October 11, 2013

16

BC First Nations LNG Summit October 9th & 10th, 2013 Discussion Paper: How do First Nations Get a Fair, Just and Honourable Agreement and Share in the Benefits that will flow from the Proposed LNG Project Developments in British Columbia

-

Upload

black-press -

Category

Documents

-

view

214 -

download

0

description

Section J of the October 11, 2013 edition of the Richmond Review

Transcript of October 11, 2013

BC First NationsLNG Summit

October 9th & 10th, 2013

Discussion Paper:How do First Nations Get a Fair, Just and Honourable Agreement and Share in the

Benefits that will flow from the Proposed LNG Project Developments in British Columbia

Table of Contents Introduction ................................................................................................................................................................................ 3

Background and Analysis .................................................................................................................................................. 4

The LNG Business and Risks ........................................................................................................... 4/6 1. What is LNG?

2. Components of an LNG Project.

3. Gas Reserves Worldwide are Enormous.

4. Economics and Risks of an LNG Project.

5. Objectives of LNG Seller and LNG Buyer.

BC LNG Projects in the Study Phase ................................................................................................. 7

Key Things Required in Advance of a Financial Investment Decision ............................................. 8

Assessment of the Proposed BC LNG Projects and Pipelines ........................................................ 8/9

What is an Energy Corridor? ........................................................................................................... 10

Types and Potential Sources of Accommodation to First Nations ........................................... 10/11

Pipeline Settlements with First Nations in Canada .................................................................. 12/13

1. Mackenzie Valley Pipeline

2. Pacific Trails Pipeline

3. Alaska Highway Pipeline Project

Strategies .................................................................................................................................... 14/15

1. LNG Company’s Strategy (Assumed)

2. Pipeline Company’s Strategy (Assumed)

3. Possible First Nations Strategies and Options

4. Negotiate Separately versus Negotiate as a Group

Conclusions ............................................................................................................................................................................ 16

References .............................................................................................................................................................................. 16

BC First Nations Energy Mining Council 2

Introduction

First Nations have Aboriginal title and rights to the lands and resources in British Columbia.

Domestic and International laws are clear that First Nations have a role in decisions prior to any

development.

On too many occasions First Nations have not received the benefits promised from projects that

were developed on their lands.

Decisions have been made for land use that has impacted the First Nations way of life and

traditional sites without consultation and appropriate accommodation for the impact.

Some projects develop and the benefits do not materialize or are abandoned and leave behind

the destruction on the land for First Nations to manage. Others create disappointment when

they do not proceed after much hard work in the First Nations communities.

A number of coastal LNG project proposals have been announced that would result in pipelines

being constructed on First Nations Lands. The cumulative impact of these projects is of major

concern and First Nations need to be consulted and accommodated.

First Nations insist that their title, rights, and interests be dealt with through government-to-

government engagement. Discussions need to be had on shared land management, shared

decision making and revenue sharing. In addition, agreements between the companies and the

impacted First Nations must also occur.

The purpose of this paper is to inform First Nations about the economics of LNG projects and facilitate

discussion on strategies for ensuring First Nations title and rights are acknowledged and a fair share of

benefits is received.

BC First Nations Energy Mining Council 3

Background and Analysis

The LNG Business and Risks

1. What is LNG? LNG is natural gas that when chilled to -160 Celsius turns to liquid 1/600 its original size. In this state it can be transported by ship or truck.

