Office of Inspector General Audit Tips for FEMA Public ... Conference... · Audit Tips for FEMA...

27

Office of Inspector General Audit Tips for FEMA Public Assistance Grant Recipients and Subrecipients Tonda L. Hadley, Director Central Regional Office-South Office of Emergency Management Oversight Texas Department of Emergency Management Conference May 2017

Transcript of Office of Inspector General Audit Tips for FEMA Public ... Conference... · Audit Tips for FEMA...

Office of Inspector General

Audit Tips for FEMA Public Assistance

Grant Recipients and Subrecipients

Tonda L. Hadley, Director

Central Regional Office-South

Office of Emergency Management Oversight

Texas Department of Emergency Management Conference

May 2017

www.oig.dhs.gov

or follow us on Twitter @DHSOIG

Overview DHS OIG Organization

Emergency Management Oversight (EMO) Mission

EMO Audits More than Disasters

How We Select Grant Audits

Life Cycle Audit Approach

Annual Audit Tips Report

Applicable Criteria

Audit Finding Examples

Key Points to Remember

Questions

2

Office of Inspector General

www.oig.dhs.gov

or follow us on Twitter @DHSOIG

DHS OIG

3

Inspector General John Roth

Deputy Inspector General John V. Kelly

Information

Technology Audits

Inspections

& Evaluations

Enterprise

Risk Identification

& Management

Audits

Management

Chief of Staff

Assistant

Inspectors General

Investigations

Emergency Management

Oversight

External Affairs

Counsel to

Inspector General Laurel Loomis Rimon

Integrity and Quality

Oversight

Whistleblower

Protection

Unit

FOIA Unit

www.oig.dhs.gov

or follow us on Twitter @DHSOIG

Emergency Management Oversight

(EMO) MISSION –

Provide aggressive and ongoing audit effort to ensure that disaster

relief funds are spent appropriately;

Identify fraud, waste, and abuse as early as possible;

Keep Congress, the Secretary, the Administrator of FEMA and others

fully informed on problems relating to disaster operations and

assistance programs;

Focus heavily weighted toward prevention through review of internal

controls and monitoring; and

Advise DHS and FEMA officials on contracts, grants, and purchase

transactions before they are approved.

4

www.oig.dhs.gov

or follow us on Twitter @DHSOIG

EMO Audits More than Disasters

Recent Shift from Disaster Relief Funds (DRF)

to Appropriated Funds

Allows Us to Audit All FEMA Activities,

Including Non-DRF Programs such as the

National Flood Insurance Program and

Preparedness Grants and Programs

This presentation focuses on our disaster grant

audits

5

www.oig.dhs.gov

or follow us on Twitter @DHSOIG

Emergency Management Oversight

(EMO)

HOW DO WE SELECT AUDITS?

The OIG considers several factors in determining which

activities to audit. These factors include:

the risk of fraud, waste, and abuse of Federal funds;

statutory and regulatory requirements;

current or potential dollar magnitude;

requests from congressional, FEMA, or State officials; and

reports/allegations of impropriety or problems in implementing FEMA

programs.

6

www.oig.dhs.gov

or follow us on Twitter @DHSOIG 7

Office of Inspector General

Focuses on Public Assistance Grant Phases

Response

Recovery

Close Out

Proactive Approach includes 4 Types of Audits Deployment Audits

Capacity Audits

Early Warning Audits

Traditional Audits

Life Cycle Approach for Grant Audits

www.oig.dhs.gov

or follow us on Twitter @DHSOIG

Annual Audit Tips Report

This report provides an overview of—

OIG responsibilities;

Federal statutes, regulations, and guidelines applicable to

disaster grants;

Frequent audit findings; and

Key points to remember when administering FEMA grants.

8

www.oig.dhs.gov

or follow us on Twitter @DHSOIG

Annual Audit Tips Report

Using this report should assist disaster

assistance applicants:

document and account for disaster-related costs;

minimize the loss of FEMA disaster assistance funds;

maximize financial recovery; and

prevent fraud, waste, and abuse of disaster funds.

