Nov 2014 Credit Worthiness

12

1 Department / author Department / author Assessing your customers cr edit worthiness Mike Buggy – Ri sk Underwrit ing F4G event 19th November 2014

Transcript of Nov 2014 Credit Worthiness

7/25/2019 Nov 2014 Credit Worthiness

http://slidepdf.com/reader/full/nov-2014-credit-worthiness 1/12

1

Department / authorDepartment / author

Assessing your customers credit

worthiness

Mike Buggy – Risk Underwriting

F4G event 19th November 2014

7/25/2019 Nov 2014 Credit Worthiness

http://slidepdf.com/reader/full/nov-2014-credit-worthiness 2/12

2

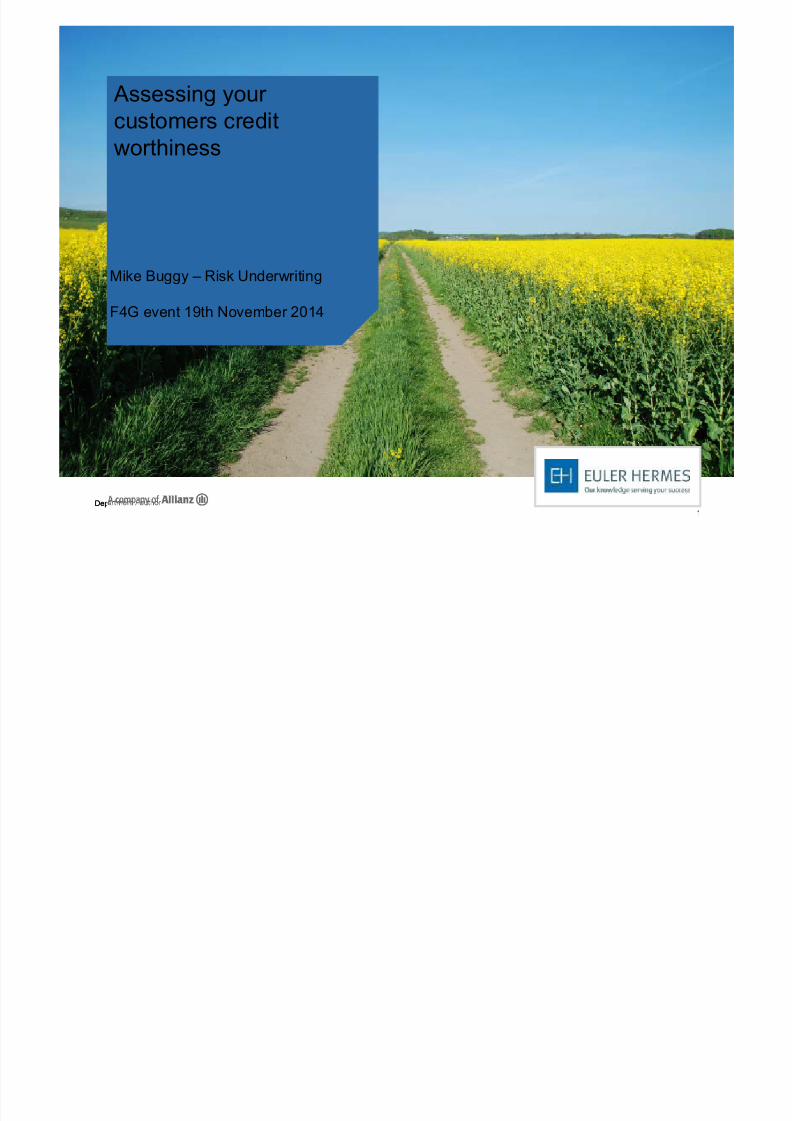

Bad Debt and Insolvency Matters...

