Offshore market outlook - marinemoney.com · Snapshot of offshore utilization and dayrate...

14

Offshore market outlook Marine Money Offshore – China Offshore Finance Forum 25 June 2015 Please refer to important disclosures at the end of this document Andy Yeo Direct: +65 64 08 98 10 Email: [email protected]

Transcript of Offshore market outlook - marinemoney.com · Snapshot of offshore utilization and dayrate...

Offshore market outlook

Marine Money Offshore – China Offshore Finance Forum

25 June 2015

Please refer to important disclosures at the end of this document

Andy Yeo

Direct: +65 64 08 98 10 Email: [email protected]

2

Rio de Janeiro

Oslo (HQ), Stockholm, Copenhagen, Helsinki,

New York

Singapore

Calgary

Los Angeles

Aberdeen

Stavanger, Trondheim, Malmö

Perth

London

Houston

Paris

Pareto Securities short introduction

Pareto’s offices and selected international clients Capital raised across the Oil Service sector* (2006-14)

Selected Pareto transactions

2,9183,567

314971

2,8602,060

3,446 3,4762,380

4,683

1,090

1,235624

1,7482,710

707 522

223

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

2006 2007 2008 2009 2010 2011 2012 2013 2014

Bond Equity

USDm

7,601

4,658

1,549 1,595

4,608 4,770

4,153 3,999

2,602

*Includes only drilling, supply and subsea sectors

January 2014

Sole Lead Arranger

5-year senior secured fixed rate bonds

USD 725m

March 2013

Sole Lead Manager

5 year senior secured bond

USD 575m

June 2014

Private placement of shares

USD 200m

Joint Lead Manager

April 2014

Joint Financial Advisor

Sale of company to Mermaid Marine

Australia Ltd.

USD 566m

March 2013

Joint Lead Manager

5 year senior unsecured bond

NOK 1,800m

June 2015

Joint Lead Manager

Public placement of shares

USD 200m

December 2013

Joint Lead Manager

6 year senior unsecured bond

USD 400m

November 2013

Global Coordinator & Sole Bookrunner

Private placement of shares

USD 250m

3

Offshore market developments over the last year

Brent price (per bbl): USD 114 (25 Jun 2014), USD 47 (14 Jan 2015), USD 60-65 (current)

OilCos cut E&P spending; expected to be down ~15% p.a. in 2015E and potentially flat in 2016E

