Objectives 1. Explain what is meant by term ‘Capital Investment’ and how a business decides...

30

Objectives 1. Explain what is meant by term ‘Capital Investment’ and how a business decides which project to invest in 2. State the two main methods that you need to be able to calculate and use for appraising Capital Investment 3. Calculate Payback Periods and list the advantages and disadvantages of this method 4. Explain what is meant by the ‘time value of money’. Evaluate Capital Investments using the DCF method, making appropriate recommendations and list the advantages and disadvantages of using DCF 5. Discuss what is meant by a Perpetuity and an Annuity 6. Make recommendations on a proposed Capital Investment using IRR

-

Upload

melanie-ariel-allen -

Category

Documents

-

view

214 -

download

1

Transcript of Objectives 1. Explain what is meant by term ‘Capital Investment’ and how a business decides...

Objectives1. Explain what is meant by term ‘Capital Investment’ and how a business decides which project to invest in 2. State the two main methods that you need to be able to calculate and use for appraising Capital Investment 3. Calculate Payback Periods and list the advantages and disadvantages of this method 4. Explain what is meant by the ‘time value of money’. Evaluate Capital Investments using the DCF method, making appropriate recommendations and list the advantages and disadvantages of using DCF 5. Discuss what is meant by a Perpetuity and an Annuity 6. Make recommendations on a proposed Capital Investment using IRR 7. Estimate IRR 8. Access Blackboard (off site) and complete a quiz to test your knowledge and understanding of this topic area

AAT Level 3Capital Investment Appraisal (CIA)

What is Capital Investment?

