On the relation between unemployment and housing tenure...

123

UNIVERSITEIT GENT FACULTEIT ECONOMIE EN BEDRIJFSKUNDE ACADEMIEJAAR 2013 – 2014 On the relation between unemployment and housing tenure: the European baby boomer generation Masterproef voorgedragen tot het bekomen van de graad van Master of Science in de Handelswetenschappen Miguel Vandenbussche en Maxime Verhenne onder leiding van Prof. Dr. Carine Smolders

Transcript of On the relation between unemployment and housing tenure...

UNIVERSITEIT GENT

FACULTEIT ECONOMIE EN BEDRIJFSKUNDE

ACADEMIEJAAR 2013 – 2014

On the relation between unemployment and housing tenure: the European baby

boomer generation

Masterproef voorgedragen tot het bekomen van de graad van

Master of Science in de Handelswetenschappen

Miguel Vandenbussche en Maxime Verhenne

onder leiding van

Prof. Dr. Carine Smolders

GHENT UNIVERSITY

FACULTY OF ECONOMICS AND BUSINESS ADMINISTRATION

ACADEMIC YEAR 2013-2014

On the relation between unemployment and housing tenure: the European baby

boomer generation

Thesis presented in fulfillment of the requirements for the degree of

Master of Science in Commercial Sciences

Miguel Vandenbussche and Maxime Verhenne

under the supervision of

Prof. Dr. Carine Smolders

Preface

Ghent, May 2014

We made this thesis as a completion of the Master of Science in Commercial Sciences,

Finance and Risk management at the Faculty of Economics and Business Administration of

Ghent University in the academic year of 2013-2014.

The past year we have been investigating the remarkable relationship between unemployment

and home ownership that was described by a vast amount of academic literature. We wanted

to make a unique contribution to the literature and therefore decided to observe the

relationship for a specific age group that was not yet made, namely the baby boomer

generation. These days, this age group is hot topic for policy makers across Europe as the

baby boomers start to enter retirement age in large numbers.

With help of simple statistical analyses on the data of the SHARE database we were able to

make an academic contribution to the literature. Therefore we would like to thank Josette

Janssen to give us access to the dataset. We must also recognize it is one of the rare large-

scale datasets that is freely retrievable for students.

Furthermore we would also like to thank the people behind the Flemish Policy Research

Centre on Fiscal Policy to supply us with specific information concerning the recent findings

on the subject. Special thanks go to Daan Isebaert and Jan Rouwendal for their presentations

at a study day in Brussels.

Finally, with this preface we would like to underline the gratitude to our promoter, Professor

Carine Smolders, who guided us trough this academic route and gave us the opportunity to

explore this subject profoundly.

Enjoy your reading,

Miguel Vandenbussche and Maxime Verhenne

Acknowledgement

This paper uses data from SHARE wave 4 release 1.1.1, as of March 28th 2013 (DOI:

10.6103/SHARE.w4.111) and SHARE wave 1 and 2 release 2.6.0, as of November 29 2013

(DOI: 10.6103/SHARE.w1.260 and 10.6103/SHARE.w2.260). The SHARE data collection

has been primarily funded by the European Commission through the 5th Framework

Programme (project QLK6-CT-2001-00360 in the thematic programme Quality of Life),

through the 6th Framework Programme (projects SHARE-I3, RII-CT-2006-062193,

COMPARE, CIT5- CT-2005-028857, and SHARELIFE, CIT4-CT-2006-028812) and

through the 7th Framework Programme (SHARE-PREP, N° 211909, SHARE-LEAP, N°

227822 and SHARE M4, N° 261982). Additional funding from the U.S. National Institute on

Aging (U01 AG09740-13S2, P01 AG005842, P01 AG08291, P30 AG12815, R21 AG025169,

Y1-AG-4553-01, IAG BSR06-11 and OGHA 04-064) and the German Ministry of Education

and Research as well as from various national sources is gratefully acknowledged (see

www.share-project.org for a full list of funding institutions).

Table of Contents

1. Introduction .................................................................................................................... 1

2. Literature ........................................................................................................................ 5

2.1 Unemployment ................................................................................................... 5

2.1.1 Definition .................................................................................................. 7

2.1.2 Photograph ................................................................................................ 8

2.1.3 The rise of the unemployment rate in Europe ......................................... 10

2.2 Home ownership .............................................................................................. 12

2.2.1 Definition ................................................................................................ 12

2.2.2 Photograph .............................................................................................. 13

2.2.3 Home ownership stimuli ......................................................................... 15

2.2.4 Perverse effects of home ownership stimuli ........................................... 19

2.3 The relation between home ownership and unemployment ............................. 21

2.3.1 The Oswald hypothesis ........................................................................... 21

2.3.2 Macro academic research ........................................................................ 23

2.3.3 Micro academic research ......................................................................... 24

2.4 The role of financial assets ............................................................................... 26

3. Data ................................................................................................................................ 27

4. Methodology ................................................................................................................. 28

4.1 Oswald correlation for baby boomers across European countries (RQ1) ........ 28

4.2 The nuance in housing tenure (RQ2) ............................................................... 29

4.3 The role of financial assets (RQ3) ................................................................... 29

4.4 The unemployment equation (RQ4) ................................................................ 31

5. Results ........................................................................................................................... 32

