On Demographics, Growth and Investing Society Oklahoma...• 25% maximum tax rate on qualified ......

45

On Demographics, Growth and Investing When the structural collides with the cyclical CFA Society Oklahoma D. Harris Kere, CFA Investment Strategist Aegon Asset Management US March 13, 2018 Aegon Asset Management is the global investment management brand of the Aegon Group N.V. and is comprised of Aegon USA Investment Management, LLC (Aegon Asset Management US), Aegon USA Realty Advisors, LLC (Aegon Real Assets US), Kames Capital plc (Kames Capital) and other Aegon affiliates. Aegon Asset Management US, Aegon Real Assets US, and Kames Capital are SEC registered investment advisers. For institutional use only.

Transcript of On Demographics, Growth and Investing Society Oklahoma...• 25% maximum tax rate on qualified ......

On Demographics, Growth and Investing When the structural collides with the cyclical

CFA Society Oklahoma

D. Harris Kere, CFAInvestment StrategistAegon Asset Management US

March 13, 2018

Aegon Asset Management is the global investment management brand of the Aegon Group N.V. and is comprised of Aegon USA Investment Management, LLC (Aegon Asset Management US), Aegon USA Realty Advisors, LLC (Aegon Real Assets US), Kames Capital plc (Kames Capital) and other Aegon affiliates. Aegon Asset Management US, Aegon Real Assets US, and Kames Capital are SEC registered investment advisers. For institutional use only.

2For institutional use only

On demographics, growth and investing

• Cyclical outlook – The see-saw years

• Trend growth – The goal posts have moved

• Productivity outlook

• Demographics

• Inflation

• Investment implications

3For institutional use only

Sizing up the expansion

Early 50s

Mid 50s

Late 50s

1960s

Early 70s

Mid-late 70s

Early 80s

Mid-late 80s

1990s

2000s

Current Cycle

R² = 0.7622

-

5

10

15

20

25

30

35

40

45

0.0 0.5 1.0 1.5 2.0 2.5

Len

gth

of

Cyc

le (

qtr

s)

Average Expansion Excess Speed vs. Potential % (Real GDP Growth, QoQ Saar)

Expansion pace relative to potential tends to drive cycle length

Source: Bureau of Economic Analysis, Congressional Budget Office,, National Bureau of Economic Research, Aegon AM US. As of Dec 2017.

4For institutional use only

Forecasts

Forecast

2015 2016 2017 2018 2019 2020 2021

GDP (Real %, YoY) 2.60 1.60 2.30 2.80 2.30 1.80 1.00

Unemployment (%) 5.30 4.90 4.40 3.90 3.70 4.10 4.80

Core PCE 1.30 1.70 1.50 1.90 2.00 1.80 1.70

Fed Funds (%) 0.50 0.75 1.50 2.00 2.50 1.75 1.25

10-year Treasury (%) 2.27 2.45 2.41 3.10 3.20 2.50 2.05

Source: Bureau of Economic Analysis, Congressional Budget Office, Haver Analytics, Aegon AM US. As of Feb 2018.

5For institutional use only

Forecasts

Source: Bloomberg, Aegon AM US. As of Feb 2018.

2.2

2.3

2.4

2.5

2.6

2.7

2.8

Jan-17 Feb-17 Mar-17 Apr-17 May-17 Jun-17 Jul-17 Aug-17 Sep-17 Oct-17 Nov-17 Dec-17 Jan-18 As ofFeb-18

Rea

l GD

P G

row

th, %

2018 GDP Forecasts

Bloomberg 2018 GDP Consensus AAM US Macro Strategy '18 GDP

Forecasts

Feb-15

6For institutional use only

Tax Cuts and Jobs Act highlights

Source: US Congress

Corporate

• Reduces the corporate tax rate to 21% (25% for personal services) from 35%

• Allows 100% expensing of certain business property through 2022

• Limits/reduces business interest deduction

• Limits Net Operating Loss deduction to 80% of taxable income

Individual

• Seven Brackets: 10%, 12%, 22%, 24%, 32%, 35%, 37%

• Standard Deduction increased to $24k for married joint filers, $12k for singles

• 25% maximum tax rate on qualified business income of individuals

• Increases the Child Tax Credit

• Deductions for State & Local Taxes limited to $10k

• Doubles Estate and Gift Tax exemption from $5MM to $10MM

• Repeal of Individual and Corporate Alternative Minimum Tax

7For institutional use only

The goal post has shifted

(5)

(4)

(3)

(2)

(1)

-

1

2

3

4

5

6

7

8

9

19

51

19

53

19

55

19

57

19

59

19

61

19

63

19

65

19

67

19

69

19

71

19

73

19

75

19

77

19

79

19

81

19

83

19

85

19

87

19

89

19

91

19

93

19

95

19

97

19

99

20

01

20

03

20

05

20

07

20

09

20

11

20

13

20

15

20

17

20

19

20

21

20

23

20

25

20

27

GD

P %

Diff GDP: Potential GDP: Actual

Source: BEA, CBO, HAVER, Aegon AM US. As of Jan 2018.

'Slow Growth in Absolute Terms, But Still Decent Relative to Potential'US Growth - Actual vs. Potential

Forecasts

8For institutional use only

Pressuring trend growth lower

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

5.5

6.0

19

51

19

53

19

55

19

57

19

59

19

61

19

63

19

65

19

67

19

69

19

71

19

73

19

75

19

77

19

79

19

81

19

83

19

85

19

87

19

89

19

91

19

93

19

95

19

97

19

99

20

01

20

03

20

05

20

07

20

09

20

11

20

13

20

15

20

17

20

19

20

21

20

23

20

25

20

27

Demographics suggest that 3% trend growth is highly unlikely

CBO Potential Real GDP (0.5% Labor Force Growth) 0.7% LF Growth 1% LF Growth 1.4% LF Growth (1950-2016 avg)

Source: Congressional Budget Office, Haver Analytics, Aegon AM US. As of June 30, 2017.

