OFFER FOR SALE OF SHARES - invest.pk

46

INVESTORS ARE ADVISED IN THEIR OWN INTEREST TO CAREFULLY READ THE CONTENTS OF THIS OFFER FOR SALE DOCUMENT, PARTICULARLY THE URISK FACTORS GIVEN AT PARA 4.7 U, BEFORE MAKING ANY INVESTMENT DECISION. SUBMISSION OF FICTITIOUS AND MULTIPLE (MORE THAN ONE) APPLICATIONS IS PROHIBITED AND SUCH APPLICATIONS’ MONEY IS LIABLE TO CONFISCATION UNDER SECTION 18A OF THE SECURITIES AND EXCHANGE ORDINANCE, 1969. OFFER FOR SALE OF SHARES PRESENT OFFER CONSIST OF 59,748,500 ORDINARY SHARES (13.28% OF PAIDUP CAPITAL) WITH A GREENSHOE OPTION OF AN ADDITIONAL 60,000,000 ORDINARY SHARES (13.33% OF PAIDUP CAPITAL) IN CASE OF OVER- SUBSCRIPTION AT AN OFFER PRICE OF PKR 21/- PER SHARE (INCLUDING A PREMIUM OF PKR 11/- PER SHARE) THIS IS NOT A PROSPECTUS BY ARIF HABIB BANK LIMITED, BUT AN OFFER FOR SALE BY ARIF HABIB SECURITIES LIMITED, THE PARENT COMPANY, OUT OF ITS EXISTING SHAREHOLDING IN ARIF HABIB BANK LIMITED The subscription list will Insha’Allah open at the commencement of banking hours on 29 December, 2007 and will close on 31 December, 2007 at the close of banking hours Advisor & Arranger Underwriters Allied Bank Limited Bank Alfalah Limited Faysal Bank Limited Habib Bank Limited The Bank of Punjab United Bank Limited First Dawood Investment Bank Limited Pak Kuwait Investment Co. (Pvt.) Limited Live Securities (Pvt.) Limited AKD Securities Limited Pak Oman Investment Company Limited Pervez Ahmed Securities Limited Saudi Pak Industrial and Agricultural Investment Company (Pvt.) Limited FDM Capital Securities (Pvt.) Limited Dawood Equities Limited Munaf Sattar Securities (Pvt.) Limited Pak Brunei Investment Co. Ltd. Saudi Pak Leasing Company Limited The date of publication of this Offer for Sale Document is 20 December, 2007

Transcript of OFFER FOR SALE OF SHARES - invest.pk

INVESTORS ARE ADVISED IN THEIR OWN INTEREST TO CAREFULLY READ THE CONTENTS OF THIS OFFER FOR SALE DOCUMENT, PARTICULARLY THE URISK FACTORS GIVEN AT PARA

4.7 U, BEFORE MAKING ANY INVESTMENT DECISION.

SUBMISSION OF FICTITIOUS AND MULTIPLE (MORE THAN ONE) APPLICATIONS IS PROHIBITED AND SUCH APPLICATIONS’ MONEY IS LIABLE TO CONFISCATION UNDER

SECTION 18A OF THE SECURITIES AND EXCHANGE ORDINANCE, 1969.

OFFER FOR SALE OF SHARES

PRESENT OFFER CONSIST OF 59,748,500 ORDINARY SHARES (13.28% OF PAIDUP CAPITAL) WITH A GREENSHOE OPTION OF AN ADDITIONAL 60,000,000

ORDINARY SHARES (13.33% OF PAIDUP CAPITAL) IN CASE OF OVER- SUBSCRIPTION AT AN OFFER PRICE OF PKR 21/- PER SHARE

(INCLUDING A PREMIUM OF PKR 11/- PER SHARE)

THIS IS NOT A PROSPECTUS BY ARIF HABIB BANK LIMITED, BUT AN OFFER FOR SALE BY ARIF HABIB SECURITIES LIMITED, THE PARENT COMPANY, OUT OF ITS

EXISTING SHAREHOLDING IN ARIF HABIB BANK LIMITED

The subscription list will Insha’Allah open at the commencement of banking hours on 29 December, 2007 and will close on 31 December, 2007 at the close of banking hours

Advisor & Arranger

Underwriters Allied Bank Limited Bank Alfalah Limited Faysal Bank Limited Habib Bank Limited The Bank of Punjab United Bank Limited First Dawood Investment Bank Limited Pak Kuwait Investment Co. (Pvt.) Limited Live Securities (Pvt.) Limited AKD Securities Limited Pak Oman Investment Company Limited Pervez Ahmed Securities Limited Saudi Pak Industrial and Agricultural Investment Company (Pvt.) Limited FDM Capital Securities (Pvt.) Limited

Dawood Equities Limited Munaf Sattar Securities (Pvt.) Limited Pak Brunei Investment Co. Ltd. Saudi Pak Leasing Company Limited

The date of publication of this Offer for Sale Document is

20 December, 2007

Offer for Sale of Ordinary Shares Arif Habib Bank Limited

GLOSSARY OF TECHNICAL TERMS AND ABBREVIATIONS

AHSL Arif Habib Securities Limited CDA Central Depositories Act, 1997 CDC The Central Depository Company of Pakistan Limited CDS Central Depository System CFS Continuous Funding System CNIC Computerized National Identity Card The Commission / SECP The Securities & Exchange Commission of Pakistan The Bank / AHBL Arif Habib Bank Limited Correspondent Banking Banking activities pertaining to international trade & guarantees CVT Capital Value Tax Cyber Banking Online banking Delivery Channels Include branch network, ATMs etc. EPS Earnings Per Share GOP Government Of Pakistan OFFER Offer for Sale of 59,748,500 shares of PKR 21/- per share at a premium of

PKR 11/- per share of Arif Habib Bank Limited, out of the existing shareholding of Arif Habib Securities Limited in the Bank (with a green show option of 60,000,000 shares in case of oversubscription)

OFSD Offer For Sale Document ITO Income Tax Ordinance, 2001 KIBOR Karachi Inter Bank Offered Rate K Thousand Large Banks / Big Banks Include: Allied Bank Limited, Habib Bank Limited, MCB Bank Limited,

Standard Chartered Bank Limited, United Bank Ltd., National Bank of Pakistan

L / C Letter of Credit Mid-market Refers to medium sized corporate & SME borrowers NIM Net Interest Margin NP Margin Net Profit Margin Ordinance The Companies Ordinance, 1984

PACRA Pakistan Credit Rating Agency Peer Banks Include Big Banks, 2P

ndP Tier Bank & 3P

rdP Tier Banks

SBP State Bank of Pakistan Smart Branches Technology intensive branch setups with few human resource Stock Exchange / KSE The Karachi Stock Exchange (Guarantee) Limited

WHT Withholding Tax 2P

ndP Tier Banks Include: ABN Amro Bank, Askari Commercial Bank Limited, Alfalah

Bank Limited, Bank of Punjab, Faysal Bank Limited, Habib Metropolitan Bank Limited, PICIC Commercial Bank Limited

3P

rdP Tier Banks Include: Atlas Bank Limited, Bank Al Habib Limited, Bank of Khyber,

Bank Islami Pakistan, Crescent Commercial Bank Limited, JS Bank Limited, KASB Bank Limited, Meezan Bank Limited, My Bank Limited, NIB Bank Limited, Saudi Pak Commercial Bank Limited, Soneri Bank Ltd.

Offer for Sale of Ordinary Shares Arif Habib Bank Limited

TABLE OF CONTENTS

TU1UT TUAPPROVALS AND LISTING AT THE STOCK EXCHANGEUT .......................................................... 1 TU2UT TUSHARE CAPITAL AND RELATED MATTERSUT.................................................................................. 3 TU3UT TUUNDERWRITING, COMMISSIONS, BROKERAGE, AND OTHER EXPENSESUT...................... 10 TU4UT TUHISTORY AND PROSPECTSUT .............................................................................................................. 12 TU5UT TUFINANCIAL INFORMATIONUT ............................................................................................................ 18 TU6UT TUMANAGEMENT AND RELATED MATTERSUT ................................................................................. 24 TU7UT TUMISCELLANEOUS UT................................................................................................................................ 28 TU8UT TUAPPLICATION AND TRANSFER INSTRUCTIONSUT ...................................................................... 34 TU9UT TUSIGNATORIES TO THE OFFER FOR SALE DOCUMENTUT.......................................................... 38 TU10UT TUMEMORANDUM OF ASSOCIATIONUT................................................................................................ 39 11. APPLICATION FORMS

Offer for Sale of Ordinary Shares Arif Habib Bank Limited

- 1 -

PART 1

1 APPROVALS AND LISTING AT THE STOCK EXCHANGE

1.1 APPROVAL OF THE SECURITIES & EXCHANGE COMMISSION OF PAKISTAN

The approval of the Securities & Exchange Commission of Pakistan (“SECP” or “the Commission”) has been obtained for the issue, circulation, and publication of this Offer for Sale Document (“OFSD”) as required under section 62, read with section 57 and section 61 of the Companies Ordinance, 1984 (“the Ordinance”).

It must be distinctly understood that in giving this approval, the SECP does not take any responsibility for the financial soundness of any scheme stated herein or for the correctness of any of the statements made or opinions expressed with regard to them.

The SECP has not evaluated the quality of the offer, including justification for the premium, and its approval of the offer should not be construed as any commitment to the same. The public / investors should conduct their own independent investigation and analysis regarding the quality of the offer before subscribing.

1.2 CLEARANCE OF THE OFFER FOR SALE DOCUMENT BY THE STOCK EXCHANGE

The OFSD has been cleared by the Karachi Stock Exchange (Guarantee) Limited (“KSE” or “the Stock Exchange”) in accordance with the requirements of its Listing Regulations. While clearing this OFSD, the Stock Exchange neither guarantees the correctness of the contents of this document nor the viability of Arif Habib Bank Limited (“AHBL” or “the Bank”).

The Stock Exchange has not evaluated the quality of the issue, including the justification for the premium and its approval should not be construed as any commitment to the same. The public / investors should conduct their own independent investigation and analysis regarding the quality of the offer before subscribing.

1.3 FILING OF THE OFFER FOR SALE DOCUMENT AND OTHER DOCUMENTS WITH THE REGISTRAR OF COMPANIES

On behalf of Arif Habib Securities Limited (“AHSL” or “the Offerer”), the Bank has delivered to the Registrar of Companies, Companies Registration Office (“CRO”), Karachi, as required under section 57(3) and 57(4) of the Ordinance, a copy of the OFSD signed on behalf of AHSL, together with the following documents attached hereto:

(a) A letter dated October 22, 2007 from the Auditors of the Bank, M/s. M. Yousuf Adil Saleem & Co., Chartered Accountants, consenting to the publication of their name in the OFSD, as required under section 55 of the Companies Ordinance, 1984, which contains in Part V certain statements and reports issued by them as experts (which consent has not been withdrawn).

(b) Written confirmations of the Auditors, Legal Advisor, and Bankers to the Offer mentioned in this OFSD consenting to act in their respective capacities, as required under section 57(5) of the Ordinance.

(c) Copies of material contracts and agreements mentioned in Part 7.8 of this OFSD as required under section 57(4) of the Ordinance.

(d) Consent of the Directors and Chief Executive of the Bank who have consented to their respective appointments being made and their having been named or described as such Directors and Managing Director / Chief Executive in this OFSD, as required under Section 57(3) of the Ordinance, read with sub-clause (1) of clause (4) of part 1 of the second schedule of the Ordinance.

Offer for Sale of Ordinary Shares Arif Habib Bank Limited

- 2 -

1.4 LISTING AT THE STOCK EXCHANGE

An application has been made to the Karachi Stock Exchange for permission to deal in and for the quotation of the shares of the Bank.