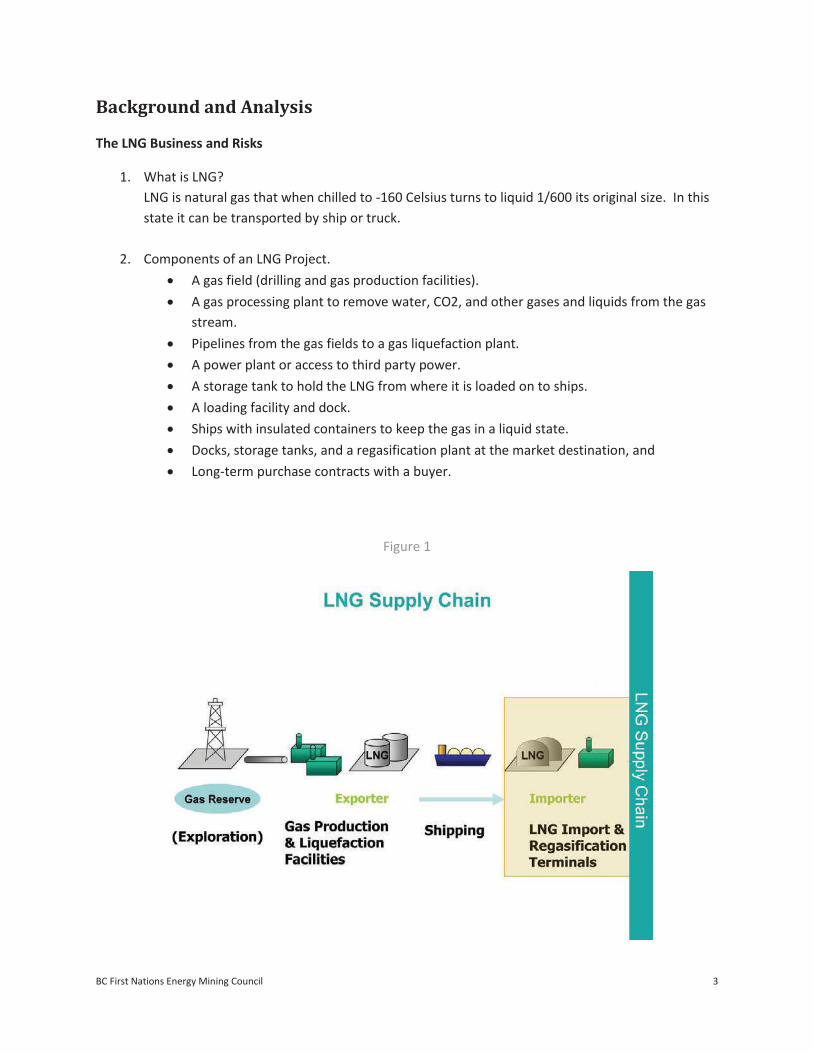

2. Components of an LNG Project. A gas field (drilling and gas production facilities). A gas processing plant to remove water, CO2, and other gases and liquids from the gas

stream. Pipelines from the gas fields to a gas liquefaction plant. A power plant or access to third party power. A storage tank to hold the LNG from where it is loaded on to ships. A loading facility and dock. Ships with insulated containers to keep the gas in a liquid state. Docks, storage tanks, and a regasification plant at the market destination, and Long-term purchase contracts with a buyer.

