Okt 2, 2014 Astra Agro Lestari Trimegah Securities Tbk - COMPANY FOCUS 3 FFB and 3 rd party purchase...

14

COMPANY FOCUS PT Trimegah Securities Tbk - www.trimegah.com 1 24% upside to DCF-based target price The one year target price implies that there are substantial price appreci- ation ahead and currently AALI is undervalued. Our recommendation are based DCF analysis over a 10 year period and forward P/E analysis for robustness. According to our DCF analysis using WACC 10.0% the target price is Rp. 28.500 or 23.3% increase. This implies 14.3x 2015 PE, slightly lower than historical average of 14.8x PE. According to our target price the implied EV/Ha nucleus is $16.740. Why buy Comparing AALI to peers, FFB yield, oil extraction rate and CPO yields are one of the highest in the sector and we expect those number to remain relatively stable over the valuation period. CPO futures (1m) has declined from RM2600/ton beginning of this year to as low as 1937/ton but has recently rebounded to RM2217/ton, we expect this to rise to at least RM2400/ton level by early Jan15. CPO production has been increas- ing and slightly exceeded our expectations in 1H14, mainly due to more than expected 3 rd party FFB purchase. The YoY EPS growth rate 1H14 was 90,9% and we expect the YoY 2013—2014 EPS growth rate will be slightly lower, or 53%, mainly due to lowering CPO prices in the latter half of the year. The EPS growth is expected to be 11.6% and 8.6% in the following years. We use 2400/2500 RM/ton CPO price in our 2014/15 forecast and let it increase at 2% per year (global inflation) from 2016. Diversified more downstream The long term prospect for the company looks good but we are aware that AALI will fuel its revenue growth with 3rd party purchase. We expect that 3 rd party FFB CAGR will be 9.9% from 2014-2024 wile nucleus production CAGR will be roughly 3%, hence the profitability margins will decrease over the valuation period. AALI sets a target of 45% coming from 3 rd party which will be discuss further later in this report. Conclusions Currently AALI is undervalued and we conclude that investors should invest in AALI. DCF analysis implies strong buy and it is backed up by our P/E ratio analysis. Currently AALI generates good cash flow in this bear market and AALI is expected generate good cash flow over the valuation period. EV/Ha nucleus is currently priced at $14.590 and EV/EBITDA is 7.68 and 13x 2014 PE and 11.6x 2016 PE. PT Astra Agro Lestari Tbk is a leading palm oil producer in Indonesia, estab- lished since 33 years ago and headquar- tered in Jakarta Share Price Rp23,100 Sector Plantation Price Target Rp28.500 (23.8%) Year end Dec 2013 2014E 2015F 2016F 2017F Sales 12,675 16,333 19,169 20,541 22,341 Net Profit 1,834 2,805 3,130 3,398 3,618 EPS (Rp) 1,165 1,781 1,987 2,158 2,297 EPS Growth (%) -21.8% 53.0% 11.6% 8.6% 6.5% DPS (Rp) 1,608 1,946 2,034 2,135 2241 BVPS (Rp) 9,502 10,351 11,396 12,216 13,107 P/E (x) 15.1 15.0 13,0 11,6 10,7 Div Yield (%) 6.96% 8.43% 8.81% 9.24% 9.70% Astra Agro Lestari Company Focus BUY Rp. 28,500 Ragnar Benediktsson ([email protected]) Sebastian Tobing ([email protected]) Okt 2, 2014 Reuters Code AALI.JK Bloomberg Code AALI.IJ Issued Shares (m) 1,575 Mkt Cap (Rpbn) 36,219 Avg. Value Daily 6 month (Rpm) Rp41,334 52-Wk range Rp29,850/Rp13,100 PT. Astra International Tbk 79.7% Public 20.3% EPS 14F 15F Consensus (Rp) 1,787 1,924 TRIM vs Cons. (%) (34.8) (7.4) Strong Established Undervalued Company Company Update Stock Data Major Shareholders Consensus Stock Price - 1,000,000 2,000,000 3,000,000 4,000,000 5,000,000 6,000,000 7,000,000 8,000,000 - 5,000 10,000 15,000 20,000 25,000 30,000 35,000 Aug-13 Oct-13 Dec-13 Feb-14 Apr-14 Jun-14 Aug-14 Volume Price

Transcript of Okt 2, 2014 Astra Agro Lestari Trimegah Securities Tbk - COMPANY FOCUS 3 FFB and 3 rd party purchase...

COMPANY FOCUS PT Trimegah Securities Tbk - www.trimegah.com 1

24% upside to DCF-based target price The one year target price implies that there are substantial price appreci-ation ahead and currently AALI is undervalued. Our recommendation are

based DCF analysis over a 10 year period and forward P/E analysis for robustness. According to our DCF analysis using WACC 10.0% the target price is Rp. 28.500 or 23.3% increase. This implies 14.3x 2015 PE, slightly lower than historical average of 14.8x PE. According to our target price the implied EV/Ha nucleus is $16.740.

Why buy

Comparing AALI to peers, FFB yield, oil extraction rate and CPO yields are one of the highest in the sector and we expect those number to remain relatively stable over the valuation period. CPO futures (1m) has

declined from RM2600/ton beginning of this year to as low as 1937/ton but has recently rebounded to RM2217/ton, we expect this to rise to at least RM2400/ton level by early Jan15. CPO production has been increas-ing and slightly exceeded our expectations in 1H14, mainly due to more than expected 3rd party FFB purchase. The YoY EPS growth rate 1H14 was 90,9% and we expect the YoY 2013—2014 EPS growth rate will be slightly lower, or 53%, mainly due to lowering CPO prices in the latter

half of the year. The EPS growth is expected to be 11.6% and 8.6% in the following years. We use 2400/2500 RM/ton CPO price in our 2014/15 forecast and let it increase at 2% per year (global inflation) from 2016. Diversified more downstream The long term prospect for the company looks good but we are aware

that AALI will fuel its revenue growth with 3rd party purchase. We expect that 3rd party FFB CAGR will be 9.9% from 2014-2024 wile nucleus production CAGR will be roughly 3%, hence the profitability margins will decrease over the valuation period. AALI sets a target of 45% coming from 3rd party which will be discuss further later in this report. Conclusions

Currently AALI is undervalued and we conclude that investors should invest in AALI. DCF analysis implies strong buy and it is backed up by our P/E ratio analysis. Currently AALI generates good cash flow in this bear market and AALI is expected generate good cash flow over the valuation period. EV/Ha nucleus is currently priced at $14.590 and EV/EBITDA is

7.68 and 13x 2014 PE and 11.6x 2016 PE.