40%of a Company’s asset

s aretypically in the form of its

outstanding sales ledger

7/25/2019 Nov 2014 Credit Worthiness

http://slidepdf.com/reader/full/nov-2014-credit-worthiness 3/12

3

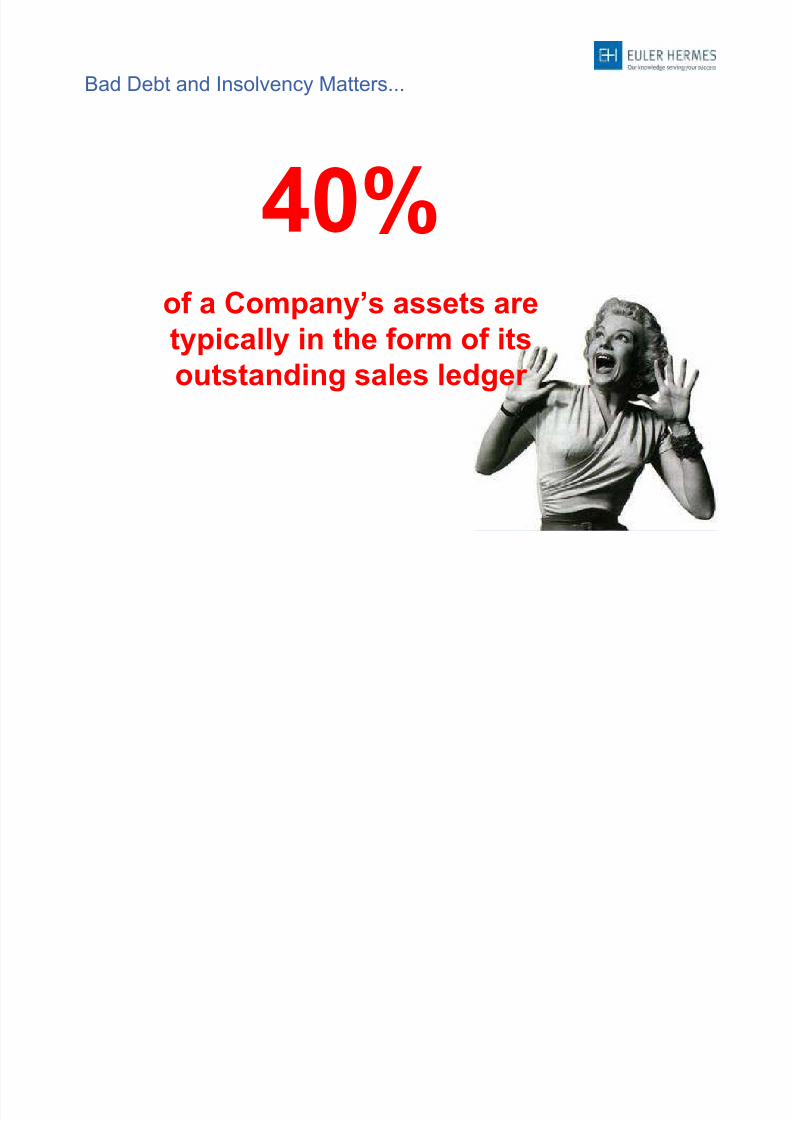

Sector and Buyer risks: the importance of Information

There is much more than financial accounts and payment experience

3

Buyer Risk

Supplier

Creditor

Pressure Unexpected

Change of

Management

Changes InSecurity

Performance

Against

Expectations

Ageing

Debtor

Profile

Acquisition/Disposal

Introduction

Of Reporting

Accountants

Deteriorating