Figure 1

BC First Nations Energy Mining Council 4

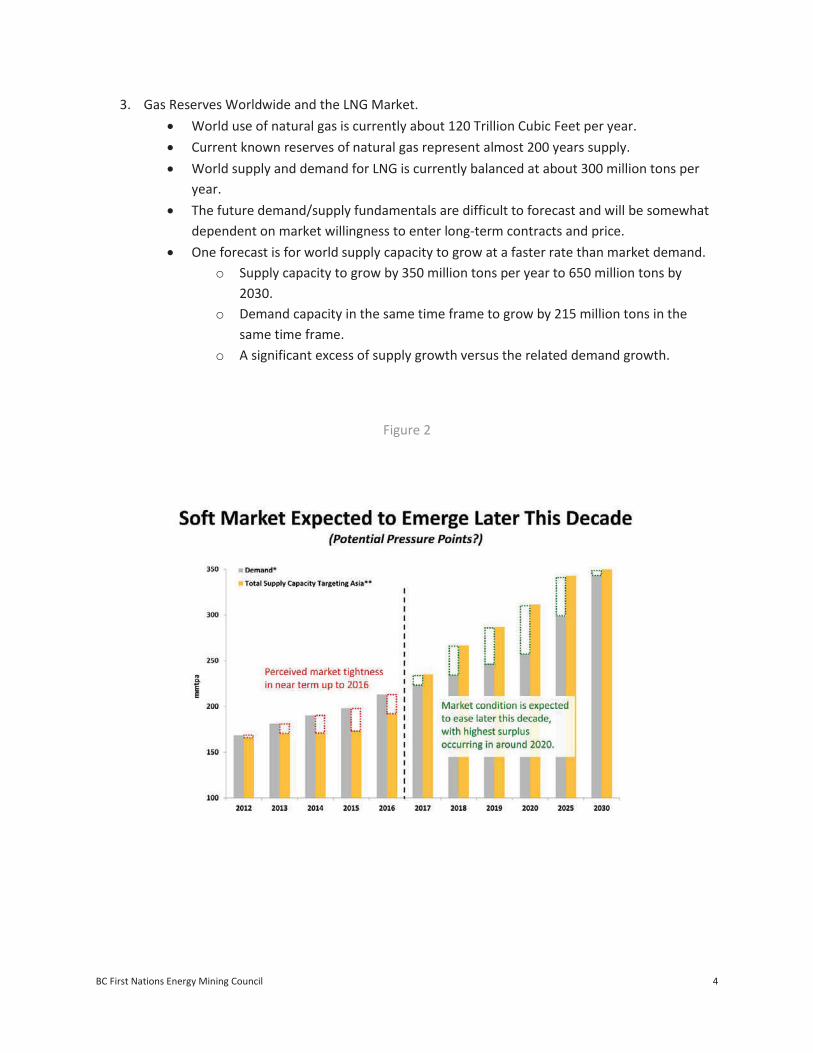

3. Gas Reserves Worldwide and the LNG Market.

World use of natural gas is currently about 120 Trillion Cubic Feet per year.

Current known reserves of natural gas represent almost 200 years supply.

World supply and demand for LNG is currently balanced at about 300 million tons per

year.

The future demand/supply fundamentals are difficult to forecast and will be somewhat

dependent on market willingness to enter long-term contracts and price.

One forecast is for world supply capacity to grow at a faster rate than market demand.

o Supply capacity to grow by 350 million tons per year to 650 million tons by

2030.

o Demand capacity in the same time frame to grow by 215 million tons in the

same time frame.

o A significant excess of supply growth versus the related demand growth.

Figure 2

BC First Nations Energy Mining Council 5

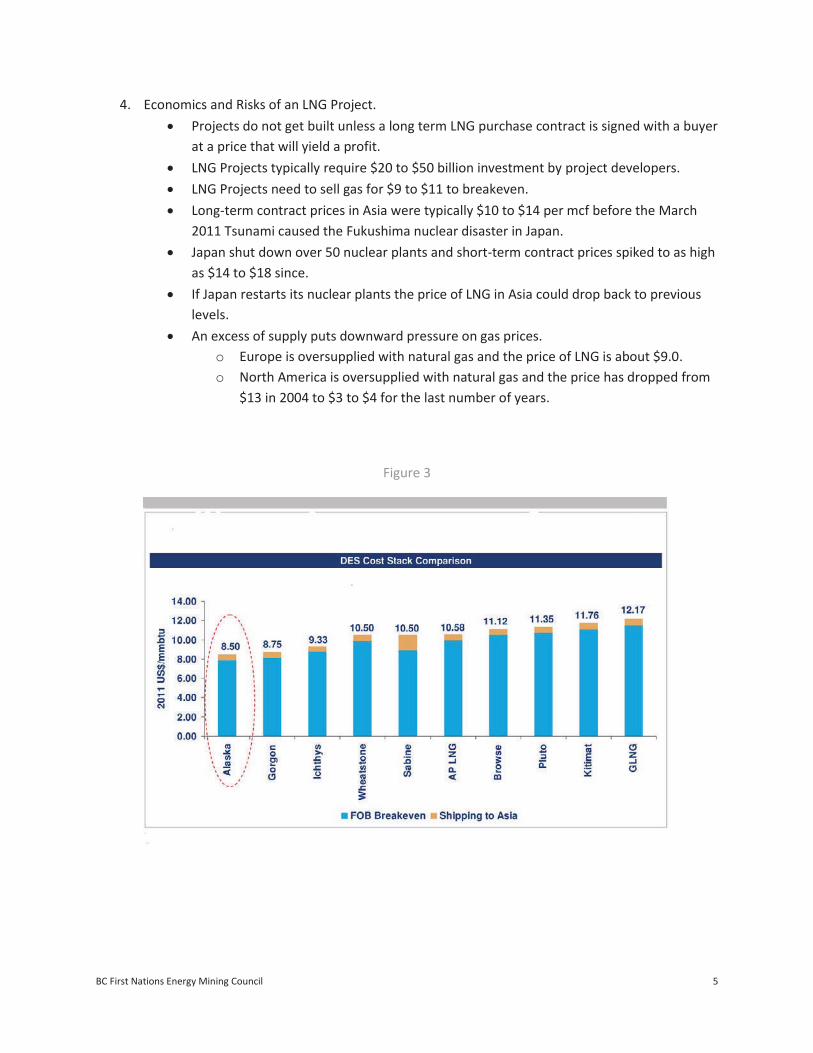

4. Economics and Risks of an LNG Project.

Projects do not get built unless a long term LNG purchase contract is signed with a buyer

at a price that will yield a profit.

