On the Brink

31

Inside Out Andrew Duguid DOI: 10.1057/9781137299307.0006 Palgrave Macmillan Please respect intellectual property rights This material is copyright and its use is restricted by our standard site license terms and conditions (see palgraveconnect.com/pc/connect/info/terms_conditions.html). If you plan to copy, distribute or share in any format, including, for the avoidance of doubt, posting on websites, you need the express prior permission of Palgrave Macmillan. To request permission please contact [email protected].

-

Upload

palgrave-macmillan-professional-business -

Category

Documents

-

view

241 -

download

1

description

Andrew Duguid

Transcript of On the Brink

Inside OutAndrew DuguidDOI: 10.1057/9781137299307.0006Palgrave Macmillan

Please respect intellectual property rights

This material is copyright and its use is restricted by our standard site license terms and conditions (see palgraveconnect.com/pc/connect/info/terms_conditions.html). If you plan to copy, distribute or share in any format, including, for the avoidanceof doubt, posting on websites, you need the express prior permission of PalgraveMacmillan. To request permission please contact [email protected].

It was the best of times, it was the worst of times ... it was the spring of hope, it was the winter of despair, we had everything before us...

Charles Dickens, A Tale of Two Cities

1

INS IDE OUT

10.1057/9781137299307 - On the Brink, Andrew Duguid

Co

pyr

igh

t m

ater

ial f

rom

ww

w.p

alg

rave

con

nec

t.co

m -

lice

nse

d t

o P

alg

rave

Mac

mill

an -

Pal

gra

veC

on

nec

t -

2014

-08-

20

ON THE BRINK2

At an Extraordinary Meeting of Lloyd’s members held in London’s Royal Albert Hall in May 1993, a retired Englishman moved towards the micro-

phone. After commending the efforts of the new Chairman and Chief Executive, he said: ‘A man’s word is his bond, but it no longer is at Lloyd’s. There are 30 Names who have taken their own lives. Sir, with your permission, I want to have one minute’s silence.’

There were good grounds for disputing the number and the cause of these suicides. The Chairman simply added: ‘We should include in that minute all those who are facing problems with which they feel they cannot deal.’ Several thousand members bowed their heads.

***

Seven years earlier, all seemed well as Queen Elizabeth II opened Lloyd’s gleam-ing new stainless steel building in the heart of the City of London’s financial district. There had been scandals, but they were being dealt with. The new, multi-storey trading floor was a hive of activity. A huge expansion in member-ship was still underway. A new Council was busy making new rules, empowered by its own Act of Parliament. The Chairman, Peter Miller, was articulate, ener-getic and very bullish.

Coping with disasters is what an insurance marketplace is for: fires, earth-quakes, hurricanes, plane crashes and acts of terrorism. For decades, most of the several hundred syndicates at Lloyd’s were insuring these and other risks and declaring profits to their members. But soon after moving to futuristic premises, problems from the past began to emerge. These were much more gradual and insidious than an earthquake. Some were quicker than others to notice these trends. By 1991, nearly everyone was getting worried, angry or both.

Members of Lloyd’s were known as Names because their names were origi-nally listed at the bottom of the insurance policies they supported – ‘under-writ-ten’. In the early 1990s, many Names found that instead of receiving a cheque, they were asked to write one. Demands for cheques increased. Disappointment soon turned to anger. The men who ran Lloyd’s were at first unable to grasp or solve the crisis. New leadership was badly needed.

Outwardly, Lloyd’s seemed a respectable, settled institution, fixed in its ways, with a long history and shared values. But inside, on the trading floor – known as ‘the Room’ – it was a hothouse of changing fortunes. Its market players included real experts, weaker elements, a few rebels, the odd crook, con-formists, contrarians, innovation and opportunity. Individualism1 was a creed.

By contrast, its outside Names had little in common and almost no idea of what went on within. Under pressure of big losses, they turned out to contain a

10.1057/9781137299307 - On the Brink, Andrew Duguid

Co

pyr

igh

t m

ater

ial f

rom

ww

w.p

alg

rave

con

nec

t.co

m -

lice

nse

d t

o P

alg

rave

Mac

mill

an -

Pal

gra

veC

on

nec

t -

2014

-08-

20

INS IDE OUT 3

range of talents. Normally passive, Names found new ways of working together to protect their interests: all kinds of self-help groups sprang to life. Their story is as compelling as the changes in how Lloyd’s was run, and the character of their leaders every bit as critical.

Before the story can be told, the institution and its people must be intro-duced. The rest of this chapter describes Lloyd’s to those not acquainted with it. Most Names had no detailed understanding of the insurance business, nor is this required of the reader. Technical language is kept to a minimum.

THE TRADERS

Trust – confident belief in or reliance on the character of somebodyHonour – a fine sense of and strict allegiance to what is due or right

The market began in Edward Lloyd’s coffee house, frequented by sea captains, ship-owners and merchants. Marine insurance was first transacted there around 1688: some merchants would offer to reimburse ship-owners for the loss of their ships and cargoes on a particular voyage, in return for a premium. Over the next 100 years, Lloyd’s, and London too, became pre-eminent in the shipping world. The market branched out to insure against fire, theft and many other hazards. Representing all sorts of worldwide clients, Lloyd’s brokers shopped around, buying tailor-made insurance policies from many specialist underwriters.

Originally, these underwriters took on risks exclusively for themselves. Later they formed syndicates that included others – family and close associ-ates at first – who put their wealth at risk in the hope of earning a profit. These Names played no active part in underwriting. Normally, they were quiescent silent partners.

Over more than three centuries of trading, Lloyd’s has seen good times and bad. The market gained a reputation for innovation and solid security, espe-cially in America after a dramatic response to the San Francisco earthquake in 1906: ‘Pay all claims in full, irrespective of the terms of their policies’, said the telegram from legendary Lloyd’s underwriter Cuthbert Heath, in many ways the father of Lloyd’s in the twentieth century, to his local agent.

As it grew, the Lloyd’s market moved eight times. Its latest home is striking. An innovative architect, Richard Rogers, won the competition to design it with a flexible concept, not a drawing. Often described as inside-out, it is like a glass and concrete cathedral on the inside, with trading floors stacked vertically, linked by conspicuous escalators. Outside are all the services – pipes, staircases and glass elevators. To celebrate the official opening, an entire vintage of Veuve Clicquot champagne was acquired.

10.1057/9781137299307 - On the Brink, Andrew Duguid

Co

pyr

igh

t m

ater

ial f

rom

ww

w.p

alg

rave

con

nec

t.co

m -

lice

nse

d t

o P

alg

rave

Mac

mill

an -

Pal

gra

veC

on

nec

t -

2014

-08-

20

ON THE BRINK4

Every day, thousands of brokers poured onto the new trading floors to strike deals with underwriters at their boxes, as their desks were known. The noise and bustle rose to a crescendo by late morning. At the rostrum in the centre of the room, with the glass atrium rising 12 floors above it, a waiter (so-called due to Lloyd’s coffee-house origins) announced a stream of messages. The brokers car-ried heavy leather slipcases with information about the ‘risk’ their clients wanted to insure – a factory, an oil rig or a group of doctors’ liabilities. Each risk was summarised on a paper ‘slip’. With a speed reflecting the level of trust between the parties, contracts were often quickly agreed after a brief, sometimes jaunty, exchange of words.

Much store was – and still is – set by the face-to-face encounter between broker and underwriter. They meet each other often – socially as well as in the Underwriting Room. The broker’s job is to get the best terms for his cli-ent; the underwriter tries to strike a deal that will make a profit for his syn-dicate. The two parties can often agree on contracts that serve both interests. That is the essence of any market.

Buying and selling insurance is unlike trading goods or everyday shop-ping. For a modest premium of a few hundred pounds, an insurer may be required to pay out millions of pounds in compensation to an accident victim. An underwriter takes on many contracts, expecting to pay large claims rarely. Normally he, in turn, insures his syndicate against unusual losses; this is called

Picture 1 The trading floor at Lloyd’s, known as the Room. Reproduced by per-mission of Lloyd’s

10.1057/9781137299307 - On the Brink, Andrew Duguid

Co

pyr

igh

t m

ater

ial f

rom

ww

w.p

alg

rave

con

nec

t.co

m -

lice

nse

d t

o P

alg

rave

Mac

mill

an -

Pal

gra

veC

on

nec

t -

2014

-08-

20

INS IDE OUT 5

reinsurance. If his claims are bigger than expected, he will be reimbursed by his reinsurer to the extent agreed in their contract.2 London – including both Lloyd’s and nearby insurance companies – is a world centre for buying and selling insurance and reinsurance. Relationships among insurers are complex: they may compete with each other for business; they may share in big risks; and they may reinsure one another. At Lloyd’s, all these transactions are done through brokers.

