dpemou.nic.indpemou.nic.in/MOUFiles/Note on Analysis of Key issues... · Web viewBoard’s...

111

Performance of Central Public Sector Enterprises: Note on Analysis of Key Issues FINAL REPORT Sponsored By Department of Public Enterprises Government of India Submitted By 1

Transcript of dpemou.nic.indpemou.nic.in/MOUFiles/Note on Analysis of Key issues... · Web viewBoard’s...

Performance of Central Public Sector Enterprises:

Note on Analysis of Key Issues

FINAL REPORT

Sponsored By

Department of Public EnterprisesGovernment of India

Submitted By

Centre for Corporate Governance & Social ResponsibilityInternational Management Institute

New Delhi

24th December 2012

1

TABLE OF CONTENTS

Topic Page No

Introduction 04

Team 06

Methodology 08-09

Overview of CPSEs 11-17

Analysis of Issues 19-49

Recommendations withResponsibility Matrix 51-81

2

INTRODUCTION

3

Award and Scope of the Project

The project is awarded by the Department of Public Enterprises (DPE), Ministry of Heavy Industries & Public Enterprises, Government of India, as “Note on Analysis of Key issues – R&D, CSR, Corporate Governance and Sustainable Development, Increase in Profit of Profit Making CPSEs and Reduction of Loss Making CPSEs’.

The objective of the project to analyse six key issues and submit a report with recommendations on the issues as follows:1. Corporate Governance2. CSR3. Sustainable Development4. R & D5. Increase in profit of profit making CPSEs6. Reduction of loss of loss making CPSEs

It is also expected that first draft report to be submitted on Dec. 05, 2012 , final draft report by Dec. 17, 2012and final report by Dec 24,2012.

4

TEAM

5

Team for the Project

Name Designation Qualification

Professor Arun Kumar RathChairman, Centre for

Corporate Governance & Social Responsibility

M.Sc. Ph.D Former Secretary, GoI

Professor Shailendra NigamConvenor, Centre for

Corporate Governance & Social Responsibility

MBA, LL.B & PhD

Professor Prashant Gupta Associate Professor of Finance MMS, LL.B & PhD

In addition to above few other members of IMI New Delhi assisted in the completion of the report

6

METHODLOGY

7

Methodology:

Objective of this study involves Analysis of Key issues relating to performance of Central Public Sector Enterprise (CPSEs) based upon the MoU Documents signed by various CPSEs with their respective ministries for the year 2010-2011, and other related documents. The study covers four non financial parameters and two financial parameters related to profit and loss of CPSEs as follows:

1. Corporate Governance2. CSR3. Sustainable Development4. R & D5. Increase in profit of profit making CPSEs6. Reduction of loss of loss making CPSEs

The methodology adopted is detailed as following:

i. As a first step of the research study, a detailed understanding of the MoU guidelines of the Dept. of Public Enterprises, GOI for the year 2010-11 and its relevance for the CPSE’s was ensured, and has been referred to frequently at various places in the overall draft of the report.

ii. To discover how CPSEs are performing with regards to their performance on various MoU parameters, secondary Data analysis of 20 % of CPSE’s from the PE Survey Report for 2010-2011, their annual reports and 30% of the MoUs signed by the CPSEs for the said year 2010-2011 was conducted. These 30% representative CPSEs are drawn in a stratified manner with representation from each of the following categories: Maha ratna, Nav ratna, Mini ratna, profit making, loss making and sick enterprises.

iii. Inputs were taken from deliberations in the conference of CPSE board members in the Director’s Conclave organized on September 28th-29th by IMI at Greater Noida to have an overall understanding to the key issues of CPSEs.

iv. We also interviewed Joint Secretaries, Director MoU, other senior officers of DPE and other ministries, officials of from BRPSE and management division of DPE, heads of divisions of CPSEs, academic experts, subject experts and senior executives from a number of private sector companies to understand the practical issues facing organizations today on the key parameters. The interviews were conducted in a conversational manner in order to gather meaningful information.

8

v. These insights contributed to a richer understanding of the issues and in the development of recommendations that seek to answers strategic questions.

vi. Based on the information generated from two Advisory Committee meetings of the Centre for Corporate Governance and Social Responsibility, IMI New Delhi held on September 7 th

and November 27th, the study has made an assessment of the strengths and weaknesses of the key Issues of the six parameters, and has suggested improvements accordingly

vii. Interactions with representatives of CPSE’s from all the above five categories were held and specific inputs from the respective CPSEs were gathered to understand the sector specific dynamics and characteristics.

viii. A panel discussion of representatives of about 25 CPSEs and representatives of DPE was organized on 29th November’ 2012 and their perspectives were captured.

ix. In addition to above, Corporate Governance Voluntary Guidelines 2009, Ministry of Corporate Affairs, GOI, ISO 26000:2010, Guidance on Social Responsibility of International Standards Organization, Business strategies for Sustainable Development by International Institute of Sustainable Development, Corporate Governance, Best Practice Reporting of Price water house Coopers, KPMG on CSR in India, National Voluntary Guidelines on Social, Environmental & Economic Responsibilities of Business in India of Global Compact Network to name few were also referred, to develop the recommendations for the study.

x. The recommendations have generally emerged out of discussions and deliberations with representatives of stakeholders including CPSEs, academia, government departments and other concerned agencies in respect of their relevance and applicability.

9

OVERVIEW

10

Overview of Central Public Sector Enterprises

The opportunities available to the corporations in the twenty first century are multifarious and the advantages tremendous. The modern corporations have been hailed as the future agents of change, development and social welfare. Recognising the power of the modern corporation to exert a centripetal attraction to draw wealth together into aggregations of constantly increasing size, it is predicted that in future, the corporation would dominate over the State as the dominant form of economic organization.

In view of the enormous power of the modern corporation, good governance of corporate entities has gained prominence in the last two decades. Proper governance of companies has become as crucial to the world economy as the proper governing of countries. The corporation, has become the principal driver of economic growth and improved living standards. Corporations create jobs, produce a wide array of goods and services and generate wealth and income for stakeholders.

The state-owned public enterprises have made significant contributions to economic development and hold great potential for future growth of national economies. It is true that the processes of liberalisation, privatisation and globalisation have brought about significant reduction in state control over the commercial enterprises across the world. Nevertheless, public enterprises continue to remain a dominant feature of the economy in India.

The state-owned enterprises have to fulfil the twin objectives of commercial efficiency and social responsibility. The challenge for the enterprises arises out of the need for them to ensure a reasonable return on investment, while discharging their constitutional and social obligations. As wings of the welfare state, the enterprises have the mandate to act as model employers, and conduct their business in a transparent manner. Further, they have to protect the interests of all stakeholders e.g., the employees, customers, suppliers, creditors and the community. The environment of competition and globalisation being faced by the public enterprises makes the tasks all the more challenging.

It is necessary to analyse the issues concerning good governance and profitability of public enterprises .At the same time it is useful to identify the challenges faced by them in the twenty first century and suggest policy initiatives to make the public enterprises dynamic, competitive and performance-oriented.

11

The Strategic Role of the Board of Directors

The Board of Directors has to play a strategic role for better governance of the corporation. Experience, expertise and competence of the Directors are critical factors for value addition to its business. In agency theory, Board is seen mainly as a control mechanism, regularising and supervising the managers on behalf of the shareholders.

Boards of directors are a crucial part of the corporate structure. The board’s primary role is to monitor management on behalf of the shareholders .The law imposes on the board a strict and absolute fiduciary duty to ensure that a company is run in the long term interests of the owners, the shareholders.

Independence of Directors will be cornerstone of corporate governance in the twenty first century. This will ensure that the Board takes independent and objective decision in the best interests of the corporation and all stakeholders. The board should be able to exercise objective independent judgement on corporate affairs. Boards should consider assigning a sufficient number of non-executive board members capable of exercising independent judgement to tasks where there is a potential for conflict of interest. Examples of such key responsibilities are ensuring the integrity of financial and non-financial reporting, the review of related party transactions, nomination of board members and key executives, and board remuneration.