LNG Projects typically require $20 to $50 billion investment by project developers.

LNG Projects need to sell gas for $9 to $11 to breakeven.

Long-term contract prices in Asia were typically $10 to $14 per mcf before the March

2011 Tsunami caused the Fukushima nuclear disaster in Japan.

Japan shut down over 50 nuclear plants and short-term contract prices spiked to as high

as $14 to $18 since.

If Japan restarts its nuclear plants the price of LNG in Asia could drop back to previous

levels.

An excess of supply puts downward pressure on gas prices.

o Europe is oversupplied with natural gas and the price of LNG is about $9.0.

o North America is oversupplied with natural gas and the price has dropped from

$13 in 2004 to $3 to $4 for the last number of years.

Figure 3

BC First Nations Energy Mining Council 6

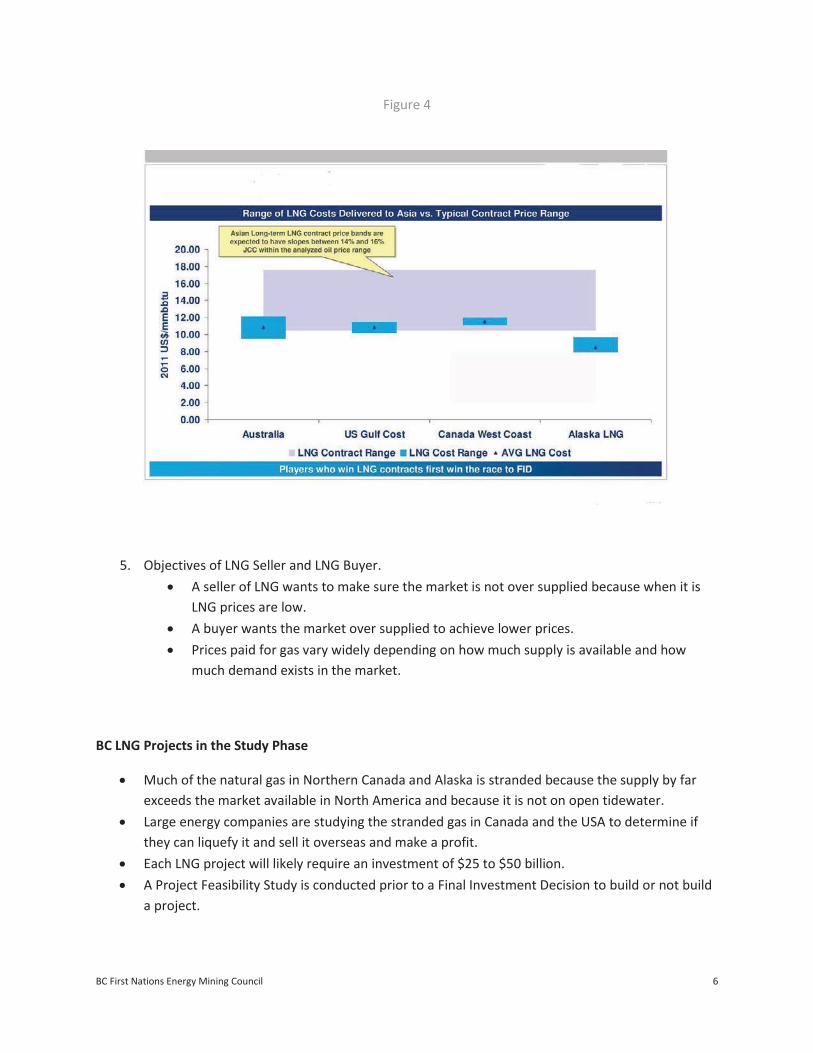

Figure 4

5. Objectives of LNG Seller and LNG Buyer. A seller of LNG wants to make sure the market is not over supplied because when it is

LNG prices are low. A buyer wants the market over supplied to achieve lower prices. Prices paid for gas vary widely depending on how much supply is available and how

much demand exists in the market.

