ONTARIO GUIDE TO CASE COSTING Ministry of Health and Long ... · 5.3.1 Operating Room ... case...

158

ONTARIO GUIDE TO CASE COSTING Ministry of Health and Long-Term Care Version 6.1 Fiscal Year 2008/2009

Transcript of ONTARIO GUIDE TO CASE COSTING Ministry of Health and Long ... · 5.3.1 Operating Room ... case...

ONTARIO GUIDE TO CASE COSTING

Ministry of Health and Long-Term Care

Version 6.1 Fiscal Year 2008/2009

MINISTRY OF HEALTH AND LONG-TERM CARE Ontario Guide to Case Costing Health System Information Management and Investment Division Health Data Branch

Changes for Fiscal Year 2008/09 are highlighted in yellow

ONTARIO GUIDE TO CASE COSTING

Table of Contents THIS GUIDE ...............................................................................................................................................................5

HOW THIS MANUAL IS ORGANIZED .................................................................................................................5

CHAPTER 1: WHY THE INVESTMENT IN CASE COSTING? .........................................................................7

CHAPTER 2: OVERVIEW OF THE CASE COSTING METHODOLOGY .......................................................8 2.1 Conceptual Model of Case Costing .....................................................................................................................8 2.2 Introduction to the OCCI Case Costing Methodology.........................................................................................9 2.3 Four Steps of Case Costing................................................................................................................................13 2.4 Evolution of the OCCI Case Costing Methodology ..........................................................................................13

2.4.1 Changing Hospital Production—Program Management ......................................................................14 2.4.2 Extending the Methodology to Ambulatory, Complex continuing Care, Mental Health and Rehabilitation.....................................................................................................................................................14 2.4.3 A Framework for “Case” Costing ...........................................................................................................15

CHAPTER 3: STEP 1: GATHER THE DATA ......................................................................................................16 3.1 Financial Data....................................................................................................................................................16

3.1.1 MIS Standards ..........................................................................................................................................16 3.1.2 Functional Centre Cost Assignment........................................................................................................18 Allowable Recoveries and Revenues in Case Costing .....................................................................................23 3.1.3 Separating Inpatient, Outpatient and Non-Patient Operating Costs ...................................................23 3.1.4 Patient Revenue ........................................................................................................................................24 3.1.5 Other Hospital Costs ................................................................................................................................24

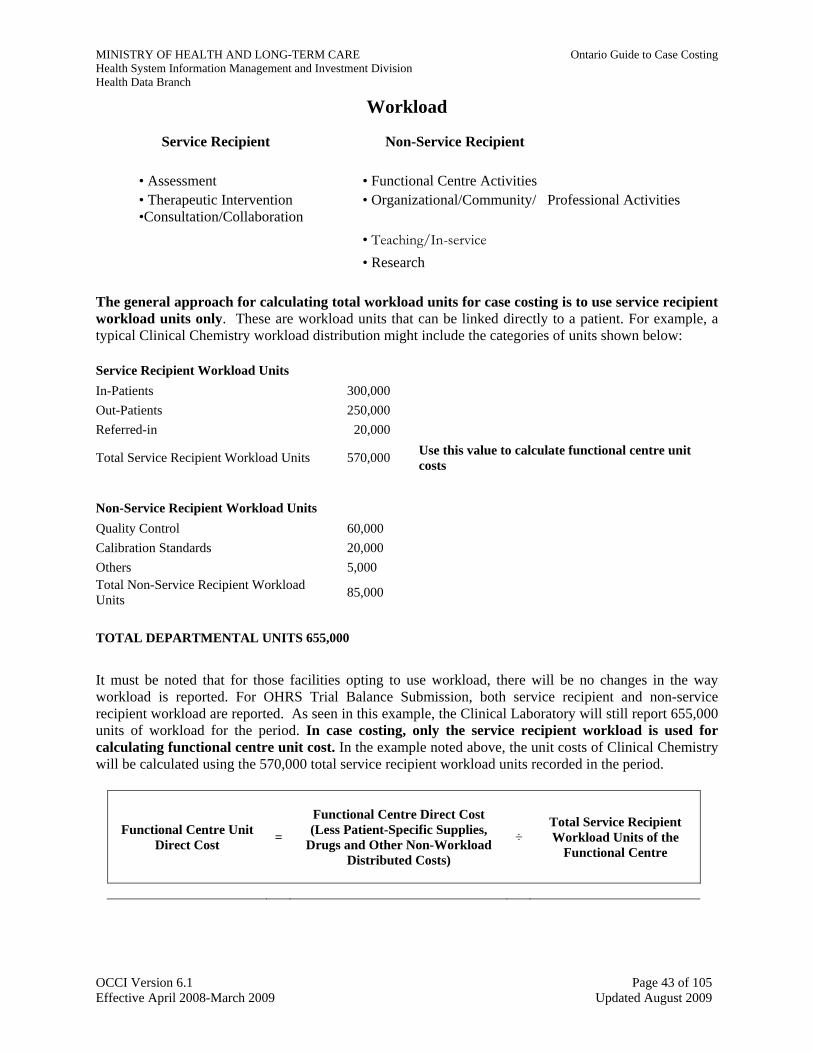

3.2 Cost Distribution Bases .....................................................................................................................................26 3.2.1 Workload ...................................................................................................................................................26 3.2.2 Patient Hours Data ...................................................................................................................................30

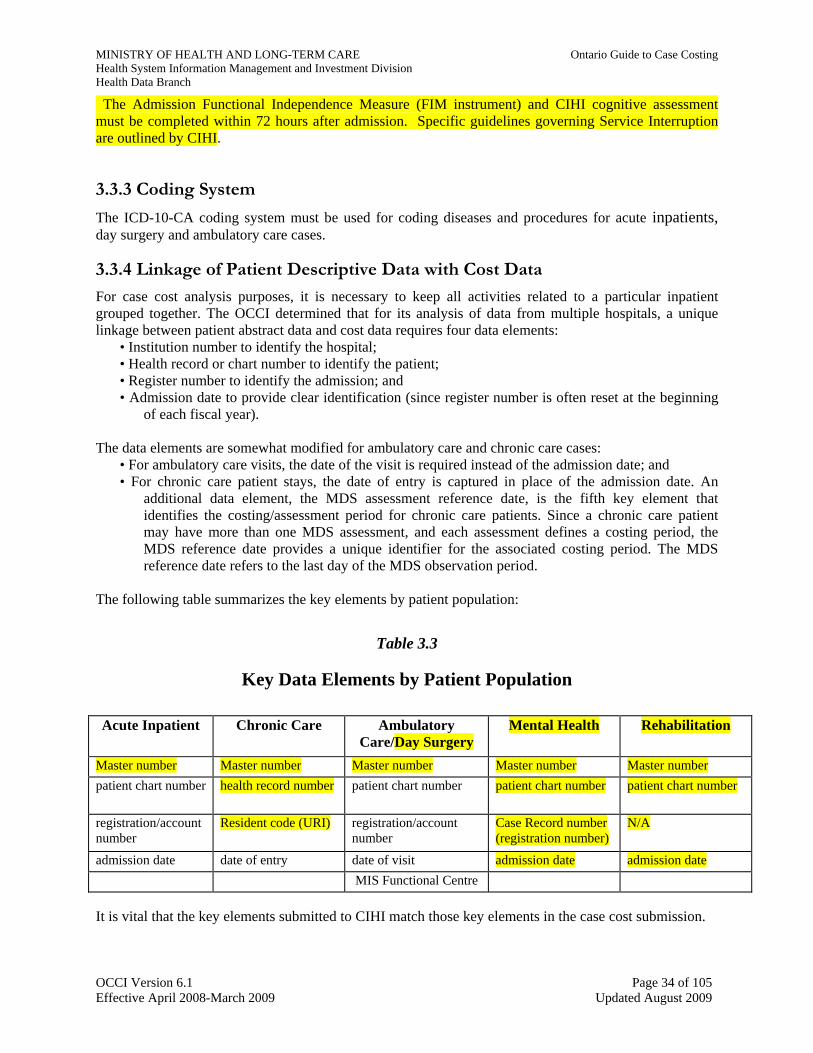

3.3 Patient Descriptive Data ....................................................................................................................................30 3.3.1 Data Quality ..............................................................................................................................................30 3.3.2 CIHI and OCCI Coding Requirements ..................................................................................................31 3.3.3 Coding System...........................................................................................................................................34 3.3.4 Linkage of Patient Descriptive Data with Cost Data .............................................................................34 3.3.5 Useful Additional Patient Descriptive Data............................................................................................35

CHAPTER 4: STEP 2: ALLOCATE INDIRECT COSTS....................................................................................36 4.1 Allocation of Indirect Costs vs. Distribution of Direct Costs ............................................................................36 4.2 Indirect Cost Allocation Using SEAM ..............................................................................................................36 4.3 Indirect Cost Allocation Bases ..........................................................................................................................36 4.4 What TCC Costs are to be Allocated as Indirect Costs?....................................................................................37

CHAPTER 5: STEP 3: CALCULATE FUNCTIONAL CENTRE UNIT COSTS OR INTERMEDIATE PRODUCT COSTS ...................................................................................................................................................40

5.1 The General Ledger, Accounting Guidelines, and Variable and Fixed Costs ...................................................40 5.2 Functional Centre Unit Costs.............................................................................................................................41

5.2.2 The Functional Centre Unit Cost Calculation........................................................................................42 5.2.3 Type 1 - Using Nursing Workload to Calculate Functional Centre Unit Cost ....................................42

5.3 Using the Patient Hours Methodology...............................................................................................................45

OCCI Version 6.1 Page 2 of 105 Effective April 2008-March 2009 Updated August 2009

MINISTRY OF HEALTH AND LONG-TERM CARE Ontario Guide to Case Costing Health System Information Management and Investment Division Health Data Branch