Financial

Performance

Profits

Warning Press

Reports

Change In

Ownership

Restructuring

Change In

Funding

Structure

Increase

Cost Of Debt

Breach Of

Covenants

7/25/2019 Nov 2014 Credit Worthiness

http://slidepdf.com/reader/full/nov-2014-credit-worthiness 4/12

4

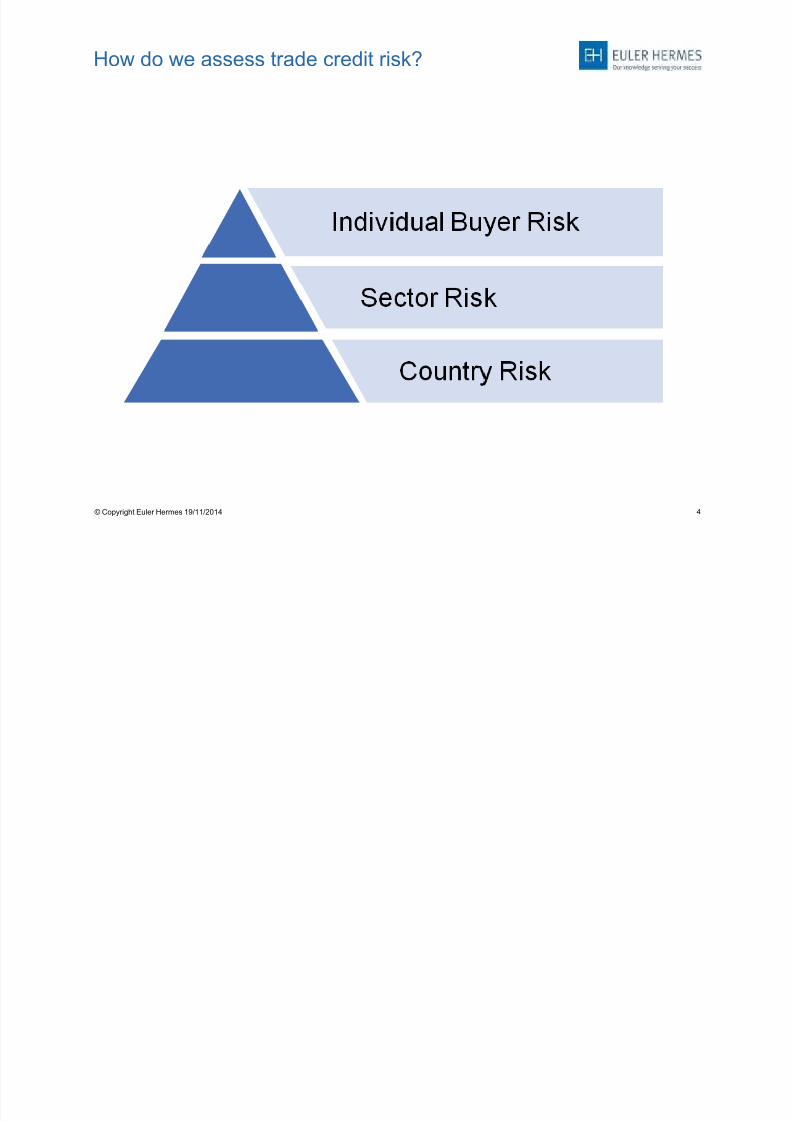

How do we assess trade credit risk?

© Copyright Euler Hermes 19/11/2014

7/25/2019 Nov 2014 Credit Worthiness

http://slidepdf.com/reader/full/nov-2014-credit-worthiness 5/12

5

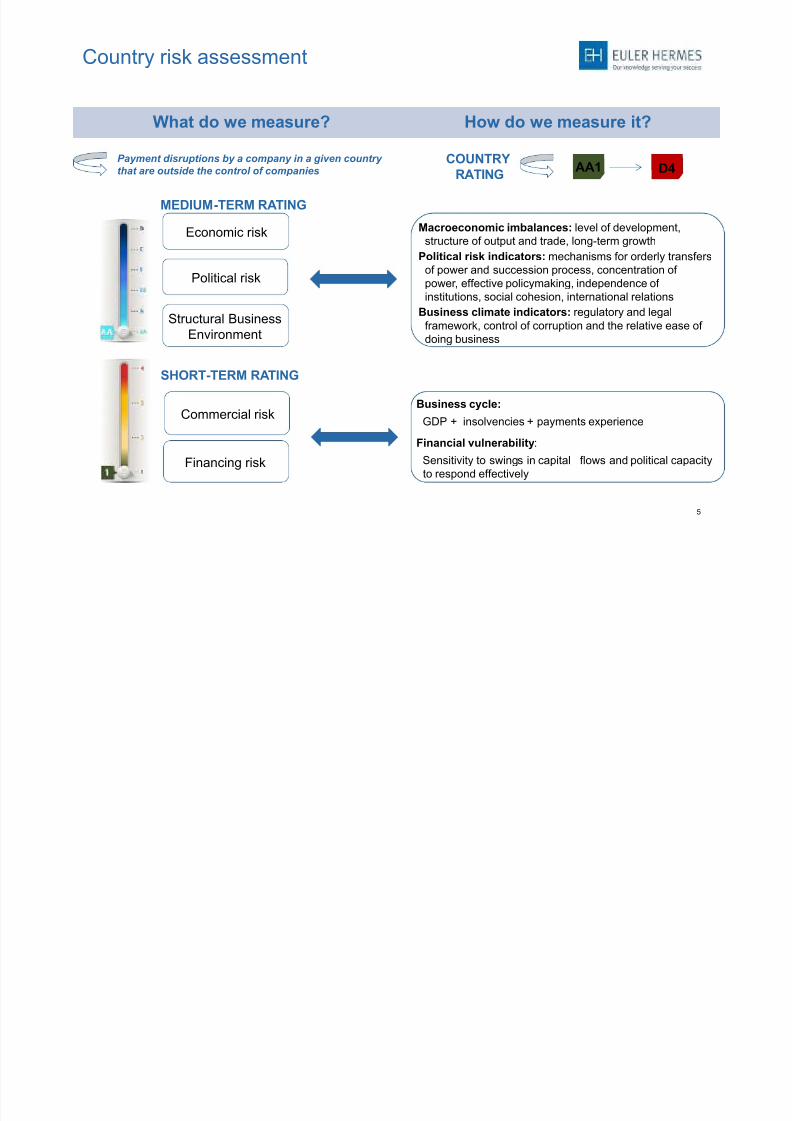

What do we measure? How do we measure it?

