Ohio Income Tax: Snowbirds Clipped by Ohio Supreme … · Ohio Income Tax: Snowbirds Clipped by...

25

10/7/2015 1 Ohio Income Tax: Snowbirds Clipped by Ohio Supreme Court Steven A. Dimengo, JD, CPA, MT 3800 Embassy Parkway, Suite 300 Akron, OH 44333 (330) 258-6460 [email protected] Richard B. Fry III, JD, MT 3800 Embassy Parkway, Suite 300 Akron, OH 44333 (330) 258-6423 [email protected] Ronald F. Wayne, JD 1375 East Ninth Street, Suite 1700 Cleveland, Ohio 44114 216-615-7349 [email protected] October 7, 2015 INTRODUCTION Importance of “resident” status. Historic Tests Common law domicile test. Bright-line domicile presumption. The Cunningham decision and how to plan accordingly. Will there be a legislative fix? Estate planning concerns and pitfalls. Pros / Cons of Ohio and Florida residency Importance of Residency Ohio resident = Ohio domicile. R.C. 5747.24 “bright-line” test.

Transcript of Ohio Income Tax: Snowbirds Clipped by Ohio Supreme … · Ohio Income Tax: Snowbirds Clipped by...

10/7/2015

1

Ohio Income Tax:Snowbirds Clipped by

Ohio Supreme Court

Steven A. Dimengo, JD, CPA, MT3800 Embassy Parkway,Suite 300Akron, OH 44333(330) [email protected]

Richard B. Fry III, JD, MT3800 Embassy Parkway,Suite 300Akron, OH 44333(330) [email protected]

Ronald F. Wayne, JD1375 East Ninth Street,Suite 1700Cleveland, Ohio [email protected]

October 7, 2015

INTRODUCTION

Importance of “resident” status.

Historic Tests

Common law domicile test.

Bright-line domicile presumption.

The Cunningham decision and how to planaccordingly.

Will there be a legislative fix?

Estate planning concerns and pitfalls.

Pros / Cons of Ohio and Florida residency

Importance of Residency

Ohio resident = Ohio domicile.

R.C. 5747.24 “bright-line” test.

10/7/2015

2

Importance of Residency

Ohio resident:

Taxed on all income.

Credit to extent income tax paid toanother state (limited by Ohio taxotherwise due).

Ohio Nonresident

Taxed on income earned / sitused toOhio (via credit to extent incomeearned outside Ohio).

Core situsing provisions.

R.C. 5747.20

R.C. 5747.21

R.C. 5747.212

Background

Nontaxable Income For Nonresidentsof Ohio:

“Retirement income” (includingpayments from certain nonqualifiedplans).

Investment income from intangibleassets (e.g., interest, dividends,capital gains).

Non-compete payments

Non-Ohio business income.

10/7/2015

3

Background Pass-ThroughEntity (“PTE”) Interest Sale

R.C. 5747.212: Owning ≥ 20% interest in PTE during 3-year period ending last day of tax year;gain from sale of interest apportioned to Ohiousing average of PTE’s apportionment ratios forprior 3 years. Also applies to C corporations with ≤ 5 owners (or

having a > 50% owner).

Parallel provision for sale of assets (e.g., situsgoodwill).

Residency Historically

For income tax purposes, a resident issomeone domiciled in the state.

Determined by common-law test.

A person may have multipleresidences, but only one domicile.

Common-Law Domicile Test

Focus on intent – very subjective.

A person’s domicile is their permanentlegal residence intended to be usedfor an indefinite period, and to which,the person intends to return whenabsent.

