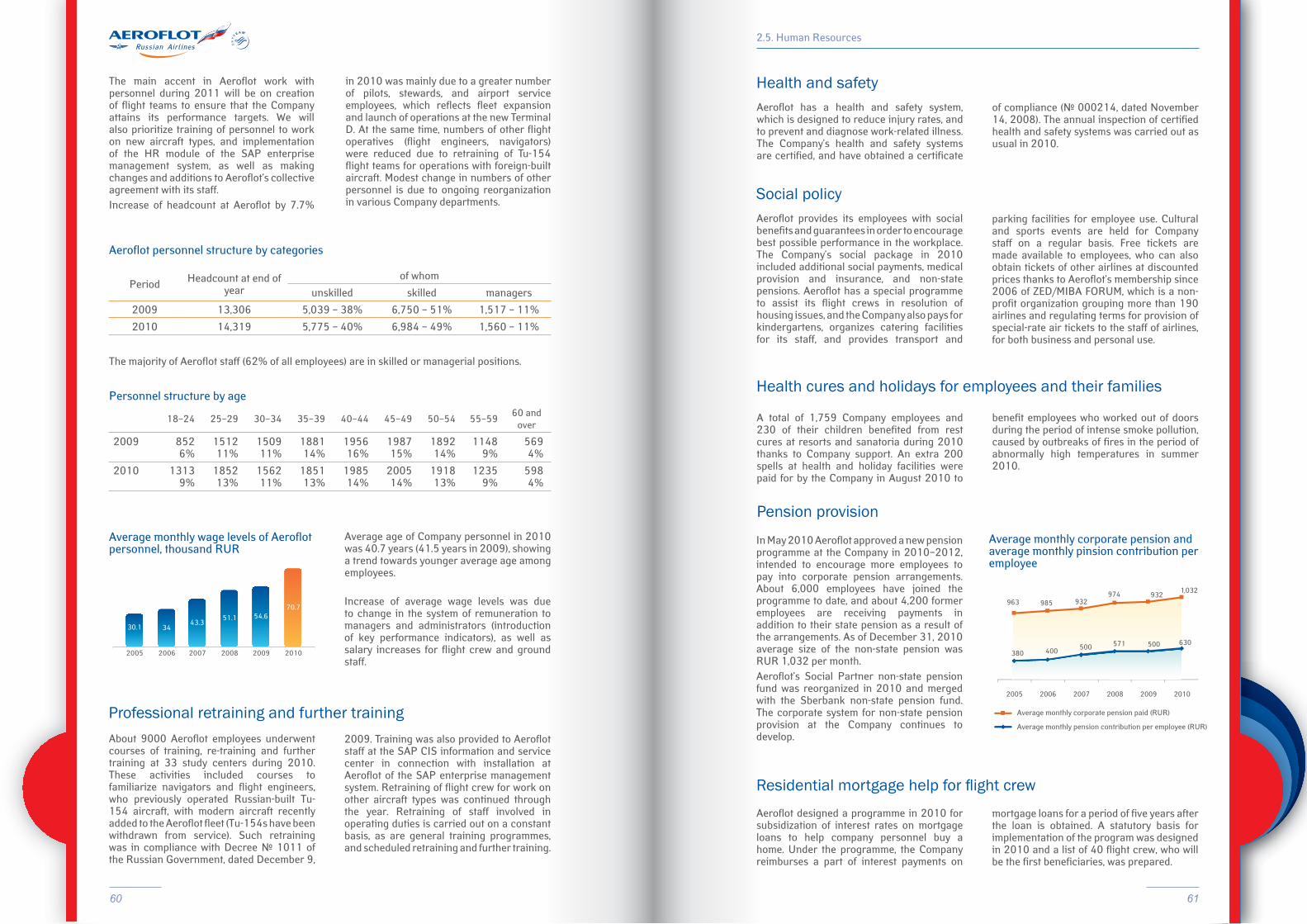

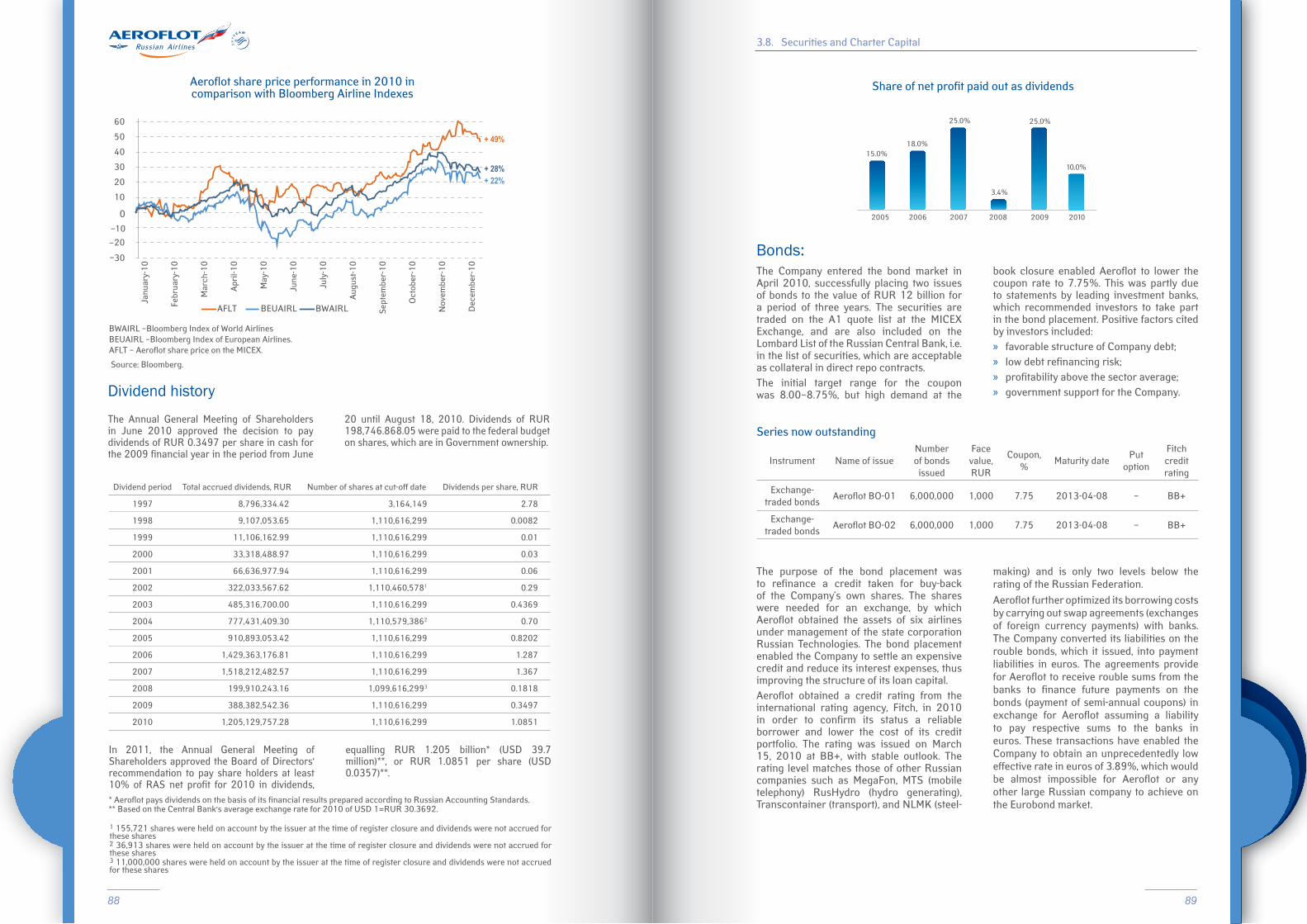

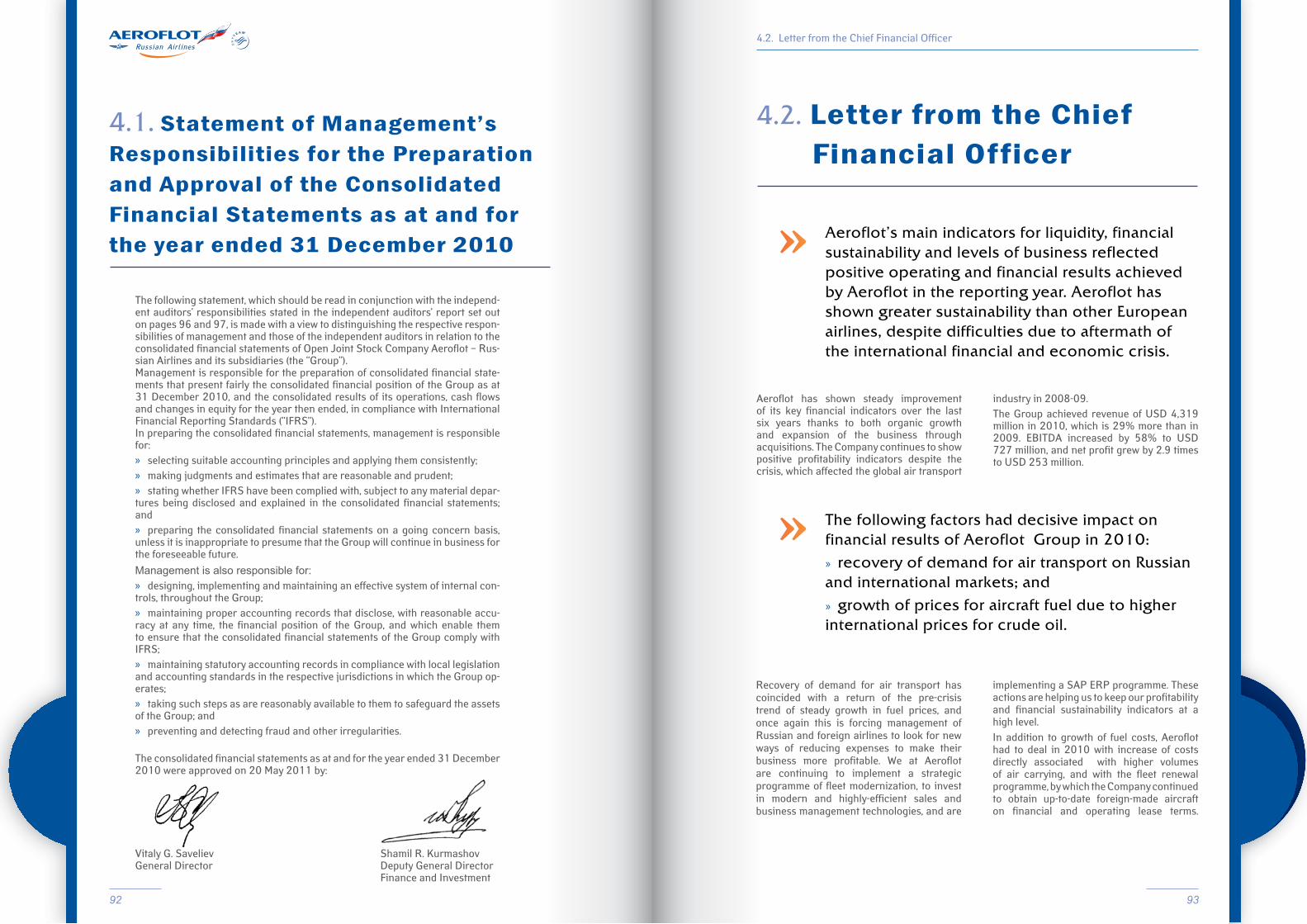

МС - Aeroflot · 2018-10-09 · 6 7 1.1. About the Company 1.1. About the Company Aeroflot is the...

91

Transcript of МС - Aeroflot · 2018-10-09 · 6 7 1.1. About the Company 1.1. About the Company Aeroflot is the...

