NOTICE CIVIL CASE COVER SHEET - Stop · PDF fileJudicial Council of California CM-010 [Rev....

59

CM-010 ATTORNEY OR PARTY WITHOUT ATTORNEY (Name, State Bar number, and address): FOR COURT USE ONLY TELEPHONE NO.: FAX NO.: ATTORNEY FOR (Name): SUPERIOR COURT OF CALIFORNIA, COUNTY OF STREET ADDRESS: MAILING ADDRESS: CITY AND ZIP CODE: BRANCH NAME: CASE NAME: CIVIL CASE COVER SHEET Complex Case Designation Limited Unlimited Counter Joinder (Amount (Amount demanded is demanded Filed with first appearance by defendant (Cal. Rules of Court, rule 3.402) $25,000 or less) exceeds $25,000) Items 1–6 below must be completed (see instructions on page 2). 1. Check one box below for the case type that best describes this case: Auto Tort Contract Provisionally Complex Civil Litigation (Cal. Rules of Court, rules 3.400–3.403) Auto (22) Breach of contract/warranty (06) Uninsured motorist (46) Other collections (09) Antitrust/Trade regulation (03) Other PI/PD/WD (Personal Injury/Property Damage/Wrongful Death) Tort Construction defect (10) Insurance coverage (18) Mass tort (40) Rule 3.740 collections (09) Asbestos (04) Securities litigation (28) Real Property Product liability (24) Environmental/Toxic tort (30) Eminent domain/Inverse condemnation (14) Medical malpractice (45) Insurance coverage claims arising from the above listed provisionally complex case types (41) Other PI/PD/WD (23) Wrongful eviction (33) Non-PI/PD/WD (Other) Tort Enforcement of Judgment Business tort/unfair business practice (07) Enforcement of judgment (20) Civil rights (08) Commercial (31) Miscellaneous Civil Complaint Defamation (13) Residential (32) RICO (27) Fraud (16) Drugs (38) Other complaint (not specified above) (42) Intellectual property (19) Judicial Review Miscellaneous Civil Petition Asset forfeiture (05) Partnership and corporate governance (21) Petition re: arbitration award (11) Employment Writ of mandate (02) Wrongful termination (36) Other judicial review (39) is 2. This case is not complex under rule 3.400 of the California Rules of Court. If the case is complex, mark the factors requiring exceptional judicial management: Extensive motion practice raising difficult or novel issues that will be time-consuming to resolve Large number of witnesses a. b. f. c. 3. Remedies sought (check all that apply): punitive a. monetary nonmonetary; declaratory or injunctive relief c. 4. Number of causes of action (specify): is is not a class action suit. 5. This case Date: (TYPE OR PRINT NAME) (SIGNATURE OF PARTY OR ATTORNEY FOR PARTY) NOTICE Plaintiff must file this cover sheet with the first paper filed in the action or proceeding (except small claims cases or cases filed under the Probate Code, Family Code, or Welfare and Institutions Code). (Cal. Rules of Court, rule 3.220.) Failure to file may result in sanctions. File this cover sheet in addition to any cover sheet required by local court rule. If this case is complex under rule 3.400 et seq. of the California Rules of Court, you must serve a copy of this cover sheet on all other parties to the action or proceeding. Unless this is a collections case under rule 3.740 or a complex case, this cover sheet will be used for statistical purposes only. Page 1 of 2 Cal. Rules of Court, rules 2.30, 3.220, 3.400–3.403, 3.740; Cal. Standards of Judicial Administration, std. 3.10 www.courtinfo.ca.gov Form Adopted for Mandatory Use Judicial Council of California CM-010 [Rev. July 1, 2007] CIVIL CASE COVER SHEET Other non-PI/PD/WD tort (35) Professional negligence (25) Other real property (26) Other petition (not specified above) (43) Other employment (15) e. d. Substantial amount of documentary evidence Large number of separately represented parties Coordination with related actions pending in one or more courts in other counties, states, or countries, or in a federal court Substantial postjudgment judicial supervision Unlawful Detainer CASE NUMBER: JUDGE: DEPT: • • • • If there are any known related cases, file and serve a notice of related case. (You may use form CM-015.) 6. b. Other contract (37)

-

Upload

nguyenhanh -

Category

Documents

-

view

213 -

download

0

Transcript of NOTICE CIVIL CASE COVER SHEET - Stop · PDF fileJudicial Council of California CM-010 [Rev....

CM-010ATTORNEY OR PARTY WITHOUT ATTORNEY (Name, State Bar number, and address): FOR COURT USE ONLY

TELEPHONE NO.: FAX NO.:

ATTORNEY FOR (Name):

SUPERIOR COURT OF CALIFORNIA, COUNTY OFSTREET ADDRESS:

MAILING ADDRESS:

CITY AND ZIP CODE:

BRANCH NAME:

CASE NAME:

CIVIL CASE COVER SHEET Complex Case DesignationLimitedUnlimited

Counter Joinder(Amount(Amountdemanded isdemanded Filed with first appearance by defendant

(Cal. Rules of Court, rule 3.402)$25,000 or less)exceeds $25,000)Items 1–6 below must be completed (see instructions on page 2).

1. Check one box below for the case type that best describes this case:Auto Tort Contract Provisionally Complex Civil Litigation

(Cal. Rules of Court, rules 3.400–3.403)Auto (22) Breach of contract/warranty (06)Uninsured motorist (46)

Other collections (09)Antitrust/Trade regulation (03)

Other PI/PD/WD (Personal Injury/Property Damage/Wrongful Death) Tort

Construction defect (10)Insurance coverage (18) Mass tort (40)

Rule 3.740 collections (09)

Asbestos (04) Securities litigation (28)Real PropertyProduct liability (24) Environmental/Toxic tort (30)

Eminent domain/Inverse condemnation (14)

Medical malpractice (45) Insurance coverage claims arising from the above listed provisionally complex case types (41)

Other PI/PD/WD (23)Wrongful eviction (33) Non-PI/PD/WD (Other) Tort

Enforcement of JudgmentBusiness tort/unfair business practice (07) Enforcement of judgment (20)Civil rights (08)

Commercial (31) Miscellaneous Civil ComplaintDefamation (13)Residential (32) RICO (27)Fraud (16)Drugs (38) Other complaint (not specified above) (42)Intellectual property (19)

Judicial Review Miscellaneous Civil PetitionAsset forfeiture (05) Partnership and corporate governance (21) Petition re: arbitration award (11)EmploymentWrit of mandate (02)Wrongful termination (36) Other judicial review (39)

is2. This case is not complex under rule 3.400 of the California Rules of Court. If the case is complex, mark thefactors requiring exceptional judicial management:

Extensive motion practice raising difficult or novel issues that will be time-consuming to resolve

Large number of witnesses a.b.

f.c.

3. Remedies sought (check all that apply): punitivea. monetary nonmonetary; declaratory or injunctive relief c.4. Number of causes of action (specify):

is is not a class action suit.5. This case

Date:

(TYPE OR PRINT NAME) (SIGNATURE OF PARTY OR ATTORNEY FOR PARTY)

NOTICEPlaintiff must file this cover sheet with the first paper filed in the action or proceeding (except small claims cases or cases filedunder the Probate Code, Family Code, or Welfare and Institutions Code). (Cal. Rules of Court, rule 3.220.) Failure to file may result in sanctions.File this cover sheet in addition to any cover sheet required by local court rule.If this case is complex under rule 3.400 et seq. of the California Rules of Court, you must serve a copy of this cover sheet on allother parties to the action or proceeding. Unless this is a collections case under rule 3.740 or a complex case, this cover sheet will be used for statistical purposes only.

