November 2011 Newsletter

9

Social Market Foundation | Newsletter November 2011 | Page 1 www.smf.co.uk | @smfthinktank Newsletter November 2011 Welcome to this edition of the SMF newsletter As the Chancellor prepares to deliver his autumn statement and growth review, it is clear that 2011 has been a year of extraordinary turbulence in the global economy. With continuing sovereign debt crises in the Eurozone, widespread concern over unemployment, and most major developed economies subject to successive growth forecast downgrades, some huge questions hang over politicians from all parties in the UK: where will economic growth come from? What role should the state have in bailing out failing businesses? And what does a functioning and responsible capitalist economy look like for the future? To mark our 21st year, the SMF invited eight high-profile commentators to contribute essays on these vital questions and more, which have formed our recent publication Markets in a State. This was launched earlier in the month by the Leader of the Opposition, Ed Miliband at an event which also included contributions from Vicky Pryce of FTI consulting, Daniel Franklin of the Economist and Lord David Owen. More information about this publication is on page 4 and details of Ed Miliband’s speech are on page 5. Today the SMF launches its latest publication, The Parent Trap: Illustrating the growing cost of childcare. This new analysis looks at the changing level of financial support and the rising cost of formal childcare between 2006 - the peak of public financial support for childcare - and 2015, to show how much of their own money families will have to find to fill the growing gap. It highlights a growing affordability crisis, where parents on low incomes will have to find 60% more from their own pockets in 2015 for the same amount of childcare, compared to 2006. Further details are on page 5. This newsletter also contains details of our exciting programme of events between now and Christmas. On 15 December we are delighted to welcome Danny Alexander and Iain Duncan Smith to join other distinguished speakers at a half-day conference on social impact bonds. This event will explore the uses and applications of this innovative form of funding in a range of public services, from early years to welfare reform. More details are on page 7 or on the SMF website. Contents Welcome to this edition 1 Director’s note: Plan B by any other name 3 Latest publications 4 Ed Miliband launches Markets in a State 5 John Springford: Apprenticeships - Rhineland envy 6 Events 7 Nigel Keohane: Why competition isn't working in HE 8 Event report: Encouraging Responsible universities 9

-

Upload

leonora-merry -

Category

Documents

-

view

214 -

download

0

description

SMF's November newsletter 2011

Transcript of November 2011 Newsletter

Social Market Foundation | Newsletter November 2011 | Page 1

www.smf.co.uk | @smfthinktank

Newsletter November 2011

Welcome to this edition of the SMF newsletter As the Chancellor prepares to deliver his autumn statement and growth review, it is

clear that 2011 has been a year of extraordinary turbulence in the global economy.

With continuing sovereign debt crises in the Eurozone, widespread concern over

unemployment, and most major developed economies subject to successive growth

forecast downgrades, some huge questions hang over politicians from all parties in

the UK: where will economic growth come from? What role should the state have in

bailing out failing businesses? And what does a functioning and responsible capitalist

economy look like for the future?

To mark our 21st year, the SMF invited eight high-profile commentators to contribute

essays on these vital questions and more, which have formed our recent publication

Markets in a State. This was launched earlier in the month by the Leader of the

Opposition, Ed Miliband at an event which also included contributions from Vicky

Pryce of FTI consulting, Daniel Franklin of the Economist and Lord David Owen.

More information about this publication is on page 4 and details of Ed Miliband’s

speech are on page 5.

Today the SMF launches its latest publication, The Parent Trap: Illustrating the

growing cost of childcare. This new analysis looks at the changing level of financial

support and the rising cost of formal childcare between 2006 - the peak of public

financial support for childcare - and 2015, to show how much of their own money

families will have to find to fill the growing gap. It highlights a growing affordability

crisis, where parents on low incomes will have to find 60% more from their own

pockets in 2015 for the same amount of childcare, compared to 2006. Further details

are on page 5.

This newsletter also contains details of our exciting programme of events between

now and Christmas. On 15 December we are delighted to welcome Danny

Alexander and Iain Duncan Smith to join other distinguished speakers at a half-day

conference on social impact bonds. This event will explore the uses and applications

of this innovative form of funding in a range of public services, from early years to

welfare reform. More details are on page 7 or on the SMF website.