9

www.oig.dhs.gov

or follow us on Twitter @DHSOIG

Audit Tips

Applicable Federal Statutes and Regulations

Include the Following:

Robert T. Stafford Disaster Relief and Emergency Assistance

Act

44 Code of Federal Regulations (CFR)

2 CFR Part 200: Uniform Administrative Requirements, Cost

Principles, and Audit Requirements for Federal Awards

10

www.oig.dhs.gov

or follow us on Twitter @DHSOIG

Audit Tips

Applicable FEMA Guidelines Include:

Public Assistance Program and Policy Guide (FEMA First

Issued in January 2016 and Recently Updated)

FEMA 329, Debris Estimating Field Guide (September 2010),

Hazard Mitigation Assistance (HMA) Unified Guidance, and

Public Assistance Policy on Stafford Act Section 705 (FP-205-

081-2, March 31, 2016)

11

www.oig.dhs.gov

or follow us on Twitter @DHSOIG

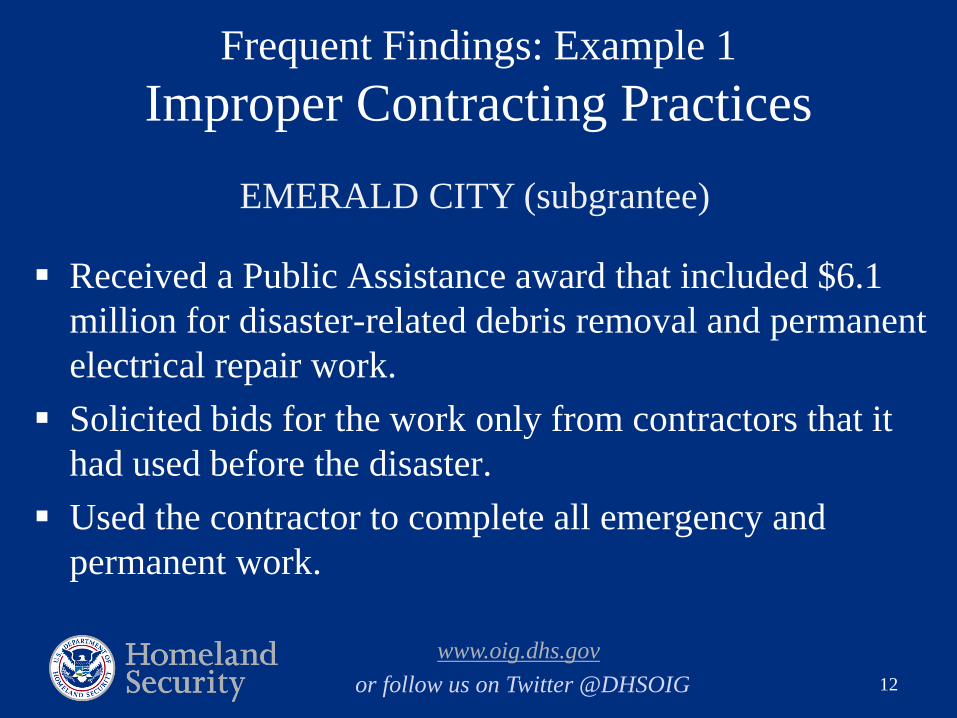

Frequent Findings: Example 1

Improper Contracting Practices

12

Received a Public Assistance award that included $6.1

million for disaster-related debris removal and permanent

electrical repair work.

Solicited bids for the work only from contractors that it

had used before the disaster.

Used the contractor to complete all emergency and

permanent work.

EMERALD CITY (subgrantee)

www.oig.dhs.gov

or follow us on Twitter @DHSOIG

2 CFR 200.317 to .326 requires all non-federal entities (other

than states) to comply with the following procurement standards:

Retain records of procurement

process and bid selection

Use T&M contracts only as a last

resort and with a ceiling price

Perform a cost analysis

Negotiate profit as a separate

element

13

Frequent Findings: Example 1 (cont.)

Improper Contracting Costs

Full and open competition

Affirmative steps to assure the use of

small and minority firms, women’s

business enterprises, and labor surplus

area firms when possible

Maintain contract oversight

Maintain written standards of conduct

www.oig.dhs.gov

or follow us on Twitter @DHSOIG

As part of the audit, Emerald City officials stated that they procured the

contracts under exigent circumstances.