Page 1 of 2Cal. Rules of Court, rules 2.30, 3.220, 3.400–3.403, 3.740;

Cal. Standards of Judicial Administration, std. 3.10www.courtinfo.ca.gov

Form Adopted for Mandatory Use Judicial Council of CaliforniaCM-010 [Rev. July 1, 2007]

CIVIL CASE COVER SHEET

Other non-PI/PD/WD tort (35)Professional negligence (25)

Other real property (26)

Other petition (not specified above) (43)

Other employment (15)

e.d.

Substantial amount of documentary evidence

Large number of separately represented parties Coordination with related actions pending in one or more courtsin other counties, states, or countries, or in a federal court Substantial postjudgment judicial supervision

Unlawful Detainer

CASE NUMBER:

JUDGE:

DEPT:

•

•••

If there are any known related cases, file and serve a notice of related case. (You may use form CM-015.)6.

b.

Other contract (37)

Auto (22)–Personal Injury/PropertyAuto Tort

case involves an uninsured motorist claim subject to arbitration, check this item instead of Auto)

Uninsured Motorist (46) (if theDamage/Wrongful Death

INSTRUCTIONS ON HOW TO COMPLETE THE COVER SHEET To Plaintiffs and Others Filing First Papers. If you are filing a first paper (for example, a complaint) in a civil case, you must complete and file, along with your first paper, the Civil Case Cover Sheet contained on page 1. This information will be used to compile statistics about the types and numbers of cases filed. You must complete items 1 through 6 on the sheet. In item 1, you must check one box for the case type that best describes the case. If the case fits both a general and a more specific type of case listed in item 1, check the more specific one. If the case has multiple causes of action, check the box that best indicates the primary cause of action. To assist you in completing the sheet, examples of the cases that belong under each case type in item 1 are provided below. A cover sheet must be filed only with your initial paper. Failure to file a cover sheet with the first paper filed in a civil case may subject a party, its counsel, or both to sanctions under rules 2.30 and 3.220 of the California Rules of Court.

To Parties in Complex Cases. In complex cases only, parties must also use the Civil Case Cover Sheet to designate whether the case is complex. If a plaintiff believes the case is complex under rule 3.400 of the California Rules of Court, this must be indicated by completing the appropriate boxes in items 1 and 2. If a plaintiff designates a case as complex, the cover sheet must be served with the complaint on all parties to the action. A defendant may file and serve no later than the time of its first appearance a joinder in the plaintiff's designation, a counter-designation that the case is not complex, or, if the plaintiff has made no designation, a designation that the case is complex. CASE TYPES AND EXAMPLES

Contract Provisionally Complex Civil Litigation (Cal. Rules of Court Rules 3.400–3.403)Breach of Contract/Warranty (06)

Breach of Rental/LeaseContract (not unlawful detainer

Antitrust/Trade Regulation (03) Construction Defect (10) Claims Involving Mass Tort (40) Securities Litigation (28) Environmental/Toxic Tort (30)

or wrongful eviction)Contract/Warranty Breach–Seller

Plaintiff (not fraud or negligence)Negligent Breach of Contract/

WarrantyInsurance Coverage Claims

Other Breach of Contract/Warranty(arising from provisionally complex case type listed above) (41)

Collections (e.g., money owed, open

Other PI/PD/WD (Personal Injury/ Property Damage/Wrongful Death) Tort

book accounts) (09)Collection Case–Seller Plaintiff

Asbestos (04)Enforcement of Judgment

Other Promissory Note/Collections

Enforcement of Judgment (20)Asbestos Property Damage

CaseAsbestos Personal Injury/

Insurance Coverage (not provisionally

Abstract of Judgment (Out of

Wrongful Death

complex) (18)

County)Confession of Judgment (non-

Product Liability (not asbestos or

Auto Subrogationtoxic/environmental) (24)

domestic relations)

Other CoverageOther Contract (37)

Medical Malpractice (45)Sister State Judgment

Medical Malpractice–Administrative Agency Award

Contractual FraudPhysicians & Surgeons

(not unpaid taxes) Petition/Certification of Entry of Judgment on Unpaid Taxes

Other Contract DisputeOther Professional Health Care

MalpracticeReal Property

Eminent Domain/InverseOther PI/PD/WD (23)

Other Enforcement of Judgment

Premises Liability (e.g., slipCondemnation (14)

Case

and fall)Wrongful Eviction (33)Intentional Bodily Injury/PD/WDOther Real Property (e.g., quiet title) (26)

Miscellaneous Civil ComplaintRICO (27)

(e.g., assault, vandalism)Writ of Possession of Real PropertyMortgage Foreclosure

Intentional Infliction of

Other Complaint (not specifiedabove) (42)

Emotional DistressQuiet TitleNegligent Infliction of

Declaratory Relief Only

Other Real Property (not eminent domain, landlord/tenant, or foreclosure)

Injunctive Relief Only (non-

Emotional DistressOther PI/PD/WD

harassment)Mechanics Lien

Non-PI/PD/WD (Other) TortUnlawful Detainer

Other Commercial Complaint

Business Tort/Unfair Business

Case (non-tort/non-complex)

Commercial (31)Residential (32)

Practice (07) Civil Rights (e.g., discrimination, false arrest) (not civil

Other Civil Complaint (non-tort/non-complex)

Drugs (38) (if the case involves illegaldrugs, check this item; otherwise, report as Commercial or Residential)

Miscellaneous Civil Petition

harassment) (08)Defamation (e.g., slander, libel)

Partnership and Corporate

(13)

Governance (21)

Judicial ReviewFraud (16)

Other Petition (not specified

Asset Forfeiture (05)

above) (43)

Intellectual Property (19) Petition Re: Arbitration Award (11)

Civil Harassment

Professional Negligence (25) Writ of Mandate (02)

Workplace Violence

Legal Malpractice Other Professional Malpractice (not medical or legal)Other Non-PI/PD/WD Tort (35)

Writ–Administrative Mandamus Writ–Mandamus on Limited Court

Elder/Dependent AdultAbuse

Case Matter

Election Contest

Writ–Other Limited Court Case

Petition for Name Change

Review

Petition for Relief From Late

EmploymentClaim

Other Judicial Review (39)Wrongful Termination (36) Other Employment (15) Review of Health Officer Order

Notice of Appeal–Labor Commissioner Appeals

Other Civil Petition

CM-010 [Rev. July 1, 2007] Page 2 of 2CIVIL CASE COVER SHEET

CM-010

To Parties in Rule 3.740 Collections Cases. A "collections case" under rule 3.740 is defined as an action for recovery of money owed in a sum stated to be certain that is not more than $25,000, exclusive of interest and attorney's fees, arising from a transaction in which property, services, or money was acquired on credit. A collections case does not include an action seeking the following: (1) tort damages, (2) punitive damages, (3) recovery of real property, (4) recovery of personal property, or (5) a prejudgment writ of attachment. The identification of a case as a rule 3.740 collections case on this form means that it will be exempt from the general time-for-service requirements and case management rules, unless a defendant files a responsive pleading. A rule 3.740 collections case will be subject to the requirements for service and obtaining a judgment in rule 3.740.

