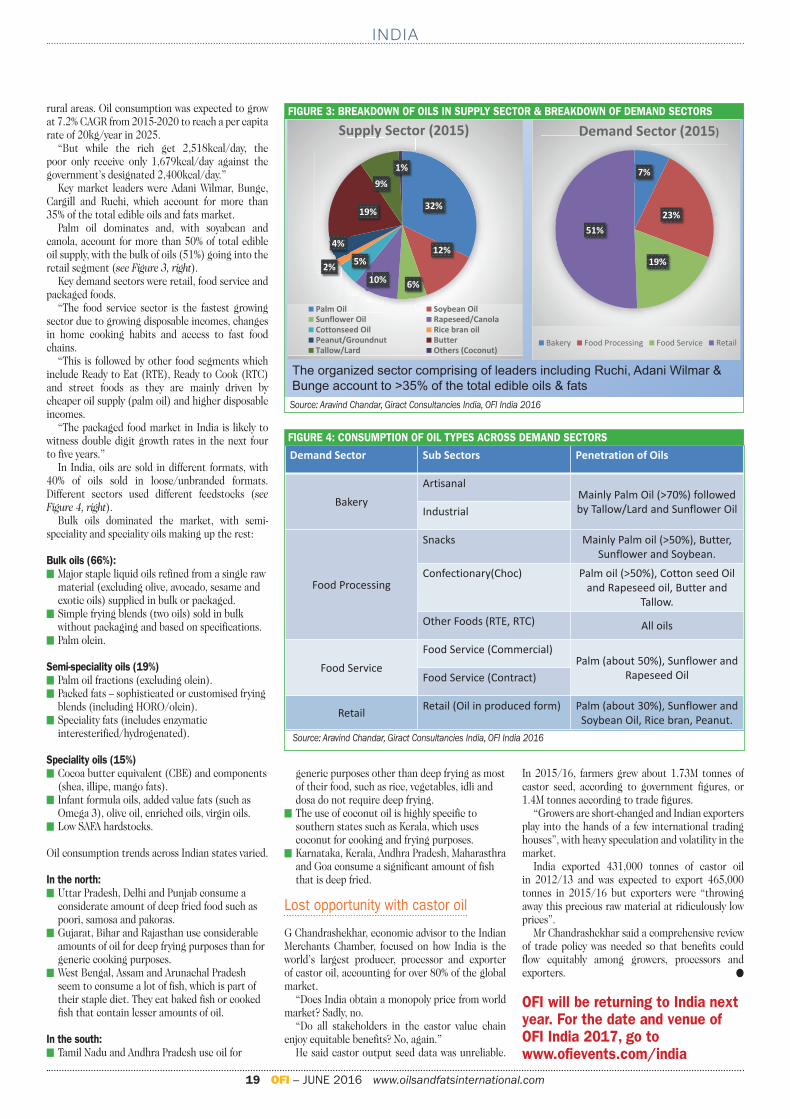

OFI June 2016

42

June 2016 ᔡ Vol 32 No 5 www.oilsandfatsinternational.com INDIA Overcoming challenges BLEACHING EARTHS Salt of the earth

-

Upload

oils-fats-international -

Category

Documents

-

view

370 -

download

2

description

Â

Transcript of OFI June 2016

June 2016 � Vol 32 No 5www.oilsandfatsinternational.com

INDIAOvercomingchallenges

BLEACHINGEARTHSSalt of the earth

June cover 16 final.indd 1 07/06/2016 10:25

Leading edge technologies for the oils & fats industry

Science behind Technology

Qualistock™ Plus Continuous Deodorizer

iConFrac™

Continuous FractionationNano Reactors® - Neutralization/biodiesel

Enzymatic Interesterification

Desmet Ballestra delivers tailor-made engineering and procurement services covering each step of the Industry, from oilseed preparation, prepressing and extraction to oil processing plants including refining and fat modification processes, as well as oleochemicals and biodiesel technologies.

Desmet Ballestra masters the processing of 40 raw materials, including soyabean, sunflower seed, rapeseed/canola, palm oil, groundnut, cottonseed oil etc. Desmet Ballestra has supplied small, medium and very large plants to more than 1,700 processors in 150 countries, covering over 6,000 process sections.

Desmet Ballestra is highly regarded worldwide for its experience, innovation, outstanding project management, dedicated customer service and environmentally friendly processes.

2016-A4-FatModif-Refining.indd 1 5/3/16 5:19 PMOFI June IFC_desmet.indd 1 13/06/2016 12:58

FEATURES

INDIA

17 Overcoming challenges

PLANT, EQUIPMENT & TECHNOLOGY

20 2016 listing & wallchart

BLEACHING EARTHS

26 Salt of the earth

OLEOCHEMICALS

32 Dream or nightmare?

MOROCCO

34 Fighting for China

THE BUSINESS MAGAZINE FOR THE OILS AND FATS INDUSTRY

1 OFI – JUNE 2016 www.oilsandfatsinternational.com

CONTENTSVOL. 32 NO. 5 JUNE 2016

EDITORIAL:

Editor: Serena LimTel: +44 (0)1737 855066E-mail: [email protected]

Editorial Assistant: Rose HalesTel: +44 (0)1737 855157E-mail: [email protected]

SALES:

Sales Manager: Mark Winthrop-WallaceTel: +44 (0)1737 855 114E-mail: [email protected]

Sales Consultant: Anita RevisTel: +44 (0)1737 855068E-mail: [email protected]

Chinese Sales Executive: Erik HeathTel: +44 (0)1737 855108E-mail: [email protected]

PRODUCTION:

Production Editor: Carol BairdE-mail: [email protected]

CORPORATE:

Managing Director: Steve DiproseTel: +44 (0)1737 855164E-mail: [email protected]

SUBSCRIPTIONS: Elizabeth BarfordTel: +44 (0)1737 855028E-mail: [email protected]: Subscriptions, Quartz House, 20 Clarendon Road, Redhill, Surrey, RH1 1QX, UK

Annual Subscription: UK £145, Overseas £168.Two years: UK £261, Overseas £302. Single copy £36

© 2016 Quartz Business Media ISSN 0267-8853

Website: www.oilsandfatsinternational.com

A member of FOSFA

Oils & Fats International (USPS No: 020-747) is published eight times/year by Quartz Business Media Ltd and distributed in the USA by DSW, 75 Aberdeen Road, Emigsville PA 17318-0437. Periodicals postage paid at Emigsville, PA. POSTMASTER: Send address changes to Oils & Fats c/o PO Box 437, Emigsville, PA 17318-0437

Published by Quartz Business Media Ltd Quartz House, 20 Clarendon RoadRedhill, Surrey RH1 1QX, UKTel: +44 (0)1737 855000Fax: +44 (0)1737 855034 E-mail: [email protected]

Printed by Pensord Press, Gwent, Wales

@oilsandfatsint Oils & Fats International

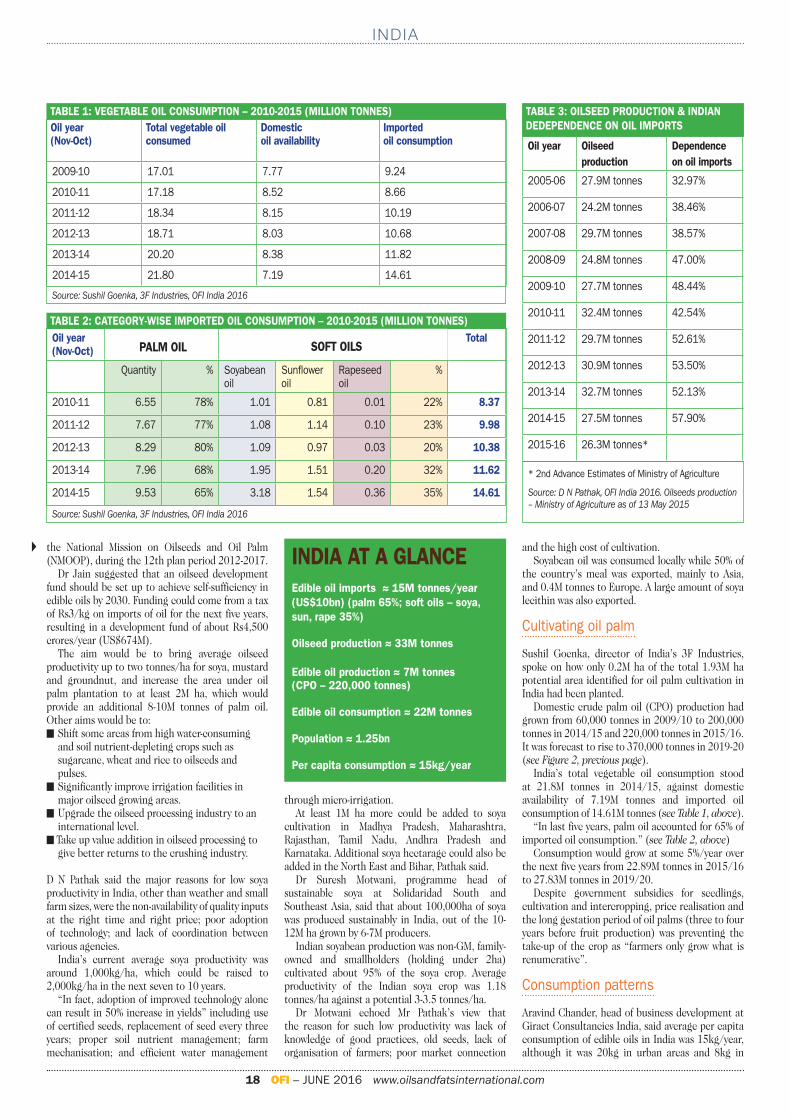

WITH EDIBLE OIL IMPORTS ACCOUNTING FOR NEARLY 60% OF INDIA’S CONSUMPTION REQUIREMENTS, THE COUNTRY NEEDS TO LOOK AT RAISING OILSEED PRODUCTIVITY AND EXPANDING GROWING AREAS P17

PHOT

O: K

ARAN

DAEV

/ AD

OBE

STOC

K

NEWS & EVENTSComment

The Paris climate deal and the Trump effect

News

IOI in U-turn over moveto sue RSPO

Biofuels News

EPA proposes 18.8bn gallons of biofuels blending for 2017

Biotech News

Monsanto rejects Bayer’s US$62bn bid

Transport & Logistics News

Louis Dreyfus seeks investment in port logistics in Middle East

Renewable Materials News

Amyris in venture with South Korea’s CJ

Diary of Events

International Market Review

Statistics

2

2

6

8

12

10

14

36

15

PHOTO: CLARIANT

June contents.indd 1 14/06/2016 11:29

IOI in U-turn over move to sue RSPO

2 OFI – JUNE 2016 www.oilsandfatsinternational.com

NEWS

COMMENT

The Paris climate dealand the Trump effect

More than 170 nations officially signed the landmark Paris climate agreement in New York on 22 April following its adoption

in December (see Comment, OFI February 2016). The agreement aims to limit global temperature rises to below 20C and enters into force if at least 55 nations representing 55% of global greenhouse gas (GHG) emissions ratify it.

