NPA Mgmtt.by Suchet Bangera

39

"NPA Management" In Partial Fulfillment of the Requirement For Master of Management Studies For The Academic Year 2002-2003 From The University Of Mumbai. Submitted by: Suchet D Bangera MMS FINANCE N.L.Dalmia Institute Of Management Studies And Research.

-

Upload

gavendralhukkhuram -

Category

Documents

-

view

221 -

download

0

Transcript of NPA Mgmtt.by Suchet Bangera

8/2/2019 NPA Mgmtt.by Suchet Bangera

http://slidepdf.com/reader/full/npa-mgmttby-suchet-bangera 1/39

"NPA Management"

In Partial Fulfillment of the Requirement For Master of

Management Studies For The

Academic Year

2002-2003

From The University Of Mumbai.

Submitted by:

Suchet D Bangera

MMS FINANCE

N.L.Dalmia Institute Of Management Studies And Research.

8/2/2019 NPA Mgmtt.by Suchet Bangera

http://slidepdf.com/reader/full/npa-mgmttby-suchet-bangera 2/39

CERTIFICATE

N.L.Dalmia Institute of Management Studies and Research

This is to certify that the project entitled

“NPA Management”

is successfully completed by Mr.Suchet Bangera

during the second year of his course in

Partial fulfillment of the Master of Management Studies

under the University of Mumbai through

N.L.Dalmia Institute of Management Studies and Research, Mumbai.

This project represents the work done by

Mr.Suchet Bangera under my guidance.

Guided By-

Mr. Sunil Mahajan

(Faculty Finance)

8/2/2019 NPA Mgmtt.by Suchet Bangera

http://slidepdf.com/reader/full/npa-mgmttby-suchet-bangera 3/39

ACKNOWLEDGEMENT

I express my heart- felt indebtness and gratitude to Prof P.L.Arya , Director,

N.L.Dalmia Institute of Management Studies and Research for his

encouragement and support.

I sincerely wish to acknowledge Prof Sunil Mahajan for his keen interest

and valuable guidance on this program.

I would also like to express my deep sense of gratitude to Mr.Mehernosh

Nogamawalla, Assistant Manager, ICICI Bank for his noteworthy

suggestions, constant inspiration and unstinted guidance in carrying out this

venture.

Place: Signature

Date:

(Suchet Bangera)

8/2/2019 NPA Mgmtt.by Suchet Bangera

http://slidepdf.com/reader/full/npa-mgmttby-suchet-bangera 4/39

NPA MANAGEMENT

ABSTRACT

The aim of the project is to study NPA from 2 perspective, Firstly ,an indepth analysis of

the NPAs in the three major financial institution in India and Secondly on the basis of acomparative study of NPAs in India in the Global context.

Financial sector reforms in India has progressed rapidly on aspects like Interest rate

deregulation, prudential norms, reduction in reserve requirement and barriers to entry. But

progress on the structural- institutional aspects has been much slower and is a cause of

concern. The sheltering of weak institution while liberalizing operational rules of the game

is making implementation of operational changes difficult and ineffective. To be truly

effective, there requires to be changes to be done to tackle the NPA problem spanning the

entire gamut of judiciary, political and the bureaucracy.

This project deals with the experience of the 3 major financial institution in India and the

experience of other Asian countries in handling of NPAs.It further looks into the effect of

the reforms on the level of NPAs and suggests mechanisms to handle the problem by

drawing on experiences from other countries.

4 NLDIMSR

8/2/2019 NPA Mgmtt.by Suchet Bangera

http://slidepdf.com/reader/full/npa-mgmttby-suchet-bangera 5/39

NPA MANAGEMENT

CONTENTS

CHAPTER SUBJECT PAGE NO.

Chapter-1 Introduction 1

Chapter -2 Research Methodology (2-3)

2-1 Objectives 2

2-2 Scope 2

2-3 Limitation 3

2-4 Research Design 3

2-5 Sources of Data 3

SECTION –A

NPA Management

Chapter -3 Introduction to NPAs (5-10)

3-1 Non-Performance of Assets 5

3-2 Definition of NPAs 5

3-3 Asset Classification 6

3-4 Partial recoveries of NPA 6

3-5 Provisioning & Write- offs 7

3-6 Charging of Interest on NPAs 8

Chapter-4 Over view of the Three Indian Fls (10-11)

4-1 About the Institution -ICICI 10

4-2 IDBI 11

4-3 IFCI 11

Chapter-5 Analysis on NPA management level of FIs (12-

14)

5 NLDIMSR

8/2/2019 NPA Mgmtt.by Suchet Bangera

http://slidepdf.com/reader/full/npa-mgmttby-suchet-bangera 6/39

NPA MANAGEMENT

5-1 Comparative Analysis of FIs 13

5-2 Comments 13

Chapter-6 Coping Strategies of Fls (15-19)

6-1 ICICI Ltd. 15

6-2 IFCI Ltd. 17

6-3 IDBI Ltd. 18

SECTION -B

A comparative study of Non Performing Assets in India in the Global context

- Similarities and dissimilarities, remedial measures.

Chapter-7 Overview of performance

(21-24)

7-1 Based on Gross and Net NPAs

22

7-2 Based on Loan loss provisioning

22

7-3 Sector wise split up

23

Chapter-10 Solutions

(34-37)

Conclusion

37

Annexure RBI Guidelines

38-40

Bibliography

6 NLDIMSR

8/2/2019 NPA Mgmtt.by Suchet Bangera

http://slidepdf.com/reader/full/npa-mgmttby-suchet-bangera 7/39

NPA MANAGEMENT

CHAPTER-1

INTRODUCTION

The Indian Financial institution and Banks are facing a very grim situation today, due to

rising level of non-perfoming assets (NPAs) . This factors adversely hits the bottom line,

thus yielding low profits for the organization It calls for Planning and executing clear, exit

strategies on the part of these Fls and NPAs being a cause for serious concern,I have

decided to draw attention on this aspect in the present project.