1

CORALIA OWENS 1

852 VINTAGE WAY 2

LOS ALAMOS, CA 93440. 3

SUPERIOR COURT OF CALIFORNIA 4

COUNTY OF SANTA BARBARA 5

CORALIA OWENS ) CASE NO: 6

PLAINTIFF, ) VERIFIED COMPLAINT 7

VS ) 1. DECLARATORY RELIEF 8

WORLD SAVING BANK, FSB; ) 2.BREACH OF CONTRACT 9

GOLDEN WEST SAVINGS ASSCIATION SERVICE ) 3.NEGLIGENCE 10

COMPANY; ) 4.INTENTIONAL 11

NBS DEFAULT SERVICES, LLC; ) MISREPRESENTATION 12

DOES 1-3 ) 5.WRONGFUL FORECLOSURE 13

AND ALL PERSONS CLAIMING (A) ANY LEGAL ) 6.SETTING ASIDE 14

OR EQUITABLE RIGHT, TITLE, ESTATE, LIEN, ) FORECLOSURE 15

OR INTEREST IN THE PROPERTY DESCRIBED ) 7.UNJUST ENRICHMENT 16

IN THE COMPLAINT ADVERSE TO THE ) 8.BREACH OF COVENANT OF 17

PLAINTIFF’S TITLE, OR (B) ANY CLOUD ON ) GOOD FAITH AND FAIR DEALING 18

PLAINTIFF’S TITLE OF THE PROPERTY, ) 9.CANCELLATION OF 19

DEFENDANTS, ) INSTRUMENTS 20

) 10.VIOLATION OF CALIFORNIA 21

) BUSINESS AND PROFESSIONS 22

) CODE 23

) 11.QUIET TITLE 24

Plaintiff, Coralia Owens, for her complaint against defendants allege and states as 25

follows: 26

Plaintiff, Coralia Owens, resident of P.O Box 1083 Los Alamos, California, brings the 27

civil action against the defendants seeking declaratory relief under Section 1060 of 28

the Code of Civil Procedure, unjust enrichment under Section 3426.3 of the Code of 29

Civil Procedure, breach of contract under Section 3300 of the Code of Civil 30

Procedure, breach of implied good faith and fair dealing under Section 325 of 31

2

California Civil Jury Instructions, cancellation of instruments under Sections 3412-1

3414 of the Code of Civil Procedure, violation of California business and professions 2

code under Section 17200 of the Code of Civil Procedure and quiet title under 3

section 760.020 of the Code of Civil Procedure. 4

This action arises in reference to the plaintiff’s property with the address P.O Box 5

1083, Los Alamos, California, the owner of which, Coralia Owens was finding it 6

difficult to make the mortgage payments because the mortgage payments had shoot 7

up a lot and the head of the household, J.H Owens had passed away. Shortly before 8

his death, he had incurred a lot of debt due to which they were forced into 9

bankruptcy and until that matter could have been concluded, a lien has been placed 10

upon his social security. The Los Alamos house has always been and will always be 11

very special to the plaintiff and her family as her son has been raised in that area 12

and her two grandchildren have been attending local schools there. Additionally, the 13

plaintiff’s late husband is buried nearby and their ability to visit him regularly gives 14

them comfort and a sense of wellbeing. The plaintiff believes that with her current 15

income and some financial assistance which she receives from her son it would be 16

logical and best for her to resort to a more reasonable monthly mortgage payment 17

which could keep her and her family in the family home. 18

II.GENERAL ALLEGATIONS 19

(AGAINST ALL DEFENDANTS) 20

1.The plaintiff and her family had moved from Los Alamos, CA, home in February of 21

2006 into the Portville, CA, home. In September of 2012, the plaintiff and her family 22

moved back to Los Alamos, CA, home and at time, their monthly mortgage payments 23

had jumped from $750 to $3,700. 24

2. On July 14, 2006, a Deed of Trust was made in which the borrower was J.H Owens, 25

a married man, the lender was World Savings Bank, FSB and the amount mentioned 26

herein was U.S $ 596,000.00 for which the trustee was Golden West Savings 27

Association Service Company. 28

3. On July 17, 2006, a Inter Spousal transfer deed was made which was recorded on 29

July 21, 2006. 30

4. On July 10, 2012, a Notice of Default and election to sell under Deed of Trust dated 31

3

July 14, 2006 was issued. 1

5. On November 6, 2012, A Notice of Trustee’s Sale was recorded mentioning the 2

sale date on which the auction will take place. 3

6. On April 1, 2013, the head of the household, J.H Owens had passed away. Shortly 4

before his death, he had incurred a lot of debt which forced them into bankruptcy 5

and until that matter could be concluded, a lien was placed upon his social security. 6

7. Currently, the plaintiff feels that after the death of her husband, she is being taken 7

advantage of. Since her late husband was of the generation in which the man of the 8

household would take care of most, if not all, financial decisions and her opinions 9

were never considered and many were made without consulting her or without her 10

knowledge. 11

8. Since the plaintiff’s husband passed away, the plaintiff believes that the bank is 12

taking advantage of her precarious financial position to advance its own agenda and 13

thus leaving the plaintiff in this bind. The bank has made it very clear to the plaintiff 14

that they want her to be out of her house. 15

9. The plaintiff has been working for some time with Mr. Edward Anguiano of Legal 16

Foreclosure Services, Inc., 135 W. Shaw Ave. # 106, Fresno, CA, 559-478-2928 who 17

had advised the plaintiff to discontinue making mortgage payments and a loan 18

modification was guaranteed. 19

10. Based upon her current financial distress and ongoing bankruptcy, the plaintiff 20

has been asking to reduce her monthly mortgage payments to reasonable amount of 21

$1000. 22

11. The plaintiff feels that this option of reducing her monthly mortgage payments 23

would be sustainable for her in reference to the current tax bracket she is in and 24

moneys left to her by her husband is not available to her at this time. 25

12. The plaintiff is very attached to her Los Alamos house and says that Los Alamos 26

house has always been and will be very special to her where she raised her son and 27

her two grandchildren have been attending local schools there. Plaintiff’s late 28

husband has also been buried nearby where she can visit him on a regular basis 29

which gives her comfort and sense of wellbeing. 30

4

13. Thus, the plaintiff believes that a more reasonable monthly mortgage payment 1

can keep her and her family in her family home. 2

14. It is pertinent to mention that the plaintiff had a right to get her monthly 3

mortgage payments modified. A homeowner’s submission of an application and 4

financial documentation has been held to be sufficient consideration for a promise 5

by a banking institution to modify a mortgage as held in the case of Bosque v. Wells 6

Fargo Bank, supra, 762 F. Supp. 2d at 352-353. Turbeville v. JPMorgan Chase Bank, 7

supra, 2011 U.S. Dist. 8

III.PARTIES 9

15. Plaintiff, Coralia Owens, is a citizen of Los Alamos, California. The plaintiff, now 10

and at all times relevant to this complaint was the owner of the house with an 11

address 852 Vintage way, Los Alamos, California 93440 and is commonly known as 12