5.1 Descriptive summary ........................................................................................ 32

5.2 Oswald correlation across European countries (RQ1) ..................................... 35

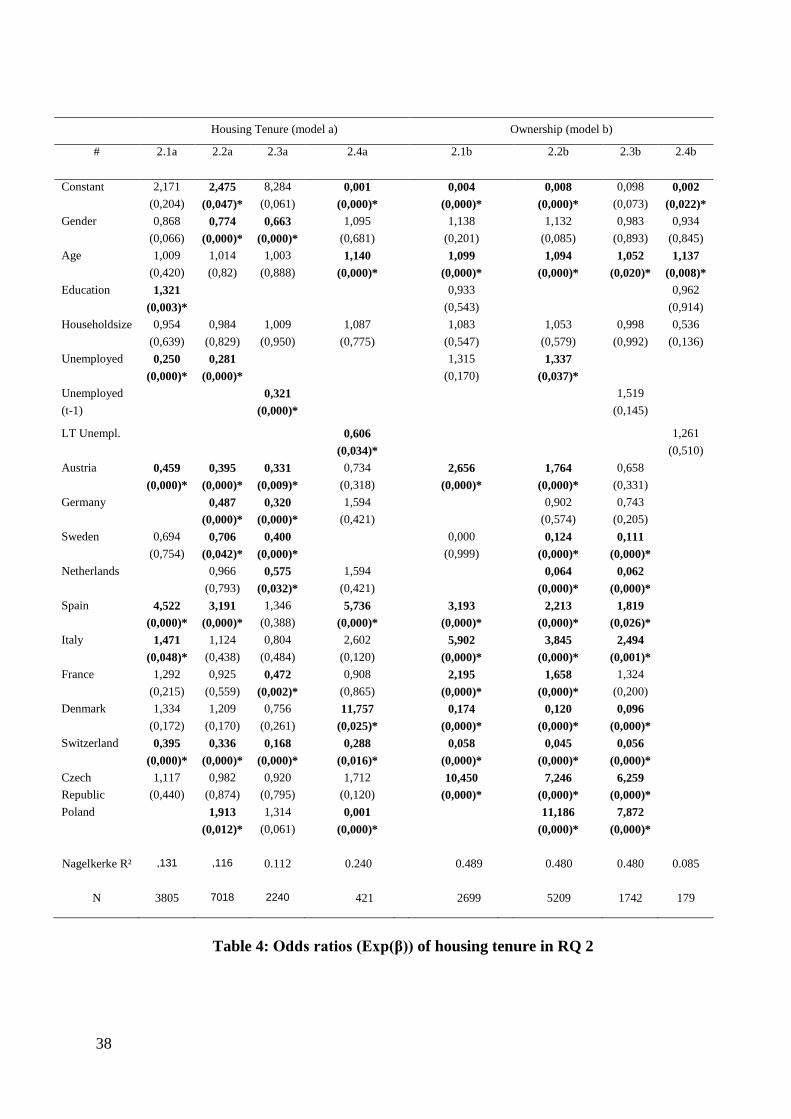

5.3 The nuance in housing tenure (RQ2) ............................................................... 37

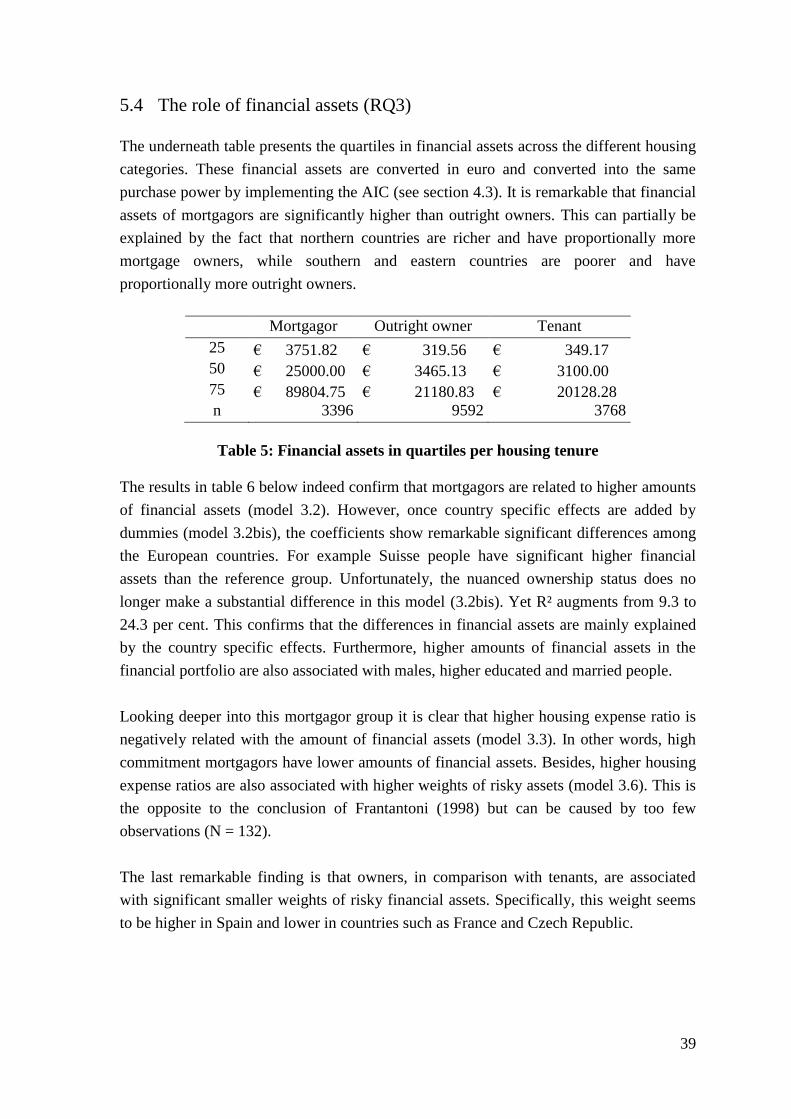

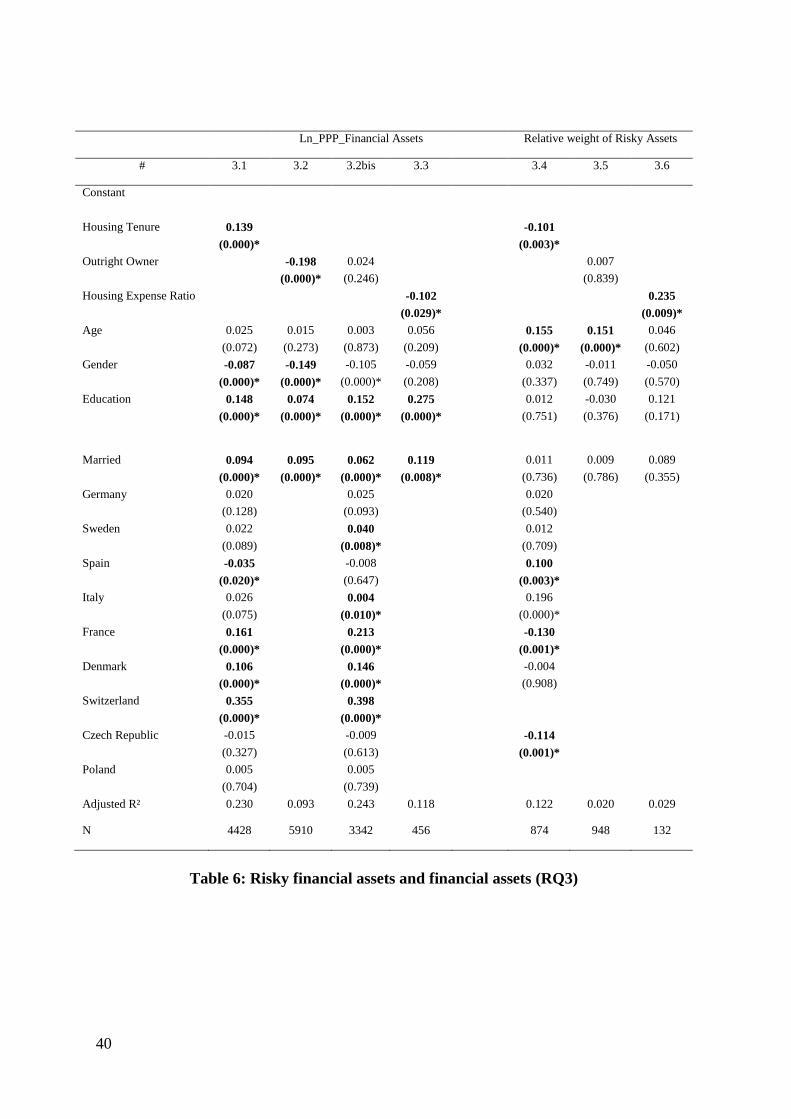

5.4 The role of financial assets (RQ3) ................................................................... 39

5.5 The unemployment equation (RQ4) ................................................................ 41

6. Conclusion ..................................................................................................................... 43

7. Final remarks of the authors ....................................................................................... 44

8. References ..................................................................................................................... 45

Appendix A .............................................................................................................................. 50

Appendix B .............................................................................................................................. 52

Appendix C .............................................................................................................................. 54

1

On the relation between unemployment and housing tenure:

the European baby boomers generation

Abstract

At aggregated level most developed countries are found to have a strong positive correlation between

the rate of unemployment and the rate of home ownership. In academic literature, this phenomenon is

called the Oswald Hypothesis because of Andrew Oswald’s 1996’s pioneering working paper on this

issue. He argued that the rising home ownership rates in OECD countries causes higher rates of

unemployment. As a result of this proposal, a lot of academic work was written that revealed new

insights. In this paper the hypothesis is tested on the so called baby boomer generation (people born

between 1946 and 1964) because, according to academics and policy makers, this specific working age

group bears longer unemployment spells and has a higher probability on being home owner. The

statistical analysis in this paper starts with the correlation for baby boomers across a selection of

European countries that indeed confirms the hypothesis. Later on, the micro level results of this paper

are more nuanced and show that outright owners have a significantly higher chance on being

unemployed and that they are associated with smaller amounts of financial assets in comparison with

mortgagors.

1 Introduction

"There are three kinds of lies: lies, damned lies and statistics." (Mark Twain, 1898)1

This one-line joke is one that many academics and students in economic science ever get

confronted with. Nevertheless, this statement bears an important lesson on the negative

perception for both writers and readers of statistics. On the one hand it is important that

economists and statisticians explain their work at an appropriate level so it can attain

many people. On the other hand it is important that readers are precarious, but try to

understand the point where the human science of economics can meet the exact science of

statistics, so it can be clear how to interpret these statistical results and that readers are for

instance able to apply the correct interpretation of the words ‘correlation’ and ‘causality’.

Essentially, this is what the theory of Oswald is all about. During the 1990s the British

professor - and later on many more academics - found strong correlation between two

macroeconomic fundamentals, which are home ownership and unemployment. The

Oswald hypothesis (Oswald, 1996) states that the growing rate of home ownership in

most developed countries causes higher rates of unemployment. The common sense

explanation argues that living in one’s own house makes people less mobile on labor

markets. Intuitively this is logic, because owners cannot move at the same speed and cost

as renters when looking for a job. One feature that is often investigated in the literature is

the unemployment spell that should – in theory – be longer for home owners compared

with renters, because owners literally ‘stick’ to their homes. In other words, rising home

ownership seems to slowdown the inner mobility at labor markets. But is this really true?

1 Quote retrieved from the autobiography of Mark Twain (Neider, 1959)

2

At a certain moment in time the growing home ownership rate in most OECD countries2

was even mentioned as the missing puzzle part in the economic theory of the natural rate

of unemployment, that was developed in the early sixties of the previous century by

Phelps and Friedman (1968). Nonetheless, this relatively strong correlation does not mean

that - in fact - a casual relation exists between these two macroeconomic indicators.

However, since Oswald presented his rough findings in 1996, a bunch of academic work

followed to unravel the possible mechanisms behind this correlation.