To deal with this topic, I have adopted a two-pronged strategy.

Firstly I made an in depth analysis of the existing level of NPAs of country's three leading

financial 'institutions, namely -ICICI, IDBI and IFCI. Then, analysis of the strategies

adapted by them to cope with this problem has been carried out.

Secondly, to obtain further insight in this matter, I have also focussed on the levels of

NPAs in other Asian countries and try to bring out measures responsible for their reduction

in NPAs .

7 NLDIMSR

8/2/2019 NPA Mgmtt.by Suchet Bangera

http://slidepdf.com/reader/full/npa-mgmttby-suchet-bangera 8/39

NPA MANAGEMENT

I hope this project will enable in throwing light on key areas of finance and also assist in

addressing the current situation of NPAs to some extent.

CHAPTER-II

RESEARCH METHODOLOGY

2.1 OBJECTIVES

• The purpose of doing this project is mainly to make a thorough study on

NPA

• To study the level of NPA in the leading- Indian Fls, and how they are

coping with this problem.

• To make a comparative study on the three Fls and gauging their efficiency

on this ground.

• The objective also includes exploring the situation of other Asian Countries

in dealing with NPAs.

• To suggest few financial restructuring measures,by giving solutions.

8 NLDIMSR

8/2/2019 NPA Mgmtt.by Suchet Bangera

http://slidepdf.com/reader/full/npa-mgmttby-suchet-bangera 9/39

NPA MANAGEMENT

2.2 SCOPE

The predicted scope for the first half of the study, is as follows:

• To study all the financial statements.

• To make a comparative analysis on the level of NPAs .

• Bringing out the results of financial statements through ratio analysis.

• Charting out the strategies adopted by these Fls to cope with this problem

in future.

The scope for the second half of the study, can be outlined as follows:

• To study overview of performance in the global arena

• To make a comparative analysis on the level of NPAs in the Asian

countries .

• The similarities and Dissimilarities.

• Charting out the strategies adopted to cope with this problem in future.

2.3 LIMITATIONS

Every project and its results possess their own limitations. So also does this project. These

limitations are in terms of:

• Time constraint- Due to lack of sufficient time, the study could not be made very

comprehensive.

• The inferences drawn are true only keeping in mind the assumptions taken.

2.4 RESEARCH DESIGN

9 NLDIMSR

8/2/2019 NPA Mgmtt.by Suchet Bangera

http://slidepdf.com/reader/full/npa-mgmttby-suchet-bangera 10/39

NPA MANAGEMENT

The first half of the study dealt with NPAs and their management by the three leading

financial institutions. The research design used was descriptive in nature. The second half

comprised of an in depth analysis of NPAs in other Asian countries. The research design

used was analytical and exploratory in nature.

2.5 SOURCES OF DATA

Secondary sources:

Information from Published Material, for example, Annual reports of the

companies, organizations, RBI guidelines circulars, Case papers on NPAs and also, from

Internet websites.

SECTION -A NPA MANAGEMENT

IN INDIAN FIs.

10 NLDIMSR

8/2/2019 NPA Mgmtt.by Suchet Bangera

http://slidepdf.com/reader/full/npa-mgmttby-suchet-bangera 11/39

NPA MANAGEMENT

CHAPTER-III

INTRODUCTION OF NPAs

3.1 NON- PERFORMING ASSETS

In the year 1994, the Committee on the Financial System under the Chairmanship

of Shri. M. Narasimham had considered the existing system prevailing in banks and

financial institutions (FIs) for income recognition, classification of assets and provisioning

for bad debts and recommended that the policy of income recognition should be objective

and based on record of recovery, rather than on any subjective considerations. Keeping

this in view, the Committee issued several guidelines to these institutions, which were

modified from time to time. But, before we examine the RBI guidelines on income.

Recognition, asset classification, provisioning and other related matters, we should

understand the basic terms referred in these guidelines.

11 NLDIMSR

8/2/2019 NPA Mgmtt.by Suchet Bangera

http://slidepdf.com/reader/full/npa-mgmttby-suchet-bangera 12/39

NPA MANAGEMENT

3.2 DEFINITION OF NON-PERFORMING ASSETS (NPAs)

The Committee has defined a NPA as an advance where, as on the date of the

balance Sheet of the FI,

(a) In respect of term loans, interest remains ‘past due' for a period of more than 180

days,

(b) In respect of bills purchased/discounted, the bills remain overdue and unpaid for a

period of more than, 180 days and

(c) In respect of other advances, any amount to be received remains 'past due' for a

period of more than 180 days. In other words, an asset becomes non-performing

when it ceases to generate income for a Fl.

In this context, an amount is considered 'past due' when it remains outstanding for

30 days beyond the due date. Thus, while interest may become 'due' on, say 31 March

1993, it becomes 'Past due' on 30 April 1993. Furthermore, NPA was to be defined as a

credit/loan facility in respect of which interest has remained 'past -due') for a period of four

quarters during the year ending 31 March 1994, three quarters during the year ending 31

March 1995 and two quarters during the year ending 31 March 1996 and onwards.

3.3 ASSET CLASSIFICATION

As from the end of the accounting year, 1993-94, all Fls had to classify their

loans/advances into four broad groups, viz.

(i) Standard assets,

(ii) Sub-standard assets,

(iii)Doubtful assets and

(iv)Loss assets.