10/7/2015

4

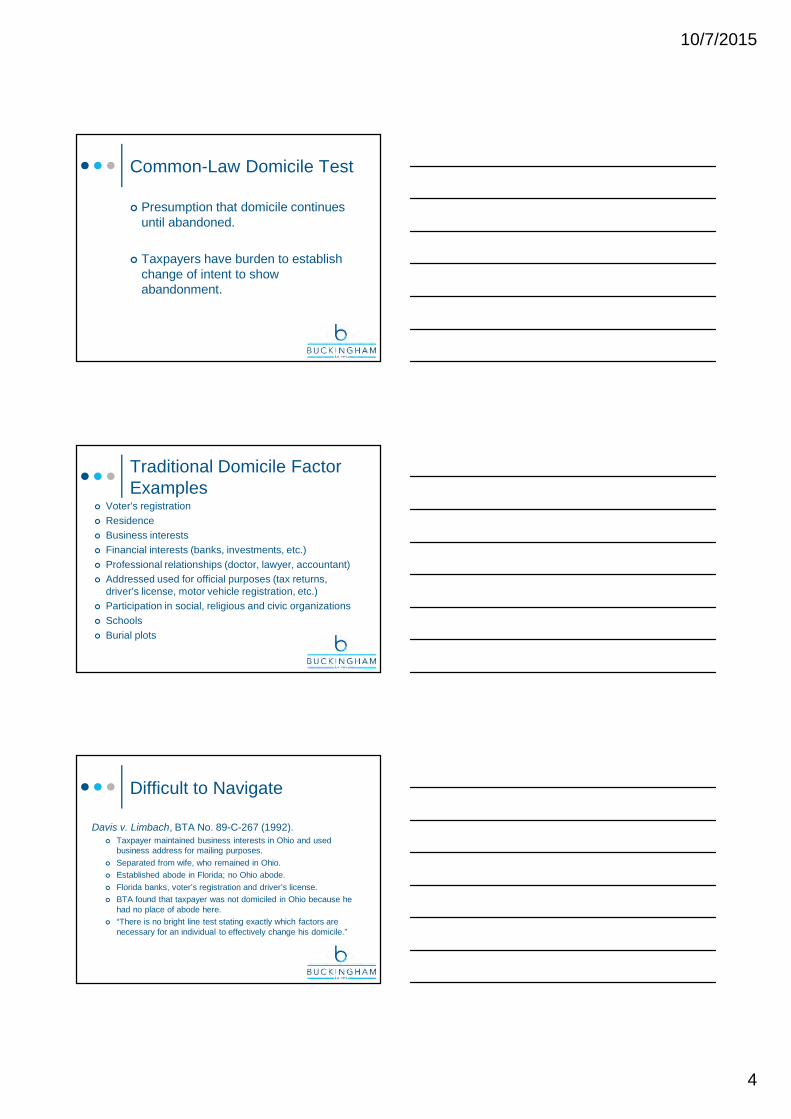

Common-Law Domicile Test

Presumption that domicile continuesuntil abandoned.

Taxpayers have burden to establishchange of intent to showabandonment.

Traditional Domicile FactorExamples

Voter’s registration

Residence

Business interests

Financial interests (banks, investments, etc.)

Professional relationships (doctor, lawyer, accountant)

Addressed used for official purposes (tax returns,driver’s license, motor vehicle registration, etc.)

Participation in social, religious and civic organizations

Schools

Burial plots

Difficult to Navigate

Davis v. Limbach, BTA No. 89-C-267 (1992). Taxpayer maintained business interests in Ohio and used

business address for mailing purposes.

Separated from wife, who remained in Ohio.

Established abode in Florida; no Ohio abode.

Florida banks, voter’s registration and driver’s license.

BTA found that taxpayer was not domiciled in Ohio because hehad no place of abode here.

“There is no bright line test stating exactly which factors arenecessary for an individual to effectively change his domicile.”

10/7/2015

5

Bright-Line Test Enacted

Series of presumptions based uponOhio contact periods. R.C. 5747.24.

“Contact period” occurs when awayovernight from the individual’s non-Ohioabode and, while away, spends any part oftwo consecutive days in Ohio.

Does not apply to part-year residents.

Irrebuttable Presumption

Bright-line residency elements:

Non-Ohio abode;

Satisfy contact period test; and

File Non-Ohio Residency Affidavit (Form IT DA).

“The presumption … is irrebuttable unless theindividual fails to timely file the [Affidavit] ormakes a false statement.” R.C. 5747.24(B).

Relaxing ofContact Period Test

Originally, no more than 120 Ohiocontact periods.

2007 – Fewer than 183 Ohio contactperiods.

2015 – No more than 212 Ohiocontact periods.

10/7/2015

6

Tax Commissioner RuleOhio Admin. Code 5703-7-16

Factors not to be considered: Financial institutions, lenders, investment brokers

Professional service providers (e.g., doctors, lawyers,accountants)

Civic or charitable organization membership

Passive business interests

Schools

Burial plots

Relevant factors: Ohio contact periods

Comparison with activities in previous years

Any other factor

Cunningham

<183 Ohio contact periods.

Tennessee home entire year.

Timely filed affidavit.

Contradiction

Ohio homestead exemption.

Principal residence under penalties ofperjury.

Domicile affidavit.

Non-Ohio domicile entire year underpenalty of perjury.

Agreed Ohio common law domicile.

10/7/2015

7

BTA

Accuracy of taxpayer’s statement withreference to contact periods and non-Ohio home.

Supreme Court

Common law domicile.

Intent to reside indefinitely.

Old domicile continues until new oneestablished (i.e., need abandonment).