PT Astra Agro Lestari Tbk is a leading palm oil producer in Indonesia, estab-lished since 33 years ago and headquar-tered in Jakarta

Share Price Rp23,100

Sector Plantation

Price Target Rp28.500 (23.8%)

Year end Dec 2013 2014E 2015F 2016F 2017F

Sales 12,675 16,333 19,169 20,541 22,341

Net Profit 1,834 2,805 3,130 3,398 3,618

EPS (Rp) 1,165 1,781 1,987 2,158 2,297

EPS Growth (%) -21.8% 53.0% 11.6% 8.6% 6.5%

DPS (Rp) 1,608 1,946 2,034 2,135 2241

BVPS (Rp) 9,502 10,351 11,396 12,216 13,107

P/E (x) 15.1 15.0 13,0 11,6 10,7

Div Yield (%) 6.96% 8.43% 8.81% 9.24% 9.70%

Astra Agro Lestari Company Focus

BUY Rp. 28,500

Ragnar Benediktsson

Sebastian Tobing

Okt 2, 2014

Reuters Code AALI.JK

Bloomberg Code AALI.IJ

Issued Shares (m) 1,575

Mkt Cap (Rpbn) 36,219

Avg. Value Daily 6 month (Rpm)

Rp41,334

52-Wk range Rp29,850/Rp13,100

PT. Astra International Tbk 79.7%

Public 20.3%

EPS 14F 15F

Consensus (Rp) 1,787 1,924

TRIM vs Cons. (%) (34.8) (7.4)

Strong Established Undervalued Company

Company Update

Stock Data

Major Shareholders

Consensus

Stock Price

-

1,000 ,000

2,000 ,000

3,000 ,000

4,000 ,000

5,000 ,000

6,000 ,000

7,000 ,000

8,000 ,000

-

5,000

10,000

15,000

20,000

25,000

30,000

35,000

Aug-13 Oct-13 Dec-13 Feb-14 A pr-14 Jun -14 Aug-14

Volume Price

PT Trimegah Securities Tbk - www.trimegah.com COMPANY FOCUS 2

In the section here below we will cover some positive and negative aspects of AALI. We strongly believe that the positive fac-tors outweigh the negative ones. For example we see further downstream as a positive and a negative factor. We see low level of debt as a positive factor but could come negative if the cash balance of the company will be to high.

Positive

We believe that further downstream business into Olein is positive for the company for the diversification benefits it holds. AALI already started producing Olein, Stearin and PFAD which sell at a premium to CPO and there is virtually no conversion loss from CPO to those products. There are tax benefits associated with this diversification strategy if the CPO price will increase signifi-cantly in the future. If CPO prices goes up, tax goes up, and AALI can shift its production more into Olein and other derivatives. We believe that cash generation will increase during next years that might cause for an increase in the dividend payout ratio or even support further expansion of its operations if any opportunity arises. Revenues are indirectly linked to USD that serves as a diversification strategy for long term investors. Currently AALI has a gearing ratio (total debt/total equity) of 46% which has increased during the past years. However, the company has been expanding and we believe that the gearing will decrease to 34% even with expected increase in dividend payout ratio. A recently passed law that allows plantations firms to deduct part of income VAT to its export tax can affect that company's net income if AALI will increase its CPO exports. Of the 280k ha AALI manages, 87.9% are mature plantations while the rest is immature. 45.3% of the mature estates are at prime age, or 7~18 years. AALI replanting rate is expected to be low or roughly 2,500 Ha per annum while new plating is estimated to be 8-10,000 ha per annum according to AALI spokesperson. Increased 3rd party purchase might indicate lack of land-bank so we lower our estimation of new plantings to 6,000 ha per annum.

1) Downstream— Increased revenue . FFB and CPO production is up 44% compared to 8M13 to 8M14.

2) Strong cash generation

3) Revenues linked to USD

4) Low debt level— Company can expand without increasing the risk substantially

5) Expected Increase in Dividend

6) Increased Asset Turnover

7) Low Current Market Price with high upside potential

Negative

We expect that the internal growth of AALI will be relatively slow with low re-and new plantings rate. In order to drive growth, AALI has set a target ratio of 45% of its total FFB processed will come from 3rd party. Since AALI will increase its 3rd party FFB all profitability margins will decrease and that is our main concerns for AALI and its investors. We expect that ROE will decrease slightly in the valuation period due to lowering profit margin but on the other hand, asset turnover is expected to increase due to 3rd party FFB. AALI average age profile is 14.2 years at the end of 2013 and with the rate of re-plant (2,500 per annum) and new plantings (6,000 per annum) we expect the profile to increase. We believe that the re-planting rate is low since around 7,500 ha are currently over 25 years old in 2014. The company does not disclose the land-bank it owns and we assume around 6,000 ha per year of new plantings for conservative reasons. The company is highly subjective to commodity price risk and FX risk as all the other CPO companies. AALI has to some extent diversified that risk away since it has started further downstream business, Olein, Stearin and PFAD. The company currently has low level of debt that might cause the management to ineffi-ciently manage its cash since it does not have to meet high interest payments. This can be managed with increased dividend as we expect over the valuation period. 1) Downstream—Lower Profitability Margins causing ROE to drop 2) Low Re– and New Plantings 3) Slow Internal FFB Growth 4) Commodity Price Risk and Social Risk among other risk factors 5) Low Level of Debt—High cash position not allocated into further expansion. Offset by increased Dividend, re-purchase