12 NLDIMSR

8/2/2019 NPA Mgmtt.by Suchet Bangera

http://slidepdf.com/reader/full/npa-mgmttby-suchet-bangera 13/39

NPA MANAGEMENT

Broadly speaking, classification of assets into the above categories should be done

taking into account the degree of well-defined credit weaknesses and extent of dependence

on collateral security for realization of dues.

(i) Standard asset:

These are Assets that do not disclose any problems or which do not carry any risk other

than normal business risk.

(ii) Sub-standard assets:

Assets (i) that are non performing for a period not exceeding two years or (ii) that have

been renegotiated or rescheduled after the project to which they relate has commenced

production are classified as sub-standard assets.

Eg) A term loan should be treated as substandard, if the installments of principal are

Overdue for two quarters but not exceeding two years.

(iii) Doubtful assets:

Assets (1) that are non-performing for more than two years or where there are

potential threats to recoveries on account of erosion in the value of security and other

factors such as fraud are classified as doubtful assets.

(iv) Loss assets:

Assets (i) the losses on which are crystallized or (ii) that are considered

uncollectible are classified as loss assets. Payments on renegotiated or rescheduled

loans should have no past due amounts for one year after renegotiations or

rescheduling, as the case may be, in order for the loan to be upgraded. Further, if

interest or installments of principal is in arrears for any two quarters out of four

quarters during the year, the credit facility should be treated as NPAs, although the

default may not be continuously for two quarters during the year.

13 NLDIMSR

8/2/2019 NPA Mgmtt.by Suchet Bangera

http://slidepdf.com/reader/full/npa-mgmttby-suchet-bangera 14/39

NPA MANAGEMENT

3.4 PARTLAL RECOVERIES OF NPAS

Interest partly recovered on NPAs may be credited to income account but it

should be ensured that the credits in the accounts towards interest are not out of fresh/

additional credit facility sanctioned to the borrowers concerned.

3.5 PROVISIONING AND WRITE-OFFS

Standard assets: A 0.25% general provision.

Sub-standard assets: A 10% provision.

Doubtful assets: A 1OO% write-off is made for the unsecured portion of the doubtful asset

and charged against income. The value assigned to the collateral securing a loan is that

reflected on the borrowers books or that determined by third party appraisers to be

Realizable. In those cases where there is a secured portion of the asset, provision of 20% to

50% is made depending upon the period for which the asset remains doubtful.

Provisions on such secured assets are made as follows upto 1 year-20%, 1 to 3 years-30%

and more than 3 years 50%.

Loss assets: The entire asset is written off/provided for.

3.6 CHARGING OF INTEREST ON NPAs.

(a) As per the RBI guidelines, none of the Fls were to charge and take to income

account, interest on any NPA. So far as bills purchased/ discounted/ rediscounted

are concerned, overdue interest should not be charged and taken to income account

unless it is realized. In respect of all NPAs, interest accrued and other charges like

fees and commission credited to income account during the previous accounting

years but which have not been actually realized should be reversed or provided for

14 NLDIMSR

8/2/2019 NPA Mgmtt.by Suchet Bangera

http://slidepdf.com/reader/full/npa-mgmttby-suchet-bangera 15/39

NPA MANAGEMENT

in the current accounting period. From the year 1999-2000, the unrealised income

booked in loan ledger on NPAs, if any need to be reversed in the year the asset

becomes NPA.

(b) In case of new projects, where moratorium period is available for payment of

interest becomes 'due' only after the moratorium period is over.

(c) In case of housing loans or other advances granted to staff members, where interest

is payable after recovery of principal, interest need not be considered as 'past

due' from the first quarter onwards. They should be classified, as NPA only

when there is default in payment of 'interest on the due of payment.

(d) In case of borrowers who have been granted more than one loan or credit facility,

all the dues from them will have to be treated as NPA when an individual loan or

facility or part thereof has become irregular.

(e) The availability of security or net worth of borrower/guarantor should not be taken

into account for the purpose of treating an advance as NPA or otherwise, as income

recognition is based on record of recovery.

(f) In case of loans /credit facilities extended to a unit by more than one Fl under

formal consortium arrangement, those loans/ facilities which have been classified as 'sub-

standard', 'doubtful' or ‘loss' by the concerned leader, should be so classified by the other

members of the consortium and requisite provision, in accordance with the prescribed

norms, will have to be made thereof.

15 NLDIMSR

8/2/2019 NPA Mgmtt.by Suchet Bangera

http://slidepdf.com/reader/full/npa-mgmttby-suchet-bangera 16/39

NPA MANAGEMENT

CHAPTER-IV

OVERVIEW OF THREE LEADING INDIAN

FINANCIAL INSTITUTIONS (FIs)

1 ICICI Ltd.

2 IFCI Ltd.

3 IDBI

4.1 ABOUT THE INSTITUTIONS:

1 INDUSTRIAL CREDIT AND INVESTMENT CORPORATION OF INDIA

LTD. ( ICICI LTD.)

ICICI Ltd. was founded by the World Bank, the Government of India and

representatives of private industry on January 5, 1955 to encourage and assist industrial

development and investment in India. Over the years, ICICI has evolved into a

diversified financial institution. ICICI's principal business activities include medium-term and long-term project financing for the infrastructure and manufacturing sectors,

corporate finance to meet the treasury requirements of Indian companies, lease finance as

well as a comprehensive range of financial and advisory services. For regulatory and

strategic reasons, ICICI set up specialised subsidiaries in the areas of commercial

banking, investment banking, non-banking finance, investor servicing, broking, venture

16 NLDIMSR

8/2/2019 NPA Mgmtt.by Suchet Bangera

http://slidepdf.com/reader/full/npa-mgmttby-suchet-bangera 17/39

NPA MANAGEMENT

capital financing and state-level infrastructure financing. Also, on 22nd September 1999,

it became the first Indian Company to get listed in NYSE, marking the successful

completion of a US $ 500 million capital-raising programme. ICICI has therefore created

a virtual Universal Banking Group that offers a comprehensive range of financial

products and services.

