OK_0411_Trmmed

36

OIADA, P.O. Box 6905, Moore, OK 73153 PRSRT Standard U.S. Postage PAID DALLAS, TEXAS Permit No. 2079 Change Service Requested OIADA, P.O. Box 6905, Moore, OK 73153 Jim Holman Named OIADA Quality Dealer for 2011 Page 4 Compliance Benchmarks Page 6 Tax Changes for Small Businesses Page 16

description

OIADA, P.O. Box 6905, Moore, OK 73153 OIADA, P.O. Box 6905, Moore, OK 73153 PRSRT Standard DALLAS, TEXAS U.S. Postage Permit No. 2079

Transcript of OK_0411_Trmmed

OIADA, P.O. Box 6905, Moore, OK 73153

PRSRT Standard

U.S. Postage

PAIDDALLAS, TEXAS

Permit No. 2079

Change Service Requested

OIADA, P.O. Box 6905, Moore, OK 73153

Jim Holman Named OIADA Quality Dealer for 2011Page 4

Compliance BenchmarksPage 6

Tax Changes for Small BusinessesPage 16

APRIL 2011 D E A L E R S ’ R E S O U R C E

3

w w w . e - o i a d a . c o m

OIADAOFFICE813 NORTHWEST 34TH MOORE, OK 73160EMAIL: [email protected]

ROSE & ODELL MORGAN, Executive DirectorsJACKIE GARNER, Office Manager

AMBER SNOOK, Administrative AssistantJARED MORGAN, Electronics/Software Technician

LYNNA KAY, ProgrammerSTEVE MORGAN, ConsultantMIKE MORGAN,Technical Aide

al.netal.net

NATIONAL INDEPENDENT AUTOMOBILE DEALERS ASSOCIATION

NIADA HEADQUARTERS:

PHONE (817) 640-3838FOR ADVERTISING INFORMATION CONTACT: TROY GRAFF (800) 682-3837 OR [email protected]’ RESOURCE IS A PUBLICATION OF AUTOMOTIVE DEAL-ERS RESOURCE OF OKLAHOMA (ADR) PRODUCED ON BEHALF OF THE OKLAHOMA INDEPENDENT AUTOMOBILE DEALERS AS-SOCIATION (OIADA), P.O. BOX 6905, MOORE, OK 73153. THE DEALERS’ RESOURCE IS PUBLISHED MONTHLY BY THE NATIONAL INDEPENDENT AUTOMOBILE DEALERS ASSOCIATION SERVICES CORPORATION. PERIODICAL POSTAGE PAID AT ARLINGTON, TX, AND AT ADDITIONAL OFFICES. POSTMASTER: SEND ADDRESS CHANGES TO OIADA, P.O. BOX 6905, MOORE, OK 73153. THE STATEMENTS AND OPINIONS EXPRESSED HEREIN ARE THOSE OF THE INDIVIDUAL AUTHORS AND DO NOT NECESSARILY REP-RESENT THE VIEWS OF ADR OF OKLAHOMA, THE OKLAHOMA INDEPENDENT AUTOMOBILE DEALERS ASSOCIATION OR THE NATIONAL INDEPENDENT AUTOMOBILE DEALERS ASSOCIA-TION. LIKEWISE, THE APPEARANCE OF ADVERTISERS, OR THEIR IDENTIFICATION AS MEMBERS OF OIADA OR NIADA DOES NOT CONSTITUTE AN ENDORSEMENT OF THE PRODUCTS OR SERVIC-ES FEATURED. COPYRIGHT © 2011 BY O&R MORGAN, INC. DBA OIADA. ALL RIGHTS RESERVED. DEALERS’ RESOURCE IS A PUBLI-CATION OF AUTOMOTIVE DEALERS RESOURCE OF OKLAHOMA ON BEHALF OF THE OKLAHOMA INDEPENDENT AUTOMOBILE DEALERS ASSOCIATION (OIADA), BUT IS MAILED TO ALL DEAL-ERS IN THE STATE IN AN EFFORT TO EDUCATE AND ENCOUR-AGE NON-MEMBERS TO JOIN THE ASSOCIATION AND SUPPORT OUR EFFORTS TO IMPROVE THE IMAGE AND PROFIT POTENTIAL OF THE INDUSTRY. FOR 55 YEARS, WE HAVE WORKED TO REP-RESENT THE INDEPENDENT MOTOR VEHICLE DEALER IN OKLA-HOMA. WE NEED YOUR SUPPORT.FRONT COVER BY Mike MorganSTATE MAGAZINE MGR./SALESEDITORPRODUCTION MGR.ART/PRODUCTION MGR. PRINTING

MAGAZINECONTENTSNINSIDE

ADVERTISERSINDEX

PRESIDENTChris GoadRegal Motors3515 N. MayOklahoma City, OK [email protected]

CHAIRMAN OF THE BOARDJohn EasttomAuto Mart of Elk CityP.O. Box 981Elk City, OK [email protected]

SECRETARY/ TREASURERBruce BeamDealers Auto Auction of OKC1028 S. PortlandOklahoma City, OK 73147405-947-2886www.daaokc.com

VICE PRESIDENTSJohn T. Longacre, IVTaft Motors, Inc.722 S. Linden St.Sapulpa, [email protected]

Julian CoddingReliable Motors, Inc.9201 S. ShieldsOklahoma City, [email protected]

Monte ShockleyShockley Auto Sales2605 N. BroadwayPoteau, OK 74953918-647-3999

[email protected] Glenn McDanielI-35 Credit Auto1113 SE 51st St.Oklahoma City, OK [email protected]

David McQuerryMcQuerry Motors, Inc.1302 N. Harrison St.Shawnee, OK [email protected]

11 ADESA 17

7 5

219

19

151813

4 Jim Holman Named OIADA Quality Dealer for 2011

6 Compliance Benchmarks

16 Tax Changes for Small Businesses

FOR INFORMATION ON HOW TO BECOME A MEMBER OF OIADA PLEASE CONTACT ROSE OR ODELL MORGAN AT 405-232-2947.

BOARD OF DIRECTORS

D E A L E R S ’ R E S O U R C E APRIL 2011

4

w w w . e - o i a d a . c o m

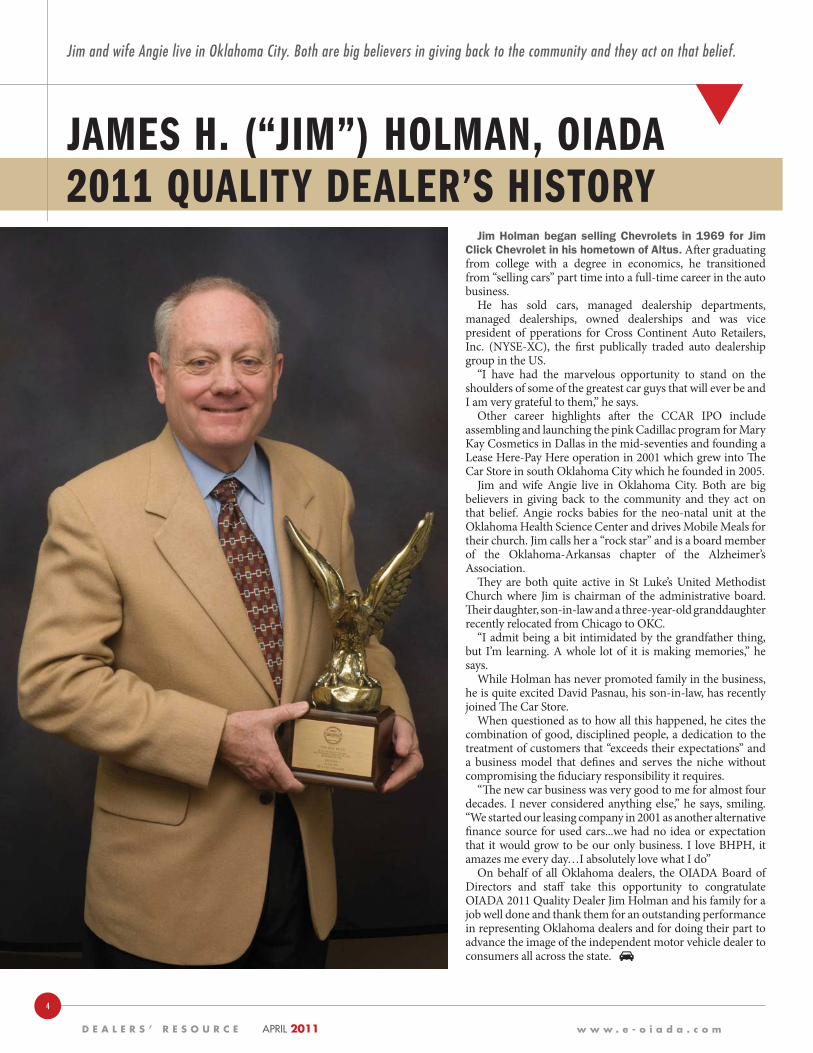

JAMES H. (“JIM”) HOLMAN, OIADA 2011 QUALITY DEALER’S HISTORY

Jim and wife Angie live in Oklahoma City. Both are big believers in giving back to the community and they act on that belief.

Jim Holman began selling Chevrolets in 1969 for Jim

Click Chevrolet in his hometown of Altus. After graduating from college with a degree in economics, he transitioned from “selling cars” part time into a full-time career in the auto business.

He has sold cars, managed dealership departments, managed dealerships, owned dealerships and was vice president of pperations for Cross Continent Auto Retailers, Inc. (NYSE-XC), the first publically traded auto dealership group in the US.

“I have had the marvelous opportunity to stand on the shoulders of some of the greatest car guys that will ever be and I am very grateful to them,” he says.

Other career highlights after the CCAR IPO include assembling and launching the pink Cadillac program for Mary Kay Cosmetics in Dallas in the mid-seventies and founding a Lease Here-Pay Here operation in 2001 which grew into The Car Store in south Oklahoma City which he founded in 2005.

Jim and wife Angie live in Oklahoma City. Both are big believers in giving back to the community and they act on that belief. Angie rocks babies for the neo-natal unit at the Oklahoma Health Science Center and drives Mobile Meals for their church. Jim calls her a “rock star” and is a board member of the Oklahoma-Arkansas chapter of the Alzheimer’s Association.