Forecasts

0.7% Labor

Force Growth

1.0% Labor

Force Growth

1.4% Labor Force Growth

(1950-2016 avg.)

9For institutional use only

Especially as productivity growth may hit a ceiling

1.0

1.5

2.0

2.5

3.0

3.5

4.0

19

77

19

79

19

81

19

83

19

85

19

87

19

89

19

91

19

93

19

95

19

97

19

99

20

01

20

03

20

05

20

07

20

09

20

11

20

13

20

15

20

17

20

19

20

21

20

23

20

25

Can Trumponomics boost long-term productivity?If so, real trend growth can accelerate, but upside is limited

Scenario 1 - GDPp (1.7% Trend Productivity)

Scenario 2 - GDPp (2.0% Trend Productivity)

CBO's Official Potential Real GDP Growth (Implies 1.4% Trend Productivity)

Source: Haver Analytics, Congressional Budget Office, Aegon AM US. As of Nov 2016.

Forecasts

10For institutional use only

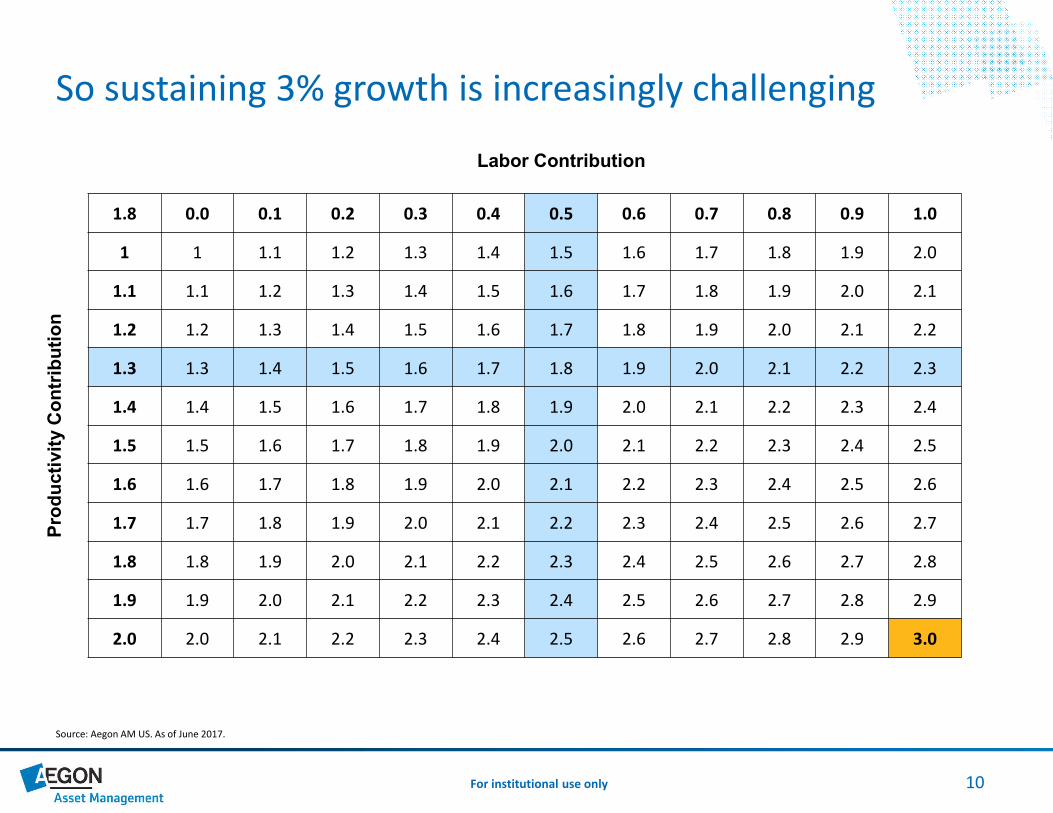

So sustaining 3% growth is increasingly challenging

Labor Contribution

1.8 0.0 0.1 0.2 0.3 0.4 0.5 0.6 0.7 0.8 0.9 1.0

Pro

du

cti

vit

y C

on

trib

uti

on

1 1 1.1 1.2 1.3 1.4 1.5 1.6 1.7 1.8 1.9 2.0

1.1 1.1 1.2 1.3 1.4 1.5 1.6 1.7 1.8 1.9 2.0 2.1

1.2 1.2 1.3 1.4 1.5 1.6 1.7 1.8 1.9 2.0 2.1 2.2

1.3 1.3 1.4 1.5 1.6 1.7 1.8 1.9 2.0 2.1 2.2 2.3

1.4 1.4 1.5 1.6 1.7 1.8 1.9 2.0 2.1 2.2 2.3 2.4

1.5 1.5 1.6 1.7 1.8 1.9 2.0 2.1 2.2 2.3 2.4 2.5

1.6 1.6 1.7 1.8 1.9 2.0 2.1 2.2 2.3 2.4 2.5 2.6

1.7 1.7 1.8 1.9 2.0 2.1 2.2 2.3 2.4 2.5 2.6 2.7

1.8 1.8 1.9 2.0 2.1 2.2 2.3 2.4 2.5 2.6 2.7 2.8

1.9 1.9 2.0 2.1 2.2 2.3 2.4 2.5 2.6 2.7 2.8 2.9

2.0 2.0 2.1 2.2 2.3 2.4 2.5 2.6 2.7 2.8 2.9 3.0

Source: Aegon AM US. As of June 2017.