Supreme Court

Bright-line statute does not affectsubstantive law of domicile.

R.C. 5747.24 incorporates/preservescommon law domicile.

10/7/2015

8

Supreme Court

Taxpayer statement can be false if notsupported by common law domicile.

Tax Commissioner need only identify“substantial basis” for rejecting claimof non-Ohio domicile.

Contradictory statement in homesteadexemption.

Dissent

False statement confined to contactperiods / non-Ohio abode.

Necessary to provide certainty.

Post Cunningham

Proposed Legislation.

10/7/2015

9

Proposed Legislation

Accuracy of affidavit tied to contact periods/ non-Ohio abode entire year.

Common law domicile irrelevant.

Clarification of existing law, reflecting intentprior to Cunningham (i.e., refund claimsallowed).

Planning

Focus on common law domicilecalendar year prior to “contact period”calendar year.

Eliminate Ohio home?

Planning with respect to incomereceipt.

Plan

Plan

Plan

Moving to Florida?Estate Planning andOther Considerations

You make the call.

10/7/2015

10

10/7/2015

11

Florida:

No estate tax.No income tax.Unlimited HomesteadExemptionReal Property Homestead taxexemption--$50K + 3%appreciation

Ohio:

No estate tax

Income tax up to 5.39%

Homestead Exemption limited to$132,900

Real property Homestead TaxExemption-$25K (and less than $30KAGI after 2014

10/7/2015

12

Ohio Estate PlanningAdvantages

Ohio Legacy Trusts=DAPT

Ohio Wholly Discretionary Trusts.

Springing Powers of Attorney

Shorter S/L on Breach of FiduciaryDuties.

How to Memorialize FloridaDomicile

Steps to Take to Be Recognized as aFloridian

File a declaration of domicile at thecounty courthouse. Send a copy tothe appropriate taxing authority inyour former state.

How to Memorialize FloridaDomicile - Continued

Obtain a Florida driver’s license.

Register to vote (and vote) only inFlorida.

Apply for the homestead exemption ifyou own a residence in Florida.

10/7/2015

13

How to Memorialize FloridaDomicile - Suggestions

Transfer your out-of-state accounts to a bank in Florida.

Arrange for direct deposits such as Social Security intoyour Florida bank account.

Open a safe-deposit box at a Florida financial institution..

Move personal items with significant monetary value toFlorida.

Change the address of brokerage accounts to your newFlorida address.

move your account to the Florida office of your existingnational brokerage firm or to a local brokerage firm.

How to Memorialize FloridaDomicile - Suggestions

File federal income tax returns using your Floridaaddress. File a final state income tax return as a part-yearresident through the day you moved from your formerstate. Then, if you receive no income from your formerstate, stop filing state income tax returns. If you stillreceive income from your former state, file a nonresidentincome tax return for that portion of your income.

Declare Florida your legal residence when you make orrevise your will.

Use your Florida address in all business and socialcorrespondence.

How to Memorialize FloridaDomicile - Suggestions

Identify Florida in written and oral communication as yourpermanent home.

Document the days you spend in every state, ensuringthat you spend more time in Florida than any other state.

Register your vehicles in Florida.

Notify credit card companies and creditors of your newaddress.

Notify insurance companies of your new address and thatyour vehicles and valuable personal property are nowlocated in Florida.

10/7/2015

14

How to Memorialize FloridaDomicile - Suggestions

Become active in Florida community or politicalorganizations, religious institutions or clubs. Resign fromprivate clubs in your former state or convert yourmemberships to nonresident memberships.

Become a patient of a Florida doctor and dentist andhave your records transferred to them.

Purchase a cemetery lot or crypt in Florida.

If you have a professional or occupational license andintend to continue working, obtain a Florida license.

Change the address on your passport

Your Ohio Will is Validbut….

Florida has self-proving Wills

Your Ohio power of attorney is validin Florida but…..

Springing powers not recognized inFlorida.

Hot Powers need to be initialed.

Certifications of Powers of Attorneysimilar in both states

10/7/2015

15

Your healthcare documents are validin every state, but…

Health Care professionals moreconversant with their own forms.

Create separate documents for bothstates.

Different anatomical gift forms.

Your Ohio Trust is Valid in Floridaand Every State, but…

Consider change of situs and choice of law.

Should be executed with same formalities as a FloridaWill.

Florida does not have DAPT or statutory whollydiscretionary trusts.

No Florida Residency Statute?

Short of year-round residency, there isno bright line test for determiningwhether someone is a resident ofFlorida.