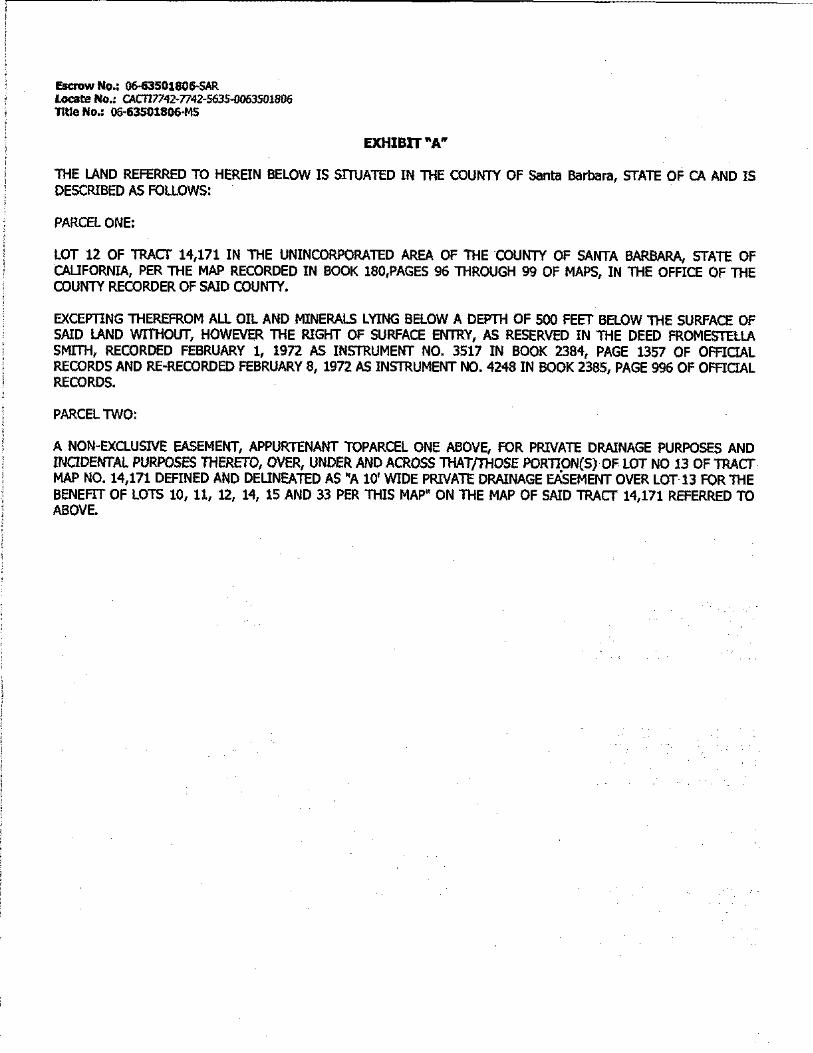

LOT 12 OF TRACT 14,171IN THE UNINCORPORATED AREA OF THE COUNTY OF 13

SANTA BARBARA, STATE OF CALIFORNIAPER THE MAP RECORDED IN BOOK 180, 14

PAGES 96 THROUGH 99 OF MAPS IN THE OFFICE OF THE COUNTY RECORDER OF 15

THE SAID COUNTY (Herein referred to as the “subject property”). The legal 16

description of the subject property is attached as Exhibit A and incorporated here 17

by reference. 18

16.Defendant, WORLD SAVINGS BANK, FSBis, and at all times relevant was, a 19

Federal Savings Bank which is organized and exists under the laws of the United 20

States with its address-1901, Harrison Street, Oakland, CA 94612. Plaintiff will 21

amend this complaint to allege its true principle place of business when ascertained. 22

17. Defendant, GOLDEN WEST SAVINGS ASSOCIATION SERVICE COMPNAY is, and 23

at all times relevant was, operating as a subsidiary of Wells Fargo Bank National 24

Association. Plaintiff will amend this complaint to allege its true principle place of 25

business when ascertained. 26

18. Defendant, NBS DEFAULT SERVICES, LLC is, and at all times relevant was, 27

National Bankruptcy Services, headquartered in Dallas, Texas was founded in 1999 28

to deliver cost effective bankruptcy servicing solutions in the lending and servicing 29

industries with its address- 301 E. Ocean Blvd. Suite 1720, Long Beach, CA 90802. 30

5

Plaintiff will amend this complaint to allege its true principle place of business when 1

ascertained. 2

19. “All Persons Unknown, Claiming Any Legal or Equitable Right, Title, Estate, Lien, 3

Or Interest In The Property Described In The Complaint Adverse to Plaintiff’s Title, 4

Or Any Cloud On Plaintiffs’ Title Thereto” are sued herein pursuant to California 5

Code of Civil Procedure Section 762.020(a). 6

20. Plaintiff does not know the true names and capacities of the defendants sued 7

herein as DOES 1-3 through, inclusive, and therefore sues said defendants by 8

fictitious names. Plaintiff is informed and based on such information and belief aver 9

that each of the defendants is contractually, strictly, negligently, intentionally, 10

vicariously liable and or otherwise legally responsible in some manner for the acts 11

and omissions described herein. Plaintiff will amend this complaint to set forth the 12

true names and capacities of each defendant when the same are ascertained. 13

21. Plaintiff is informed and believe and thereon allege that each of the defendants 14

are responsible in some manner for the pattern and practice of events herein 15

alleged, or are a necessary party for obtaining appropriate relief. In performing each 16

of the acts alleged in this complaint and in omitting to do those acts that are alleged 17

in this complaint to have been legally required, each defendant acted as an agent for 18

each and all other defendants. The injuries inflicted upon plaintiff occurred because 19

of the actions and omissions of each and all of the defendants. 20

22. WHEREFORE, plaintiff prays judgment against the defendants as set forth 21

below: 22

IV.JURISDICTION AND VENUE 23

23. The Superior Court for the State of California has jurisdiction over this action 24

due to Defendants’ violations of California Laws, including Breach of California 25

contracts and numerous violations of California Statutory provisions including 26

Business and Professions Code, Section 17200. Venue is proper in Santa Barbara 27

County because many of the contracts were entered into in Santa Barbara and much 28

of the injury to the Plaintiff’s personal property occurred in Santa Barbara County. 29

This court has the jurisdiction and the venue is proper of the claims alleged in this 30

complaint. Code of Civil Procedure section 1060 authorizes declaratory relief and 31

6

the Code of Civil Procedure Sections 1060-1060.5 governs the action. Section 3426.3 1

governs unjust enrichment, Section 3300 governs breach of contract, Sections 3412-2

3414 govern cancellation of instruments, Section 17200 governs violation of 3

California business and professions code, Section 760.020 governs an action to quiet 4

title. Breach of implied good faith and fair dealing is governed by Section 325 of 5

California Civil Jury Instructions. The right to an action for accounting and actions 6

for competition are generally governed by case laws. This civil action arises under 7

the laws of the State of California. 8

V.BACKGROUND FACTS AND FIRST CAUSE OF ACTION 9

(DECLARATORY RELIEF) 10

(AGAINST ALL DEFENDANTS) 11

24. On July 14, 2006, J.H Owens, as borrower, was induced to sign a written 12

promissory note in the amount of Five Hundred Ninety Six and 00/100 Dollars (U.S. 13

$596,000.00) plus accrued and deferred interest. A copy of the promissory note is 14

not available to attach as an exhibit to incorporate here by reference, because 15

Plaintiff was not given a final copy. 16

25. On the same day and as part of the same transaction, J.H Owens, as trustor, was 17

further induced to sign a Deed of Trust conveying the real property/subject 18

property described in paragraph 15 to defendant World Savings Bank, FSB to secure 19

payment of the principal sum and interest as provided in the note. A copy of the 20

Deed of Trust is attached as Exhibit Band is incorporated here by reference. 21

26. On July 17, 2006, an Inter Spousal transfer deed was issued which acknowledged 22

that Coralia Owens, spouse of grantor granted to J.H Owens, a married man as his 23

sole and separate property, the real property in the city of Los Alamos, County of 24