Countries which have pledged to ratify the agreement this year include China – the

world’s biggest emitter of emissions – and the USA, two countries which together account for 38% of global emissions.

China has pledged early accession before it hosts the G20 summit for the first time in September.

However, noticeably absent from the list of early adopters are India, Japan and the EU. The EU – which accounts for 12% of global emissions – counts as one signatory and former French Foreign Minister Laurent Fabius, who presided over the UN climate deal, says it will be “damaging” if the bloc is late to ratify.

In the USA, leaders in the ethanol sector have already criticised the government for not including biofuels in the country’s GHG reduction plans.

While 37 countries have included biofuels in their Intended National Determined Contributions (INDCs), the USA has not.

“It is beyond baffling that biofuels or the Renewable Fuel Standard were not included in the US plans to reduce GHG emissions,” said Renewable Fuel Association president and CEO Bob Dinneen. “As the US signs the Paris Agreement, it needs to look no further than its own backyard and fully implement the most potent and proven weapon to combat climate change – the RFS.”

Meanwhile, the rest of the world can only watch and wonder what effect Donald Trump, the presumptive Republican presidential candidate, may have on the deal.

Without mentioning names, Fabius recently told an audience in London: “Think about the impact of the coming US presidential elections [in November]. If a climate change denier was to be elected, it would threaten dramatically global action against climate disruption. We must not think that everything is settled.”

Trump has already said he is “not a great believer in manmade climate change” and told supporters at a North Dakota rally that he would “cancel the Paris climate agreement and stop all payments of US tax dollars to UN global warming programmes”.

So can the USA scupper the deal? Not if other big emitters such as China, the EU, Russia, India, Japan and Brazil ratify it – once 55 countries accounting for 55% of GHG emissions ratify the deal, it enters into legal force, making it difficult for countries to withdraw.

Of course, while the agreement is a historic step in the right direction, much work still remains to be done.

Apart from the fact that each country’s target for emission reduction is voluntary and there is no enforcement if a target is not met, Fabius has pointed to the need to tackle emissions from aviation and maritime transport, which were omitted from the UN talks, and which he said are urgent. He also called for a renewed focus on the possibility of putting a price on carbon, pointing to a Chinese plan to institute a national system of carbon trading from next year.

“We have to avoid being lazy. We have to be calm, and to be hopeful,” he says. �

Malaysia’s IOI Corporation Berhad (IOI) has decided

not to sue the Roundtable on Sustainable Palm Oil (RSPO), which suspended IOI on 1 April following a year-long investigation into allegations that it had failed to protect forests and peat areas.

IOI had announced on 9 May that it was filing a challenge in the Zurich District Court of Switzerland against its suspension.

However, on 6 June, IOI said it would be withdrawing its lawsuit.

“Since the filing of the challenge, IOI has engaged with many of our stakeholders – such as customers, NGOs and the RSPO – to resolve the matter,” said CEO Dato’ Lee Yeow Chor.

IOI had agreed to an action plan to adopt the RSPO’s highest level of accreditation – the Next certification system – by the end of this year, he said.

Following the RSPO’s suspension, major food companies such as Nestlé, Mars, Unilever and Kelloggs dropped IOI as a supplier.

Lee previously said the suspension had affected IOI’s current RSPO contract commitments and had caused significant disruption to certain parts of the European and American food manufacturing sector.

“Our appeal was principally made on two aspects of the suspension decision: one is that the decision should not cover the downstream processing units which are certified under a different set of rules; another is that the decision should not affect existing certified palm oil purchase and sales contracts which have already been entered into prior to the suspension decision.”

Lee said that since the suspension, IOI has had several discussions with the complainant, conducted a four-day field verification visit with Global Environmental Centre (GEC) – a specialist firm in peat and high conservation value matters – and had started to implement the improvement measures suggested by GEC.

IOI grows and processes palm oil, with some 152,000ha of oil palm plantations in Malaysia and 83,000ha in Indonesia. It is also the largest oleochemical manufacturer in Asia, and has a speciality fats business operated under Loders Croklaan.

The RSPO said it would not comment on IOI’s announcement that it was dropping the lawsuit until the legal case was officially dropped in a conciliatory hearing scheduled for 14 June, the Guardian newspaper said.

Senate scraps palm oil taxOn 12 May, the French Senate scrapped a controversial tax on palm

oil when it adopted a revised version of its biodiversity bill, reports Reuters.

The Senate had earlier approved the €300/tonne palm oil tax on 21 January to encourage sustainable practices in the palm oil sector but the proposal was widely condemned by leading producers, Indonesia and Malaysia.

In March, the National Assembly approved the tax, but sharply reduced its level to start at €30/tonne, and excluded oils produced in a sustainable way (see News, OFI May 2016).

Reuters said the latest version of the biodiversity bill adopted by the Senate scrapped the additional tax on palm oil altogether, with senators saying it could be against international trade rules and that it would be more appropriate in a finance legislation.

However, the decision was not final as the two houses of the French parliament now had to reach an agreement, or the bill would end up at the National Assembly, which had the final word, the report said.

Malaysia and Indonesia have both said the tax is discriminatory, and Indonesia raised the issue at the World Trade Organization in March.

France imports about 100,000 tonnes/year of Indonesian palm oil and bought 11,000 tonnes of Malaysian palm oil last year, Reuters has reported.

June Comment and News.indd 1 13/06/2016 11:12

Ruchi Soya and Adani Wilmar form joint venture in IndiaIndia’s Ruchi Soya and Adani Wilmar

announced on 25 May that they plan to set up a joint venture to tap into the country’s rising food demand and purchasing power.

The joint venture will have the exclusive right to originate, market and distribute finished products from both companies including oilseeds and vegetable oils, derivatives and by-products; soya foods, by-products and all other food products; oleochemicals; biodiesel; grains; and castor oil and derivatives.

Adani Wilmar will own 66.66% of the joint venture and Ruchi Soya the remaining 33.34%.

They said integrating activities would help realise savings in origination, distribution, handling and sales.

Adani Wilmar and Ruchi said the joint venture was conceived looking at India’s complex agricultural environment, where declining farm productivity was occurring in the

face of rising consumption patterns.This mismatch could be partially eased by

optimising and improving the supply chain networks of both groups, they said.

“We are very bullish on Indian demand for high quality food products due to population and economic growth,” said Kuok Khoon Hong, chairman and CEO of Wilmar.

Adani Wilmar is a joint venture between Indian multinational, the Adani Group, and Asian agribusiness giant Wilmar International. It currently owns refineries in 17 locations across India, has eight crushing units and 18 toll packing units, amounting to a refining capacity of over 10,400 tonnes/day, seed crushing capacity of 7,400 tonnes/day and packaging capacity of 9,000 tonnes/day, according to World-Grain.com.

Ruchi Soya is India’s largest manufacturer of edible oils, vanaspati, bakery fats and

soya foods (see company profile, OFI January 2015). According to Ruchi, it has over 6,000 distributors covering 600,000 retail outlets. It has 4.02M tonnes of oilseed extraction capacity in 11 locations; 2.99M tonnes of edible oil refining capacity in 14 locations; 0.52M tonnes of palm fruit processing capacity in two locations; 0.52M tonnes of vanaspati and bakery fats manufacturing capacity in seven locations; and 3.29M tonnes of soya meal production capacity in 11 locations. � In May, Ruchi Soya reported a net loss of Rs 891.29 crore (US$13.35M) for the 2016 year ending on 31 March, compared with a Rs 60.93 crore profit (US$912M) in 2015. “Performance was adversely impacted by sustained pressure in the global commodities market, a weak and erratic monsoon, foreign exchange fluctuations and the overall economic downturn,” the company said.

Molinos Rio de la Plata – one of Argentina’s largest branded food products company – will

invest US$70M to expand its soya operations in San Lorenzo, Santa Fe, Argentina’s cabinet chief Marcos Peña announced at a press conference on 29 April.

The investment would expand storage for soyabeans and meal, enhance cereals operation and increase annual processing to 6M tonnes of oilseeds and 2M tonnes of exports, World-Grain.com said.

The company was also investing an additional US$3.5M in working capital to improve logistics and add space for processing and handling grain exports.

Argentinean officials said the investment was

the result of new government policies designed to promote economic growth in Argentina including the removal of export quotas; the scrapping of export taxes on wheat, corn, soya meal and soya oil exports; a cut in soyabean export taxes; and the floating of the peso.

Work on the San Lorenzo plant would begin in three months and take some two years to complete.

Molinos Río de la Plata is a large exporter of sunflower oil and one of Argentina’s main exporters of bottled oil. It also produces a wide range of packaged foods for domestic consumption including bottled oil, margarine, pasta and frozen foods.

3 OFI – JUNE 2016 www.oilsandfatsinternational.com

NEWS

INDIA: Consumer products giant Hindustan Unilever (HUL) has split its foods and refreshments business into two separate divisions as it faces mounting pressure from established local rivals such as Dabur India, Marico and ITC, Nikkei Asian Review reported on 3 June.

The Indian unit of Anglo-Dutch consumer giant Unilever Plc makes branded products ranging from soaps to ice-creams.

Its foods segment represented its biggest opportunity but was its weakest performer, the report quoted ICICI Securities as saying. Although HUL had strong brands in foods, it had been unable to establish itself in the higher growth segments of packaged food, such as noodles, dairy and biscuits, ICIC said.