Source: TRIM Research

Figure 1: Average age profile of Nucleous and Plasma as of 2024 and planting rate

Immature

11%

Mature 4-15

years53%

O ld age 15<

36%

2024—Age Profile

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

7.00%

8.00%

-

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

2009 2011 2013 2015 2017 2019 2021 2023

Nucleus New and Re-planting % of total Nucleus area

PT Trimegah Securities Tbk - www.trimegah.com COMPANY FOCUS 3

FFB and 3rd party purchase

In our valuation, the expected CAGR of total nucleus area will be 2.6% which is the same as AALI achieved from 2008—2013. In 2013 the average age was 14.4 years of total trees (included plasma) while we predict the average age will slightly increase but still having majority of its trees in prime in 2024. We come to that conclusion with the estimated rate of replanting and new planting given by company spokesperson. Total FFB produced in 2013 by AALI was 5,12 mtons and with a 25.6% ratio of third party purchase the total FFB processed by AALI was 6,89 mtons. We estimate that FFB will be 12.6 mtons in 2024 with 45% ratio of 3rd party purchase. That accumulates to FFB processed by AALI to be CAGR 5.7% from 2014—2024 and FFB CAGR from Nucleus will be 3.8%. The growth will come from the 3rd party purchase with estimated CAGR of 11.6%. By increasing the 3rd party FFB will ultimately lead to lowering margins. However if we set the target of 45% in 2014 and hold it fixed over the valuation period, we see a slight increase in efficiency, that is increasing profitability margins

CPO production

The CAGR of AALI’s CPO production from 2008—2013 was 9.41%, rising from 0.98 mton to 1.54 mton. We expect that CPO CAGR from 2013—2024 will be 5.63% and CPO processed by AALI will rise to 2.81 mton in 2024 with 1.258 mton coming from Nucleus with CAGR of 2.378%. The average CPO- and Kernal extraction rate in 2013 were 22.34% and 4.76% respectively which we assume will increase at 0.5% rate over the valuation period.

CPO and its derivatives

AALI has already implemented new downstream strategy by starting producing Olein, Stearin and PFDA products at the compa-ny’s refinery at Mamuju, West Sulawesi. Joint Venture Company in Singapore (Astra-KLK Pte Ltd) was established for this purpose. This JV Company is the marketing arm to sell AALI these products and will sell the them directly to customer in India & China. AALI sets a target of 40% (600k ton 2014) of all its CPO productions will be allocated into Olein productions. The export tax on Olein products ranges from 3-4% while the tax for CPO is 9% ~ 20% and the price spread today between CPO and Olein is roughly 7.5% and average five year historical difference is 8.449%. The Olein extraction rate is estimated at 75%, Stearin 20% and PFAD is 5% according to company spokesmen. AALI moved more upstream into seedlings which we exclude from our valuations since the revenue generation is only expected to start in 2018 and the fact that other companies, such as SGRO have more competitive advantage over AALI. The cost however, is included in our valuation as a increase in R&D ex-penses. Additionally the company planted 500 ha of rubber in 2013 which we exclude from our valuations. We do not know weather or not AALI has more land-bank for its rubber plantations or if it will only use those 500 ha to produce rubber in the future.

Source: TRIM Research

Figure 2: Total FFB production Figure 3: Total CPO and Derivatives

0

2000

4000

6000

8000

10000

12000

14000

2008

2010

2012

2014E

2016E

2018E

2020E

2022E

2024E

FF

B '0

00

to

ns

FFB Produced FFB include 3rd Party

-

500

1,000

1,500

2,000

2,500

3,000

3,500

2008

2010

2012

2014E

2016E

2018E

2020E

2022E

2024E

CP

O'0

00

to

ns

CPO Production Kernel Production

Olein Production

PT Trimegah Securities Tbk - www.trimegah.com COMPANY FOCUS 4

Revenues

We expect the CAGR of revenues from 2014—2024 will be 8.6% compared to GAGR of 9.2% from 2008—2013. The growth in revenue mostly comes from 3rd party FFB, which we expect to be CAGR 11.57% over the valuation period, which ultimately leads to diminishing profitability margins. The NI CAGR growth over the same period is expected to be 6.3% In our valuation we assume that the benchmark price for 2014 will be 2,400 ringgit per ton and 2,500 ringgit per ton in 2015 and increase at a 2% yearly rate there after. We can at most let the CPO price increase with world inflation for conservative reasons. Five year historical ave. price of Kernel is roughly 60% of CPO and we use that assumption in our valuation. Olein is sold at a premium of (8.5%) to CPO and we use that premium over the valuation period and a 3.5% tax rate. Same assumptions are used for Stea-rin and PFAD. Since we assume that the price of CPO will increase 2% per annum from 2,500 MYR so our tax rate we use for CPO prices will range from 13.83% ~ 16.1%.

We are aware that the growth numbers seem to be bullish. However, if we assume that AALI gets the 45% FFB 3rd party target ratio in 2015, the revenues will be the same at the end of the period. We just assume for a steady growth in the 3rd party FFB purchase to smooth the revenues over the valuation period. We can also expect that the 45% target might be reached in the near future. However, according to our calculation that will decrease the valuation of the company, due to lower margins in the initial periods. We also assume that AALI does not have the capacity yet to have 45% 3rd party ratio. We expect the CPO sales will decline YoY 33.9% 2013 to 2014 while production will increase 17.3% from 2013 – 2014 since AALI is allocating to Olein. However, 8M14 FFB is up YoY 43.9% and CPO 44%, mostly due to the increase in 3rd party FFB. So this year historical numbers are not far from our expectations, we just want to smooth the expectations over the valuation period.