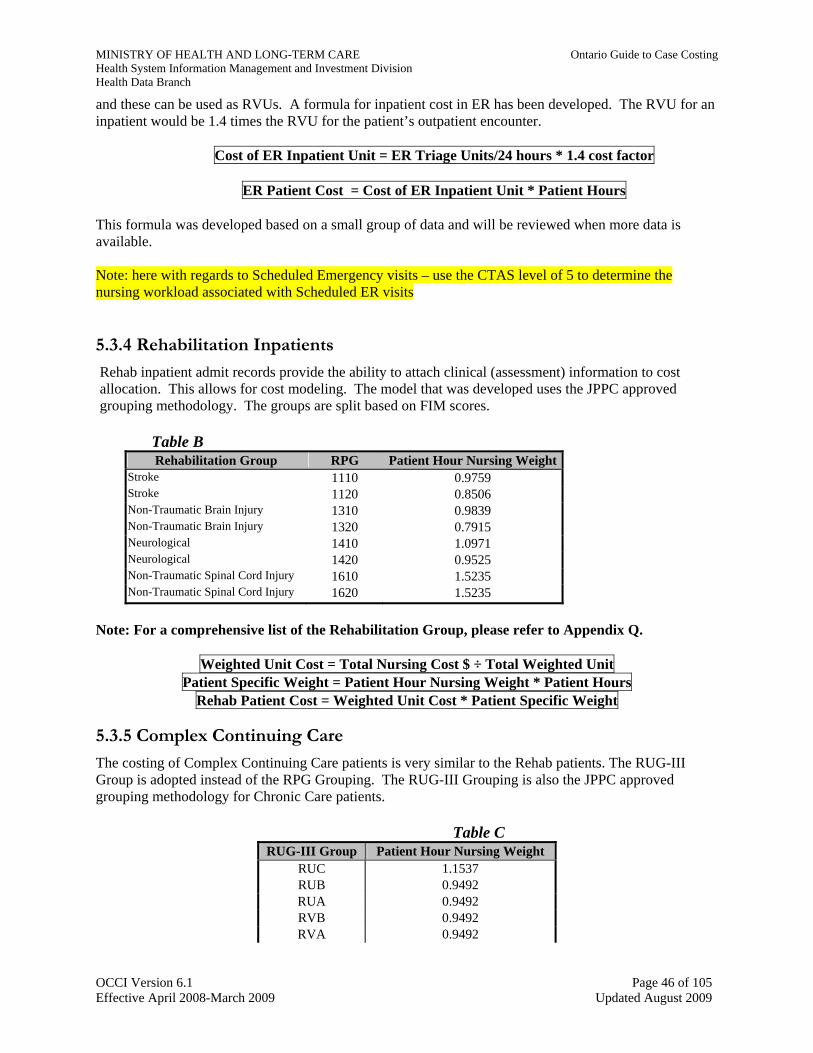

5.3.1 Operating Room........................................................................................................................................45 5.3.2 Obstetrics...................................................................................................................................................45 5.3.3 Emergency Room......................................................................................................................................45 5.3.4 Rehabilitation Inpatients..........................................................................................................................46 5.3.5 Complex Continuing Care .......................................................................................................................46

5.4 Method 2: Calculating Intermediate Product Costs ...........................................................................................47 5.4.1 Information Required to Calculate Intermediate Product Costs .........................................................47 5.4.2 Intermediate Product Cost Calculation ..................................................................................................48

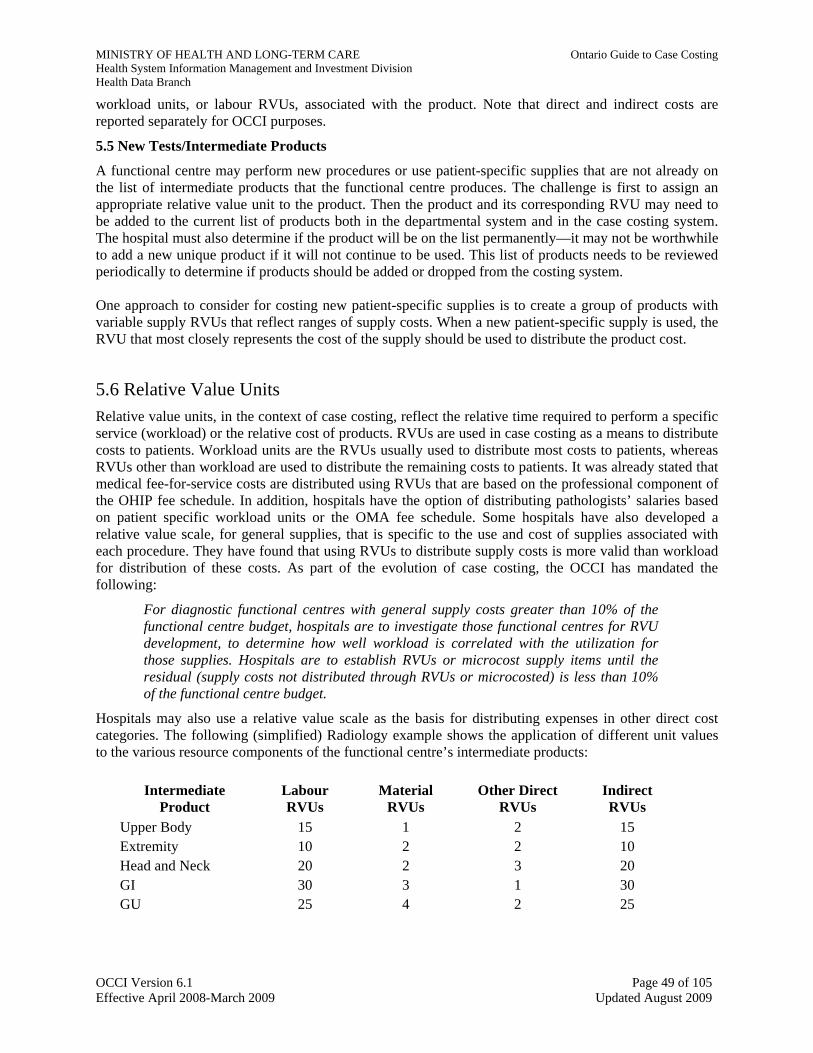

5.5 New Tests/Intermediate Products ......................................................................................................................49 5.6 Relative Value Units..........................................................................................................................................49

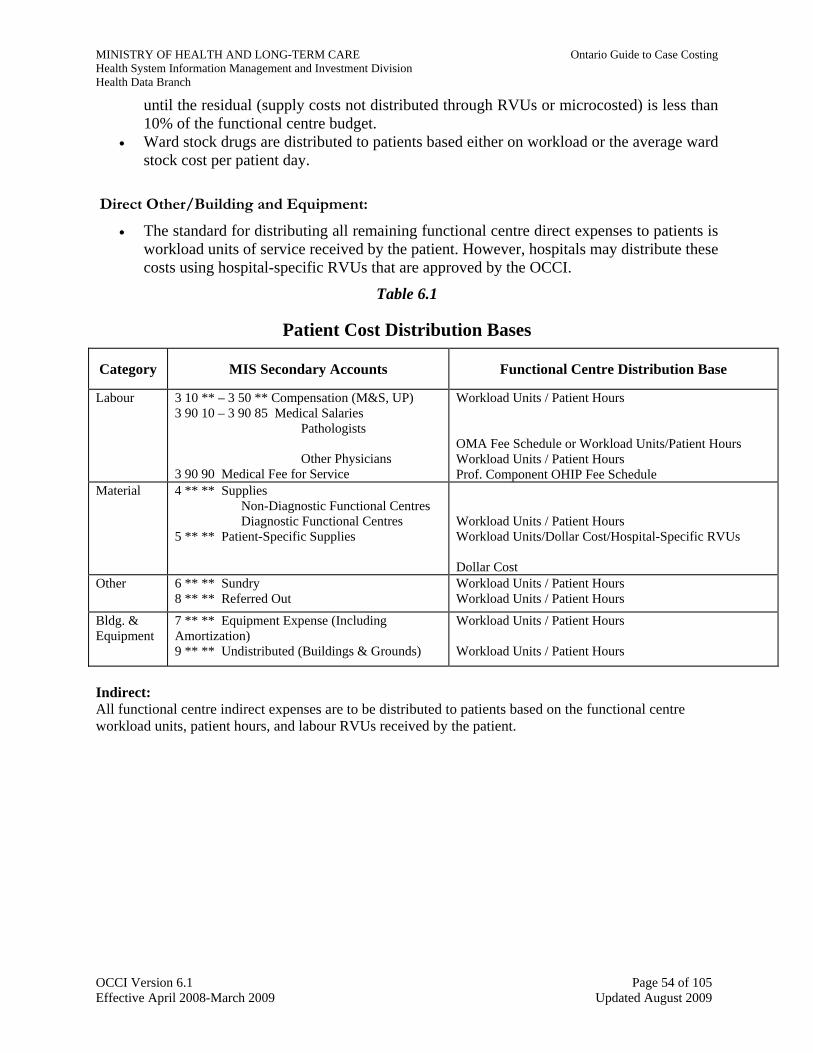

CHAPTER 6: STEP 4: DISTRIBUTE COSTS TO PATIENTS...........................................................................51 6.1.1 Type 1: Distributing Functional Centre Unit Cost to Patients based on Workload ........................................51 6.1.2 Type 2: Distributing Functional Centre Unit Cost to Patients based on Patient Hours ..................................52 6.2 Intermediate Product Costing ............................................................................................................................53 6.3 Patient Cost Distribution Bases .........................................................................................................................53

CHAPTER 7: BRINGING IT ALL TOGETHER..................................................................................................55 7.1 Departmental Data is Interfaced with the Case Costing System........................................................................55 7.2 Options for Reporting Case Costs .....................................................................................................................56

7.2.1 Costs by Day of Stay (Submission Requirement effective FY 05/06) ...................................................56 7.2.2 Variable/Fixed Detail - Option for Internal Reporting .........................................................................57 7.2.3 Service-Specific Data Elements ...............................................................................................................57 7.2.4 Procedure Detail .......................................................................................................................................58

7.3 A Framework for “Case” Costing......................................................................................................................58 CHAPTER 8: DEPARTMENTAL CASE COSTING STANDARDS ..................................................................61

8.1 Nursing Inpatient Functional Centres ................................................................................................................61 8.2 Allied Health......................................................................................................................................................61 8.3 Clinical Nutrition...............................................................................................................................................62 8.4 Clinical Laboratory............................................................................................................................................62 8.5 Diagnostic Imaging............................................................................................................................................65 8.6 Financial Services..............................................................................................................................................67 8.7 Health Records ..................................................................................................................................................67

8.7.1 Ensuring Quality of Patient Descriptive Data ........................................................................................67 8.7.2 Coding of Basic and Optional Data Items Needed for Case Costing....................................................68 8.7.3 CIHI Mandatory Data..............................................................................................................................68

8.8 Information Systems..........................................................................................................................................69 8.9 Pharmacy/Drug Costs ........................................................................................................................................70

CHAPTER 9: AMBULATORY, CHRONIC CARE AND MENTAL HEALTH STANDARDS.......................74 9.1 Ambulatory Care ...............................................................................................................................................74 9.2 Mental Health and Chronic Care .......................................................................................................................75

CHAPTER 10: COSTING IN A PROGRAM MANAGEMENT HOSPITAL ....................................................79 10.1 Gathering Data................................................................................................................................................79 10.2 Allocating Indirect Costs .................................................................................................................................80 10.3 Calculating and Distributing Product Costs.....................................................................................................80 10.4 Product Line Costing .......................................................................................................................................81

CHAPTER 11: IMPLEMENTING CASE COSTING...........................................................................................82 11.1 Challenges of Implementation .........................................................................................................................82 11.2 Implementation Time-Frames..........................................................................................................................83 11.3 Implementation Sequence................................................................................................................................84 11.4 Education/Promotion/Orientation....................................................................................................................84 11.5 Data Flow Models and Methodologies ............................................................................................................85

OCCI Version 6.1 Page 3 of 105 Effective April 2008-March 2009 Updated August 2009