11For institutional use only

Potential sources for productivity upside

Physical

• Autonomous vehicles

• Advanced robotics

• New materials

• 3D printing

Digital

• The Internet of Things (IoT)

Biological

• Genomics – Positive for labor force and productivity

Source: Klaus Schwab, The Fourth Industrial Revolution, 2016

The 4th Industrial Revolution – Key megatrends

12For institutional use only

Defining the generations

Source: Haver Analytics; Upside by Gronbach & Moye

Birth Years Births (mm) Age Today Midpoint

GI Generation 1905 - 1924 56.6 112 - 93 103

Silent Generation 1925 - 1944 52.5 92 - 73 83

Baby Boomers 1945 - 1964 78.2 72 - 53 63

Gen X 1965 - 1984 69.5 52 - 33 43

Gen Y (Millennials) 1985 - 2004 79.5 32 - 13 23

Gen Z 2005-- 40.9* 12-- 6

*as of 2014

13For institutional use only

The demographic tailwind...

Source: Bureau of Labor Statistics, Congressional Budget Office, Aegon AM US. As of June 2017.

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

Total Labor Force Growth Total Male LF Total Female Labor Force

Average annual labor force growth

1960s 1970s 1980s 1990s 2000s Since 2010 2017-2027 (CBO)

Total Male Labor Force

14For institutional use only

...is now a demographic headwind

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

4.5%

5.0%

1960s 1970s 1980s 1990s 2000s Since 2010 2017-2027(CBO)

Average annual labor force and potential real GDP growth

Total Labor Force Growth Potential Real GDP Growth

Sources: Bureau of Labor Statistics, Congressional Budget Office, Aegon AM US. As of June 2017.

15For institutional use only

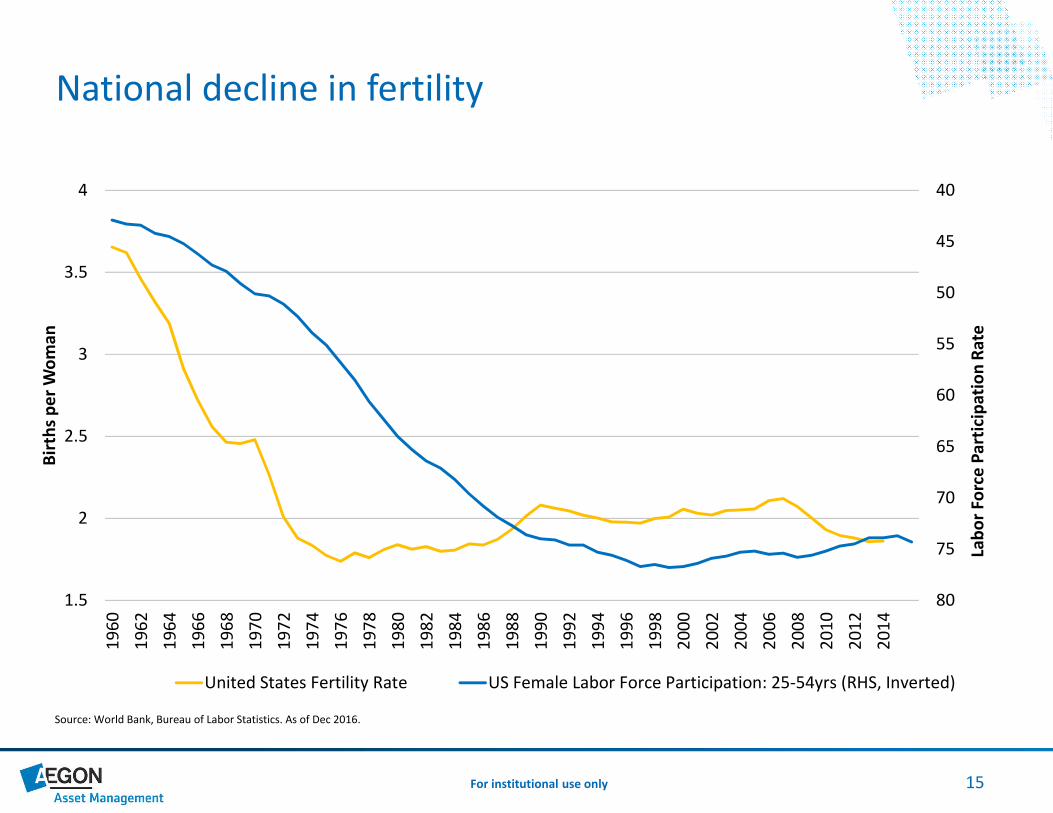

National decline in fertility

40

45

50

55

60

65

70

75

801.5

2

2.5

3

3.5

4

19

60

19

62

19

64

19

66

19

68

19

70

19

72

19

74

19

76

19

78

19

80

19

82

19

84

19

86

19

88

19

90

19

92

19

94

19

96

19

98

20

00

20

02

20

04

20

06

20

08

20

10

20

12

20

14

Lab

or

Forc

e P

arti

cip

atio

n R

ate

Bir

ths

pe

r W

om

an

United States Fertility Rate US Female Labor Force Participation: 25-54yrs (RHS, Inverted)

Source: World Bank, Bureau of Labor Statistics. As of Dec 2016.

16For institutional use only

The ‘Booming’ impact...

5.0%

7.0%

9.0%

11.0%

13.0%

15.0%

17.0%

19.0%

21.0%

23.0%

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

19

01

19

05

19

09

19

13

19

17

19

21

19

25

19

29

19

33

19

37

19

41

19

45

19

49

19

53

19

57

19

61

19

65

19

69

19

73

19

77

19

81

19

85

19

89

19

93

19

97

20

01

20

05

20

09

20

13

55-74 55-74

Total Population % Total Population (RHS)Source: Haver Analytics. As of Dec 2016.

17For institutional use only

...combined with a shrinking prime age workforce...

