One-Day Audit Training

172

CSP Audit Training St. Paul, Minnesota July 19, 2007

Transcript of One-Day Audit Training

CSP Audit Training

St. Paul, Minnesota

July 19, 2007

Tentative Agenda 8:30 - 8:45 Welcome 8:45 - 9:30 Background of SST - Scott Peterson, Executive Director 9:30 - 10:30 Overview of Certification Process for CSPs - Gary Centilvre and David Thompson 10:30 - 10:45 Break 10:45 - 12:00 Overview of CSP Operations - Taxware and Avalara 1:00 - 1:30 Overview of Compliance Audit Process 1:30 - 2:30 Audit Core Team's Responsibilities, Procedures & Deadlines 2:30 - 2:45 Break 2:45 - 4:00 Member State Auditor Responsibilities, Procedures & Deadlines 4:00 - 4:30 Questions 4:30 Closing The following is the hotel information for St. Paul. The rates are as of May 30: Embassy Suites Hotel, 175 E. 10th St., Saint Paul, 651-224-5400 or 800-362-2779 (No Government rate available) $159 per night + tax Crown Plaza Riverfront, 11 East Kellogg Boulevard, St. Paul, 651-292-1900 or 800-Holiday (No Government rate available) $199 per night + tax; ARRP $156 per night + tax Holiday Inn River Centre, 175 W. 7th St., St. Paul, 651-225-1515 Government rate: $113 per night + tax City Center Hotel- St Paul, 411 Minnesota St, St Paul, MN 55101, (651) 291-8800, (866) 781-8800 (No Government rate available) $159 per night + tax Country Inn & Suites by Carlson-Roseville, 2905 Snelling Ave N St Paul, MN 55113, (651) 628-3500 Government rate: $103.55 per night + tax Country Inn By Carlson, 6003 Hudson Rd, Woodbury, MN 55125, (651) 739-7300; 800-456-4000 Government rate: $60 per night + tax Radisson Hotels & Resorts: Radisson Hotel Roseville, 2540 Cleveland Ave N, Roseville, MN 55113, (651) 636-4567

Government rate: $133.00 per night + tax Courtyard by Marriott, 1352 Northland Dr, Mendota Heights, MN 55120, (651) 452-2000 Government rate: $80.00 per night + tax Courtyard by Marriott: Roseville, 2905 Centre Pointe Dr, St Paul, MN 55113, (651) 746-8000; 800-321-2211 Government rate: $113.00 per night + tax Holiday Inn-ST. PAUL-I-94-EAST (3M AREA), 2201 BURNS AVE., ST. PAUL, 651-7312220; 800-Holiday Government rate: $95.00 per night + tax

1

Certified Service ProvidersAudit Training WorkshopJuly 19, 2007

Scott PetersonExecutive Director

Streamline Sales Tax Governing Board

Certified Service ProvidersAudit Training Workshop

Purpose of training:– Explain what is a CSP and CAS.– Introduce you to them.– Explain the CSP contract.– Explain the CSP certification process.– Have the CSP’s explain their systems.

2

What is SST?

A government/business effort to simplify sales and use tax administration.Two areas of emphasis:

– Current collectors– Remote sellers

Why– Business need to have simpler system.– States need to maintain a viable tax structure.

How– 44 states, local governments and hundreds of businesses

working together.

Why a Simplified Sales Tax System is Why a Simplified Sales Tax System is Important to GovernmentImportant to Government

Simpler administration of tax.Improved compliance from existing taxpayers.Possible increase in available audit hours.Addresses the collection of remote sales.

3

Why a Simplified Sales Tax System is Why a Simplified Sales Tax System is Important to BusinessImportant to Business

Reduces cost of compliance.Improves compliance.Reduces audit burden.Addresses multistate issues.

New Technology To Simplify

Central registration system.Database matching rate to local jurisdiction.Database of boundary information.Taxability matrix.Certified technology for sellers.

4

Certified Technology

Two versions:Certified service providers.Certified automated systems.

SST used RFP to seek software companies.States evaluated software that assists sellers in their sales tax administrative responsibility.

Certified Technology -Certified Service Providers

A third party to whom a seller can out-source their sales tax administrative responsibility.The third party:

– Knows what products and services are taxable.– Where they are taxable.– The rate at which they are taxed.– Populates the seller’s accounting software.– Compiles the information into a complete tax return.– Files the tax return and remits the tax.

The third party is liable for errors in the integration of the system.

5

Certified Technology -Certified Service Providers

Under contract with the Governing Board.Contract expires June 2007.SCOPE OF SERVICES: “Except as otherwise provided in this section, the Contractor agrees to and shall perform all of the sales and use tax functions of each Seller with whom it contracts as a CSP, other than such Seller’s obligation to remit tax on its own purchases, for each Member State and Associate Member State in which the Seller is registered to collect sales and use tax.”

Certified Technology -Certified Service Providers

Use an Automated System.Integrate the Automated System with the system of a Seller.File tax returns and informational returns as provided for in Section 318 of the SSUTA on behalf of each Seller.Protect the privacy of tax information it obtains.Maintain compliance with the provisions of the Minimum Standards for Certification document.

6

Certified Technology -Certified Service Providers

State compensated when providing service to volunteers.Compensation rates are based upon the volume of Taxes Due from each Volunteer Seller with whom the Contractor agrees to provide services as a CSP.Compensation ranges from 8% of taxes due to 2% of taxes due.Rates of compensation shall reset annually for services performed on behalf of each Volunteer Seller.The Contractor shall provide electronic reports to the ExecutiveCommittee on a quarterly basis that explain how the Contractor's compensation was calculated.

Certified Technology -Certified Service Providers

Each State shall, pursuant to the terms of SSUTA Sections 306 and 328, relieve the Contractor, and any Seller registered under theSSUTA with which the latter contracts, from liability to the states and their local jurisdictions for having charged and collected the incorrect amount of sales or use tax resulting from the Contractor or any of its SSUTA-registered contracting Sellers relying on erroneous data on tax rates, boundaries, or taxing jurisdiction assignments which have been listed in the state’s rates and boundaries databases, and erroneous data provided in the taxability matrix provided by the Member State or Associate Member State pursuant to Section 328.In accordance with SSUTA, each State shall review and certify that the Automated System utilized by the Contractor determines accurately whether or not a category of items or transactions listed in theAutomated System is exempt from tax in accordance with each state’s law.

7

Certified Technology -Certified Service Providers

The Contractor shall have ten (10) days from the date of notification by a State to revise the Automated System to conform with changes to: the tax rates, boundaries, or taxing jurisdiction assignments which have been listed in the state’s rates and boundaries databases; the taxability matrix provided by the State pursuant to Section 328 of the SSUTA; and the classification of the taxability of a category of items or transactions pursuant to Section 502 of the SSUTA. In the event the Contractor fails to make such changes, beginning on the eleventh day after notification the Contractor shall be liable for failure to collect the correct amount of Seller Taxes owed to the State, plus any additional charges or amounts that the laws of the State impose for the nonpayment of sales and use taxes, and shall be in Breach of this Contract.

Certified Technology -Certified Service Providers

The Governing Board, Member States and Associate Member States are not responsible for mapping, which is defined as classification of an item or transaction within a certified category. The Contractor is liable for mapping errors resultingin failure to collect the correct amount of Seller Taxes owed tothe Member State or Associate Member State, plus any additional charges or amounts that the laws of the Member State or Associate Member State impose for the nonpayment of sales and use taxes. Nothing herein shall prohibit the Contractor from providing, in its contracts with Sellers, for indemnification from Sellers to reimburse the Contractor for liability resulting from mapping errors to the extent that such errors are due to the actions or inactions of a Seller.

8

Certified Technology -Certified Service Providers

The Contractor shall not be liable for the failure to remit Seller Taxes when due, … to the extent that (a) the laws of a State relieve the Contractor or the Seller from liability to the state and its local jurisdictions for having remitted the incorrect amount of sales or use tax and (b) the incorrect amount resulted from the Contractor’s reasonable reliance on an issue made available for review but not discovered in the certification process. If both (a) and (b) are satisfied, the Contractor’s sole obligation and liability for such unpaid taxes shall be to correct the issue within a reasonable amount of time (not to exceed ten (10) days unless an extension is granted by the Executive Committee) from receipt of the State’s notice of the incorrect amounts. In the event the Contractor is unable to correct the issue causing the incorrect amounts to be charged and collected, beginning on the first day after the time allotted in the previous sentence the Contractor shall be liable for failure to collect the correct amount of Seller Taxes owed to the State, … and shall be in Breach of this Contract.

Certified Technology -Certified Automated Systems

A third party to whom a seller can out-source their sales tax determinations.The third party:

– Knows what products and services are taxable.– Where they are taxable.– The rate at which they are taxed.– Populates the seller’s accounting software.

The seller remains liable for filing tax returns and payment of the tax.The seller is liable for errors that occur in the integration of the certified system into their own system.

9

Certified Technology -Certified Automated Systems

Under contract with the Governing Board.Contract expires June 2007.

Certified Service Providers

QUESTIONS

Contact Information:Scott PetersonExecutive DirectorStreamlined Sales Tax Governing Board615-460-9330Scott.Peterson@sstgb.orgwww.streamlinedsalestax.org

1

Streamlined Sales TaxStreamlined Sales TaxCertification CommitteeCertification Committee

andandTesting CentralTesting Central

OverviewOverview

July 19, 2007July 19, 2007

Streamlined Sales TaxStreamlined Sales Tax

CSP Evaluation CommitteeCSP Evaluation CommitteeEvaluation and CertificationEvaluation and CertificationFormalizing the ProcessFormalizing the ProcessCertification CommitteeCertification CommitteeTesting CentralTesting CentralChange Control AdministrationChange Control AdministrationFTP SiteFTP Site

2

CSP Evaluation CommitteeCSP Evaluation CommitteeFormulate certification processCreate documentationDetermine minimum requirementsEvaluate RFP responsesEstablish criteria for certificationConduct security assessments and site inspections of potential CSP’s Establish test proceduresManage testing processMake recommendations to Governing Board

Certification TimelineCertification TimelineRFP issued November ‘04CSP Eval Committee formed - February ’05Review of RFP responses – March ‘05 Seven companies selected for evaluation – April ‘05System testing begins with three service providers -October ‘05Tentative Awards/Contract/Cost negotiations –April/May ‘06Final Contract Award to Certified Service Providers –June 2006

3

Certified Service ProviderCertified Service Provider

“An agent certified under the Agreement to perform all of the seller’s sales and use tax functions, other than the seller’s obligation to remit tax on its own purchases.”

(sec.203, SSUTA)

Certified Service ProviderCertified Service Provider

A third party that provides a sales tax administration system that is certified by the member States of the SSUTA.

