OF QUAID E-AZAM SOLAR POWER · 4 Hydel(Tarbela IV and 2 others) 1,679 6 LNG (3*1200) 3,600 7...

13

PRIVATIZATION OF QUAID-E-AZAM SOLAR POWER PRELIMINARY INFORMATION MEMORANDUM JULY 2017 In collaboration with 1

-

Upload

vuongthien -

Category

Documents

-

view

213 -

download

0

Transcript of OF QUAID E-AZAM SOLAR POWER · 4 Hydel(Tarbela IV and 2 others) 1,679 6 LNG (3*1200) 3,600 7...

PRIVATIZATION OF QUAID-E-AZAM SOLAR POWER

PRELIMINARY INFORMATION MEMORANDUM JULY 2017

In collaboration with

1

TRANSACTION BACKGROUND

2

The Government of Punjab, Pakistan (“GOPb”), which currently owns 100% of Quaid e Azam Solar Power (Pvt.) Ltd (“QASP” or the “Company”) seeks to divest its entire stake in QASP along with management control to a qualified local and/or international strategic bidder. The Punjab Privatization Board (“PPB”) on behalf of the GOPb thus invites Expression of Interest (“EOI”) from investors interested in acquiring 100% of QASP’s share capital.

GOPb / PPB has appointed a Financial Advisory Consortium comprising of United Bank Limited (Lead Financial Advisor), EY Ford Rhodes (Accounting and Tax Advisor), HaidermotaBNR (Legal Advisor) and ensibo GmbH (Technical Advisor) to conduct this transaction.

QASP’s power plant is located in Bhawalpur while its registered office is in Lahore.

Bahawalpur

Lahore

CAPACITY

100 MW

CAPACITY FACTOR

18.27%

25Y LEVELIZED TARIFF

US c14.97/kWh

GUARANTEED USD EQUITY IRR OF

17%

FY2016 REVENUE PKR 2.95 Bn

FY2016 ASSETS PKR 16.7 Bn

1ST SOLAR POWER PLANT IN PAKISTAN

CREDIT RATING AA- (JCR-VIS)

TRANSACTION OVERVIEW

ECONOMIC FUNDAMENTALS

3

13.7

11.0

7.7 7.2

2.5

4.78 4.8

12

9.5 10

9.5

6 6 5.75

0

2

4

6

8

10

12

14

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

2011 2012 2013 2014 2015 2016 2017

CPI Inflation % Policy Rate %

Nominal & Real GDP 2013-2018

3.62 3.84 3.68

4.05 4.04

4.71

5.20 5.60

0

1

2

3

4

5

6

0

50

100

150

200

250

300

350

2011 2012 2013 2014 2015 2016 2017E 2018E

Nominal GDP ($ bn) Real GDP Growth %

0

200

400

600

800

1000

1200

1400

1600

1800

155

160

165

170

175

180

185

190

195

200

205

2011 2012 2013 2014 2015 2016 2017E 2018E

Po

pu

lati

on

(M

n)

Population Mn GDP per capita $

18,243

15,288

11,019

14,141

18,699

23,098

20,520

2011 2012 2013 2014 2015 2016 2017

Pakistan has a population of 188 Mn (2015), of

which 30% is within 25-30 years age bracket,

signifying growth potential for the country.

Economic growth has gained momentum on

improving macro economic fundamentals backed

by GDP growth, lower discount rate, improving

external outlook and consistently improving

political / security environment.

Lower oil prices have also pulled down the

inflation trajectory with YoY monthly CPI clocking

at below 5% for the past 3 years.

An overall positive economic outlook and $20 bn+

foreign reserves have enhanced investor

confidence and upgraded country rating for

Pakistan by Moody’s from Caa1 in 2013 to B3 in

2017

Source: World Bank Database Source: World Bank Database

Source: World Bank Database Source: World Bank Database

2012 2013 2014 2015 2016 2017

Rating (Moody’s) Caa1 Caa1 Caa1 B3 B3 B3

Outlook Stable Negative Stable Stable Stable Stable

Source: Moody’s Rating Agency

GDP per capita forecast

CPI and Policy Rate Liquid Foreign Reserves (USD mn)

ECONOMIC FUNDAMENTALS

4

STRATEGIC LOCATION CONSISTENT ENERGY SUPPLY CPEC INITIATIVES 1. 2. 3.