LATIN AMERICA: On 1 June, Unilever announced it had agreed to sell its AdeS soya beverage business for US$575M to Coca Cola. The AdeS brand is currently present in Argentina, Bolivia, Brazil, Chile, Colombia Mexico, Paraguay and Uruguay.

USA: Cargill said on 2 May that it has agreed to sell its Dressing, Sauces and Mayonnaise (DSM) business to Ventura Foods, with completion of the transaction expected in the second quarter of 2016. Ventura Foods produces custom and proprietary dressings, sauces, mayonnaises, oils and other flavourings.

IN BRIEF

Singapore’s Olam International announced on 1 June that

it had paid US$24M to buy the remaining 50% stake in Acacia Investments it does not already own with its joint venture partner.

On completion of the acquisition, expected in June, Acacia will become a wholly owned subsidiary of Olam.

Acacia had a significant presence in edible oils refining and distribution in East Africa, Olam said.

“The acquisition allows us to consolidate all our edible oils operations in Mozambique and realise synergies in distribution and brands,” said Olam managing director and CEO of its palm and rubber businesses, Ranveer Chauhan.

Olam supplies ingredients, processed and packaged products including edible nuts, coffee, cocoa, sugar, grains, edible oils and spices, with palm oil plantation interests in Africa.

Olam buys out Africa’s Acacia

New soya crush capacity for ADMArcher Daniels Midland

Company (ADM) announced on 2 June that it had successfully started up new soyabean crushing capacity at its oilseeds plant in Straubing, Germany (pictured) and is now looking at further expanding its soya crushing options at other facilities in northwest Europe.

“The future of crushing soyabeans in Europe looks healthy, and we are looking very closely at where we can best expand crush in Europe,” said Jon Turney, general manager, ADM European soybean crush.

“We see scale, due to the marginal cost per tonne, as a key for our continued success as a destination soya crusher in order to ensure we are able to compete with origin crushers importing meal into the region. Adding switch capability to our plants allows us to utilise our assets more towards the protein markets when EU oil markets are under pressure.”

ADM said Straubing’s new capacity allowed the site to crush soyabeans sourced from the Danube region in order to market European non-GMO soya meal and oil to customers in Western Europe.� In May, ADM released its first quarter 2016 results ending 31 March, reporting “challenging market conditions particularly affecting agricultural services”, which had an operating profit of US$76M, down from US$118M in the same quarter in 2015. Oilseeds operating profit was US$261M, falling US$231M from strong results a year ago.

Molinos to expand soya operations in San Lorenzo

June Comment and News.indd 2 13/06/2016 11:12

NEWS

WORLD: Eleven of the world’s largest food and beverage companies including Kelloggs, Mars, Nestlé and Unilever, have pledged to phase out industrially-produced trans fat by the end of 2018 at the latest.

The members of the International Food & Beverage Alliance (IFBA) said they had agreed a common global objective to reduce trans fatty acids (TFAs) in their products to nutritionally insignificant levels (less than 1g of trans fat per 100g of product) worldwide.

As well as Kellogg, Mars, Nestlé and Unilever, other members of the IFBA are the Coca-Cola Company, Ferrero, General Mills, Grupo Bimbo, McDonald’s, Mondelez International and PepsiCo.

CHINA/BRAZIL: China’s Hunan Dakang Pasture Farming Co Ltd has bought a controlling stake in Brazilian grains company Fiagril Participações SA, the latest effort by Chinese merchants to secure future food supply in Brazil, Reuters reported at the end of April. Sources quoted by the news agency said the Chinese firm bought a 57% stake in Fiagril in a deal worth around US$290M.

Fiagril operates grain trading and processing operations and is based in Mato Grosso state. The deal did not include Fiagril’s shipping, biofuels and seed production units, Reuters said.

USA: TerraVia (formerly Solazyme) and Bunge Ltd announced on 4 May that they are launching a sustainable DHA speciality feed ingredient based on algae targeting the aquaculture market, which currently spends around US$3bn in omega 3 ingredients.

AlgaPrime DHA will be produced at the companies’ joint venture facility in Brazil, where full product scale-up was reached in late 2015.

IN BRIEF EFSA sounds warning on process contaminants in vegetable oils

4 OFI – JUNE 2016 www.oilsandfatsinternational.com

Sustainable palm buyers can help specific producers

Glycerol-based process contaminants found in palm and other vegetable oils, margarines

and some processed foods raise potential health concerns for younger consumers and for people who consume a high amount of these products, the European Food Safety Authority (EFSA) said on 3 May.

The EFSA assessed the health risks of glycidyl fatty acid esters (GE), 3-monochloropropanediol (3-MCPD), and 2-monochloropropanediol (2-MCPD) and their fatty acid esters. The substances form during food processing, particularly when refining vegetable oils at high temperatures of around 200°C.

“The highest levels of GE, as well as 3-MCPD and 2-MCPD (including esters), were found in palm oils and palm fats, followed by other oils and fats,” the EFSA said. “For consumers aged three and above, margarines, pastries and cakes were the main sources of exposure.”

The EFSA’s expert Panel on Contaminants in the

Food Chain (CONTAM) considered information on the toxicity of glycidol (the parent compound of GE), assuming a complete conversion of the esters into glycidol following ingestion.

“There is sufficient evidence that glycidol is genotoxic and carcinogenic, therefore the CONTAM Panel did not set a safe level for GE,” said Dr Helle Knutsen, chair of the CONTAM Panel.

The panel concluded that GE is a potential health concern for all younger age groups with average exposures, and for consumers with high exposure in all age groups. “The exposure to GE of babies consuming solely infant formula is a particular concern,” said Dr Knutsen.

It set a tolerable daily intake (TDI) of 0.8 micrograms per kilogram of body weight per day for 3-MCPD and its fatty acid esters. Toxicological information was too limited to set a safe level for 2-MCPD.

Buyers of palm oil can now choose to support specific,

named producers when purchasing GreenPalm certificates, which now include the name, address and GPS location of the sustainably certified mill trading each certificate, GreenPalm announced on 8 June.

Previously, Roundtable on Sustainable Palm Oil (RSPO)-certified mills submitted their certificates for sale into a collective pot on the GreenPalm

trading platform market. Account names were known, but buyers received no mill transparency

“Now, buyers can select the RSPO-certified grower or mill they wish to support via GreenPalm’s off-market deal facility, or can focus their sustainable sourcing on a particular geographical area,” GreenPalm said.

GreenPalm enables buyers to off-set their purchases of palm oil, palm kernel oil or palm kernel expeller by paying the producer for

an equivalent volume of RSPO-certified material.

“This is currently the only route for some buyers of palm fractions and derivatives to source certified sustainable palm products,” GreenPalm said.

“GreenPalm is also the only practical way to support the estimated 40% of palm producers who cannot export to countries, and certified growers or mills that cannot sell physical material into the segregated supply chain.”

GrainCorp to close crushing siteAustralian oilseed crusher

GrainCorp announced at the end of April that it is shutting down its Riverland Oilseeds canola crushing site at Millicent, South Australia in late September.

The firm said the 100 tonnes/day plant – its smallest canola crushing site – was too far from customers and not big enough.

The announcement comes in the wake of the closure of its Brisbane oil refining and packing plant.

GrainCorp has been restructuring its oils business, spending US$61M to upgrade its new vegetable oil refining, packing and bottling lines for spreads, oils and dressings in Melbourne (see News, OFI May 2016). Work to upgrade its Numurkah plant in northern Victoria to produce refined food

grade canola oil has just finished, and it is building 25% more capacity into the site, which will have a canola crush capacity of 240,000 tonnes/year.

GrainCorp also recently upped crushing capacity at its West Australian oilseed crushing site at Pinjarra to 200 tonnes/day.

“While we are investing to grow our edible oils processing capability in Australia, we are also seeking to maximise our efficiency to keep Australian oils and meals competitive,” general manager of supply chain and operations Doug Belavic said.

GrainCorp acquired the Millicent, Pinjarra and Numurkah plants from vegetable oil crusher and storage company Gardner Smith for US$268M in 2012 as part of a bigger US$361M deal incorporating the purchase of Integro Foods, said The Land.

Commodity giant Glencore is in talks to sell a further

9.9% stake in its agriculture unit, following its agreement to sell a 40% stake to Canada Pension Plan Investment Board (CPPIB) in April, says Reuters.

The report quoted two sources who said Glencore was negotiating with bidders that missed out on the 40% sale.

Bidders for the 9.9% stake – valued at some US$625M – included a Canadian pension fund, state-backed Saudi Agricultural and Livestock Investment Co and Qatar’s sovereign wealth fund, Reuters said.

On 6 April, Glencore confirmed it had sold a 40% stake in its agriculture unit for US$2.5bn to CPPIB (see News, OFI May 2016).

Glencore has been restructuring to reduce its debt.

Glencore may sell a further stake

CORRECTIONIn the March/April issue of OFI, a ‘Brief’ on page 4 on the European Food Safety Authority Panel of Contaminants giving a positive opinion on the use of detoxified jatropha kernel meal in animal feed should have been labelled ‘Europe’, not ‘China’.

June Comment and News.indd 3 13/06/2016 11:12

1-800-366-2563 • www.cpm.net1-651-639-8900 • www.crowniron.com

Together

… we’re your completely integrated preparation system

FlakingCracking Hull SeparationConditioning/Drying

Crown Iron Works is well known for bringing you world-class oilseed preparation systems. But by adding CPM Roskamp Champion’s high-quality equipment to the mix, you have the world’s best and only

integrated preparation system.