10/7/2015

16

Ronald F. Wayne, JDBUCKINGHAM, DOOLITTLE & BURROUGHS, LLC1375 East Ninth Street, Suite 1700Cleveland, Ohio 44114P: [email protected]

Thank You!Steven A. Dimengo, JD, CPA, MTBUCKINGHAM, DOOLITTLE & BURROUGHS, LLC3800 Embassy Parkway, Suite 300Akron, OH 44333(330) [email protected]

Richard B. Fry III, JD, MTBUCKINGHAM, DOOLITTLE & BURROUGHS, LLC3800 Embassy Parkway, Suite 300Akron, OH 44333(330) [email protected]

© 2015 Cleveland Metropolitan Bar Association. Reprinted with permission.

BAR JOURNALFEATURE

By RonAld F. WAynE

1. Ohio no longer has an estate tax and never had a gift tax.As of January 1, 2013, Ohio joined the ranks of thirty other progressive states that have no estate or inheritance tax. Prior to repeal, this nasty, final tax was payable if the value of the net estate was over $338,000. A seven percent rate applied to any net taxable value over $500,000 so an estate of $2,000,000 was reduced by about $114,000 in Ohio estate tax liability. Only very small estates, surviving spouses and charities escaped the wrath of this tax. Ohio’s generation-skipping transfer tax has also been eliminated. Ohioans no longer need to flee to other states or count the number of days spent out of Ohio to avoid this tax.

2. Ohio’s new Power of Attorney statute protects the elderly and disabled better than ever.Powers of Attorney executed after March 22, 2012, must specifically list any of the seven “hot powers” if they are to be available to the Agent. These “hot powers” are the ability of the agent to: (1) Create, amend or terminate a trust; (2) Make a gift; (3) Change rights of survivorship; (4) Change a beneficiary designation; (5) Delegate authority; (6) Waive the right to be a beneficiary of a joint and survivor designation; and (7) Exercise fiduciary powers.

The statute also permits interested parties to conduct a swift, meaningful and court-supervised inquiry into the activities of the Agent before all of Principal’s assets are dissipated. Interested parties include: (1) The principal or the agent; (2) Another fiduciary acting for the principal; (3) Health-care surrogates; (4) The principal’s spouse, parent or descendant; (5) A presumptive heir; (6) A person who has a financial interest in the principal’s estate; (7) A governmental agency that protects the principal; (8) The principal’s caregiver; (9) A person asked to accept the power of attorney.

These two provisions are designed to curb past abuses of Powers of Attorney by bad actors using generic powers without supervision to feather their own nests. Powers executed before the effective date of the Act are still valid, but should be updated to make sure that only necessary and appropriate powers are available to the Agent.

3. The Ohio Trust Code provides comprehensive guidance.Prior to the enactment of the §5801 of the Ohio Revised Code, it was difficult for lawyers in Ohio to provide definitive advice regarding the creation, administration, reporting, modification and termination of trusts.

Under the Ohio Trust Code, practitioners, courts and all parties to Trusts have a comprehensive framework to address all

aspects of Trust administration. Divergent local practices and inconsistent court rulings have been replaced by this compendium of Ohio trust law. As a result, Ohio administrations are crisper and cleaner. This makes Ohio a more attractive location for trust administration, resulting in the retention of assets in Ohio and other economic benefits.

4. Ohio’s Decanting Statute provides another tool to fix broken Trusts. Ohio is one of only fourteen states with decanting statutes. §5808.18 permits the transfer of assets from a less then optimum Trust to a more favorable Trust to accomplish desired objectives.

Decanting is easiest with Trusts that give Trustees absolute power to make distributions of principal. §5808.18(B) may be used where a Trustee has authority to distribute principal to or for the benefit of one or more beneficiaries pursuant to an ascertainable standard. §5808.18(C) discusses limitations on the provisions of the receiving Trust which may not modify or reduce the current right of a beneficiary to mandatory distributions.

The new Trust may include a spendthrift provision, grant beneficiaries a power of appointment, divide or combine trusts, change a trust’s governing law, remedy tax problems, change administrative provisions and/or name a Trust protector who can remove a Trustee under certain circumstances. When decanting is added to Ohio’s existing remedies of Private and Judicial Settlement Agreements, Common Law Settlement and Release Agreements and Judicial Reformation, Ohio becomes a leader among states that permit Trust modification to adapt to changing circumstances or correct scrivener errors.

