On the Simple Economics of Advertising, Marketing, and...

50

On the Simple Economics of Advertising, Marketing, and Product Design Justin P. Johnson Johnson Graduate School of Management, Cornell University [email protected] David P. Myatt Department of Economics and St. Catherine’s College, Oxford University [email protected] August 2004. 1 Oxford University Economics Discussion Paper 185. We propose a framework for analyzing transformations of the demand facing a mo- nopolist. Our approach is based on the observation that such transformations fre- quently stem from changes in the dispersion of consumers’ valuations, which lead to rotations of the demand curve. In a wide variety of settings, profits are a U-shaped function of dispersion. The monopolist will adopt a mass-market posture when dis- persion is low, and a niche posture when dispersion is high. We investigate numerous applications of our framework, including product design and development; adver- tising, marketing and sales advice; and the construction of quality-differentiated product lines. We also suggest a new taxonomy of advertising, distinguishing be- tween hype, which shifts demand, and real information, which rotates demand. 1. Shaping Consumer Demand The shape of the demand curve for a product is fundamental to the behavior and profitabil- ity of a supplier. Demand is influenced by many factors, some of which are exogenous, such as consumers’ incomes and preferences, and others of which are endogenous. For instance, advertising, marketing, and product design are all activities that shape demand. Here we develop an approach to analyzing the changing demand for a monopolist’s product that is broadly applicable and yet easily understood in terms of basic economic concepts. This approach stems from the observation that demand-shaping activities often change the dis- persion of consumers’ valuations, which leads not to a shift but rather to a rotation of the demand curve. To motivate our study, first consider an alteration to a product’s original design. If consumers unanimously prefer the new version then the consequences are simple: The demand curve shifts outward, so that for any given quantity, revenue must increase. Thus, a monopolist will modify the design unless there are countervailing factors such as an increase in costs. 1 We thank seminar participants, especially Meg Meyer and Paul Klemperer, for helpful comments.

Transcript of On the Simple Economics of Advertising, Marketing, and...

On the Simple Economics ofAdvertising, Marketing, and Product Design

Justin P. Johnson

Johnson Graduate School of Management, Cornell University

David P. Myatt

Department of Economics and St. Catherine’s College, Oxford University

August 2004.1

Oxford University Economics Discussion Paper 185.

We propose a framework for analyzing transformations of the demand facing a mo-nopolist. Our approach is based on the observation that such transformations fre-quently stem from changes in the dispersion of consumers’ valuations, which lead torotations of the demand curve. In a wide variety of settings, profits are a U-shapedfunction of dispersion. The monopolist will adopt a mass-market posture when dis-persion is low, and a niche posture when dispersion is high. We investigate numerousapplications of our framework, including product design and development; adver-tising, marketing and sales advice; and the construction of quality-differentiatedproduct lines. We also suggest a new taxonomy of advertising, distinguishing be-tween hype, which shifts demand, and real information, which rotates demand.

1. Shaping Consumer Demand

The shape of the demand curve for a product is fundamental to the behavior and profitabil-

ity of a supplier. Demand is influenced by many factors, some of which are exogenous, such

as consumers’ incomes and preferences, and others of which are endogenous. For instance,

advertising, marketing, and product design are all activities that shape demand. Here we

develop an approach to analyzing the changing demand for a monopolist’s product that is

broadly applicable and yet easily understood in terms of basic economic concepts. This

approach stems from the observation that demand-shaping activities often change the dis-

persion of consumers’ valuations, which leads not to a shift but rather to a rotation of the

demand curve.

To motivate our study, first consider an alteration to a product’s original design. If consumers

unanimously prefer the new version then the consequences are simple: The demand curve

shifts outward, so that for any given quantity, revenue must increase. Thus, a monopolist

will modify the design unless there are countervailing factors such as an increase in costs.

1We thank seminar participants, especially Meg Meyer and Paul Klemperer, for helpful comments.

2

In other situations, product design is less straightforward. For example, a design change

may appeal to some consumers, while displeasing others. Often this will correspond to a

change in the dispersion of demand (by which we mean an increase in the dispersion of the

distribution of consumers’ willingness-to-pay) rather than a simple shift.

As further motivation, consider advertising and marketing activities. If product promotion

is unambiguously persuasive, or informs consumers of a product’s existence, then it will

shift the demand curve outward. As with product design, however, the effects may be

more complex. This will be so when advertising provides pre-sales information that enables

consumers to better ascertain their true underlying idiosyncratic preferences for the product.

For instance, a marketing campaign may provide many details of a product’s style and

function, or it may simply hype the product’s existence. Providing detailed information may

discourage some customers from purchasing while encouraging others. Thus, the consequence

of providing information is an increase in the dispersion of demand.

Our approach encompasses such situations in which the shape of a demand curve is deter-

mined by the dispersion of consumers’ willingness-to-pay. While this analysis is somewhat

more subtle than that involving mere shifts in demand, the end results nonetheless turn out

to be fairly straightforward. The reason is that an increase in dispersion frequently induces

a clockwise rotation of the demand curve. Therefore, understanding the simple economics of

demand rotation suffices to comprehend the motivations for a monopolist to mold demand

(or to understand responses consequent to an exogenous demand transformation) in a variety

of settings. Thus we consider a family of demand curves indexed by a sequence of clockwise

rotations, and investigate the effect of increased dispersion.

When consumers’ valuations for the product are relatively homogeneous, the demand curve

will be relatively flat. Typically, a monopolist will choose to serve a large fraction of potential

consumers. Heuristically, the marginal consumer is “below average” in the distribution of

valuations. Following an increase in dispersion, the demand curve rotates clockwise. This

will push the willingness-to-pay of the marginal consumer down, and monopoly profits will

fall. Eventually, the steepening demand curve will prompt the monopolist to restrict sales

to a relatively small fraction of potential consumers. The marginal consumer will then be

“above average” and respond positively to increases in dispersion; monopoly profits increase

as the demand curve rotates clockwise. Building upon this intuition we show that, in a

wide variety of circumstances, monopoly profits are “U-shaped” (that is, quasi-convex) in

the dispersion of demand. Such profits achieve a maximum when the dispersion is either

maximized or minimized. Consequently, a monopolist will wish to use any tools at her

disposal, such as her advertising and product-design decisions, to pursue one of these two

extremes. We identify, therefore, two distinct marketing mixes that the monopolist may

wish to deploy.

3

First, the monopolist may stake out a “mass market” position, in which her product is sold

to many consumers. In this case, her goal is to minimize the dispersion of demand. In pursuit

of this goal, the product will be designed to have universal appeal, with controversial design

features being eschewed; it will offer something for everyone. Any advertising will highlight

the existence of the product, but will not allow consumers precisely to learn of their true

match with the product’s characteristics. Such a marketing mix will ensure that consumers

share similar valuations for the product, so that we will see a “plain vanilla” product design

promoted by an advertising campaign consisting of “pure hype.”

Second, the alternative is the adoption of a “niche” position, where few units are sold. The

monopolist aims to maximize the dispersion of demand. The product design will have ex-

treme characteristics that appeal to specialized tastes; it will pander to the highest extreme.

Many consumers will strongly dislike the product, but those who like it will love it. This

product design will be accompanied by advertising and detailed sales advice containing “real

information” that allows consumers to learn of their true match with the product’s attributes.

A number of applications flow from our basic observation that many factors influence the

shape of demand. For instance, building upon the intuition above, we introduce a new tax-

onomy of advertising, distinguising between hype and real information. Promotional hype

corresponds to the traditional notions of informative and persuasive advertising. It high-

lights the existence of the product, promotes any feature that is unambiguously valuable,

or otherwise increases the willingness-to-pay of all consumers; it shifts the demand curve

outward. Real information, on the other hand, allows a consumer to learn of his personal

match with the product’s characteristics; as we show, it rotates the demand curve. Employ-

ing this taxonomy, we study an advertising life-cycle in which a monopolist’s choice of both

the intensity of an advertising campaign and its real-information content change over time

in response to consumer learning. We also examine the decision to introduce an improved

version of an existing product, and relate this to issues such as the existing stock of consumer

knowledge regarding the brand. Furthermore, we are able to ascertain the response of these

decisions to other endogenous variables, such as the product’s design, as well as exogenous

variables, such as inequality in the income distribution.

