“OMB Circular A-123 How Does EVERY Manager Get Involved?”

51

“ “ OMB Circular A-123 OMB Circular A-123 How Does EVERY Manager How Does EVERY Manager Get Involved?” Get Involved?”

-

Upload

keshawn-goodness -

Category

Documents

-

view

222 -

download

2

Transcript of “OMB Circular A-123 How Does EVERY Manager Get Involved?”

““OMB Circular A-123OMB Circular A-123

How Does EVERY Manager How Does EVERY Manager Get Involved?”Get Involved?”

Philip J. GizaPhilip J. Giza

FMS Senior Accountant FMS Senior Accountant Financial Management ServicesFinancial Management ServicesProgram Support CenterProgram Support CenterDepartment of Health & Human Department of Health & Human ServicesServices

Association of Government AccountantsAssociation of Government AccountantsRichmond ChapterRichmond ChapterHenrico Training Center, Richmond, VAHenrico Training Center, Richmond, VAOMB Circular A-123 -OMB Circular A-123 -

How Does EVERY Manager Get How Does EVERY Manager Get Involved?Involved?

Wednesday, May 16th, 2007Wednesday, May 16th, 2007

8:45 am to 9:35 am8:45 am to 9:35 am

Philip J. GizaPhilip J. Giza

[email protected]@psc.hhs.gov

301-443-3499301-443-3499

44

SOXSOX

SOX or Sarbanes-Oxley or Sarbanes-Oxley of 2002 or section 404 of the Sarbanes-Oxley Act of 2002 was enacted in response to corporate accountability failures of the past several years and contains a provision calling for management’s assessment of internal control over financial reporting similar to the long-standing requirements for executive branch agencies in 31 U.S.C. § 3512 (c),(d), commonly referred to as the Federal Managers’ Financial Integrity Act (FMFIA), to issue annual statements of assurance over internal control in the agency.

Opinions on internal control over financial reporting as required by the Sarbanes-Oxley Act for publicly traded companies are important to protect investors by improving the accuracy and reliability of corporate disclosures made pursuant to the securities laws.

Regulators, public companies, audit firms, and investors generally agree that the Sarbanes-Oxley Act of 2002 has had a positive and significant impact on investor protection and confidence.

At the same time, the costs associated with the Sarbanes-Oxley Act have been significant and additional steps should be taken to improve the efficiency and cost-effectiveness of its implementation.

55

SOX to A-123SOX to A-123

In initiating the revisions to Circular No. A-123, OMB cited the new internal control requirements for publicly traded companies that are contained in section 404 of the Sarbanes-Oxley Act of 2002.

Federal agencies also have a duty to attain and maintain the public’s trust and confidence.

Specifically, federal agencies have a stewardship obligation to prevent fraud, waste, and abuse; to use tax dollars appropriately; and to ensure financial accountability to the President, the Congress, and the American people.

In the broadest context, internal control represents an organization’s plans, methods, and procedures used to meet its missions, goals, and objectives and serves as the first line of defense in safeguarding assets and preventing and detecting errors, fraud, waste, abuse, and mismanagement.

66

Circular A-123: Circular A-123: BackgroundBackground

Federal Managers’ Financial Integrity Act (FMFIA) of 1982 Federal Managers’ Financial Integrity Act (FMFIA) of 1982 and its implementing regulation, OMB Circular A-123and its implementing regulation, OMB Circular A-123

Rigorous Implementation of the 1980s - -> Rigorous Implementation of the 1980s - -> - - > Focus shifted to CFO Act Audits in 1990s- - > Focus shifted to CFO Act Audits in 1990s

Corporate Scandals led to Sarbanes-Oxley Act of 2002 Corporate Scandals led to Sarbanes-Oxley Act of 2002 (SOX) and Revised OMB Circular A-123 (December 2004)(SOX) and Revised OMB Circular A-123 (December 2004)

Revised Circular A-123 Requires Management to Revised Circular A-123 Requires Management to Assess, Test, Document, and ReportAssess, Test, Document, and Report on Internal on Internal Controls Over Financial Reporting (ICOFR) by using Controls Over Financial Reporting (ICOFR) by using prescribed methodology included in Appendix Aprescribed methodology included in Appendix A

77

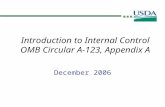

A-123 New & ImprovedA-123 New & Improved

The Office of Management and Budget (OMB) revised its Circular Number A-123, in December 2004 (effective beginning with fiscal year 2006) to:– strengthen the requirements for conducting

management’s assessment of internal control over financial reporting.

Major revisions contained in Appendix A of the circular:– include requiring CFO Act agency management to

annually assess the adequacy of internal control over financial reporting,

– provide a report on identified material weaknesses and corrective actions,

– and provide separate assurance on the agency’s internal control over financial reporting.

