OLIVE OIL MARKETOLIVE OIL MARKET COMSUMER PROFILE and CONSUMPTION

21

OLIVE OIL MARKET OLIVE OIL MARKET COMSUMER PROFILE and CONSUMPTION PATTERNS CONSUMPTION PATTERNS C i Dik Cengiz Dikmen Türkiye June 2011 June 2011

Transcript of OLIVE OIL MARKETOLIVE OIL MARKET COMSUMER PROFILE and CONSUMPTION

OLIVE OIL MARKETOLIVE OIL MARKETCOMSUMER PROFILE and

CONSUMPTION PATTERNSCONSUMPTION PATTERNS

C i DikCengiz DikmenTürkiye

June 2011June 2011

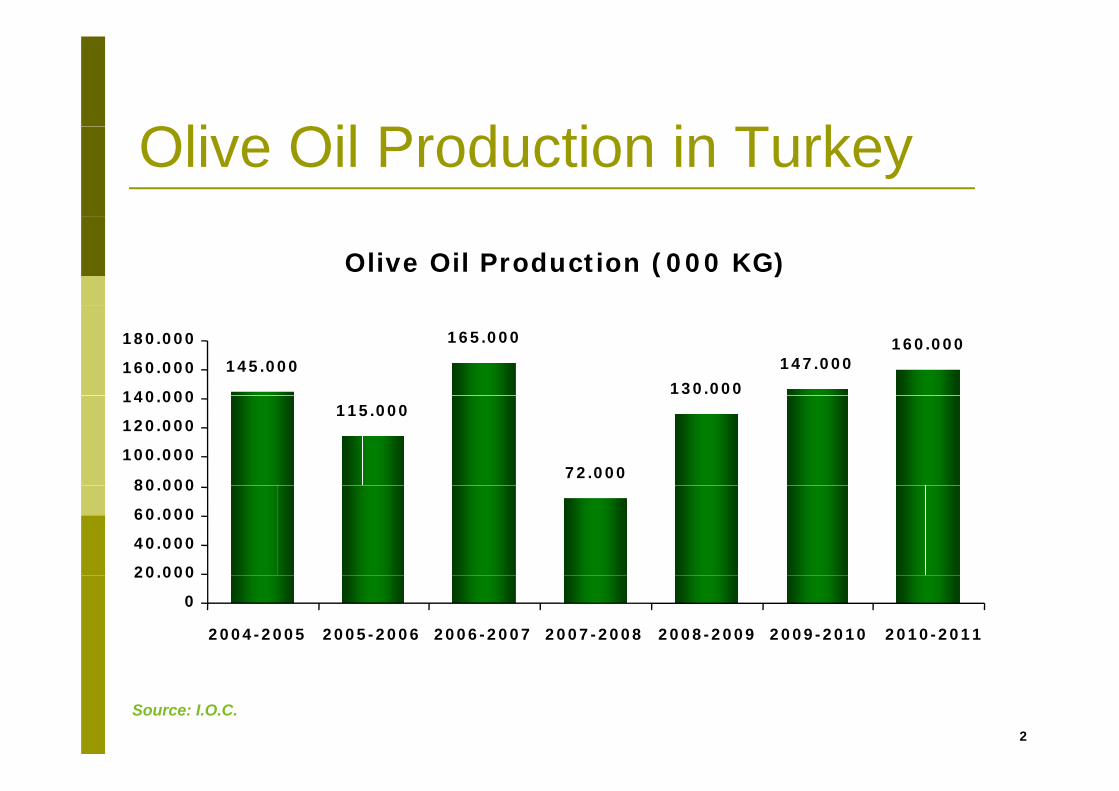

Oli Oil P d ti i T kOlive Oil Production in Turkey

Olive Oil Production (000 KG)

145.000

165.000

130.000

147.000160.000

140 000

160.000

180.000

115.000

72.00080 000

100.000

120.000

140.000

20.000

40.000

60.000

80.000

0

20.000

2004-2005 2005-2006 2006-2007 2007-2008 2008-2009 2009-2010 2010-2011

2

Source: I.O.C.

Oli Oil C ti i T kOlive Oil Consumption in Turkey

Olive Oil Consumption (000 KG)

80.000 85.000

108.000 110.000 115.000

100.000

120.000

140.000

60.00050.000

40.000

60.000

80.000

0

20.000

2004-2005 2005-2006 2006-2007 2007-2008 2008-2009 2009-2010 2010-2011*

3

Source: I.O.C. *Forecast

M k tMarketEdible Oil Market in TurkeyOlive Oil Market

kMarket Structure Market Growth SegmentsSegments

Sales ChannelPackaging PreferencesPackaging Preferences

4

Edibl Oil M k tEdible Oil MarketOn value base, edible oil make 71 % of total oil market .I 2010 dibl il t d d b 6 % In 2010, edible oil category decreased by 6 %.