The Bank shall stand provisionally listed for trading and for the quotation of its shares on the Exchange from the date of publication of OFSD, or any other date as may be specified by the KSE under the “Regulation for Future Trading in Provisionally Listed Companies”.

If for any reason, the application for formal listing is not accepted by the Stock Exchange, the Bank undertakes that a notice to that effect will immediately be published in the press, and thereafter application money to the applicants will be refunded in pursuance of this Offer for Sale Document, as required under the provisions of section 72 of the Ordinance.

Offer for Sale of Ordinary Shares Arif Habib Bank Limited

- 3 -

PART 2

2 SHARE CAPITAL AND RELATED MATTERS

2.1 SHARE CAPITAL

No. of shares Face value Premium Total AUTHORIZED CAPITAL

600,000,000 Ordinary shares of Rs. 10/- each 6,000,000,000 6,000,000,000

ISSUED, SUBSCRIBED, & PAID

UP CAPITAL

Issued for cash

428,500,000 Ordinary shares of Rs. 10/- each 4,285,000,000 1,500,000,000 5,785,000,000 Other than cash

21,500,000 Ordinary shares of Rs. 10/- each 215,000,000 - 215,000,000

450,000,000 Total 4,500,000,000 1,500,000,000 6,000,000,000

No. of shares Face value Premium Total THE EXISTING ISSUED, SUBSCRIBED & PAID UP CAPITAL OF THE BANK IS HELD AS FOLLOWS:

Directors of the Bank 1 Mr. Arif Habib 10 - 101 Mr. Salim Chamdia 10 - 10

1,000,001 Mr. Nasim Beg 10,000,010 - 10,000,01015,001 Syed Ajaz Ahmed 150,010 - 150,01075,001 Mr. Asad Ullah Khawaja 750,010 250,000 1,000,010

1 Mr. Abdul Hamid Miah 10 - 10 Shares held by Sponsors

417,082,292 M/s. Arif Habib Securities Ltd. 4,170,822,920 1,497,232,500 5,668,055,420 Others

29,500,000 Rupali Bank Limited 295,000,000 - 295,000,0002,327,702 Arif Habib Group Employees 23,277,020 2,517,500 25,794,520

450,000,000 Total 4,500,000,000 1,500,000,000 6,000,000,000

PRESENT OFFER No. of shares Face value Premium Total

2,987,425 Employees of the Bank 29,874,250 32,861,675 62,735,92556,761,075 General Public 567,610,750 624,371,825 1,191,982,57559,748,500 TOTAL 597,485,000 657,233,500 1,254,718,500

UNotesU: (i) As per SBP licence condition (i) the Bank shall be a public limited company and listed on the stock

exchange(s) and a minimum of 50% shares shall be offered to the general public within 2 years. The Bank through letter (BPRD (LCGD-04)/625-71/26573/2007/0682) dated October 09, 2007, has obtained NOC from the State Bank of Pakistan for divestment of 149.74 million shares to the general public.

(ii) As per SBP licence condition ix, sponsor directors shall not dispose off their shares for an initial period of 3 years and thereafter only with the specific written approval of the SBP.

(iii) In case of oversubscription, the Offerer shall exercise the Greenshoe option, and offer up to 60,000,000 (13.33% of paid up capital) additional ordinary shares out of Offerer’s shareholding in the Bank.

(iv) The Board of Directors of Arif Habib Securities Limited in the meeting held on October 29, 2007, has approved specie distribution of 1 share of Arif Habib Bank Limited (AHBL) for every 10 shares of Arif Habib Securities Limited (AHSL) held by its shareholders. Accordingly, a total of 30 million shares of AHBL will be issued to the shareholders of AHSL.

Offer for Sale of Ordinary Shares Arif Habib Bank Limited

- 4 -

(v) As per Rule 3(I) (IV) of the Companies (Issue of Capital) Rules, 1996, the sponsors shall, at all times, retain at least twenty five per cent (25%) of the paid-up capital of the Bank.

(vi) As per Listing Regulation No. 6(A) (7) of the KSE, sponsors’ shareholding in excess of 25% shall not be saleable for a period of six months from the date of public subscription.

(vii) The employees of the Bank have been given a preferential allocation of 2,987,425 ordinary shares (comprising of 5% of the total shares offered excluding the Greenshoe option) in the Offer for Sale of the Bank’s shares to which they will subscribe on the day of public subscription.

(viii) The shares subscribed by the employees of the Bank shall not be saleable for a period of 6 months from the date of public subscription as per Listing Regulation 6(A) 7(ii).

(ix) On 08 April, 2006, 21,500,000 shares of Rs. 10/- each amounting to the total value of Rs. 215,000,000/- were issued for consideration other than cash, pursuant to the scheme of amalgamation of Rupali Bank Limited (Pakistan operations) with and into Arif Habib Rupali Bank Limited.

2.2 OPENING AND CLOSING OF SUBSCRIPTION LIST

The subscription list will Insha’Allah open on 29 December, 2007 at the commencement of banking hours and will close on 31 December, 2007 at the close of banking hours.

2.3 INVESTOR ELIGIBILITY

All Pakistani residents, provident funds/trusts, pension/gratuity funds (subject to the term of their trust deeds), financial institutions and companies, body corporate or other legal entities (to the extent permitted by their constitutive or corporate documents, as the case may be) are allowed to subscribe to the shares offered to the general public.

2.4 OFFER PRICE, MINIMUM AMOUNT OF APPLICATION, AND BASIS OF ALLOTMENT OF SHARES

(a) This offer is being made at a price of Rs. 21/- per share of par value of Rs. 10 each. The offer price includes a premium of Rs. 11 per share.

(b) Applications must be made for 500 shares or in multiples of 500 shares only. Applications, which are neither for 500 shares nor for multiples of 500 shares, shall be rejected.

(c) The minimum amount of application for subscription of 500 shares both in cases of physical transfer and transfer under book-entry system is Rs. 10,500/-. The transfer fee shall be borne by the Offerer.

(d) Application for shares below the value of Rs. 10,500/- will not be entertained.

(e) FICTITIOUS AND MULTIPLE APPLICATIONS (MORE THAN ONE APPLICATION BY A SINGLE APPLICANT) ARE PROHIBITED AND SUCH APPLICATION MONEY SHALL BE LIABLE TO CONFISCATION UNDER SECTION 18-A OF THE SECURITIES AND EXCHANGE ORDINANCE, 1969.

(f) If the shares to be offered to the general public are sufficient for the purpose to accommodate all the applications then, all applications shall be accommodated.

(g) If this offer is oversubscribed in terms of number of applications and amount, the shares will be allotted by conducting computer balloting in the presence of representatives of the Stock Exchange in the following manner:

i. If all applications for 500 shares can be accommodated, then all such applications will be

accommodated first. If all applications for 500 shares cannot be accommodated, then balloting will be held among the applications for 500 shares only.

ii. If all applications for 500 shares have been accommodated, and shares are still available for allocation,

then all applications for 1,000 shares will be accommodated. If all applications for 1,000 shares cannot be accommodated, then balloting will be held among applications for 1,000 shares only.

Offer for Sale of Ordinary Shares Arif Habib Bank Limited

- 5 -

iii. If all applications for 500 shares and 1,000 shares have been accommodated, and shares are still available for allocation, then all applications for 1,500 shares will be accommodated. If all applications for 1,500 shares cannot be accommodated, then balloting will be held among applications for 1,500 shares only.

iv. If all applications for 500, 1,000 and 1,500 shares have been accommodated, and shares are still

available for allotment, then all applications for 2,000 shares will be accommodated. If all applications for 2,000 shares cannot be accommodated, then balloting will be held among applications for 2,000 shares only.

v. After the allotment in the above mentioned manner, the balance shares, if any, will be allotted in the

following manner:

1. If the remaining shares are sufficient to accommodate each application for over 2,000 shares, then 2,000 shares will be allotted to each applicant and the remaining shares will be allotted on a pro-rata basis.

2. If the remaining shares are not sufficient to accommodate all remaining applications for at least

2,000 shares, then balloting will be conducted for allocation of 2,000 shares to each successful applicant.

(h) If the offer is over subscribed in terms of amount only, then the allocation of shares will be made in the

following manner:

(i) First preference will be given to applicants who applied for 500 shares; (ii) Next preference will be given to applicants who applied for 1,000 shares; (iii) Next preference will be given to applicants who applied for 1,500 shares;

(iv) Next preference will be given to applicants who applied for 2,000 shares; (v) After allocation in the above manner, the balance shares, if any, will be allotted on pro- rata basis to the applicants who applied for more than 2,000 shares.

(i) Allocation of shares will be subject to the scrutiny of the applications.

(j) Applications, which do not meet the aforementioned requirements, or applications which are incomplete, will be rejected.

(k) This is an “Offer for Sale” of 59,748,500 ordinary shares (13.28% of paid up capital) of the Bank by the Offerer out of its shareholding in the Bank through the Karachi Stock Exchange. In case of oversubscription, the Offerer shall exercise greenshoe option, and offer up to 60,000,000 additional ordinary shares (13.33% of paid up capital) out of its shareholding in the Bank.

2.5 REFUND OF SUBSCRIPTION MONEY TO UNSUCCESSFUL APPLICANTS

The Bank on behalf of the Offerer, shall take a decision within 10 days of the closure of the subscription list as to which applications have been accepted or are successful. Refund of money in case of unaccepted or unsuccessful applications will be made within 10 days of the date of such decision, as required under the provisions of section 71 of the Ordinance.

As per sub-section (2) of section 71 of the Ordinance, if the refund as required by sub-section 1 of section 71 of the Ordinance is not made within the time specified therein, the Offerer shall be liable to repay the money with surcharge at the rate of 1.5%, for every month or part thereof from the expiration of the 15P

thP day and, in addition,

to a fine not exceeding Rs. 5,000 and in the case of continuing offence, to a further fine not exceeding Rs. 100 per day after the said 15P

thP day of which default continues. Provided, the Offerer shall not be liable if it proves that the

default in making the refund was not due to misconduct or negligence on its part.