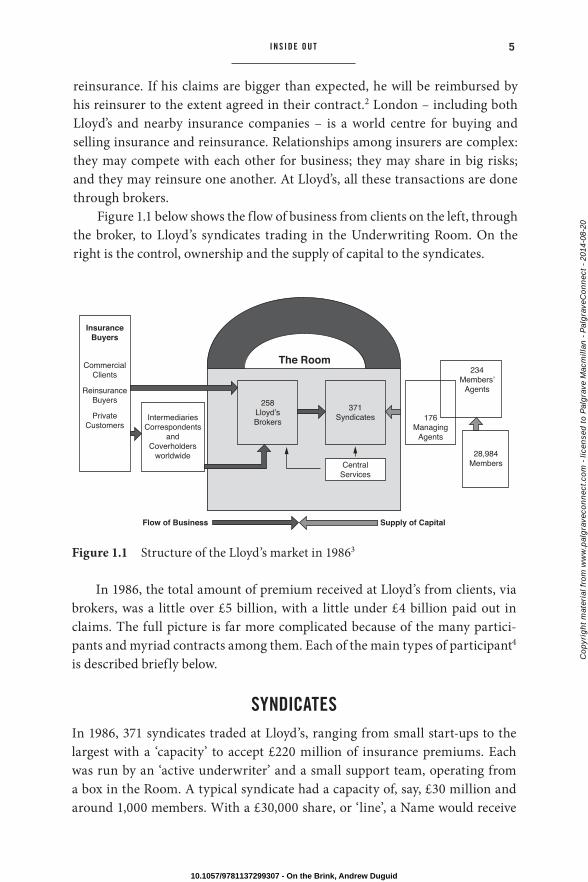

Figure 1.1 below shows the flow of business from clients on the left, through the broker, to Lloyd’s syndicates trading in the Underwriting Room. On the right is the control, ownership and the supply of capital to the syndicates.

InsuranceBuyers

CommercialClients

ReinsuranceBuyers

PrivateCustomers

IntermediariesCorrespondents

andCoverholders

worldwide

258Lloyd’sBrokers

371Syndicates

CentralServices

176Managing

Agents

234Members’

Agents

28,984Members

The Room

Flow of Business Supply of Capital

Figure 1.1 Structure of the Lloyd’s market in 19863

In 1986, the total amount of premium received at Lloyd’s from clients, via brokers, was a little over £5 billion, with a little under £4 billion paid out in claims. The full picture is far more complicated because of the many partici-pants and myriad contracts among them. Each of the main types of participant4 is described briefly below.

SYNDICATES

In 1986, 371 syndicates traded at Lloyd’s, ranging from small start-ups to the largest with a ‘capacity’ to accept £220 million of insurance premiums. Each was run by an ‘active underwriter’ and a small support team, operating from a box in the Room. A typical syndicate had a capacity of, say, £30 million and around 1,000 members. With a £30,000 share, or ‘line’, a Name would receive

10.1057/9781137299307 - On the Brink, Andrew Duguid

Co

pyr

igh

t m

ater

ial f

rom

ww

w.p

alg

rave

con

nec

t.co

m -

lice

nse

d t

o P

alg

rave

Mac

mill

an -

Pal

gra

veC

on

nec

t -

2014

-08-

20

ON THE BRINK6

one-thousandth of this syndicate’s profits or losses. Some had bigger or smaller shares. The underwriter was always a member of his own syndicate.

In the Room, each risk is first offered to a ‘leading’ underwriter, who may agree a price and take a share of the risk. Other syndicates are then invited to take further shares as ‘followers’.5 The ‘leader’ negotiates with the broker over the price, terms and conditions of the policy, and plays the main role in settling any claims. There is kudos in being a successful leader. Followers watch the results of leaders very closely. Dealing is brisk, as there are thousands of brokers, with plenty of slips, and hundreds of underwriters. News, rumours, gossip and jokes travel around the Room with astonishing speed. At lunchtime, the Room empties completely and all the nearby pubs and restaurants are crowded with these traders and their teams.

An insurance buyer normally knows more about his risks than the seller. For example, a car owner knows more about its state and his own family’s driv-ing habits than his insurer. In the same way, a direct insurer knows more about what he has covered than his reinsurer can possibly know. That is why, under insurance law, a buyer and his broker are required to tell the underwriter, in good faith,6 what they know about the risk for which they seek cover, otherwise the transaction would be unreasonably one-sided. If the broker misleads the underwriter, the contract is void, but if he deals regularly with him, the under-writer will rely on him for truthful information. The broker, in turn, will be fairly confident that when his client’s claims arise, they will be paid promptly, without too many quibbles. Relationships are built up over many years of trad-ing in the Room.

Brokers and underwriters were often introduced through a family connec-tion, and came from a variety of social backgrounds: public schools,7 grammar schools and those with less cultivated accents who had left school at 16. Colin Murray, who joined as a broker after a spell in the Army, saw variety as a source of strength: ‘It was a complete mix of men of every background. In the market I couldn’t give a damn if a chap was at grammar school, a bog-standard compre-hensive, or Eton, it made no difference to me. People were aware that some had large estates and others lived in the East End, but in the market it didn’t mat-ter.’ Murray spent ten years as a broker, ten as a deputy underwriter, ten as the ‘active’ underwriter of ‘Syndicate 510’ and finally ten years as the Chairman of his managing agency, Kiln. Like many agencies, it bears the name of its founder, in this case, Murray’s mentor, Robert Kiln.

Learning was by doing. In the 1980s, few underwriters had undergone for-mal professional training. Not many were university graduates. Most had started out young, often in a clerical role – either at the box or with a broking firm. Some had family connections. A few aspiring underwriters took Chartered Insurance

10.1057/9781137299307 - On the Brink, Andrew Duguid

Co

pyr

igh

t m

ater

ial f

rom

ww

w.p

alg

rave

con

nec

t.co

m -

lice

nse

d t

o P

alg

rave

Mac

mill

an -

Pal

gra

veC

on

nec

t -

2014

-08-

20

INS IDE OUT 7

Institute courses and examinations in their spare time to become Associates (ACII) or Fellows (FCII). Introduced to the Lloyd’s market by his brother, Bryan Kellett first worked for a broker. A grammar-school product without a univer-sity degree, he looked for an edge over his contemporaries. He heard about ACII qualifications, studied, took the Part 1 exams, and won the Institute prize. On the strength of this, he was offered his first job on a Lloyd’s underwriting box. Soon he became a leading underwriter. Eventually, he secured broker support for set-ting up his own syndicate. Later he became President of the Chartered Insurance Institute, Chairman of the Lloyd’s Underwriters Non-Marine Association (LUNMA or NMA) and was elected to the governing Council of Lloyd’s.

Most underwriters specialised in certain kinds of business. Although what they knew had been learned on the job, rather than through studies, the accu-mulated expertise of the best was formidable. Some leaders built worldwide reputations for their in-depth knowledge, sometimes of esoteric subjects. Hugh Jago was said to know more about Chicago’s drains than the city authority itself, having insured them for 20 years. Tony Medniuk knew the safety records, cul-tures and procedures of the world’s leading airlines. At the other end of the spectrum, some underwriters were completely out of their depth, entering fields for which they were unqualified by intellect or experience.

Knowledge was one route to success. Another was flexibility. It was a matter of pride that practically any risk could be underwritten at Lloyd’s, including the legs of an actress or a wine-taster’s nose, or pioneering on the frontier of tech-nology through oil exploration rigs, satellites or nuclear energy. Underwriters were open to persuasion to look at something new or in a new way, often citing the old maxim: ‘There’s no such thing as a bad risk, only a bad rate.’ In this spirit, new kinds of insurance contract were invented. Varying in size and char-acter, Lloyd’s syndicates were generally small enough for one man to exercise tight control over the business. Some were collegiate, holding a team meeting to review each day’s trading, sharing information and instilling a collective sense of responsibility for performance. Others were run more secretively: one under-writer would not allow his deputy to see the claims record of the business he wrote. Some did not allow the use of first names. In 1986, very few employed women.

MANAGING AGENTS

Underwriters are employed by firms called managing agents. Like lawyers, under-writers are notoriously hard to manage; those who have tried it often liken it to herd-ing cats. The job requires an independence of mind that resists interference. Some were dominant personalities within their own firm. Robert Kiln was chairman

10.1057/9781137299307 - On the Brink, Andrew Duguid

Co

pyr

igh

t m

ater

ial f

rom

ww

w.p

alg

rave

con

nec

t.co

m -

lice

nse

d t

o P

alg

rave

Mac

mill

an -

Pal

gra

veC

on

nec

t -

2014

-08-

20

ON THE BRINK8

of the managing agency he founded, and its chief underwriter until 1974, when he handed that role to Colin Murray. When he stepped down, the Kiln agency ran seven syndicates. Stephen Merrett doubled as the agency chairman and chief underwriter for the Merrett group, in which he was also the largest shareholder.