5. Ohio’s Legacy Trust may be the best Domestic Asset Protection Trust in the Country. Since March 27, 2013, individuals may create an irrevocable Legacy Trust utilizing an Ohio qualified Trustee. The assets of the trust are generally exempt from creditors’ claims yet the creator of the trust can retain certain rights to trust principal and interest during the term of the Trust. The Trustee may be guided by a purely discretionary standard or according to another permissible standard in the trust instrument but not an ascertainable standard. The Settlor may retain the power to veto distributions and invade Trust principal up to 5% annually. During life, the grantor may remove and replace a trustee or

If You Live in Ohio, You Are Darned Lucky!Ten Good Reasons Why Ohio Is a Great State for Estate Planning

© 2015 Cleveland Metropolitan Bar Association. Reprinted with permission.

trust advisor. Upon death, the grantor can have a non-general power of appointment.

If a transfer into the Trust is not a fraudulent conveyance, creditors are barred from seeking recovery against the Trust assets after, at the latest, eighteen months from a transfer of property into the trust. This creditor protection does not apply to child support and, in some cases, alimony obligations. If properly drafted and funded, the Legacy Trust can provide some protection when a Prenuptial Agreement is unobtainable.

6. Ohio’s LLC Statute provides enhanced asset protection. As of May 4, 2012, the Ohio Limited Liability Company Act provides that a charging order is the exclusive remedy of a judgment creditor against an LLC member. Prior Ohio law was unclear as to whether a judgment creditor had additional remedies to foreclose on a member’s interest. Unlike Florida’s Single Member LLC Statute, Ohio law is now eminently clear that the underlying assets of the LLC are not available to satisfy creditors’ claims.

A charging order only directs that any distributions intended for the member will instead be paid to the judgment creditor. LLC managers can often defer actual distributions for indefinite periods of time, and even distribute phantom income. Both of these factors create an atmosphere for negotiation during which the creditor’s claims may be substantially compromised.

7. The Ohio Probate Code continues to improve. Despite the many probate avoidance devices available to Ohioans today, families who do no planning default into probate. Fortunately and systematically, the Ohio Probate Code has been amended. Deadlines have tightened and administrations have become more streamlined over time. Beneficiaries enjoy increased transparency and are not at the mercy of dilatory executors in the inventory, appraisement or distribution of assets.

Ohio law provides flexibility in choosing the optimal form of administration ranging from instantaneous summary administrations, to releases of assets without administration, to full administrations. Practitioners have the discretion to choose formal administration even if the probate assets are small but the need for flexibility and a duly appointed fiduciary are great.

Beneficiaries are permitted to examine executors under oath and review their activities during the course of a probate administration to make sure that assets are properly protected, invested and distributed as promptly as possible.

8. Ohio’s creditors’ claim statute in probate administrations protects decedents’ estates. Ohio law requires that most claims against an estate must be presented to the administrator within six months of the decedent’s death, not six months after the appointment of the administrator. Most other states also require a formal publication for creditors in order to commence the statute of limitations on claims. Ohio’s Revised Code §2117 applies to “claims arising out of contract, out of tort, on cognovit notes, or on judgments, whether due or not due, secured or unsecured, liquidated or unliquidated.”

It is the responsibility of the creditor to file a timely claim and, if necessary, have an administrator appointed within the six month period so that the claim can be properly presented. Even though an individual who is later appointed as administrator receives a notification of claim within the six month period, this is not good enough. Even valid claims which do not meet the presentation requirements need not be paid by the administrator.

9. Ohio’s Transfer and Payable on Death Statutes avoid pitfalls associated with joint property. The advantage of utilizing a TOD Affidavit for Ohio real estate is that the owner/affiant remains the sole owner of the property and, therefore, need not worry about creditors’ claims or judgment liens against a joint tenant.

Only if the affiant owns the real estate on the date of her death does the Transfer on Death beneficiary receive an interest in the property. Prior to death, the affiant is free to sell to dispose of the property without the approval of the TOD beneficiary.

Ohio also permits the registration of bank accounts in payable on death form with the same advantages as those stated above for real property.

Finally, Ohio permits transferrable on death designations for other intangible assets, including publically-traded or closely-held stocks, bonds and other securities. The proper utilization of these devices allows for extremely flexible estate planning opportunities in Ohio not available in other states, including Florida.

10. Continuing cooperation between local and state Bar Associations and the Ohio legislature benefits Ohio citizens.The Ohio State Bar Association and many local Bar Associations, including the CMBA, communicate and cooperate with Ohio’s legislative branches in the best interest of Ohioans. Well-intentioned and dedicated members of the Bar devote significant time and intellect to reviewing, updating and proposing legislation to make Ohio a more attractive place to live and work. The Ohio State Bar Association Certification Program provides a reliable way for consumers to find well-qualified lawyers in their areas of need without resort to the whims of search engine optimization or online hyperbole.

For these reasons and many others, if you live in Ohio, you’re darned lucky!

