Novartis GB06 engl

236

ANNUAL REPORT 2006

Transcript of Novartis GB06 engl

WWW.NOVARTIS.COM ANNUAL REPORT 2006AN

NU

AL R

EP

OR

T 2

00

6 119863_Nova_001_002_ug_e.qxp 24.1.2007 13:10 Uhr Seite 1

1

We want to discover, develop and successfully marketinnovative products to prevent and cure diseases, to ease suffering and to enhance the quality of life.

We also want to provide a shareholder return that reflectsoutstanding performance and to adequately reward those who invest ideas and work in our company.

OUR MISSION

GROUP REVIEW

Overview 2

Letter from Daniel Vasella 5

OPERATIONAL REVIEW

Pharmaceuticals 12

Vaccines and Diagnostics 36

Sandoz 42

Consumer Health 50

CORPORATE CITIZENSHIP

Introduction 56

Commitment to Patients 61

Novartis Foundation for 68Sustainable Development

Commitment to Our People 71

Commitment to Health, 77Safety and Environment

Commitment to Ethical 84Business Conduct

Independent Assurance Report 89

Risk Management 91

CORPORATE GOVERNANCE

Commitment to Corporate Governance 93

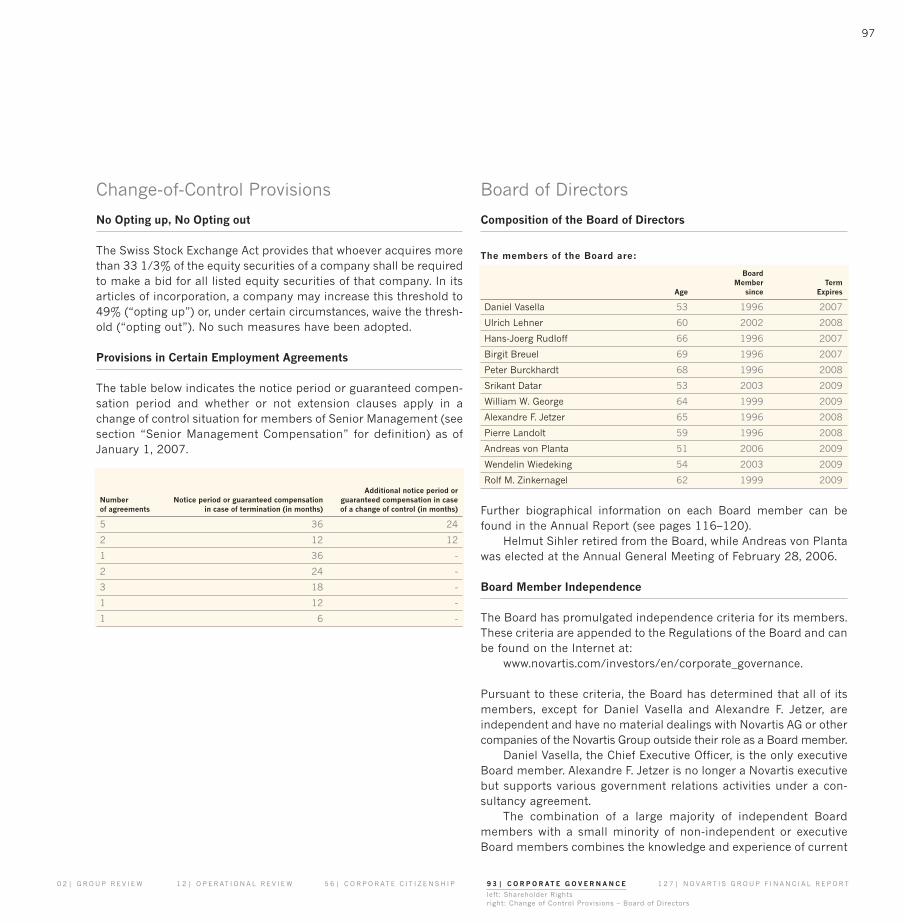

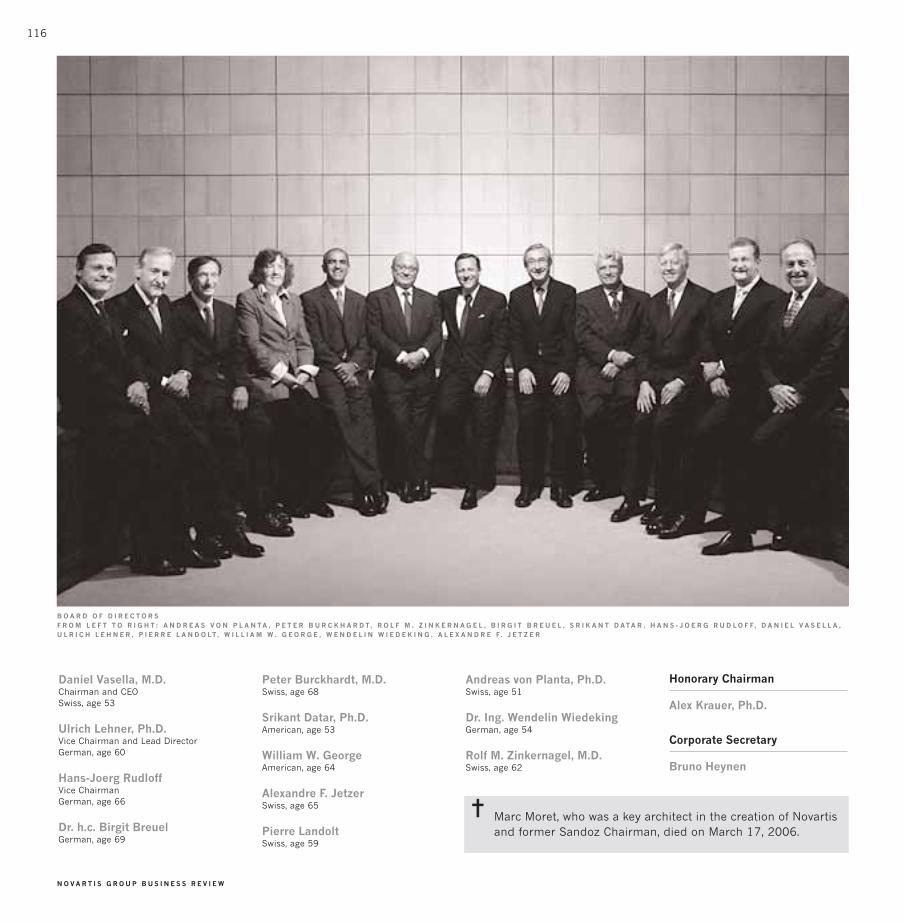

Board of Directors 116

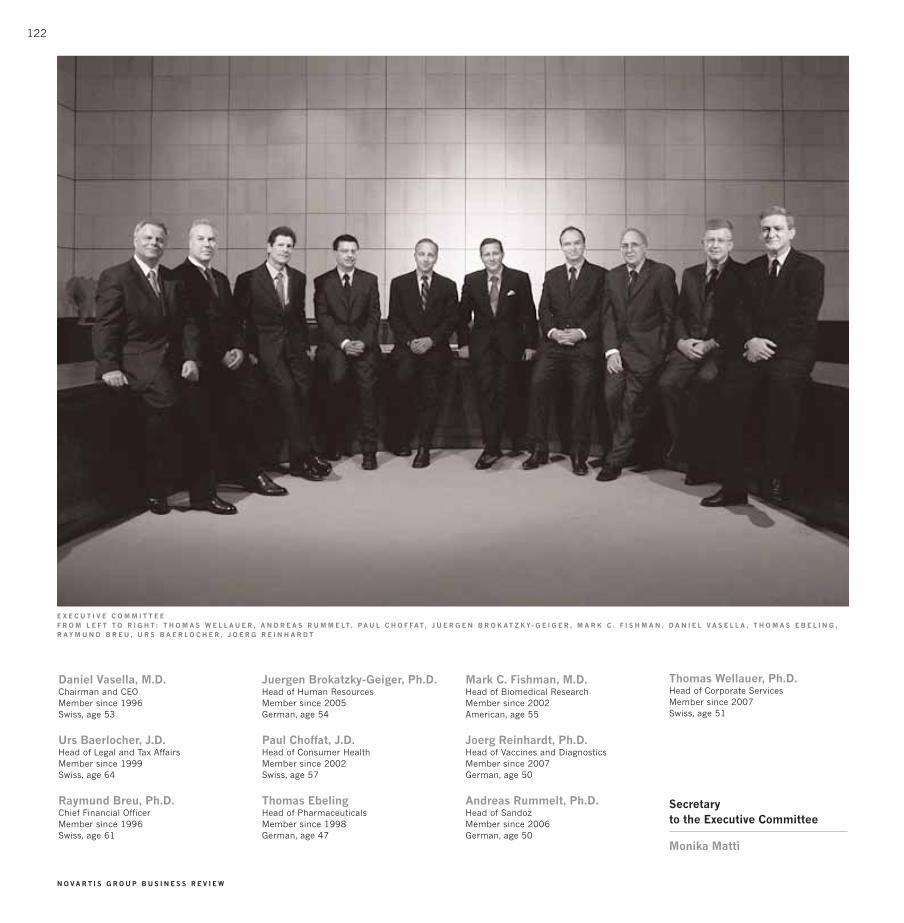

Executive Committee 122

Business Unit Heads 125

NOVARTIS GROUP FINANCIAL REPORT 2006

Contents 127

Operating & Financial Review 130

Equity Strategy 153

Novartis Group Consolidated 156Financial Statements

Novartis AG Financial Statements 224

Key Dates 2007 230

Contact Addresses 231

CONTENTS

I N S I D E F R O N T C O V E R : K A M E D A M E D I C A L C E N T E R ; K A M O G A W A C I T Y , C H I B A , J A P A NF R O N T C O V E R : G R U P O D E A P O I O A O A D O L E S C E N T E E À C R I A N Ç A C O M C Â N C E R ; S Ã O P A U L O , B R A Z I L

119863_Nova_000_000_web_e.qxp 24.1.2007 13:19 Uhr Seite 1

2

N O V A R T I S G R O U P B U S I N E S S R E V I E W

KEY FIGURES – GROUP1

(In USD millions unless indicated otherwise)

2006 2005

Group net sales 37 020 32 212Group operating income 8 174 6 905Return on sales (%) 22.1 21.4Group net income 7 202 6 141Research and development 5 364 4 846Research and development

as % of Group net sales 14.5 15.0Free cash flow 4 340 4 673Number of associates at year-end 100 735 90 924

1 Including discontinuing operations

SHARE INFORMATION

2006 2005

Return on average equity (%) 19.3 19.0Earnings per share (USD)1 3.06 2.63Operating cash flow per share (USD) 3.76 3.46ADS price at year-end (USD) 57.44 52.48Share price at year-end (CHF) 70.25 69.05Pay-out ratio based on outstanding

shares (%) 36 33

1 Average number of shares outstanding in 2006: 2 345 232 126(2005: 2 332 848 144)

61%PHARMACEUTICALS

3%VACCINES

AND DIAGNOSTICS

16%SANDOZ

20%CONSUMER HEALTH

2006 GROUP NET SALES BY DIVISION

2006 OPERATING INCOME BY DIVISION1

77%PHARMACEUTICALS

8%SANDOZ

15%CONSUMER HEALTH

Novartis is a world leader in providing medicines to protect health, prevent and treat disease, and toimprove well-being.