Pakistan is situated right at the junction of Central Asia, China, the Middle East and South Asia.

Pakistan has the potential to become one of Asia’s premier trade, energy and transport corridor

It serves as the lowest cost land route to Central Asian countries

China – which is Pakistan’s biggest trading partner – signed an agreement, the China Pakistan Economic Corridor (CPEC). The agreements consists of infrastructure expenditure of $54 bn

C. $35 billion allocated for Energy projects only, which includes 900 MW Solar Power Plant at the same site as QASPL’s

USD 16 Billion LNG supply deal with Qatar to ensure consistent energy supply to Pakistan to support its power generation and domestic energy needs

ECONOMIC STABILITY IMPROVED LAW & ORDER CLASSIFICATION TO MSCI

EM STATUS

Pakistani Rupee has been one of the relatively stable currencies in the emerging markets amidst decline in oil prices (average of 3.9% depreciation in FY16)

Central Bank is following a relaxed monetary policy to promote investment, bringing benchmark rates down from 12% in 2011 to 5.75% in 2016 and maintaining at the same rate.

Given strong stock market fundamentals in place, MSCI has reclassified Pakistan in its Emerging Market Index this year, providing an impetus for increased foreign investment

Pakistan’s security forces have achieved significant success in improving the law and order in the country as witnessed through a significant decline in terrorism

The ongoing operations against militants throughout the country will further improve the overall security situation in the country

4. 5. 6.

POWER SECTOR SNAPSHOT

5

Pakistan’s high dependence on imported oil for electricity

generation has contributed to high cost of electricity during the

past decade.

The energy mix will change in favor of hydel, coal and gas based

power generation over the next 5 years due to increasing

emphasis on RLNG, coal, hydel and renewable based power

generation.

Favorable Power sector policies with equitable and time-tested

concessionary framework incorporating adequate lender

protection and guaranteed USD based equity returns have

encouraged private sector participation in electricity generation

since the 90’s.

Source: NEPRA – State of the industry Report 2016

Source: NEPRA state of industry report 2016 Source: NEPRA State of the Industry Report 2016 Source: NEPRA State of the Industry Report 2016

Electricity Generation (GWh)

Demand and Supply scenario (MW) Primary Energy Supplies by Source (MTOE)

Installed Generation by Source (MW) Energy Consumption by Sector (GWh)

Overview

Public Hydro 6,902

Public Thermal 5,762

Nuclear 787

IPPs Hydro 214

IPPs Thermal 8,948

KEL 1,909

Renewable 852

Gas 30

Oil 25

LNG Import, 0.47

LPG, 0.46

Coal 5

Hydro 7.75

Nuclear 1.4

Renewable 0.2

Source: NEPRA state of industry report 2016

45

,73

1

46

,38

0

48

,91

5

50

,17

4

52

,13

9

53

,56

4

52

,27

5

56

,78

3

58

,74

2

59

,85

8

-

10,000

20,000

30,000

40,000

50,000

60,000

70,000

2012 2013 2014 2015 2016

Public Sector Private Sector

46%

7.5%

26.5%

9.0%

11%

-

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

90,000

100,000

2012 2013 2014 2015 2016

Domestic Commercial Industrial Agriculture Others

12

,32

0

14

,60

0

16

,17

0

16

,50

0

17

,26

1

18

,94

0

18

,82

7

20

,57

6

21

,70

1

22

,55

9

-

5,000

10,000

15,000

20,000

25,000

2012 2013 2014 2015 2016Firm Supply Demand

PAKISTAN’S ELECTRICITY GENERATION – WAY FORWARD

6

Pakistan is expected to achieve power surplus by 2020

due to new additions to power generation under foreign

& local investments.