The OIG determined that the subrecipient had restored electrical power to

almost all of its customers over the next 10 weeks. After such time, exigent

circumstances no longer existed to warrant the use of noncompetitive

contracts.

The OIG also determined that because the solicitation of bids came from a

limited number of contractors, full and open competition did not occur.

FEMA had no assurance that contract costs were reasonable or that minority

firms, women’s business enterprises, and labor surplus area firms had an

opportunity to bid on the work.

The OIG questioned $6.1 million because Emerald City did not meet Federal

procurement standards.

14

Frequent Findings: Example 1 (cont.)

Improper Contracting Costs

www.oig.dhs.gov

or follow us on Twitter @DHSOIG

Frequent Findings: Example 2

Unsupported Costs

15

1. Used contract labor to complete 7 large projects to repair an

electrical distribution system.

Submitted a copy of Invoice 3B as support for labor costs in all 7 PWs. The

invoice contained a single line item for $194,000 labeled “Salary.”

No additional documentation was submitted for labor at the time of

closeout.

2. Claimed a total of $1.7 million across the 7 PWs for materials

withdrawn from existing inventory, using the replacement cost

method.

Bedrock (subgrantee)

www.oig.dhs.gov

or follow us on Twitter @DHSOIG

1. Federal cost principles (2 CFR 200.403(g) require recipients

and subrecipients to adequately document costs that they

claim under Federal programs.

2. OMB Circular A-122, Attachment A, A (2)(c), requires

recipients and subrecipients to be consistent with policies and

procedures that apply uniformly to both federally-financed

and other activities of the organization.

16

Frequent Findings: Example 2 (cont.)

Unsupported Costs

www.oig.dhs.gov

or follow us on Twitter @DHSOIG

Bedrock could not provide supporting documentation for the labor claim of

$194,000 in Invoice 3B.

The labor contractor later provided redacted time sheets and payroll registers,

claiming that it could not provide the sensitive identifying information to the

subrecipient. The time sheets and the payroll registers appeared to match;

however, they totaled $174,000.

The documentation did not indicate which employee completed what work or

if the work was directly assignable to any of the 7 large PWs.

The OIG questioned $194,000 because Bedrock could not support the

accuracy of the claimed labor costs.

17

Frequent Findings: Example 2 (cont.)

Unsupported Costs

www.oig.dhs.gov

or follow us on Twitter @DHSOIG

The Bedrock policy and procedures state that inventory valuation is

determined using the average cost method.

The OIG also determined that had the subrecipient used its standard

method of inventory pricing, the cost of materials would have been

$1 million less than the amount claimed.

The OIG did not question $700,000 of material costs associated with

actual repairs, but did question the $1 million Bedrock claimed for

existing inventory costs because the claim was not consistent with

Federal cost principles.

18

Frequent Findings: Example 2 (cont.)

Unsupported Costs

www.oig.dhs.gov

or follow us on Twitter @DHSOIG

Frequent Findings: Example 3

Poor Project Accounting

19

1. Created an account within its automated accounting system

designated as “ice storm disaster” to account for $15 million

FEMA grant.

All costs incurred during the incident period were included in this account

with no segregation of eligible and non-eligible disaster related

expenditures.

No additional system of accounting, such as spreadsheets or project files,

was employed to track Federal grant funds received.

2. The journal of expenditures contained reference to Payroll for

$950,000 with no reference to projects, pay period(s), or daily

activity reports.

METROPOLIS (subgrantee)

www.oig.dhs.gov

or follow us on Twitter @DHSOIG

Federal regulations (2 CFR 200.302 and 44 CFR 206.205)

require recipients and subrecipients to maintain a system that

accounts for FEMA funds on a project-by-project basis.

The system must disclose the financial results for all FEMA-

funded activities accurately, currently, and completely.

The system must identify funds received and dispersed, and

reference source documentation (i.e., cancelled checks, invoices,

payroll, time and attendance records, contracts, etc.).

20

Frequent Findings: Example 3 (cont.)

Poor Project Accounting

www.oig.dhs.gov

or follow us on Twitter @DHSOIG

• Metropolis did not account for the

expenditures on a project-by-

project basis.

• Further, the single account

comingled eligible and non-

eligible disaster-related

expenditures.