Economic risk

Political risk

Structural Business

Environment

MEDIUM-TERM RATING

Payment disruptions by a company in a given country

that are outside the control of companies

SHORT-TERM RATING

Commercial risk

Financing risk

AA1 D4COUNTRY

RATING

Macroeconomic imbalances: level of development,

structure of output and trade, long-term growth

Political risk indicators: mechanisms for orderly transfers

of power and succession process, concentration of

power, effective policymaking, independence of

institutions, social cohesion, international relations

Business climate indicators: regulatory and legal

framework, control of corruption and the relative ease of

doing business

Business cycle:

GDP + insolvencies + payments experience

Financial vulnerability:

Sensitivity to swings in capital flows and political capacity

to respond effectively

Country risk assessment

7/25/2019 Nov 2014 Credit Worthiness

http://slidepdf.com/reader/full/nov-2014-credit-worthiness 6/12

6

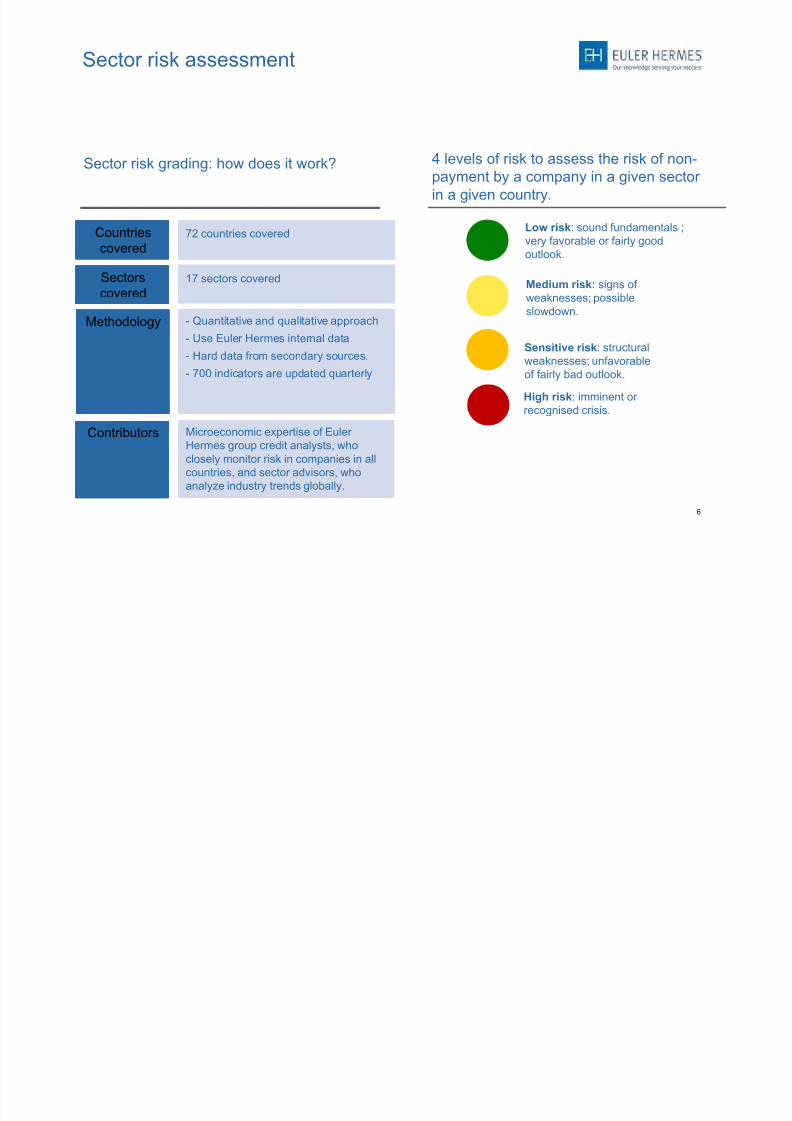

Low risk: sound fundamentals ;

very favorable or fairly good

outlook.

Sensitive risk: structural

weaknesses; unfavorable

of fairly bad outlook.

Medium risk: signs of

weaknesses; possibleslowdown.

High risk: imminent or

recognised crisis.

72 countries covered72 countries coveredCountries

covered

Countries

covered

Sectors

covered

Sectors

covered

17 sectors covered17 sectors covered

MethodologyMethodology - Quantitative and qualitative approach

- Use Euler Hermes internal data

- Hard data from secondary sources.

- 700 indicators are updated quarterly

- Quantitative and qualitative approach

- Use Euler Hermes internal data

- Hard data from secondary sources.

- 700 indicators are updated quarterly

4 levels of risk to assess the risk of non-

payment by a company in a given sector

in a given country.

Sector risk assessment

ContributorsContributors Microeconomic expertise of Euler

Hermes group credit analysts, who

closely monitor risk in companies in all

countries, and sector advisors, who

analyze industry trends globally.

Microeconomic expertise of Euler

Hermes group credit analysts, who

closely monitor risk in companies in all

countries, and sector advisors, who

analyze industry trends globally.

Sector risk grading: how does it work?