In general, the results across studies are not really consistent. Most of the academic

studies confirm the theory on aggregated data such as in the United States (Green and

Hendershott, 2001) or in Belgium (Isebaert et al, 2013). Since these results suffer from

aggregation bias, more ambiguous research followed on micro data. The results on data

of individuals showed insights for the literature, however they were not really consistent

across time or across countries that could be the result of the fixed-country effects. For

example the Spanish phenomenon in housing culture where obtaining a house for the

children is a family matter (Earley, 2004). Early micro analysis focused on the

unemployment spells of individuals that showed various results. In the U.S.,

unemployment spells were shorter for home owners (Green and Henderschott, 2001) in

contrary to France were this was found to be longer for home owners (Brunet et Lesueur,

2003). Notable is that some concepts became more nuanced, such as the difference of the

effect between an outright home owner and a mortgagor3, and the difference between the

public versus the private renter. A mortgagor for instance has a strong incentive to find a

new job because the mortgage has to be paid off.

Academic literature brings, however, an important problem of the results of Oswald’s

hypothesis that is named endogeneity bias. This problem is typically situated in social and

economic science and can lead to a rejection of a hypothesis that in fact is true.

According to the lectures of Reichstein (2013) the bias can be summarized underlying

two important features. First, omitted variable bias can lead to endogeneity problem such

as described by Van Leuvensteijn and Koning (2004) that certain variables in the model

have limited characteristics that are indeed important for the mechanism. The example

that the authors phrase is job commitment that can explain the housing tenure of people.

This shows that certain variables could be overlooked – or omitted - when explaining

housing tenure or the general unemployment rate model of Oswald. Second, another form

2 The Organization for Economic Co-operation and Development (OECD) current Member countries are:

Australia, Austria, Belgium, Canada, Chile, Czech Republic, Denmark, Estonia, Finland, France, Germany,

Greece, Hungary, Iceland, Ireland, Israel, Italy, Japan, Korea, Luxembourg, Mexico, Netherlands, New

Zealand, Norway, Poland, Portugal, Slovak Republic, Slovenia, Spain, Sweden, Switzerland, Turkey,

United Kingdom, United States 3 In this paper the mortgagor is “the borrower in a mortgage, typically a homeowner” (Oxford dictionary,

2014). The mortgagee however is defined as “the person who is the lender in a mortgage, typically a bank,

building society, or saving and loan association” (Oxford dictionary, 2014)

3

of the endogeneity problem was explained by L’Horty and Sari (2010) which is the

simultaneity bias. It is when variables are determined simultaneously and hence it is not

clear which one evokes the other one. In other words, this reverse causality can be a bias

of the theory because intuitively it is not clear whether someone is (un)employed because

he is a home owner or instead the fact that home ownership makes someone

(un)employed. This paper is however able to work with lagged variables of the tenure

status to address this latter problem. It is a good attempt to solve this problem, but not

completely (Reed, 2013).

Literature does not only link home ownership to unemployment, as there are other

variables that can be influential to both home ownership and unemployment. A possible

suggestion is the role of financial assets, of which less is known in literature. For instance,

Fratantoni (1998) linked housing tenure with the relative weight of investments in risky

assets and found mortgagors to be significantly more risk averse. Financial wealth itself

can also be an incentive to longer unemployment spells as it can be consumed during the

unemployed period (Gruber, 2001). Another relevant finding in this story is that generous

unemployment insurance benefits can undermine labor mobility. Feldstein (1973) for

instance argued that unemployment insurance was responsible for a rise in unemployment

rate. However, he also found that a lot of the benefit receivers were not especially low in

the income distribution. In this optic the Oswald theory may be specifically located with

unemployed (outright) owners who can combine the consumption of financial assets with

the benefits of unemployment insurance during the unemployment spell. That off course

is an incentive for longer unemployment spells.

In this paper the European baby boomer generation is taken into account. The United

States Census Bureau defines this generation as the people that were born in the post-war

housing and education society that started from 1946 and lasted until 1964. The argument

to work with this age group is dual. First, this age group has a significant higher

probability of being home owners in comparison with younger age groups (Andrews and

Caldera Sánchez, 2011). This is relevant, because in developed societies most of their

citizens dream to own their own house one day. In accordance with this dream, it is

plausible that in the year 2011 most of the baby boomers must have achieved their dream,

since the eldest boomers achieved the age of 65, which is the end of working age4. In the

opposite point-of-view, it is logic to perceive the baby boom renters as such that this

tenant choice is either the result of financial restrictions or either a well-thought-out

choice to be flexible in life or work situation and thus not a temporarily situation in order

to still achieve the dream of acquiring one’s own house. This paper’s scope is important

because temporarily housing situations can blur the underlying mechanism(s) of the

4 The SHARE questionnaires were hold in 2011. The oldest baby boomers (born in 1946) achieved the age

65 in the year 2011. (2011 minus 1946 equals 65)

4

theory. Second, it is proved that older workers of 55 years and older have a significant

lower mobility on labor markets because they spend far more time searching for work.

For instance the U.S. average searching period was found to be 56.1 weeks for this age

group in comparison with 35.1 weeks for unemployed at age less than 55 (Rix, 2013).

Thus, these dual finding seems to confirm the Oswald hypothesis across age groups.

Therefore this paper will investigate how strong this correlation really is across European

countries and what the underlying effects may be, such as the role of financial assets.

This paper uses the dataset of the Survey of Health, Ageing and Retirement in Europe

(SHARE) that serves data on European citizens at the age of 50 or more. In the first wave

the data extend to 30,816 observations across twelve countries while seven years later the

database of the fourth wave covers 58,489 individuals over fifteen European countries

plus Israel. In fact only twelve countries are taken into account since the regression

models required appropriate variables and lagged variables are used taken from the

second wave. Nonetheless, these data are ideal because the scope in age fits perfectly with

the age scope of the fourth wave. At the time of the interviews in 2011, the baby boomer

generations was between age 46/47 and age 64/65, which is the eldest age group of the

then labor force.

This papers’ first research question (RQ) checks if the European baby boomer generation

exhibits the correlation on a big dataset (N = 9738) across a selection of European

countries5. This correlation - that is measured with help of an ordinary least squares

(OLS) estimate – is expected to be stronger than Oswald’s original one across the OECD

countries (1997) because of the specific scope in age.

Then, the second RQ applies the nuance of the tenure status that is modeled as dependant

variable by making a sub selection between owners and renters and between outright

owners and mortgagors. In fact, this model tries to predict the probability for each of

these tenure statuses through the effect of unemployment and other control variables such

as gender, education or income. In line with other academic work, it is expected to

observe the incentive of a mortgagor to have a smaller chance on unemployment, because

- intuitively - this person needs to pay off the mortgage and is not willing to lose his or

her house and thus less unemployed.

The third RQ brings up a financial approach to the theory. First a model checks if housing

tenure of the baby boomers effects their choice of holding financial assets. In line with

Frantantoni (1998) it is expected that mortgagors give less weight to risky financial assets

5 The selected countries in the SHARE database for RQ1 are Austria, Belgium, Czech Republic, Denmark,

Estonia, France, Germany, Hungary, Italy, Netherlands, Poland, Portugal, Slovenia, Spain, Sweden and

Switzerland.

5

such as stocks, bonds and mutual funds, in comparison to outright owners.

Eventually, this paper investigates a general unemployment equation in line with Oswald

with help of a logistic model that implies the features of the previous questions, which are

the nuance of the housing tenure, financial assets, weight of risky assets in the financial

portfolio.

The second section offers a brief view on the literature that pursued Oswald’s (1996) up

to now, but the section is initiated with a photograph on the indicators ‘unemployment’

and ‘home ownership’, joined with an academic approach on these two macroeconomic

indicators. The third and fourth section incorporates the investigated data with the chosen

methodology. Eventually the results of this methods are shown in section five, just before

the conclusion in the sixth section. Finally, the paper is extended with a discussion for

future research.

2 Literature

2.1 Unemployment

“Unemployment insurance is a pre-paid vacation for freeloaders” (Ronald Reagan, 1966)

The era of Ronald Reagan is often described as ‘neoliberal’ and is in the optic of

oversimplified one-liners probably not different from other eras. The former Governor of

California depicts unemployment as a comfortable position because his statement builds a

bridge between the pleasant thought of vacation and the choice to be unemployed. In fact,

when Reagan became President of the U.S. in 1981 the unemployment rate was rising to

very high levels as a result of the lasting recession due to the oil crisis of 1973. When the

rollercoaster of the business cycle is speeding downwards, workers do not have much of a

voluntary choice when employers - en masse - go astray. Besides, academics have

pointed to the bitter fruits of joblessness. It is proved that being unemployed is a form of

distress that statistically bears significantly higher suicide rates, especially for men, since

the risk of suicide death in e.g. England and Wales (Charlton et al., 1992) was found to be

three times greater than average. Other results from the United Kingdom by Platt and

Kreitman (1985) even found a twelve time greater than average chance of attempting

suicide for long term unemployed Brits. An even more remarkable finding is Oswald’s

(1997) who observed that the rising suicide rate in Western countries since the 1970s

moves along with the rising unemployment rates. (Oswald, 1997).