Novartis is the only company with leadership positions in patented and generic pharmaceuticals, vaccinesand over-the-counter medicines.

In 2006, Novartis continued to strengthen these strategic growth platforms to meet the needs of patientsand society in a dynamically changing healthcare environment.

GROUP

GROUP NET SALES, OPERATING INCOME AND NET INCOME(Index: 2002 = 100%)

190

175

160

145

130

115

100

20021 20032 20042 2005 2006

Net sales Operating income Net income 1 Not adjusted for new IFRS accounting rules 2 Pro forma adjusted for new IFRS accounting rules

FINANCIAL HIGHLIGHTS

1 Vaccines and Diagnostics had less than 1% impact on Divisional total operating income

119863_Nova_000_000_web_e.qxp 24.1.2007 13:19 Uhr Seite 2

3

0 2 | G R O U P R E V I E W 1 2 | O P E R AT I O N A L R E V I E W 5 6 | C O R P O R AT E C I T I Z E N S H I P 9 3 | C O R P O R AT E G O V E R N A N C E 1 2 7 | N O V A R T I S G R O U P F I N A N C I A L R E P O R T

left: Group Overviewright: News in 2006

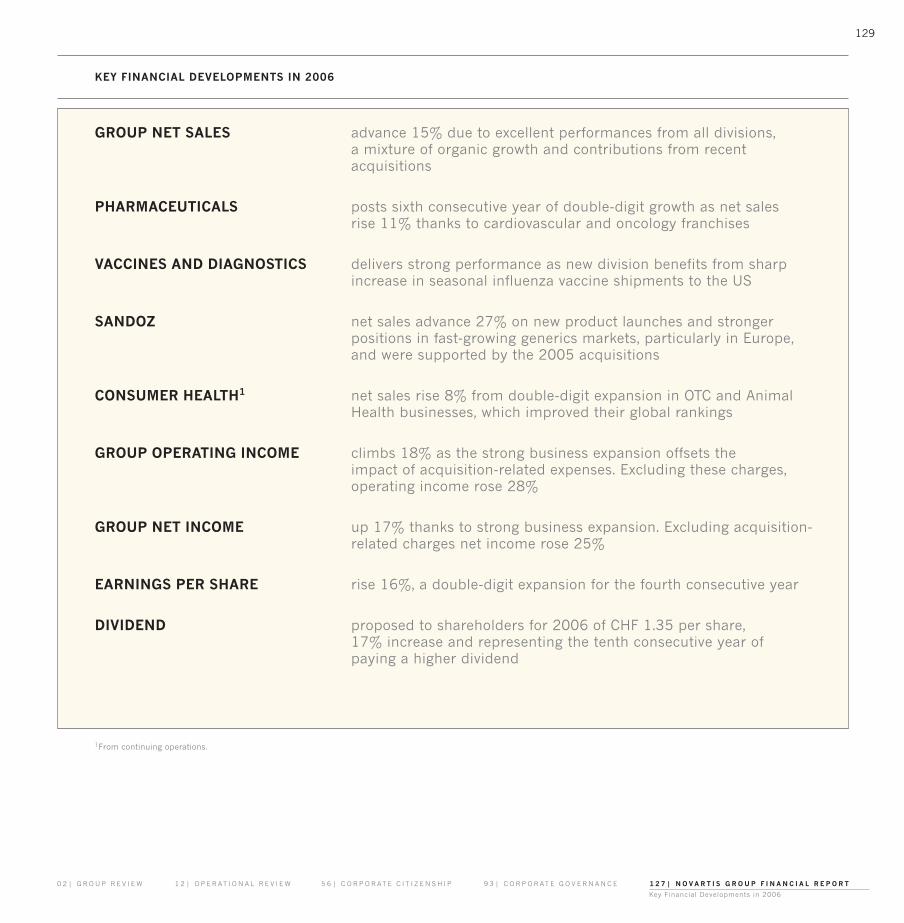

GROUP Dynamic 2006 performance from all divisions thanks to a mixture oforganic growth and contributions from recent acquisitions. Group netsales up 15% (+14% in local currencies) to USD 37.0 billion, led byPharmaceuticals. Operating income advances 18% as strong organicgrowth more than offsets acquisition-related costs.

PHARMACEUTICALS Market share gains and double-digit growth in Cardiovascular andOncology franchises drive 11% (+11% lc) net sales increase to USD 22.6 billion. Operating income improvement of 11% despite one-time acquisition costs; up 17% excluding these charges.

VACCINES AND DIAGNOSTICS New strategic growth platform created following Chiron acquisition,making Novartis the world’s second-largest supplier of influenza vaccines in the US. Double-digit net sales growth following April 2006 acquisition.

SANDOZ Sandoz integration of Hexal and Eon Labs largely completed, perform-ing well as sales up 27% (+25% lc) on good underlying retail genericsgrowth. Operating income rises sharply on operational improvements.

CONSUMER HEALTH OTC and Animal Health climb in global rankings thanks to strategicbrands, targeted acquisitions and product innovations. Medical Nutrition, with 2006 sales of approximately USD 1.0 billion, to bedivested during 2007. Net sales, excluding Medical Nutrition, rise 8% (+8% lc) while operating income advances 12%.

PIPELINE One of the industry’s strongest pipelines, with 138 projects in development, focusing on areas of high unmet need. Key R&D areasare cardiovascular/metabolic conditions, oncology and neuroscienceas well as respiratory and infectious diseases.

RESEARCH New discovery approaches and focus on biotechnology compounds at Novartis Institutes for BioMedical Research lead to increase innumber of early-stage projects.

CORPORATE CITIZENSHIP Novartis access-to-medicine programs for those in need reach 33.6 million patients in 2006 through contributions valued at USD 755 million.

DIVIDEND Proposal to shareholders for 2006 of CHF 1.35 per share, an increase of 17% and representing the tenth consecutive year of paying a higher dividend.

NEWS IN 2006

119863_Nova_000_000_web_e.qxp 24.1.2007 13:19 Uhr Seite 3

4

N O V A R T I S G R O U P B U S I N E S S R E V I E W

R H E U M A T O L O G Y S C I E N T I F I C R E S E A R C H I N S T I T U T E ; M O S C O W , R U S S I A

119863_Nova_000_000_web_e.qxp 24.1.2007 13:19 Uhr Seite 4

5

0 2 | G R O U P R E V I E W 1 2 | O P E R AT I O N A L R E V I E W 5 6 | C O R P O R AT E C I T I Z E N S H I P 9 3 | C O R P O R AT E G O V E R N A N C E 1 2 7 | N O V A R T I S G R O U P F I N A N C I A L R E P O R T

Letter from Daniel Vasella

D A N I E L V A S E L L A , M . D .

DEAR SHAREHOLDERS:

It gives me great pleasure in our eleventh busi-ness year to report another set of recordresults.

• Group net sales rose 15% (+14% in localcurrencies) to USD 37 billion

• Operating income advanced 18% to USD8.2 billion

• Net income grew 17% to USD 7.2 billion• Earnings per share (EPS) were up 16%• Free cash flow reached USD 4.3 billion

This outstanding performance reflects ourcontinuous focus on innovation and building abroad portfolio around growth areas of thehealthcare sector. Ultimately, the skills andcommitment of our associates are the key fac-tors for our success, and I would like to thankthem for their contributions.

The pharmaceutical industry is confrontedwith conflicting trends. Demand is continu-ally rising for healthcare services, medicines,vaccines and diagnostics, which is generatinghigher costs that in many countries areincreasingly the focal point of political andsocial debate. Studies have repeatedly proventhat appropriate use of medicines generallyreduces treatment costs and also that themajority of healthcare cost increases are gen-erated in hospitals. However, the pharmaceu-tical industry remains the primary target in thecost debate even though medicines accountfor only 10% to 20% of overall costs, depend-ing on the country.

Still, the healthcare sector will remain adynamic growth area in the future driven bythe following trends:

• The aging of the world’s population contin-ues unabated, generating steadily increas-ing demand for medicines due to the risingincidence of degenerative diseases andcancer as people grow older. The approach-ing wave of retirements in the post-war

“baby boomer” generation will further stimu-late demand in our most important markets.

• The strong economic expansion in popu-lous countries such as China, India andRussia is translating into over-proportionalgrowth in demand for healthcare services.Accompanying this economic growth hasbeen the increasing adoption of lifestylestypical of affluent, industrial countries. That, in turn, has led to a higher incidenceof obesity, chronic cardiovascular disease,diabetes, cancer and lung diseases.

• Finally, new technologies are enabling thediscovery and development of innovativemedicines for patients suffering from otherwise untreatable diseases.

At the same time, our industry faces chal-lenges ranging from government price controlsand intensified competition to increasinglystringent regulatory controls that are escalat-ing the costs of Research & Development.Product liability risks, which can be very cost-ly, are another important factor that is attract-ing a great deal of attention and fueling fun-damental distrust of the industry.

The most far-reaching cost reduction meas-ures taken by various governments includepromoting greater use of generic pharmaceu-ticals, sales of which are likely to experiencedouble-digit growth in the coming years asopposed to the anticipated single-digit growthforecast for patent-protected medicines.

In these industry conditions, “business asusual” is no longer a viable long-term option.Identifying and addressing the needs ofpatients remains at the forefront of all that wedo. This includes taking a serious look at theeconomic and political realities in whichpatients live because this plays a major role indetermining how products are made availableto them. This is why our business portfolio sys-tematically reflects the dynamically changinghealthcare market: growing demand for inno-

119863_Nova_000_000_web_e.qxp 24.1.2007 13:19 Uhr Seite 5

6

N O V A R T I S G R O U P B U S I N E S S R E V I E W

vative medicines (Pharmaceuticals), the risingsupport for greater use of cheaper generics(Sandoz), the increasingly prominent role ofvaccines (Vaccines and Diagnostics) and greaterempowerment of patients (Consumer Health).