Contents

Welcome to this edition 1

Director’s note: Plan B by any

other name 3

Latest publications 4

Ed Miliband launches Markets

in a State 5

John Springford: Apprenticeships -

Rhineland envy 6

Events 7

Nigel Keohane: Why competition

isn't working in HE 8

Event report: Encouraging

Responsible universities 9

Social Market Foundation | Newsletter November 2011 | Page 2

www.smf.co.uk | @smfthinktank

December will also see two Chalk + Talk lunchtime lectures, completing our

successful series for 2011. On 1 December Professor Henry Overman will discuss the

regional growth dilemma, and on 15 December Lord Layard of LSE to talk about

wellbeing. Further details of both events can be found on page 7.

Growth

Back in September, at the SMF’s keynote event at both the Liberal Democrat and

Conservative party conferences, Oliver Letwin , Danny Alexander , Brendan Barber

and SMF Director Ian Mulheirn discussed where growth in the UK economy could

come from. A short video of highlights from the event is available online. On page 3 of

this newsletter, Ian Mulheirn revisits some of the themes covered at that event,

arguing that the Chancellor’s plans to use off-balance sheet capital spending to boost

the economy is a welcome Plan B - in all but name.

Skills

Regardless of the differences between the political parties on how to create growth,

what unites politicians in all parties is the need to tackle the large numbers of

unemployed people with low skill levels. Early in 2012 the SMF will be publishing a

major paper on adult skills. On page 6 its author, John Springford, offers a critique of

apprenticeships in the UK and argues that the Government’s fixation with

apprenticeships as an end in themselves is missing the point when it comes to

boosting the UK economy.

Higher Education

Last week the SMF hosted a half-day conference on the new Higher Education

funding regime with David Willetts . The event looked at how the university reform

agenda would affect competition in HE, university funding and student access. On

page 8 of this newsletter, SMF Deputy Director Nigel Keohane argues that the real

barrier to increased competition in HE is the cap on student numbers. A summary of

the Encouraging Responsible Universities event is on page 9.

As we move into 2012, SMF will be continuing to produce bold and rigorous research

proposals including on skills, childcare, and financial resilience so look out for our

work on these. We will also be continuing our popular Chalk + Talk lunchtime lecture

series and will be running events on welfare reform and justice early in the new year.

2012 will also see the launch of our new website, so keep an eye on www.smf.co.uk.

Thank you for reading SMF newsletters in 2011 and Happy Christmas!

The Social Market Foundation is an

independent public policy think-tank,

developing and advancing innovative

solutions across a broad range of

economic and social policy.

We publish original research, hold

seminars and debates in Westminster

and beyond, and run a diverse

programme of events at the three

main party conferences.

Since its foundation in 1989, the work

of the SMF has been principally

devoted to promoting the social

market philosophy, which seeks to

marry markets and social justice. It

neither sees the market as a necessary

evil nor as an end in itself but as a

means to improve people’s lives. It is

underpinned by adherence to two key

principles: first, a positive preference

for market mechanisms, while

recognising that a truly pro-market

approach is often not a free-market

one; and second, a belief that a

sustainable market economy rests on

social and political foundations that

are widely regarded as fair.

Our work aims to elucidate these ideas

and to explain why the social market

is a fruitful source of solutions to

public policy problems.

For further information please contact

Leonora Merry - [email protected]

Social Market Foundation

11 Tufton Street

Westminster

London

SW1P 3QB

020 7222 7060

Social Market Foundation | Newsletter November 2011 | Page 3

www.smf.co.uk | @smfthinktank

Director’s Note: Plan B by any other name

Despite the message of austerity, the Government has swung into action with all manner of growth-promoting measures. Some are wise and some less so. But all of them use the

public sector balance sheet to some extent. They might not call it Plan B, but the shift from austerity is remarkable. And far from ‘getting out of the way’, the Treasury is rightly

getting involved. The remaining question is whether these interventions are big enough to pull the economy out of the quagmire.