V l Ch (%)V l Sh (%) V l Ch (%) P i Ch (%)Val. Chg (%)

-4

6

FATS&OILS

EDIBLE OIL

Val. Share (%)

71

Vol. Chg (%)

1

Price Chg (%)

5-6

-4

EDIBLE OIL

MARGARINE

71

18 -5

-1

1

-5

13BUTTER11 0 14

5

Source: Nielsen Türkiye Retail Report 2010

Edibl Oil M k tEdible Oil MarketSunflower Oil category which makes more than 70 Sunflower Oil category which makes more than 70 % of all edible oil consumption in volume has increased while olive oil category has decreased in 20102010.

74 5

Edible Oil Category Volume Shares

70,2 74,5

16,57,6 3,9 1,0

10,9 7,42,2

4,716,5

7,610,93,9 1,02,2

Sunflower Oil Olive Oil Canola OilCanola Oil Hazelnut OilCorn Oil

6

Source: Nielsen Türkiye Retail Report 2010 – Total Turkey W/O Bim

2009 2010

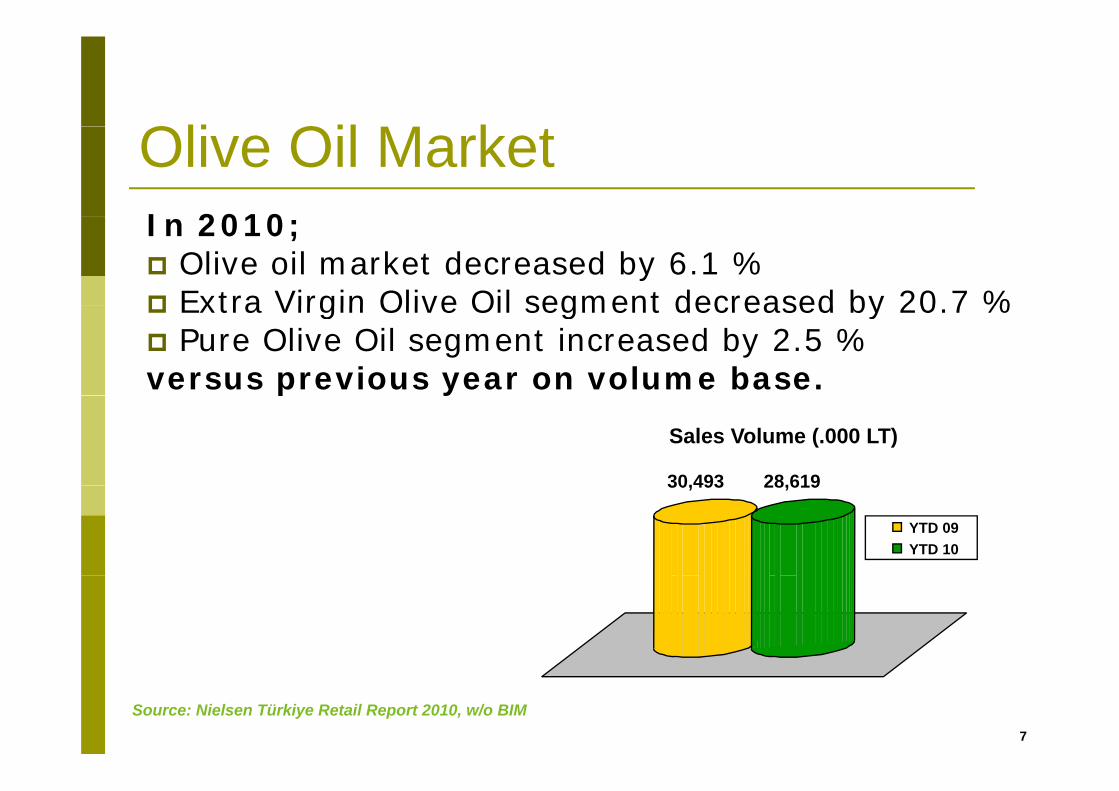

Oli Oil M k tI 2010

Olive Oil MarketIn 2010;

Olive oil market decreased by 6.1 %Extra Virgin Olive Oil segment decreased by 20 7 % Extra Virgin Olive Oil segment decreased by 20.7 % Pure Olive Oil segment increased by 2.5 %

versus previous year on volume base.p y

30,493 28,619

Sales Volume (.000 LT)