2 INDUSTRIAL FINANCE CORPORATION OF INDIA (IFCI)

IFCI, the first Development Finance Institution in India, Was set 1948, as a Statutory

Corporation, to pioneer institutional credit to Medium and large industries. IFCI was also

the first institution in financial sector to be converted from a Statutory Corporation into a

public limited company. It also has two wholly owned subsidiaries; namely, IFCI

Financial services Ltd. and IFCI Venture Capital Funds

3 INDUSTRIAL DEVELOPMENT BANKOF INDIA (IDBI)

IDBI is also considered as one of the premier financial institutions of India. It offers a

range of financial services, like in the form of Direct Finance (project finance and non-

project finance). It also pays due emphasis to Infrastructure finance; Venture Capital

and Fee based services. They comprise activities such as issue management, corporate

advisory services, credit syndication and debenture/mortgage trusteeship. IDBI opens

Letters of Credit and effects foreign currency remittances on behalf of its assisted units

for import of capital goods/ services. IDBI has a few wholly owned subsidiaries too

engaged in specific sectors. These were mainly established to cater to the needs of the

developing economy as well as to equip it to face the challenges thrown by the global

economy. Prime amongst its subsidiaries are Small Industries Development Bank of

India (SIDBI); IDBI Bank Ltd.; IDBI Capital Market Services Ltd. (ICMS) and IDBI

Investment Management Company Ltd. (IIMCO).

17 NLDIMSR

8/2/2019 NPA Mgmtt.by Suchet Bangera

http://slidepdf.com/reader/full/npa-mgmttby-suchet-bangera 18/39

NPA MANAGEMENT

CHAPTER-V

ANALYSIS ON NPA MANAGEMENT

LEVEL OF THE THREE Fls.

Over the past few years, the rapid reduction in trade barriers and integration with

global markets, along with the downtrend in global commodity markets, has caused

difficulty in the Indian economy to those commercial enterprises with cost inefficiencies,

high debt burden, poor technology and fragmented capacities. As a result, while the Indian

economy has continued to grow, although at a slower rate than in past periods, certain

corporate and commercial enterprises have had to adopt certain measures to restructure

their operations to deal with the financial stress they have encountered. Against this

backdrop, we are going to analyse the strategies adopted by the earlier mentioned Fls tocope up with this serious problem. Before this, let us take a look on the current level of

NPAs of these institutions.

18 NLDIMSR

8/2/2019 NPA Mgmtt.by Suchet Bangera

http://slidepdf.com/reader/full/npa-mgmttby-suchet-bangera 19/39

NPA MANAGEMENT

5. 1 COMPARATIVE ANALYSIS OF THE FINANCLAL INSTITUTIONS'

STRENGTH & FEATURES:

(As on March 3lst 2001)

Particulars ICICI IFCI IDBI

Ratings AAA AA+ AAA

PLRs 12.5% 13% 13 %

RATIOS-

-ROA (%) 2.25 18.8 2.37

- R 0 E (%) 21.1 7.6 17.2

cap.ad.ratio 11.9 11.4 13.4

EPS 21.3 3.1 2.3

Net N P L/N.Worth 69.5 214.1 64.5

Div.payout ratio 25.8 21.6 14.9

% Net NPA to

Total Assets- 7.8 21.5 12

NPA classification

- L o s s 0 0 0

-Doubtful 3.1 8.6 4.3

-Substandard 4.7 12.9 7.7

5.2 COMMENTS

19 NLDIMSR

8/2/2019 NPA Mgmtt.by Suchet Bangera

http://slidepdf.com/reader/full/npa-mgmttby-suchet-bangera 20/39

NPA MANAGEMENT

From the above cited figures, we can see! That currently, of the (Fls) ICICI, is the

Market Outperformed; IDBI is the Market Performer, whereas IFCI is the Market

Underperforrner.

ICICI has been successful to a great extent in curbing its level of NPAs in

comparison to the other Institutions where it is still quite high but after its subsequent

merger with its subsidiary ICICI Bank, its NPA levels have come down drastically.

IDBI appears extensively affected by the economic slow down. It is losing its

premier position to ICICI, though only in incremental loan disbursals, and both profitability

and asset quality are under significant strain. On the other hand, ICICI is demonstrating a

high degree of resilience amidst currently adverse conditions. It is continuing business

growth while designing new initiatives to tackle non-performing loans.

IFCI is believed to have had far worse asset quality than other FIs and banks. As its

fee income is relatively quite less than ICICI and IDBI, it implies that its profit drivers are

weak. Also, it appears that IFCI is less vigorous in exploiting opportunities for fee 'income

unlike the other two Fls.

From the above figure it is evidently observed that ICICI has a favorable Return on

Assets ratio (ROA), capital adequacy ratio; Return on Equity and EPS. Also, while on one

hand it has an attractive dividend payout -ratio, on the other hand, it has low level of NPA,

which compliments or favours the bottomline. This however is not the case with IDBI and

more importantly with IFCI. Here, the case is just the reverse for the latter and this ruins

the bottomline of the Organisation.