Our results are not artifacts of an assumption that a monopolist sells but a single product:

We extend our analysis to a multiproduct monopolist offering a product line of vertically

differentiated goods. In this setting a consumer’s type corresponds to a preference for in-

creased quality, and monopoly profits are U-shaped in the dispersion of such types. We

also present a number of comparative statics relating the length and mix of a product line

to consumer-type dispersion. For instance, when types are more disperse a monopolist will

tend to serve a smaller overall share of the market, but do so with more products.

4

Our work is related to several distinct fields of economic inquiry. We believe that fully con-

veying such relationships is best accomplished by deferring thorough review to the individual

subsequent sections. However, a few notes are in order here. In Section 2, we investigate the

response of a single-product monopolist’s profits and output to the dispersion of demand.

Our notion of dispersion builds upon the classic work of Rothschild and Stiglitz (1970, 1971)

and the single-crossing property of distribution functions studied by Diamond and Stiglitz

(1974) and Hammond (1974). In Section 3 we apply our theory to product design and

development. Our approach to product design is based upon Lancastrian (1966, 1971) char-

acteristics, and the analysis of product development is assisted by a result of Jewitt (1987).

In Section 4 we turn to advertising, sales advice and other marketing activities. Our study

of the incentives to equip consumers with private information exploits the insights of Lewis

and Sappington (1991, 1994), and complements Ottaviani and Prat’s (2001) work on public

information supply. Section 5’s consideration of a multiproduct monopolist selling vertically

differentiated goods builds upon the classic Mussa-Rosen (1978) model.

Taken together, a fundamental point emerging from our results is that demand-transforming

events interact with a broad array of decision variables, so that reaching a better understand-

ing of these events is critical to understanding a firm’s overall activities. Equally important

is that studying changes in the dispersion of demand frequently reduces to the study of sim-

ple rotations of demand, so that basic economic intuition is all that is required to explore a

range of issues including advertising, marketing, and product design.

2. Demand Dispersion and a Monopolist’s Preference for Extremes

Our goal here is to provide the core theoretical framework upon which we build in later

sections. We consider a scenario in which a monopolist sells a single product, and investigate

the relationship between the shape of the distribution of consumers’ willingness-to-pay and

the monopolist’s profits, quantity, and price.

2.1. A Single-Product Monopoly Model. A single-product monopolist serves a unit

mass of consumers, each of whom has (at most) unit demand for her product. An individual

consumer’s type θ ∈ R is his valuation, or his willingness-to-pay, for a single unit: Facing a

price of p ≥ 0, he demands a single unit of the product if and only if θ > p. The type θ does

not necessarily represent a consumer’s true payoff (in monetary terms) from consumption:

At the time of purchase, a consumer might well be uncertain of either the product’s precise

attributes, or indeed his own tastes. Our interpretation is that θ represents the certainty

equivalent of the lottery obtained from a purchase. Thus, if a consumer is risk-neutral, then

θ is his expected monetary valuation for a single unit of the product. On the cost side, if

the monopolist supplies z units then she incurs costs of C(z).

5

We consider a family of distributions {Fs(θ)} indexed by s ∈ S = [sL, sH ] ⊆ R. For a

particular s, types are drawn from Fs(θ), with support on some open interval of R. Fs(θ) is

twice continuously differentiable in θ and s, and fs(θ) is its strictly positive density.

Fixing s, Fs(θ) yields a demand curve: At a price of p, z = 1−Fs(p) consumers will purchase,

yielding revenue of p(1−Fs(p)). At times, we will find it convenient to view the monopolist

as setting quantity rather than price. To this end, we write Ps(z) for the type (or willingness-

to-pay) of the consumer with a mass z of others above him. Hence, if the monopolist wishes

to sell z units, then she must set a price of p = Ps(z). Thus Ps(z) is the inverse-demand

curve, and must satisfy z = 1−Fs(Ps(z)), or equivalently Ps(z) = F−1s (1−z). We write π(s)

for the monopolist’s maximized profits given a consumer-valuation distribution Fs(θ). When

uniquely defined (for instance, when marginal revenue is decreasing and costs are convex)

we write z∗s for the monopoly quantity and p∗s for the monopoly price:

π(s) = maxz∈[0,1]

{zPs(z)− C(z)}, z∗s = arg maxz∈[0,1]

{zPs(z)− C(z)}, and p∗s = Ps(z∗s).

2.2. Indexing the Shape of Consumer Demand. Exogenous shifts in the environment,

and actions taken by the monopolist, the consumers, or some third party, may all influence

the distribution Fs(θ) (equivalently, the demand curve) faced by the monopolist, and hence

her profitability. An exploration of this relationship between the nature of demand and

profitability requires a comparison of Fs(θ) and Fr(θ) for r, s ∈ S. If Fs(θ) is higher than

Fr(θ) in the sense of strict first-order stochastic dominance (following classic definitions,

such as that of Lehmann (1955), so that Fs(θ) < Fr(θ) for all θ) then the inverse-demand

curve shifts up from Pr(z) to Ps(z), and the monopolist’s profits must increase. For instance,

if the monopolist benefits from a product innovation that is unambiguously valued by all

consumers, then her profits will rise. Similarly, if advertising (perhaps the promotion of a

product innovation) convinces all consumers of the product’s merits, then profits again will

be higher (putting aside potential changes in the cost structure).

Simple shifts in demand, however, are not our primary focus. We wish to consider the shape

of the demand curve, and in particular situations in which Fs(θ) is “more disperse” or “more

heterogeneous” than Fr(θ).2 For instance, and as discussed in Section 1, a modification

to the product’s design may increase the valuation of some consumers, while reducing the

valuation of others. Similarly, advertising or sales advice may convince some consumers of

the product’s merits, while persuading others that the product does not meet their needs. We

consider concrete examples of these scenarios in Sections 3–4. For our preliminary analysis,

however, we require a measure of “riskiness” to rank different distributions.3

2Our distinction is motivated by Atkinson’s (1970, p. 245) suggestion to “separate shifts in the distributionfrom changes in its shape and confine the term inequality to the latter aspect.”3There is no uncertainty over the demand curve faced by the monopolist; our work is distinct from that ofLeland (1972) and Coes (1977) who considered a risk-averse firm faced by a stochastic demand curve.

6

0 1 2 3 4

Consumer Valuation θ

..............................................................................................................

r

s

........

........

........

........

........

........

........

........

.................

...............

........

........

........

................

....................•

θsr..........•

θsr

............. ............. ............. fr(θ)

................................................................fs(θ)

............. ............. .............................................................................................................................................................................................................................

.........................................................................................................................................................................

.......................... ............. ............. ............. .............

......................................

...............................

...........................................................................................................................................................................

.....................................

.......................................................................................................................................................................................................................................................................................................................................................

(a) Density Functions fr(θ) and fs(θ)

0 1 2 3 4

Consumer Valuation θ

........

........

.......................

...............

..........................................................................................

.

.

.

.

.

.•

θ†sr

............. ............. .............Fr(θ)

................................................................Fs(θ)

............. ............. ............. ............. ..........................

...................................................................................................................................................................................................

............. ............. ............. ............. ............. ............. .............

.................................................................

........................................

...............................

..................................................................................................................................................................................................................................................................................................................................................................................................

...................................

.............................................

................................................

(b) Distribution Functions Fr(θ) and Fs(θ)