7/25/2019 Nov 2014 Credit Worthiness

http://slidepdf.com/reader/full/nov-2014-credit-worthiness 7/12

7

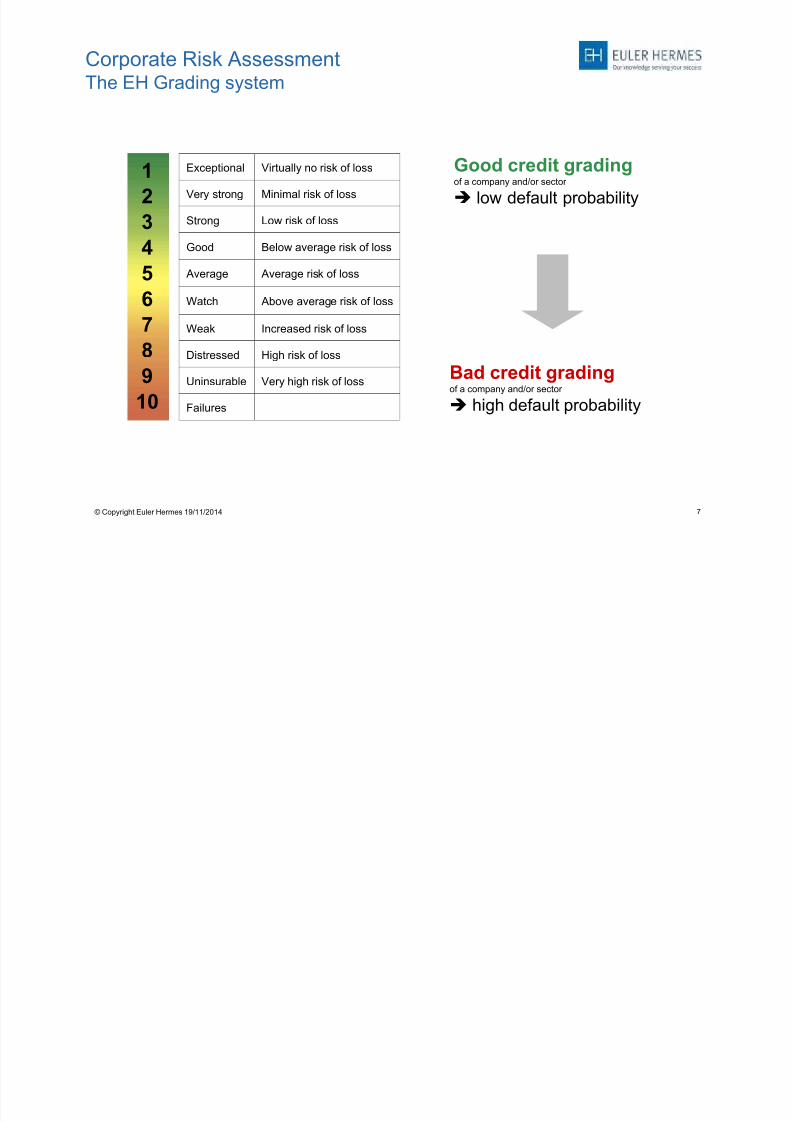

Corporate Risk AssessmentThe EH Grading system

© Copyright Euler Hermes 19/11/2014

Exceptional Virtually no risk of loss

Very strong Minimal risk of loss

Strong Low risk of loss

Good Below average risk of loss

Average Average risk of loss

Watch Above average risk of loss

Weak Increased risk of loss

Distressed High risk of loss

Uninsurable Very high risk of loss

Failures

Good credit gradingof a company and/or sector

low default probability

Bad credit gradingof a company and/or sector

high default probability

1

23

4

5

67

8

9

10

7/25/2019 Nov 2014 Credit Worthiness