30,493 28,619

YTD 09YTD 10

7

Source: Nielsen Türkiye Retail Report 2010, w/o BIM

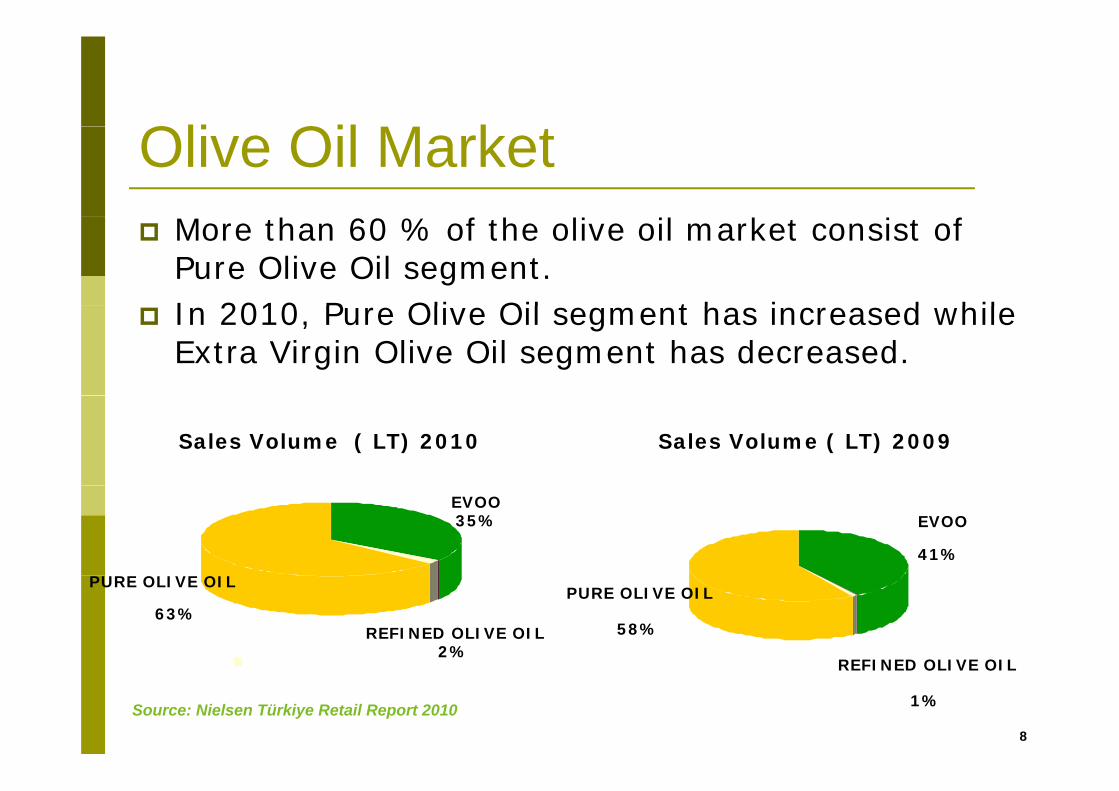

Oli Oil M k tOlive Oil MarketMore than 60 % of the olive oil market consist of Pure Olive Oil segment. I 2010 P Oli Oil t h i d hil In 2010, Pure Olive Oil segment has increased while Extra Virgin Olive Oil segment has decreased.

Sales Volume ( LT) 2010 Sales Volume ( LT) 2009

EVOO35% EVOO

41%

PURE OLIVE OIL

63%REFINED OLIVE OIL

2%

PURE OLIVE OIL

58%

REFINED OLIVE OIL

8

Source: Nielsen Türkiye Retail Report 2010

REFINED OLIVE OIL

1%

Oli Oil M k tOlive Oil MarketOlive oil consumption is stable except Ramadan period. Before and during Ramadan, the volume increases increases.

Olive Oil Consumption Volume Trend

(lt)

msu

mpt

ion

ve O

il C

omO

liv

9

Source: Nielsen Türkiye Retail Report 2010

Oli Oil S l Ch lOlive oil is generally purchased from supermarkets

Olive Oil Sales ChannelsOlive oil is generally purchased from supermarkets or hypermarkets. It is almost the same for all cities. Grocery does not have an important effect on the Grocery does not have an important effect on the olive oil channel split, but on the other hand, a small percent still buy olive oil from groceries.

Supermarkets are preferred for group buying. Hypermarkets are preferred for variety of products and price advantage. Groceries are chosen to buy oli e oil beca se of p o imit to the point of olive oil because of proximity to the point of consumption.