20 NLDIMSR

8/2/2019 NPA Mgmtt.by Suchet Bangera

http://slidepdf.com/reader/full/npa-mgmttby-suchet-bangera 21/39

NPA MANAGEMENT

CHAPTER-VI

COPING STRATEGIES OF THE THREE FIs

MEASURES UNDER TAKEN BY THE FIs TO REDUCE NPA LEVEL IN THEIR RESPECTIVE ORGANISATIONS

6.1 ICICI Ltd.

During the year 1998-99, ICICI continually focused on proactive management of

problem loans. It set in place a process involving a detailed and periodic analysis of its

performing assets portfolio, to determine on an on-going basis, the health of every

borrower account in the loan portfolio.One major step taken by ICICI

• ICICI used the interest cover approach to determine stress levels in the

performing assets portfolio. Conceptually, this approach involves

21 NLDIMSR

8/2/2019 NPA Mgmtt.by Suchet Bangera

http://slidepdf.com/reader/full/npa-mgmttby-suchet-bangera 22/39

NPA MANAGEMENT

assessing the underlying cash flows of the borrower and then determining

adequacy of interest cover after allowing for all expenses required to

maintain the corporate as a going concern.

• For projections, typically a worst-case scenario is used for product and

input prices and capacity utilisation levels.

• ICICI has followed a two-pronged approach towards non-performing loans

depending on whether these are viable or unviable companies.

> In respect of viable companies, which have economically sized plants,

strong sponsors and modern technology, ICICI has focused on restructuring

to minimise losses, enhancing security mechanisms, and pledging of

additional collateral or injection of additional sponsor equity.

> In respect of unviable companies, which are essentially uneconomical

projects, ICICI adopts an aggressive approach

Aimed at out-of-court settlements, enforcing collateral and driving

consolidation.

• Its efforts in tackling non-performing loans have been spearheaded by the

Special Asset Management Group, which was created to focus exclusively

on large non-performing loans and problem loans.

• Further, it is also taking measures to enhance the security structures in

accounts under stress. This is being done through the pledge of promoter’s

shareholding, the right to convert debt into equity at par so as to transfer

control to ICICI and escrow mechanisms to capture cash flows.

• The institution is also striving to facilitate the integration of fragmented

capacities, catalyse the merger of weak and unviable units through

22 NLDIMSR

8/2/2019 NPA Mgmtt.by Suchet Bangera

http://slidepdf.com/reader/full/npa-mgmttby-suchet-bangera 23/39

NPA MANAGEMENT

technology upgradation, enable financial restructuring and take early steps

for legal action where deemed necessary.

ICICI firmly believes that all these measures will enable the industry and the

economy to emerge stronger once the restructuring process is complete.

6.2 IFCI Ltd

IFCI is making continual efforts to reduce the level of NPAs by playing a proactive

role on the restructuring of borrower concerns, since it has become necessary to restructure

their viability in the rapidly changing business environment.

• A new division named the Corporate Restructuring Division has been set up

at the Corporate Office of IFCI to strengthen restructuring activities

amongst borrower concerns.

• Sustained efforts in this direction are also being made through the timely

grant of reliefs and concessions, encouragement to mergers and

amalgamations with healthy companies, and one-time settlement of dues.

• In addition, a continuous monitoring of large exposures is also being

undertaken, in order to prevent new cases from slipping into the NPA

category.

• IFCI has also adopted a host of measures, against this backdrop, which

include restructuring the asset portfolio, restricting exposure to chronic

industries and individual companies and invoking the state government

guarantees which have failed to make payments.

23 NLDIMSR

8/2/2019 NPA Mgmtt.by Suchet Bangera

http://slidepdf.com/reader/full/npa-mgmttby-suchet-bangera 24/39

NPA MANAGEMENT

• The institution also sought one-time settlement in respect to government

-guaranteed cases.

All these measures were incorporated by IFCI with the view that it will ensure

recovery of atleast 50 to 60 per cent of the NPAs within a period of 3-4 years.

6.3 IDBI

IDBI has also drawn major plans to restructure its non-performing assets and high

interest costs. They can be elucidated in the following:

• Astringent reworking of the non-performing loans is done, involving

extending of maturity in cases, which are deemed viable.

•Further, the (FI) is also in the process of lowering its interest rates for some

of its borrowers who were finding it difficult to repay due to high rates.

But this was to be done only on the condition that they pay 50 per cent pre

payment premium. This approach was selective and would apply only to

those companies whose accounts were good and whom the Fl would want

to retain as customers.

• IDBI also set up Close Monitoring Cells (CMCS) for constantly monitoring

performance of assisted companies to improve recovery

And initiate timely remedial action.

24 NLDIMSR

8/2/2019 NPA Mgmtt.by Suchet Bangera

http://slidepdf.com/reader/full/npa-mgmttby-suchet-bangera 25/39

NPA MANAGEMENT

• Restructuring Committees (RCs) have also been set up in various zones to

tackle NPAS. The RCs look into the long-term viability of projects and

recommend restructuring schemes to various delegated authorities.

• For expeditious decision-making, Empowered Committee (EMC) and High

Powered Committee (HPC) have been set up. These Committees consider

OTS and restructuring proposals involving waivers.

• In order to improve credit quality, credit appraisal and delivery systems have

been further strengthened. It has also taken steps to monitor cash flows

through proper mechanisms-.

• IDBI has also resorting to additional security by way of pledge of promoters

equity, additional collateral, conversion of loan into equity, etc.

With improvement in the economic scenario and restructuring measures initiated by

the Bank, it is expected that some of the NPAs of this institution would become performing

within a few years.

Apart from incorporating individual strategies to cope with the rising NPA level,

the three Fls had approached the banking division with a proposal to form a common asset

reconstruction company (ARC) to clean up their balance sheets. The plan envisages

transfer of only large accounts that are common to the institutions. If all the lenders free

their rights on a debtor and give it to one entity, it can fight with the debtor and recover

whatever money can come. Though it is still in the conceptual stage, it is yet to be seen

how far thing improves if the plan materialises.