BC LNG Projects in the Study Phase

Much of the natural gas in Northern Canada and Alaska is stranded because the supply by far exceeds the market available in North America and because it is not on open tidewater.

Large energy companies are studying the stranded gas in Canada and the USA to determine if they can liquefy it and sell it overseas and make a profit.

Each LNG project will likely require an investment of $25 to $50 billion. A Project Feasibility Study is conducted prior to a Final Investment Decision to build or not build

a project.

BC First Nations Energy Mining Council 7

The key things required in advance of a Final Investment Decision to build the project are:

Market studies to determine demand and selling price of the gas.

Drilling to prove the gas reserves required are present.

Commitment of the gas reserves to the LNG project.

Approval of the National Energy Board to export the gas.

LNG plant site selection.

Pipeline route selection.

Consultation and accommodation with First Nations.

First Nations capacity development and funding.

Environmental and traditional knowledge studies.

Regulatory approvals.

Negotiated and committed access to the land.

Engineering based cost estimate of the project.

Asian regulatory approvals and final investment decisions for the import of the gas and

construction of the receiving facilities.

Comparison of risk and profitability to alternative projects in BC and other parts of the world.

Signed long-term sales purchase agreements between LNG Producers and Asian buyers.

BC LNG Projects are in the Project Feasibility and Study phase leading up to the Final Investment Decision that will determine if the projects will be constructed or not.

Assessment of the Proposed BC LNG Projects and Pipelines

1. Too many projects are proposed – while likely some will be built - not all projects can be built

and it is possible none of the projects will be built.

Kitimat LNG – Pacific Trails - Chevron, Apache 10 mm tons.

Pacific NW LNG – Lelu Island - Prince Rupert –TransCanada- Petronas, Japan Expl - 19.7

mm tons.

LNG Canada – Kitimat –TransCanada - Shell, Korea Gas, Mitsubishi of Japan, PetroChina-

24 mm tons.

Douglas Channel – Kitimat LNG Partners- PNG - Haisla Nation – 1.8 mm tons.

Prince Rupert LNG – BG – 21.6 mm tons.

WCC LNG – Kitimat or Prince Rupert – Imperial Oil, Exxon, 30 mm tons.

2. Sharing of fewer LNG projects amongst Chevron, Shell, and Petronas would reduce risk and

increase profit:

Already partners in various other ventures around the world.

Not over supply market.

Better LNG prices.

Fewer pipelines.

Not compete for scarce materials and labor.

BC First Nations Energy Mining Council 8

Fewer First Nations to negotiate with.

3. In Australian three LNG plants and separate pipelines were built side by side. None of the

projects is earning a good return. Sharing projects instead of building competing projects yields

higher returns and lower risk because it is easier to control market pricing and costs to build the

projects.

4. There is not enough capacity in Canada or North America to build all projects in the same time

frame. There is already competition for limited labor, materials, capital and engineering

amongst Oil Sands Plants, LNG Projects, other Pipeline Projects, and other non-energy projects

worldwide. The BC LNG proponents know of the shortage of resources and the cost overruns

than can result. Their Final Investment Decisions will highlight these risks.

5. The BC LNG Proponents are doing Project Studies on LNG Projects in other countries. They have

potential LNG projects in the United States, East Africa, Australia, Russia, and Middle East.

6. These projects are in competition with BC to supply the Pacific LNG market.

7. Canada has an abundance of stranded natural gas that is available for export. It has good access

to the Asian markets with a 10-day sailing time versus 7 days for Australia and 14 days for the

Middle East.

8. Risks for BC LNG Projects include access to First Nations lands, length of the regulatory

processes, and the taxes that the BC Government will require have not yet been announced.

9. Exporting significant quantities of LNG could cause the price of domestic supplies of energy and

the cost of labor in Canada to increase.

Inflation for Canadians and cost pressures for manufacturing.

Increased profits for companies selling natural gas into the Canadian market.

10. Canada in 2012 produced 13 bcf/d of gas. If all the contemplated BC LNG projects preceded it

could double this level of production.

11. Not all LNG projects being studied worldwide can be constructed. The BC LNG projects are in a

race with each other and with LNG projects worldwide to get to Final Investment Decision.