Public Enterprise Management in India– A Paradigm Shift

Liberalization of the economy in 1991 resulted in a paradigm shift in the policy of the Govt. of India towards the public sector enterprises. The enterprises lost the monopoly assured by the government. The regime of commanding heights for the public sector gave way to the environment of market economy. State protection and budget support available to the public enterprises in the twentieth century has given place to challenge of competition and domination of market forces in the twenty first century .The paradigm shift in public sector policy changed the scenario from controlled economy to market economy, full govt. ownership to disinvestment, unlimited life to threat of liquidation, employment generation to manpower rationalization ,liberal budget support to withdrawal of support, departmental Board to independent Board and limited autonomy to enhanced autonomy.

The public sector has to face competition instead of protection .Public enterprises were subjected to disinvestment to reduce state ownership. The non-performing and sick public enterprises faced the prospect of closure due to withdrawal of budgetary grants. At the same time, the government reduced excessive control over the enterprises and granted certain measure of autonomy to the PSEs. Boards of the enterprises were given powers to take objective and informed decisions. Board’s independence was enhanced by minimizing the presence of government directors and by inducting outside independent directors in the Board.

12

In the last half century, the central public sector enterprises have passed through four phases of growth. The first phase (1956-1991) was marked by commanding heights for the public sector .The second phase (1991 onwards) was guided by Policy of Economic Liberalisation with the following elements:

Strategic, high-tech and essential infrastructure area to be opened up to the private sector.

Sick PSEs be referred to BIFR. Social security mechanism to protect workers. A part of the government’s share-holding in the public sector would be offered. Autonomy to Public Sector Professionalization of public sector Boards . MOU between Enterprise and Ministry.

Third phase (1999-2004) saw the privatisation of some CPSEs either in full or part under the Policy of Privatisation of Public Enterprises in force with following policy guidelines:

Restructure & revive potentially viable PSEs.

Close down PSEs, which cannot be revived.

Reduce Government equity in non – strategic PSEs to 26% or lower.

Interest of Employees will be protected.

In the fourth phase, the government policy provided for strong and effective public sector under the National Common Minimum Programme (June 2004) as :

Strong & effective public sector.

Social objectives to be met by commercial functioning.

Full managerial , commercial autonomy to profit making PSUs

Generally, no privatization of profit making companies.

Existing Navratnas will be retained in the public sector.

To modernize & restructure sick CPSEs.

CPSEs are encouraged to enter capital market.

Chronically sick CPSEs to be sold off/closed.

Economic reforms with human face.

Central PSEs

From a mere five central public enterprises in 1951 with an investment of Rs.29 cr the Central Public Sector has grown to a size of 249 CPSEs with an investment of Rs.6,66,848 cr

13

in March 2011. The ten year performance of CPSEs is given in Table 1.The CPSEs play a critical role in the Indian economy and contributed to the growth in the economy. The highlights of the performance of CPSEs (2010-11) as per PE Survey are :

14

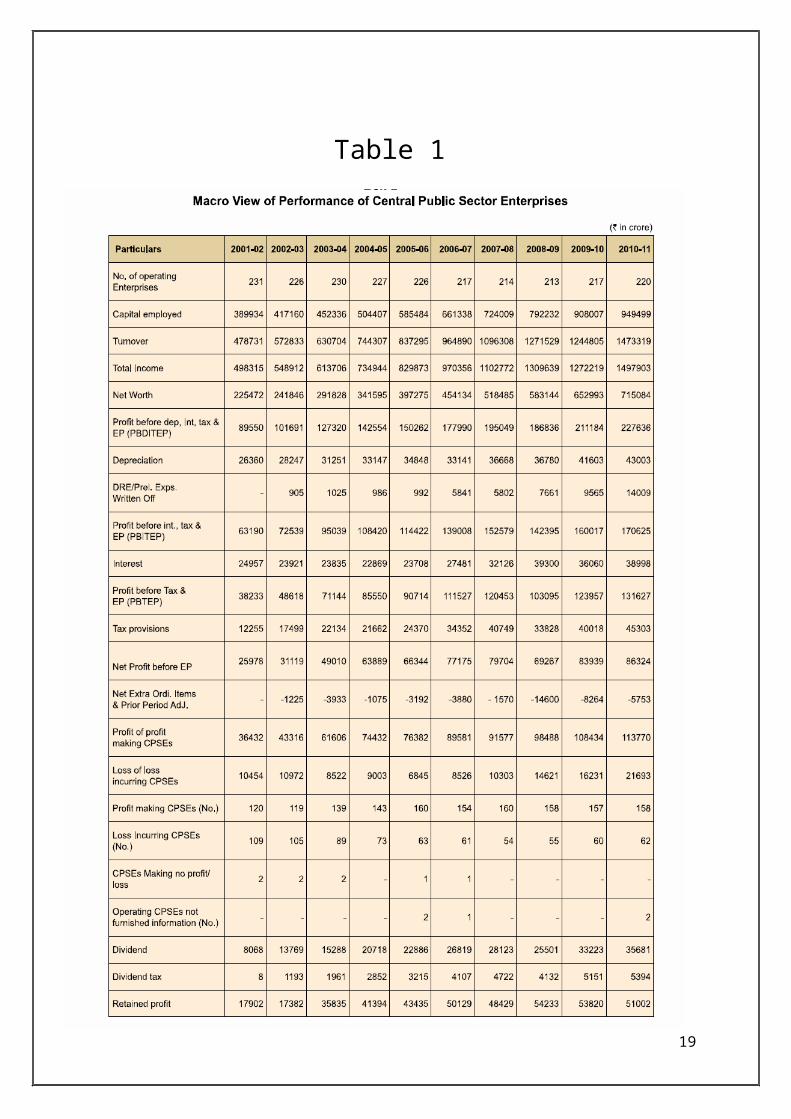

Table 1

15

(i) Total investment (equity plus long term loans) in all CPSEs stood at Rs.6,66,848 crore as on 31.3.2011 compared to Rs.5,80,784 crore as on 31.3.2010, recording a growth of 14.82%.

(ii) Total turnover of all CPSEs during 2010-11 was Rs.14,73,319 crore compared to Rs.12,44,805 crore in the previous year showing an increase of 18.36%.

(iii) Profit of profit making CPSEs stood at Rs.1,13,770 crore during 2010-11 compared to Rs.1,08,434 crore in 2009-10 showing a growth of 4.92%.

(iv) Loss of loss incurring CPSEs stood at Rs.21,693 crore in 2010-11 compared to Rs.16,231 crore in 2009-10 showing an increase in loss by 33.57%.

(v) Overall net profit of all 220 CPSEs during 2010-11 stood at Rs.92,077 crore compared to Rs.92,203 crore during 2009-10 showing a reduction of 0.14%.

(vi) Reserves & Surplus of all CPSEs went up from Rs.6,05,637 crore in 2009-10 to Rs.6,55,488 core in 2010-11, showing an increase by 8.23%.

(vii) Net worth of all CPSEs went up from Rs.6,59,437 crore in 2009-10 to Rs.7,23,128 crore in 2010-11 registering a growth of 9.66%.

(viii) Contribution of CPSEs to Central Exchequer by way of excise duty, customs duty, corporate tax, interest on Central Government loans, dividend and other duties and taxes increased from Rs.1,39,918 crore in 2009-10 to Rs.1,56,124 crore in 2010-11, showing an increase of 11.58%.

(ix) Foreign exchange earnings through exports of goods and services increased from Rs.84,224 crore in 2009-10 to Rs.97,004 crore in 2010-11, showing a growth of 15.17%.