88

Federal Legislative History:Federal Legislative History:Integration and Coordination with Other Control ActivitiesIntegration and Coordination with Other Control Activities

Federal Agencies = 15 Departments and ~ 86 Federal Agencies = 15 Departments and ~ 86 Independent AgenciesIndependent Agencies– are subject to numerous legislative and regulatory are subject to numerous legislative and regulatory

requirements that promote and support an effective requirements that promote and support an effective internal control structure. internal control structure.

Management should coordinate and integrate the Management should coordinate and integrate the Internal Control over Financial Reports (ICOFR) Internal Control over Financial Reports (ICOFR) assessment with these reviews, including FMFIA and assessment with these reviews, including FMFIA and other existing internal reviews to leverage the benefit other existing internal reviews to leverage the benefit of work already being performed and avoid duplication of work already being performed and avoid duplication of effort. of effort.

99

Examples of existing control-related Examples of existing control-related activitiesactivities

include those listed below. include those listed below.

Federal Managers’ Financial Integrity Act of 1982 (FMFIA);Federal Managers’ Financial Integrity Act of 1982 (FMFIA); Federal Financial Management Improvement Act of 1996 Federal Financial Management Improvement Act of 1996

(FFMIA);(FFMIA); Chief Financial Officers Act of 1990, as amended (CFO Act);Chief Financial Officers Act of 1990, as amended (CFO Act); Improper Payments Information Act of 2002 (IPIA);Improper Payments Information Act of 2002 (IPIA); Section 831 of the Defense Authorization Act of 2002 Section 831 of the Defense Authorization Act of 2002

(Recovery Auditing);(Recovery Auditing); Single Audit Act, as amended;Single Audit Act, as amended; Inspector General Act of 1978 (IG Act);Inspector General Act of 1978 (IG Act); Federal Information Security Management Act of 2002 Federal Information Security Management Act of 2002

(FISMA);(FISMA); Information Technology Management Reform Act of 1996 Information Technology Management Reform Act of 1996

(Clinger Cohen Act)(Clinger Cohen Act) Enterprise Architecture Documentation; andEnterprise Architecture Documentation; and Financial Management Systems Documentation.Financial Management Systems Documentation.

1010

OMB A-123 Related Legislation & Regulatory OMB A-123 Related Legislation & Regulatory RequirementsRequirements

Integration and Coordination with Other Control Integration and Coordination with Other Control ActivitiesActivities

(another view)(another view)

Accounting and Auditing Act of 1950Accounting and Auditing Act of 1950– The Grandfather of legislation for Internal Controls The Grandfather of legislation for Internal Controls

Federal Financial Management Improvement Act of 1996 (FFMIA)Federal Financial Management Improvement Act of 1996 (FFMIA)– An Act to amend the Accounting and Auditing Act of 1950 to require An Act to amend the Accounting and Auditing Act of 1950 to require

ongoing evaluations and reports on the adequacy of the systems of ongoing evaluations and reports on the adequacy of the systems of internal accounting and administrative control of each executiveinternal accounting and administrative control of each executive

and others are:and others are:

Chief Financial Officers Act of 1990, as amended (CFO Act);Chief Financial Officers Act of 1990, as amended (CFO Act); Improper Payments Information Act of 2002 (IPIA);Improper Payments Information Act of 2002 (IPIA); Section 831 of the Defense Authorization Act of 2002 (Recovery Auditing);Section 831 of the Defense Authorization Act of 2002 (Recovery Auditing); Single Audit Act, as amended;Single Audit Act, as amended; Inspector General Act of 1978 (IG Act);Inspector General Act of 1978 (IG Act); Federal Information Security Management Act of 2002 (FISMA);Federal Information Security Management Act of 2002 (FISMA); Information Technology Management Reform Act of 1996 (Clinger Cohen Act)Information Technology Management Reform Act of 1996 (Clinger Cohen Act) Enterprise Architecture Documentation; andEnterprise Architecture Documentation; and Financial Management Systems Documentation.Financial Management Systems Documentation.

1111

An Agency’s FMFIA An Agency’s FMFIA assessment should …assessment should …

Consider the work done to comply with these Consider the work done to comply with these various statutes, as well as the laws and various statutes, as well as the laws and regulations identified in the ICOFR Process. regulations identified in the ICOFR Process.

Use that information to determine the extent Use that information to determine the extent to which such work contributes to the overall to which such work contributes to the overall assessment and whether any deficiencies assessment and whether any deficiencies identified should be included in the FMFIA identified should be included in the FMFIA report.report.

1212

Assessment of Internal ControlsAssessment of Internal Controls

Administrative and Program ComplianceAdministrative and Program Compliance

The assessment of internal controls over operations The assessment of internal controls over operations (administrative and program) reports whether those (administrative and program) reports whether those controls are operating effectively. controls are operating effectively.

The assessment is based:The assessment is based:– on general management knowledge gained from daily on general management knowledge gained from daily

operations of agency programs and systems, operations of agency programs and systems, – management reviews to assess internal controls, management reviews to assess internal controls, – and other available sources. and other available sources.