30.0%

32.0%

34.0%

36.0%

38.0%

40.0%

42.0%

44.0%

46.0%

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

19

01

19

05

19

09

19

13

19

17

19

21

19

25

19

29

19

33

19

37

19

41

19

45

19

49

19

53

19

57

19

61

19

65

19

69

19

73

19

77

19

81

19

85

19

89

19

93

19

97

20

01

20

05

20

09

20

13

25-54 25-54

Total Population % Total Population (RHS)Source: Haver Analytics. As of Dec 2016.

18For institutional use only

...stresses the old age dependency ratios

3.0x

3.5x

4.0x

4.5x

5.0x

5.5x

6.0x

6.5x

7.0x

7.5x

8.0x

19

48

19

51

19

54

19

57

19

60

19

63

19

66

19

69

19

72

19

75

19

78

19

81

19

84

19

87

19

90

19

93

19

96

19

99

20

02

20

05

20

08

20

11

20

14

Dependency ratios (20-64 / 65-plus)

Dependency Ratio Dependency Ratio (LFPR Adj.)

Source: Haver Analytics. As of Dec 2016.

Dependency ratios (20-64/ 65-plus)

(Labor Force Participation Rates Adj.)

19For institutional use only

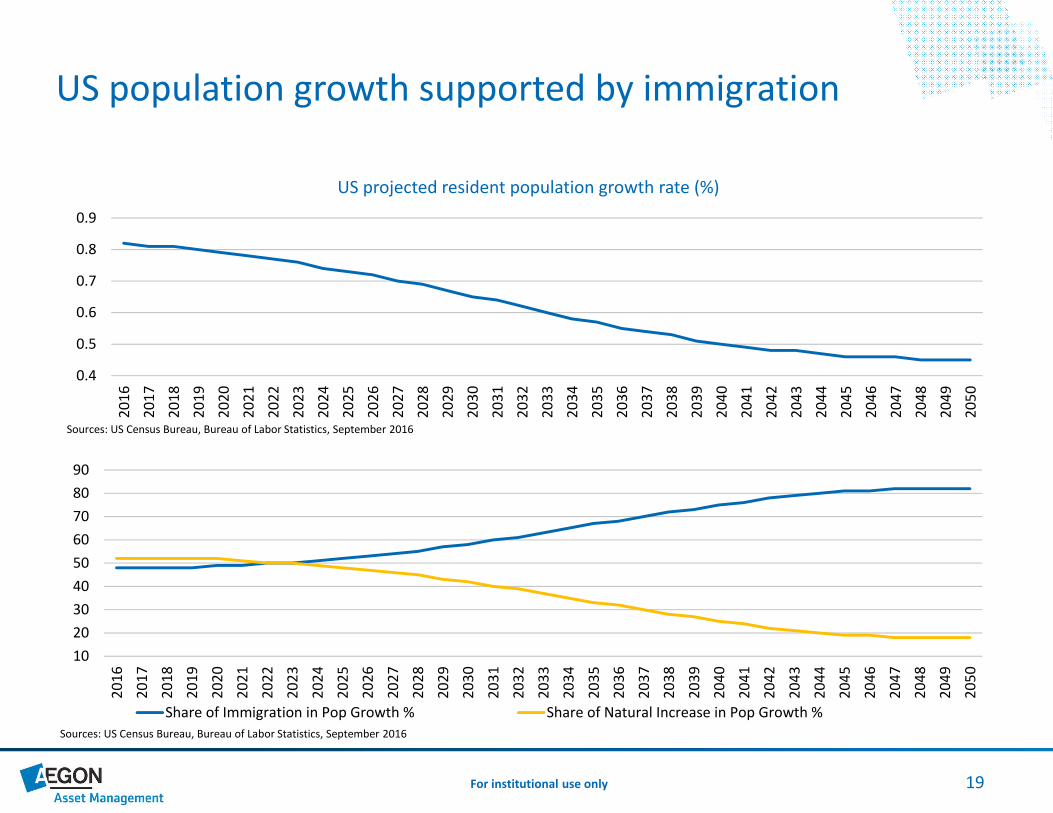

US population growth supported by immigration

0.4

0.5

0.6

0.7

0.8

0.9

20

16

20

17

20

18

20

19

20

20

20

21

20

22

20

23

20

24

20

25

20

26

20

27

20

28

20

29

20

30

20

31

20

32

20

33

20

34

20

35

20

36

20

37

20

38

20

39

20

40

20

41

20

42

20

43

20

44

20

45

20

46

20

47

20

48

20

49

20

50

US projected resident population growth rate (%)