(x) CPSEs employed 14.44 lakh people (excluding casual labours) in 2010-11 compared to 14.90 lakh in 2009-10, showing a decrease in employees by 3.09%.

GOI delegated varying degrees of financial powers to the Boards of CPSEs depending on size, performance, and profitability of the company. Boards can incur capital expenditure up to different limits as per category of PSU. Grant of enhanced powers include power of incurring capital expenditure, joint venture, HR policies, raising capital from domestic and international markets etc. The categories are:

1. Profit making enterprises,

16

2. Mini Ratna Enterprises,

3. Nava Ratna Enterprises

4. Maha Ratna Enterprises

The contributions of CPSEs have been many fold .The product profile of CPSEs has been far and wide covering every sector of the economy. Central public sector enterprises offer a wide range of products and services which include manufacturing of steel; heavy machinery, machine tools, instruments, heavy machine building equipments, heavy electrical equipments for thermal and hydel stations, transportation equipments, telecommunication equipment, ships, sub-marines, fertilizers, drugs and pharmaceuticals, petrochemicals, cement textile, mining of coal and minerals, extraction and refining of crude oil, operation of air, sea, river and road transport, national and international trade, consultancy, contract and construction services, inland and overseas telecommunication services, generation and transmission of power, financial services, a few consumer items such as newsprint, paper and contraceptives, hotel and tourists services, etc.The CPSEs have played a strategic role in the national economy and made significant contributions to the economy like :

Building strong Industrial and infrastructure base for India

Major presence in vital sectors like petroleum, power, telecom, steel, aviation, coal, mining, engineering

Monopoly in defence industries, atomic energy, railways.

Section 25 companies provide welfare services to SCs, STs, backward classes, minorities, handicapped.

Employment generation (-14.44lakh manpower as on -)

Turnover Rs- lakh as on –Rs 14.73 lac cr

Contribution to Exchequer – Rs. 1,56lac Cr

Competition/cooperation with private sector.

Ensuring price stability of vital and sensitive products ( like oil ,gas steel ,coal ,power , aluminium )and protection of consumer interests

India brand promotion

17

ANALYSISOF

ISSUES

18

CORPORATE GOVERNANCE

19

CORPORATE GOVERNANCE

With the globalization of business, corporate governance, a term virtually unknown earlier, has now become a mainstream topic. Every country is critically examining its corporate laws and regulations and adopting new standards to enhance corporate ethics and accountability.

CPSEs must ensure good governance to be effective in the competitive environment. Emphasis must be placed as much on performance and delivery as on corporate governance. Corporate governance deals with the accountability of management of the company to the shareholders, fiduciaries duties of directors, disclosure of strategic information regarding the company, audit of transactions, control and direction by the Board and above all, responsibility to the society. There is an increasing demand from the stakeholders for adoption of socially relevant corporate governance practices.

The Board of Directors, being the fulcrum of the corporate governance structure, has to play a strategic role in securing sustainable development of the company to safeguard the long – term interests of shareholders.

DPE have issued corporate governance guidelines and corporate governance (CG) Score for CPSEs. It is necessary to review the 100 pt format for assessment of CG score for CPSEs, based upon experience of last one year. It may be appropriate to revise some of the parameters in the format or to modify the award of the marks to individual parameters.

One of the first endeavours was the Confederation of Indian Industry: Code for Desirable Corporate Governance, developed by a committee chaired by Rahul Bajaj, a leading industrial magnate. The committee was formed in 1996 and submitted its code in April 1998. Later the SEBI constituted two committees to look into the issue of corporate governance; the first chaired by Kumar Mangalam Birla, and the second by Narayana Murthy. The first Committee submitted its report in early 2000, and the second three years later. These two committees have been instrumental in bringing about far reaching changes in corporate governance in India through the formulation of Clause 49 of Listing Agreement.

Concurrent with these initiatives by the SEBI, the Department of Company Affairs of the Government of India also began contemplating improvements in corporate governance. These efforts included the establishment of a study group to operationalize the Birla Committee recommendations in 2000, the Naresh Chandra Committee on Corporate Audit and Governance in 2002, and the Expert

20

Committee on Corporate Law (J.J. Irani Committee) in late 2004. All of these efforts were aimed at reforming the existing Companies Act of 1956 that still forms the backbone of corporate law in India.

Clause 49 of the Listing Agreements

The SEBI implemented the recommendations of the Birla Committee through the enactment of Clause 49 of the Listing Agreements. Clause 49 may well be viewed as a milestone in the evolution of corporate governance practices in India. The key mandatory features of Clause 49 regulations deal with the following: (i) composition of the board of directors; (ii) the composition and functioning of the audit committee; (iii) governance and disclosures regarding subsidiary companies; (iv) disclosures by the company; (vi) CEO/CFO certification of financial results; (vi) reporting on corporate governance as part of the annual report; and (vii) certification of compliance of a company with the provisions of Clause 49.

The composition and proper functioning of the board of directors emerges as the key area of focus for Clause 49. It stipulates that non-executive members should comprise at least half of a board of directors. It defines an “independent” director and requires that independent directors comprise at least half of a board of directors if the chairperson is an executive director and at least a third if the chairperson is a non-executive director. It also lays down rules regarding compensation of board members, sets caps on committee memberships and chairmanships, lays down the minimum number and frequency of board meetings, and mandates certain disclosures for board members.

Clause 49 pays special attention to the composition and functioning of the audit committee, requiring at least three members on it, with an independent Director as Chairman and with two-thirds made up of independent directors. The Clause spells out the role and powers of the audit committee and stipulates minimum number and frequency of and the quorum at the committee meetings. With regard to “material” non-listed subsidiary companies (those with turnover/net worth exceeding 20% of a holding company’s turnover/net worth), Clause 49 stipulates that at least one independent director of the holding company must serve on the board of the subsidiary. The audit committee of the holding company should review the subsidiary’s financial statements, particularly its investment plans. The minutes of the subsidiary’s board meetings should be presented at the board meeting of the holding company, and the board members of the latter should be made aware of all “significant” (likely to exceed in value 10% of total revenues/expenses/assets/liabilities of the subsidiary) transactions entered into by the subsidiary.

The areas where Clause 49 stipulates specific corporate disclosures are: (i) related party transactions; (ii) accounting treatment; (iii) risk management procedures; (iv) proceeds from various kinds of share issues; (v) remuneration of directors; (vi) a Management Discussion and Analysis section in the annual report discussing general business conditions and outlook; and (vii) background and committee memberships of new directors as well as presentations to analysts. In addition, a board committee with a non-executive chair is required to address shareholder/investor grievances. Finally, it is mandated that the process of share transfer (that had been a long-standing problem in India) be expedited by delegating authority to an officer or committee or to the registrar and share transfer agents.

The CEO and CFO or their equivalents need to sign on the company’s financial statements and disclosures and accept responsibility for establishing and maintaining effective internal control systems. The company is also required to provide a separate section of corporate governance in its annual report, with a detailed compliance report on corporate governance. It is also required to

21

submit a quarterly compliance report to the stock exchange where it is listed. Finally, it needs to get its compliance with the mandatory specifications of Clause 49 certified by auditors or by practicing company secretaries. In addition to these mandatory requirements, Clause 49 also mentions non-mandatory requirements concerning the facilities for a non-executive chairman, the remuneration committee, half-yearly reporting of financial performance to shareholders, moving towards unqualified financial statements, training and performance evaluation of board members, and perhaps most notably a clear “whistle blower” policy.

By and large, the provision of Clause 49 with respect to the distinction drawn between boards headed by executive and non-executive chairmen and the lower required share of independent directors is special to India—and is also somewhat intriguing, given the prevalence of family-run business groups. The market reaction to the corporate governance improvements sought by Clause 49 seems to have been quite positive.