1313

General Management knowledge for a Federal General Management knowledge for a Federal Agency can and should include the following:Agency can and should include the following:

Audits of financial statements under the Chief Financial Audits of financial statements under the Chief Financial Officers Act of 1990, as amended (CFO Act); Officers Act of 1990, as amended (CFO Act);

IG and GAO reports;IG and GAO reports;

Reviews of financial systems under Federal Financial Reviews of financial systems under Federal Financial Management Improvement Act of 1996 (FFMIA) or OMB Management Improvement Act of 1996 (FFMIA) or OMB Circular A-127, Financial Systems;Circular A-127, Financial Systems;

Annual evaluations under Federal Information Security Annual evaluations under Federal Information Security Management Act of 2002 (FISMA) and OMB Circular A-130, Management Act of 2002 (FISMA) and OMB Circular A-130, Management of Federal Information ResourcesManagement of Federal Information Resources;;

Government Performance and Results Act (GPRA) annual Government Performance and Results Act (GPRA) annual performance plans and reports;performance plans and reports;

1414

And also the following sources:And also the following sources:

Program Assessment Rating Tool (PART) Assessments;Program Assessment Rating Tool (PART) Assessments; Improper Payments Information Act of 2002 (IPIA) risk Improper Payments Information Act of 2002 (IPIA) risk

assessments and reports;assessments and reports; Single audit reports;Single audit reports; Management reviews with internal control assessment Management reviews with internal control assessment

as a by-product;as a by-product; Reports and other information provided by Reports and other information provided by

Congressional committees; Congressional committees; Program evaluations;Program evaluations; Other reviews or reports related to Federal Agency Other reviews or reports related to Federal Agency

operations; andoperations; and Results from tests of key controls performed as part of Results from tests of key controls performed as part of

the ICOFR assessment under Appendix A. the ICOFR assessment under Appendix A.

1515

The content and source of survey tools, testing The content and source of survey tools, testing instruments, etc. used by the program manager instruments, etc. used by the program manager should be coordinated through an Internal Control should be coordinated through an Internal Control Officer.Officer.

For FMFIA, A-123 requires that agency managers and For FMFIA, A-123 requires that agency managers and employees identify deficiencies in internal controls from employees identify deficiencies in internal controls from the sources listed above and the results of their internal the sources listed above and the results of their internal control assessment process and report the control control assessment process and report the control deficiencies.deficiencies.

Management must document the findings/conclusions Management must document the findings/conclusions of all Internal Control Reviews and ensure that such of all Internal Control Reviews and ensure that such evaluations/self-assessments are adequately planned evaluations/self-assessments are adequately planned and coordinated.and coordinated.

All reports, work papers, correspondence, and related All reports, work papers, correspondence, and related memoranda are to be maintained by the sub-memoranda are to be maintained by the sub-organization and readily available for inspection by the organization and readily available for inspection by the Agency.Agency.

1616

Congress recognized the importance of internal Congress recognized the importance of internal controls.controls.

57 years ago, 57 years ago, – the Budget and Accounting the Budget and Accounting

Procedures Act of 1950 became the Procedures Act of 1950 became the first major act to place primary first major act to place primary responsibility for establishing and responsibility for establishing and maintaining internal control squarely maintaining internal control squarely on the shoulders of MANAGEMENT. on the shoulders of MANAGEMENT.

And to put all of the And to put all of the

related A-123 history related A-123 history

into perspective, into perspective,

the first major Accounting Act the first major Accounting Act occurred 57 years ago and …occurred 57 years ago and …

1818

… … Jamestown, Virginia Jamestown, Virginia was settled was settled

400 400 years ago, years ago,

on on Monday, May 14Monday, May 14thth, 1607., 1607.

1919

Federal Government-Wide Results: Federal Government-Wide Results: FY 2006 Status of the FY 2006 Status of the ImplementationImplementationof A-123, Appendix A =of A-123, Appendix A =

All 24 CFO Act agencies or 100% completed first year All 24 CFO Act agencies or 100% completed first year of A-123 implementation.of A-123 implementation.

16 of the 24 CFO Act agencies or 66% implemented a 16 of the 24 CFO Act agencies or 66% implemented a full scope A-123 assessment (testing all key processes)full scope A-123 assessment (testing all key processes)

8 of the 24 CFO Act agencies or 33% implemented a 8 of the 24 CFO Act agencies or 33% implemented a multi-year phased-in assessment (testing a portion of multi-year phased-in assessment (testing a portion of the key processes) and provided plans for testing the the key processes) and provided plans for testing the remaining processes within three years.remaining processes within three years.

Government-wide internal control material (FMFIA) Government-wide internal control material (FMFIA) weaknesses increased by 12% from 2005.weaknesses increased by 12% from 2005.