Sources: US Census Bureau, Bureau of Labor Statistics, September 2016

10

20

30

40

50

60

70

80

90

20

16

20

17

20

18

20

19

20

20

20

21

20

22

20

23

20

24

20

25

20

26

20

27

20

28

20

29

20

30

20

31

20

32

20

33

20

34

20

35

20

36

20

37

20

38

20

39

20

40

20

41

20

42

20

43

20

44

20

45

20

46

20

47

20

48

20

49

20

50

Share of Immigration in Pop Growth % Share of Natural Increase in Pop Growth %

Sources: US Census Bureau, Bureau of Labor Statistics, September 2016

20For institutional use only

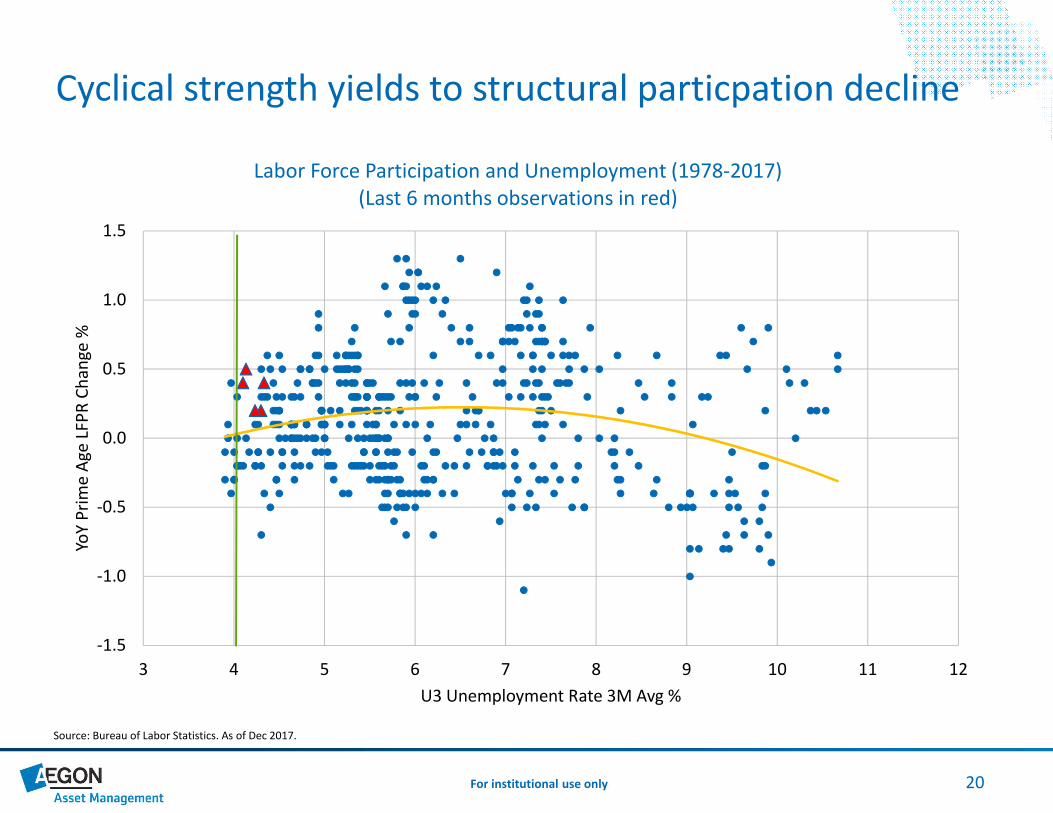

Cyclical strength yields to structural particpation decline

Source: Bureau of Labor Statistics. As of Dec 2017.

-1.5

-1.0

-0.5

0.0

0.5

1.0

1.5

3 4 5 6 7 8 9 10 11 12

YoY

Pri

me

Age

LFP

R C

han

ge %

U3 Unemployment Rate 3M Avg %

Labor Force Participation and Unemployment (1978-2017) (Last 6 months observations in red)

21For institutional use only

A global decline in fertility

1

2

3

4

5

6

19

60

19

62

19

64

19

66

19

68

19

70

19

72

19

74

19

76

19

78

19

80

19

82

19

84

19

86

19

88

19

90

19

92

19

94

19

96

19

98

20

00

20

02

20

04

20

06

20

08

20

10

20

12

20

14

20

16

Fertility rates (%)

World High income Low & middle income

Source: World Bank World Development Indicators. As of August 2017

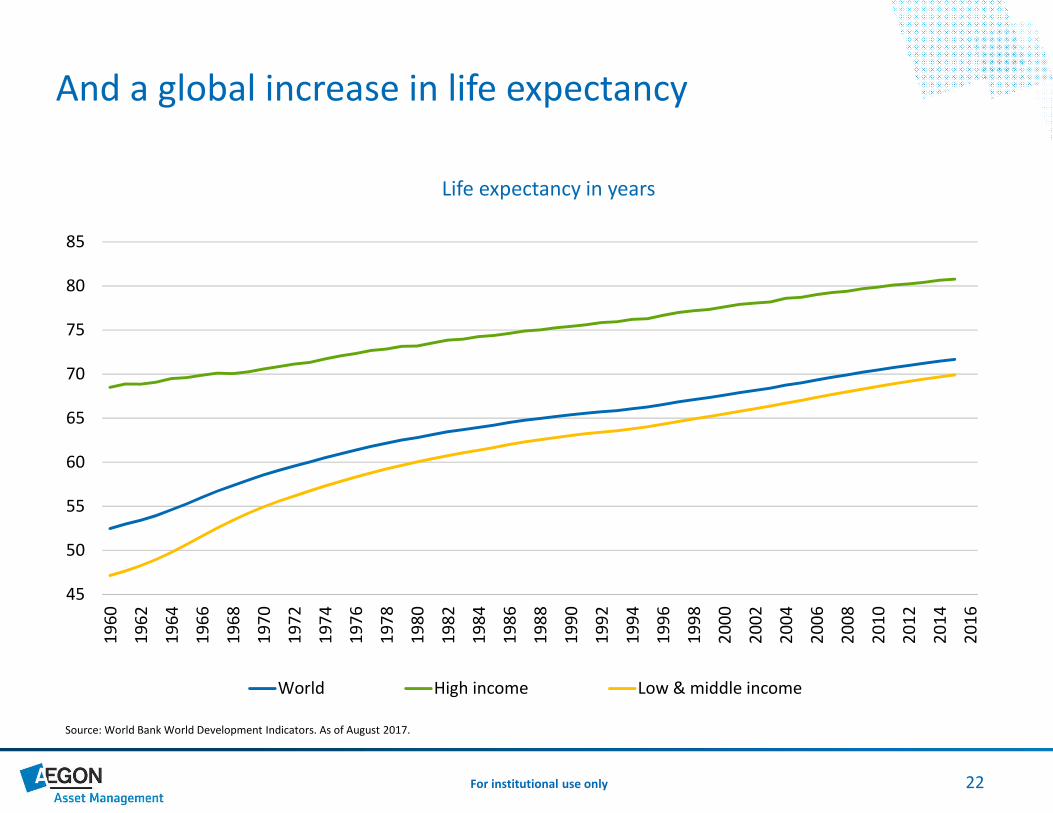

22For institutional use only

And a global increase in life expectancy

45

50

55

60

65

70

75

80

85

19

60

19

62

19

64

19

66

19

68

19

70

19

72

19

74

19

76

19

78

19

80

19

82

19

84

19

86

19

88

19

90

19

92

19

94

19

96

19

98

20

00

20

02

20

04

20

06

20

08

20

10

20

12

20

14

20

16

Life expectancy in years

World High income Low & middle income

Source: World Bank World Development Indicators. As of August 2017.