MINISTRY OF HEALTH AND LONG-TERM CARE Ontario Guide to Case Costing Health System Information Management and Investment Division Health Data Branch

CHAPTER 12: EVALUATING CASE COSTING.................................................................................................87 12.1 The Approach to Evaluation ............................................................................................................................87 12.2 MIS Functional Centre Framework .................................................................................................................88 12.3 Patient Identification for Linkage ....................................................................................................................89 12.4 Workload Measurement...................................................................................................................................89 12.5 General and Patient-Specific Supply Costs .....................................................................................................90 12.6 Labour Hours...................................................................................................................................................91

CHAPTER 13: FREQUENTLY ASKED QUESTIONS........................................................................................93

APPENDIX 1: THE CASE COSTING METHODOLOGY IN ACTION: A NUMERICAL EXAMPLE........96

APPENDIX 2: ALLOWABLE RECOVERIES AND REVENUES IN CASE COSTING (FOR 2008/09) ....104

OCCI Version 6.1 Page 4 of 105 Effective April 2008-March 2009 Updated August 2009

MINISTRY OF HEALTH AND LONG-TERM CARE Ontario Guide to Case Costing Health System Information Management and Investment Division Health Data Branch

This Guide

In keeping with the previous version of the Ontario Guide to Case Costing, this manual is intended to serve as a primary resource for learning and implementing case costing. It presents the methodology used to produce case costs and many of the important details that should be considered to get case costing started. As the Guide is reviewed, there are additional materials, such as the Canadian Institute for Health Information’s MIS (Management Information System) Standards and Ontario’s version of the MIS Standards, the Ontario Healthcare Reporting Standards (OHRS), that can be used as a reference to compliment the Guide. A list of these reference materials is found in Appendix A. Case costing relies on financial, clinical and statistical data. Prior to costing, there must be a review of departmental information and data collection and reporting systems. This manual is a practical reference and guidance to:

• Evaluate current systems capability • Develop an action plan • Implement the systems and procedure changes needed for case costing

This Guide has been revised from earlier versions. The principal changes in this version occur in the following areas:

• Presentation of the conceptual basis of the case costing methodology • A more thorough presentation of the costing standards • An example of the case cost calculation • The standards for chronic care mental health and ambulatory care costing • The standards for Patient Hours as the alternative approach to nursing cost allocation • The case costing methodology applied to program management • A chapter dedicated to answering frequently asked questions

It is expected that modifications to the case costing standards will continue to be made as hospitals change their approach to service delivery. The case costing standards must adapt to hospital innovations so that case cost data remains relevant and useful for management decision-making at all levels. The Guide reflects the knowledge and experience of the Ontario Case Cost Initiative hospital participants. A history of the Project and a profile of OCCI hospitals are found in Appendices B and C. With the contribution of the OCCI hospitals to the Guide, it will fulfill its purpose: to provide readers with a good understanding of case costing, and the issues and details of implementing case costing in the hospital.

How this Manual is Organized

The material in this manual is presented in logical progression.

Chapter Content 1 Outlines the potential uses of case costing data at the hospital level 2 Provides an overview of the case costing methodology.

Describe in detail the four general steps of the OCCI case costing methodology: • gathering and organizing data (Chapter 3) • allocating indirect costs (Chapter 4)

3 to 6 • calculating functional centre unit costs/intermediate product costs (Chapter 5)

• distributing costs to patients (Chapter 6) A numerical example illustrating the case costing methodology is presented in Appendix 1.

7 Describes the process of bringing together statistical, financial and clinical data; discusses the final output of the case cost data.

OCCI Version 6.1 Page 5 of 105 Effective April 2008-March 2009 Updated August 2009

MINISTRY OF HEALTH AND LONG-TERM CARE Ontario Guide to Case Costing Health System Information Management and Investment Division Health Data Branch

8 Provides the case costing standards for nursing, allied health, clinical nutrition, clinical laboratory, diagnostic imaging, financial services, health records, information systems and pharmacy.

9 Explains the costing requirements for ambulatory care, chronic care and mental health.

10 Describes the application of the case costing methodology to hospitals organized by program.

11 Discusses a general approach to implementing case costing

12 Provides tips to help evaluate the newly implemented case costing.

13

Presents Project Managers’ frequently asked questions in a question and answer format where questions are related to the implementation of the case costing methodology.

OCCI Version 6.1 Page 6 of 105 Effective April 2008-March 2009 Updated August 2009

MINISTRY OF HEALTH AND LONG-TERM CARE Ontario Guide to Case Costing Health System Information Management and Investment Division Health Data Branch

Chapter 1: Why the investment in case costing?

In recent years, case costing has generated considerable interest and enthusiasm. It provides much needed data to inform decision-making at all levels in the hospital. Hospital managers have turned to case costing information when faced with important decisions about the types of services to deliver and how to deliver them. Many hospitals with case costing systems find the information invaluable for strategic and operational planning and management, especially in the current environment of decreasing resources, increased demand for services, and greater emphasis on quality. Case cost data has also been used to demonstrate good value for resources used, which is increasingly relevant in today’s focus on accountability in health care.

Hospitals already have financial and management reporting structures in place for tallying costs and reporting by functional centre (also known as department or cost centre) so why implement case costing if departmental financial information is readily available? The reason is that case costing allows another perspective when analyzing financial information. Case costing provides answers to important management and planning questions that cannot traditionally be answered with departmental management and financial information alone. These questions include:

• What are our top patient businesses (e.g., by program, referral area, funding source, etc.)? • What are our revenues and expenses in each business area? • Is there an opportunity to improve resource utilization for specific patients or groups of patients? • What are the variations in resource use among clinically similar patients? How can these variations be

reduced to increase overall quality and to direct our resources more appropriately? • What are the cost impacts of realigning programs? • What is a fair price to charge an out-of-country patient for a craniotomy? • How do case costs compare to our peers for similar patients? • What are the differences in costs between treatment options for a particular type of case? • Is it more expensive to provide certain laboratory services in-house or to purchase them from another

facility?

Case costing provides information to support many kinds of analysis and initiatives. OCCI hospitals also report using case cost data for the following activities:

• Evaluation/development of patient care treatment maps/critical care paths • Development of program budgets and variance reporting • Feasibility and impact analysis, e.g., adding a new program, physician, etc. • Productivity analysis/evaluation of program efficiency • Modeling (“what if...”) and forecasting • Evaluation of moving from inpatient to outpatient procedures • Comparison of hospital position (costs) vs. funding

Not only is case cost data important for hospital decision-making, but it can also be used in health care system reform efforts by providing support to hospital funding, research and policy development initiatives. More information on current and expected uses and analyses of case cost data can be found in Appendix D. Implementation of case costing does not need to be cumbersome. It takes effort to gather patient-specific cost and workload data, but the overall impact can be managed by carefully designing these systems. The key is to gather patient-specific data as a by-product of care delivery documentation and communications. This manual provides some helpful tips for successful implementation of case costing. The case costing approach described in this Guide generates case costs by integrating financial, clinical and statistical data. With case costing fully in place, new views can be generated to help answer operational management and planning questions while still providing the necessary departmental management information that the hospital is accustomed to using.

OCCI Version 6.1 Page 7 of 105 Effective April 2008-March 2009 Updated August 2009

MINISTRY OF HEALTH AND LONG-TERM CARE Ontario Guide to Case Costing Health System Information Management and Investment Division Health Data Branch

Chapter 2: Overview of the Case Costing Methodology

In order to develop good cost data, first identify and understand what will be costed. Once a solid understanding of the context in which patient-specific costs are generated, explore the methodology that will assist in developing case costs. The OCCI standards are rules specific to the OCCI that are largely based on the MIS Standards and the OHRS. The OCCI methodology is operationalized through the OCCI standards that have been developed to ensure comparability and quality of the data. This chapter presents the conceptual model on which the OCCI case costing methodology is based. Then, the four steps to the case costing methodology are introduced. Lastly, the current issues identified in the evolution of case costing are explored.

2.1 Conceptual Model of Case Costing

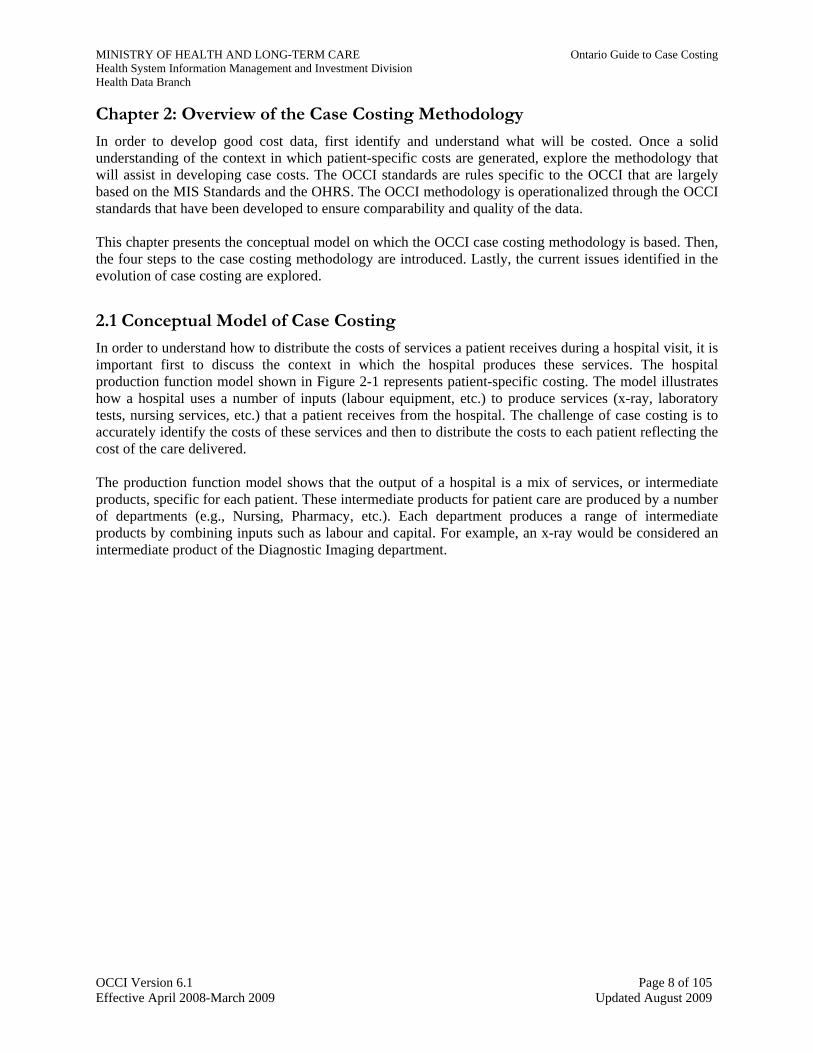

In order to understand how to distribute the costs of services a patient receives during a hospital visit, it is important first to discuss the context in which the hospital produces these services. The hospital production function model shown in Figure 2-1 represents patient-specific costing. The model illustrates how a hospital uses a number of inputs (labour equipment, etc.) to produce services (x-ray, laboratory tests, nursing services, etc.) that a patient receives from the hospital. The challenge of case costing is to accurately identify the costs of these services and then to distribute the costs to each patient reflecting the cost of the care delivered. The production function model shows that the output of a hospital is a mix of services, or intermediate products, specific for each patient. These intermediate products for patient care are produced by a number of departments (e.g., Nursing, Pharmacy, etc.). Each department produces a range of intermediate products by combining inputs such as labour and capital. For example, an x-ray would be considered an intermediate product of the Diagnostic Imaging department.