2020

Government-Wide Results: Government-Wide Results: FMFIA Issues Identified by Agency Heads FMFIA Issues Identified by Agency Heads

as of FY 2005 and FY 2006 = as of FY 2005 and FY 2006 =

Section 2Section 2

Overall InternalOverall Internal

Control WeaknessesControl Weaknesses

Section 4Section 4

SystemsSystems

NonconformancesNonconformances

20052005 20062006 20052005 20062006

BeginningBeginning 8383 6868 1515 1616

NewNew 2020 3636 66 1515

ResolvedResolved 3333 1515 22 44

ConsolidateConsolidatedd

11 55 00 00

ReassessedReassessed

11 44 00 33

EndingEnding 6868 8080 1616 1414

2121

Why did the Federal material Why did the Federal material weaknesses increase in 2006?weaknesses increase in 2006?

Transparency was achieved in many agencies?Transparency was achieved in many agencies?

Federal Agencies successfully reached the non-Federal Agencies successfully reached the non-accountant/financial managers who are provided more accountant/financial managers who are provided more of the organization’s vulnerabilities or “hidden” issues?of the organization’s vulnerabilities or “hidden” issues?

Amnesty was given in 2006; turn in your “findings” and Amnesty was given in 2006; turn in your “findings” and no (or few) questions are asked in 2006?no (or few) questions are asked in 2006?

““Show us now or show others later” was explained Show us now or show others later” was explained well?well?

Process/Cycle memos’ documented procedures in Process/Cycle memos’ documented procedures in 2005 showed the discovered anomalies in managers’ 2005 showed the discovered anomalies in managers’ processes?processes?

2222

Corrective Action Plan or Corrective Action Plan or CAPCAP

(guideline examples for your (guideline examples for your consideration)consideration)

– Year the issue was first identifiedYear the issue was first identified– Organization official to monitor progressOrganization official to monitor progress– Progress performance indicatorsProgress performance indicators– Quantifiable target or milestone Quantifiable target or milestone

progressprogress– Original targeted corrective action dateOriginal targeted corrective action date– Revised targeted corrective action dateRevised targeted corrective action date– Actual corrective action dateActual corrective action date

2323

Why have we not solved ALL of the Why have we not solved ALL of the accounting accounting IC issues since the first OMB A-123 in IC issues since the first OMB A-123 in

1983?1983? Did we have the right people with the right skills in the right Did we have the right people with the right skills in the right

positions?positions?

Did we listen to the “noise?.”Did we listen to the “noise?.”

Did we bring “bad” news out ASAP & “fix” the process and Did we bring “bad” news out ASAP & “fix” the process and not the people?not the people?

Could the “Feds” consolidate their A-123 related legislation, Could the “Feds” consolidate their A-123 related legislation, Acts, etc.? Are there too many? Acts, etc.? Are there too many?

– There are KEY legislations, acts, and circulars, and documents There are KEY legislations, acts, and circulars, and documents that have invented the financial wheel.that have invented the financial wheel.

– There is some overlap, duplication, or redundancy that has There is some overlap, duplication, or redundancy that has occurred over the last 57 years.occurred over the last 57 years.

Could Revised OMB A-123 be the start of a consolidation Could Revised OMB A-123 be the start of a consolidation process?process?

2424

Highlights of GAO-05-321T, a report to the Subcommittee on Highlights of GAO-05-321T, a report to the Subcommittee on Government Government

Management, Finance, and Accountability, Committee on Management, Finance, and Accountability, Committee on Government Government

Reform, House of RepresentativesReform, House of Representatives

Internal control is at the heart of accountability Internal control is at the heart of accountability for our nation’s resources and how effectively for our nation’s resources and how effectively government uses them. government uses them.

The testimony –The testimony –– outlined the importance of internal control, outlined the importance of internal control, – summarized the Congress’s long-standing interest in summarized the Congress’s long-standing interest in

internal control and the related statutory framework,internal control and the related statutory framework,– discussed GAO’s experiences and lessons learned discussed GAO’s experiences and lessons learned

from agency assessments since the early 1980s, from agency assessments since the early 1980s, – and provided GAO’s views on the Office of and provided GAO’s views on the Office of

Management and Budget’s (OMB) recent revisions to Management and Budget’s (OMB) recent revisions to its 2004 Circular A-123.its 2004 Circular A-123.