They are both quite active in St Luke’s United Methodist Church where Jim is chairman of the administrative board. Their daughter, son-in-law and a three-year-old granddaughter recently relocated from Chicago to OKC.

“I admit being a bit intimidated by the grandfather thing, but I’m learning. A whole lot of it is making memories,” he says.

While Holman has never promoted family in the business, he is quite excited David Pasnau, his son-in-law, has recently joined The Car Store.

When questioned as to how all this happened, he cites the combination of good, disciplined people, a dedication to the treatment of customers that “exceeds their expectations” and a business model that defines and serves the niche without compromising the fiduciary responsibility it requires.

“The new car business was very good to me for almost four decades. I never considered anything else,” he says, smiling. “We started our leasing company in 2001 as another alternative finance source for used cars...we had no idea or expectation that it would grow to be our only business. I love BHPH, it amazes me every day…I absolutely love what I do”

On behalf of all Oklahoma dealers, the OIADA Board of Directors and staff take this opportunity to congratulate OIADA 2011 Quality Dealer Jim Holman and his family for a job well done and thank them for an outstanding performance in representing Oklahoma dealers and for doing their part to advance the image of the independent motor vehicle dealer to consumers all across the state.

��

D E A L E R S ’ R E S O U R C E APRIL 2011

6

w w w . e - o i a d a . c o m

When dealers think about bench-marks, financial and numerical items such as profitability, expenses, inventory turn and finance and insurance penetra-

tion come to mind. Often overlooked are benchmarks for legal and regulatory com-pliance, which can have a significant im-pact on a dealership’s bottom line. We fre-quently receive inquiries requesting advice on what a motor vehicle dealer should be doing in this area.

The following list of suggestions will help you set legal and regulatory compli-ance benchmarks for various areas within your dealership:

Paperwork: Dealers should have their paperwork reviewed and, as necessary, updated on a yearly basis. Having a rela-tionship with a paperwork vendor capable of keeping you apprised of compliance is-sues as they develop will help streamline this process. You should also limit who within the dealership has authority to re-vise the paperwork and have procedures in place to ensure employees don’t use paper-work brought from outside sources, such as the last dealership where they worked. Regularly auditing actual deals can help to ensure paperwork is being properly com-pleted and computers are properly pro-grammed to print information in the ap-propriate places.

Advertising: Those who create your deal-ership’s advertisements should be familiar with the Federal Truth in Lending and Leasing acts and state advertising laws. Your ads should be reviewed for compli-ance with these laws. Regardless of wheth-er they appear in the newspaper, on TV, in a letter to a potential customer, or on the dealerships’ store window, your advertise-ments must contain mandated disclosures if you use any of the triggering terms de-fined in Regulations Z and M. They must also contain any material limitations or ex-clusions disclosed in a clear and conspicu-ous manner. Direct mailers and telephone solicitations or follow-up calls can raise a whole host of other issues. If mailers are sent to a list of prescreened customers or guarantee financing, for example, there

are numerous other laws to consider, in-cluding the Fair Credit Reporting Act, federal and state privacy laws, the Driver’s Privacy Protection Act and your state’s credit repairs and services act. On a final note, remember to keep copies of all ads in case you need to respond to a consumer or regulatory inquiry about an offer or the contents of a particular one.

Finance and Insurance: Dealers should start their list of compliance benchmarks in the F&I department with making sure they have a copy of a dealer agreement for each lender and service provider with whom the dealership does business. These agree-ments and any related materials should always be reviewed by someone who has knowledge about both the products be-ing offered and our industry. Reviewing dealer agreements and properly training employees on how to sell service contracts, GAP agreements, insurance products and any other aftermarket products sold at the dealership can go a long way in protecting your dealership from potential liability. All too often we find dealers rely on represen-tations made by the third party as to the compliance of its marketing materials, the products it offers and even the training it provides to the dealership’s employees. For those who use a F&I menu, remember to revise it whenever you begin or cease of-fering a product so it accurately reflects the products and services available at the dealership. If product disclosures, finance charges and payment terms in the retail in-stallment contracts and lease agreements are calculated by a computer program, you should also take time to verify that the required information and related calcula-tions are in compliance with applicable laws.

Employees: All potential employees should be required to complete an employ-ment application and, at a minimum, you should contact references to verify that the individual is qualified for the position. Depending upon the job responsibilities and access the applicant will have to confi-dential information about your dealership and customers, you may also wish to con-

duct background investigations or obtain a credit report. All employees should also receive an employee handbook that con-tains information about the dealership’s in-ternal policies and procedures. Remember to address issues such as who has access to pull and/or review credit reports, whether customer information belongs exclusively to the dealership and whether employees are permitted to remove such information from the dealership both during the term of employment and afterwards. If specific agreements are made with respect to com-mission payments and bonuses, you may also wish to enter into a separate written employment or compensation agreement. Employee handbooks should be updated regularly and employees should always be required to acknowledge in writing that they have received and read the materials. Just as important is requiring all employ-ees to attend training and/or educational seminars related to their duties at the deal-ership, not just at the time they are hired, but on an ongoing basis.

Privacy Policies and Customer Iden-tification Procedures: Every dealer should have a privacy policy that accurate-ly reflects the dealership’s business prac-tices with respect to collecting and sharing customer information and a comprehen-sive written information security program

F IN A NC I A L B E NC HM A RK S HE L P T HE B O T T OM L INE , C OMPL I A NC E B E NC HM A RK S P R O T EC T I T

OFTEN OVERLOOKED ARE BENCHMARKS

FOR LEGAL AND REGULATORY COMPLIANCE,

WHICH CAN HAVE A SIGNIFICANT IMPACT ON A DEALERSHIP’S

BOTTOM LINE.

APRIL 2011 D E A L E R S ’ R E S O U R C E

7

w w w . e - o i a d a . c o m

that describes how the dealership protects the confidentiality of the information col-lected. Access to customer information and other dealership records should be limited to authorized employees who need the information to complete their employ-ment responsibilities. Customer informa-tion must be obtained to verify the iden-tity of customers and the dealership has to have procedures to ensure it doesn’t enter into transactions with any individual or entity that appears on the list of Specially Designated Nationals and Blocked Per-sons maintained by the Office of Foreign Asset Control. Motor vehicle dealers are responsible not only for implementing their own privacy policies and procedures, but must also take steps to ensure that the lenders and service providers with whom they share information have taken steps to maintain the confidentiality of customer information.

Dealership Website and Computer Systems: The same policies and proce-dures that apply in your day-to-day trans-actions apply when conducting business online. Online advertisements must com-ply with federal and state advertising laws and should be updated and deleted on a regular basis. Dealers who permit con-sumers to submit credit applications elec-tronically must post their privacy policies online and, if they obtain credit reports online, they must be capable of retaining copies for a minimum of 25 months. Keep in mind also that many of the same pre-cautions taken with respect to your paper-work apply to your dealership’s computer system. Computer systems and programs should be reviewed and updated regularly. You should also limit who has the ability to update software applications, take steps to prevent and prepare for a systems fail-ure and ensure that data is eliminated or hard drives removed when disposing of computers and any other electronic media and records.

If you have already developed legal and regulatory compliance benchmarks and they meet or exceed those discussed here, then you are on the right track. As you read these words, however, and found yourself thinking we raised a lot of good ideas, then its time to take the next step and put a plan of action in place. Formalizing legal and regulatory compliance benchmarks that help ensure your dealership’s paperwork and day-to-day sales and business activi-ties are in compliance with the law will not only help minimize overall legal exposure, but will help your dealership sell more cars and keep them sold, increasing the dealer-ship’s overall profitability.

This article is for general information purposes only. You should contact legal counsel for specific application.

D E A L E R S ’ R E S O U R C E APRIL 2011

8

w w w . e - o i a d a . c o m

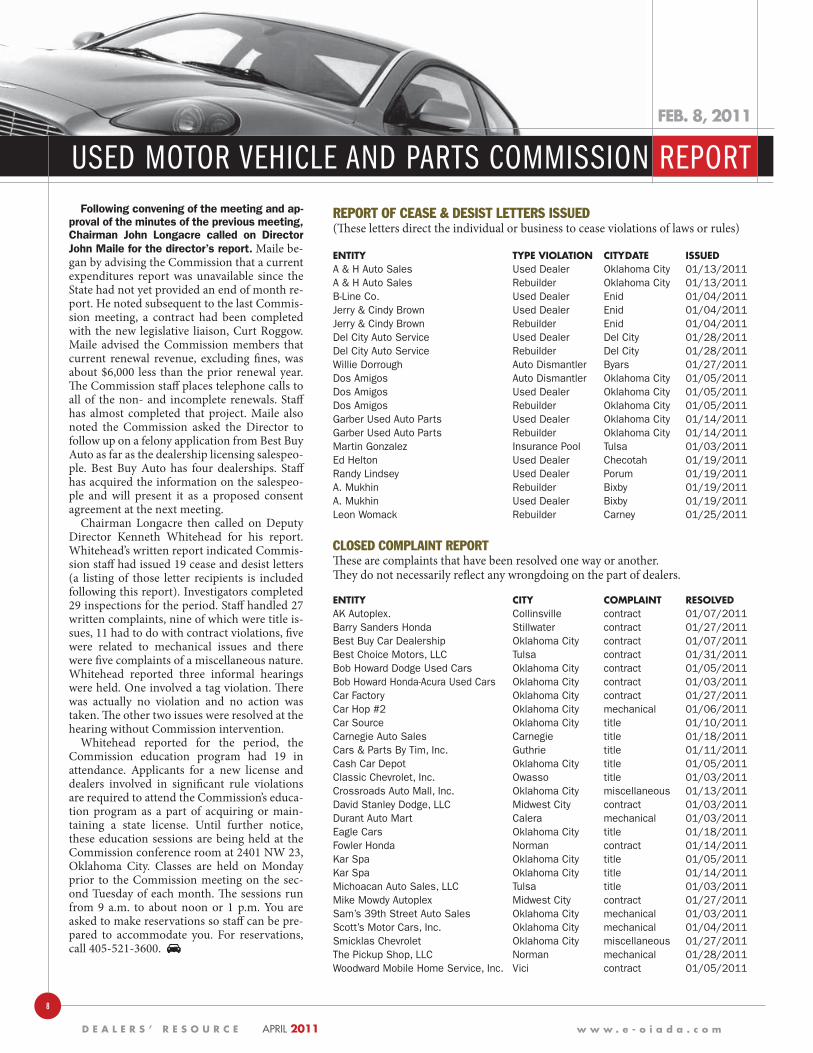

FEB. 8, 2011

REPORT OF CEASE & DESIST LETTERS ISSUED(These letters direct the individual or business to cease violations of laws or rules)