Very limited new contract awards in the offshore sector

Increasing number of early contract terminations and contract renegotiations

Utilization and dayrates hit across the offshore sectors

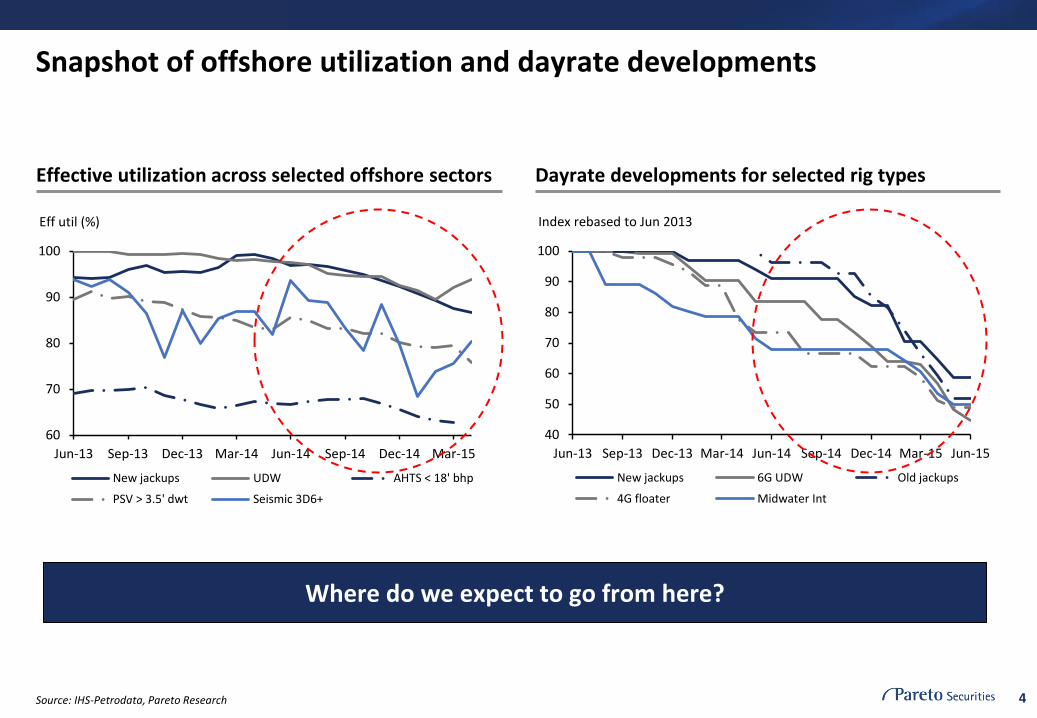

4

60

70

80

90

100

Jun-13 Sep-13 Dec-13 Mar-14 Jun-14 Sep-14 Dec-14 Mar-15

New jackups UDW AHTS < 18' bhp

PSV > 3.5' dwt Seismic 3D6+

Eff util (%)

Snapshot of offshore utilization and dayrate developments

Effective utilization across selected offshore sectors Dayrate developments for selected rig types

Source: IHS-Petrodata, Pareto Research

Where do we expect to go from here?

40

50

60

70

80

90

100

Jun-13 Sep-13 Dec-13 Mar-14 Jun-14 Sep-14 Dec-14 Mar-15 Jun-15

New jackups 6G UDW Old jackups

4G floater Midwater Int

Index rebased to Jun 2013

5 *Spread cost vares widely from well to well and based on the type of work Source: Pareto Research

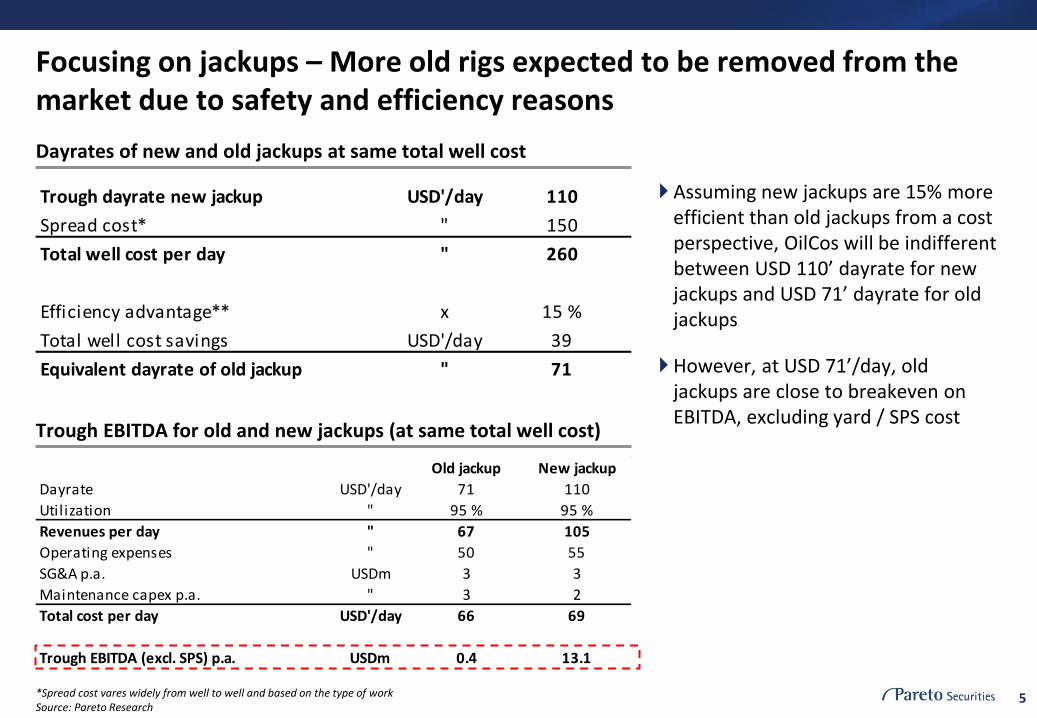

Focusing on jackups – More old rigs expected to be removed from the market due to safety and efficiency reasons