Determines what is taxable and what is exemptSources the sale and calculates the correct taxReports and remits to the correct jurisdictionProtects privacy of taxpayer information

4

CSP Requirements CSP Requirements (source: RFP11/01/04)(source: RFP11/01/04)

Uniform SourcingExemption ProcessingUniform RoundingRate and Boundary ChangesTax Collection Procedures

Liability ReliefTax Remittance ProceduresRecord Retention ProceduresAudit RequirementsTax Privacy

Evaluation Criteria CategoriesEvaluation Criteria Categories(Compiled from SSUTA, RFP and Certification Standards)(Compiled from SSUTA, RFP and Certification Standards)

Background and experienceFinancial soundnessProject staffing and organizationTechnical ApproachCertification Standards - General ControlsApplication ControlsSystem Modification Accuracy

Sufficiency of informationTransaction Speed and Data SecurityPrivacy Standards and Data ProtectionElectronic format capabilities and sampling procedures Cost proposalExecution of proposal

5

Acceptance RequirementsAcceptance Requirements

Execute test decks successfullyExecute test decks successfullySuccessfully test single entry screenSuccessfully test single entry screenSuccessfully complete endSuccessfully complete end--toto--end testingend testingApproval of tax rulesApproval of tax rulesActivity report capabilitiesActivity report capabilitiesFinancial soundness assessmentFinancial soundness assessmentAll other requirements of SSUTA All other requirements of SSUTA (sec. 501B)(sec. 501B)

and Certification Standardsand Certification Standards

Article V Article V –– Provider and System Provider and System CertificationCertification

Article V of the Rules and Procedures of the Article V of the Rules and Procedures of the SST Governing Board, Inc. adopted in April SST Governing Board, Inc. adopted in April ’’0606Rule 501, Article V formalized the Certification Rule 501, Article V formalized the Certification processprocessRules 501.2Rules 501.2--501.4 Certification and acceptance 501.4 Certification and acceptance requirements for service providers, requirements for service providers, Recertification processRecertification processRules 501.5Rules 501.5--501.6 Certification and acceptance 501.6 Certification and acceptance requirements for automated systemsrequirements for automated systems

6

Appendices to Article VAppendices to Article V‘‘AA’’ Timeline and CertTimeline and Cert

Process FlowProcess Flow‘‘BB’’ Initial timeline andInitial timeline and

Cert Process FlowCert Process Flow‘‘CC’’ Criteria for CSPCriteria for CSP

Eval (min. standards)Eval (min. standards)‘‘DD’’ RFP Criteria forRFP Criteria for

EvaluationEvaluation‘‘EE’’ Testing Process forTesting Process for

Certification of ServiceCertification of ServiceProviders Providers

‘‘FF’’ FTP Site AdministrationFTP Site Administration‘‘GG’’ Certification StandardsCertification Standards‘‘HH’’ Recertification ProcessRecertification Process‘‘II’’ Recertification TimelineRecertification Timeline

and Process Flowand Process Flow‘‘JJ’’ Model 2 AutomatedModel 2 Automated

System CertificationSystem CertificationProcess FlowProcess Flow

‘‘KK’’ Testing Process forTesting Process forCertification of Model 2Certification of Model 2Automated SystemsAutomated Systems

Certification CommitteeCertification Committee

Rule 501.7, Article V establishes SST Rule 501.7, Article V establishes SST Certification CommitteeCertification Committee

Certification Committee advises the Governing Board on Certification Committee advises the Governing Board on matters pertaining to the evaluation, testing, certification matters pertaining to the evaluation, testing, certification and recertification of service providers and automated and recertification of service providers and automated systems. The Committee will consider and respond to systems. The Committee will consider and respond to those matters referred to it from the Governing Board or those matters referred to it from the Governing Board or its committees regarding evaluation, testing, certification its committees regarding evaluation, testing, certification or recertification. The Committee may also recommend or recertification. The Committee may also recommend items to the Governing Board for consideration. items to the Governing Board for consideration.

7

Testing CentralTesting Central

Rule 501.8, Article V establishes Rule 501.8, Article V establishes Testing CentralTesting Central

An administrative process to manage and document An administrative process to manage and document communication between member states, Certified communication between member states, Certified Service Providers, Certified Service Provider candidates, Service Providers, Certified Service Provider candidates, Certified Automated System providers and/or Certified Certified Automated System providers and/or Certified Automated System applicants regarding testing and Automated System applicants regarding testing and changes.changes.

Testing CentralTesting Central

Presented byPresented byDavid ThompsonDavid Thompson

IT Director, SSTGB Inc.IT Director, SSTGB [email protected]@SSTGB.org

931931--387387--22802280

8

Testing Central developed by the Testing Central developed by the Certification Committee in 2006Certification Committee in 2006

First maintained by Kansas and First maintained by Kansas and TennesseeTennessee

Currently maintained by Streamlined Sales Currently maintained by Streamlined Sales Tax Governing Board Inc.Tax Governing Board Inc.

Testing Central ResponsibilitiesTesting Central Responsibilities

Maintain historical data regarding system Maintain historical data regarding system changes changes

Monitor necessary system changes and testing Monitor necessary system changes and testing

Notify states of completed changes and the date Notify states of completed changes and the date of production of production

9

Testing Central ResponsibilitiesTesting Central Responsibilities

Monitor testing time of member states Monitor testing time of member states

Provide reports upon request of outstanding and Provide reports upon request of outstanding and completed system changes completed system changes

Maintain system to capture complete change Maintain system to capture complete change data data

TESTING CENTRAL FORMSTESTING CENTRAL FORMS

State Change Request State Change Request –– Form TC0001Form TC0001Completed by States to indicate problems or Completed by States to indicate problems or a necessary change in a CSP systema necessary change in a CSP system

CSP/CAS Change Request CSP/CAS Change Request –– Form Form TC0005TC0005

Completed by CSP/CAS to notify state of Completed by CSP/CAS to notify state of system changes or problemssystem changes or problems

10

State Notice of R&B Change State Notice of R&B Change –– Form TC0006 (Optional)Form TC0006 (Optional)Completed by States to allow Testing Central to notify CSP/CAS Completed by States to allow Testing Central to notify CSP/CAS of changes in the Rates and/or Boundary filesof changes in the Rates and/or Boundary files

Allowance Indicator Form Allowance Indicator Form –– F0004F0004Completed by CSP/CAS to allow Testing Central to indicate Completed by CSP/CAS to allow Testing Central to indicate which states will pay CSP/CAS compensationwhich states will pay CSP/CAS compensation

Changes LogChanges LogExcel spreadsheet maintained to list all change requests, dates,Excel spreadsheet maintained to list all change requests, dates,actions and commentsactions and comments

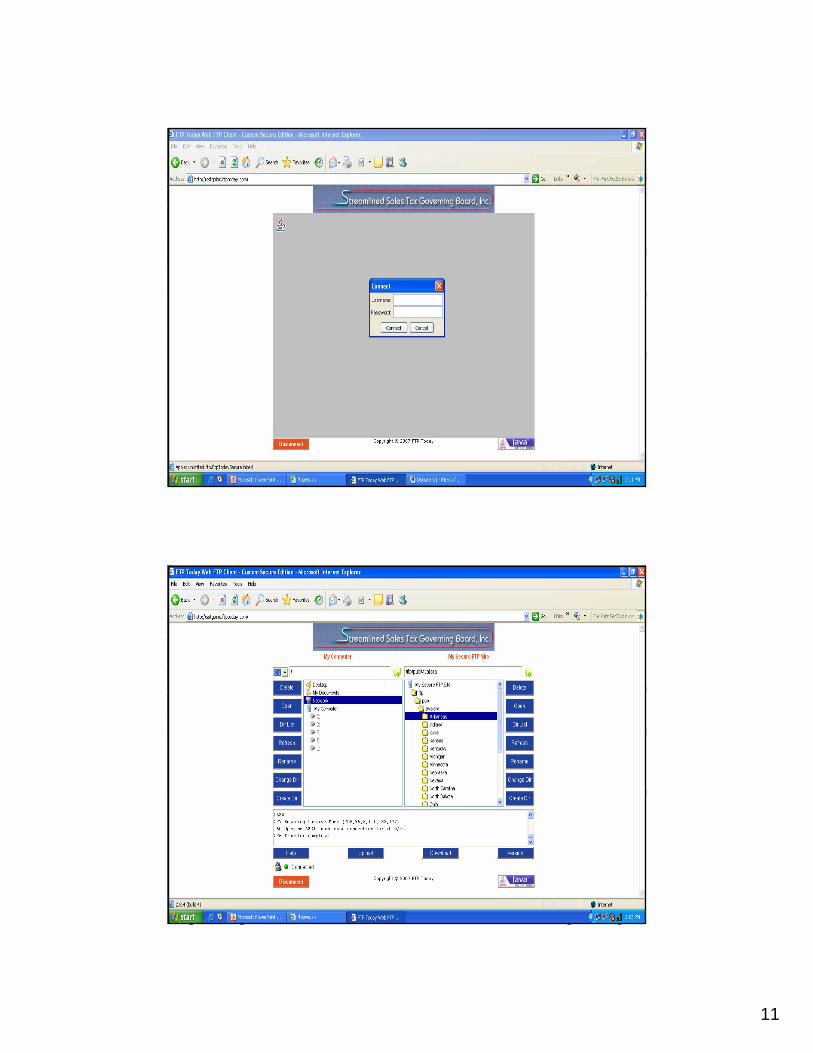

FTA SiteFTA Site

FTP Site StructureFTP Site Structure

FTP Site Access:FTP Site Access:

User ID and Password sent to each state, CSP and Core Team User ID and Password sent to each state, CSP and Core Team

FTP Site LocationFTP Site Location

http://http://sstgbinc.ftptoday.comsstgbinc.ftptoday.com

11

12

Testing CentralTesting Central

David ThompsonDavid [email protected]@SSTGB.org

931931--387387--22802280

1

Audit Core TeamResponsibilities

ProceduresDeadlines

Presented by Bob Muller, Steve Krovitz, Roger Wright, and Toni Webster

I (we) need two volunteers

Volunteer #1Why do we care? We don’t understand!

Volunteer #2It’s getting late, take a look at your watch!

2

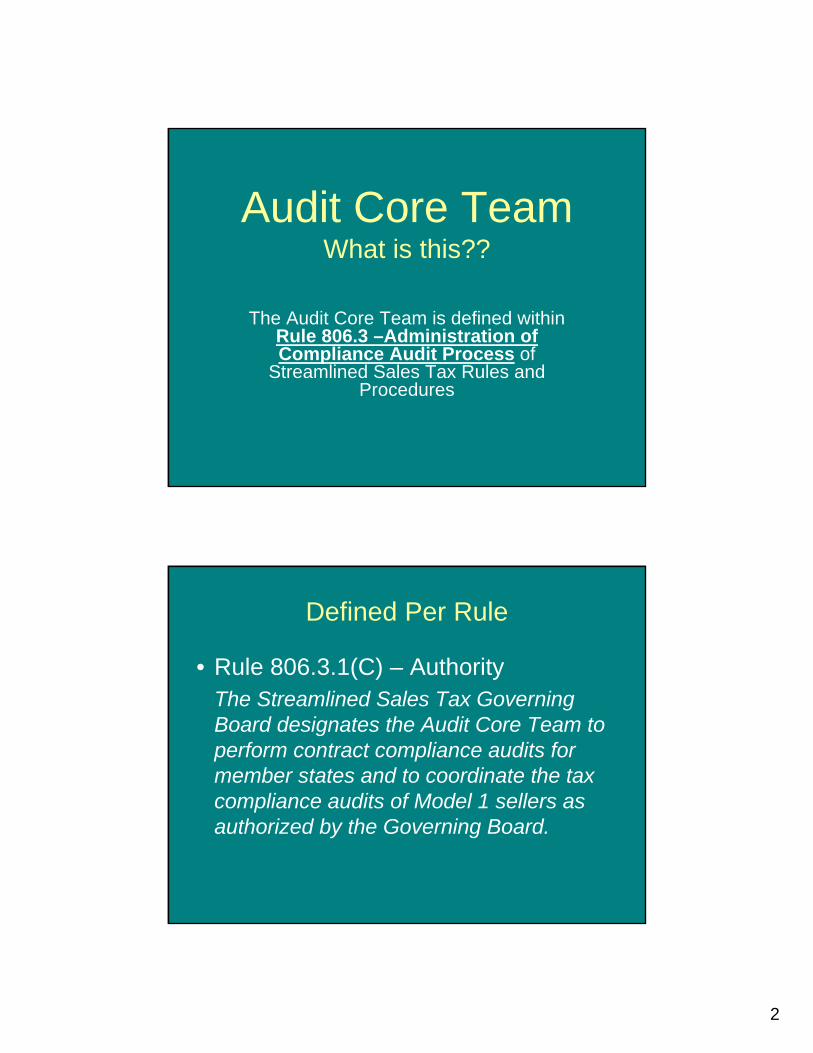

Audit Core TeamWhat is this??