Tuesday’s Autumn Statement is likely to be overshadowed by a wrenching reappraisal of

the outlook for the public finances from the Office for Budget Responsibility (OBR). That, presumably, is why the Government has been getting its retaliation in early by drip-

feeding elements of the growth plan over the past week. The unpopular bits - like the rumoured axing of higher rate tax relief for pensions and perhaps a freeze on the only

non-frozen element of the Working Tax Credit – will surely come out on bad-news Tuesday. Nevertheless, what we’ve heard from the Government on growth is a big shift

away from the old language of public sector cuts alone being a sufficient growth strategy.

First let’s deal with the less good parts of the plan. Last week a big fanfare was made about a new mortgage indemnity scheme for first-time buyers. Taking on residential

mortgage risk that banks aren’t prepared to touch is an unfortunate use of the government’s balance sheet, to put it mildly. And using taxpayers’ money to try to re-

inflate the UK property ponzi scheme is good for almost nobody.

Then there’s youth unemployment. In the face of nasty jobless figures, the Government also announced some labour demand policies to try to encourage employers to hire

young jobseekers. The main plan is to provide large financial incentives for firms to hire young workers who’ve been out of work for over nine months. While the intentions are

good, the evidence suggests that policies like these do little to help and are a waste of

money. The vast majority of firms who hire to take advantage of this kind of offer would have hired someone anyway – it may just be that now they fill the vacancy with a young

person at the expense of a no-less-deserving older unemployed worker.

The sad truth is that high rates of unemployment can’t be tackled by tinkering in the labour market – with either regulation or hiring subsidies. The only real solution lies in

improving the macroeconomic outlook to stimulate demand. And it’s here that the most interesting parts of the growth plan are taking shape.

At his party’s conference in October, the chancellor announced plans for easing the flow

of credit to small companies. The more detailed plan is to issue between £20bn and

£40bn of guarantees for banks lending to small and medium-sized enterprises (SMEs) – a substantially larger scheme than most people anticipated. The question is whether the

move will increase the level of lending to SMEs – as it must in order to have an impact on

growth - rather than simply lowering the cost of borrowing to existing customers.

Alongside this, there are Treasury plans afoot to facilitate greater private investment in

infrastructure. They hope to attract pension and sovereign wealth funds into large capital projects like road-building, rail and energy infrastructure. Of course, since these investors

usually put their money in Government bonds, you could argue that the Government should simply use public finance to fund an infrastructure boost. But that might

compromise the Treasury’s hawkish image. So the aim is to achieve the low costs of government borrowing in a way that gets the borrowing off the Treasury’s books. As

with the housing scheme and the credit easing plan, the only way to lower the cost of borrowing is for government to shoulder the risk of private investments. So Mr Osborne

“They might not call

it Plan B, but the shift

from austerity is

remarkable. And far

from ‘getting out of

the way’, the Treasury

is rightly getting

involved”

Ian Mulheirn, Director, SMF

Social Market Foundation | Newsletter November 2011 | Page 4

www.smf.co.uk | @smfthinktank

Publications

Markets in a State? The Social Market Foundation at 21

The Social Market Foundation was founded in late 1989, as state socialism collapsed in Europe. Today, a global economic crisis has brought us to another fork in the road. We face economic stagnation and a heavy burden of government debt. The consequences of the crash will reverberate for years to come and the relationship between the state and the market will inevitably be redefined. But how? Social market thinking can guide us on the uncertain road ahead. To mark its 21st year, the Social Market Foundation commissioned essays by leading politicians, academics and journalists on social market policy in a period of sustained economic crisis. In this wide-ranging collection, Mary Ann Sieghart, Ian Mulheirn, Philip Collins, David Lipsey, David Owen, Peter Lilley, Robert Skidelsky, Dieter Helm and John Kay suggest how the boundaries between the state and the market should be redrawn.

The Parent Trap: Illustrating the growing cost of

childcare

High-quality, affordable formal childcare is critical for children’s development and parental employment, bringing significant private and public benefits. In this analysis, the SMF explores the changing level of financial support and the rising cost of formal childcare between 2006-07 – the high-water mark of public financial support for childcare – and 2015-16. The paper demonstrates how childcare affordability has deteriorated and will continue to decline in the years ahead.

Download Markets in a State

Download The Parent Trap

hopes to entice the private sector to stump up by guaranteeing things – in the case of

infrastructure projects a respectable long-term return on investment.