We have the best portfolio to optimally lever-age growth opportunities in healthcare in theinterest of both our customers and sharehold-ers while also reducing risks.

Novartis has defined the following strategic ini-tiatives:

• Invest vigorously in R&D to continue bringingnew and innovative products to the market

• Strengthen the Sandoz generics business,which provides affordable treatmentoptions following the expiry of patents

• Expand businesses with synergy potential,such as between Pharmaceuticals, OTC andAnimal Health

• Further build our new growth platform inVaccines and Diagnostics by focusing onpreventive medicine

We sharpened our focus on these priorities in2006, which resulted in the healthcare busi-nesses now accounting for 96% of total netsales compared to just 45% in 1995.

Pharmaceuticals is our most importantdivision, again growing faster than the mar-ket. Strong demand for our top cardiovascularand oncology drugs led the performance.Sales growth in the US and in emerging mar-kets such as China and Russia were particu-larly dynamic, with the performance in Europeless robust. The extraordinary success of ourantihypertensive medicine Diovan is poised tocontinue its dynamic growth. Our cancer ther-apy Gleevec/Glivec generated sales of overUSD 2.5 billion in only its fifth year. Two othercancer medicines, Zometa and Femara, havealso developed well.

Vaccines and Diagnostics enjoyed impres-sive growth, with the integration of the newlyacquired Chiron business proceeding smooth-ly and the successful resolution of qualityproblems in influenza vaccine production. Ournew cell culture production technology forinfluenza vaccines could save lives in the eventof a pandemic flu outbreak due to the shorterlead times. A new seasonal influenza vaccinebased on this technology was submitted forEuropean approval in 2006. New diseases,such as avian flu and SARS as well as resistantbacterial and fungal infections, will continue togenerate strong demand in the future for newvaccines and medicines.

Sandoz expanded its retail generics business,particularly in the US, Eastern and SouthernEurope, Russia, Switzerland, Canada, and Aus-tralia. In Germany, the impact of severe pricepressure was felt. Our recombinant growthhormone Omnitrope became the first follow-on version of an approved biotechnology drugto be granted US and European approvals.Given the large number of biotechnologydrugs already without or set to lose patent pro-tection in the coming years, these so-called“biosimilars” are expected to play an increas-ingly important role by providing patients withaffordable, safe and effective alternatives to theoriginal treatments.

The Consumer Health Division performedvery well as the OTC and Animal Health busi-nesses each posted double-digit net salesgrowth. In line with our continued focus onhealthcare, we signed a definitive agreementto divest the Medical Nutrition business. I amconvinced this transaction is an ideal solutionfor Medical Nutrition, one that offers the man-agement and associates of this business thebest future prospects. Proceeds from thetransaction will further strengthen our financialposition and provide greater strategic flexibility.

Of course, the successes of our businessesdepends not only on strategic objectives butalso in executing them successfully, particu-larly in R&D.

We are planning to launch several innova-tive medicines during the next two yearsand will keep investing vigorously in R&D.We will also further complement our own R&Dprograms through alliances and collaborationsfor development compounds and cutting-edgetechnologies.

Novartis has 138 projects in clinical devel-opment. Among these are 50 new molecularentities (NMEs) and 88 life-cycle managementprojects with new indications or formulations.In 2006, over 20 new projects were added tothe pipeline. Key areas of R&D are cardiovas-cular/metabolic diseases, cancer and neuro-logical conditions as well as respiratory andinfectious diseases.

Shortly before the end of 2006, we receivedapproval from the US Food and Drug Admin-istration (FDA) for Exforge (valsartan andamlodipine), a single-tablet combination of thetwo most prescribed antihypertensives in theirrespective classes, and expect Europeanapproval to follow during the course of thisyear. We also anticipate regulatory decisions in2007 for two other important medicines: Tekturna/Rasilez (aliskiren), a renin inhibitorfor the treatment of hypertension, and Galvus(vildagliptin), a once-daily oral treatment forpatients with type 2 diabetes. The US regula-tory agency extended its review after recentlyavailable data for both Tekturna/Rasilez andGalvus were submitted to clarify open ques-tions. Delays are unfortunately part of ourindustry and inherent in the R&D process.

For two other development compounds, thesubmissions for US and European regulatoryapprovals were accelerated and completedearlier than planned in 2006. Tasigna (nilo-

119863_Nova_000_000_web_e.qxp 24.1.2007 13:19 Uhr Seite 6

7

0 2 | G R O U P R E V I E W 1 2 | O P E R AT I O N A L R E V I E W 5 6 | C O R P O R AT E C I T I Z E N S H I P 9 3 | C O R P O R AT E G O V E R N A N C E 1 2 7 | N O V A R T I S G R O U P F I N A N C I A L R E P O R T

Letter from Daniel Vasella

tinib) is a new treatment option for patientswith certain forms of chronic myeloid leukemiawho have resistance and/or intolerance totreatment with our Gleevec/Glivec, while Aclasta/Reclast (zoledronic acid) is a conven-ient once-yearly infusion lasting only 15 min-utes as a treatment for women with post-menopausal osteoporosis.

Among the many innovative compounds inlate-stage development at Novartis, I would liketo particularly highlight FTY720 and RAD001.

FTY720 (fingolimod) is seeking to become thefirst oral once-daily therapy for patients withrelapsing multiple sclerosis, a condition esti-mated to affect more than 2.5 million patientsworldwide and women at twice the rate asmen. This compound is now in the final stageof development after an earlier Phase II trialshowed positive results during two years oftreatment in helping patients with this poten-tially debilitating neurological condition. Sub-mission is on track for 2009.

RAD001 (everolimus) is a novel oral com-pound in development to inhibit a cell signal-ing pathway called mTOR considered to be animportant therapeutic target in oncology. Ateffective and well-tolerated doses, RAD001 hasdemonstrated broad clinical activity in patientswith various tumor types. This compound actsby directly inhibiting both the growth of tumorcells as well as the formation of new blood ves-sels (angiogenesis). If positive results areachieved in clinical trials with difficult-to-treatforms of cancer, the first regulatory submis-sions could be submitted as early as 2008.

The Novartis Institutes for BioMedical Research(NIBR), created four years ago to strengthen thecompany’s long tradition in drug discovery, isbolstering the pipeline through new discoveryapproaches and an increasing focus on biotech-nology compounds. We are expanding our exist-ing development activities in China by estab-

lishing an integrated R&D institute in Shanghaithat will focus on diseases particular to theregion, such as liver cancer. This is not a “typi-cal” China investment focused on cost savingsbut one aimed at gaining access to the coun-try’s vast talent pool and scientific promise. Thechoice of Shanghai reflects the vitality and eco-nomic potential of this city and the changingglobal economy; it is imperative to have a stronglocal presence in this fast-growing environment.

Novartis has been rapidly advancing itspipeline by complementing internal effortswith collaborations and targeted acquisitions.Last year, we acquired the UK biopharmaceu-ticals company NeuTec and added two com-pounds – Mycograb for fungal infections andAurograb for bacterial infections – that will fur-ther strengthen our presence in the fast-grow-ing hospital infections segment.

Let me close by offering some perspectives onthe challenges facing the pharmaceuticalindustry and how we are addressing the sig-nificant social and political changes underway:

Innovation is our core activity. We must notallow the challenging political environment todistract us from our ultimate goal: discovering,developing and quickly bringing to the marketnew drugs with real therapeutic benefits toboth individual patients and to society. Thepharmaceutical industry is not without criticism,but thanks to the important contributions ofmedicines and vaccines, many infectious diseases can now be prevented or effectivelytreated. Survival rates for children sufferingfrom cancer have doubled in the last 25 years,while the incidence of strokes and heart attackshave been significantly reduced. Novartis medicines – from Gleevec/Glivec and Neoral toCoartem and Clozaril/Leponex – have positivelychanged the lives of thousands, if not millions,of patients around the world. These patientshave benefited enormously from the successof our industry and also Novartis.

Intellectual property rights are central to theeconomy. Without them, many of the breath-taking technological developments since theIndustrial Revolution would not have occurred.Protecting innovation is the best protection forpatients, laying the foundation for the massiveinvestments made by the pharmaceuticalsindustry in R&D that are vital to medicalprogress. Novartis will continue to resist thepressure to soften its position on the need tovigorously protect intellectual property in favorof short-term political gain.

Reputation is valuable capital in the form oftrust, but a resource that cannot be stockpiled.It must be earned daily. Novartis enjoys anexcellent international reputation. However, wemust better explain to the public the positiveimpact of our industry, how it functions, thebenefits of our products for society and therelationship between risk, reward and innova-tion. Our industry has failed to communicateeffectively on the substantial role medicinesplay in reducing overall healthcare costs. Itwould be a serious setback if the demand forinnovative medicines continues but without anunderstanding that innovation requires enor-mous investments and risks – in other words,that innovation has its price.

Corporate citizenship is taken seriously atNovartis and is an integral component of ourbusiness strategy. Our access-to-medicine programs in 2006 reached over 33 millionpatients worldwide, with contributions totalingUSD 755 million. This represented some 2%of our total Group net sales donated to disad-vantaged patients.

The Novartis Institute for Tropical Diseases inSingapore has expanded its research activitiesto include malaria along with tuberculosis anddengue fever, diseases that are still troublingand common in developing countries. Wedecided in 2006 to sharply reduce the averagetreatment price of Coartem, the most effective

119863_Nova_000_000_ih_e.qxp 25.1.2007 10:34 Uhr Seite 7

8

N O V A R T I S G R O U P B U S I N E S S R E V I E W

anti-malaria drug, to USD 1.00 – a loss-mak-ing activity for us. More than 60 million treat-ments were delivered to endemic countrieslast year, a dramatic increase from only fourmillion in 2004 due to our expanded produc-tion capacity.

We are doing what we believe is right: helpingpatients in need while also strengthening ourposition as a reliable partner in the health sec-tor. At the same time, corporate citizenshipalso calls for a strong sense of reality, and thismeans rejecting overblown expectations ofsome stakeholders. We cannot assume theresponsibilities of governments. Well-func-tioning access-to-medicine programs requiregovernments to create the appropriate infra-structure and distribution networks, providelegal certainty and a safe environment – all ofwhich we cannot provide. This can only beachieved through the collaboration of allinvolved stakeholders. It is imperative thatpharmaceutical companies, governments,international organizations and NGOs worktogether to ensure that patients in needreceive proper care.