МС 1

AEROFLOTANNUAL REPORT

2010

QUALITY

GROWTH

EFFICIENCY

Moscow – 2011

2 3

ContentsIII. Corporate governance and securities 66

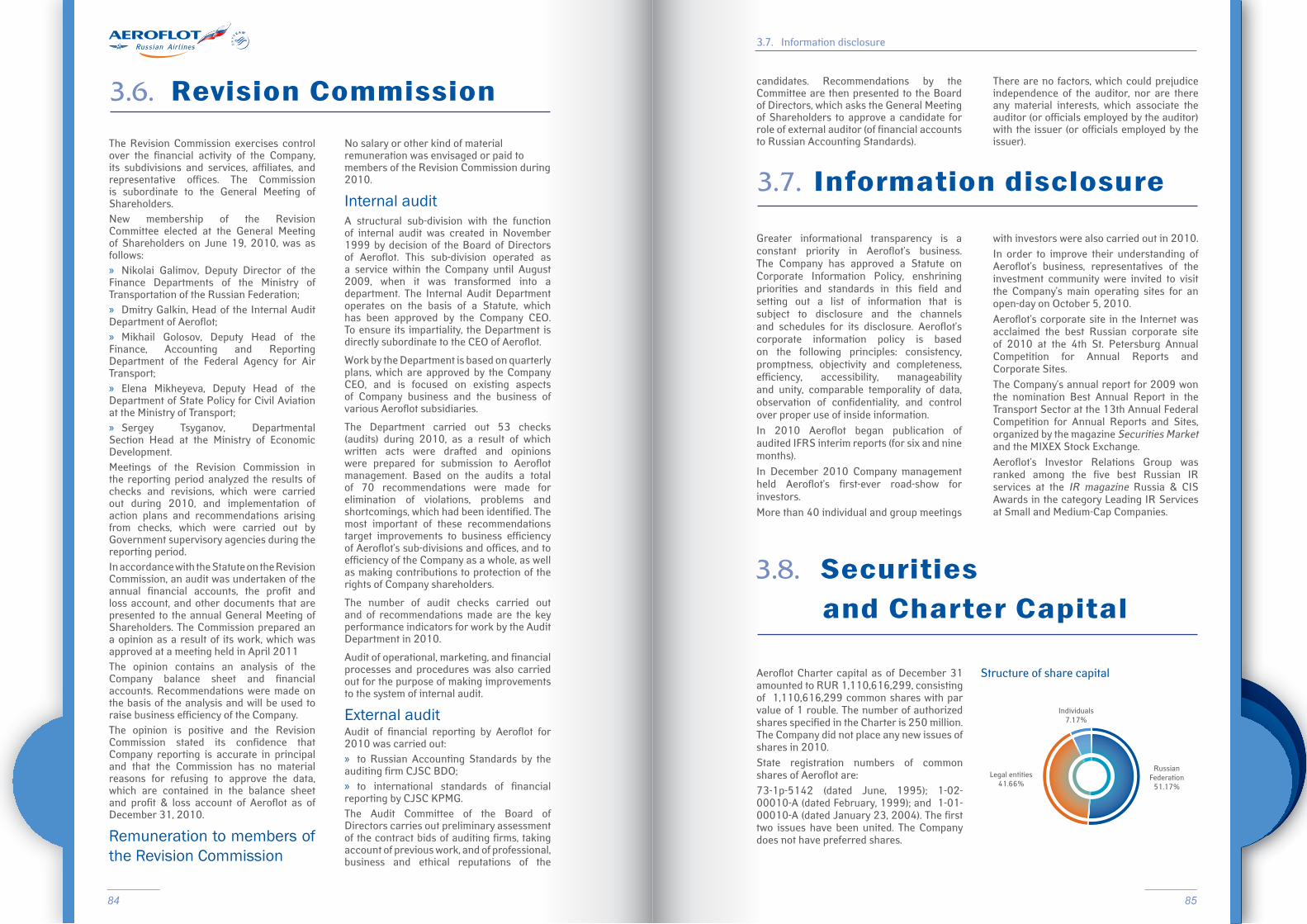

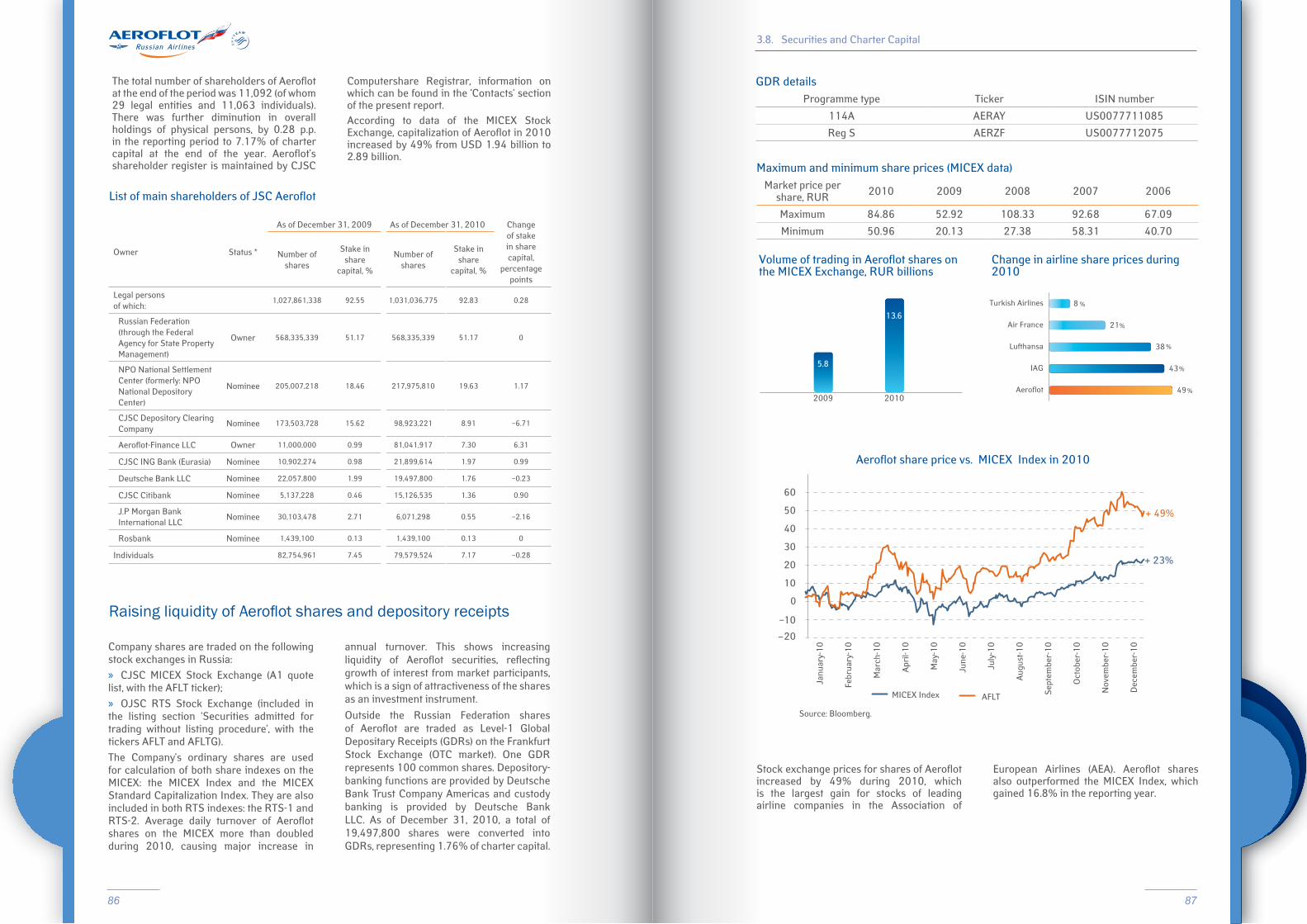

3.1. Corporate governance principles 683.2. Meetings of Shareholders in 2010 683.3. Board of Directors 693.4. Committees of the Board of Directors 753.5. Executive Board 763.6. Revision Commission 843.7. Information disclosure 853.8. Securities and Charter Capital 85

IV. Financial Reporting 904.1. Statement of Management’s Responsibilities for the Preparation and Approval of the Consolidated Financial Statements as at and for the year ended 31 December 2010 924.2. Letter from the Chief Financial Officer 934.3. Independent Auditors` Report 964.4. Overview of financial results 984.5. Consolidated Financial Statements 103

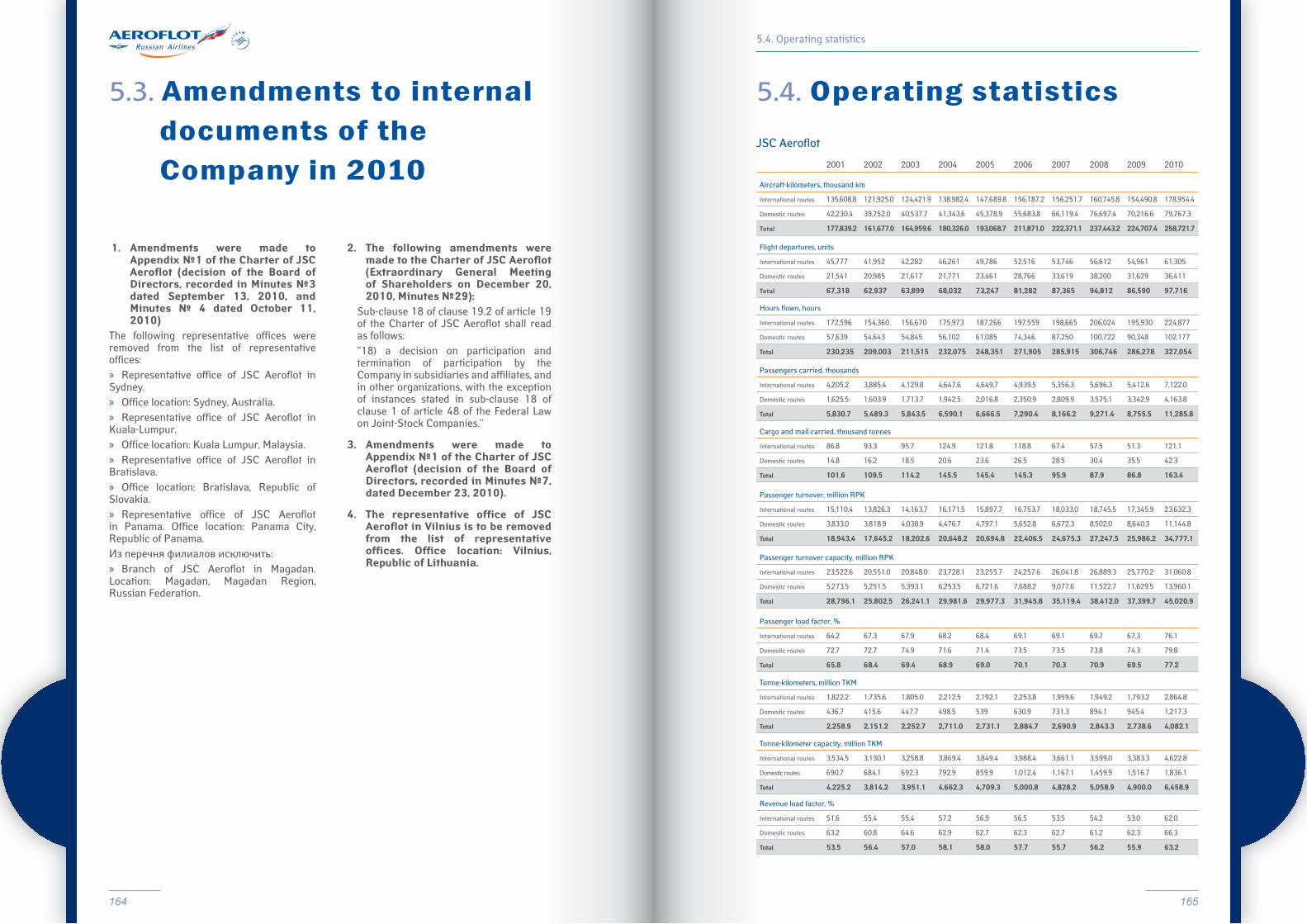

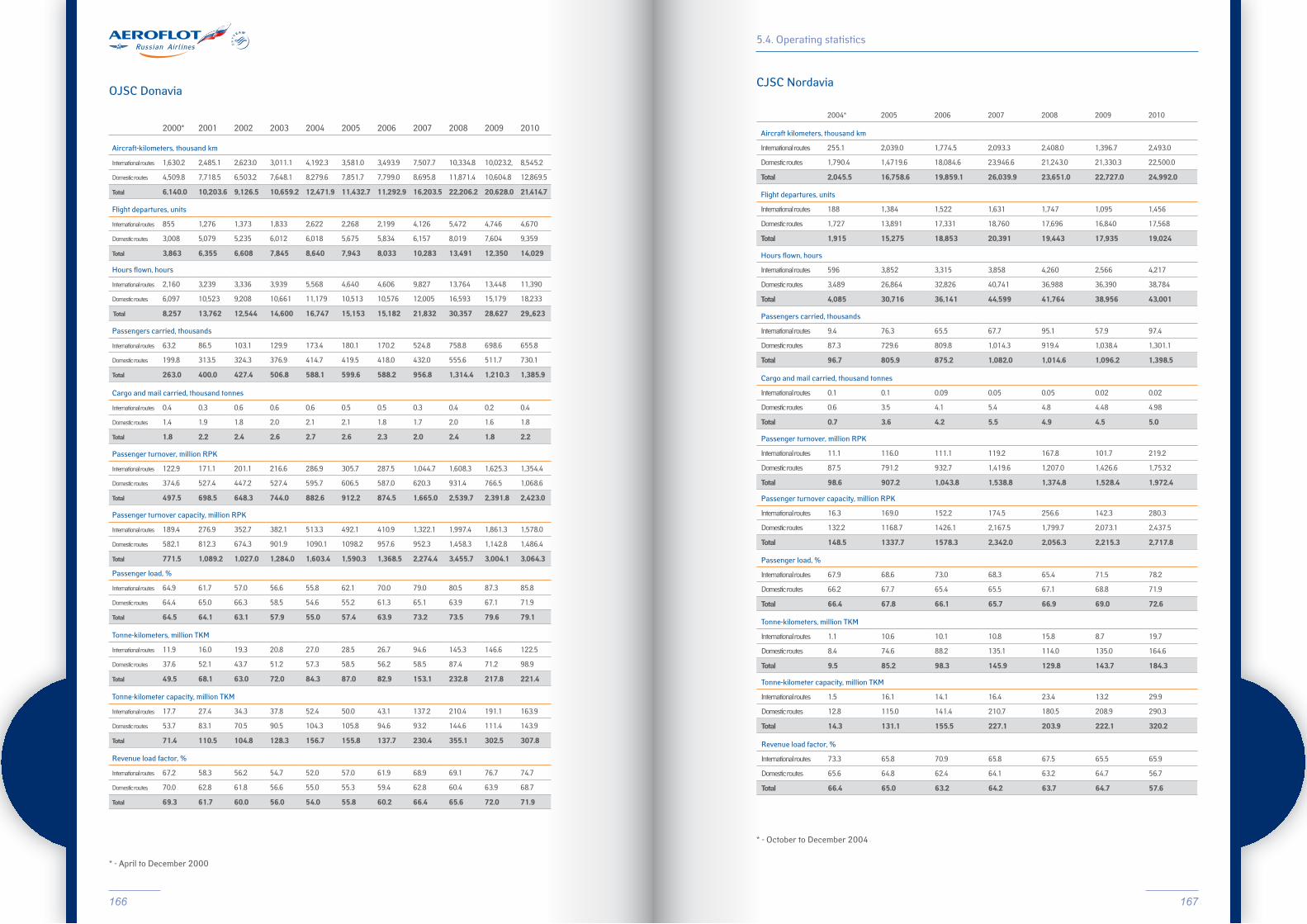

V. Appendixes 1485.1. Large transactions and related party transactions approved by the Board of Directors and the General Meeting of Shareholders 1485.2. Information on observance of the code of corporate conduct 1545.3. Amendments to internal documents of the Company in 2010 1645.4. Operating statistics 1655.5. Energy consumption in 2010 1685.6. Terms and abbreviations used in this Annual Report 1685.7. List of offices and representative offices 170 List of the Company’s own sales offices, representative offices and branches in the Russian Federation 170 List of representative offices abroad 1715.8. Contact Information 176

I. About the Company 41.1. About the Company 61.2. Key numbers 81.3. Route map and aircraft fleet 101.4. Key events 121.5. Letter from the Chairman of the Board of Directors 171.6. Letter from the CEO 21

II. Review of business 242.1. State of the industry 262.2. Development strategy 332.3. Operations 40 Safety and security 40 Transport operations 41 Route network 44 Aircraft fleet 47 Maintenance and repair 49 Brand and service quality development 50 Information technology 52 Marketing and sales 53 Subsidiaries and affiliates 542.4. Risk and risk management 562.5. Human Resources 59 HR policy 59 Study and Training center 622.6. Social responsibility 63 Environment 63 Charity and social work 64

Contents

4 5

I. ABOUT THE COMPANY

6 7

1.1. About the Company

1.1. About the Company

Aeroflot is the leading airline in Russia and the CIS and one of the 25 biggest airline companies in the world (measured by Air Transport World). In 2010 the Company took 23.7% of the Russian air transportation market by passenger turnover (26.7% including subsidiaries). Aeroflot Group carried 14.1 million passengers and 170,600 tonnes of cargo and mail in the reporting year.

Aeroflot took first place in 2010 for the first time by passenger numbers on domestic routes, carrying 4.16 million passengers inside Russia, more than any other operator on the Russian market.

Aeroflot Group’s route network is the biggest in the region, with 167 destinations in 48 countries of the world.

Aeroflot is a member of the SkyTeam global airline alliance. The combined network of the alliance includes 898 destinations in 169 countries, giving the passengers of alliance members almost unlimited travel possibilities.

The Group’s fleet consist of 143 aircraft, 29 of them operated by Nordavia and 14 planes operated by Donavia subsidiary. Aeroflot’s aircraft fleet without subsidiaries is among the youngest in Europe, and numbered 100 aircraft at the start of 2011.

Aeroflot is based in Moscow, at Sheremetyevo International Airport. A new terminal, Terminal D, was brought into operation at Aeroflot’s home Airport at the end of 2009, and most flights by Aeroflot and its partners were transferred there in the course of 2010.

Aeroflot’s development strategy targets further transformation of the Company into a global network carrier and one of the world leaders in air transport. The Russian Government has decided that Aeroflot will be the basis for consolidation of the six airline companies belonging to the state corporation Russian Technologies (Rossiya Airlines, Kavminvodyavia, Orenburg Airlines, Vladivostok Avia, Saratov Airlines and Sakhalin Airlines).

Aeroflot was included in the list of Russia’s strategic enterprises and strategic joint-stock companies by Decree № 1009 of the President of the Russian Federation, dated August 4, 2004.