Hence the urgency expressed by TransCanada pipelines to have First Nations negotiations

completed by mid 2014.

BC First Nations Energy Mining Council 9

What is an Energy Corridor?

There have been discussions of an Energy Corridor.

An Energy Corridor is a negotiated agreement between First Nations and Government that must

consider First Nations title and rights and contains First Nations land use terms of shared management,

shared decision making and shared revenues.

The terms to build a pipeline are known in advance to First Nations and to persons wishing to

build a pipeline.

First Nations that wish to participate in the Energy Corridor Agreement can do so.

It can be one strip or piece of land where all gas pipelines must be constructed on meeting the

terms or it could be multiple pieces of land if engineering and economics require.

Types and Potential Sources of Accommodation to First Nations

1. Types of accommodation include jobs, training, business opportunities, capacity funding, and

money and/or equity ownership.

2. Sources of accommodation can include Revenue sharing with Governments and Energy

Companies and accommodation from Pipeline Company for impact on the land.

3. Assuming an LNG price of $14.50 total revenues from a 3 bcf/d LNG plant are estimated at $15

billion per year or $400 to $800 billion over the 25 to 50 year life of a project. If costs are $10

the profit could be $4 billion per year or $100 to $200 billion over the life of the project.

4. The taxes governments will take from the project have not yet been announced but it is

reasonable to assume taxes of at least $3 billion per year or $75 billion or more in the first 25

years.

BC Government receives Royalties from gas production and Income Tax from profits.

Royalties are paid whether there is a profit or not.

Federal Government receives Income Tax on profits.

Municipal Governments receive Property Tax Revenues whether there is profit or not.

5. Pipeline companies will make the least money in an LNG project, typically 2 to $3 billion dollars

over the entire life of the project.

Pipeline companies typically receive a fixed return on their equity invested of 8 to 12%.

Return is largest in year 1 and declines each year until it is almost zero after 25 years.

First Nations accommodation that comes out of pipeline company profit is limited to a

percentage of the profit.

BC First Nations Energy Mining Council 10

First Nations accommodation from pipeline companies if billed to Energy companies is

not limited by pipeline profit.

6. Pipeline Throughput Charge.

No history.

The concept is First Nations receive a royalty for every mcf of gas that passes through

the pipeline.

A 3 bcf/d pipeline would yield $11 million per year for every 1-cent royalty charge.

A 2-cent royalty charge would yield $1.1 billion over 50 years.

Unlikely this type of agreement can be made with the pipeline company. Pipeline

companies do not make money on the gas that flows through the pipeline. They are

merely transporting it for other parties.

Unlikely the Energy companies will negotiate directly with First Nations.

o Some of them are Oil Sands Producers.

o They will claim it is not their pipeline.

o But it is their gas in the pipeline.

May have to negotiate Royalty with the Province.

7. The parties that have the big money are the governments and the energy companies. Not the

pipeline companies.

8. Accommodation from the energy company could be a throughput charge for every mcf of gas

that flows through the pipeline or from the BC government a sharing of the royalty charged on

gas sales.

9. The greater the capital cost of the project the greater the accommodation to First Nations.

The Profit they will make is dependent on the Capital Cost of the Pipelines and three things they

have already negotiated with the LNG Project Proponents.

The Rate of Return on their investments.

Whether the accommodation they pay to First Nations for crossing their land will come

out of Pipeline Profits or will be billed to the LNG Project Proponents separately.

They are responsible for cost overrun risk.

10. Care must be taken not to accept a onetime deal that allows the pipelines or LNG projects to

expand beyond their initial capacity without payment of additional accommodation when the

project expands.

BC First Nations Energy Mining Council 11

Examples of Pipeline Settlements with First Nations in Canada

Pipelines that operate as Limited Partnerships have approximately 50% more cash flow to distribute to

the Equity Owners than do Pipelines that are Limited Companies. That is because Limited Partnerships

do not pay income tax before they distribute their cash flow. Limited Companies must pay income tax

before they distribute cash to the equity owners.

Equity ownership in a Limited Partnership is much better than equity ownership in a Limited Company.

Mackenzie Valley Pipeline (Limited Partnership)

Mackenzie Valley First Nations had the right to purchase 33.3% of the pipeline project.

The pipeline was estimated to cost $4.8 billion.