However, a change of heart for this first – skeptical – paragraph may be found with the

6

time frame. Into the late 1970s, the Federal Reserve6 had a hard time making choices

between unemployment and inflation. Theory and practice used to show a strong trade-off

between these two macroeconomic indicators, that was named the Phillips curve. But by

the beginning of the decade the effect seemed to be gone for good due to the rational

expectations of workers and unions who claimed wages, that could capture the expected

inflation. As a result, the reality in the 1970s showed both high unemployment and high

inflation. This devastating finding on the Phillips curve came by Phelps and Friedman

(1968), Lucas (1976) and others. It’s because of these observations that the policy

performed under ‘the Reagan Administration’ had to make choices in order to drop the

high unemployment rates7 from the early 1980s. The chosen policy was – similar to the

introducing quote – quite harsh. It incorporated a decline in minimum wages, a full

taxation of unemployment insurance and work requirement for the unemployed.

Nonetheless, it was very successful as the unemployment rate dropped to its natural level

at the end of his Presidency8. His chief economic advisor even stated: “It was very

successful, especially in comparison with Europe, where the unemployment protection

policies led to double digit unemployment rates.” (Feldstein, 1997). Despite, critics argue

that this pride statement is questionable because the fundamental reason for change of the

economic climate and that of unemployment is not per se due to the chosen policy but

rather to the underlying business cycle that moves up and down every now and then and

is merely based on the monetary policy. (Krugman, 1982). In line with this critique,

recent work of Drehmann et al. (2012) reminds us to the financial cycle that is very

influential – more precisely procyclical - to this business cycle (see figure 1). In fact, the

financial cycle tracks the level of credit and property prices and moves along in intervals

of about sixteen years which is twice as slow as the business cycle. According to the

authors’ observations, the beginning of the 1980s showed a very strong upward trend for

this financial cycle that probably is due to the effect of financial liberalization. So it is

doubtful whether specific unemployment policies had such a great effect on lowering the

unemployment level. It seems rather the effect of bigger phenomena. Yet, less is known

about these real drivers such as the financial cycle.

6 The Federal Reserve is the central banking system of the United States that has mandate on the U.S.

monetary policy. (Meltzer, 2010) 7 According to the statistics of the United States Department of Labor, the rate of unemployment reached

9.7% in 1982. (U.S. Department of Labor, 2014) 8 The unemployment rate in 1988 was 5.5%. (U.S. Department of Labor, 2014)

7

Figure 1: The financial and business cycles in the United States (Drehman et al.,

2012)

Returning back to unemployment on individual level, financial incentives are at work as

well. A working paper of Tatsiramos (2006) argues that an unemployment insurance

reduces the incentive for leaving unemployment. When comparing the diverse

unemployment insurance systems across Europe it is clear that more generous systems

lead to longer periods of unemployment for individual unemployed persons. The writer’s

diagnose is that welfare countries in Europe have taken away the incentive to work.

Hence, it is notable that the phenomenon of unemployment is not easy to understand and

that analyzing, debating, avoiding this phenomenon should happen with an appropriate

level of distinction. For instance the distinction between structural and cyclical

unemployment that was discussed in the previous paragraph. Besides, this can be for

instance very country specific, such as the well known and unique example of Denmark.

The country is perceived as a “flexicurity” welfare state because it has a highly flexible

labor market with high mobility and a high employment rate in combination with good

protection mechanisms for workers, such as high minimum wages and long generous

unemployment insurances (Andersen, Svarer, 2007). As it is notable, these country-

specific incentives must be distinct when analyzing this macroeconomic indicator.

2.1.1 Definition

Unemployment seems easy to understand, but it in fact it’s not. Observing unemployment

rates in reports, papers or policy programs may be misleading because definitions of the

concept can vary. Briefly, two categories of definitions can be observed

First, in sensu stricto, the most known and applied definition of unemployment is the one

used for the harmonized unemployment rates in OECD countries. The applied definition

8

is based on the International Labor Organization (ILO) that defines unemployment as “a

person - at working age who - in a certain reference period is:

without work, that is, were not in paid employment or self employment during

the reference period;

currently available for work, that is, were available for paid employment or

self-employment during the reference period; and

seeking work, that is, had taken specific steps in a specified recent period to

seek paid employment or self-employment. “(ILO Conference of Labour

Statisticians, October 1982)

Second, in sensu lato, broader definitions of being unemployed are found. In line with the

application of the critique of Brandolini et al. (2004) the unemployed can be divided into

four groups:

i. persons who do not want a job

ii. persons who are not searching but might take a job if offered,

iii. persons who are looking for a job and took specific steps in the last four weeks

(this is similar as the definition of the ILO)

iv. and finally persons who are searching for a job but took their last step more

than four weeks before the observation moment.

The ILO standard only incorporates category three and defines the other categories as

inactive people. According to Brandolini et al. (2004) it is because of the negligence of

category four that approximately one fifth of the European unemployed during the 1990s

was left out of the unemployment statistics. The reason is that the arbitrary chosen four

week period does not capture this group. In fact, this was revealed during the 1990s by

the Italian Statistics Agency (Istat) that did not apply this ‘four weeks’ rule. (Brandolini et

al, 2004). Notable is that the author suggests that the best distinction for the definition is

to check whether an unemployed person is really looking for a job or not. Besides, one

can also argue whether category two or even one concerns unemployed persons, as being

long term unemployed can be demotivating for the individual.

2.1.2 Photograph

Europe’s unemployment rates are heterogeneous (see table 1). With the help from the

Organization for Economic Co-operation and Development (OECD) statistics, this

section presents a brief picture of the 2011 harmonized unemployment rates and its

evolution (see figure 2) between 1990 and 2010 for all age groups.

9

Austria 4.1 % Italy 8.4 %

Belgium 7.2 % Netherlands 4.5 %

Czech Republic 6.7 % Poland 9.7 %

Denmark 7.6 % Portugal 12.9 %

Estonia 12.4 % Slovenia 8.2 %

France 9.2 % Spain 21.6 %

Germany 6 % Sweden 7.8 %

Hungary 11 % Switzerland 4 %

source: data retrieved from OECD statistics

Table 1: Harmonized Unemployment Rates for a selection of European countries

(2010)

Figure 2: Evolution of the harmonized unemployment rates (2010)

As the second part of our paper will focus on the baby boom generation, a more closer

look on the unemployment characteristics of these age group is interesting. According to

the unemployment rates given by OECD labor force statistics, the unemployment rate of

the age category 55-64 is not especially higher than for younger workers in most

countries. Belgium for example had an unemployment rate of 5.4 per cent for the age

category older than 55 in comparison with 7.4 per cent for the age category 25-54 in the

year 2013. This false perception is described by Rones (1983) on a dataset of the 1960s

and 1970s. These unemployment figures can be explained by several things such as the

fact that older workers are less likely to get unemployed by the cyclical effects of an

economy, older workers are often more protected in the working agreements, instead of

laying off the older employers firms often offer financial provision to get an early

retirement. Also important is the described lower unemployment rate for woman.

0

2

4

6

8

10

12

14

16

18

20

22

24

1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010

source: data retrieved from OECD statistics

Austria Belgium

Denmark France

Germany Italy

Spain Sweden

10

Especially in older data it is acceptable that older woman have lower unemployment rates

as they withdraw from the labor market more often because of lack of the career-

orientation (Rones, 1983). It is however proved that older workers generally have a

significant lower mobility on labor markets because they spend far more time searching

for work. For instance the U.S. average searching period was found to be 56.1 weeks for

this age group in comparison with 35.1 weeks for unemployed at age less than 55 (Rix,

2013). So this false perception of older workers is in fact true but only in case of the

unemployment spell and thus not in the unemployment rate.

2.1.3 The rise of the unemployment rate in Europe

Figure 3: The unemployment rate for EU-15 (Blanchard, 2006)

Literature is clear. Most of the European countries have seen unemployment rates

growing since the 1970s. The above figure by Blanchard (2006) - retrieved from the

OECD database – shows a significant growth of the relative share of unemployed

Europeans9 across the past decades. Moreover, the fluctuations of the unemployment rate

seems to be more volatile as it moves with the business cycle. (Blanchard, 2006) This is a

remarkably finding because during the same period the U.S. unemployment rate didn’t

show such a trend at all. In fact, the U.S. unemployment rate was quite stable over time

and before the 1970s it was consistently higher than the European rates. (Blanchard,

2006). According to Solow, the most remarkably about the European rate is that it

dominates the business cycle. (Solow, 2000) This means that the growing part of

unemployment is rather structural and less a result of recessions in the business cycle

9 The EU-15 countries are: Austria, Belgium, Denmark, Finland, France, Germany,

Greece, Ireland, Italy, Luxembourg, Netherlands, Portugal, Spain, Sweden and United

Kingdom

11

rollercoaster.