When Robert Hiscox took over his father’s managing agency, Hiscox, it was small and precarious. It had suffered while his father, Ralph, had given prior-ity to his other role as Chairman of Lloyd’s. Robert says: ‘We had lost money for five years running. We had only 17 Names, and were frightened of every handwritten letter we received, in case it was a resignation.’ He built a team in which each member focused on particular areas and encouraged brokers to join his syndicate. He found that: ‘If I said “no” to a broker a lot, he backed me. That strengthened my resolve to underwrite sensibly.’ His Syndicate 33 gained in reputation; with good results and low fees, it built a following among working Names. When he retired in 2013, Hiscox Ltd had an annual turnover exceeding £1.6 billion and an enviable reputation.

Another large managing agency, Sturge, had been acquired from its found-ing family. It was built up by David Coleridge and Ralph Rokeby-Johnson and floated as a public company. Merrett planned to float too, but a few years later it sank. At one stage there was concern in the market about the growing domi-nance of these two agencies. Ten years later, both were gone. From 1986 to 1996, the fortunes of the top agents and syndicates8 were transformed. Others took the place of the biggest. Historically, many agents had been owned or control-led by brokers. But in 1982, concern about conflicts of interest led the British Parliament9 to require brokers to sell their stakes in managing agencies. This was called compulsory divestment.10

LLOYD’S BROKERS

Only accredited Lloyd’s brokers can enter the Room. Most did not trade exclu-sively with Lloyd’s syndicates, but also with insurance companies – some domestic, many foreign-owned – operating in the nearby district. The bigger brokers brought around 40 per cent of their business to Lloyd’s. A large brok-ing firm contained many specialist divisions: reinsurance and direct business; North American and other continents; marine and non-marine; liability and property and so on. Smaller brokers specialised in fewer fields. Most risks origi-nated overseas and were first handled by a local broker based near the original client. The client paid a commission to its local broker and to the London broker with access to Lloyd’s.

The US was the biggest overseas market for Lloyd’s, providing around one-third of its business. The larger American brokers disliked sharing

10.1057/9781137299307 - On the Brink, Andrew Duguid

Co

pyr

igh

t m

ater

ial f

rom

ww

w.p

alg

rave

con

nec

t.co

m -

lice

nse

d t

o P

alg

rave

Mac

mill

an -

Pal

gra

veC

on

nec

t -

2014

-08-

20

INS IDE OUT 9

commission. In the 1970s and 1980s, they wanted to own brokers in London. At first rebuffed, eventually their offers were too much to resist. After a long courtship and a failed hostile takeover, Marsh & McLennan bought C.T. Bowring, the second-largest London broker, in 1980. Several Bowring brokers left to set up their own businesses. Alexander & Alexander’s acqui-sition of Alexander Howden uncovered a scandal, which is discussed later. Willis Faber – the largest marine broker in London – eventually merged with another US company to form Willis Corroon. Sedgwick grew to be the largest British-owned broker.11

The leading figures among the brokers were all members of Lloyd’s and were well-known there. A few became involved in running it: Peter Miller, Chairman of T.R. Miller, was Chairman of Lloyd’s for four years from 1984. David Rowland, Chairman of Stewart Wrightson, later Sedgwick, was first elected to the Council of Lloyd’s for 1987–90. Other brokers became deputy chairmen. Philip Wroughton, Chairman of Marsh UK, was elected to the Council in 1991. The Lloyd’s Insurance Brokers’ Committee (LIBC), a powerful trade association, concerted brokers’ views, making sure Lloyd’s knew them. Lloyd’s rules required all transactions to involve a broker, paid by commission or fee, even when one syndicate was reinsuring another. These arrangements were vigorously defended through the LIBC, whose members preferred Lloyd’s as their regulator. Lloyd’s was – and still is – seen as the quintessential brokers’ market.

Traders in the Room are very observant. Some brokers are seen as the big beasts of the jungle, looking out for prey. Others are smaller and less colour-ful; some are thought sneaky. The slightest signal is noticed: a lowered tone of voice, unusual body language. When they engage with an underwriter, there are outward rituals to be observed. Negotiation is something of a contest, framed within well-understood conventions. The broker often begins by addressing the underwriter as ‘Sir’, sometimes a little theatrically. Information is exchanged and evaluated. Decisions are often reached quickly. Once made, they are always adhered to. The story is told of a broker who queued late one afternoon to see a well-known underwriter, who had to leave just before a deal could be negoti-ated. That night the vessel sank. The next morning, the broker explained his dilemma. The underwriter looked him in the eye and asked for a categorical assurance that he had been in the queue. On receiving this, he said he would write it, back-dating it to the time at which he would have written it the night before. The ship was covered and the claim was paid. This was described to the author as ‘Old Lloyd’s at its best’.

***

10.1057/9781137299307 - On the Brink, Andrew Duguid

Co

pyr

igh

t m

ater

ial f

rom

ww

w.p

alg

rave

con

nec

t.co

m -

lice

nse

d t

o P

alg

rave

Mac

mill

an -

Pal

gra

veC

on

nec

t -

2014

-08-

20

ON THE BRINK10

Underwriters need to concentrate hard. A day in the Room can be exhausting. A single unwise decision on a big risk can have massive consequences. Some people had enviable reputations: their stock could rise and fall, usually built up over many years of consistent trading, patiently developing in-depth knowledge and making steady profits. Some people had reputations as weaker elements; a few were known to display less judgement after a good lunch. A few underwrit-ers made excellent mentors. Andrew Beazley and Bryan Kellett were trained by Charles Skey, widely regarded as one of the market’s best. But in the absence of proper qualifications, dodgy or indifferent underwriters also tended to replicate themselves. One was nicknamed the ‘Nodding Donkey’ because he always said yes. The result was inevitable.

Dealings between brokers and underwriters were not just a matter of knowl-edge or technique. One senior figure says he had to choose between two talented underwriters. He selected the taller, on the grounds that when an important broker came to the box, it was necessary to stand up and not be dominated. Another describes the engagement as a bit like a game of rugby or contesting barristers in the adversarial system – ‘very British’.

Underwriters and brokers each employ specialists, like claims-handlers, who work closely with outside lawyers and loss adjusters based in Britain, the US and elsewhere. The pugnacious Jim Teff, for example, Head of Claims for Janson Green, trained as a lawyer and became a recognised market expert on US liabilities. Chris Ventiroso, Claims Director at Murray Lawrence and Partners, trained as a reinsurance specialist. Efficient claims adjustment and payment forms an important part of the market’s reputation. Because many syndicates share in each risk, co-ordination across the market is usually needed.

Claims issues can sometimes be contentious. Where a conflict may exist, a claims broker acts as the agent of the insured client. His dealings with leading claims-handlers are a bit like those between a broker and an underwriter: a con-test between professionals, framed by conventions. A claims man (or woman) who flouts the norms will quickly acquire a bad reputation. Other professionals play key roles at Lloyd’s: accountants, lawyers, IT specialists and so on. Many non-professional support roles outside the room – secretarial and clerical – brought employment in the Lloyd’s market to around 30,000 in the 1980s.

THE NAMES

Who were the people that joined as Lloyd’s members, usually as silent partners? The terms ‘members’ and ‘Names’ are interchangeable. Those who worked in the market, called working Names, comprised around 15 per cent of all mem-bers in 1986. Generalisations about Names are dangerous: no two person’s