The pipeline was to be financed 70% with debt and 30% with equity (typically savings -

money the investor already has).

The Mackenzie Valley First Nations needed $1.6 billion of debt financing ($1.15 billion

for the 70% debt component plus $0.47 billion to purchase the 30% equity component).

The $1.15 billion debt component could be borrowed. The $0.47 billion equity

component would have been difficult to borrow without a Government Guarantee.

Assuming they were able to finance the equity purchase the Aboriginal Pipeline Group

of the Mackenzie Valley estimated the First Nations could have received $800 million

(before tax) over the 20-year life of the project.

Pacific Trails Pipeline (Limited Partnership)

Pacific Trails First Nations had the right to purchase 30% of the equity in that pipeline

including the equity for pipeline expansions.

Unlike the Mackenzie Valley First Nations the Pacific Trails First Nations were not

required to borrow the 70% debt component of the total financing. The pipeline

company would borrow 100% of the 70% debt component.

The First Nations required approximately $150 million to complete the equity purchase.

The government of BC agreed to give the First Nations $30 to complete the purchase

and the First Nations would have been required to borrow the other $120 million. The

$120 million would have been very difficult to borrow.

BC First Nations Energy Mining Council 12

The project was subsequently changed and the pipeline ceased to be a separate entity

so there was no equity to purchase.

The $200 million settlement appears to be a good proxy for the value of that right to

purchase 30% equity.

Alaska Highway Pipeline Project (Limited Company)

Alaska Highway First Nations were negotiating equity purchase in the TransCanada

owned Alaska Highway Pipeline Project.

The First Nations would have been required to borrow the money to purchase the

equity. TransCanada was agreeable to financing enhancements that would have

assisted the First Nations in their attempt to borrow the money (something the

Mackenzie Valley and Pacific Trails First Nations did not have).

The equity purchase would have been difficult to finance without a Government

Guarantee.

TransCanada would not offer more than 10% of the equity.

The Alaska Highway First Nations were seeking accommodation greater than what

TransCanada was offering, the right to purchase the equity up to two years after the

project was constructed, and the right to sell the equity interest to a third party without

a Right of First Refusal for TransCanada.

The parties could not resolve the differences and TransCanada broke off negotiations on

equity.

Lower Churchill Falls Hydro Project

Agreement signed amongst the Innu of Labrador, the Government of Canada,

Newfoundland and Labrador.

Benefits to Innu estimated in excess of $1 Billion, including a 5% royalty on

Newfoundland Labrador crown corporations net project revenues.

Government of Canada provided loan guarantee to project of $6.3 billion settled Innu

Land Claim and Redress Agreement related to 1960’s Churchill Falls hydro development.

The Government of Canada and Newfoundland Labrador made this project happen

through agreements they signed with the Innu - industry is not part of the agreement.

BC First Nations Energy Mining Council 13

Strategies

LNG Energy Companies Strategy (Assumed)

1. Put a pipeline company with limited profit between LNG project and negotiations with First

Nations.

2. Build alliances with other proposed LNG projects, share ownership, and reduce risk.

3. Build more than one pipeline on a pipeline right of way and service more than one LNG Project.

Pipeline Strategy (Assumed)

1. Settle First Nations accommodation for approximately same accommodation as Pacific Trails

Settlement ($200 million even though pipeline will cost 3 times as much).

2. Define options for alternative pipeline routes to each LNG Project.

3. Avoid and build around anticipated pockets of First Nations resistance.

4. Make a reasonable approach to consultation and dealing with First Nations.

Negotiate with First Nations individually and pick off as many as possible to

demonstrate reasonable effort to consult.

If negotiation fails to secure entire pipeline route and if build around not feasible,

o government legislate project in national interest.

o have court set compensation.

First Nations have accepted the Pacific Trails Pipeline and if some accept TransCanada

offer evidence is pipeline on land is only a matter of compensation to First Nations.

Possible First Nations Negotiating Strategies and Options

1. While the pipeline company will own the pipe in the ground - the gas in the pipeline is part of

the LNG project.

Gas could flow through the pipeline for 50 to 75 years or more.

The pipeline company profits and their offer of accommodation will end in about 25

years.

2. Seek royalty for gas that flows through the pipeline and accommodation for the pipeline impact

on the land.

