Objectives - Blackburn, Childers & Steagall, CPAs · Objectives • Learn valuable computer...

13

5/16/2016 1 Chad Kisner, CPA, CISA, CITP Objectives • Learn valuable computer assisted auditing tools and techniques (CAATTs) to take back to your firm. These techniques include analysis of high‐risk audit areas such as those associated with fraud risks. • Learn how to leverage the AICPA Audit Data Standards and CAAT applications available in the marketplace to streamline audit processes. • Learn about techniques and tools, practical application of techniques in common risk areas and focused analyses and findings.

Transcript of Objectives - Blackburn, Childers & Steagall, CPAs · Objectives • Learn valuable computer...

5/16/2016

1

Chad Kisner, CPA, CISA, CITP

Objectives

• Learn valuable computer assisted auditing tools and techniques (CAATTs) to take back to your firm. These techniques include analysis of high‐risk audit areas such as those associated with fraud risks.

• Learn how to leverage the AICPA Audit Data Standards and CAAT applications available in the marketplace to streamline audit processes.

• Learn about techniques and tools, practical application of techniques in common risk areas and focused analyses and findings.

5/16/2016

2

Agenda• CAATs

• Definitions/Overview

• Audit Data Standards

• Discussion of Tests and Testing Ideas

What are CAATs?

• Tools• Packages designed for data analysis

• Database queries, report writers

• Spreadsheets

• Techniques• Manipulate data

• Analyze data from different sources

• Compare financial and non‐financial data

5/16/2016

3

AICPA Publications

• Evolution of Auditing: From the Traditional Approach to the Future Audit – November 2012

• Reimagining Auditing in a Wired World –August 2014

• See last page of this presentation for live links

CAATs & Substantive Procedures

• These can replace and/or supplement traditional substantive procedures• Allows the auditor to analyze 100% instead of sample

• Provides stratification/statistical analysis and improved sample selection

• Understanding related activities can help identify value added CAAT tests.

• Requirements• Integrity of Data

• Normalization of Data

5/16/2016

4

Consideration of Fraud –AU‐C Section 240

• The auditor should ordinarily presume that there is a risk of material misstatement due to fraud relating to revenue recognition AU‐C Section 240 provides examples of procedures to address risk of fraud related to revenue recognition• Substantive analytical procedures relating to revenue using disaggregated data

• Computer‐assisted audit techniques

• Discussions with personnel outside of finance

• Physical observation of sales cut‐off

• Testing controls

• AICPA –AU‐C Section 240 link to PDF on last page

What are Data Analytics?

• Data Analysis is defined as the process of looking at and summarizing data with the intent to extract useful information and develop conclusions. It employs various technologies and programming techniques

• Benefits of Data Analytics• Identify anomalies, patterns and indicators of risk

• Analyze large populations of data instead of samples

• Analyze data from disparate datasets, multiple systems or locations

5/16/2016

5

Phases of Data Analytics

• Acquire the Data

• Transformation and Standardization

• Management

• Analysis

• Reporting

Data Acquisition

• Types of client data that are acquired:• Invoices

• Journal Entries

• Employee Records

• Vendor Information

• Customer Information

• Acquire client’s data from multiple locations and/or systems

• Acquire client’s data from various media types and file formats

• Acquire large volumes of data

5/16/2016

6

Data Transformation & Standardization

• Standardize data from multiple systems

• Types of data needing transformation or standardization:• Names and addresses

• Date conversion

• Currency conversion

• Customer codes

Data Management

• Tools used to import, validate and analyze data• IDEA

• ACL

• Active Data for Excel

5/16/2016

7

Data Analysis

• Identify patterns of fraud• Vendors consistently at or just below signatory limit

• Payment of duplicate invoices

• Round dollar transactions

• Ghost employee analysis, including SSN comparison

• Conduct trend analysis• Change in vendors/amount spent with vendors over time

• Identify data anomalies• Manual journal entries made after 11:00 pm or on holidays

• Understand results• Iterative process, providing additional information when needed

