Noteworthy Tax Court Facts

15

Hooper Cornell, PLLC 250 Bobwhite Ct., Suite 300 Boise, Idaho 83706 Tel: 208.344.2527 www.hoopercornell.com Interesting Facts Every Tax Attorney Can (and Should) Know About United States Tax Court

-

Upload

keithpinkerton -

Category

Documents

-

view

196 -

download

0

Transcript of Noteworthy Tax Court Facts

Hooper Cornell, PLLC250 Bobwhite Ct., Suite 300

Boise, Idaho 83706Tel: 208.344.2527

www.hoopercornell.com

Interesting Facts Every Tax Attorney Can (and Should) Know About United States Tax Court

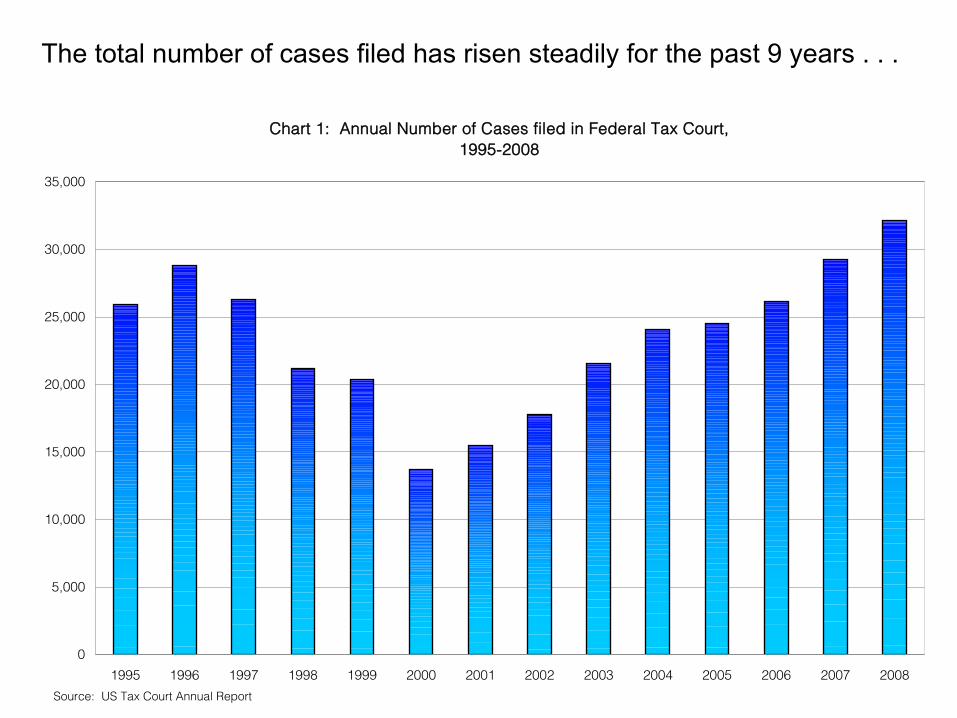

The total number of cases filed has risen steadily for the past 9 years . . .