The Audit Core Team is defined within Rule 806.3 –Administration of Compliance Audit Process of

Streamlined Sales Tax Rules and Procedures

Defined Per Rule

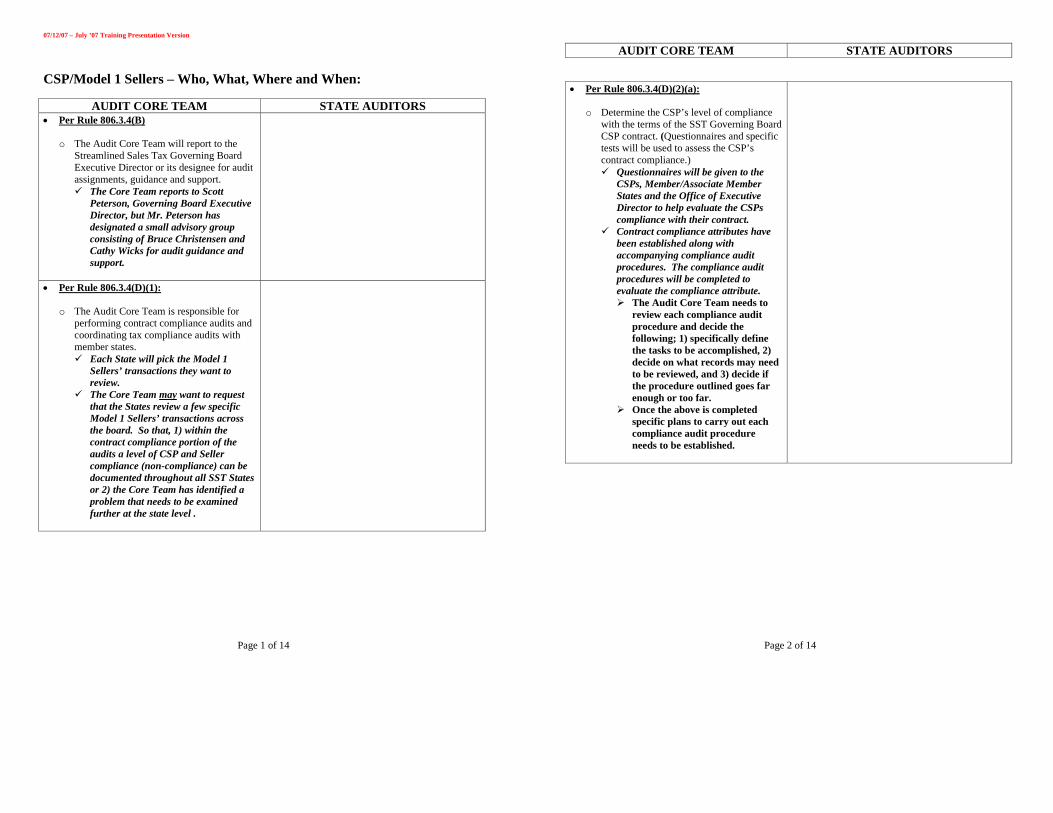

• Rule 806.3.1(C) – AuthorityThe Streamlined Sales Tax Governing Board designates the Audit Core Team to perform contract compliance audits for member states and to coordinate the tax compliance audits of Model 1 sellers as authorized by the Governing Board.

3

Defined Per Rule

• Rule 806.3.2(D) – Audit Core TeamThe Audit Core Team is a group of designated representatives from full member states who are responsible for coordinating compliance audits, performing contract compliance audits and compiling feedback reports for the Governing Board.

Defined Per Rule

• Rule 806.3.4(B) – Audit Core Team -Reporting Relationship

The Audit Core Team will report to the Streamlined Sales Tax Governing Board Executive Director or its designee for audit assignments, guidance and support.

4

Who is the Core Team

Steve KrovitzMinnesota Department

Of Revenue

Toni WebsterOklahoma TaxCommission

Who is the Core Team

Roger WrightWest Virginia Dept.Of Tax & Revenue

Bob MullerIndiana Department

Of Revenue

5

Does everyone understand the

Core Team concept?

Simply Stated -What We Do:• The Audit Core Team will complete a

contract compliance audit of all active Certified Service Providers (CSPs).

What You Do:• The Member and Associate Member State

Auditors will complete the tax compliance audit on sales transactions processed by the active CSPs.

6

The SST Rules Defines the Compliance Audit Process

• Rule 806.3.5 – Compliance Audit of a CSPA. The Compliance Audit of a CSP and its Model 1 sellers will include a contract compliance audit of the CSP and tax compliance audits of Model 1 sellers’ transactions processed through the CSP’s system.

B. The contract compliance audit of the CSP will be performed by the Audit Core Team. The tax compliance audits of the Model 1 sellers will be performed by member states under the coordination of the Audit Core Team.

Clear as Day!(Right!!!!)

7

The Audit Core Team:• Will evaluate all pertinent elements of the

current contract between the CSPs and the Streamlined Sales Tax Governing Board and assess each CSP’s compliance with the terms of the contract.

• As part of this contract compliance audit, they will audit areas where they are in the unique position to review. Then advise the Member and Associate Member State Auditors if problems exist that would impact the tax compliance audits.

• Will perform tax compliance audits on sales transactions of Model 1 sellers processed by the CSPs.

• As part of the CSP compliance audit process, they will report audit exceptions to the Audit Core Team.

The Member and Associate Member State Auditors:

8

When the rubber hits the road, it may be a little bumpy from time to time. Why….?

Because

• This type of audit has never been done before.

• Theory does not always equal practice.• Sometimes the road to knowledge can be

full of potholes.

9

-Solution-The Core Team will:• work hard• attempt to communicate effectively with everyone• be flexible in our approaches • keep the goal in focus

-Goal-

To complete a timely, accurate, and professional audit that meets the needs and expectations of the Streamlined Sales Tax Governing Board.

The Core Team will provide the State Auditors with two reports.• A preliminary report of findings will be

issued to the state auditors in later part of October 2007. This report will include any audit results discovered by the Core Team that could be relevant to the tax compliance audits.

• The final contract compliance audit will be given to each Member and Associate Member State in March of 2008.

10

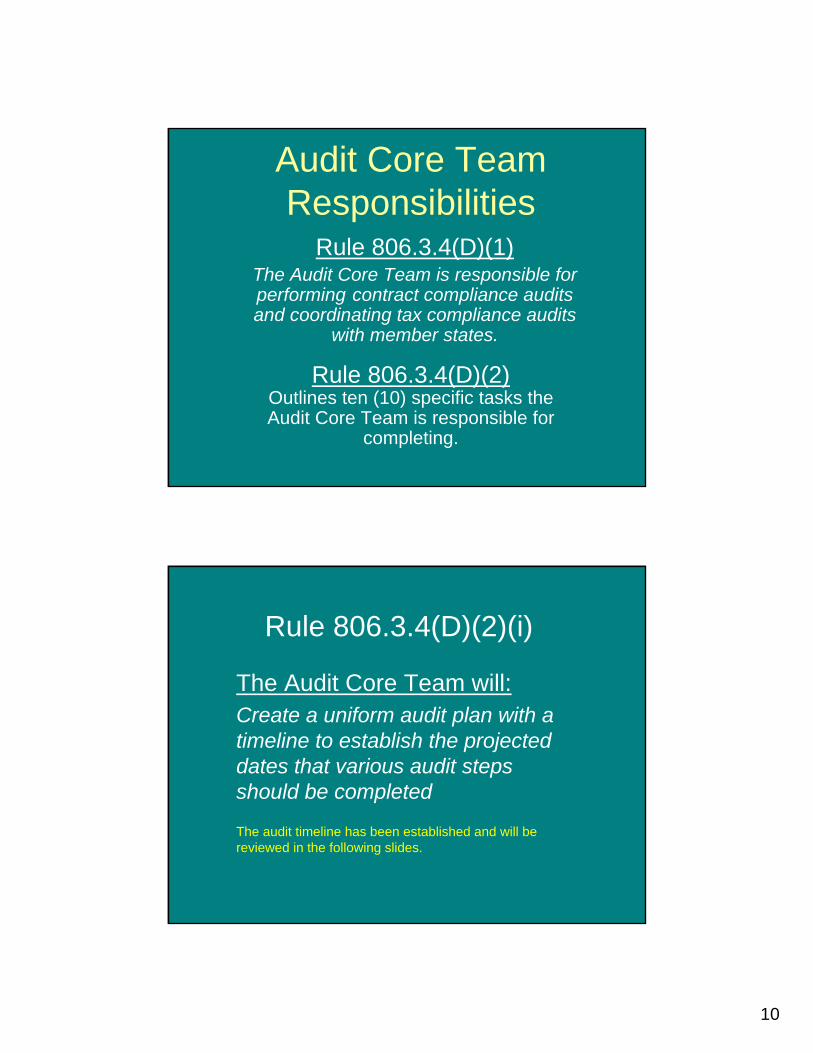

Audit Core TeamResponsibilities

Rule 806.3.4(D)(1)The Audit Core Team is responsible for performing contract compliance audits and coordinating tax compliance audits

with member states.

Rule 806.3.4(D)(2)Outlines ten (10) specific tasks the Audit Core Team is responsible for

completing.

Rule 806.3.4(D)(2)(i)

The Audit Core Team will:Create a uniform audit plan with a timeline to establish the projected dates that various audit steps should be completed

The audit timeline has been established and will be reviewed in the following slides.

11

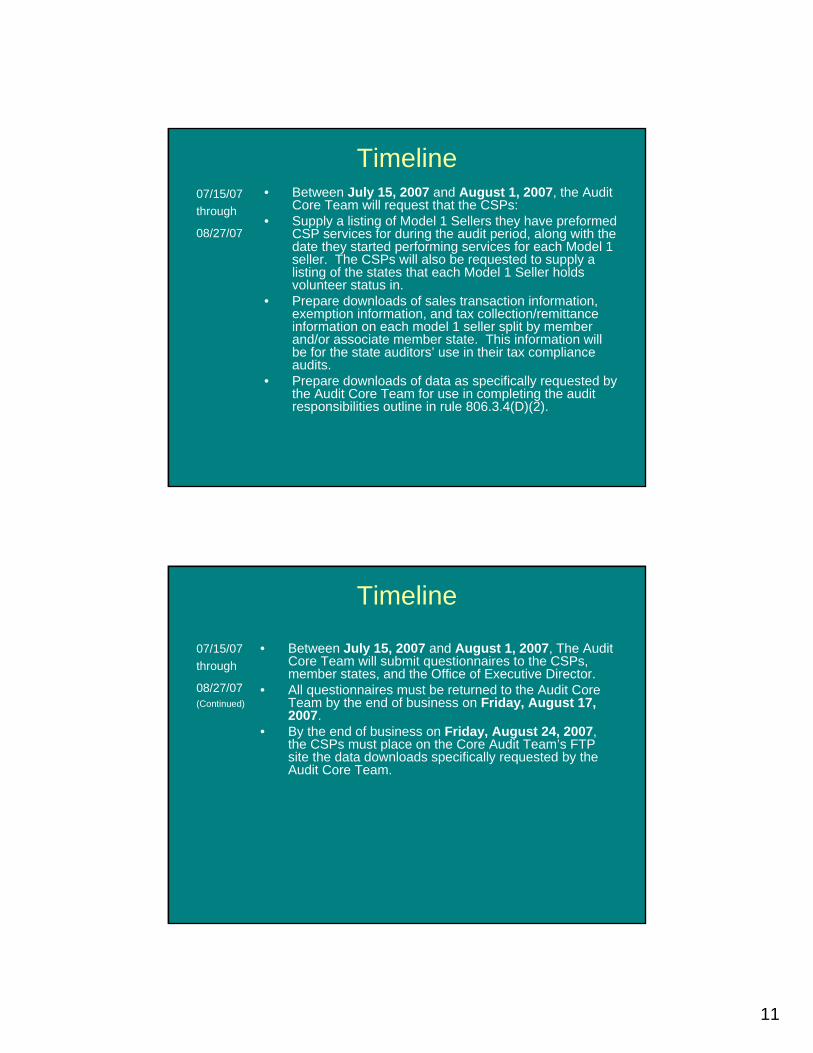

Timeline07/15/07through

08/27/07

• Between July 15, 2007 and August 1, 2007, the Audit Core Team will request that the CSPs:

• Supply a listing of Model 1 Sellers they have preformed CSP services for during the audit period, along with the date they started performing services for each Model 1 seller. The CSPs will also be requested to supply a listing of the states that each Model 1 Seller holds volunteer status in.