Towards better Corporate Governance in Public Enterprises

The share of public enterprises in India represents a substantial part of the GDP, employment and market capitalisation. They continue to make significant contributions in almost all sectors of the national economy and earn sizeable revenues for the state. Their overall performance has been comparable to and sometimes even higher than the corporations in the private and multinational sectors. In spite of spate of disinvestments and privatisation, the public enterprises continue to remain a dominant feature of the economy. Nevertheless, public enterprises face distinct governance challenges. They may suffer just as much from ownership interference as from totally passive or distant ownership by the state. Corporate governance problems arise from the fact that the accountability for the performance of SOEs involves a complex chain of agents like the management, board, government Directors, the ministries and the government. The principals (owners) on behalf of the state are not clearly or easily identifiable. In such a situation, there is a clear dilution of accountability. To comply with such complex web of accountabilities in efficient decision making and good corporate governance is a challenge for public enterprises.

The main criticisms in the governance of SOEs have been interference by outside sources of power in the affairs of the enterprises. Interference may take place in the selection, appointment of CMDs and Directors in the Board and senior management as well as in the decision-making process. Such interference may also be in respect of investments, raw material purchases, recruitment, downsizing, transfers, promotions, outsourcing, vendor selection, transport contracts, labour contracts, civil work and selection of bankers/insurers and the like in one form or the other.

Arjun Sengupta Committee Report (2005) on autonomy and empowerment of CPSEs recommended inter alia that :

Departments should be custodians of public enterprises on behalf of Government and public at large.

Ministries to maintain arms-length-distance from the CPSEs

Not more than two Govt. nominees on the Board.

22

In extraordinary situations, Govt. may give instructions to the Company only through directives as per due procedure.

There should be a negative list of areas which must be kept away from the intervention of the Government due to their commercial, operational or administrative nature.

Government need to initiate policy measures to improve corporate governance in India’s public sector. The code for public enterprises should cover their legal and regulatory framework, the ownership issues of the state, issues of accountability of the principals (owners) and the agents like the Directors and managers, equitable treatment of shareholders other than the state, protection of interests of all stakeholders, issues of transparency and disclosures, and finally the authority, responsibility and accountability of the Board of Directors. Globally accepted codes like the OECD Code ( 2005 ) may be taken as benchmarks.

Department of Public Enterprise (DPE) also came out with Corporate Governance guidelines for CPSEs time to time. These guidelines on Corporate Governance are formulated with the objective that the CPSEs follow the guidelines in their functioning. Proper implementation of these guidelines would protect the interest of shareholders and relevant stakeholders.

The Department of Public Enterprises (DPE) had issued guidelines on composition of Board of Directors of Central Public Sector Enterprises (CPSEs) in 1992. According to these guidelines at least one-third of the Directors on the Board of a CPSE should be non-official Directors. The Maharatna, Navratna and Miniratna schemes provide that exercise of the enhanced powers delegated to these CPSEs is subject to the condition that their Boards are professionalised by inducting adequate number of non-official Directors, with minimum of four in case of Maharatna, Navratnas and minimum of three in case of Miniratnas. The schemes for Maharatna, Navratna and Miniratna CPSEs also provide for setting up of Audit Committees.

In November 2001, DPE issued further guidelines on the composition of Board of Directors of listed CPSEs. It provided that the number of Independent Directors should be at least one-third of the Board if the Chairman is non-executive, and not less than 50% if the Board has an executive Chairman. Relevant extracts of Clause 49 of the Listing Agreement with Stock Exchanges issued by Securities and Exchange Board of India (SEBI) forms part of the said guidelines.

To bring in more transparency and accountability in the functioning of CPSEs, the Government in June, 2007 introduced, Guidelines on Corporate Governance for CPSEs. These Guidelines were of voluntary nature. Since the issue of these guidelines, the CPSEs have had the opportunity to implement them for the whole of the financial year 2008-09. These Guidelines have been modified and improved upon based on the experience gained during the experimental period of one year. The Government have felt the need for continuing the adoption of good Corporate Governance Guidelines by CPSEs for ensuring higher level of transparency and decided to make these Guidelines mandatory and applicable to all CPSEs.

Apart from these instructions of DPE, the CPSEs are governed by the Companies Act, 1956 and regulations of various authorities like Comptroller and Auditor General of India (C&AG), Central Vigilance Commission (CVC), Administrative Ministries, other nodal Ministries, etc. Further, some principles of Corporate Governance are already in vogue in public sector because (a) the Chairman,

23

Managing Director and Directors are appointed independently through a prescribed procedure; (b) Statutory auditors are appointed independently by the C&AG; (c) Arbitrary actions, if any, of the Management can be challenged through writ petitions; (d) Remuneration of Directors, employees, etc. are determined on the basis of recommendations of Pay Committees constituted for this purpose; etc.

Effective corporate governance in the public enterprises requires proper balance among the power tripod of the government, the board and the management. The government as the owner, the board as the decision-making authority and the managers as the agents of the owners have to play their mutually supportive roles. They have to observe the rules of distribution of authority and responsibility among them.

Accountability implies accounting for one’s actions and to report on the achievement (or failure with explanation) of the objectives and responsibilities assigned to an individual or group: Three main issues arise in this regard : Accountability for what? To whom? And How? It involves methods and procedures of assessing accountability. Public enterprise management involves multiple levels of accountability in respect of their relationship with the government and its ministries, parliament and its committees, CAG, CVC, Courts (enterprises being wings of welfare state), media , statutory bodies, society and of course shareholders ( particularly in listed companies).

The government nominee Director in the Board of CPSE enjoys a privileged status in the Board. Certain decisions cannot be taken in his absence. Board meetings are usually fixed keeping in mind his availability. On one hand he is the nodal officer in the Ministry for the affairs of the particular CPSE: on the other he is also a Director in the Board, who has the responsibility of ensuring that the rules, regulations and policies of the Ministry and the government are complied with while arriving at decisions in the boardroom. He is also expected to report back to his Ministry on important aspects regarding deliberations in the boardroom. Further he is also the link between the CPSE and the government. He is expected to take necessary follow up action in the Ministry. He is to provide information to the Ministry and look intervention by the Ministry/Government, as necessary.

In view of the above, the duties responsibilities and accountability of government nominee Director regarding his work in Boardroom needs to be revisited and specified in the contemporary environment of faster decision making and empowerment of Board for facing emerging challenges. The contribution of government nominee Directors to the company, should be evaluated appropriately by the Board / Ministry like other Directors (Functional/Independent).

Duties, responsibilities and accountability of the majority shareholders are vital aspects of corporate governance architecture. Similarly rights and safeguards of minority shareholders assume significance with increasing levels of disinvestment of government shareholding in the CPSEs. In this context the day-to-day working relationship between the owners and the management of the enterprise needs to be stated clearly and should be well understood without ambiguity. The AGE (Adhoc Group of Experts) report (2005) submitted under Chairmanship of Arjun Sengupta can be basis for further refinement of Ministry-CPSE relationship in the emerging competitive environment. Often there are fears of audit and vigilance investigation in minds of executives while taking decisions in the company. The enforcement mechanism of vigilance and audit wings may be made

24

more affective; at the same time facility of pre audit or prevention vigilance must be made available to executives and wings of the enterprise if requested by them in the decision making process.

The following role models for the three entities namely the Shareholders (Govt), Directors and Managers (forming the tripod of corporate governance) can be considered:

Role of the Government

(1) The government as the majority owner must establish a clear and consistent ownership policy with ownership functions defined.

(2) Power and responsibility on behalf of the government should be spelt out at appropriate levels in clear terms with concomitant accountability.

(3) Government must allow full functional autonomy to the public enterprises.(4) Government must not interfere in the day-to-day management of the enterprises and allow the

Boards to exercise their authority in an independent manner.(5) The government should establish transparent nomination processes for Board of Directors of

the enterprise. The boards should be appropriately composed to ensure their objective and independent judgement.