Chart 1: Annual Number of Cases filed in Federal Tax Court, 1995-2008

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

Source: US Tax Court Annual Report

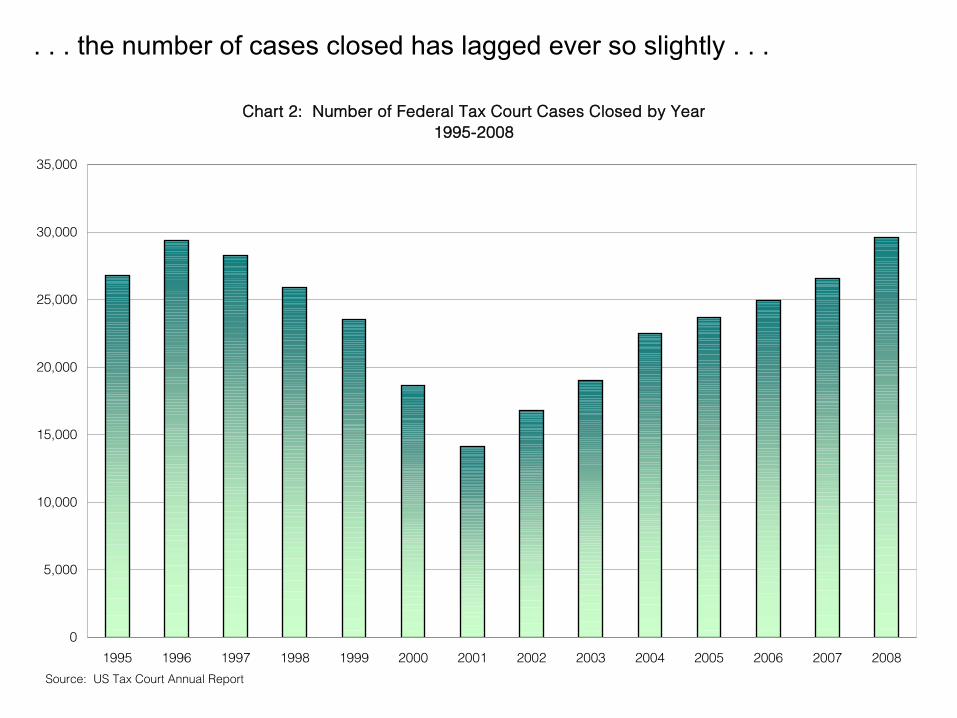

. . . the number of cases closed has lagged ever so slightly . . .

Chart 2: Number of Federal Tax Court Cases Closed by Year 1995-2008

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

Source: US Tax Court Annual Report

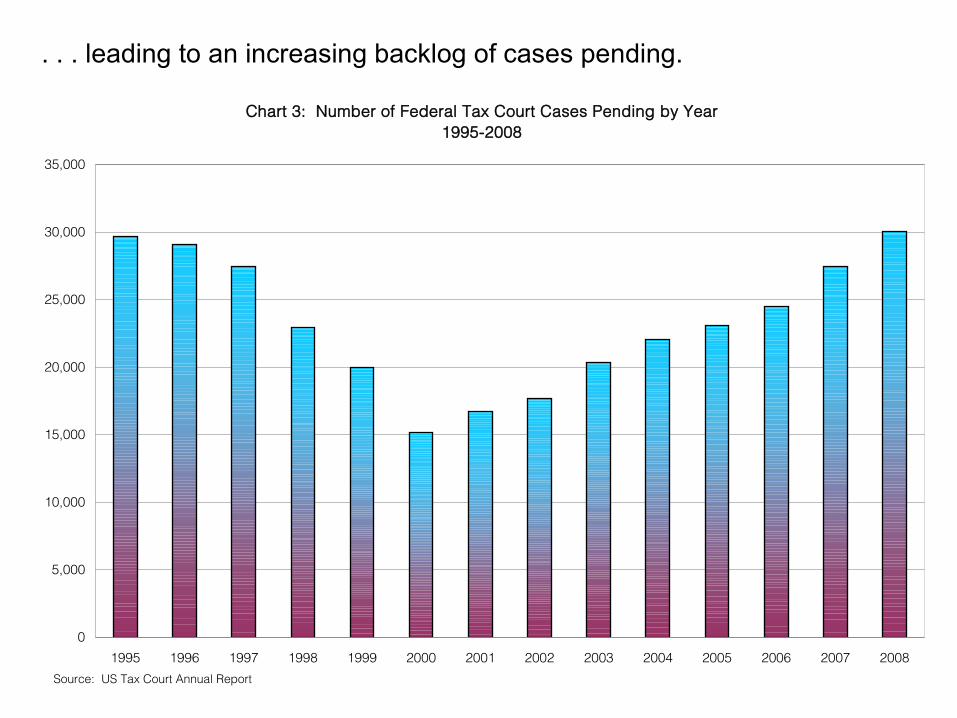

. . . leading to an increasing backlog of cases pending.