10Source: Olive Oil Usage Habits Search, 2008

Oli Oil P k i P fOlive Oil Packaging Preferences

Most preferred package is tin 5 lt (almost 50 % ti )consumption)

2 lt and 1 lt packs comes the second and the thirdthird.

11

Oli Oil P k i P f5 lt tin is preferred due to ;

Olive Oil Packaging Preferences5 lt tin is preferred due to ;

Decrease purchase frequencyAffordable prices

Small sizes can are preferred because;Narrow spaces in the kitchensNarrow spaces in the kitchensPromotionsLess expenditure

Olive Oil is a price sensitive category and promotions are closely monitored by consumers. promotions are closely monitored by consumers.

On the other hand, brand awareness and reliability is still important.

12Source: Ipsos KMG

Consumer Profile and Consumption Patterns

Consumer Profile Olive Oil Perception Advantages and Disadvantages of Olive OilDishes Cooked with Olive Oil

13

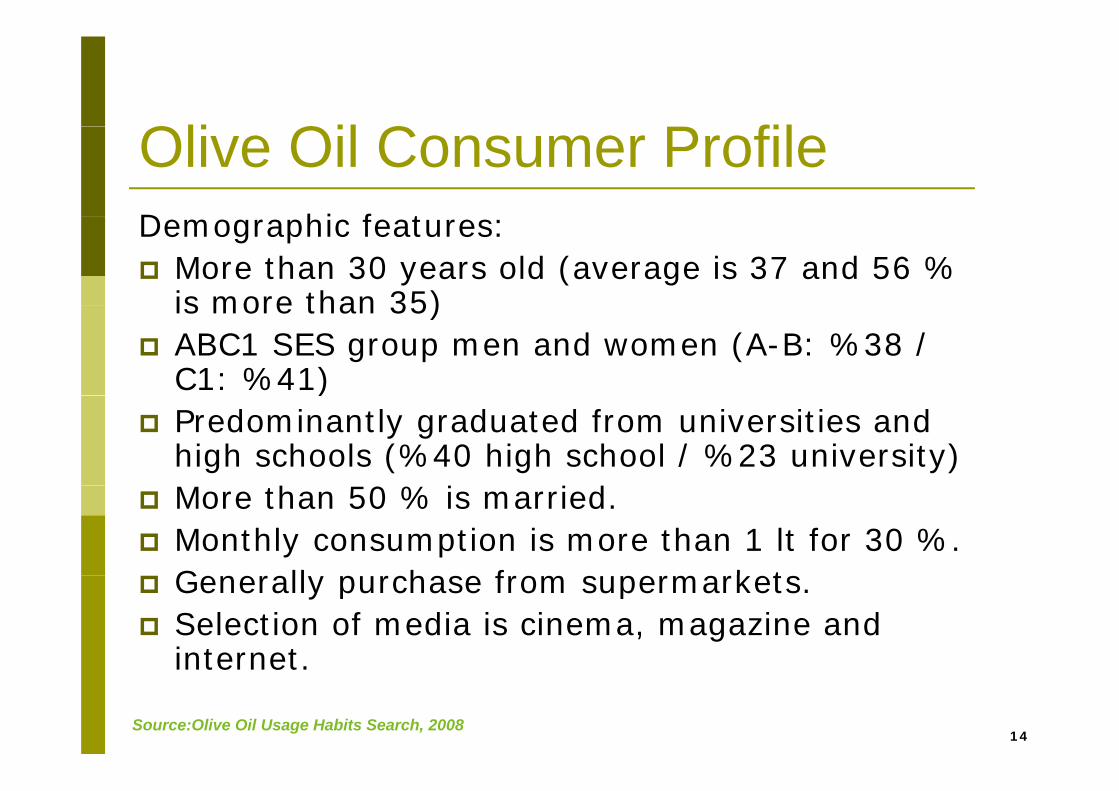

Oli Oil C P filOlive Oil Consumer ProfileD hi f t Demographic features:

More than 30 years old (average is 37 and 56 % is more than 35) is more than 35) ABC1 SES group men and women (A-B: %38 / C1: %41) )Predominantly graduated from universities and high schools (%40 high school / %23 university)

h 0 % i i dMore than 50 % is married.Monthly consumption is more than 1 lt for 30 %.Gene all p chase f om s pe ma ketsGenerally purchase from supermarkets.Selection of media is cinema, magazine and internet

14

internet.