25 NLDIMSR

8/2/2019 NPA Mgmtt.by Suchet Bangera

http://slidepdf.com/reader/full/npa-mgmttby-suchet-bangera 26/39

NPA MANAGEMENT

SECTION -B

NPA MANAGEMENT –

GLOBAL CONTEXT.

26 NLDIMSR

8/2/2019 NPA Mgmtt.by Suchet Bangera

http://slidepdf.com/reader/full/npa-mgmttby-suchet-bangera 27/39

NPA MANAGEMENT

Introduction

After nationalization, the initial mandate that banks were given was to expand their

branch network increase the savings rate & extend credit to the rural & SSI sectors. This

mandate has been achieved admirably. Since the early 90’s the focus has shifted towards

improving quality of assets & better risk management.

The Narsimhan Committee has recommended prudential norms on income recognition,

asset classification & provisioning. In a change from the past, Income recognition is

now not on an accrual basis but when it is actually received. Past problems faced by

banks were to a great extent attributable to this.

Classification of what an NPA is has changed with tightening of prudential norms.

Currently an asset is “non-performing” if interest or installments of principal due

remains unpaid for more than 180 days.

27 NLDIMSR

8/2/2019 NPA Mgmtt.by Suchet Bangera

http://slidepdf.com/reader/full/npa-mgmttby-suchet-bangera 28/39

NPA MANAGEMENT

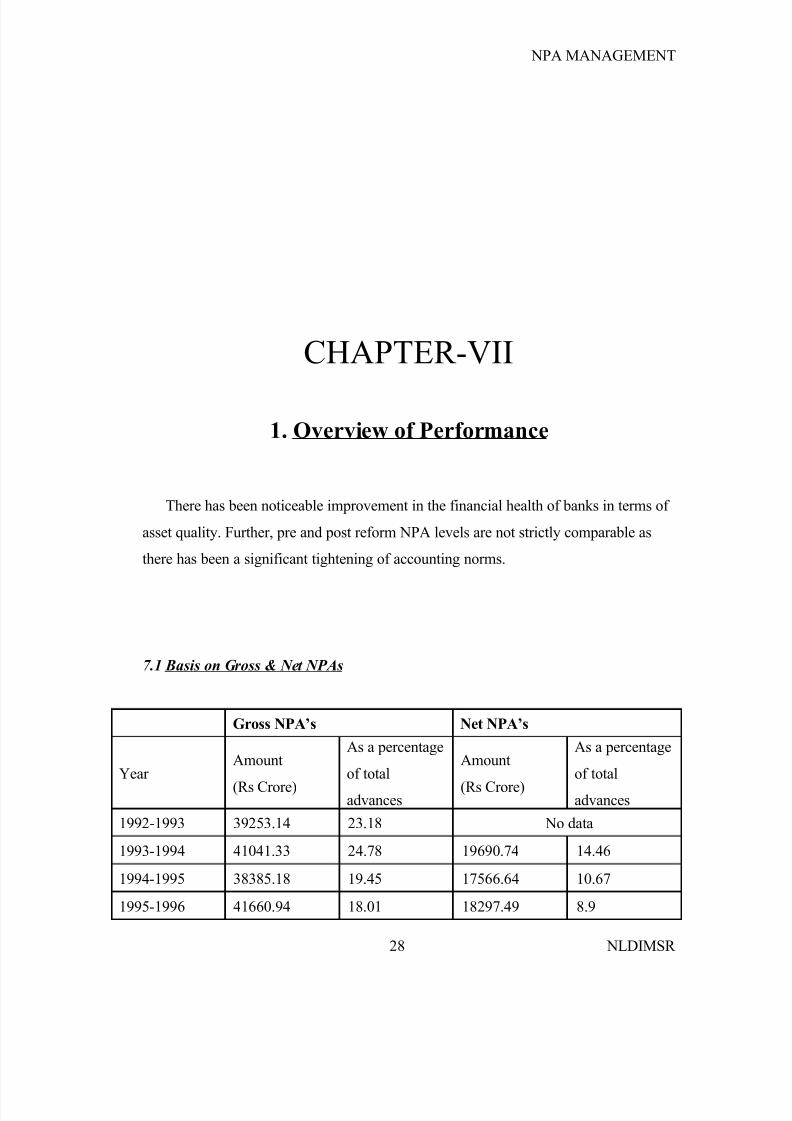

CHAPTER-VII

1. Overview of Performance

There has been noticeable improvement in the financial health of banks in terms of

asset quality. Further, pre and post reform NPA levels are not strictly comparable as

there has been a significant tightening of accounting norms.

7.1 Basis on Gross & Net NPAs

Gross NPA’s Net NPA’s

Year Amount

(Rs Crore)

As a percentage

of total

advances

Amount

(Rs Crore)

As a percentage

of total

advances

1992-1993 39253.14 23.18 No data

1993-1994 41041.33 24.78 19690.74 14.46

1994-1995 38385.18 19.45 17566.64 10.67

1995-1996 41660.94 18.01 18297.49 8.9

28 NLDIMSR

8/2/2019 NPA Mgmtt.by Suchet Bangera

http://slidepdf.com/reader/full/npa-mgmttby-suchet-bangera 29/39

NPA MANAGEMENT

1996-1997 43577.09 17.84 20284.73 9.18

1997-1998 45652.64 16.02 21232.13 8.15

1998-1999 51710.5 15.89 24211.49 8.13

1999-2000 53294.02 14.02 26187.6 7.422000-2001 54773.16 12.4 27968.11 6.74

Exhibit 1

7.2 Based on loan loss provisioning

The net NPAs have continually declined from 14.46% in 1993-1994 to 2000-2001.

RBI regulations require that banks build provisions upto at least 50% of their gross

NPAs. The current provisioning is 35% gross NPAs.