Santa Barbara, State of California which was recorded on July 21, 2006. A copy of the 25

Inter Spousal Transfer Deed is attached as Exhibit C and is incorporated here by 26

reference. 27

27. On July 10,2012, a Notice of Default and Election to sell under Deed of Trust was 28

issued stating that NBS Default Services, LLC, is either the original trustee, the duly 29

appointed substituted trustee, or acting as agent for the trustee or beneficiary under 30

a Deed of Trust dated July 14, 2006, executed by J.H Owens, a married man, as 31

7

Trustor, to secure certain obligations in favor of World Savings Bank, FSB, its 1

successors and/or assignees, A Federal Savings Bank as Beneficiary recorded on July 2

21, 2006 as Document Number 2006-0057544, of official records in the office of the 3

recorder of Santa Barbara County, California. The amount due as of July 10, 2012 is 4

$23,312.67 which will increase until the account becomes current. A copy of the 5

Notice of Default and Election to sell is attached as Exhibit D and incorporated here 6

by reference. 7

28. On November 6, 2012, a Notice of Trustee’s Sale was recorded which stated that 8

a default under a Deed of Trust dated July 14, 2006 was declared and unless no 9

action is taken to protect the subject property, it would be sold at public auction to 10

the highest bidder for cash. A copy of the Notice of Trustee’s Sale is attached as 11

Exhibit E and incorporated here by reference. 12

29. The plaintiff’s monthly mortgage payments had jumped from $750 to $3,700 13

which became difficult for her to pay because as it is a lot of debt was incurred due 14

to which they were forced into bankruptcy and her husband had passed away 15

whose money was also not available to her at this time. With her current income 16

and some financial assistance from her son, she believed that a more reasonable 17

monthly mortgage payment would let her and her family keep her family house. 18

30. The plaintiff’s rights have been enfranchised upon by not allowing her different 19

avenues of protecting or saving her home. The plaintiff did not have a fair chance to 20

save herhome as the plaintiff never got any proper assistance and was not provided 21

any options to save her house. 22

31. The plaintiff was never contacted by the defendants, on their own to inform her 23

about the method of operation for loan modification even though it is included in 24

any service provider’s duty to inform their customer about their services. Thus, the 25

Notice of Default sent to the plaintiff is invalid as it violates section 2923.5 of the 26

California Civil Procedure. 27

32. Plaintiff has no adequate and speedy remedy to resolve the parties’ dispute 28

other than by a declaratory judgment from this court. Because of the urgency and 29

importance of the issues presented by the parties’ dispute, it is necessary and 30

appropriate for the court to resolve this dispute by issuing a judicial declaration 31

8

determining the respective rights and obligations of the parties with respect to the 1

alleged agreement. 2

VI.SECOND CAUSE OF ACTION 3

(BREACH OF CONTRACT) 4

(AGAINST ALL DEFENDANTS) 5

33. Plaintiff incorporates all of the forgoing allegations in all previous paragraphs as 6

though fully set forth herein. 7

34. Defendants had failed to perform the promised services to the plaintiff failing 8

which the defendants had breached one or more provisions under the subject 9

agreements or contracts. 10

35. Pursuant to the Laws of California, the defendant’s conduct was a substantial 11

factor in causing the plaintiff irreparable harm in terms of depriving him from other 12

modus operandi to set aside foreclosure or loan modification by which they had 13

breached the terms of contract. 14

36. As a proximate result of the negligence and carelessness of Defendants as set 15

forth above, Plaintiff has suffered, and continues to suffer, general and special 16

damages. 17

37. As a consequence of Defendant’s Breach of the agreements, the plaintiff has 18

suffered damages in an amount to be proven at trial, including attorneys’ fees under 19

civil code, section 1717. 20

VII.THIRD CAUSE OF ACTION 21

(NEGLIGENCE) 22

(AGAINST ALL DEFENDANTS) 23

38. Plaintiff incorporates all of the forgoing allegations in all previous paragraphs as 24

though fully set forth herein. 25

39. At all times relevant herein all the defendants, acting as Plaintiff’s lenders and 26

servicers, owed a duty to exercise reasonable care and skill to maintain accurate 27

loan records in a proper manner and to discharge and fulfill the other incidents 28

attendant to the maintenance, accounting and servicing of loan records, including, 29

but not limited, to disclosing to Plaintiff’s the status of any foreclosure actions taken 30

by it, disclosing who owned Plaintiff’s Loan to Plaintiff, refraining from taking any 31

9

action against Plaintiff that it did not have the legal authority to do, and providing all 1

relevant information regarding the Loan Plaintiff had with them to Plaintiff. 2

40. In taking the actions as mentioned above, and in failing to take the actions as 3

mentioned above, defendants had breached their duty of care and skill to Plaintiff in 4

the servicing of Plaintiff’s loan by, among other things, failing to disclose to Plaintiff 5

that it was foreclosing on Plaintiff’s subject property, treating other defendants as 6

separate entity to confuse and mislead the Plaintiffs, preparing and recording false 7

documents, and foreclosing on the subject property without having the legal 8

authority and/or proper documentation to do so. 9

41. All the defendants had breached their duty of care and skill to Plaintiff by failing 10

to properly train and supervise their agents and employees with regard to laws of 11

California regarding the executions and recording of foreclosure documents, 12

executing the documents without the legal authority to do so; failing to follow laws 13

of California with regard to foreclosures, including, but not limited to, acting as the 14

trustee under the Deed of Trust when it did not have the legal authority to do so; 15

and taking actions against Plaintiff even when they did not have the legal authority 16

to do so. 17

42. Plaintiff is informed and believe, and on the basis of that information and belief 18

allege, that provided all the defendants had used proper skill and care in dealing 19

with the plaintiff’s matter, plaintiff might have been able to save his home without 20

facing so much of hassle. 21

43. As a direct and proximate result of negligence and carelessness on the part of the 22

defendants as mentioned above, plaintiff suffered, and continues to suffer general 23

and special damages in an amount to be determined at the trial. 24

VIII.FOURTH CAUSE OF ACTION 25

(INTENTIONAL MISREPRESENTATION) 26

(AGAINST ALL DEFENDANTS) 27

44. Plaintiff incorporates all of the forgoing allegations in all previous paragraphs as 28

though fully set forth herein. 29

10

45. Defendants have willfully concealed many facts from the Plaintiff especially with 1

regard to the loan modification plans(reducing monthly mortgage payments) which 2

clearly show an intentional misrepresentation on the part of the Defendants. 3

46. Plaintiff was informed and believed that the representation by Defendants as to 4

the status of foreclosure and sale was a false representation because the Plaintiff 5

was not informed by the Defendants that there are remedies available to them 6

before the commencement of the foreclosure proceedings such as the forbearance 7

plans, mediation plan, Home Saver’s plans etc. and due diligence is not adhered to 8

by the defendants. 9

Plaintiff relies on the guidelines laid down by the Office of 10

Comptroller of Currency in “Operating standards for scheduled foreclosure sales” 11

dated April 19, 2013 in Minimum Pre-Foreclosure Sale Review Standards which 12

says that: “The servicer will promptly determine whether the borrower is currently 13

in an active loss mitigation program or is being actively considered for or has 14

requested consideration under the Making Home Affordable Modification Program 15

(HAMP) or other modification or loss mitigation program as further defined in 16

Standard Number 9, and whether further foreclosure proceedings and/or the 17

scheduled foreclosure sale should be postponed, suspended or cancelled as required 18

by program standards as applicable.” A copy of the guidelines is attached as Exhibit 19