Source: TRIM Research

Figure 4: Trimegah revenue, cost and net income forecast for AALI

(Rpbr) 2013 2014 2015E 2016E 2017E 2018E 2019E 2020E 2021E 2022E

Revenue 12,675 16,333 19,169 20,541 22,341 24,380 26,105 28,572 31,529 33,791

-CPO revenue 11,479 7,929 9,282 10,028 10,901 11,890 12,589 13,771 15,188 16,270

-Kernel revenue 1,188 1,981 2,164 2,169 2,369 2,597 2,763 3,038 3,367 3,625

-Olein revenue 0 4,817 5,844 6,313 6,863 7,485 8,136 8,900 9,816 10,514

-Rubber and others 0 1,606 1,880 2,031 2,208 2,408 2,617 2,863 3,157 3,382

- % Change - 28,9% 17,4% 7,2% 8,8% 9,1% 7,1% 9,5% 10,3% 7,2%

COGS 8,593 11,074 13,010 14,239 15,606 17,192 18,550 20,544 22,988 24,793

Gross profit 4,082 5,259 6,159 6,303 6,735 7,189 7,555 8,028 8,540 8,998

-% Sales 32,2% 32,2% 32,1% 30,7% 30,1% 29,5% 28,9% 28,1% 27,1% 26,6%

Administrative 586 661 769 826 888 970 1.030 1.126 1.228 1.318

Sales & Marketing 491 633 743 796 866 945 1.012 1.108 1.222 1.310

EBIT 3,012

3,964

4,647

4,681

4,981

5,274

5,513

5,794

6,090

6,370

-% Sales 23,8% 24,3% 24,2% 22,8% 22,3% 21,6% 21,1% 20,3% 19,3% 18,9%

Other Income or Expenses

(399) 260

78

105

119

137

149

163

182

201

EBT 2,605

4,224

4,725

4,785

5,100

5,411

5,662

5,958

6,272

6,571

Income tax (702)

(1.014)

(1.142) (1.156)

(1.232)

(1.308)

(1.368)

(1.440)

(1.516)

(1.588)

Net Income 1,834

2,805

3,130

3,398

3,618

3,832

4,004

4,203

4,411

4,614

-% Sales 14,5% 17,2% 16,3% 16,5% 16,2% 15,7% 15,3% 14,7% 14,0% 13,7%

PT Trimegah Securities Tbk - www.trimegah.com COMPANY FOCUS 5

Source: TRIM research

Figure 5: YoY Growth for AALI for the initial valuation period

COGS, OPEX, EBIT and Net Income

After AALI started to purchase FFB from 3rd party the gross profit margin has been falling. Before AALI started purchase 3rd

party FFB, the gross profit margin was on average 41.43% from 2008 - 2011. After the company started purchasing third party

FFB the margin lowered to 32.2% in 2013. We assume an average gross profit margin of 30.5% over the entire forecast period

with roughly 27.5 gross profit margin for perpetuity. We expect that AALI growth will come from 3rd party FFB, hence we expect

all margins to decrease. Gross profit margin is expected to be on average around 30.5% and will drop to 27.1% in 2024. The

most dominant factor in COGS is the total raw materials used and processing cost and we allocate all the 3rd party FFB pur-

chase cost into that category. The remaining cost is incurred by AALI own FFB production, which we historically link to its nucle-

us estates. We expect AALI cost for its own production will increase additionally 3% per year. Harvesting and maintenance cost

are directly linked to revenue while salary is expected to lower from CAGR 10.9% as of 2013 and reach CAGR 7.5% in 2017 to

perpetuity. We assume OPEX to be roughly 8% of revenue over the valuation period.

EBITDA margin will be on average 24.3% from 2014 – 2024 with an EBITDA margin as of 2014 at 28.12% and 21.8% into

perpetuity. EBIT margin will be on average 21.16% from 2014 – 2024 with an EBIT margin as of 2014 at 27.7% and 19.8% for

perpetuity. NI growth is expected to be 53% in 2014 and 11.19% for 2015 and 8.58% in 2016. NI margin is expected to fall

over the period to approximately 14.0% for perpetuity and the average NI margin is expected to be 15.22% over the valuation

period.

Source: TRIM Research

Figure 6: Expected Revenues stream, COGS, gross profit margin and NI margin

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

40.0%

45.0%

50.0%

Rp-

Rp5,000

Rp10,000

Rp15,000

Rp20,000

Rp25,000

Rp30,000

Rp35,000

Rp40,000

2008 2010 2012 2014E 2016E 2018E 2020E 2022E 2024E

Revenue COGS Gross Profit Margin NI margin

YoY Growth 2013 2014E 2015F 2016F 2017F

Revenue 9,60% 28.86% 17.36% 7.16% 8,76%

Gross Profit -6,32% 28,83% 17,12% 2,34% 6,86%

Operating Profit -13,01% 31,94% 17,23% 0,72% 6,42%

Net Profit -21,84% 52,96% 11,57% 8,58% 6,46%

Planted area 3,48% 4,09% 3,93% 2,52% 2,46%

FFB Production -6,80% 8,85% 3,43% 2,45% 2,80%

FFB Incl. 3rd Party 3,99% 12,82% 6,15% 5,39% 6,04%

CPO Production 4,22% 13,41% 6,68% 5,92% 6,57%

ASP 5.64% 1.52% 9.73% 2.00% 2.00%

PT Trimegah Securities Tbk - www.trimegah.com COMPANY FOCUS 6

Financial leverage will decrease from 43% to roughly 33.8% over the entire valuation period. Currently it is historically high

since the financial leverage was 15.22% in 2012. and under 10% prior to that. We expect that long term debt will be paid off

in coming years and most of the operations will be financed with operating cash flow and short term bank loans.