8 98

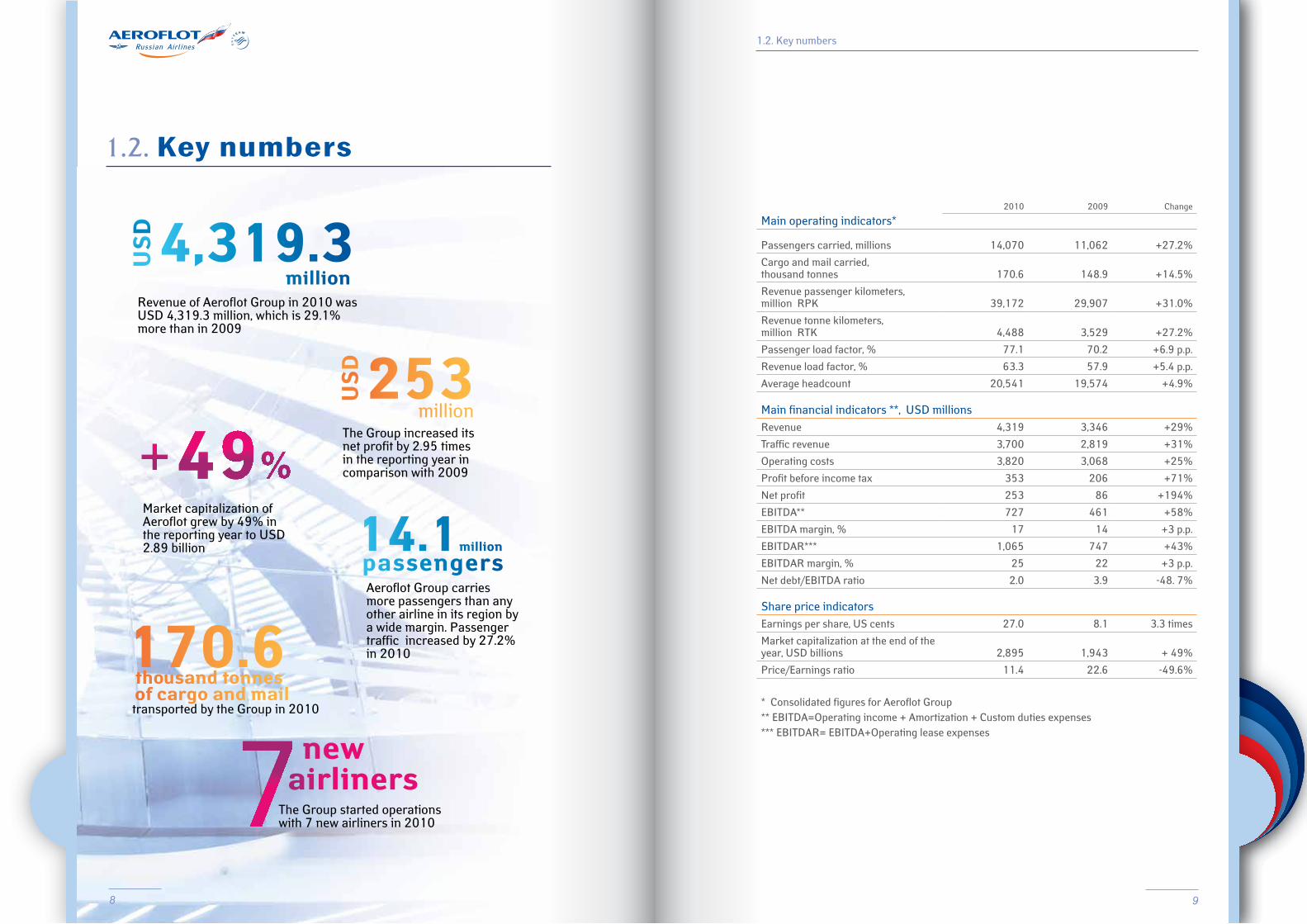

1.2. Key numbers

1.2. Key numbers

Main operating indicators*2010 2009 Change

Passengers carried, millions 14,070 11,062 +27.2%

Cargo and mail carried, thousand tonnes 170.6 148.9 +14.5%

Revenue passenger kilometers, million RPK 39,172 29,907 +31.0%

Revenue tonne kilometers, million RTK 4,488 3,529 +27.2%

Passenger load factor, % 77.1 70.2 +6.9 p.p.

Revenue load factor, % 63.3 57.9 +5.4 p.p.

Average headcount 20,541 19,574 +4.9%

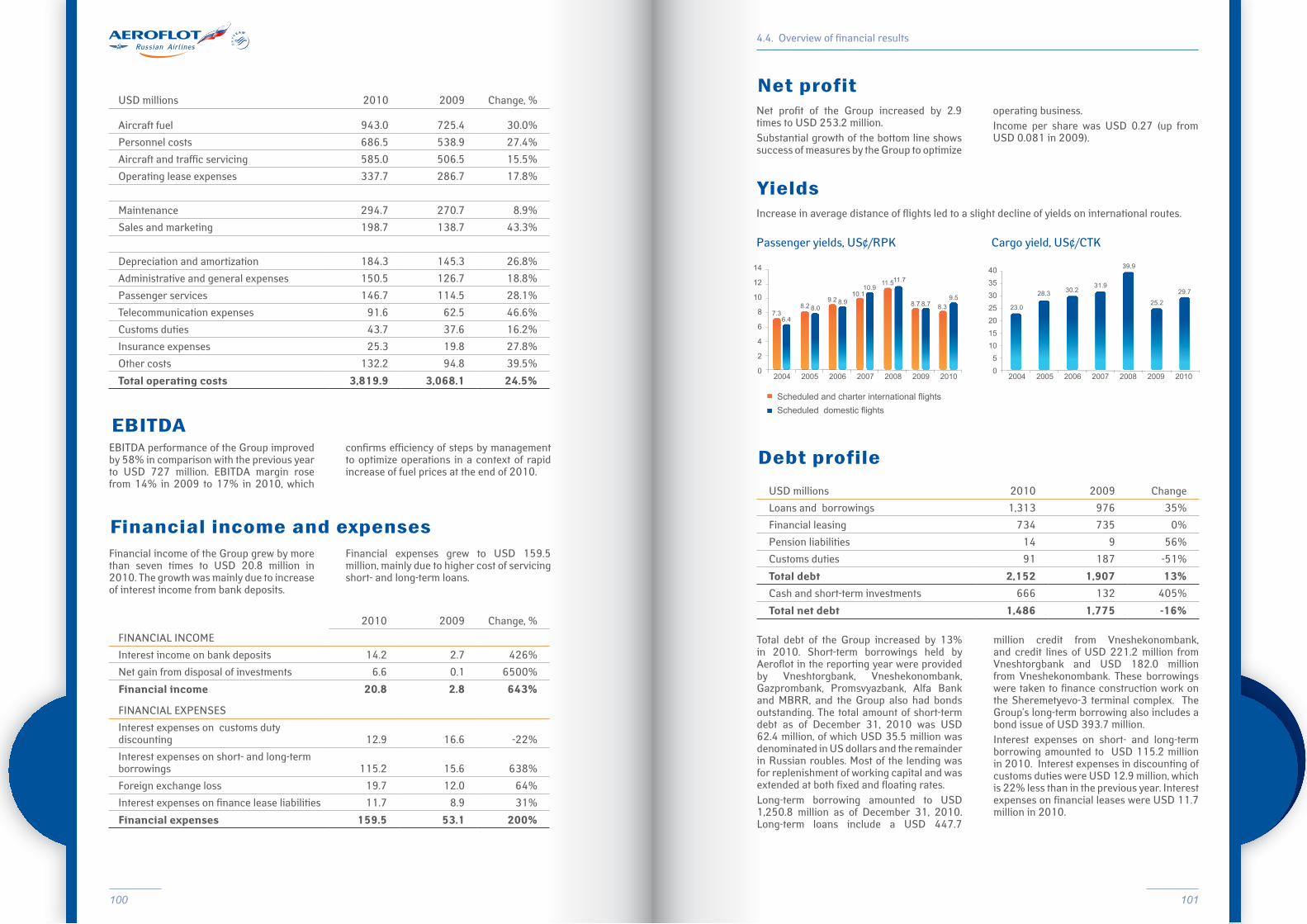

Main financial indicators **, USD millions Revenue 4,319 3,346 +29%

Traffic revenue 3,700 2,819 +31%

Operating costs 3,820 3,068 +25%

Profit before income tax 353 206 +71%

Net profit 253 86 +194%

EBITDA** 727 461 +58%

EBITDA margin, % 17 14 +3 p.p.

EBITDAR*** 1,065 747 +43%

EBITDAR margin, % 25 22 +3 p.p.

Net debt/EBITDA ratio 2.0 3.9 -48. 7%

Share price indicators Earnings per share, US cents 27.0 8.1 3.3 times

Market capitalization at the end of the year, USD billions 2,895 1,943 + 49%

Price/Earnings ratio 11.4 22.6 -49.6%

* Consolidated figures for Aeroflot Group ** EBITDA=Operating income + Amortization + Custom duties expenses*** EBITDAR= EBITDA+Operating lease expenses

4,319.3million

US

D

Revenue of Aeroflot Group in 2010 was USD 4,319.3 million, which is 29.1% more than in 2009

253 million

US

D

The Group increased its net profit by 2.95 times in the reporting year in comparison with 2009

Market capitalization of Aeroflot grew by 49% in the reporting year to USD 2.89 billion 14.1million

passengersAeroflot Group carries more passengers than any other airline in its region by a wide margin. Passenger traffic increased by 27.2% in 2010170.6

thousand tonnes of cargo and mail transported by the Group in 2010

new airliners

The Group started operations with 7 new airliners in 2010

10 11

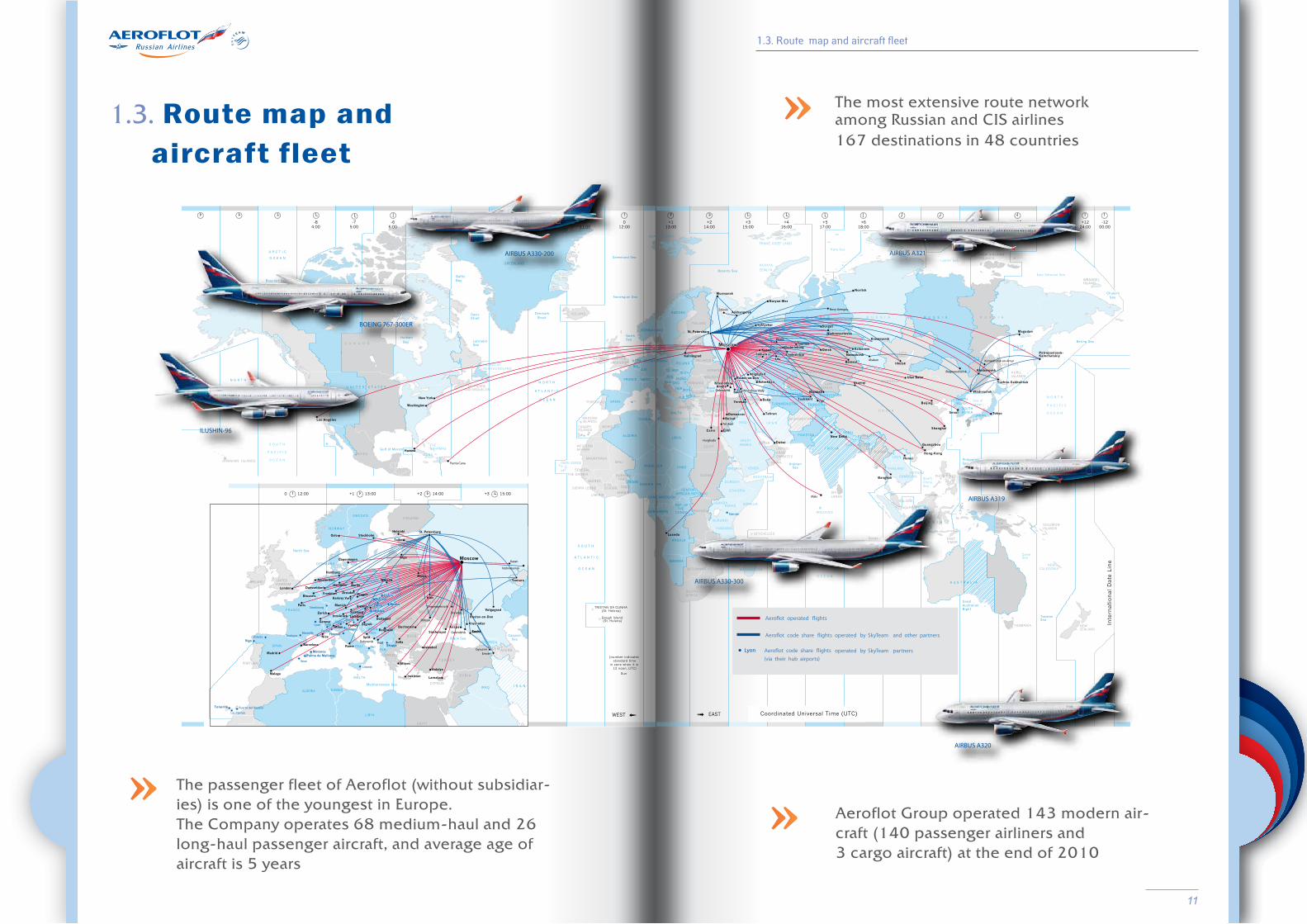

1.3. Route map and aircraft fleet

1.3. Route map and aircraft fleet

Aeroflot Group operated 143 modern air-craft (140 passenger airliners and 3 cargo aircraft) at the end of 2010

The most extensive route network among Russian and CIS airlines 167 destinations in 48 countries

»

The passenger fleet of Aeroflot (without subsidiar-ies) is one of the youngest in Europe. The Company operates 68 medium-haul and 26 long-haul passenger aircraft, and average age of aircraft is 5 years

» »

12 13

The most important event of 2010 was the decision by the Russian Government on transfer to Aeroflot of six airline operators belonging to the state corporation Russian Technologies.

»

1.4. Key events

Prague route in May. In July dozens of new flights (to Irkutsk, Murmansk, Ekaterinburg, Nizhnevartovsk, Tyumen, Chelyabinsk, Barnaul, Novosibirsk and Krasnoyarsk) were added to those previously operated (from Moscow to Kaliningrad and cities in Germany) in conjunction with Rossiya Airlines. » The Company is developing its freight

and mail network. In April Aeroflot became the first Russian airline to carry mail for the French post office.

» Aeroflot added new aircraft to its fleet. A 9th Airbus A330 and a 33rd A320 were received in January; the 10th A330 arrived in April; the 34th A320 and 17th A321 in October; the 35th A320 in November; and the 18th A321 in December.

» In November the Aeroflot Board of Directors gave the go-ahead for creation of the Aeroflot Aviation School, a non-state education establishment based on the Company’s Air Personnel Training Department and the Aviabusiness school of business.

» The long-haul route network was expanded for the winter schedule 2010/2011. New regular flights started to Goa (India), Phuket (Thailand), Punta Cana (Dominican Republic) and regular flights resumed to Male (Maldives) and Denpasar (Indonesia). The network was further expanded to include Moscow—Tel Aviv—Moscow in August and Moscow—Kazan—Moscow in September. » Aeroflot is developing cooperation under

current codesharing agreements with Russian and foreign airlines. Aeroflot and Air France decided to broaden commercial cooperation in March. Aeroflot and Czech Airlines began sharing the Prague—Krakow—

» The first stage of Aeroflot’s Payment Gateway was introduced in 2010.

» In February Aeroflot and Sberbank of Russia held the first open electronic auction of blocks of seats for tour companies ahead of the 2010 summer season. Block auctions were also held in August for the 2010/2011 winter schedule.

» Aeroflot’s Electronic Marketplace for tenders of goods and services was inaugurated in July 2010.

» Alfa Bank has handled Internet payments by plastic card for Aeroflot since August 2010. Now payments for air tickets booked online are processed by Alfa Bank’s system exclusively, without use of intermediaries. » In December Aeroflot made its debut on

the social networks Facebook, In Contact (a Russian analogue of Facebook), and the microblogging site Twitter. The Company CEO Vitaly Saveliev has started a personal blog on LiveJournal and tweets on Twitter.