2525

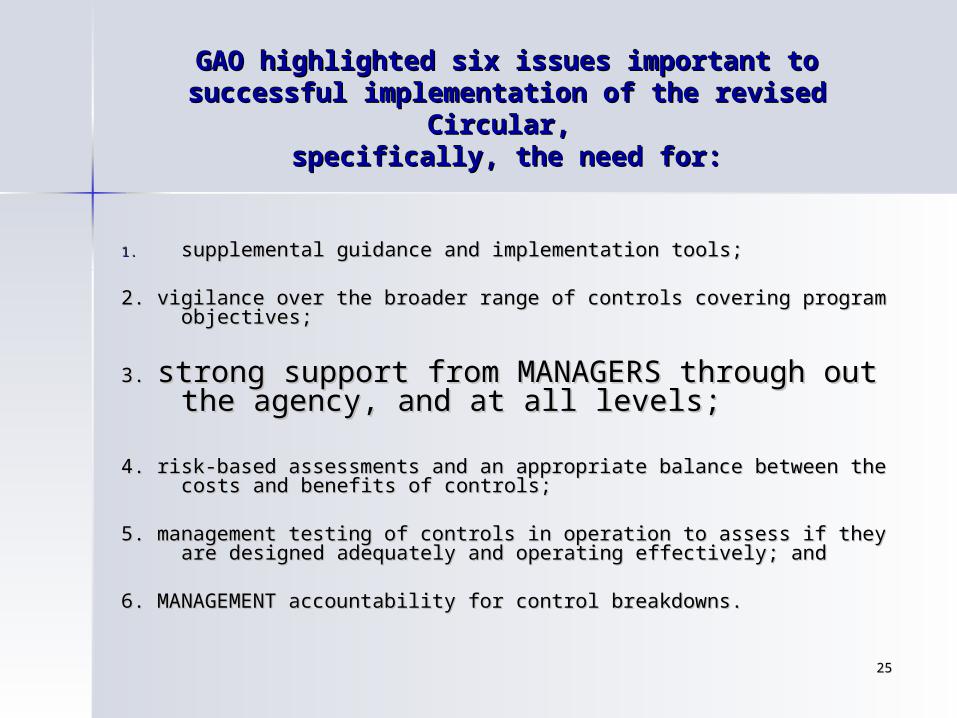

GAO highlighted six issues important to successful GAO highlighted six issues important to successful implementation of the revised Circular, implementation of the revised Circular,

specifically, the need for:specifically, the need for:

1.1. supplemental guidance and implementation tools;supplemental guidance and implementation tools;

2. vigilance over the broader range of controls covering program 2. vigilance over the broader range of controls covering program objectives;objectives;

3. 3. strong support from MANAGERS through out strong support from MANAGERS through out the agency, and at all levels;the agency, and at all levels;

4. risk-based assessments and an appropriate balance between the 4. risk-based assessments and an appropriate balance between the costs and benefits of controls;costs and benefits of controls;

5. management testing of controls in operation to assess if they are 5. management testing of controls in operation to assess if they are designed adequately and operating effectively; anddesigned adequately and operating effectively; and

6. MANAGEMENT accountability for control breakdowns.6. MANAGEMENT accountability for control breakdowns.

2626

What GAO said and found:What GAO said and found:

Internal control represents an organization’s Internal control represents an organization’s plans, methods, and procedures used to meet plans, methods, and procedures used to meet its missions, goals, and objectives and serves its missions, goals, and objectives and serves as the first line of defense in safeguarding as the first line of defense in safeguarding assets and preventing and detecting errors, assets and preventing and detecting errors, fraud, waste, abuse, and mismanagement. fraud, waste, abuse, and mismanagement.

Internal control provides reasonable assurance Internal control provides reasonable assurance that an organizations’ objectives are achieved that an organizations’ objectives are achieved through (1) effective and efficient operations, through (1) effective and efficient operations, (2) reliable financial reporting, and (3) (2) reliable financial reporting, and (3) compliance with laws and regulations. compliance with laws and regulations.

2727

Polling Question for Polling Question for you !you !My organization has a comprehensive and My organization has a comprehensive and

coordinated approach to internal control coordinated approach to internal control management?management?

Possible Answers:Possible Answers: Yes Yes

NoNo

I do not know - I am just waiting for Joe K., Ester I do not know - I am just waiting for Joe K., Ester H., Mike B., Joe D., Mike W., and Valerie T. to H., Mike B., Joe D., Mike W., and Valerie T. to speak after you.speak after you.

2828

Circular A-123, Appendix Circular A-123, Appendix AA

Evaluate Internal Control at the entity level using Evaluate Internal Control at the entity level using COSO Framework (GAO Checklist)COSO Framework (GAO Checklist)– Assess Tone at the TopAssess Tone at the Top– Perform Risk AssessmentsPerform Risk Assessments

Evaluate Internal Control at the Process, Transaction, Evaluate Internal Control at the Process, Transaction, or Application Level (Agency Guidance Manual)or Application Level (Agency Guidance Manual)– Identify and gain an understanding of Major Business Identify and gain an understanding of Major Business

CyclesCycles– Identify and test significant cyclesIdentify and test significant cycles

This work could also provide support for overall FMFIA This work could also provide support for overall FMFIA assurance statement relating to operations and assurance statement relating to operations and compliance objectivescompliance objectives

2929

Who makes up your Organization’s “Board of Directors” Who makes up your Organization’s “Board of Directors” (OMB-123 or Accounting Style)?(OMB-123 or Accounting Style)?

Or Or Who was and is responsible under the Evolution of the A-123?Who was and is responsible under the Evolution of the A-123?

1983 Original OMB A-1231983 Original OMB A-123– Answer = CFO, Senior Accountant, or anyone who was not Answer = CFO, Senior Accountant, or anyone who was not

wearing green eye shades and using columnar pads of paper (as wearing green eye shades and using columnar pads of paper (as PCs only started to became popular.)PCs only started to became popular.)