Chart 3: Number of Federal Tax Court Cases Pending by Year 1995-2008

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

Source: US Tax Court Annual Report

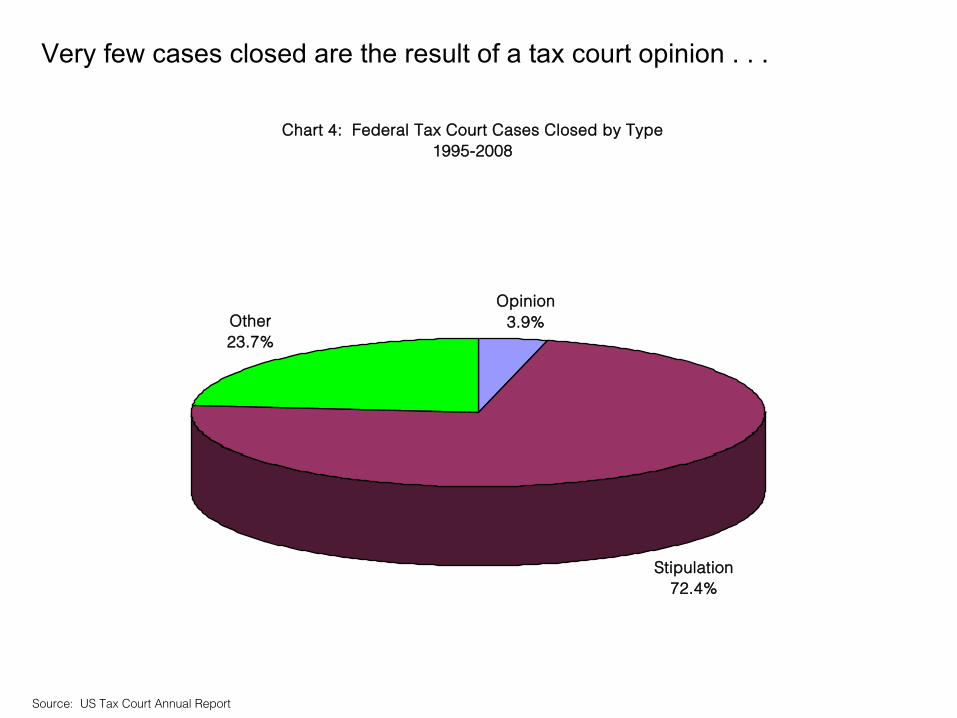

Very few cases closed are the result of a tax court opinion . . .

Chart 4: Federal Tax Court Cases Closed by Type 1995-2008

Opinion3.9%

Stipulation72.4%

Other23.7%

Source: US Tax Court Annual Report

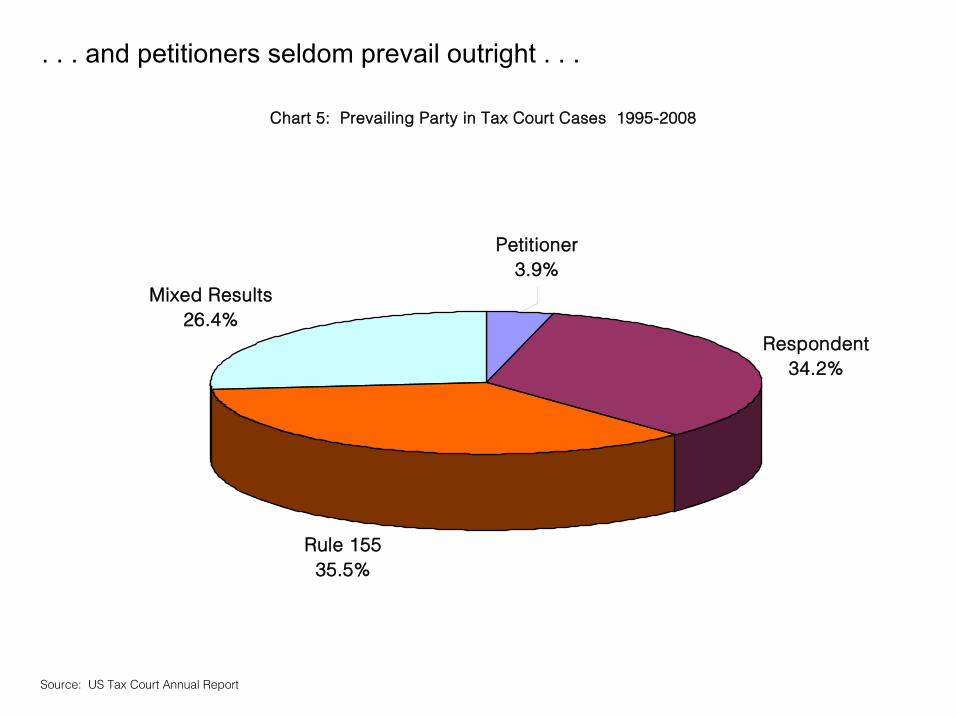

. . . and petitioners seldom prevail outright . . .