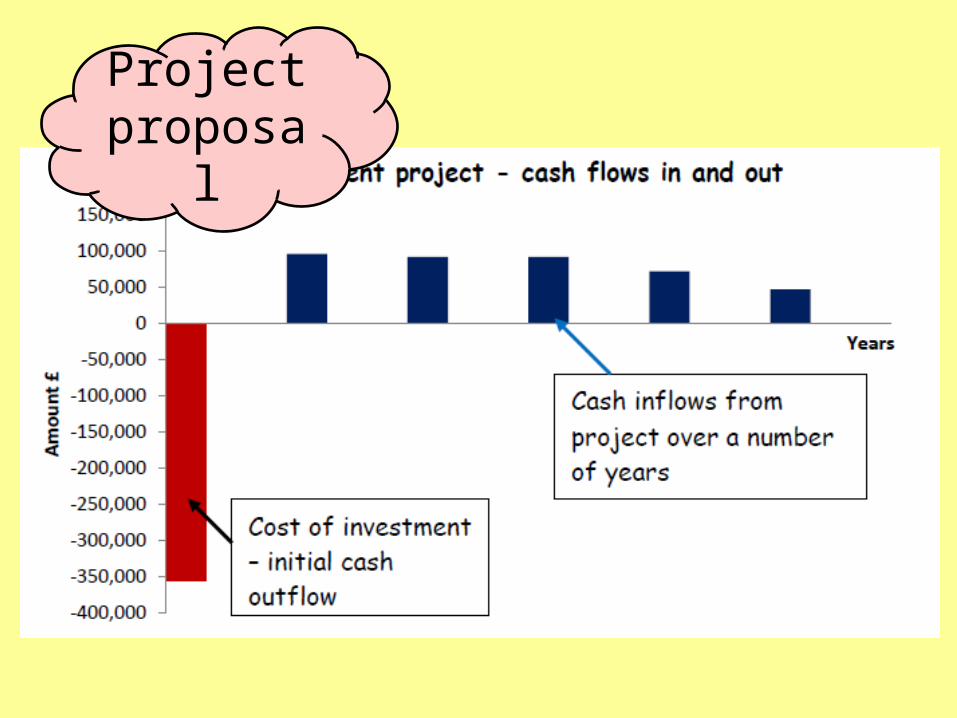

Project proposal

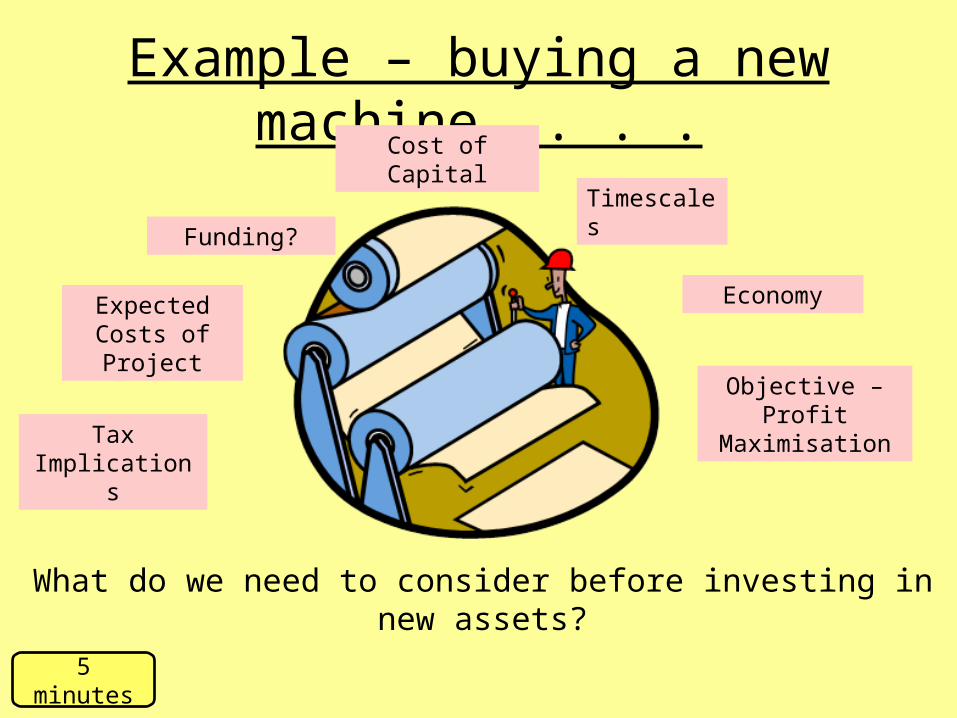

Example – buying a new machine. . . .

What do we need to consider before investing in new assets?

Funding?