10.1057/9781137299307 - On the Brink, Andrew Duguid

Co

pyr

igh

t m

ater

ial f

rom

ww

w.p

alg

rave

con

nec

t.co

m -

lice

nse

d t

o P

alg

rave

Mac

mill

an -

Pal

gra

veC

on

nec

t -

2014

-08-

20

INS IDE OUT 11

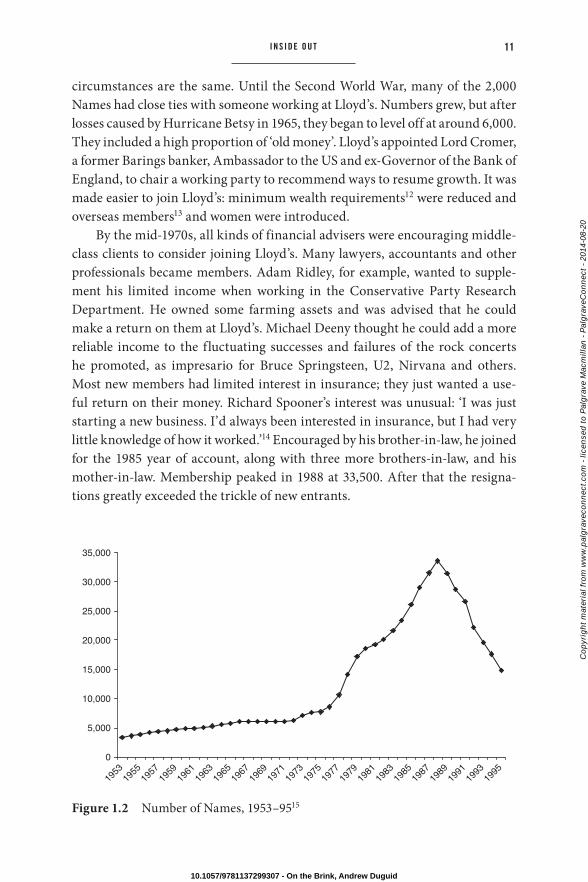

circumstances are the same. Until the Second World War, many of the 2,000 Names had close ties with someone working at Lloyd’s. Numbers grew, but after losses caused by Hurricane Betsy in 1965, they began to level off at around 6,000. They included a high proportion of ‘old money’. Lloyd’s appointed Lord Cromer, a former Barings banker, Ambassador to the US and ex-Governor of the Bank of England, to chair a working party to recommend ways to resume growth. It was made easier to join Lloyd’s: minimum wealth requirements12 were reduced and overseas members13 and women were introduced.

By the mid-1970s, all kinds of financial advisers were encouraging middle-class clients to consider joining Lloyd’s. Many lawyers, accountants and other professionals became members. Adam Ridley, for example, wanted to supple-ment his limited income when working in the Conservative Party Research Department. He owned some farming assets and was advised that he could make a return on them at Lloyd’s. Michael Deeny thought he could add a more reliable income to the fluctuating successes and failures of the rock concerts he promoted, as impresario for Bruce Springsteen, U2, Nirvana and others. Most new members had limited interest in insurance; they just wanted a use-ful return on their money. Richard Spooner’s interest was unusual: ‘I was just starting a new business. I’d always been interested in insurance, but I had very little knowledge of how it worked.’14 Encouraged by his brother-in-law, he joined for the 1985 year of account, along with three more brothers-in-law, and his mother-in-law. Membership peaked in 1988 at 33,500. After that the resigna-tions greatly exceeded the trickle of new entrants.

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

1953

1955

1957

1959

1961

1963

1965

1967

1969

1971

1973

1975

1977

1979

1981

1983

1985

1987

1989

1991

1993

1995

Figure 1.2 Number of Names, 1953–9515

10.1057/9781137299307 - On the Brink, Andrew Duguid

Co

pyr

igh

t m

ater

ial f

rom

ww

w.p

alg

rave

con

nec

t.co

m -

lice

nse

d t

o P

alg

rave

Mac

mill

an -

Pal

gra

veC

on

nec

t -

2014

-08-

20

ON THE BRINK12

MEMBERS’ AGENTS

Each member was looked after by his members’ agent, a little like having a per-sonal stockbroker, on whom he would rely heavily for guidance in the arcane ways of Lloyd’s. Some were flamboyant characters. John Donner, for example, toured Australia and New Zealand in a Rolls Royce, a signal that one could do well out of Lloyd’s. He recruited John Stace, an enthusiastic New Zealander, who eventually moved to Britain, fell out with Donner and established his own members’ agency, Stace Barr. Robin Kingsley ran the Lime Street members’ agency. The son of a stock-broker, he first worked as a junior on a marine underwriting box, then became a broker before his role as an agent. He had strong connections with the world of ten-nis, first approaching some tennis stars, it was said, in the changing-room baths.

In the 1980s, John Gordon ran one of the largest members’ agencies, Sedgwick, owned by one of the big brokers. Respected as thoughtful, ethical and considerate, Gordon did charity work at weekends in his native Dublin. He wore a small cross on his lapel, giving him a slightly priestly quality. Nigel Hanbury was a serving soldier when his father said he should become a member of Lloyd’s and gave him the money to do it. He joined at 21, the minimum age. Profits began to flow and he thought: ‘I’m getting cheques bigger than my salary, I’d bet-ter become a broker myself.’16 A few years later, after working for two large bro-kers, he joined Sturge and ‘learned the ropes about how to be a members’ agent’. He made many six-week business trips to the US, where he ‘travelled to various cities seeing a great many people. I did the mid to west coast, we would go out to our various stations where introducers would line up suitable people. You’d talk them through it. If they wanted to take it further, they would have to fly over here [to London] and do their verification meeting, and have it all explained. The introducers were generally highly respected people in their communities’.

Before 1960, managing agents dealt with their own Names, who were allowed only one agent for each main class of business. The role and number of specialist members’ agents grew in the 1970s in line with the growth of the membership. Some were independent, while others were owned by managing agents or by brokers. By 1982, there were 270 members’ agents.17 They began to consolidate: ten years later, there were 83 and by 2013, there were only three.

Some members’ agents came clean about the risks; others were much less forthright. Some were later accused of being downright misleading. When one Name asked about the impact of a catastrophe, he was told it was ‘only a gin and tonic’. By contrast, Peter Green, for emphasis, used to ask a prospective member to get out his cheque book, sign a cheque, made out to him, leaving the amount and date blank. He tucked it in his shirt pocket and said that was what member-ship of Lloyd’s amounted to. This was highly unusual.

10.1057/9781137299307 - On the Brink, Andrew Duguid

Co

pyr

igh

t m

ater

ial f

rom

ww

w.p

alg

rave

con

nec

t.co

m -

lice

nse

d t

o P

alg

rave

Mac

mill

an -

Pal

gra

veC

on

nec

t -

2014

-08-

20

INS IDE OUT 13

JOINING UP

Outside Lloyd’s, Names were often inaccurately described as investors. Each was a ‘sole trader’, carrying on the business of insurance. All sole traders have unlimited liability; it was not unique to Lloyd’s. It is the historic form of trading, still used today by barristers and by many other professionals then. The combi-nation of insurance, with its potential for big claims, and unlimited liability was to prove disastrous for many Names.

From 1978 onwards, each new member was required to sign a ‘verification’ form,18 confirming that he had understood the key features of membership, including unlimited liability and a warning that losses could be made. This was first introduced on the advice of Lloyd’s perceptive US General Counsel, who believed it would ‘reduce the risk of disgruntled US members bringing private lawsuits against their underwriting agents under the US Securities Act of 1933’. The influence of US laws and customs on Lloyd’s is a recurring theme in this story. Names’ agency agreements with their agents provided for disputes to be subject to English law in English courts or London arbitration. From 1986, it became a condition of underwriting for all Names to sign an agreement with Lloyd’s, the General Undertaking, whereby they agreed that any dispute in con-nection with their membership or underwriting at Lloyd’s should be decided in the English courts subject to English law. Years later, some US Names fought repeatedly for a US court hearing, arguing that their rights as US citizens had been violated.

Picture 2 Intended to impress: the Adam Room at Lloyd’s. Reproduced by per-mission of Lloyd’s

10.1057/9781137299307 - On the Brink, Andrew Duguid

Co

pyr

igh

t m

ater

ial f

rom

ww

w.p

alg

rave

con

nec

t.co

m -

lice

nse

d t

o P

alg

rave

Mac

mill

an -

Pal

gra

veC

on

nec

t -

2014

-08-

20

ON THE BRINK14

The admission process led to a ‘Rota’ interview with a Lloyd’s elder states-man. Each new member dressed smartly for this important occasion, held in the Adam Room, an elaborate eighteenth-century masterpiece. Intended to impress, it had been transplanted from an historic English country house into Lloyd’s modern buildings. The interview acted as a check that the individual had been properly informed about Lloyd’s and the risks and responsibilities he was about to take on. Lloyd’s set much store by this safeguard; even overseas members were required to attend in person. Only a tiny handful of exceptions were made for those physically unable to make the trip. Toby Jessell was a busy MP who nearly became a member in 1988. He had signed all the papers when invited to his Rota interview. He felt it unnecessary and could not spare the time. When Lloyd’s insisted, he suggested a Deputy Chairmen should visit him in the House of Commons instead. Lloyd’s would not depart from procedure. Jessell considers himself to have had a lucky escape.

In December 1986, after much delay, Lloyd’s published Membership: The Issues,19 setting out the risks very explicitly. By then, the great boom in membership was nearly over. Years afterwards, insiders recalled the warnings given at Rota interviews as clear, solemn and unmistakable. Some Names recalled the interview very differ-ently, saying their agent had winked at them, plied them with wine beforehand and generally made light of the procedure. Some claimed it had been hard to take seri-ously the ‘old buffoon’ who conducted it: he was just ‘going through the motions’.