Dayrates of new and old jackups at same total well cost

Assuming new jackups are 15% more efficient than old jackups from a cost perspective, OilCos will be indifferent between USD 110’ dayrate for new jackups and USD 71’ dayrate for old jackups

However, at USD 71’/day, old jackups are close to breakeven on EBITDA, excluding yard / SPS cost

Trough dayrate new jackup USD'/day 110

Spread cost* " 150

Total well cost per day " 260

Efficiency advantage** x 15 %

Total well cost savings USD'/day 39

Equivalent dayrate of old jackup " 71

Trough EBITDA for old and new jackups (at same total well cost)

Old jackup New jackup

Dayrate USD'/day 71 110

Utilization " 95 % 95 %

Revenues per day " 67 105

Operating expenses " 50 55

SG&A p.a. USDm 3 3

Maintenance capex p.a. " 3 2

Total cost per day USD'/day 66 69

Trough EBITDA (excl. SPS) p.a. USDm 0.4 13.1

6

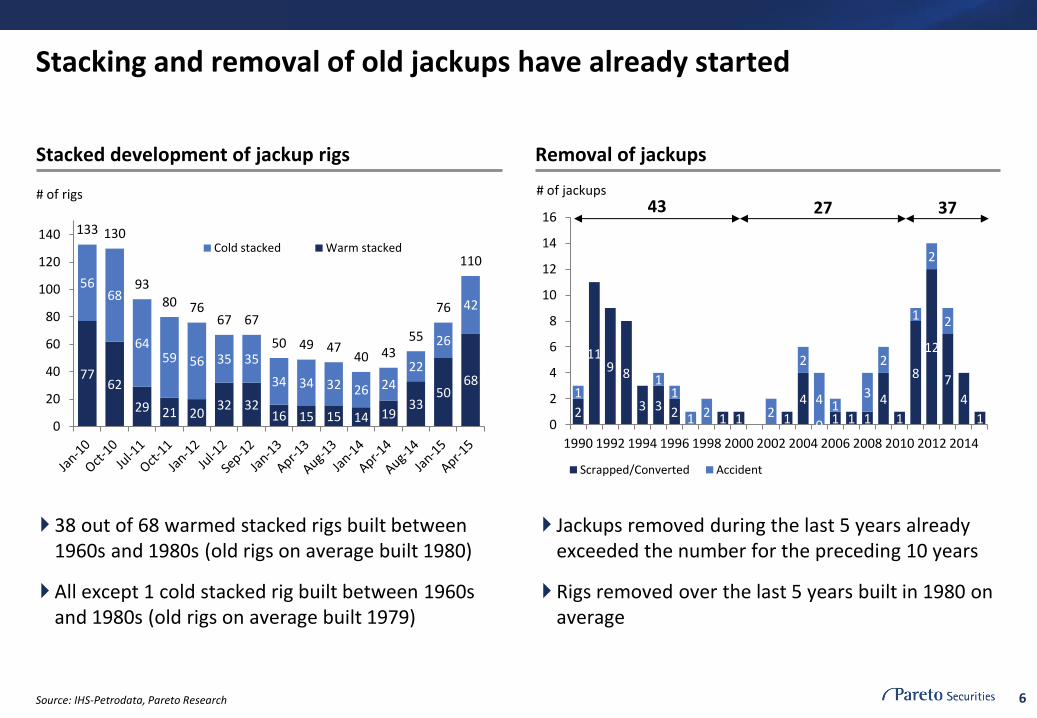

Stacking and removal of old jackups have already started

Source: IHS-Petrodata, Pareto Research

Stacked development of jackup rigs Removal of jackups

2

119 8

3 3 2 1 1 1

4

0 1 1 1

4

1

8

12

7

4

1

11

1

1 2 2

2

4 13

2

1

2

2

0

2

4

6

8

10

12

14

16

1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014

Scrapped/Converted Accident

# of jackups

37 27 43

38 out of 68 warmed stacked rigs built between 1960s and 1980s (old rigs on average built 1980)