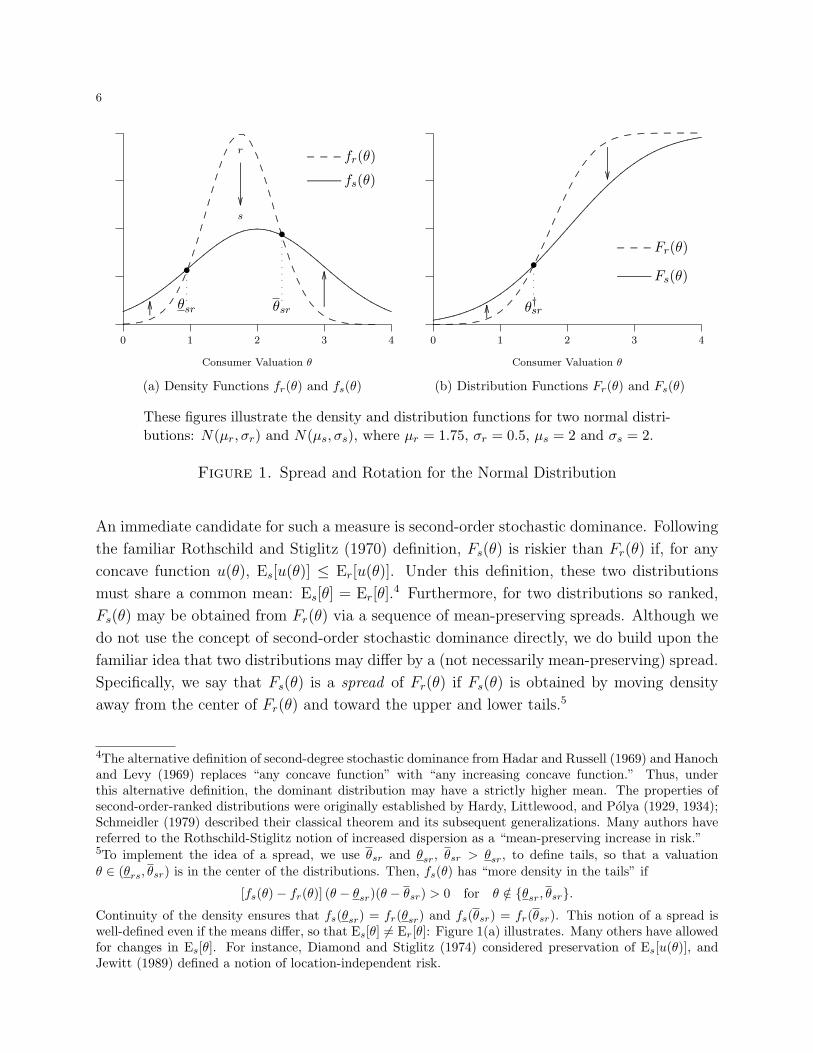

These figures illustrate the density and distribution functions for two normal distri-butions: N(µr, σr) and N(µs, σs), where µr = 1.75, σr = 0.5, µs = 2 and σs = 2.

Figure 1. Spread and Rotation for the Normal Distribution

An immediate candidate for such a measure is second-order stochastic dominance. Following

the familiar Rothschild and Stiglitz (1970) definition, Fs(θ) is riskier than Fr(θ) if, for any

concave function u(θ), Es[u(θ)] ≤ Er[u(θ)]. Under this definition, these two distributions

must share a common mean: Es[θ] = Er[θ].4 Furthermore, for two distributions so ranked,

Fs(θ) may be obtained from Fr(θ) via a sequence of mean-preserving spreads. Although we

do not use the concept of second-order stochastic dominance directly, we do build upon the

familiar idea that two distributions may differ by a (not necessarily mean-preserving) spread.

Specifically, we say that Fs(θ) is a spread of Fr(θ) if Fs(θ) is obtained by moving density

away from the center of Fr(θ) and toward the upper and lower tails.5

4The alternative definition of second-degree stochastic dominance from Hadar and Russell (1969) and Hanochand Levy (1969) replaces “any concave function” with “any increasing concave function.” Thus, underthis alternative definition, the dominant distribution may have a strictly higher mean. The properties ofsecond-order-ranked distributions were originally established by Hardy, Littlewood, and Polya (1929, 1934);Schmeidler (1979) described their classical theorem and its subsequent generalizations. Many authors havereferred to the Rothschild-Stiglitz notion of increased dispersion as a “mean-preserving increase in risk.”5To implement the idea of a spread, we use θsr and θsr, θsr > θsr, to define tails, so that a valuationθ ∈ (θrs, θsr) is in the center of the distributions. Then, fs(θ) has “more density in the tails” if

[fs(θ)− fr(θ)] (θ − θsr)(θ − θsr) > 0 for θ /∈ {θsr, θsr}.Continuity of the density ensures that fs(θsr) = fr(θsr) and fs(θsr) = fr(θsr). This notion of a spread iswell-defined even if the means differ, so that Es[θ] 6= Er[θ]: Figure 1(a) illustrates. Many others have allowedfor changes in Es[θ]. For instance, Diamond and Stiglitz (1974) considered preservation of Es[u(θ)], andJewitt (1989) defined a notion of location-independent risk.

7

When Fs(θ) is a spread of Fr(θ), the two distributions must cross at a single point θ†sr.

This is the center of the spread exercise: For θ < θ†sr, weight is pushed down into the lower

tail, so that Fs(θ) > Fr(θ); for θ > θ†sr, weight is pushed up into the upper tail, so that

Fs(θ) < Fr(θ). We call θ†sr the rotation point of the spread, since the cumulative distribution

function “rotates” around it.6 Figure 1(b) illustrates this effect. We may also consider local

changes in s, which may yield a local spread of the distribution Fs(θ).7 For such a local

spread, there is some rotation point θ†s such that Fs(θ) is increasing in s for θ < θ†s, and

decreasing in s for θ > θ†s. In fact, a rotation is a weaker measure of increased dispersion

than a spread.8 It is central to our analysis, and hence we state it as a formal definition.

Definition 1. Fs(θ) is a rotation of Fr(θ) if, for some rotation point θ†sr,

[Fs(θ)− Fr(θ)] (θ − θ†sr) < 0 for θ 6= θ†sr.

A local change in s leads to a local rotation of Fs(θ) if, for some rotation point θ†s,

∂Fs(θ)

∂s(θ − θ†s) < 0 for θ 6= θ†s.

If this holds for all s ∈ S, then {Fs(θ)}s∈S is ordered by a sequence of local rotations.

Definition 1 stipulates that two cumulative distribution functions, differing by a (clockwise)

rotation, must cross only once. Employing this notion, Diamond and Stiglitz (1974) de-

scribed the difference between distributions as satisfying a single-crossing property, whereas

Hammond (1974) defined the corresponding random variables to be simply intertwined. It is

well known that such a relationship corresponds to an increase in riskiness in the following

sense: If, for some increasing function u(θ), Es[u(θ)] ≤ Er[u(θ)], and v(θ) is more risk-averse

than u(θ) in the sense of Arrow (1970) and Pratt (1964), then Es[v(θ)] < Er[v(θ)].9

6In Section 1 we used the terms “below average” and “above average” to describe a marginal consumer.When comparing Fr(θ) and Fs(θ) the “average consumer” has type θ = θ†sr.7Since s is drawn from the interval S = [sL, sH ], and Fs(θ) is continuously differentiable, local changes in smay be considered. We say that such a change leads to a local spread of Fs(θ) if, for some θs < θs,

∂fs(θ)∂s

(θ − θs)(θ − θs) > 0 for θ /∈ {θs, θs},

where, once again, continuity ensures that ∂fs(θs)/∂s = ∂fs(θs)/∂s = 0.8For a rotation, the distribution functions cross once. Their densities, however, may cross an arbitrarynumber of times. If they differ by a spread, then their densities will cross only twice. Although we restrictour analysis to rotations throughout the paper, our results (particularly Proposition 1) do extend to measuresof increased dispersion that involve multiple rotation points; we return to this issue later in the paper.9Formally, v(θ) is a concave transformation of u(θ) and hence displays a higher coefficient of absolute risk-aversion. Then, if an agent with utility function u(θ) prefers the distribution Fr(θ), then so will the (morerisk-averse) agent with utility function v(θ). This result has been proved independently by a number ofdifferent authors. It was the focus of Hammond’s (1974) paper, appeared as a lemma in Grossman and Hart(1983, p. 151), and formed a basis for the contributions of Jewitt (1987, 1989).

8

Henceforth in this section, we will assume that the family {Fs(θ)}s∈S is ordered by a se-

quence of local rotations.10,11 It follows that the associated family of inverse-demand curves

{Ps(z)}s∈S is also ordered by a sequence of local rotations; for each s there is a rotation

quantity z†s ∈ [0, 1] that satisfies z†s = 1− Fs(θ†s), and

∂Ps(z)

∂s(z − z†s) < 0 for z 6= z†s.

Thus a local increase in s results in a clockwise rotation of the inverse-demand curve around

the quantity-price pair of z = z†s and p = θ†s. This ensures that the inverse-demand curve

becomes steeper, and hence less elastic, when evaluated at the rotation quantity z†s.12

A special case of the local-rotation ordering is obtained when we consider a family of distri-

butions that are indexed by scale and location parameters: An increase in dispersion then

corresponds to an increase in variance. We employ the following definition.13

Definition 2. The family {Fs(θ)}s∈S is ordered by a sequence of mean-variance shifts if,

for some distribution F (θ) with zero mean, unit variance, and density f(θ) > 0,

Fs(θ) = F

(θ − µ(s)

σ(s)

),

where µ(s) and σ(s) are continuously differentiable, σ(s) > 0 and σ′(s) > 0.