Ronald F. Wayne is a partner at Buckingham, Doolittle & Burroughs, LLC. He is licensed in Ohio, Florida and New Jersey. Mr. Wayne is a Certified Specialist in

the practice of Estate Planning, Trust and Probate Law. He has been a CMBA member since 1978. He can be reached at (216) 615-7349 or [email protected].

bdblaw.com

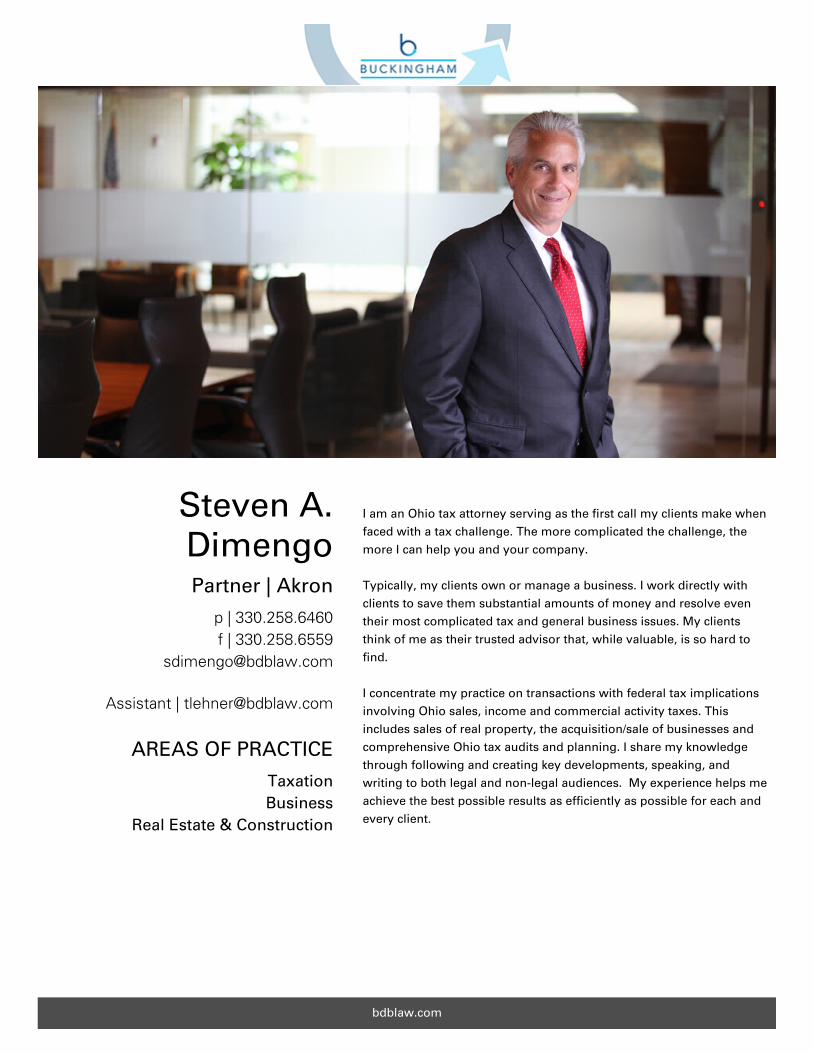

Steven A.DimengoPartner | Akron

p | 330.258.6460f | 330.258.6559

Assistant | [email protected]

AREAS OF PRACTICE

TaxationBusiness

Real Estate & Construction

I am an Ohio tax attorney serving as the first call my clients make whenfaced with a tax challenge. The more complicated the challenge, themore I can help you and your company.

Typically, my clients own or manage a business. I work directly withclients to save them substantial amounts of money and resolve eventheir most complicated tax and general business issues. My clientsthink of me as their trusted advisor that, while valuable, is so hard tofind.

I concentrate my practice on transactions with federal tax implicationsinvolving Ohio sales, income and commercial activity taxes. Thisincludes sales of real property, the acquisition/sale of businesses andcomprehensive Ohio tax audits and planning. I share my knowledgethrough following and creating key developments, speaking, andwriting to both legal and non-legal audiences. My experience helps meachieve the best possible results as efficiently as possible for each andevery client.

bdblaw.com

ExperienceServes as department head of the Taxation Section of the Business Practice Group (also served 1995-2006)

Practices primarily in consultation and representation with respect to federal, multistate and Ohio tax law

matters

Engaged to structure proposed transactions in a manner to obtain optimum tax minimization

Involved in representation before the Ohio Tax Commissioner, Ohio Board of Tax Appeals and the Ohio

Supreme Court, as well as before the Internal Revenue Service

Served as Business Practice Group Leader

Served as vice president, secretary and treasurer of the firm’s board of managers

Joined the firm as an associate in 1989; elected partner in 1994

REPRESENTATIVE MATTERS/REPORTED CASES

Marc Glassman, Inc. v. Levin, 119 Ohio St. 3d 254, 2008-Ohio-3819

Stein, Inc. v. Tracy, 84 Ohio St. 3d. 501 (1999).