7.3 Sector wise split-up

As can be seen the main culprits are not the priority sectors or PSU’s but are the

large industries. If government sops to agriculture & SSI’s are excluded, the NPA in

the priority sectors is even lower.

Borrowing segment wise

distribution of Gross NPA’s

Gross NPA on March 31, 201

Amount

(Rs crore)Percentage of total NPA

Public sector units 1334.05 2.44

Large industries 11498.1 20.99

Medium industries 8658.69 15.81

Other non priority sectors 9516.62 17.37

29 NLDIMSR

8/2/2019 NPA Mgmtt.by Suchet Bangera

http://slidepdf.com/reader/full/npa-mgmttby-suchet-bangera 30/39

NPA MANAGEMENT

Agriculture 7311.4 13.35

Small sector industries 10284.97 18.78

Other priority sectors 6169.33 11.72

Exhibit 2

The problem India faces is not lack of strict prudential norms but

1. The legal impediments and the time consuming nature of asset disposal process.

2. ‘Postponement’ of the problems in order to report higher earnings.

3. Manipulation by the debtors using political influence.

A perverse effect of the slow legal process is that banks are shying away from risks by

investing a greater than required proportion of the assets in the form of sovereign debt

paper.

The government recently enacted the Asset Reconstruction Ordinance to try and tackle

the problem. It gave wide-ranging powers for banks to dispose of assets & allowed

creation if Asset Reconstruction Companies for this purpose.

30 NLDIMSR

8/2/2019 NPA Mgmtt.by Suchet Bangera

http://slidepdf.com/reader/full/npa-mgmttby-suchet-bangera 31/39

NPA MANAGEMENT

CHAPTER-X

Solutions

• Don’t Eliminate –Manage!

Studies have shown that management of NPAs rather than elimination is prudent.

India’s growth rate and bank spreads are higher than western nations. As a result

we can support a non-zero level of NPAs which balances the risk vis-à-vis return

appropriate to the Indian context.

• Effectiveness of ARCs

Concerns have been raised about the relevance to India. A significant percentage of

the NPAs of the PSB’s are in the priority sector. Loans in rural areas are difficult to

collect and banks by virtue of their sheet reach are better placed to recover these

loans. Lok Adalats and debt Recovery Tribunals are other effective mechanism to

handle this task. ARCs should focus on borrowers. Further, there is a need for

private sector and foreign participation in the ARC. Private parties will look for

active resolution of the problem and not mearly regard it as a book transaction.

Moving NPAs to an ARC doesn’t get rid of the problem. In China, potential

investors are still worried about the risks of non-enforcement of ownership rights of

the assets they purchase from the ARCs.Actions and measures have to be taken to

build investor confidence.

31 NLDIMSR

8/2/2019 NPA Mgmtt.by Suchet Bangera

http://slidepdf.com/reader/full/npa-mgmttby-suchet-bangera 32/39

NPA MANAGEMENT

Well Developed Capital markets

Numerous papers have stressed the criticality of a well-developed capital market in

the restructuring process. A capital market brings liquidity and mechanism for write

off of loans. Without this a bank may postpone the NPA problem for fear of capital

adequacy problems and resort to tactics like evergreening. Monitoring by

bondholders is better as they have no motive to sustain uneconomic activity.

Further, the banks can manage credit risk better as it is easier to sell or securitize

loans and negotiate credit derivatives. Indian debt market is relatively under

developed and attention should be focused on building liquidity and volumes.

Contextual Decision-making

Regulations must incorporate a contextual perspective (like temporary cash flow

problems) and clients should be handled in a manner, which reflects true value of

their assets and future potential to pay. The top management should delegate

authority and back decisions of this kind taken by middle level managers.

Effects of Capital norm tightening

There is a fear that disposal through the provision of excessive reserves may result

in a deflationary spiral. A through provision of reserves will have no negative

impact on the long-term dividends paid to the shareholders. Firstly, it helps restore

credibility in the financial system. Further, an adjustment mechanism can be

created by which the capital gains and future profits that will result from the

disposal of NPAs will pass back to the creditors as the tax payers who incurred the

losses today. The swift disposal of NPAs during the Great Depression in the middle

of a severe deflationary current helped restore the credibility of the financial

system.

Realignment of performance matrix

Traditional performance measures like ROE and NPA Ratio are not really

indicative of performance-A high volume of bad lending today will impact

32 NLDIMSR

8/2/2019 NPA Mgmtt.by Suchet Bangera

http://slidepdf.com/reader/full/npa-mgmttby-suchet-bangera 33/39

NPA MANAGEMENT

positively on ROE, asset growth and NPA ratio and only show up 5 years later as

NPAs.The complexity of the balance sheet makes it impossible to disaggregate the

impact of these actions even if stricter disclosure norms are put in place.

Economic Value of Equity (EVE) (or Market value) and Economic value of Equity

at Risk (EVER) are useful mechanisms to handle this problem. EVE is the value of

the firm if its assets are instantaneously liquidated (assuming the availability of the

liquid markets). Books Values vis-a- vis EVE comparisons give an idea of whether

the ‘fair’ value is being reflected. EVER can be computed by using ‘what if’

scenarios like downgrading the ratings of assets or changing interest rates. Now, at

every stage banks can check if their actions are consistent with the goal of

maximizing EVE, subject to an acceptable level of EVER.

Consistency of Purpose!