Chart 5: Prevailing Party in Tax Court Cases 1995-2008

Rule 15535.5%

Mixed Results26.4%

Respondent34.2%

Petitioner3.9%

Source: US Tax Court Annual Report

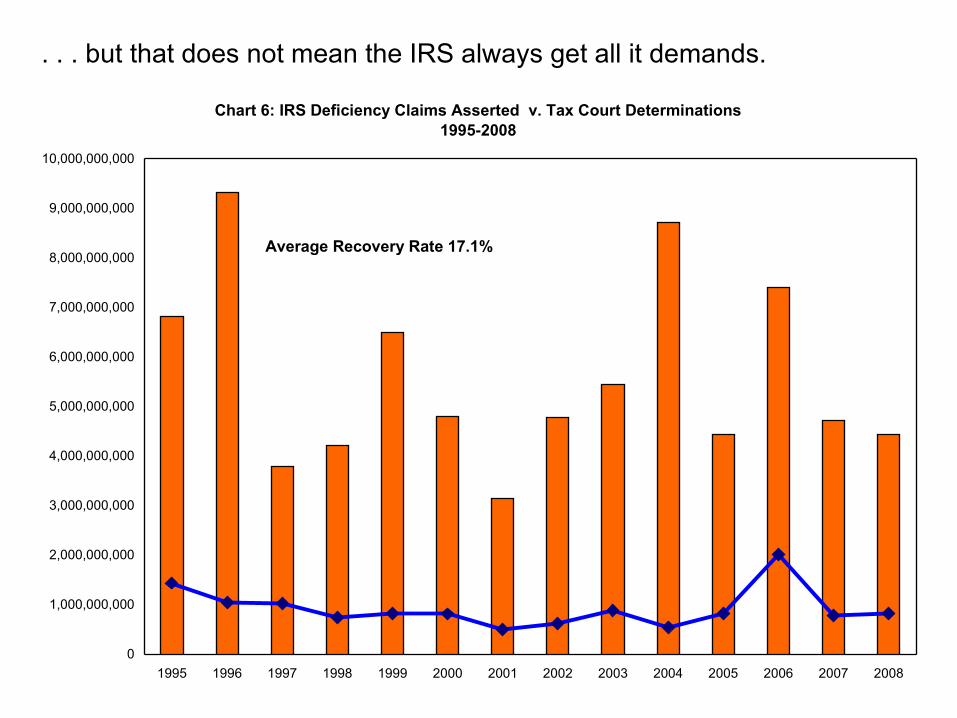

. . . but that does not mean the IRS always get all it demands.