http://slidepdf.com/reader/full/nov-2014-credit-worthiness 8/12

8

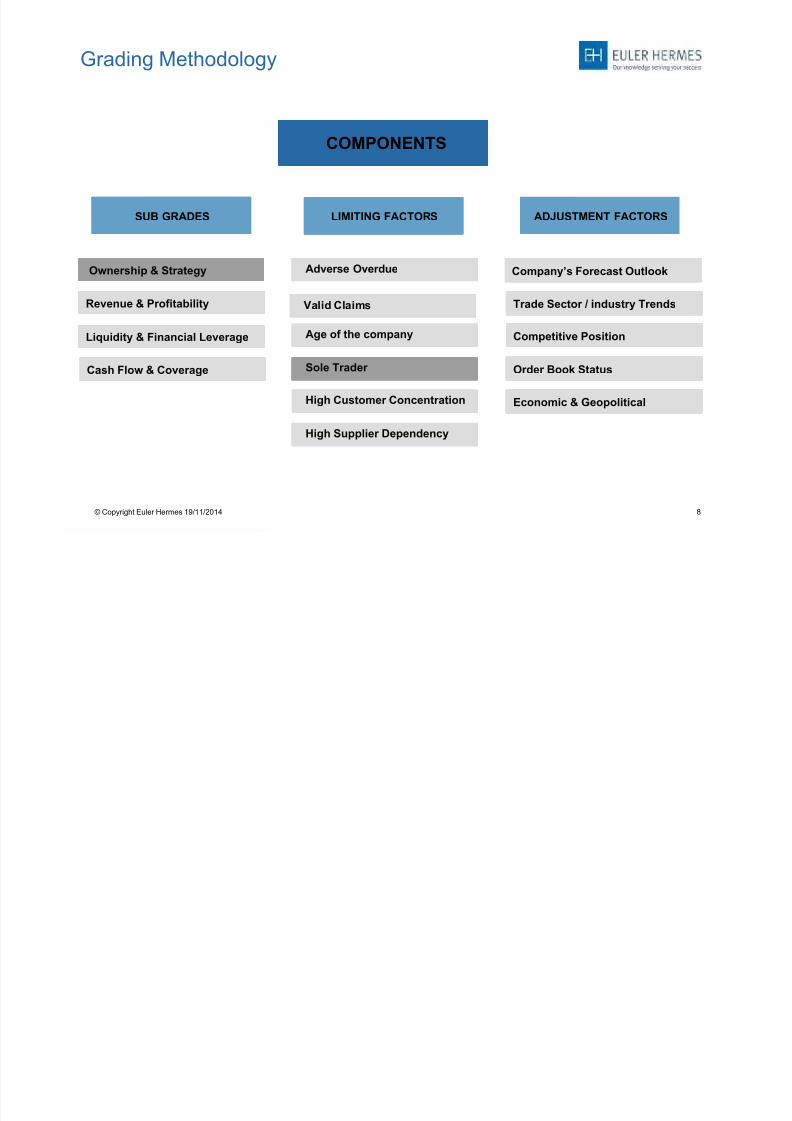

Grading Methodology

© Copyright Euler Hermes 19/11/2014

COMPONENTSCOMPONENTS

Ownership & StrategyOwnership & Strategy

Revenue & ProfitabilityRevenue & Profitability

Liquidity & Financial LeverageLiquidity & Financial Leverage

Cash Flow & CoverageCash Flow & Coverage

Adverse OverdueAdverse Overdue

Valid ClaimsValid Claims

Age of the companyAge of the company

Sole Trader Sole Trader

High Customer ConcentrationHigh Customer Concentration

High Supplier DependencyHigh Supplier Dependency

Company’s Forecast OutlookCompany’s Forecast Outlook

Trade Sector / industry TrendsTrade Sector / industry Trends

Competitive PositionCompetitive Position