ENTITY TYPE VIOLATION CITY DATE ISSUEDA & H Auto Sales Used Dealer Oklahoma City 01/13/2011A & H Auto Sales Rebuilder Oklahoma City 01/13/2011B-Line Co. Used Dealer Enid 01/04/2011Jerry & Cindy Brown Used Dealer Enid 01/04/2011Jerry & Cindy Brown Rebuilder Enid 01/04/2011Del City Auto Service Used Dealer Del City 01/28/2011Del City Auto Service Rebuilder Del City 01/28/2011Willie Dorrough Auto Dismantler Byars 01/27/2011Dos Amigos Auto Dismantler Oklahoma City 01/05/2011Dos Amigos Used Dealer Oklahoma City 01/05/2011Dos Amigos Rebuilder Oklahoma City 01/05/2011Garber Used Auto Parts Used Dealer Oklahoma City 01/14/2011Garber Used Auto Parts Rebuilder Oklahoma City 01/14/2011Martin Gonzalez Insurance Pool Tulsa 01/03/2011Ed Helton Used Dealer Checotah 01/19/2011Randy Lindsey Used Dealer Porum 01/19/2011A. Mukhin Rebuilder Bixby 01/19/2011A. Mukhin Used Dealer Bixby 01/19/2011Leon Womack Rebuilder Carney 01/25/2011

CLOSED COMPLAINT REPORTThese are complaints that have been resolved one way or another.They do not necessarily reflect any wrongdoing on the part of dealers.

ENTITY CITY COMPLAINT RESOLVEDAK Autoplex. Collinsville contract 01/07/2011Barry Sanders Honda Stillwater contract 01/27/2011Best Buy Car Dealership Oklahoma City contract 01/07/2011Best Choice Motors, LLC Tulsa contract 01/31/2011Bob Howard Dodge Used Cars Oklahoma City contract 01/05/2011Bob Howard Honda-Acura Used Cars Oklahoma City contract 01/03/2011Car Factory Oklahoma City contract 01/27/2011Car Hop #2 Oklahoma City mechanical 01/06/2011Car Source Oklahoma City title 01/10/2011Carnegie Auto Sales Carnegie title 01/18/2011Cars & Parts By Tim, Inc. Guthrie title 01/11/2011Cash Car Depot Oklahoma City title 01/05/2011Classic Chevrolet, Inc. Owasso title 01/03/2011Crossroads Auto Mall, Inc. Oklahoma City miscellaneous 01/13/2011David Stanley Dodge, LLC Midwest City contract 01/03/2011Durant Auto Mart Calera mechanical 01/03/2011Eagle Cars Oklahoma City title 01/18/2011Fowler Honda Norman contract 01/14/2011Kar Spa Oklahoma City title 01/05/2011Kar Spa Oklahoma City title 01/14/2011Michoacan Auto Sales, LLC Tulsa title 01/03/2011Mike Mowdy Autoplex Midwest City contract 01/27/2011Sam’s 39th Street Auto Sales Oklahoma City mechanical 01/03/2011Scott’s Motor Cars, Inc. Oklahoma City mechanical 01/04/2011Smicklas Chevrolet Oklahoma City miscellaneous 01/27/2011The Pickup Shop, LLC Norman mechanical 01/28/2011Woodward Mobile Home Service, Inc. Vici contract 01/05/2011

Following convening of the meeting and ap-proval of the minutes of the previous meeting, Chairman John Longacre called on Director

John Maile for the director’s report. Maile be-gan by advising the Commission that a current expenditures report was unavailable since the State had not yet provided an end of month re-port. He noted subsequent to the last Commis-sion meeting, a contract had been completed with the new legislative liaison, Curt Roggow. Maile advised the Commission members that current renewal revenue, excluding fines, was about $6,000 less than the prior renewal year. The Commission staff places telephone calls to all of the non- and incomplete renewals. Staff has almost completed that project. Maile also noted the Commission asked the Director to follow up on a felony application from Best Buy Auto as far as the dealership licensing salespeo-ple. Best Buy Auto has four dealerships. Staff has acquired the information on the salespeo-ple and will present it as a proposed consent agreement at the next meeting.

Chairman Longacre then called on Deputy Director Kenneth Whitehead for his report. Whitehead’s written report indicated Commis-sion staff had issued 19 cease and desist letters (a listing of those letter recipients is included following this report). Investigators completed 29 inspections for the period. Staff handled 27 written complaints, nine of which were title is-sues, 11 had to do with contract violations, five were related to mechanical issues and there were five complaints of a miscellaneous nature. Whitehead reported three informal hearings were held. One involved a tag violation. There was actually no violation and no action was taken. The other two issues were resolved at the hearing without Commission intervention.

Whitehead reported for the period, the Commission education program had 19 in attendance. Applicants for a new license and dealers involved in significant rule violations are required to attend the Commission’s educa-tion program as a part of acquiring or main-taining a state license. Until further notice, these education sessions are being held at the Commission conference room at 2401 NW 23, Oklahoma City. Classes are held on Monday prior to the Commission meeting on the sec-ond Tuesday of each month. The sessions run from 9 a.m. to about noon or 1 p.m. You are asked to make reservations so staff can be pre-pared to accommodate you. For reservations, call 405-521-3600.

USED MOTOR VEHICLE AND PARTS COMMISSION REPORT

APRIL 2011 D E A L E R S ’ R E S O U R C E

9

w w w . e - o i a d a . c o m

L E G I S L AT I V E R E P O R T

BY OIADA/ADR STAFF

BYOIADA/ADRSTAFF

HB 1201 - InmanRequires any seller of a motor vehicle to disclose in writing to the buyer all warranty repairs, modifications or other warranty work performed on the motor vehicle.Bill History: 01-18-11 H Filed, sent to Economic Development Committee

HB 1260 - Rousselot - Shell BillEstablishes the Motor Vehicle Analysis Act.Bill History: 01-18-11 H Filed, sent to Rules Committee

HB 1295 - Derby Any driver that causes an accident that does not comply with the Compulsory Insurance Law will have their vehicle towed home and placed in a tire boot until the time that the accident is paid in full and the driver has insurance.Bill History: 01-19-11 H Filed, sent to Rules Committee

HB 1536 - Blackwell Removes the limit on discounts or credits for trade-in vehicles as prescribed by the Oklahoma Tax Commission; EMERGENCY.Bill History: 01-20-11 H Filed, sent to Appropriations Committee – Sub Committee on Revenue & Tax

HB 1743 - JohnsonEmpowers the Corporation Commission to supervise, govern and control wrecker fees, tariffs, and rates for transporting and storing vehicles removed in a non-consent tow; empowers the Commission to set the fees and charges; EMERGENCY.Bill History: 01-20-11 H Filed, sent to Public Safety Committee

HB 1761 - Nelson - Shell BillCreates the “Motor Vehicle Records Act of 2011.”Bill History: 01-20-11 H Filed, sent to Rules Committee

HB 2140 - SteeleCreates the State Government Administrative Process Consolidation and Reorganization – Agency Consolidation.Bill History: 02-15-11 Voted Committee Substitute Do Pass from Government Modernization CommitteeSB 197 - Aldridge Lowers fee for motor vehicle transfer from $10 to $5; Changes wording from “may” to “shall.” Makes mandatory the use of the “Notice of Transfer” on the bottom of Oklahoma Titles.Bill History: 01-11-11 S Filed, amended by Senate Committee on Appropriations – Title stricken Senate Finance Committee

SB 201 - AldridgeAllows local municipalities, counties, or the Department of Public Safety to place holds on the registration renewal for motor vehicles associated with violations; allows fees to be collected by motor license agents.Bill History: 01-11-11 S Filed, sent to Finance Committee

SB 215 - Adelson A new law creating the Oklahoma Motor Vehicle Inspection Act. Requires annual inspections of all motor vehicles; Prohibits the operation of unsafe motor vehicles; Confers authority upon the Commissioner of Public Safety to supervise. Sets inspection fee at $35.Bill History: 01-11-11 S Filed, sent to Public Safety Committee & also Appropriations Committee

SB 343 - Johnson, Rob Directs the Oklahoma Tax Commission to implement a pilot program for an electronic, print on-demand, temporary license plate issuance system for use by motor vehicle dealers. Pilot program for an electronic, print on-demand, temporary license plate issuance system for use by motor vehicle dealers. Bill History: 01-18-11 S Filed, referred to Finance Committee – Heard in Committee and Laid Over – Dead for now.

SB 448 - BarringtonAuthorizes the Department of Public Safety to take possession of any vehicle document or plate that is in violation of state law.Bill History: 01-18-11 S Filed, sent to Rules Committee

SB 503Department of Consumer Credit – setting fees – abolishing advisory committee.Bill History: 01-18-11 S Filed, sent to Business & Commerce Committee

SB 729 - MazzeiRemoves the listing of motor number, date first sold, distinguishing marks, and statement of source of title from the application for a motor vehicle title.Bill History: 01-18-11 S Filed, sent to Senate Finance -Title Stricken – Do Pass

D E A L E R S ’ R E S O U R C E APRIL 2011

10

w w w . e - o i a d a . c o m

Our team at Manheim Consulting had the pleasure of interviewing NIADA President Anthony Underwood for a question and answer session discussing the state of the used vehicle market from the perspective of independent dealers as we compiled the recently released, 16th annual Used Car Market Report (UCMR).

Underwood framed the challenges facing independent dealers in a way that confirmed what our data was telling us: independents are encountering higher prices for inventory at the wholesale level and finding fewer pre-owned vehicles in the marketplace.