2004 Revised A-1232004 Revised A-123– Current Possible Answers = CFO Council, Oversight board, Current Possible Answers = CFO Council, Oversight board,

Governance Board, County Executives, and Financial and Program Governance Board, County Executives, and Financial and Program StakeholdersStakeholders

2004 Revised A-123 Short Answer 2004 Revised A-123 Short Answer – Every MANAGER in the entire organizationEvery MANAGER in the entire organization

Future Answer for most agencies + Present Answer for a Future Answer for most agencies + Present Answer for a Select fewSelect few– Everyone in the organizationEveryone in the organization

3030

A COSOA COSO internal control internal control framework for your ideasframework for your ideas

3131

What is the What is the Environment of your Environment of your Organization?Organization? Tone at the top?Tone at the top?

– Positive; process and results oriented; and “attack” the processes, Positive; process and results oriented; and “attack” the processes, not the messenger or the people?not the messenger or the people?

Documentation?Documentation?– Would we rather shred it or document it?Would we rather shred it or document it?

Communication?Communication?– Is there collaboration on financial, administrative, AND program Is there collaboration on financial, administrative, AND program

issues?issues?– Are our employees and managers able to speak up when the find Are our employees and managers able to speak up when the find

problems and situations?problems and situations?– Is there a history of dialogue and honest communication Is there a history of dialogue and honest communication

Do you get out of our cubicles, offices, and buildings, to meet face-to-Do you get out of our cubicles, offices, and buildings, to meet face-to-face?face?

Transparency?Transparency?– Your policy/themes or just your windows?Your policy/themes or just your windows?

Transitions?Transitions?– How did Jennifer Cavedo transition AGA Richmond Chapter to Joy How did Jennifer Cavedo transition AGA Richmond Chapter to Joy

Yeh?Yeh?

3232

Marketing OMB A-123 Marketing OMB A-123 and Internal Controls:and Internal Controls:

Understanding your non-Understanding your non-accounting audienceaccounting audience

Simplifying the Accounting jargon Simplifying the Accounting jargon ……– KISS (Keep it simple and short)KISS (Keep it simple and short)

3333

Marketing OMB A-123 and Internal Marketing OMB A-123 and Internal Controls: Controls: (continued)(continued)

Legalese (noun) or Law Jargon = Legalese (noun) or Law Jargon =

– language that is typically used in legal documents, language that is typically used in legal documents, and is generally considered by lay people to be and is generally considered by lay people to be difficult to understand.difficult to understand.

Accounting Speak, Accountingese, or Accounting Jargon Accounting Speak, Accountingese, or Accounting Jargon = =

– language that is typically used in accounting language that is typically used in accounting documents, and is universally considered by lay documents, and is universally considered by lay people to be impossible to understand and boring to people to be impossible to understand and boring to read.read.

3434

One example of the One example of the Marketing of A-123:Marketing of A-123:

The first draft of a letter I wrote to introduce the OMB A-123 to an The first draft of a letter I wrote to introduce the OMB A-123 to an Agency’s executives and sub-organizations’ executives, did NOT use Agency’s executives and sub-organizations’ executives, did NOT use these two words - “Internal Controls.” these two words - “Internal Controls.”

Why? (Their eyes would have …)Why? (Their eyes would have …)

The draft letter was not written “DOWN to the audience”, instead it The draft letter was not written “DOWN to the audience”, instead it was written “TO the audience.” was written “TO the audience.”

Understanding our audience, brings us closer to successfully Understanding our audience, brings us closer to successfully marketing to the managers we want to reach. marketing to the managers we want to reach.

In most of the Federal 13 Departments and 86 agencies, the focus is In most of the Federal 13 Departments and 86 agencies, the focus is Program related and not Administrative. As accountants and Program related and not Administrative. As accountants and finance types, we should, we must understand our customers to be finance types, we should, we must understand our customers to be able to relate and translate our “Accountingease” to their able to relate and translate our “Accountingease” to their professional perspectives. professional perspectives.

3535

How heavy is this How heavy is this bottle of water? bottle of water?

What is your answer and how do What is your answer and how do you interpret what I am really you interpret what I am really asking and communicating in my asking and communicating in my question?question?

3636

Answers to questions Answers to questions depend on …depend on … How our customer interprets our How our customer interprets our

communications.communications.

How comfortable he or she is with How comfortable he or she is with Accounting, Auditing Financial, Accounting, Auditing Financial, and internal control terms.and internal control terms.

And hundreds of factors …And hundreds of factors …

3737

The text book answer The text book answer is …is …

It depends on how long …It depends on how long …

This is how difficult it is for most of our customers This is how difficult it is for most of our customers to understand what we are attempting to to understand what we are attempting to accomplish when we ask our “A-123 questions.”accomplish when we ask our “A-123 questions.”

Many of our customer managers are focused and Many of our customer managers are focused and involved with their own professions and not as involved with their own professions and not as much on “administrative support” functions and much on “administrative support” functions and professions such as accounting, finance, etc. professions such as accounting, finance, etc.