Projects under CPEC are expected to generate more than

6,000 MW in 2017-18 and another 2,910 MW beyond

2018

Other than CPEC, there are many other power projects

being undertaken by private sector and the Government

and are expected to contribute additional generation of

7,748MW in 2017-18 wehile projects worth 27,940 MW

are in the pipeline (including those at feasibility stage)

going beyond 2018

24,871 26,105

27,408 28,773

20,304

23,734

26,480

29,895

2016-17 2017-18 2018-19 2019-20

NTDC Peak Demand (MW) Projected Capacity (MW)

Projected New Power Generation Capacity

CP

EC -

Ad

dit

ion

al G

en

era

tio

ns

(MW

s)

Sr No Project Name 2017 2018 Beyond

1 Coal-based power project at RYK, Punjab 1,320

2 Coal-based power project at Sahiwal 1,320

3 Imported Coal-based project at Port Qasim, 1,320

4 Engro coal-fired power project 660

5 SSRL coal-based power plant 1,320

6 Coal-based power project at Muzaffargarh 1,320

7 Suki Kinari Hydropower KPK 870

8 Karot Hydropower project Punjab 720

Total 2,640 3,300 2,910

Oth

er E

ne

rgy

Pro

ject

s -

Ad

dit

ion

al

Ge

ner

atio

n (

MW

s)

1 Neelum Jehlum 969

2 Chashma Nuclear (C4) 340

3 Wind (Other than CPEC) 500

4 Hydel(Tarbela IV and 2 others) 1,679

6 LNG (3*1200) 3,600

7 Jamshoro Coal Power Plant 660 660

8 K2 & K3 2,200

9 CASA 1000 1,000

10 Dasu 1& 2 4,280

11 Diamer Basha 4,800

12 Others 15,000

Total 7,088 660 27,940

Source: NEPRA and News Article

Source: NEPRA

Demand and Supply Forecast

SOLAR POTENTIAL IN PAKISTAN

7

Pakistan has tremendous potential to meet its power

demand needs from renewable energy sources and, in

particular, solar.

Solar irradiance levels in parts of Pakistan, particularly in the

southwest, are on par with the best in the world with global

horizontal irradiance (GHI) values over 1500 kWh/m² in over

90% of the country’s land area 2. The annual mean value of

GHI for whole Pakistan, based on preliminary analysis by The

World Bank, is 2071 kWh/m².

The maps reveal that even areas receiving the least average annual irradiation are better than Germany’s best regions for solar power generation

Source: World Bank Group (2015). Solar Modeling Report

750

1,250

1,750

2,250

2,750

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

An

nu

al S

un

shin

e H

ou

rs

Pakistan Northern Regions Sindh Balochistan Punjab

31

.5

16

.9

13

.5 1

6.5

18

.5

6.7

10

.4

14.5

10

11.2

0

5

10

15

20

25

30

35

South Africa(ComparativeProcurement)

Jorden (Round1: FIT, Round 2:

Competitive)

Pakistan (WindFIT)

Pakistan (SolarFIT)

Round 1 Round 2 Round 3

NEPRA recently replaced upfront tariff (FIT) with competitive bidding tariff (benchmark tariff likely to be US Cents 6/kWh – Zorlu’s tariff for 100MW solar plant)

Source: World Bank Group (2015). Solar Modeling Report

Source: NEPRA

Annual suns of GHI based on satellite estimates

Declining Tariffs (US Cents/kWh) High Solar Irradiance in Punjab

Source: World Bank Group (2015). Solar Modeling Report

Capacity (MW) Number of Projects Sponsors

>50 7

ET Solar (Pvt.) Ltd, Forshine Pakistan, Siddiqsons Solar

Ltd, M/s Solar Blue Pvt. Ltd., M/s Jafri & Associates, M/s

Integrated Power Solution

>30, 50> 1 Asia Petroleum Ltd

>20, 30> 3 ET Solar (Pvt.) Ltd, M/s R.E. Solar Pvt. Ltd.