In response, these dealers are focusing on sound inventory management practices, and using all available sales channels – including online – to source just the right inventory to meet their customers’ needs. We examined these and other trends in the UCMR, which is Manheim’s annual analysis of the forces shaping the used auto industry. As part of the Manheim-NIADA Dealer’s Edge partnership, I’m happy to let you know you can download the entire report free of charge by taking a very brief survey at www.surveymonkey.com/s/manheim.

As a comprehensive analysis of the trends shaping the automotive industry, the 2011 UCMR contains much more valuable information pertaining to independent dealers, as well as chapters on other aspects of the industry, including rental, leasing, fleets, repossessions and salvage. I encourage NIADA members to download their free copy of the UCMR, and as always, please e-mail me any time with your questions.

BY TOM WEBBTom Webb is chief economist for Manheim Consulting. Contact him at [email protected], follow him via Twitter at www.twitter.com/TomWebb_Manheim and read his blog at www.manheimconsulting.typepad.com.

Independents Remain Profitable in Challenging Environment

Portfolio General Management Group and The Warranty Group/First Extended have joined NIADA to jointly provide the best profit solutions to independent dealers who sell vehicle service contracts and other ownership protection products, such as GAP, anti-

theft and appearance protection. The unique benefit of the offering is NIADA dealers will profit from VSC sales and from premiums and investment income.

Portfolio and The Warranty Group are the nation’s leading providers of reinsurance management for F&I products sold in dealerships. The dealer’s profits from reinsurance are considerable. Since 1990, more than three million Portfolio contracts have been issued totaling more than $1.2 billion put into dealer-owned reinsurance companies. After claims are paid and investment income earned, Portfolio dealers average an after-tax return of more than 40 percent of the money put into their companies. Reinsurance is the NIADA dealer’s best way to profit twice from the same sale in the dealership.

“We see no reason why NIADA dealers should not have the same profit opportunities that franchised dealers have enjoyed for years,” said Steve Burke, Portfolio president. “Portfolio’s philosophy of 100-percent ownership by the dealer means that they can build a new personal wealth asset from activities already taking place in their dealerships. We joined NIADA to help its dealers take advantage of this opportunity.”

Patrick Donahue, president of Resource Dealer Group of The Warranty Group, said, “We are looking forward to working with Portfolio’s agents to help NIADA dealers choose the best option in a dealer-owned program. Our First Extended Service Corporation and Resource have worked hand-in-hand with Portfolio for over two decades as allies in the effort to give the dealer every available benefit from being in this business.”

Jeffrey Braatz, NIADA’s 2009 National Quality Dealer of the Year, welcomes Portfolio to NIADA and recommends them highly. “Five years ago, I didn’t think such a program could be true to its promise,” he said. “Now I not only have a personal asset to take care of my family’s future, but one that helps me take care of my customers.”

FOR MORE INFORMATION, VISIT WWW PORTFOLIOREINSURANCE.COM OR CALL STEVE BURKE AT 877-789-6200.

PORTFOLIO, THE WARR ANT Y GROUP/FIRST E X TENDED JOIN NIADA

®

D E A L E R S ’ R E S O U R C E APRIL 2011

12

w w w . e - o i a d a . c o m

As previously reported in this pub-

lication, the Dodd-Frank Wall Street

Reform and Consumer Protection Act,

or Dodd-Frank Act, was enacted in July

2010. Among other actions, Dodd-Frank established the new Bureau of Consumer Financial Protection (CFPB) within the Federal Reserve. While significant author-ity over certain financial institutions (in-cluding Buy Here-Pay Here dealers), has been granted the CFPB, the Federal Trade Commission continues as primary en-forcement authority for most regulations governing motor vehicle dealers. More importantly, Dodd-Frank granted new rulemaking authority to the FTC specifi-cally with respect to motor vehicle dealers.

In recent correspondence from the FTC to the Reserve dated Jan. 26, FTC Secre-tary Donald S. Clark expounded on the FTC’s future activities with regards to Dodd-Frank. In Secretary Clark’s words:

“The Dodd-Frank Act, enacted in July 2010, substantially restructured the fi-nancial services law enforcement and regulatory system. Under the Act, the Commission [FTC] retains it authority to enforce Regulations B, E, M, and Z (and was granted the authority to enforce any Bureau of Consumer Financial Protec-tion (“CFPB”) rules) regarding the enti-ties within the FTC’s jurisdiction; these include most providers of financial ser-vices that are not banks, thrifts, and fed-eral credit unions. The Dodd-Frank Act requires that the Commission and the CFPB coordinate certain law enforcement activities, and negotiate an agreement to do so by January 21, 2012. The Commis-sion is committed to continuing to vigor-ously enforce Regulations B, E, M, and Z. The FTC looks forward to coordinating with the Board, the CFPB, and other fed-eral agencies in the implementation of the Dodd-Frank Act.

“Finally, Section 1029 of the Dodd-Frank Act gives the Commission new and expanded authority regarding motor ve-hicle dealers. The FTC retains its current law enforcement authority over motor vehicle dealers, although it will share that authority with the CFPB with respect to

dealers engaged in certain practices. The Commission also obtains new authority as of July 21, 2011, to issue rules prohibit-ing unfair and deceptive acts and practices in connection with motor vehicle dealers, using the notice and comment rulemaking procedures in Section 553 of the Admin-istrative Procedure Act rather than the more elaborate rulemaking procedures in Section 18 of the FTC Act. In connection with this new authority, the FTC is con-ducting outreach activities and reviewing a wide range of motor vehicle dealer prac-tices. Section 1029 of the Dodd-Frank Act also requires the FTC and Board to coor-dinate with the CFPB’s Office of Service Member Affairs to address certain motor vehicle issues related to members of the military. The Commission looks forward to working with the Board, the CFPB, and other federal agencies on this initiative.”

As mentioned by Secretary Clark, the FTC retains authority to enforce regula-tions B (“Equal Credit Opportunity”), E (“Electronic Fund Transfer”), M (“Con-sumer Leasing”), and Z (“Truth In Lend-ing”). In addition, the commission will have authority to enforce any CFPB rules. This enforcement authority is not insignif-icant. Penalties and sanctions imposed on companies through agreements settling non-compliance allegations can be severe and long-lasting.

For example, last September, the com-mission announced a settlement to halt discriminatory practices by a mortgage company allegedly charging Hispanic consumers higher prices for mortgage loans than similarly situated non-Hispan-ic white consumers. The FTC’s complaint had alleged the defendants violated the Equal Credit Opportunity Act (ECOA) and its implementing Regulation B, as well as the FTC Act, by charging different prices to Hispanic consumers that could not be explained by their credit character-istics or underwriting risk.

The settlement permanently prohibits defendants from discriminating on the basis of national origin in credit transac-tions, or otherwise failing to comply with ECOA and Regulation B. The order fur-

ther requires defendants to implement various fair lending policies, training pro-grams, and to satisfy certain compliance reporting guidelines. Additionally, the order imposes a $5.5 million judgment, all but $1.5 million of which is suspended based on defendants’ financial situation.

In February, the commission issued a news release regarding cases resulting from their ongoing campaign to protect consumers’ personal information. Three companies whose business is reselling consumers’ credit reports agreed to settle FTC charges that they did not take rea-sonable steps to protect consumers’ per-sonal information, failures that allowed computer hackers to access that data.

Under the Fair Credit Reporting Act, the resellers were charged with failing to protect their internet portals. In addition, the resellers were charged with violating the Gramm-Leach-Bliley Safeguards Rule by failing to design and implement infor-mation safeguards to control the risks to consumer information; to regularly test or monitor the effectiveness of their controls and procedures; to evaluate and adjust their information security programs in light of known or identified risks; and to have comprehensive information security programs.

The settlements require the companies to strengthen their data security proce-dures, meet prescribed record-keeping provisions to allow the FTC to monitor compliance, and submit to independent security program audits for 20 years.

Our industry is highly regulated, both at the state and federal levels. And if FTC Secretary Clark’s comments are any indi-cation, oversight will become more, not less, intrusive. Compliance will become both more difficult and more critical.

At OIADA, we believe it is our respon-sibility as the used dealer association for Oklahoma to not only keep our dealers informed of relevant regulatory issues, but to also assist you in your compliance efforts. For more information regarding compliance issues and solutions, contact us at 405-232-2947 or [email protected].

���Our industry is highly regulated, both at the state and federal levels. And if FTC Secretary Clark’s comments are any indication, oversight will become more, not less, intrusive. Compliance will become both more difficult and more critical.

12

Word from the FTC

BY A

DR

STA

FF

D E A L E R S ’ R E S O U R C E APRIL 2011

14

w w w . e - o i a d a . c o m

The proper classification of independent

contractors versus employees continues

to be an issue with enforcement agencies

at both the state and federal levels.

It is critical you, the business owner, cor-rectly determine whether the individuals providing services are employees or indepen-dent contractors. Generally, you must with-hold income taxes, withhold and pay Social Security and Medicare taxes and pay unem-ployment tax on wages paid to an employee. You don’t generally have to withhold or pay any taxes on payments to independent con-tractors.

If you are a business owner hiring or con-tracting with other individuals to provide services, you must determine whether the individuals – including salespersons - pro-viding services are employees or independent contractors.

Before you can determine how to treat pay-ments you make for services, you must first know the business relationship that exists between you and the person performing the services. The person performing the services may be:

An independent contractorAn employee (common-law employee)A statutory employeeA statutory non-employeeIn determining whether the person provid-

ing service is an employee or an independent contractor, all information that provides evi-dence of the degree of control and indepen-dence must be considered. You should know the following about hiring people as indepen-dent contractors versus hiring them as em-ployees.

The IRS uses three characteristics to deter-mine the relationship between businesses and workers:

means.

-

If you have the right to control or direct not only what is to be done, but also how it is to be done, then your workers are most likely em-ployees.

If you can direct or control only the result of the work done and not the means and methods

of accomplishing the result, then your workers are probably independent contractors.

Employers who misclassify workers as independent contractors can end up with substantial tax bills. Additionally, they can face penalties for failing to pay employment taxes and for failing to file required tax forms. Workers can avoid higher tax bills and lost benefits if they know their proper status.

Both employers and workers can ask the IRS to make a determination on whether a specific individual is an independent con-tractor or an employee by filing a Form SS-8, Determination of Worker Status for Purposes of Federal Employment Taxes and Income Tax Withholding, with the IRS.