OCCI Version 6.1 Page 8 of 105 Effective April 2008-March 2009 Updated August 2009

MINISTRY OF HEALTH AND LONG-TERM CARE Ontario Guide to Case Costing Health System Information Management and Investment Division Health Data Branch

Figure 2-1

Hospital Production Function Model

The patient-specific mix of intermediate products received is driven by a number of patient characteristics that are unique for each encounter or visit. These characteristics include demographic (e.g., sex, age) and clinical (e.g., diagnoses) information. For instance, the types and quantities of products provided to a stroke patient will differ from those provided to a mother delivering a child. In addition to consuming inputs, these patient care departments also consume services from a number of departments that do not directly produce intermediate products for patient care. These are the traditional overhead, or support and administration, departments such as Finance and Housekeeping. The services produced by these departments are the indirect costs incurred by each of the patient care departments.

2.2 Introduction to the OCCI Case Costing Methodology

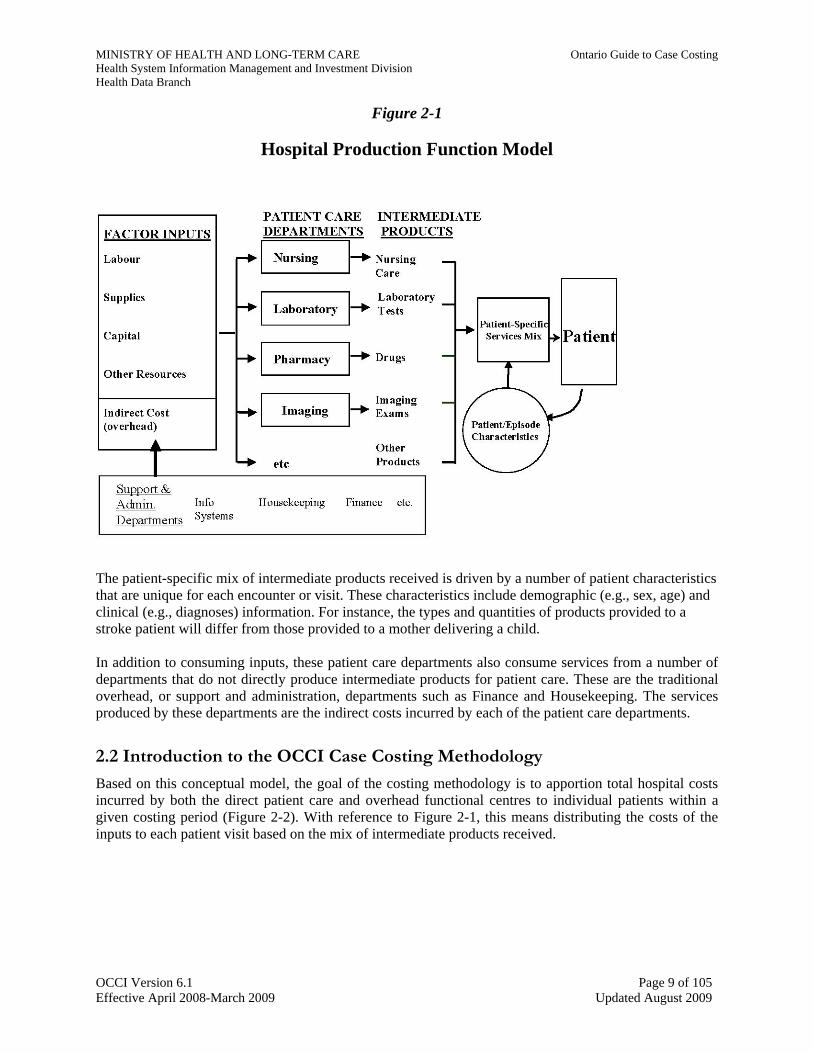

Based on this conceptual model, the goal of the costing methodology is to apportion total hospital costs incurred by both the direct patient care and overhead functional centres to individual patients within a given costing period (Figure 2-2). With reference to Figure 2-1, this means distributing the costs of the inputs to each patient visit based on the mix of intermediate products received.

OCCI Version 6.1 Page 9 of 105 Effective April 2008-March 2009 Updated August 2009

MINISTRY OF HEALTH AND LONG-TERM CARE Ontario Guide to Case Costing Health System Information Management and Investment Division Health Data Branch

Figure 2-2

The Goal

To accomplish this, the OCCI has developed a case costing methodology based largely on the Canadian Institute for Health Information’s (CIHI) MIS Standards (Standards for Management Information Systems in Canadian Health Service Organizations). The methodology relies on two important features of the MIS Standards: the Functional Centre Framework and the Chart of Accounts.

The MIS Standards and the Case Costing Methodology

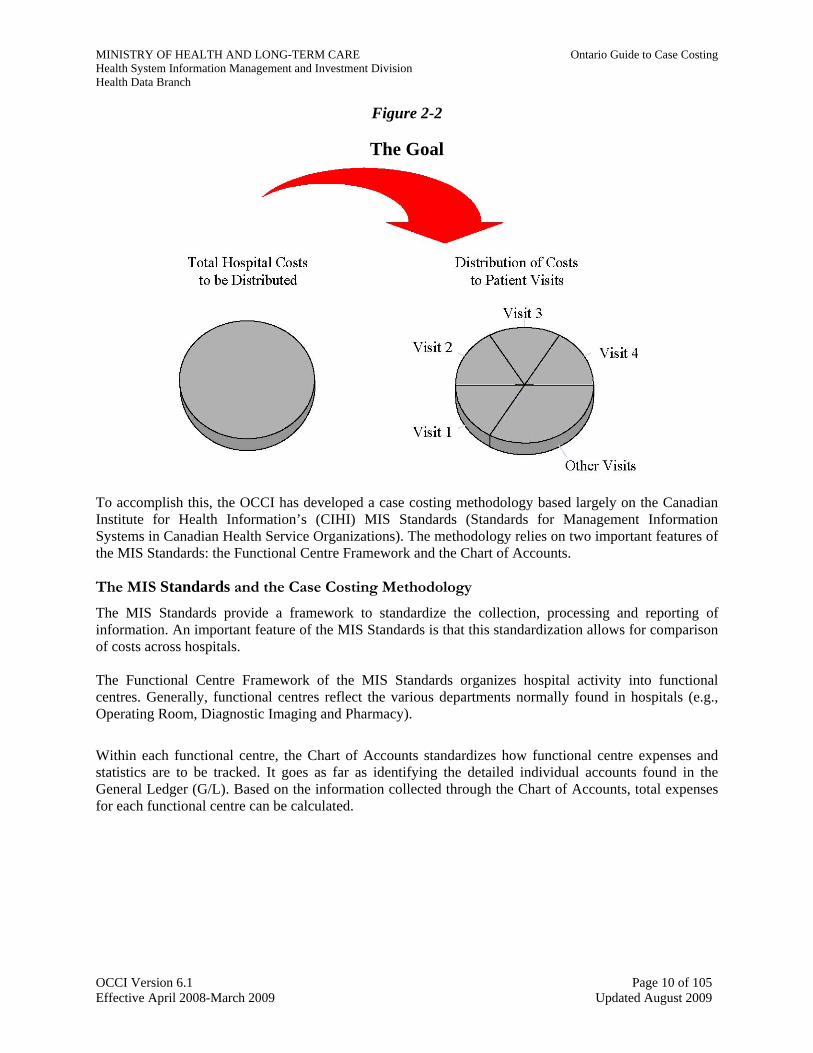

The MIS Standards provide a framework to standardize the collection, processing and reporting of information. An important feature of the MIS Standards is that this standardization allows for comparison of costs across hospitals. The Functional Centre Framework of the MIS Standards organizes hospital activity into functional centres. Generally, functional centres reflect the various departments normally found in hospitals (e.g., Operating Room, Diagnostic Imaging and Pharmacy).

Within each functional centre, the Chart of Accounts standardizes how functional centre expenses and statistics are to be tracked. It goes as far as identifying the detailed individual accounts found in the General Ledger (G/L). Based on the information collected through the Chart of Accounts, total expenses for each functional centre can be calculated.

OCCI Version 6.1 Page 10 of 105 Effective April 2008-March 2009 Updated August 2009

MINISTRY OF HEALTH AND LONG-TERM CARE Ontario Guide to Case Costing Health System Information Management and Investment Division Health Data Branch

Figure 2-3

Total Hospital Costs are Tracked by Functional Centre

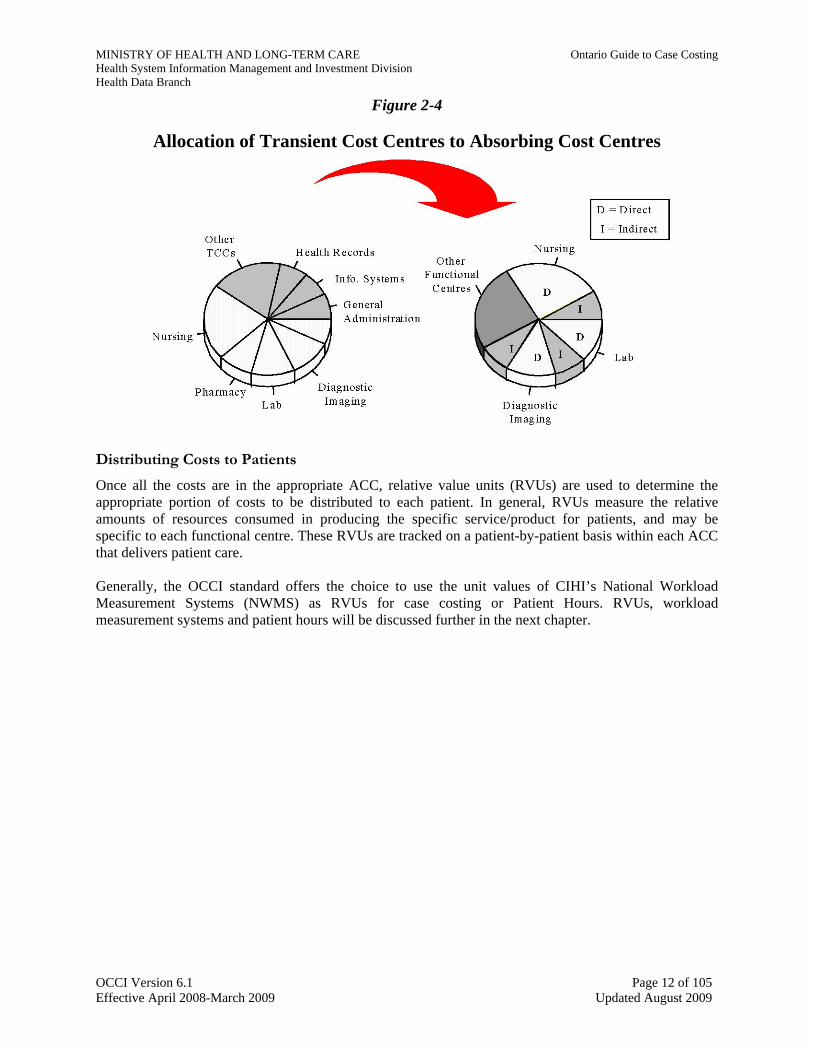

Allocating Indirect Costs Functional centres are categorized as either transient cost centres (TCCs) or absorbing cost centres (ACCs). TCCs are generally the support and administrative, or overhead, departments within a hospital. ACCs are generally the patient care departments. Once each functional centre is designated as either a TCC or ACC, a methodology is required which allocates a portion of each TCCs expenses to each ACC. The resulting allocated expenses are referred to as indirect costs. The original ACC costs are referred to as direct costs. The direct costs and the allocated indirect costs make up the full costs of the ACC. The OCCI uses the Simultaneous Equation Allocation Methodology (SEAM) to allocate the indirect costs. Each TCCs costs are allocated to each of the ACCs based on a system of linear equations.