• Prepare downloads of sales transaction information, exemption information, and tax collection/remittance information on each model 1 seller split by member and/or associate member state. This information will be for the state auditors’ use in their tax compliance audits.

• Prepare downloads of data as specifically requested by the Audit Core Team for use in completing the audit responsibilities outline in rule 806.3.4(D)(2).

Timeline

07/15/07through

08/27/07(Continued)

• Between July 15, 2007 and August 1, 2007, The Audit Core Team will submit questionnaires to the CSPs, member states, and the Office of Executive Director.

• All questionnaires must be returned to the Audit Core Team by the end of business on Friday, August 17, 2007.

• By the end of business on Friday, August 24, 2007, the CSPs must place on the Core Audit Team’s FTP site the data downloads specifically requested by the Audit Core Team.

12

Timeline

08/28/07and 08/31/07

• The Audit Core Team will meet in St. Paul, Minnesota to review the completed questionnaires, go over data downloads, and finalize the CSP field work plans. An all day meeting is scheduled for Tuesday, August 28, 2007 and a half day meeting is planned for the morning of Friday, August 31, 2007.

Timeline

09/01/07through 10/15/07

• The Audit Core Team will complete field work at the CSPs location (it is important that during this time frame the Audit Core Team complete all field work in areas that could lead to an audit adjustment by any member/ associate member state).

• By October 1, 2007, the CSPs must place on each member state’s or associate member state’s FTP site the state specific sales transaction information, exemption information, and tax collection/remittance information for each model 1 seller they performed CSP services for.

• By October 15, 2007, The Audit Core Team will prepare preliminary reports that will be forwarded to the member states and associate member states detailing work completed in potential audit adjustment areas.

13

Timeline

10/16/07through

12/15/07

• During this period of time, the Audit Core Team can continue to work on and finalize the contract compliance portion of CSP audits.

• The member and associate member states will review the model 1 sellers’ records and prepare reports that notify the Audit Core Team of their findings.

• The member and associate member states’ preliminary feedback reports must be forwarded to the Audit Core Team by the end of business on Friday, December 14, 2007.

Timeline

12/16/07through 01/15/08

• The Audit Core Team will compile a report on the initial findings of the contract compliance audit and the member/associate member states’ tax compliance audits and submit the report to the CSP.

• Each CSP compliance audit initial findings must be forwarded to the respective CSP by the end of business on Tuesday, January 15, 2008.

14

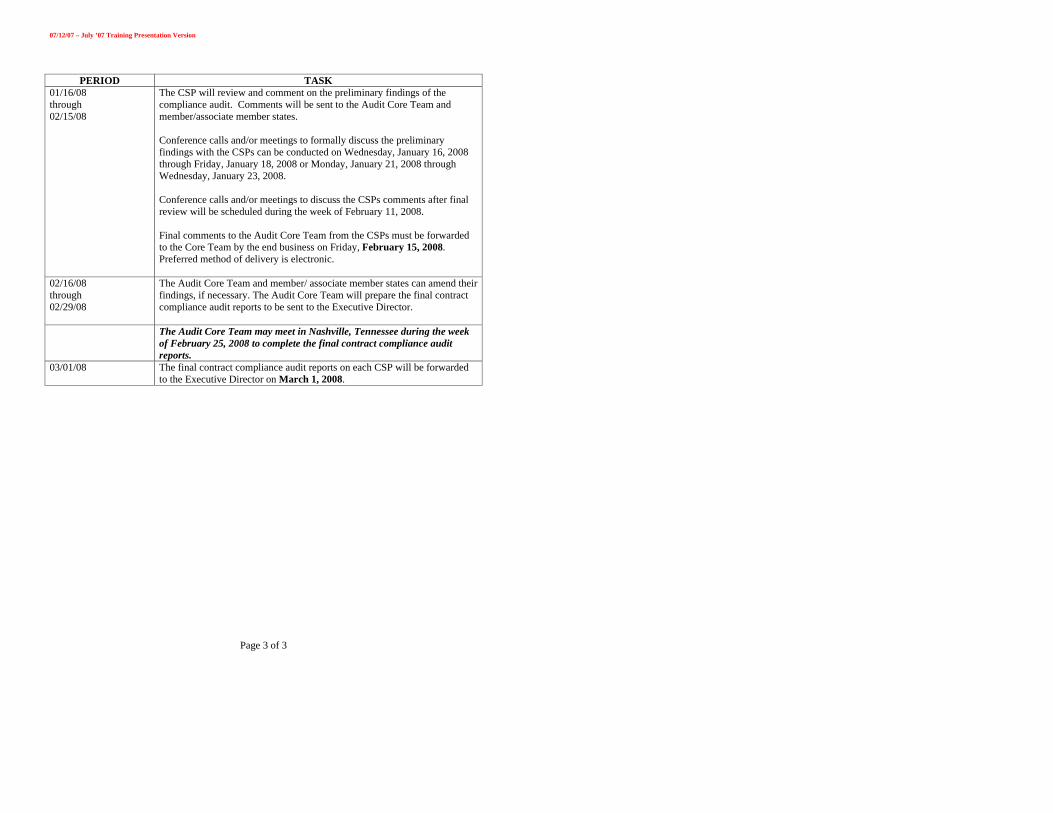

Timeline01/16/08through 02/15/08

• The CSP will review and comment on the preliminary findings of the compliance audit. Comments will be sent to the Audit Core Team and member/associate member states.

• Conference calls and/or meetings to formally discuss the preliminary findings with the CSPs can be conducted on Wednesday, January 16, 2008 through Friday, January 18, 2008 or Monday, January 21, 2008 through Wednesday, January 23, 2008.

• Conference calls and/or meetings to discuss the CSPs comments after final review will be scheduled during the week of February 11, 2008.

• Final comments to the Audit Core Team from the CSPs must be forwarded to the Core Team by the end business on Friday, February 15, 2008. Preferred method of delivery is electronic.

Timeline02/16/08through 02/29/08

03/01/08

• The audit core team and member/ associate member states can amend their findings, if necessary. The audit core team will prepare the final contract compliance audit reports to be sent to the executive director.

The final contract compliance audit reports on each CSP will be forwarded to the Executive Director on March 1, 2008.

15

Rule 806.3.4(D)(2)(g)The Audit Core Team will:Acquire a list of sellers represented by each CSP and provide this information to the Streamlined Sales Tax Governing Board member statesThis information will be requested and forwarded to the various states.

Rule 806.3.4(D)(2)(h)The Audit Core Team will:Coordinate with state auditors a download of all sales processed by the CSP for each seller, which will be available through access to a FTP site maintained by the SSTGB, Inc. to receive electronic records

The Audit Core Team will request that the CSPs download each states model 1 sellers’ transactions to the states FTP site. The Audit Core Team will follow-up to be assured the data is properly transferred.

16

ATTENTION !!!

• The next five areas to be discussed could result in audit findings relevant to the tax compliance audits.

Rule 806.3.4(D)(2)(e)The Audit Core Team will:Verify that all tax collected was remitted timely to the appropriate tax authority

Through sampling (statistical and/or random) and evaluation of the CSPs system, the Audit Core Team will verify that taxes collected are being remitted to the proper tax authority. As part of these procedures, sourcing will be evaluated.

17

Rule 806.3.4(D)(2)(f)The Audit Core Team will:Verify that sales were accurately reported by the CSP/Seller on simplified electronic returns (SERs)

Through statistical and/or random sampling the Audit Core Team will verify that both gross sales and net taxable sales are being properly reported on the simplified electronic returns.

Rule 806.3.4(D)(2)(b)The Audit Core Team will:Verify that compensation was calculated properly for all volunteer sellers

The Audit Core Team will evaluate the CSP’s system to be assured it is calculating compensation as dictated in the contract. Quarterly Compensation reports will be audited. A sampling of filed simplified electronic returns will be reviewed.

18

Compensation:

• You may find the manner be which compensation is calculated interesting. Compensation is addressed in Section D of the current contract between the CSPs and SST Governing Board. The compensation formula can be reviewed in section “D.5”, the rate adjustment process is outlined in section “D.6”, and resetting rates annually is addressed in section “D.7”.

Rule 806.3.4(D)(2)(d)The Audit Core Team will:Verify that the appropriate entity use exemption data elements are captured by the CSP system

The Audit Core Team will sample to be confident the CSP is obtaining the proper exemption data elements. The Core Team may request exception reports indicating missing exemption data elements.

19

Rule 806.3.4(D)(2)(c)The Audit Core Team will:Verify that appropriate procedures for mapping exist, are in conformance with the mapping requirements, and are followed in the initial mapping setup, as well as during updates and corrections to mapping The Audit Core Team will review the CSP’s mapping policies and procedures. They will also sample the CSPs’ mapping of their model 1 seller’s products to the generic taxability matrix categories.

Rule 806.3.4(D)(2)(a)The Audit Core Team will:Determine the CSP’s level of compliance with the terms of the CSP contract. (Questionnaires and specific tests will be used to assess the CSP’s contract compliance.)

The Audit Core Team will issue questionnaires to the CSPs, each Member/Associate Member State, and the Office of Executive Director addressing various elements of the contract. The completed questionnaires will be analyzed and used as the starting point of the contract compliance audit.

(continued)

20

Over a number of months, the SST Audit Committee isolated areas of definite audit interest in the CSP contract. The AuditCore Team will specifically look at these areas and complete various compliance audit procedures to assess the CSPs compliance with the contract.

Rule 806.3.4(D)(2)(a) - continued

Rule 806.3.4(D)(2)(j)The Audit Core Team will:Compile the feedback reports from the member states, summarize the findings and report to the Executive Director of the Streamlined Sales Tax Governing Board. The summaries must comply with confidentiality restrictions that apply to the SST Governing Board regarding disclosure.

Continued – next slide

21

For each CSP, the Audit Core Team will incorporate its findings from the contract compliance audit with the feedback reports from the Member and Associate Member States into a final compliance audit package to be issued to the Executive Director of the Streamlined Sales Tax Governing Board.

The Executive Director and the Governing Board will use these audits to evaluate the CSPs for contract renewal.