Cost of Capital

Expected Costs of Project

Timescales

Tax Implications

Economy

Objective – Profit

Maximisation

5 minutes

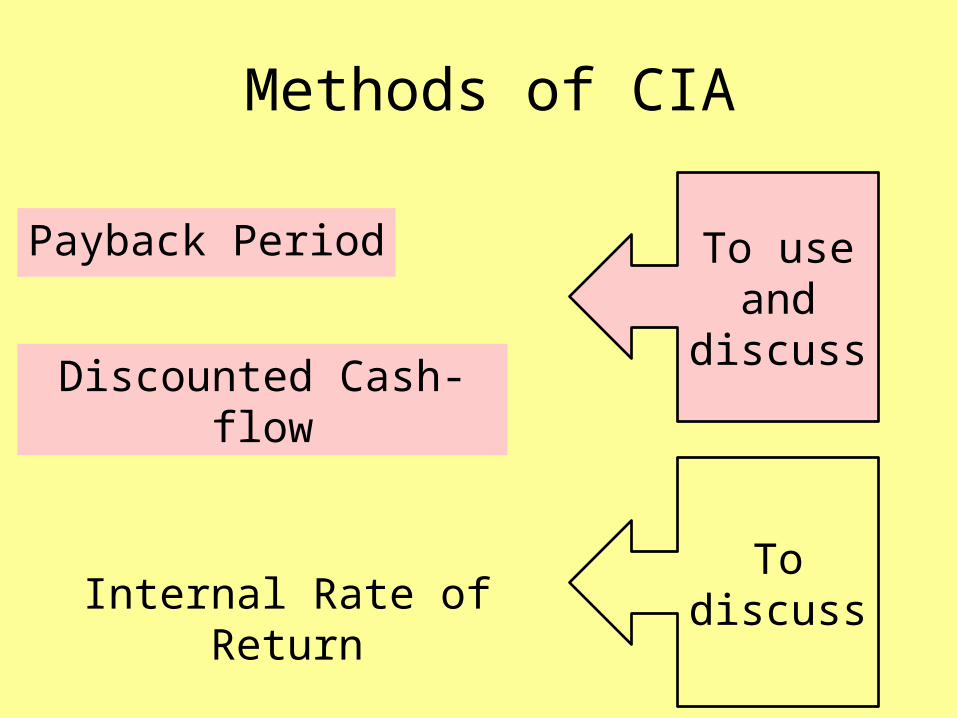

Methods of CIA

Payback Period

Discounted Cash-flow

Internal Rate of ReturnTo

discuss

To use and

discuss

Payback Period (Activity 1)Machine C costs £100,000

Scrap Value?

Year 1

Spend (£100,000)Expected Income £40,000

(£60,000)

(£60,000)

(£30,000)0

£30,000£55,000

Payback Period (Activity 1)

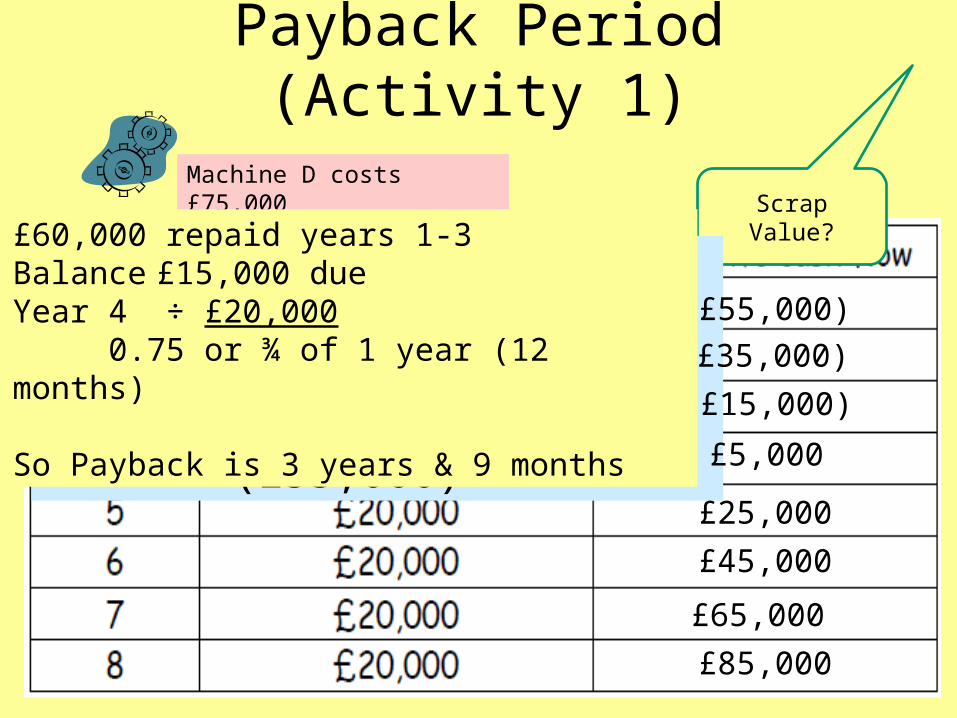

Machine D costs £75,000

Scrap Value?

Year 1

Spend (£75,000)Expected Income £20,000

(£55,000)

(£55,000)

(£35,000)

(£15,000)

£5,000

£25,000

£45,000

£65,000

£85,000

£60,000 repaid years 1-3Balance £15,000 dueYear 4 ÷ £20,000

0.75 or ¾ of 1 year (12 months)