• The OIG questioned the entire $15

million grant because the costs

were not auditable by project.

21

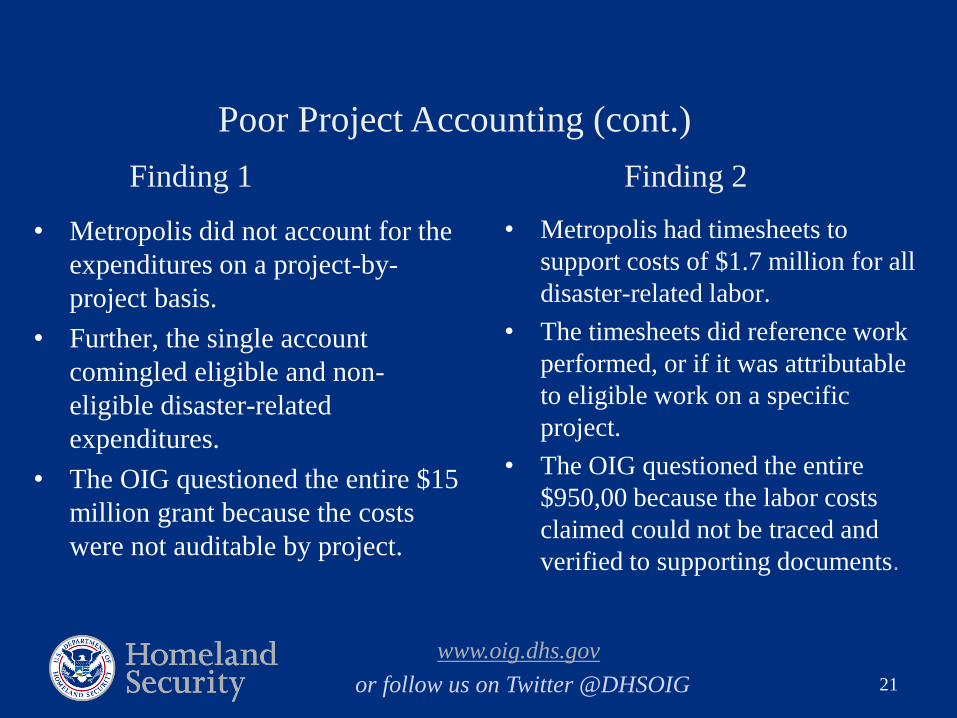

Poor Project Accounting (cont.)

• Metropolis had timesheets to

support costs of $1.7 million for all

disaster-related labor.

• The timesheets did reference work

performed, or if it was attributable

to eligible work on a specific

project.

• The OIG questioned the entire

$950,00 because the labor costs

claimed could not be traced and

verified to supporting documents.

Finding 1 Finding 2

www.oig.dhs.gov

or follow us on Twitter @DHSOIG

Frequent Findings: Example 4

Direct Administrative Costs

22

Contracted with Bruce Wayne Consulting (BWC) to perform all grant management

functions.

7 BWC employees traveled from Los Angeles to Gotham City and remained on-site for 6

weeks (42 days), rented individual cars, lodged at The Grand Hotel, and leased office

space at an area strip mall.

On behalf of Gotham City, BWC attended all meetings, conducted site visits, prepared

PW packets complete with disaster-related expenditures and supporting documentation,

delivered packets to the JFO, reviewed and signed PWs upon completion.

In a separate contract, BWC was also hired to manage closeout requests when the

recovery projects were complete.

Claimed a total of $752,000 direct administrative costs for BWC services allocated

evenly across the 10 small and 4 large PWs submitted to FEMA.

GOTHAM CITY (subgrantee)

www.oig.dhs.gov

or follow us on Twitter @DHSOIG

• Costs identified specifically with a

particular final cost objective… or can be

assigned to such activities relatively

easily with a high degree of accuracy

(2 CFR 200.413(a))

• Costs incurred that can be identified

separately and assigned to a specific

project (44 CFR 207.6(c)) and treated

consistently across all Federal awards and

other activities. (2 CFR 200.413(b))

FEMA Disaster Assistance Policy

9525.9.

23

Frequent Findings: Example 4 (cont.)