Like previously stated we expect that the profitability margins will decrease along with ROE and ROA over the valuation period.

When researching the causes for the ROE drop, it is mainly caused by lowering NI margin and lower financial gearing. Asset

turnover will increase slightly over the period since we expect that 3rd party FFB purchase will fuel AALI sales and they will

grow faster than AALI assets. Our expectations can be seen in the following graphs for further understanding.

Source: TRIM Research

Figure 7: Profitability margins will decrease due to increase in 3rd party FFB

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

35%

0.5

0.7

0.9

1.1

1.3

1.5

1.7

2009 2011 2013 2015 2017 2019 2021 2023

Assets Turnover Financial Gearing Profit Margin ROE

Source: TRIM Research

Figure 8: Expected Profitability Margins

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

2008

2010

2012

2014E

2016E

2018E

2020E

2022E

2024E

Gross Profit Margin EBITDA margin EBIT margin NI margin

PT Trimegah Securities Tbk - www.trimegah.com COMPANY FOCUS 7

Source: TRIM Research

We assume CAPEX will be stable over the valuation period due to same rate of planting and fixed asset growth rate. AALI needs

one CPO mill for every 5,000 Ha of land therefore we estimate a steady fixed asset growth over the valuation period and we

assume one CPO mill per year. The CAPEX increase seen in year 2012 – 2014 is partly due high planting rate and also building

refinery for its Olein production. The CAPEX can decrease if AALI emphasis more on re-plantings instead of new plantings and

still using the 8,500 Ha per annum estimates and that might increase AALI value of 2-4% from our estimated target price. To

estimate the fixed assets we use five year historical growth and use that as a proxy for the entire valuation period. When

looking at H1-2014 we are fairly close to the fixed assets AALI reports using that method. Regarding the plantations part of the

CAPEX, we calculate a ratio of the book value of planted nucleus over hectares of nucleus. We use a five year historical ratio

and apply that ratio to find the expected cost plus inflationary effects.

We expect that AALI will be able to relatively sustain its ROIC over our estimated WACC of 10.001%. Therefore AALI is able to

create additional value for its stakeholder. The average ROIC from 2008—2013 was 31.8% but declined to 20.1% in 2013. The

1H14 ROIC was 11.43% and we expect the 2014 ROIC to be around 23.5% by using expected average CPO price MYR 2,500.

We expect the average ROIC over the valuation period to be around 22% and slightly giving in in the latter part of our valua-

tion but still over the AALI estimated WACC, further supporting our estimation that AALI is currently under-valued in the mar-

ket.

Source: xxxx

Figure 10: Return on invested capital over the valuation period

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

2009 2011 2013 2015E 2017E 2019E 2021E 2023E

ROIC

Figure 11: Expected CAPEX and Depreciation over the valuation period Figure 9: Expected CAPEX and Depreciation over the valuation period

Rp-

Rp500

Rp1,000

Rp1,500

Rp2,000

Rp2,500

Rp3,000

2009

2011

2013

2015E

2017E

2019E

2021E

2023E

Yearly depreciation expenses CAPEX

PT Trimegah Securities Tbk - www.trimegah.com COMPANY FOCUS 8

Source: TRIM Research

Beta 0,803

Dept premium 5,00%

Risk free rate 7,500%

Cost of Debt 3,920%

Debt in WACC Calculations 8,920%

Cost of Debt after tax 6,690%

Market Risk 12,500%

TAX 25,00%

D/D+E 31,38%

E/E+D 68,62%

CAPM 11,52%

Special Risk Premium 0%

Cost of Equity 11,515%

Long Term Growth 3,000%

WACC 10,001%

WACC Calculations

Figure 11: WACC calculations with terminal growth of 3%

Cost of equity and the weighted average cost of capital

To calculate the cost of equity we use 5 year adjusted beta since it approximately captures one economic cycle of CPO price

fluctuations. The explanatory power of our model captures roughly 12.5% of AALI movements to the market. A special risk

premium can be added that captures the idiosyncratic risk of the company among other risks factors that our model does not

capture. This added risk lowers the valuation of the company and can be looked as a more conservative approach to the valua-

tion. It is difficult to valuate special risk premium for individual companies so we simple show how a special risk premium

added on the cost of equity will affect the target price. That can be seen on the following page.

We assume that the risk free rate is 7.5% and the market risk premium is 5%. Therefore our estimated cost of equity is

11.515%. The cost of debt is calculated using the actual paid interest to debt and debt premium of 5%. The long term tax rate

used is 25% which is the maximum tax bracket in Indonesia. However, we use 30% tax rate in 2014 and 2015 for our P/E

valuation since it more resembles current tax rate. The current D/E ratio is 45.7% with a target ratio of 25% and the calculat-

ed WACC is 10.001%.

Source: xxxx

PT Trimegah Securities Tbk - www.trimegah.com COMPANY FOCUS 9

Source: TRIM Research

Periods 2016E 2017E 2018E 2019E 2020E 2021E 2022E 2023E 2024E

EBIT x (1 - tax) 3.511

3.736

3.955

4.135

4.346

4.568

4.778

5.044

5.355

Capital Expenditure (1.558)

(1.561)

(1.541)

(1.502)

(1.442)

(1.489)

(1.538)

(1.589)

(1.641)

Changes in NonCash WorkCap (3)

25

24

18

20

17

21

32

40

Depreciation & Amortization 724

762

797

829

857

885

915

945

977

Minority Interest 191

208

227

243

266

293

314

329

346

FCFF 2.482

2.753

3.008

3.237

3.514

3.688

3.861

4.103

4.384

Discount Factor 0,9091

0,8264

0,7513

0,6830

0,6209

0,5644

0,5131

0,4665

0,4241

PV of FCFF 2.256

2.275

2.260

2.211

2.182

2.082

1.981

1.914

1.859

Terminal Value 64.191

Sum of PV of FCFF 19.020

PV of Terminal Value 27.221

Cash & Marketable Sec 306

Debt 1.693

DCF Value 44.854

Total shares (million) 1.575

Target Price 28.484

Current Price 23,100

Difference from current market price

23.3%

Recommendation BUY

Figure 12: Expected Free Cash Flow to Firm over the valuation period

Cash flow valuation and sensitivity analysis

In this valuation we are looking at target price of 2016. According to our assumptions in the DCF analysis of AALI, there is

still underlying value in the stock that has yet to be realized. We conclude that each share should be valued at be Rp. 28.500.