Client: Crown Iron Works Publication: OFI Insertion Date: May/June Ad Size: Full Page 4c Bleed Creative: Refining — English

OFI June p05_crown iron works.indd 5 10/06/2016 12:43

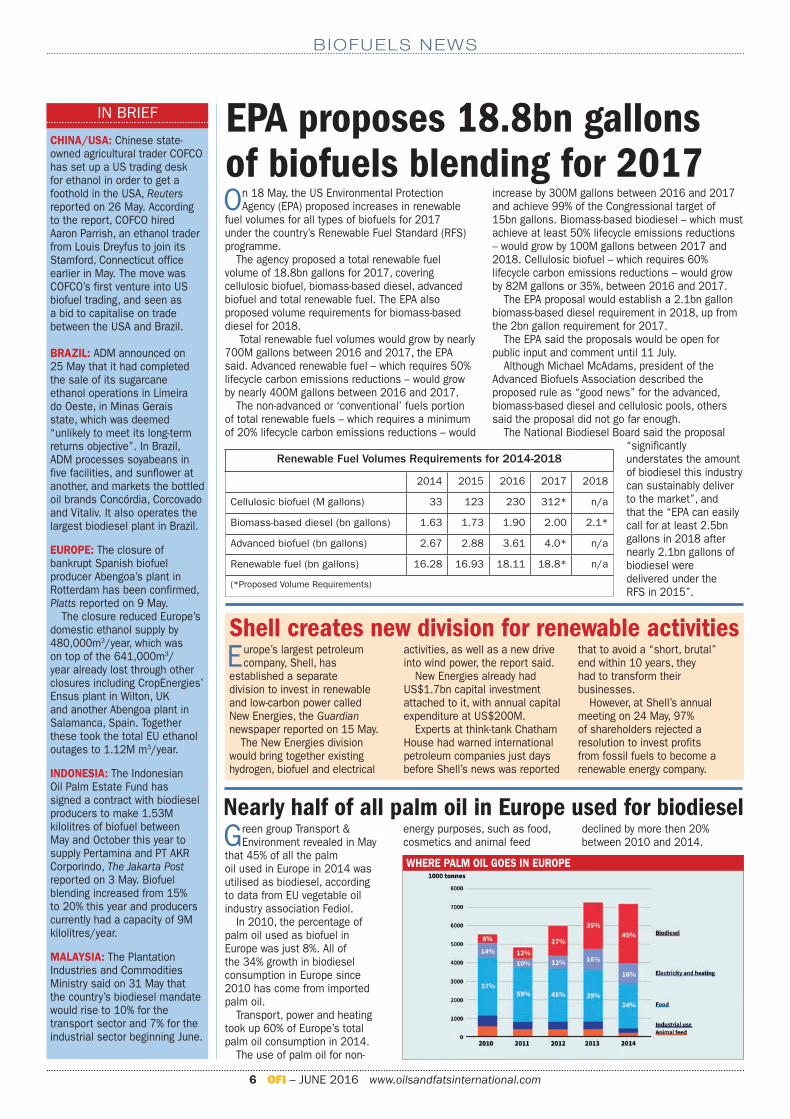

On 18 May, the US Environmental Protection Agency (EPA) proposed increases in renewable

fuel volumes for all types of biofuels for 2017 under the country’s Renewable Fuel Standard (RFS) programme.

The agency proposed a total renewable fuel volume of 18.8bn gallons for 2017, covering cellulosic biofuel, biomass-based diesel, advanced biofuel and total renewable fuel. The EPA also proposed volume requirements for biomass-based diesel for 2018.

Total renewable fuel volumes would grow by nearly 700M gallons between 2016 and 2017, the EPA said. Advanced renewable fuel – which requires 50% lifecycle carbon emissions reductions – would grow by nearly 400M gallons between 2016 and 2017.

The non-advanced or ‘conventional’ fuels portion of total renewable fuels – which requires a minimum of 20% lifecycle carbon emissions reductions – would

increase by 300M gallons between 2016 and 2017 and achieve 99% of the Congressional target of 15bn gallons. Biomass-based biodiesel – which must achieve at least 50% lifecycle emissions reductions – would grow by 100M gallons between 2017 and 2018. Cellulosic biofuel – which requires 60% lifecycle carbon emissions reductions – would grow by 82M gallons or 35%, between 2016 and 2017.

The EPA proposal would establish a 2.1bn gallon biomass-based diesel requirement in 2018, up from the 2bn gallon requirement for 2017.

The EPA said the proposals would be open for public input and comment until 11 July.

Although Michael McAdams, president of the Advanced Biofuels Association described the proposed rule as “good news” for the advanced, biomass-based diesel and cellulosic pools, others said the proposal did not go far enough.

The National Biodiesel Board said the proposal “significantly understates the amount of biodiesel this industry can sustainably deliver to the market”, and that the “EPA can easily call for at least 2.5bn gallons in 2018 after nearly 2.1bn gallons of biodiesel were delivered under the RFS in 2015”.

BIOFUELS NEWS

CHINA/USA: Chinese state-owned agricultural trader COFCO has set up a US trading desk for ethanol in order to get a foothold in the USA, Reuters reported on 26 May. According to the report, COFCO hired Aaron Parrish, an ethanol trader from Louis Dreyfus to join its Stamford, Connecticut office earlier in May. The move was COFCO’s first venture into US biofuel trading, and seen as a bid to capitalise on trade between the USA and Brazil.

BRAZIL: ADM announced on 25 May that it had completed the sale of its sugarcane ethanol operations in Limeira do Oeste, in Minas Gerais state, which was deemed “unlikely to meet its long-term returns objective”. In Brazil, ADM processes soyabeans in five facilities, and sunflower at another, and markets the bottled oil brands Concórdia, Corcovado and Vitaliv. It also operates the largest biodiesel plant in Brazil.

EUROPE: The closure of bankrupt Spanish biofuel producer Abengoa’s plant in Rotterdam has been confirmed, Platts reported on 9 May.

The closure reduced Europe’s domestic ethanol supply by 480,000m3/year, which was on top of the 641,000m3/year already lost through other closures including CropEnergies’ Ensus plant in Wilton, UK and another Abengoa plant in Salamanca, Spain. Together these took the total EU ethanol outages to 1.12M m3/year.

INDONESIA: The Indonesian Oil Palm Estate Fund has signed a contract with biodiesel producers to make 1.53M kilolitres of biofuel between May and October this year to supply Pertamina and PT AKR Corporindo, The Jakarta Post reported on 3 May. Biofuel blending increased from 15% to 20% this year and producers currently had a capacity of 9M kilolitres/year.

MALAYSIA: The Plantation Industries and Commodities Ministry said on 31 May that the country’s biodiesel mandate would rise to 10% for the transport sector and 7% for the industrial sector beginning June.

SOURCE: TRANSPORT & ENVIRONMENT / FEDIOL

IN BRIEF EPA proposes 18.8bn gallons of biofuels blending for 2017

Shell creates new division for renewable activities Europe’s largest petroleum

company, Shell, has established a separate division to invest in renewable and low-carbon power called New Energies, the Guardian newspaper reported on 15 May.

The New Energies division would bring together existing hydrogen, biofuel and electrical

activities, as well as a new drive into wind power, the report said.

New Energies already had US$1.7bn capital investment attached to it, with annual capital expenditure at US$200M.

Experts at think-tank Chatham House had warned international petroleum companies just days before Shell’s news was reported

that to avoid a “short, brutal” end within 10 years, they had to transform their businesses.

However, at Shell’s annual meeting on 24 May, 97% of shareholders rejected a resolution to invest profits from fossil fuels to become a renewable energy company.

6 OFI – JUNE 2016 www.oilsandfatsinternational.com

Renewable Fuel Volumes Requirements for 2014-2018

2014 2015 2016 2017 2018

Cellulosic biofuel (M gallons) 33 123 230 312* n/a

Biomass-based diesel (bn gallons) 1.63 1.73 1.90 2.00 2.1*

Advanced biofuel (bn gallons) 2.67 2.88 3.61 4.0* n/a

Renewable fuel (bn gallons) 16.28 16.93 18.11 18.8* n/a

(*Proposed Volume Requirements)

Green group Transport & Environment revealed in May

that 45% of all the palm oil used in Europe in 2014 was utilised as biodiesel, according to data from EU vegetable oil industry association Fediol.

In 2010, the percentage of palm oil used as biofuel in Europe was just 8%. All of the 34% growth in biodiesel consumption in Europe since 2010 has come from imported palm oil.

Transport, power and heating took up 60% of Europe’s total palm oil consumption in 2014.

The use of palm oil for non-

energy purposes, such as food, cosmetics and animal feed

declined by more then 20% between 2010 and 2014.

Nearly half of all palm oil in Europe used for biodiesel

WHERE PALM OIL GOES IN EUROPE

June Biofuel News.indd 1 13/06/2016 11:55

BIOFUELS NEWS

7 OFI – JUNE 2016 www.oilsandfatsinternational.com

Sofiproteol cuts back biodiesel productionDue to lower than expected demand,

France’s Avril Sofipreteol announced on 21 April that it would cut its biodiesel production this year, says Biofuels Digest.

Demand was expected to be 928,000 tonnes this year, compared to 1.5M tonnes last year, with the fall in demand was attributed to a several factors, including higher rapeseed prices, instability in the demand structure from unstable EU biodiesel blending policies, competitive drop-in biomass-based fuels and overcapacity in the EU biodiesel market, Biofuels Digest said.

Court annuls EU’s anti-dumping duty on US ethanolThe European Court of Justice

(ECJ) has annulled the European Union’s (EU) 9.5% anti-dumping duty on all ethanol imported from the USA, which has been in place since February 2013.

The decision affects imports by four US producers: Patriot Renewable Fuels, Plymouth Energy, Poet and Platinum Ethanol, according to Reuters.

The ECJ ruled on 9 June that the anti-dumping duty of US$83.03/tonne was invalid because the European Commission (EC) was required by EU law to give each sampled US company its own anti-dumping rate, Biofuels International said.

“It found that the EU should have imposed individual dumping duties for these producers instead of applying a general country-wide

duty,” said ePure, the European renewable ethanol association.

In May 2013, the US Renewable Fuels Association (RFA) and Growth Energy filed a joint complaint against the duty, citing 10 violations of established trade law.

Biofuels International said that before the duty was imposed, the EU had represented a 300M gallon market for the US ethanol

industry.The EU now has approximately

two months to file an appeal against the ruling.� The EU filed an appeal on 20 May against the World Trade Organization’s (WTO) March ruling in favour of Argentina over the EU’s anti-dumping duties on biodiesel imports from the country (see also Biofuels News, OFI May 2016).

EC refers Poland to EU Court of Justice over REDThe European Commission (EC) has referred

Poland to the EU Court of Justice for failing to fully comply with the EU Renewable Energy Directive (RED), according to an EC press release.

“Firstly, fuels can only be marketed if specific fuel requirements are in place but such requirements do not exist for hydrotreated vegetable oil (HVO), a biofuel imported into Poland,” it said.