We must overcome a culture of blaming eachother; the precarious situation in many devel-oping countries is far too serious for symbolicposturing. We are seeking an open dialoguewith all stakeholder groups, one based onmutual trust and tolerance with the aim oflong-term success – not only in access-to-medicine initiatives but also in day-to-daybusiness activities.

Strong values are critical during this time ofrapid change. Now more than ever, strong val-ues are important to hold a company togeth-er: to concentrate energies, guide decisionsand place greater focus on performance objec-tives. Our success during the last 10 years hasbeen based on such values – a consistent focuson performance and results, an open cultureand acting responsibly for patients and soci-

eties. The values of a company become par-ticularly evident during a takeover situation,where there is often a temptation to simplyabsorb the acquired company. I personally seeacquisitions – such as those during the lasttwo years involving Hexal, Eon Labs and Chi-ron – as learning opportunities and assurancethat monotony, complacency and self-satis-faction have no chance of taking hold in ourorganization.

Balancing global aspirations and localidentities is a constant task. The process ofglobalization is not a one-way street; to thinkso would be a dangerous illusion. We mustrespect local and national customs, whetherthey involve languages, cultural aspects or thelaw. At the same time, we have established andare implementing standards throughoutNovartis – particularly our Code of Conductand our Corporate Citizenship Policy andguidelines. For example, Novartis has initiateda “living wage” program to set minimum paystandards around the world for its associates.We expect similar conduct from our businesspartners. We have also set strict global envi-ronmental and safety standards, ones that arethe same at our Basel headquarters as indeveloping countries.

As a shareholder, you naturally have an inter-est in the performance of your company. Ourinnovative and risk-diversified portfolio hasdelivered strong returns when looking at shareprice gains, dividends and spin-offs. Indeed,the value of an investment in Novartis morethan tripled from January 1, 1996, to Decem-ber 31, 2006, exceeding the total shareholderreturn of most of our competitors. I am confi-dent that Novartis will continue to be suc-cessful. Since the creation of Novartis in1996, our company has been a leader ofchange and progress, not a passive observ-er. This remains the case today thanks to ourforward-looking strategy, our considerablepowers of innovation, operational excellence

and solid basic values – Novartis has what ittakes to identify future opportunities and totranslate them into commercial success.

Dr. Marc Moret, a talented leader who servedas Chairman of the Board of Directors of San-doz until the merger with Ciba-Geigy in 1996,passed away on March 17, 2006. One of hismost impressive achievements was certainlythe creation of Novartis. With a strategic fore-sight still admired today, he realized much ear-lier than others how such strong, global organ-izations could succeed in an increasinglycompetitive environment.

The skills, dedication, and integrity of our asso-ciates have enabled us to secure our placeamong the world's most respected and suc-cessful pharmaceutical companies. When itcomes to setting the strategic direction,appointing the best talent to key positions andensuring effective control, our Board of Direc-tors plays a vital role. Dr. h.c. Birgit Breuel willleave the Board at the end of her term at theAnnual General Meeting in March 2007. Wewould like to thank Dr. Breuel for her efficientand valuable contribution to the work of theBoards of both Ciba-Geigy AG and Novartis AG.

I would also like to again thank our associates,whose excellent performance during 2006enabled Novartis to achieve both another yearof record results and improve the lives ofcountless patients worldwide.

My thanks also to you, our shareholders, forthe trust you continue to place in Novartis.

Sincerely,

Daniel Vasella, M.D.Chairman and Chief Executive Officer

119863_Nova_000_000_web_e.qxp 24.1.2007 13:19 Uhr Seite 8

9

0 2 | G R O U P R E V I E W 1 2 | O P E R AT I O N A L R E V I E W 5 6 | C O R P O R AT E C I T I Z E N S H I P 9 3 | C O R P O R AT E G O V E R N A N C E 1 2 7 | N O V A R T I S G R O U P F I N A N C I A L R E P O R T

Letter from Daniel Vasella

T E M B I S A H O S P I T A L ; J O H A N N E S B U R G , S O U T H A F R I C A

119863_Nova_000_000_web_e.qxp 24.1.2007 13:19 Uhr Seite 9

10

N O V A R T I S G R O U P B U S I N E S S R E V I E W

P H A R M A C Y ; M O S C O W , R U S S I A

119863_Nova_000_000_web_e.qxp 24.1.2007 13:19 Uhr Seite 10

11

E M E R G E N C Y D E P A R T M E N T, H O S P I T A L D A S C L Í N I C A S ; S Ã O P A U L O , B R A Z I L

119863_Nova_000_000_web_e.qxp 24.1.2007 13:19 Uhr Seite 11

12

N O V A R T I S G R O U P B U S I N E S S R E V I E W

Excellent performance in our biggest and most profitable business thanks to dynamic growth and market share gains. Approvals were received for new products and indicationsaddressing the needs of patients worldwide.

Strong net sales growth of 11% (+11% lc) to USD 22.6 billion driven by many top-selling products growing at double-digit rates as well as outstanding performances in the US andpriority emerging growth markets.

Operating income rises 17% excluding one-time charges related to integration of Chironpharmaceuticals business, but up 11% to USD 6.7 billion on a reported basis, in line withsales growth.

Cardiovascular, Oncology and Neuroscience franchises all deliver double-digit net sales growth. Hypertension leader Diovan achieves USD 4.2 billion in net sales, while the Oncology drug Gleevec/Glivec tops USD 2.5 billion and Femara delivers 33% growth in localcurrencies.

2007 and 2008 set to be exciting years for new product launches, with approvals pending in the US and Europe – particularly for Exforge and Tekturna (hypertension) as well as Galvus (type 2 diabetes) and Lucentis (blindness).

One of the industry’s top-rated pipelines with six compounds moving into pivotal late-stage trials, led by FTY720 (multiple sclerosis), QAB149 (asthma and COPD), AGO178(depression), RAD001 (cancer), ABF656 (hepatitis C) and SOM230 (Cushing’s disease).

PHARMACEUTICALS

119863_Nova_000_000_web_e.qxp 24.1.2007 13:19 Uhr Seite 12

13

0 2 | G R O U P R E V I E W 1 2 | O P E R AT I O N A L R E V I E W 5 6 | C O R P O R AT E C I T I Z E N S H I P 9 3 | C O R P O R AT E G O V E R N A N C E 1 2 7 | N O V A R T I S G R O U P F I N A N C I A L R E P O R T

Pharmaceuticals

Net sales Operating income 1 Not adjusted for new IFRS accounting rules 2 Pro forma adjusted for new IFRS accounting rules

KEY FIGURES(In USD millions unless indicated otherwise)

2006 2005

Net sales 22 576 20 262Operating income 6 703 6 014Research and development 4 265 3 972Research and development

as % of net sales 18.9 19.6Free cash flow 6 501 5 968Net operating assets 13 640 8 807Additions to property,

plant & equipment1 1 135 686Number of associates at year-end 54 314 49 308

1 Excluding impact of business combinations

NET SALES AND OPERATING INCOME(Index: 2002 = 100%)

180

160

140

120

100

20021 20032 20042 2005 2006

2006

PORTFOLIO REJUVENATION(Net sales in USD millions)

20 000

15 000

10 000

5 000

0

2002 2003 2004 2005

NET SALES BY REGION

2006 2005

US 42% 40%

Europe 32% 34%

Africa/AsiaAustralia 18% 19%

Canada andLatin America 8% 7%

PHARMACEUTICALS

Launch products(0-2 years)

New products(2-5 years)

Mature brands(>5 years)

Non-patentedproducts

119863_Nova_000_000_web_e.qxp 24.1.2007 13:19 Uhr Seite 13

14

N O V A R T I S G R O U P B U S I N E S S R E V I E W

The Novartis Pharmaceuticalsclinical pipeline holds a broad stream of 138 promising future products,with 104 projects in Phase IIand beyond as of December2006, including both newmolecular entities and additional indications or formulations for marketedproducts.

Glossary of terms:

Compound Molecular entity

Generic name International Nonpropri-etary Name (INN) designated by the WorldHealth Organization (WHO)

Indication A disease or condition forwhich a particular drug is believed to bean appropriate therapy

Phase I First clinical trials in patients todetermine safety, tolerability and usuallyproof of concept

Phase II Clinical trials in patients to deter-mine dose ranging, safety and efficacy

Phase III Large clinical trials to determinedefinitive safety and efficacy in patients

Submitted In registration

Therapeutic area Project/compound Generic name Indication

Cardiovascular Galvus vildagliptin Type 2 diabetesand Metabolism Tekturna1/Rasilez1 aliskiren Hypertension

Exforge1 valsartan, amlodipine Hypertension

Diovan/Starlix valsartan, nateglinide Prevention of new-onset type 2 diabetes,NAVIGATOR2 cardiovascular morbidity and mortality

Lotrel ACCOMPLISH amlodipine, benazepril High-risk hypertension

Oncology & Tasigna1 nilotinib Chronic myeloid leukemia (CML)Hematology Tasigna1 nilotinib Gastrointestinal Stromal Tumor (GIST)

PTK7876 vatalanib Colorectal cancer, solid tumors

Gleevec/Glivec imatinib mesylate Glioblastoma multiforme

EPO906 patupilone Ovarian cancer and other solid tumors

RAD001 everolimus Renal cell cancer, pancreatic isletcell tumor and other solid tumors

SOM230 pasireotide Acromegaly, GEP9 tumors, neuroendocrinetumors, Cushing’s Disease

PKC412 midostaurin Acute myeloid leukemia (AML)

LBQ707 gimatecan Solid tumors

LBH589 – Cutaneous T-cell lymphoma,hematologic tumors

Neuroscience Comtan entacapone Parkinson’s disease

Exelon Patch rivastigmine Dementia

LIC477 licarbazepine Bipolar disorder

AGO178 agomelatine10 Depression

FTY720 fingolimod Multiple sclerosis

SAB378 – Chronic pain

Respiratory QAB149 indacaterol COPD11

MFF258 formoterol and mometasone Asthma/COPD11

NVA237 glycopyrronium bromide COPD11

Ophthalmics Lucentis12 ranibizumab Age-related macular degeneration (AMD)Dermatology Lamisil terbinafine Fungal infection of the scalp in childrenGastrointestinal & PTK787 vatalanib AMD14

Urology (ODGU)Elidel pimecrolimus Dry eye

Zelnorm/Zelmac tegaserod Irritable bowel syndrome with constipation

Zelnorm/Zelmac tegaserod Functional dyspepsia

Infectious Certican everolimus Prevention of organ rejectionDiseases, Tyzeka/Sebivo telbivudine Hepatitis BTransplantation Mycograb efungumab Severe fungal infections& Immunology