1.4. Key events

Fleet modernization and expansion

Information technology

Service improvements

Development of the route network

» In April the mobile phone company MegaFon signed a contract with Aeroflot to install base stations on board Aeroflot aircraft and in December Aeroflot became the first Russian air carrier to offer passengers in-flight mobile telephony.

» The Company’s in-flight magazine received a thorough makeover in June 2010.

» From July Aeroflot began to offer check-in by mobile phone for its flights, and in November Aeroflot was the first Russian airline to offer the service outside Russia (at London’s Heathrow airport).

» Market research shows that passengers trust Aeroflot. Customer loyalty was measured in July by the international strategic consultancy Bain & Company using Net Promoter Score (a specialized index). Aeroflot had an NPS index of 44%, which

puts it ahead of many competitors in the industry. The survey found that a large share of Aeroflot customers would recommend Company services to their friends.

» Aeroflot works continuously to improve the quality and range of its passenger services. A new business and economy-class in-flight menu was introduced in March. A joint programme with Wimm-Bill-Dann Foods, ‘Healthy Eating in the Air and on the Ground’, was launched in June.

» In November Aeroflot opened its new-generation central ticket office in Moscow. The new office uses electronic queue management and maximizes customer options to ensure efficient, high-quality passenger service. Systems at the office recognize privileged status of members of the Aeroflot Bonus programme.

14 15

» Aeroflot won two of the main categories in the national Wings of Russia prizes for 2010: Airline of the Year – Domestic Passenger Carrier Group I (for high-volume carriers), and Airline of the Year – International Scheduled Carrier.

» Aeroflot was the first Russian company to be included in the list of the world’s 25 largest airlines, published by Air Transport World.

» Aeroflot was awarded the Russian transport industry’s national prize, the Golden Chariot, in the category Best Transport Company in the Crisis Period.

» The Airline was a prizewinner in Russia’s first professional awards for business tourism – the Russian Business Travel & MICE Award, – winning the nomination for Outstanding Contribution to Development of Civil Aviation.

» Aeroflot was the most punctual Russian carrier according to FlightStats.

» Vitaly Saveliev, Aeroflot Executive Board Chairman and CEO, received the Company of the Year prize in the category Personal Contribution to the Development of the Transport Industry in Russia.

Achievements and awards

1.4 Key events

» Aeroflot’s 36th Airbus A320 aircraft entered service. The new craft was given the name V. Glushko in honor of Valentin Glushko, the outstanding Soviet scientist who created liquid fuel technologies for rocket engines. » Aeroflot placed an order with Boeing

Corporation for delivery of eight Boeing 777 aircraft.

» Aeroflot decided to sell 100% of its subsidiary airline, Nordavia, as part of actions to optimize Group structure. » The next Annual General Meeting was

scheduled for June 29, 2011.

Key events after the reporting period

» In March the credit ratings agency Fitch rated Aeroflot BB+, with stable outlook.

» In April 2010 the Company entered the bond market and made two successful bond issues for a total of RUR 12 billion with three-

year maturity. The securities were listed on

MICEX Quote List A1 and also included in the

Lombard List of the Central Bank of Russia.

The Company in capital markets

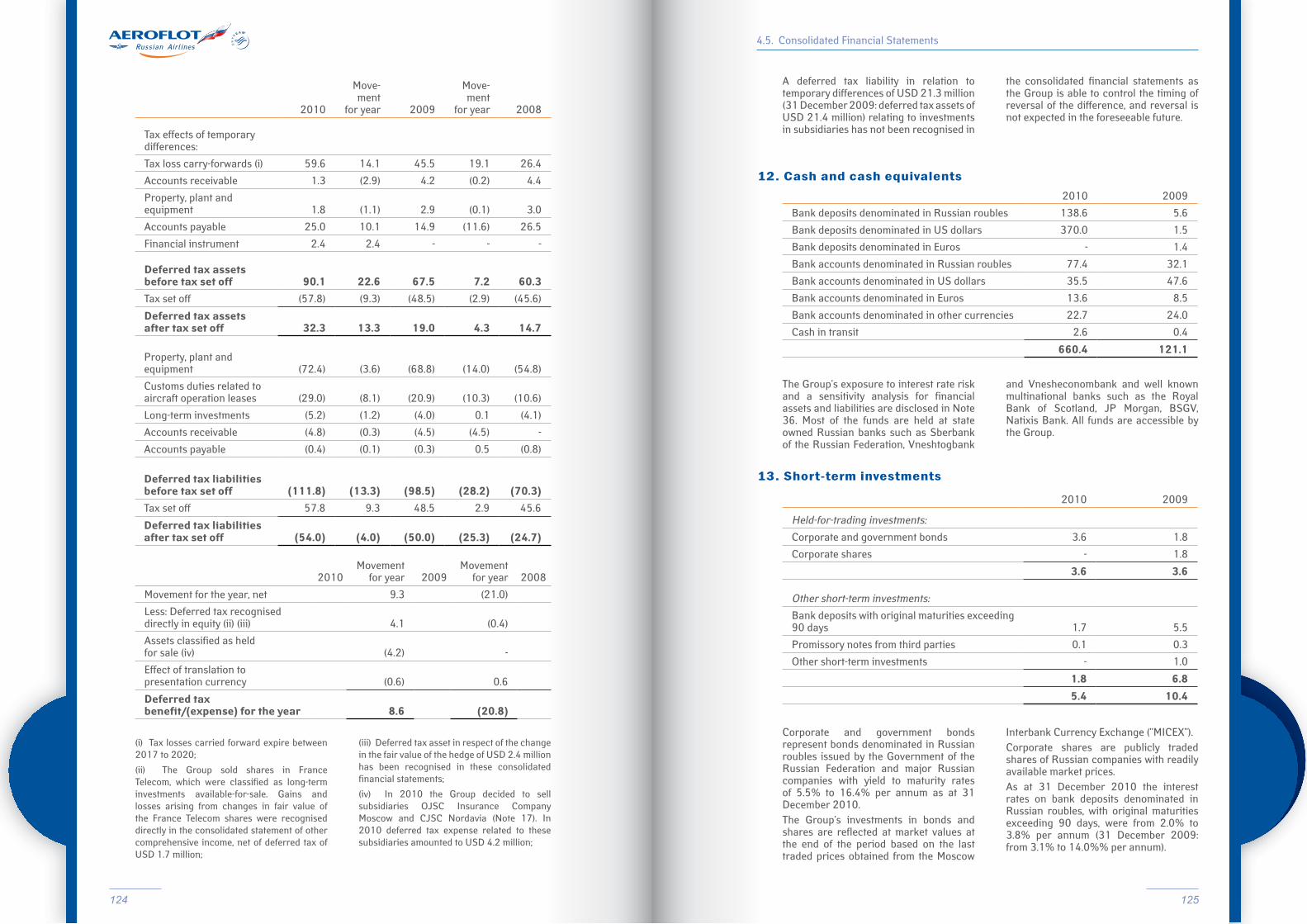

» In March Aeroflot took part, for the fourth time, in the Train of Hope national charity event, organized by Radio Russia as part of the Children’s Question social project.

» Following the eruption of the Eyjafjallajökull volcano in Iceland in April, Aeroflot laid on additional flights on European routes and accepted all passengers with valid tickets who had been unable to depart from airports, which were closed down, but managed to reach others still in operation.

» Aeroflot ran its Comrades in Arms programme from May 3 to 27, in honor of the 65th anniversary of victory in the Great Patriotic War, offering specially discounted flights to veterans.

» In September 2010 Aeroflot, in cooperation with the Give Life charity, held

an auction of paintings by children receiving assistance from Give Life programmes. All proceeds were used to enable children with health problems to travel for medical treatment.

» Aeroflot has taken a lead among Russian companies by providing social transport under a 2010 government programme designed to widen access to air travel between the Russian Far East and European Russia. About 95,000 passengers benefited from discounted fares between April 1 and October 31, 2010 representing an increase of 3.5 times compared with the same period of 2009.

» In February Aeroflot was the official carrier of the Russian ice hockey team to the world championships in Vancouver.

Social responsibility

» Aeroflot was judged to be the Quietest Airline in Prague Airport’s annual awards. » A survey by the Russian Public Opinion

Research Center (VTsIOM) found that Aeroflot is the most popular airline among foreign passengers flying to Russia. » Aeroflot was awarded the national

business prize Company of the Year 2010 in the Transport category. » Aeroflot is among the top ten most

recognized and trusted Russian brands, according to surveys by the ROMIR Holding. » Swiss courts returned CHF 53.5 million,

which were taken from the Company by fraud more than 10 years ago and had been frozen in Switzerland.

» The Aeroflot annual report for 2009 won the Transport Industry Best Annual Report award at the 13th Annual Report and Website Competition organized by Securities Market magazine and the MICEX Stock Exchange.

» The Aeroflot website won an award for Best Corporate Website of 2010 at the 4th St. Petersburg Corporate Website and Annual Report Competition.

» The Aeroflot investor relations group entered the top-five Russian IR services, as judged by IR magazine Russia & CIS Awards in the category Leading IR Service of Small and Medium-Cap Companies.

16 17

1.5. Letter from the Chairman of the Board of Directors

1.5. Letter from the Chairman of the Board of Directors

Dear Colleagues,

The airline industry experienced a transformation in 2010, reversing decline and establishing a confident growth trend. This much-awaited and gratifying turnaround opens up new horizons for Aeroflot. We can now pursue innovative development in order to capitalize on our potential and achieve a breakthrough in quality of our business.

Air passenger numbers in Russia grew at record rates in 2010. Russian airlines carried about 57 million passengers, which is the highest-ever number in the post-Soviet period and represents an increase of 26% on 2009. The rate of growth was three times above the world average.

Aeroflot’s rate of growth was even higher, making the national flag carrier the locomotive of world-beating performance by Russian airlines. Aeroflot Group accounts for around a quarter of all air transport services by Russian operators. Incorporation of airline assets of the state corporation Russian Technologies will raise Aeroflot Group’s share of the Russian market to about 40%.

Growth of the airline business has been helped by positive developments in the Russian economy, including revival of manufacturing, increase of real incomes, and the Government’s determination to support and develop the transport industry. Investment in the Russian transport sector was about RUR 1 trillion last year, representing an increase of 8% on 2009 in real terms. Development of innovative solutions has become an absolute priority in transport, as all sectors of the Russian economy.

18 19

A favorable situation in the economy is a necessary condition for business success, but that success will not be achieved unless a company can turn its opportunities to good advantage. The management team, which has led Aeroflot for the last two years, has amply demonstrated its ability to do that. Financial analysts have noted that the national carrier is carrying more cargo and more passengers, improving its profitability and maintaining tight control over costs. These achievements have improved Aeroflot’s credit rating and attractiveness to investors, paving the way for dynamic growth of market capitalization.

Aeroflot’s position as the Russian flag carrier remains as strong as ever. The Company contributes a large part of total industry performance and is the source of efficiency-boosting innovation. The Company operates successfully in the interest of its shareholders, including the largest shareholder, the Russian Government.

Aeroflot is the cornerstone of the airline industry in Russia, both shaping the future of airline business in the country and stimulating development of many other parts of the economy.

One of the key modernization tasks facing the country – that of increasing people’s mobility – would not be possible without Aeroflot. The Airline has therefore made leadership on the domestic air transport market into a strategy priority. This is being achieved without detriment to Aeroflot’s position as a top player on international routes, enhanced by membership of the SkyTeam global alliance.

Aeroflot’s status as the national carrier is more than an honorary title. It entails serious major responsibilities to Russia and its people, and our future tasks include consolidation of the Russian airline sector, increasing its efficiency and raising its authority and competitiveness on the world market.

Russia’s leading airline is well placed to achieve its strategic objectives, thanks to Europe’s youngest aircraft fleet, an extensive route network, a broad client base, high standards of service and up-to-date technology and business methods.

Aeroflot can also continue to count on the support of Government in all matters of importance in the future.

The Company’s main asset is its staff who are a close-knit team, highly qualified, motivated and infinitely devoted to what they do.

Aeroflot has much potential to attain new heights in 2011, both inside Russia and on key foreign markets. I am confident that, with the active support of its shareholders, our Company will realize that potential.

Minister of Transport of the Russian Federation Igor Levitin

1.5. Letter from the Chairman of the Board of Directors

20 21

1.6. Letter from the CEO

1.6. Letter from the CEO

Dear Shareholders,

Aeroflot achieved record results in 2010, offering an excellent basis for future development of both our Company and the entire Russian civil aviation industry.

We proved our resilience by putting the crisis of 2009 behind us and we showed our true worth as industry leaders by achieving growth rates without precedent in recent years.

Our Company carried 11.3 million passengers in 2010, which is more than ever before. We were the biggest carrier on domestic flights for the first time in our history, and we achieved record levels of carrying in the summer period when passenger numbers were in excess of one million per month. Aeroflot Group of companies transported over 14 million people in total during 2010, representing about one quarter of all carrying by Russian airlines, and we achieved this result during a period of rapid industry growth.

Not only are we in profit, but our profits are growing steadily. The bottom line of Aeroflot Group in 2010 was USD 253.2 million, which is almost three times the level in 2009. Revenue increased by 29% to USD 4,319.3 million, outpacing operating costs, which rose by 24.5% to USD 3,819.9 million. The influential international journal Air Transport World places our company among the world’s 25 leading airlines by levels of operating and net profit.

The best interests of shareholders are the touchstone of our business, so I am particularly glad to note a 49% rise in our market capitalization during 2010 to a level of USD 2.89 billion by the end of the year. Fitch international rating agency gave our Company a BB+ rating with stable outlook and Aeroflot shares offered one of the best yields among Russian stocks in 2010 (measured by trading on the MICEX Stock Exchange). Aeroflot shares still have much growth potential: investment analysts suggest that our – and your– company remains 30% undervalued.

22 23

We intend to realize our potential by keeping our position at the forefront of the global aviation industry. We are consistently implementing new technology and business methods in all spheres, making us an innovation company as well as a transport company. In 2010 we became the first Russian air carrier to offer mobile telephony and Internet access on board our aircraft, our passengers can check in by mobile phone, and our corporate website has been rated the best in Russia. Aeroflot is also becoming increasingly interactive by expanding its presence on social networks. We have inaugurated electronic auctions for sale of blocks of seats, and the Aeroflot Electronic Marketplace has been brought into operation for competitive tendering of goods and services.

Aeroflot’s aircraft fleet is already the youngest in Europe and is becoming even younger and more efficient. Our policy is to achieve an optimum combination of top-quality, Western-built aircraft with advanced Russian aerospace technology. We place particular hopes on an innovative Russian design – the Sukhoi SuperJet-100, – which will be a worthy addition to our already strong and modern fleet of aircraft.

Aeroflot is a European leader by standards of on-board customer service, as confirmed by authoritative industry surveys. According to the British airline portal, Skyscanner, our Company is 4th in the world for quality of in-flight meals and Aeroflot’s cabin crew uniform ranked in the top-10 for style. In 2010 we were the first Russian airline to obtain a customer loyalty rating, achieving an NPS score of 44%, which is better than most European carriers and in line with the best Asian and American airlines. A survey by the leading Russian opinion-poll company, VTsIOM, found that Aeroflot was the most popular carrier for foreign travelers to Russia in 2010.

We are proud to note that our achievements in 2010 were recognized by twenty awards. These included:

- winner of the Transport Section in Russia’s Company of the Year awards;

- winner in two categories of the Wings of Russia prize: Best Domestic Passenger Carrier and Best International Passenger Carrier;

- acknowledgement as Best Transport Company in the Crisis Period as part of the Golden Chariot national prizes for the Russian transport industry.