“Secondly, preferential treatment is given to fuel operators who source at least 70% of their biofuels from Polish manufacturers and when the biofuels are produced predominantly from raw materials originating in certain countries.”

The RED requires all member states

to ensure that at least 10% of all energy consumed in transport comes from renewable sources. Biofuels can be used to meet this target but must meet the REC’s sustainability requirements.

Member states must also treat sustainable biofuels and their raw materials equally, regardless of their origin.

The EC said it had sent Poland a letter of formal notice in February 2014 over its concerns, followed by a reasoned opinion in April. “However, the Polish authorities have still not completely addressed the EC’s concerns. Therefore the Commission deems it necessary to refer the case to the Court of Justice.”

Dupps Pressor with HCPR yields up to 50 kg more high-value fat every hour.

Lower your fat residuals. Learn how at www.dupps.com or (937) 855-6555.The Dupps Company • Germantown, OH • U.S.A.

• You can’t afford excess residual fat. A Dupps Pressor® screw press with the new Hybrid HCPR (High Compression Press Release) shaft can dramatically lower residuals in most rendered products.

• HCPR combines high compression with a release/re-compression feature — just like squeezing a sponge twice releases more moisture, the HCPR shaft compresses material twice to release more fat.

• In many cases, the HCPR Shaft can be retrofitted to your existing Pressors.

Extract more fat

June Biofuel News.indd 2 13/06/2016 11:55

Report withdrawn

Monsanto rejects Bayer’s US$62bn bid

8 OFI – JUNE 2016 www.oilsandfatsinternational.com

BIOTECH NEWS

The world’s largest seed company, Monsanto Co, has turned down a US$62bn

acquisition offer from German chemical and pharmaceutical multinational Bayer AG on 24 May, saying it was “incomplete and financially inadequate”, Reuters reports.

A deal would have created the world’s largest supplier of seeds and farm chemicals.

Monsanto chief executive Hugh Grant said “the current proposal significantly undervalues our company and also does not adequately address or provide reassurance for some of the potential financing and regulatory

execution risks relating to the acquisition”.Bayer said it looked forward to engaging

in constructive discussions with Monsanto, which said it was open to engage in further negotiations.

A Monsanto-Bayer combination was unlikely to raise significant anti-trust hurdles because there was little overlap in the companies’ products, analysts said in a Bloomberg report.

Monsanto owns the Roundup brand herbicide, while Bayer CropScience has products in crop protection, seeds and plant biotechnology.

The crop chemicals industry has recently experienced a wave of consolidation, with Dow Chemical merging with DuPont, and China National Chemical Corp bidding US$43bn in February to acquire Syngenta AG. Monsanto’s US$45bn bid for Syngenta failed last year.

With a global slump in agricultural commodities hurting demand for products, a deal with Bayer would help Monsanto reduce its reliance on the agriculture industry, while Monsanto would strengthen Bayer’s seed business, one of the company’s priorities, the Bloomberg report said.

WORLD: BASF’s Crop Protection division announced it had put into operation a new R&D centre at its headquarters in Limburgerhof, Germany, on 21 April. The centre will house two research areas – biological crop protection and seed solutions. In February, BASF had announced it would be halving the 700 jobs at its plant biotechnology research unit – 140 in North American and 180 in Europe.

Research and field sites in Belgium, Brazil, Germany, and the USA would be reduced in size and field testing sites in Hawaii, India and Puerto Rico would be closed, with restructuring expected to be completed by the end of this year. Plant biotech research would focus on high potential projects in herbicide tolerance and fungal resistant soyabean. The project on polyunsaturated omega-3 fatty acids in canola seeds would be continued; and yield and stress collaboration agreement with Monsanto on corn and soyabeans was not affected. However, rice yield and corn fungal resistance projects would be discontinued.

BRAZIL: US biotech company Ceres Inc announced on 2 May that it had received approval to field-test its biotech sugarcane in Brazil, with trials expected to start by mid-June.

Ceres will test biomass, sugar yield and stress tolerant traits in several commercial sugarcane cultivars adapted to Brazil’s major production areas. It said in similar trials performed outside Brazil last year, plants with drought resistant traits maintained biomass yields with half the water usually required.

IN BRIEF

Concern over import of GM soya The Soybean Processors

Association of India (SOPA) has urged the government to investigate the possible import of GM soyabeans into India which may be breaking plant quarantine and environmental regulations, reports the Financial Express.

“It has come to our knowledge that soyabean is being imported into India from various countries,” D N Pathak, SOPA executive director, wrote in a 6 May letter to the Union Minister for Environment, Forest and Climate Change. “We request immediate investigation into all soyabean imports to ensure that plant quarantine and environmental regulations are strictly followed.”

The Financial Express said separate regulations governed the import of soyabean seeds for sowing and for consumption or processing. The import of GM food

items also required approval from the Genetic Engineering Appraisal Committee (GEAC).

“To the best of our knowledge, none of the plant quarantine conditions has been fulfilled by the importers and approval of GEAC has also not been obtained for the import of any GM soyabean,” Pathak wrote.

Currently, Bt cotton is the only GM crop approved for commercial cultivation in India.

Last August, GEAC authorised field trials of GM rice, mustard, chickpea and brinjal, the Solvent Extractors’ Association (SEA) said in its February newsletter.

However, in February, GEAC deferred a decision on the cultivation of a GM hybrid mustard, the Indian Express said. It was holding public consultations and the hybrid was due back at GEAC for approval by the end of May.

Monsanto will not launch new seeds in ArgentinaMonsanto has cancelled plans to launch new

biotech soyabeans in Argentina and may withdraw other seeds already sold there in an escalation of its dispute over royalty payments for its seed, the Wall Street Journal (WSJ) reported on 17 May.

The US biotech giant argues that royalty collection is essential to make a profit and under its terms of use for its seeds, known as Intacta Soy, farmers have to pay royalties when purchasing the seed or when selling their crop to grain elevators and export terminals. A clause allows Monsanto to inspect shipments for the presence of its Intacta technology to assess royalty charges, which farmers, traders and exporters have branded illegal.

In April, President Mauricio Macri’s Agricultural Ministry banned all tests on grain shipments without prior government approval and its request for more time to push farmers to pay royalties was rejected by Monsanto.

Monsanto now says it will not launch new soyabeans in Argentina, called Roundup Ready 2 Xtend, which are engineered to resist a more

powerful weedkiller and which it had planned to begin selling in October.

It will continue selling Intacta RR2 seeds, engineered to withstand glyphosate herbicide and repel worms, but is considering its position in the country.

“We are doing a full review of our business plans there,” Michael Frank, chief commercial officer for Monsanto, told an investor conference, according to a WSJ report on 10 May. “We will be very diligent in our efforts to secure our investments and intellectual property there.”

The newspaper said Argentina was one of the biggest overseas markets for US agricultural firms, growing about 13.6% of the world’s GM crops last year. Its purchases of seeds and pesticides generated about 5.8% of Monsanto’s US$15bn in sales in fiscal year 2015.

Monsanto has also threatened to leave India over royalty disputes that it, and its local partner, Maharashtra Hybrid Seeds Co (Mahyco) are able to charge for biotech cotton seed royalties (see Biotech News, OFI May 2016).

The US Environmental Protection Agency (EPA) published a

report on 29 April concluding that the weedkiller glyphosate is “not likely to be carcinogenic to humans” but then pulled the report offline just three days later.

The report from the EPA’s cancer assessment review committee was published on the regulations.gov website the EPA manages but was taken down on 2 May, Reuters said.

The EPA said the documents were “preliminary” and were part of its broader review of glyphosate and its potential human health and environmental risks, which was due to be completed by the end of 2016, Reuters reported.

Glyphosate is found in herbicides widely used with GM crops which the World Health Organization last year said was a probable human carcinogen.

Biotech News June.indd 1 09/06/2016 12:50

OFI June p09_lipico.indd 9 10/06/2016 12:48

USA: Leading North American biofuels producer Renewable Energy Group (REG) is expanding its storage capacity for feedstock and biodiesel with its recent US$1.5M purchase of an adjacent Bunge Milling tank complex facility, the company announced on 2 May.

The tanks were being connected to REG Danville’s existing infrastructure and would increase the biorefinery’s storage capacity for feedstock by at least 950,000 gallons and biodiesel by up to 12M gallons.

In July 2015, REG began a separate US$31M upgrade at its multi-feedstock 45M gallon capacity Danville biorefinery to optimise storage and logistics, and add biodiesel distillation capabilities. The upgrade is due to be completed later this year.

CANADA: Grain shippers and farm groups are calling for the extension of emergency regulations enacted by the government in response to major grain transportation bottlenecking during the winter of 2013/14, which are due to expire on 1 August, reports Oilseed & Grain News.

Bill C-30 includes an increase of railway interswitching from 30km of an interchange to 160km. Interswitching is a commercial agreement between railway companies whereby one railway company will carry traffic for the other to ensure that captive shippers (shippers with only one choice of railway) have fair and reasonable access to the rail system at a regulated rate. The Canadian National and Canadian Pacific railways have opposed the legislation since its passing.

IN BRIEF Louis Dreyfus seeks investmentin port logistics in Middle EastGlobal commodity trading group

Louis Dreyfus Company is looking to invest in port logistics in the Middle East, especially Egypt, as the sector continues to lag behind market growth, reports Hellenic Shipping News.

“The markets are growing and in most cases the ports remain largely governmental and have probably been a little bit slower to move than the private sector,” James Wild, head of Louis Dreyfus Middle East and East Africa, told Reuters.

Wild said his company also saw opportunities in Saudi Arabia as the country sought to privatise its grain operations and in post-sanctions Iran.

“We see opportunities with

certain countries opening up both from a sanctions perspective like Iran and also from potentially a privatisation programme with Saudi Arabia, both of which provide volume which is important for us,” he said on the sidelines of the May Global Grain conference in Dubai.

Wild added that it was too early to tell whether Louis Dreyfus would actively seek a stake in the Saudi Grains Organization (SAGO), which was looking to sell a stake to a strategic buyer as part of its privatisation.

Saudi Arabia was considering privatising various state bodies under its Vision 2030 economic reform plan announced in April, aimed at reducing the kingdom’s

reliance on oil, the report said.Louis Dreyfus – in the midst of

a leaership shake-up – announced a reduction in its board size from seven to five on 19 May, with former CEO Serge Schoen and former Goldman Sachs managing director Steven Wirsch stepping down, Reuters reported.