LDC300 valtorcitabine Hepatitis B(IDTI)Albuferon Albumin interferon alpha 2-b Hepatitis C

NM28316 valopacitabine Hepatitis C

Aurograb – Severe Staphylococcus aureus infections

AEB071 – Transplantation (organ rejection)

Arthritis & Bone Aclasta17 zoledronic acid Paget’s disease of the bone(AB) Aclasta17 zoledronic acid Osteoporosis

Prexige18 lumiracoxib Osteoarthritis, acute pain, primary dysmenorrhea

ACZ885 – Muckle Wells syndrome

ACZ885 – Rheumatoid arthritis

SMC021 calcitonin Osteoporosis

1 Trade name pending regulatory approval2 NAVIGATOR trial examining combination therapy of

Diovan and Starlix3 Bcr-Abl: Breakpoint cluster region-Abelson fusion protein 4 c-Kit: an important receptor tyrosine kinase protein 5 Platelet-derived growth factor receptor protein6 Co-development with Schering AG; registration strategy

under review7 Vascular endothelial growth factor receptor protein8 Mammalian target of rapamycin protein9 Gastroenteropancreatic10 Licensed from Servier; Novartis has rights in the US 11 Chronic obstructive pulmonary disease12 Approved in US; Novartis has rights outside North America13 Vascular endothelial growth factor14 Age-related macular degeneration15 Novartis plans to appeal opinion from European Medicines

Agency (EMEA) committee recommending against Europeanapproval of Zelmac

16 Idenix compound; Novartis has exercised option to license17 Zoledronic acid (5 mg) is marketed under the trade name Aclasta

in Europe and is awaiting US approval of a new trade name18 Lumiracoxib is marketed under the trade name Prexige in vari-

ous markets and is awaiting US approval of a new trade name19 Tentative approval – pending expiration of amlodipine besylate

pediatric exclusivity

119863_Nova_000_000_web_e.qxp 24.1.2007 13:19 Uhr Seite 14

15

0 2 | G R O U P R E V I E W 1 2 | O P E R AT I O N A L R E V I E W 5 6 | C O R P O R AT E C I T I Z E N S H I P 9 3 | C O R P O R AT E G O V E R N A N C E 1 2 7 | N O V A R T I S G R O U P F I N A N C I A L R E P O R T

Pharmaceuticals

Mechanism of action Formulation Planned submission dates Phase I Phase II Phase III Submitted

Dipeptidyl peptidase 4 (DPP 4) inhibitor Oral Submitted EU, US

Renin inhibitor Oral Submitted EU, US

Angiotensin-II receptor antagonist (ARB) Oral Submitted EU, (approved US)19

and calcium channel blocker

Angiotensin-II receptor antagonist (ARB) Oral >2010and insulin secretagogue

Angiotensin I converting enzyme (ACE) Oral 2009inhibitor and calcium channel blocker

Bcr-Abl3, c-Kit4 and PDGFR5 inhibitor Oral Submitted EU, US

Bcr-Abl3, c-Kit4 and PDGFR5 inhibitor Oral 2009

VEGFR7 inhibitor Oral 2007

Bcr-Abl3, c-Kit4 and PDGFR5 inhibitor Oral 2008

Microtubule depolymerization inhibitor Intravenous 2009

mTOR8 inhibitor Oral 2008

Somatostatin analogue Injection 2009

Signal transduction inhibitor Oral >2010

Topoisomerase-I inhibitor Oral >2010

Deacetylase inhibitor Oral 2008

Catechol-O-methyltransferase inhibitor Oral Submitted Japan, (approved EU, US)

Cholinesterase inhibitor Transdermal Patch Submitted EU, US

Voltage-sensitive sodium channel blocker Oral 2008

Melatonin (M1/2) receptor agonist and serotonin Oral 2008(5-HT2C) receptor antagonist

Sphingosine-1-phosphate receptor modulator Oral 2009

Cannabinoid-1 receptor agonist Oral >2010

Once-daily beta-2 agonist Inhalation 2008

Once-daily beta-2 agonist and long-acting steroid Inhalation 2008

Long acting antimuscarinic Inhalation >2010

VEGF13 blocker Intra-vitreal injection Submitted EU

Fungal squalene epoxidase inhibitor Oral Submitted US

Angiogenesis inhibitor Oral >2010

T-cell and mast cell inhibitor Eye drops >2010

5HT4-receptor agonist Oral 2007 (EU)15, (approved US)

5HT4-receptor agonist Oral 2008

Growth-factor-induced cell proliferation inhibitor Oral Submitted US, Japan, (approved EU)

Viral polymerase inhibitor Oral Submitted EU, (approved US)

Anti-HSP90 antibody Intravenous 2009 (US), (submitted EU)

Viral polymerase inhibitor Oral 2009

Long-acting interferon Intravenous 2009

Viral polymerase inhibitor Oral >2010

Anti-Staph. aureus antibody Intravenous >2010

Protein Kinase C inhibitor Oral >2010

Bisphosphonate: osteoclast inhibitor Intravenous Submitted US, (approved EU)

Bisphosphonate: osteoclast inhibitor Intravenous Submitted EU, US

Cyclo-oxygenase-2 inhibitor Oral 2007 (US), (approved EU)

Anti-interleukin-1 beta (IL-1β) antibody Injection 2009

Anti-IL-1β antibody Injection >2010

Regulator of calcium homeostasis Oral >2010

119863_Nova_000_000_web_e.qxp 24.1.2007 13:19 Uhr Seite 15

16

N O V A R T I S G R O U P B U S I N E S S R E V I E W

T R A D I T I O N A L C H I N E S E M E D I C I N E ; M A C A U , C H I N A

119863_Nova_000_000_web_e.qxp 24.1.2007 13:19 Uhr Seite 16

17

0 2 | G R O U P R E V I E W 1 2 | O P E R AT I O N A L R E V I E W 5 6 | C O R P O R AT E C I T I Z E N S H I P 9 3 | C O R P O R AT E G O V E R N A N C E 1 2 7 | N O V A R T I S G R O U P F I N A N C I A L R E P O R T

Pharmaceuticals

High blood pressure and its consequences affect one in four adults – more than a billion people worldwide – and kill more than 7 million people every year. Type 2 diabetes causes 3 million deaths annually. Both diseases remain under-diagnosed and poorly treated – but Novartis is poised to expand its broad Cardiovascular and Metabolism portfolio, offering patients and physicians break-through innovations with the potential to transform treatment.

CARDIOVASCULAR AND METABOLISM

lar and Metabolism franchise. Galvus(vildagliptin) and Tekturna1 (aliskiren) com-pleted clinical testing last year and are nowunder regulatory review in both the US andEurope for treatment of type 2 diabetes andhypertension, respectively.

“We are very confident of the efficacyand safety profiles of Galvus and Tekturna,”says Thomas Ebeling, Head of the Pharma-ceuticals Division and member of the Executive Committee of Novartis. “And weare ready to roll as soon as we receive thego-ahead from regulators.”

Both medicines have innovative mecha-nisms of action and may offer patients theadded promise of delaying, or perhaps evenpreventing, disease onset. Novartis has em-barked on major “outcome” trial programsfor Galvus and Tekturna to realize their fullmedical and commercial potential. Tekturnawas developed in collaboration with Speedel.

Outcome studies can span severalyears, involve thousands of patients and costhundreds of millions of dollars – but they areviewed as the gold standard in demonstrat-ing safety and efficacy of a drug to patientsand physicians. They also are considered thegold standard of value-for-money by cost-conscious governments, insurers and otherpayors.

“We drove Diovan success by creatingand continuously adding to outcome data,”says John Glasspool, Head of the Cardiovas-cular and Metabolism Business Franchise atNovartis. “We aim to do the same for Galvusand Tekturna, and move medical practice1 Marketed under the brand name Rasilez outside the US

US regulatory approval of Exforge in Decem-ber culminated a year packed with submis-sions and decisions for Novartis, setting thestage for a series of major launches over thenext two years.

Exforge is the first treatment for highblood pressure to combine the two mostprescribed, branded antihypertensive medi-cines in their classes – Diovan and the calci-um channel blocker amlodipine besylate.Tentative approval by the US Food and DrugAdministration will permit the launch ofExforge in September 2007, after the expi-ration of market exclusivity for amlodipinebesylate.

In an extensive clinical program involv-ing over 5 000 patients, Exforge helped up to 9 out of 10 patients reach their treat-ment goal (diastolic blood pressure under90 mm Hg, or more than a 10 mm Hg reduc-tion in diastolic pressure from baseline).That high proportion of treatment successstands in sharp contrast to the estimated 7of 10 people with high blood pressure todaywho either remain undiagnosed or fail toreach their blood pressure targets.

“Exforge offers a potential solution tomany people with high blood pressure whocurrently need two or more medicines tocontrol their illness,” says James Shannon,M.D., Head of Pharmaceutical Developmentat Novartis.

Meanwhile, two additional breakthroughmedicines from Novartis are poised to forti-fy the dynamic portfolio of the Cardiovascu-

119863_Nova_000_000_web_e.qxp 24.1.2007 13:19 Uhr Seite 17

18

N O V A R T I S G R O U P B U S I N E S S R E V I E W

forward with studies we believe will demon-strate that these novel therapies can preventand modify progression of type 2 diabetes andhypertension, and ultimately help save lives.”

The Diovan Heritage

Exforge builds upon the heritage of Diovan,the flagship antihypertensive treatmentfrom Novartis. Diovan sustained buoyantgrowth during 2006 as sales climbed 15%,to USD 4.2 billion. Already the world’s mostprescribed angiotensin receptor blocker(ARB), Diovan is expected to pass brandedamlodipine this year and become the top-selling medication for high blood pressureworldwide.

The success of Diovan has been fueledby powerful efficacy and a broad range ofapproved indications. Those multiple appli-cations reflect a comprehensive program of outcome studies involving more than 40 000 patients across the cardiovascularcontinuum.

The megatrial program delivered newresults in 2006 when the biggest clinicalstudy of an ARB to date in Japan confirmedthe efficacy of Diovan, as well as its excellentcardiovascular profile, compared to theother studied antihypertensive therapies.The JIKEI Heart Study – involving more than3 000 patients, and conducted by the JikeiUniversity School of Medicine in Tokyo – washalted early for ethical reasons after aninterim statistical analysis showed Diovanhad reduced stroke by 40%, and heart fail-ure by 46%, compared to non-ARB therapiesbeing used as comparators.