10Note that we do not require any two distinct members, Fs(θ) and Fr(θ), to be ordered by a rotation. Ofcourse, if θ†s = θ† for all s, then any pair of distributions Fr(θ) and Fs(θ) do differ by a rotation. Furthermore,even if θ†s is not constant, we may rank Fr(θ) and Fs(θ) in their upper and lower tails. Formally, if r < s,

θ < infs′∈[r,s]

θ†s′ ⇒ Fr(θ) < Fs(θ), and θ > sups′∈[r,s]

θ†s′ ⇒ Fr(θ) > Fs(θ).

Definition 1 insists that Fr(θ) and Fs(θ) cross at some point θ†sr. We could, of course, weaken this bypermitting pairs of distributions that do not cross, and hence are ordered by first-order stochastic dominance;this would be accomplished by allowing θ†sr to take values outside the support of θ. Hammond (1974) allowedfor distributions that are either simply intertwined (this differs slightly from our definition, by allowing fordistributions that coincide on some interval) or first-order-dominance ranked. When one of these orderingsholds, the distributions are “simply related.” Hammond (1974, p. 1069) observed that many families ofdistributions have members that are all simply related, including the (separate) families of uniform, normal,geometric, exponential, gamma and beta distributions.11When all distributions in the family share a common mean, a local-rotation ordering is sufficient to ensurethat any distinct pair of distributions are ordered by second-order stochastic dominance. A partial converseis also true. For instance, suppose that, for a finite set S, distributions are ordered by second-order stochasticdominance. Following Rothschild and Stiglitz (1970) and Machina and Pratt (1997), we may construct asequence of mean-preserving spreads (and hence rotations) linking each pair. In such a manner, we mayobtain an (expanded) family of distributions ordered by a sequence of local rotations.12If we were to specify a family of demand curves index by decreasing elasticity, then we would need tospecify whether the elasticities of two curves are to be compared at a common quantity, or a common price.Whatever the convention adopted, if Ps(z) to be less elastic than Pr(z) then it must be steeper wheneverthe demand curves cross. This further implies that they must cross only once. Thus an elasticity-orderedfamily of demand curves must be ordered by a sequence of local rotations.13If a family is ordered by a sequence of local rotations, then the distributions of any increasing transformationof θ are so ordered. Hence Definition 2 could be weakened, while retaining many of our results, by allowingfor distributions corresponding to an increasing transformation of θ to satisfy the definition.

9

0.00 0.25 0.50 0.75 1.00

Quantity z

........

........

........

........

........

...................

...............

..........................................................

............. ............. ............. ............. ............. ............. ............. ............. ............. ............. ............. ............. ............. ............. ............. ............. ............. s = 14

..................................................................................................................................................................................................................................................................................................................................................................................................................................................................................... s = 2

(a) Rotating Inverse-Demand Ps(z)

0 1 2 3 4

Standard Deviation of Valuations s

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

•

s

z∗s > z†s

π′(s) < 0

(Mass Market)

z∗s < z†s

π′(s) > 0

(Niche)

z†s

z∗s

............. ............. ............. ............. ............. ............. ............. ............. ............. ............. ............. ............. ............. ............. ............. ............. ............. ............. .....

..................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................

(b) z∗s versus z†s

These figures illustrate the rotation of the inverse-demand function Ps(z) and therelative size of the monopoly quantity z∗s and rotation quantile 1− z†s. The specifi-cation is θ ∼ N(µ(s), s2), where µ(s) = 2.45 + 0.05s2.

Figure 2. Inverse-Demand Rotation and Niche versus Mass-Market

Thus Fs(θ) has a mean of µ(s), a standard deviation of σ(s), and inverse-demand

Ps(z) = µ(s) + σ(s)P (z),

where P (z) = F−1(1 − z). Insisting that σ′(s) > 0 ensures that the family is ordered by a

sequence of local rotations.14 Since σ′(s) > 0 is required, it is without loss of generality to

set σ(s) = s when convenient, yielding the inverse-demand function Ps(z) = µ(s) + sP (z).

Many specifications meet the requirements of Definition 2. For instance, a family of normal

distributions (from which the illustrations of Figure 1 are taken) does so.

2.3. Quasi-Convexity of Profits and a Preference for Extremes. We turn now to

consider the response of the monopolist’s profits to changes in the dispersion index s. We have

noted that, from a quantity-setting perspective, her inverse-demand curve rotates clockwise

around z†s following a local increase in s.15 If the monopolist supplies z units then, for z < z†s,

the price received is increasing in s. For z > z†s, it is decreasing in s.

A straightforward intuition is that, for z∗s > z†s, the monopolist acts as a “mass market”

supplier. By supplying more than z†s, she ensures that the marginal consumer, with type

θ = p∗s = Ps(z∗s), lies below the rotation point θ†s. An increase in s pushes consumers away

14It is straightforward to show that the rotation point satisfies θ†s = µ(s)− σ(s)µ′(s)/σ′(s). When σ(s) = sthis simplifies to θ†s = µ(s)− sµ′(s), and the rotation quantity satisfies z†s = 1− F (−µ′(s)).15The term “demand rotation” was used by Aislabie and Tisdell (1988), who related the slope to marketingdecisions. They referred to flat and steep demand curves as “bandwagon-type” and “snob-type” respectively.

10

from θ†s. Hence, it pushes the type (and willingness-to-pay) of the marginal consumer down.

Since the price is determined by the identity of the marginal consumer, and not the average

consumer, both the price and profits fall. In contrast, when z∗s < z†s, the monopolist acts

as a “niche” operator, by restricting supply to a smaller fraction of the potential consumer

base. The same logic ensures that profits increase with s. Employing the envelope theorem,

∂π(s)

∂s(z∗s − z†s) < 0 for z∗s 6= z†s.

This does not suffice to characterize the effect of increases in s across the entire interval S,

since the sign of (z∗s − z†s) might well change a number of times. There is, however, a simple

sufficient condition that ensures that the sign changes at most once.16

Proposition 1. Suppose that the family of distributions {Fs(θ)}s∈S is ordered by a sequence

of local rotations. Further suppose that the rotation point θ†s is decreasing in s, or equivalently

that the rotation quantity z†s is increasing in s. Then π(s) is a quasi-convex function of s.

maxs∈S π(s) ∈ {π(sL), π(sH)}, and hence the monopolist prefers the extremes sL and sH .

Quasi-convex profits are highest when consumers’ valuations are either as heterogeneous

as possible, or as homogeneous as possible. If the monopolist were able to choose s, then

she would take either an extreme niche posture (by setting s = sH) or an extreme mass-

market posture (the opposite extreme of s = sL). Furthermore, as either sL or sH increase,

π(sH)− π(sL) crosses from negative to positive at most once.

Proposition 1 follows from the observation that, as s rises, the monopolist will never switch

from a niche position to a mass-market position. If she were to do so, then we could find

an interval [s′, s′′] ⊆ S such that z∗s′ < z†s′ ≤ z†s′′ < z∗s′′ . As s rises from s′ to s′′, the rotation

quantity z†s increases, and hence ∂Ps(z∗s′)/∂s > 0 throughout. Similarly, ∂Ps(z

∗s′′)/∂s < 0

over the same interval. But this implies that, for s = s′′, a supply of z∗s′ is strictly more

profitable than a supply of z∗s′′ . This is a contradiction. It follows that the monotonicity

of z†s is sufficient (but not necessary) to guarantee that once s is sufficiently large to make

a niche operation optimal, the monopolist will never wish to switch back to mass-market

supply. This ensures that π′(s) remains positive for all larger s, and π(s) is a quasi-convex

(hence either monotonic or “U-shaped”) function.17

Monotonicity of z†s (equivalently, θ†s) is straighforward to check. If z < z†s, then ∂Ps(z)/∂s >

0, so that the price is locally increasing in s. Since z†s is increasing, the same is true for

16Proofs omitted from the text are contained in Appendix A.17Figure 2 illustrates this result, where Fs(θ) is drawn from a family of normal distributions. Consider ans such that z∗s − z†s = 0. As s increases, the clockwise rotation steepens the demand curve, and hencereduces the elasticity. This reduction in elasticity implies that the monopoly quantity z∗s moves down. Byassumption, z†s is increasing. It follows that z∗s − z†s must cross zero at most once, and from above. Thiscrossing (if it occurs) is the single transition from mass-market to niche supply.