OCCI Version 6.1 Page 11 of 105 Effective April 2008-March 2009 Updated August 2009

MINISTRY OF HEALTH AND LONG-TERM CARE Ontario Guide to Case Costing Health System Information Management and Investment Division Health Data Branch

Figure 2-4

Allocation of Transient Cost Centres to Absorbing Cost Centres

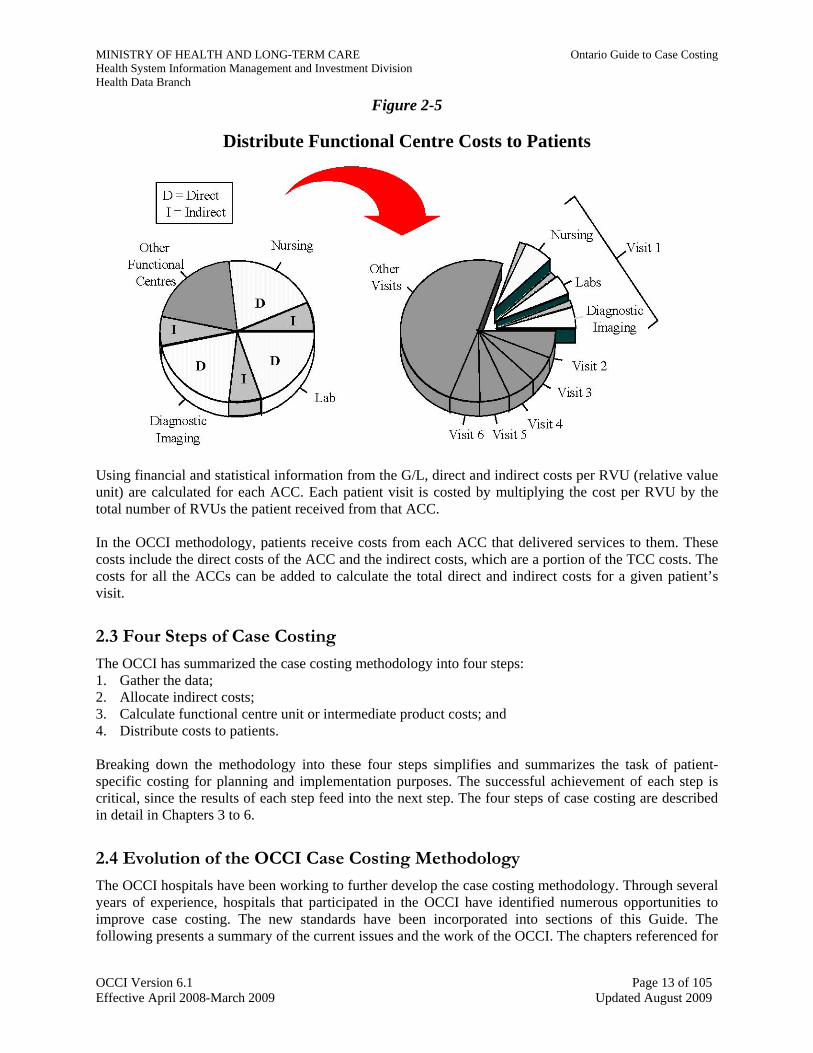

Distributing Costs to Patients Once all the costs are in the appropriate ACC, relative value units (RVUs) are used to determine the appropriate portion of costs to be distributed to each patient. In general, RVUs measure the relative amounts of resources consumed in producing the specific service/product for patients, and may be specific to each functional centre. These RVUs are tracked on a patient-by-patient basis within each ACC that delivers patient care. Generally, the OCCI standard offers the choice to use the unit values of CIHI’s National Workload Measurement Systems (NWMS) as RVUs for case costing or Patient Hours. RVUs, workload measurement systems and patient hours will be discussed further in the next chapter.

OCCI Version 6.1 Page 12 of 105 Effective April 2008-March 2009 Updated August 2009

MINISTRY OF HEALTH AND LONG-TERM CARE Ontario Guide to Case Costing Health System Information Management and Investment Division Health Data Branch

Figure 2-5

Distribute Functional Centre Costs to Patients

Using financial and statistical information from the G/L, direct and indirect costs per RVU (relative value unit) are calculated for each ACC. Each patient visit is costed by multiplying the cost per RVU by the total number of RVUs the patient received from that ACC. In the OCCI methodology, patients receive costs from each ACC that delivered services to them. These costs include the direct costs of the ACC and the indirect costs, which are a portion of the TCC costs. The costs for all the ACCs can be added to calculate the total direct and indirect costs for a given patient’s visit.

2.3 Four Steps of Case Costing

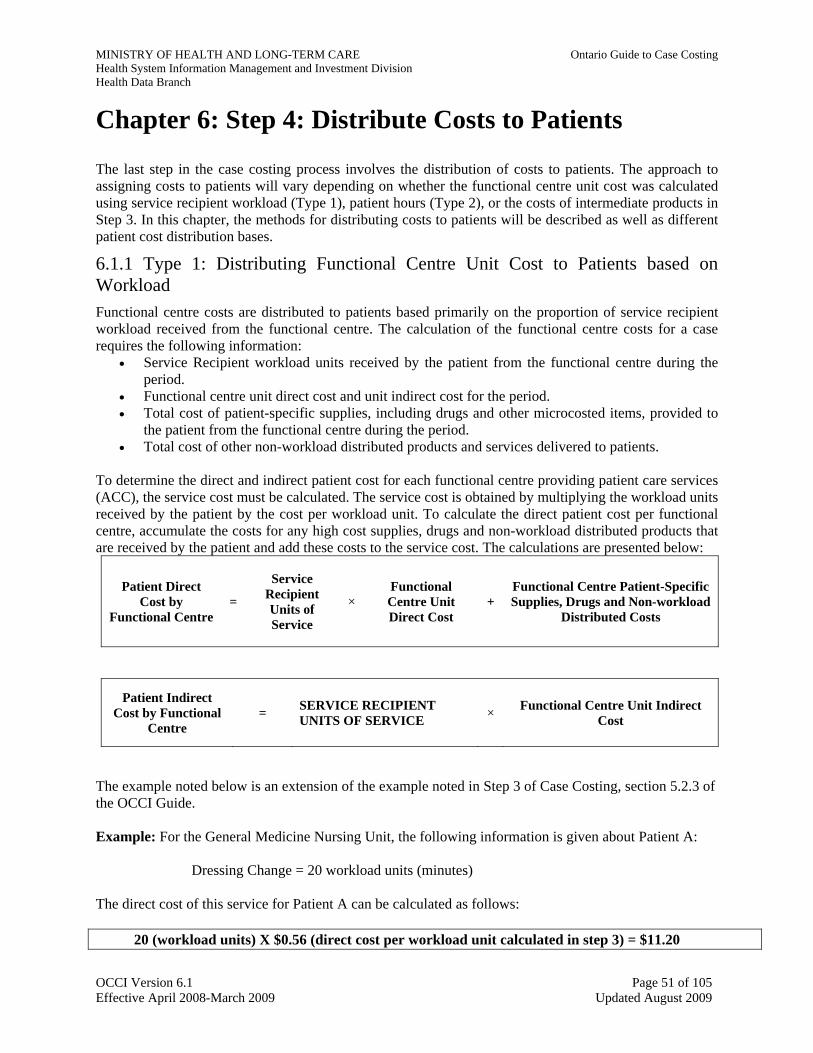

The OCCI has summarized the case costing methodology into four steps: 1. Gather the data; 2. Allocate indirect costs; 3. Calculate functional centre unit or intermediate product costs; and 4. Distribute costs to patients. Breaking down the methodology into these four steps simplifies and summarizes the task of patient-specific costing for planning and implementation purposes. The successful achievement of each step is critical, since the results of each step feed into the next step. The four steps of case costing are described in detail in Chapters 3 to 6.

2.4 Evolution of the OCCI Case Costing Methodology

The OCCI hospitals have been working to further develop the case costing methodology. Through several years of experience, hospitals that participated in the OCCI have identified numerous opportunities to improve case costing. The new standards have been incorporated into sections of this Guide. The following presents a summary of the current issues and the work of the OCCI. The chapters referenced for

OCCI Version 6.1 Page 13 of 105 Effective April 2008-March 2009 Updated August 2009

MINISTRY OF HEALTH AND LONG-TERM CARE Ontario Guide to Case Costing Health System Information Management and Investment Division Health Data Branch

each issue contain further details as well as some discussion of the impact they will have on the OCCI case costing methodology.

2.4.1 Changing Hospital Production—Program Management

Ontario hospitals have recently undergone radical changes in the way they deliver patient care. Traditionally, hospitals have been organized such that the departments that produce the intermediate products are divided along discipline-specific lines, shown in Figure 2-1.

Many hospitals have begun moving towards organizing and managing patient care delivery through the program management approach. This approach involves programs, instead of departments, being directly responsible for delivering direct patient care. The programs displace traditional functional centres as the primary organization unit for the production of intermediate products. Each program may produce a broad range of intermediate products, from nursing care to laboratory tests to social work services. Program management involves more than just re-organizing departments into programs. A key component of program management is the use of multi-skilled workers. Patient care staff, and possibly support staff, within a patient care program would be multi-skilled to provide a variety of services and products. Since any staff can provide a range of intermediate products, systems to accurately capture and cost each activity within the program are required. Hospitals have implemented many aspects of program management to varying degrees. The challenge now is to develop a costing methodology that can be applied to any hospital setting such that the costs produced are relevant for internal decision-making and are externally comparable to other hospitals, including those that are organized departmentally. The lack of a “standardized” approach for program management organization poses a number of issues. The OCCI has examined options to develop case costs in a program management organization. Chapter 11 presents the issues and methodology to calculate costs in this setting.