Offer for Sale of Ordinary Shares Arif Habib Bank Limited

- 6 -

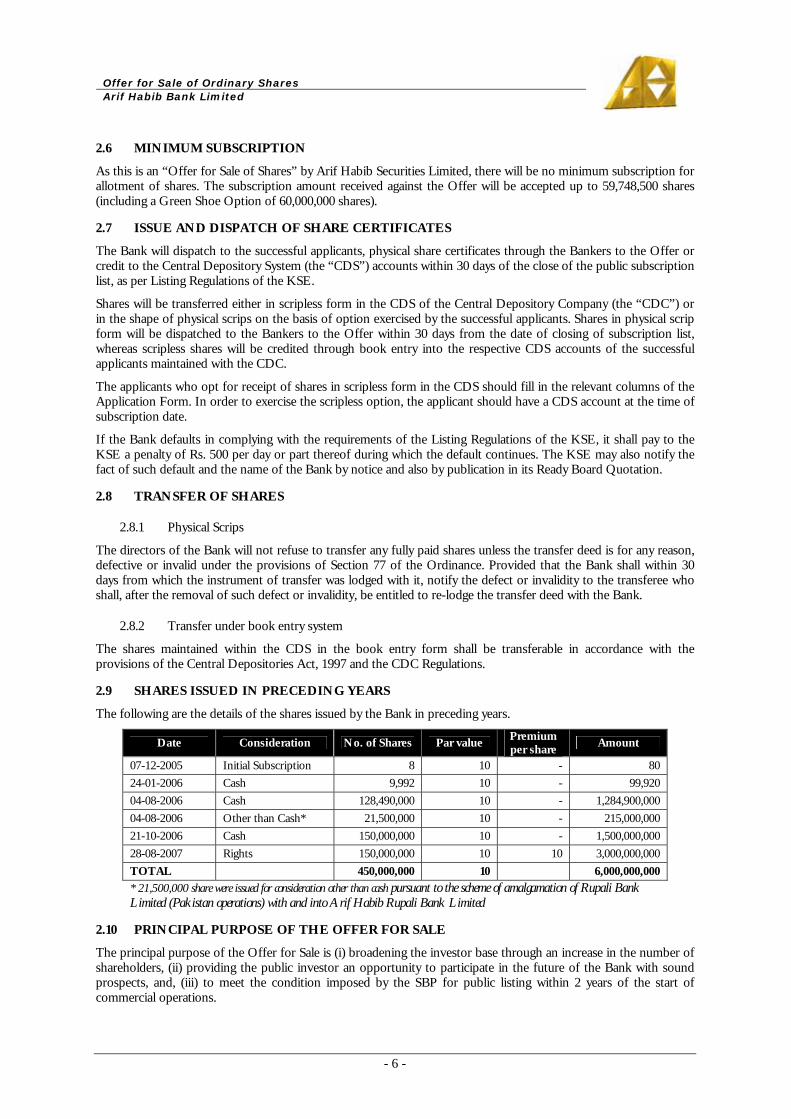

2.6 MINIMUM SUBSCRIPTION

As this is an “Offer for Sale of Shares” by Arif Habib Securities Limited, there will be no minimum subscription for allotment of shares. The subscription amount received against the Offer will be accepted up to 59,748,500 shares (including a Green Shoe Option of 60,000,000 shares).

2.7 ISSUE AND DISPATCH OF SHARE CERTIFICATES

The Bank will dispatch to the successful applicants, physical share certificates through the Bankers to the Offer or credit to the Central Depository System (the “CDS”) accounts within 30 days of the close of the public subscription list, as per Listing Regulations of the KSE.

Shares will be transferred either in scripless form in the CDS of the Central Depository Company (the “CDC”) or in the shape of physical scrips on the basis of option exercised by the successful applicants. Shares in physical scrip form will be dispatched to the Bankers to the Offer within 30 days from the date of closing of subscription list, whereas scripless shares will be credited through book entry into the respective CDS accounts of the successful applicants maintained with the CDC.

The applicants who opt for receipt of shares in scripless form in the CDS should fill in the relevant columns of the Application Form. In order to exercise the scripless option, the applicant should have a CDS account at the time of subscription date.

If the Bank defaults in complying with the requirements of the Listing Regulations of the KSE, it shall pay to the KSE a penalty of Rs. 500 per day or part thereof during which the default continues. The KSE may also notify the fact of such default and the name of the Bank by notice and also by publication in its Ready Board Quotation.

2.8 TRANSFER OF SHARES

2.8.1 Physical Scrips

The directors of the Bank will not refuse to transfer any fully paid shares unless the transfer deed is for any reason, defective or invalid under the provisions of Section 77 of the Ordinance. Provided that the Bank shall within 30 days from which the instrument of transfer was lodged with it, notify the defect or invalidity to the transferee who shall, after the removal of such defect or invalidity, be entitled to re-lodge the transfer deed with the Bank.

2.8.2 Transfer under book entry system

The shares maintained within the CDS in the book entry form shall be transferable in accordance with the provisions of the Central Depositories Act, 1997 and the CDC Regulations.

2.9 SHARES ISSUED IN PRECEDING YEARS

The following are the details of the shares issued by the Bank in preceding years.

Date Consideration No. of Shares Par value Premium per share

Amount

07-12-2005 Initial Subscription 8 10 - 8024-01-2006 Cash 9,992 10 - 99,92004-08-2006 Cash 128,490,000 10 - 1,284,900,00004-08-2006 Other than Cash* 21,500,000 10 - 215,000,00021-10-2006 Cash 150,000,000 10 - 1,500,000,00028-08-2007 Rights 150,000,000 10 10 3,000,000,000TOTAL 450,000,000 10 6,000,000,000

* 21,500,000 share were issued for consideration other than cash pursuant to the scheme of amalgamation of Rupali Bank Limited (Pakistan operations) with and into Arif Habib Rupali Bank Limited

2.10 PRINCIPAL PURPOSE OF THE OFFER FOR SALE

The principal purpose of the Offer for Sale is (i) broadening the investor base through an increase in the number of shareholders, (ii) providing the public investor an opportunity to participate in the future of the Bank with sound prospects, and, (iii) to meet the condition imposed by the SBP for public listing within 2 years of the start of commercial operations.

Offer for Sale of Ordinary Shares Arif Habib Bank Limited

- 7 -

2.11 INTEREST OF SHAREHOLDERS

None of the shareholders of the Bank have any special or other interest in the property or profits of the Bank, other than as shareholders of the Bank.

2.12 DIVIDEND POLICY

The rights in respect of capital and dividends attached to each share are and will be the same. AHBL in general meeting may declare dividends but no dividends shall exceed the amount recommended by the directors.

The directors may from time to time pay to the members such interim dividends as appear to the directors to be justified by the profits of the Bank. No dividends shall be paid otherwise than out of the profits of the Bank for the year or any other undistributed profits. No unpaid dividend shall bear interest or mark-up against the Bank. The dividend shall be paid within the period stipulated in the Ordinance.

2.13 ELIGIBILITY FOR DIVIDEND

The disinvested shares of the Bank shall rank pari passu with the existing ordinary shares in all matters including the right to such bonus or right issue and dividend, as may be declared by the Bank subsequent to the date of this OFSD. No dividends have been declared by the Bank till the date of the publication of Offer for Sale Document.

2.14 DEDUCTION OF ZAKAT

Income distribution will be subject to the deduction of Zakat at source pursuant to the provisions of the Zakat and Ushr Ordinance, 1980 (XVIII of 1980).

2.15 WITHHOLDING TAX ON DIVIDENDS

Dividend distribution to the shareholders will be subject to withholding tax at source under section 150 of the Income Tax Ordinance, 2001 (“IT Ordinance”) at the rate of 10% for all shareholders as per the Finance Bill, 2007. The tax will be deducted at source and will be deemed to be full and final liability in respect of such profits.

2.16 EXEMPTION FROM CAPITAL GAINS

Capital gains derived from the sale of listed securities are not liable to income tax pursuant to clause (110) of part 1 of the second schedule of the Income Tax Ordinance. This exemption is presently available up to the income year ending June 30, 2008.

2.17 CAPITAL VALUE TAX (CVT) & WITHHOLDING TAX ON SALE / PURCHASE OF SHARES

Pursuant to the provision of section 233(A) of the Income Tax Ordinance and Capital Value Tax (Finance Act 1989) the following charges are applicable on sale and purchase of securities:

(a) 0.02% CVT will be charged on purchase of all shares, modaraba certificates, and instruments of redeemable capital as defined in the Ordinance.

(b) 0.01% WHT will be charged on sale of all shares, modaraba certificates, and instruments of redeemable capital as defined in the Ordinance.

2.18 DEFERRED TAXATION

Deferred tax is recognized using the balance sheet liability method on all temporary differences between the amounts attributed to the assets and liabilities for financial reporting purposes and amounts used for taxation purposes. Deferred tax is not recognized on differences relating to investments in subsidiaries to the extent that they are not likely to reverse in the foreseeable future. Deferred tax asset is measured at the tax rates that are expected to be applied to the temporary differences, based on the laws that have been enacted or substantively enacted at the reporting date. A deferred tax asset is recognized only to the extent that it is probable that future taxable profits will be available against which the assets can be utilized.

As on August 31, 2007, the Bank has made a provision of PKR 33.432 million on account of deferred tax liability.

Offer for Sale of Ordinary Shares Arif Habib Bank Limited

- 8 -

2.19 JUSTIFICATION FOR THE PREMIUM

The premium of Rs. 11 per share on the face value of Rs 10 per share is considered adequately justified, based on the following:

Attractive valuation TP

1PT

At the price to book value (PBV) multiple of 1.54 X, the offer price is at a deep discount relative to the Bank’s peers.

Benchmark Sector Big banks 2nd tier banks 3rd tier banksBenchmark P/BV multiple TP

2PT 3.5 4.0 2.5 2.8

Fair value 47.64 54.44 34.03 38.11

Offer price at discount to fair value 55.91% 61.43% 38.28% 44.89% Prospects and synergies

The Bank has started its operations with a clear vision and a strategy to gradually expand its products and services, focusing on carefully chosen niches. Business development initiatives tap synergies with the Group concerns. This strategy, supported by positive growth outlook for the commercial banking sector, is expected to provide critical mass and solid foundation to build franchise value. The Bank has, within a short period of time, established nine on-line branches across four cities including Karachi, Lahore, Islamabad and Multan. Its roll-out plan is on course and it has achieved positive profits. Brand franchise The Group has had two successful listings of its financial sector companies: Arif Habib Securities Limited (listed in May 2001), and Arif Habib Limited (listed in December 2006). Both have significantly outperformed the KSE-100 index on a sustained basis as depicted below: Annualized total returns Time horizon

KSE-100 Index Company DifferenceArif Habib Securities Limited Jun 01-Oct 07 44.84% 127.73% + 82.89% Arif Habib Limited Jan 07-Oct 07 37.72% 123.65% + 85.93%Source: Bloomberg

The track record of these companies has created strong goodwill among the investing public.

TP

1PT For details regarding names of Big banks, Tier II banks, and Tier III banks, please refer to the glossary section

TP

2PT P/BV multiple: calculations are based on closing prices dated 02 November 2007, and book values as on September 2007

Offer for Sale of Ordinary Shares Arif Habib Bank Limited

- 9 -

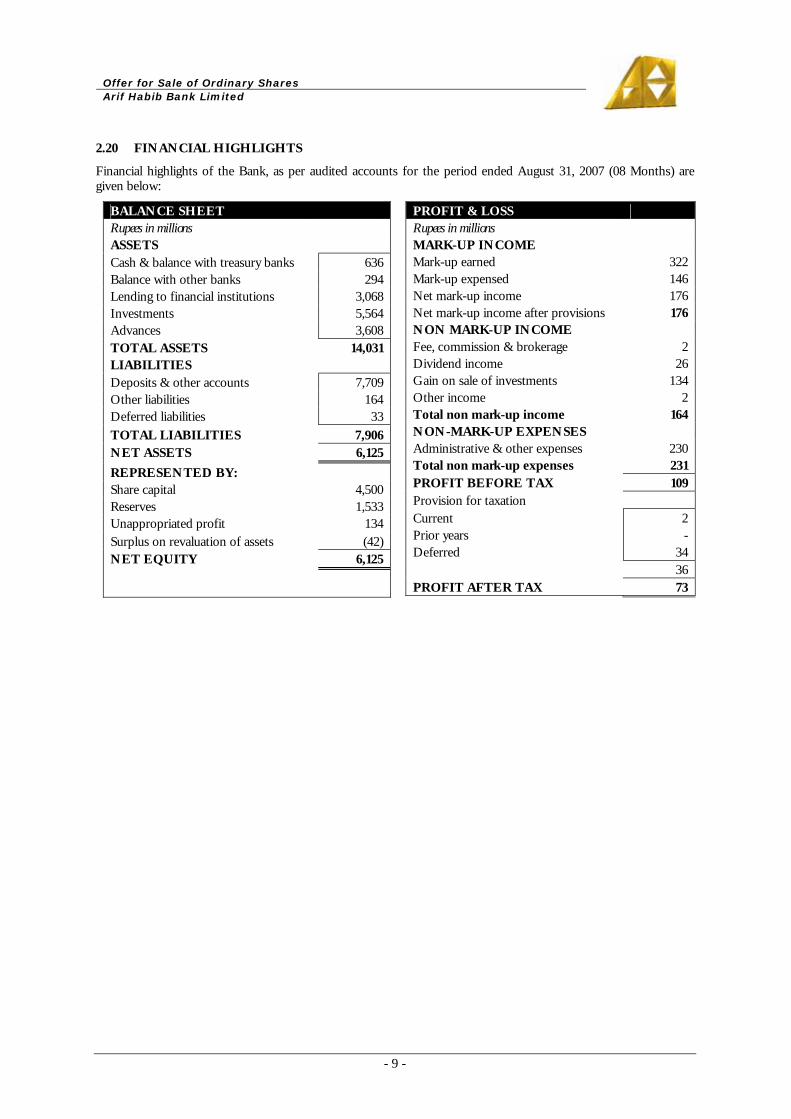

2.20 FINANCIAL HIGHLIGHTS

Financial highlights of the Bank, as per audited accounts for the period ended August 31, 2007 (08 Months) are given below:

BALANCE SHEET Rupees in millions ASSETS Cash & balance with treasury banks 636Balance with other banks 294Lending to financial institutions 3,068Investments 5,564Advances 3,608TOTAL ASSETS 14,031LIABILITIES Deposits & other accounts 7,709Other liabilities 164Deferred liabilities 33TOTAL LIABILITIES 7,906NET ASSETS 6,125

REPRESENTED BY: Share capital 4,500Reserves 1,533Unappropriated profit 134Surplus on revaluation of assets (42)NET EQUITY 6,125

PROFIT & LOSS Rupees in millions MARK-UP INCOME Mark-up earned 322Mark-up expensed 146Net mark-up income 176Net mark-up income after provisions 176NON MARK-UP INCOME Fee, commission & brokerage 2Dividend income 26Gain on sale of investments 134Other income 2Total non mark-up income 164NON-MARK-UP EXPENSES Administrative & other expenses 230Total non mark-up expenses 231PROFIT BEFORE TAX 109Provision for taxation Current 2Prior years -Deferred 34 36PROFIT AFTER TAX 73

Offer for Sale of Ordinary Shares Arif Habib Bank Limited

- 10 -

PART 3

3 UNDERWRITING, COMMISSIONS, BROKERAGE, AND OTHER EXPENSES

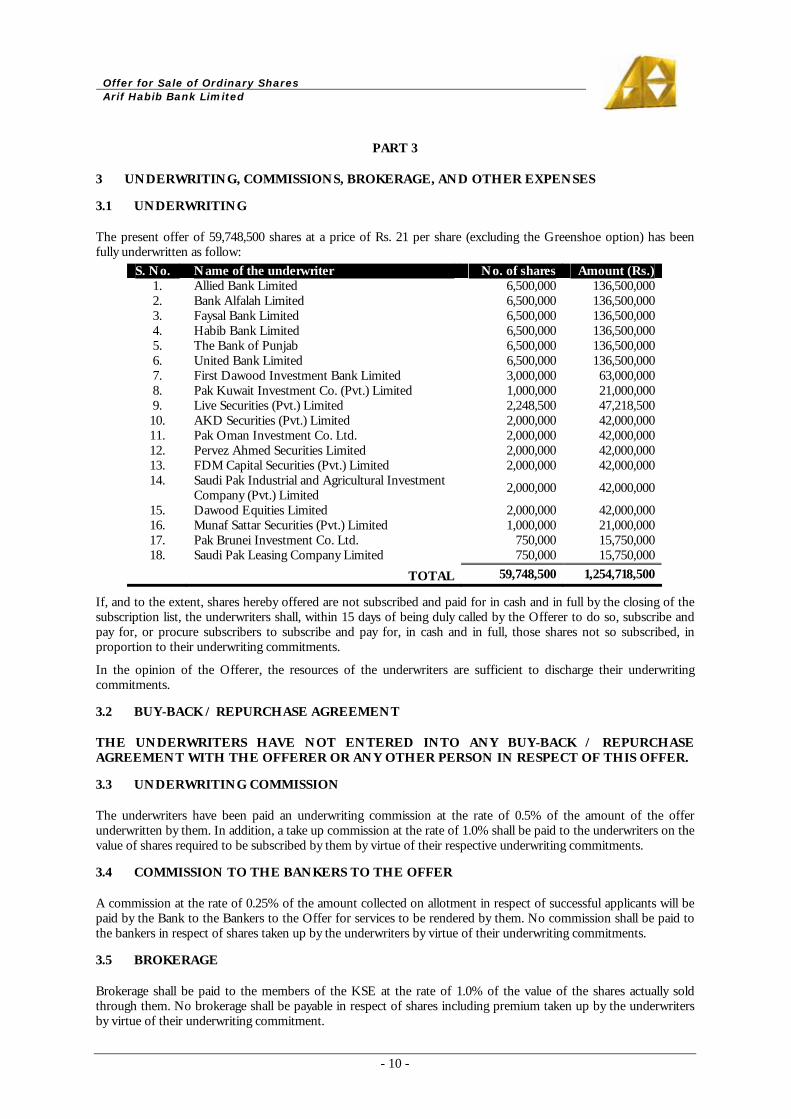

3.1 UNDERWRITING

The present offer of 59,748,500 shares at a price of Rs. 21 per share (excluding the Greenshoe option) has been fully underwritten as follow:

S. No. Name of the underwriter No. of shares Amount (Rs.)1. Allied Bank Limited 6,500,000 136,500,0002. Bank Alfalah Limited 6,500,000 136,500,0003. Faysal Bank Limited 6,500,000 136,500,0004. Habib Bank Limited 6,500,000 136,500,0005. The Bank of Punjab 6,500,000 136,500,0006. United Bank Limited 6,500,000 136,500,0007. First Dawood Investment Bank Limited 3,000,000 63,000,0008. Pak Kuwait Investment Co. (Pvt.) Limited 1,000,000 21,000,0009. Live Securities (Pvt.) Limited 2,248,500 47,218,50010. AKD Securities (Pvt.) Limited 2,000,000 42,000,00011. Pak Oman Investment Co. Ltd. 2,000,000 42,000,00012. Pervez Ahmed Securities Limited 2,000,000 42,000,00013. FDM Capital Securities (Pvt.) Limited 2,000,000 42,000,00014. Saudi Pak Industrial and Agricultural Investment

Company (Pvt.) Limited 2,000,000 42,000,000

15. Dawood Equities Limited 2,000,000 42,000,00016. Munaf Sattar Securities (Pvt.) Limited 1,000,000 21,000,00017. Pak Brunei Investment Co. Ltd. 750,000 15,750,00018. Saudi Pak Leasing Company Limited 750,000 15,750,000

TOTAL 59,748,500 1,254,718,500

If, and to the extent, shares hereby offered are not subscribed and paid for in cash and in full by the closing of the subscription list, the underwriters shall, within 15 days of being duly called by the Offerer to do so, subscribe and pay for, or procure subscribers to subscribe and pay for, in cash and in full, those shares not so subscribed, in proportion to their underwriting commitments.

In the opinion of the Offerer, the resources of the underwriters are sufficient to discharge their underwriting commitments.

3.2 BUY-BACK / REPURCHASE AGREEMENT

THE UNDERWRITERS HAVE NOT ENTERED INTO ANY BUY-BACK / REPURCHASE AGREEMENT WITH THE OFFERER OR ANY OTHER PERSON IN RESPECT OF THIS OFFER.

3.3 UNDERWRITING COMMISSION

The underwriters have been paid an underwriting commission at the rate of 0.5% of the amount of the offer underwritten by them. In addition, a take up commission at the rate of 1.0% shall be paid to the underwriters on the value of shares required to be subscribed by them by virtue of their respective underwriting commitments.

3.4 COMMISSION TO THE BANKERS TO THE OFFER

A commission at the rate of 0.25% of the amount collected on allotment in respect of successful applicants will be paid by the Bank to the Bankers to the Offer for services to be rendered by them. No commission shall be paid to the bankers in respect of shares taken up by the underwriters by virtue of their underwriting commitments.

3.5 BROKERAGE

Brokerage shall be paid to the members of the KSE at the rate of 1.0% of the value of the shares actually sold through them. No brokerage shall be payable in respect of shares including premium taken up by the underwriters by virtue of their underwriting commitment.

Offer for Sale of Ordinary Shares Arif Habib Bank Limited

- 11 -

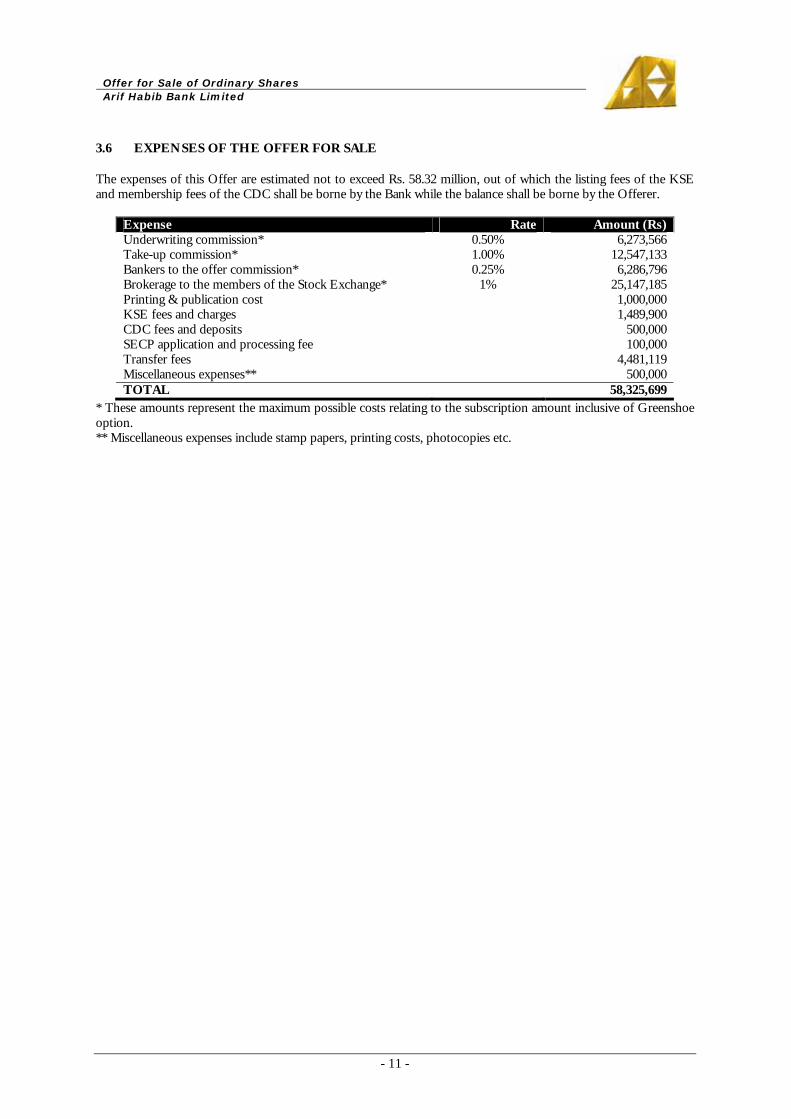

3.6 EXPENSES OF THE OFFER FOR SALE

The expenses of this Offer are estimated not to exceed Rs. 58.32 million, out of which the listing fees of the KSE and membership fees of the CDC shall be borne by the Bank while the balance shall be borne by the Offerer.