Diana Wallace was one of a dozen20 at her Rota interview in 1984. Later, in a letter, she recalled the moment when the ‘Very Important kind of Beak Person’ from the Lloyd’s hierarchy explained matters and invited questions. She had the temerity to ask if membership ‘could involve forfeiture of all one’s earthly treasures – pic-tures, books, furniture, bits and bobs generally, and just about everything one holds dear?’ ‘Who is this lady?’, came the response. Her agent spoke up. The elder states-man said: ‘I think, Mrs Wallace, your interests will be well attended.’ No more was said. Afterwards she received a ‘wounded and rather indignant telephone call’ from her agent, who told her that it was ‘unheard of’ for a Name to question the VIP and that it had not been a very clever thing to do. ‘Silly me’ she wrote, eight years later, facing huge losses, ‘at least I made some attempt to fly the flag of sporting challenge over the unnerving scene of my decimation.’ She wrote to suggest that ‘this form of mesmeric intimidation’ might in future be ‘less of an admonitory lecture and more of a helpful exchange’. She said the pomp and mystique ‘made even the agents quite jumpy, as though it was Prize-Giving Day’ and totally overcame its purpose of con-veying a clear understanding of the commercial venture involved. Another member who joined eight years later said it felt a bit like going to church: ‘We might as well have been at Buckingham Palace, I could not have felt more reassured.’

10.1057/9781137299307 - On the Brink, Andrew Duguid

Co

pyr

igh

t m

ater

ial f

rom

ww

w.p

alg

rave

con

nec

t.co

m -

lice

nse

d t

o P

alg

rave

Mac

mill

an -

Pal

gra

veC

on

nec

t -

2014

-08-

20

INS IDE OUT 15

At the final stage of ‘election’ to membership, the list of prospective Names went to the Committee of Lloyd’s for approval. A mahogany box was carried around the table by a waiter. Each Committee member voted by solemnly plac-ing a white marble through a hole in the box, where it fell with a loud clatter. Very occasionally, a new member was turned down – or blackballed – because some previous dealings had cast doubt on his reliability. Almost invariably, though, the balls were dropped into the slot marked ‘yes’, meaning that another batch of Names were formally admitted and on the hook, for better or worse.

The Rota interview also checked that the prospective Name had understood how past liabilities were dealt with at Lloyd’s.21 Intense debate surrounded this later: many Names claimed never to have understood it. You could inherit lia-bilities written long before you joined. They could follow you to the grave and beyond. Few Lloyd’s members – even insiders – understood just how unending and lethal these could be. Unlike a shareholder in a conventional company, the new member’s liability was unlimited: everything he or she owned was now at risk.

People were encouraged to think of Lloyd’s membership as a long-term commitment, the very opposite of making a quick gain. New members had to be patient. Historically, Lloyd’s insurance of ships and cargoes involved long sea journeys; as a result, it could take time before the extent of any losses was known. Lloyd’s operated a unique accounting system: each syndicate’s year of account remained ‘open’ until three years had elapsed. Only then was the profit or loss determined. As Lloyd’s business broadened, this accounting system was also used for other insurance categories, like fire, property and theft. But where liabilities22 are insured, it can take much longer than three years for the true value of claims to emerge.

Liabilities reflect the duties that people and firms owe each other. All driv-ers are required to have liability insurance, so that an accident victim can be adequately compensated, no matter how impecunious the driver who hits them. In a complex society, insuring liabilities is big business. Compensation levels are often established by court judgments or compromised on the courtroom steps, and can take many years to be sorted out. The 25,000 Names who joined Lloyd’s during two decades of growth did not realise that a time-bomb of ‘latent’ liabilities was quietly ticking in the US.

SYNDICATE SELECTION

It was often said that a Name’s most important decision was his23 choice of mem-bers’ agent. A few Names met several and chose carefully, but many met only

10.1057/9781137299307 - On the Brink, Andrew Duguid

Co

pyr

igh

t m

ater

ial f

rom

ww

w.p

alg

rave

con

nec

t.co

m -

lice

nse

d t

o P

alg

rave

Mac

mill

an -

Pal

gra

veC

on

nec

t -

2014

-08-

20

ON THE BRINK16

one, often through a relative or a personal adviser. They did not realise that com-mission was often paid for these referrals. For many people, inexperienced in the ways of the City or Lloyd’s, it would have been awkward to ask to meet other agents. They were grateful to have met one at all; he seemed personable and helpful. Many felt flattered or lucky to have been approached. They were driven on by very high tax rates on income earned elsewhere and the prospects of good returns at Lloyd’s, encouraged by their new best friend.

Names depended on their members’ agent to find their syndicates. This would determine their fate: like the game of Snakes and Ladders, you could mount a financial ladder and do well, or climb on the back of a long slippery snake, from which it could become impossible to escape. Each members’ agency had its own approach. If part of a ‘combined’ agency,24 like Sturge, the new Name’s portfolio would start with the ‘in-house’ syndicates, operated by the group. An independent or broker-owned members’ agent would have estab-lished relationships, providing Names to syndicates they knew well. There were many complaints from new Names about access to the more profitable syndicates. A balanced portfolio would include lower-risk syndicates to offset the riskier ones. But some Names, including those joining through Kingsley’s Lime Street Agency, found themselves with a ruinous concentration of high-risk business.

Some agents took care to introduce the new member to his prospective underwriters. New members tried to assess their characters on the basis of these brief encounters. Occasionally they backed off quickly, but most of the time they felt reassured. When Donald Cameron joined through Sturge in 1991, he recalls meeting ‘smooth well-spoken gentlemen in very well-cut suits’. By then, losses were apparent elsewhere. They mentioned ‘bad publicity’, but assured him ‘with us you are absolutely safe, we have reinsured against all this, you have nothing to worry about’. They believed it and so did he. They were wrong.

THE ASSOCIATION OF LLOYD’S MEMBERS

In the late 1970s, Lloyd’s attracted publicity through scandals and high-profile members. The British press is especially interested in writing about the royal family, aristocrats, descendants of national heroes, wealthy foreigners, pop stars, tennis stars and so on. All of these categories were well represented among Lloyd’s Names, together with 60 members of the House of Commons and 230 members of the House of Lords. However, the vast majority of those who joined during the big expansion were not celebrities; they were middle-class people who wanted to earn an extra return on their relatively limited capital. Frequently their main asset was their home. Although this was not admissible, a bank

10.1057/9781137299307 - On the Brink, Andrew Duguid

Co

pyr

igh

t m

ater

ial f

rom

ww

w.p

alg

rave

con

nec

t.co

m -

lice

nse

d t

o P

alg

rave

Mac

mill

an -

Pal

gra

veC

on

nec

t -

2014

-08-

20

INS IDE OUT 17

guarantee, secured on the home, was fine. The minimum required wealth for external British members to ‘show’ was only £50,000 from 1970 to 1984, when it was increased to £100,000. In 1988,25 the overall premium limit (OPL) for a Name showing this amount was £250,000; the deposit required was £50,000 or 20 per cent of OPL for British residents and 28 per cent for residents elsewhere. The changing requirements are shown in Appendix 2.

The high-profile element of Lloyd’s membership meant that when problems occurred, they could be guaranteed plenty of public attention. Apologists might say that a rapidly expanding market was likely to produce the occasional exam-ple of excessive greed or dishonesty. Lloyd’s authorities had to deter, detect and punish these breaches. Some offences were isolated; others appeared to reveal more widespread flaws in the structure, culture or levels of competence and honesty.

As membership grew, scandals occurred and attitudes changed, members felt the need to band together. One group formed around the Sasse26 affair and another around the new Lloyd’s Act and the creation of the first published set of ‘Lloyd’s League Tables’. Until their publication, members knew only the results of the few syndicates which they had joined. This new analysis was led by John Rew and Charles Sturge for the 1977 and 1978 results, published in 1981 under the name Chatset. John Moore, then a Financial Times (FT) jour-nalist, described it as a move which ‘has left the Lloyd’s establishment purple with rage’. The figures showed Ian ‘Goldfinger’ Posgate topping the charts. His members would receive a cheque for £2,000 for each £10,000 line. Posgate had underwritten a larger amount of premium than the rules allowed, but there was a clamour to join his syndicate.

After some initial rivalry, the two groups merged to form the Association of Lloyd’s Members (ALM). In 1983 a Conservative MP, Tom Benyon, became its first Chairman, with nearly 1,000 Lloyd’s members. An early newsletter defined its aims as being to improve the understanding of Lloyd’s among members, to represent their collective views, to help select external members standing as can-didates for the new Council and to provide a link to them. In 1985, Benyon was succeeded by Anthony Haynes, who was determined to make the ALM a still more effective voice. He thought Lloyd’s did not always give enough care to the providers of its capital: ‘But if we are to play a more active part as Names, our role must be constructive and positive – working with, and not against, the sys-tem.’ In 1987, he clashed with the same journalist, John Moore, who accused the ALM of becoming too cosy with Lloyd’s. Haynes disagreed: working behind the scenes, they had achieved nearly everything they sought. As the crisis unfolded, conflict developed between groups of Names and Lloyd’s. By contrast, the ALM was consistently moderate in its approach. Its influence steadily increased.