Source:Olive Oil Usage Habits Search, 2008

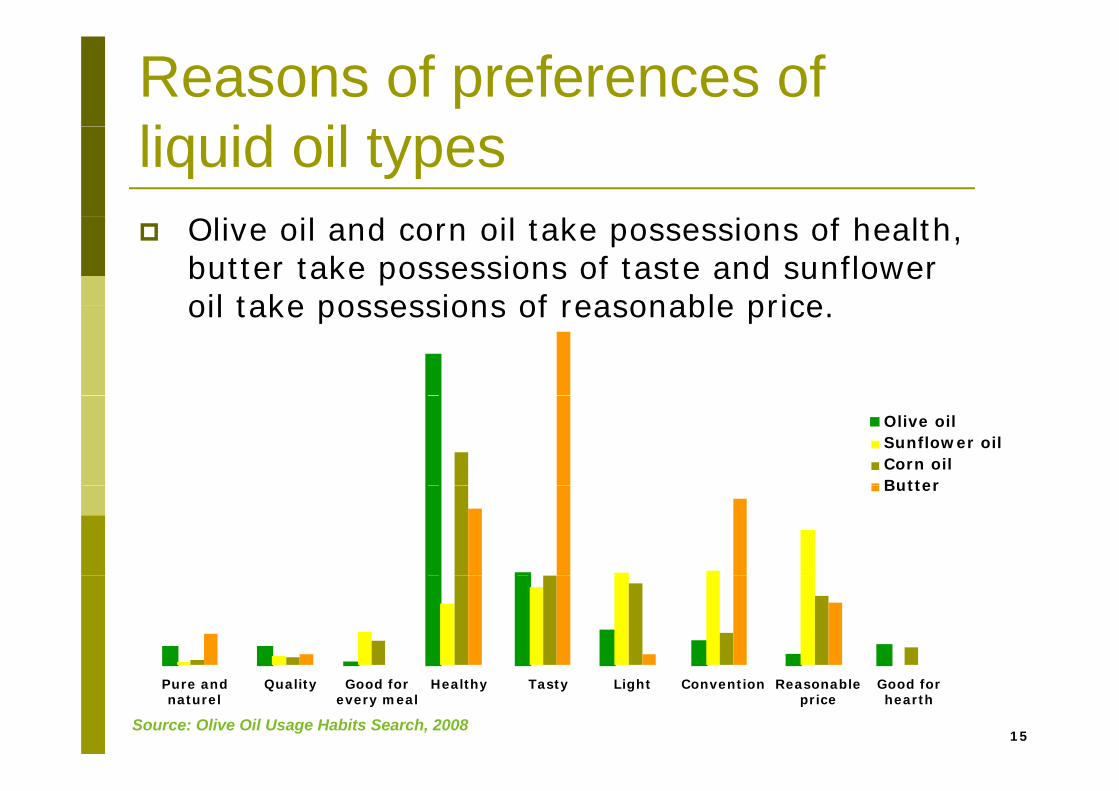

Reasons of preferences of li id il tliquid oil types

Olive oil and corn oil take possessions of health, butter take possessions of taste and sunflower oil take possessions of reasonable price oil take possessions of reasonable price.