F and incorporated here by reference. 20

47. Herein the representations made by all the defendants were not true and there 21

were no reasonable grounds for believing the representations to be true when they 22

made them. 23

48. Defendants thereby intended to defraud the plaintiff. As a direct and proximate 24

result of Defendants’ wrongful conduct, plaintiff suffered the damages as alleged 25

herein. 26

49. Defendants’ conduct was oppressive, fraudulent, and malicious and plaintiffs are 27

entitled to recover punitive damages pursuant to California Civil Code Section 3294. 28

It is pertinent to mention here that an agreement by 29

which a lender agreed to forbear from exercising the right of foreclosure under a 30

deed of trust securing an interest in real property comes within the statute of 31

11

fraudsas held in the case of Secrest v. Security National Mortgage Loan Trust 2002-1

2, 167 Cal.App.4th 544, 84(Cal.App. Dist.4 10/09/2008. 2

IX.FIFTH CAUSE OF ACTION 3

(WRONGFUL FORECLOSURE) 4

(AGAINST ALL DEFENDANTS) 5

50. Plaintiff incorporates all of the forgoing allegations in all previous paragraphs as 6

though fully set forth herein. 7

51. Plaintiff further alleges on the basis of information and belief thereon that the 8

loan was sold or transferred without notifying the Plaintiff in writing. Therefore, the 9

loan is void of legal rights to enforce it. 10

52. Additionally, the Foreclosing Defendants violated California Civil Code Section 11

2923.5(a), which requires a “mortgagee, beneficiary or authorized agent” to “contact 12

the borrower or person by telephone in order to assess the borrower’ financial 13

situation and explore options for the borrower to avoid foreclosure.” Section 14

2923.5(b) requires a default notice to include a declaration “from the mortgagee, 15

beneficiary, or authorized agent” of compliance with section 2923.5, including 16

attempt “with due diligence to contact the borrower as required by this section.” 17

53. It is pertinent to mention here that none of the Foreclosing Defendants tried to 18

contact or contacted the Plaintiff to discuss their financial situation. Thereafter 19

defendants failed to act with due diligence which was obligatory on their part as 20

provided under the laws of California. Moreover, none of the Foreclosing Defendants 21

explored options along with the Plaintiff to avoid foreclosure. They have falsely 22

mentioned that “attempts to contact the borrower have been unsuccessful … despite 23

the due diligence of the beneficiary of the authorized agent…” which is strongly 24

denied herein because in fact, no such attempts to contact the Plaintiff had ever 25

been made by any of the defendants. Additionally, none of the Foreclosing 26

Defendants informed the Plaintiff of other options to set aside foreclosure. 27

Accordingly, the Foreclosing Defendants did not fulfill their legal obligations to the 28

Plaintiff. 29

54. Thus, the Foreclosing Defendants engaged in a fraudulent foreclosure of the 30

Subject Property in which the Foreclosing Defendants did not have the legal 31

12

authority to foreclose. Alternatively, even if it is believed, for argument’s sake that 1

they did have the legal authority for such a foreclosure of the Subject Property, it is 2

apparent on the face of the abovementioned records that they failed to comply with 3

the laws of California. 4

55. As a result of the alleged wrongs, Plaintiff has suffered general and special 5

damages equal to an amount which is to be determined at the trial. 6

X.SIXTH CAUSE OF ACTION 7

(SETTING ASIDE FORECLOSURE) 8

(AGAINST ALL DEFENDANTS) 9

56. Plaintiff incorporates all of the forgoing allegations in all previous paragraphs as 10

though fully set forth herein. 11

57. Defendant, NBS Default Services, LLC, sent a notice to the Plaintiff of her default 12

on July 10, 2012. However, the defendants did not access the financial situations of 13

the Plaintiff and did not allow him to explore the options to avoid the foreclosure. 14

This is against the laws of California in regard to foreclosure. 15

58. Plaintiff had been asking for help to reduce the monthly mortgage payments but 16

the defendant without having a proper communication with the plaintiff in this 17

regard issued a notice for foreclosure. There was willful misrepresentation by the 18

Defendants in this case. 19

59. It is a well-established principle that a foreclosure may be set aside on the basis 20

of fraud or procedural irregularity. There was a procedural irregularity in this case 21

of foreclosure and the same must be set aside accordingly. 22

60. The procedure for foreclosure was not fair and regular. There were irregularities 23

in the foreclosure on account of which its validity is challenged herein. 24

61. The foreclosure done by the Defendants is against equity and wrongful, hence it 25

must be set aside by virtue of the facts alleged above. 26

62. Plaintiff has no other plain, speedy or adequate remedy, and the injunctive relief 27

prayed for below is necessary and appropriate at this time to prevent irreparable 28

loss to plaintiff’s interests. 29

XI.SEVENTH CAUSE OF ACTION 30

(UNJUST ENRICHMENT) 31

13

(AGAINST ALL DEFENDANTS) 1

63. Plaintiff incorporates all of the forgoing allegations in all previous paragraphs as 2

though fully set forth herein. 3

64. By their wrongful acts and omissions, the Foreclosing Defendants have been 4

unjustly enriched at the expense of the plaintiff, and thus the plaintiff has been 5

unjustly deprived of their rights and interests. 6

65. Therefore, Plaintiff seeks restitution from the Foreclosing Defendants, and an 7

order of this Court disgorging all profits, benefits, and other compensation obtained 8

by the Foreclosing Defendants from their wrongful conduct. 9

XII.EIGHT CAUSE OF ACTION 10

(BREACH OF COVENANT OF GOOD FAITH AND FAIR DEALING) 11

(AGAINST ALL DEFFENDANTS) 12

66. Plaintiff incorporates all of the forgoing allegations in all previous paragraphs as 13

though fully set forth herein. 14

67. Defendants had a duty of good faith and fair dealing in the performance and 15

enforcement of deed of trust dated July 14, 2006, wherein the defendants had a 16

discretionary power, affecting the rights of the plaintiff to be informed about the 17

loan modifications plans and modus operandi to set aside the foreclosure in cases 18

pertaining to default, which was omitted by the defendants deliberately. 19

68. The plaintiff fulfilled all the obligations prior to the default and was in a 20

condition to pay the installments but at a reasonable monthly mortgage payment 21

amount for which she had made a request of reducing it to $1000. Thereafter, 22

instead of fairly introducing the plaintiffs to alternative loan modification plans and 23

modus operandi to set aside the foreclosure, defendants omitted their duty 24

enumerated under the Office of Comptroller of Currency in Operating Standards For 25

Scheduled Foreclosure Sales dated 19th April, 2013. 26

Guideline no. 6 under Minimum Pre-Foreclosure Sale Review Standards reads as: 27

“The servicer must determine whether the loan is currently under loss mitigation or 28

other retention review or such review has been requested by the borrower as part 29

of the foreclosure process. If so, did servicer notify the borrower that all conditions 30

necessary to effect the loss mitigation or retention action have not been met, what is 31