So Payback is 3 years & 9 months

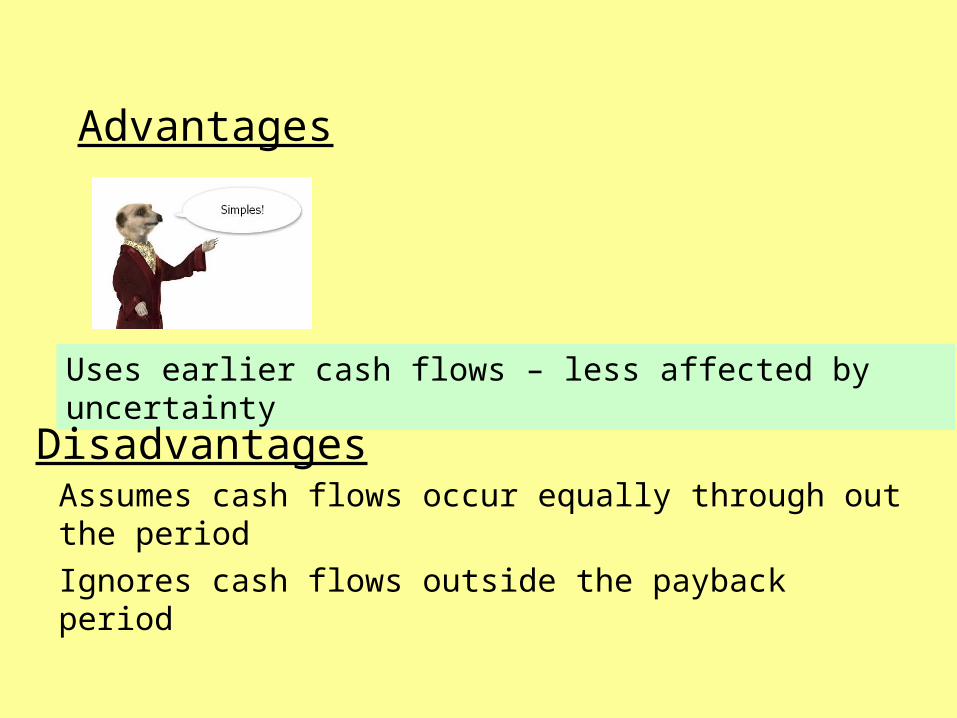

Assumes cash flows occur equally through out the period

Advantages

Uses earlier cash flows – less affected by uncertainty

Disadvantages

Ignores cash flows outside the payback period

Try these . . .