Economic & GeopoliticalEconomic & Geopolitical

Order Book StatusOrder Book Status

ADJUSTMENT FACTORSADJUSTMENT FACTORSLIMITING FACTORSLIMITING FACTORSSUB GRADESSUB GRADES

7/25/2019 Nov 2014 Credit Worthiness

http://slidepdf.com/reader/full/nov-2014-credit-worthiness 9/12

9

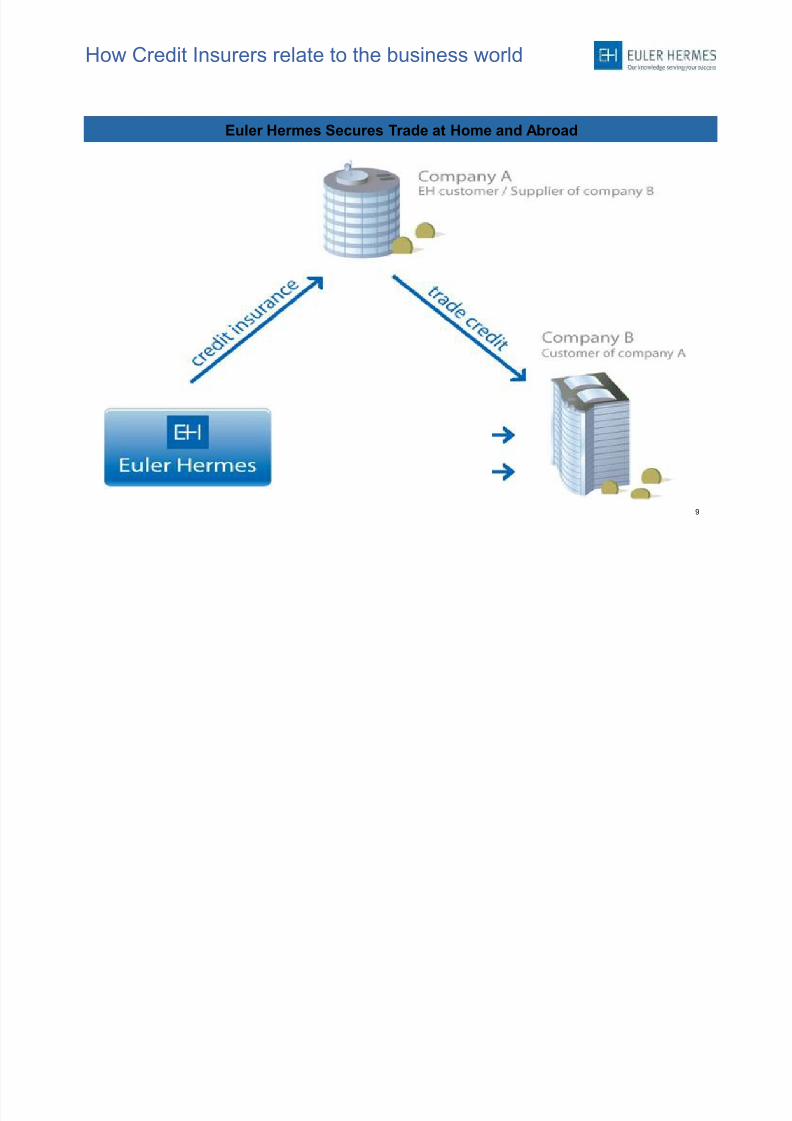

How Credit Insurers relate to the business world

Euler Hermes Secures Trade at Home and Abroad

7/25/2019 Nov 2014 Credit Worthiness

http://slidepdf.com/reader/full/nov-2014-credit-worthiness 10/12

10

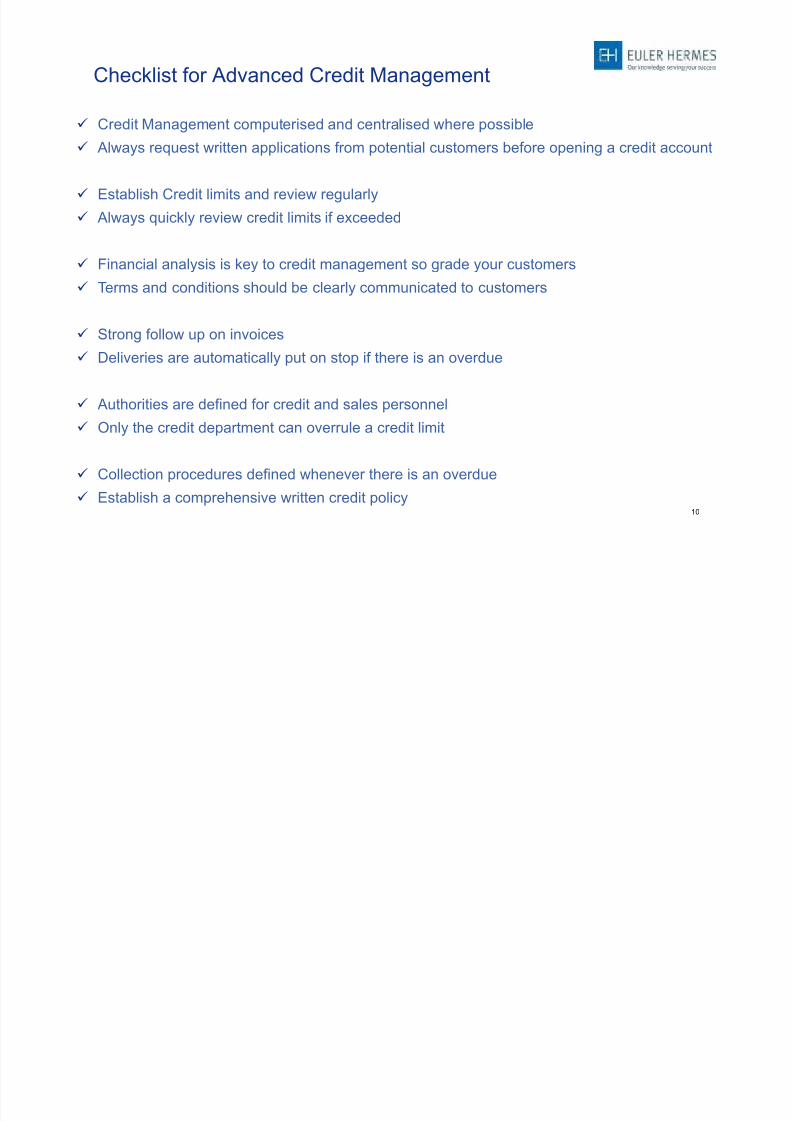

Checklist for Advanced Credit Management

Credit Management computerised and centralised where possible

Always request written applications from potential customers before opening a credit account