WCI Steel, Inc. v. Testa, 129 Ohio St. 3d 256, 2011-Ohio-3280.

Crown Communications, Inc. v. Testa, 2013-Ohio-3126.

Funtime, Inc. v. Zaino, 105 Ohio St. 3d 74 (2004).

The Dannon Company Co., Inc. v. Tracy, Ohio BTA Case No. 97-M-233 (September 11, 1998).

General Electric Credit of Tennessee v. Tracy, Ohio BTA Case No. 95-K-221 (June 27, 1997).

E.G. Baldwin & Associates, Inc. v. Tracy, Ohio BTA Case No. 95-K-222 (May 30, 1997).

Express Packaging, Inc. v. Limbach, Ohio BTA Case No. 89-K-22 (September 18, 1992).

U.C. Industries v. Limbach, Ohio BTA Case No. 89-J-1070 (August 7, 1992).

WCI Steel, Inc. v. Testa, Ohio BTA No. 2005-A-1565 (December 28, 2012).

Reiter Dairy, Inc. v. Limbach, Ohio BTA No. 90-Z-503 (January 15, 1993).

Haberman v. Tracy, Ohio BTA 91-A-1639 (March 19, 1993).

Heartland Education Community, Inc. v. Testa, Ohio BTA No. 2012-277 (September 3, 2014).

Education & AdmissionsThe University of Akron Law School, Akron, Ohio (J.D., cum laude, 1986)

The University of Akron, Akron, Ohio (M.A., 1986)

The University of Akron, Akron, Ohio (B.A., magna cum laude, 1983)

Certified Public Accountant (1987)

Admissions

Ohio Bar

U.S. District Court

U.S. Tax Court

Awards & HonorsListed in Best Lawyers in America® (2003-2016)

Selected for inclusion in Ohio’s Super Lawyers® (2004-2015), as voted by his peers

Martindale-Hubbell Peer Review Rating of AV® Preeminent™, which is the highest possible rating in both legal

and ethical standards as established by confidential opinions from members of the Bar.

Selected for inclusion in Ohio’s Super Lawyers Business Edition® for Tax Law (2014)

Recipient: Distinguished Alumni Award from the Archbishop Hoban High School Alumni Association (2013)

bdblaw.com

Named Akron Best Lawyers® ‘Tax Lawyer of the Year’ (2012)

Listed in Super Lawyers Corporate Counsel Edition® for Tax Law (2009)

Listed in Northern Ohio Live – Ohio’s Top Lawyers (2003)

Listed in Inside Business Magazine as a Leading Lawyer in Northeast Ohio in Tax Law, as voted by his peers

(2001)

Recipient: Dr. Frank L. Simonetti Distinguished Alumni Award from the University of Akron College of Business

(2015)

Professional & Civic InvolvementAdjunct Professor: The University of Akron Master of Taxation Program (State and Local Tax)

Secretary and Trustee: Archbishop Hoban High School

Past Affiliations

Appointed: Ohio Tax Commissioner’s Advisory Council

Associations

Member: Taxation Section: Akron Bar Association

Member: American Bar Association

Member: Ohio State Bar Association

Chair, Taxation Section, including Sales & Use Tax Subcommittee: Ohio State Bar Association

bdblaw.com

Richard B. Fry IIIPartner | Akron

p | 330.258.6423f | 330.258.6559

Assistant | [email protected]

AREAS OF PRACTICE

TaxationBusiness

Real Estate & Construction

As a business tax attorney, I represent small to mid-size businessowners and managers who seek my trusted advice on significanttransactions and difficult challenges facing their businesses. I advisemy clients on state and local tax issues, counsel clients on commercialand real estate transactions, and resolve state and local taxcontroversies on behalf of my clients.

I have vast experience with Ohio and multistate tax issues, includingOhio sales/use tax, commercial activity tax, and personal income taxaudits, appeals and planning. Because of my tax background, I oftenadvise clients on the business and tax implications related to theircorporate structure and significant transactions.