You can learn more about the critical de-termination of a worker’s status as an inde-pendent contractor or employee at IRS.gov by selecting the Small Business link. Ad-ditional resources include IRS Publication 15-A, Employer’s Supplemental Tax Guide, Publication 1779, Independent Contractor or Employee, and Publication 1976, Do You Qualify for Relief under Section 530? These publications and Form SS-8 are available on the IRS website or by calling the IRS at 800-829-3676 (800-TAX-FORM).

Businesses must weigh all these factors when determining whether a worker is an employee or independent contractor. Some factors may indicate the worker is an em-ployee while other factors indicate that the worker is an independent contractor. There is no magic or set number of factors that makes the worker an employee or an independent contractor, and no one factor stands alone in making this determination. Also, factors which are relevant in one situation may not be relevant in another.

The keys are to look at the entire relation-ship, consider the degree or extent of the right to direct and control, and finally, to document each of the factors used in coming up with the determination.

��Common Law RulesUnder common law rules, anyone who per-

forms services for you is your employee if you can control what will be done and how it will be done. This is so even when you give the employee freedom of action. What matters is you have the right to control the details of how the services are performed. People such as doctors, dentists, veterinarians, lawyers, accountants or auctioneers who are in an independent trade, business or profession in which they offer their services to the general public are generally independent contractors.

However, whether these people are indepen-dent contractors or employees depends on the facts in each case. The general rule is an individual is an independent contractor if the payer has the right to control or direct only the result of the work and not what will be done and how it will be done.

��Form SS-8If, after reviewing the three categories of

evidence, it is still unclear whether a worker is an employee or an independent contractor, Form SS-8, Determination of Worker Status for Purposes of Federal Employment Taxes and Income Tax Withholding (PDF), can be filed with the IRS. The form may be filed by either the business or the worker. The IRS will review the facts and circumstances and offi-cially determine the worker’s status.

Be aware it can take at least six months to get a determination, but a business that con-tinually hires the same types of workers to perform particular services may want to con-sider filing the Form SS-8 (PDF).

���Consequences of Treating an Employee as an Independent Cotractor

If you classify an employee as an indepen-dent contractor and you have no reasonable basis for doing so, you may be held liable for employment taxes for that worker (the relief provisions, discussed below, will not apply). See Internal Revenue Code section 3509 for more information.

��Relief ProvisionsIf you have a reasonable basis for not treat-

ing a worker as an employee, you may be re-lieved from having to pay employment taxes for that worker. To get this relief, you must file all required federal information returns on a basis consistent with your treatment of the worker. You (or your predecessor) must not have treated any worker holding a substan-tially similar position as an employee for any periods beginning after 1977. See Publication 1976, Section 530 Employment Tax Relief Re-quirements (PDF) for more information.

��Misclassified Workers Can File Social Security Tax Form

Workers who believe they’ve been improp-erly classified as independent contractors by an employer can use Form 8919, Uncollected Social Security and Medicare Tax on Wages, to figure and report the employee’s share of uncollected Social Security and Medicare taxes due on their compensation.

Independent Contractor � (S E L F - E M P L O Y E D) O R E M P L O Y E E ?

BY A

DR

STA

FF

D E A L E R S ’ R E S O U R C E APRIL 2011

16

w w w . e - o i a d a . c o m

During 2010, new laws, such as the Af-

fordable Care Act and the Small Business

Jobs Act of 2010, created or expanded de-

ductions and credits small businesses and

self-employed individuals should consider

when completing their tax returns and mak-

ing business decisions in 2011.

Health Insurance Deduction Reduces Self Employment Tax

With the enactment of the Small Business Jobs Act of 2010, self-employed taxpayers who pay their own health insurance costs can now reduce their net earnings from self-employment by these costs. Previously, the self-employed health insurance deduction was allowed only for income tax purposes. For tax year 2010, self-employed taxpayers can also reduce their net earnings from self employment subject to SE taxes on Schedule SE by the amount of self-employed health insurance deduction claimed on line 29 on Form 1040.

Taxpayers can claim the self-employed health insurance deduction if the insurance plan is established under their business and if any of the following are true:

profit for the year,

to figure net earnings from self-employ-ment on Schedule SE, or

-tion in which the taxpayer was a more-than-2-percent shareholder.

Small Business Health Care Tax CreditIn general, the Small Business Health Care

Tax Credit is available to small employers that pay at least half of the premiums for single health insurance coverage for their employ-ees. It is specifically targeted to help small businesses and tax-exempt organizations that primarily employ moderate- and lower-income workers.

Small businesses can claim the credit for 2010 through 2013 and for any two years af-ter that. For tax years 2010 to 2013, the maxi-mum credit is 35 percent of premiums paid by eligible small businesses and 25 percent of premiums paid by eligible tax-exempt orga-nizations. Beginning in 2014, the maximum tax credit will increase to 50 percent of pre-miums paid by eligible small business em-ployers and 35 percent of premiums paid by eligible tax-exempt organizations.

The maximum credit goes to smaller em-ployers –– those with 10 or fewer full-time equivalent (FTE) employees –– paying an-nual average wages of $25,000 or less. The credit is completely phased out for employers that have 25 or more FTEs or that pay average wages of $50,000 or more per year. Because the eligibility rules are based in part on the number of FTEs, not the number of employ-ees, employers that use part-time workers may qualify even if they employ more than 25 individuals.

Eligible small businesses will first use Form 8941 to figure the credit and then include the amount of the credit as part of the general business credit on its income tax return.

General Business Credit for EmployersThe general business credits of eligible

small businesses in 2010 are not subject to alternative minimum tax. The new law allows general business credits to offset both regular income tax and alternative minimum tax of eligible small businesses as described in Sec-tion 2012 of the Small Business Jobs Act. The provision is effective for any general business credits determined in the first taxable year beginning after Dec. 31, 2009, and to any car-ryback of such credits. For a list of the general business credits, see Form 3800.

Small Businesses Can Benefit from Higher Expensing / Depreciation Limits

For tax years beginning in 2010 and 2011, small businesses can expense up to $500,000 of the first $2 million of certain business property placed in service during the year.

In general, businesses can choose to treat the cost of certain property as an expense and deduct it in the year the property is placed in service instead of depreciating it over several years. This property is frequently referred to as section 179 property, after the relevant sec-tion in the Internal Revenue Code.

Section 179 property is property that you acquire by purchase for use in the active con-duct of your trade or business, including:

-ings and their structural components) used as:

-duction, or extraction or of furnishing transportation, communications, electric-ity, gas, water, or sewage disposal services;

with any of the activities in (1) above; or

of the activities in (1) above for the bulk storage of fungible commodities.

horticultural structures.

their structural components) used in connection with distributing petroleum or any primary product of petroleum.

Section 179 property generally does not in-clude land, investment property (section 212 property), property used mainly outside the United States, property used mainly to furnish lodging and air conditioning or heating units.

The Small Business Jobs Act (SBJA) of 2010 increases the section 179 limitations on expensing of depreciable business assets for tax years beginning in 2010 and 2011 and expands temporarily the definition of section 179 property, for tax years beginning in 2010 and 2011, to include certain qualified real property a taxpayer elects to treat as section 179 property. Qualified real property means qualified leasehold improvement property, qualified restaurant property, and qualified retail improvement property.

The $500,000 amount provided under the new law is reduced, but not below zero, if the cost of all section 179 property placed in ser-vice by the taxpayer during the tax year ex-ceeds $2 million.

For tax years beginning in 2012, the maxi-mum amount is $125,000; before enactment of the 2010 tax relief legislation, it was set at $25,000.

Depreciation limits on business vehiclesThe total depreciation deduction (includ-

ing the section 179 expense deduction and the 50 or 100 percent bonus depreciation) you can take for a passenger automobile (that is not a truck or a van) you use in your business and first placed in service in 2010 is increased to $11,060. The maximum deduc-tion you can take for a truck or van you use in your business and first placed in service in 2010 is increased to $11,160. If you do not take any bonus depreciation for the passen-ger automobile, truck, or van you use in your business and first placed in service in 2010, the maximum deduction you can take for a passenger automobile is $3,060 and for a truck or van is $3,160.

CONTINUED ON PAGE 18

TA X CHANGES FOR SMALL BUSINESSES

D E A L E R S ’ R E S O U R C E APRIL 2011

18

w w w . e - o i a d a . c o m

50 or 100 Percent Bonus DepreciationGenerally, businesses can take a spe-

cial depreciation allowance to recover part of the cost of qualified property placed in service during the tax year. The allowance applies only for the first year you place the property in service.

Businesses that acquire and place quali-fied property into service after Sept. 8, 2010, can now claim a depreciation allowance of 100 percent of the cost of the property. The property must be placed in service be-fore Jan. 1, 2012 (Jan. 14, 2013 in the case of certain longer-lived and transportation property). Businesses that acquire qualified property during 2010 on or before Sept. 8, 2010, can claim a depreciation allowance of 50 percent of the cost of the property. The property must be placed in service before Jan. 1, 2013 (Jan. 1, 2014 in the case of cer-tain longer production period property and for certain aircraft.)

The allowance is an additional deduction

you can take after any section 179 deduc-tion and before you figure regular deprecia-tion under MACRS for the year you place the property in service. The types of prop-erty that can be depreciated are described in the instructions to Form 4562.

Small Businesses To Use EFTPS for Deposits Beginning in 2011

The paper coupon system for federal tax deposits will no longer be maintained by the Treasury Department after Dec. 31, 2010. Most businesses must now make deposits and pay federal taxes through the Electronic Federal Tax Payment System (EFTPS). Us-ing EFTPS to make federal tax deposits pro-vides substantial benefits to both taxpayers and the government. EFTPS users can make tax payments 24 hours a day, seven days a week from home or the office.

Deposits can be made online with a com-puter or by telephone. EFTPS also signifi-cantly reduces payment-related errors that

could result in a penalty. The system helps taxpayers schedule dates to make payments even when they are out of town or on vaca-tion when a payment is due. EFTPS business users can schedule payments up to 120 days in advance of the desired payment date.

Information on EFTPS, including how to enroll, can be found online at www.irs.gov or by calling EFTPS Customer Service at 1-800-555-4477.