Expense Rate Amount (Rs)Underwriting commission* 0.50% 6,273,566Take-up commission* 1.00% 12,547,133Bankers to the offer commission* 0.25% 6,286,796Brokerage to the members of the Stock Exchange* 1% 25,147,185Printing & publication cost 1,000,000KSE fees and charges 1,489,900CDC fees and deposits 500,000SECP application and processing fee 100,000Transfer fees 4,481,119Miscellaneous expenses** 500,000TOTAL 58,325,699

* These amounts represent the maximum possible costs relating to the subscription amount inclusive of Greenshoe option. ** Miscellaneous expenses include stamp papers, printing costs, photocopies etc.

Offer for Sale of Ordinary Shares Arif Habib Bank Limited

- 12 -

PART 4 4 HISTORY AND PROSPECTS

4.1 HISTORY

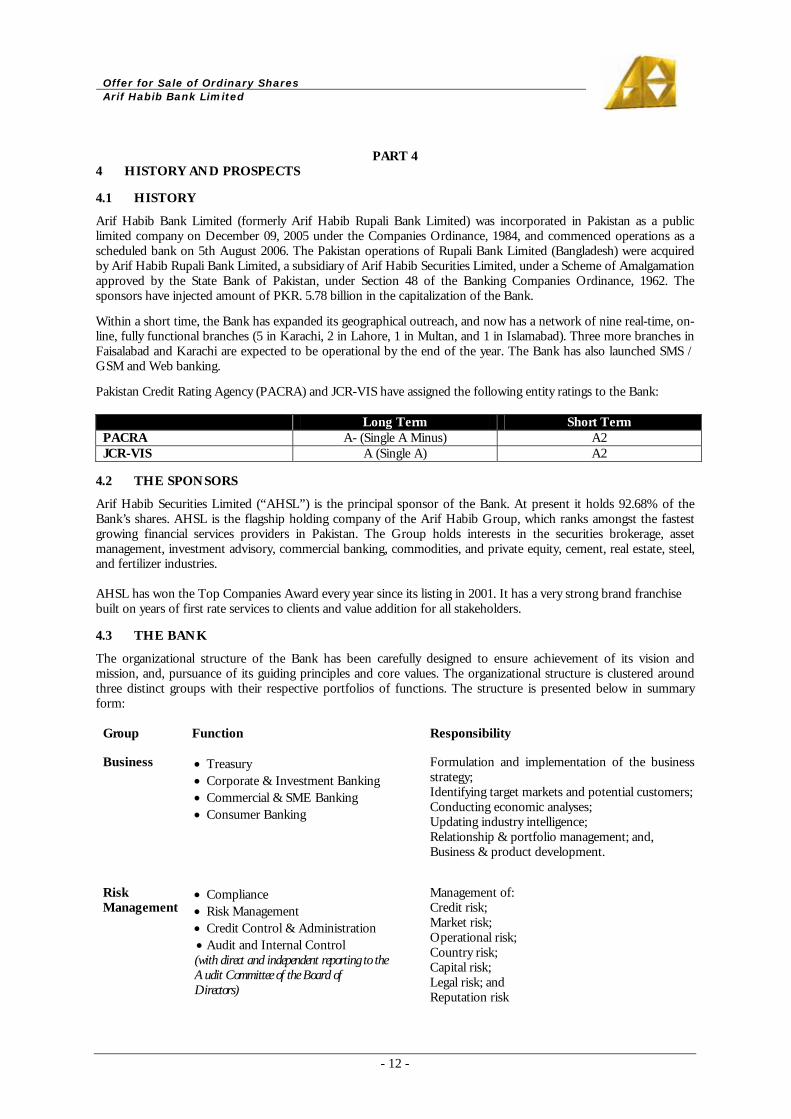

Arif Habib Bank Limited (formerly Arif Habib Rupali Bank Limited) was incorporated in Pakistan as a public limited company on December 09, 2005 under the Companies Ordinance, 1984, and commenced operations as a scheduled bank on 5th August 2006. The Pakistan operations of Rupali Bank Limited (Bangladesh) were acquired by Arif Habib Rupali Bank Limited, a subsidiary of Arif Habib Securities Limited, under a Scheme of Amalgamation approved by the State Bank of Pakistan, under Section 48 of the Banking Companies Ordinance, 1962. The sponsors have injected amount of PKR. 5.78 billion in the capitalization of the Bank. Within a short time, the Bank has expanded its geographical outreach, and now has a network of nine real-time, on-line, fully functional branches (5 in Karachi, 2 in Lahore, 1 in Multan, and 1 in Islamabad). Three more branches in Faisalabad and Karachi are expected to be operational by the end of the year. The Bank has also launched SMS / GSM and Web banking. Pakistan Credit Rating Agency (PACRA) and JCR-VIS have assigned the following entity ratings to the Bank:

Long Term Short Term PACRA A- (Single A Minus) A2 JCR-VIS A (Single A) A2

4.2 THE SPONSORS

TArif Habib Securities Limited (“AHSL”) is the principal sponsor of the Bank. At present it holds 92.68% of the Bank’s shares. AHSL is the flagship holding company of the Arif Habib Group, which ranks amongst the fastest growing financial services providers in Pakistan. The Group holds interests in the securities brokerage, asset management, investment advisory, commercial banking, commodities, and private equity, cement, real estate, steel, and fertilizer industries. AHSL has won the Top Companies Award every year since its listing in 2001. It has a very strong brand franchise built on years of first rate services to clients and value addition for all stakeholders.

4.3 THE BANK

The organizational structure of the Bank has been carefully designed to ensure achievement of its vision and mission, and, pursuance of its guiding principles and core values. The organizational structure is clustered around three distinct groups with their respective portfolios of functions. The structure is presented below in summary form:

Group Function Responsibility

Business • Treasury • Corporate & Investment Banking • Commercial & SME Banking • Consumer Banking

Formulation and implementation of the business strategy; Identifying target markets and potential customers; Conducting economic analyses; Updating industry intelligence; Relationship & portfolio management; and, Business & product development.

Risk Management

• Compliance • Risk Management • Credit Control & Administration • Audit and Internal Control (with direct and independent reporting to the Audit Committee of the Board of Directors)

Management of: Credit risk; Market risk; Operational risk; Country risk; Capital risk; Legal risk; and Reputation risk

Offer for Sale of Ordinary Shares Arif Habib Bank Limited

- 13 -

Support • Operations • Administration and Human

Resource Management • Finance • Information Technology • Strategic Planning & Development

Strong operating platform; Human resource management to foster creativity, team spirit, and performance driven culture; Credible financial and accounting practices in accordance with international standards, and commitment to full disclosure and transparency; Robust and secured IT infrastructure with the capability to generate real time MIS; Clearly define and devise business, operating, and risk management strategies, based on prevailing and anticipated market environment; and Provide support to enable each division of the Bank to fully meet customers’ expectations.

The management has implemented a sound risk management framework for prudent risk assumption, mitigation, and control. Clearly defined risk management policies and procedures are in place, which cover all activities of the Bank. The basic principles of these policies and procedures are to ensure that:

(i) Risk exposure remains within the limits established by the Board of Directors; (ii) Decisions are in line with the business strategy and objectives of the Bank; (iii) Expected payoffs adequately compensate for the risks assumed; (iv) Risk decisions are explicit and clear; (v) Prudential exposure limits are maintained; and, (vi) Business managers remain accountable for the risks they pass a judgment on.

The Bank is following a multi-tiered approach towards risk management. The ultimate risk management responsibility is vested with the Board of Directors. The Risk Management Group functions as the first line of defense. It comprises of three divisions – credit, compliance, and risk management. The Bank has a state of the art IT setup based on Sun Sparc and Sybase Adaptive Servers. The Bank is using hPLUS TM, a platform-independent, truly centralized, real time online banking application, as its Core Banking Module. All branches are connected through secured radio links for primary connectivity and DSL for secondary connectivity. The infrastructure supports all delivery channels with the capacity to handle 100 online branches. The system has the inbuilt flexibility to support 1000+ branches.

4.4 GROUP OVERVIEW

The Arif Habib Group ranks amongst the fastest growing financial services providers in Pakistan. The success has been made possible by a strong brand franchise built on decades of first-rate services to clients. The Group takes pride in its orientation towards client service. Its key success factors include continuous investment in staff, systems, capacity building, and its insistence on global best practices at all times. The Group holds interests in the securities brokerage, investment and financial advisory, investment management, commercial banking, commodities, private equity, cement, real estate, steel, and fertilizer industries. Several of the Group operations are synergetic and complementary. The Arif Habib Group, through independent entities, operates across the financial services industry:

Name of Group Company Industry / Major Business Arif Habib Securities Limited Investments & Holding Company Arif Habib Bank Limited Commercial Banking Arif Habib Investment Management Limited Asset Management Arif Habib Limited Securities Brokerage & Corporate Finance Pakistan Private Equity Management Limited Private Equity Arif Habib DMCC Commodities Brokerage

Offer for Sale of Ordinary Shares Arif Habib Bank Limited

- 14 -

4.5 SECTOR OVERVIEWTP

3PT

The stellar performance of Pakistani banks witnessed over the last five years stems from their exposure to one of the fastest growing economies in Asia. With one of the highest net interest margins in the region, the profitability of the sector is likely to remain strong over the medium term. High profitability over the last five years has induced the banks to invest in their systems, service capacity, infrastructure, and product development. Over the last five years, banks have been involved in cleaning up their balance sheets and building up the loan portfolios. The strategic thrusts for the future appear to be product innovation and exploration of un-served and under-served market segments. As capital requirements continue to rise and competition heats up, it is expected that banks will compete harder to gain market share and generate incremental returns.

4.5.1 Assets, liabilities, and equity

In the year 2006, the industry balance sheet size crossed the level of PKR 4 trillion. It witnessed a 17% growth in that year. The growth in assets is mainly funded through continued inflows of deposits, borrowings, and equity of the banking companies. Deposits have contributed 60 percent to the growth in total assets followed by equity and borrowings jointly accounting for 32 percent. The loans portfolio of commercial banks has grown from PKR 896 billion in the year 2000 to PKR 2,430 billion in 2006, recording a cumulative growth of over 170% over the six year period. Advances are concentrated in the corporate sector (53%) with a growing share of consumer loans and SME lending. During the year 2006, deposits of the banking system grew strongly at the rate of 13.1% on account of inward remittances, foreign direct / portfolio investments, expanding outreach, and aggressive marketing of products and services. During 2006, 17.4 percent of the growth in total assets was funded by the equity of the banks. This is reflected by an increase of Rs. 113 billion in the equity of banks in 2006 as compared to an increase of PKR 91 billion in 2005. One of the primary considerations for equity enhancement is the minimum capital requirement regime for the banks. The SBP has directed banks to increase their paid-up capital to at least PKR 6 billion by the end of 2009. Banks have undertaken capital injections in various forms such as fresh equity injection, stock dividends, and consolidation to meet the minimum capital requirements. It is expected that this trend will continue over the medium term.

4.5.2 Profitability

The banking sector has shown impressive profitability growth over the last five years. The sector has posted pre tax profits over PKR 123 billion for the year 2006. After tax profits surged to PKR 84 billion for the same period, recording YoY growth of 33%. Pakistani banks have enjoyed healthy net interest margins (NIM) in the recent past. This was made possible in part by the monetary tightening enforced by SBP to counter inflationary pressures. With deposit rates not moving in tandem with lending and investment returns, banks saw a sharp increase in spreads on a growing asset base. Over the last three years, banks have successfully maintained the increased spreads despite rise in deposit cost.