Upcoming Major Solar Power Projects

QASPL – OVERVIEW OF THE ASSET

8

Principal Activity Own, operate and maintain the power plant

Installed Capacity

100 MW

Location District Bhawalpur, Punjab

Governance Independent Board & Professional Management

Technical Specifications

− 395,120 Polycrystalline Photo Voltaic (PV) modules (255 Wp each)

− 1,300 DC Combiner Boxes − 200 Inverters (500 KW) − 100 Transformers (0.315 / 33 kV) − 33kV Collection System Loops (20 feeders)

Net Output (FY2016)

154,005 MWh

Operational Efficiency (FY2016)

Capacity Factor: 18.27%

Off-taker Central Power Purchasing Agency (CPPA-G)

Applicable Framework

Renewable Energy Act 2006

Employees 66 (Dec’16)

Rating (JCR-VIS) AA-

Established as a part of GoPb’s initiative to establish a 1,000 MW solar park in Bahawalpur.

Incorporated in September 2013 and achieved COD in July 2015.

During its first 18 months of operation, QASP generated approved energy of 232,660 MWh, while operating at a capacity factor of 18.27% against NEPRA’s benchmarks of 223,094 MWh and 17.5% respectively.

Key Milestones

Plant Details

Project Cost & Contractors

• TBEA EPC & O&M Contractor

• 13,301 PKR mn EPC Cost

• 456.8 PKR mn Non-EPC Cost

• 14,946.8 PKR mn Total Adjusted Cost

Introduction

EPC and O&M contract with

TBEA Signing of Land

lease Agreement

2nd June 2014 10th June 2014

Energy Purchase Agreement with

CPPA-G

8th July 2014

Tariff Determination

by NEPRA

22nd Jan 2015

Achieved Commercial Operations

15th Jul 2015

TECHNICAL SNAPSHOT

9

9,120

13,942

15,155 14,517

11,431

10,418 9,710

15,031

12,775

6,000

7,000

8,000

9,000

10,000

11,000

12,000

13,000

14,000

15,000

16,000

MW

h

Actual Production (MWh) NEPRA's target

PERFORMANCE RATIO [FEB 16 – FEB 17]

75.4%

UNITS EXPORT TO NATIONAL GRID

[JUL 16 – JUN 16]

153.9 GWH

O&M CONTRACT [DURATION]

25 YEARS

HOUSES POWERED

50,000 – 100,000 Plant Type

Ground-mounted Photovoltaic Plant

Installation type Fixed installation

DC-Capacity 100,967 kWp (based on flash test data)

PV Modules Manufacturer JA Solar

Inverter & Combiner boxes TBEA SunOasis

Mounting Structure TBEA SunOasis

Foundation TBEA SunOasis

Plant Details

QASPL is achieving higher efficiency than NEPRA’s benchmark for the two successive years. As at 30 June 2017, QASPL exported 153.9 GWh to the national grid, which is more than NEPRA’s 152.2 GWh benchmark, with 15 days left in the year end.

On-site monitoring via SCADA system

High plant availability is ensured by on-site monitoring and short response times

Source: QASPL’s Management

STRONG FINANCIAL POSITION

10

2,956

1,492

84

7

43

3 1

,01

5

68

6

0

0.2

0.4

0.6

0.8

1

1.2

-

500

1,000

1,500

2,000

2,500

3,000

3,500

FY16 6m17

Sales Cost of Sales Net Profit

16,744 16,622

4,4

16

4,5

01

-

4,000

8,000

12,000

16,000

20,000

FY16 6m17

Total Assets

Total Liabilities

Total Equity

Source: QASP’s financial accounts

Profitability and growth (PKR mn) Operating Profits and EBITDA (PKR mn) Gross Margin and Net profit Margin

Balance Sheet Snapshot (PKR mn)

Revenues generated during FY16 and 6m17 amounted to PKR 3.0 billion and PKR 1.5 billion

respectively, while gross margin was reported at around 71% for corresponding period. The

company’s profitability draws support from high margins with net income reported at PKR 1.0

billion for FY16A and PKR 0.7 billion for 6m17.