All except 1 cold stacked rig built between 1960s and 1980s (old rigs on average built 1979)

Jackups removed during the last 5 years already exceeded the number for the preceding 10 years

Rigs removed over the last 5 years built in 1980 on average

7762

29 21 2032 32

16 15 15 14 1933

5068

5668

6459 56 35 35

34 34 32 26 2422

26

42

133 130

9380 76

67 67

50 49 4740 43

55

76

110

0

20

40

60

80

100

120

140Cold stacked Warm stacked

# of rigs

7

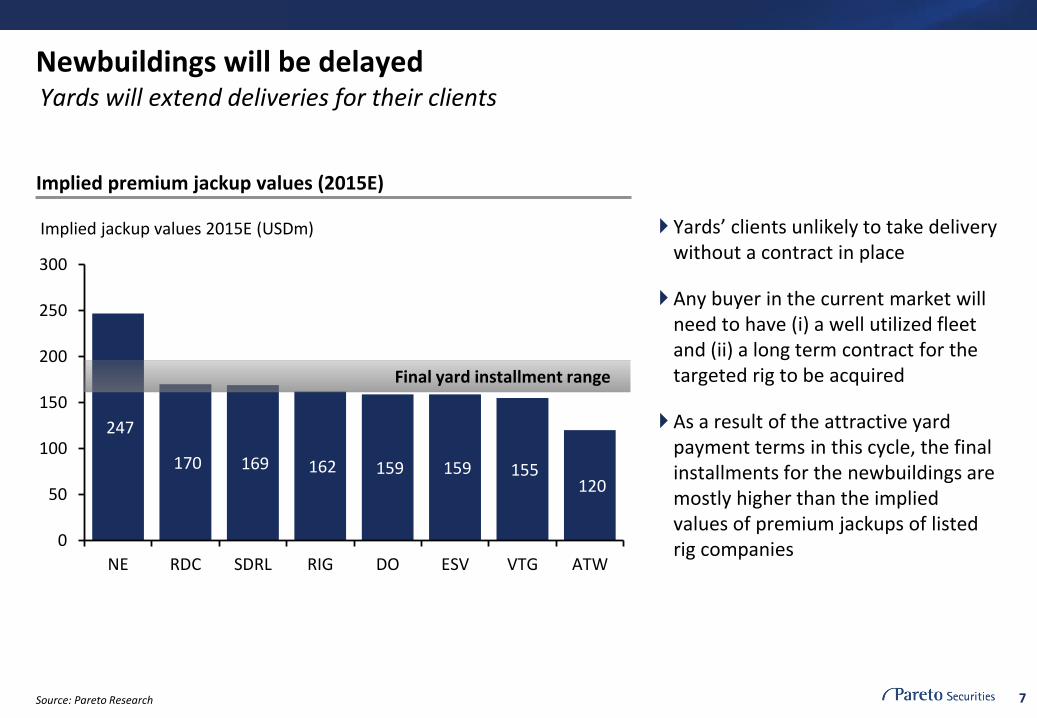

Newbuildings will be delayed

Implied premium jackup values (2015E)

Yards’ clients unlikely to take delivery without a contract in place

Any buyer in the current market will need to have (i) a well utilized fleet and (ii) a long term contract for the targeted rig to be acquired

As a result of the attractive yard payment terms in this cycle, the final installments for the newbuildings are mostly higher than the implied values of premium jackups of listed rig companies

247

170 169 162 159 159 155 120

0

50

100

150

200

250

300

NE RDC SDRL RIG DO ESV VTG ATW

Implied jackup values 2015E (USDm)