11

larger s. Thus, fixing z, ∂Ps(z)/∂s > 0 crosses zero at most once, and this must be an

upcrossing. Equivalently, the price Ps(z) is, for fixed z, a quasi-convex function of the

dispersion parameter s. This observation forms part of the following lemma.

Lemma 1. When the family {Fs(θs)}s∈S is ordered by a sequence of local rotations,

(1) θ†s is a decreasing function of s,

(2) z†s is an increasing function of s,

(3) Fs(θ) is a quasi-concave function of s for all θ, and

(4) Ps(z) is a quasi-convex function of s for all z,

are all equivalent statements. Further, if the family is ordered by a sequence of mean-variance

shifts, then (i)–(iv) hold if and only if µ′(s)/σ′(s) is weakly increasing in s.

For a family of distributions ordered by a sequence of mean-variance shifts (Definition 2) the

requirement that µ′(s)/σ′(s) be weakly increasing is equivalent to the inequality µ′′(s)σ′(s) ≥µ′(s)σ′′(s).18 Of course, in the mean-variance shift case, we may set σ(s) = s without loss,

and reduce the final statement of Lemma 1 to µ′′(s) ≥ 0: As we move through the variance-

ordered family of distributions, the mean is a convex function of the standard deviation.

As we show subsequently, the conditions of Lemma 1 are satisfied for many applications.

Furthermore, an alternative proof of Proposition 1 follows from the observations that (i)

Lemma 1 applies, so that Ps(z) is quasi-convex in s, and (ii) π(s) = maxz∈[0,1]{zPs(z)−C(z)}is the maximum of quasi-convex functions, and so is itself quasi-convex.19

2.4. Niche versus Mass-Market Operation. In the previous section we categorized a

monopolist’s posture as either being a niche or a mass-market one, depending on whether

she is serving fewer or more than z†s consumers, respectively. Here we continue to make use

of this distinction, and show how it is useful in categorizing the change in the monopolist’s

optimal output z∗s in response to shifts in s.

Detailed comparative statics require more structure than that possessed by an arbitrary

family of demand curves ordered by local rotations. The reason is that such comparative

statics depend on properties of marginal revenue, and the rotation ordering is broad enough

18If µ(s) is increasing, then this inequality is equivalent to −µ′′(s)/µ′(s) ≤ −σ′′(s)/σ′(s), which says thatµ(s) is less concave than σ(s), in the Arrow (1970) and Pratt (1964) sense.19Notice that this proof applies even when the family of distributions is not ordered by a sequence of localrotations. As suggested in Footnote 8, Lemma 1 and Proposition 1 may be modified to cope with moregenerality. Exploring this, notice that for a family ordered by a sequence of local rotations, θ†s the is onlyvaluation at which demand is stationary (to first order) in response to a local change in s. More generally,there may be many such points. We can subdivide such rotation points into an ordered, alternating, sequenceof two types: Clockwise rotation points (the inverse-demand curve steepens with s), and anti-clockwiserotation points (inverse-demand becomes shallower with s). For quasi-convexity of profits, we require anyclockwise rotation to be decreasing, and any anti-clockwise rotation point to be increasing.

12

to impose few restrictions on the dependence of marginal revenue on s. Therefore, we

specialize to the case of mean-variance shifts (Definition 2), taking σ(s) = s and µ′′(s) ≥ 0

so that Proposition 1 holds. We also assume that C(z) is convex and differentiable, and that

Ps(z) exhibits decreasing marginal revenue. Note that, since Ps(z) = µ(s)+ sP (z), marginal

revenue is given by

MRs(z) = Ps(z) + zP ′s(z) = µ(s) + s [P (z) + zP ′(z)] = µ(s) + sMR(z),

where MR(z) is the marginal revenue associated with the inverse-demand curve P (z). Thus,

Ps(z) exhibits decreasing marginal revenue exactly when MR(z) is decreasing, i.e., whenever

the foundational inverse-demand curve P (z) exhibits decreasing marginal revenue.

This common assumption of decreasing marginal revenue MR(z) turns out to have powerful

consequences in this setting. It ensures that increases in s correspond to clockwise rotations

not only of the inverse-demand curve Ps(z), but also of the marginal revenue curve MRs(z).

This in turn generates a number of other results, summarized in the following proposition.

Proposition 2. Suppose that the family of distributions is ordered by a sequence of mean-

variance shifts, so that Fs(θ) = F ((θ − µ(s))/s), that µ(s) is convex, and that P (z) =

F−1(1−z) exhibits decreasing marginal revenue. Then π(s) is convex in s, and the monopoly

supply z∗s is quasi-convex in s. Furthermore, marginal revenue satisfies:

(1) A local increase in s rotates marginal revenue clockwise around some z‡s ∈ [0, 1],

(2) for each z, marginal revenue is convex in s,

(3) z‡s is increasing in s and satisfies z‡s < z†s, and

(4) the rotation point of marginal revenue MR‡s = MRs(z

‡s) is weakly decreasing in s.

Turning back to the monopoly supply z∗s , and for a constant marginal cost c,

(5) if c > MR‡sL

then z∗s is increasing for all s,

(6) if c < MR‡sH

then z∗s is decreasing for all s,

(7) otherwise z∗s is non-monotonic, and minimized for interior s ∈ (sL, sH). Finally,

(8) if µ(s) = µ for all s, then z∗s is increasing for µ > c, and decreasing for µ < c.

Because marginal revenue rotates (clockwise) around some rotation quantity z‡s as s increases,

comparative statics on the monopoly output depend on whether MR‡s = MRs(z

‡s) is above

or below marginal cost.20 Since z‡s < z†s, this is in turn connected to whether the monopolist

is adopting a niche or a mass-market posture. This is easiest to see when there is a constant

marginal cost, and so we suppose for discussion purposes that C(z) = cz.

20Proposition 2 allows marginal revenue to “rotate” around z‡s = 0 or z‡s = 1. For instance, z‡s = 0corresponds to a case in which marginal revenue falls for all z > 0 in response to a local increase in s.

13

Category Marginal Cost Output ∂π(s)/∂s ∂z∗s/∂s

Expanding Niche c > MR‡s > MR†

s z∗s < z‡s < z†s positive positive

Contracting Niche MR‡s > c > MR†

s z‡s < z∗s < z†s positive negative

Contracting Mass Market MR‡s > MR†

s > c z‡s < z†s < z∗s negative negative

Table 1. Categories of Monopoly Response to a Local Increase in s

Precisely, if c > MR‡s, then the intersection of marginal cost and marginal revenue must

occur below z‡s, and so monopoly output must satisfy z∗s < z‡s < z†s. With a local increase

in s, marginal revenue rotates clockwise around z‡s, and hence, given z∗ < z‡s, we know that

∂MRs(z∗s)/∂s > 0. This implies that z∗s is locally increasing in s. Of course, z∗s < z†s, so that

∂Ps(z∗s)/∂s > 0. We conclude that profit and output both increase with s, corresponding to

an expanding niche market. If c < MR†s, then similar reasoning ensures that the monopolist’s

profit-maximizing output must satisfy z∗ > z†s > z‡s: An increase in s leads to a contracting

mass-market. Finally, when MR‡s > c > MR†

s, profits rise while output falls: A contracting

niche market. Table 1 provides a summary of these responses to s.

2.5. Illustration. Here we use a family of uniform distributions to illustrate our results.

Example 1. Valuations are uniform on an interval of width 2s, centered at µ > 0, so that

θ ∼ U [µ− s, µ+ s]. The monopolist faces a constant marginal cost of c > 0.

Example 1 generates a simple linear demand curve: Ps(z) = µ + s(1 − 2z). As s increases,

this demand curve rotates around the constant rotation point characterized by θ† = µ and

z† = 12, so that Proposition 1 applies. Furthermore, increases in dispersion are both mean

and median preserving. We also observe that profits z(Ps(z) − c) are linear in s. Thus

π(s) = maxz∈[0,1] z(Ps(z) − c) is the maximum of convex functions and is itself convex; a

stronger conclusion than that of Proposition 1.