10.1057/9781137299307 - On the Brink, Andrew Duguid

Co

pyr

igh

t m

ater

ial f

rom

ww

w.p

alg

rave

con

nec

t.co

m -

lice

nse

d t

o P

alg

rave

Mac

mill

an -

Pal

gra

veC

on

nec

t -

2014

-08-

20

ON THE BRINK18

THE CORPORATION

In the original coffee house, waiters served traders. Gradually their duties extended. When the new building was opened, 90 waiters, still wearing tradi-tional uniform, looked after security, took messages and performed other duties. They were nearly all men, with a tradition of long service and a strong sense of comradeship. The few remaining are still conspicuous. Only a small num-ber of other staff, working under a secretary, were employed by Lloyd’s in the nineteenth century. When the Society of Lloyd’s was incorporated by the 1871 Lloyd’s Act, the central body and its staff became known as the Corporation. In the twentieth century, its role expanded.

By 1986, the Corporation employed around 2,000 people. Several senior officers had been recruited from outside Lloyd’s, from both the private and pub-lic27 sectors. Among its middle and junior ranks, staff turnover was low. Many people had worked there all their life. Newer recruits included accountants, spe-cialists in IT systems, lawyers and other professionals.

The Corporation provided services to the market and supported its self-regulatory machinery. Departments checked and issued Lloyd’s policies,28 set-tled claims in the marine market,29 registered each agent, collected syndicate data, produced ‘global’ reports showing overall financial results for the market, managed the premises, operated the central accounting system enabling the flow of money between brokers and syndicates, and provided computer sys-tems. Lloyd’s representatives in various overseas markets stood ready to accept service of suit on behalf of syndicates. They also helped to ensure that Lloyd’s complied with local rules. Their supervision was made difficult – sometimes comically so – by Lloyd’s tribal habits.

To a complete outsider, these various groups – underwriters, brokers, man-aging agents, members’ agents, claims specialists, accountants, waiters, support staff and the Corporation employees – were all part of the ‘Lloyd’s Community’, a phrase that was often used when the speaker wanted to emphasise its unity of purpose. To a Name, who in his main life was far removed from the market, all of these people were loosely seen as ‘insiders’. But whether being extolled or crit-icised, the notion of a single community of insiders was an over-simplification. Lloyd’s in the 1980s was seriously tribal.

TRIBALISM

Within the underwriting market were well-defined tribes: marine, non-marine, motor and aviation markets, each with their customs and their separate market associations, provoking strong loyalties. They argued over matters like space in

10.1057/9781137299307 - On the Brink, Andrew Duguid

Co

pyr

igh

t m

ater

ial f

rom

ww

w.p

alg

rave

con

nec

t.co

m -

lice

nse

d t

o P

alg

rave

Mac

mill

an -

Pal

gra

veC

on

nec

t -

2014

-08-

20

INS IDE OUT 19

the underwriting room. Tradition had it that the marine market, as the ‘senior’ market, enjoyed the ground floor. In the new building, this was a big trading advantage – resented by others, not least because the distinction between marine and other syndicates was increasingly blurred. In the previous building it was just about possible to see everyone at once: the non-marine market was on a gal-lery surrounding the others on the ground floor. In the new building, each floor was a separate world. To reach the upper galleries, a broker had to take a lift or ride slowly up several escalators. The architect called the glass lifts and escala-tors a ‘celebration of movement’. Busy brokers found them painfully slow.

The traditional marine world was in decline: shipping volumes fell steeply in the 1970s and 1980s. Marine underwriters looked elsewhere for expansion. Encroachment became an issue. Non-marine specialists thought marine under-writers lacked the expertise to rate ‘their’ risks properly. Non-mariners also thought the bigger ‘lines’ taken by large marine syndicates symptomatic of a less collegiate approach. The main walkway between boxes that led from the front door was known as ‘alphabet alley’ because it contained underwriters Agnew, Brockbank and Charman. It was also known as ‘ego alley’.

Attitudes towards members’ agents illustrate another tribal distinction. The members’ agent who understood the trends at work in different market sec-tors, building relationships with a range of underwriters, could serve his Names’ interests well. Some approached this in a professional manner, developing an in-house capability for analysis. Stace Barr, for example, grew rapidly from a start-up with a second-hand desk to one of the largest in ten years. But the gen-eral view of members’ agents among underwriters was not respectful: some did not conceal their contempt for this ‘lesser breed’, especially if asked what they saw as cheeky questions about their performance or aggregate exposure to risk. When new syndicates were formed, underwriters were keen to secure support from members’ agents. Loyalties and resentments were built up. Years later, John Charman, a successful underwriter, recalled his supporters fondly, refusing to deal with some who had been unhelpful in his early days.

On the trading floor, the sharpest tribal distinction was between under-writers and brokers. As the source of all business, some underwriters felt the need to cultivate brokers, but to stay on their guard. They were seen as the sales-men, the smooth talkers, making light of difficulties. Many underwriters had started life as brokers. They understood attempts to talk them into taking a risk at too low a price or on too generous terms. Some brokers were seen as always looking for weakness; sadly they often found it on another box. They called you ‘Sir’ by convention, but not necessarily out of respect.

In the 1980s, most senior and middle-ranking brokers were themselves underwriting Names. Their juniors aspired to be Names. Many broking firms

10.1057/9781137299307 - On the Brink, Andrew Duguid

Co

pyr

igh

t m

ater

ial f

rom

ww

w.p

alg

rave

con

nec

t.co

m -

lice

nse

d t

o P

alg

rave

Mac

mill

an -

Pal

gra

veC

on

nec

t -

2014

-08-

20

ON THE BRINK20

encouraged this, often providing interest-free loans. Any broker who was a Name wanted his syndicates to be profitable. To insiders, this shared member-ship was part of the glue that held the whole system together.

To brokers, some of the underwriters seemed arrogant and vain. A few were seen as lazy. It was necessary to show them a little deference. Added flattery often paid off. If one wouldn’t take on a dubious risk, another often would. Particularly in the late 1980s, with burgeoning capacity, someone, somewhere in the Lloyd’s mar-ket would take on most risks. Danger lay where underwriters accepted hospitality from brokers; most were careful to avoid anything excessive, but a few were not.

There were many cross-currents: ownership issues, membership issues, rivalries, close bonds and cold shoulders. The concept of reciprocity is central. Favours tend to be returned with a favour. Thus, a broking firm that brings val-ued business may be offered a chance to place important reinsurance contracts on behalf of the underwriter, thereby earning commission. Underwriters’ atti-tudes towards brokers were a little schizophrenic: the source of business but also the source of much that was wrong. Brokers had plenty of complaints about the market too: old-fashioned, cumbersome claims procedures, too many small syn-dicates wanting small shares and heavy transaction costs. A big complaint from both sides was the flow of money: it moved like glue on its way from client to underwriter, while the broker earned the interest. Claims payments to clients were said to suffer the same fate. Brokers countered with complaints about delays in authorising payments. If one talked to a group of underwriters on almost any subject, within minutes they would start on the iniquities of the brokers and vice versa. All markets generate attitudes like this until they face a common threat.

There was one thing upon which the more extreme among these warring tribes could all agree: a belief that the Corporation was a bloated bureaucracy. To many, it was beneath contempt. It had grown unjustifiably. Staff were seen as uncommercial, some were seen as self-aggrandising. Their job titles were a bit of a joke, from ‘Chief Executive’ downwards. The ‘regulation’ of the market they attempted to provide was ineffective and misplaced, and was often aimed at the wrong targets. They lacked respect for trading skills. Corporation staff were spoken of collectively, and a little contemptuously, as the ‘civil service’. To many, it was the ‘f***ing Corporation’, its requests resented as a burden on the free operation of the market. This might sound like an over-sensitive caricature, but tribal instincts and stereotypes were at work.