Source: Pareto Research

Final yard installment range

Yards will extend deliveries for their clients

8

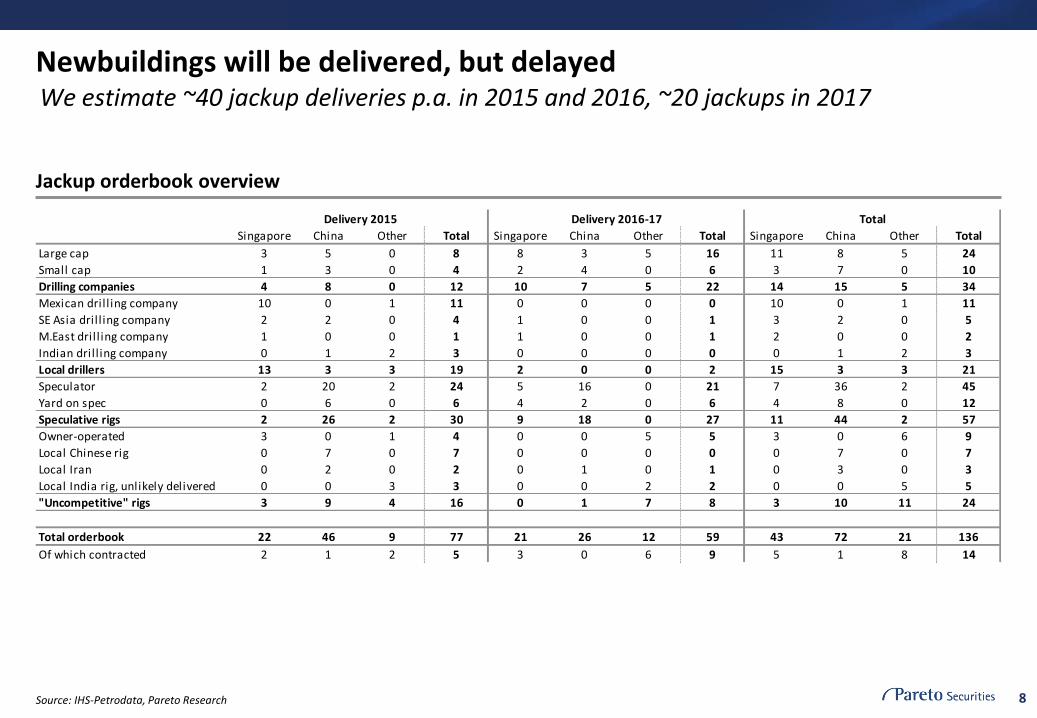

Newbuildings will be delivered, but delayed

Jackup orderbook overview

Singapore China Other Total Singapore China Other Total Singapore China Other Total