3. Form an Energy Corridor or Corridors in negotiation with province to include shared

management, shared decision making, and revenue sharing.

4. It is recommended that negotiations occur in the following order:

Government to government negotiations with the Province:

o capacity funding.

o shared management and decision-making.

o revenue sharing for as long as the gas flows through the pipeline.

Seek negotiations with the Energy Companies to discuss a throughput charge for as long

as the gas flows.

BC First Nations Energy Mining Council 14

Negotiate with the pipeline company for jobs, business opportunities, and

accommodation for impact on land.

o Pacific Trails capital cost was $1.5 Billion and accommodation to First Nations

was $200.

o Coastal Gas Link and Prince Rupert Link guesstimated cost $4.5 billion each -

accommodation should be $600 million each.

Seek contribution from the Federal Government.

5. Develop scenarios before the meetings to determine the First Nations communications or asks.

6. Do not say No Pipeline even if you do not want an LNG project, gas development or a pipeline.

It takes away your negotiating position.

The objective is to negotiate benefits and accommodation.

If you do not want a development say I need to study it and request funding.

If you want a project say you need funding and say how much accommodation

is required.

Negotiate Separately versus Negotiate as a Group

1. First Nations that negotiate separately.

Have less land to offer and less negotiating power.

o Companies have more risk of getting others on side so not worth as much.

Other side will try to divide and conquer and do any deals with the First Nations that

have least capacity.

Pipeline may look to build around or have government and courts settle with First

Nations if they do not accept what other First nations accept.

Unlikely government or energy companies will negotiate with individual first nations.

o Will not have a say in what is negotiated for all by bigger group.

2. Power is obtained by working together. If First Nations on a pipeline route work together:

Power to ensure they get a reasonable share of profits.

Better chance of getting negotiations with Province and Energy companies.

Offer the pipeline company settlement of a larger piece of land.

No route of least resistance if all First Nations are aligned.

3. Maximum negotiation power would result if all of the First Nations on all pipeline routes worked

together and negotiated accommodation for all routes at the same time.

Eliminates the prospect that pipeline companies will go to an alternate route with more

agreeable First Nations.

Heightens the likelihood that a deal will get done before offshore opportunities displace

the BC opportunity.

BC First Nations Energy Mining Council 15

Conclusions and Assessment

1. Working together gives the greatest opportunity to participate in the desired outcome.

Government to government discussions on shared management, decision-making, and

revenue sharing.

Gives negotiating power to First Nations instead of Pipeline Companies.

2. Negotiate Energy Corridors with the Province for First Nations to join.

3. Negotiate accommodation for as long as gas flows through the pipeline – not 25 years as

proposed by a pipeline company.

4. LNG is a competitive business between LNG Projects in Canada and LNG Projects in other

nations. Assuming Final Investment Decisions can be made by end of 2014 or mid 2015 it is

likely one or two projects will be built. However it is also possible that none of the projects will

be built if the economics and risk factors of competing projects in other countries are better.

5. Negotiate with Governments, Energy Companies, and Pipelines to share revenues and provide

financial n accommodation.

6. Know when you have a deal:

Idea is have LNG companies build a project in Canada – not elsewhere in the world.

No project - none of the precedent setting benefits or financial accommodation.

The LNG companies pay everyone from the revenue from the sale of LNG.

o They are the source of revenue to Governments, Pipelines, First Nations, Others.

o It does not matter who pays the First Nations because all of the money is from

the LNG sales.

References

Figure 1. Alfred Sorenson Kitimat LNG June 3, 2006 (modified).

Figure 2. Robert Smith, FGE Dubai August 23, 2012 Asian Natural Gas: A Softer Market is coming.

Figure 3. Wood Mackenzie Alaskan LNG Exports Competitiveness Study July 27, 2011 (modified).

Figure 4. Wood Mackenzie Alaskan LNG Exports Competitiveness Study July 27, 2011 (modified).

Disclaimer: This Discussion Paper has been prepared for the limited purpose of identifying for First Nations, a number of considerations that may be relevant before participating in any economic activity associated with natural gas. The BC First Nations Energy and Mining Council and the authors of this Discussion Paper will not accept any responsibility for the accuracy and correctness of the contents. Accordingly any reliance by any person upon the contents of this Discussion Paper shall be at the sole risk of that person and without any legal recourse against the FNEMC or the authors.