(6) Boards should have the powers to appoint and remove the Directors in the first stage and have the same authority in respect of the CEO at an appropriate stage in due course.

(7) The enterprises should not be asked to perform duties not mandated by laws or regulations(8) The government should dilute its shareholding to a level of 75% and even below upto 51% by

offering the shares to general public, mutual funds and financial institutions. This will unleash the vast potential locked up in the public enterprises.

(9) The government as the majority shareholder should respect the voice of the minority shareholders and not impose its will on other shareholders. There should be more democracy for all shareholders.

(10) The government should decide and declare a negative list of items and activities over which there will be full authority of the Board without any interference from government.

Role of the Board of Director

(1) The Boards of the public enterprises should consist of competent, capable and experienced professionals who can take independent and informed decisions in the best interest of the public enterprises.

(2) The Board should be independent of both the owners and the management, in particular, the Board of public enterprises should maintain arms-length distance from the government.

(3) Directors should act with integrity and be held accountable for their actions. The Board should assess its own performance.

(4) The independent directors as conscience keepers of the corporations should be selected by the Board and appointed by the shareholders with clear duties and responsibilities. The independent directors should be more proactive in initiating board agendas aimed at ethics, social responsibility and sustainability of the enterprise. The performance of the independent Directors should be evaluated by the Board based upon their self-assessment.

25

(5) The Directors should ask questions to elicit full information from the management. Passive acceptance of the views of the management by the Board may not be in the interests of the company.

(6) The Board should balance the interests of all stakeholders in an objective and judicious manner.(7) The Board should earmark a certain percentage of its net profits for activities towards corporate

social responsibility. However, while doing so, the Board should commit resources of the company judiciously keeping in view the long-term interests of the company.

(8) The Board should strive towards continued value addition to the public enterprise and ensure its long-term sustainability. The Board should have a risk management plan in line with the strategy of the private sector corporations.

(9) The Board must give adequate information on important activities of the public enterprises to all shareholders.

(10) The Board should rationalise the internal audit system and internal vigilance mechanism to build up effective processes and procedures in the corporation.

Role of the Managers

(1) The managers, as the agents of the shareholders and the officers of the Board, should be professionally competent, responsible and trustworthy.

(2) The managers should devote their fulltime attention for value addition to the enterprise. They should be loyal and diligent in discharge of their duties.

(3) The managers will have to ensure observance of code of ethics in their work in relation with the customers, vendors and business partners.

(4) Managers must help the Board reduce agency costs of management.(5) Every manager must strive to observe utmost economy, cut down cost of production and

eliminate wasteful expenditure in order to make the enterprise competitive.(6) Every manager should contribute to prevention of malpractices, corruption and abuse of

authority in the enterprises and should act as whistle blower to unearth malpractices and cases of breach of ethical values in the enterprise.

(7) The advantage of professional competence possessed by the managers in public enterprises must translate into higher productivity and creativity in the interest of long-term sustainability of the public enterprises.

Other issues which are relevant for better corporate governance of CPSEs are:

Non Filling of posts of CMDs, functional directors and independent directors in time: This issue emerged during the Director’s Conclave organised on 28th-29th September’12, wherein majority of the participants shared it as a key limiting factor in having right Corporate governance.

CMD is not associated in the selection of independent directors or functional directors. (whereas in private sector only CMD appoints them): During the same conclave, it also

26

emerged as a unanimous expectation that not involving CMD in the selection of the IDs or Functional Directors leads to having members with divergent perspectives, which actually derails decision making

Training of functional directors / Independent directors / government directors (In particular few government directors go for training even though many of them may not have any experience in corporate governance or public enterprise management: This aspect was captured during the panel discussion of representatives of CPSEs and DPE being organised on 29th November’12 at Delhi, wherein number of participants shared, the lack of understanding of board members about the real issues and challenges faced by CPSEs in operationalizing their demands. Thus the suggestion of sensitizing them for atleast a week was proposed.

Remuneration of independent directors is very low as compared to much higher compensation in private sector: This aspect of remunerating the board members of CPSEs was shared by the people who are actually on the board of various companies both in public and private sector. They put it across as a de-motivating factor and a reason of less attendance in CPSE board meetings. This was captured from the two Advisory committee meetings of Centre for Corporate Governance & Social Responsibility, IMI New Delhi and also the Director’s Conclave.

Absence of risk management plan as approved by the board: This is one issue of corporate governance which was pointed out during the MDP on MoU Document attended by senior executives of CPSEs, interaction with the heads of divisions of CPSEs and also in the panel discussion held on 29th November’12

27

CORPORATE SOCIAL RESPONSIBILITY

28

CORPORATE SOCIAL RESPONSIBILITY

Corporate social responsibility (CSR) promotes a vision of business accountability to a wide range of stakeholders, besides shareholders and investors. Key areas of concern are environmental protection and the wellbeing of employees, the community and civil society in general, both now and in the future.

The concept of CSR is underpinned by the idea that corporations can no longer act as isolated economic entities operating in detachment from broader society. Traditional views about competitiveness, survival and profitability are being swept away.

Some of the drivers pushing business towards CSR include:

1. The shrinking role of government

In the past, governments have relied on legislation and regulation to deliver social and environmental objectives in the business sector. Shrinking government resources, coupled with a distrust of regulations, has led to the exploration of voluntary and non-regulatory initiatives instead.

2. Demands for greater disclosure

There is a growing demand for corporate disclosure from stakeholders, including customers, suppliers, employees, communities, investors, and activist organizations.

3. Increased customer interest

There is evidence that the ethical conduct of companies exerts a growing influence on the purchasing decisions of customers. In a recent survey by Environics International, more than one in five consumers reported having either rewarded or punished companies based on their perceived social performance.

29

4. Growing investor pressure

Investors are changing the way they assess companies' performance, and are making decisions based on criteria that include ethical concerns. The Social Investment Forum reports that in the US in 1999, there was more than $2 trillion worth of assets invested in portfolios that used screens linked to the environment and social responsibility. A separate survey by Environics International revealed that more than a quarter of share-owning Americans took into account ethical considerations when buying and selling stocks.

5. Competitive labour markets

Employees are increasingly looking beyond paychecks and benefits, and seeking out employers whose philosophies and operating practices match their own principles. In order to hire and retain skilled employees, companies are being forced to improve working conditions.

6. Supplier relations

As stakeholders are becoming increasingly interested in business affairs, many companies are taking steps to ensure that their partners conduct themselves in a socially responsible manner. Some are introducing codes of conduct for their suppliers, to ensure that other companies' policies or practices do not tarnish their reputation.

Some of the positive outcomes that can arise when businesses adopt a policy of social responsibility include:

1. Company benefits:

Improved financial performance; Lower operating costs;

Enhanced brand image and reputation;

Increased sales and customer loyalty;

Greater productivity and quality;

More ability to attract and retain employees;

Reduced regulatory oversight;

Access to capital;

Workforce diversity;

Product safety and decreased liability.

2. Benefits to the community and the general public:

Charitable contributions; Employee volunteer programmes;

Corporate involvement in community education, employment and homelessness programmes;

30

Product safety and quality.

3. Environmental benefits:

Greater material recyclability; Better product durability and functionality;

Greater use of renewable resources;

Integration of environmental management tools into business plans, including life-cycle assessment and costing, environmental management standards, and eco-labelling.

Nevertheless, many companies continue to overlook CSR in the supply chain - for example by importing and retailing timber that has been illegally harvested. While governments can impose embargos and penalties on offending companies, the organizations themselves can make a commitment to sustainability by being more discerning in their choice of suppliers.

The concept of corporate social responsibility is now firmly rooted on the global business agenda. But in order to move from theory to concrete action, many obstacles need to be overcome.

A key challenge facing business is the need for more reliable indicators of progress in the field of CSR, along with the dissemination of CSR strategies. Transparency and dialogue can help to make a business appear more trustworthy, and push up the standards of other organizations at the same time.