6m17 earnings include one-off income of PKR 119.3 million recorded on account of liquidated

damages recoverable from the O&M contractor.

At Dec16, total asset base of the company amounted to PKR 16.6 billion. Major assets include

operating fixed assets of PKR 12.9 billion, mainly representing plant and ancillary equipment, and

cash and bank balances of PKR 2.5 billion, jointly representing c.93% of total assets.

2,081

1,208

2,646

1,484

83.60%

85.90%

82.00%

82.50%

83.00%

83.50%

84.00%

84.50%

85.00%

85.50%

86.00%

86.50%

-

500

1,000

1,500

2,000

2,500

3,000

FY16 6m17

Operating profit EBITDA Adj EBITDA Margin

72% 71%

34%

46%

0%

10%

20%

30%

40%

50%

60%

70%

80%

1 2

Gross Profit Margin (%) Net Profit Margin (%)

APPROVED TARIFF STRUCTURE & FEATURES

11

Tariff Structure

• Tariff Period: 25 years

• Tariff structure guarantees a fixed return under Capacity Purchase Payments (“CPP”) and Energy Purchase Payments (“EPP”)

• Capacity payments comprises of a fixed component of the tariff which covers shareholder’s return and debt servicing thereby ensuring stable dividends in case of declining energy offtake.

• Indexations:

• Debt servicing component of the tariff seizes subsequent to repayment of debt (after 10 years of operation). Consequently, the reference tariff for Years 11-25 stands at 6.99 PKR/kWh.

Total Tariff =

19.0888 PKR/kWh

Debt Servicing:

11.972

ROE: 4.6996

O&M: 2.417

Ye

ar 1-1

0

O&M: 2.417

ROE: 4.6996

Total Tariff =

7.1168 PKR/kWh

Ye

ar 11

-25

*QASP has submitted that it has procured local financing at KIBOR plus 300 bps as against the allowed KIBOR plus 350 bps, in accordance with Authority's upfront tariff determination the savings are to be shared in the ratio of 60:40 between power purchaser and the sponsor respectively.

Levelized Tariff: 15.22 PKR/kWh 14.97 US Cents/kWh

• As per O&M contract O&M

• 10-year repayment period of loan Debt service – principal

• 350bps spread over KIBOR* Debt service – interest

• guaranteed 17% equity return ROE

• Linked to local CPI O&M (Local – 80%)

• Linked to US CPI and USD/PKR parity O&M (Foreign – 20%)

• Linked to fluctuations in KIBOR Debt service – interest

• Linked to USD/PKR parity ROE

12

•DEADLINE FOR SUBMISSION OF EOI & SOQ

• BIDDER DUE DILIGENCE • SUBMISSION OF COMMENTS, CLARIFICATIONS ON BIDDING DOCUMENTS FROM PREQUALIFIED BIDDERS • PRE-BID MEETING (IF REQUIRED)

• RECEIPT AND EVALUATION OF SOQS •ANNOUNCEMENT OF PREQUALIFIED BIDDERS AND ISSUANCE OF BIDDING DOCUMENTS •DUE DILIGENCE COMMENCEMENT

• SUBMISSION OF EARNEST MONEY • BIDDING / APPROVAL & ANNOUNCEMENT OF SUCCESSFUL BIDDER / ISSUANCE OF LOA • CCP APPROVAL • EXECUTION OF SPA / PAYMENT OF PURCHASE PRICE/ TRANSFER OF SHARES AND MANAGEMENT CONTROL