So, what is this theory of the natural rate of unemployment all about? Today, most

macroeconomic course books threat this concept, that was initially formulated in the

1960s by two economists named Milton Friedman and Edmund Phelps. The formulation

was in fact very simple: “an economy will have a sort of constant rate of unemployment

that is rather structural because it is evoked by factors such as labor market imperfections,

costs of information, deceleration or non access to vacancy information and costs of

mobility” (Friedman, 1968). This statement was based on the perception of looking at

labor markets through the eyes of equilibrium models, the so called Walrasian systems.

As the professor argued, it is important to note that this rate depends on the policy of the

nation or of a central bank and, as a result of this, is not per se unchangeable over time.

Therefore, many teachers and writers need to note that the word ‘natural’ of the theory of

the natural rate of unemployment is rather confusing because it – as for example the

European rate - moves over time.

According to Blanchard and Katz (1996), the past research between the 1970s and the

1990s on the potential explanations of this rising unemployment rate are various and

rather unreliable because unrevealing this puzzle was neither consistent across time, nor

across countries. The potential determinants that were presented by academics over these

years drove from the increase of price of energy, the slowdown of productivity growth

(Bruno and Sachs, 1985), the impact of taxes on wages (Bean et al., 1986), loss of skills

due to long term unemployment (Blanchard, 1991), labor market rigidities such as the

firm’s cost and term of firing workers (OECD Jobs Study, 1994) or either the growth of

unskilled workers due to fast technological progress (Krugman, 1994). One can off course

argue about the country specific differences, but the utter diagnose, which Blanchard and

Katz mentioned in 1996 at the bottom line of their paper is the discrepancy between

macroeconomic view on the natural rate of unemployment and the micro economic

findings by labor economics. Or to use their words: “We thus end with a plea for more

joint efforts by macro and labor economists to better integrate theoretical and empirical

work on wage determination and unemployment.”

Later on, it was Flatau et al (2003) who first related the Oswald hypothesis as a possible

explanation of the rise in the natural rate of unemployment for the observed OECD

countries. The hypothesis is that the rising rate of home ownership since the second world

war is not strictly due to labor-market characteristics, but a possible consequence of the

growing home ownership rate in most developed countries.

12

2.2 Home ownership

“Deep in the hearts of most American families glows, however faintly, the spark of desire

for home ownership.” (U.S. Department of Commerce, 1942)

Owning your own house is one of the main purposes in life for most of us and is an

important part of the American Dream. The benefits of owning your own house are

enormous: it stabilizes communities and leads to more responsibility for the living

environment (diPasquale, Glaeser, 1999), houses look greater because the owner has a

strong incentive to maintain them (Coulson, 2002) and it has a positive effect to personal

satisfaction and self-esteem (Rohe, Stegman, 1994).

However, recent events - such as the U.S. housing bubble burst of 2007 - showed that the

benefits of this dream doesn’t always follow reality. This is an indication that policy

makers need to be thoughtful when implementing this part of the American Dream. Also

other perverse effects can be part of the double edged sword of home ownership.

2.2.1 Definition

Literature defines home owners as owner-occupiers: “a housing unit is owner-occupied if

the owner or co-owner lives in the unit, even if it is mortgaged or not fully paid for.” (U.

S. Census Bureau). This means for example that someone who owns a house but lives in a

rental apartment is no longer perceived as a home owner, but instead as a tenant.

However, according to Proxenos (2002) there is no strict definition of home ownership

itself. The interpretation of home ownership differs from one country to the next. Where

one country considers a mobile home as ownership, another country would not. Also the

definition of home ownership tells nothing about the quality of the owner-occupied

houses. This can lead to an over-estimation bias between the home ownership in countries

especially at a global scale. This means that in some cases it is not justified to compare

these rates as they are not based on the same funding definitions, this estimation can lead

to misleading results. Besides, it is also possible that a bias appears in surveys when the

concept of home ownership is not well defined to the respondents.

13

Since the 1990s, organizations such as the OECD and Eurostat started tracking the rates

of home owners of nations in order to benchmark. These percentages represent the sum of

dwellings that are owned outright or purchased with a mortgage in relation to the total

dwelling stock. This latter incorporates the total of home owners plus tenants. (European

Mortgage Federation, 2004). Thus, the rate is equated as follows:

2.2.2 Photograph: ownership rate

When investigating these ownership rates, two facts are consistent across academic

research. First, on a long time horizon nearly all countries experienced a growth of the

share of home owners. Second, these ownership rates strongly differ across countries

(Andrews and Caldera Sanchez, 2011). The overall average home ownership rate once

was measured across 106 countries on data from the World Bank and it was found 67.8

per cent with a median of 69.3 per cent. (Fisher and Jaffe, 2003). For a selection of

OECD countries, Andrews and Caldera Sanchez (2011) describe this evolution and build

models to decompose its determinants. However, the they strongly differ. For example in

2004 Spain had an ownership rate of 83.2 per cent while Switzerland’s did not even

reached half this percentage with 38.4 per cent.

A more nuanced way of observing the housing tenure of citizens is the distinction

between private or public renter and the distinction between a mortgagor or a household

that has no outright owner as this was confirmed recently by researchers such as Nijkamp

and Rouwendal (2007). The EU Statistics on Income and Living Conditions (EU-SILC)

survey measures a range of structural indicators of living conditions. One is the tenure

status of the individual households. (see Figure 4) A few substantial differences between

the member states arise. Northern countries as Denmark, Netherlands, Sweden and also

Switzerland have very little outright owners, but instead a very substantial share of

mortgagors. Also countries such as Germany, Austria and Switzerland have

proportionally a high share of renters compared to the other countries. For instance the

share of Swiss tenants is almost 60 per cent.

14

Figure 4: Housing tenure in Europe (2010)

When investigating the determinants of these heterogeneous rates, some predictive power

was found for the effect of housing credit. (Fisher and Jaffe, 2003) Most countries’

policies offer a contribution scheme for housing finance. However, a single equation

model for explaining the traditional economic determinants of home ownership rate

across countries was not consistent. The country specific differences on cultural, law,

economic or political fields seems to be too harsh to make a generalized econometric

model with consistent results. It seems that incentives for ownership are very diverse

across countries.

Although there is perception that home ownership is linked to the wealth and strength of

an economy, such as suggested in the American dream, the adverse is proved by the

poorer European countries where ownership rates are very high, such as Greece and Spain

(Earley, 2004). This could for instance be caused by the cultural differences between the

more northern and the southern European countries. This is explained by the fact that in

southern societies have strong traditions of the family being involved in the

accommodation choices of their children. An example of this is the proportion of children

living at home that was found the highest in these southern countries (Earley, 2004). This

means that children stay longer with their parents so that they have a better financial

support when eventually leaving the family home. It seems logic that this phenomenon

leads to lower demand of rental units in these states. And thus the rental market is

underdeveloped.

0%

20%

40%

60%

80%

100%

Owner, no outstanding mortgage or housing loan (=outright owner) Owner, with mortgage or loan (mortgagee) Tenant, rent at market price Tenant, rent at reduced price or free

source: data retrieved from Eurostat, based on EU-SILC

15

Also remarkable are the Eastern European countries that have very high ownership rates

as a result of the communist legacy. During the communistic era it was the state that

owned a large share of the housing system. These housing units were part of cooperatives

during the 1980s. After the fall of communism in 1989, most of the countries experienced

a wave of privatization of ownership. As a result homes were offered for free to its

inhabitants and almost every ex-communistic country developed these remarkable high

rates of home ownership (Struyk, 2000).

2.2.3 Home Ownership Stimuli

“When it comes to economics people have emotions, it's not like chemistry or physics”

(Shiller, 2013)

These days, the most persistent feature to promote home ownership seems to be the home

mortgage interest deduction (HMID) systems in fiscal policies. This system gained a lot

of popularity among tax payers, since they are able to reduce their fiscal expenses.

However, another pallet of less known or less rational stimuli for home ownership exists.

Irrationality and herd behavior

As houses are often seen as an important asset investment, it may be interesting to

perceive decision making stimuli with a financial approach. Let’s start with two of the

three 2013 Nobel Prize winners in Economic Science, Robert Shiller and Eugene Fama.

Something strange appears in their financial theories. These academics totally disagree.

The 1970s were - concerning financial theories - the golden decade for the “efficient

markets” theory. Fama said that capital markets were “efficient”. This is the case when

investors of capital products act completely rational because their decisions to buy or sell

are based on all available information at the moment of their transaction. Fama argued

that all available information is thus reflected in the price of this asset (Fama, 1970).