Commercial viability of a corporate enterprise is vital for survival. Yet profit alone cannot guarantee its long term sustainability. The non-financial objectives have implications for society and environment and are becoming increasingly significant for future of business organizations. There is growing acceptance that it is not enough to just comply with the provisions of law or economics, but to go beyond compliance and invest more into human capital, the environment and the society. The concepts of social responsibility & sustainable development are emerging as major issues of corporate strategy.

Buyers, investors and employees are likely to favour companies that apply CSR principles, when buying, investing, or deciding to work. Further according to KPMG survey CSR has become mainstream. The proportion of the world’s 250 largest companies issuing annual reports on CSR increased from 50% in 2005 to 80% in 2008.

The problem with corporate social responsibility (CSR) is that nobody is very clear about what exactly it encompasses. The Indian government has been trying to make it mandatory for companies to spend at least 2% of net profits on CSR. Facing strong criticism, it gave up the effort in 2009 and made the spending voluntary. But the debate continues.

If the proposed rule had come into play, the government would have had to spell out what constitutes CSR. That would have gone some way in removing the vagueness that exists about the term. Today, CSR to some companies means providing lunch to employees. To others, it's about

31

tackling global warming and environmental issues. Instead of defining CSR, the Indian government recast it as "responsible business" in a set of voluntary guidelines for firms

Industry has been almost totally against a mandatory clause. The Federation of Indian Chambers of Commerce & Industry (FICCI) has suggested tax breaks instead for those who meet the voluntary targets. Rival chamber the Confederation of Indian Industry (CII) says that compulsory corporate responsibility would be counterproductive. "Companies may resort to camouflaging activities to meet such regulations, particularly during recessionary periods and economic downturns," argues the lobbying group.

India's philanthropic community is also against compulsory CSR. "It is a crazy idea," says Dhaval Udani, CEO of non-governmental organization (NGO) GiveIndia. "Once you make it mandatory, people will find ways and means to get out of it. The rules will be so vague that the reporting will be even vaguer." Deval Sanghavi, co-founder & CEO of Dasra, a strategic philanthropy foundation, agrees. "I am not in favor of mandatory CSR. When you make things mandatory, the chances of their not being done are greater," he notes.

Industrialist Adi Godrej adds, "It's good to say that [CSR] is desirable. Then people should decide [what to do] on their own." Philanthropist Rohini Nilekani is more critical. "I just don't get it," she says. "This is outsourcing of governance. This is taking the failure of the state and the corporates and trying to create a model out of it. If you want, you tax the corporates and put the money into social programs. But you can't dictate CSR."

The world over, very few countries have a CSR requirement; Saudi Arabia is possibly the only exception. "The laws in developed countries do not stipulate mandatory CSR contributions," according to KPMG partner (development sector practice) Sudhir Singh Dungarpur. "In the recent past, many European countries have specified that companies must include CSR information in their annual reports."

India may become the world’s first country to make corporate social responsibility mandatory . Paths have been cleared for reintroduction of the Companies Bill, 2011, in the ongoing winter session. If the bill is passed after endorsing all the propositions made by the Parliamentary Standing Committee on Finance, corporate social responsibility (CSR) would become mandatory for the first time in the world in any country.

The statement advocates that those companies with net worth above Rs. 500 crore, or an annual turnover of over Rs. 1,000 crore, shall earmark 2 percent of average net profits of three years towards CSR. In the draft Companies Bill, 2009, the CSR clause was voluntary, though it was mandatory for companies to disclose their CSR spending to shareholders. It also suggested that company boards should have at least one female member.

Another problem of implementation of CSR activities is that there should not be one CSR Hub for the entire country. Number of CSR monitoring Hubs may be created across the country. They are supposed to be doing data collection, monitoring, survey & benchmarking, field study, project formulation and also evaluation. In view of huge volume of work involved, it is advisable that more agencies be involved.

32

The MoU guidelines lay stress on the link of Corporate Social Responsibility with sustainable development and define Corporate Social Responsibility (CSR) as a philosophy wherein organizations serve the interest of society by taking responsibility for the impact of their activities on customers, employees, shareholders, communities and the environment in all aspects of their operations. Decisions of corporations should be based upon social and environmental consequences. Shareholders and investors prefer investing in companies with high social responsibility. Consumers are sensitized to CSR policies of companies while buying goods and services. This brings pressure on corporations to operate in economically, socially and environmentally sustainable manner.

In the context of above background research and the deliberations with all the stakeholders, the study group developed an unbiased perspective of what CSR is all about?, what are its challenges? And what really is the ailment of CPSEs?, due to which CSR initiatives has remained adhoc, sketchy and in piece meal. On the basis of evaluation of the MoU documents submitted by CPSEs for the year 2010-2011, and the above understanding, it can be inferred upon that the following issues need immediate attention from the respective stakeholders and antidotes be developed for better and improved performance of the CPSEs. The issues are:

CSR Issues:

Absence of CSR Plan approved by the board: This aspect was shared by number of representatives of CPSEs during the panel discussion and in the MDP on MoU for CPSEs that normally whatever is been implemented is on adhoc basis, onetime affair simply to comply with financial obligations to secure marks.

Regular review of CSR activities by the board: In deliberations with various stakeholders, there was a consensus that the board should have more involvement in CSR activities right from planning to review of implementation of the plans.

Rigidity of CSR guidelines: As per the submission of majority representatives of CPSEs in various interactions the flexibility in CSR guidelines is the need of the hour.

Over Emphasis on expenditure rather than outcome: On analysing the MoU documents submitted by various CPSEs for 10-11 the study group found the above as an issue of concern. This is very well reflected in the type of projects undertaken by the CPSEs in the name of CSR activities

Lack of experts / professionals in PSUs to advice on CSR: This aspect has been shared by almost every CPSE we interacted that CSR is not an important function of the organization, they are hiring right capabilities and people are given responsibility, simply either as a punitive measure or at that juncture the CPSE is not in a position to utilise that manpower

Absence of any organizational structure in CPSEs: This aspect came up in almost all the different modes of interactions followed, as stated in the methodology that one and all lack requisite infrastructure.

Social Responsibility to be part of organizational culture and not be confined only to a section. Employees to be sensitized on issues of CSR: As stated earlier also the common

33

concern of all the stakeholders raised in different deliberations is that right from the board to the last employee sensitization on issues of CSR is a must.

Absence of CSR guidelines from the company for their operations: During the MDP on MoU one thing which came out was that there are no clear cut guidelines for operationalizing the CSR activities. This point was also stressed in the panel discussion with representatives of CPSEs

With respect to MoU Document: These are an outcome of the analysis of various MoU documents submitted by different CPSEs for the year 2010-11

o Most of the CSR Projects are sketchy, half hearted and unscientifico CSR are taken on ad hoc basiso Many CSR projects are getting constituency oriented, instead of having a spread

over provincial / national scale as per requirement

34

SUSTAINABLE DEVELOPMENT

SUSTAINABLE DEVELOPMENT

Sustainable development “requires the integration of social, environmental, and economic considerations to make balanced judgments for the long term”. Business must subserve the economic, social and the environmental concerns in their growth strategy. The continuing commitment by business to behave ethically and contribute to economic development while improving the quality of life of the workforce and their families as well as that of the local community and society at large.

Sustainable Development is development that meets the needs of the present without compromising the ability of future generations to meet their own needs. Sustainable Development involves an enduring, balanced approach to economic activity, social progress and environmental

35

responsibility. While conservation of environmental resource is necessary to secure livelihoods and well-being of all, the most secure basis for conservation is to ensure that people dependent on particular resources obtain better livelihood from the fact of conservation than from degradation of the resource.