Rule 806.3.4(D)(2)(j) - continued

Final Audit Report

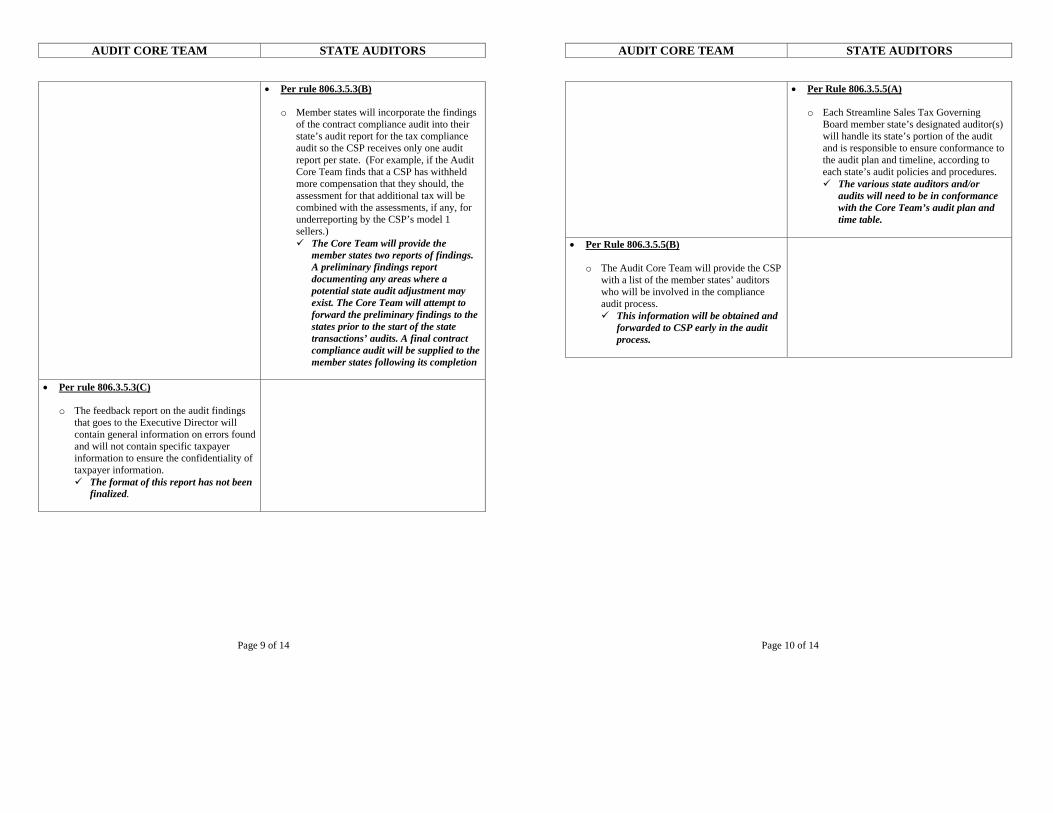

• Per rule 806.3.5.3(C)The feedback report on the audit findings that goes to the Executive Director will contain general information on errors found and will not contain specific taxpayer information to ensure the confidentiality of taxpayer information.

22

Important Dates for Member and Associate Member State Auditors

The CSP's will place on each member/associate members state's FTP site the state specific sales transaction information, exemption information, and tax collection/remittance information for each model 1 seller they performed CSP services for.

October 1, 2007Monday

All questionnaires must be returned to Audit Core Team by end of business today

August 17, 2007Friday

Audit Core team will submit questionnaire to member/associate member states.Today

Important Dates for Member and Associate Member State Auditors

Member/associate member states will review the model 1 sellers' records and prepare reports that notify the Audit Core Team of their findings.

October 16, 2007

to December 13,

2007

The Audit Core team will forward to member/associate member states reports detailing work completed in potential audit adjustment areas.

October 15, 2007Monday

23

Important Dates for Member and Associate Member State Auditors

The CSP will review and comment on the preliminary findings of the compliance audit. Comments will be sent to the Audit Core Team and member/associate member states.

December 15, 2007

toJanuary 16,

2008

All member/associate member states' preliminary feedback reports must be forwarded to the Audit Core Team by the end of business today.

December 14, 2007Friday

Important Dates for Member and Associate Member State Auditors

The final contract compliance audit report on each CSP will be forwarded to the Executive director

March 1, 2008Saturday

The Audit Core Team and member/associate member states can amend their findings, if necessary

February 16, 2008

to February 29,

2008

24

QUESTIONS???