To explore this example, we consider two separate cases. First, suppose that µ < c. Since

the mean valuation is below the marginal cost, for sufficiently small s no consumer valuation

is above c, and hence the monopolist is unable to operate profitably: z∗s = 0. For larger s,

supply becomes profitable, and the monopolist sets z∗s > 0. The marginal valuation must

satisfy Ps(z∗) > c > µ = Ps(z

†), and hence the monopolist always restricts supply to a

minority of the customer base; she is always a niche operator, and hence profits always

increase with s.

Second, suppose that µ > c. So long as z is sufficiently small, supply is always profitable,

so that z∗s > 0 for all s. When s is sufficiently small, the monopolist finds it optimal to

14

0.0 0.2 0.4 0.6 0.8 1.0

Quantity z

0.00

0.25

0.50

0.75

1.00

1.25

Pri

cep

=P

s(z

)

........

........

........

........

........

........

........

.......................

...............

..............................................................................................

.....................................................................................................................................................................................................................................................................................................................................................................................................................................................

.................................................................................. s = 0.75

..........................

..........................

..........................

..........................

..........................

..........................

..........................

..........................

..........................

..........................

..........................

.............

............. ............. ............. ....... s = 0.25

•. . . . . . . . . . . . . . . . . . . . . . . . . θ† = µ

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.z† = 1

2

(a) Inverse-Demand Curves

0.0 0.2 0.4 0.6 0.8 1.0

Dispersion s

0.0

0.2

0.4

0.6

0.8

1.0

Monopoly

Quantitiyz∗ s

..................................................................................

............. ............. ............. .......

c = 0.25

c = 0.75

............................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................

..........................

..........................

............. ............. ............. ............. ............. ............. ............. ............. .............

(b) Monopoly Supply

0.0 0.2 0.4 0.6 0.8 1.0

Dispersion s

0.00

0.05

0.10

0.15

0.20

0.25

Pro

fitsπ(s

)

............. ............. ............. ............. ............. ............. ..........................

..........................

..........................

.............

........................................................................................................................................................................................................................................................................................................................................

...............................................................

..........................................................

.......................................................

......................................................

.......................................

•

..................................................................................

............. ............. ............. .......

c = 0.25

c = 0.75

(c) U-Shaped Monopoly Profits (µ = 0.5)

0.0 0.2 0.4 0.6 0.8 1.0

Lower Bound sL

0.0

0.5

1.0

1.5

2.0

2.5

Upper−

Low

erB

ounds H

−s L

..................................................................................

............. ............. ............. .......

. . . . . . .

µ− c = 0.75

µ− c = 0.5

µ− c = 0.25................. .

.....................................................................................................................

..........................

..........................

............. .............

.........................................................................................................................................................................................................................................................................................................................................................................................................................................

(d) Mass Market versus Niche

These figures illustrate the specification of Example 1, and the results of Proposi-tions 3. Figure 3(a) illustrates inverse-demand curves for µ = 1

2 , and the clockwiserotation as s increases. Fixing µ = 1

2 , we plot the monopoly quantities z∗s and profitsπ(s) in Figures 3(b) and 3(c). Finally, Figure 3(d) illustrates the regions for which amonopolist prefers extreme dispersion (niche operation) versus minimum dispersion(mass market supply). For instance, any values of sL and sH above and to the rightof the solid line indicate π(sH) > π(sL) when µ− c = 0.75.

Figure 3. Illustrations for Example 1 and Proposition 3

15

set z∗s = 1, and serve the entire customer base. For larger s, however, the monopolist

switches from mass-market supply to become a niche operator. A fuller characterization of

the monopolist’s behavior and profitability is given by the following proposition.

Proposition 3. For Example 1, π(s) is convex and minimized by s = max{µ− c, 0}. Also,

(1) if 0 ≤ s ≤ c− µ then z∗s = 0, whereas if 0 ≤ 3s ≤ µ− c, then z∗ = 1. Otherwise,

(2) the monopolist sets z∗s = (s+ µ− c)/4s, and obtains profits π(s) = (s+ µ− c)2/8s.

(3) If sL ≥ µ− c then π(sH) ≥ π(sL) and if sH ≤ µ− c then π(sL) ≥ π(sH). Otherwise,

(4) π(sH) ≥ π(sL) if and only if sH ≥ 4π(sL) − (µ − c) +√

16π(sL)2 − 8π(sL)(µ− c),

and where the critical value for sH is decreasing in sL.

Observe that, so long as sL ≤ µ − c ≤ sH , profits are a U-shaped function of s. Of course,

π(sH) − π(sL) may be either positive or negative, although this expression is increasing in

both sH and sL. By finding pairs of upper and lower bounds to s such that π(sH) = π(sL),

we may illustrate the parameter regions in which the monopolist prefers to be a mass-market

supplier or a niche operator. For Example 1, such values are easy to calculate, and Figure 3(d)

illustrates. For each selection of µ− c, any combination of sL and sH − sL to the right and

above the line indicates the monopolist’s desire to occupy a niche position.

Before concluding our analysis of Example 1, we remove the restriction that changes in s

are mean-preserving. Allowing for general µ(s) ensures that the rotation point θ†s will move

with s. So long as µ(s) is convex, profits remain convex in s (following Proposition 2).

Furthermore, if µ(s) is linear (and hence weakly concave) π(s) remains convex. Thus, to

overturn the convexity of profits, µ(s) must be strictly concave in some regions.21

3. Product Design and Development

In Section 2, we indexed a family of valuation distributions by riskiness. Under Proposition 1

or 2, the monopolist prefers the family’s extremes. Here we describe product development

and design decisions that yield such risk-indexed families, thereby providing a microfoun-

dation for our earlier analysis. We refer to product development as the process of adding

new features to a product. In contrast, a product’s design is viewed as a bundle of different

characteristics, valuations for which may be correlated. In both scenarios, the monopolist’s

profits are maximized by choosing extreme values of design and development controls. We

also consider the impact of an exogenous change in the shape of consumer demand on the

21Suppose that µ(s) is twice continuously differentiable, and that π(s) achieves a profitable (π(s) > 0) localmaximum for some interior s ∈ (sL, sH). Straightforward algebra reveals that µ′′(s) ≤ −(s+ µ(s))/4s2 < 0.Thus µ(s) must be sufficiently concave for interior maxima to arise; quasi-convexity of the inverse-demandfunction Ps(z), and the associated monotonicity of z†s and θ†s are not necessary for the monopolist to preferthe extremes of [sL, sH ]. Equivalently, profits may be quasi-convex even if θ†s grows with s.

16

monopolist’s choices. Specifically, we investigate how an increase in the inequality of income

might prompt her to switch her design and development decisions.

3.1. Product Development. A monopolist with a basic product design is deciding which

additional features to incorporate. For instance, she may be deciding on the number of

features present in a personal digital assistant (PDA). It may be that new features are,

on average, beneficial in the sense that they increase the average willingness-to-pay of con-

sumers. However, different consumers disagree on how valuable any given feature is, and so

adding more features increases the dispersion of demand. For example, adding telephony

capabilities may appeal less to those who already have mobile phones, or similarly adding

more applications may benefit some while annoying others who find that they muddle the

interface. Intuitively, the monopolist may face a tradeoff, as adding new features in a sense

may both shift the demand curve outwards, yet also rotate it. Of course, given our previous

work, it is not surprising that the firm may desire either increased or reduced dispersion, so

that even if new features detract on average from consumers’ willingness-to-pay, they may

still optimally be incorporated if increased dispersion is preferred.22

To investigate further, we suppose that the monopolist begins with a basic product design.

A consumer’s valuation θ0 for it is drawn from F0(θ0). For simplicity, we assume that this

distribution has a strictly positive density f0(θ0) on the real line.23 If the monopolist chooses

to retain the basic design, then a consumer’s willingness-to-pay satisfies θ = θ0, and hence is

drawn from F0(θ). Next, we allow the monopolist to develop her product via a cumulative

sequence of design innovations. In a discrete setting, there are n steps in this process. A

consumer’s valuation for the ith innovation is εi, drawn from Gi(εi) with density gi(εi) on

R. If the monopolist follows the development process up to the ith step, then a consumer’s

willingness-to-pay satisfies θ = θ0+∑

j≤i εj, with distribution Fi(θ). For many specifications,

the sequence {Fi(θi)}i∈{1,...,n} will be ordered by some notion of riskiness.24

22For instance, BMW’s installation of the “iDrive” system in its 5-series and 7-series automobiles has gen-erated some controversy in the press. In an early review, Hutton (2001) described it as “a computer-agecontrol system which eliminates the forest of buttons on the dashboard and replaces them with menus on ascreen, accessed by a control knob on the centre console.” Such a system does not appeal to everyone; manyreviewers described the system as confusing for the typical user. Referring to such reviewers, Wilkinson(2002) commented that “everybody . . . praised the car but used the occasion to take potshots at . . . theiDrive system.” Nevertheless, some drivers will appreciate its merits. Wilkinson (2002) went on to quote aBMW engineer’s claim that “West Coast early adopters love the iDrive from the beginning, while the EastCoast Luddites are much more conservative.” Putting his stereotypes aside, his claim was that some lovethe iDrive system, while others hate it; an increase in the dispersion of valuations.23We could restrict support to some open interval of R, at the cost of introducing additional notation.24Product development will not necessarily increase the riskiness of consumer valuations. For instance, ifε1 = µ − θ0, then for i = 1, F1(θ) will be a degenerate distribution with all mass at θ = µ. For thisspecification, the first step in the development process offsets all risk in the initial distribution F0(θ).