Many underwriters felt as much loyalty to their tribe as to Lloyd’s itself. Claims specialists felt under-regarded by underwriters; everyone poured scorn on lawyers. Non-marine underwriters saw themselves as the true insurance pro-fessionals; to them, the mariners represented the past, still clinging to residual privileges. Mariners resented them as jumped-up Johnny-come-latelies. Aviators had their own sense of distinctiveness and self-importance, as did motor

10.1057/9781137299307 - On the Brink, Andrew Duguid

Co

pyr

igh

t m

ater

ial f

rom

ww

w.p

alg

rave

con

nec

t.co

m -

lice

nse

d t

o P

alg

rave

Mac

mill

an -

Pal

gra

veC

on

nec

t -

2014

-08-

20

INS IDE OUT 21

underwriters. Many of the underwriting associations’ staff had occupied their positions for a long time. Defenders of the rights and privileges of their sectional interests, they imbibed and shared the market view of the Corporation, some-times echoing their masters with extra stridency.

Many of the Corporation staff reciprocated. Often suspicious of the entre-preneurial market culture, they thought differently and ate in a separate, sub-sidised canteen. Long-serving staff were used to this. Newer recruits found the attitudes they encountered much harder to take. Among the hundreds of syndi-cates were odd exceptions. One aviation underwriter, John Tilling, had started out as a corporation employee. He was always approachable. Less rare was the migration of qualified Corporation staff to better-paid jobs in the market. A few individuals built bridges across the cultural divides. Lloyd’s first Chief Executive, Ian Hay Davison, battled hard to break down what he referred to as the ‘green baize door’ separating the market and the Corporation, with some success at the senior levels, but much of the time, a ‘them and us’ attitude pre-vailed on both sides. This gulf contributed to Lloyd’s inability to see and act on the problems that lay hidden below the surface.

New agents often lacked the arrogance of long-standing colleagues. For example, Andrew Beazley and Nick Furlonge set up shop in 1986 with a rented room and second-hand furniture. They were too busy creating a business to worry about old tribes. They were glad of any support, cultivating contacts wherever they could. They were part of a newer breed that helped Lloyd’s to shed its skin. Over the next two decades, Beazley became the third-largest man-aging agency at Lloyd’s with a turnover exceeding £1 billion. Stephen Catlin, John Charman and Mark Brockbank were among those who started businesses that began on a very small scale and rapidly established strong positions in the market. They preferred making money to tribal warfare.

Humour plays a big part in life at Lloyd’s. A cynical underwriter, Ralph Rokeby-Johnson, came up with unflattering nicknames for every well-known personal-ity in the marketplace. He described the Chief Executive as having undergone a ‘Charisma Bypass’. His demeaning nicknames included the compliant ‘Nodding Donkey’. ‘Time Bomb Terry’ described someone (correctly) thought to take exces-sive risk, while ‘Judas’ was used for someone who once switched allegiance. Others included the ‘Sewer Rat’, ‘Fly Button’, ‘Mission Impossible’, ‘Liberace’, the ‘Flower Arranger’, the ‘Tailor’s Dummy’ and ‘Half-Pratt’. One powerful broker was known as ‘God’. The originator of these colourful phrases was known as ‘Satan’.

INSTITUTIONAL VALUES

Any institution develops its own conventions, traditions, myths and values. Although prizing individualism, Lloyd’s required conformity in some matters

10.1057/9781137299307 - On the Brink, Andrew Duguid

Co

pyr

igh

t m

ater

ial f

rom

ww

w.p

alg

rave

con

nec

t.co

m -

lice

nse

d t

o P

alg

rave

Mac

mill

an -

Pal

gra

veC

on

nec

t -

2014

-08-

20

ON THE BRINK22

and resisted change. For all its tribalism and rivalry, the Lloyd’s market engen-dered a very real sense of belonging, especially among the more senior ranks of underwriters and brokers whose interests the system served well. They might regard the Corporation, the accountants and the support staff as hangers-on, but they also believed that Lloyd’s was very special. They were very defensive of the institution when it came under attack from the press, Parliament or com-petitors. With only rare exception, they were susceptible to the authority of the Chairman and the Committee of Lloyd’s.

Few institutions were more conscious of their uniqueness than Lloyd’s: its myths were strongly believed. It was said that unlimited liability made Lloyd’s uniquely strong, conjuring up an image of unlimited resources. Lloyd’s under-writers were thought to be uniquely creative because they operated flexibly as small units, while backed by the whole institution. This was the catechism, eagerly taught to the newcomer, who was keen to learn and repeat it. Interference from government or elsewhere was anathema. The world outside Lloyd’s was not quite its equal. Those who worked in the nearby ‘company market’ were only too well aware of this irritating sense of superiority.

This self-belief was uplifting for those concerned, but it tended to reinforce a stifling orthodoxy, notably in the strength and virtue of unlimited liability and blind faith in market mechanisms. Amid growing concern about the impact of losses, the Council told members in 1990 that it had once again reviewed unlim-ited liability and concluded that it should remain as the basis for underwriting. The ideology of Lloyd’s explains the initial attitudes towards big losses when they began to emerge: Lloyd’s was all about risk, each member was responsible for his losses and his duty was to pay up without argument. Names even con-templating legal action were regarded as traitors. For insurance disputes, there was a long-standing preference for arbitration over resorting to the courts.

This brief introduction can only scratch the surface of the inter-dependent network of relationships and loyalties that together make a functioning mar-ketplace. It would be seriously deficient if it emphasised loyalty to tribes at the expense of the intense loyalty also often felt towards individual firms. Among the managing and members’ agents, and the brokers, there were many firms whose culture had been shaped by a strong personality. At any one time, some of these firms were starting up, others were growing, sometimes quickly, while others had reached maturity or were in decline. Some had a well-defined hous-estyle, quickly adopted by those who joined the firm.

Some had rigorous disciplines of their own, usually owing much to the strong character of one particular underwriter. Robert Kiln was an extreme case. He started work in Lloyd’s in 1937. During the Second World War, he lost a leg and suffered partial deafness. Returning to Lloyd’s in 1945, he became an

10.1057/9781137299307 - On the Brink, Andrew Duguid

Co

pyr

igh

t m

ater

ial f

rom

ww

w.p

alg

rave

con

nec

t.co

m -

lice

nse

d t

o P

alg

rave

Mac

mill

an -

Pal

gra

veC

on

nec

t -

2014

-08-

20

INS IDE OUT 23

innovative non-marine underwriter, forming his agency in 1962. He played an active role in Lloyd’s affairs, with nine years as a member of the Committee of Lloyd’s. He became well-known for his forthright views and active as a speaker and writer. He also wrote a textbook on reinsurance which became a classic.

Kiln was intensely proud of the best aspects of Lloyd’s. In a 1978 lecture, he attributed its success to the ability of those in Lloyd’s to rely on each other’s word. He said: ‘We come to Lloyd’s to work and for profit, and working for profit is worthwhile ... if we in Lloyd’s ever lose our integrity or do things which we know to be dishonourable, then that will be the beginning of the end ... con-fidence will evaporate and the whole edifice will collapse.’

Kiln’s syndicate had well-defined procedures for assessing risk. He took a very dim view of sloppy practice in others. In many respects, his firm was a beacon of rectitude. By contrast, there were also agents and syndicates with few inherited disciplines. If their biggest asset was the charm or pliability of their underwriter, they were likely to be in big trouble. To handle the increasing complexity of modern business required sophisticated techniques: exhaustive record-keeping systems, analysis, projections and so on. For some syndicates, the deep water of liabilities and complicated reinsurance contracts went over their heads; they drowned, taking many Names with them. Nevertheless, the independence of each underwriter was the prevailing ethic. Only when the scale of damage was nearly fatal to the whole institution did this notion change.

While the expertise was variable, the tribal instincts strong, and the quality of firms and individuals mixed, the values and loyalties of those at the core of the market were widely shared and deeply ingrained. As the story of the mid-1990s crisis unfolded, tradition had to be sacrificed on a big scale. Change was forced by the need to prove solvency to regulators, respond to a large-scale rebellion by Names and attract fresh capital. Self-interest and the survival instinct were important drivers in the search for a workable solution. But loyalty to an institu-tion under threat was another powerful force.

***

External Names were much less intimately involved with Lloyd’s than those who spent their working lives in Lime Street. Most had allegiances outside Lloyd’s, but as the losses mounted, groups of Lloyd’s Names found a common cause. New groups were formed – people united by their anger and determination to lessen the impact of big losses on their lives. They discovered leaders within their ranks, they hired lawyers and went to the courts seeking recompense. Some went further and attacked the institution and everything it seemed to them to stand for: greed, amateurism, deception, dishonesty and downright fraud.