Reports

• Reconciliations• Reconcile general ledger activity to trial balances

• Payroll• Compare the outstanding check list to bank statements

• Customers• Analyze A/R credits per customer

• Vendors• Analyze vendors and costs

5/16/2016

8

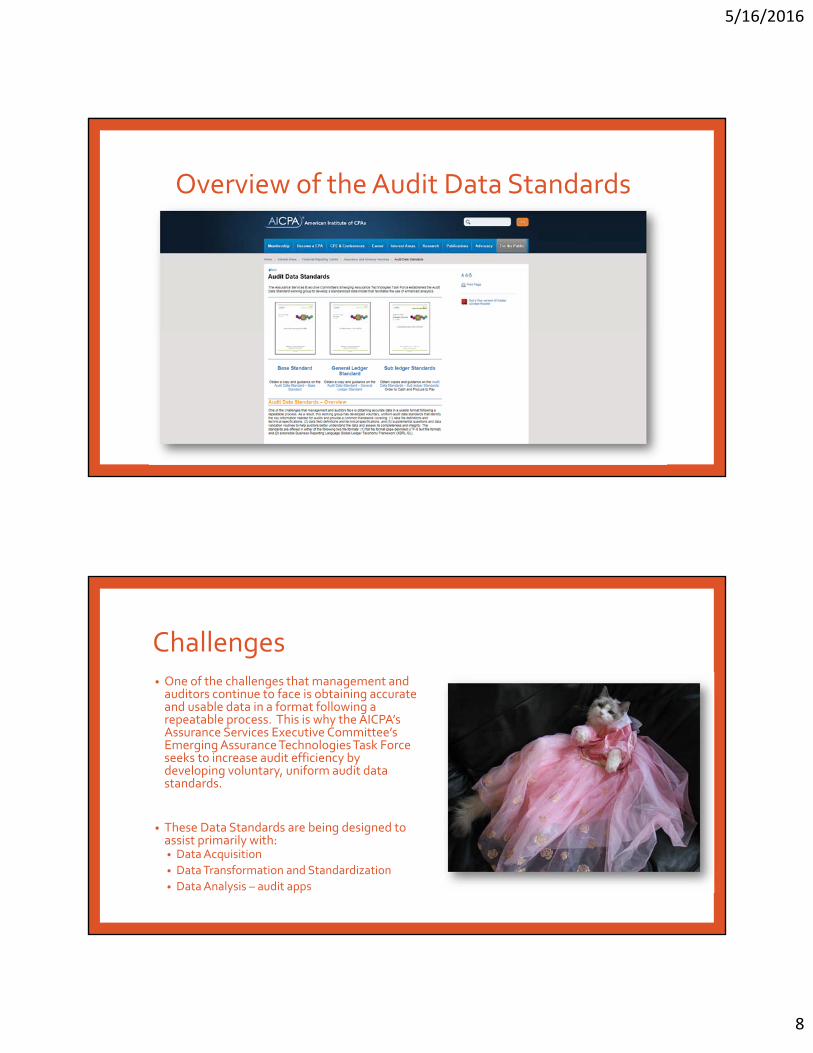

Overview of the Audit Data Standards

Challenges• One of the challenges that management and auditors continue to face is obtaining accurate and usable data in a format following a repeatable process. This is why the AICPA’s Assurance Services Executive Committee’s Emerging Assurance Technologies Task Force seeks to increase audit efficiency by developing voluntary, uniform audit data standards.

• These Data Standards are being designed to assist primarily with:• Data Acquisition

• Data Transformation and Standardization

• Data Analysis – audit apps

5/16/2016

9

Benefits of Audit Data Standards

• Standard set of company data available on demand

• Drill down and identify higher risk areas

• Standardize analyses across business units with different reporting systems in place

• Better evaluate key metrics in order to substantively predict company performance

• Analyze growth opportunities

• Search for questionable transactions

Discussion of Tests & Testing Ideas

General Ledger1. Suspicious weekend or holiday journal entries

2. Duplicate journal entries: same account, same amount

3. GL period close cut‐off

4. Segregation of duties: Parked vs. Posted

5. New GL accounts

6. No change balance sheet accounts

7. Segregation of duties: Poster vs. Creator of JE

8. Even dollar JE amounts

9. Split entry JE over approval limit

10. Authorized user changes

11. Outstanding JE to suspense accounts

12. GL period close: Period re‐opened

5/16/2016

10

Discussion of Tests & Testing IdeasSales/Revenue/Receivables

1. Duplicate invoices

2. Excessive write‐offs

3. Unauthorized adjustments

4. Manual discounts

5. A/R aging

6. Critical period sales volume

7. Duplicate / ghost customers

8. Excessive refunds

9. Incorrect sales price

10. Credit memos vs A/R

11. Excessive unauthorized discounts

12. Segregation of duties: updating v. approving credit limits

13. Unauthorized price changes

Discussion of Tests & Testing IdeasPurchase Cards

1. Top 15 spenders

2. Phantom merchants

3. High transaction volume

4. Duplicate cards

5. Keyword testing

6. Split purchases

7. Inactive employees

8. Round amounts

9. T & E and Pcard match

10. Dormant cards

11. Suspicious MCC / SIC codes

12. Excessive recognition & appreciation expenses

13. Expenses processed without receipts

14. Large transactions

15. Suspicious weekend or holiday purchases

5/16/2016

11

Discussion of Tests & Testing Ideas

Travel & Entertainment1. Airlines: ticket analysis

2. Travel claims & vacation analysis

3. Excessive meal expenses by location

4. Excessive personal payments

Discussion of Tests & Testing IdeasPayroll

1. Unusual employee master file changes

2. Excessive overtime

3. Phantom (ghost) employee

4. Duplicate employees

5. Payments after termination

6. Minimal vacation time used

7. Excessive days off

8. Multiple salary increases

9. Frequent employee master file changes

10. Active employees with no YTD earnings

11. Gross earnings over threshold

12. Unusual bonus increase

13. Unauthorized paid overtime

14. Serial vacationers

15. Missing or invalid employee data

16. Excessive hours

Evolution of Auditing: From the Traditional Approach to the Future Audit – November 2012 https://www.aicpa.org/interestareas/frc/assuranceadvisoryservices/downloadabledocuments/whitepaper_evolution-of-auditing.pdf Reimagining Auditing in a Wired World https://www.aicpa.org/InterestAreas/FRC/AssuranceAdvisoryServices/DownloadableDocuments/Whitepaper_Blue_Sky_Scenario-Pinkbook.pdf AICPA AU-C-240 https://www.aicpa.org/Research/Standards/AuditAttest/DownloadableDocuments/AU-C-00240.pdf Data Management: IDEA - https://www.audimation.com/Product-Detail/CaseWare-IDEA ACL - http://www.acl.com/ Active Data for Excel - http://www.informationactive.com/ AICPA Audit Data Standards Resource Page https://www.aicpa.org/interestareas/frc/assuranceadvisoryservices/pages/auditdatastandards.aspx