2.6)

(=) Net Revenue 99.7 91.0 84.7 92.4 85.6 84.9 66.1 58.6 64.6 70.2 73.1

(-) Opex (46.3) (45.3) (37.8) (36.0) (36.0) (38.3) (34.6) (31.0) (31.9) (40.4) (34.9)

(-) Capex (5.1) (4.0) (14.1) (20.2) (11.5) (4.7) (4.0) (4.6) (8.0) (5.8) (4.7)

(-) Restructuring Costs (2) (4.0) (9.7) - - - - - - - - -

(=) Unleveraged Free Cash Flow 44.2 32.1 32.7 36.2 38.1 41.9 27.5 23.0 24.7 23.9 33.5

Project Bonds unlevered free cash flow to be used for MIP(1) calculation purposes

Project Bond 2022 assumptions shall be revised in light of changes on N6 recontracting scenario

46

Norbe VIII & IX Cash Flow ForecastsScenario: No changes to PBR current contracts (case A)

CONFIDENTIAL SETTLEMENT COMMUNICATION SUBJECT TO FRE 408

US$ mm

Norbe VIII 2Q17 3Q17 4Q17 1Q18 2Q18 3Q18 4Q18 1Q19 2Q19 3Q19 4Q19

Gross Revenue 26.8 33.5 37.5 37.5 29.7 37.5 37.5 37.8 37.0 37.5 37.9

(-) WH Taxes (0.8) (0.9) (1.0) (1.0) (0.7) (0.7) (0.7) (0.7) (0.7) (0.7) (0.7)

(=) Net Revenue 25.9 32.6 36.5 36.5 29.0 36.8 36.8 37.1 36.3 36.8 37.1

(-) Opex (13.3) (12.6) (12.2) (11.6) (11.7) (11.7) (11.5) (11.6) (12.0) (12.0) (11.8)

(-) Capex (1.4) (1.9) (1.9) (4.5) (1.3) (4.2) (1.3) (1.2) (1.2) (1.2) (1.2)

(-) Restructuring Costs (2) (1.0) (2.4) - - - - - - - - -

(=) Unleveraged Free Cash Flow 10.2 15.6 22.4 20.4 16.1 20.9 24.0 24.3 23.1 23.6 24.1

US$ mm

Norbe IX 2Q17 3Q17 4Q17 1Q18 2Q18 3Q18 4Q18 1Q19 2Q19 3Q19 4Q19

Gross Revenue 34.8 26.9 38.6 35.2 34.6 35.2 37.5 35.2 34.8 27.2 35.6

(-) WH Taxes (1.0) (0.8) (1.0) (1.0) (0.9) (1.0) (0.9) (0.7) (0.7) (0.5) (0.7)

(=) Net Revenue 33.8 26.1 37.6 34.3 33.6 34.3 36.6 34.5 34.1 26.7 34.9

(-) Opex (14.1) (12.4) (11.9) (11.8) (12.1) (12.1) (12.0) (11.4) (11.5) (11.5) (11.3)

(-) Capex (5.5) (1.0) (1.0) (4.2) (1.2) (1.2) (4.2) (1.0) (0.9) (0.9) (0.9)

(-) Restructuring Costs (2) (1.0) (2.4) - - - - - - - - -

(=) Unleveraged Free Cash Flow 13.2 10.3 24.7 18.2 20.3 20.9 20.5 22.1 21.8 14.3 22.7

Note: Since MIP accruals are calculated as of March 1st, June 1st, Sep 1st and Dec 1st, abovementioned quarters include the three preceding months prior to each accrual date (i.e., 1Q = Dec/Jan/Feb; 2Q = Mar/Apr/May; 3Q = Jun/Jul/Aug; 4Q = Sep/Oct/Nov). (1) Management Incentive Plan as described in Bonds 2021 and 2022 Indentures.(2) Assumes conclusion of transaction in August with payment of advisor’s success fee on the same month.