Like other commodity traders, Louis Dreyfus was now grappling with ample supply, lower prices and slower economic growth that had cut margins and prompted firms to refocus, Reuters said.

In March, Louis Dreyfus reported net profit dropping 67% to US$211M last year, and it confirmed it was seeking partners to help some of its businesses expand.

Richardson capacity expansion Leading Canadian agribusiness Richardson International Limited

says it has nearly doubled the storage and receiving capacity of its export terminal in North Vancouver following the successful completion of a US$140M expansion project.

Richardson added an 80,000 tonne grain storage annex to its terminal, increasing storage capacity to 178,000 tonnes, and also upgraded its rail yard and receiving system.

“The terminal now has the ability to handle in excess of 6M tonnes/year to meet growing demand for Canadian grains and oilseeds,” it said.

Expansion work began in September 2013 and concluded earlier this year. Richardson said that despite the construction, the terminal managed to set a new handling record, shipping 5.2M tonnes of grain in 2015, against a typical year of 3M tonnes.

“Our Vancouver expansion was a significant investment to ensure we have the appropriate capacity on the West Coast,” said Curt Vossen, president and CEO of Richardson International. “We have positioned ourselves globally to efficiently move Canadian grains and oilseeds to emerging markets in Asia-Pacific and other areas.”

Richardson is a worldwide handler and merchandiser of all major Canadian-grown grains and oilseeds and a vertically-integrated processor and manufacturer of oats and canola-based products.

10 OFI – JUNE 2016 www.oilsandfatsinternational.com

TRANSPORT & LOGISTICS NEWS

Van den Bosch completes joint venture with Aspen InternationalGlobal logistics provider Van den Bosch

has concluded a joint venture with South Africa’s Aspen International (pictured), opening two new sites in Cape Town and Dubai, the company announced on 12 May.

“The main focus is on shipping liquid bulk products (food as well as chemicals) in tank containers in cooperation with Van den Bosch DMCC in Dubai,” the firms said. “The business includes shipping liquid bulk products in flexitanks, palletised dry goods in 6m and 12m general purpose containers, and perishable goods in reefer tanks and containers.”

Director Peter van den Bosch said the

cooperation was another new step ahead in the African market. “We believe in Africa’s potential and want to further develop this growth market. We have built a strong network in the past few years and we are now shipping various liquid bulk goods from, to and in Africa.”

The Dutch Van den Bosch group is active in the European oils and fats market, acting as a bulk supply chain partner for refiners such as IOI, Cargill, and Sime Darby (see OFI Transport & Logistics News, Nov/Dec 2015). It said the African continent offered many opportunities in loading edible oils and fats and volumes between Europe and Africa were growing.

New Ukraine tank farm for palm oil Ukrainian bulk liquid edible

products terminal LLC NE Terminal UPSS is planning to put a new 41,000 tonnes tank farm into operation this year to handle imported palm oil, reports APK Inform.

The company is located in Mykolayiv, southern Ukraine, at the deep-sea port of Dnepro-Bugskiy.

The port complex handles a range of cargoes including vegetable oils, molasses, palm oil, ethanol, glycerine, meal and cake, offering transshipment of bulk food cargoes and exports of molasses and vegetable oils.

It has a total storage volume of 143,000m3 with five terminals, each with a storage capacity of 25,000-40,0000 tonnes, separate pumping house and pipelines.

June Transport News.indd 1 14/06/2016 11:31

11 OFI – JUNE 2016 www.oilsandfatsinternational.com

GekaKonus GmbH · Siemensstraße 10 · D-76344 Eggenstein-Leopoldshafen Tel.: +49 (0) 721 / 9 43 74 -0 · Fax: +49 (0) 7 21/ 9 43 74 - 44 · [email protected] · www.gekakonus.net

Steam for high quality edible oil production.

Services by GekaKonus:

Engineering Design

Consulting Commissioning

After Sales Service Our experience is your advantage.

MORE THAN ENERGY

Anzeige_OFI_128x185_mm_A_01_B.indd 1 12.05.16 16:00

oilRoq GmbH has experience of 30 years in hydrogenaon plants,

interesterificaon plants and esterificaon plants.

For all customers who are interested in oil and fat modificaon:

We offer special design for dedicated applicaons like reactors,

heat exchangers and sinter metal filters.

oilRoq GmbH—Pfännerhöhe 35—D 06110 Halle—Germany—Phone: +49-345-68578071– Fax: +49-345-68578077 www.oilRoq.eu

OFI June p11_geka-&-oil roq.indd 11 10/06/2016 13:05

USA: Procter & Gamble announced on 19 May that it had launched its first bio-based detergent, Tide purclean, which it says has a 65% bio-based formula. It said the detergent was produced at a zero manufacturing waste to landfill site using 100% renewable wind power electricity and a bottle that was also 100% recyclable. The detergent will carry the USDA Certified Biobased label. CANADA/USA: Canada’s S2G Biochemicals announced on 18 April that it had begun commercial-scale production of bio-based glycols at the Memphis site of its operating partner, Pennakem LLC.

S2G’s bio-refining process was integrated into Pennakem’s existing chemical facility to convert non-food waste into usable sugar-based glycols.

“The glycols will serve as a drop-in replacement for common petroleum-based chemicals used in a wide range of consumer and industrial products such as resins, PET/PEF plastic drink containers, cosmetics, pharmaceuticals, coolants and antifreeze,” S2G said. “The economical advantages of integrating our technology into existing facilities will have a significant impact on the business case of bio-based glycols,” S2G CEO Mark Kirby added.

IN BRIEF

Amyris in venture with South Korea’s CJ

12 OFI – JUNE 2016 www.oilsandfatsinternational.com

RENEWABLE MATERIALS NEWS

Ford developing CO2-based foam and plastics

US industrial bioscience firm Amyris Inc and South Korea-based CJ CheilJedang

Corporation (CJ) announced on 20 May that they had signed an agreement to support large-scale manufacturing of Amyris’s renewable farnesene in existing CJ facilities.

CJ is a Korean-based food, feed and bioscience company and the agreement would allow Amyris to utilise CJ’s manufacturing capacity to support projected demand for products using farnesene.

“The partnership is also expected to include the opportunity for CJ Bio (a division of CJ) to market Amyris products in Asian markets as well as the potential for Amyris to develop several products for CJ Bio,” Amyris said in a press release.

The companies are aiming to complete their agreement by August.

Farnesene is a long-chain, branched hydrocarbon molecule produced by Amyris from the conversion of plant sugars. It has

applications in speciality and performance chemicals, fragrance ingredients, cosmetic emollients, polymers and solvents.

In March, Amyris had said that expected demand for farnesene was beyond the company’s current capacity at its Brotas industrial fermentation complex in Brazil.

It announced an expansion project, expected to start later this year, to add a dedicated flavours and fragrances manufacturing unit to Brotas to meet contracted demand for its flavours and fragrances molecules.

The expansion would allow current Brotas capacity to supply Amyris’s farnesene in the polymers, nutraceuticals and solvents markets through 2020.

Amyris said it entered 2016 with key customer commitments in place which represented a “substantial percentage” of planned production volume at Brotas.

“During the fourth quarter of 2015, Amyris started shipping farnesene for the commercial

production of tyres, adhesives, nutraceuticals and solvents,” it said.

“These applications are expected to consume the full production of Brotas in 2016 and keep the plant capacity sold out through 2020, including the added capacity as a result of the dedicated flavors and fragrances industrial production unit.”

Amyris said its first food ingredients collaboration was successfully underway with plans to begin producing a large-market product for this customer in 2017.

It expects existing collaboration and supply agreements to generate over US$200M in revenue through 2020 from its flavours and fragrances partners (including the five largest fragrance houses in the world) and other industry leading companies.

In January, it announced its first multi-million dollar agreement supplying farnesene to an undisclosed nutraceuticals manfacturer (see Renewable News, OFI March/April 2016).

Ford Motor Company is developing and testing new foam and plastic components using carbon dioxide

as a feedstock which researchers hope to see in Ford production vehicles within five years, reports Green Car Congress.

“Formulated with up to 50% CO2-based polyols, the foam is showing promise as it meets rigorous automotive test standards,” the 16 May report said.

“It could be employed in seating and underhood applications. CO2-derived foam will further reduce the use of fossil fuels in Ford vehicles and increase the presence of sustainable foam in the automaker’s global lineup.”

Ford began working with several companies, suppliers and universities in 2013 to find applications for captured CO2,” Green Car Congress said. This included US-based Novomer, which is commercialising a proprietary catalyst system that transforms waste

CO2 into polymers for a variety of applications, including foam and plastic, which contain up to 50% CO2 by mass.

The report said features of the Novomer catalyst included a moderate CO2-epoxide reaction, occurring at 35°–50°C temperature and 200-300 psi pressure; a fast reaction time at more than 300 times more active than previous systems developed to synthesise aliphatic polycarbonates; and a low catalyst cost that does not use precious metals.

Ford said that it had developed sustainable materials for its products for nearly two decades.

“In North America, soya foam is in every Ford vehicle. Coconut fibre backs trunk liners; recycled tyres and soya are in mirror gaskets; recycled T-shirts and denim go into carpeting; and recycled plastic bottles become Repreve fabric used in the 2016 F-150.”

Cargill acquires NatureWax from Elevance Cargill announced on

16 April that it had acquired NatureWax, a market-leading provider of natural, vegetable-based waxes, to help premium candle makers in North America meet the growing demand for cleaner, non-petroleum-based wax blends.

Cargill is buying NatureWax back from Elevance Renewable Sciences Inc after selling it to the company in 2007.

“As full owner of NatureWax, Cargill will use its global supply chain management strengths and its technical innovation capabilities to provide waxes superior to petroleum-based paraffin alternatives,” the

company said in a press release. “Vegetable-based waxes are

gaining in popularity because they burn cleaner and longer, and

because it is easier to imbue them with fragrances.”

Cargill said that going forward, Elevance would focus its efforts on developing its growing metathesis products business, a technology that creates chemical intermediates from vegetable-based feedstocks more economically than traditional methods.