According to Professor Sebu Mochizuki,M.D., of Jikei University, Chairman of theJIKEI Heart Study executive committee, thesignificantly reduced incidence of strokeshown in the trial “will be of particular inter-

est to clinicians because there is a higherprevalence of stroke in the Japanese popu-lation than in Western society.”

Biggest Killer

High blood pressure and its consequencesaffect an estimated one in four adults – a bil-lion people worldwide. The disorder is theleading cause of risk-attributable death,accounting for more than 7 million deathsper year. One person dies somewhere in theworld from a hypertension-related diseaseevery five seconds.

“Blood pressure is very poorly con-trolled,” says Matthew Weir, M.D., Professorof Medicine at University of Maryland. Evenusing a relatively unchallenging definition ofnormal blood pressure, Dr. Weir adds, only30% of patients in the US achieve goal bloodpressure. “And America does better thananyplace else. Our friends in Europe havemuch lower percentages of people with highblood pressure under control.”

Clinical studies have clearly demon-strated that effective treatment of high bloodpressure reduces coronary and renal events,and strokes. Yet to the frustration of healthauthorities around the world, it’s a formida-ble challenge to keep patients on therapylong enough to reap those benefits.

Physicians increasingly view combina-tion therapy as an important tool to improvepatient compliance. “If you use two drugs asa single entity, as opposed to giving them asmultiple tablets, there is significantly betteradherence to therapy,” Dr. Weir says. “I thinkthis is the way we have to go in the future andI suspect that sooner or later we will see thedevelopment of triple combinations as well.”

In the Exforge clinical trial program,involving more than 5 000 people withhypertension, clinically significant blood

pressure reductions and a good safety andtolerability profile were observed. “Exforgereally starts to separate from other highlyeffective agents in treatment of poorly con-trolled patients with severe hypertension,”says Ameet Nathwani, M.D., Head of ClinicalDevelopment and Medical Affairs, Cardio-vascular and Metabolism Business Fran-chise. One example, he says, is a studywhere Exforge produced greater blood pressure reductions than treatment with acombination of lisinopril and hydrochloro-thiazide.

“We believe Exforge may become themost efficacious agent in the antihyperten-sive category,” Dr. Nathwani adds.

Promise of Galvus

An estimated 240 million people worldwidehave diabetes today, and prevalence isexpected to rise rapidly, reaching 380 mil-lion people by 2025, according to the Inter-national Diabetes Federation (IDF). Over thecoming two decades, IDF estimates that thenumber of people with diabetes in Europewill rise by 20%. Corresponding increaseswill be 50% in North America, 85% in LatinAmerica and a doubling of prevalence inAfrica and South-East Asia.

Type 2 diabetes, which accounts forabout 90% of total diabetes cases, hasemerged as a public health epidemic, caus-ing more than 3 million deaths a year. Diabetes is a leading cause of blindness inadults in developed countries, as well as the most common cause of non-accident-related amputation.

Treatment costs for diabetes account forbetween 5% and 10% of national healthcarebudgets worldwide, according to IDF. Boththe human and economic costs of the disease could be reduced by aggressive

119863_Nova_000_000_web_e.qxp 24.1.2007 13:19 Uhr Seite 18

19

0 2 | G R O U P R E V I E W 1 2 | O P E R AT I O N A L R E V I E W 5 6 | C O R P O R AT E C I T I Z E N S H I P 9 3 | C O R P O R AT E G O V E R N A N C E 1 2 7 | N O V A R T I S G R O U P F I N A N C I A L R E P O R T

Pharmaceuticals

investment in prevention – particularly earlydetection to avoid onset of diabetic compli-cations.

That isn’t happening, however, and atleast half of all people with diabetes remainunaware of their condition. Type 2 diabetes,where control of blood sugar deterioratesover time, has traditionally been associatedwith advancing age and is more common inpeople who are overweight or obese, or havea family history of diabetes. That profile ischanging, however, with younger peopleincreasingly being diagnosed with the con-dition.

Dysfunction of insulin-producing isletcells in the pancreas is a major factor under-lying type 2 diabetes, together with insulinresistance, or deterioration in the body’sability to use the insulin that islet cells man-age to produce. Normally, blood glucose ismaintained at optimal levels by an exquisitebalance between insulin – the hormone thatremoves sugar from the blood to be storedas energy in cells – and glucagon, a hormonewhich releases sugar into the blood to feedthe body’s energy requirements.

Once beta islet cells which produceinsulin and alpha islet cells that produceglucagon start failing, the usual fine controlof blood glucose is disrupted. As insulinsecretion dwindles, the usual check-and-balance on glucagon weakens. Alpha cellsare unleashed to flood glucagon into theblood and drive up glucose levels, the hall-mark of type 2 diabetes.

The mechanism of action of Galvus –inhibiting an enzyme called DPP-4 – increasesinsulin release and reduces secretion ofglucagon, improving the ability of beta andalpha islet cells to appropriately sense andrespond to sugar in the blood.

“The impact of glucagon has beenundervalued, and more and more physicians

are recognizing that maintaining theglucagon/insulin balance not only can nor-malize islet function but also have an impacton insulin resistance by peripheral utiliza-tion,” Dr. Nathwani says. “That’s one of thereasons why we are really excited by the newmechanism of action.”

Galvus – a once-daily oral agent – hasbeen evaluated both as monotherapy and incombination with other antidiabetic agents.In clinical studies involving more than 4 500patients, Galvus demonstrated significantreductions in blood sugar that were sus-tained during treatment for up to two years.

Improved tolerability also sets Galvusapart from traditional oral antidiabetic med-icines – and could help to improve currentlow levels of compliance. The majority ofpatients who receive treatment for type 2diabetes today fail to reach the target levelsfor blood glucose set by the American Dia-betes Association.

“Patients aren’t treated optimally be-cause existing drugs have significant limita-tions and aren’t well tolerated,” Dr. Shannonsays. “Patients don’t like to move onto ther-apy because all drugs, including thia-zolidinediones (TZDs), are encumbered byside effects, particularly edema and weightgain. By acting against patients when theyare trying very hard to lose weight, thosedrugs create a significant psychologicalproblem that weakens adherence to therapy.”

In one head-to-head comparison be-tween Galvus and rosiglitazone, an insulinsensitizer, patients treated with Galvus had amean reduction of body weight greater thanone kilogram; there was an overall mean dif-ference of 2.8 kilograms between the Galvusand rosiglitazone groups. This weight losswas achieved with blood sugar-lowering effi-cacy comparable to rosiglitazone.

Extended Review

Late last year, Novartis announced a three-month extension of the US regulatory reviewof Galvus after the company decided to sub-mit additional clinical data to the FDA. Theoriginal regulatory submission to the FDAhad included data from approximately2 800 patients, treated for up to 12 months,and the subsequent submission represent-ed data from an additional 1 000 patientyears of treatment with Galvus.

The submission of supplemental datacame in response to questions from the FDAabout lesions seen on the skin of some mon-keys treated with Galvus in a study request-ed by the agency. In that study, however,monkeys received doses several orders ofmagnitude higher than the proposed thera-peutic dose. The side effects hadn't beenseen in previous studies by Novartis in mon-keys given a therapeutic dose of Galvus.Moreover, there hasn't been a similar findingin any other species – or in any humanpatient treated with Galvus in clinical trialslasting up to 24 months.

“FDA has the right to extend the reviewperiod if they believe that a companyalready has in its possession sufficient datato address concerns the agency may have,”Dr. Shannon says. “We haven’t seen any-thing even resembling this in our patientstudies – that’s why we have submitted theadditional data.”

Underscoring that confidence, Novartishas embarked on a new round of clinicalstudies aiming to demonstrate the full po-tential of Galvus. A study known as GALIANT,involving more than 7 500 people in the US,is comparing safety and efficacy of Galvusand the TZD class of insulin sensitizers in areal-world, primary care setting. Important-ly, the GALIANT study will assess the impact

119863_Nova_000_000_web_e.qxp 24.1.2007 13:19 Uhr Seite 19

20

N O V A R T I S G R O U P B U S I N E S S R E V I E W

H E R S F L A N D O L D A G E H O M E ; J O H A N N E S B U R G , S O U T H A F R I C A

119863_Nova_000_000_web_e.qxp 24.1.2007 13:19 Uhr Seite 20

21

0 2 | G R O U P R E V I E W 1 2 | O P E R AT I O N A L R E V I E W 5 6 | C O R P O R AT E C I T I Z E N S H I P 9 3 | C O R P O R AT E G O V E R N A N C E 1 2 7 | N O V A R T I S G R O U P F I N A N C I A L R E P O R T

Pharmaceuticals

of Galvus in many different patient popula-tions, including the elderly, different ethnicgroups, and patients with varying degrees ofbody mass index.

GALIANT is seeking to confirm results ofa smaller study where patients receivingGalvus as monotherapy had significantreductions in blood sugar similar to levelsseen in patients treated with rosiglitazone, adrug in the TZD class.

The GLORIOUS program comprises fivestudies designed to demonstrate the diseasemodification potential of Galvus. The studieswill explore the potential of Galvus both toprevent progression to diabetes in groups athigh risk of developing the disease – as wellas to delay disease progression in peoplewho already have developed type 2 diabetes.

Like GALIANT, the GLORIOUS studieswill involve diverse patient populations. Onewill test the ability of Galvus to prevent pro-gression to type 2 diabetes in Asian patientswith impaired glucose tolerance, a major riskfactor. “Asian populations have a differentpathophysiology and a very high conversionrate to diabetes,” Dr. Nathwani says.

“We’re also looking to see if we can sta-bilize patients with type 2 diabetes byadding Galvus to metformin, the currentstandard of care,” he adds. “Most doctorsare already using metformin and this studywill provide cutting-edge information theywant. Often, combination studies only appearyears after a new medicine comes to market.”

The GLORIOUS program will seek toconfirm early indications that treatment withGalvus leads to meaningful reductions inblood pressure of patients, parallel with ben-eficial effects on blood sugar levels. “Weplan to look at a novel population of high-risk cardiovascular patients treated withGalvus. Endpoints will include both a reduc-tion in cardiovascular events, as well as

development of their diabetes,” Dr. Nathwaniexplains.

It is an area of longstanding interest.Novartis believes that preventing diabeteswill also lead to a reduction in cardiovascu-lar consequences.

In parallel, groundbreaking data is expect-ed from NAVIGATOR, an ongoing study in theDiovan megatrial program, that is exploringthe possibility of preventing progression oftype 2 diabetes and cardiovascular events inpeople with impaired glucose tolerance.