Olive oilSunflower oilCorn oilButterButter

15

Pure andnaturel

Quality Good forevery meal

Healthy Tasty Light Convention Reasonableprice

Good forhearth

Source: Olive Oil Usage Habits Search, 2008

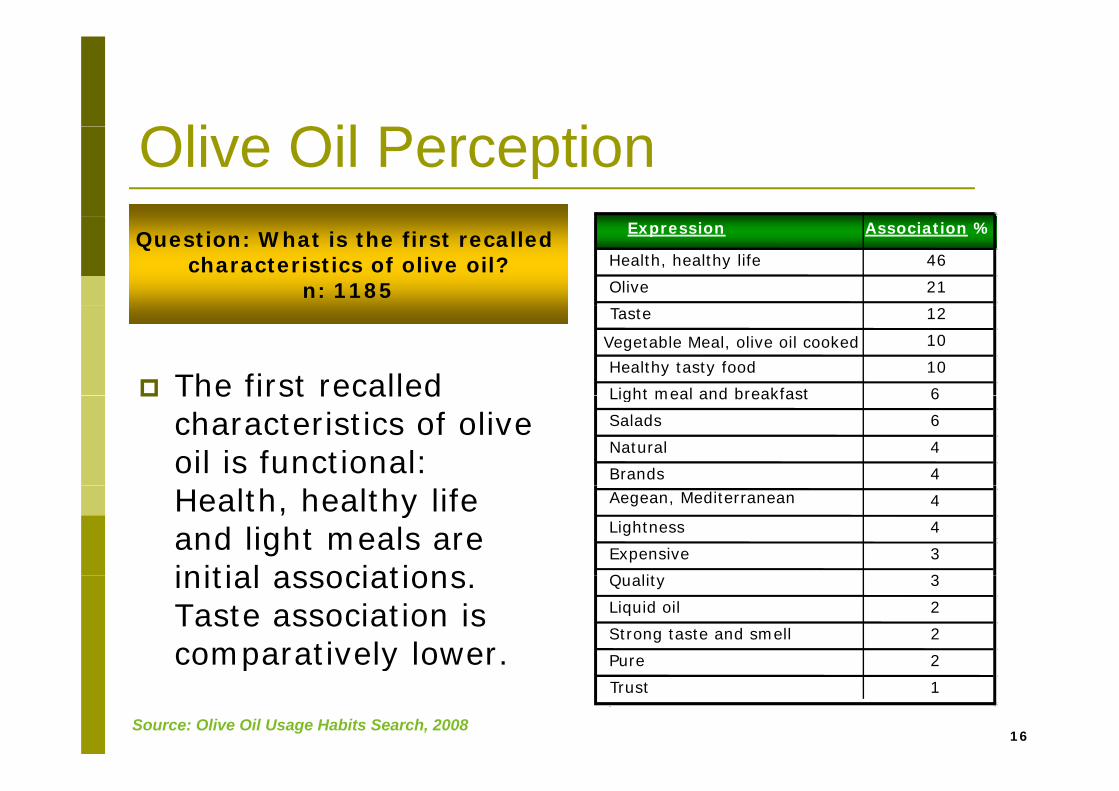

Oli Oil P tiOlive Oil PerceptionExpression Association %

Health, healthy life 46

Olive 21

Question: What is the first recalled characteristics of olive oil?

n: 1185

The first recalled

Taste 12

Vegetable Meal, olive oil cooked 10

Healthy tasty food 10

Light meal and breakfast 6The first recalled characteristics of olive oil is functional:

Light meal and breakfast 6

Salads 6

Natural 4

Brands 4

Health, healthy life and light meals are initial associations

Aegean, Mediterranean 4

Lightness 4

Expensive 3

Q lit 3initial associations. Taste association is comparatively lower.

Quality 3

Liquid oil 2

Strong taste and smell 2

Pure 2

16

co pa at e y o e Pure 2

Trust 1

Source: Olive Oil Usage Habits Search, 2008

Ad t f Oli OilAdvantages of Olive Oil

72 %Healthy

Question: What are the advantages of olive oil compared to other oils? Are there other advantages? n: 1119

9 %

11 %

72 %

Light

Tasty

Healthy

6 %

7 %

Easy to digest, stomach-friendly

Natural, pure

3 %

4 %

5 %

Does not cause blood vessel

Does not cause cholesterol

Does not exhaust hearth

1 %

3 %

3 %

Quality

Economical (more meal with less oil)