17

To illustrate this, we suppose that consumer valuations for the basic design and innovation

steps are all independent, so that var[θi] = var[θ0] +∑

j≤i var[εj], and an increase in i raises

the variance of consumer valuations. Our criterion for increased riskiness, however, is a

rotation (Definition 1), and we require further conditions on F0(θ0) and {Gi(εi)} to allow its

use. Thankfully, adding an independent innovation to a distribution results in a rotation so

long as both underlying distributions are strongly unimodal (see, e.g., Jewitt 1987), where a

variable is strongly unimodal if its density is log-concave.25 Such strong unimodality ensures

that rotations may be used to index riskiness, but does not imply that the monopolist should

take an “all or nothing” approach to product development. To move further, we turn to a

specific example. We begin by specifying a function µ(s) : [0, 1] 7→ R, and assume that

θ0 ∼ N(µ(0), σ2). µ(0) represents the mean consumer valuation given that no product

development takes place. Next, we suppose that εi ∼ N(∆µi, κ2/n), where

∆µi = µ

(i

n

)− µ

(i− 1

n

).

Thus each development step yields a normally distributed innovation to consumer valuations.

The density of the normal is log concave, and hence i indexes a sequence of rotations.

Furthermore, for a specified i, θ ∼ N(µ(s), σ2 + sκ2) where s = i/n. Finally, we consider the

properties of µ(s). We have assumed that each of the innovative steps are homoskedastic,

with variance κ2/n. Given this, we would expect the monopolist to adopt the most-valuable

development-changes first, so that ∆µi ≥ ∆µi+1.26 This amounts to a concavity restriction

on µ(s). Gathering these elements, and allowing n→∞, yields the following specification.

Example 2. For s ∈ [0, 1], valuations satisfy θ ∼ N(µ(s), σ2 + sκ2), where µ(s) is concave.

Applying Lemma 1 and Proposition 1, conditions under which profits are quasi-convex readily

emerge. First, note that by assumption, µ(s) is concave. If the standard deviation of θ were

equal to s, then we would require convexity of µ(s) to apply our results (Proposition 2). Here,

however, the standard deviation of θ is σ(s) =√σ2 + sκ2, which is concave in s. Hence, if

µ(s) is (for instance) linear in s, then the mean will be a convex function of the standard

deviation. More generally, profits are quasi-convex so long as µ(s) is “not too concave” in s.

Proposition 4. Assume the specification of Example 2. If µ′′(s) ≥ −µ′(s)/2[(σ2/κ2) + s]

then monopoly profits are quasi-convex function in s, and maximized for some s ∈ {0, 1}.

25Log-concave densities include the normal, uniform, exponential, and members of the beta and gammafamilies. See Jewitt (1987, p. 80) and Barndorff-Nielsen (1978, pp. 93–97) for more details. In the terminologyof Karlin and Proschan (1960), a strongly unimodal distribution has a Polya frequency density of order 2.In fact, the stated result follows from work in that paper and other contributions of Karlin (1957, 1968).26Note that we do not require the product development steps to increase the expected valuation. Hence thisassumption might amount to the introduction of the least-damaging development-changes first.

18

Intuitively, the reason quasi-convexity may fail when this condition does not hold is as

follows. Suppose that profits were increasing in some range, but then the above inequality

failed. Since profits were increasing, the monopolist must have been pricing to a consumer

above the rotation point. As the inequality fails, it may be that the rotation point of demand

moves upwards so that, heuristically, the marginal consumer no longer prefers additional

features. This causes profits to fall in a region, destroying quasi-convexity.

On the other hand, this condition is sufficient, not necessary, for quasi-convexity. For in-

stance, suppose that µ′(s) < 0 and µ′′(s) < 0. Then the condition above cannot hold.

Moreover, on average consumers disdain new features. Nonetheless, profits can easily be

quasi-convex. For instance, they may be monotonic when the monopolist takes an extreme

niche posture. New features lower the average willingness-to-pay, shifting the demand curve

in. However, these features also rotate the demand curve. Since the marginal consumer is

(potentially) well above the rotation point, profits increase as new features are added.

We have considered a monopolist who is able to add features to her product. When valuations

for features are independent, new features increase the riskiness of the valuation distribution,

and may also change the mean. Our analysis identifies the tradeoffs faced when deciding

whether to incorporate additional features to an existing product. In a mass-market, a

hesitant monopolist retains her original design; in a niche market, she is eager to innovate.

We now turn to a different situation, in which she chooses the mix of features in her product.

3.2. Product Design. As a second application of our results, we consider a problem of

product design faced by a monopolist who must assemble her product from a convex function

of different characteristics.27 Thus, in contrast to our analysis above, where the firm decided

whether to add new features or not, the firm must choose the mix of some set of features.

For instance, we might imagine that the monopolist operates a restaurant, and is deciding

upon the exact combination of different ingredients that go into a meal.28 Thus we are

taking Lancaster’s (1971) “characteristics” approach, in which (Lancaster 1975, p. 567) the

consumer “is assumed to derive . . . satisfaction from characteristics which cannot in general

27Thus the final product is a bundle of these different characteristics. It follows that our analysis is closelyrelated to the contributions of Stigler (1968), Adams and Yellen (1976), Schmalensee (1982, 1984), andMcAfee, McMillian, and Whinston (1989). These authors analyzed the incentive of a multiproduct monop-olist to sell goods separately, or to employ pure or mixed bundles. The difference here is increasing thecontribution of one characteristic to the mix entails the reduction of another. Nevertheless, our results justbelow illustrate how combinations of negatively correlated characteristics may be used to reduce the risk inthe distribution of consumer valuations, as in Figure I of McAfee et al (1989).28This is an example of Lancaster (1966, p. 133) who noted that “[a] meal (treated as a single good)possesses nutritional characteristics but it also possesses aesthetic characteristics, and different meals willpossess these characteristics in different relative proportions.” There other situations in which a product isliterally a convex combination of different characteristics. For instance, Andrea Prat suggested to us theexample of a radio station that must choose how to divide its airtime between different genres of music.

19

be purchased directly, but are incorporated in goods.” Other examples include automobiles

and computers, which may be blends of performance, practicality, size, and weight.

We impose two simplifications. First, the expected valuation for the final product is invariant

to the exact combination of characteristics. Thus, in contrast to our discussion of product

development, the average value of the product is constant for any design, where the average

is taken across all potential customers. Second, we again adopt the normal distribution.

Example 3. The monopolist’s product consists of n weighted characteristics, indexed by i,

with typical weight αi ∈ [0, 1] where∑n

i=1 αi = 1. A consumer’s valuation for the product

satisfies θ = µ+∑n

i=1 αiηi, where η is an n×1 multivariate normal η ∼ N(0,Σ) and |Σ| > 0.

Consumer valuations for the product are normally distributed, and satisfy

θ ∼ N(µ, s2) where s2 = α′Σα =n∑i=1

α2iσ

2i + 2

∑i<j

αiαjρijσiσj,

where σ2i is the variance of characteristic i, and ρij is the correlation coefficient between ηi

and ηj. From Section 2, the inverse demand curve is given by Ps(z) = µ + sP (z), where

P (z) = Φ−1(1 − z); from the monopolist’s viewpoint the characteristics mix matters only

insofar as it influences the variance s2 of consumer valuations. Increases in s correspond

to rotations of demand and, since µ being constant implies that the rotation point is fixed,

Proposition 1 applies: A monopolist chooses to either minimize or maximize s.