•DATA ROOM CLOSURE AND DUE DILIGENCE COMPLETION • ISSUANCE OF FINAL BIDDING DOCUMENTS AND ANNOUNCEMENT OF BIDDING DATE

TRANSACTION STEPS

• SUBMISSION OF EOI AND PROCESSING FEE • ISSUANCE OF RSOQ

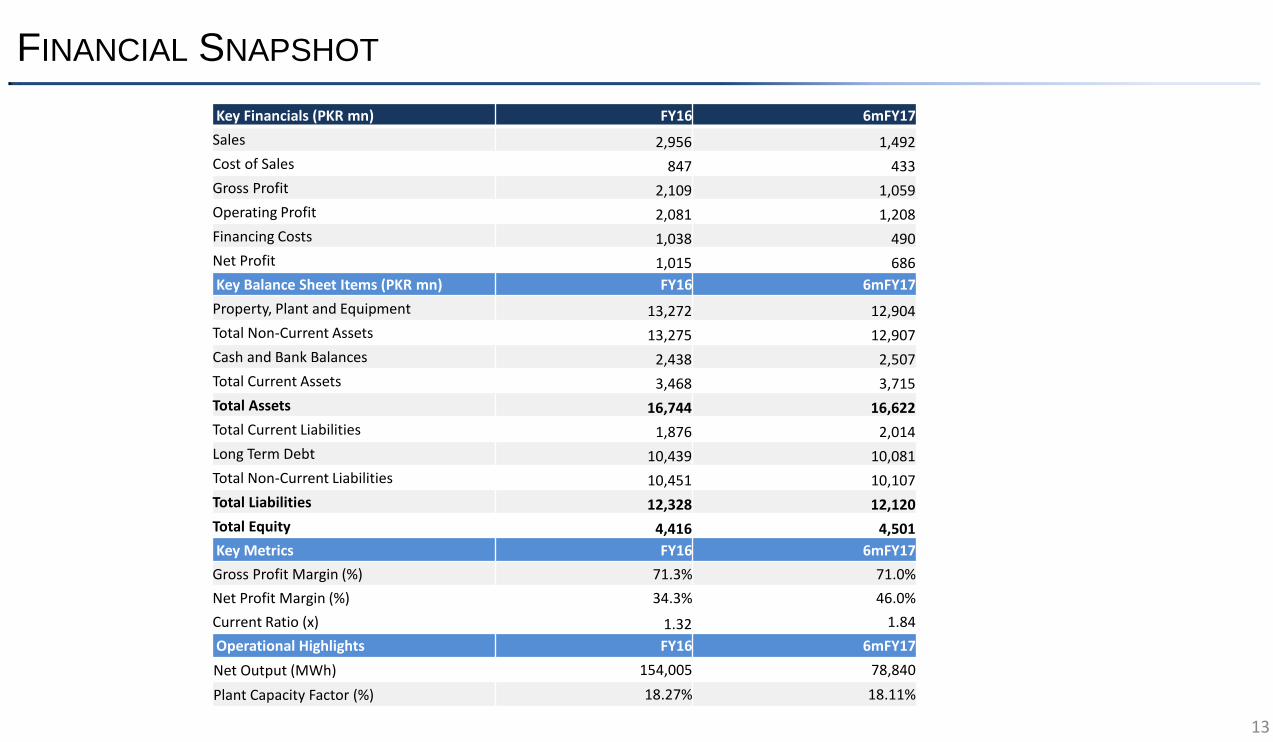

FINANCIAL SNAPSHOT

13

Key Financials (PKR mn) FY16 6mFY17

Sales 2,956 1,492

Cost of Sales 847 433

Gross Profit 2,109 1,059

Operating Profit 2,081 1,208

Financing Costs 1,038 490

Net Profit 1,015 686

Key Balance Sheet Items (PKR mn) FY16 6mFY17

Property, Plant and Equipment 13,272 12,904

Total Non-Current Assets 13,275 12,907

Cash and Bank Balances 2,438 2,507

Total Current Assets 3,468 3,715

Total Assets 16,744 16,622

Total Current Liabilities 1,876 2,014

Long Term Debt 10,439 10,081

Total Non-Current Liabilities 10,451 10,107

Total Liabilities 12,328 12,120

Total Equity 4,416 4,501

Key Metrics FY16 6mFY17

Gross Profit Margin (%) 71.3% 71.0%

Net Profit Margin (%) 34.3% 46.0%

Current Ratio (x) 1.32 1.84

Operational Highlights FY16 6mFY17

Net Output (MWh) 154,005 78,840

Plant Capacity Factor (%) 18.27% 18.11%