Does not cause blood vessel blockings, hearth-friendly

17

1 %Nitrous

Quality

Source: Olive Oil Usage Habits Search, 2008

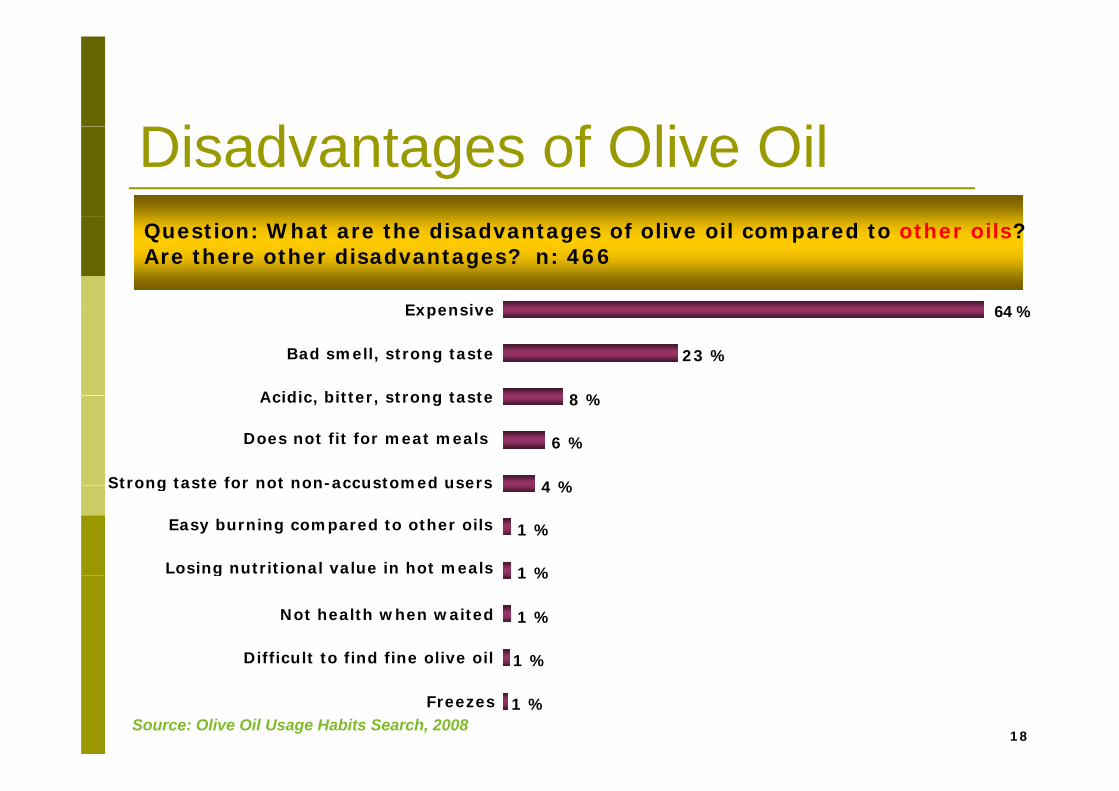

Di d t f Oli OilDisadvantages of Olive Oil

64 %E i

Question: What are the disadvantages of olive oil compared to other oils? Are there other disadvantages? n: 466

8 %

23 %

64 %

Acidic bitter strong taste

Bad smell, strong taste

Expensive

4 %

6 %

8 %

Strong taste for not non-accustomed users

Does not fit for meat meals

Acidic, bitter, strong taste

1 %

1 %

4 %

Losing nutritional value in hot meals

Easy burning compared to other oils

Strong taste for not non accustomed users

1 %

1 %

1 %

Difficult to find fine olive oil

Not health when waited

g

18

1 %

1 %

FreezesSource: Olive Oil Usage Habits Search, 2008

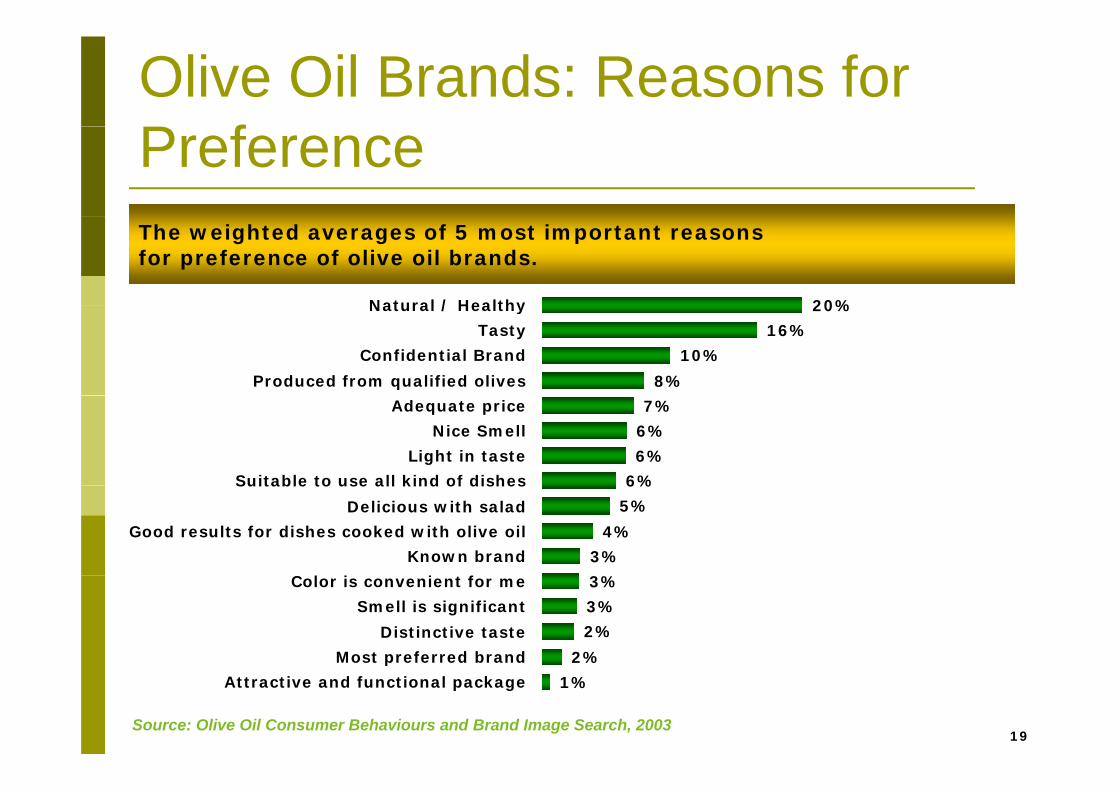

Olive Oil Brands: Reasons for P fPreference

20%Natural / Healthy

The weighted averages of 5 most important reasons for preference of olive oil brands.