Contrary, Shiller began talking about behavior finance and argued that people do not

always behave rationally. Examples come from social science and are for instance

wishful thinking or herd behavior. These features eventually can evoke so called

“irrational exuberance” in financial markets (Shiller, 2000), but also in housing markets

(Shiller, 1989). It was in this optic that Case and Shiller warned for a housing bubble on

the U.S. housing market in 2004 (Shiller and Case, 2003). According to the researchers

housing prices could no longer solely be explained by fundamentals such as population

growth, construction costs, income growth or tax rates. Their arguments were also based

on qualitative evidence that showed homebuyers’ perception of buying a house more and

more as a result of making an investment. Also, their survey showed that a major

motivation of buying a home was the expected future appreciation of the house price.

More than 90 per cent of the respondents expected an increase in home prices in the next

16

seven years. However, in reality, the U.S. housing bubble collapsed in 2007 with negative

corrections of 30 per cent10

and more resulting in prices far beneath these expectations.

So it seems that one of the incentives to buy a house can come from herd behavior and

also can be explained by irrational expectations. Briefly, these stimulus seems to be the

result from mythical expressions such as “land is scarce, prices can only rise” that should

better be replaced by “what goes up, may come down”.

Home ownership programs

Underneath this irrational expectations may lie a certain governmental policy that evoked

this. One of the systems that led to a lot of attention because it was pointed as one of the

causes of the U.S. housing bubble in 2007 is the policy that President Clinton started in

the U.S. under the name of the National Home ownership Strategy. The president defends

his policy on stimulating ownership based on its social and economic benefits:

“Home ownership encourages savings and investment. When a family buys a

home, the ripple effect is enormous. It means new home owner consumers. They

need more durable goods, like washers and dryers, refrigerators and water

heaters. And if more families could buy new homes or older homes, more

hammers will be pounding, more saws will be buzzing. Homebuilders and home

fixers will be put to work. When we boost the number of home owners in our

country, we strengthen our economy, create jobs, build up the middle class, and

build better citizens.” (Clinton, 1995)

Before the 1960s, policies facilitating home ownership were initially established to

encourage other purposes such as to boost economy out of recessions. But by the time

such a measure was eventually operational, the actual recession was already gone.

However, as these measures were enacted they had a significant impact on housing on the

long run. (Carliner, 1998) The reason why it had grown is merely due to the overall

economic growth and lower interest rates than to any specific housing policies.

Under the Clinton Administration the home ownership rate – as measured by the U.S.

Census Bureau – rose to 68 per cent by the end of 2001. (Bratt, 2002). Next came the

American Dream Down Payment Assistance Act under the Bush administration, that had

a specific target group (Bush, 2003). A budget of 200 million dollars was provided by the

government to support low income families.11

This law and many others which aimed to

create a society of home owners eventually lead to an increase of the ownership rate to a

10

According to the Case-Shiller Home Price Index (2014)

17

record height of 69.4 percent in June 2004, according to the United States Census Bureau.

Beside these programs, other aspect of pro-home ownership policies can declare the rise

of home ownership within the U.S., namely the innovations in the mortgage financing

business and the flexibility in repayment schedules (Doms and Motika, 2006). A good

example of these innovations are Fannie Mae and Freddy Mac, which are the most known

government-sponsored mortgage enterprises that had a big impact in the mortgage

financing industry as their activities raised significantly from the 1990s tot the early

2000s (Roll, 2002). During this period they contributed to the creation of the so called

‘mortgage backed securities’ (MBS) that ignored the real credit worthiness of the

individual mortgagors, and was able to pass – or secure – the risk to the financial markets.

(Diamand and Rajan, 2009).

Home Mortgage Interest Deduction (HMID)

Most of the industrialized countries handle a fiscal policy program to offer their citizens

an incentive to buy a house. The ideology in the eyes of policymakers is that private

home ownership has many benefits for society as a whole. The applied systems across

most European nations are very similar and incorporates an income tax deduction of the

interests that are charged on the outstanding mortgage linked to the property that the

owner is acquiring. This means that governments are stimulating people to take a loan for

financing one’s own house.

As mentioned by Oswald (1999) Spain and Switzerland are two very contrary cases

within European home ownership statistics. In Switzerland, the authorities do not

promote housing on national level to increase the home ownership rate. This is reflected

in the less favorable fiscal tax systems for home owners. Although interest of a mortgage

is tax deductible, it is rather low because many taxes are added. A property tax also is

added to the taxable income, which is similar to rental income. Besides, when a house is

sold a tax performs on the capital gain. (Kirchgässner, Pommerehne, 1996) This policy

can be explained by the fact that around two-thirds of the Swiss households are renters. A

characteristic of this developed rental market are the institutional investors who own more

than one fourth of this market. (Bourassa et al., 2010) The contrary is seen in Spain where

the authorities promoted home ownership for a long time. However, since the March

2012 – as a result of the economic crises and the Spanish housing bubble – interests on

mortgages and capital payment are no longer tax deductible (PWC, 2012). It will be

interesting to see what impact this measure has on the home ownership rate in the

upcoming years.

Besides, it is also questionable whether these policy measures really are (or were)

18

effective. As told by Glaeser and Shapiro (2002) these home ownership policies mainly

aided the wealthier owners instead of following the ‘American dream’ philosophy where

it is for everyone to obtain a house. Evaluating the different mortgage deduction policies

over the years the real effect on the rate of home ownership is minimal, as it has mainly

influenced the housing consumption and as a result missed its original purpose. Glaeser

and Shapiro argue that the best evidence is the fact that the U.S. ownership rate did not

augment significantly over the past 40 years although the existence of a mortgage interest

deduction has gained much of popularity among owners.

Now returning to Europe, it certainly is interesting to compare the importance of

mortgage markets within the different countries since the growing popularity of

deductable mortgage interest systems. An indicator for this type of benchmarking is the

total mortgage debt of a country relative to its GDP. (Earley, 2004) An interesting

finding – that is presented on figure 5 - is that over EU countries a negative correlation

exists between the home ownership rate and mortgage debt to GDP. Essentially, this

seems a bit perverse because the countries with higher rates of debt have smaller rates of

owners. Or in other words, countries with a high ownership rate, such as Spain, Greece,

Poland or Belgium have smaller outstanding mortgage debt. Although every country has

its own story, it is notable that this proves again poorness of a interest deduction system.

Earley (2004) argues that the level of development of finance markets and its supply and

demand are more important factors. The Southern countries for example, where

ownership rates are higher, are also poorer and so it is more riskier for southern people to

become dependent on a mortgage, hence its level of outstanding mortgage debt is rather

small.

Figure 5: Mortgage Debt to GDP ratio vs. home ownership rates (Earley, 2004)

19

2.2.4 Perverse effects of home ownership stimuli

The dream of owning your own house is widespread across Western civilization. Chasing

this dream and eventually achieving it is a self-fulfillment, a save harbor and a pleasant

thought for most people. Although ownership rates in some countries are very high,

policymakers keep pointing to the abundant benefits of owning one’s house and handle

incentives to promote this achievement. Indeed, academic literature on the benefits of

owning your own home is abundant, such as Glaeser and DiPasquale who found home

owners significantly more involved citizens which results in strong communities. On the

other hand, academics point to some perverse effects of stimulating ownership – at all

costs – for all citizens.

Credit Crisis

It’s oversimplified to find only one scapegoat for the credit crisis. In this optic the role of

home ownership is also relevant. As a result of the securitization of mortgage loans in

order to facilitate ownership to low income families, the risk that was put in the markets

was higher. Among the Americans, a perverse phenomenon rose that was named NINJA

loans that offered mortgage loans to people with No Income, No Job, or no Assets

(Coffee, 2008). At the time, prices reached higher levels relative to rent or incomes in

Ireland, Spain, the Netherlands, the United Kingdom and the United States (Diamond and

Rajan, 2009) while the general believe was that housing prices could only go up in the

long run. When the housing bubble eventually burst, the housing prices fell sharp with

corrections of 30 per cent and more (see before).

Inequality

One can also ask whether home ownership is the best way to build wealth for low-income

families. Policy makers often point to the general benefits such as the eternal rising

housing prices, that serve as a protection for the old days. Summarizing by a quote such

as “buying a house is the best investment one can make”. But is this really the full truth?

According to Galster et al. (1996) it was in 1963 that Grigsby introduced the filtering

theory of the housing market. The filtering of the housing market takes place as follows.

Prosperous citizens build new homes in new areas which are clean and modern. The

quality of these houses is outstanding, but after a few decades the quality declines

especially when these houses are not well maintained or these houses are no longer

equipped with new technologies, such as for instance energy efficient central heating.