Chart 6: IRS Deficiency Claims Asserted v. Tax Court Determinations1995-2008

0

1,000,000,000

2,000,000,000

3,000,000,000

4,000,000,000

5,000,000,000

6,000,000,000

7,000,000,000

8,000,000,000

9,000,000,000

10,000,000,000

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

Average Recovery Rate 17.1%

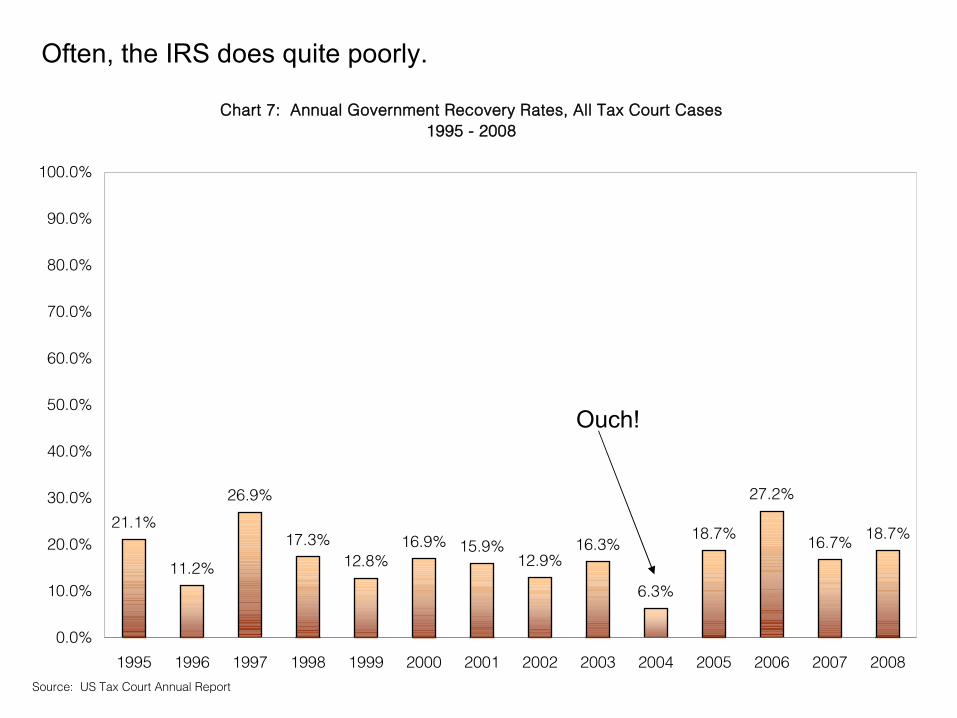

Often, the IRS does quite poorly.

Ouch!

Chart 7: Annual Government Recovery Rates, All Tax Court Cases1995 - 2008

21.1%

11.2%

26.9%

17.3%12.8%

16.9% 15.9%12.9%

16.3%

6.3%

18.7%

27.2%

16.7% 18.7%

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

80.0%

90.0%

100.0%

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008Source: US Tax Court Annual Report

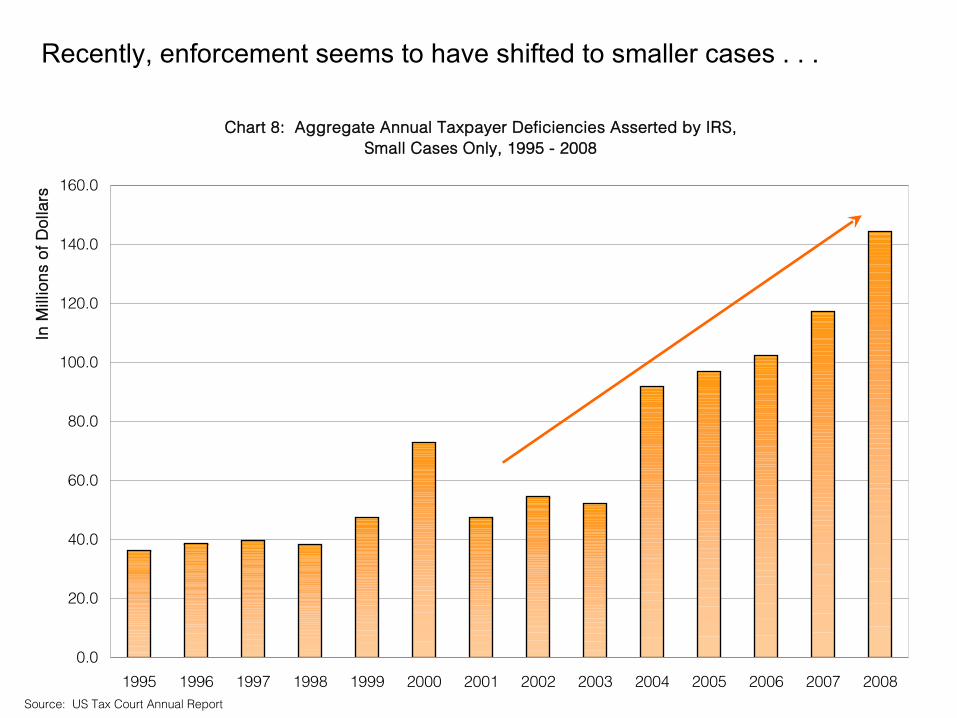

Recently, enforcement seems to have shifted to smaller cases . . .