Thank You.&

Good Luck

1

STREAMLINED SALES AND 2

USE TAX AGREEMENT 3

4

Adopted November 12, 2002 5

(Amended November 19, 2003, November 16, 2004, April 16, 2005, 6

October 1, 2005, January 13, 2006, April 18, 2006, August 30, 2006, 7

December 14, 2006, and June 23, 2007) 8

9

Streamlined Sales and Use Tax Agreement Page 1 June 23, 2007

TABLE OF CONTENTS 1

2

ARTICLE I 3

Purpose and Principle 4

101 Title . . . . . . . . . p. 6 5

102 Fundamental Purpose . . . . . . . p. 6 6

103 Taxing Authority Preserved . . . . . . p. 6 7

104 Defined Terms . . . . . . . p. 7 8

105 Treatment of Vending Machines . . . . . p. 7 9

10

ARTICLE II 11

Definitions 12

201 Agent . . . . . . . . . p. 8 13

202 Certified Automated System (CAS) . . . . . p. 8 14

203 Certified Service Provider (CSP) . . . . . p. 8 15

204 Entity-Based Exemption . . . . . . p. 8 16

205 Model 1 Seller . . . . . . . p. 8 17

206 Model 2 Seller . . . . . . . p. 8 18

207 Model 3 Seller . . . . . . . p. 8 19

208 Person . . . . . . . . p. 9 20

209 Product-Based Exemption . . . . . . p. 9 21

210 Purchaser . . . . . . . . p. 9 22

211 Registered Under This Agreement . . . . . p. 9 23

212 Seller . . . . . . . . . p. 9 24

213 State . . . . . . . . . p. 9 25

214 Use-Based Exemption . . . . . . p. 9 26

27

ARTICLE III 28

Requirements Each State Must Accept to Participate 29

301 State Level Administration. . . . . . . p. 10 30

Streamlined Sales and Use Tax Agreement Page 2 June 23, 2007

302 State and Local Tax Bases . . . . . . p. 10 1

303 Seller Registration . . . . . . . p. 10 2

304 Notice for Tax Changes . . . . . . p. 11 3

305 Local Rate and Boundary Changes . . . . . p. 11 4

306 Relief from Certain Liability . . . . . . p. 14 5

307 Database Requirements and Exceptions . . . . p. 15 6

308 State and Local Tax Rates . . . . . . p. 16 7

309 Application of General Sourcing Rules and Exclusions From the Rules p. 16 8

310 General Sourcing Rules . . . . . . p. 17 9

311 General Sourcing Definitions . . . . . p. 20 10

312 Multiple Points of Use (Effective through December 31, 2007) 11

Repealed December 14, 2006 . . . . . . p. 20 12

312 Multiple Points of Use (Effective on and after January 1, 2008) 13

Repealed December 14, 2006 . . . . . . p. 21 14

313 Direct Mail Sourcing . . . . . . . p. 22 15

314 Telecommunication and Related Services Sourcing Rule. . . p. 23 16

315 Telecommunication Sourcing Definitions (Effective through 17

Dec. 31, 2007). . . . . . . . p. 25 18

315 Telecommunication Sourcing Definitions (Effective on and after 19

January 1, 2008). . . . . . . . p. 27 20

316 Enactment of Exemptions (Effective through Dec. 31, 2007). . p. 29 21

316 Enactment of Exemptions (Effective on and after January 1, 2008) . p. 30 22

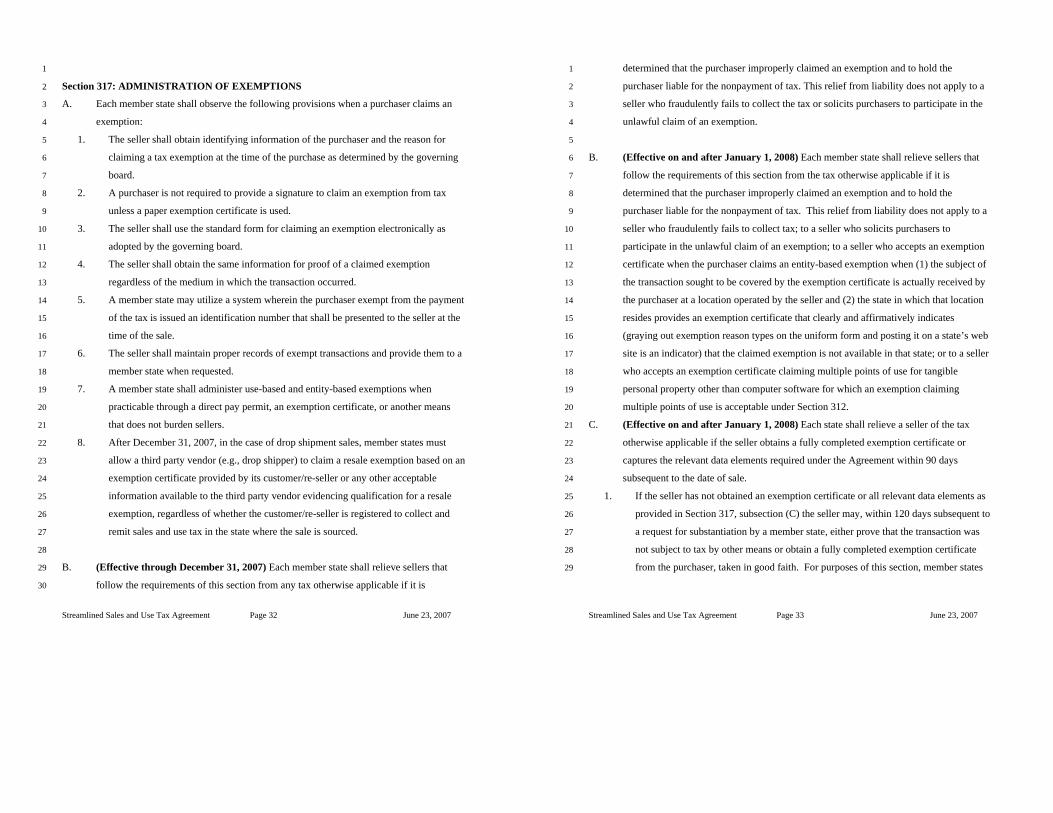

317 Administration of Exemptions . . . . . p. 32 23

318 Uniform Tax Returns . . . . . . . p. 34 24

319 Uniform Rules for Remittances of Funds . . . . p. 35 25

320 Uniform Rules for Recovery of Bad Debts . . . . p. 36 26

321 Confidentiality and Privacy Protections under Model 1 . . p. 37 27

322 Sales Tax Holidays . . . . . . . p. 39 28

323 Caps and Thresholds . . . . . . . p. 43 29

324 Rounding Rule . . . . . . . p. 43 30

Streamlined Sales and Use Tax Agreement Page 3 June 23, 2007

325 Customer Refund Procedures . . . . . . p. 44 1

326 Direct Pay Permit . . . . . . . p. 45 2

327 Library of Definitions . . . . . . p. 45 3

328 Taxability Matrix . . . . . . . p. 46 4

329 Effective Date for Rate Changes . . . . . p. 46 5

330 Bundled Transactions (Effective on and after January 1, 2008) . p. 46 6

331 Relief From Certain Liability (Effective on and after January 1, 2009) p. 47 7

8

ARTICLE IV 9

Seller Registration 10

401 Seller Participation . . . . . . . p. 49 11

402 Amnesty for Registration . . . . . . p. 49 12

403 Method of Remittance . . . . . . . p. 50 13

404 Registration by an Agent . . . . . . p. 51 14

15

ARTICLE V 16

Provider and System Certification 17

501 Certification of Service Providers and Automated Systems . . p. 52 18

502 State Review and Approval of Certified Automated System 19

Software and Certain Liability Relief (Effective on and after 20

January 1, 2008). . . . . . . . p. 53 21

22

ARTICLE VI 23

Monetary Allowances for New Technological 24

Models For Sales Tax Collection 25

601 Monetary Allowance Under Model 1 . . . . . p. 55 26

602 Monetary Allowance for Model 2 Sellers . . . . p. 55 27

603 Monetary Allowance for Model 3 Sellers 28

and All Other Sellers Not Under Models 1 or 2 . . . p. 56 29

30

Streamlined Sales and Use Tax Agreement Page 4 June 23, 2007

ARTICLE VII 1

Agreement Organization 2

701 Effective Date . . . . . . . . p. 57 3

702 Approval of Initial States . . . . . . p. 57 4

703 Streamlined Sales Tax Implementing States . . . . p. 58 5

704 Consideration of Petitions . . . . . . p. 60 6

705 Associate Membership . . . . . . p. 60 7

8

ARTICLE VIII 9

State Entry and Withdrawal 10

801 Entry Into Agreement . . . . . . p. 63 11

802 Certificate of Compliance . . . . . . p. 64 12

803 Annual Recertification of Member States . . . . p. 64 13

804 Requirements for Membership Approval . . . . p. 65 14

805 Compliance . . . . . . . . p. 65 15

806 Agreement Administration . . . . . . p. 65 16

807 Open Meetings . . . . . . . p. 66 17

808 Withdrawal of Membership or Expulsion of a Member. . . p. 67 18

809 Sanction of Member States . . . . . . p. 68 19

810 State and Local Advisory Council . . . . . p. 69 20

811 Business Advisory Council . . . . . . p. 69 21

22

ARTICLE IX 23

Amendments and Interpretations 24

901 Amendments to Agreement . . . . . . p. 70 25

902 Interpretations of Agreement . . . . . . p. 70 26

903 Definition Requests . . . . . . . p. 71 27

28

ARTICLE X 29

Issue Resolution Process 30

Streamlined Sales and Use Tax Agreement Page 5 June 23, 2007

1001 Rules and Procedures for Dispute Resolution . . . p. 72 1

1002 Petition for Resolution . . . . . . p. 72 2

1003 Final Decision of Governing Board . . . . . p. 72 3

1004 Limited Scope of this Article . . . . . . p. 72 4

5

ARTICLE XI 6

Relationship of Agreement to Member States and Persons 7

1101 Cooperating Sovereigns . . . . . . p. 74 8

1102 Relationship to State Law . . . . . . p. 74 9

1103 Limited Binding and Beneficial Effect . . . . p. 74 10

1104 Final Determinations . . . . . . . p. 75 11

12

ARTICLE XII 13

Review of Costs and Benefits Associated with the System 14

1201 Review of Costs and Benefits . . . . . . p. 76 15

16

Appendix A 17

Petition for Membership. . . . . . . . p. 77 18

Appendix B 19

Index of Definitions . . . . . . . . p. 78 20

Appendix C 21

Library of Definitions . . . . . . . . p. 82 22

Appendix D 23

Library of Interpretations . . . . . . . p. 109 24

Streamlined Sales and Use Tax Agreement Page 6 June 23, 2007

ARTICLE I 1

PURPOSE AND PRINCIPLE 2

3

Section 101: TITLE 4

This multistate Agreement shall be referred to, cited, and known as the Streamlined Sales and 5

Use Tax Agreement. 6

7

Section 102: FUNDAMENTAL PURPOSE 8

It is the purpose of this Agreement to simplify and modernize sales and use tax administration in 9

the member states in order to substantially reduce the burden of tax compliance. The Agreement 10

focuses on improving sales and use tax administration systems for all sellers and for all types of 11

commerce through all of the following: 12

A. State level administration of sales and use tax collections. 13

B. Uniformity in the state and local tax bases. 14

C. Uniformity of major tax base definitions. 15

D. Central, electronic registration system for all member states. 16

E. Simplification of state and local tax rates. 17

F. Uniform sourcing rules for all taxable transactions. 18

G. Simplified administration of exemptions. 19

H. Simplified tax returns. 20

I. Simplification of tax remittances. 21

J. Protection of consumer privacy. 22

23

Section 103: TAXING AUTHORITY PRESERVED 24

This Agreement shall not be construed as intending to influence a member state to impose a tax 25

on or provide an exemption from tax for any item or service. However, if a member state 26

chooses to tax an item or exempt an item from tax, that state shall adhere to the provisions 27

concerning definitions as set out in Article III of this Agreement. 28

29

Streamlined Sales and Use Tax Agreement Page 7 June 23, 2007

Section 104: DEFINED TERMS 1

This Agreement defines terms for use within the Agreement and for application in the sales and 2

use tax laws of the member states. The definition of a term is not intended to influence the 3

interpretation or application of that term with respect to other tax types. 4

5

An alphabetical list of all the terms defined in the Agreement and their location in the Agreement 6

is found in Appendix B of this Agreement, the Index of Definitions. Terms defined for use 7

within this Agreement are set out in Article II of the Agreement. Many of the uniform definitions 8

for application in the sales and use tax laws of the member states are set out in Appendix C of 9

this Agreement, the Library of Definitions. Definitions that are not set out in Appendix C are 10

defined when applied in a particular section of the Agreement and are set out in that section of 11

the Agreement. The appendices have the same effect as the Articles in the Agreement. 12

13

Section 105: TREATMENT OF VENDING MACHINES 14

The provisions of the Agreement do not apply to vending machines sales. The Agreement does 15

not restrict how a member state taxes vending machine sales. 16

Streamlined Sales and Use Tax Agreement Page 8 June 23, 2007

ARTICLE II 1

DEFINITIONS 2

3

The following definitions apply in this Agreement: 4

Section 201: AGENT 5

A person appointed by a seller to represent the seller before the member states. 6

Section 202: CERTIFIED AUTOMATED SYSTEM (CAS) 7

Software certified under the Agreement to calculate the tax imposed by each jurisdiction on a 8

transaction, determine the amount of tax to remit to the appropriate state, and maintain a record 9

of the transaction. 10

Section 203: CERTIFIED SERVICE PROVIDER (CSP) 11

An agent certified under the Agreement to perform all the seller's sales and use tax functions, 12

other than the seller's obligation to remit tax on its own purchases. 13

Section 204: ENTITY-BASED EXEMPTION 14

An exemption based on who purchases the product or who sells the product. An exemption that 15

is available to all individuals shall not be considered an entity-based exemption. 16

Compiler’s note: On October 1, 2005 Section 204 was amended by adding the second sentence. Each member state 17

shall comply with the October 1, 2005 amendment to this section no later than January 1, 2008. 18

Section 205: MODEL 1 SELLER 19

A seller that has selected a CSP as its agent to perform all the seller's sales and use tax functions, 20

other than the seller's obligation to remit tax on its own purchases. 21

Section 206: MODEL 2 SELLER 22

A seller that has selected a CAS to perform part of its sales and use tax functions, but retains 23

responsibility for remitting the tax. 24

Section 207: MODEL 3 SELLER 25

A seller that has sales in at least five member states, has total annual sales revenue of at least five 26

hundred million dollars, has a proprietary system that calculates the amount of tax due each 27

jurisdiction, and has entered into a performance agreement with the member states that 28

establishes a tax performance standard for the seller. As used in this definition, a seller includes 29

an affiliated group of sellers using the same proprietary system. 30

31 Streamlined Sales and Use Tax Agreement Page 9 June 23, 2007

Section 208: PERSON 1

An individual, trust, estate, fiduciary, partnership, limited liability company, limited liability 2

partnership, corporation, or any other legal entity. 3

Section 209: PRODUCT-BASED EXEMPTION 4

An exemption based on the description of the product and not based on who purchases the 5

product or how the purchaser intends to use the product. 6

Section 210: PURCHASER 7

A person to whom a sale of personal property is made or to whom a service is furnished. 8

Section 211: REGISTERED UNDER THIS AGREEMENT 9

Registration by a seller with the member states under the central registration system provided in 10

Article IV of this Agreement. 11

Section 212: SELLER 12

A person making sales, leases, or rentals of personal property or services. 13

Section 213: STATE 14

Any state of the United States, the District of Columbia, and the Commonwealth of Puerto Rico. 15

Compiler’s note: On April 18, 2006 Section 213 was amended as follows: “Any state of the United States, and the 16

District of Columbia and the Commonwealth of Puerto Rico.” The amendment to this section became effective upon 17

adoption. 18

Section 214: USE-BASED EXEMPTION 19

An exemption based on a specified use of the product by the purchaser. 20

Compiler’s note: On October 1, 2005 Section 214 was amended as follows: “An exemption based on a specified use 21

of the product by the purchaser’s use of the product.” Each member state shall comply with the October 1, 2005 22

amendment to this section no later than January 1, 2008. 23

Streamlined Sales and Use Tax Agreement Page 10 June 23, 2007

ARTICLE III 1

REQUIREMENTS EACH STATE MUST ACCEPT TO PARTICIPATE 2

3

Section 301: STATE LEVEL ADMINISTRATION 4

Each member state shall provide state level administration of sales and use taxes. The state level 5

administration may be performed by a member state's Tax Commission, Department of Revenue, 6

or any other single entity designated by state law. Sellers are only required to register with, file 7

returns with, and remit funds to the state level authority. Each member state shall provide for 8

collection of any local taxes and distribution of them to the appropriate taxing jurisdictions. 9

Each member state shall conduct, or authorize others to conduct on its behalf, all audits of the 10

sellers registered under the Agreement for that state’s tax and the tax of its local jurisdictions, 11

and local jurisdictions shall not conduct independent sales or use tax audits of sellers registered 12

under the Agreement. 13

14

Section 302: STATE AND LOCAL TAX BASES 15

Through December 31, 2005, if a member state has local jurisdictions that levy a sales or use tax, 16

all local jurisdictions in the state shall have a common tax base. After December 31, 2005, the 17

tax base for local jurisdictions shall be identical to the state tax base unless otherwise prohibited 18

by federal law. This section does not apply to sales or use taxes levied on the retail sale or 19

transfer of motor vehicles, aircraft, watercraft, modular homes, manufactured homes, or mobile 20

homes. 21

22

Section 303: SELLER REGISTRATION 23

Each member state shall participate in an online sales and use tax registration system in 24

cooperation with the other member states. Under this system: 25

A. A seller registering under the Agreement is registered in each of the member states. 26

B. The member states agree not to require the payment of any registration fees or other 27

charges for a seller to register in a state in which the seller has no legal requirement to 28

register. 29

C. A written signature from the seller is not required. 30

Streamlined Sales and Use Tax Agreement Page 11 June 23, 2007

D. An agent may register a seller under uniform procedures adopted by the member states. 1

E. A seller may cancel its registration under the system at any time under uniform 2

procedures adopted by the governing board. Cancellation does not relieve the seller of its 3

liability for remitting to the proper states any taxes collected. 4

5

Section 304: NOTICE FOR STATE TAX CHANGES 6

A. Each member state shall lessen the difficulties faced by sellers when there is a change in 7

a state sales or use tax rate or base by making a reasonable effort to do all of the 8

following: 9

1. Provide sellers with as much advance notice as practicable of a rate change. 10

2. Limit the effective date of a rate change to the first day of a calendar quarter. 11

3. Notify sellers of legislative changes in the tax base and amendments to sales and use 12

tax rules and regulations. 13

B. Failure of a seller to receive notice or failure of a member state to provide notice or limit 14

the effective date of a rate change shall not relieve the seller of its obligation to collect 15

sales or use taxes for that member state. 16

17

Section 305: LOCAL RATE AND BOUNDARY CHANGES 18

Each member state that has local jurisdictions that levy a sales or use tax shall: 19

A. Provide that local rate changes will be effective only on the first day of a calendar 20

quarter after a minimum of sixty days’ notice to sellers. 21

B. Apply local sales tax rate changes to purchases from printed catalogs wherein the 22

purchaser computed the tax based upon local tax rates published in the catalog only on 23

the first day of a calendar quarter after a minimum of one hundred twenty days’ notice to 24

sellers. 25

C. For sales and use tax purposes only, apply local jurisdiction boundary changes only on 26

the first day of a calendar quarter after a minimum of sixty days’ notice to sellers. 27