The main drivers of our results come mainly from low current market value of AALI and AALI will be able to double its reve-

nue during the next 10 years. Additionally, beta of CPO companies are often under 1, therefore we use low WACC. We be-

lieve that AALI is under valued in the current CPO bear market and we expect that the share price will increase over 20%

when the CPO prices will increase. Currently the 1-month forward price has reached over 2,220 ringgit/mt.

Special Risk Premium Value (Rp)

0.50% 27,041

1.00% 25,728

1.50% 24,529

2.00% 23,429

2.50% 22,416

WACC

10.34%

10.69%

11.02%

11.37%

11.72%

3.00% 12.06% 21,481

As can be seen by adding a special risk premium to the cost of

equity, there is a lot of room for the equity risk to increase

before it falls below the current market value . This further

strengthens our believes that AALI is undervalued in this cur-

rent bear market.

PT Trimegah Securities Tbk - www.trimegah.com COMPANY FOCUS 10

P/E band and peer comparison

AALI’S P/E band indicates that investors should strongly buy in ALLI with its current market price. According to our assump-

tions in the one year forward P/E analysis that there is even greater underlying value in the stock that has yet to be realized.

The calculated expected price from our P/E analysis strongly supports our DCF analysis. The five year average forward PE is

14.83 and expected EPS 2015 Rp. 1.987 implies a price of Rp. 29.500.

When comparing AALI to its peers, AALI is slightly over its peers when looking at the price rations. However, AALI is perform-

ing above average when looking at the extraction rates and yields which can be seen in next page and that explains to some

extent the comparative price difference between AALI and others.

The final conclusion is that investors should buy in AALI for few several reasons that are in no particular order

1) Upside potential of over 24% and could reach as high as 28.4% (P/E analysis)

2) Cash generating company even in record bear market

3) Low financial leverage

4) Revenues linked to foreign exchange that will bring diversification benefits for an investor

5) Above average FFB yield and CPO extraction rates that are expected to remain stable or even increase

Source: TRIM Research

Figure 13: Forward P/E band

Company EV/Ha EV/EBITDA P/EBITDA P/E P/E14 P/E15 P/B

Average $ 14,138 6.6 6.4 16.5 13.0 10.2 2.6

AALI $ 14,590 7.7 7.8 14.8 13.0 12.1 3.4

SMAR $ 20,766 - 7.5 18.5 - - 2.6

SIMP $ 7,584 5.7 4.9 14.3 12.0 10.9 0.9

LSIP $ 8,519 6.4 - 12.5 12.2 11.5 1.9

SSMS $ 30,823 8.4 7.8 13.8 15.5 12.5 5.3

SGRO $ 6,036 5.6 5.2 14.0 11.1 9.5 1.4

DSNG $ 17,070 6.1 7.5 32.9 11.2 9.9 4.3

Figure 14: Ratio analysis of peers: Consensus Estimates

Source: TRIM Research

0.00

5.00

10.00

15.00

20.00

25.00

Jan-08 Jul-08 Jan-09 Jul-09 Jan-10 Jul-10 Jan-11 Jul-11 Jan-12 Jul-12 Jan-13 Jul-13 Jan-14 Jul-14

Fwd PE -2 Stdv -1 Stdv Average PE +1 Stdv +2 Stdv

PT Trimegah Securities Tbk - www.trimegah.com COMPANY FOCUS 11

Risk Factors

AALI is mostly affected by external risk factors which are beyond the company’s control such as exchange rate risk and com-

modity price risk. AALI has implemented a system of cash received in advance from domestic sales transactions and that

mitigates their cash flow risk. Additionally to that, the allocation into Olein will diversify the revenue stream of the company.

The company business operations are dominated by the up-keep of the palm oil trees. The main risk AALI faces here is if the

spread of cost and CPO will decrease. To some extent AALI has mitigated this risk by putting more effort in its own production

of biomass fertilizers to reduce chemical fertilizers.

The liquidity risk management includes managing the profile of loans maturities and funding sources and maintaining sufficient

cash positions of all times. AALI has entered into agreements with banks that are ready to provide financing facilities for AALI if

needed. AALI actively seeks for a competitive cost of capital to refinances its loans. Currently the company has a cash position

of Rp.692 bn 1H14, which is a small deduction from previous year. AALI quick ratio is something to be concern about since it

has been 0.2 since 2012 while it was always over 1.0 from 2008—2010. The cash ratio tells similar story but is more conserva-

tive approach to evaluating the liquidity. We don't expect that the quick ratio will gain its former position until 2020 or 2021

and it might cause some liquidity problems.

The legal risk AALI faces is due to land constitutes and disputes. In 2012 and 2013 the cost of legal process due to this risk

raised considerable. The Company mitigates this risk by having completed all documents and permits for land holding. There is

a possibility of catastrophic risk that is caused by natural disasters. To mitigating this risk, the Company spreads this risk with

several insurance firms and different operating locations.

To mitigate the supplier risk, no suppliers of FFB exceeds 10% of AALI net revenue.

The company’s operations are located in Sumatera, Kalimantan and Sulawesi which causes additional cost for the company but

mitigates Catastrophic Risk.