The term SD came into widespread use in 1987, when the World Commission on Environment and Development of the United Nations published a report known as ‘‘Brutland Report’’. This report stated that sustainable development seeks to “meet the needs of the present without compromising the ability of the future generation to meet their own needs’’ The SD concept gave rise to the triple bottom line approach for adoption by business corporations .The objectives of business should be three fold namely profit , people and planet . Business must subserve the economic , social and the environmental concerns in their growth strategy.

For the business community, sustainability is more than mere window-dressing. By adopting sustainable practices, companies can gain competitive edge, increase their market share, and boost shareholder value. What's more, the growing demand for 'green' products has created major new markets in which sharp-eyed eco-entrepreneurs are reaping rewards. Growing environmental concerns, coupled with public pressure and stricter regulations, are changing the way people do business across the world. Industry is on a three-stage journey from environmental compliance, through environmental risk management, to long-term sustainable development strategies.

Companies integrate sustainable development into their business strategies. Sustainable development is a natural extension of many corporate environmental policies. In the pursuit of economic, environmental and community benefits, management considers the long-term interests and needs of the stakeholders.

Sustainable development strategies uncover business opportunities in issues which, in earlier stages of the journey, might be regarded as costs to be borne or risks to be mitigated. Results include new business processes with reduced external impacts, improved financial performance, and an enhanced reputation among communities and stakeholders.

For the business enterprise, sustainable development means adopting strategies and activities that meet the needs of the enterprise and its stakeholders today while protecting, sustaining and enhancing the human and natural resources that will be needed in the future.

From the year 2010-2011, Department of Public Enterprises has included Sustainable Development as a compulsory element for CPSEs under ‘Non Financial parameters’ having a weightage of 5% (5 Marks) in MoU for CPSEs

After going through the various stages of our methodology explained before, the study group consolidated the following major issues related to Sustainable Development, which are the challenges faced by CPSEs by the year 2010-2011 and are in need of immediate response:

S D Issues:

Overlap between CSR and SD may take place, thus it requires clarity: As per the submission of majority representatives of CPSEs in various interactions overlap of CSR and SD is a major point of concern. The operation executives look forward for far better clarity from the boards.

36

At present SD is reduced to implementing few schemes on a scattered basis. Comprehensive SD plan for an entire company must be drawn, and schemes must be part of the comprehensive plan: On analysing the MoU documents submitted by various CPSEs for 10-11 the study group found the above as an issue of concern. This is very well reflected in the type of projects undertaken by the CPSEs in the name of SD activities

SD reporting is not taking place nor a proper format of SD reporting is evolved: It came up during various interactions that in majority of the CPSEs excluding few Maha & Nava Ratnas none of them have a standard format for SD reporting.

Review of SD by the boards is not taking place: During the panel discussion with representatives of CPSEs it was stressed that SD do not get adequate attention from the boards and thus very few schemes are being implemented on year to year basis.

Non -availability of expert manpower and Training of executives on SD is minimal: This aspect was captured during the panel discussion of representatives of CPSEs and DPE where lack of availability and also training of involved manpower on challenges faced by CPSEs with respect to SD is negligible.

Sensitizing entire organization on challenges of SD: The common concern of all the stakeholders raised in different deliberations is that right from the board to the last employee sensitization on challenges of SD is not happening.

37

RESEARCH &

DEVELOPMENT

RESEARCH & DEVELOPMENT

Research and development, often called R&D, is a phrase that means different things in different applications. In the world of business, research and development is the phase in a product's life.

Research and development is an investment in a company's future - companies that do not spend sufficiently in R&D are often said to be 'eating the seed corn'; that is, when their current product lines become outdated and overtaken by their competitors, they will not have viable successors in the pipeline. So how much is reasonable to spend on research and development? That is highly dependent both on the technology area and how fast the market is moving. Two percent of company revenue, not profit, might be enough in a fairly sedate market, but to keep up in rapidly changing markets, companies should expect to spend fifteen percent or more in research and development just to keep up with the rest of the pack.

38

In any well-run company, research and development have strictly commercial functions - to further the company's business objectives by creating better products, to improve operational processes and to provide expert advice to the rest of the company and to customers.

Manufacturing companies must overcome significant obstacles in the research and development arena if they are to maintain a strong market position. By enhancing innovation and speeding time-to-market, companies can win market share and avoid negative product margins.

R&D assumes great value for the business enterprises due to rapid changes in technology, competitive market and customer demands. In the present MoU format five marks are reserved for each CPSE irrespective of the type or need for R&D in the enterprises. It is appropriate to examine whether non-manufacturing enterprise or even all manufacturing enterprises need the R&D expenditure or not.

The basic rationale behind R&D activities is the changed business environment, highly competitive markets, the rapid pace of change in technology, stringent quality control criteria, heightened expectations and demands of customers, lack of transfer of technology and know-how from competitors, etc.

R&D activities by CPSEs results in substantial increase in market share and demonstrable increase in competitiveness. It leads to greater increase in profitability for manufacturing firms and a greater reduction in costs for services firms. R&D activities can help strengthen our country’s technological strength and ensure growth and creation of jobs in the country, and also allow CPSEs to address the new challenges and opportunities in an increasingly global world.Focused R&D activities, combined with new international partnerships, can help address pressing global issues such as climate change, health, food security and poverty.

To take advantage of improvement opportunities, it is important first to identify the R&D-related barriers to improved innovation:

Lack of alignment between marketing and R&D Collaboration in a matrix environment Costs of development Lack of an innovation culture Fragmented research efforts for feedback and collaboration Ineffective Product Lifecycle Management Insufficient resources and difficulty getting manufacturing and purchasing to play

stronger roles Pressure to shorten time to product release

Targeting Areas for ImprovementOpportunities to improve management and execution of innovation initiatives include:

Continually monitoring performance of the innovation process by developing and implementing appropriate metrics for performance measurement

Increasing stakeholder involvement in the innovation process through clear definition of roles and responsibilities

Viewing suppliers as strategic partners, not just low-cost providers

39

Developing advanced methods for customer segmentation Evolving an R&D organizational structure that improves cross-functional collaboration

From the ongoing discussions with various stakeholders and their understanding of the parameter Research & Development of the MoU Document, the study group while analyzing the actual MoU documents of CPSEs for the year 2010-2011 ended up with the following outcomes which are an impediment for a better performance by the CPSEs. The issues thus identified and for which recommendations are provided at a later part are:Issues:

Many CPSEs do not have any relevance of R & D, hence they need not be burdened with R&D activities: This aspect came up in almost all the different modes of interactions with the representatives of CPSEs and from all stakeholders.

Manpower, establishment, and administrative cost are drawn from R&D budgets and credited towards R&D expenditure. There should be a yardstick to limit non research expenditure as a percent of R&D budget: This aspect of limiting non research expenditure was captured during the panel discussion of representatives of CPSEs and DPE and also on analysing the MoU documents submitted by various CPSEs for 10-11

Only dedicated and committed executives be selected and posted in R&D wings and R&D units should not be used as a dumping ground: As per the submission of majority representatives of CPSEs in various interactions it was shared that R&D is used as a non productive posting.

R&D should not result in unproductive work and it should be evaluated in terms of advantages and benefits accruing to the company: On analysing the submitted MoU documents, it inferred that many a times R&D expenditure is not directly related to the CPSE and results in no worthwhile contribution

Synergy may be established among different CPSEs, national research labs, academic institutions and other scientific bodies for more effective R&D work and also to avoid duplication: This is one issue which was pointed out during the MDP on MoU Document attended by senior executives of CPSEs, wherein they stressed the synergy among various research organizations.

It is for consideration to establish monitoring organizations for activities of a particular sector of R&D to channelize and coordinate the resources of different CPSEs working in same sector. It may be inter PSU coordination body managed by a lead PSU: This aspect was captured from the interactions with the representatives of CPSEs during the panel discussion organised by DPE, executives were of the opinion of having a coordinated research under holding CPSEs or under one CPSE per sector.