2.4.2 Extending the Methodology to Ambulatory, Complex continuing Care, Mental Health and Rehabilitation

The OCCI case costing methodology was originally developed to cost acute inpatients and was then modified for day surgery patients. The methodology has also been extended to cost Ambulatory, Complex Continuing Care patients, Mental Health and Rehabilitation. Many aspects of the methodology for Ambulatory, Complex Continuing Care , Mental Health and Rehabilitation are the same as for acute inpatients. Utilization/workload is captured on a patient-specific basis, financial information is tracked on a standardized basis using the MIS Standards, and patients are assigned costs based on the total number of intermediate products received. To collect the patient descriptive data for ambulatory care, the OCCI has adopted the CIHI National Ambulatory Care Reporting System (NACRS). NACRS is a service provider-based system whereby a minimum data set, with patient-specific demographic (e.g., age, sex) and clinical (e.g., diagnosis and procedure codes) data, is captured for each outpatient functional centre that has provided care. To define the complex continuing care and mental health encounter, the OCCI standards require the collection of the InterRAI Complex continuing Care Minimum Data Set (MDS v2), RAI –Mental Health Assessment and the Rehab Minimum Data Set. The OCCI case costing methodology and the case costing standards described in Chapters 3 to 6 apply to complex continuing care and ambulatory care, with specific standards summarized in Chapter 10.

OCCI Version 6.1 Page 14 of 105 Effective April 2008-March 2009 Updated August 2009

MINISTRY OF HEALTH AND LONG-TERM CARE Ontario Guide to Case Costing Health System Information Management and Investment Division Health Data Branch

2.4.3 A Framework for “Case” Costing The care provided for a given health condition can involve a variety of different interactions between the patient and the hospital. It would be of great value to be able to measure the cost of treating a patient over the entire episode of illness. For example, many patients now receive follow-up care on an outpatient basis after being admitted to hospital for a surgical procedure. The outpatient visit is related to the same health condition that required surgery. The ability to link the two visits together would provide a better estimate of the total costs for treating that condition. The OCCI has developed a six-level framework that links the various visits a patient has across different health care facilities for the treatment of a given health condition. The current information systems in Ontario hospitals allow the costs of the individual visit to be determined. Implementation of the proposed framework, described in Chapter 8, will identify the true “case” costs across various health care providers.

OCCI Version 6.1 Page 15 of 105 Effective April 2008-March 2009 Updated August 2009

MINISTRY OF HEALTH AND LONG-TERM CARE Ontario Guide to Case Costing Health System Information Management and Investment Division Health Data Branch

Chapter 3: Step 1: Gather the Data A standardized methodology has been developed with the goal of producing high quality case cost data. Reliable and valid data— financial, statistical and patient descriptive data—is necessary to produce high quality case costs. To obtain the data, follow data preparation and collection rules, audit the processes that generate the data and ensures that a particular case’s costs can be traced.

Data Reliability and Validity Reliability is the degree of consistency with which an instrument measures the attribute it is supposed to be measuring. Validity is the degree to which an instrument measures what it is supposed to measure.

- Pollit and Humgler, 1983

In the four chapters that follow (Chapters 3 to 6), there is a focus on what must be done to produce high quality cost data, by categorizing, allocating, and distributing costs. These standards were originally developed for acute inpatient and day surgery costing. Gathering data is the first step in the case costing process. The OCCI data standards for gathering financial and statistical data are based largely on the MIS Standards, which provide the framework for collection and organization of hospital statistical and financial data. Standards are necessary to ensure the comparability of data. In this chapter, the OCCI standards for the collection of financial, statistical and patient descriptive data (health records data) are presented.

3.1 Financial Data

3.1.1 MIS Standards The MIS Standards define a framework for the compilation and comparison of financial and statistical data. Since the MIS Standards are the starting point for case costing, hospitals wishing to implement case costing should become familiar with the MIS Standards. The standards presented here expand or clarify accounting issues and their treatment, as well as any additions to or modifications of the existing MIS Standards needed for case costing purposes. Appendix E provides an overview of the MIS Standards and the Ontario Healthcare Reporting Standards (OHRS).

The Glossary of Terms in the MIS Standards and OHRS provides definitions for key accounting terms. Some of those definitions are reproduced in this manual. Some definitions have been modified or were developed specifically to meet the objectives of Ontario case cost development.

OHRS Account Codes Functional centre numbers are listed in the Ontario Healthcare Reporting System User Guide version 6.2, Appendix A. Revenue and expense codes are listed in the Ontario Healthcare Reporting System User Guide version 6.2, Appendix B. See the OHRS Glossary for functional centre and revenue and expense account definitions.

Hospitals must adhere to the account structure presented in the MIS Standards and the account codes presented in the OHRS Chart of Accounts. When they differ, the OHRS overrides the MIS Chart of Accounts. With the province-wide implementation of MIS Account Codes, hospitals are encouraged to convert fully. If a hospital does not use OHRS General Ledger account codes, it is required that the account codes used be mapped into OHRS functional centres and revenue and expense accounts.

OCCI Version 6.1 Page 16 of 105 Effective April 2008-March 2009 Updated August 2009

MINISTRY OF HEALTH AND LONG-TERM CARE Ontario Guide to Case Costing Health System Information Management and Investment Division Health Data Branch

Note that the “roll-up” is built into the MIS Chart of Accounts numbering system. To safeguard the “roll-up”, be sure to define the functional centres at the lowest level needed to break out costs internally, and be sure that all of a lower level account rolls up to one account at the next level up. For fiscal year 05/06 submissions, small hospitals are required to submit case cost data at MIS Level 3 accounts while all other hospitals will need at least some MIS Level 4 accounts and some will need to go to MIS Level 5, depending upon size and complexity of service.

Functional Centres - High Cost Equipment

One way to isolate high equipment costs and distribute them to the patients who receive their benefit is to establish additional functional centres specifically for such high cost equipment. This approach is especially appropriate if the non-labour cost per service exceeds $250. Note that a suitable relative value unit system is needed to distribute costs to patients. This mechanism of establishing separate functional centres for high cost equipment enables hospitals to develop more accurate patient case costs. Hospitals can still compare their costs with those of hospitals that do not have these functional centres by rolling up to a common level, such as Level 3, and comparing at that level.

MIS Code Format Asterisks (*) are used in an account code to indicate that any valid code may be used in this position. For example, Acct 71 4 15 ** ** refers to all Diagnostic Imaging functional centres

Several specific functional centres that isolate high cost equipment have already been defined in the MIS Standards. They are listed in the table below.

Table 3.1

Functional Centres with High Cost Equipment OHRS Functional Centre

Number Functional Centre Cost Item

71 3 40 25 ** Day/Night Care, Surgical/Procedural Equip/Supplies 71 4 10 25 ** Clinical Chemistry Equipment 71 4 15 ** X-Ray Equip/Supplies 71 4 15 25 Computed Tomography Equipment 71 4 15 30 ** Diagnostic Ultrasound Equipment 71 4 15 40 Nuclear Medicine Equip/Supplies 71 4 15 44 Cardiac Catheterization Laboratory Supplies 71 4 15 70 Magnetic Resonance Imaging Equipment

Functional Centres for Patient Care Administration and Support

Patient Care departments with several functional centres and a large administrative and support staff may find it beneficial to set up a specific administrative and support functional centre for the department. The MIS Standards provide a suggested account structure for functional centres such as Laboratory, Diagnostic Imaging, Pharmacy and Nursing. It is easier to achieve a representative distribution of these administrative and support costs to patients using this approach. Some further considerations on the use of functional centres for departmental administration and support are discussed in section 3.1.2, Functional

OCCI Version 6.1 Page 17 of 105 Effective April 2008-March 2009 Updated August 2009

MINISTRY OF HEALTH AND LONG-TERM CARE Ontario Guide to Case Costing Health System Information Management and Investment Division Health Data Branch

Centre Cost Assignment. Note that patient care administration and support functional centre costs are assigned to the patient care functional centres as a direct cost.

3.1.2 Functional Centre Cost Assignment The Functional Centre Reporting sections of the MIS Standards specify how financial and statistical data should be collected and organized for case costing. Assigning expenses to the proper functional centres is crucial to achieve accurate case costs. In this section, the OCCI standards are described, which are based on the MIS Standards for assigning hospital expenses to functional centres. There is also a detailed explanation of the OCCI standards associated with the following expenses: salaries and benefits, physician compensation, patient care administration and support, supplies, drugs, amortization and leasing of equipment, and maintenance of major clinical equipment.

Salaries and Benefits

Salaries and benefits are usually the largest component of a functional centre’s costs. The MIS secondary account codes for salaries and benefits are as follows:

310** Worked Salaries 330** Benefit Salaries 340** Benefit Contributions 390** Purchased Service Salary (or Fee-for-Service) Worked salaries, benefit salaries and purchased service salaries represent the three categories of salaries. Benefits contributions are also known as fringe benefits. The OCCI standards require that salaries and benefits of personnel be assigned to the functional centres in which they work. This standard applies to all unit-producing personnel (those capturing workload), medical personnel, and management and operational support personnel. More information on labour costs related to these broad occupational groups is found in this section under Labour Hours Data, Patient Care Administration and Support, and Physician Salaries and Fees. Education and research staff salaries are assigned differently from the salaries of other hospital personnel. If education and research staff perform unit-producing work instead of regular functional centre staff, these hours spent performing unit-producing work and the associated salaries are assigned to the functional centre receiving the service. Otherwise, their hours and salaries are assigned to the appropriate Education or Research functional centre. Students receiving compensation should have their costs distributed to the appropriate functional centres at the actual rate of compensation. Students who are not compensated by the hospital will have no labour expenses assigned to functional centres. An employee’s uncompensated overtime hours will also be assigned no value. Although worked hours are not reported for unpaid students and unpaid overtime hours, workload is still collected, effectively reducing the cost per RVU. There should be mechanisms in place to distribute benefits to the appropriate functional centres. Depending on the accounting system, there might be a need to post benefits into one account, and then distribute benefit costs to each functional centre in proportion to salaries. To maintain comparability of reporting among hospitals, costs such as benefit contribution expense must not be treated as overhead (indirect costs).

MIS Standards Change Benefits Accounting Hospitals historically have excluded benefits Contributions (Fringe Benefits) from functional centre reporting. MIS Standards require distribution of Benefits

OCCI Version 6.1 Page 18 of 105 Effective April 2008-March 2009 Updated August 2009

MINISTRY OF HEALTH AND LONG-TERM CARE Ontario Guide to Case Costing Health System Information Management and Investment Division Health Data Branch

Hospitals should ensure that year-end payroll accruals are distributed to the functional centres. Both salaries and benefit contributions need to be accrued. Accruals are necessary in order to match salary and benefit contributions with workload statistics to provide a more accurate cost per workload unit.