14

needed to meet those conditions, and the date necessary to cure the deficiencies to 1

avoid further foreclosure action? If a borrower submitted a complete loan 2

modification application after the foreclosure referral, did the servicer comply with 3

any applicable dual track restrictions? 4

69. By virtue of the Defendants’ willful and wrongful conduct as herein alleged 5

above, Plaintiff is entitled to general and special damages according to the proof at 6

trial, as well as punitive and exemplary damages as determined by this Court. 7

XIII.NINTH CAUSE OF ACTION 8

(CANCELLATION OF INSTRUMENTS) 9

(AGAINST ALL DEFENDANTS) 10

70. Plaintiff incorporates all of the forgoing allegations in all previous paragraphs as 11

though fully set forth herein. 12

71. If the wrongfully recorded Notice of Default (NOD) and Notice of Trustee’s Sale 13

(NOTS) are left outstanding, Plaintiff will continue to suffer further losses and 14

damages. 15

72. Plaintiff therefore seeks cancellation of the following recorded instruments: 16

a) NOTICE OF DEFAULT (Exhibit D); and 17

b) NOTICE OF TRUSTEE’S SALE (Exhibit E). 18

73. Plaintiff is informed and believe, and therefore allege, that the Foreclosing 19

Defendants acted willfully and with a conscious disregard for Plaintiffs’ rights and 20

with a specific intent to harm the Plaintiff, by causing the Notice of Default and the 21

Notice of Trustee’s Sale to be prepared and recorded without a factual or legal basis 22

for doing so. 23

74. Based upon the information and belief, these acts by Defendants constituted 24

fraud, oppression and malice under California Civil Code Section 3294. Defendants 25

acted with a conscious disregard for the requirements to conduct a non-judicial 26

foreclosure sale knowing they had taken a calculated risk that the Plaintiff would 27

not contest. 28

75. By virtue of the Defendants’ willful and wrongful conduct as herein alleged 29

above, Plaintiff is entitled to general and special damages according to proof at trial, 30

as well as punitive and exemplary damages as determined by this Court. 31

15

It is pertinent to mention here that, other grounds 1

for setting aside a trustee’s sale in the case law include assertions that no breach 2

occurred, that the borrower was not in default, that the deed of trust was void, that 3

the sale was the result of sham bidding or an attempt to restrict competition in 4

bidding, or that the trustee did not have the power to foreclose (Lona v. Citibank, 5

N.A., supra, 202 Cal.App.4th at p. 106). 6

XIV.TENTH CAUSE OF ACTION 7

(VIOLATION OF CALIFORNIA BUSINESS AND PROFESSIONS CODE) 8

(AGAINST ALL DEFENDANTS) 9

76. Plaintiff incorporates all of the forgoing allegations in all previous paragraphs as 10

though fully set forth herein. 11

77. California Business & Professions Code Section 17200, prohibits acts of unfair 12

competition, which means and includes any “fraudulent business act or practice .....” 13

and conduct which is “likely to deceive” and is “fraudulent” within the meaning of 14

Section 17200. 15

78. As described above, the Foreclosing Defendants’ acts and practices are likely to 16

deceive, constituting a fraudulent business act or practice. This conduct is ongoing 17

and continues till date. 18

79. The Foreclosing Defendants engage in deceptive business practices with respect 19

to mortgage loan servicing, deeds of trust and assignment of deed, foreclosure of 20

residential properties and related matters by:- 21

(a) Assessing improper or excessive late fees; 22

(b) Instituting improper or premature foreclosure proceedings to generate 23

unwarranted fees; 24

(c) Improperly characterizing customers’ accounts as being in default or delinquent 25

status to generate unwarranted fees; 26

(d) Seeking to collect, and collecting, various improper fees, costs and charges, that 27

are either not legally due under the mortgage contract or California law, or that are 28

in excess of amounts legally due; 29

(e) Failing to provide adequate monthly statement information to customers 30

16

regarding the status of their accounts, payments owed, and/or basis for fees 1

assessed; 2

(f) Misapplying or failing to apply customer payments; 3

(g) Treating borrowers as in default on their loans even though the borrowers have 4

tendered timely and sufficient payments or have otherwise complied with mortgage 5

requirements or California law; 6

(h) Ignoring grace periods; 7

(i) Mishandling borrowers’ mortgage payments and failing to timely or properly 8

credit payments received, resulting in late charges, delinquencies or default; 9

(j) Failing to disclose the Fees, costs and charges allowable under the mortgage 10

contract; 11

(k) Acting as beneficiaries and trustees without the legal authority to do so and; 12

(l) Executing and recording false and misleading documents. 13

80. The Foreclosing Defendants engage in a uniform pattern and practice of unfair 14

and overly-aggressive servicing that result in the assessment of unwarranted and 15

unfair fees against California consumers, and premature default often resulting in 16

unfair and illegal foreclosure proceedings. The scheme implemented by the 17

Foreclosing Defendants is designed to defraud California consumers and enrich the 18

Foreclosing Defendants. The foregoing acts and practices have caused substantial 19

harm to California consumers. 20

81. As a direct and proximate cause of the unlawful, unfair and fraudulent acts and 21

practices of the Foreclosing Defendants, Plaintiff and California consumers have 22

suffered and will continue to suffer damages in the form of unfair and unwarranted 23

late fees and other improper fees and charges. The Plaintiff is therefore entitled to 24

attorney’s fees as available under California Business and Professions Code Sec. 25

17200 and related sections. 26

82. It is pertinent to mention here that because Section 17200 is written in the 27

disjunctive, it establishes three varieties of unfair competition acts or practices 28

which are unlawful, or unfair or fraudulent. In other words a practice is prohibited 29

as “unfair” or “deceptive” even if not unlawful and vice versa. This was said in the 30

case of Puentes V. Wells Fargo Home Mortgage Inc., 160 Cal. App. 4th 638. 31

17

XV.ELEVENTH CAUSE OF ACTION 1

(QUIET TITLE) 2

(AGAINST ALL DEFENDANTS) 3

83. Plaintiff incorporates all of the forgoing allegations in all previous paragraphs as 4

though fully set forth herein. 5

84. Plaintiff is the equitable owner of the Subject Property, the legal description of 6

which is mentioned in Para 15. 7

85. Plaintiff seeks to quiet title against the claims of Defendants as the Title 8

Defendants hold themselves out as entitled to fee simple ownership of the Subject 9

Property by and through their purchase of the property. In fact, the Title Defendants 10

had no right to title or interest in the Subject Property and no right to entertain any 11

rights of ownership including the right to foreclosure, offering the Subject Property 12

for sale at a trustee’s sale, demanding possession or filing cases for unlawful 13

detainer. Nevertheless, the Title Defendants proceeded with a non-judicial 14

foreclosure sale, illegally and with unclean hands. 15

86. Plaintiff is seeking to quiet title against the claims of all defendants; whether or 16

not the claim(s) or cloud(s) is, or are, known; and the unknown, uncertain, or 17

contingent claim, if any, of any defendant. The claim of defendant(s) is without any 18

right whatsoever and such defendants have no right, title, estate, lien, or interest 19