Direct Administrative Costs

Direct Administrative Costs

• Indirect costs, administrative expenses, and

any other expenses not directly chargeable to

a specific project.

(44 CFR 207.2)

• A reasonable calculation of pass-through

funds (if any) for management costs to its

subgrantees must be identified in the

grantee’s Admin Plan.

(44 CFR 206.207(b)(iii)(K))

• Can be used only for the administration of

the grant, cannot be charged directly to a

project, and are considered management

costs. (44 CFR 207.6(a-b))

Management (324) Costs

www.oig.dhs.gov

or follow us on Twitter @DHSOIG

Key Points to Remember

1. Designate a person to coordinate the accumulation of records.

2. Establish a separate and distinct account for recording revenue

and expenditures, and a separate identifier for each distinct

FEMA project.

3. Ensure that the final claim for each project is supported by

amounts recorded in the accounting system.

4. Ensure that each expenditure is recorded in the accounting

books and is referenced to supporting source documentation

(checks, invoices, etc.) that can be readily retrieved

24

www.oig.dhs.gov

or follow us on Twitter @DHSOIG

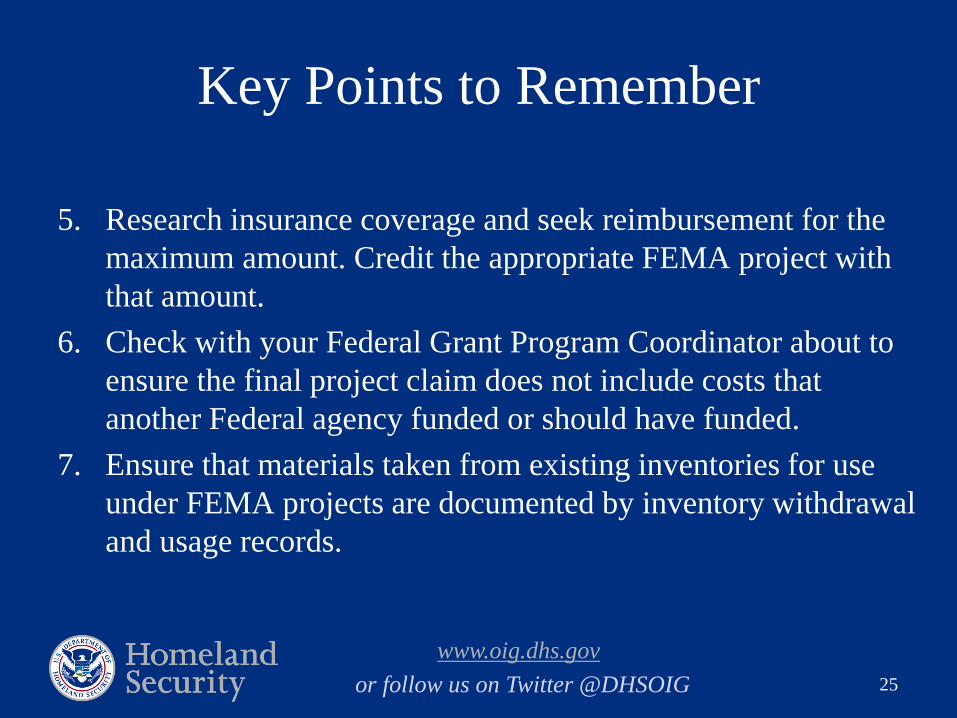

Key Points to Remember

5. Research insurance coverage and seek reimbursement for the

maximum amount. Credit the appropriate FEMA project with

that amount.

6. Check with your Federal Grant Program Coordinator about to

ensure the final project claim does not include costs that

another Federal agency funded or should have funded.

7. Ensure that materials taken from existing inventories for use

under FEMA projects are documented by inventory withdrawal

and usage records.

25

www.oig.dhs.gov

or follow us on Twitter @DHSOIG

Key Points to Remember

8. Ensure that expenditures claimed under the FEMA project are

reasonable and necessary, are authorized under the scope of

work, and directly benefit the project.

9. Ensure that costs claimed as Direct Administrative Costs do

not include indirect costs allocated across multiple projects.

26

www.oig.dhs.gov

or follow us on Twitter @DHSOIG 27

Questions