10.1057/9781137299307 - On the Brink, Andrew Duguid

Co

pyr

igh

t m

ater

ial f

rom

ww

w.p

alg

rave

con

nec

t.co

m -

lice

nse

d t

o P

alg

rave

Mac

mill

an -

Pal

gra

veC

on

nec

t -

2014

-08-

20

ON THE BRINK24

GUARDIANS

Quis Custodiet ipsos custodes? (Who will guard the guards themselves?)Juvenal

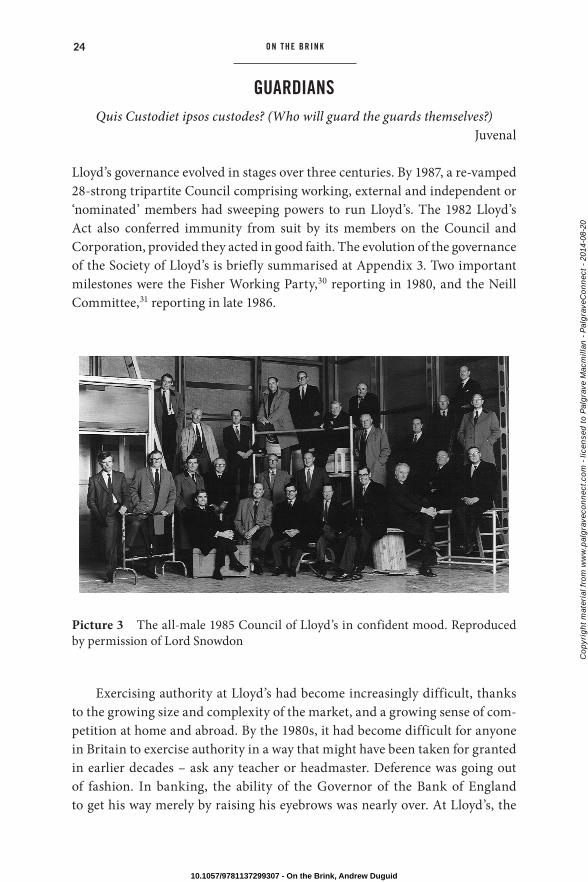

Lloyd’s governance evolved in stages over three centuries. By 1987, a re-vamped 28-strong tripartite Council comprising working, external and independent or ‘nominated’ members had sweeping powers to run Lloyd’s. The 1982 Lloyd’s Act also conferred immunity from suit by its members on the Council and Corporation, provided they acted in good faith. The evolution of the governance of the Society of Lloyd’s is briefly summarised at Appendix 3. Two important milestones were the Fisher Working Party,30 reporting in 1980, and the Neill Committee,31 reporting in late 1986.

Exercising authority at Lloyd’s had become increasingly difficult, thanks to the growing size and complexity of the market, and a growing sense of com-petition at home and abroad. By the 1980s, it had become difficult for anyone in Britain to exercise authority in a way that might have been taken for granted in earlier decades – ask any teacher or headmaster. Deference was going out of fashion. In banking, the ability of the Governor of the Bank of England to get his way merely by raising his eyebrows was nearly over. At Lloyd’s, the

Picture 3 The all-male 1985 Council of Lloyd’s in confident mood. Reproduced by permission of Lord Snowdon

10.1057/9781137299307 - On the Brink, Andrew Duguid

Co

pyr

igh

t m

ater

ial f

rom

ww

w.p

alg

rave

con

nec

t.co

m -

lice

nse

d t

o P

alg

rave

Mac

mill

an -

Pal

gra

veC

on

nec

t -

2014

-08-

20

INS IDE OUT 25

various scandals of the 1970s had tested the authority of the Committee and the Chairman, exposing their powers as inadequate to run a complex interna-tional marketplace. The constitution and its cumbersome procedures needed updating: the Fisher Working Party was asked to make proposals. The chal-lenge to authority came in several forms. Christopher Moran was expelled from the market; Ian Posgate was suspended32 from underwriting for a time. Other scandals stretched the Committee’s ability to deal with miscreants and rebels.

In late 1982, soon after Parliament passed the new Lloyd’s Act, fresh scandals emerged. Against this background, the Governor of the Bank of England, Gordon Richardson, persuaded a reluctant Lloyd’s to accept an out-side figure of stature in a new role as Chief Executive. Until then the most senior role in the Corporation had been the Secretary-General, whose role was too deferential to be source of authority. An independent Chief Executive was seen as essential to counter the suspicions now surrounding the market. The new man, Ian Hay Davison, was also made a member of the Council and a Deputy Chairman of Lloyd’s to give him added authority. He was a crusader. Many elements in the market, including the next Chairman, Peter Miller, found it hard to accept the new pattern in the spirit intended by the Governor. As such, much of the body politic tried to reject this transplanted organ.

Following an uncomfortable tenure from 1983 to 1985, Davison left, say-ing the rotten apples had begun to infect the barrel. His book, A View of the Room, which appeared two years later, was dedicated ‘to the external members of Lloyd’s on whose behalf the mission was carried out’. It did not foresee the problems to come. His successor was Alan Lord, a very able ex-Treasury civil servant who had been tempted into the private sector to become Chief Executive of the British manufacturer Dunlop. His gruff Lancashire manner and apparent intellectual arrogance did not win him many friends in the mar-ket; he did not court popularity. An intensely private person, those who knew him respected his intelligence, total integrity and his dry sense of humour. Miller, the Chairman, only served champagne. At one of his many receptions, Lord, a whisky-drinker by preference, picked up a glass, muttering: ‘We prac-tically wash our socks in this stuff here.’ When he eventually stood down, a perceptive tribute by the editor of Lloyd’s List recognised his many virtues, crediting him for the steadiness of his hand. But the ship was lurching towards the rocks.

From 1983 to 1993, the Council delegated supervision of the market to the Committee of Lloyd’s, comprising its elected working members. The Council met monthly, but the Committee met each week. Matters affecting the market

10.1057/9781137299307 - On the Brink, Andrew Duguid

Co

pyr

igh

t m

ater

ial f

rom

ww

w.p

alg

rave

con

nec

t.co

m -

lice

nse

d t

o P

alg

rave

Mac

mill

an -

Pal

gra

veC

on

nec

t -

2014

-08-

20

ON THE BRINK26

were brought to the full Council if they required a byelaw. New byelaws required the support of a majority of both the working members and the external and nominated members taken together.

The Committee, a descendant of earlier arrangements, still operated in a somewhat ritualistic way. Members spoke in order of their seniority. First up was the longest-serving member, referred to by the Chairman as ‘Mr Senior’. The pro-cedure could be quite frustrating for a new boy (there were no new women), who was often reduced to expressing agreement with an earlier speaker. Meetings ended with a solemn reading of recent deaths among members, at which point heads were reverently bowed. It had the air of church service. At the end of each meeting, there was an informal session, for which senior Corporation staff were required to leave, which went unrecorded. This was followed by a lunch that gave a chance for more informal discussion, to which a handful of senior staff were invited by rotation. Excellent wines were supplied from the Lloyd’s cellar. The lunch habit dies hard: at the time of writing, the members of the last Committee of Lloyd’s, replaced by a new Market Board in 1993, still lunch together every December.

Authority over Lloyd’s did not stop at the Council. The law in most coun-tries recognises the special character of insurance. Protecting individuals and businesses from the effects of disaster, a modern economy could not function without it. To play this role, it must be reliable. Because an insurance failure can be so damaging, insurers are tightly controlled in most countries. It would be too easy for unscrupulous people to sell insurance – which is simply a promise to pay – and then fail to pay up. In Britain there have been few insurance fail-ures; there have been hundreds in America, where the regulation of insurance is performed at the state, not the federal, level. Every insurer’s ability to pay when needed – its solvency – is closely watched by government regulators. In Britain this was done by the Board of Trade, which became part of the Department of Trade and Industry (DTI) in 1970.

Insurance law in Britain exempted Lloyd’s members from registration as insurers, but required that an annual solvency certificate was provided to the DTI on behalf of every Name. In the rare event that an individual could not show assets sufficient to cover his liabilities, Lloyd’s own central assets were ‘earmarked’ to cover the deficiency. As the losses mounted, this rarity became frequent and eventually almost overwhelming. Lloyd’s also had to demonstrate its collective solvency to the DTI and to various overseas authorities. Foreign regulators tended to treat Lloyd’s as a single entity. In the US, Lloyd’s holds licences to conduct business in Illinois, Kentucky and the US Virgin Islands – in the jargon it is an ‘admitted’ insurer in those states, able to underwrite all kinds of insurance. (Kentucky is the centre for horse

10.1057/9781137299307 - On the Brink, Andrew Duguid

Co

pyr

igh

t m

ater

ial f

rom

ww

w.p

alg

rave

con

nec

t.co

m -

lice

nse

d t

o P

alg

rave

Mac

mill

an -

Pal

gra

veC

on

nec

t -

2014

-08-

20

INS IDE OUT 27

racing and breeding; Lloyd’s is big in ‘equine’ or ‘bloodstock’ insurance.) In all other US states, Lloyd’s syndicates are eligible to write reinsurance – much less closely regulated – and commercial business unavailable locally, known as ‘surplus lines’.