Labour Hours Data

Labour costs account for about three-quarters of a hospital's operating costs. Because labour is such a large cost component, incorrectly assigned labour costs can lead to distorted case costs, even at the summary reporting level used for developing Ontario case costs. Most hospitals face a major challenge in documenting staff assignments, especially in Nursing where many temporary, casual, agency and float pool staff may work their shifts on different units each day. Developing correct labour costs for each functional centre requires good information on shifts worked in each functional centre.

It is expected that a hospital's recording system will have the ability to assign an employee’s hours to the functional centre in which they worked, to the nearest hour. This will ensure precise labour charges to each functional centre. For case cost development, it is also important that labour costs (hours), in each functional centre, are assigned to the proper MIS Secondary Account. Remember that staff involved in both unit-producing and management and support activities to a significant extent, must have their hours (and benefits) split between the Management and Operational Support (3 10 **), and Unit-Producing (3 50 **) Secondary Accounts. Accurate recording of labour hour data will provide meaningful information for managing workload and staffing levels, and for monitoring productivity and cost effectiveness. The division of labour hours into unit-producing and management and operational support hours is also important for Step 3 of the case costing process, when labour costs will be designated as variable or fixed (see Section 5.1). Medical personnel labour hours are treated differently than unit producing, management and operational support labour hours. Medical personnel are compensated for their professional medical services, either on a fee-for-service or salary basis. Physicians do not collect workload, and their labour hours and expenses are assigned to the Medical Personnel (3 90 **) Secondary Accounts. The section entitled Physician Salaries and Fees provides greater detail on how to handle physician activity. The hospital's central payroll time and attendance system will most likely be the feeder system which contributes the labour hours to the General Ledger Chart of Accounts and Statistics on an ongoing basis. Functional centres are responsible for accurately recording the time being inputted into the payroll system (either manually or electronically). As an alternative to using the payroll system, hours could be entered through a separate entry module linked to the workload management or costing system. The payroll system has the advantage that the labour cost output to the costing system module can come directly from the hospital's financial systems, so that existing management reports will reflect the more accurate labour distribution immediately. Any other approach could mean double data entry and create the potential for data reconciliation problems. Department-specific labour data requirements will be noted later in Chapter 8, Departmental Case Costing Standards.

Physician Salaries and Fees

Most hospitals have some physicians who are remunerated by the hospital through a contractual arrangement. Typically, physician remuneration consists of fee-for-service (e.g., radiologists) or salary

OCCI Version 6.1 Page 19 of 105 Effective April 2008-March 2009 Updated August 2009

MINISTRY OF HEALTH AND LONG-TERM CARE Ontario Guide to Case Costing Health System Information Management and Investment Division Health Data Branch

(e.g., pathologists). Compensation expenses for physicians, as with other hospital workers, should be charged as a direct cost to the functional centre in which the individual works.

Physicians who cannot be identified clearly with one functional centre prior to service provision should have their expenses charged to the appropriate Medical Resources functional centre (71207, 71307, 71507). These costs must be eventually cleared by assigning them to patient care functional centres, as direct costs, based on an estimate of time the physicians spent providing services to each of the functional centres. These costs should be distributed to patients based on workload collected in the functional centre.

Sometimes physicians perform management functions in addition to patient care work. In this case, remember that hours spent performing management functions must be assigned to the appropriate patient care administration functional centre, if this is a separate functional centre in the hospital. For example, a physician who is also the head of the Diagnostic Imaging department would have to record the hours spent performing management functions in the Diagnostic Imaging—Administration functional centre (7141510).

Note that for case costing is only interested in physician compensation if the physician is remunerated by the hospital. Many physicians (e.g., surgeons) working in the hospital are not compensated by the hospital but rather are directly compensated through the Ministry of Health and Long-Term Care via OHIP billings.

Patient Care Administration and Support

Particularly in larger hospitals, patient care administration and support functional centres have been established to isolate general management and support function staff and supply costs from those of the nursing, diagnostic or treatment areas. In smaller hospitals, these management and support functions are simply another activity of unit-producers and are already part of the functional centre’s costs. All costs contained in separate support and administration functional centres must be cleared through distribution to the functional centres that they support. These costs should be assigned as a direct cost to the patient care centres they support. Total functional centre workload, total department cost or estimates of the time staff spend providing services to functional centres can be used as the basis for the assignment. Patient care administration and support functional centres include the following:

• Inpatient Nursing

7120510 - Nursing Administration 7120520 - Clinical Resources (centralized)

20 - IV Therapy 40 - Enterostomal Therapy

2092 - Transplant Coordination/Organ Procurement 2094 - Palliative Care Team

7120600 - Program Management Administration • Ambulatory Care

7130500 - Ambulatory Care Administration 7130600 - Program Management Administration • Clinics

7135005 - Clinic Administration • Diagnostic and Therapeutic Services

7140600 - Program Management Administration

OCCI Version 6.1 Page 20 of 105 Effective April 2008-March 2009 Updated August 2009

MINISTRY OF HEALTH AND LONG-TERM CARE Ontario Guide to Case Costing Health System Information Management and Investment Division Health Data Branch

• Laboratory

7141010 - Clinical Laboratory - Administration 7141015 - Clinical Laboratory - Support Services 7141020 - Specimen Procurement and Dispatch • Diagnostic Imaging

7141510 - Diagnostic Imaging - Administration • Respiratory Therapy

7143510 - Respiratory Therapy - Administration • Pharmacy

7144010 - Pharmacy – Administration • Rehabilitation Services

7144900 - Rehabilitation Services - Administration • Community Services

7150500 - Community Services Administration

Supplies

For case costing purposes, distinguish between general and patient-specific supplies since these costs are distributed to patients differently. In the section that follows, general and patient-specific supplies are defined as well as how these costs are assigned to functional centres.

General Supplies General Supplies include all stationery, medical supplies, surgical supplies, ward stock drugs, laundry and other miscellaneous supply items. General supply items are charged to the functional centre using the supplies. The costs for general supplies are a component of each functional centre's total direct operating costs and are included when the functional centre's cost per unit is determined.

Patient-Specific Supplies It is not practical to “charge” all supplies to patients when doing case costing because it would mean accounting for each dressing, each tongue depressor, etc. However, if the costs of high-cost supplies are averaged, individual case costs could be distorted. To address this issue, a dollar limit has been established by the OCCI for tracking supplies or supply assemblies of $250 or greater to the patient. Therefore, any item or related grouping of supplies, or "supply assemblies" with a unit or assembly cost of $250 or more should be tracked to the patient as a patient-specific supply. A set of separate accounts in MIS broad group 5 is used to record patient-specific supplies.

Note that the MIS Standards have eliminated the $250 threshold for tracking patient-specific supplies as of April 1, 1999. The MIS Standards now require hospitals to track certain expensive supplies, which are “traceable” to patients. The OCCI does not require hospitals to capture supply or supply assemblies less than $250. However, decide to track items or assemblies that cost less than the $250 limit, especially those items which account for a large percentage of the functional centre's total supply cost. Typically, there are high cost supplies in the Operating Room and

OCCI Version 6.1 Page 21 of 105 Effective April 2008-March 2009 Updated August 2009

MINISTRY OF HEALTH AND LONG-TERM CARE Ontario Guide to Case Costing Health System Information Management and Investment Division Health Data Branch

Diagnostic Imaging.

A supply assembly is a group of supply items that is used together in a patient-specific procedure. For example, a supply assembly for an orthopedic procedure may consist of one $100 prosthesis and six $50 screws. The patient-specific supply cost of this assembly totals $400.

The requirement to identify patient-specific supply costs could have a significant impact upon the hospital's current manual and automated supply management practices and systems. Examples of some of the issues that are likely to arise in many functional centres include:

• Are patient-specific supply items identified on an ongoing basis?

Patient-Specific Supplies Supplies and “supply assemblies” that cost over

$250. • Individually dispensed drugs, including PRN

medication, must be tracked and their costs assigned directly to the patient.

• Are the patient-specific supplies tracked that may account for a high proportion of the functional centre's supply budget but cost less than $250?

• Can the current materials management system track both inventory and non-inventory items? • Will direct purchase items need to be catalogued for ongoing tracking? • If supplies are charged back to the functional centres prior to usage (e.g., through the use of

exchange carts or departmental (unofficial inventories), how are actual usage identified? • Can the current materials management system support the tracking of patient-specific cost items

(i.e., either stand alone or integrated with the order entry/results reporting system and/or other ancillary systems)?

• Is a departmental materials management system or other specific programs required for the support of these functional centre specific requirements?

• Can the current systems support maintaining supply assembly lists and costs through a "bill of materials" or other methodology?

Drugs

Drugs are also classified as supplies. For case costing, distinguish between individually dispensed drugs and ward stock drugs. All individually dispensed drugs, regardless of their cost, are tracked and assigned directly to the patient. PRN (as needed) medication that is not kept as ward stock is also captured on a patient-specific basis. These patient-specific costs are excluded from the functional centre unit cost/intermediate product cost calculation. Ward stock drugs are general supplies and therefore are not captured on a patient-specific basis.

The MIS Standards (Section 3.3) specify that all drug costs (patient-specific and ward stock) must be distributed to the consuming functional centre. The OCCI case costing methodology differs from the MIS Standards. Individually dispensed drugs are charged to Pharmacy. However, ward stock drugs must be assigned to the appropriate Nursing functional centre. There are also some specific drugs and related items, administered through other functional centres, that must be charged to those functional centres. For example:

• Anaesthetic agents and other drug items administered through the Operating Room are assigned to the Operating Room.

• Non-medicated IV solution costs are charged to the appropriate Nursing functional centres. • Medical gas costs are charged to the administering department.

OCCI Version 6.1 Page 22 of 105 Effective April 2008-March 2009 Updated August 2009

MINISTRY OF HEALTH AND LONG-TERM CARE Ontario Guide to Case Costing Health System Information Management and Investment Division Health Data Branch

Amortization and Leasing Expenses Historically, amortization and leasing expenses were simply charged to Administration. For case costing, amortization and leasing costs must be assigned to functional centres using the equipment. The patient cost distribution process will distribute these costs correctly to the patients receiving service from the functional centre as direct costs of the functional centre. Hospitals must comply with the OHRS requirements for amortization rates. In Ontario, the threshold for capitalization is a minimum of $1,000. Each corporation will be allowed to establish their threshold amount at $1,000 or higher.

Maintenance

Maintenance of major clinical equipment performed by the hospital's maintenance and/or biomedical department should be charged to the department receiving the service. The maintenance department should have a mechanism to document the service provided (i.e., work order system) and provide an input document for the accounting posting. At the end of the accounting period, when the cost allocation is performed, the maintenance department's costs would be reduced by the dollars charged directly to the departments served. The remainder would be allocated as indirect costs according to the cost allocation formula.