8%

10%

16%

20%

Produced from qualified olives

Confidential Brand

Tasty

Natural / Healthy

6%

6%

6%

7%

Suitable to use all kind of dishes

Light in taste

Nice Smell

Adequate price

3%

4%

5%

6%

l i i f

Known brand

Good results for dishes cooked with olive oil

Delicious with salad

Suitable to use all kind of dishes

2%

2%

3%

3%

Most preferred brand

Distinctive taste

Smell is significant

Color is convenient for me

19Source: Olive Oil Consumer Behaviours and Brand Image Search, 2003

1%Attractive and functional package

p

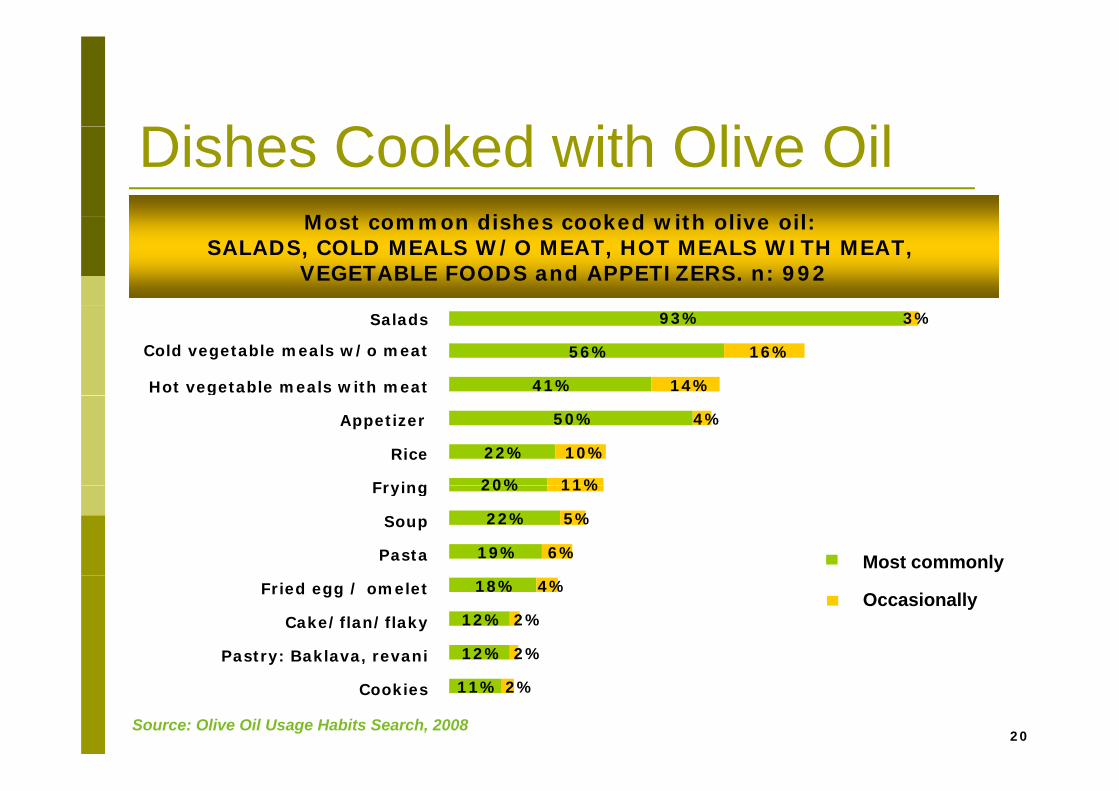

Di h C k d ith Oli OilDishes Cooked with Olive OilM t di h k d ith li il Most common dishes cooked with olive oil:

SALADS, COLD MEALS W/O MEAT, HOT MEALS WITH MEAT, VEGETABLE FOODS and APPETIZERS. n: 992

41%

56%

93%

14%

16%

3%

Hot vegetable meals with meat

Cold vegetable meals w/o meat

Salads

20%

22%

50%

11%

10%

4%

Frying

Rice

Appetizer

g

19%

22%

20%

6%

5%

11%

Pasta

Soup

Frying

Most commonly

12%

12%

18%

2%

2%

4%

Pastry: Baklava, revani

Cake/flan/flaky

Fried egg / omelet Occasionally

20

11% 2%Cookies

Source: Olive Oil Usage Habits Search, 2008

Thank You…