3838

Marketing of OMB A-123’s Marketing of OMB A-123’s concepts to our customersconcepts to our customers

Who is our target audience in the Who is our target audience in the Federal universe?Federal universe?

What are the HR classifications of What are the HR classifications of these managers or types of functions these managers or types of functions they manage?they manage?

What are your organization’s major What are your organization’s major transaction cycles and sub-cycles.transaction cycles and sub-cycles.

3939

Next few slides will Next few slides will show =show = Major transaction cycles and their sub-cycles.Major transaction cycles and their sub-cycles.

This is similar to the “Old” JFMIP circle This is similar to the “Old” JFMIP circle flowcharts.flowcharts.

Examples of how sub-organizations could Examples of how sub-organizations could ensure that all significant financial statement ensure that all significant financial statement accounts are covered and the key controls at accounts are covered and the key controls at the sub-cycle level are addressed.the sub-cycle level are addressed.

4040

Major Transaction Major Transaction CycleCycle

Examples of Sub-CyclesExamples of Sub-Cycles

Funds ManagementFunds Management Fund Balance with TreasuryFund Balance with TreasuryInvestmentsInvestments

Financial ReportingFinancial Reporting General Ledger MaintenanceGeneral Ledger MaintenanceAccount Analysis & ReconciliationAccount Analysis & ReconciliationNotes & Supplementary InformationNotes & Supplementary Information

External Financial ReportingExternal Financial ReportingContingenciesContingenciesFinancial CloseoutFinancial Closeout

Budget Execution and Budget Execution and MonitoringMonitoring

ExecutionExecution MonitoringMonitoring

Human Resources ManagementHuman Resources Management PayrollPayrollTime and AttendanceTime and Attendance

Personnel (Hiring/Terminating)Personnel (Hiring/Terminating)BenefitsBenefits

Purchasing and ProcurementPurchasing and Procurement Requests and AwardsRequests and AwardsReceipt of Goods/ServicesReceipt of Goods/ServicesContracts MonitoringContracts Monitoring

Contract CloseoutsContract CloseoutsCash Disbursements / PaymentsCash Disbursements / Payments

RevenueRevenue BillingBillingInteragency AgreementsInteragency Agreements

Non-Exchange RevenueNon-Exchange RevenueCash ReceiptsCash Receipts

Disaster ReliefDisaster Relief Program Eligibility and CoverageProgram Eligibility and CoverageObligations and BillingsObligations and BillingsClaims ProcessingClaims Processing

Interagency AgreementsInteragency AgreementsReportingReporting

Inventory ControlInventory Control AcquisitionAcquisitionDistributionDistribution

DisposalsDisposalsInventory CountInventory Count

Property ManagementProperty Management Capital Acquisition RequestsCapital Acquisition RequestsDepreciationDepreciationCapitalizationCapitalization

DisposalsDisposalsLeases (Operating or Capital)Leases (Operating or Capital)

Grants ManagementGrants Management Requests and AwardsRequests and AwardsMonitoringMonitoringCloseoutsCloseouts

MedicaidMedicaidSCHIPSCHIPPaymentsPayments

Entitlement Benefits Due and Entitlement Benefits Due and PayablePayable

MedicareMedicareMedicaid/SCHIPMedicaid/SCHIP

Medicare Advantage and Part DMedicare Advantage and Part D

Benefits PaymentsBenefits Payments Medicare Fee for ServiceMedicare Fee for ServiceMedicare AdvantageMedicare Advantage

Part DPart D

Social InsuranceSocial Insurance Trust Fund ATrust Fund ATrust Fund BTrust Fund B

Trust Fund DTrust Fund D

4141

Human Resources, Human Capital, Human Resources, Human Capital, or Personnel Management - or Personnel Management -

ExamplesExamples

Newly hired accountants and auditors must be able to Newly hired accountants and auditors must be able to identify, understand, and resolve legal and regulatory identify, understand, and resolve legal and regulatory compliance issues. compliance issues.

Develop tomorrow's stakeholders – identifying Develop tomorrow's stakeholders – identifying candidates with skills and backgrounds to work in the candidates with skills and backgrounds to work in the current environment. current environment.

Pre-employment screening for all managers (and Pre-employment screening for all managers (and employees)employees)– Efficient Interview processesEfficient Interview processes– Employment Investigation RequirementsEmployment Investigation Requirements– Position Descriptions that include financial Position Descriptions that include financial

responsibilities.responsibilities.

4242

Federal GrantsFederal Grants

In my previous position as the HHS director, my In my previous position as the HHS director, my division paid out the grants for HHS and 12 other division paid out the grants for HHS and 12 other Federal Agencies. Federal Agencies.

These grant funds (a $1 billion a work day) for 12 These grant funds (a $1 billion a work day) for 12 Federal Agencies continue to flow down through Federal Agencies continue to flow down through 32,000 accounts to the states and local areas, and to 32,000 accounts to the states and local areas, and to 127 other countries.127 other countries.

To what degree do you believe I promoted internal To what degree do you believe I promoted internal control to my worldwide customers and stakeholders? control to my worldwide customers and stakeholders?