Source: Company

Figure 15. FY13 and 1H14 FFB Yield (MT/Ha) (LHS) and CPO Oil Extraction Rate (RHS)

Source: Company

Figure 16. FY13 and 1H14 CPO Yield (MT/Ha)

0

5

10

15

20

25

30

0

5

10

15

20

25

30

SS

MS

DS

NG

AA

LI

GA

R

FIR

ST r

es

SIM

P

LS

IP

BW

PT

SG

RO

FFB YIELD (MT/Ha) FY13 FFB YIELD (MT/Ha) 6M14

FFB YIELD (MT/Ha) SECTOR FFB YIELD (MT/Ha) SECTOR

18.0%

19.0%

20.0%

21.0%

22.0%

23.0%

24.0%

25.0%

18.0%

19.0%

20.0%

21.0%

22.0%

23.0%

24.0%

25.0%

SS

MS

DS

NG

AA

LI

GA

R

FIR

ST r

es

SIM

P

LS

IP

BW

PT

SG

RO

Oil Extraction Rate 6M14 Oil Extraction Rate SECTOR

5.1

6.4

4.6 4.74.3

3.6 3.8 3.7

2.62.9 3

2.3 2.51.8 1.8 2

1.3 1.4

0

1

2

3

4

5

6

7

SSMS DSNG AALI GAR FIRST res SIMP LSIP BWPT SGRO

CPO Yield (MT/Ha) FY13 CPO Yield (MT/Ha) 6M14

CPO Yield (MT/Ha) SECTOR '13 4,3 CPO Yield (MT/Ha) SECTOR '14 2,2

PT Trimegah Securities Tbk - www.trimegah.com COMPANY FOCUS 12

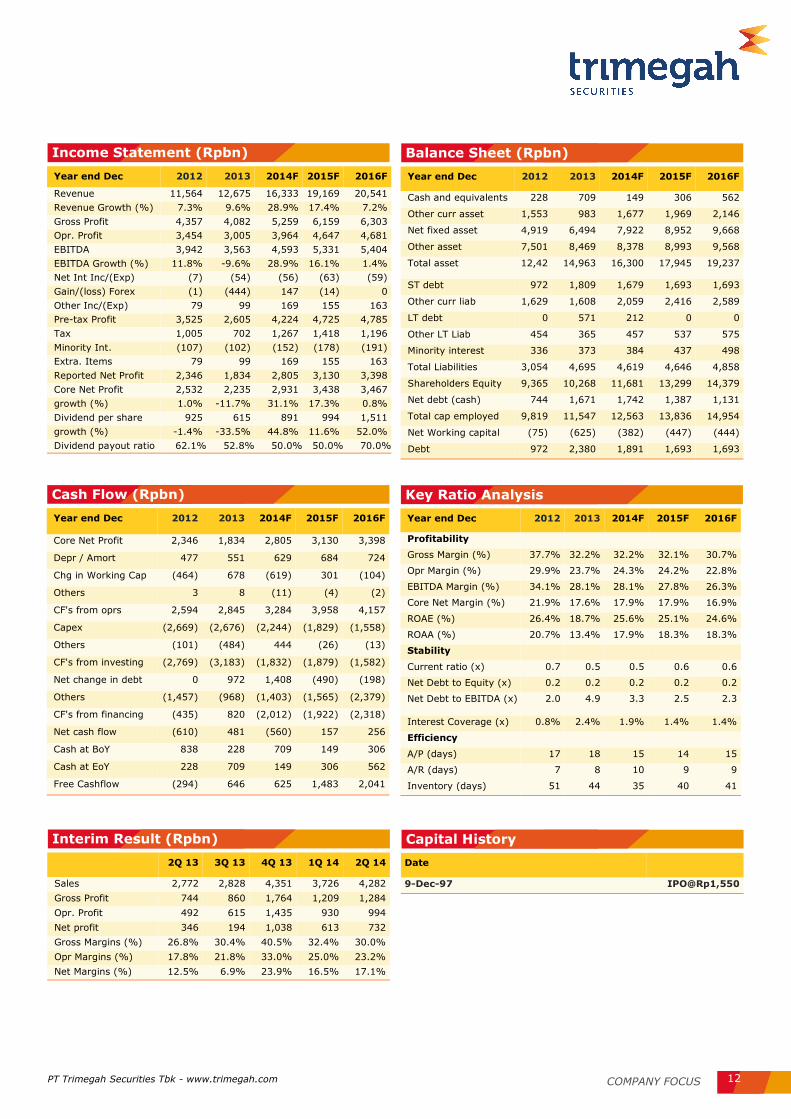

Income Statement (Rpbn)

Year end Dec 2012 2013 2014F 2015F 2016F

Revenue 11,564 12,675 16,333 19,169 20,541

Revenue Growth (%) 7.3% 9.6% 28.9% 17.4% 7.2%

Gross Profit 4,357 4,082 5,259 6,159 6,303

Opr. Profit 3,454 3,005 3,964 4,647 4,681

EBITDA 3,942 3,563 4,593 5,331 5,404

EBITDA Growth (%) 11.8% -9.6% 28.9% 16.1% 1.4%

Net Int Inc/(Exp) (7) (54) (56) (63) (59)

Gain/(loss) Forex (1) (444) 147 (14) 0

Other Inc/(Exp) 79 99 169 155 163

Pre-tax Profit 3,525 2,605 4,224 4,725 4,785

Tax 1,005 702 1,267 1,418 1,196

Minority Int. (107) (102) (152) (178) (191)

Extra. Items 79 99 169 155 163

Reported Net Profit 2,346 1,834 2,805 3,130 3,398

Core Net Profit 2,532 2,235 2,931 3,438 3,467

growth (%) 1.0% -11.7% 31.1% 17.3% 0.8%

Dividend per share 925 615 891 994 1,511

growth (%) -1.4% -33.5% 44.8% 11.6% 52.0%

Dividend payout ratio 62.1% 52.8% 50.0% 50.0% 70.0%

Balance Sheet (Rpbn)