Some businesses paying a minimal amount of tax may make their payments with the related tax return, instead of us-ing EFTPS. More details regarding taxes re-quired to be deposited using EFTPS, dollar thresholds and other specific requirements are described on page 2 of IRS Publication 15, (Circular E) Employer’s Tax Guide.

F O R M O R E I N F O R M A T I O N , V I S I T W W W . I R S . G O V .

CONTINUED FROM PAGE 16 TA X CHANGES FOR SMALL BUSINESSES

APRIL 2011 D E A L E R S ’ R E S O U R C E

19

w w w . e - o i a d a . c o m

What’s on the credit and debit card receipts you give your customers? The Federal Trade Commission, the nation’s consumer protection agency, reminds companies they are required to check their receipts and make sure they’re complying with a law that’s been in effect for all businesses since Dec. 1, 2006.

According to the federal Fair and Accurate Credit Transaction Act (FACTA), the electronically printed credit and debit card receipts you give your customers must shorten — or truncate — the account information. You may include no more than the last five digits of the card number, and you must delete the card’s expiration date. For example, a receipt that truncates the credit card number and deletes the expiration date could look like this:

ACCT: ***********12345 EXP: ****

Why is it important for businesses to make sure they’re complying with this law? Credit card numbers on sales receipts are a golden ticket for fraudsters and identity thieves. Savvy businesses appreciate the importance of protecting their customers — and themselves — from credit card crime.

But there are other important reasons to make sure your slips are shipshape. Noncompliance could open a company up to an FTC law enforcement action, including civil penalties and injunctive relief. In addition, the law allows consumers to sue businesses that don’t comply and to collect damages and attorney’s fees.

While Congress passed this provision in December 2003, it was phased in gradually, requiring merchants with newer electronic card processing machines to comply by December 2004. Merchants with older machines were given until Dec. 1, 2006. So now all companies that electronically print credit or debit card receipts must truncate the information on the copy they give their customers. That’s why it’s important to make sure all your equipment complies with the law.

Several details of the law are worth noting: it applies only to electronically printed receipts, not to handwritten or imprinted ones. Plus, it applies only to receipts you give your customer at point of sale, not to any transaction record you retain. Be aware, however, when you keep your customers’ personal information — including account data — you have an obligation to keep it safe. Read Protecting Personal Information: A Guide for Business, available at ftc.gov/infosecurity, for tips on safeguarding sensitive data.

The FTC works for the consumer to prevent fraudulent, deceptive, and unfair practices in the marketplace and to provide information to businesses to help them comply with the law. To file a complaint or to get free information on consumer issues, visit ftc.gov or call 877-FTC-HELP (877-382-4357); TTY: 1-866-653-4261. The FTC enters Internet, telemarketing, identity theft and other fraud-related complaints into Consumer Sentinel, a secure, online database available to hundreds of civil and criminal law enforcement agencies in the U.S. and abroad.

CREDIT CARD NUMBERS ON SALES RECEIPTS ARE A GOLDEN TICKET FOR FRAUDSTERS AND IDENTITY THIEVES.

��

Federal Law, Credit Card Receipts and Your Dealership

D E A L E R S ’ R E S O U R C E APRIL 2011

20

w w w . e - o i a d a . c o m

Anyone can start selling cars using the

Internet, but those who are most successful

give buyers the right information during the

shopping process. Sellers can break through the clutter of online used car sales by giving consumers photos, compelling descriptions and vehicle history while they shop.

If you’re not already online, you need to be. Eighty percent of consumers today use the Internet to help find their next car. Furthermore, shoppers visit less than two dealerships before deciding to buy – conducting research online before visiting any lot.

Typically, they start by visiting third-party automalls like AutoTrader.com and Cars.com. A quick search can return hundreds of listings for vehicles similar in style and price. Since you can’t sell online shoppers face-to-face, your listings have to do the talking.

Focus your marketing efforts on two lead-generating areas that attract the most attention: Search Results Pages (SRPs) and Vehicle Details Pages (VDPs).

The SRPs and VDPs are the most

prominent places to communicate the value of your used car inventory online. When shoppers click on SRPs, they go to VDPs to browse additional photos, read about features, see the vehicle history and locate the seller. Getting shoppers to click on SRP listings generates more leads from your VDPs.

The vehicle description you provide on SRPs is your first opportunity to reach shoppers. Try to describe the car’s benefits as if shoppers were standing in front of you. Be brief but informative. For example, you might say, “this van comfortably fits up to eight people” or, “we offer low financing” or, “includes Free Carfax Vehicle History Report.” You don’t want potential customers glancing past your listings because they didn’t peak their interest.

Photos are another way seasoned online sellers grab the attention of used car shoppers on SRPs. Use the best image as the SRP ‘thumbnail’ image on SRPs and save detailed images for the VDP.

You can build confidence with online

consumers by linking Carfax Reports to SRP and VDP listings. Shoppers are more likely to buy from open and up-front sellers and your listings will stand out even more.

To connect with online shoppers, you need to think like them. By giving buyers relevant information to help them make an educated decision, you can compete online and sell cars faster.

Top dealers consistently get more leads because they pay attention to how their car listings appeal to online consumers. Make your SRPs stand out in the crowded online marketplace and more shoppers will click through to your VDPs. More clicks equals more leads and ultimately, more sales.

BY DALE POLLAK AND LANCE VICKERY Dale Pollak, founder of vAuto, is a highly sought-after authority on maximizing profits from used vehicle operations, working extensively with Dealer 20 Groups, Dealer Associations and large dealer enterprises across the country. In addition to his regular contributions to auto industry publications like Dealer Magazine, Pollak is a published author of 2 books, Velocity: From the Front Line to the Bottom Line and Velocity 2.0: Paint, Pixels and Profitability.Lance Vickery is director of dealer business at Carfax and has spent more than 25 years in the auto industry.

ONLINE SALES SUCCES S: L E T Y O U R L I S T I N G S D O T H E T A L K I N G

SALE

S

APRIL 2011 D E A L E R S ’ R E S O U R C E

21

w w w . e - o i a d a . c o m

The following list includes members who joined or renewed their OIADA/NIADA mem-

bership during January 2011. We express our sincere appreciation for all the members

of OIADA and we extend our invitation to dealers who are not members. A membership

application can be found elsewhere in this newsletter. We urge you to be an active part

of maintaining a strong and effective used car industry voice in the legislative and reg-

ulatory environment. With the current Congress, we need that voice more than ever!

Chris Goad, President

COMPANY NAME JOINED CITY

N Diffee Motor Cars South, Inc. Gary Pitcock 2011 Oklahoma CityR JS Wholesale Autos Jeff Skaggs 1997 Sand SpringsR Thoroughbred Motors, Inc. Daniel R. Derr 1993 Oklahoma CityR Reynolds Ford, Inc. Richard L. Reynolds 2010 NormanR Newell Coach Corp. Karl Blade 1993 MiamiR Bob Moore Mazda Bob Moore Mazda 2004 Oklahoma CityR Brown Ford, Inc. Eddie Brown, Jr. 2010 CordellR Reliable Motors, Inc. Julian K. Codding 2005 Oklahoma CityR Car Mart #1 Bryan Adams 1996 TulsaR Mike Mowdy Autoplex Mike Mowdy 2008 Midwest CityR Smalygo Auto Wholesale, Inc. Kelly Smalygo 2007 ClaremoreR Alpha Auto Finders Jeffery E. Jones 1999 StillwaterR Carter’s Car Country Lee Ann Carter 1994 ComancheR Greenwood Motors Rick Gore 2010 Oklahoma CityR Madill Superlot C. T. Hutchens 2005 MadillR I-35 Auto Mall, LLC I-35 Auto Mall, LLC 2007 Oklahoma CityR Choctaw Autoplex, LLC Mike West 2004 ChoctawR Speedline Used Cars, LLC Johnny Nix 2004 McAlesterR GWC Warranty Corp. The Guardian Warranty Corp. 2002 Avoca, PA

O I A D A N E W A N D R E N E WA L

M E M B E R S

D E A L E R S ’ R E S O U R C E APRIL 2011

22

w w w . e - o i a d a . c o m

FEDERAL ADVOCATESLOBBYING REPORT

F E B R U A R Y 2 0 1 1

��12th Congress IssuesOn Feb. 3, Federal Advocates met with

NADA to discuss upcoming issues for the 112th Congress and various pending matters. As we jointly see it, the issues for Congress are fuel economy and green gas within the context of energy legislation, the Consumer Financial Protection Bureau and its mandates, the Toyota Safety Bill (which we both believe is dead), possible Congressional oversight that may impact the industry and the National Highway Traffic Safety Administration reauthorization effort (a priority of Sen. Jay Rockefeller, D-WV, who’s chairman of the Senate Commerce Committee).

Harrington also mentioned a General Accounting Office study (see separate heading) which Rep. Ed Towns, D-NY, and chairman of the 111th Congress House Governmental Affairs Committee, requested on section 310 of the Senate Toyota bill. It would’ve required dealers to provide info to buyers on a vehicle’s history.

Lastly, we both agreed it’s important to continue monitoring relevant activity of the FTC.

���Consumer Financial Protection Bureau Meetings

On March 4, NIADA General Counsel Keith Whann and Federal Advocates will be meeting with Holly Petraeus, director of the Consumer Financial Protection Bureau’s Office of Service Member Affairs, to introduce NIADA and to discuss various auto industry issues related to the newly-created CFPB. In addition, a meeting request is pending with Richard Cordray, CFPB general counsel, to discuss various consumer auto issues and the soon-to-be appointed Consumer Advisory Board.

��SBA Floorplan Financing ProgramThe federal government relaunched its

suspended floorplan financing program for small dealerships, this time with loan limits of $5 million rather than $2 million. The Small Business Administration’s new rules, which addressed nuts-and-bolts questions of how the financing will work, were published online in the Federal Register on Feb. 8. The Obama administration began a pilot floorplan program in May 2009 during the depths of the recession, but it never got off the ground because of banks’ reluctance to extend credit. A law enacted in September 2010 increased the loan limits and in October, the SBA adopted a rule expanding eligibility for the program to the majority of dealerships. The SBA also suspended the program in October and has been working since with lenders in an attempt to increase their participation. The pilot program will continue through September 2013. To address various issues related to the program, a conference call was held with Whann, and the SBA’s Steven Smits, associate administrator, and Patrick Kelley, senior advisor, Office of Capital Access.