Activity 2 & 3

Activity 2 - Answer

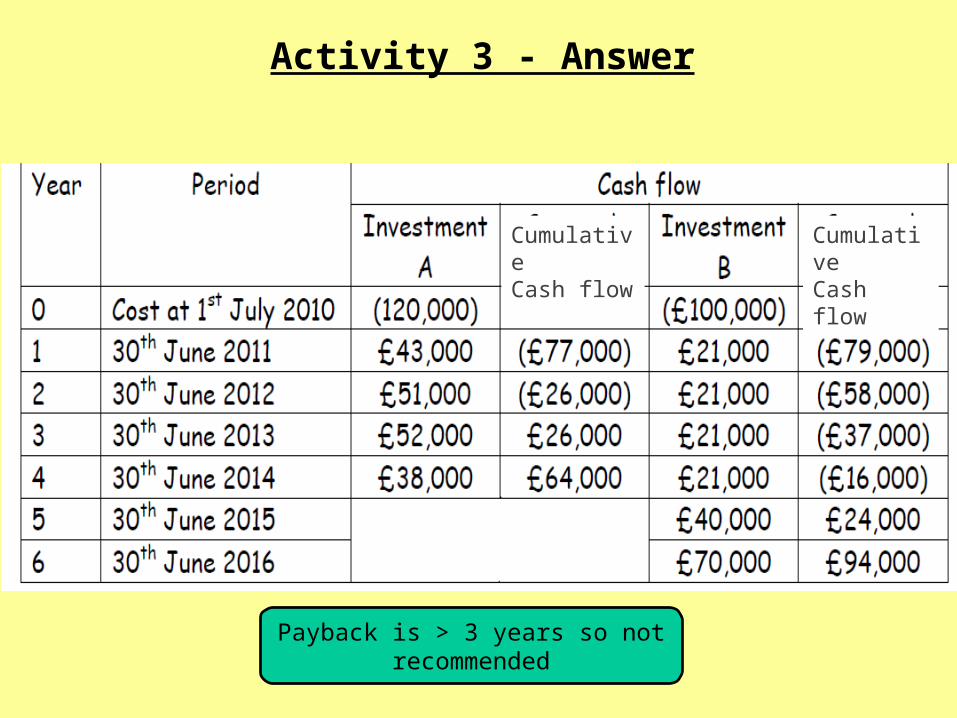

Activity 3 - Answer

CumulativeCash flow

CumulativeCash flow

Payback is > 3 years so not recommended

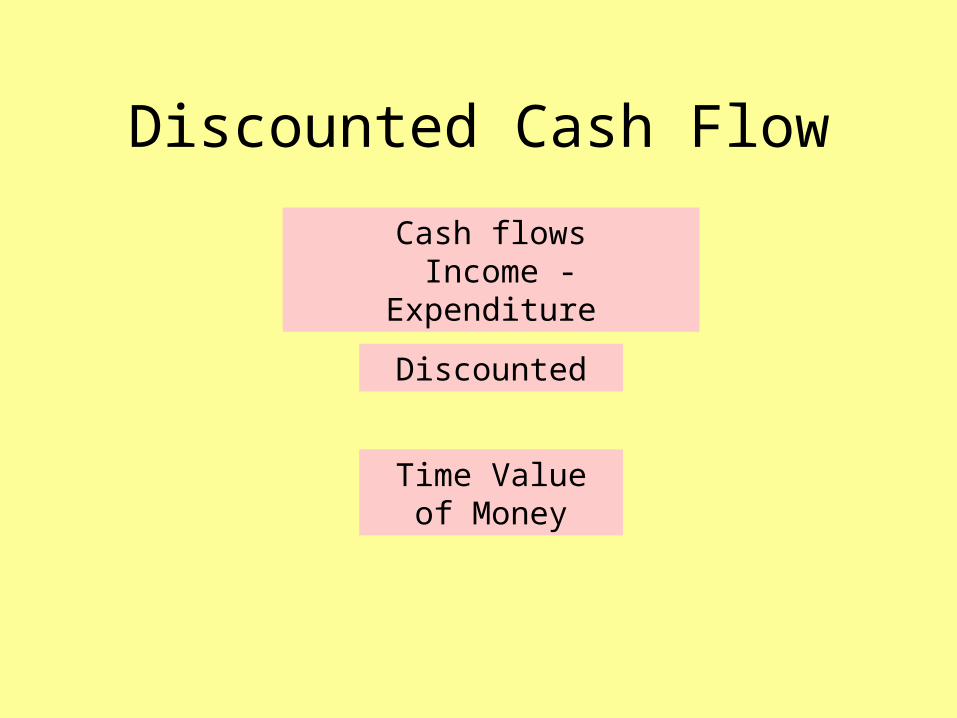

Discounted Cash Flow

Time Value of Money

Cash flows Income - Expenditure

Discounted

£10

Investment Preference – If you have money now you can invest it which means your money will be worth more in future than it is now.

Consumption Preference – You are likely to be able to but more with £10 today than with £10 in a years timeRisk Preference – Receiving your money back sooner rather than later reduces the risk of default on the loan

Time Value of Money

Our preference to have the money NOW rather than wait and receive it at a later date