Some experts argues that the current organizational competencies, regulatory

framework, quality of disclosure and incentive structure produce an inconsistent

framework, which leads to an unsustainable performance level for a bank. Macro

level issues will have to be addressed in order to root out the problem. Processes at

every stage of an assets life impact the overall quality of the intermediation process

and so a consistent set of procedures are necessary to handle the problem

Legal Issues

There have been instances of banks extending credit to doubtful debtors (who

willfully default on debt) and getting kickbacks for the same. Ineffective legal

mechanisms and inadequate internal control mechanisms have made this problem

grow-quick action has to be taken on both counts so that both the defaulters and the

authorizing officer are punished heavily. Without this, all the mechanisms

suggested above may prove to be ineffective.

33 NLDIMSR

8/2/2019 NPA Mgmtt.by Suchet Bangera

http://slidepdf.com/reader/full/npa-mgmttby-suchet-bangera 34/39

NPA MANAGEMENT

CONCLUSION

The project stresses the importance of a sound understanding of the macro

economic variables and systemic issues pertaining to banks and the economy for

solving the NPA problem along with the criticality of a strong legal framework.

Foreign experiences must be utilized along with a clear understanding of the localconditions to create a tailor made solution, which is transparent and fair to all

stakeholders.

34 NLDIMSR

8/2/2019 NPA Mgmtt.by Suchet Bangera

http://slidepdf.com/reader/full/npa-mgmttby-suchet-bangera 35/39

NPA MANAGEMENT

ANNEXURE

RBI GUIDELINES TO FIs (For rehabilitation of sick industrial units)

Characteristics of these guidelines are discussed below:

(i) Tackling incipient sickness:

There is need to gear up the organisational machinery in the banks and Fls for

taking effective measure to detect incipient sickness and safeguard their interests. In this

context the steps necessary to be taken include-

• Pre and post-sanction inspection.

• Stock verification and stock audit,

• Continuous supervision over large accounts,

• Proper documentation ,

• Proper training and guidance to the staff at operational level,

• Preparation and furnishing detailed checklist for scrutinising Quarterly

Information System(QIS), statements to the operating staff and taking

follow-up action,

• System of taking appropriate action by banks and FIS

• Concept of 'accountability' at branch level to be made more effective.

(i) Co-ordination between Financial Institutions and amongst

banks:

(ii) Participation in rehabilitation packages-

(iii) Group approach:

35 NLDIMSR

8/2/2019 NPA Mgmtt.by Suchet Bangera

http://slidepdf.com/reader/full/npa-mgmttby-suchet-bangera 36/39

NPA MANAGEMENT

• When units in an 'industrial group becomes sick, the 'institutions should

examine whether sickness has arisen on account of internal factors such as

mismanagement, diversion of funds, neglect, etc., or on account of

external factors and take adequate steps accordingly.

• Recall of advances: - There should be proper consultation among the banks

and FIs so that the decision to recall advances is taken jointly.

• Preparation of Packages:- While preparing packages, the overall objective

of the Operating Agency/Lead Institution should be the rehabilitation of

the unit, keeping in view the sacrifices that the participating agencies

would be prepared to make. The following factors can be taken 'into

consideration-

> Where management deficiency is found to be the reason for sickness, it should

be ensured that the dishonest and/or incompetent management is removed so

that the rehabilitation package can succeed. Where the management is weak, it

should be strengthened by inducting professional managers/nominees of banks/

Financial Institutions. Constitution of Management Committees may also be

considered where necessary.

> Considering the overall need to strengthen the equity base of sick industrial units,

FIs, Banks should insist on promoters' augmenting the capital base. Where necessary,

restructuring of the equity should also be considered.

> Expansion, diversification should be encouraged only where it is imperative.

> A definite time frame for compliance of the package by each of the agencies

should be clearly spelt out in consultation with the agencies concerned and should

be given to BEFR.

> A Nodal Agency should be designated for monitoring the implementation of the

rehabilitation package by all agencies.

36 NLDIMSR

8/2/2019 NPA Mgmtt.by Suchet Bangera

http://slidepdf.com/reader/full/npa-mgmttby-suchet-bangera 37/39

NPA MANAGEMENT

• Implementation of Packages-Fls and banks should ensure that there is sufficient

delegation of powers so that the time lag between sanction of the scheme by the

BIFR and formal approval by the Board/competent authority is minimised and

delay in implementation of the rehabilitation package does not arise on this

account.

• Monitoring the implementation of packages

• Furnishing of information to Board for Industrial and Financial Reconstruction

(BIFR).

• Training arrangements.

37 NLDIMSR

8/2/2019 NPA Mgmtt.by Suchet Bangera

http://slidepdf.com/reader/full/npa-mgmttby-suchet-bangera 38/39

NPA MANAGEMENT

BIBLIOGRAPHY

I Books

1. Chandra P.C., Financial Management Principles & Practice.

2. Khan & Jain, Finincial Management

3. Panday I.M., Financial Management4. Kothiri C.R., Research Methodology

11. Magazines

1. Investor

2. Business India

3. Business Today

111. Newspapers

1. The Economic Times

2. The Business Standard

3. The Financial Express

I V. Published Material

I. 2000-2001 Annual Report of IFCI

2. 2000-2001 Annual Report of ICICI

3 2000-2001 Annual Re-port of IDBI

4. RBI Guidelines Circulars on Income Recognition and Asset Classification

38 NLDIMSR

8/2/2019 NPA Mgmtt.by Suchet Bangera

http://slidepdf.com/reader/full/npa-mgmttby-suchet-bangera 39/39

NPA MANAGEMENT

V. Other Sources Internet Websites

I. www.indiainfoline.com

2.

3. www.rbi.org.com

![By, [Blue Team] Bauyrzhan Aitileu Muneeb Mahmood Vinaykumar Bangera.](https://static.fdocuments.us/doc/165x107/5a4d1b467f8b9ab0599a3648/by-blue-team-bauyrzhan-aitileu-muneeb-mahmood-vinaykumar-bangera.jpg)