D. Provide and maintain a database that describes boundary changes for all taxing 28

jurisdictions. This database shall include a description of the change and the effective 29

date of the change for sales and use tax purposes. 30

Streamlined Sales and Use Tax Agreement Page 12 June 23, 2007

E. Provide and maintain a database of all sales and use tax rates for all of the jurisdictions 1

levying taxes within the state. For the identification of states, counties, cities, and 2

parishes, codes corresponding to the rates must be provided according to Federal 3

Information Processing Standards (FIPS) as developed by the National Institute of 4

Standards and Technology. For the identification of all other jurisdictions, codes 5

corresponding to the rates must be in the format determined by the governing board. 6

F. Provide and maintain a database that assigns each five digit and nine digit zip code 7

within a member state to the proper tax rates and jurisdictions. The state must apply the 8

lowest combined tax rate imposed in the zip code area if the area includes more than one 9

tax rate in any level of taxing jurisdictions. If a nine digit zip code designation is not 10

available for a street address or if a seller or CSP is unable to determine the nine digit zip 11

code designation applicable to a purchase after exercising due diligence to determine the 12

designation, the seller or CSP may apply the rate for the five digit zip code area. For the 13

purposes of this section, there is a rebuttable presumption that a seller or CSP has 14

exercised due diligence if the seller has attempted to determine the nine digit zip code 15

designation by utilizing software approved by the governing board that makes this 16

designation from the street address and the five digit zip code applicable to a purchase. 17

G. Have the option of providing address-based boundary database records for assigning 18

taxing jurisdictions and their associated rates which shall be in addition to the 19

requirements of subsection (F) of this section. The database records must be in the same 20

approved format as the database records pursuant to subsection (F) of this section and 21

must meet the requirements developed pursuant to the federal Mobile 22

Telecommunications Sourcing Act (4 U.S.C.A. Sec. 119(a)). The governing board may 23

allow a member state to require sellers that register under this Agreement to use an 24

address-based database provided by that member state. If any member state develops 25

address-based assignment database records pursuant to the Agreement, a seller or CSP 26

may use those database records in place of the five and nine-digit zip code database 27

records provided for in subsection (F) of this section. If a seller or CSP is unable to 28

determine the applicable rate and jurisdiction using an address-based database record 29

after exercising due diligence, the seller or CSP may apply the nine digit zip code 30

Streamlined Sales and Use Tax Agreement Page 13 June 23, 2007

designation applicable to a purchase. If a nine-digit zip code designation is not available 1

for a street address or if a seller or CSP is unable to determine the nine digit zip code 2

designation applicable to a purchase after exercising due diligence to determine the 3

designation, the seller or CSP may apply the rate for the five digit zip code area. For the 4

purposes of this section, there is a rebuttable presumption that a seller or CSP has 5

exercised due diligence if the seller or CSP has attempted to determine the tax rate and 6

jurisdiction by utilizing software approved by the governing board that makes this 7

assignment from the address and zip code information applicable to the purchase. 8

H. States that have met the requirements of subsection (F) may also elect to certify vendor 9

provided address-based databases for assigning tax rates and jurisdictions. The 10

databases must be in the same approved format as the database records pursuant to (G) 11

of this section and must meet the requirements developed pursuant to the federal Mobile 12

Telecommunications Sourcing Act (4 U.S.C.A. Sec. 119 (a)). If a state certifies a 13

vendor address-based database, a seller or CSP may use that database in place of the 14

database provided for in subsection (F) or (G) of this section. Vendors providing 15

address-based databases may request certification of their databases from the governing 16

board. Certification by the governing board does not replace the requirement that the 17

databases be certified by the states individually. 18

I. Make databases provided pursuant to subsections (E), (F), (G) and (H) available to a 19

seller or CSP by the first day of the month prior to the first day of a calendar quarter. 20

Databases must be in a format approved by the governing board and available on each 21

state’s website or other location determined by the governing board. 22

Compiler’s note: On October 1, 2005 the following amendments were made to Section 305: 23

1. In Section 305 (F) “or CSP” was added after each “seller.” In addition, in two places “of a 24

purchaser” was replaced with “applicable to a purchase.” 25

2. Section 305 (G) was amended as follows: “Participate with other member states in the 26

development of an Have the option of providing address-based system database records for 27

assigning taxing jurisdictions and their associated rates which shall be in addition to the 28

requirements of subsection (F) of this section. The system database records must be in the same 29

approved format as the database records pursuant to subsection (F) of this section and must meet 30

the requirements developed pursuant to the federal Mobile Telecommunications Sourcing Act (4 31

U.S.C. Sec. 119) (4 U.S.C.A. Sec.119 (a)). The governing board may allow a member state to 32

Streamlined Sales and Use Tax Agreement Page 14 June 23, 2007

require sellers that register under this Agreement to use an address-based system database 1

provided by that member state. If any member state develops an address-based assignment system 2

database records pursuant to the Mobile Telecommunications Sourcing Act Agreement, a seller or 3

CSP may use that system those database records in place of the system five and nine-digit zip code 4

database records provided for in subsection (F) of this section. If a seller or CSP is unable to 5

determine the applicable rate and jurisdiction using an address-based database record after 6

exercising due diligence, the seller or CSP may apply the nine digit zip code designation 7

applicable to a purchase. If a nine-digit zip code designation is not available for a street address 8

or if a seller or CSP is unable to determine the nine digit zip code designation applicable to a 9

purchase after exercising due diligence to determine the designation, the seller or CSP may apply 10

the rate for the five digit zip code area. For the purposes of this section, there is a rebuttable 11

presumption that a seller or CSP has exercised due diligence if the seller or CSP has attempted to 12

determine the tax rate and jurisdiction by utilizing software approved by the governing board that 13

makes this assignment from the address and zip code information applicable to the purchase”. 14

3. Section305 (H) was added. 15

The amendment to this section became effective upon adoption. 16

Compiler’s note: On June 23, 2007 subsection I was added. 17

18

Section 306: RELIEF FROM CERTAIN LIABILITY 19

Each member state shall relieve sellers and CSPs using databases pursuant to subsections (F), 20

(G) and (H) of Section 305 from liability to the member state and local jurisdictions for having 21

charged and collected the incorrect amount of sales or use tax resulting from the seller or CSP 22

relying on erroneous data provided by a member state on tax rates, boundaries, or taxing 23

jurisdiction assignments. After providing adequate notice as determined by the governing board, 24

a member state that provides an address-based database for assigning taxing jurisdictions 25

pursuant to Section 305, subsection (G) or (H) may cease providing liability relief for errors 26

resulting from the reliance on the database provided by the member state under the provisions of 27

Section 305, subsection (F). If a seller demonstrates that requiring the use of the address-based 28

database would create an undue hardship, a member state and the governing board may extend 29

the relief from liability to such seller for a designated period of time. 30

Compiler’s note: On October 1, 2005 Section 306 was amended as follows: “Each member state shall relieve sellers 31

and CSPs using databases pursuant to subsections (F), (G) and (H) from liability to the member state and local 32

jurisdictions for having charged and collected the incorrect amount of sales or use tax resulting from the seller or 33

Streamlined Sales and Use Tax Agreement Page 15 June 23, 2007

CSP relying on erroneous data provided by a member state on tax rates, boundaries, or taxing jurisdiction 1

assignments. After providing adequate notice as determined by the governing board, a A member state that provides 2

an address-based system database for assigning taxing jurisdictions pursuant to Section 305, subsection (G) or 3

pursuant to the federal Mobile Telecommunications Sourcing Act will not be required to provide or (H) may cease 4

providing liability relief for errors resulting from the reliance on the information database provided by the member 5

state under the provisions of Section 305, subsection (F). If a seller demonstrates that requiring the use of the 6

address-based database would create an undue hardship, a member state and the governing board may extend the 7

relief from liability to such seller for a designated period of time.” 8

The amendment to this section became effective upon adoption. 9

10

Section 307: DATABASE REQUIREMENTS AND EXCEPTIONS 11

A. The electronic databases provided for in Section 305, subsections (D), (E), (F), and (G) 12

shall be in a downloadable format approved by the governing board. The databases may 13

be directly provided by the state or provided by a vendor as designated by the state. A 14

database provided by a vendor as designated by a state shall be applicable to and subject 15

to all provisions of Sections 305, 306 and this section. These databases must be 16

provided at no cost to the user of the database. 17

B. The provisions of Section 305, subsections (F) and (G) do not apply when the purchased 18

product is received by the purchaser at the business location of the seller. 19

C. The databases provided by Section 305, subsections (D), (E), (F), and (G) are not a 20

requirement of a state prior to entering into the Agreement. A seller that did not have a 21

requirement to register in a state prior to registering pursuant to this Agreement or a CSP 22

shall not be required to collect sales or use taxes for a state until the first day of the 23

calendar quarter commencing more than sixty days after the state has provided the 24

databases required by Section 305, subsections (D), (E), and (F). Provided, for the initial 25

implementation of the Agreement pursuant to Section 701, a CSP shall be required to 26

collect sales or use taxes for each member state, subject to the provisions of Section 705, 27

pursuant to the terms of the operating agreement entered into between the CSP and the 28

governing board in order to provide adequate time for testing and loading of the 29

databases. 30

Compiler’s note: On October 1, 2005 the following amendments were made to Section 307: 31

Section 307 (A) was amended by adding the last three sentences. 32

Streamlined Sales and Use Tax Agreement Page 16 June 23, 2007

Section 307 (C) was amended by adding “and (G)” after “(F),” deleting the second sentence (The governing board 1

shall establish the effective dates for availability and use of the databases.) and adding the last two sentences. 2

The amendment to this section became effective upon adoption. 3

4

Section 308: STATE AND LOCAL TAX RATES 5

A. No member state shall have multiple state sales and use tax rates on items of personal 6

property or services, except that a member state may impose a single additional rate, 7

which may be zero, on food and food ingredients and drugs as defined by state law 8

pursuant to the Agreement. In addition, if federal law prohibits the imposition of local 9

tax on a product that is subject to state tax, the state may impose an additional rate on 10

such product, provided such rate achieves tax parity for similar products. 11

B. A member state that has local jurisdictions that levy a sales or use tax shall not have 12

more than one local sales tax rate or more than one local use tax rate per local 13

jurisdiction. If the local jurisdiction levies both a sales tax and use tax, the local rates 14

must be identical. 15

C. The provisions of this section do not apply to sales or use taxes levied on electricity, 16

piped natural or artificial gas, or other heating fuels delivered by the seller, or the retail 17

sale or transfer of motor vehicles, aircraft, watercraft, modular homes, manufactured 18

homes, or mobile homes. 19

Compiler’s note: On April 18, 2006 Section 308A was amended by deleting “after December 31, 2005” following 20

“or services” and by adding the second sentence. The amendment to this section became effective upon adoption. 21

22

Section 309: APPLICATION OF GENERAL SOURCING RULES AND EXCLUSIONS 23

FROM THE RULES 24

A. Each member state shall agree to require sellers to source the retail sale of a product in 25

accordance with Section 310. The provisions of Section 310 apply regardless of the 26

characterization of a product as tangible personal property, a digital good, or a service. 27

The provisions of Section 310 only apply to determine a seller's obligation to pay or 28

collect and remit a sales or use tax with respect to the seller's retail sale of a product. 29