In 2010 a study by the leading Russian market researcher, ROMIR, showed that Aeroflot is now one of the top-10 most recognized and trusted Russian brands. The British consultancy, Brand Finance, calculates that the Aeroflot brand is worth over USD 1 billion, making it one of the top-20 most valuable airline names in the world.

Our company – your company – is the mainstay of Russia’s aviation industry and associated sectors of the national economy. Thanks to our progressive development, Russian airport infrastructure is improving, new runways are being built, and Russian aircraft manufacturers are obtaining new orders.

We have achieved much, and we look forward to achieving more. Aeroflot intends to become a global airline, capable of matching and outperforming the best in the world. With Russia now on the threshold of WTO membership, an internationally competitive flag carrier is more important than ever.

Our main goal is to enter the top-5 carriers in Europe and top-20 in the world by passenger numbers before 2025, setting a target of 70 million passengers a year. This goal determines our other strategic objectives up to 2025. Development of domestic carrying is a special priority, as we recognize the importance of enabling Russians to be more mobile and make better use of transit capacity. Our targets for international routes are also ambitious.

We believe that all these targets are absolutely realistic, particular in view of our project – backed by the Russian Government – to consolidate the Russian airline industry. Integration of six regional airlines, which we are obtaining from their current owner, Russian Technologies, will strengthen our position as the standard-bearer for Russian aviation, increasing our share of the Russian air travel market and our presence abroad.

Such is our and your Company. Aeroflot – a Company to be proud of.

Vitaly Saveliev

1.6. Letter from the CEO

24 25

II. REVIEW OF BUSINESS

26 27

Favorable current indicators for the industry in 2010 coincided with events, which give a clearer picture of how the global aviation system will be shaped in the future. National carriers, having survived a temporary reversal of their fortunes due to the global financial crisis, continued to move towards a global model by increasing their presence in various geographic markets and diversifying the services, which they offer.According to International Air Transport Association (IATA) data, published in June 2011, total world passenger volumes in 2010 were up by 8.1% over 2009 at 2. 7 billion. IATA predicts that the air travel market will expand to 3.3 billion passengers by 2014, with most of the growth caused by rise of the Asia-Pacific region economies, led by China.

According to IATA, total industry passenger revenues in 2010 were USD 425 billion, which is 14% more than in 2009. However, the average one-way air fare has not yet regained its pre-crisis level of 2007.

World passenger traffic grew by 8.2% in 2010 but the growth was unevenly distributed across different regions. The leading region was the Middle East (+17.8% against +11.2% in 2009), which was predictable given that the region specializes in transit traffic. Asia-Pacific countries (+9%), Latin America (+8.2%) and North America (+7.4%) had results close to the global average. The European market showed growth of 5.1%,

which is below the industry average.

Total cargo in 2010, according to provisional IATA figures, was 45.8 million tonnes, which is 12% more than in 2009 and 1% more than 2008. Cargo revenue grew by USD 18 billion from 2009, but by only USD 3 billion in comparison with 2008. Total revenue cargo kilometers increased by 20.6% in comparison with 2009.

Processes of consolidation and development of global airline alliances continued apace in 2010. These processes are leading to emergence in the not-too-distant future of transnational airline groups, which will be among the world’s top-100 companies in terms of turnover.In 2010 consolidation focused on airlines in South and North America, Western Europe and the CIS. In the USA the largest market players continued to come together to create new giants. The merger of Delta and NWA was followed by that of United Airlines and Continental.The Latin American airline industry also continued to consolidate and generate new large players, capable of becoming global companies in due course. The Latin American market experienced its biggest-ever event with the creation of a new player, LATAM Airlines Group, from the merger of two leading and rapidly growing operators – LAN Airlines and TAM of Brazil.Europe continued to set up joint business projects with American companies to operate on transatlantic routes. One such joint project between British Airways, Iberia

and American Airlines started operations in 2010. A further wave of mergers and takeovers is expected in the coming year, resulting primarily from the changing situation in northern Europe and British Airways’ intention to acquire a number of regional companies in different parts of the world.Consolidation also affected the CIS as mergers took place in both Russia and Ukraine. The largest consolidation project in Russia was the start of takeover by Aeroflot of the assets of the state corporation Russian Technologies. Favorable geographical location of Moscow on the shortest route between East Asia and Europe gives Russia’s largest airline excellent chances of becoming one of the big players in the emerging world air travel market. In Ukraine, local airlines continued to coalesce around Ukrainian Aviation Group, which today controls around 60% of the local air industry. The new long-haul market architecture is dominated by airlines with above-average service standards, reflecting increasing demand worldwide for premium (business and economy-plus) travel.

2.1. State of the industry

Leading airlines are progressing from a theoretical interest in biofuels to practical steps for use of such fuels. The pioneers in this direction have been Lufthansa and British Airways. Lufthansa announced opening of the world’s first commercial flights using mixed fuel, to be operated from spring 2011 on the Hamburg—Frankfurt route by an Airbus A321. British Airways and the

American company Solena have launched a joint project to build a biofuel plant near London, which will supply British Airways flights from 2014.At present the main function of flights using biofuel is as an image tactic. But experts expect new technology to emerge, which will make biofuels much less expensive by 2015.

2.1. State of the industry

The global market for air transport

The global airline industry developed well in 2010

Growth across regional markets is uneven, and is led by countries of the Middle East, Asia-Pacific and Latin America

Main international market trends are towards consolidation and further development of airline alliances

Leading aircraft manufacturers and carriers have begun to investigate the potential of biofuels, signaling an important innovative trend in the global airline market

Medium-term trends in passenger numbers

Data: IATA.

bil

lio

n p

ass

eng

ers

28 29

The Russian air transport market

The Russian air transport market showed strong growth in 2010, far exceeding growth of the world market.

Most of the growth was due to increasing demand for international flights on popular tourist routes.

Industry consolidation and integration continues, leading to the emergence in Russia of major global market players.

The Russian air transport market grew steadily in 2010. According to Transport Clearing House (TCH) data, Russian airlines carried almost 57 million passengers last year. That is 26.2% more than in 2009,

when passengers carried by Russian airlines numbered 45.1 million. Total passenger traffic on Russian airlines increased by 30% to 147.118 billion RPK in 2010.

Trends in passenger numbers on Russian airlines

Average flight distance of Russian airlines

Russian airlines carried a total of 22.7 million passengers on international routes in 2010, which is 30% more than in 2009 and 17% more than in 2008. Average flight distance increased from 2960 to 3150 km. According to TCH, 13.5 million passengers entered Russia on international routes with foreign airlines, which is 17% more than in 2009. Moscow and St. Petersburg accounted for 87% of the passenger flow.Scheduled flights to CIS countries represented only a small proportion (13%) of the market, but grew by 23% from 2009 to 3.5 million passengers.

The reporting year saw further processes of consolidation and infrastructure modernization, as well as long-awaited growth of interest in development of regional flights.The centerpiece of consolidation in the reporting year was the Russian Government’s decision to transfer six Russian airlines belonging to the state corporation Russian Technologies to management by Aeroflot.In Russian regions there were tentative signs in 2010 of some decentralization of Russian passenger traffic. But these processes

Source: TCH.

Source: TCH.

Total passenger numbers on domestic routes were 29.2 million in 2010, which is 23% more than in 2009 and 11% more than 2008. However, average flight distance was unchanged at 2000 km, showing that structure of the domestic route network, unlike that of the international network, did not undergo any major changes. Passenger numbers on regional airlines grew by 14% compared with 2009 to 1.5 million passengers. However, this market segment failed to regain pre-crisis levels of 2008.

remain weak at present, and Moscow routes are expected to keep their domination for a considerable time to come.Inter-regional flights, unlike other market segments, failed to regain pre-crisis levels in 2010. Regular domestic routes outside Moscow accounted for only 22% of all regular domestic flights, whereas in 2008 the figure was 27%. Air transport decentralization and creation of regional hubs will occur proportionally to creation of fully-fledged inter-regional centers of business activity across Russia.

The reverse of 2009 proved short-lived. Recovery from the crisis of the 1990s has resumed and the industry has set about creation of a large national carrier to represent Russia in the global market

»Passengers carried by Russian airlines, million passengers

Passenger turnover of Russian airlines, billion RPK

» 0

5

10

15

20

25

30

35

International Domestic

2.1. State of the industry

Most growth in 2010 came from international routes, mainly as a result of increasing demand for flights to popular tourist destinations. International travel accounted

for 49% of carrying by Russian airlines in 2010, following a long period at around 47-47%.

International

Domestic

Mill

ion

pas

sen

gers

km

International Domestic

30 31

2.1. State of the industry

Structure of the Russian air transport market (international RPK)

Structure of the Russian air transport market (domestic passenger numbers)

Structure of the Russian air transport market (domestic RPK)

Structure of the Russian air transport market (international passenger numbers)

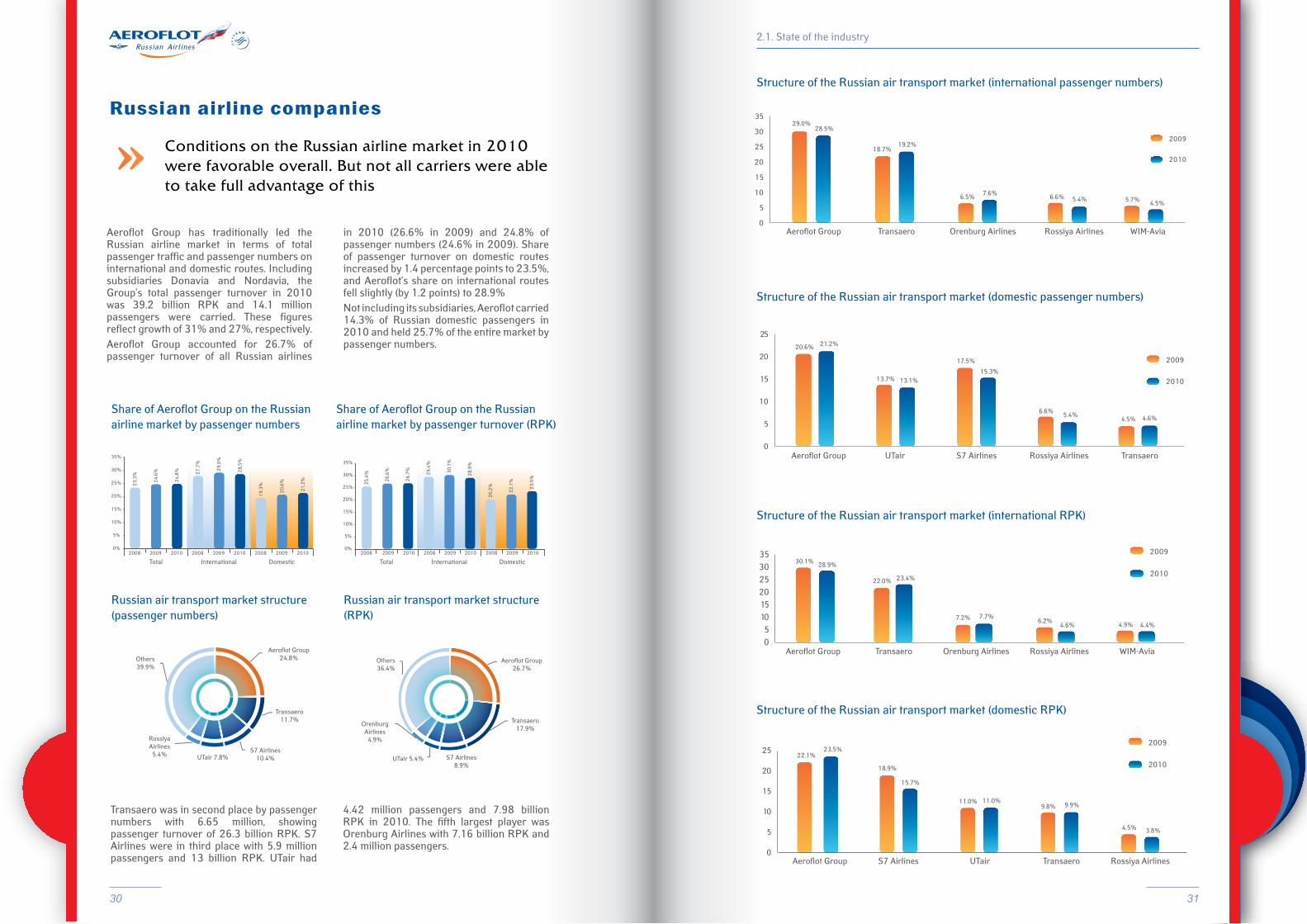

Russian airline companies

Conditions on the Russian airline market in 2010 were favorable overall. But not all carriers were able to take full advantage of this

»Aeroflot Group has traditionally led the Russian airline market in terms of total passenger traffic and passenger numbers on international and domestic routes. Including subsidiaries Donavia and Nordavia, the Group’s total passenger turnover in 2010 was 39.2 billion RPK and 14.1 million passengers were carried. These figures reflect growth of 31% and 27%, respectively.Aeroflot Group accounted for 26.7% of passenger turnover of all Russian airlines

in 2010 (26.6% in 2009) and 24.8% of passenger numbers (24.6% in 2009). Share of passenger turnover on domestic routes increased by 1.4 percentage points to 23.5%, and Aeroflot’s share on international routes fell slightly (by 1.2 points) to 28.9%Not including its subsidiaries, Aeroflot carried 14.3% of Russian domestic passengers in 2010 and held 25.7% of the entire market by passenger numbers.

Russian air transport market structure (passenger numbers)

Russian air transport market structure (RPK)

Transaero was in second place by passenger numbers with 6.65 million, showing passenger turnover of 26.3 billion RPK. S7 Airlines were in third place with 5.9 million passengers and 13 billion RPK. UTair had

4.42 million passengers and 7.98 billion RPK in 2010. The fifth largest player was Orenburg Airlines with 7.16 billion RPK and 2.4 million passengers.

Share of Aeroflot Group on the Russian airline market by passenger numbers

Share of Aeroflot Group on the Russian airline market by passenger turnover (RPK)

Total International Domestic Total International Domestic

Others 39.9%

Rossiya Airlines

5.4% UTair 7.8%S7 Airlines

10.4%

Transaero 11.7%

Aeroflot Group 24.8% Others

36.4%Aeroflot Group

26.7%

Transaero 17.9%

S7 Airlines 8.9%

UTair 5.4%

Orenburg Airlines

4.9%

Aeroflot Group Transaero Orenburg Airlines Rossiya Airlines WIM-Avia

Aeroflot Group UTair S7 Airlines Rossiya Airlines Transaero

Aeroflot Group Transaero Orenburg Airlines Rossiya Airlines WIM-Avia

Aeroflot Group S7 Airlines UTair Transaero Rossiya Airlines

29.0%28.5%

18.7%19.2%

6.5% 7.6% 6.6% 5.4% 5.7% 4.5%

20.6% 21.2%

13.7% 13.1%

17.5%

15.3%

6.6%5.4%

4.5% 4.6%

30.1% 28.9%

22.0% 23.4%

7.2% 7.7%6.2%

4.6% 4.9% 4.4%

22.1%23.5%

18.9%

15.7%

11.0% 11.0%9.8% 9.9%

4.5% 3.8%

32 33

Aeroflot’s strategic goal is to create a global network airline, which is among the best in the world for service and innovation, and a leader on the international airline market.

The basis for innovative growth will be advanced technology as a means of increasing efficiency, reducing costs and improving services. Advanced technologies and innovation will be used to improve every aspect of the Company’s business and safeguard flight safety.