“In the VALUE study, treatment with Diovan reduced new-onset diabetes by23%,” Dr. Nathwani says. “We’re confidentthat GLORIOUS and NAVIGATOR will providedefinitive evidence that reducing new-onsetdiabetes can prevent heart attacks andstroke.”

“A Long Way to Go…”

Medicines blocking the renin-angiotensin-aldosterone system (RAAS), including ACEinhibitors and ARBs, have led to someimpressive advances in treatment of highblood pressure. “Yet current therapies havenot delivered the major reductions of cardiovascular outcomes researchers andphysicians had hoped for,” Dr. Weir says.“There is a long way yet to go.”

Part of the problem seems to be a bio-logical bypass route that, over time, circum-vents the effect of some drugs that block theoutputs of the RAAS. For several decadesresearchers have speculated that directlyinhibiting the activation point of RAAS maybe more effective. The enzyme renin is thekey activator of the RAAS.

Tekturna, the new first-in-class directrenin inhibitor from Novartis, represents thefirst new treatment approach for high bloodpressure in more than a decade.

Regulatory applications for Tekturnafiled in Europe and the US last year includ-ed data from 44 clinical trials, involvingalmost 8 000 people with hypertension.Results show Tekturna produces sustained,double-digit reductions in blood pressurebeyond 24 hours, with placebo-like tolera-bility within the expected therapeutic doserange.

In particular, clinical data presented latelast year highlighted the power of Tekturnato offer “beyond 24-hour” blood pressurecontrol during up to a full year of therapy.“Control beyond 24 hours may give doctorsconfidence that if a patient does occasional-ly miss a dose, which happens fairly often inthe real world, there would not be a bloodpressure penalty to be paid,” Dr. Weir says.“And that could be a very positive attributein selecting an antihypertensive.”

The FDA’s review of Tekturna was extend-ed by three months in December to enablethe agency to consider additional data sub-mitted by Novartis to support the safety pro-file of the new medicine. Novartis continuesto work closely with the FDA and is confidentthat the supplementary information will helpsecure approval of Tekturna in the US.

Demonstrating Concrete Benefits

A more definitive assessment of renin inhi-bition will come in the Tekturna outcomeprogram called ASPIRE HIGHER – a suite ofstudies involving more than 30 000 peoplewith high blood pressure that will be con-ducted over the coming five years. ASPIREHIGHER aims to demonstrate that Tekturnahas the potential to redefine treatment stan-dards and provide long-term benefitsbeyond blood pressure control – such aspreventing hypertension or the onset of dia-betes, and reducing cardiovascular mortali-

119863_Nova_000_000_web_e.qxp 24.1.2007 13:19 Uhr Seite 21

22

N O V A R T I S G R O U P B U S I N E S S R E V I E W

gram. “Although the science is still emerg-ing, direct renin inhibition may offer substantial benefits to patients,” says Hans-Henrik Parving, M.D., a researcher at theSteno Diabetes Center in Denmark and leadinvestigator for ALTITUDE.

Patients and physicians around theworld will be watching. “Outcome trials suchas Val-HEFT, VALIANT and JIKEI are worthgold to doctors,” says Alan Gradman, M.D.,Chief of Cardiovascular Diseases at TheWestern Pennsylvania Hospital in Pitts-burgh, Pennsylvania.

“Many patients have co-morbidities likekidney disease or a history of heart attackthat I have to consider when treating them.These outcome trials not only advance car-diovascular medicine, they help me answerkey questions about treating patients on aday-to-day basis,” Dr. Gradman adds. “Welook forward to the results of megatrials likeNAVIGATOR as well as the outcome trialsNovartis is planning for Tekturna and Galvus.”

ty and morbidity among high-risk patientsstill at an early stage of the disease.

Direct renin inhibition may offer a ben-eficial effect for both the kidney and theheart. In studies to date, Novartisresearchers have identified a dose-depend-ent increase in renal blood flow amongpatients treated with Tekturna. Resultsexpected this year from studies called AVOIDand ALOFT could give early insight into apossible protective effect of Tekturna.

Moreover, studies have shown that Tekturna reduces plasma renin activity (PRA)– and some scientists believe that loweringPRA will reduce the risk of heart attacks andkidney failure. “There is a huge hypertensivepopulation out there at risk of developingcardiovascular and renal disease,” Dr. Shan-non says. “But if there are concrete benefitsbeyond blood pressure from reducing PRA,we still have to demonstrate them in theASPIRE HIGHER program.”

One opportunity will be a study calledALTITUDE, part of the ASPIRE HIGHER pro-

119863_Nova_000_000_web_e.qxp 24.1.2007 13:19 Uhr Seite 22

23

0 2 | G R O U P R E V I E W 1 2 | O P E R AT I O N A L R E V I E W 5 6 | C O R P O R AT E C I T I Z E N S H I P 9 3 | C O R P O R AT E G O V E R N A N C E 1 2 7 | N O V A R T I S G R O U P F I N A N C I A L R E P O R T

Pharmaceuticals

R H E U M A T O L O G Y S C I E N T I F I C R E S E A R C H I N S T I T U T E ; M O S C O W , R U S S I A

119863_Nova_000_000_web_e.qxp 24.1.2007 13:19 Uhr Seite 23

24

N O V A R T I S G R O U P B U S I N E S S R E V I E W

T R A N S F U S I O N R O O M , D I A G N O S T I C A N D T H E R A P E U T I C C E N T E R O F T R A D I T I O N A L C H I N E S E M E D I C I N E , S H U G U A N G H O S P I T A L ; S H A N G H A I , C H I N A

119863_Nova_000_000_web_e.qxp 24.1.2007 13:19 Uhr Seite 24

25

0 2 | G R O U P R E V I E W 1 2 | O P E R AT I O N A L R E V I E W 5 6 | C O R P O R AT E C I T I Z E N S H I P 9 3 | C O R P O R AT E G O V E R N A N C E 1 2 7 | N O V A R T I S G R O U P F I N A N C I A L R E P O R T

Pharmaceuticals

dose, Exjade has the potential to greatlyenhance acceptance of therapy not justamong people with thalassemia, but also ironoverload in transfused patients with sicklecell disease, myelodysplastic syndromes andother rare anemias.

Leyla Agaoglu, M.D., a hematologistbased in Istanbul, Turkey, sees many peoplewith thalassemia in her practice, reflectingthe relatively high incidence of the disorderamong people of Mediterranean origin orancestry, as well as people of Asian andAfrican descent. Dr. Agaoglu calls Exjade andGlivec, the breakthrough, targeted anticancertherapy from Novartis, “the two most signif-icant advances in hematology in decades.”

Centuries of migration by people cross-ing borders in search of a better life havespread thalassemia and other transfusion-related anemias around the world – buteffective treatment hasn’t kept pace. Up totwo-thirds of the estimated 40 000 people inthe US who have iron overload as a result ofregular blood transfusions don’t currentlyreceive iron chelation therapy. If patientsdon’t receive adequate chelation, iron canaccumulate in the liver, the heart and variousendocrine organs, eventually causing organfailure, significant morbidity and early death.

Ms. Langan insists that Exjade couldmake a positive impact on many people inthe US, and around the world. As she told theFDA panel: “Children could go to sleepoverswithout fear of ridicule and their parentscould let them go without being afraid thekids would skip their medicine. Young adultswould feel more confident and accepted at

Iron overload is a potentially life-threatening disorder – a consequence of repeatedblood transfusions required to treat disorders ranging from thalassemia to sickle cell disease. The promise of Exjade is greater convenience for patients currentlyreceiving treatment – and expansion of benefits to people who haven’t previouslybeen treated.

ONCOLOGY AND HEMATOLOGY

Cathi-Jo Langan – CJ to her friends – wasborn with beta thalassemia, a disease causedby a genetic mutation that damages redblood cells.

Ms. Langan has survived thanks to regu-lar blood transfusions since the age of three– yet those repeated transfusions also have aserious side effect, a potentially fatal build-upof iron in her body. For years, she kept theiron overload under control by injecting amedicine from Novartis called Desferal.

Desferal is an iron chelator that removesexcess iron from the body. The drug is welltolerated and effective – but requires cum-bersome infusions via a portable pump thattake up to 12 hours a day, five to seven daysa week. Eventually, that lifelong regimenbecame all but unbearable to Ms. Langan.

Speaking at an open hearing at the USFood and Drug Administration, she described“pushing and pushing with all my might toget this needle into my stomach but it wouldnever penetrate, causing much aggravationand ending with me sitting on my floor, inpure desperation.”

In 2003, she joined a clinical study test-ing a new oral iron chelator from Novartis.The drug is called Exjade (deferasirox) and itis formulated as a tablet that can be dis-persed in a glass of juice or water. “I cannottell you how much Exjade has changed mylife,” Ms. Langan adds.

As the first and only once-daily oral ironchelator, Exjade is an important break-through in providing continuous protectionagainst the harmful effects of excess iron dueto blood transfusions. With a single daily

119863_Nova_000_000_web_e.qxp 24.1.2007 13:19 Uhr Seite 25

26

N O V A R T I S G R O U P B U S I N E S S R E V I E W

tial data from the US and Switzerland showthat patients who weren’t previously receiv-ing chelation therapy account for about 50%of Exjade prescription volume.

“And treatment of transfusional ironoverload could turn out to be just the begin-ning,” Mr. Epstein adds. “New studies inother disease areas may expand the numberof people who can benefit from Exjade.” Onesuch study is already underway – testingExjade in treatment of hereditary hemochro-matosis, a genetic disorder leading to abnor-mal accumulation of iron in the liver, heartand endocrine organs.

To address the needs of US patientsundergoing chelation therapy, Novartis hasimplemented a patient support program –called EPASS Complete Care. EPASSincludes features ranging from convenienthome delivery of prescription refills by amail-order pharmacy, to ongoing compli-ance programs and individual case man-agement regarding prescription reimburse-ment coverage.

Unmet medical need, and the opportu-nity for Exjade, may be even greater outsidethe US and Europe – where the majority ofthalassemic patients live, often withoutaccess to universal medical care. Writing inthe New England Journal of Medicine in2005, hematologists Deborah Rund, M.D.,and Eliezer Rachmilewitz, M.D., noted thatthalassemia is among the most commongenetic disorders worldwide. Most patientswith the disease, however, reside in less devel-oped countries where “safe transfusion” andchelation are not universally available.

“Many patients with thalassemia inunderdeveloped nations die in childhood oradolescence. Programs that provide accept-able care, including transfusion of safe bloodand supportive therapy including chelation,must be established,” the authors added.