Chart 8: Aggregate Annual Taxpayer Deficiencies Asserted by IRS, Small Cases Only, 1995 - 2008

0.0

20.0

40.0

60.0

80.0

100.0

120.0

140.0

160.0

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

In M

illio

ns o

f Dol

lars

Source: US Tax Court Annual Report

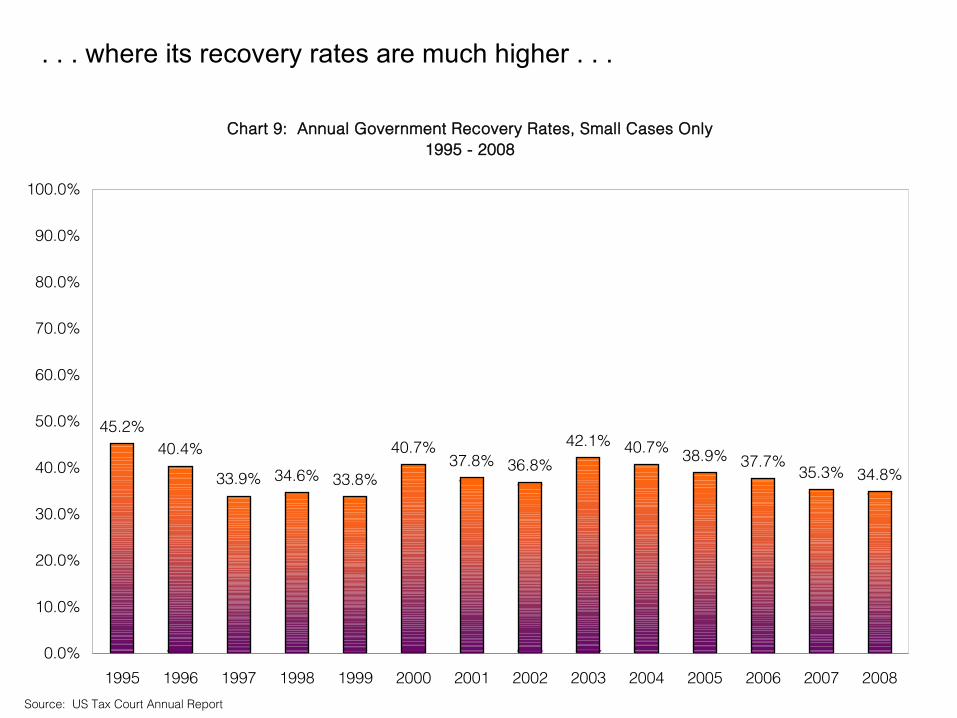

. . . where its recovery rates are much higher . . .