It would be a huge U-turn for the Government now to try and kick-start growth by borrowing to invest in infrastructure and SMEs directly. After all, you ‘can’t get out of a

debt crisis by taking on more debt’, right? But it’s a neat trick to get others to do the borrowing for you by offering to cover any of their losses down the line. That way you

get the same real world results without adding to the sea of red ink in the government’s books. Welcome though they are, these guarantees are no fiscal free

lunch. Loading the taxpayer up with financial risk is economically no different to loading them up with investment in risky infrastructure schemes. This, then, is a

scheme that sticks to the letter but not the spirit of the tough fiscal rules.

The government is right to stick to its plans to cut current spending. Indeed, this week

the OBR is likely to warn it of the need to make yet more cuts. But, as the SMF has been arguing for some time, that doesn’t mean that austerity is the only alternative.

The emerging investment strategy is finally moving in the right direction. It remains to be seen whether the infrastructure plan can get off the ground and whether the credit

easing will expand lending sufficiently. Either way the shift from austerity to a Plan B is clear. Thank goodness for that.

“...it’s a neat trick to

get others to do the

borrowing for you by

offering to cover any

of their losses down

the line.“

Social Market Foundation | Newsletter November 2011 | Page 5

www.smf.co.uk | @smfthinktank

Rt Hon Ed Miliband launches SMF publication

Markets in a State

Leader of the Opposition Rt Hon Ed Miliband MP delivered a speech to the Social Market Foundation on 17 November to launch the SMF's latest publication, Markets in

a State. The Labour leader called for "a new, more responsible, productive capitalism" that is "hard-headed - not soft-hearted." Mr Miliband outlined five plans for a new economy that works for all: reconnecting finance and the 'real economy'; encouraging long-termism in business; addressing the shortage of vocational skills in the economy; a new commitment to responsibility over executive pay; and challenging the large concentrations of private power. At the event, kindly sponsored by Nationwide and hosted by Arup, Ed Miliband called for: “An economy that creates long-term value based on investment and commitment. Better-quality jobs that reverse the decline of middle-class incomes, and set firms up to compete on the basis of skills and quality. And a sustainable economy, diverse enough to protect Britain against external and fiscal shocks, with environmental sustainability built in rather than bolted on.“ He said: “This cannot be reduced to a case for more government and less markets. We should be passionate about the progress healthy markets can bring. But passionate too about the difference government can make working with the private sector.” Mr Miliband's speech was preceded by a panel discussion on the state’s role in making our economy work better, one of the main themes of Markets in a State, with Rt Hon Lord Owen, Vicky Pryce of FTI consulting and Daniel Franklin of the Economist.

“We should be

passionate about

the progress healthy

markets can bring.

But passionate too

about the difference

government can

make working with

the private sector.”

Rt Hon Ed Miliband MP,

Speech to SMF, 17/11

Ed Miliband delivers his speech to the SMF at Arup in Central London (top) SMF Director Ian Mulheirn greets Ed Miliband before the speech (bottom)

Download a full copy of Ed Miliband’s speech to the SMF

Social Market Foundation | Newsletter November 2011 | Page 6

www.smf.co.uk | @smfthinktank

Apprenticeships: Rhineland envy Now that the financial crisis wave has dashed the UK’s economic model on the rocks,

politicians are gazing across the North Sea with envy at Germany. Many in Westminster want to replicate German manufacturing and exports prowess. German

training is held up as a beacon to follow, with ‘parity of esteem’ between vocational and academic qualifications, and apprenticeships that are long and heavy on training

– not just a vehicle for cheap labour.

The Government has caught on. Its big idea is to increase by 100,000 the number of apprenticeships offered annually by 2014. The rationale, according to Skills Minister

John Hayes MP, is that “apprenticeships say to people, ‘Aspire, whoever you are and whatever your background. All that’s required is the strength of will to take the first

step.’”

More prosaically, the Government is attracted to apprenticeships because they are ‘demand led’: employers hire apprentices because they want cheap labour now, the

Government will pay for formal training, and the apprentice will learn on the job. The Government argues that apprenticeships entail ‘co-investment’ because employers

have to offer a minimum wage of £2.60 per hour, while the Government pays for an off-the-job training course.