Detailed cash flow forecast, for informative purposes only

47

ODN I & II Cash Flow ForecastsScenario: No changes to PBR current contracts (case A)

CONFIDENTIAL SETTLEMENT COMMUNICATION SUBJECT TO FRE 408

US$ mm

ODN I 2Q17 3Q17 4Q17 1Q18 2Q18 3Q18 4Q18 1Q19 2Q19 3Q19 4Q19

Gross Revenue 36.9 32.1 32.5 29.7 34.1 33.4 33.7 26.1 32.9 33.4 33.7

(-) WH Taxes (0.9) (0.9) (0.9) (0.8) (0.8) (0.7) (0.7) (0.5) (0.6) (0.7) (0.7)

(=) Net Revenue 35.9 31.3 31.6 28.9 33.3 32.7 33.0 25.6 32.3 32.7 33.0

(-) Opex (13.5) (13.5) (13.0) (12.2) (12.1) (12.1) (12.0) (11.6) (11.8) (11.8) (11.7)

(-) Capex (1.0) (1.1) (11.3) (8.2) (2.1) (2.1) (2.1) (1.6) (1.4) (1.4) (1.4)

(-) Restructuring Costs (2) (1.0) (2.4) - - - - - - - - -

(=) Unleveraged Free Cash Flow 20.5 14.2 7.3 8.6 19.1 18.5 19.0 12.3 19.1 19.5 20.0

US$ mm

ODN II 2Q17 3Q17 4Q17 1Q18 2Q18 3Q18 4Q18 1Q19 2Q19 3Q19 4Q19

Gross Revenue 32.8 32.1 24.9 32.5 24.8 33.4 33.7 33.7 32.9 33.4 26.1

(-) WH Taxes (0.9) (0.9) (0.7) (0.9) (0.6) (0.7) (0.7) (0.7) (0.6) (0.7) (0.5)

(=) Net Revenue 31.9 31.2 24.1 31.6 24.2 32.7 33.0 33.0 32.3 32.7 25.6

(-) Opex (15.5) (14.2) (13.7) (12.8) (12.7) (12.7) (12.6) (12.1) (12.1) (12.1) (12.0)

(-) Capex (3.0) (1.4) (1.4) (10.4) (7.5) (1.9) (1.9) (1.5) (1.3) (1.3) (1.3)

(-) Restructuring Costs (2) (1.0) (2.4) - - - - - - - - -

(=) Unleveraged Free Cash Flow 12.4 13.2 9.0 8.4 3.9 18.1 18.5 19.5 18.9 19.3 12.4

Detailed cash flow forecast, for informative purposes only

Note: Since MIP accruals are calculated as of March 1st, June 1st, Sep 1st and Dec 1st, abovementioned quarters include the three preceding months prior to each accrual date (i.e., 1Q = Dec/Jan/Feb; 2Q = Mar/Apr/May; 3Q = Jun/Jul/Aug; 4Q = Sep/Oct/Nov). (1) Management Incentive Plan as described in Bonds 2021 and 2022 Indentures.(2) Assumes conclusion of transaction in August with payment of advisor’s success fee on the same month.

48

Norbe VI & ODN Tay IV Cash Flow ForecastsScenario: No changes to PBR current contracts (case A)

CONFIDENTIAL SETTLEMENT COMMUNICATION SUBJECT TO FRE 408

US$ mm

Norbe VI 2Q17 3Q17 4Q17 1Q18 2Q18 3Q18 4Q18 1Q19 2Q19 3Q19 4Q19

Gross Revenue 34.9 31.2 31.8 31.7 30.9 21.3 - - - 5.2 16.0

(-) WH Taxes (3.1) (2.7) (2.8) (2.8) (2.7) (1.8) - - - (0.5) (1.4)

(=) Net Revenue 31.8 28.5 28.9 28.9 28.2 19.4 - - - 4.8 14.5

(-) Opex (13.6) (11.6) (11.1) (10.9) (11.2) (13.4) (10.0) (7.3) (8.0) (16.5) (11.3)

(-) Capex (0.8) (1.4) (1.4) (1.7) (1.9) (0.6) - (1.5) (5.3) (3.2) (2.1)

(-) Restructuring Costs (2) (1.0) (2.4) - - - - - - - - -