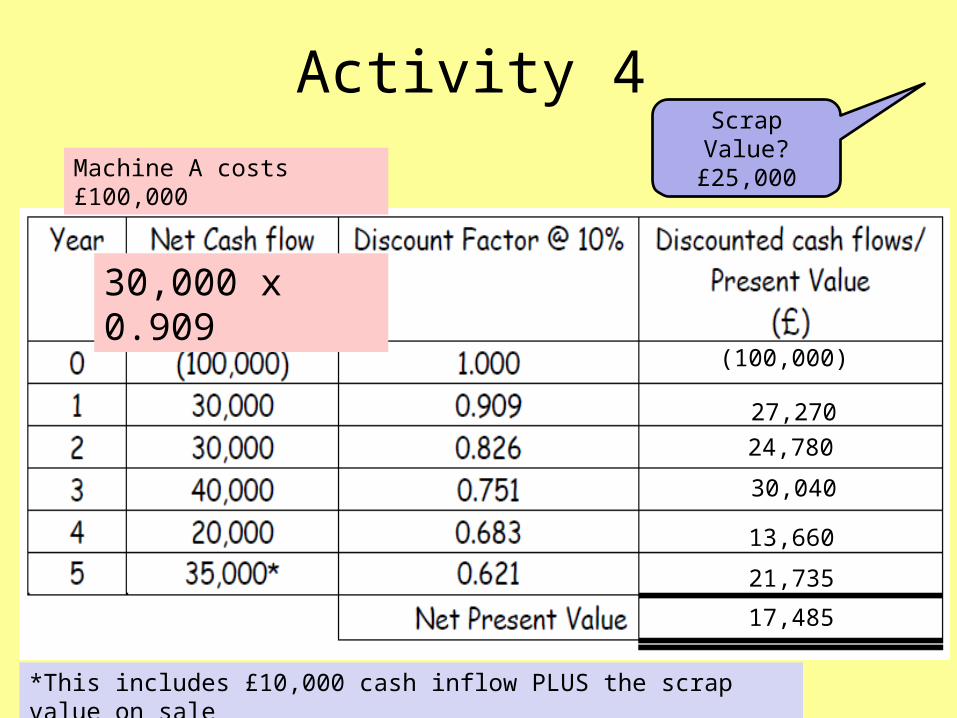

Activity 4Machine A costs £100,000

Scrap Value?£25,000

(100,000)

27,270

30,000 x 0.909

24,780

30,040

13,660

21,735

17,485

*This includes £10,000 cash inflow PLUS the scrap value on sale

(£60,000)

Use table (P4)

1.00

0.909

0.826

0.751

0.683

0.621

(60,000)

22,725

20,650

11,265

10,245

6,210

11,095

Notes on NPV

Only considers ACTUAL cash-flows

Depreciation

Resale value at end of period

Net Cash flow = Inflows - Outflows

Advantages

Based on cash flows over entire lifetime

Disadvantages

Makes various assumptions which may not be accurate- Cost of capital- Prediction of cash flowsMore complicated to calculate

Activity 5

Try these . . . .