These provisions do not affect the obligation of a purchaser or lessee to remit tax on the 30

use of the product to the taxing jurisdictions of that use. 31

Streamlined Sales and Use Tax Agreement Page 17 June 23, 2007

B. Sections 310 and 312 do not apply to sales or use taxes levied on the following: 1

1. The retail sale or transfer of watercraft, modular homes, manufactured homes, or 2

mobile homes. These items must be sourced according to the requirements of each 3

member state. 4

2. The retail sale, excluding lease or rental, of motor vehicles, trailers, semi-trailers, or 5

aircraft that do not qualify as transportation equipment, as defined in Section 310, 6

subsection (D). The retail sale of these items shall be sourced according to the 7

requirements of each member state, and the lease or rental of these items must be 8

sourced according to Section 310, subsection (C). 9

3. Telecommunications services and ancillary services, as set out in Section 315, and 10

Internet access service shall be sourced in accordance with Section 314. 11

4. Until December 31, 2009, florist sales as defined by each member state. Prior to this 12

date, these items must be sourced according to the requirements of each member 13

state. 14

Compiler’s note: On October 1, 2005 Section 309 (B)(4) was amended by deleting 2005 and inserting 2007. The 15

amendment to this section became effective upon adoption. Compiler’s note: On December 14, 2006 Section 309 16

(b) was amended as follows: “Section Sections 310 and 312 does do”, and 309 (B) (3) was amended by adding 17

“and ancillary services” following “services” and “and Internet access service” before “shall”. 18

Compiler’s note: On June 23, 2007 the date in subsection B 4 was changed from “December 31, 2007” to 19

December 31, 2009.” 20

21

Section 310: GENERAL SOURCING RULES 22

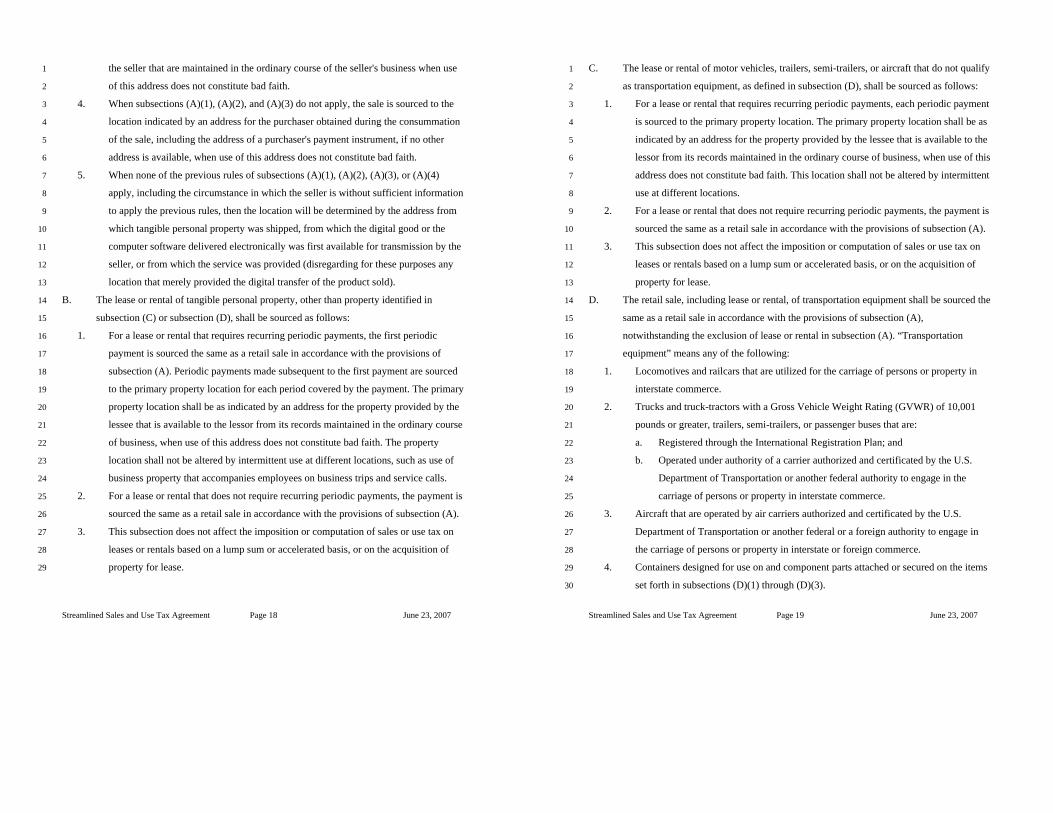

A. The retail sale, excluding lease or rental, of a product shall be sourced as follows: 23

1. When the product is received by the purchaser at a business location of the seller, the 24

sale is sourced to that business location. 25

2. When the product is not received by the purchaser at a business location of the seller, 26

the sale is sourced to the location where receipt by the purchaser (or the purchaser's 27

donee, designated as such by the purchaser) occurs, including the location indicated 28

by instructions for delivery to the purchaser (or donee), known to the seller. 29

3. When subsections (A)(1) and (A)(2) do not apply, the sale is sourced to the location 30

indicated by an address for the purchaser that is available from the business records of 31

Streamlined Sales and Use Tax Agreement Page 18 June 23, 2007

the seller that are maintained in the ordinary course of the seller's business when use 1

of this address does not constitute bad faith. 2

4. When subsections (A)(1), (A)(2), and (A)(3) do not apply, the sale is sourced to the 3

location indicated by an address for the purchaser obtained during the consummation 4

of the sale, including the address of a purchaser's payment instrument, if no other 5

address is available, when use of this address does not constitute bad faith. 6

5. When none of the previous rules of subsections (A)(1), (A)(2), (A)(3), or (A)(4) 7

apply, including the circumstance in which the seller is without sufficient information 8

to apply the previous rules, then the location will be determined by the address from 9

which tangible personal property was shipped, from which the digital good or the 10

computer software delivered electronically was first available for transmission by the 11

seller, or from which the service was provided (disregarding for these purposes any 12

location that merely provided the digital transfer of the product sold). 13

B. The lease or rental of tangible personal property, other than property identified in 14

subsection (C) or subsection (D), shall be sourced as follows: 15

1. For a lease or rental that requires recurring periodic payments, the first periodic 16

payment is sourced the same as a retail sale in accordance with the provisions of 17

subsection (A). Periodic payments made subsequent to the first payment are sourced 18

to the primary property location for each period covered by the payment. The primary 19

property location shall be as indicated by an address for the property provided by the 20

lessee that is available to the lessor from its records maintained in the ordinary course 21

of business, when use of this address does not constitute bad faith. The property 22

location shall not be altered by intermittent use at different locations, such as use of 23

business property that accompanies employees on business trips and service calls. 24

2. For a lease or rental that does not require recurring periodic payments, the payment is 25

sourced the same as a retail sale in accordance with the provisions of subsection (A). 26

3. This subsection does not affect the imposition or computation of sales or use tax on 27

leases or rentals based on a lump sum or accelerated basis, or on the acquisition of 28

property for lease. 29

Streamlined Sales and Use Tax Agreement Page 19 June 23, 2007

C. The lease or rental of motor vehicles, trailers, semi-trailers, or aircraft that do not qualify 1

as transportation equipment, as defined in subsection (D), shall be sourced as follows: 2

1. For a lease or rental that requires recurring periodic payments, each periodic payment 3

is sourced to the primary property location. The primary property location shall be as 4

indicated by an address for the property provided by the lessee that is available to the 5

lessor from its records maintained in the ordinary course of business, when use of this 6

address does not constitute bad faith. This location shall not be altered by intermittent 7

use at different locations. 8

2. For a lease or rental that does not require recurring periodic payments, the payment is 9

sourced the same as a retail sale in accordance with the provisions of subsection (A). 10

3. This subsection does not affect the imposition or computation of sales or use tax on 11

leases or rentals based on a lump sum or accelerated basis, or on the acquisition of 12

property for lease. 13

D. The retail sale, including lease or rental, of transportation equipment shall be sourced the 14

same as a retail sale in accordance with the provisions of subsection (A), 15

notwithstanding the exclusion of lease or rental in subsection (A). “Transportation 16

equipment” means any of the following: 17

1. Locomotives and railcars that are utilized for the carriage of persons or property in 18

interstate commerce. 19

2. Trucks and truck-tractors with a Gross Vehicle Weight Rating (GVWR) of 10,001 20

pounds or greater, trailers, semi-trailers, or passenger buses that are: 21

a. Registered through the International Registration Plan; and 22

b. Operated under authority of a carrier authorized and certificated by the U.S. 23

Department of Transportation or another federal authority to engage in the 24

carriage of persons or property in interstate commerce. 25

3. Aircraft that are operated by air carriers authorized and certificated by the U.S. 26

Department of Transportation or another federal or a foreign authority to engage in 27

the carriage of persons or property in interstate or foreign commerce. 28

4. Containers designed for use on and component parts attached or secured on the items 29

set forth in subsections (D)(1) through (D)(3). 30

Streamlined Sales and Use Tax Agreement Page 20 June 23, 2007

Compiler’s note: The Governing Board issued an interpretation of Section 310C on April 18, 2006. That 1

interpretation can be found in the Library of Interpretations. 2

3

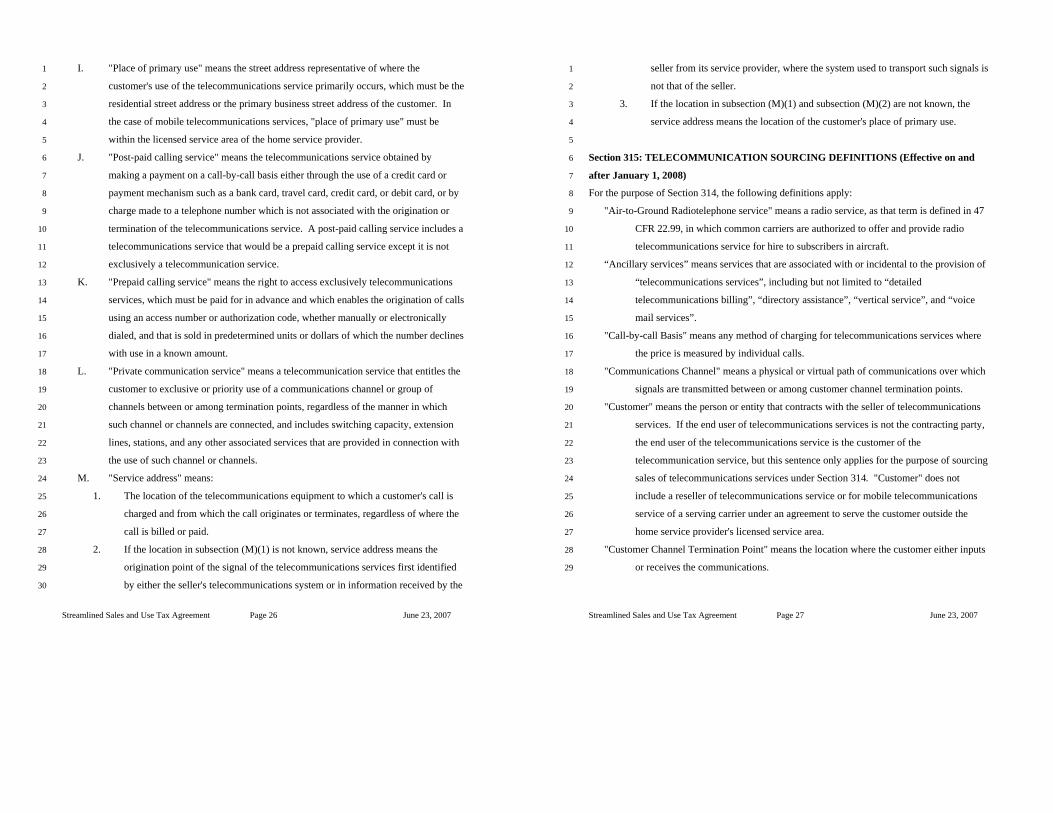

Section 311: GENERAL SOURCING DEFINITIONS 4

For the purposes of Section 310, subsection (A), the terms "receive" and "receipt" mean: 5

A. Taking possession of tangible personal property, 6

B. Making first use of services, or 7

C. Taking possession or making first use of digital goods, whichever comes first. 8