23For institutional use only

Lead to slower population growth rates

-0.25

0.25

0.75

1.25

1.75

2.25

2.75

1955 1960 1965 1970 1975 1980 1985 1990 1995 2000 2005 2010 2015 2020 2025 2030 2035 2040 2045 2050

Population growth rates (%)

WORLD Advanced Economies Emerging Economies ex Least Dev

Source: UN World Population Prospects, Medium-Variant Estimates. As of June 2017.

Emerging Economies ex- Least Developed

Forecasts

24For institutional use only

And a global silver economy

0

5

10

15

20

25

30

35

40

45

2015 2020 2025 2030 2035

Nu

mb

er o

f co

un

trie

s

Aging in the world a headwind to GDP growth

Number of countries with more 65+ adults than kids under 15 % of World GDP Represented (2015 Current $ Data)

Source: UN Population Division Medium-Variant Pop Estimates, World Bank. As of Dec 2015.

25For institutional use only

And a shrinking global labor force

-0.5%

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

1980-2015 2015-2050

Working age population (CAGR)

Sub-Saharan Africa G7 World

Source: World Bank, Aegon AM US. As of Dec 2016.

0.0%

2.5%

5.0%

7.5%

10.0%

12.5%

15.0%

17.5%

20.0%

22.5%

25.0%

27.5%

30.0%

32.5%

2015 2050

Regional as % of world working age population

Sub-Saharan Africa G-7

Source: World Bank, Aegon AM US. As of Dec 2016.

26For institutional use only

Go where the growth is...NOT

Median GDP-Weighted Ease of Doing Business Average

Africa 114 124.3 119

Ease of Doing Business Rank South Africa 73 21.9

Ease of Doing Business Rank Senegal 153 2.0

Ease of Doing Business Rank Nigeria 169 78.1

Ease of Doing Business Rank Ghana 114 4.1

Ease of Doing Business Rank Ivory Coast 142 4.3

Ease of Doing Business Rank Kenya 108 6.6

Ease of Doing Business Rank Morocco 75 7.2

Median GDP-Weighted Ease of Doing Business Average

G7 15 14.7 21

Ease of Doing Business Rank United States 7 3.7

Ease of Doing Business Rank Germany 15 1.5

Ease of Doing Business Rank Canada 14 0.6

Ease of Doing Business Rank Japan 34 4.1

Ease of Doing Business Rank France 27 1.9

Ease of Doing Business Rank Italy 45 2.4

Ease of Doing Business Rank United Kingdom 6 0.5

Source: World Bank, Bloomberg. As of Dec 2016.

27For institutional use only

A Sustained GDP Growth Edge to Emerging Economies

-2

-1

0

1

2

3

4

5

6

7

-4

-2

0

2

4

6

8

10

12

19

80

19

81

19

82

19

83

19

84

19

85

19

86

19

87

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

20

19

20

20

20

21

20

22

Rea

l GD

P G

row

th %

Rea

l GD

P G

row

th %

Emerging market and developing economies

Major advanced economies (G7)

Growth Gap - Emergning minus Major Advanced (rhs)

Source: IMF World Economic Outlook, October 2017

Forecasts

28For institutional use only

Prompting a global yield hunt

Japan

US Securitized

IG Industrials

Global HY

EM USD

Euro Corp

IG Financials

US HY

SpainItaly

UK

Non US Sec

Germany

Euro Agg IndustrialsEuro Sec

Spain

Euro Financials

Euro Banking

Pan-Euro HY

Australia

Canada

USTsy

Ireland.

Australian corp

-2

-1

0

1

2

3

4

5

6

7

YTW

Global hunt for yield

B3AAA

Source: Barclays Live, Aegon AM US. As of Sept. 2017.

Market Cap is represented by the size of each Bubble & Yield by the midpoint.

29For institutional use only

Advanced economies growing older

40

50

60

70

80

90

100

1950 1955 1960 1965 1970 1975 1980 1985 1990 1995 2000 2005 2010 2015 2020 2025 2030 2035 2040 2045 2050

Dependency ratios (Ages 0-14 and 65+, %)

United States of America Japan United Kingdom Germany

Source: UN World Population Prospects. As of June 2017

Forecasts

30For institutional use only

More time spent in retirement

United States 12/31/1970 12/31/1990 12/31/2010

Average Retirement Age 68 65 66

Life Expectancy 71 75 79

2.4 10.5 13.0

China

Average Retirement Age 67 67 67

Life Expectancy 59 69 75

-8.0 2.1 8.0

Japan

Average Retirement Age 73 71 70

Life Expectancy 72 79 83

-0.8 8.2 12.8

Germany

Average Retirement Age 60 60 62

Life Expectancy 71 75 80

10.3 14.9 18.0

Source: Organization for Economic Co-operation and Development, World Bank, Bloomberg, Aegon AM US. As of Dec 2016.