Large cap 3 5 0 8 8 3 5 16 11 8 5 24

Small cap 1 3 0 4 2 4 0 6 3 7 0 10

Drilling companies 4 8 0 12 10 7 5 22 14 15 5 34

Mexican dril l ing company 10 0 1 11 0 0 0 0 10 0 1 11

SE Asia dril l ing company 2 2 0 4 1 0 0 1 3 2 0 5

M.East dril l ing company 1 0 0 1 1 0 0 1 2 0 0 2

Indian dril l ing company 0 1 2 3 0 0 0 0 0 1 2 3

Local drillers 13 3 3 19 2 0 0 2 15 3 3 21

Speculator 2 20 2 24 5 16 0 21 7 36 2 45

Yard on spec 0 6 0 6 4 2 0 6 4 8 0 12

Speculative rigs 2 26 2 30 9 18 0 27 11 44 2 57

Owner-operated 3 0 1 4 0 0 5 5 3 0 6 9

Local Chinese rig 0 7 0 7 0 0 0 0 0 7 0 7

Local Iran 0 2 0 2 0 1 0 1 0 3 0 3

Local India rig, unlikely delivered 0 0 3 3 0 0 2 2 0 0 5 5

"Uncompetitive" rigs 3 9 4 16 0 1 7 8 3 10 11 24

Total orderbook 22 46 9 77 21 26 12 59 43 72 21 136

Of which contracted 2 1 2 5 3 0 6 9 5 1 8 14

Delivery 2015 Delivery 2016-17 Total

Source: IHS-Petrodata, Pareto Research

We estimate ~40 jackup deliveries p.a. in 2015 and 2016, ~20 jackups in 2017

9

Lower demand expected in the shorter term

Jackup supply / demand summary

Source: IHS-Petrodata, Pareto Research

320 324 342 358 367 371 373 371 385 396 420 422 421 411 392 370 352

77 62 29 21 20 32 32 16 15 1514 19 33 50 68 80

7556 68 64 59 56 35 35 34 34 32 26 24 22 26 42 66 139

50%

60%

70%

80%

90%

100%

050

100150200250300350400450500550

Contracted Warm stacked Cold stacked Marketed utilization

# of rigs

Driven by South East Asia due to high fleet growth over the past decade

10

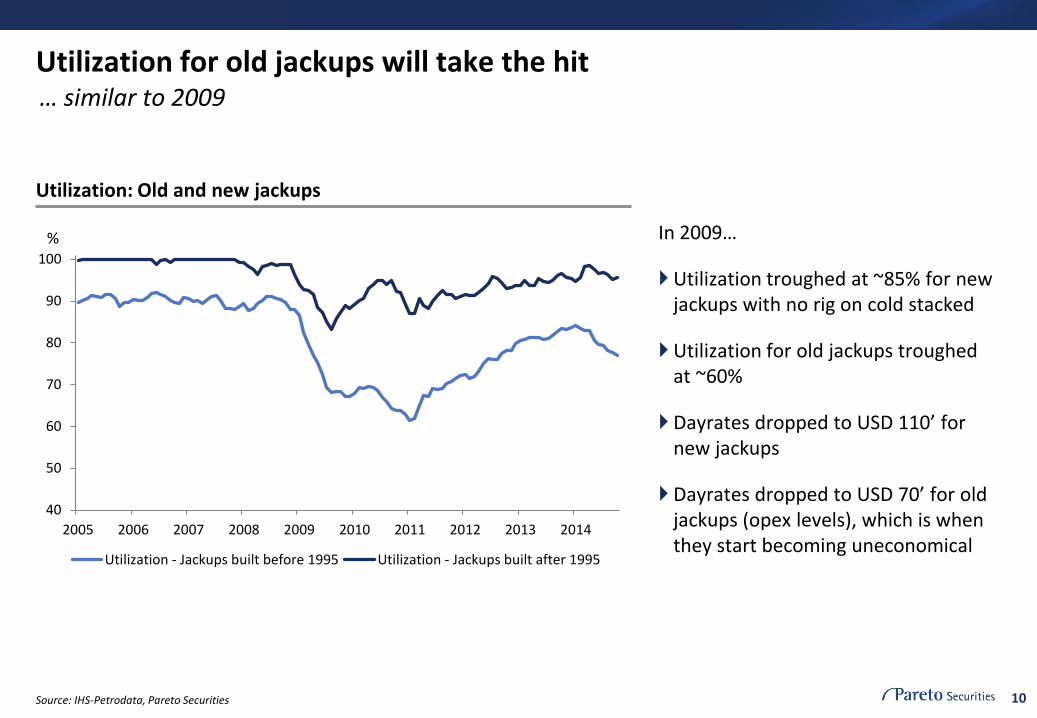

Utilization for old jackups will take the hit

Source: IHS-Petrodata, Pareto Securities

Utilization: Old and new jackups

In 2009…

Utilization troughed at ~85% for new jackups with no rig on cold stacked

Utilization for old jackups troughed at ~60%

Dayrates dropped to USD 110’ for new jackups

Dayrates dropped to USD 70’ for old jackups (opex levels), which is when they start becoming uneconomical

40

50

60

70

80

90

100

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Utilization - Jackups built before 1995 Utilization - Jackups built after 1995