4.5.3 Outlook

The growth projections for the economy suggest that the momentum is likely to continue over the medium term. Deposit growth will likely be fueled by the steady flow of workers’ remittances and increase in banks’ outreach. Corporate credit demand is likely to grow at a slower pace in view of the monetary tightening. However, SME and agriculture sectors still hold immense potential to increase their share in the total loan mix. Interest spreads do not seem to face a rapid decline, which bodes well for continuous profitability of the industry.

3 Banking Survey 2005 – KPMG Taseer Hadi & Company Banking Sector Review 2005-06: State Bank of Pakistan

Offer for Sale of Ordinary Shares Arif Habib Bank Limited

- 15 -

Despite significant growth over the past five years, private sector debt / GDP ratio of 27 percent is still low in Pakistan as judged by cross country comparison. Likewise only 30-35 percent of the adult population has bank accounts. Agriculture and SME credit reaches only 1.5 and 0.17 million borrowers, respectively, and financing to these sectors, despite increases in recent times still accounts for a mere 5.9 percent and 17.4 percent of the total private sector credit. This presents a window of opportunity for banks to reduce the risk of slowdown in their growth. The sector dynamics dictate the need for diversification and outreach in terms of products and customer categories. Industry players are gearing up efforts to support the balance sheet growth and sustain profitability.

4.6 FUTURE PROSPECTS

The business strategy of the Bank is based on differentiation in products and services in carefully chosen market niches. The strategy is centered on exploitation of synergies with the Group concerns and capitalizing on the Group’s strengths, expertise, and brand equity in various disciplines of financial services. The market niches have been carefully chosen and prioritized on the basis of competitive strengths, level of competition, and sector dynamics. The roll out plans fully addresses the growth objectives and infrastructure / systems requirements. The business plan of the Bank is based on a “block building” principle. This calls for gradual addition of product and service lines, fully exploiting the competitive edge, and achieving strategic objectives in selected market niches. In line with its strategy of differentiation, the Bank has initially focused on corporate / wealth management. Based on the Group’s strength and expertise, the Bank is well-poised to emerge as the bank of choice in this under-served niche. The Bank has also rolled out corporate and investment banking services, targeting corporate and large commercial segments. These identified niches are expected to provide a critical mass in the near term, establishing a foundation to build a strong franchise. Medium term plans include the Bank’s entry into commercial mid-markets / SMEs, and the consumer finance segments. These comprise the core commercial banking segments. With the expansion in branch network, it is expected that these, together with cooperate banking activities will account for significantly larger proportion of the Bank’s total business going forward. From the very outset, the Bank aims to be fully compliant with all internal and external regulations. The management and the board are committed to follow the international best practices without fail. The Bank’s intentions to be compliant with the Basel II capital accord can be gauged from the fact that it started its operations with a Tier I capital well in excess of the minimum requirements. As of August 31, 2007 (audited figures), the Bank’s equity figures stood at PKR 6,125/- million. This implies large headroom for book expansion while still being fully in conformity with the Basel II capital requirements.

4.6.1 Geographical presence

The Bank is planning to establish a network of 100 branches (including several smart branches) by the year 2012. The branch expansion plan is based on centralized processing center i.e. “factory and boutique concept” with secure, real-time, and state of the art IT capability. This concept will enable the Bank to establish and configure extensive delivery channels with inherent cost efficiencies.

4.6.2 Deposit generation

The strategy on deposits is based on balanced growth in terms of tenor, size, cost, segmentation, and diversification. Corresponding to the branch expansion, the Bank plans to build business development teams to penetrate the mass market. The growth plan and the strategy are based on the idea of establishing cross selling channels in all operating divisions of the Bank as well as with other Group concerns.

4.6.3 Assets

To obtain the critical mass, the Bank is initially focusing on corporate and large commercial segments. This strategy is based on the principle of reaping the benefit of a large capital base, deployment of resources, and containment of credit risk. The Bank’s planned entry into the mid-market and consumer segments will further diversify the advances portfolio, improve the spread, and optimize the risks – returns profile.

Offer for Sale of Ordinary Shares Arif Habib Bank Limited

- 16 -

4.6.4 General banking

A state of the art technology base enables the Bank to establish cost efficient delivery channels. In addition, it also facilitates simultaneous roll out of products and services across the entire network.

4.6.5 Correspondent banking

The Bank is in the process of building correspondent banking relationships with various local and international institutions. At present, 23 local and 40 foreign banks have established such relationships with the Bank. A total of 150 correspondent relationships are targeted for 2008.

4.7 RISK FACTORS

The Offerer wishes to highlight the following risk factors, which may affect the returns on investment in the Bank:

Deposit cost risk Fixed cost deposits are exposed to interest rate risk. A rapid decline in interest rates may lead to the Bank’s marginal lending and investments at lower rates, while fixed term deposit rates may remain higher. The Bank plans to control and manage this risk through its deposit mobilization strategy. The strategy aims to maintain an optimal deposit mix, controlling the weighted average cost. The differentiation strategy of the Bank is focused towards the highest levels of client service, to ensure deposit retention. Interest rate risk Fixed rate advances and investments are exposed to interest rate risk. Interest rate fluctuations may affect the yield on these assets. The Bank’s treasury operation is managing the interest rate risk of fixed rate instruments, with a proactive asset allocation strategy. The lending portfolio is largely based on floating mark-up rates. This facilitates fair management of both assets and liabilities. Deposit growth risk The banking sector is becoming increasingly competitive and there is a risk that the deposit growth objectives of the Bank may not be achieved. The performance of the Bank during the last one year reflects the likely success of the Bank’s strategy. With the expansion in the branch network, products, and services, sustained deposit growth is expected. Operational risk The Bank is exposed to operational risk stemming from the nature of the business, complexity of financial instruments and products, and cyber banking. The management has assembled a team of qualified and experienced professionals to implement its growth strategy and manage risks in line with global best practices. The Bank has a state of the art IT infrastructure with real time MIS and risk analysis capability. A comprehensive risk management framework is in place, providing constant oversight to the front offices. The management is committed to adhere to the regulatory requirements and industry best practices in all areas of operations. Growth objectives are carefully balanced with the need to implement adequate systems and controls. Regulatory risk Changes in regulatory framework may affect the profitability of the Bank. Continued financial sector reforms and regulatory evolution in Pakistan have compelled banks to more actively manage their operations and continuously upgrade their systems and controls. The Bank, in line with the operating philosophy of the Group, is committed to comply with all regulatory requirements and standards of practice. Assessment and implementation of systems and controls remain dynamic, proactive, and continuous. Operational policies and procedures ensure compliance with regulatory requirements at all times. A case in point is the fact that the Bank is far ahead of several of its peers in terms of minimum capital requirement.

Offer for Sale of Ordinary Shares Arif Habib Bank Limited

- 17 -

Credit risk Like all lending institutions, the Bank is exposed to credit risk. Credit risk refers to the probability of overdue / defaults by borrowers of the Bank. The Bank has a separate credit and risk management function to oversee the credit and lending operations. Credit policies govern the building of assets and specify requirements in terms of limits, collateral, etc. Credit operations are aligned with the strategic objectives and balanced with a multi-tiered system of checks and controls. Competition risk The Bank may be affected by increasing competition in the industry. The stiffening competition may lead to rising cost of deposits and very competitive lending rates. The Bank’s strategy is based on carefully choosing niches to operate in, exploiting its expertise and the Group’s goodwill. This business model differentiates the Bank from various other players in the industry. The success of the Bank’s business model is likely to enhance its franchise value further. Capital market risk The investment portfolio of the Bank is exposed to capital market risk. Value of equity investment held by the Bank may be adversely affected if the stock market performs poorly. The proven expertise of the management to manage capital market operations and generate value in varying market conditions sufficiently mitigates this risk. The shareholders of AHBL will also be exposed to capital market risk. Share price of the Bank will be dependent upon its own as well as stock market’s performance. Currency risk The Bank has to maintain positions in foreign currency with respect to trade finance operations. More specifically, financing of international trade transactions give rise to the need of buying, selling, and holding foreign currencies. Any adverse movement in foreign exchange rates may reduce the value of foreign currency assets of the Bank.

This risk is considered adequately controlled by internally set country and currency limits and regulatory guidelines.

IT IS STATED THAT ALL MATERIAL RISK FACTORS WITH RESPECT TO THIS OFFER HAVE BEEN DISCLOSED AND NOTHING HAS BEEN CONCEALED.

Offer for Sale of Ordinary Shares Arif Habib Bank Limited

- 18 -

PART 5

5 FINANCIAL INFORMATION

5.1 AUDITORS’ CERTIFICATE UNDER SECTION 53(1) READ WITH SUB-SECTION 28, SECTION 2, OF PART 1 OF THE SECOND SCHEDULE OF THE COMPANIES ORDINANCE, 1984, FOR THE OFFER FOR SALE OF SHARES OF ARIF HABIB BANK LIMITED

01—08 /0547 October 22, 2007 The Board of Directors Arif Habib Bank Limited 2/1, R.Y. 16, Old Queens Road Karachi. Dear Sirs, Auditors’ report under section 53(1) read with clause 28 of section 2 of part 1 of the second schedule to the Companies Ordinance, 1984, for the purpose of inclusion in the Offer for Sale Document for listing on Stock Exchange(s) We have reviewed the audited financial statements of Arif Habib Bank Limited (the Bank) for the period ended December 31, 2006 and August 31, 2007, in accordance with section 53(1) read with clause 28 of section 2 of part 1 of the second schedule to the Companies Ordinance, 1984. 2. Modification in Auditor’s Reports Un-modified auditor’s reports were issued for the period ended December 31, 2006 and August 31, 2007. 3. Major Developments since incorporation 3.1 December 31, 2006

The Bank was incorporated in Pakistan as a public limited company on December 09, 2005 under the Companies Ordinance, 1984. The Bank obtained certificate of commencement of business from Securities and Exchange Commission of Pakistan on April 10, 2006. As at December 31, 2006, the bank had 7 branches. The State Bank of Pakistan sanctioned a scheme of amalgamation under section 48 of the Banking Companies Ordinance, 1962, on July 07, 2006 by virtue of which Rupali Bank Limited – Pakistan Branch (here-in-after referred as “RBL”) was amalgamated with the Bank on August 04, 2006. This scheme of amalgamation had been approved by the shareholders of the bank in an extraordinary general meeting held on May 17, 2006. The Bank obtained Certificate of Commencement of Business from SBP effective from August 05, 2006. According to the scheme all the properties, assets and liabilities and all the rights and obligations of RBL as at August 04, 2006 stood amalgamated with the bank.