When low-income families look for affordable houses their scope often is restricted to

these old houses that fit within their budgets. Often a miscalculation of the price is made

because future costs of maintenance are not taking into account. The fact that lower

income families tend to buy older homes that are affordable at the moment leads to higher

20

risk that the house loses its value. Especially when this old house is located in a

neighborhoods that bears a higher risk on vacancy. When demand for these houses lowers

the price will fall too. Add up a mortgage or loan that is linked to the property and this

story can even get more dangerous such as described by McCarthy, Van Zandt and Rohe

(2013). Is it fair that low income families need to make monthly mortgage repayments for

a fixed total amount that is higher as the future value of the property itself? From the

opposite point-of-view high-income families build new houses at new areas and repay a

mortgage for a total amount of which the chance that the price will rise is much higher.

Besides, the risk for low-income families is leveraged since they hold larger portions of

their wealth in housing. Therefore, Chaterjee (1996) argues that if home ownership would

not be so attractive, only households that could effort it would buy houses so there would

be smaller mortgages taken. This leads to less risk because the hold portfolios would be

more diversified.

Are HMID effective?

Mortgage deductions can even work discouraging for achieving home ownership.

Simulation models in studies have clearly shown that in some countries the value of the

deduction is capitalized into the price of the home prices themselves (Nakagami, Pareira,

1994). This certainly is a perverse effect because often young families – who often belong

to lower income groups – are financially more restrict to buy their dream. In the

simulation of Nakagami and Pareira an elimination of the interest deductibility would

mean that the price of renting becomes relatively cheaper in comparison with the price of

owning. As a result of this the rental market will bloom and as a result it will lower the

demand for houses on the housing market, which in a market economy means lowering

housing prices. What these researchers did not mention is that in real life such an

elimination may be abrupt and can lead to a shock on the housing market.

One can also question the effectiveness of offering taxation incentives for home owners.

Mann (2000) argues that countries such as Canada, New Zealand and Australia have

similar ownership rates in comparison with the U.S. despite they don’t apply HMID.

Also, when the United Kingdom reduced the deductible amounts there was no significant

drop in home ownership rates. Also for the U.S. the rate of home owners stayed rather

constant since the 1960 despite the application of HMID. (Glaeser and Shapiro, 2002)

Asset rich, income poor

Another issue an possible result of raising the home ownership rate in developed

countries is the phenomenon of “asset rich, income poor”. It describes the majority of the

elderly who have significantly higher levels of housing wealth, but are often beneath or

flirting with the poverty definition of income because pensions are less generous.

21

Research on this topic is however limited. Dolaning and Ronald (2010) point to Belgium

where this effect appears. A proposed solution for the income poorness is the reversed

mortgage in which the house is consumed in order to add an extra monthly premium to

the retirement pension income (Bradbury, 2010). In Australia Bradbury (2010)

investigated if elderly consume their housing assets during retirement. This was not really

the case. However the researcher found that the average Australian older person is indeed

asset rich but income poor.

2.3 The relation between home ownership and unemployment

This section connects the two latter sections. Next to the discussed perverse effects of

being a home owner, this section arrives at the most remarkable one among them. In

1996, British economist Andrew Oswald stated that the rising home ownership rates in

OECD countries causes higher unemployment rates (Oswald, 1996). In the pile of

academic work that followed on this statement one can distinct two levels of research that

are essential to understand the problemacy. At first level, macro academic work focuses

on the characteristics of countries or regions in order to proof the theory. Yet, a second

step of the theory has followed, that investigates the relationship on individual level. Such

a micro research is ideal to reveal the small-scale incentives of people that are underneath

the emerging correlation.

2.3.1 The Oswald Hypothesis

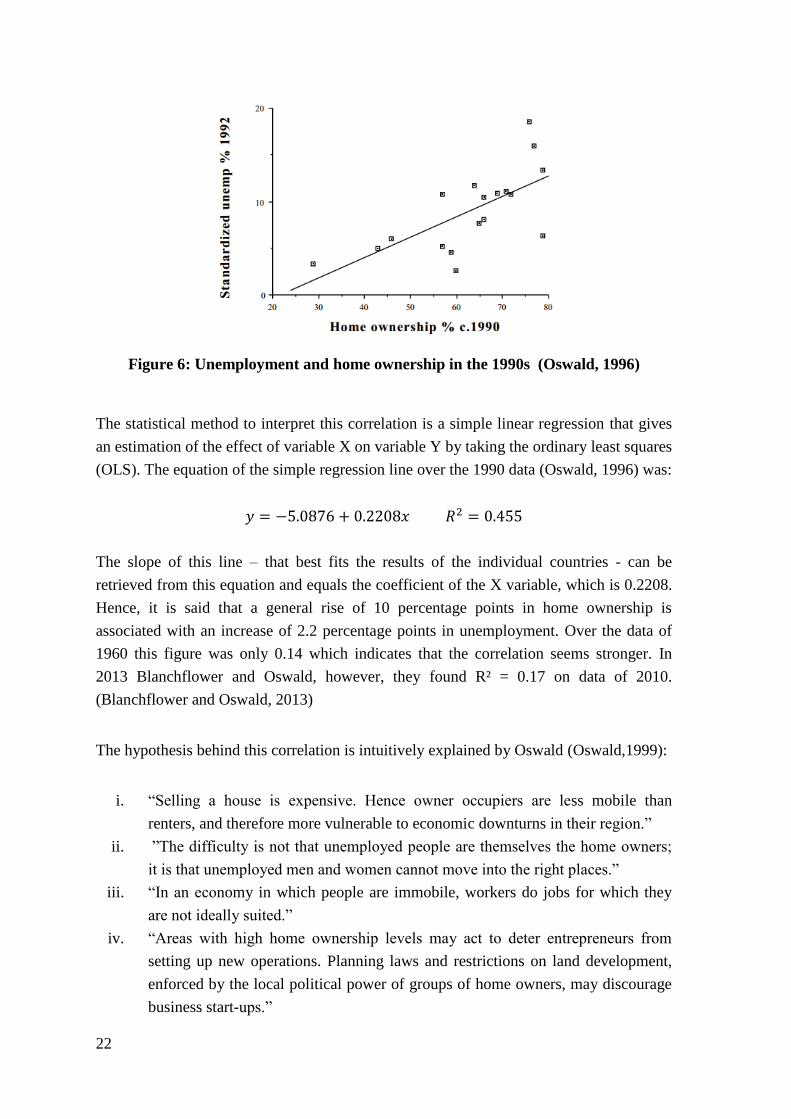

In 1996 Oswald published his first paper concerning the hypothesis that a rise in the

unemployment rate is explained by an increase in home ownership, or in other words a

decline of the private rental market. The original working paper shows a strong

correlation between the rate of unemployment and home ownership rate of a selection of

industrialized nations, as depicted on figure 6. Visually this positive relation is

demonstrated by a scatter plot between the two variables for a selection of industrialized

countries in the 1960s. These different countries - graphically represented by dots -

exhibit a linear relationship indicating a correlation of these two variables. Countries with

a high degree of ownership like Spain (75%) have a higher unemployment rate (18%) and

vice versa, for example, Switzerland that combines a low unemployment rate (4%) with a

low ownership rate (28%). (Oswald, 1996) However, this chart only shows a statistical

correlation. This means that unemployment and home ownership of countries tend to vary

together. However it is not known whether this relationship is causal, nor are the country

specific effects explained.

22

Figure 6: Unemployment and home ownership in the 1990s (Oswald, 1996)

The statistical method to interpret this correlation is a simple linear regression that gives

an estimation of the effect of variable X on variable Y by taking the ordinary least squares

(OLS). The equation of the simple regression line over the 1990 data (Oswald, 1996) was:

The slope of this line – that best fits the results of the individual countries - can be

retrieved from this equation and equals the coefficient of the X variable, which is 0.2208.

Hence, it is said that a general rise of 10 percentage points in home ownership is

associated with an increase of 2.2 percentage points in unemployment. Over the data of

1960 this figure was only 0.14 which indicates that the correlation seems stronger. In

2013 Blanchflower and Oswald, however, they found R² = 0.17 on data of 2010.

(Blanchflower and Oswald, 2013)

The hypothesis behind this correlation is intuitively explained by Oswald (Oswald,1999):

i. “Selling a house is expensive. Hence owner occupiers are less mobile than

renters, and therefore more vulnerable to economic downturns in their region.”

ii. ”The difficulty is not that unemployed people are themselves the home owners;

it is that unemployed men and women cannot move into the right places.”

iii. “In an economy in which people are immobile, workers do jobs for which they

are not ideally suited.”

iv. “Areas with high home ownership levels may act to deter entrepreneurs from

setting up new operations. Planning laws and restrictions on land development,

enforced by the local political power of groups of home owners, may discourage

business start-ups.”