%

… similar to 2009

11

The positive news: Costs are down 25+% the past year

Source: Pareto Research

Maria cost down ~15% from December Kaombo cost down ~20% in 2014

USD 70/bbl is the new USD 100/bbl

SURFSURF

Equipment

Equipment

Rigs

Rigs

Other

Other

0

500

1,000

1,500

2,000

2,500

Old New

USDm

SURF SURF

FPSO

FPSO

Equipment

Equipment

Umbilicals

Umbilicals

Rigs

Rigs

Other

Other

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

20,000

Old New

USDm

12

There is plenty of capital available, ready to invest at the right price

USD 200m equity raised via registered direct offering

Uses of net proceeds: Working capital and general corporate purposes

Launch date 2 June 2015, completion date 3 June 2015

Placement price: USD 7/share, 13% discount to last close

Geographical split on demand: 67% US, 15% UK, 18% others

Ocean Rig’s recent equity raise is a very good example

The key is to be able to differentiate from peers (e.g. valuation, structure, etc.)

13

Summary

The current offshore market is challenging

However, demand will recover, driven initially by lower development / breakeven costs for OilCo’s; USD 70/bbl is the new USD 100/bbl

Supply must adjust to balance the market; restructuring has started for some

Capital is available for companies with modern assets with the right structure and price

14

Contact details

www.paretosec.com | Bloomberg: PASE (go) | Reuters: PARETO

Oslo (Norway) Pareto Securities AS Dronning Mauds gate 3 PO Box 1411 Vika N-0115 Oslo NORWAY Tel: +47 22 87 87 00

Stavanger (Norway) Pareto Securities AS Haakon VIIs gate 8 PO Box 163 N-4001 Stavanger NORWAY Tel: +47 51 83 63 00

Trondheim (Norway) Pareto Securities AS Nordre gate 11 PO Box 971 Sentrum N-7410 Trondheim NORWAY Tel: +47 21 50 74 60

Malmö (Sweden) Pareto Securities AB Stortorget 13 S-211 22 Malmö SWEDEN Tel: +46 40 750 20

Rio de Janeiro (Brazil) Pareto Securities Ltda Av. Presidente Wilson 231, 9° andar Rio de Janeiro, RJ 20030-021 BRAZIL Tel: +55 21 3578-5620

Stockholm (Sweden) Pareto Securities AB Berzelii Park 9 PO Box 7415 S-103 91 Stockholm SWEDEN Tel: +46 8 402 50 00

Helsinki (Finland) Pareto Securities Oy Aleksanterinkatu 44, 6th floor FI-00100 Helsinki FINLAND Tel: +358 9 8866 6000

Copenhagen (Denmark) Pareto Securities AS Copenhagen Branch Bredgade 30 DK-1260 Copenhagen DENMARK Tel: +45 78 73 48 00

Perth (Australia) Pareto Securities Pty Ltd Level 24 77 St Georges Tce Perth, Western Australia AUSTRALIA, 6000 Tel: +61 8 6141 3366

Singapore Pareto Securities Pte Ltd 16 Collyer Quay #27-02 Income at Raffles Singapore 049318 SINGAPORE Tel: +65 6408 9800

London (UK) Pareto Securities Ltd 8 Angel Court London EC2R 7HJ UNITED KINGDOM Tel: +44 20 7786 4370

New York (US) Pareto Securities Inc 150 East 52nd Street, 29th floor New York NY 10022 USA Tel: +1 212 829-4200

Houston (US) Pareto Securities Inc 8 Greenway Plaza, Suite 818 Houston, TX 77046 USA Tel: +1 832 831-1895

Aberdeen (UK) Pareto Securities Ltd 46 Carden Place Aberdeen, AB10 1UP UNITED KINGDOM Tel: +44 1224 433466

Los Angeles (US) Pareto Securities Inc 9465 Wilshire Blvd, Suite 300 Beverly Hills, CA 90212 USA Tel: +1 424 284 4000

Calgary (Canada) Pareto Securities AS, Calgary Branch Suite 2600, 144 – 4 Avenue SW Calgary AB T2P 3N4 CANADA Tel: +1 403 398 2177

Paris (France) Pareto Securities AS, Paris Branch 11 BD Jean Mermoz 92200 Neuilly Sur Seine FRANCE Tel: +33 141921234