3.2 August 31, 2007 3.2.1 Number of branches increased from 7 to 9 during the period. 4. Balance Sheet of Arif Habib Bank Limited 4.1 In accordance with Section 53(1) read with Clause 28(1) of Section 2 of Part I of the Second Schedule to

the Company Ordinance, 1984, we report that:

Offer for Sale of Ordinary Shares Arif Habib Bank Limited

- 19 -

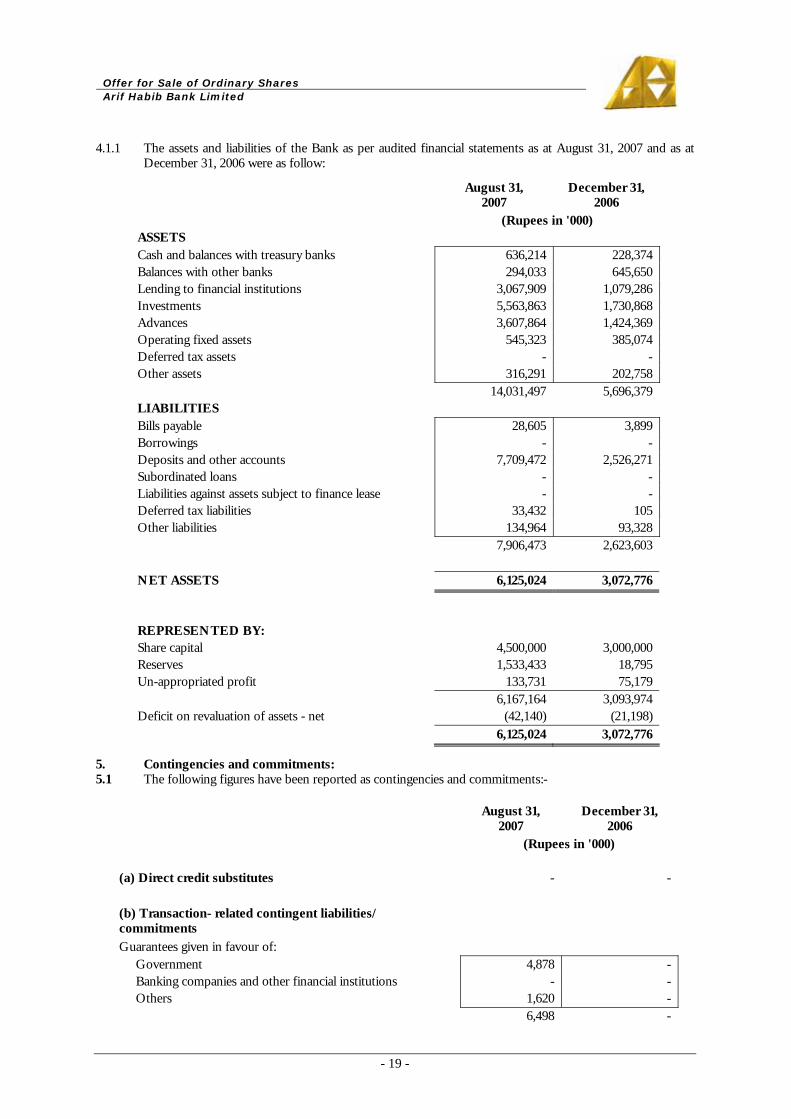

4.1.1 The assets and liabilities of the Bank as per audited financial statements as at August 31, 2007 and as at December 31, 2006 were as follow:

August 31, 2007

December 31, 2006

(Rupees in '000) ASSETS Cash and balances with treasury banks 636,214 228,374 Balances with other banks 294,033 645,650 Lending to financial institutions 3,067,909 1,079,286 Investments 5,563,863 1,730,868 Advances 3,607,864 1,424,369 Operating fixed assets 545,323 385,074 Deferred tax assets - - Other assets 316,291 202,758 14,031,497 5,696,379 LIABILITIES Bills payable 28,605 3,899 Borrowings - - Deposits and other accounts 7,709,472 2,526,271 Subordinated loans - - Liabilities against assets subject to finance lease - - Deferred tax liabilities 33,432 105 Other liabilities 134,964 93,328 7,906,473 2,623,603 NET ASSETS 6,125,024 3,072,776

REPRESENTED BY: Share capital 4,500,000 3,000,000 Reserves 1,533,433 18,795 Un-appropriated profit 133,731 75,179 6,167,164 3,093,974 Deficit on revaluation of assets - net (42,140) (21,198) 6,125,024 3,072,776

5. Contingencies and commitments: 5.1 The following figures have been reported as contingencies and commitments:-

August 31, 2007

December 31, 2006

(Rupees in '000) (a) Direct credit substitutes - - (b) Transaction- related contingent liabilities/ commitments

Guarantees given in favour of: Government 4,878 - Banking companies and other financial institutions - - Others 1,620 - 6,498 -

Offer for Sale of Ordinary Shares Arif Habib Bank Limited

- 20 -

(c) Trade-related contingent liabilities Letter of credit 98,118 - Acceptances - - 98,118 - (d) Other contingencies - claim against Bank not acknowledge as debt

83,903 83,903

(e) Commitments in respect of forward lending Forward call lending - - Forward repurchase agreement lending - 49,286 Commitments to extend credit - - - 49,286 (f) Commitment in respect of future contracts Purchase - 3,501 Sale - 26,736 - 30,237 (g) Commitments for the acquisition of operating assets Civil works 16,786 14,168 Acquisition of computer software 18,299 38,876 35,085 53,044 (h) Underwriting commitment - 50,000

(i) In the year 2005, Taxation Officer completed assessment for tax year 2003 of Rupali Bank Limited – Pakistan

Branch (RBL) and created an additional tax demand of Rs. 42.241 million on account of disallowance of provision made by RBL against non performing advances amounting to Rs. 89.12 million. The order of Commission of Income Tax was set aside by the Commissioner Income Tax (Appeals) vide its Order Nos. 65, 66 dated June 22, 2005 for reconsideration by the Taxation Officer, in the light of orders passed by higher forum in this context. RBL, as well as the tax department, have filed (Appeal) with Income Tax Appellate Tribunal against the order of the Commissioner of Income Tax Appeals which is pending. No provision has been made in this respect in these financial statements as in the opinion of Tax Consultants; the case is likely to decide in favour of RBL based on precedents.

6. Profit and loss accounts for the last financial years 6.1 The profit and loss accounts of the Bank for period ended December 31, 2006 and August 31, 2007 as per

audited financial statements are set out below:

August 31, 2007

December 31, 2006

(Rupees in '000) Mark-up / return / interest earned 322,010 142,802Mark-up / return / interest expensed (145,783) (23,309) 176,227 119,493

Provision against non-performing loans and advances - 24Provision for diminution in the value of investment - net - -Bad debts written off directly - - - 24Net mark-up / interest income after provisions 176,227 119,469

Offer for Sale of Ordinary Shares Arif Habib Bank Limited

- 21 -

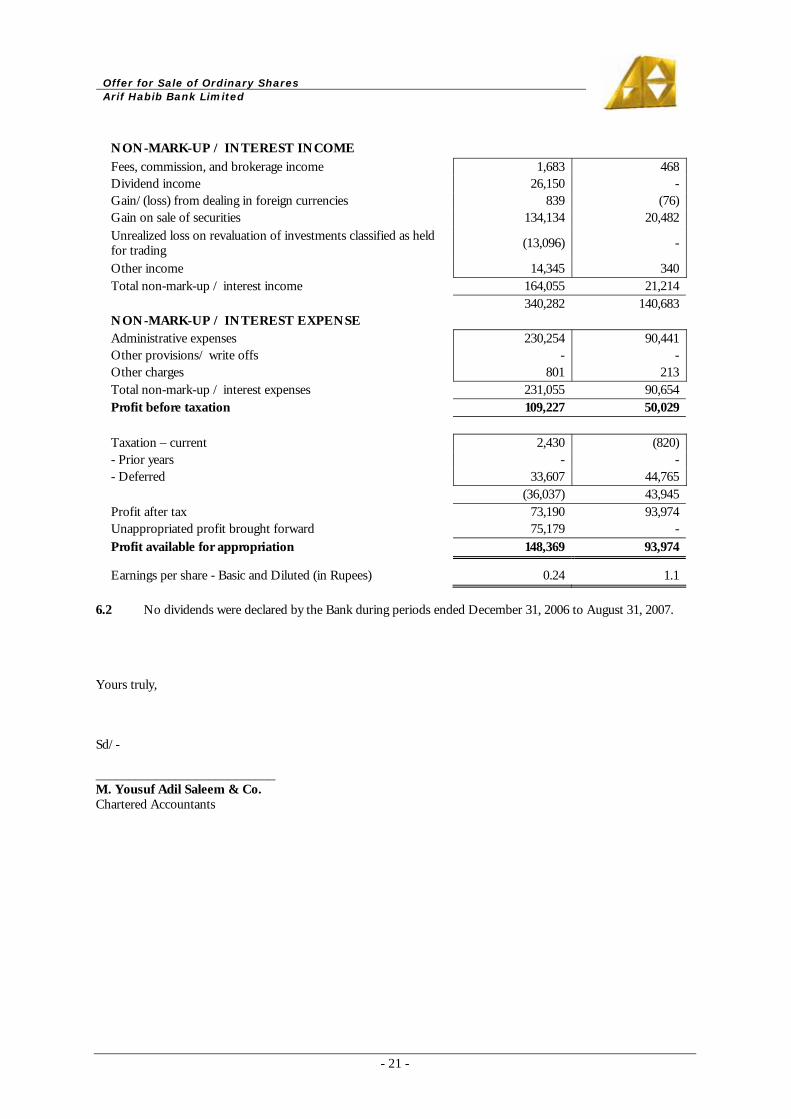

NON-MARK-UP / INTEREST INCOME

Fees, commission, and brokerage income 1,683 468Dividend income 26,150 -Gain/(loss) from dealing in foreign currencies 839 (76)Gain on sale of securities 134,134 20,482Unrealized loss on revaluation of investments classified as held for trading (13,096) -

Other income 14,345 340Total non-mark-up / interest income 164,055 21,214 340,282 140,683NON-MARK-UP / INTEREST EXPENSE Administrative expenses 230,254 90,441Other provisions/ write offs - -Other charges 801 213Total non-mark-up / interest expenses 231,055 90,654Profit before taxation 109,227 50,029 Taxation – current 2,430 (820)- Prior years - -- Deferred 33,607 44,765 (36,037) 43,945Profit after tax 73,190 93,974Unappropriated profit brought forward 75,179 -Profit available for appropriation 148,369 93,974

Earnings per share - Basic and Diluted (in Rupees) 0.24 1.1 6.2 No dividends were declared by the Bank during periods ended December 31, 2006 to August 31, 2007. Yours truly, Sd/- ___________________________ M. Yousuf Adil Saleem & Co. Chartered Accountants

Offer for Sale of Ordinary Shares Arif Habib Bank Limited

- 22 -

5.2 SHARE BREAK-UP VALUE CERTIFICATE

01—08 / 0546 October 22, 2007

The Board of Directors Arif Habib Bank Limited 2/1, R.Y. 16, Old Queens Road Karachi. Dear Sirs,

BREAKUP VALUE PER SHARE OF ARIF HABIB BANK LIMITED

We are pleased to confirm that the break-up value per share of Arif Habib Bank Limited as per the audited financial statements as at August 31, 2007 for each ordinary share of Rs. 10/- each has been worked out as under:

Rupees in “000”

Share capital 4,500,000

Reserves 1,533,433

Unappropriated profit 133,731

Deficit on revaluation of investment (42,140)

6,125,024

Number of ordinary shares 450,000,000

Break-up value per share (Rupees) 13.61

Yours truly,

Sd/-

___________________________ M. Yousuf Adil Saleem & Co. Chartered Accountants

Offer for Sale of Ordinary Shares Arif Habib Bank Limited

- 23 -

5.3 AUDITORS CERTIFICATE ON ISSUED, SUBSCRIBED, AND PAID UP CAPITAL OF THE BANK

01-08 / 0545 October 22, 2007

The Board of Directors Arif Habib Bank Limited 2/1, R.Y. 16, Old Queens Road Karachi.

Dear Sirs,

AUDITORS’ CERTIFICATE ON ISSUED, SUBSCRIBED, AND PAID-UP CAPITAL OF THE BANK

No. of shares Rupees (‘000)

428,500,000 Issued for cash 4,285,000

21,500,000 Issued for consideration other than cash 215,000

450,000,000 4,500,000

Yours truly,

Sd/-

___________________________ M. Yousuf Adil Saleem & Co. Chartered Accountants

5.4 FINANCIAL YEAR

The financial year of the Bank commences on the 1P

stP day of January and ends on the 31P

stP day of December of each

year.