Year end Dec 2012 2013 2014F 2015F 2016F

Cash and equivalents 228 709 149 306 562

Other curr asset 1,553 983 1,677 1,969 2,146

Net fixed asset 4,919 6,494 7,922 8,952 9,668

Other asset 7,501 8,469 8,378 8,993 9,568

Total asset 12,42 14,963 16,300 17,945 19,237

ST debt 972 1,809 1,679 1,693 1,693

Other curr liab 1,629 1,608 2,059 2,416 2,589

LT debt 0 571 212 0 0

Other LT Liab 454 365 457 537 575

Minority interest 336 373 384 437 498

Total Liabilities 3,054 4,695 4,619 4,646 4,858

Shareholders Equity 9,365 10,268 11,681 13,299 14,379

Net debt (cash) 744 1,671 1,742 1,387 1,131

Total cap employed 9,819 11,547 12,563 13,836 14,954

Net Working capital (75) (625) (382) (447) (444)

Debt 972 2,380 1,891 1,693 1,693

Cash Flow (Rpbn)

Year end Dec 2012 2013 2014F 2015F 2016F

Core Net Profit 2,346 1,834 2,805 3,130 3,398

Depr / Amort 477 551 629 684 724

Chg in Working Cap (464) 678 (619) 301 (104)

Others 3 8 (11) (4) (2)

CF's from oprs 2,594 2,845 3,284 3,958 4,157

Capex (2,669) (2,676) (2,244) (1,829) (1,558)

Others (101) (484) 444 (26) (13)

CF's from investing (2,769) (3,183) (1,832) (1,879) (1,582)

Net change in debt 0 972 1,408 (490) (198)

Others (1,457) (968) (1,403) (1,565) (2,379)

CF's from financing (435) 820 (2,012) (1,922) (2,318)

Net cash flow (610) 481 (560) 157 256

Cash at BoY 838 228 709 149 306

Cash at EoY 228 709 149 306 562

Free Cashflow (294) 646 625 1,483 2,041

Key Ratio Analysis

Year end Dec 2012 2013 2014F 2015F 2016F

Profitability

Gross Margin (%) 37.7% 32.2% 32.2% 32.1% 30.7%

Opr Margin (%) 29.9% 23.7% 24.3% 24.2% 22.8%

EBITDA Margin (%) 34.1% 28.1% 28.1% 27.8% 26.3%

Core Net Margin (%) 21.9% 17.6% 17.9% 17.9% 16.9%

ROAE (%) 26.4% 18.7% 25.6% 25.1% 24.6%

ROAA (%) 20.7% 13.4% 17.9% 18.3% 18.3%

Stability Current ratio (x) 0.7 0.5 0.5 0.6 0.6

Net Debt to Equity (x) 0.2 0.2 0.2 0.2 0.2

Net Debt to EBITDA (x) 2.0 4.9 3.3 2.5 2.3

Interest Coverage (x) 0.8% 2.4% 1.9% 1.4% 1.4%

Efficiency A/P (days) 17 18 15 14 15

A/R (days) 7 8 10 9 9

Inventory (days) 51 44 35 40 41

Interim Result (Rpbn)

2Q 13 3Q 13 4Q 13 1Q 14 2Q 14

Sales 2,772 2,828 4,351 3,726 4,282

Gross Profit 744 860 1,764 1,209 1,284

Opr. Profit 492 615 1,435 930 994

Net profit 346 194 1,038 613 732

Gross Margins (%) 26.8% 30.4% 40.5% 32.4% 30.0%

Opr Margins (%) 17.8% 21.8% 33.0% 25.0% 23.2%

Net Margins (%) 12.5% 6.9% 23.9% 16.5% 17.1%

Capital History

Date

9-Dec-97 IPO@Rp1,550

PT Trimegah Securities Tbk - www.trimegah.com COMPANY FOCUS 13

Source: TRIM Research

Figure 17: CPO daily prices from 2008 until today

MYR -

MYR 1,000

MYR 2,000

MYR 3,000

MYR 4,000

MYR 5,000

1/2

/2

00

8

7/2

/2

00

8

1/2

/2

00

9

7/2

/2

00

9

1/2

/2

01

0

7/2

/2

01

0

1/2

/2

01

1

7/2

/2

01

1

1/2

/2

01

2

7/2

/2

01

2

1/2

/2

01

3

7/2

/2

01

3

1/2

/2

01

4

7/2

/2

01

4

CPO 1m Forward

PT Trimegah Securities Tbk

Gedung Artha Graha 18th Floor

Jl. Jend. Sudirman Kav. 52-53

Jakarta 12190, Indonesia

t. +62-21 2924 9088

f. +62-21 2924 9150

www.trimegah.com

DISCLAIMER

This report has been prepared by PT Trimegah Securities Tbk on behalf of itself and its affiliated companies and is provided for information

purposes only. Under no circumstances is it to be used or considered as an offer to sell, or a solicitation of any offer to buy. This report has

been produced independently and the forecasts, opinions and expectations contained herein are entirely those of Trimegah Securities.

While all reasonable care has been taken to ensure that information contained herein is not untrue or misleading at the time of publication,

Trimegah Securities makes no representation as to its accuracy or completeness and it should not be relied upon as such. This report is

provided solely for the information of clients of Trimegah Securities who are expected to make their own investment decisions without reliance

on this report. Neither Trimegah Securities nor any officer or employee of Trimegah Securities accept any liability whatsoever for any direct or

consequential loss arising from any use of this report or its contents. Trimegah Securities and/or persons connected with it may have acted

upon or used the information herein contained, or the research or analysis on which it is based, before publication. Trimegah Securities may in

future participate in an offering of the company’s equity securities.