Cargill supplies vegetable-derived, bio-based industrial products, including personal care products, dielectric fluid, lubricants, detergents, agrichemicals, asphalt and CASE (coatings, adhesives, elastomers, sealants), flexible foams, paints, inks and coatings.

PHOT

O: A

DOBE

STO

CK

June Renewable News.indd 1 14/06/2016 11:29

Celite®

Cynersorb

www.imerys-perfmins.com

OFI June p13_imerys.indd 13 13/06/2016 15:09

DIARY OF EVENTS

14 OFI – JUNE 2016 www.oilsandfatsinternational.com

4-9 SEPTEMBER 2016FOSFA Basic Introductory CourseVENUE: Royal Holloway, University of London Egham, Surrey, UKCONTACT: Anna Baran, FOSFA InternationalUK. Tel: +44 20 7283 5511E-mail: [email protected]: www.fosfa.org/events/middle-managers-course/

20-22 SEPTEMBER 20169th Biofuels International ConferenceVENUE: Ghent, BelgiumCONTACT: Tracy Whitehead, Biofuels International, UKTel: +44 20 8687 4138E-mail: [email protected]: www.biofuels-news.com/conference

19-21 OCTOBER 2016OFIC 2016VENUE: Hotel Istana, Kuala Lumpur, MalaysiaCONTACT: OFIC 2016 Secretariat, c/o MOSTA Malaysia. Tel: +603 7118 2062/2064E-mail: [email protected]: www.mosta.org.my

21-22 OCTOBER 2016PORAM Annual Forum, Dinner, Golf ChallengeLOCATION: One World Hotel, Bandar Utama Selangor Darul Ehsan, Malaysia CONTACT: PORAM, Malaysia. Tel: +603 7492 0006; E-mail: [email protected]: http://poram.org.my/p/wp-content/uploads/2014/01/PORAM-annual-event-A4-2016.pdf

10 NOVEMBER 2016FOSFA Annual DinnerVENUE: Battersea Evolution, London, UKCONTACT: Gemma Hale, FOSFA, UKTel: +44 20 7283 5511E-mail: [email protected]: www.fosfa.org

14-16 NOVEMBER 2016Oilseed and Grain Trade Summit/Organic & Non-GMO ForumVENUE: Hyatt Regency Hotel, Minneapolis, USACONTACT: Sule Basa, HighQuest Partners, USAE-mail: [email protected]: www.oilseedandgraintrade.com orwww.ongforum.org

7 SEPTEMBER 20164th International Conference on “Black Sea Oil Trade”VENUE: Hilton Kyiv Hotel, UkraineCONTACT: Julia Feofilova, UkrAgroConsult Ukraine. Tel: +38 44 4514637E-mail: [email protected]: http://bso.blackseagrainconference.com/en

15 SEPTEMBER 2016High-Oleic Market: Evolution of DevelopmentVENUE: Hotel Alfavito, Kiev, UkraineCONTACT: APK-Inform, UkraineTel: +380 562 320 795, +380 562 321 595E-mail: [email protected]: www.apk-inform.com/en/conferences/sunflower2016/about

12-13 OCTOBER 2016Malaysian Palm Oil Trade Fair & SeminarVENUE: Kuala Lumpur, MalaysiaCONTACT: Mohd Izham Hassan, Malaysia Palm Oil Council. E-mail: [email protected] or [email protected]; Website: www.mpoc.org.my/Palm_Oil_Trade_Fair_and_Seminar_(POTS)_2016_Announcement.aspx

7-10 NOVEMBER 201619th Annual FO Lichts World Ethanol & BiofuelsVENUE: Steigenberger Wiltcher’s Hotel Brussels, BelgiumCONTACT: Informa Agra Customer Services, UKTel: +44 20 3377 3658E-mail: [email protected]: www.worldethanolandbiofuel.com

21-23 SEPTEMBER 2016Globoil 2016 VENUE: Grand Hyatt, Goa, IndiaCONTACT: Tefla’s, IndiaTel: +91 22-26304816/17Email: [email protected]/[email protected]: www.globoilindia.com

28-29 SEPTEMBER 20167th International Oilseeds & Oils 2016VENUE: Barcelona, SpainCONTACT: APK-Inform, UkraineTel: +380 562 320 795, +380 562 321 595 E-mail: [email protected]: www.apk-inform.com/en/conferences/oo2016/about

17-21 OCTOBER 2016National Renderers Association (NRA) 83rd Annual ConventionVENUE: The Ritz-Carlton Amelia Island, Florida USA. CONTACT: NRA, USA. Tel: +1 703 6830 155E-mail: [email protected]: www.nationalrenderers.org

6-8 SEPTEMBER 20163rd High Oleic Oils CongressVENUE: Toulouse, FranceCONTACT: FAT & Associés, FranceTel: +33 567 339 206; Fax: +33 567 339 203Website: www.higholeicmarket.com/hoc-2016

18-21 SEPTEMBER 201614th Eurofedlipid CongressVENUE: International Convention Center (ICC) Ghent, BelgiumCONTACT: Eurofedlipid, GermanyTel: +49 69/79 17533Fax: +49 69/79 17564E-mail: [email protected]: www.eurofedlipid.org/meetings/ghent2016/

For a full listing of oils and fats industry events,

go to: www.ofimagazine.com

26-29 JUNE 20166th International Conference on Algal Biomass, Biofuels & BioproductsVENUE: San Diego, USACONTACT: Elsevier ConferencesUK ; Tel: +44 1865 843 337E-mail: [email protected]: www.algalbbb.com

3-8 JULY 201622nd International Symposium on Plant LipidsVENUE: Paulinerkirche, Göttingen, GermanyCONTACT: Euroefedlipid, GermanyTel: +49 69/79 17533E-mail: [email protected]: www.eurofedlipid.org/meetings/goettingen2016/index.php

13-14 JULY 201613th Oleochem Outlook 2016VENUE: Chengdu, China CONTACT: Cris Zhou, Enmore GroupTel: +86 21 5155 0927E-mail: [email protected]: www.enmore.com

9-10 AUGUST 2016Malaysia-China Palm Oil Trade Fair & Seminar (POTS) VENUE: Tianjin, ChinaCONTACT: Lim Teck Chaii, Malaysian Palm Oil Council; [email protected] or Desmond Ng, E-mail: [email protected]: www.mpoc.org.my/Palm_Oil_Trade_Fair_and_Seminar_(POTS)_2016_Announcement.aspx

18-19 AUGUST 2016Palmex Thailand VENUE: CO-OP Exhibition Centre, Surat Thani ThailandCONTACT: Fireworks Media (Thailand) Co LtdTel: +66 2513 1418; Fax: +66 2513 1419E-mail: [email protected]: www.thaipalmoil.com

June diary 1 page.indd 1 14/06/2016 11:33

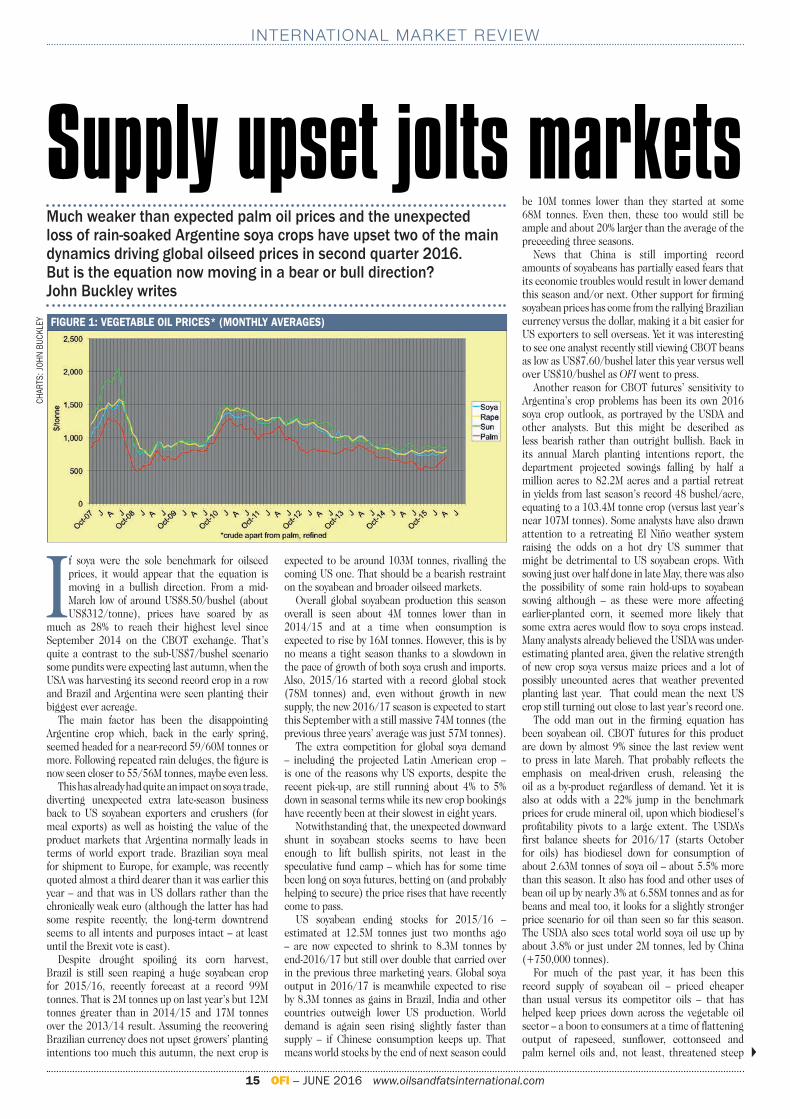

Supply upset jolts marketsMuch weaker than expected palm oil prices and the unexpected loss of rain-soaked Argentine soya crops have upset two of the main dynamics driving global oilseed prices in second quarter 2016. But is the equation now moving in a bear or bull direction? John Buckley writes

INTERNATIONAL MARKET REVIEW

15 OFI – JUNE 2016 www.oilsandfatsinternational.com

If soya were the sole benchmark for oilseed prices, it would appear that the equation is moving in a bullish direction. From a mid-March low of around US$8.50/bushel (about US$312/tonne), prices have soared by as

much as 28% to reach their highest level since September 2014 on the CBOT exchange. That’s quite a contrast to the sub-US$7/bushel scenario some pundits were expecting last autumn, when the USA was harvesting its second record crop in a row and Brazil and Argentina were seen planting their biggest ever acreage.