Incorporation of six Russian airlines, further development of cooperation in the SkyTeam alliance and successful implementation of the Company’s fleet programme will ensure improving results for Aeroflot in the near term, preparing the Airline for the next stage of its ambitious plans to transform itself into a global player.

2.2. Development strategy

2.2. Development strategy

The Russian air transport sector, which was the first to feel effects of the global crisis on the airline market, returned to its long-term growth trajectory in 2010

»Russian airlines carried some 926,400 tonnes of cargo in 2010, which is 30.1% more than in 2009 and 19% more than 2008. Cargo turnover increased by 32.4% to 4715.4 million CTK in 2010.

There was increasing differentiation between international and domestic business in 2010. Growth of 36% in international carrying exceeded even the best pre-crisis rates, but the domestic market barely returned to pre-crisis levels. Russian airlines carried some 661,700 tonnes of cargo on international routes, which is 16% more than in 2009. Domestic cargo was 28% of the total. Stability of domestic cargo business, which is relatively independent of macroeconomic fluctuations, reflects traditional ‘northern deliveries’ (air cargoes of supplies to isolated settlements in northern Russia), which make up the bulk of domestic cargo traffic.The leading Russian cargo carrier in 2010 was AirBridgeCargo (part of Volga-Dnepr Group of Companies). Aeroflot was in second place, with a substantial increase due to returning cargo business. The Group’s total cargo traffic in 2010 was 962.2 million CTK, an increase of 15%, and the total volume of cargo was up 14.6% to 170,600 tonnes.

Cargo and mail carried by Russian airlines, thousand tonnes

Structure of the Russian air cargo market

Others 22%

Aviastar–TU 2%

Transaero 4%

S7 Airlines 5%

Polet 5%

Aeroflot Group 19%

Volga-Dnepr Group of

Companies 43%

Moscow Sheremetyevodeveloped into a majorinternational hub

Leader in the domesticairline marketWell developed

long-haul network

Market leader in quality

Leader in global and transit markets

STRATEGIC GOAL – Transformation into a global

network airline

34 35

D e v e l o p m e n t o f t h e r o u t e n e t w o r k

E x p a n s i o n o f s e r v i c e s t o b u s i n e s s a n d e c o n o m y -c l a s s p a s s e n g e r s , p e r s o n a l i z e d s e r v i c e s a n d i m p r o v e m e n t o f q u a l i t y :

A i r l i n e c o n s o l i d a t i o n s t r e n g t h e n i n g A e r o f l o t ’ s p o s i t i o n s o n t h e d o m e s t i c m a r ke t

C r e a t i n g a n e f f i c i e n t , m o d e r n a i r c r a f t f l e e t

M o b i l e p h o n e c h e c k- i n a n d o n - b o a r d I n t e r n e t

Following the Russian Government decision to transfer aviation assets of Russian Technologies to Aeroflot, a management committee has been established to oversee Aeroflot’s incorporation of the airlines, which are as follows:

» OJSC Vladivostok Avia; » OJSC Saratov Airlines; » OJSC Sakhalin Airlines; » Rossiya Airlines; » Orenburg Airlines; » Kavminvodyavia.

The committee includes managers of both Aeroflot and of the airlines concerned.

Flights have begun on seven new international and two new domestic Russian routes.The number of passengers on SkyTeam alliance partner flights grew by 7.6% compared with 2009 to 170,000.

» New on-board cateringFrom summer 2010 passengers on regular flights are being offered new catering, with new ingredients in snacks and main courses.

» New in-flight magazinesPassengers are being offered a range of in-flight magazines, Aeroflot, Aeroflot Premium and Aeroflot Style.

» New tariffsTariff rules have been simplified and new tariff plans have been produced for the whole Group. All published tariffs are now grouped into two service classes: business class (‘status’ and ‘comfort’ grades) and economy (‘status’, ‘comfort’, ‘budget’ and ‘promo’).

» Simplified passport control proceduresA separate passport control channel for international business-class passengers is now available at Terminal D.

Aeroflot has signed a contract for delivery of 11 Airbus A330-300 aircraft in 2011 and 2012.An agreement has been signed with Boeing Corporation for delivery of eight Boeing 777 aircraft in 2013–2106 in order to develop long-haul routes and increase capacity.

» Mobile check-inMobile check-in has been introduced at Sheremetyevo Terminal D (Moscow), Pulkovo (St. Petersburg), and London Heathrow. Aeroflot is the first Russian airline to launch a mobile check-in service abroad.

» Online check-inAeroflot passengers can now check in online in more cities, including Vienna, Dusseldorf, Hamburg, Madrid, Hanover, Munich and Hong Kong (a total of 48 cities in Russia and worldwide).

» On-board Internet and mobile telephonyMegaFon mobile phone base stations are now installed on board five Aeroflot aircraft.

Implementation of key tasks in 2010:

2.2. Development strategy

36 37

E l e c t r o n i c t e n d e r i n g f o r b l o c k s a l e s

B o o s t i n g d i r e c t s a l e s

G e n e r a t e a n d m a i n t a i n p a s s e n g e r f e e d b a c k

P r o m o t e t h e b r a n d a n d i n c r e a s e d o m e s t i c s a l e s

I S O c e r t i f i c a t i o n

Aeroflot has opened a new dedicated central ticket office in Moscow (at 10 Arbat Street). The office will be able to handle 60% more customers than conventional sales offices by using electronic queue management and will offer customers the greatest possible range of options to improve service efficiency and quality. Office systems recognize privileged status of members of the Aeroflot Bonus frequent flyer programme.

Aeroflot has entered the social networks and Facebook and In Contact, as well as the microblogging site, Twitter. The CEO, Vitaly Saveliev, has also started a personal blog on LiveJournal and his tweets appear on Twitter.

Aeroflot won the Russian national prize for Business of the Year 2010 in the Transport section.Aeroflot’s website won the prize for Best Corporate Website of 2010 at the 4th St. Petersburg Competition for Corporate Websites and Annual Reports.Aeroflot won the two main sections of the national prize Wings of Russia 2010, being acclaimed Airline of the Year among both domestic high-volume carriers and international scheduled carriers.

The company’s quality management system successfully passed a re-certification audit of compliance with the ISO 9001:2008 international standard. Confirmation of Aeroflot’s ISO 9001 certification demonstrates the Company’s ability to maintain consistently high levels of service.

Blocks of seats for the winter 2010/2011 season have been sold to tour companies via open electronic auctions. The auctions were held using Sberbank’s Automated Trading System (an electronic marketplace, approved by the Russian Government).

2.2. Development strategy

I m p r o v e m e n t s t o t h e f r e q u e n t f l y e r p r o g r a m m e

Aeroflot’s frequent flyer programme, Aeroflot Bonus, has been harmonized with programmes of its SkyTeam partners.

38 39

» an extensive and high-frequency route network; » effective and harmonious sales

cooperation with other members of the SkyTeam alliance in the European and North American markets; » modern, fuel-efficient aircraft; » consistently high-quality service,

equivalent to that of leading European companies; » an effective customer loyalty programme

and client relations system; » a strong, recognizable brand; » highly qualified, highly motivated staff; » a stable financial position.

2.2. Development strategy

Ke y t a s k s i n 2 011 » focus on core business and increase efficiency of cooperation between Group sub-divisions; » expand market presence, principally

by incorporation of assets of Russian Technologies and development of partner relations with other members of the SkyTeam alliance; » offer a wide range of Aeroflot Group

products across all consumer segments; » improve product quality and make

innovations, including mobile check-in and on-board Internet and mobile telephone services; » ensure an efficient procurement system

for equipment and goods; » expand the aircraft fleet to enable market-

beating growth of traffic volumes in the medium and long term; » start operations with Russian-made SSJ

regional-class aircraft; » meet Company needs for qualified flight

crews using the Company’s own training capacities (the Aeroflot Aviation School); » ensure business continuity and crisis

resilience of Aeroflot Group companies.

St r a t e g i c o b j e c t i v e s :

M a r ke t o b j e c t i v e s o f A e r o f l o t G r o u p

Strategic goals and objectives of Aeroflot Group

» become a world airline market leader in major regional segments (routes from Russia and the CIS to Europe and Asia) and global transit markets (Europe-Asia); » establish Moscow Sheremetyevo as a

major international hub and encourage the creation of appropriate infrastructure; » maintain and consolidate dominance of

the domestic airline market; » create a well developed long-haul network

linking major global air transport markets; » become a market leader in quality.

Domestic market: maintain and increase domestic market share.International flights: maintain a leading position in the key market of flights to Europe and greatly improve Aeroflot’s position in the market for air transport to Asia.Global transit market: significantly increase Aeroflot’s presence in the key transit market between Europe and Asia.Non-scheduled segment: attain a dominant position in the market for tourist flights to Europe, Asia and the Middle East.The strategic aim of becoming a global carrier also requires diversification over several market segments – long haul, charter and budget – and consequent product differentiation.The Company is working to create the internal and external conditions necessary to achieve a sustainable competitive advantage: » well developed hub infrastructure; » dominant positions in key segments of the

domestic market (the Moscow Air Cluster, St. Petersburg and the Far East);

» The strategic goal of Aeroflot Group is to transform itself into a global network airline. However, its primary goal is to reinforce its position in the Russian domestic and CIS market.

40 41

»

»

»

»

An innovative approach to development is of decisive importance for Aeroflot today, and management views innovation as a key competitive strength

Flight safety and aviation security have absolute priority for Aeroflot

Flight safety is ensured by an efficient modern fleet of aircraft, highly qualified crews and an effective flight safety department

Flight safety meets the stringent requirements applicable to all members of the SkyTeam alliance

2.3. Operations

2.3. Operations

The Company is taking a fresh look at all aspects of its business, developing and introducing new innovative approaches to passenger service quality, business efficiency, manageability and economy of resources.In 2010 Aeroflot set up an innovative development committee under the Executive Board of Management and designed a programme concept for innovative development. The concept addresses the medium term (five to seven years) against the background of priorities set by state policy for science, technology and innovation. It contains a set of measures to develop and introduce original, world-class technologies, products and services. It is integrated with the airline’s development strategy

and designed to improve performance, measured by key criteria, through drastic reduction of the cost of air transport without detriment to the customer experience, saving energy, increasing productivity and making operations more environmentally friendly.

Special attention in design of the innovative development concept was given to creation of suitable corporate mechanisms and structures. The concept also envisages collaboration with leading universities and scientific organizations in Russia and elsewhere.

The Board of Directors has approved the Aeroflot work plan for innovation and R&D during 2011-13 and granted R&D funding in the amount of RUR 128 million for 2011.

Aeroflot operates under a wide range of Russian and international requirements and recommendations relating to flight safety. In 2010 Rosaviatsia and the civil aviation operator certification center made inspections of compliance with certification requirements with a view to extension of Aeroflot’s air operator certificate. Having passed all its inspections, Aeroflot had its air operator certificate, number 001, extended to September 9, 2012.

Aeroflot representatives are actively involved in the work of the Aviation Security Functional Experts (ASFE) group of the SkyTeam alliance, which is responsible to SkyTeam’s core management for the three priority areas: Safety, Security and Quality (SSQ). Aeroflot representatives participated in the annual ASFE meeting held on May 20-21, 2010 in Mexico. Work by the ASFE is carried out at both strategic and operational levels: » shared situation awareness at common

destinations; » common methodology of route network

risk assessment and management; » common positions on core issues of

cooperation with the authorities in various countries; » consolidated cooperation with all national

and international organizations.The IATA-recommended Security

The Company has an established and effective system for detecting and guarding against all safety risks. Aeroflot’s compliance with the highest standards of flight safety and aviation security has been demonstrated by a number of inspections: » IATA operational safety audit (IOSA)

certificate and IOSA Operator status extended to 2011 (audit conducted in 2009). » Internal audit of compliance with the

requirements of the Operational Safety section of IOSA. » IATA Safety Audit of Ground Operations

(ISAGO) of Aeroflot conducted in 2009; certificate extended to 2011. » Aeroflot’s ISO 9001 certification

confirmed.

» In 2010 a commission of the Russian Federal Air Transport Agency (Rosaviatsia) confirmed the operator’s ability to operate passenger flights safely and to a high level of quality.

» Rosaviatsia’s inspection of the compliance of Aeroflot’s aviation security measures with the certification requirements of the Rosaviatsia Transport Safety Division resulted in Aeroflot’s aviation safety certificate (number FAVT A.07.00348 dated July 2, 2010) being extended for a further two years.

The Safety Assessment of Foreign Aircraft (SAFA) Programme has been running at airports in European Civil Aviation Conference (ECAC) member states since 2000. Inspections carried out in 2010 showed that Aeroflot’s aircraft are entirely compliant with flight safety rules. Analysis of safety margins of Russian airlines shows that Aeroflot is the leading Russian operator in terms of flight safety.

Management System (SeMS), creatively adapted for each airline, is used as common basis for ensuring protection of the operations of SkyTeam members against acts of unlawful interference.In 2010 the Company continued to work on application and further improvement of the existing system for management of risks associated with acts of unlawful interference in its activities. A new system has been introduced to share aviation security information across the route network based on technology used by SkyTeam.

In the interests of airport security the Company maintains its own sniffer-dog section. It has 40 adult animals of a unique jackal-dog hybrid breed and expert handlers. The Aeroflot sniffer-dog section works to protect the Company’s own sites and aircraft and its home airport of Sheremetyevo.

Safety and security

Aeroflot improved its performance by all main indicators in 2010 as the recovery from the financial crisis continued and demand

increased on international and domestic routes.