So the Coalition is making the same mistake its predecessor did: pick types of training

it thinks will lead to jobs, and chuck money at an unreformed system.

The evidence on apprenticeships suggests many are of questionable value. While in Germany, courses take between two and four years and apprentices have to spend a

third to half their time in formal training, British apprentices have to only spend two hours a week in training and a larger proportion drop out. Apprenticeships here are

associated with higher wages than taught courses, but this may be due to the sectors the apprenticeships are in (more apprenticeships are offered in high skilled sectors like

engineering).

Increasingly apprenticeships are being undertaken in the service sector, where the evidence suggests returns are far lower or not apparent at all. Steven McIntosh at

Sheffield University found higher wages for ex-apprentices in only four of eleven services sectors in 2004. If the Government simply floods the market with

apprenticeships, many will be taken in economic sectors where their value is questionable.

Furthermore many of the Government’s new apprenticeships are in fact pre-existing employer-led training that has merely been rebranded as such. Some new

‘apprenticeships’ are in fact very similar in content to the in-work training that has

gone before. The courses are usually short (the average apprenticeship lasts for 28

weeks); and many are at a low level of skill. Employers are unwilling to countenance

expensive and lengthy training when they may not recoup the outlay.

So instead of subsidising a type of training it thinks works, Government could pay

training providers by results. The one thing we can know for sure about unemployed people is that their needs are different. If one provider gets more of its apprentices

into sustained employment than another, it could be rewarded. Equally, if it finds that

some people do better by taking an academic qualification, a payment by results system would get them to tell its students this, and try to get them to take it – if it is

right for them.

Ministers should stop picking training winners in the hope of aping the Rhineland

model. A proper market in training is better than soggy corporatism – with Government giving employers cheap labour and getting shoddy training in return.

“The Coalition is

making the same

mistake its

predecessor did: pick

types of training it

thinks will lead to

jobs, and chuck

money at an

unreformed system”

John Springford, Senior Researcher, SMF

Social Market Foundation | Newsletter November 2011 | Page 7

www.smf.co.uk | @smfthinktank

Events

Risk and Reward: can social impact bonds breathe new

life into public services?

Date: Thursday 15 December 2011

Speakers: Rt Hon Iain Duncan Smith MP, Secretary of State, DWP

Rt Hon Danny Alexander MP, Chief Secretary to the Treasury

Venue: The British Academy, 10 Carlton House Terrace

Register online here

The Coalition Government is seeking to bring about a revolution in the way public services are run. Instead of a top-down model, where public services are delivered according to set targets, ministers are keen to explore alternative models where providers are held accountable through consumer choice and outcome-based payments. Social impact bonds, in which investors assume some of the risk - and attract financial reward – for achieving set policy goals, are one such innovative model. The benefits of attracting private capital to public services in troubled economic times are obvious. But in which new policy areas can social impact bonds be deployed? Can private capital really fill the gap left by public sector cuts? And how can social impact bonds be designed in order to attract significant amounts of private capital?

SMF Chalk + Talk: The regional growth dilemma: how

do we narrow the north-south divide?

Date: Thursday 1 December 2011, 12.30pm

Speaker: Professor Henry Overman, LSE

Venue: SMF, 11 Tufton St, Westminster, SW1P 3QB

Register online here.

The Government’s plans for regional growth are starting to take shape. But as they disburse the Regional Growth Fund and look towards land auctions and planning liberalisation in housing policy, is the Government using the most effective tools for tackling the problem of unbalanced regional growth? This event will look at the options available to policymakers in this area.

SMF Chalk + Talk: Whose wellbeing is it anyway?

• Date: Thursday 15 December, 15.30pm

• Venue: SMF, 11 Tufton St, Westminster, SW1P 3QB

• Speaker: Professor Richard Layard, LSE

Register online here

Has the relentless pursuit of economic growth made us miserable? Can a wellbeing index compete with GDP as a measure of prosperity? And can macroeconomic policies really make a difference to our happiness as a society? Come along to the SMF’s last Chalk + Talk session of 2011 and discuss these questions and more with Lord Layard, one of the UK’s leading thinkers on wellbeing and happiness. And enjoy a festive mince pie to boost your own happiness too!