Chart 9: Annual Government Recovery Rates, Small Cases Only1995 - 2008

45.2%40.4%

33.9% 34.6% 33.8%

40.7%37.8% 36.8%

42.1% 40.7% 38.9% 37.7%35.3% 34.8%

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

80.0%

90.0%

100.0%

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

Source: US Tax Court Annual Report

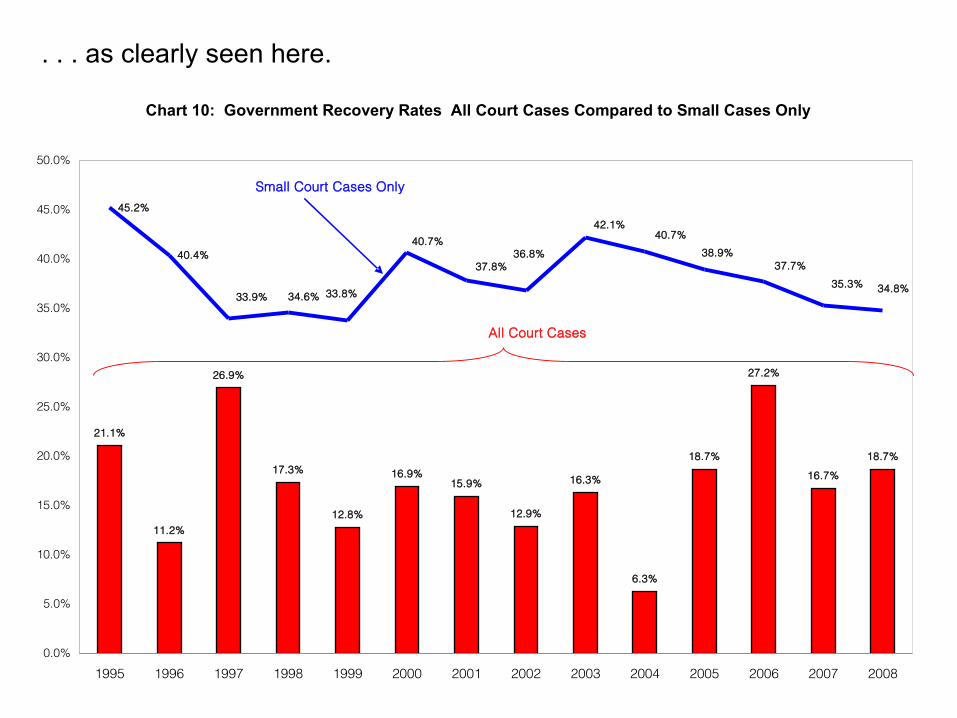

. . . as clearly seen here.

Chart 10: Government Recovery Rates All Court Cases Compared to Small Cases Only

21.1%

11.2%

26.9%

17.3%

12.8%

16.9%15.9%

12.9%

16.3%

6.3%

18.7%

27.2%

16.7%

18.7%

45.2%

40.4%

34.8%

37.7%

35.3%33.9% 34.6%

40.7%

37.8%

42.1%40.7%

38.9%

33.8%

36.8%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

40.0%

45.0%

50.0%

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

Small Court Cases Only

All Court Cases

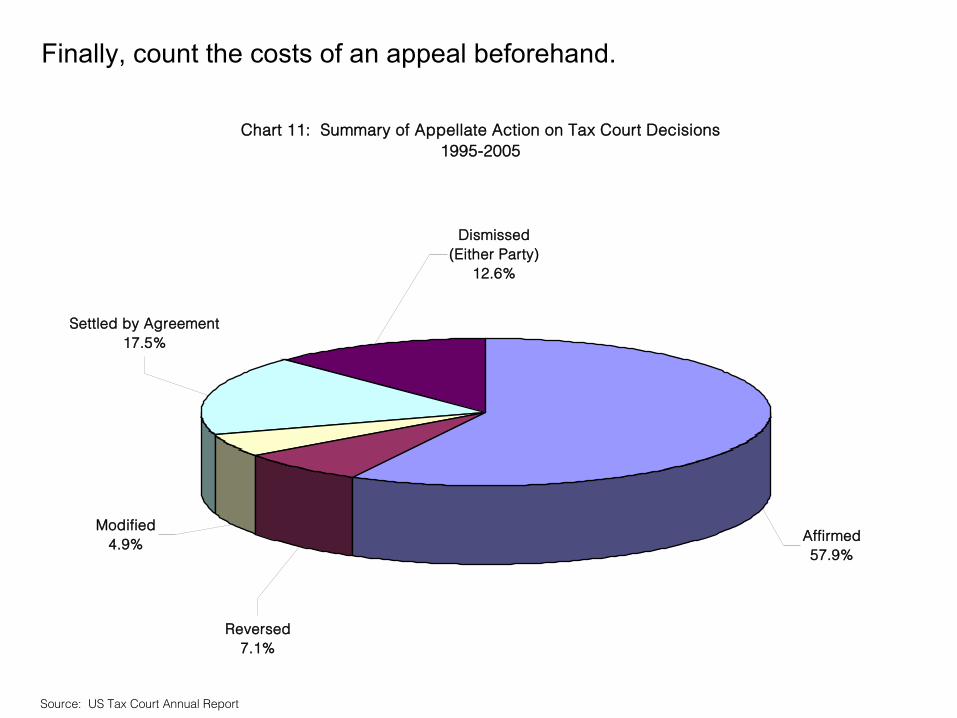

Finally, count the costs of an appeal beforehand.