��Department of DefensePam McClelland, a DOD senior

program analyst, has taken over for Dave Julian and Frank Emery in the Office of Military Community and Family Planning in the Office of the Deputy Undersecretary of Defense. Per a conversation with her on Feb. 15, NIADA will send information to her, at her request, on how the association can assist service members in purchasing pre-owned vehicles. Pending her review, a meeting or conference call will be scheduled with Whann.

��GAO StudyThe GAO review was requested by Rep.

Towns earlier last year that focused on the auto safety recall process. As part of the review, GAO is speaking with all of the stakeholders in the process such as dealerships and dealership representatives. GAO’s audit work is nearing its completion and GAO is due to issue the report on June 15. Pending that, Jim Leonard, an analyst with the GAO’s Physical Infrastructure Team, has discussed with NIADA its views on the issue and the role of pre-owned vehicle dealerships. NIADA’s Mike Linn and Whann discussed this issue with Jim Leonard and other analysts of the GAO earlier this month.

��White House Meeting ScheduledA March 4 meeting with Steve Croley,

special assistant to the President for Justice and Regulatory Policy in the Office of Domestic Policy, has been scheduled to introduce the association to the administration and to provide a briefing on its views on auto consumer issues.

FEDERAL ADVOCATES is NIADA’s governmental advocacy partner. To read past lobbying reports, visit www.niada.com/legislative_and_legal.php

As part of the review, GAO is speaking with all of the stakeholders in the process such as dealerships and dealership representatives.

APRIL 2011 D E A L E R S ’ R E S O U R C E

23

w w w . e - o i a d a . c o m

LICENSE APPLICANTS APPROVED

The applicants, as listed in the Agenda for the Used Motor Vehicle and Parts

Commission Regular Meeting of Feb. 8 were considered for issuance of used

motor vehicle dealer licenses and wholesale vehicle dealer licenses. The

applications were approved pending compliance with the state licensing laws

and rules, and subject to final approval by commission staff.

COMPANY NAME CITY

#1 Auto Bob Dabirian Oklahoma CityA & H Auto Sales Majid Asadi Oklahoma CityAltus Motorsports Janette Nassaney Altus George NassaneyAmer Camaro & Firebird Auto Br Gary Berlin Warr AcresBakerboys Yamaha Laura Baker Oklahoma City Chandler C. BakerBargain Motors Ronald Renzelman WilsonC & C Truck Sales & Leasing Dennis B. Watson El RenoCarney Classics John C. Butler CarneyCars 4 Less Naveed Ferdowsian Oklahoma CityCash4carsokc.com Douglas Ray Oklahoma CityChampion Auto Sales, LLC Homayoon Ahmadirahdari Oklahoma CityCollins Used Cars Sherman Collins StilwellConner Used Cars Stephen Conner LawtonCummins Ford Lincoln, Inc. Loyd B. Cummins Weatherford Chad Cummins Wade DorseyDavid Stanley Hyundai, LLC David Stanley Oklahoma CityDiesels N Stuff Peter Parker Tulsa Theodore Brett SwabDyer Auto Sales Troy Dyer HeavenerFirst Auto Finance Carl White TulsaGuymon Auto Sales Curtis Ryan Purdy Guymon Chad CritserI-35 Auto Mall, LLC Steven M. Meston Oklahoma City Lawrence Matthes Dillard IR LM Dillard Holding Trust V Dillard 1991 GST Exemp Trust John Roderick BatesI-35 Sports & Imports David Akbaran Moore Michael AkbaranIntegrity Auto Finance Dillard 1991 GST Exemp Trust Oklahoma City John Roderick Bates LM Dillard Holding Trust V Steven M. Meston Lawrence Matthes Dillard IRIntegrity Motors Scott Foust YukonJamatt RV Sales Jason Blake Poteau Sandra Blake

COMPANY NAME CITY

Payless Auto Sales Mohommad Rez Moumenzadeh EdmondSRB Wholesale Road Sharon Brittain Edmond Ronald Brittain

COMPANY NAME CITY

Jim Wheeler’s Auto Sales Jim Wheeler TulsaJS & P Auto Leasing & Sales, Inc. Collin Sharp Glenpool Bryan BermanK. C. Auto Kelly C. Clifton Tulsa Linda Clifton Kam Motor Sales, LLC Amanda Luong TulsaL.A. Auto Sales, Inc. Sue Holliday Chickasha Larry A. HollidayLawton Motorsports Janette D. Nassaney Lawton George H. NassaneyLowest Price Auto Parts & Sales, Inc. Mohammad Momennia Oklahoma CityMalibu’s Auto Sales, LLC Clint Edward Wilson Moore Greg RushingMcNair’s Auto Sales Phillip J. McNair MarlowMimi Auto Pradeep K. Metpally Oklahoma CityNoble Truck Sales Russell D. Anglin NobleOK Trans Auto Sales Felicia Mack Oklahoma City Brian MackPerformance Cycle Gerald Tims BethanyR & E Exotic Autos, LLC Eric Gove Newkirk Ronald Redenins R & T Salvage & Used Cars, LLC Aurelio E. Hernandez Trejo Del CityRatcliffe Auto Group, LLC Kimberly Ratcliffe Madill Jonathan RatcliffeRoyal Rides, LLC Tony Anderson MarlowSelect Auto Sales Jeffrey Dykes Jenks Danny SwitzerStillwater Auto Center Armondo Oliphant Stillwater James Bradley NashSudden Death Motors Wendy Barns Enid Jeremy MunsellThe Right Choice Motors, LLC Kenneth L. Cabelka Lawton Majella Sue CabelkeTJ Motors Mohammadreza Tajbakhsh Oklahoma CityUnited Trucks & Autos John Christopher Pritchard MuskogeeVIP Auto, Inc. Aaron Daniel Johnson CarnegieWest Pointe Chrysler, Jeep, Dodge Performance Dodge, Inc. Oklahoma City Smicklas Brothers, LLCWilliamson Truck Auto Sales Karen J. Williamson Prague Kim L. Wilson