4343

Grant Payment And Cycle Memo - Grant Payment And Cycle Memo - ExamplesExamples

((OPDIV = an operating division)OPDIV = an operating division)

4444

RISK – Are our we or our RISK – Are our we or our managers ignoring A-123 managers ignoring A-123

issues?issues?If so …If so … What is the probability that the What is the probability that the

Washington Post or the Richmond Washington Post or the Richmond Time-Dispatch will find out about this Time-Dispatch will find out about this before you do as the CFO, accountant, before you do as the CFO, accountant, auditor, or financial guru? auditor, or financial guru?

Do you know your Newspaper/Internet Do you know your Newspaper/Internet factors and rating?factors and rating?

4545

My interpretations & My interpretations & presentations …presentations … of the numerous acts, circulars, of the numerous acts, circulars,

legislation, documents and examples legislation, documents and examples presented today are for teaching presented today are for teaching purposes. Use the tools presented to go purposes. Use the tools presented to go back and read the intent and richness of back and read the intent and richness of the original documents.the original documents.

Present and market A-123 and its 57 years Present and market A-123 and its 57 years of historical support in a way that is of historical support in a way that is meaningful and useful to each of your meaningful and useful to each of your managers in the organizations you serve. managers in the organizations you serve.

Latest news on the non-governmental SOX & A-Latest news on the non-governmental SOX & A-123.123.

Will they be strengthened or diluted in 2007 and Will they be strengthened or diluted in 2007 and 2008? 2008?

What is your opinion?What is your opinion?

Some people say, Some people say, ‘‘Where SOX and private industry goes, Where SOX and private industry goes, so shall the government.’ so shall the government.’

What do you believe?What do you believe?

4747

Try one of these A-123 Try one of these A-123 Sites:Sites:

CFO Council’s “CFO Council’s “Implementation Guide for OMB Circular Implementation Guide for OMB Circular A-123A-123.”.”

The Audit ProcessThe Audit Process (2nd Edition – January 3, 2005) by (2nd Edition – January 3, 2005) by the HHS OIG’s Office of Audit Services (the HHS OIG’s Office of Audit Services (http://oig.hhs.gov/organization/OAS/OIGAuditProcess.phttp://oig.hhs.gov/organization/OAS/OIGAuditProcess.pdfdf

OMB Circular No. A-123, OMB Circular No. A-123, Management’s Responsibility Management’s Responsibility for Internal Controlfor Internal Control, (, (http://www.whitehouse.gov/omb/circulars/a123/a123_rhttp://www.whitehouse.gov/omb/circulars/a123/a123_rev.pdfev.pdf))

4848

More Sites:More Sites:

CFO Council Implementation Guide for OMB Circular CFO Council Implementation Guide for OMB Circular No. A-123, No. A-123, Management’s Responsibility for Internal Management’s Responsibility for Internal ControlControl, Appendix A, , Appendix A, Internal Control over Financial Internal Control over Financial ReportingReporting ( (http://www.cfoc.gov/documents/Implementation_Guidhttp://www.cfoc.gov/documents/Implementation_Guide_for_OMB_Circular_A-123.pdfe_for_OMB_Circular_A-123.pdf))

GAO: GAO: Standards for Internal Control in the Federal Standards for Internal Control in the Federal GovernmentGovernment, November 1999, , November 1999, GAO/AIMD-00-21.3.1GAO/AIMD-00-21.3.1 ( (http://www.gao.gov/special.pubs/ai00021p.pdfhttp://www.gao.gov/special.pubs/ai00021p.pdf) )

GAO: GAO: Internal Control Management and Evaluation Internal Control Management and Evaluation ToolTool, August 2001, GAO-01-1008G (, August 2001, GAO-01-1008G (http://www.gao.gov/new.items/d011008g.pdfhttp://www.gao.gov/new.items/d011008g.pdf

4949

Contact these Contact these Organizations’ sites for Organizations’ sites for their OMB A-123 their OMB A-123 perspectives:perspectives: U.S. GovernmentU.S. Government Federal Departments & AgenciesFederal Departments & Agencies Federal Office of Inspector Federal Office of Inspector

Generals (OIGs)Generals (OIGs) State & Local GovernmentsState & Local Governments Accounting, Auditing, Consulting Accounting, Auditing, Consulting

CorporationsCorporations

5050

Thank You for your Thank You for your time and your input.time and your input.

– Philip J. GizaPhilip J. Giza

– [email protected]@psc.hhs.gov

– Direct = 301-443-3499 Direct = 301-443-3499

Address:Address:– Department of HHSDepartment of HHS– Philip Giza, FMSPhilip Giza, FMS– 5600 Fishers Lane, Suite 18B-455600 Fishers Lane, Suite 18B-45– Rockville, MD 20852-1750Rockville, MD 20852-1750

5151

OMB A-123 & Its Rich OMB A-123 & Its Rich HistoryHistory

… … just the end of the just the end of the Beginning.Beginning.