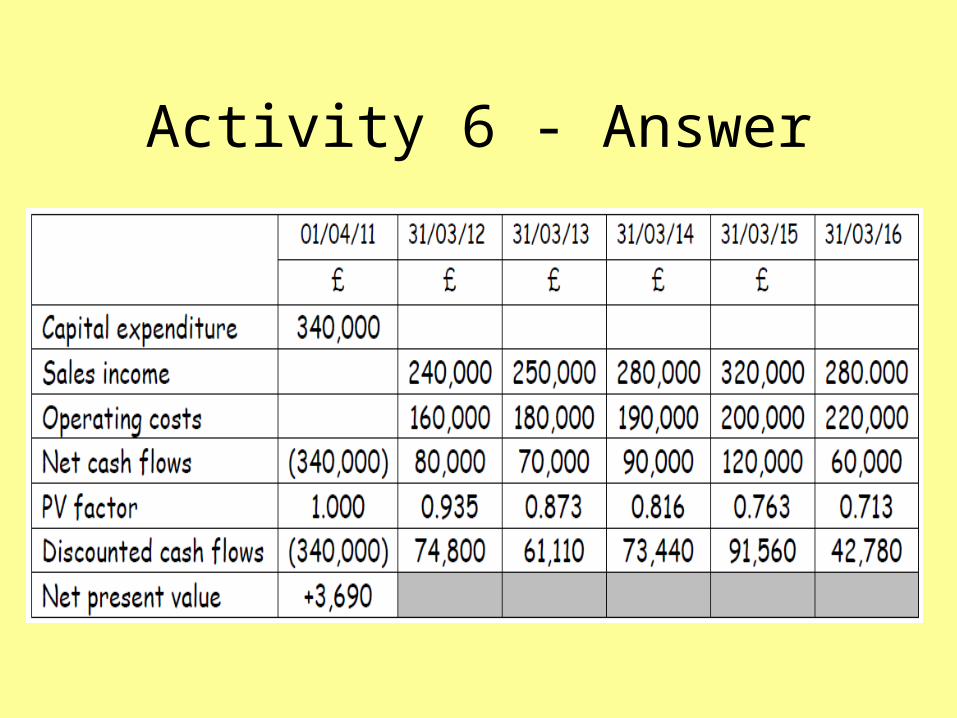

Activity 6 - 9

Activity 6 - Answer

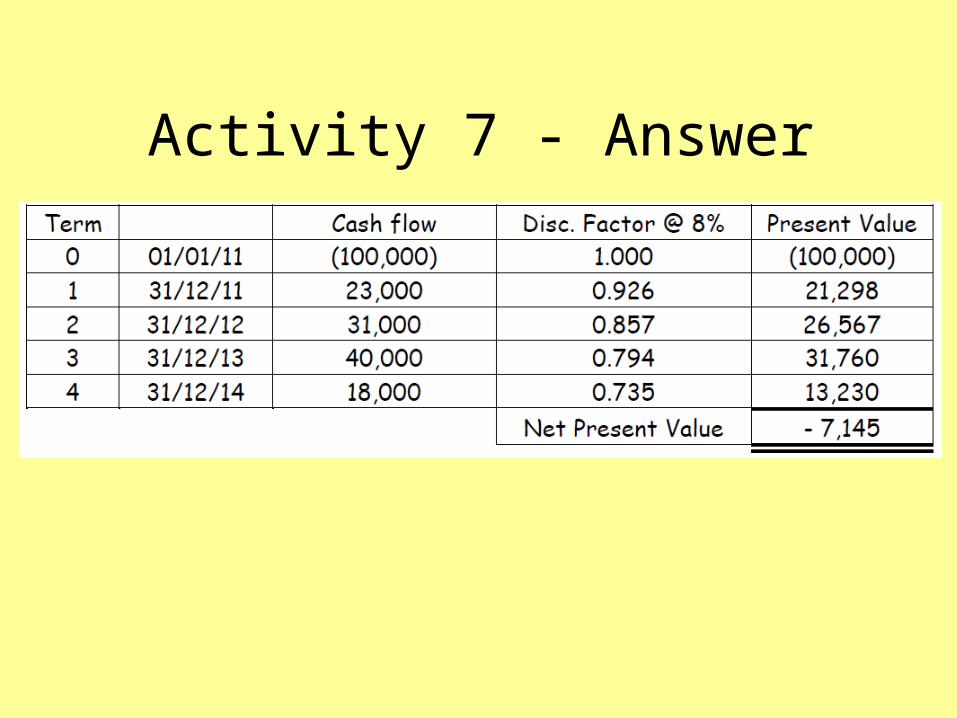

Activity 7 - Answer

Activity 8 & 9Check with Kate

Activity 10 Net Present Costs (NPC)

(100,000)

(37,040)

(35,994)

(36,206)

(36,015)(245,255)

(340,000) (148,160)

(154,260)

(150,860)

(147,000)(940,280)

Activity 10 Net Present Costs (NPC)

Try Activity 11

Internal Rate of Return

Definition

The discount rate which, when applied to project cash flows gives a zero net present value

How it works . . . .

IRR is the % rate which gives a ZERO NPV

Question 13

You have been asked to evaluate a proposed project with capital expenditure totalling £100000 using a PV factor (rate of interest) of 8%. You have calculated that the NPV for that project is +8520.

What is likely to be the IRR?

a) 6% b) 8% c) 10% d) 14%

Top tip!Give a higher IRR where you have a positive NPV, and a

lower one where you have a negative

Try Activity 13 b & c