Join the SMF Business

Forum

Critical to our ability to deliver

the innovative and creative

policy reports and events for

which we are known is the close

partnership we enjoy with

organisations in the private

sector through our Business

Forum. SMF Business Forum

partners benefit from the

opportunity to deepen their

understanding of the policy

agenda through attendance at

exclusive events and by being

kept in regular touch with the

SMF’s research programme.

Particular benefits include:

• Places at our thrice-yearly Business Forum lunches

where a guest speaker makes a short speech and those present have the opportunity to ask questions and exchange views.

• This bi-monthly e-newsletter and a new tailored Business Forum e-newsletter summarising recent research reports.

• Copies of all our new research reports and policy essays.

• The opportunity to request briefings from SMF staff on their areas of expertise.

• Invitations to SMF events.

• The opportunity to partner with us at the three annual party conferences at a reduced rate.

For more information or to join the Business Forum, contact Leonora Merry at [email protected] or telephone 0207 227 4401.

Social Market Foundation | Newsletter November 2011 | Page 8

www.smf.co.uk | @smfthinktank

Revised tuition fees: a sign of things that aren’t to

come?

Government measures promoting university competition to bring down fees had

some success last month. But the effectiveness of these changes exposes the bigger

problem that the market in higher education isn't working

Twenty-four universities and three further education colleges have applied to set their

fees below £7,500 to compete for the 20,000 cut-price places set aside by the

government for 2012-13. Although the access watchdog has not made public the

details of those institutions that have made the grade, it's likely that around 20% of

institutions will end up charging below the £7,500 bar.

On the surface, the news will provide comfort to ministers that their reforms will be

both affordable and marginally more acceptable to Middle England. Yet this minor

victory is the exception that proves the rule. There is little to suggest that this

milestone represents the first of many major market readjustments that will bring

quality more into line with higher tuition fees, nor that the majority of institutions will

suddenly be motivated by market pressures to lower their prices. Not because, as

some believe, a market in higher education can never work. But because the 2012 HE

market will still be hampered due to the cap on overall student numbers.

A glance at the fees that universities are set to charge suggests that a lot of

readjustment is still necessary. While one fifth of institutions will ask for average fees of

below £7,500, a third will be congregated at the very top of the £9,000 cap. The

remainder will cram themselves somewhere between £7,500 and £9,000.

This clustering on price presents a range of problems to both students and the

government. For the student, it means that price will act as a very poor signal for

quality – so students are likely only to be confused by the range of options and will

find it hard to identify the best value courses. For the government, the lack of

downward pressure on fees will mean that the Exchequer will have to pick up an

unnecessarily large bill at the end of it all.

These are symptoms of the fact that competition in the HE marketplace remains very

weak. On the positive side, the government has sought to ensure that prospective

students can access additional information on teaching quality and graduate earnings

to help them decide where best to study. There are also reforms in train that will

increase the diversity of the sector and bring in new providers to compete.

However, the overriding obstacle to a fully functioning market is that universities can

only compete on the margins due to the cap on student numbers. This plays itself out

as a vicious circle: high fees will leave many students unable to repay their whole debt;

exposure to this bad debt leaves the Exchequer little option but to cap the number of

students to limit the cost; with demand much higher than the quota of places,

competition between universities is emasculated, blunting incentives to improve

quality or cut fees. Without more competition, the results are likely to disappoint:

institutions with bad teaching, offering poor value for money, will thrive alongside

high quality ones; and students will face higher fees without the kind of service they

have a right to expect.

The incentives for universities to compete for students taking lower-cost courses – and

the parallel 65,000 places for AAB students – are there, then, exactly because the HE

“The overriding

obstacle to a fully

functioning market

is that universities

can only compete on

the margins due to

the cap on student

numbers. This plays

itself out as a vicious

circle.”

Nigel Keohane

Deputy Director,

SMF

Social Market Foundation | Newsletter November 2011 | Page 9

www.smf.co.uk | @smfthinktank

market cannot be expected to function properly. Fiddling at the margins won't do

much to change the fact that the HE market is stillborn.

There are ways to get round this. One idea put forward last year by the Social Market

Foundation would be to shift more of the risk of loan non-repayment on to

universities themselves rather than taxpayers. HE institutions would therefore have a

strong incentive to ensure that their graduates went on to productive employment,

and the state could remove the stultifying student quota without having to bear the

extra cost.