Chart 11: Summary of Appellate Action on Tax Court Decisions 1995-2005

Affirmed57.9%

Reversed7.1%

Modified4.9%

Settled by Agreement17.5%

Dismissed (Either Party)

12.6%

Source: US Tax Court Annual Report

About Hooper Cornell’s Valuation Practice

While we cannot provide this . . .

We may be able to help avoid this . . .

IRS

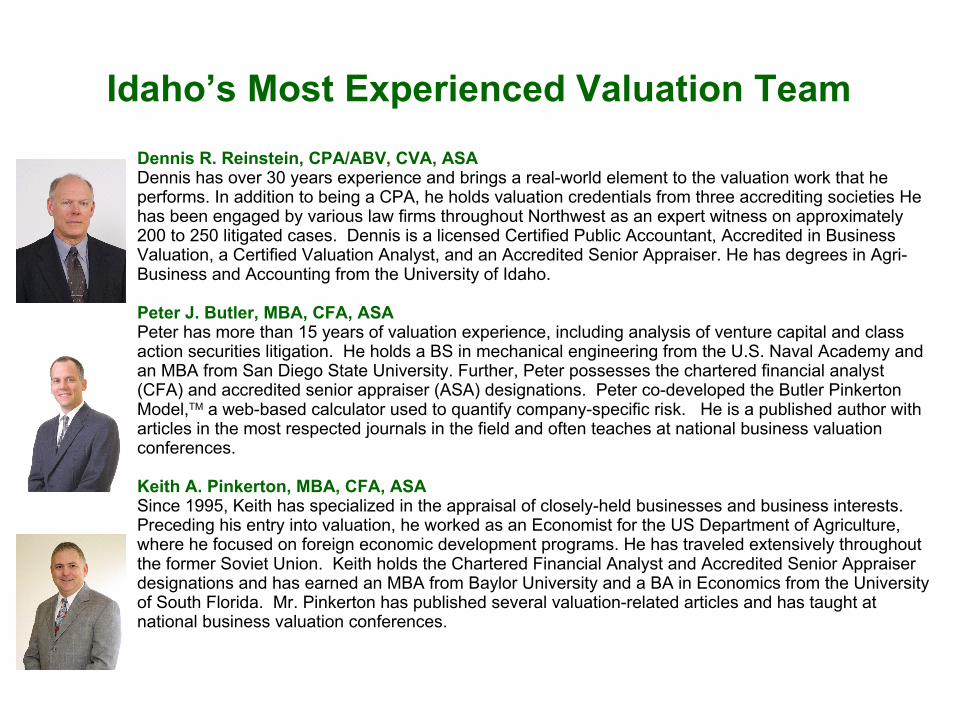

Idaho’s Most Experienced Valuation Team

Dennis R. Reinstein, CPA/ABV, CVA, ASADennis has over 30 years experience and brings a real-world element to the valuation work that he performs. In addition to being a CPA, he holds valuation credentials from three accrediting societies He has been engaged by various law firms throughout Northwest as an expert witness on approximately 200 to 250 litigated cases. Dennis is a licensed Certified Public Accountant, Accredited in Business Valuation, a Certified Valuation Analyst, and an Accredited Senior Appraiser. He has degrees in Agri-Business and Accounting from the University of Idaho.

Peter J. Butler, MBA, CFA, ASAPeter has more than 15 years of valuation experience, including analysis of venture capital and class action securities litigation. He holds a BS in mechanical engineering from the U.S. Naval Academy and an MBA from San Diego State University. Further, Peter possesses the chartered financial analyst (CFA) and accredited senior appraiser (ASA) designations. Peter co-developed the Butler Pinkerton Model,TM a web-based calculator used to quantify company-specific risk. He is a published author with articles in the most respected journals in the field and often teaches at national business valuation conferences.

Keith A. Pinkerton, MBA, CFA, ASASince 1995, Keith has specialized in the appraisal of closely-held businesses and business interests. Preceding his entry into valuation, he worked as an Economist for the US Department of Agriculture, where he focused on foreign economic development programs. He has traveled extensively throughout the former Soviet Union. Keith holds the Chartered Financial Analyst and Accredited Senior Appraiser designations and has earned an MBA from Baylor University and a BA in Economics from the University of South Florida. Mr. Pinkerton has published several valuation-related articles and has taught at national business valuation conferences.