» Aeroflot Group’s 2010 results show positive trends for all main performance indicators

Transport operations

42 43

International Domestic Passenger load factor

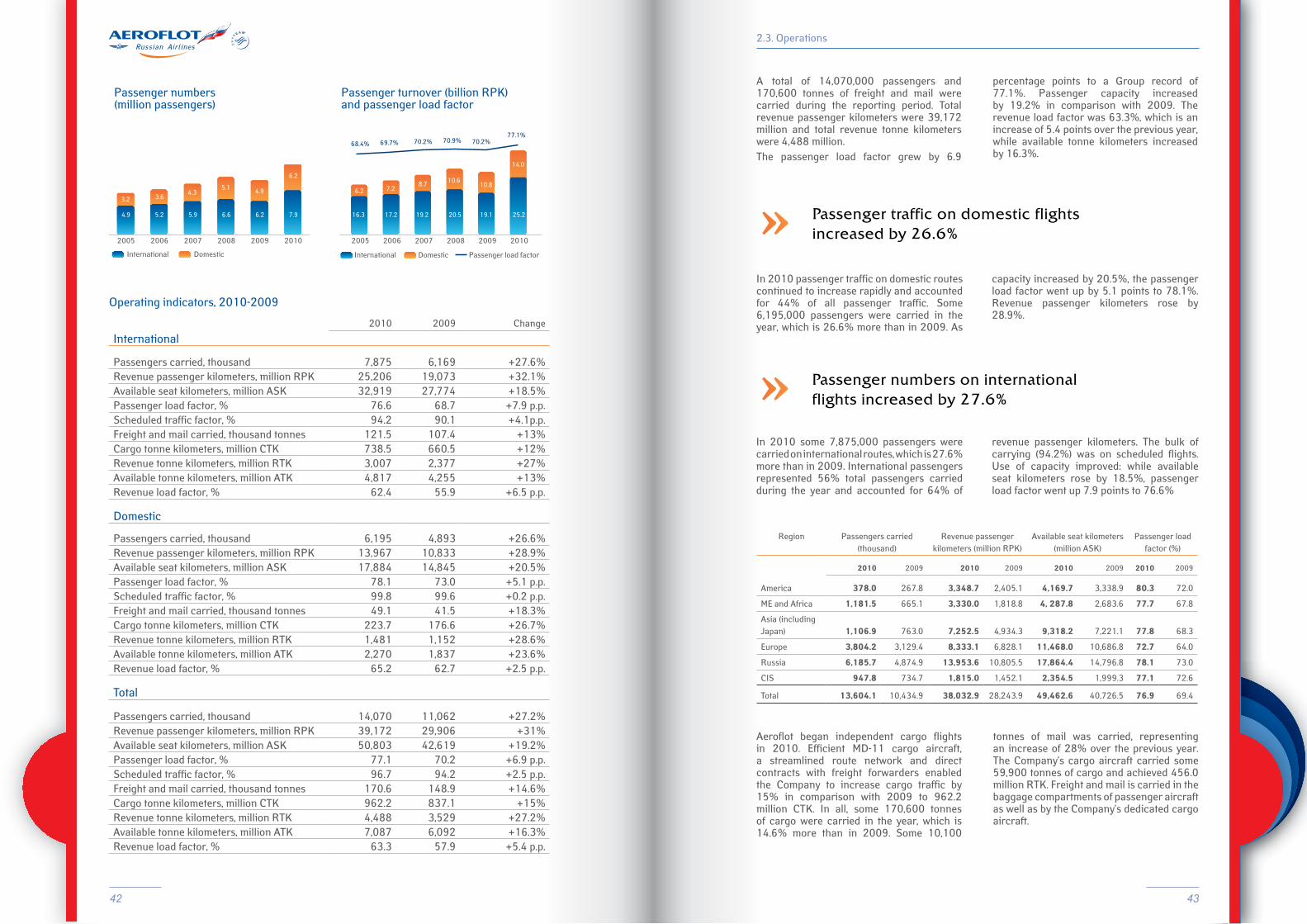

Operating indicators, 2010-2009

2.3. Operations

Passenger turnover (billion RPK) and passenger load factor

Passenger numbers (million passengers)

2010 2009 Change

International

Passengers carried, thousand 7,875 6,169 +27.6%Revenue passenger kilometers, million RPK 25,206 19,073 +32.1%Available seat kilometers, million ASK 32,919 27,774 +18.5%Passenger load factor, % 76.6 68.7 +7.9 p.p.Scheduled traffic factor, % 94.2 90.1 +4.1p.p.Freight and mail carried, thousand tonnes 121.5 107.4 +13%Cargo tonne kilometers, million CTK 738.5 660.5 +12%Revenue tonne kilometers, million RTK 3,007 2,377 +27%Available tonne kilometers, million ATK 4,817 4,255 +13%Revenue load factor, % 62.4 55.9 +6.5 p.p.

Domestic

Passengers carried, thousand 6,195 4,893 +26.6%Revenue passenger kilometers, million RPK 13,967 10,833 +28.9%Available seat kilometers, million ASK 17,884 14,845 +20.5%Passenger load factor, % 78.1 73.0 +5.1 p.p.Scheduled traffic factor, % 99.8 99.6 +0.2 p.p.Freight and mail carried, thousand tonnes 49.1 41.5 +18.3%Cargo tonne kilometers, million CTK 223.7 176.6 +26.7%Revenue tonne kilometers, million RTK 1,481 1,152 +28.6%Available tonne kilometers, million ATK 2,270 1,837 +23.6%Revenue load factor, % 65.2 62.7 +2.5 p.p.

Total

Passengers carried, thousand 14,070 11,062 +27.2%Revenue passenger kilometers, million RPK 39,172 29,906 +31%Available seat kilometers, million ASK 50,803 42,619 +19.2%Passenger load factor, % 77.1 70.2 +6.9 p.p.Scheduled traffic factor, % 96.7 94.2 +2.5 p.p.Freight and mail carried, thousand tonnes 170.6 148.9 +14.6%Cargo tonne kilometers, million CTK 962.2 837.1 +15%Revenue tonne kilometers, million RTK 4,488 3,529 +27.2%Available tonne kilometers, million ATK 7,087 6,092 +16.3%Revenue load factor, % 63.3 57.9 +5.4 p.p.

A total of 14,070,000 passengers and 170,600 tonnes of freight and mail were carried during the reporting period. Total revenue passenger kilometers were 39,172 million and total revenue tonne kilometers were 4,488 million.The passenger load factor grew by 6.9

percentage points to a Group record of 77.1%. Passenger capacity increased by 19.2% in comparison with 2009. The revenue load factor was 63.3%, which is an increase of 5.4 points over the previous year, while available tonne kilometers increased by 16.3%.

In 2010 passenger traffic on domestic routes continued to increase rapidly and accounted for 44% of all passenger traffic. Some 6,195,000 passengers were carried in the year, which is 26.6% more than in 2009. As

In 2010 some 7,875,000 passengers were carried on international routes, which is 27.6% more than in 2009. International passengers represented 56% total passengers carried during the year and accounted for 64% of

capacity increased by 20.5%, the passenger load factor went up by 5.1 points to 78.1%. Revenue passenger kilometers rose by 28.9%.

revenue passenger kilometers. The bulk of carrying (94.2%) was on scheduled flights. Use of capacity improved: while available seat kilometers rose by 18.5%, passenger load factor went up 7.9 points to 76.6%

»

»

Passenger traffic on domestic flights increased by 26.6%

Passenger numbers on international flights increased by 27.6%

Region Passengers carried (thousand)

Revenue passenger kilometers (million RPK)

Available seat kilometers (million ASK)

Passenger load factor (%)

America

2010 2009 2010 2009 2010 2009 2010 2009

378.0 267.8 3,348.7 2,405.1 4,169.7 3,338.9 80.3 72.0

ME and Africa 1,181.5 665.1 3,330.0 1,818.8 4, 287.8 2,683.6 77.7 67.8

Asia (including Japan) 1,106.9 763.0 7,252.5 4,934.3 9,318.2 7,221.1 77.8 68.3

Europe 3,804.2 3,129.4 8,333.1 6,828.1 11,468.0 10,686.8 72.7 64.0

Russia 6,185.7 4,874.9 13,953.6 10,805.5 17,864.4 14,796.8 78.1 73.0

CIS 947.8 734.7 1,815.0 1,452.1 2,354.5 1,999.3 77.1 72.6

Total 13,604.1 10,434.9 38,032.9 28,243.9 49,462.6 40,726.5 76.9 69.4

Aeroflot began independent cargo flights in 2010. Efficient MD-11 cargo aircraft, a streamlined route network and direct contracts with freight forwarders enabled the Company to increase cargo traffic by 15% in comparison with 2009 to 962.2 million CTK. In all, some 170,600 tonnes of cargo were carried in the year, which is 14.6% more than in 2009. Some 10,100

tonnes of mail was carried, representing an increase of 28% over the previous year. The Company’s cargo aircraft carried some 59,900 tonnes of cargo and achieved 456.0 million RTK. Freight and mail is carried in the baggage compartments of passenger aircraft as well as by the Company’s dedicated cargo aircraft.

68.4% 69.7% 70.2% 70.9% 70.2% 77.1%

16.3 17.2 19.2 20.5 19.1 25.2

14.0

6.2 7.28.7 10.6

10.8

International Domestic

4.9 5.2 5.9 6.6 6.2 7.9

3.2 3.6 4.3

5.1 4.9

6.2

44 45

International Domestic Revenue load factor

2.3. Operations

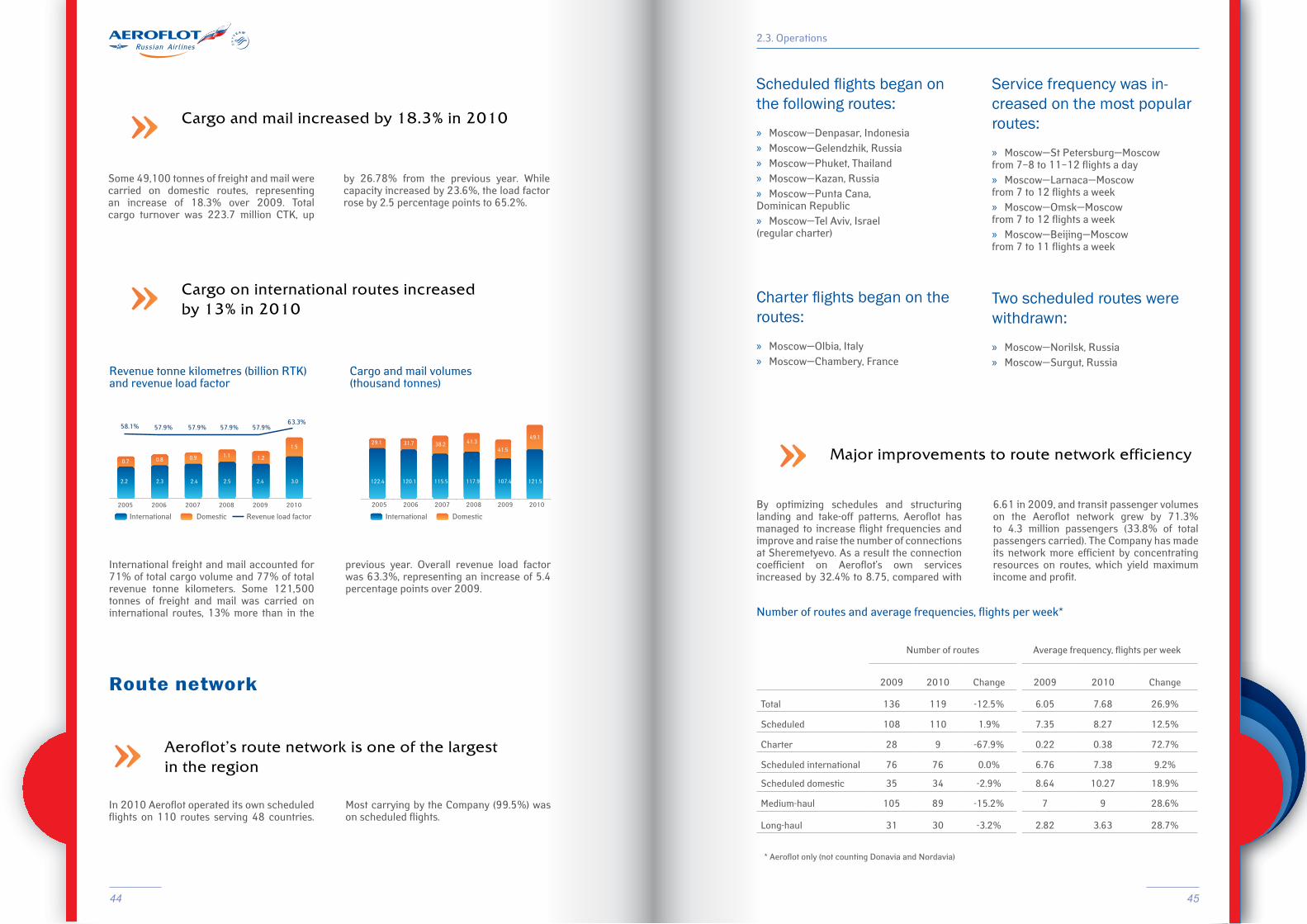

Some 49,100 tonnes of freight and mail were carried on domestic routes, representing an increase of 18.3% over 2009. Total cargo turnover was 223.7 million CTK, up

International freight and mail accounted for 71% of total cargo volume and 77% of total revenue tonne kilometers. Some 121,500 tonnes of freight and mail was carried on international routes, 13% more than in the

previous year. Overall revenue load factor was 63.3%, representing an increase of 5.4 percentage points over 2009.

by 26.78% from the previous year. While capacity increased by 23.6%, the load factor rose by 2.5 percentage points to 65.2%.

»

»

Cargo and mail increased by 18.3% in 2010

Cargo on international routes increased by 13% in 2010

Revenue tonne kilometres (billion RTK) and revenue load factor

Cargo and mail volumes (thousand tonnes)

» Aeroflot’s route network is one of the largest in the region

Route network

In 2010 Aeroflot operated its own scheduled flights on 110 routes serving 48 countries.

Most carrying by the Company (99.5%) was on scheduled flights.

Scheduled flights began on the following routes:

» Moscow—Denpasar, Indonesia » Moscow—Gelendzhik, Russia » Moscow—Phuket, Thailand » Moscow—Kazan, Russia » Moscow—Punta Cana,

Dominican Republic » Moscow—Tel Aviv, Israel

(regular charter)

Charter flights began on the routes:

» Moscow—Olbia, Italy » Moscow—Chambery, France

Service frequency was in-creased on the most popular routes:

» Moscow—St Petersburg—Moscow from 7–8 to 11–12 flights a day » Moscow—Larnaca—Moscow

from 7 to 12 flights a week » Moscow—Omsk—Moscow

from 7 to 12 flights a week » Moscow—Beijing—Moscow

from 7 to 11 flights a week

Two scheduled routes were withdrawn:

» Moscow—Norilsk, Russia » Moscow—Surgut, Russia

» Major improvements to route network efficiency

By optimizing schedules and structuring landing and take-off patterns, Aeroflot has managed to increase flight frequencies and improve and raise the number of connections at Sheremetyevo. As a result the connection coefficient on Aeroflot’s own services increased by 32.4% to 8.75, compared with

6.61 in 2009, and transit passenger volumes on the Aeroflot network grew by 71.3% to 4.3 million passengers (33.8% of total passengers carried). The Company has made its network more efficient by concentrating resources on routes, which yield maximum income and profit.

Number of routes and average frequencies, flights per week*

Number of routes Average frequency, flights per week

2009 2010 Change 2009 2010 Change

Total 136 119 -12.5% 6.05 7.68 26.9%

Scheduled 108 110 1.9% 7.35 8.27 12.5%

Charter 28 9 -67.9% 0.22 0.38 72.7%

Scheduled international 76 76 0.0% 6.76 7.38 9.2%

Scheduled domestic 35 34 -2.9% 8.64 10.27 18.9%

Medium-haul 105 89 -15.2% 7 9 28.6%

Long-haul 31 30 -3.2% 2.82 3.63 28.7%

* Aeroflot only (not counting Donavia and Nordavia)

2.2 2.3 2.4 2.5 2.4 3.0

0.7 0.8 0.9 1.1 1.2

1.5

58.1% 57.9% 57.9% 57.9% 57.9% 63.3%

29.1

122.4 120.1 115.5 117.9 107.4 121.5

31.7 38.2 41.3 41.5

49.1

International Domestic

46 47

2.3. Operations

»

»

Passengers carried under codesharing agreements increased by 37.3% in 2010

Membership of the SkyTeam alliance broadens passenger choice and ensures international standards of quality

At the start of 2011 Aeroflot had codesharing agreements with 28 foreign and Russian airlines and interline agreements with 196 airlines, 6 of them Russian and 12 from CIS countries.In the past year (2010) Aeroflot carried almost 1.6 million passengers on marketing flights under codeshare agreements, which is 37.3% more than in 2009. Of these, 78% were flights inside Russia and 22%

were international flights. Aeroflot’s biggest codesharing partners last year were Czech Airlines, Air France, Belavia, Alitalia and KLM (among foreign airlines), and Nordavia, Donavia and Rossiya (among Russian airlines). Codeshare arrangements enabled Aeroflot to increase flight frequencies, access restricted markets, expand the route network and make more effective use of its own fleet.