23

v. “Home owners commute much more than renters, and over longer distances, and

this may lead to transport congestion that makes getting to work more costly and

difficult for everyone”

Although these arguments seem plausible they do not necessarily are true because

correlation on aggregated data is not able to prove the effects of individual persons, nor it

is possible to show a casual relation. Nonetheless, if this hypothesis is indeed correct it

would be a good explanation for the rise in the natural rate of unemployment in Europe

and other industrialized nations. So, despite this first indication, the question remains

whether unemployment is also one of these perverse effects of stimulating home

ownership across OECD countries.

2.3.2 Macro Academic Research

Early work that followed to Oswald’s working paper found evidence in favor of the

hypothesis. It was confirmed with Nickell and Layard (1999) for a selection of OECD

countries and with Green and Henderschott (2001) on U.S. data. According to Rouwendal

and Nijkamp (2007) the only exception is Spain where Barrios Garcia and Rodriguez

Hernandez (2004) found the opposite across Spanish provinces because the higher home

ownership rates were associated with lower unemployment rates. Also today the

hypothesis is often confirmed on macro data: for districts in Belgium (Isebaert et al.,

2013) and across OECD countries (Blanchflower and Oswald, 2013). These macro

studies suffer, however, from aggregation bias because the relationship between

unemployment and ownership is located on the individual level, that cannot only be

proven with aggregated data. Excessive generalizations from individuals based on these

macro data are dangerous since they can be totally opposite to reality.

Nonetheless, an interesting finding on the macro level is Germany (Lerbs, 2010) for

which Oswald’s hypothesis was investigated with data of 1998 and 2006 for the

individual Bundes Staten in Germany. A first cross-sectional estimate on these regional

data did not confirm the hypothesis. Neither a significant difference was found for the

dummy between East and West Germany. The researcher argued that factors such as

participation and productivity dominate the labor markets and thus the effect of housing

tenure is marginal. However, a fixed effects panel model found little evidence in favor of

the hypothesis that could be explained by the fact that this model is able to solve a major

problem in cross-sectional research that is called unobserved heterogeneity bias. This can

be the case if for instance a specific region has proportionally more high skilled workers

who have higher chances on being owner coincided with lower chances on being

unemployed.

24

2.3.3 Micro Academic Research

Since it is hard to make conclusions for the underlying mechanisms of the correlation at

aggregated level, academics have applied micro analysis. A scrutiny on the individual

level is advantageous because it can track and unravel the behavior mechanism(s) behind

this correlation and hence is no longer suffering from aggregation bias. So again, the

question is raised: are owners more unemployed than renters? Or do they stay longer

unemployed than renters?

A common feature that is often tested is indeed the duration of unemployment. It were

Goss and Phillips (1997) who first searched for significance with housing tenure as a

explanatory variable. Contrary to the hypothesis, ownership was found to reduce the

duration of unemployment. However, the effect for mortgagors is stronger than for

outright owners. Intuitively the incentive to work is stronger for a mortgagor because he

wants to maintain the bought house. (Nijkamp and Rouwendal, 2007)

In contrast to their macro study of 2001, Green and Hendershott (2001), did only find

little evidence on U.S. micro data from the Panel Study of Income Dynamics (PSID) with

the help of hazard equations for the effect of home ownership on the employment spell.

More specific, the relation was positive but about eight times smaller than Oswalds’

indication which is a ten per cent raise in ownership the leads to a two per cent rise in

unemployment. Also Coulson and Fisher (2002) did a micro-investigation on these PSID

data. They found no evidence at all in favor of the Oswald hypothesis because their

models showed that home owners have a smaller chance on unemployment, experience a

smaller duration of unemployment and enjoy higher wages. These contradictory results to

Oswald could be explained by the fact that some variables were not taken into account,

for example the mobility of renters or the distinction between outright owners and

mortgagors that was applied before.

Nonetheless, even today the effect seems little in the U.S. as Taskin en Yaman (2012)

used micro data over a period between 1996 and 2011. They accounted for the

unobserved heterogeneity by the use of a special model that is called the full information

maximum likelihood (FIML) method. Such a model is capable of making stable estimates

even when sets have missing values. They found that ownership does indeed reduce the

job finding hazard but again at a much smaller level than Oswald’s suggestion.

In Europe, Brunet and Lesueur (2003) went through French micro data to test if the

housing tenure is able to explain the unemployment spell. Logistic results from 3965

French individuals were however not able to reject Oswald hypothesis since home

ownership was positively related to unemployment duration. Research of Ahn and

Blazques (2007) on the European Community Household Panel (ECHP) showed mixed

25

results: Spain (no), Denmark (yes), France (weak). The researchers point remarkably to

another explanation on the effect. It seems that the degree of mobility is more a result of

satisfaction with job or home. The results of Munch et al. (2006) could clearly reject the

hypothesis for the Danish people because they found that ownership lowers the

unemployment duration. The researchers instead argue that a low labor mobility may

causes unemployment and not per se the home ownership. They argue that the effect of

ownership is not relevant for countries with low labor mobility such as in most European

countries. “By contrast in the U.S. where geographical mobility is more important on the

labor market, the effect of raising ownership may lead to higher levels of

unemployment.” (Munch et al, 2006)

In the Netherlands, research was conducted to the effects of home ownership on labor

mobility. Van Leuvensteijn en Koning (2004) could not reject the hypothesis as they

concluded: "Unemployed owners seem more likely to move than unemployed tenants."

Hence, this seems logic because Netherland has a extreme high proportion of mortgagees

that – as mentioned before by Goss and Phillips – has an impact on the financial incentive

of not wanting to lose their houses. This was also confirmed in the research of Rouwendal

and Nijkamp (2007), they found that the theory is correct Oswald for owners without a

mortgage, but not for home owners with a mortgage. This incentive was also found for

Belgium by Baert et al. (2013).

The contribution to the literature of Van Leuvensteijn and De Graaff (2007) was more

broader than the hypothesis. They found that home owners have a smaller chance on

unemployment because the researchers observed lower exit rates out of the current job

spell. They argue that it is not home ownership which has a positive effect on

unemployment, but it are the transaction costs on the housing market that causes a weaker

labor mobility.

Academic literature brings up an important problem of the results of Oswald’s hypothesis

that is named endogeneity bias. This problem is typically situated in social and economic

science and can lead to a rejection of a hypothesis that in fact is true. (Reichstein, 2013)

According to the lectures of Reichstein, the bias can be summarized underlying two

important features. First, omitted variable bias can lead to endogeneity problem such as

described by Van Leuvensteijn and Koning (2004) that certain variables in the model

have limited characteristics that are indeed important for the mechanism. The example

that the authors phrase is job commitment that can explain the housing tenure of people.

This shows that certain variables could be overlooked – or omitted - when explaining

housing tenure or the general unemployment rate model of Oswald. Second, another form

of the endogeneity problem was explained by L’Horty and Sari (2010), the simultaneity

bias. That is when variables are determined simultaneously and hence it is not clear which

26

one evokes the other one. In other words, this reverse causality can be a bias of the theory

because intuitively it is not clear whether someone is (un)employed because he is a home

owner or instead the fact that home ownership makes someone (un)employed. This latter

problem can be solved by taking lagged variables that are suffering from it. This common

practice is a good attempt, but it is not completely correct (Reed, 2013).

2.4 The role of Financial Assets and Unemployment Insurance

Literature does not only link home ownership to unemployment, as there are other

variables that can be both influential to home ownership and to unemployment. A

possible variable is the role of financial assets of which less is known in literature. For

instance, Frantantoni (1998) linked housing tenure with the relative weight of investments

in risky assets. First he showed that the average home owner has a higher amount of

financial asset than the average renter. Second, he found that a mortgage commitment is

associated to reduced risky assets holdings. Also Becker and Shabani showed that

mortgagors are 10 per cent less likely to own stocks or 37 per cent less likely to own

bonds. (Becker and Shabani, 2010) This may be a possible link in the Oswald theory.

Such a financial wealth itself may be an incentive to longer unemployment spells as it can

be consumed during the unemployed period. Gruber (2002) found that the wealth of the

unemployed population is quite diverse as it undertakes a substantial heterogeneity,

especially when measured at the start of the unemployed period. His micro data of the

1980s and 1990s were very extreme as one-third of the American workers was not even

able to replace 10 per cent of their income loss. In this paper Gruber also refers to Baily

(1978) who argued that the optimal level of unemployment insurance for a worker should

be in function of the private resources that this person can consume during the

unemployment spell. This is, in our opinion, a possible incentive for outright owners to

have longer unemployment spells because they were found to be associated with higher

financial assets, especially with higher financial risky assets.

Another relevant finding in this story is that generous unemployment insurance benefits

can undermine labor mobility. Feldstein (1973) for instance argued that indeed

unemployment insurance was responsible for a rise in unemployment rate. However, he

also found that a lot of the benefit receivers were not located especially low in the income

distribution. In this optic the Oswald theory may be specifically located with unemployed