40

41

Increasing Profits of The Profit Making

CPSEs

Increasing Profits of the Profit Making CPSEs

Section 11 (2) of the Indian Companies Act – 1956 says “.......more than 20 persons joining to carry on any business with the object of profit and gain, must form a company and get registered.”

Since all the PSEs are registered as ‘company’ under the Indian companies Act, it is the responsibility of all PSEs to earn profits, whatever business they are in to. Sometimes many people argue that public sector undertaking public money and they must care for social welfare at large but this should

42

also not been forgotten that all companies are meant to create profit/gain. If a company not generating profits and using public money, it is more serious matter.

Indian government also has withdrawn budgetary support to the public sector companies. This support is now available to only some companies as exceptional case and that too for some specific purpose like payment of salary etc or if there is any revival package given to the company. So it has become rather more important for all PSEs to earn profits for its own survival in future.

To enable PSEs to generate profits, government also has given some flexibilities and autonomy in certain decision making and also extended some financial powers to use them for their benefits (refer DPE guidelines). This is important for the CPSEs to use and exercise these powers like Strategic alliances, Joint Ventures and Mergers & Amalgamations (M&A) etc. as discussed in the DPE-CPSE joint meeting on Nov. 28, 2012, it is also important to see whether the profitable PSEs are exercising these autonomy and financial powers for enhancing profits.

First thing that has come up after meeting and discussions with executives of various PSEs, is that what is the operating level, at what these companies are operating. During analysis of MoU agreements of selected CPSEs, it is seen that many profitable PSEs are generating profits not largely because of their operating profits and efficiency but because of the large interest earnings, that is non-operating income. This is a worrying sign as company’s management don’t think of increasing operating efficiency/productivity to produce and sale more. Capacity utilisation is vital and companies should think of increasing productivity, resulting in to higher sales and improving profits.

Working capital management is also essential to improve the efficiency of the companies. Working capital management has three important pillars; Cash Management, Inventory Management and Receivables Management. If, managed properly, each of these pillars may contribute significantly to improve on efficiency in operations, hence enhancement in profitability and absolute profits as well. Very efficient cash management is must as idle or unutilised cash may result in inefficiency. However, focus on earning through surplus cash by investing in fixed income generating securities and not on improving the operations by spending in capital assets to earn better revenues is also not appreciable.

It is observed that many CPSEs sit on large cash, usually invested somewhere to earn profits but management of these companies do not plan to utilise it by investing it in new projects/ventures and/or not identify the further growth areas and new investment avenues for long-term. By doing this profitable CPSEs will not only increase their profits but also create more employment and contribute in GDP growth. Proactive management is required to make some bold steps and look beyond the normal. New technologies or investment in R&D efforts may also be evaluated.

Another important thing came up during the discussions that PSEs of same or related sector may think of creating a kind of synergy between them, which is mutually beneficial to all the contributors. This may be done by pooling resources for R&D or creating a common supply chain and or logistics to reduce the cost of operations and increasing profits for all participating PSEs. Some of the participating CPSEs may be sick/loss making PSEs, which may also be benefitted with this symbiotic relationship and may reduce their losses.

It seen generally that listed companies behave in more transparent and ethical manner due to the listing requirements and regulatory norms related to governance, disclosure, ethical behaviour and

43

publicly available documents and statements. All profitable PSEs may be considered for the listing in stock exchanges. This may improve not only their governance and transparency but also operating efficiency.

High risk is a key to high gain. Now time has come that CPSEs must use the risk management tools effectively and should take calculative risk with informed decisions. Entrepreneurial skills and approach is needed at the board level as well as at all functional level. Also to face challenges of increasing global competition, benchmarking with the best in the industry is to be done to find out real gap and CPSEs to realign themselves as per the requirement. Management needs to change the mindset and should think out of box and beyond the normal.

Based on the above discussions during the course of time, following are the main issues identified:

Increase in the operating efficiency to enhance operating profits: As it has come up during the discussion in the DPE-CPSE joint meeting on Nov. 28, 2012, all CPSEs need to carefully watch the operating efficiency to enhance the profits. Non-operating profits specially interest earnings should be supplementary not the major source of income.

Proper utilisation of autonomy and financial powers given to the PSEs: Though, CPSEs are given autonomy in taking decision and also some financial flexibility is given in terms of JVs and M&A, but after analyzing MoU agreements it is observed that CPSEs are not utilizing the benefits of this autonomy and financial flexibility. CPSEs may create more value to business by venturing in to profitable and mutually beneficial JVs and M&As.

Pooling resources for better utilization to save cost and improving profitability: During the Director’s Conclave, organized by IMI in September 2012 it has come up that many CPSEs work in same or related industrial domain. These CPSEs may pool/join their resources or create common facilities/services to save on cost, in turn improving operating efficiency. Like joint R&D efforts, common supply chain and logistics etc. may be some example of these activities.

Effective Working Capital Management: for better efficiency and reducing cost, effective Working Capital Management is must for any company. CPSEs must emphasize on this aspect, especially effective cash management. DPE has suggested in its guidelines that investment may be made in public sector mutual funds. It is observed during the discussion with various executives of the CPSEs that they rely more on fixed income options and seldom invest in mutual funds.

Courage to plan and start long-term investments/projects for better utilization of profits/surplus cash: for profit making CPSEs, it is important to manage their profits optimally and reinvest in creating long-term projects for expansion or for new business line identified by the management, either for backward or forward integration.

Listing of profitable CPSEs: In all discussions, at Director’s Conclave to DPE-CPSE joint meeting, this was emphasized. Listing of CPSEs leads to better governance, transparency and accountability.

44

Benchmarking with global standards: to face the increased global competition, competitiveness of CPSEs to be reassessed and enhanced. As told by various executives, benchmarking with global standards and processes will help CPSEs to identify the gaps and specific areas of improvements. CPSEs should realign their strategic plans as per the requirement.

Pro-active management to look beyond: As quoted by Padamshree Dr. Preetam Singh in the Director’s conclave in September 2012 and endorsed by many other eminent speakers, “management needs to look within, look around and look beyond”. A very proactive management with an entrepreneurial outlook is required to steer the CPSEs who are capable of becoming global leaders in their area of operations.

45

REDUCING LOSS OF LOSS MAKING CPSEs

46

Reducing Losses of Loss Making CPSEs

Many CPSEs are running in losses for years. To deal with this situation and to help and theses companies, Sick Industrial Companies Act (SICA), 1985 was brought which is enforced in 1991 and effective from 1992. Under the provisions of Sick Industrial Companies (Special Provision) Act (SICA),1985 the CPSEs have to be referred to Board for Industrial and Financial Reconstruction (BIFR) on their becoming sick/insolvent. They are referred to the BIFR if the cumulative loss is equal or more than the net worth of the company. According to PSE survey, 64 companies have been referred to BIFR, out of which 45 companies are in operation till 31.03.2011. It is seen that the process of appointment of Official liquidator (OL) for winding up of a company or process of revival/rehabilitation sanction is very slow.

The Government, furthermore, constituted the Board for Reconstruction of Public Sector Enterprises (BRPSE) in 2004, as an advisory body to address the task of strengthening, modernizing, reviving and restructuring sick and loss making CPSE’s. In comparison to BIFR, which sanctioned 14 cases of revival (between 1992-2007), BRPSE has recommended 159 revival cases (between 2005-2011). BRPSE considers any company sick if it has accumulated losses in any financial year equal to 50% or more of its average net worth during 4 years, immediately preceding, such financial year and/or as per the provisions of the SICA.

There has been significant improvement in the overall condition of these enterprises in recent years. In comparison to 111 sick CPSEs in March, 2002, there were 45 sick CPSEs in March, 2011

(Source: Public Enterprise Survey, 2010-11)

Reasons for Sickness in CPSEs