31For institutional use only

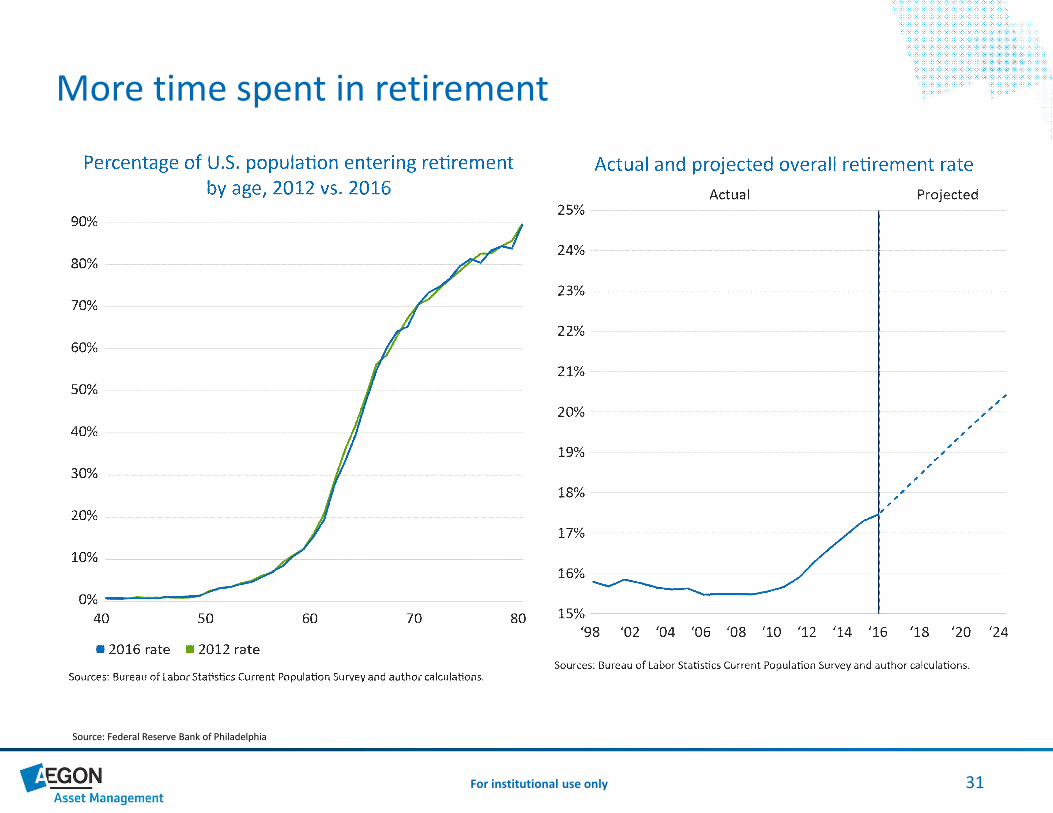

More time spent in retirement

Source: Federal Reserve Bank of Philadelphia

32For institutional use only

More time spent in unfunded retirement

-12%

-9%

-6%

-3%

0%

3%

6%

9%

12%

15%

18%

-5%

-4%

-3%

-2%

-1%

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Average returns – public pension plans

Avg Assumed Return Avg ann return since 2001 Avg 1-yr investment return (RHS)

Source: publicplansdata.org. As of Dec 2016.

Average annual return since 2001

33For institutional use only

More time spent in unfunded retirement

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1

1.1

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Public pension plans funded ratio

Source: publicplansdata.org. As of Dec 2016.

34For institutional use only

More time spent in unfunded retirement

-100

0

100

200

300

400

500

600

700

800

900

1,000

1,100

1,200

50%

55%

60%

65%

70%

75%

80%

85%

90%

95%

100%

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Total Public Pension Shortfall (RHS, $Billion) Percent of Unfunded State & Local Public Pension Plans

Source: publicplansdata.org. As of Dec 2016.

35For institutional use only

With budgetary pressures

3

4

5

6

7

8

9

15%

20%

25%

30%

35%

40%

45%

Retired (65+) to Working (20-64) Ratio Social Security and Medicare Spending as % of GDP (RHS)

Sources: Census Bureau, Congressional Budget Office. As of June 2017.

Forecasts

36For institutional use only

And selling a structural call on inflation

Brazil

China

France

Germany

India

Indonesia

Italy

Japan

NL

S. Africa

Turkey

US

R² = 0.408

-6

-4

-2

0

2

4

6

8

10

0 1 2 3 4 5 6 7 8 9 10

5yr

ch

ange

in D

epen

den

cy R

atio

(%

)

5 year average Annual CPI (%)

Source: IMF, World Bank, Aegon AM US. As of Dec 2016.

37For institutional use only

And as term premia are pressured lower by increasingly anchored inflation uncertainty

R² = 0.4055

-1

0

1

2

3

4

5

6

0.00 0.25 0.50 0.75 1.00 1.25 1.50 1.75 2.00 2.25 2.50

AC

M 1

0Yr

Ter

m P

rem

ium

CPI 4Qtrs ahead Forecast Dispersion (75th – 25th Percentile)

Adrian, Crump, Moench 10 year term premium vs. inflation uncertainty

Sources: Philly Fed SPF, New York Fed ACM, Aegon AM US, Bloomberg. As of June 2017.

0.00

0.50

1.00

1.50

2.00

2.50

19

81

Q3

19

83

Q2

19

85

Q1

19

86

Q4

19

88

Q3

19

90

Q2

19

92

Q1

19

93

Q4

19

95

Q3

19

97

Q2

19

99

Q1

20

00

Q4

20

02

Q3

20

04

Q2

20

06

Q1

20

07

Q4

20

09

Q3

20

11

Q2

20

13

Q1

20

14

Q4

20

16

Q3

Inflation uncertainty: CPI four quarters ahead

Sources: Philly Fed SPF. As of June 2017.

38For institutional use only

So are long Treasury yields

-2

0

2

4

6

8

10

12

14

16

-2

0

2

4

6

8

10

12

14

16

1982 1984 1986 1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014 2016

The 10-year US Treasury interest rate and its components

10-Year Treasury Yield Expected InflationNY Fed ACM Term Premium 10-Year Risk-Free Treasury Rate

Source: Federal Reserve Board, Haver Analytics. As of Jan 2018.