Recognizing the medical need fordeferasirox, Novartis will work with localhealth authorities and others on a country-by-country basis to enhance access. Formost countries, this will be accomplishedthrough the Exjade brand – but for low-income patients in countries in the Indiansubcontinent and Africa, with high medicalneed and sufficient healthcare infrastructureto support treatment, Novartis will providedeferasirox through a specific brand at apreferential price.

Life-threatening Anemia

People with thalassemia have fewer redblood cells than normal and at the sametime have inherited genetic mutations thatreduce output of hemoglobin, the protein inred blood cells that carries oxygen to allparts of the body. The result is anemia thatcan be life-threatening.

Regular transfusions normalize both thenumber of red blood cells and hemoglobinlevels – but at the same time lead to excesslevels of iron which can damage the liver,heart and other parts of the body. By thetime a patient has received 10 transfusions,significant iron overload has already begun.

The body, however, has no mechanismto remove the excess iron. Desferal, the stan-dard of care in chelation, has a half-life inthe body of 20–30 minutes and must begiven by continuous infusion. Survival isexcellent if a patient takes treatment five ormore days per week – but falls off sharply ifpatients fail to comply with prolonged dailyinfusions.

Exjade, by contrast, has a half-life of 12 to 16 hours, so a single daily dose main-tains effective levels of active chelator formore than 24 hours, ensuring that there areno gaps in chelation coverage. Clinical stud-

college,” she added. “We patients wouldhave free lives, no longer tethered to a pump.And we could have less of the anger and frus-tration that we can’t get rid of right now.”

Improving on Desferal

It took 14 years of research to deliver a suc-cessor to Desferal, a medicine launchedmore than 40 years ago and derived from anatural substance originally discovered in aniron-eating bacterium called Streptomycespilosus. Novartis scientists repeatedly en-countered obstacles in their hunt for areplacement and synthesized hundreds ofmolecules before choosing a candidate com-pound called ICL670 to enter clinical testing.

The clinical studies for ICL670 – latergiven the brand name Exjade – were thelargest program ever for an investigationaliron chelator. Data involving more than1 000 patients with a broad range of under-lying diseases demonstrated that Exjade iseffective at managing and reducing bodyiron burden.

After a “priority review” which the FDAreserves for innovations that target majorunmet medical need, Exjade was approvedin November 2005 for treatment of chroniciron overload due to blood transfusions inadults and children age two and older. InAugust 2006, the European Commissionalso granted approval for Exjade in all 25member states of the European Union tohelp patients with transfusional iron over-load. By the end of 2006, Exjade was avail-able in more than 70 countries worldwide.

In its first full year on the market, Exjadeposted sales of USD 143 million. “Theuptake has exceeded our expectations andreflects the significant unmet medical needExjade is addressing,” says David Epstein,Head of Novartis Oncology. Importantly, ini-

119863_Nova_000_000_web_e.qxp 24.1.2007 13:19 Uhr Seite 26

27

0 2 | G R O U P R E V I E W 1 2 | O P E R AT I O N A L R E V I E W 5 6 | C O R P O R AT E C I T I Z E N S H I P 9 3 | C O R P O R AT E G O V E R N A N C E 1 2 7 | N O V A R T I S G R O U P F I N A N C I A L R E P O R T

Pharmaceuticals

ies consistently demonstrated that Exjaderemoves iron from the body in a dose-dependent manner.

Patients who received Exjade doses of 20 milligrams (mg) and 30 mg per kilogramof body weight had maintenance, or reduction,in body iron burden similar to that achievedwith Desferal. In clinical trials, Exjade wasshown to be generally well tolerated withmost adverse events being mild to moderatein severity, and transient in nature.

In developed countries, virtually allpatients with the severe form of thalassemiaare routinely transfused and treated for ironoverload. According to market research byNovartis, a majority of physicians anticipatethat thalassemia patients receiving Exjadewill be treated more days per year for ironoverload than at present. Moreover, the 24-hour continuous chelation coverage pro-vided by Exjade promises to make treatmenteven more effective.

Myelodysplastic Syndromes

While Exjade has the potential to improvecompliance and efficacy among peoplealready receiving chelation therapy, the med-icine is also expected to expand use of chela-tion among undertreated patients with formsof transfusion-dependent anemia.

One example is Myelodysplastic Syn-dromes (MDS), a diverse group of bone mar-row disorders that typically affect peopleover the age of 60. Estimates suggest thatmore than 200 000 people worldwide maybe affected by MDS. Blood transfusions arethe mainstay of supportive care to managesymptoms of anemia.

“But the majority of MDS patients aren’treceiving intensive chelation therapy,” saysProfessor Norbert Gattermann, M.D., Dept. ofHematology at Heinrich-Heine University in

Dusseldorf, Germany. “There is no questionwhatsoever that Exjade is a breakthrough foriron chelation in thalassemia,” Dr. Gatter-mann adds. “But we don’t yet have reliabledata telling us how much morbidity and mortality in MDS can be attributed to ironoverload.”

Ongoing research is beginning to fill thatvacuum. A study by hematologists at the University of Pavia (Italy) demonstrated thatMDS patients who were transfusion dependenthad significantly shorter survival than thosewhose conditions didn’t require transfusions.The study found that developing a secondaryiron overload had a significant, negativeeffect on the survival of transfusion-dependentMDS patients. By contrast, at the 2006 annualmeeting of the American Society of Hema-tology, physicians from the University ofBritish Columbia (Canada) presented thefirst data documenting improvement in clinical outcome in MDS patients receivingiron chelation therapy.

In May 2005, more than 30 leadinginternational hematologists met in conjunc-tion with the 8th International Symposiumon Myelodysplastic Syndromes in Nagasaki,Japan and produced consensus guidelinesfor diagnosis, monitoring and managementof iron overload in MDS. According to Dr. Gattermann, who was a participant, theNagasaki Guidelines suggest that the MDSpatients most likely to benefit from ironchelation are those in the low-risk group,with estimated median survival of five yearsor more. “They are the candidates likely todevelop clinically relevant problems of ironoverload,” he says.

Overall, Dr. Gattermann estimates thatroughly a third of all MDS patients may becandidates for iron chelation. And even asresearch advances, demographics willexpand use of chelation therapy, he adds.

“Older age groups are expanding as apercentage of the total population in indus-trialized countries – and older age groups arethe ones with a particularly high incidence ofMDS, so we’ll see increasing numbers ofMDS patients in coming years,” Dr. Gatter-mann says. “Hematologists and physicianshave been reluctant to start iron chelationtherapy because of all the trouble with com-pliance and complications associated withDesferal. But we’ll see a greater awareness ofthe iron overload problem, and more willing-ness to begin chelation therapy in the future,because Exjade makes the problem so mucheasier to treat.”

Sickle Cell Disease

Sickle cell disease is one of the most com-mon inherited anemias treated with transfu-sions. According to the US National Institutesof Health, more than 70 000 Americans suf-fer from sickle cell disease and an estimated250 000 children worldwide are born withthe disorder every year.

The underlying cause is a mutation inthe sickle cell gene – resulting in abnormal,crescent-shaped red blood cells that canhave difficulty passing through small bloodvessels. Complications range from anemiaand frequent infections, to acute chest syn-drome – a blockage of the flow of oxygen intiny vessels in the lungs – and a dramatical-ly increased risk of stroke, when misshapenblood cells block major blood vessels thatsupply the brain with oxygen.

The mutation has persisted largelybecause it confers a survival advantageagainst falciparium malaria, the most deadlyform of malaria, and the sickle cell mutationis common in people whose families comefrom sub-Saharan Africa, the Mediterraneanregion, Latin America and India.

119863_Nova_000_000_web_e.qxp 24.1.2007 13:19 Uhr Seite 27

28

N O V A R T I S G R O U P B U S I N E S S R E V I E W

In recent decades, advances in diagno-sis and treatment have transformed sicklecell disease from a pediatric affliction oftenleading to early death, to a chronic disorderwith a median life span exceeding 40 years.But improved management of the condition– particularly broader use of chronic bloodtransfusions – could offer further benefits,says Kwaku Ohene-Frempong, M.D., Profes-sor of Pediatrics at the University of Penn-sylvania and Director of the Sickle Cell Cen-ter at the Children’s Hospital of Philadelphia.

“We know that transfusions preventstrokes as well as other complications ofsickle cell disease and we are moving into anera where more and more of our patients aregoing to receive transfusions on a chronicbasis,” Dr. Ohene-Frempong adds. “But asblood transfusions grow more common, iron overload will become one of patients’biggest problems. We are excited about thepotential for Exjade to improve complianceas well as results of chelation therapy amongour patients.”

Dr. Ohene-Frempong has an intenselypersonal connection with sickle cell disease,and as one of the world’s leading authoritiesin the field he has played a key role in land-mark research projects that helped revolu-tionize diagnosis and treatment over thepast four decades. A star athlete who re-presented his native Ghana in the 1968Olympic Games, he wasn’t aware that hecarried a defective copy of the sickle cellgene until a routine physical examinationbefore the Mexico City Olympics. “There wasa lot of concern about possible effects of thehigh altitude in Mexico City on people withthe sickle cell trait,” he recalls. “Our doctorsuggested that all team members be testedand it showed that I had the sickle cell trait.”

Four years later, after Dr. Ohene-Frempong had begun medical studies at YaleUniversity, his newborn son was diagnosedwith sickle cell disease. At the time, Yaleoperated one of only two hospitals in the USthat screened newborn babies for SCD.“Hematology textbooks at the time stillclaimed that it was impossible to detect SCDin newborns,” Dr. Ohene-Frempong says.“We were lucky to have this great doctor whomade the diagnosis, put my son on penicillinprophylaxis and began to teach my wife andme about the disease.”

Today screening of newborns for sicklecell disease is required in 49 states in the USand is routinely conducted in many coun-tries in Europe. Screening is credited formuch of the improved life expectancy forpeople with the disorder in recent decades.

During a stint back home in Ghana towork on a thesis, Dr. Ohene-Frempong wasable to foster his interest in sickle cell dis-ease. Assembling data from a large urbanhospital, he was dismayed to find that onlya handful of children had been treated forsickle cell disease during the previousdecade.

“Doctors in Ghana simply didn’t makethe diagnosis and only a tiny part of the realburden of SCD was acknowledged,” hemuses. “Unlike my son, many children weredying from this disease undiagnosed – withnobody knowing what actually had killedthem.” When he returned to Yale, he switchedthe focus of his medical studies – to hema-tology, with a special focus on sickle cell dis-ease.