whatever in the above-described subject property or any part thereof. 20

87. The conduct of the Foreclosing Defendants caused Plaintiffs to suffer general and 21

special damages in an amount to be proven at trial. 22

XVI.PRAYER FOR RELIEF 23

88. Wherefore, plaintiff prays for judgment against the defendants as follows:- 24

1. For a declaration of the rights and duties of the parties, specifically that the 25

foreclosure of plaintiffs residence was wrongful. 26

2. For an Issuance of an order cancelling trustee’s deed of sale 27

3. That defendant delivers the original purported note immediately to the clerk of 28

the court for cancellation; 29

4. For Damages, in the event that the defendant fails to surrender the purported 30

18

note for cancellation pursuant to the judgment, in the sum of amount of the 1

purported note. 2

5. To vacate the trustee’s deed. 3

6. To vacate and set aside foreclosure sale. 4

7. For Compensatory and Punitive damages; 5

8. For reasonable attorney’s fees according to proof; 6

9. For reasonable costs of suit incurred herein; and 7

10. For such other and further relief as the court may deem proper. 8

DATED: August ____, 2013 _____________________________________ 9

CORALIA OWENS 10

11

XVII.VERIFICATION 12

I, Coralia Owens, is, the plaintiff in the above-entitled action. I have read the 13

foregoing complaint and know the contents thereof. The same is true of my 14

knowledge, except as to those matters, which are thereof. The same is true of my 15

own knowledge, except as to those matters, which are therein stated on information 16

and belief, and as to those matters, I believe them to be true. 17

I declare under penalty of perjury that the foregoing is true and correct. 18

DATED: August ____, 2013 _______________________________ 19

CORALIA OWENS 20

21

22

23

24

25

EXHIBIT A

EXHIBIT B

EXHIBIT C

EXHIBIT D

EXHIBIT E

EXHIBIT F

Minimum Standards for Prioritization and Handling Borrower Files Subject to Imminent Foreclosure Sale

Operating standards for scheduled foreclosure sales April19, 2013

The minimum standards set forth in this guidance reflect sound business practice that should be part of a mortgage servicer's ongoing collections, loss mitigation and foreclosure processing functions. Accordingly, the OCC requires that all national banks and federal savings associations (collectively, "banks") that service residential mortgage loans incorporate the guidance into their ongoing business processes. Failure to comply with this guidance may result in unsafe and unsound banking practices, non-compliance with foreclosure related consent orders, as applicable, and/or require rescission of completed foreclosures.

Purpose This guidance establishes minimum standards for the handling and prioritization of borrower files that are subject to imminent (within 60 days) scheduled foreclosure sales. The purpose of this guidance is to ensure that borrowers will not lose their homes without their files receiving pre-foreclosure sale reviews conducted under the standards listed In this guidance, which also help ensure loan modifications were considered as appropriate.

Bank servicers of residential mortgages should use these review and validation standards to determine whether a scheduled foreclosure sale should be postponed, suspended or cancelled due to critical foreclosure defects in the borrower's file. These minimum review criteria are intended to ensure a level of consistency across servicers, not to supplant review and validation procedures that go beyond these minimums. Servicers that currently apply more than these minimum standards as part of their own pre-foreclosure sale review and validation procedures are expected to continue to do so.

These standards are not Intended to incorporate the final rules amending Regulation X and Regulation z issued by the CFPB on January 17, 2013, and effective on January 10, 2014, which govern mortgage servicers' loss mitigation and foreclosure processing functions. The OCC expects that all servicers will undertake appropriate action in a timely manner to ensure their practices will be compliant with the new rules by the effective date.

Overview Bank servicers of residential mortgages should monitor all borrower files in the foreclosure process at least weekly to determine if foreclosure sales are scheduled within the next 60 days. The

servicer should implement procedures to perform and document a timely pre-foreclosure sale review according to the criteria set out in this guidance and appropriately postpone, suspend or cancel t.he scheduled foreclosure sale when warranted.

The servicer will promptly determine whether the borrower is currently in an active loss mitigation program or is being actively considered for or has requested consideration under the Making Home Affordable Modification Program (HAMP) or other modification or loss mitigation program as further defined in standard number 9

Minimum Pre-Foreclosure Sale Review Standards

below, and whether further foreclosure proceedings and/or the scheduled foreclosure sale should be postponed, suspended or cancelled as required by program standards as applicable.

The following standards are a non-exhaustive list of criteria for which an exception would warrant postponement, suspension or cancellation of a foreclosure sale until the Minimum Pre-Foreclosure Sale Review Standards are satisfied. As noted above, individual servicers may apply additional standards/criteria to postpone, suspend or cancel a foreclosure sale.

Any negative response to the minimum standards detailed in this guidance will be considered a critical defect (except for standard number 7 where a positive response is a defect) and cause to postpone, suspend or cancel a scheduled foreclosure sale.

Independent control functions (such as audit, compliance, and risk management) should confirm and document servicer adherence to their own servicing standards/criteria and the standards described in this document through a program of monitoring, sampling and testing of scheduled and completed foreclosure sales.

Date of the scheduled foreclosure sale: _______

Once the date of foreclosure is established, the servicer needs to confirm the following information before foreclosing:

1. Is the loan's default status accurate?

2. Does the servicer have and can demonstrate the appropriate legal authority to foreclose (documented assignments, note endorsements, and other necessary legal documentation, as applicable)?

3. Have required foreclosure notices or other required communications to the borrower or others, as applicable, been provided in a timely manner?

4. Has the servicer taken all steps necessary to confirm whether the borrower, co-borrower, and all oblig_ors on the mortgage, trust

deed, or other security in the nature of a mortgage are entitled to protections under the Servicemembers Civil Relief Act (SCRA), including running queries through the Department of Defense database? If the borrower, co-borrower, or other obligor is subject to SCRA protections, has the servicer complied with all applicable legal requirements to foreclose?

5. Determine whether the borrower is in an active bankruptcy. If so, does the servicer have documented legal authority to foreclose?

6. Determine whether the loan is currently under loss mitigation or other retention review or such review has been requested by the borrower as part of the foreclosure process. If so, did the servicer notify the borrower that all conditions necessary to effect the loss mitigation or retention action have not been met, what is needed to meet those conditions, and the date necessary to cure the deficiencies to avoid further foreclosure action? If a borrower submitted a complete loan modification application after the foreclosure referral, did the servicer comply with any applicable dual track restrictions?

7. Is the borrower currently in an active trial loss mitigation plan?

8. Determine whether the servicer accepted any payment from the borrower in the preceding 60 days (that is, were borrower payments, including interest, principal, fees, escrow payments, applied to the borrower's account or retained in a suspense account). If so, did the servicer clearly communicate to the borrower that he or she is neither in nor being considered for a loss mitigation program, and that the bank's acceptance of the payment in no way affected the status of the foreclosure that is proceeding?

9. As applicable, was the borrower solicited for and offered a loss mitigation option, such as, those required by HAMP, government sponsored enterprise, the Federal Housing Administration, the U.S. Veterans Administration, state-level government programs under U.S. Department of Treasury, other third party investor, or the servicer's loss mitigation and modification programs? To the extent applicable, has the servicer complied with its loss mitigation obligations detailed in the National Mortgage Settlement? Have any borrower complaints, appeals, or escalations been considered and addressed?

10. Was the fully executed loan modification application submitted by the borrower, as defined by the applicable modification program, reviewed by the servicer as required, including any timeline or notice requirements?

11. Was the modification decision correct and validated as required by the applicable modification program (to include, as applicable, compliance with program requirements and accuracy of calculations and application of the NPV test) along with appropriate resolution and communication of any borrower complaint, appeal, or escalation?

12. Was the borrower or the borrower's representative (housing counselor or attorney) notified of the loan modification decision and rationale as required by program or policy guidelines?

13. If required by a GSE or other investor, has the servicer certified to the attorney conducting the foreclosure that all delinquency management requirements have been met, including that there is neither an approved payment plan arrangement nor a foreclosure alternative offer pending or accepted?