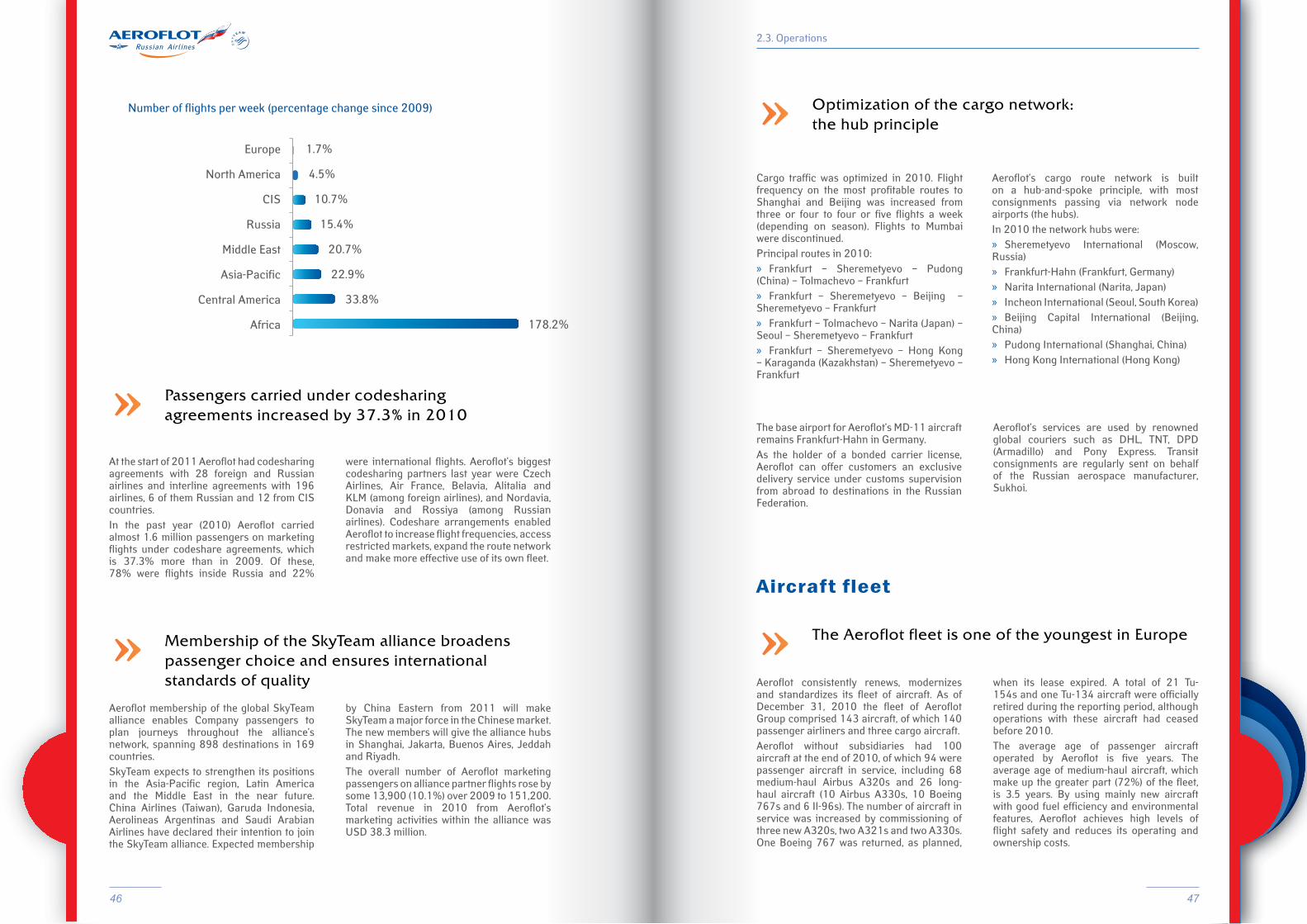

Aeroflot membership of the global SkyTeam alliance enables Company passengers to plan journeys throughout the alliance’s network, spanning 898 destinations in 169 countries.SkyTeam expects to strengthen its positions in the Asia-Pacific region, Latin America and the Middle East in the near future. China Airlines (Taiwan), Garuda Indonesia, Aerolineas Argentinas and Saudi Arabian Airlines have declared their intention to join the SkyTeam alliance. Expected membership

by China Eastern from 2011 will make SkyTeam a major force in the Chinese market. The new members will give the alliance hubs in Shanghai, Jakarta, Buenos Aires, Jeddah and Riyadh.The overall number of Aeroflot marketing passengers on alliance partner flights rose by some 13,900 (10.1%) over 2009 to 151,200. Total revenue in 2010 from Aeroflot’s marketing activities within the alliance was USD 38.3 million.

» Optimization of the cargo network: the hub principle

Cargo traffic was optimized in 2010. Flight frequency on the most profitable routes to Shanghai and Beijing was increased from three or four to four or five flights a week (depending on season). Flights to Mumbai were discontinued.Principal routes in 2010: » Frankfurt – Sheremetyevo – Pudong

(China) – Tolmachevo – Frankfurt » Frankfurt – Sheremetyevo – Beijing –

Sheremetyevo – Frankfurt » Frankfurt – Tolmachevo – Narita (Japan) –

Seoul – Sheremetyevo – Frankfurt » Frankfurt – Sheremetyevo – Hong Kong

– Karaganda (Kazakhstan) – Sheremetyevo – Frankfurt

The base airport for Aeroflot’s MD-11 aircraft remains Frankfurt-Hahn in Germany.As the holder of a bonded carrier license, Aeroflot can offer customers an exclusive delivery service under customs supervision from abroad to destinations in the Russian Federation.

Aeroflot’s services are used by renowned global couriers such as DHL, TNT, DPD (Armadillo) and Pony Express. Transit consignments are regularly sent on behalf of the Russian aerospace manufacturer, Sukhoi.

Aeroflot’s cargo route network is built on a hub-and-spoke principle, with most consignments passing via network node airports (the hubs).In 2010 the network hubs were: » Sheremetyevo International (Moscow,

Russia) » Frankfurt-Hahn (Frankfurt, Germany) » Narita International (Narita, Japan) » Incheon International (Seoul, South Korea) » Beijing Capital International (Beijing,

China) » Pudong International (Shanghai, China) » Hong Kong International (Hong Kong)

» The Aeroflot fleet is one of the youngest in Europe

Aircraft fleet

Aeroflot consistently renews, modernizes and standardizes its fleet of aircraft. As of December 31, 2010 the fleet of Aeroflot Group comprised 143 aircraft, of which 140 passenger airliners and three cargo aircraft.Aeroflot without subsidiaries had 100 aircraft at the end of 2010, of which 94 were passenger aircraft in service, including 68 medium-haul Airbus A320s and 26 long-haul aircraft (10 Airbus A330s, 10 Boeing 767s and 6 Il-96s). The number of aircraft in service was increased by commissioning of three new A320s, two A321s and two A330s. One Boeing 767 was returned, as planned,

when its lease expired. A total of 21 Tu-154s and one Tu-134 aircraft were officially retired during the reporting period, although operations with these aircraft had ceased before 2010.The average age of passenger aircraft operated by Aeroflot is five years. The average age of medium-haul aircraft, which make up the greater part (72%) of the fleet, is 3.5 years. By using mainly new aircraft with good fuel efficiency and environmental features, Aeroflot achieves high levels of flight safety and reduces its operating and ownership costs.

Number of flights per week (percentage change since 2009)

Europe

North America

CIS

Russia

Middle East

Asia-Pacific

Central America

Africa

1.7%

4.5%

10.7%

15.4%

20.7%

22.9%

33.8%

178.2%

48 49

»

»

Fuel efficiency of the fleet is steadily improving

Aeroflot will continue to receive new aircraft in 2011

Fleet renewal and modernization in 2010 meant that Aeroflot was able to improve fuel efficiency. Specific fuel consumption was

313 grammes per tonne-kilometer, which is 79 grammes less than in 2009.

Aeroflot will continue to develop its aircraft fleet in 2011 by taking delivery of new aircraft, both medium-haul A320s and long-haul A330s. The latter will replace Boeing 767-300ERs now coming to the end of their lease terms, with the result that average age of the fleet will be further reduced. All of the

Airbus craft will be delivered new from the Airbus factory in Toulouse.

In 2011 Aeroflot plans to acquire the first Russian-made Sukhoi Superjet 100 aircraft. They will both add a new regional class to the Company’s fleet and boost development of domestic air transport.

Composition of Aeroflot Group fleet as of December 31, 2010

2.3. Operations

Specific fuel consumption, grammes/TKM

Average daily flying hours by aircraft type

Type of aircraft Aeroflot - Russian Airlines

Donavia Nordavia Group total

OwnedIlyushin Il-96-300 6 - - 6Ilyushin Il-86 2 - - 2Tupolev Tu-154 1 3 - 4Tupolev Tu-134 - - 8 8Antonov An-24 - - 2 2Total owned 9 3 10 22

Financial leaseAirbus A-319 4 - - 4Airbus A-320 1 - - 1Airbus A-321 18 - - 18Boeing 737 - 5 2 7Total finance lease 23 5 2 30

Operating leaseAntonov An-24 - - 3 3Antonov An-26 - - 1 1

Ilyushin Il-86 - 1 - 1Airbus A-319 11 - - 11Airbus A-320 34 - - 34Airbus A-330 10 - - 10Boeing B-737 - 5 13 18Boeing B-767 10 - - 10McDonnell Douglas MD-11 3 - - 3Total operating lease 68 6 17 91Total fleet 100 14 29 143

Enhanced maintenance and repair capability

Maintenance and repair

Maintenance and repair of the Aeroflot fleet is designed to ensure flight safety and maintain high levels of reliability and regularity. The Company strives to optimize costs by expanding the range and raising the quality of work, which it carries out itself.In 2010 this work had to be done while new foreign-made aircraft were being added to the fleet, so learning new ways of working and advanced maintenance methods to service foreign aircraft was a priority. For the first time Aeroflot independently carried out a labor-intensive 6Y-check on eight aircraft of the A320 family.In anticipation of planned arrival of the new Sukhoi Superjet 100s, the Company has developed a comprehensive plan for their commissioning and for organization

of independent maintenance by Aeroflot. Company representatives have checked the state of completion of the aircraft at Sukhoi’s manufacturing plant at Komsomolsk-on-Amur (KnAAPO) and take an active part in working groups and the industry coordinating committee, which are devising basic requirements for maintenance programmes.Cost reduction programmes have led to increase in the amount of maintenance, which Aeroflot carries out itself and reduction of outsourcing. Current contracts with suppliers were revised in 2010, which has also reduced costs. Total effect of these initiatives was USD 16.89 million in the reporting year.

Further expansion of the Company’s aircraft component inspection and repair facilities is planned for 2011, including capabilities for refilling of portable oxygen bottles, in-house servicing and repair of emergency escape slides, life rafts, A320/A330 avionics made by Zodiac Aerospace, A320/A330 inertial and radio-frequency equipment by Honeywell International, the Teledyne Controls WGL

wireless data transmission system and A330 in-flight entertainment systems by Panasonic Avionics. The Company also plans to introduce an automated material resource planning system for maintenance, based on SAP ERP, and pre-design work began in 2011 on a new and modern maintenance hangar to be built at Sheremetyevo airport.

» Safety and efficiency are the main priorities

In 2010 Aeroflot provided maintenance services to 27 airlines and 20 other enterprises in the aerospace maintenance business. Aeroflot plans to expand these

capacities, increasing sale of aircraft maintenance services to other Russian airlines in 2011.

» Aeroflot maintains aircraft of other carriers as well as its own fleet

Il

50 51

Aeroflot strives to maintain the highest international standards of passenger service. A customer loyalty survey begun in early 2010 jointly with the American company Bain (using the Net Promoter Score system) found that Aeroflot customer loyalty was 44%, which is significantly higher than that of leading European and US carriers.Aeroflot has renewed its ‘secret passenger’ project designed to research how well

customer service standards are implemented. The results show a positive trend, with the Company’s overall score rising from 82% to 88% and one aspect of operations – the call center – scoring 94%.Aeroflot also carried out large-scale customer satisfaction and loyalty surveys during 2010 in cooperation with other organizations, including IATA, the European company EPSI, and the international SkyTeam alliance.

It is a basic requirement of SkyTeam alliance members that they provide the same level of service on all flights. In 2010 Aeroflot ran a number of programmes to harmonize services with leading companies of the alliance and helped to write a new version of the requirements.For example, from September 15, 2010 Aeroflot has been using the Passenger Information List (PIL) to give personal on-board welcomes to Elite and Elite Plus passengers and alliance bonus programme members in all classes. The SkyTeam Sky Priority project, begun in November 2010, creates a range of services at departure and arrival airports allowing passengers to pass

through all airport formalities quickly and save time on departure. These services will be offered to passengers travelling in C class (business), or Y class (economy) if they are in the Elite Plus category. Aeroflot plans to continue implementation in 2011.In November 2010 work began on the Lounge Preposition project, which assesses lounges used by C class passengers of SkyTeam members, categorizes business lounges and will enable a Team Lounge Model to be implemented. The project assesses lounges at Sheremetyevo Terminal D against a range of criteria. Evaluation of lounges at airports elsewhere in Russia is planned for 2011.

On-board services are constantly enhanced by improved catering, comfort items, equipment and entertainment systems. In 2010 Aeroflot offered new travel kits to business-class passengers on medium-haul and long-haul flights. There are proposals to vary the on-board catering to match flight duration and time of day. Interior design concepts have been devised for new aircraft.

Economy-class passengers are now served wine in addition to the existing beverage range. Specific product ranges have been devised for the six airlines new to Aeroflot. The on-board entertainment package has been expanded and improved to include a wider choice of films, music programmes, in-flight publications, and newspapers and magazines.

Compliance with SkyTeam standards

Development of on-board services

Brand and service quality development

2.3. Operations

» Service quality is a priority

Client relations

Procedures for handling customer messages to the Company (received by post, email, ticket offices, local branches) have been organized according to subject matter, enabling complaints to be dealt with much

more quickly. Aeroflot has expanded the types and amounts of compensation available at the Company’s discretion for inconvenience suffered by travelers on its flights.

Quality management improvements

The Aeroflot Bonus frequent flyer reward scheme

Brand development

The quality management system of Aeroflot and its subsidiary airlines aims to ensure that passengers arrive at their destinations in safety and comfort and with guaranteed regularity. In the past year Aeroflot has continued the process of applying the Company’s established high quality requirements to services provided by subsidiaries.In October 2010 Aeroflot successfully carried out an audit of compliance of its quality

management system with the latest version of the international ISO 9001:2008 standard and obtained the relevant internationally recognized certificate. The fact that Aeroflot is ISO 9001:2008 compliant shows maturity of its management system and ability of the Company to maintain high-quality service provision. The new standard achieves increasing integration of quality management with general business management.

In 2010 Aeroflot carried out a series of measures designed to improve services and develop and promote its loyalty scheme for frequent flyers. By the end of the year the scheme had almost 2.4 million members. Over 400,000 new members joined in 2010.A number of changes to the rules of the Aeroflot Bonus programme were made in order to improve the financial effect of the programme, attract new members and increase customer loyalty. They included: » Harmonization of the terms of Aeroflot’s

bonus programmes with equivalent programmes of SkyTeam global alliance partners. » Offering one-way flights as a new type of

Aeroflot Bonus reward. » New members may now earn points for

flights taken up to six months before joining the scheme, instead of one month. » To prevent inappropriate or commercial

use of reward tickets, the number of reward flights that may be taken is now limited to 10 a year. » Access to reward flights has been

improved by simplifying the application procedure. » The Company website now contains handy

new gadgets, including an online reward calculator for working out the number of miles needed for the next reward and a

distance calculator, which automatically takes account of the tariff paid by the traveler and his/her membership level. » Design and functionality of the