Until the quota is removed, students will get a raw deal from many universities. Some

more radical thinking is needed before all universities are genuinely competing on

price and quality.

This is an edited version of an article that first appeared on the Guardian’s Higher Education

network

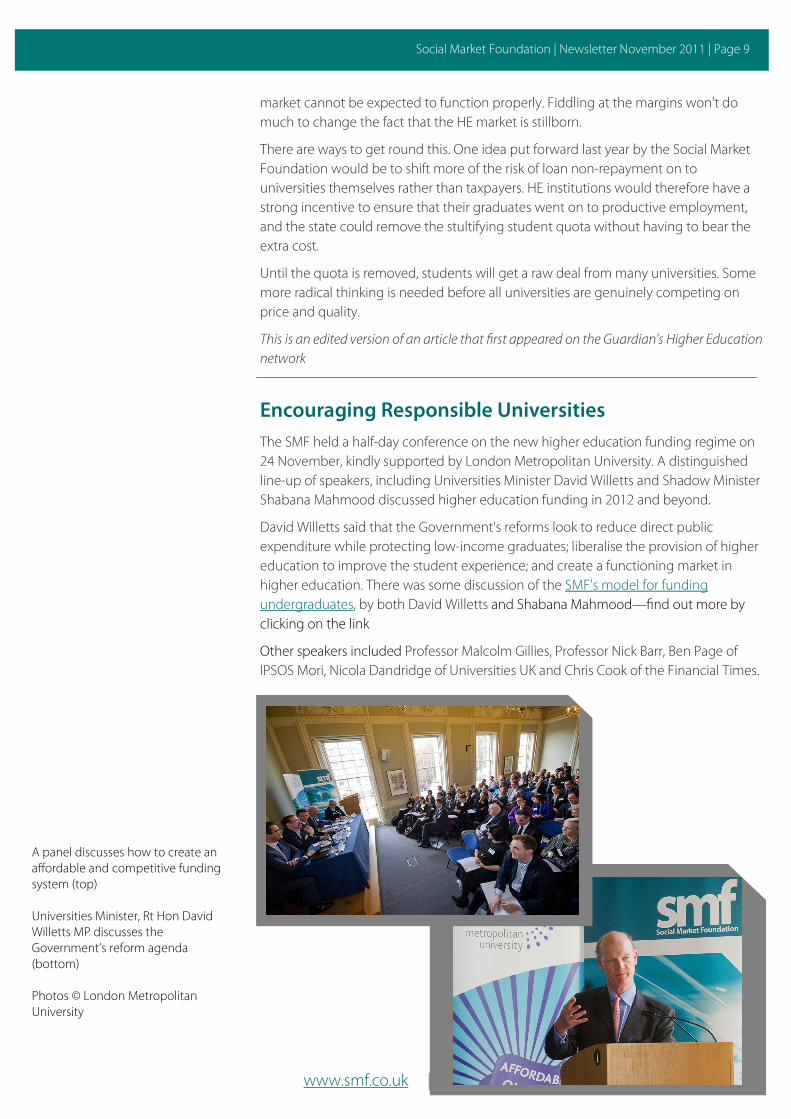

Encouraging Responsible Universities

The SMF held a half-day conference on the new higher education funding regime on

24 November, kindly supported by London Metropolitan University. A distinguished

line-up of speakers, including Universities Minister David Willetts and Shadow Minister

Shabana Mahmood discussed higher education funding in 2012 and beyond.

David Willetts said that the Government's reforms look to reduce direct public

expenditure while protecting low-income graduates; liberalise the provision of higher

education to improve the student experience; and create a functioning market in

higher education. There was some discussion of the SMF's model for funding

undergraduates, by both David Willetts and Shabana Mahmood—find out more by

clicking on the link

Other speakers included Professor Malcolm Gillies, Professor Nick Barr, Ben Page of

IPSOS Mori, Nicola Dandridge of Universities UK and Chris Cook of the Financial Times.

A panel discusses how to create an affordable and competitive funding system (top) Universities Minister, Rt Hon David Willetts MP discusses the Government’s reform agenda (bottom) Photos © London Metropolitan University