39For institutional use only

Treasuries should remain a viable portfolio hedge

-5%

-4%

-3%

-2%

-1%

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

10%

-100%-90%-80%-70%-60%-50%-40%-30%-20%-10%

0%10%20%30%40%50%60%70%80%90%

100%

Mar

-78

Mar

-79

Mar

-80

Mar

-81

Mar

-82

Mar

-83

Mar

-84

Mar

-85

Mar

-86

Mar

-87

Mar

-88

Mar

-89

Mar

-90

Mar

-91

Mar

-92

Mar

-93

Mar

-94

Mar

-95

Mar

-96

Mar

-97

Mar

-98

Mar

-99

Mar

-00

Mar

-01

Mar

-02

Mar

-03

Mar

-04

Mar

-05

Mar

-06

Mar

-07

Mar

-08

Mar

-09

Mar

-10

Mar

-11

Mar

-12

Mar

-13

Mar

-14

Mar

-15

Mar

-16

Mar

-17

Stock and Treasury bond return correlations and inflation

12mo Correlation 5Yr correlation 5Yr avg inflation, CPI YoY (RHS)

Source: Aegon AM US, Bloomberg. As of June 2017.

Sto

ck (

SPX

)

Trea

suri

es (

Bar

clay

s U

S Tr

easu

ry In

dex

)

40For institutional use only

As the relationship is yield and inflation-level dependant

0

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

-100% -80% -60% -40% -20% 0% 20% 40% 60% 80% 100%

10

Year

Tre

asu

ry Y

ield

%

Correlation

Rolling 26-week correlation (Weekly change in SPX and 10-yr yield) vs. 10-yr Level

Sources: Aegon AM US, Bloomberg. As of June 2017.

41For institutional use only

On demographics, growth and investing

• Cyclical outlook – The see-saw years

• Trend growth – The goal posts have moved

• Productivity outlook

• Demographics

• Inflation

• Investment implications

• EM v. DM

• Equities with Treasury hedge

42For institutional use only

Additional readings

Reports can be found on the AEGON Asset Management US website:

• 2018 Macro & Rates Outlook

• Structural Drivers of Low Rates

• Where Will the Flow Go? Why we favor EM. vs. DM

• Will Treasuries Remain a Viable Portfolio Hedge?

• Demographic Destiny

• Demographic Effects on Unemployment Rate (Q2 2017 Macro Outlook)

43For institutional use only

“Demographics Is Destiny”— Auguste Comte

“If we don’t change direction soon we will end up where

we are going”— Irwin Corey

44

D. Harris Kere, CFA, is an investment strategist whose

responsibilities include macro research and analytical

support for the firm’s global macro strategy efforts.

Prior to joining the firm in 2015, Harris worked for

Bank of America Merrill Lynch as an investment

manager research analyst. His responsibilities included

macro research as it relates to asset class behavior and

investment strategies in fixed income, equity and liquid

alternatives. Harris began his financial career at Bank

of America Merrill Lynch in private wealth

management. He has eight years of industry

experience. Harris received a BS in international

business and economics with a minor in applied

statistics from the Indiana University of Pennsylvania.

He is a CFA® charterholder.

Many thanks!

45For institutional use only

This material is to be used for institutional investors and not for any other purpose. The information presented is for illustrative purposes only. The enclosed information has been developed internally and/or obtained from sources believed to be reliable. This material contains current opinions of the manager and such opinions are subject to change without notice. Aegon AM US is under no obligation, expressed or implied, to update the material contained herein. This material contains general information only on investment matters; it should not be considered a comprehensive statement on any matter and should not be relied upon as such. If there is any conflict between the enclosed information and AUIM's Form ADV, the Form ADV controls. The information contained does not take into account any investor's investment objectives, particular needs, or financial situation. Nothing in this material constitutes investment, legal, accounting or tax advice, or a representation that any investment or strategy is suitable or appropriate to you. The value of any investment may fluctuate.

This document contains “forward-looking statements” which are based on change to the firm’s beliefs, as well as on a number of assumptions concerning future events based on information currently available. These statements involve certain risks, uncertainties and assumptions which are difficult to predict. Consequently, such statements cannot be guarantees and actual outcomes may differ materially from statements set forth herein. In addition. This material contains information regarding market outlook, rates of return, market indicators and other statistical information that is not intended and should not be considered an indication of actual results.

Results for certain charts and graphs are included for illustrative purposes only and should not be relied upon to assist or inform the making of any investment decisions.

Aegon USA Investment Management, LLC (“AUIM”), a wholly owned indirect subsidiary of Aegon N.V., is a U.S.-based investment adviser registered with the Securities and Exchange Commission (“SEC”) and part of Aegon Asset Management, the global investment management division of Aegon Group. AUIM is a limited liability company formed on June 1, 2001 and began managing assets on December 1, 2001. The firm definition was revised February 1, 2016 to better reflect AUIM's relationship in the broader Aegon Asset Management organization. The firm maintains a complete list and description of composites, which is available upon request.

AUIM is also registered as a Commodity Trading Advisor (CTA) with the Commodity Futures Trading Commission (CFTC) and is a member of the National Futures Association (NFA).

Aegon USA Investment Management, LLC claims compliance with the Global Investment Performance Standards (GIPS®). Please contact AUIM at [email protected] or 877-234-6862 to obtain a compliant presentation and/or a list of composite descriptions.

Recipient shall not distribute, publish, sell, license or otherwise create derivative works using any of the content of this report without the prior written consent of Aegon USA Investment Management, LLC, 4333 Edgewood Rd NE, Cedar Rapids, IA 52499.

Copyright © 2018 Aegon USA Investment Management, LLC

Disclosures

AdTrax: 1997510.5Exp Date: 3/31/2018

![Capablanca - Lasker Match 1921 [Capablanca, 1921]](https://static.fdocuments.us/doc/165x107/577cda471a28ab9e78a54085/capablanca-lasker-match-1921-capablanca-1921.jpg)