Major clinical equipment maintenance may also be provided through an external maintenance contract. Like maintenance provided by the hospital's maintenance and/or biomedical department, these charges must be assigned directly to the functional centres whose equipment is receiving the maintenance. Note that building and building equipment maintenance should be allocated as an indirect cost using the allocation statistics presented in this Guide, as there is little value in charging these costs to the absorbing cost centres directly.

Allowable Recoveries and Revenues in Case Costing

Refer to Appendix 3 “Allowable Recoveries and Revenues in Case Costing”

3.1.3 Separating Inpatient, Outpatient and Non-Patient Operating Costs Patient case costs should not be distorted by a hospital's other business activities. Our use of case cost data is best served when inpatient, outpatient, referred-in and ancillary operations are clearly and correctly separated. Hospitals are constantly seeking new ways to generate revenue. One approach is to take advantage of a hospital's strength in its support services (such as printing or food services) to provide products or services for non-hospital clients. Patient case costs should not be affected (understated or overstated) by the expenses or revenues associated with these revenue-generating activities. Wherever possible, isolate non-patient costs and revenues by establishing a separate functional centre for non-patient operations and using direct charge billing for ancillary operations that provide services both within the hospital and to outside customers. Whatever approach is used, it should support both case costing and the monitoring of the profitability and financial performance of the non-patient ancillary operations. In some instances, it may be difficult to separate patient and non-patient costs when the hospital has one functional centre containing expenses for both patient and non-patient operations. To estimate patient costs, non-patient revenue is to be used as a proxy for non-patient costs in this functional centre. This

OCCI Version 6.1 Page 23 of 105 Effective April 2008-March 2009 Updated August 2009

MINISTRY OF HEALTH AND LONG-TERM CARE Ontario Guide to Case Costing Health System Information Management and Investment Division Health Data Branch

means that there is a need to establish a mechanism to capture non-patient operating revenue, and net the same amount from the operating costs of the functional centre prior to reporting.

3.1.4 Patient Revenue Some hospitals distribute patient revenue to functional centre accounts for management reporting purposes to show departmental managers a more complete and balanced picture of their operations. If the hospital uses this approach, remember do not net the revenue for providing care to the patients when determining costs for distribution to patients. This approach applies to all patient revenue: Ministry of Health and Long-Term Care Allocation, OHIP, WCB, crutches, etc.

3.1.5 Other Hospital Costs

Which Functional Centres must be Costed? Hospitals may decide not to cost functional centres whose expenses are only a very small percentage of the total hospital costs. It may not provide much added benefit to set up systems to cost functional centres that contribute insignificantly to case costs. Nevertheless, aim to distribute a large portion of the operating costs. The OCCI has established standards for the functional centres that must be costed for certain patient populations:

Acute Inpatient For the first year of costing, hospitals must distribute at least 80% of acute inpatient operating costs to patients using approved workload measurement systems. The following core functional centres must be included as part of the 80% minimum: • 712**** to 7127*** - Nursing Inpatient Services • 71410** - Clinical Laboratory • 71415** - Diagnostic Imaging • 71440** - Pharmacy

Additional functional centres must be costed so that by the beginning of the third year of costing at least 95% of inpatient costs are distributed to patients.

Day Surgery In addition to the required functional centres for acute inpatients, the day surgery operating room must be costed. Hospitals are only required to submit qualifying day surgery cases to the OCCI as per the Joint Policy & Planning Committee definition, who receive services from either the main or day surgery operating rooms.

Ambulatory Care (excluding day surgery) Hospitals must distribute at least 80% of outpatient operating costs to patients using approved workload measurement systems. The following core functional centres must be included as part of the 80% minimum: • 71310** - Emergency • 713501070 - Medical Pre-Admission Clinic • 713501545 - Surgical Pre-Admission Clinic • 71410** - Clinical Laboratory

OCCI Version 6.1 Page 24 of 105 Effective April 2008-March 2009 Updated August 2009

MINISTRY OF HEALTH AND LONG-TERM CARE Ontario Guide to Case Costing Health System Information Management and Investment Division Health Data Branch

• 71415** - Diagnostic Imaging • 71430** - Other Diagnostic Laboratories • 71440** - Pharmacy • 71450 - Physiotherapy • 71455** - Occupational Therapy • 71470** - Social Work

If 80% of total outpatient costs cannot be distributed to patients by costing the above functional centres, a hospital-specific mix of additional ambulatory care functional centres must be costed to achieve the 80% minimum. Hospitals have the option to cost additional functional centres beyond the 80% minimum.

Chronic Care Hospitals must distribute at least 80% of chronic care operating costs to patients using approved workload measurement systems. The following core functional centres must be included as part of the 80% minimum: • 71295** - Long Term Care IP • 71450 - Physiotherapy • 71455** - Occupational Therapy • 71470** - Social Work

Mental Health

Hospitals must distribute at least 80% of mental health operating costs to patients using approved workload measurement systems. The following core functional centres must be included as part of the 80% minimum:

• 71276** - Mental Health • 71410** - Clinical Laboratory • 71415** - Diagnostic Imaging • 71430** - Other Diagnostic Laboratories • 71440** - Pharmacy • 71470** - Social Work

Rehabilitation Hospitals must distribute at least 80% of mental health operating costs to patients using approved workload measurement systems. The following core functional centres must be included as part of the 80% minimum: • 71281** - Rehabilitation

OCCI Version 6.1 Page 25 of 105 Effective April 2008-March 2009 Updated August 2009

MINISTRY OF HEALTH AND LONG-TERM CARE Ontario Guide to Case Costing Health System Information Management and Investment Division Health Data Branch

• 71450 - Physiotherapy • 71455** - Occupational Therapy • 71470** - Social Work

If costing the above functional centres cannot satisfy the 80% requirement, then a hospital-specific mix of functional centres with chronic care activity must also be costed to satisfy the minimum. Hospitals have the option to cost additional functional centres beyond the 80% minimum.

Appendix G (Calculation of Patient-Specific Cost Distribution Percentage) is a helpful tool to assess the impact of including or excluding particular functional centres. This form organizes the functional centre costs distributed to patients; the total inpatient, chronic care, mental health and outpatient costs for the reporting period; and the total functional centre costs not distributed to patients. To ensure that a consistent approach has been taken to the apportionment of costs between acute inpatient, chronic care, mental health and outpatient activity, use the information reported by the hospital’s OHRS Trial Balance submission to the Ministry of Health and Long-Term Care.

Non-Distributed Absorbing Cost Centre (ACC) Costs Hospitals will vary in the percentage of costs they distribute to patients. Some OCCI hospitals are distributing 100% of acute inpatient costs by costing all inpatient functional centres. Others, however, are including only some or none of the optional functional centres and are capturing closer to 85% of inpatient costs. Because of this variation, the OCCI employs a methodology that distributes acute inpatient costs of non-distributed patient care functional centres to patients. This methodology, to standardize the acute inpatient case cost data from OCCI hospitals, is required so that comparisons can be made between hospitals. It is only expected to be an interim measure, however, since hospitals are required to distribute 95% of total inpatient costs by the beginning of the third year of costing. Since the OCCI employs a methodology that distributes undistributed functional centre costs to patients, hospitals should ensure that they do not distribute or allocate these costs to patient care functional centres.

3.2 Cost Distribution Bases

Two data types can be used as cost distribution bases. The first type of cost distribution is based on workload. The workload cost distribution is described in the following section. Workload is described in the following section. The second type of data involves the collection of patient hours. This new methodology was developed in 2006 and is introduced in Section 3.2.2 of this guide and further discussed in Chapter 5 (see Appendix M for method details). Either workload or patient hours can be used to distribute nursing costs. Hospitals should select a system that meets their needs and is compatible with the appropriate MIS methodology.

3.2.1 Workload

Workload data serve as the cost distribution base for most functional centre costing purposes. Through order entry/results reporting, cost accounting or departmental information systems and intermediate products (such as exams, procedures and other services) are translated into workload units by functional centre for each patient. This information is linked to the specific patient through a unique encounter identifier.

Major Components of Workload Measurement Systems

• Identification and categorization of work • Identification and definition of activities

within each category • Time recording methodology • Reliability and validity measures

OCCI Version 6.1 Page 26 of 105 Effective April 2008-March 2009 Updated August 2009

MINISTRY OF HEALTH AND LONG-TERM CARE Ontario Guide to Case Costing Health System Information Management and Investment Division Health Data Branch

There are three time recording methodologies for workload measurement: average, standard and actual. The average time reflects the national average time to conduct the task, as identified by the National Workload Measurement System (NWMS). The Diagnostic workload measurement systems use average time methodologies, while the Nursing and most therapeutic workload measurement systems support both actual and standard time recording. The workload recording method should follow the NWMS that applies to the work done by the functional centre (see MIS Standards 2006, Chapter 4, for a complete list). These systems provide a standardized means of measuring the activities or outputs of each functional centre. Workload units are broadly divided into Service Recipient/Patient Care and Non-Service Recipient/Non-Patient Care workload.

Linking Workload Data to Other Case Cost Data Ideally, workload measurement can be done as a by-product of existing departmental functions. For diagnostic departments, an order entry/results reporting system can be used to minimize the impact of data collection and reporting. Case costing requires the collection and reporting of financial and statistical data on a patient-specific basis. This means a functional centre must be able to track and report workload units and services with the patient unique identifier. There is more information on linking patient and cost data in Chapter 8.

Monitoring The Workload Measurement System If realistic productivity ratios cannot be produced with the NWMS units, re-engineer the units to more appropriately reflect the workload required for various activities. Any changes should strictly follow the NWMS methodology outlined in the MIS Standards. Notify CIHI of significant differences so that an evaluation can be done about the need for revision to the NWMS. If the units are re-engineered, re-evaluate their continued use whenever the NWMS units are adjusted and whenever there is a change in technology or procedures.

Developing A Customized Workload Measurement System Some hospitals choose to develop a customized workload measurement system for functional centres where no NWMS exists. To ensure data comparability, OCCI hospitals have identified those functional centres and explained the approach used. The selection of a workload measurement methodology should ultimately rest upon the results of the methodology to reflect accurate and comprehensive outputs of the functional centre. The development of a workload measurement system must adhere to generally accepted workload measurement principles. Some of the desirable characteristics of a workload measurement system are listed below:

• Activities (procedures or intermediate products) are capable of being patient-specific. • Activities (procedures or intermediate products) are well defined, are recognizable, and are

elements of a cost centre’s function that can be considered separate outputs. • A workable number of activities (procedures or intermediate products)–normally less than 15–is

used, but enough to represent the largest portion (at least 80%) of a functional centre's worked hours.

• Relative values represent the ratios among average times necessary under average conditions to complete all aspects of measured work.

• Each activity (procedures or intermediate products) represents homogeneous elements of resource use.

• Activities (procedures or intermediate products) should be clinically and financially homogeneous.

OCCI Version 6.1 Page 27 of 105 Effective April 2008-March 2009 Updated August 2009

MINISTRY OF HEALTH AND LONG-TERM CARE Ontario Guide to Case Costing Health System Information Management and Investment Division Health Data Branch