To understand the implications for the characteristics mix, observe that s2 is convex in

the weights {αi}. To maximize s, the monopolist will wish to place all weight on the

characteristic with the highest variance: She will “pander to the highest extreme.” Many

consumers will strongly dislike this product, but those who like it will love it; the demand

curve is very steep for high values of s. In contrast, to minimize s, the monopolist will often

choose an interior solution (i.e., αi ∈ (0, 1) for each i) that offers “something for everyone.”

This product will not arouse strong disagreement, so that the distribution of willingness-to-

pay is clumped around the mean µ; the demand curve is shallow for small values of s.

Proposition 5. For Example 3, a monopolist will wish to either (i) set αi = 1 where

σ2i ∈ maxj{σ2

j}, or (ii) choose the unique vector of convex weights α∗ to minimize α′Σα.

While there is neither uncertainty nor risk aversion here, an analogy to optimal portfolio

selection exists. The design of a product bundle with something for everyone is equivalent

to that of a risk-averse individual choosing a portfolio of stocks with arbitrary covariance

matrix but common expected returns. This can be illustrated via the n = 2 case.29 Thus

29This case is closely related to Schmalensee’s (1982) pricing of product bundles in which reservation pricesare drawn from a bivariate normal. He noted that “[pure] bundling is shown to operate by reducing buyerdiversity” and that “changes in [dispersion] affect both the level and the elasticity of demand.”

20

s2 = var[θ] = α21σ

21 + α2

2σ22 + 2α1α2ρ12σ1σ2. This is minimized when α satisfies

α1

α2

=σ2

2 − ρ12σ1σ2

σ21 − ρ12σ1σ2

,

so long as this is an interior solution (i.e., ρ12 < min{σ1/σ2, σ2/σ1}). This, then, represents

the optimal Lancastrian bundle of characteristics when a monopolist wishes to take a mass-

market posture. From a portfolio choice perspective, several comparative statics emerge

readily. For instance, if the preferences for the two attributes are mostly uncorrelated, then

their relative variances are sufficient to determine the optimal mix, with the higher variance

attribute receiving less weight. Similarly, an increase in ρ12 increases the weight on the first

attribute if and only if it has a lower variance than the second attribute.

3.3. The Effect of Income Inequality. In our first two applications the monopolist influ-

enced the riskiness of the valuation distribution via her design and development decisions.

There are, of course, exogeneous factors that influence this distribution. For our third ap-

plication, we consider the effect of the distribution of income on the monopolist’s posture.

A consumer’s valuation for a product depends on his income, as well as his tastes. For a

normal good, an increase in income will increase the willingness-to-pay. Even if all consumers

share the same tastes (for a “plain vanilla” product, perhaps) variation in income will yield

a non-degenerate distribution of consumer valuations. An increase in income inequality may

result in an increase in the upper and lower bounds to the dispersion of consumer valuations.

This suggests that an increase in income inequality may prompt a monopolist to switch from

a mass-market to a niche posture. We explore this idea with the following simple example.

Example 4. A consumer’s willingness-to-pay satisfies θ = ωy, where ω is his taste for the

product and y is his income. Incomes and tastes are independent, with distributions satisfying

log y ∼ N(µ1(σ), σ2

)and logω ∼ N

(µ2(κ), κ

2).

The monopolist, with a constant marginal cost of c ≥ 0, chooses κ ∈ [κL, κH ], but not σ.

Hence σ2 indexes income inequality, and valuations are drawn from a log-normal distribution,

log θ ∼ N(µ1(σ) + µ2(

√s2 − σ2), s2

)where s2 = σ2 + κ2,

with a median of exp(µ1(σ) + µ2(√s2 − σ2)), and mean E[θ] = exp(µ1(σ) + µ2(

√s2 − σ2) +

s2/2). The choice of κ boils down to choosing the dispersion of valuations, subject to

s2 ∈ [σ2 + κ2L, σ

2 + κ2H ].30 Writing Φ(·) for the distribution function of the standard normal,

Ps(z) = exp(µ1(σ) + µ2(

√s2 − σ2) + sΦ−1(1− z)

).

30By inspection, changes in s lead to a family of distributions ordered by a sequence of local rotations.

21

We identify two special cases. First, we set µ1(σ)+µ2(κ) = µ, for some constant µ. Thus, an

increase in s, stemming from increased income-inequality or variation in tastes, will preserve

the median. By inspection, Ps(z) is quasi-convex in s; Proposition 1 applies, and hence

the monopolist will choose s ∈ {sL, sH}, or equivalently κ ∈ {κL, κH}. For the second

case, we insist that changes in σ and κ preserve the means E[y] = exp(µ1(σ) + σ2/2) and

E[ω] = exp(µ2(κ) + κ2/2); we set µ1(σ) = −σ2/2 and µ2(κ) = µ− κ2/2.31 Hence,

Ps(z) = exp

(µ− s2

2+ sΦ−1(1− z)

).

By inspection, Ps(z) is a quasi-concave function of s, and hence Lemma 1 and Proposition 1

cannot be applied.32 Nevertheless, Proposition 1 employs conditions sufficient for the quasi-

convexity of profits; they are not necessary conditions. Following the logic of Section 2.3,

profits will be quasi-convex so long as there is some s such that (s− s)(z†s − z∗s) > 0 for all

s 6= s; as s increases, z∗s crosses z†s once, and from above. Within the context of Example 4,

the following lemma determines when this is true.

Lemma 2. For the specification of Example 4, suppose that increases in income inequality

and the variability of tastes are mean-preserving, so that E[θ] = exp(µ) for some µ, and set

s2 = σ2 + κ2. Profits are quasi-convex in s for s < s and quasi-concave in s > s, where

s ≈ 0.925. In particular, if σ2 < s− κ2H , then monopoly profits are quasi-convex in κ.

Thus, so long as the dispersion of willingness-to-pay is not too large, the conclusion of Propo-

sition 1 continues to hold: the monopolist prefers the extremes of [κL, κH ].33 A microfoun-

dation for changes in κ could be obtained via, for instance, the characteristics specification

of Example 3. Here we observe that, subject to the restriction s < s, the introduction of

a “background risk” in income does not overturn the monopolist’s desire to choose design

extremes.34 Exogenous changes in the inequality of income (as indexed by σ) may, however,

determine which design extreme is preferred. In particular, observe that an increase in σ

increases both the upper bound sH and lower bound sL to the set S = [sL, sH ]. So long

as income inequality and the maximum design idiosyncrasy κH are not too great, π(s) is

quasi-convex in s, and the sign of π(sH)− π(sL) is increasing in both of these bounds.

31This ensures that mean income satisfies E[y] = 1; this is a normalization.32It is straightforward to confirm that z†s = 1− Φ(s), which is strictly decreasing in s.33To understand what it means to say that “the dispersion of willingness-to-pay is not too large,” note thatthe upper limit of s = s corresponds to a Gini coefficient of approximately 0.487.34We can relate this observation to the work of Ross (1981), Kihlstrom, Romer, and Williams (1981),Nachman (1982) and Jewitt (1987), who investigated when the comparative statics of risk aversion arepreserved following the introduction of a background risk. Notice that a rotation of the distribution of θ isequivalent to a rotation of the distribution of log θ. In turn, log θ is the sum of independent random variableswith log-concave densities. Following Jewitt (1987), if two distributions of the taste parameter ω differ by arotation, then this ranking will be preserved following the introduction of income variation. An increase inbackground risk might also correspond to an increase in the variability of consumers’ outside options.

22

Proposition 6. For Example 4, if either (i) increases in κ and σ are median preserving, or

(ii) the conditions of Lemma 2 hold, then the monopolist will choose κ ∈ {κL, κH}. There

exists σ such that the monopolist will choose κ = κH for σ > σ and κ = κL for σ < σ.

Thus an increase in income inequality may prompt a monopolist to switch from a mass market

to a niche posture. From a product-design perspective, we would expect the monopolist’s

product to offer something for everyone when consumer incomes are relatively homogeneous,

and to pander to the highest extreme when there is wider income inequality.

4. Advertising and Information Provision

In Section 3 changes in the income distribution as well as product design and development

decisions resulted in a family of valuation distributions indexed by riskiness. Here, we

provide a different microfoundation for our core theory of rotations developed in Section 2.

Specifically, we ask how the monopolist’s advertising, sales, and marketing activities might

influence the shape of demand that she faces. We identify two different functions of such