Offer for Sale of Ordinary Shares Arif Habib Bank Limited

- 24 -

PART 6

6 MANAGEMENT AND RELATED MATTERS

6.1 BOARD OF DIRECTORS OF THE BANK

Name & Address Designation Directorship in other companies

Mr. Arif Habib

86/2, 10P

thP Street, Khayaban-e-Sehar,

Phase V, D.H.A, Karachi

Chairman

Arif Habib Securities Limited Pak Arab Fertilizer (Pvt.) Limited Arif Habib Equity (Pvt.) Limited Thatta Cement Company Limited

Fatima Fertilizer Company Limited Takaful Pakistan Limited

Essa Textiles & Commodities (Pvt.) Limited Arif Habib DMCC

Nooriabad Spinning Mills (Pvt.) Limited Al Ameera Arif Habib (Pvt.) Limited

Pakistan Premier Fund Limited Pakistan Private Equity Management Ltd.

Pakistan Security Printing Corp. Ltd. Real Estate Modaraba Management Ltd.

NCEL Building Management Ltd. Rotocast Engineering (Pvt.) Limited Sukh Chayn Gardens (Pvt.) Limited

Pakistan Engineering Company Limited Safe Mix Concrete Products (Pvt.) Limited

Mr. Kamal Uddin Khan

House No. 248, Street No. 5 Officer Colony, Old Cavalry Ground, Cantt. Lahore.

President / CEO None

Mr. Salim Chamdia

14 / 1, 2P

ndP Gizri Street, Phase - IV

D.H.A., Karachi.

Executive Director

Arif Habib Investment Management Limited Pak Arab Fertilizer (Pvt.) Limited

Al Ameera Arif Habib (Pvt.) Limited Essa Textile & Commodity (Pvt.) Limited

Lucky Cotton Mills (Pvt.) Limited Nooriabad Spinning Mills (Pvt.) Limited Salima Chamdia Securities (Pvt.) Limited

Sun Textile Mills (Pvt.) Limited

Mr. Nasim Beg

F-16 / 6, Block - 4, Clifton, Karachi.

Director

Arif Habib Securities Limited Arif Habib Investment Management Limited

Pak Arab Fertilizer (Pvt.) Limited Real Estate Modaraba Management Co. Ltd.

Pakistan Private Equity Management Limited. Essa Cement Industries Limited.

Javedan Cement Limited Rotocast Engineering (Pvt.) Limited

Syed Ajaz Ahmad

J-166, Block - 3, P.E.C.H.S, Karachi.

Director / Company Secretary

Arif Habib Securities Limited Pakistan Premier Fund Limited

Mr. Asad Ullah Khawaja

House No. 3A, 3P

rdP North Street

Phase - 1, D.H.A., Karachi.

Director

Arif Habib Securities Limited Murree Brewery Company Limited

Packages Limited Pakistan Private Equity Management Ltd.

PICIC Investment Management Ltd. Mr. Abdul Hamid Miah

34, Dilkusha, C/A, Dhaka, Bangladesh.

Director Rupali Bank Limited

Offer for Sale of Ordinary Shares Arif Habib Bank Limited

- 25 -

6.2 PROFILES OF THE DIRECTORS

6.2.1 Mr. Arif Habib – Chairman of the Board Mr. Arif Habib is a prominent member of the financial community and a first rate entrepreneur. He is the Chairman and Chief Executive Officer of Arif Habib Securities Limited. He has been associated with the Karachi Stock Exchange since 1971. He has the distinction of being elected Chairman / President of the Karachi Stock Exchange on six different occasions during the past fifteen years. Mr. Habib has contributed significantly towards key modernizations to the Pakistani capital markets. He is also the founding Chairman of the Central Depository Company of Pakistan, member of the board of Security Printing Corporation of Pakistan, and Chairman Pak Arab Fertilizer Limited, Fatima Fertilizer Company Limited, and Thatta Cement Company Limited. Mr. Habib holds a degree in commerce. 6.2.2 Mr. Kamaluddin Khan – President and CEO Mr. Kamaluddin Khan is a seasoned banker with over twenty five years of experience in the financial services industry. Mr. Khan joined Arif Habib Bank in January 2006 and has been instrumental in the implementation of its growth and business development strategy. Prior to joining the Group, he was associated with Societe Generale for over seven years, serving the bank as Area Manager, Lahore, and Regional Director, Middle East. During his tenure, he provided strategic direction to the bank’s corporate objectives in the Middle East, India, and Pakistan. He had also been associated with Mashreq Bank, Dubai as Vice President-Commercial Banking, and Bank of America as Vice President-International Private Banking. His core areas of expertise include investment and corporate banking, private banking, capital market operations, and structuring / distribution of derivatives. Mr. Khan holds an M.S. in Computer Science from Quaid-e-Azam University, Islamabad, and professional qualification in Investment Banking and Corporate Finance from Kellogg Graduate School of Management at Evanston, Northwestern University, USA. He has attended several training courses and workshops on banking and higher management skills. 6.2.3 Mr. Asadullah Khawaja Mr. Asadullah Khawaja is a senior professional with over four decades of work experience in the financial and industrial sectors. He was associated with the Investment Corporation of Pakistan from 1966 to 2000, serving the organization as Managing Director during the last five years of his tenure. His core areas of expertise include investment banking, project financing, investment advisory, credit analysis, capital market operations, and portfolio management. Presently, he is serving as the chairman of the boards of Packages Limited and PICIC Asset Management Company Limited. Mr. Khawaja has attended several professional training courses on public sector policy and management, investment analysis, and portfolio management, conducted by various institutes such as Harvard University, the World Bank, University of Pennsylvania, University of Cambridge, etc. 6.2.4 Mr. Nasim Beg A chartered accountant by profession, Mr. Nasim Beg is a seasoned professional and one of the leading figures in the asset management industry of Pakistan. He has been associated with the Group since 2000. His current position is as the Chief Executive Officer of Arif Habib Investment Management Limited. Mr. Beg has been responsible for development and growth of the Group’s mutual fund business from conceptual stage. His successful management and leadership have enabled the business to achieve significant growth on a sustained business. Prior to joining the Arif Habib Group, Mr. Beg served National Investment Trust as its Deputy Chief Executive. 6.2.5 Mr. Salim Chamdia Mr. Chamdia is a Chartered Accountant by profession. He is a former Chairman of the Karachi Stock Exchange and was the founder Chairman of National Commodity Exchange Limited. During the last several years, he has actively contributed towards the modernization of the Karachi Stock Exchange. 6.2.6 Mr. Md. Abdullah Hamid Miah A representative of Rupali group, Mr. Hamid Miah is the Managing Director of Rupali Bank Limited, Bangladesh. 6.2.7 Syed Ajaz Ahmed – Director and Company Secretary Mr. Ajaz Ahmed has been associated with the Group since 2001 and is currently serving as Head of Operations-Arif Habib Investment Management Limited. He has over a decade of work experience in asset management, audit, and financial consulting. Mr. Ahmed is a Fellow of Institute of Cost and Management Accountants of Pakistan and also holds a degree in law.

6.3 OVERDUE LOANS

There are no overdue loans (local or foreign currency) on the Bank or its Directors.

Offer for Sale of Ordinary Shares Arif Habib Bank Limited

- 26 -

6.4 NUMBER OF DIRECTORS

Pursuant to section 174(2) of the Ordinance, the number of directors of a listed company shall not be less than seven. At present, the Bank’s board of directors consists of seven directors.

6.5 DIVIDEND RECORDS OF OTHER LISTED COMPANIES IN WHICH DIRECTORS HOLD DIRECTORSHIPS

Name of Company 2007 2006 2005 2004 2003

Arif Habib Securities Limited 75% 322.33%B

100% 66.66%B

100% 50%B

150% 150%B

100% 33.33%B

Al-Abbas Cement Ind. Ltd. Nil Nil Nil Nil 5%

Javedan Cement Limited Nil 56.7% Nil Nil Nil

Murree Brewery Co. Ltd. 50% 10%B

50% 10%B

50% 10%B Nil 85%

Packages Limited Nil 60% 5%B 60% Nil 20%

20%B

Pakistan Premier Fund Ltd. 25% 15%B 40% 15%

25%B 12.5% 25%B

12.5%B

6.6 QUALIFICATION OF DIRECTORS

A director must be a member unless he is a person representing the Government or an institution or authority that is a member, or is a whole time working director who is an employee of the Bank, or a Chief Executive or a person representing a creditor. In case of directors representing special interests holding shares of the requisite value, no such share qualification shall be required provided intimation in writing as to such representation is lodged with the Bank within two months of the appointment of such directors.

6.7 ELECTION OF DIRECTORS

The directors shall comply with the provisions of sections 174 to 178, 180, and 184 of the Ordinance, relating to the election of directors and matters ancillary thereto. The present directors of the Bank were elected on March 31, 2007, for a period of three years.

6.8 REMUNERATION OF THE DIRECTORS

As per clause 64 of the Articles of Association of the Bank, “the remuneration of a Director for performing extra services, including holding of office of Chairman, and the remuneration to be paid to any Director for attending the meeting of Directors or a committee of Directors shall from time to time be determined by the Board in accordance with the Ordinance and the Banking Companies Ordinance”.

6.9 BENEFITS TO THE PROMOTERS AND OFFICERS DURING THE LAST TWO YEARS

No amount of benefits has been paid or given during the last two years or is intended to be paid or given to any promoter or to any officer of the Bank other than as remuneration for services rendered as whole-time executives of the Bank and such remuneration for services shall be borne by the Bank.

6.10 INTEREST OF DIRECTORS

The directors may be deemed to be interested to the extent of fees payable to them for attending board meetings. The directors performing whole time service to the Bank may also be deemed interested in the remuneration payable to them by the Bank. The directors may also be deemed to be interested, to the extent of any shares held by each of them in the Bank, the dividends to be declared by the Bank.

6.11 INTEREST OF DIRECTORS IN PROPERTY ACQUIRED BY THE BANK

None of the directors of the Bank have or have had any interest in any property acquired by the Bank in the last 2 years or now proposed to be acquired.

Offer for Sale of Ordinary Shares Arif Habib Bank Limited

- 27 -

6.12 VOTING RIGHTS

The rights and privileges, including voting rights, attached to the ordinary shares of the Bank are equal.

6.13 POWERS OF DIRECTORS

The entire control and management of the Bank is vested in the board of directors, who may exercise all such powers that are, by the Ordinance or by the Bank’s Articles of Association, required to be exercised by the Bank in general meeting.

6.14 BORROWING POWERS

Subject to the provisions of section 196 of the Companies Ordinance, 1984, the directors may from time to time at their discretion borrow such sum or sums as they may think fit for the purpose of the Bank, including from any banks or financial institutions and secure the payment or repayment of such sum or sums in such manner and upon such terms as the directors think fit.

6.15 INDEMNITY

Section 134 of the Bank’s Articles of Association reads as follows:

“Every officer or agent for the time being of the company may be indemnified out of the assets of the company against any liability incurred by him in defending any proceedings, whether civil or criminal, arising out of his dealings in relation to the affairs of the company, except those brought by the company against him, in which judgment is given in his favour or in which he is acquitted, or in connection with any application under section 488 in which relief is granted to him by the Court.”

6.16 INVESTMENT IN ASSOCIATED COMPANIES

The Bank in its extra ordinary general meeting held on Saturday, 17 November 2007, decided the following: “The following limits of equity investments in associated companies be and are hereby considered and approved within the Guidelines prescribed by Prudential Regulations of State Bank of Pakistan and other regulatory bodies”.

Name of Companies Proposed Amount

(Rupees in million)