My ability to understand my clients' business and tax objectives, andhelp them achieve those objectives in a practical manner withoutdisrupting commercial operations, is one of the many benefits I canoffer you and your business.

bdblaw.com

ExperienceWorks in the Business Practice Group and has experience in a wide variety of areas, including federal and state

tax matters, mergers and acquisitions, real estate, litigation and business organizations

Focuses on state and local tax matters, including Ohio tax controversies, sales and use tax and multistate tax

planning

Joined the firm as an associate in 2008; was elected partner in 2015

REPORTED CASES

Crown Communications, Inc. v. Testa, 2013-Ohio-3126.

Heartland Education Community, Inc. v. Testa, Ohio BTA No. 2012-277 (Sept. 3, 2014).

Education & AdmissionsThe University of Akron School of Law, Akron, Ohio (J.D., summa cum laude, 2008)

The University of Akron, Akron, Ohio (M.A., 2008)

Kent State University, Kent, Ohio (B.B.A., cum laude, 2003)

Mount Union College, Alliance, Ohio (B.A., cum laude, 1992)

American Junior Year in Heidelberg Program, Heidelberg, Germany (1990)

Admissions

Ohio Bar

Co-Chair: Sales & Use Tax Subcommittee of the Ohio State Bar Association, Taxation Committee

U.S. District Court, Northern District of Ohio

U.S. Tax Court

Awards & HonorsRecipient: Judge Harold and Jeanette White Scholarship (2006-2007)

Recipient: Ohio State Bar Association, Labor and Employment Law Student Achievement Award

Professional & Civic InvolvementMember: Akron Tax Club

Member: Boys & Girls Club of the Western Reserve, Aspire! Committee

Member: Boys & Girls Club of the Western Reserve, Marketing Committee

Associations

Member: Akron Bar Association

Member: American Bar Association

Member: Ohio State Bar Association, Taxation Committee

bdblaw.com

Ronald F. WaynePartner | Cleveland

p | 216.615.7349f | 216.621.5440

Assistant | [email protected]

AREAS OF PRACTICE

Trusts & Estates

I am a trusts and estates attorney with a focus on estate planning,probate, and elder law. I assist my clients with the efficient transfer ofwealth from generation to generation, business succession plans, andprobate and trust litigation matters.

I listen closely to individuals’ and families’ needs and desires so I canprotect the assets they have worked hard to accumulate. Ivigorously defend my clients against the Internal Revenue Service andminimize their income, estate or gift tax liabilities. For aging clients, Iwork to ensure your assets are not ravaged by long-term care costs.For parents of children with dependencies, disabilities, or financialissues, my goal is to ensure that your children have a secure financialfuture. For business owners, I assist you in selling your business ortransferring it to subsequent generations.

I design and implement estate plans based upon what is of importanceto you. Simply put, I am here to protect your wealth, your business andyour family.

bdblaw.com

ExperienceAdministers complex trusts and probate estates in Ohio

Designs and implements multigenerational family estate and business succession plans

Represents individuals before the Internal Revenue Service in estate, gift and personal income tax controversies

Certified by the Ohio State Bar Association as a Specialist in Estate Planning, Trust & Probate Law under

guidelines established by the Supreme Court of Ohio’s Commission on Certification of Attorneys as Specialists

REPORTED CASES

In re Estate of Hernton, 164 Ohio App. 3d 306 (9th Dist., Lorain County 2005)

Education & AdmissionsCleveland-Marshall College of Law, Cleveland, Ohio (J.D., cum laude, 1978)

Cleveland State University, Cleveland, Ohio (B.A., magna cum laude, 1974)

Admissions

Ohio Bar

New Jersey Bar

Florida Bar

U.S. District Court, Northern District of Ohio

U.S. Tax Court

United States Supreme Court

Awards & HonorsListed in Best Lawyers in America® (2010-2016)

Recognized in Best Lawyers Business Edition® for Trusts and Estates Law (2015)

Selected for inclusion in Ohio’s Super Lawyers® (2004-2015), as voted by his peers

Martindale-Hubbell Peer Review Rating of AV® Preeminent™, which is the highest possible rating in both legal

and ethical standards as established by confidential opinions from members of the Bar

Professional & Civic InvolvementFormer Delegate: Estate Planning Council of Cleveland

Member: University Hospitals Planned Giving Advisory Committee

Member: The Lawyers Guild of the Catholic Diocese of Cleveland

Member: St. Basil the Great Parish Finance and Endowment Committees

Member, Board of Directors: Society of Financial Services Professionals

Member: Estate Planning Advisory Council of Case Western Reserve University

Lifetime Charter Member: Elder Care Matters Alliance

Associations

Member: Cleveland Metropolitan Bar Association, Probate and Estate Planning Section

Member: Florida Bar Association, Real Property, Probate & Trust Section

Member: Ohio State Bar Association, Elder Law Committee