Establish Credit limits and review regularly Always quickly review credit limits if exceeded

Financial analysis is key to credit management so grade your customers

Terms and conditions should be clearly communicated to customers

Strong follow up on invoices

Deliveries are automatically put on stop if there is an overdue

Authorities are defined for credit and sales personnel

Only the credit department can overrule a credit limit

Collection procedures defined whenever there is an overdue

Establish a comprehensive written credit policy

7/25/2019 Nov 2014 Credit Worthiness

http://slidepdf.com/reader/full/nov-2014-credit-worthiness 11/12

11© Copyright Euler Hermes

19/11/2014

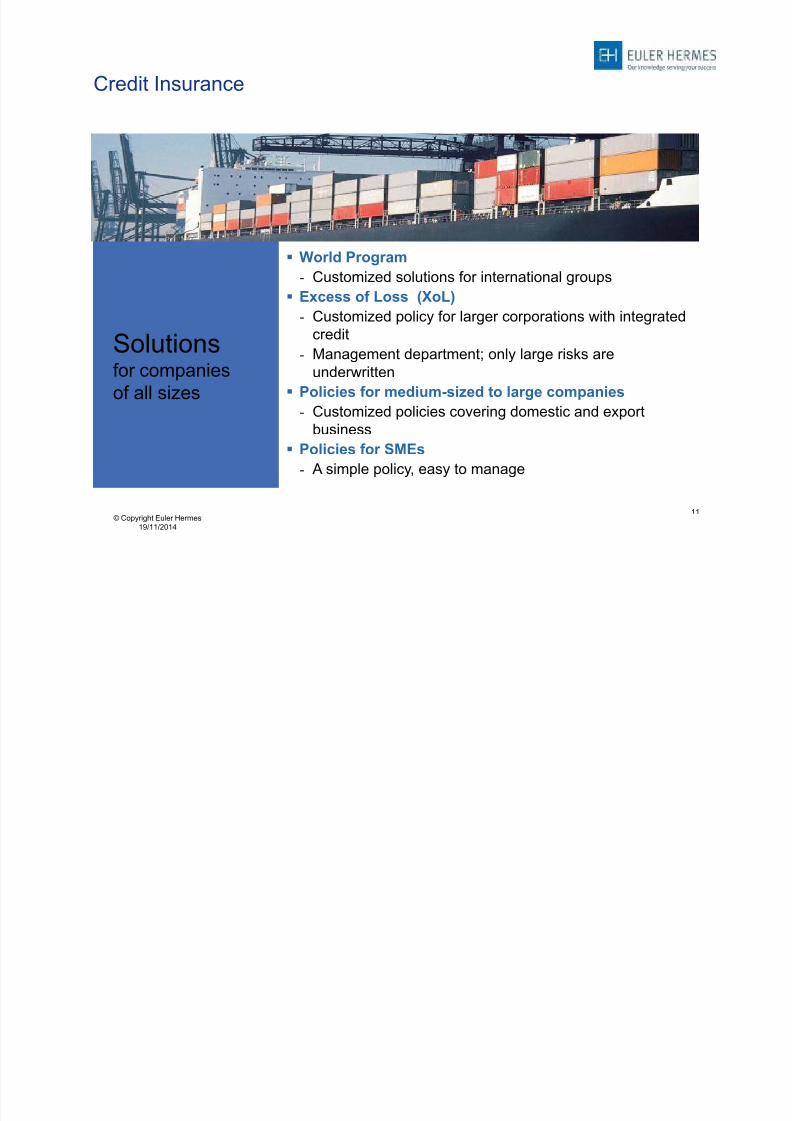

Credit Insurance

Solutionsfor companies

of all sizes

World Program

- Customized solutions for international groups

Excess of Loss (XoL)- Customized policy for larger corporations with integrated

credit

- Management department; only large risks are

underwritten

Policies for medium-sized to large companies- Customized policies covering domestic and export

business

Policies for SMEs

- A simple policy, easy to manage

7/25/2019 Nov 2014 Credit Worthiness

http://slidepdf.com/reader/full/nov-2014-credit-worthiness 12/12

12

Thank you for your attention

Find out more via our website..

Product Frequency Summary Content

Economic

Outlook

Every month Macro, sector, insolvencies,

special report

WERO Every week Know what is happening

worldwide with a shortupdate

Country Report Quarterly, 90+ a

year

Operational and risk

dimension

Economic Insight 20+ a year Short analysis on specific

topics

World Risk Map Every Quarter See country risks in seconds

Industry Reports 30+ a year Produced by group

economists or jointly with

Euler Hermes local team, we

are close to you

Or our App.. (iPhone, iPad, Android)