USED DEALER LICENSES

WHOLESALE USED DEALER LICENSES

OIADASELECT

PROVIDERS

D E A L E R S ’ R E S O U R C E APRIL 2011

26

w w w . e - o i a d a . c o m

APRIL 2011 D E A L E R S ’ R E S O U R C E

27

w w w . e - o i a d a . c o m

D E A L E R S ’ R E S O U R C E APRIL 2011

28

w w w . e - o i a d a . c o m

APRIL 2011 D E A L E R S ’ R E S O U R C E

29

w w w . e - o i a d a . c o m

D E A L E R S ’ R E S O U R C E APRIL 2011

30

w w w . e - o i a d a . c o m

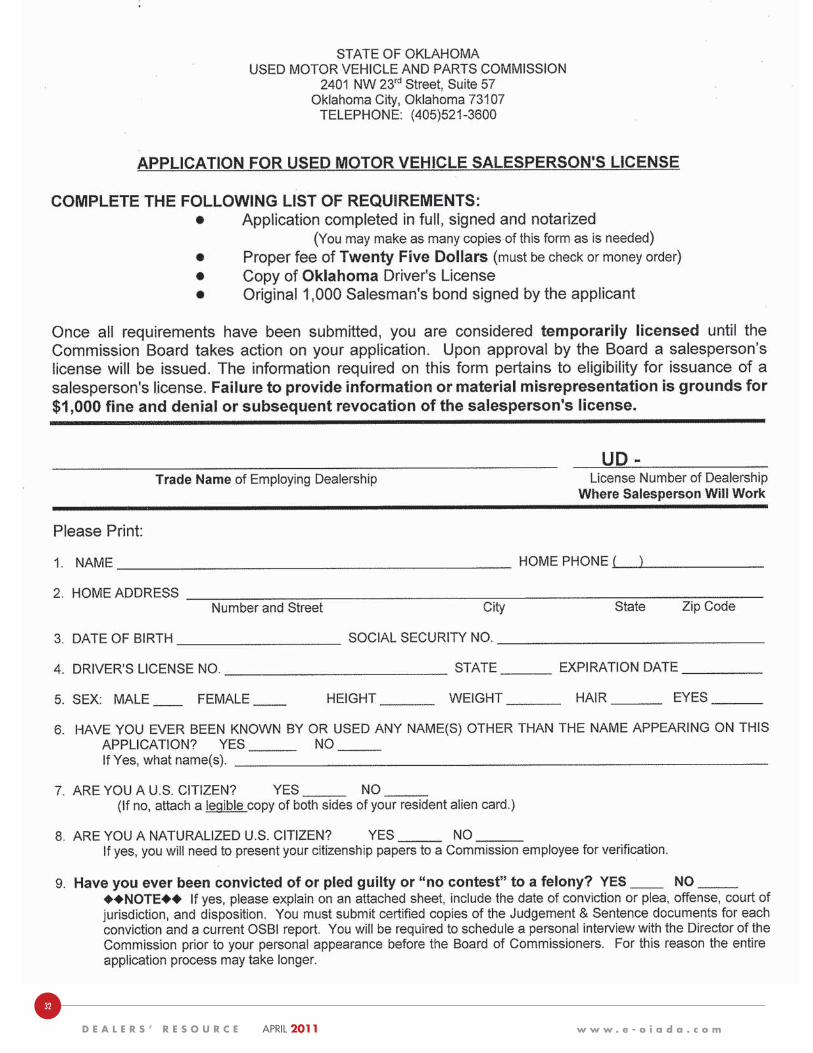

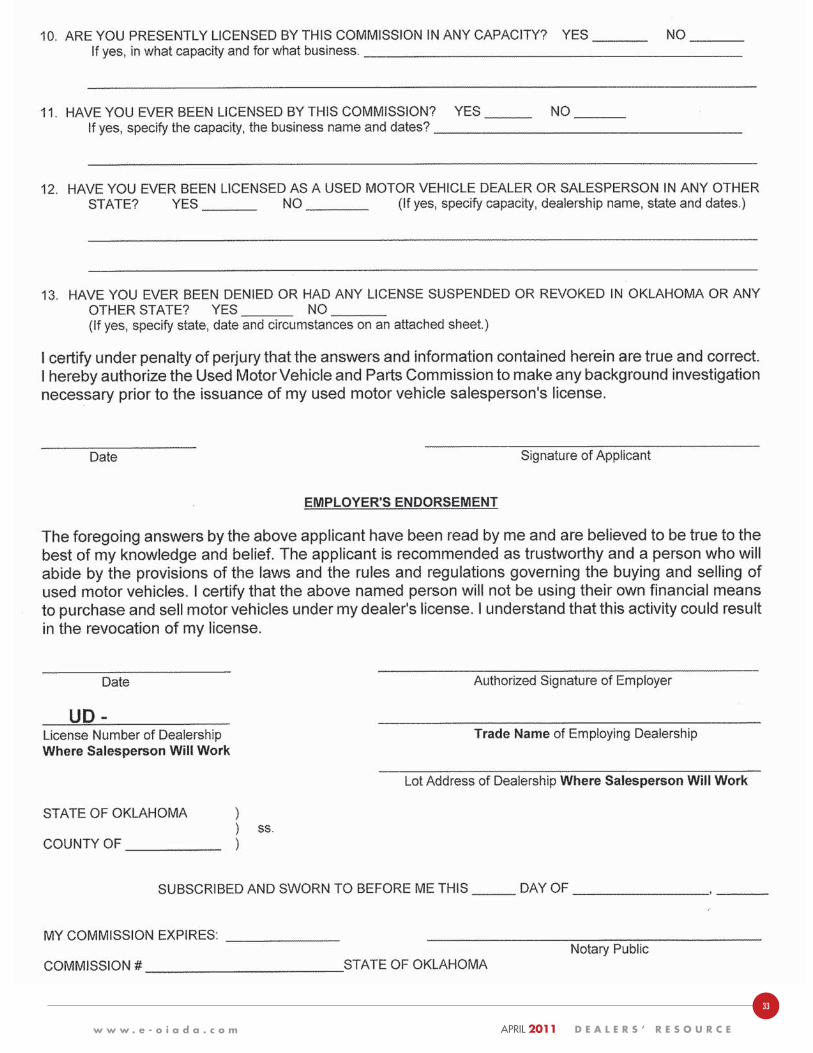

It is the responsibility of each licensed used car dealer to license all salespersons. Upon hiring a salesperson, the dealer shall provide to the Used Motor Vehicle and Parts Commission a signed and notarized Salesperson’s application, check or money order filing fee of $25.00, original $1,000.00 Salesperson’s surety bond signed by the applicant, and a photo copy of the salesperson’s driver’s license.

Once all requirements have been submitted, the salesperson is considered temporarily licensed until the Commission takes action on the application. All temporary salesperson license applications shall be submitted for approval to issue permanent license at the first monthly Commission meeting following receipt of the application.

A permanent salesperson’s license shall be issued after approval of the applicant by the Commission. A salesperson’s license shall consist of an identification card bearing the name, signature of the salesperson, social security number, name of employer, address, signature of the Executive Director, and the dealer’s license number prefixed with UD (UD-0000). The individual shall carry the card upon his person at all times when acting as a used motor vehicle salesperson at the licensee location.

The Oklahoma Used Motor Vehicle and Parts Commission regulations consider anyone who engages in the activities listed below to be a used motor vehicle salesperson requiring licensing:

A used motor vehicle salesperson is anyone who:

1. receives gain or compensation of any kind, directly or indirectly, regularly or occasionally for, or negotiates for, sale or trade of a specified used motor vehicle for a specified used motor vehicle dealer, or

2. operates as a broker only for a specified used motor vehicle dealer, or

3. receives compensation for referral of a prospective buyer to his employer or acts on behalf of the dealer in the purchase or sale of a used motor vehicle, or

4. is authorized to transfer and/or sign titles for the dealership, or

5. displays or offers used motor vehicles for sale for the dealership at a licensed location,

6. acts in the capacity of sales manager or finance and insurance manager or acts in any capacity as part of the sales process,

7. does not otherwise come under the definition of a wholesale used motor vehicle dealer and/or is not required to obtain a license as a wholesale used motor vehicle dealer, but is authorized by a person licensed by the Oklahoma Motor Vehicle Commission to sell new or unused motor vehicles, (franchise dealer) to purchase and sell used motor vehicles without direct supervision by the “franchise dealer,” whether at auction or otherwise, to-wit: a “wholesaler” or individual who pays the “franchise dealer” a draft or check fee for vehicles purchased using the “franchise dealer’s” used motor vehicle dealer’s license; or who is required to compensate the “franchise dealer” for any loss arising from the sale of a vehicle; or who in any manner operates independently of the ordinary business of the “franchise dealer.”

The Oklahoma Used Motor Vehicle and Parts Commission regulations prescribe the following with regard to licensed salespersons:

1. A salesperson’s license shall not authorize the person to refer a prospective customer or consumer to another used motor vehicle dealer and obtain compensation therefore without an employment relationship with the other used motor vehicle dealer.

2. A license for a used motor vehicle salesperson will not be issued, renewed, or endorsed until the employing dealer is licensed and has certified that the applicant for said license is in his employ. Dealers’ payrolls and other evidence will be checked to ascertain that all salespersons for such dealers are licensed. It is not intended that the dealer be required to pay for licenses for its salespersons. However, the dealer may do so on a reimbursable basis, or any other plan satisfactory to its dealership organization. All salespersons licenses will be sent to the dealer for distribution to the respective applicants, and the dealer will determine that all its personnel required to obtain licenses have done so.

3. If the salesperson changes employer, the licensee shall immediately mail the license to the Commission for its endorsement of the change of employer. There shall be no charge for such

endorsement. The licensee shall keep his license on his person while engaged in his business and shall display it upon request; however, there shall be no penalty for not having the license upon his person when he has submitted it to the Commission for its endorsement of a change of employer.

4. The dealer will notify the Commission in writing when a salesperson’s employment is terminated. The dealer may be liable for actions of the salesperson until proper notice is filed with the Commission.

5. Each salesperson shall surrender his identification card to the Commission for endorsement of change of employer, before again engaging in the business as a salesperson for another used motor vehicle dealer or as a used motor vehicle dealer.

6. A used motor vehicle salesperson’s license shall permit the licensee to engage in the activities of a used motor vehicle salesperson. A salesperson’s license does not entitle the licensee to perform as a dealer. A used motor vehicle salesperson’s license does not entitle a person to separately own vehicles for sale or any interest in the vehicles or dealer business without first qualifying as a partner, corporate member, or part owner of the dealership and meeting the qualifications of a dealer.

7. A salesperson may not hold more than one used motor vehicle salesperson’s license at any one time or be employed by or sell for any dealer other than the dealer and at the address designated on the salesperson’s license, with the exception that the licensed dealer has more than one location. Then the licensed dealer and licensed salesperson may sell on each location properly licensed as additional locations.

8. A salesperson’s license shall not be issued for an individual who is not actively engaged in the activities of a used motor vehicle salesperson, nor shall it be issued for the purpose of allowing an individual to operate a vehicle with a used motor vehicle dealer’s plate for any use not benefiting the dealer’s business.

An application for Used Motor Vehicle Salesperson’s License is included in this newsletter. You may make copies of this form for filing with the Used Motor Vehicle and Parts

OKL A HOM A USED MOTOR VEHICLE S A LE SPERSONSL ICENS ING REQUIREMENT S A ND DE A LERSHIP

RE SPONSIBIL IT IE SBY ADR STAFF

APRIL 2011 D E A L E R S ’ R E S O U R C E

31

w w w . e - o i a d a . c o m

Social media continues to be a white-hot subject. It’s fueled in no small part by the top players in the field that are beginning to

look more like financially viable businesses. Twitter is predicting $150 million in revenue this year. Foursquare has six million users and its co-founder would have you believe it’s worth $250 million. Facebook banked an astonishing $1.86 billion in revenue in 2010 and some analysts value the company at $50 billion.

That’s not bad for a set of businesses the oldest of which hasn’t seen a seventh birthday.

Social network users are engaged on an hourly basis sharing family pictures, relationship status, resumes, and opinions on every subject imaginable. A growing number of consumers have both personal and professional profiles and an overwhelming 93 percent of those active in social media expect businesses to have a social media presence.

Many independent dealers know this is a powerful and influential space, but only a minority are clear about how to manage their presence and what, if any, ROI can be derived from a commercial online presence.

It’s important to remember the five laws of social media.

It is social

This means that all social media interaction is about a conversation between at least two people. Many dealerships make the mistake of operating in a broadcast mode, blasting out information about sales, products, and business offerings. In the social space, this is unwanted noise. The magic happens when the employees of the dealership, customers, potential buyers, and brand enthusiasts all build an organic discussion around individual objectives. Dealers want to sell cars. Consumers want to get to and from work reliably, express their style, and get a good deal.

One dealership in the Southwest offers a regular schedule of updates that includes maintenance and performance tips updated by its chief mechanic, as well as the latest information available about vehicle reliability. Site guests believe the dealership isn’t just trying to sell them just any car, but a car they can rely on.

It is personal

The most effective social online presence comes with a face and a personality. The important thing for dealers to know is a real human advocate creates credibility with customers. The communication style should be personal, too. Dealers know their markets and their customers. Great online community mangers talk to guests as if they were standing on the showroom floor.

Top social marketers have potential customers arrive at the dealership shaking hands and saying how good it is to finally meet.

Content is kingThose interested in your social media

presence have an expectation you’ll deliver information they can use. Customers see the dealer as an authority on automobiles. They look to dealerships for information that will guide them through a sea of choices to the car best suited for them. Dealers delivering online content on things such as vehicle reliability, overall satisfaction and trends are far more likely to have shoppers visit their store.

Don’t spam

Social media sites are not substitutes for radio, TV or newspaper advertising. Community members aren’t interested in sale specials, inventory, financing or information if those things aren’t catered to their specific needs. This does not mean dealers shouldn’t post inventory for customers to see; what it does mean is dealers shouldn’t blast fans with service deals and lowered prices. In social media, a business or a friend can be banished with one click.

Listen and respondThis one seems easy, as most businesspeople