The main factor has been the disappointing Argentine crop which, back in the early spring, seemed headed for a near-record 59/60M tonnes or more. Following repeated rain deluges, the figure is now seen closer to 55/56M tonnes, maybe even less.

This has already had quite an impact on soya trade, diverting unexpected extra late-season business back to US soyabean exporters and crushers (for meal exports) as well as hoisting the value of the product markets that Argentina normally leads in terms of world export trade. Brazilian soya meal for shipment to Europe, for example, was recently quoted almost a third dearer than it was earlier this year – and that was in US dollars rather than the chronically weak euro (although the latter has had some respite recently, the long-term downtrend seems to all intents and purposes intact – at least until the Brexit vote is cast).

Despite drought spoiling its corn harvest, Brazil is still seen reaping a huge soyabean crop for 2015/16, recently forecast at a record 99M tonnes. That is 2M tonnes up on last year’s but 12M tonnes greater than in 2014/15 and 17M tonnes over the 2013/14 result. Assuming the recovering Brazilian currency does not upset growers’ planting intentions too much this autumn, the next crop is

expected to be around 103M tonnes, rivalling the coming US one. That should be a bearish restraint on the soyabean and broader oilseed markets.

Overall global soyabean production this season overall is seen about 4M tonnes lower than in 2014/15 and at a time when consumption is expected to rise by 16M tonnes. However, this is by no means a tight season thanks to a slowdown in the pace of growth of both soya crush and imports. Also, 2015/16 started with a record global stock (78M tonnes) and, even without growth in new supply, the new 2016/17 season is expected to start this September with a still massive 74M tonnes (the previous three years’ average was just 57M tonnes).

The extra competition for global soya demand – including the projected Latin American crop – is one of the reasons why US exports, despite the recent pick-up, are still running about 4% to 5% down in seasonal terms while its new crop bookings have recently been at their slowest in eight years.

Notwithstanding that, the unexpected downward shunt in soyabean stocks seems to have been enough to lift bullish spirits, not least in the speculative fund camp – which has for some time been long on soya futures, betting on (and probably helping to secure) the price rises that have recently come to pass.

US soyabean ending stocks for 2015/16 – estimated at 12.5M tonnes just two months ago – are now expected to shrink to 8.3M tonnes by end-2016/17 but still over double that carried over in the previous three marketing years. Global soya output in 2016/17 is meanwhile expected to rise by 8.3M tonnes as gains in Brazil, India and other countries outweigh lower US production. World demand is again seen rising slightly faster than supply – if Chinese consumption keeps up. That means world stocks by the end of next season could

be 10M tonnes lower than they started at some 68M tonnes. Even then, these too would still be ample and about 20% larger than the average of the preceeding three seasons.

News that China is still importing record amounts of soyabeans has partially eased fears that its economic troubles would result in lower demand this season and/or next. Other support for firming soyabean prices has come from the rallying Brazilian currency versus the dollar, making it a bit easier for US exporters to sell overseas. Yet it was interesting to see one analyst recently still viewing CBOT beans as low as US$7.60/bushel later this year versus well over US$10/bushel as OFI went to press.

Another reason for CBOT futures’ sensitivity to Argentina’s crop problems has been its own 2016 soya crop outlook, as portrayed by the USDA and other analysts. But this might be described as less bearish rather than outright bullish. Back in its annual March planting intentions report, the department projected sowings falling by half a million acres to 82.2M acres and a partial retreat in yields from last season’s record 48 bushel/acre, equating to a 103.4M tonne crop (versus last year’s near 107M tonnes). Some analysts have also drawn attention to a retreating El Niño weather system raising the odds on a hot dry US summer that might be detrimental to US soyabean crops. With sowing just over half done in late May, there was also the possibility of some rain hold-ups to soyabean sowing although – as these were more affecting earlier-planted corn, it seemed more likely that some extra acres would flow to soya crops instead. Many analysts already believed the USDA was under-estimating planted area, given the relative strength of new crop soya versus maize prices and a lot of possibly uncounted acres that weather prevented planting last year. That could mean the next US crop still turning out close to last year’s record one.

The odd man out in the firming equation has been soyabean oil. CBOT futures for this product are down by almost 9% since the last review went to press in late March. That probably reflects the emphasis on meal-driven crush, releasing the oil as a by-product regardless of demand. Yet it is also at odds with a 22% jump in the benchmark prices for crude mineral oil, upon which biodiesel’s profitability pivots to a large extent. The USDA’s first balance sheets for 2016/17 (starts October for oils) has biodiesel down for consumption of about 2.63M tonnes of soya oil – about 5.5% more than this season. It also has food and other uses of bean oil up by nearly 3% at 6.58M tonnes and as for beans and meal too, it looks for a slightly stronger price scenario for oil than seen so far this season. The USDA also sees total world soya oil use up by about 3.8% or just under 2M tonnes, led by China (+750,000 tonnes).

For much of the past year, it has been this record supply of soyabean oil – priced cheaper than usual versus its competitor oils – that has helped keep prices down across the vegetable oil sector – a boon to consumers at a time of flattening output of rapeseed, sunflower, cottonseed and palm kernel oils and, not least, threatened steep �

FIGURE 1: VEGETABLE OIL PRICES* (MONTHLY AVERAGES)

CHAR

TS: J

OHN

BUCK

LEY

John Buckley June.indd 1 14/06/2016 11:33

CHAR

TS: J

OHN

BUCK

LEY

INTERNATIONAL MARKET REVIEW

16 OFI – JUNE 2016 www.oilsandfatsinternational.com

cuts in new supplies of palm oil.

Drastic shift in the palm oil market

The mood in the palm oil market appears to have shifted drastically since the last review. Export trade has not lived up to expectations while production seems to have fallen less steeply than expected in the wake of last year’s El Niño-inspired droughts, and is now starting to rise seasonally.

It may yet falter again, according to some of the plantation houses and other industry observers, before probably picking up more decisively later in 2016. Even so, some of those pundits who seemed most sure about major price rises for palm oil this year are now having to scale back their projections – and quite significantly too.

What seems to have been most under-estimated is the response of importers to firm palm oil prices at a time of record competition from soya oil – offered at far smaller premiums than usual to its main rival palm – to the backdrop of a stagnating global economy.

Malaysia has seen a particularly severe cut in its sales to second largest customer China, which took almost 42% less in the first four months of this year (and was still importing 33% less in April). Strong gains were seen in Malaysian sales to India (+nearly 22%) and the EU (+near 13%) but overall, annual trade was running only 7% up on the year – or 332,000 tonnes. At the same time, January/April production was down by almost 8% or about 778,000 tonnes, so stocks have tightened – but not nearly as much as the doomsayers predicted.

However, stocks could get a lot tighter – if El Niño does have a hidden legacy working through to consistently lower production through the normally peak late summer months or beyond. Estimates have yet to be withdrawn by several respected analysts for a drop in 2016 production of perhaps 1.5M tonnes or more each for both

Malaysia and top supplier Indonesia.A higher Indonesian export tax was expected

to drive some import demand back to Malaysia which re-introduced its own 5% tax on crude palm (since raised to 5.5%) to divert more, cheaper supply to domestic refiners, thereby boosting competitiveness of its value-added palm product exports (which lost share to Indonesia in recent months). Malaysia’s biodiesel sector is meanwhile pushing for a 10% palm oil blend, rising to 20% within the next two years.

The Kuala Lumpur crude palm oil futures market seems to be so far taking a sanguine view of supply/demand prospects, having dropped to a three-month low in ringgit terms in the latter half of May. In US dollar equivalent, the fall is about 14.5% from April’s multi-year highs (over US$710/tonne) taking the price more or less back to where it started in 2016, if still about 38% above 2015’s summer lows (see Figure 2, above).

The descent has probably also been influenced by more acceptance that the biodiesel outlet – for reasons quoted in past reviews (distribution and engine running issues) – may not grow quite as rapidly in origin countries as expected.

Hopefully, the next few months should shed more light on how these supply/demand factors are evolving.

Rapeseed season tight in Canada

ICE canola futures recently hit 10-month highs – up 20% from their March lows – as domestic crush maintained 12.5% year-on-year growth and farmers held back supplies for better prices. Markets also noted EU crop forecasting body MARS reducing its average yield estimate for the coming crop by about 1.8% from the earlier 3.35 tonnes/ha – not a big adjustment but a reminder of another relatively tight season ahead.

While some rain appears to be relieving affected

parts of the Canadian prairies as OFI went to press, dry, cool weather has held back crops and in some areas, even left them at risk of frost damage.

The ICE contract was also lifted by Statistics Canada’s latest stock report showing under 7.5M tonnes left against 8.33M tonnes this time last year, under-scoring the need for a decent 2016 crop. The USDA’s first take on world rapeseed markets for 2016/17 has Canada’s crop falling to 15.5M tonnes from last year’s 17.2M tonnes. It also has the EU at 21.8M tonnes against 2015’s 22.05M tonnes and 2014’s 24.6M tonnes and Ukraine’s at 1.3M tonnes versus 2015’s 1.74M tonnes and 2014’s 2.2M tonnes. Australia’s crop on the other hand is seen up 300,000 tonnes at 3.3M tonnes. India’s crop is seen 900,000 tonnes up at 6.8M tonnes but China’s down 1M tonnes to 13.3M tonnes. That left world output down by about 2M tonnes to a four-year low of 66M tonnes, implying another year of tightening stocks and firm prices.

The exception to this is China – not only the world’s largest importer/consumer of rapeseed and oil, but its biggest stockholder. (The USDA estimates it started this season with 4.2M tonnes of rapeseed oil – about 75% of world stocks although other observers say the reserve is closer to 2.8M tonnes (see Figure 3, left). Amid its broader economic challenges, the Chinese government is currently trying to rationalise its approach to stocking and the price support behind it – a shift that may hit imports of maize, sugar and rapeseed especially. Some analysts think that is the real motive behind the Chinese authorities announcing planned tight quality controls on foreign matter in incoming cargoes. Canadian exporters fear this may curb sales to their largest customer. But the move might, if it fully transpires, take some of the strain off tight supplies as China imports around 4M tonnes of rapeseed each year – around a third of total world exports.

Sunflower oil contributions boosted